Ghana’s Experience with National...Period Health financing strategy-Private sector initiative 1993...

34

Ghana’s Experience with National Health Insurance Scheme Francis-Xavier Andoh-Adjei Director of Administration National Health Insurance Authority

Transcript of Ghana’s Experience with National...Period Health financing strategy-Private sector initiative 1993...

Ghana’s Experience with National Health Insurance Scheme

Francis-Xavier Andoh-AdjeiDirector of AdministrationNational Health Insurance Authority

Contents

Historical development

NHIS: Initial processes

Key players/actors

Scheme design features

Achievements and challenges

Way forward and conclusion

Your access to healthcare

IV. Challenges & Way Forward

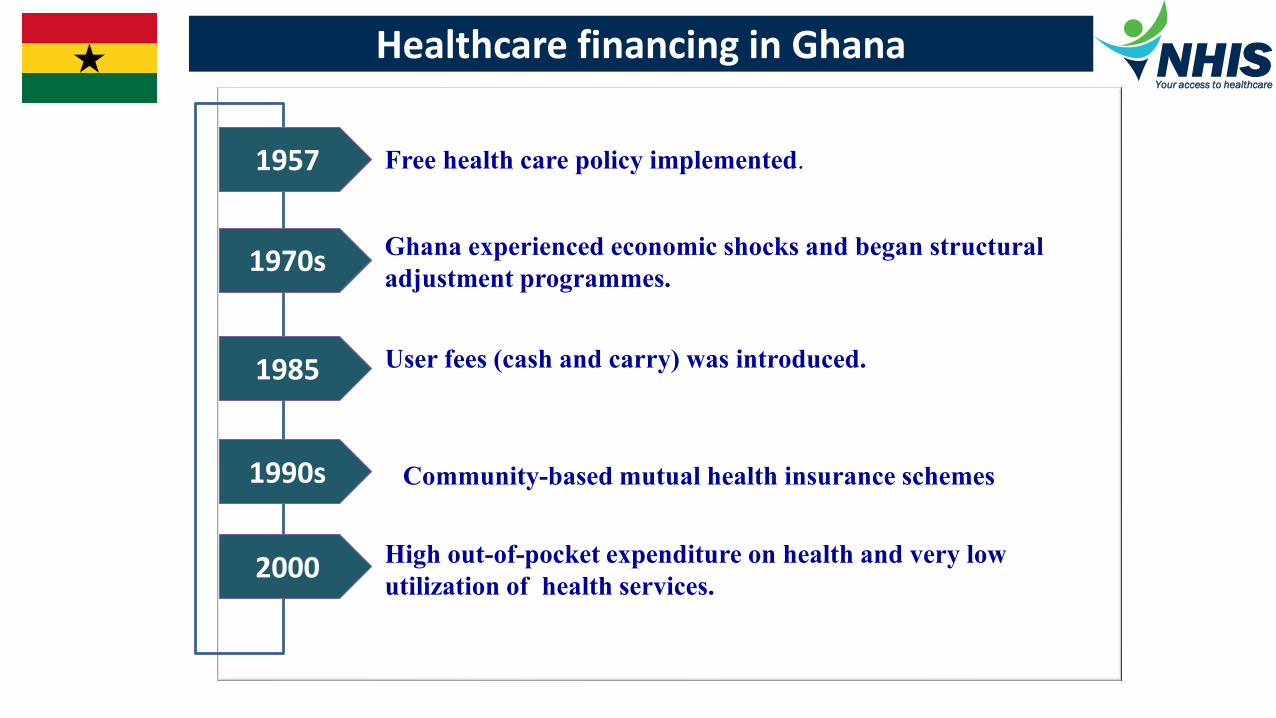

Healthcare financing in Ghana

19571957 Free health care policy implemented.

Ghana experienced economic shocks and began structural

adjustment programmes.

User fees (cash and carry) was introduced.

1970s1970s

19851985

1990s1990s Community-based mutual health insurance schemes

20002000 High out-of-pocket expenditure on health and very low

utilization of health services.

Your access to healthcare

IV. Challenges & Way Forward

Healthcare financing in Ghana

Free Maternal Care Policy

Decoupling of children from parents20082008

20032003The NHIS was established

The NHIS Act was revised in 2012 (Act 852) 20122012

Your access to healthcare

Period Health financing strategy-Private sector initiative

1993 Nationwide Mutual Medical Insurance Scheme

▪ had 20,000 subscribers in 2 years

1997 Metropolitan Health Insurance Plan: by 2001

▪ 15,000 members on full cover

▪ 25,000 members on partial cover

▪ designed package for teachers

▪ in discussion with the military for same for its civilian

employees and dependants

1999 The Ghana Healthcare Company (SSNIT)

The Civil Servants Association of Ghana

Healthcare financing in Ghana Your access to healthcare

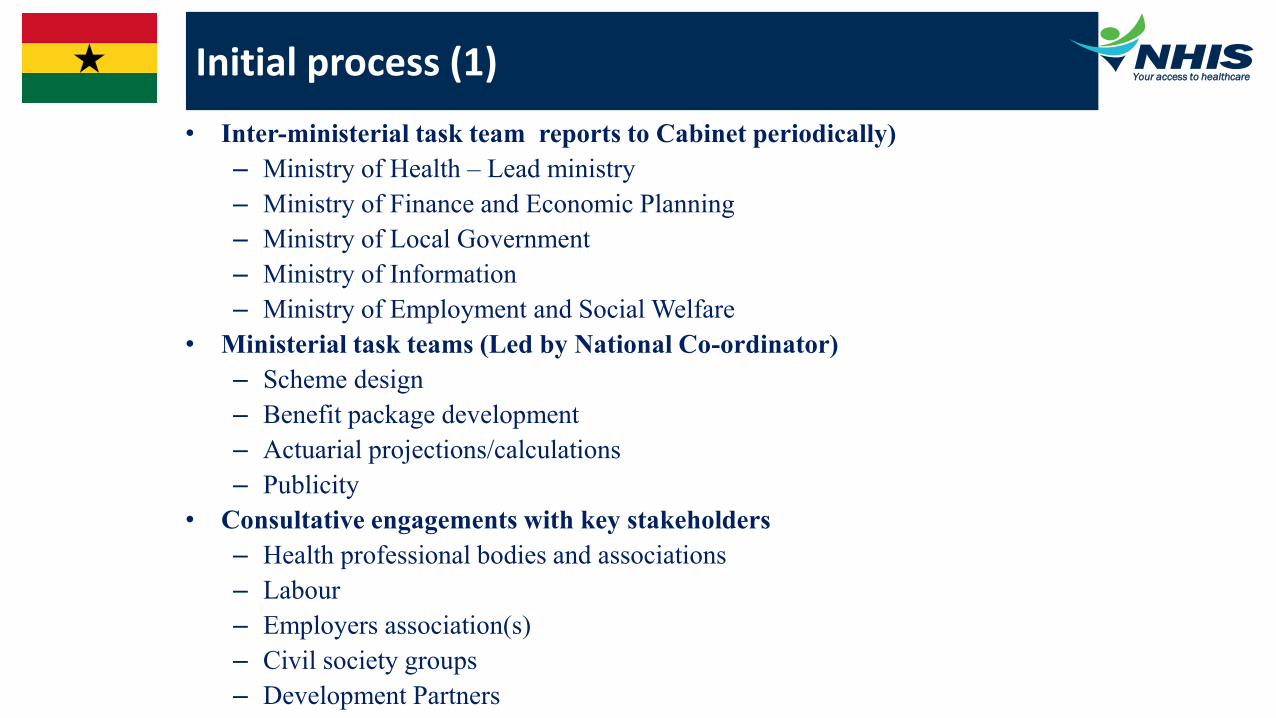

Initial processes (1)

• Inter-ministerial task team reports to Cabinet periodically)

– Ministry of Health – Lead ministry

– Ministry of Finance and Economic Planning

– Ministry of Local Government

– Ministry of Information

– Ministry of Employment and Social Welfare

• Ministerial task teams (Led by National Co-ordinator)

– Scheme design

– Benefit package development

– Actuarial projections/calculations

– Publicity

• Consultative engagements with key stakeholders

– Health professional bodies and associations

– Labour

– Employers association(s)

– Civil society groups

– Development Partners

Initial process (1) Your access to healthcare

Initial processes (2)

• NHIS policy presented to Minister of Health in 2002

• 45 districts selected for pilot

• NHIS Bill presented to Parliament in 2002 and passed into law in 2003

• Legislative Instrument presented to Parliament and approved in 2004

• NHIS policy revised to be consistent with the Law in 2004

• NHIS Council (Board) appointed in 2004

• First Chief Executive (Executive Secretary) appointed in 2004

• Formal recruitment of staff at the district level done in 2004

• Official launching of scheme in 2004

Initial process (2) Your access to healthcare

The National Health Insurance Scheme

Your access to healthcare

Scheme design features (1)

• Demand driven policy aligned to development priorities

• Country-owned

• In-country leadership

• Broad base consultation and partnership with stakeholder

• Efficiency considerations

• Sustainability

• Scalability

Scheme design features (1) Key characteristicsYour access to healthcare

10

Significant revisions in the Law include the following:

A Mandatory NHIS

A Unified NHIS with District Offices

Premium exemptions for persons with Mental

Disorders

Expenditure cap of 10% on non-core NHIS activities

Relevant family planning package- (now piloting) - Obuasi

Board oversight committee for

i. Scheme operations

ii. Private Health Insurance schemes

iii. Fund operations

Scheme design features (2) Legal reviewYour access to healthcare

Scheme design features (3) Financing model

Financing Options:

i. Bismarck model (Social health insurance)

ii. Beveridge model (Tax revenue)

iii. Community Based Schemes

iv. Combination of any of these models

Financing Options:

i. Bismarck model (Social health insurance)

ii. Beveridge model (Tax revenue)

iii. Community Based Schemes

iv. Combination of any of these models

Your access to healthcare

Key Players in Ghana’s NHIS ArchitectureYour access to healthcare

Sources of funding for health & NHISYour access to healthcare

World Bank report on NHIS

Benefit PackageYour access to healthcare

• Estimated 95% of diseases covered – (clinically reported in Ghana)• Not reviewed since NHIS launched 15 years ago• Providers can practice selective service

Benefit PackageYour access to healthcare

• The NHIS Benefit package is considered very generous and

comprehensive as it covers over 90% of disease conditions in Ghana

The benefit package covers• Outpatient services (General & specialist consultations, diagnostics,

medicines, HIV/AIDS symptomatic treatment for opportunistic infections, etc.)

• Inpatient services (General & specialist inpatient care, diagnostics, medicines, etc.)

• Oral health and Eye care• Maternity care (including caesarean session)• Emergencies (Crises situations such as Medical and surgical

emergencies as well as Road accidents)

Benefit Package – Exclusion List

• (a) Rehabilitation other than physiotherapy;

• (b) Appliances and prostheses

• (c) Cosmetic surgeries and aesthetic treatments;

• (d) HIV retroviral drugs

• (e) Assisted Reproduction

• (j) Dialysis for chronic renal failure;

• (l) Cancer treatment other than cervical and breast cancer;

• (m) Organ transplantation;

• (o) Diagnosis and treatment abroad;

• (p) Medical examinations for purposes of visa applications, educational, institutional, driving license;

• (r) Mortuary Services.

Your access to healthcare

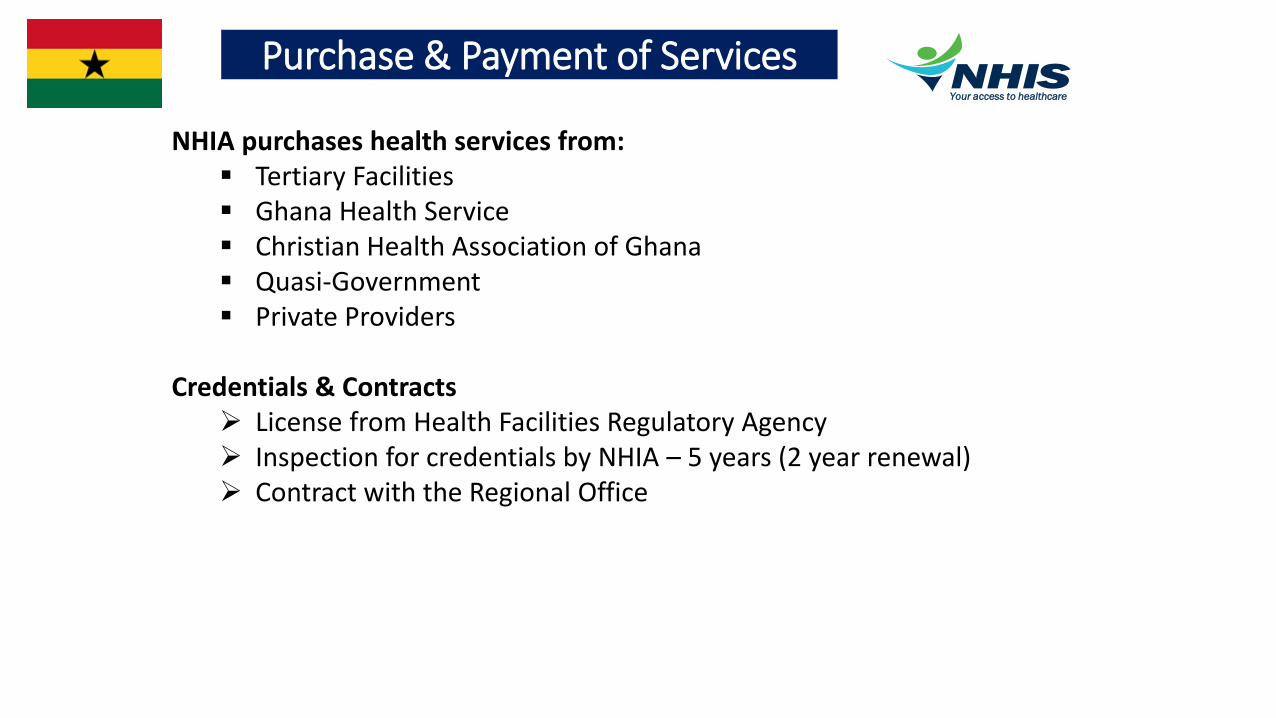

Purchase & Payment of ServicesYour access to healthcare

NHIA purchases health services from:▪ Tertiary Facilities▪ Ghana Health Service▪ Christian Health Association of Ghana▪ Quasi-Government▪ Private Providers

Credentials & Contracts➢ License from Health Facilities Regulatory Agency➢ Inspection for credentials by NHIA – 5 years (2 year renewal)➢ Contract with the Regional Office

Purchase & Payment of ServicesYour access to healthcare

A mix of provider payment methods:❑ Fee For Service Medicines❑ Diagnosis-Related Groupings In-patient & Outpatient Specialist Services

❑ Capitation Primary Care Package

FFS FFS

G-DRG FFS

G-DRG & CAPITATION FFS

G-DRG FFS

ServicesServices MedicinesMedicines

20052005

20082008

20122012

20162016

Your access to healthcare

Quality - Credentialing

IV. Challenges & Way Forward

Credentialed facilities (4,078)

IV. Challenges & Way Forward

Your access to healthcare

Public65%

Mission5%

Private29%

Quasi-government

1%

Achievements of NHIS

21

IV. Challenges & Way ForwardIV. Challenges & Way Forward

Your access to healthcare

Mobile Renewal Solution

BENEFIT PACKAGE:

This option gives a brief overview of benefit package with call center number to find out more

MEDICINE LIST: This option lists top 10 medicines and prompts members to call CallCentre to know about comprehensive medicine list and package

CHECK EXPIRY: Using

this option, members are able to check when their policy is due to expire

RENEW: This option requires NHIS (or GHANA CARD) number, prompts requisite premium amount and completes payment from mobile money wallet

IV. Challenges & Way Forward

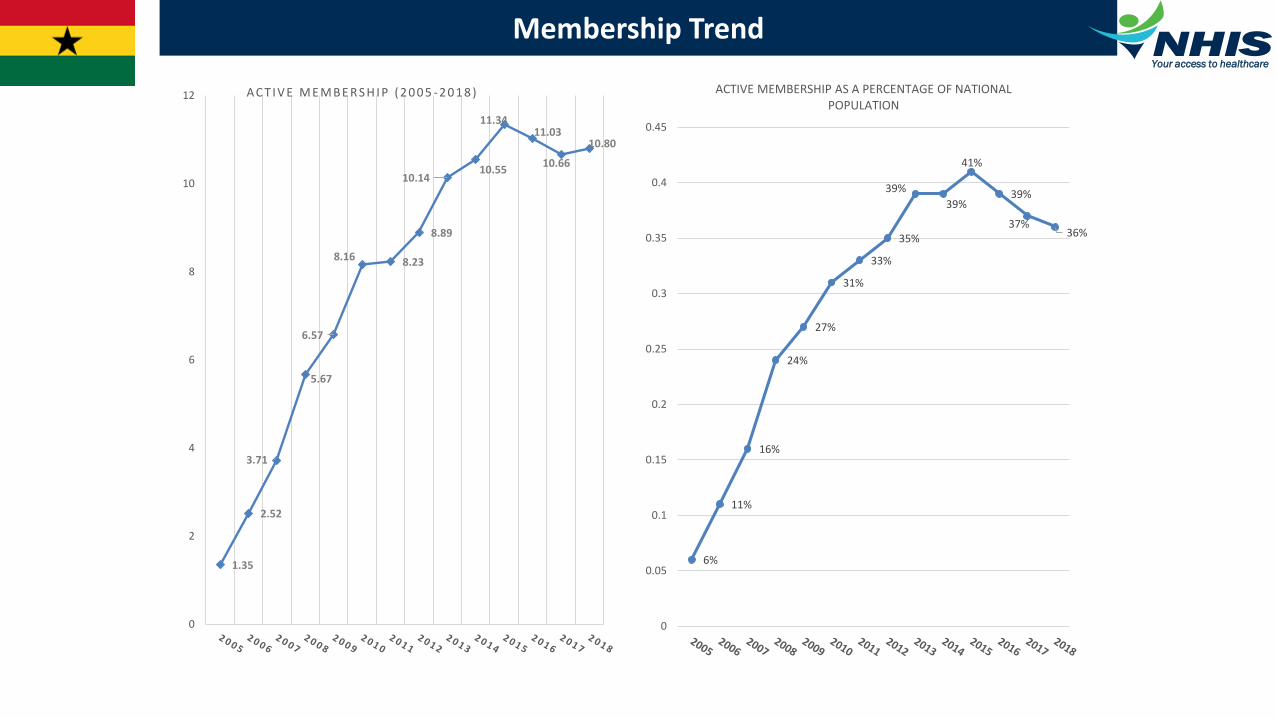

Membership Trend

1.35

2.52

3.71

5.67

6.57

8.16 8.23

8.89

10.1410.55

11.3411.03

10.66

10.80

0

2

4

6

8

10

12 A C T I V E M E M B E R S H I P ( 2 0 0 5 - 2 0 1 8 )

6%

11%

16%

24%

27%

31%

33%

35%

39%

39%

41%

39%

37%36%

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

ACTIVE MEMBERSHIP AS A PERCENTAGE OF NATIONAL POPULATION

Your access to healthcare

Exemption from contribution

✓ Children under 18

✓ Persons aged 70 and above

✓ Indigent

✓ SSNIT Pensioners

✓ Pregnant Women

✓ Persons with mental disorders

✓ Categories of disabled

Exemption from contribution

✓ Children under 18

✓ Persons aged 70 and above

✓ Indigent

✓ SSNIT Pensioners

✓ Pregnant Women

✓ Persons with mental disorders

✓ Categories of disabled

Your access to healthcare

70 YRS & ABOVE

5%

INDIGENTS 4%

INFORMAL SECTOR

31%

PREGNANT WOMEN

7%

SECURITY SERVICES

0%

SSNIT CONTRIBUTOR

S 6%

SSNIT PENSIONERS

0%

UNDER 18 47%

ACTIVE MEMBERSHIP – 10.8 MILLION (36%)

Membership by Category (December 2018)

IV. Challenges & Way Forward

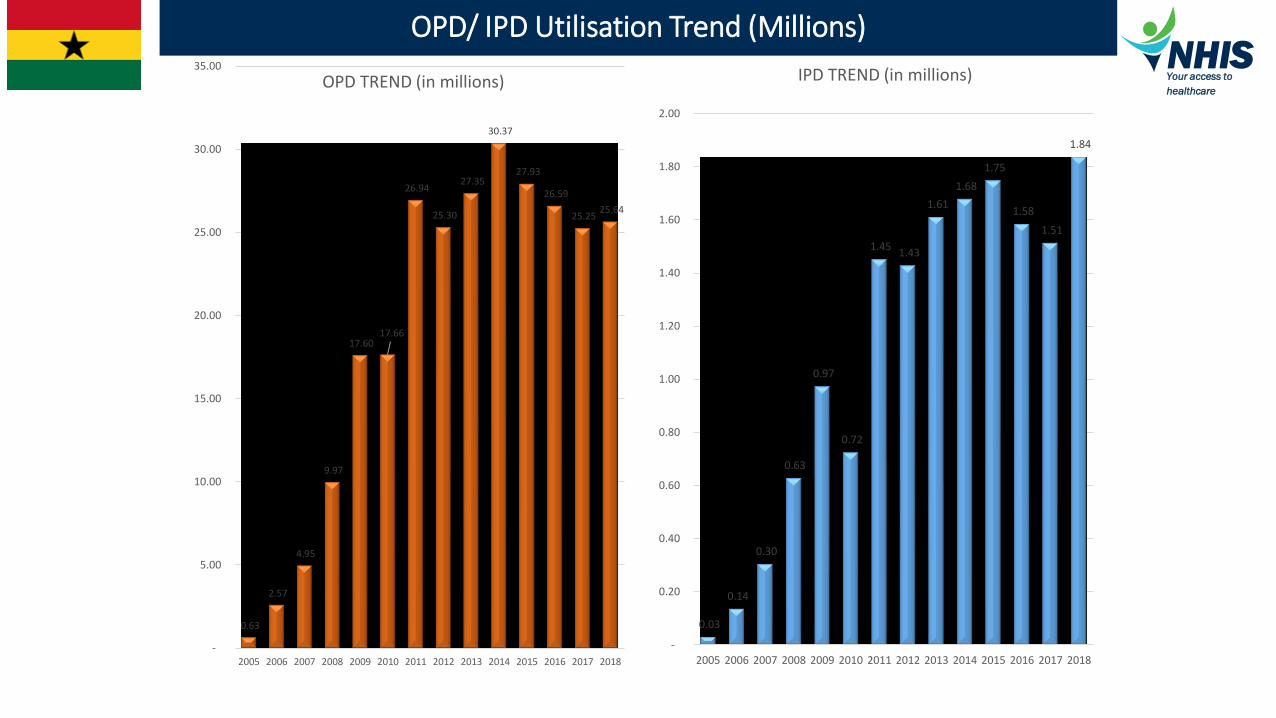

OPD/ IPD Utilisation Trend (Millions)

0.63

2.57

4.95

9.97

17.60 17.66

26.94

25.30

27.35

30.37

27.93

26.59

25.25 25.64

-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

OPD TREND (in millions)

0.03

0.14

0.30

0.63

0.97

0.72

1.45 1.43

1.61

1.68

1.75

1.58

1.51

1.84

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

IPD TREND (in millions) Your access to

healthcare

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014

CASHPayments

NHISPayments

Achievements (3) Out-of-pocket expendituresYour access

to healthcare

Health financing statistics 2000-2015

Year/indicator 2000 2004 2008 2012 2015

Current health expenditure (CHE) as % of gross domestic

product (GDP)

5 5 6 5 5

Current health expenditure (CHE) per capita in US$ 22 35 78 89 80

Domestic health expenditure (DOM) as % of current health

expenditure (CHE)

91 86 90 92 74

Domestic general government health expenditure (GGHE-

D) as % of current health expenditure (CHE)

21 20 36 48 35

Domestic private health expenditure (PVT-D) as % of

current health expenditure (CHE)

69 66 54 44 39

Domestic general government health expenditure as % of

general government expenditure

6 5 9 8 7

Out-of-pocket (OOP) as % of total expenditure on health 64 61 49 40 36

Domestic general government health expenditure (GGHE-

D) as % of gross domestic product (GDP)

1 1 2 3 2

Source: WHO Ghana Country Statistics [Accessed:31/10/2018]

Your access to

healthcare

Health Care Financing incidence (James Akazili – GHS, 2010)

• High and increasing reliance on health insurance

• Taxes are significant in the Ghana health system

• Health insurance is a key health care payment mechanism in Ghana, it is overall progressive

• Informal sector contributions is regressive

• The key to universal coverage is extension of coverage to informal sector workers who cannot contribute

Impacts of the NHIS (1)Your access to healthcare

Equity of enrollment and utilization in NHIS (Dr. Caroline Jehu-Appiah – GHS, 2010)

• Evidence of inequity in enrollment, however, once enrolled utilization is equitable

• The NHIS provides protective effect against OPD related OOP expenditure

• 73% of the insured paid OOP, although on average, the mean OOP payments were a third of what the uninsured paid

• For the uninsured poor, payments were catastrophic

Impacts of the NHIS (2)Your access to

healthcare

▪ Long-term financial sustainability

▪ Adoption of efficient provider payment methods

▪ Weak pharmaceutical supply chain

▪ Coverage of poor and vulnerable populations

▪ Quality of care challenges

▪ Lack of human resource capacity

▪ Pervasiveness of moral hazards

▪ Inadequate and non-optimized ICT systems

▪ Long-term financial sustainability

▪ Adoption of efficient provider payment methods

▪ Weak pharmaceutical supply chain

▪ Coverage of poor and vulnerable populations

▪ Quality of care challenges

▪ Lack of human resource capacity

▪ Pervasiveness of moral hazards

▪ Inadequate and non-optimized ICT systems

Challenges Ghana needs to address Your access to healthcare

…Your access to healthcare

IV. Challenges & Way Forward

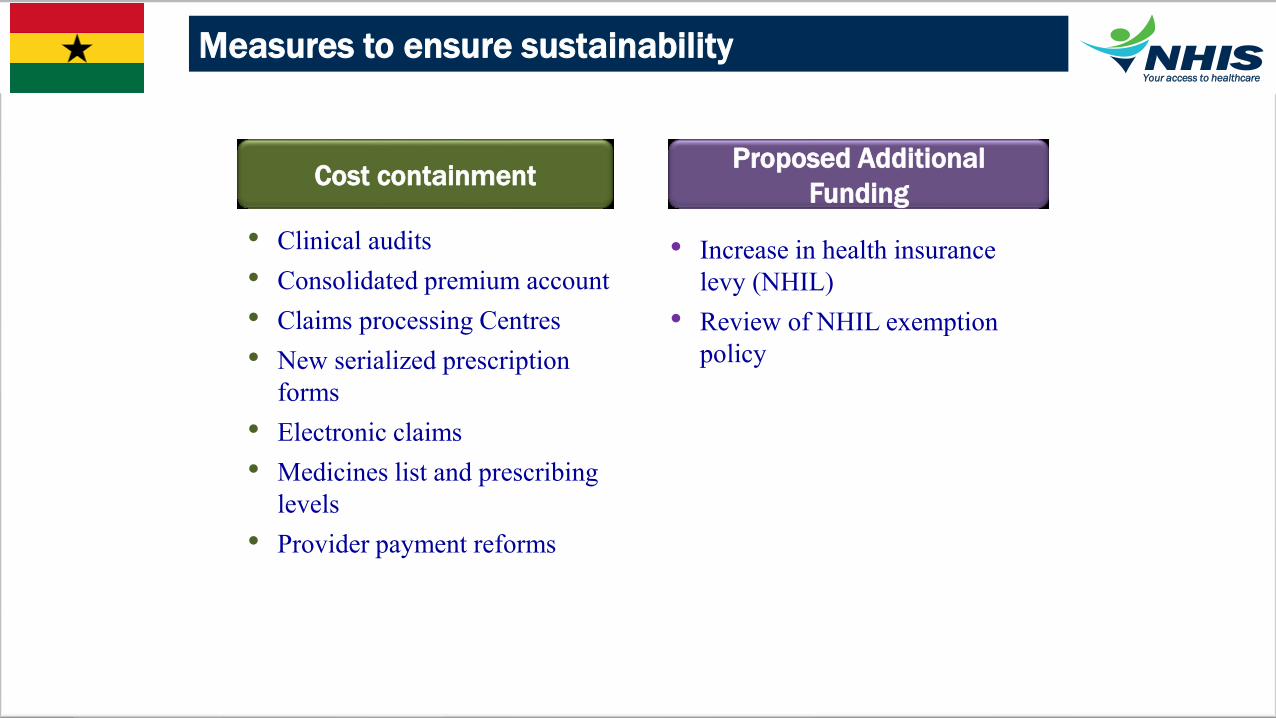

Measures to ensure sustainability

Cost containmentProposed Additional

Funding

• Clinical audits

• Consolidated premium account

• Claims processing Centres

• New serialized prescription

forms

• Electronic claims

• Medicines list and prescribing

levels

• Provider payment reforms

• Increase in health insurance

levy (NHIL)

• Review of NHIL exemption

policy

Your access to healthcare

…Your access to healthcare

IV. Challenges & Way Forward

Way Forward

• Pursue efforts at securing additional funding

• Intensify Clinical Audit

• Scale up electronic claims

• Improve computerization of operations

• Strengthen audit and risk management systems

• Enhance financial sustainability through cost containment

• Rationalize the benefit package

• Review the exemption regime

• Shorten claims processing and payment times.

Your access to

healthcare

ConclusionYour access to healthcare

• Ghanaian initiative, home grown and local leadership – Learning through experience and adaptation.

• Improved health seeking behaviour of subscribers/patients

• Over 90% of patients in both private and public facilities are health insurance subscribers.

• Over 80% of IGF of Public facilities are derived from the NHIS.

• High public confidence in the NHIS.

• Bi-partisan political will and support.

• Healthy collaboration, cooperation and support of the Ministry of Health

Your access to healthcareTHANK YOU