gep fm.qxd 12/5/02 4:16 PM Page i Global Economic Prospects

234

Global Economic Prospects and the Developing Countries 2003

Transcript of gep fm.qxd 12/5/02 4:16 PM Page i Global Economic Prospects

GlobalEconomicProspectsand the Developing Countries

2003

gep_fm.qxd 12/5/02 4:16 PM Page i

© 2003 The International Bank for Reconstruction and Development / The World Bank1818 H Street, NWWashington, DC, USA 20433Telephone: 202-473-1000Internet: www.worldbank.orgE-mail: [email protected]

All rights reserved.

1 2 3 4 04 03 02

This volume is a product of the staff of the World Bank. The findings, interpretations, andconclusions expressed herein do not necessarily reflect the views of the Board of ExecutiveDirectors of the World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. Theboundaries, colors, denominations, and other information shown on any map in this workdo not imply any judgment on the part of the World Bank concerning the legal status of anyterritory or the endorsement or acceptance of such boundaries.

Rights and Permissions

The material in this work is copyrighted. Copying and/or transmitting portions or all of thiswork without permission may be a violation of applicable law. The World Bank encouragesdissemination of its work and will normally grant permission promptly.

For permission to photocopy or reprint any part of this work, please send a request withcomplete information to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers,MA 01923, USA, telephone 978-750-8400, fax 978-750-4470, www.copyright.com

All other queries on rights and licenses, including subsidiary rights, should be addressed tothe Office of the Publisher, World Bank, 1818 H Street NW, Washington, DC 20433, USA,fax 202-522-2422, e-mail [email protected]

ISBN 0-8213-5338-1ISSN 1014-8906Library of Congress catalog card number: 91-6-440001 (serial)

gep_fm.qxd 12/5/02 4:16 PM Page ii

Contents

iii

Foreword ix

Acknowledgments xi

Summary xiii

Abbreviations and Data Notes xxi

Chapter 1 The International Economy and Prospects for Developing Countries 1A recovery constrained by major risks 4Investment cycles in developing countries 23Growth and poverty to 2015: coming changes in savings and

investment patterns 28Notes 41References 42

Chapter 2 Changes in Global Business Organization 45The surge in trade and FDI 46The rise in service sector FDI 52Global production networks 55Good policies attract FDI 66Notes 69References 71

Chapter 3 Domestic Policies to Unlock Global Opportunities 77Investment climate and investment policies 78Promoting efficient private investment: harnessing competition 85Public investment in infrastructure and human capital 103Policies to promote competition 107Notes 109References 110

gep_fm.qxd 12/5/02 4:16 PM Page iii

Chapter 4 International Agreements to Improve Investment and Competition for Development 117

International efforts to promote investment 119International agreements to promote competition and competition policy 133Conclusions 145Notes 146References 147

Appendix 1 Regional Economic Prospects 151

Appendix 2 Global Commodity Price Prospects 175

Appendix 3 Global Economic Indicators 199

Figures1.1 The recovery was initiated in a typical fashion 61.2 A brief rebound in industrial countries was underway 61.3 Rebound in industrial countries boosted production in East Asia 61.4 Non-oil commodities are recovering but stand well below previous peaks 71.5 Private sector creditors have cut debt exposures so far in 2002 91.6 FDI flows to emerging Asia are proving to be quite resilient 101.7 Investment recovery is still uncertain 101.8 World trade rebounds along with GDP, 1998–2004 131.9 2002 marks the start of a moderate recovery 151.10 LAC and MENA are not experiencing the recovery 151.11 Low case: world trade and other indicators will be much lower than

the baseline 201.12 G-7 investment falls sharply 211.13 Investment growth and net capital flows into Latin America are

strongly correlated 221.14 Oil prices spike 231.15 Investment is more volatile than GDP in East Asia 231.16 Investment is more volatile than GDP in Latin America 231.17 Central Europe and Turkey experience greater volatility in

investment than in GDP 241.18 Investment volatility declines with income 241.19 A better investment climate reduces volatility of investment cycles 251.20 Impact of policy climate on investment volatility after correcting for

income remains strong 251.21 Growth of working-age population decelerates 331.22 Productivity has not been the dominant source of growth in regions 351.23 Productivity is expected to be more significant in the longer term 351.24 Major structural shifts in investment and savings behavior have occurred 371.25 Youth dependency ratio will fall everywhere except Japan 391.26 Elderly dependency ratios will rise in some regions 392.1 Exports-to-GDP ratios have increased since the 1970s 472.2 All regions have benefited from rising FDI flows 472.3 FDI is concentrated in large countries, but many small countries receive large amounts

relative to GDP 48

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

iv

gep_fm.qxd 12/5/02 4:16 PM Page iv

2.4 The service sector dominated the 1990s mergers and acquisitions boom 492.5 Cross-border mergers and acquisitions are small compared with

stock market capitalization 492.6 U.S. aggregate concentration has held steady 502.7 Global concentration has not increased significantly 512.8 Share of FDI in the service sector increased in major industrial countries 522.9 U.S. cars are produced in many countries 552.10 Cross-border networks capture increasing shares of production and trade 562.11 The role of production networks continued to increase through

most of the 1990s 562.12 Tariff rates fell in the last two decades 572.13 Reforming countries boosted exports through production networks 582.14 Parts and components exports grew rapidly, 1981–2000 612.15 Developing countries’ share of global parts and component exports

rose between 1981 and 2000 612.16 Developing countries’ parts and component exports are highly

concentrated, 2000 622.17 Strong rule of law attracts foreign investors 662.18 Foreign investors have been shifting away from weaker investment

climate locations 672.19 Private infrastructure investment surged in the 1990s 683.1 Domestic capital is the largest source of investment in developing countries 783.2 Incentives for FDI are varied and numerous 803.3 Competition and ease of entry are associated with higher growth 863.4 Competition from imports checks markups in concentrated markets 873.5 High tariffs are correlated with lower productivity 883.6 High entry costs inhibit FDI inflows 903.7 Barriers to entry can become barriers to exit 923.8 Barriers to entry and exit allow inefficient firms to stay in the market 943.9 Difficulties in obtaining licenses and permits discourage FDI 943.10 Inefficient customs hurt Indian exports 953.11 Inefficient ports raise India’s transport costs far above competitors’

transport costs 953.12 Privatization revenues soared in the 1990s 963.13 Granting monopoly rights brings in revenues 983.14 More competition means more phones 983.15 Better infrastructure means higher growth 1053.16 Greater literacy is associated with higher growth 1063.17 Education raises the productivity of FDI, which leads to higher growth 1074.1 Countries are increasingly liberalizing their investment regimes 1234.2 South-South FDI is rising 1234.3 Share of South-South FDI in total FDI is rising 1244.4 Revealed preferences: governments shield services more often than

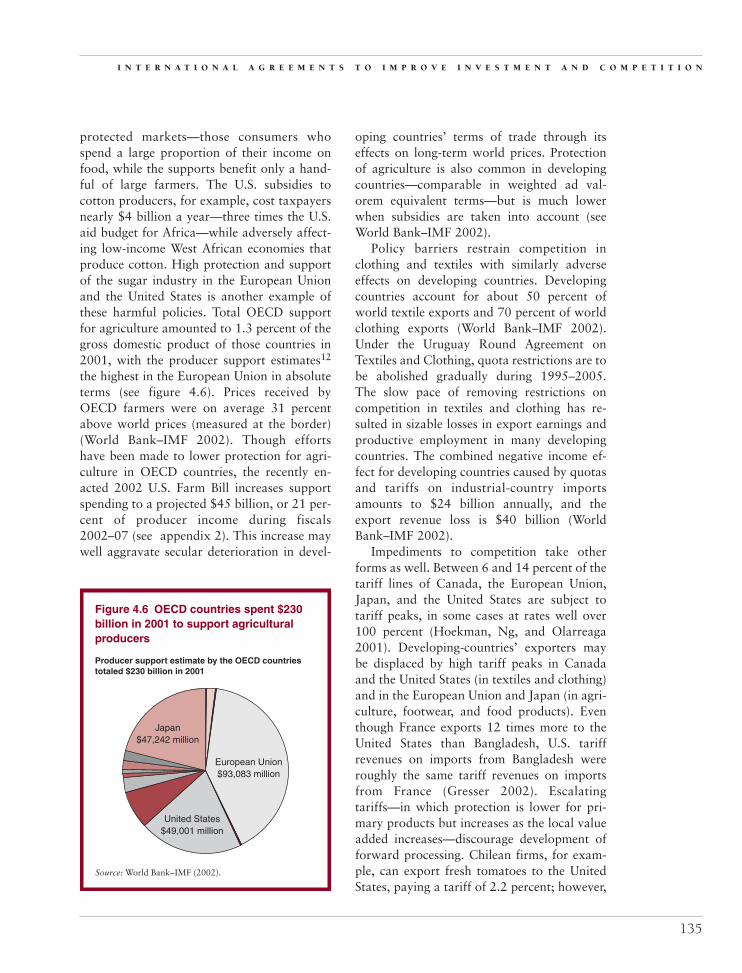

manufacturing from the winds of investment competition 1264.5 FDI is growing faster than exports and output 1284.6 OECD countries spent $230 billion in 2001 to support agricultural producers 1354.7 Imports affected by cartels rose from 1981 to 2000 for both rich and

poor countries 138

C O N T E N T S

v

gep_fm.qxd 12/5/02 4:16 PM Page v

Tables1.1 Global conditions affecting growth in developing countries and

world GDP growth 31.2 External environment for developing countries, 1991–2004 141.3 Global effects in a low-case scenario, 2003–04 201.4 Low case: contributions to global effects in 2003 211.5 Relative volatility of investment is high in developing countries 241.6 Upturns can be financed abroad and domestically 261.7 Capital inflows lead investment in middle-income countries: correlation

between investment ratios and (past or future) capital flows 261.8 Long-term prospects are projected to be stronger for most regions 291.9 Large poverty reductions in EAP and SAR partially offset by

poverty increases in SSA 301.10 Savings fall in high-income countries, but increase in most other regions 382.1 FDI inward stocks in services and manufacturing, 1988–99 522.2 Growth of exports of parts and components, 1981–2000 552.3 Export activity for product groups with the fastest growth in

world exports, 1980–98 622.4 Rapid growth and structural change experienced by

network participants 653.1 Profitability on equity, concentration, and market share (percent):

Brazil, 1971–78 993.2 Cartel enforcement in selected developing countries 1014.1 Many antidumping investigations were initiated during the 1995–2001

period 1364.2 International cartels can be expensive: estimates of sales and overcharge 1384.3 National exemptions to competition law for exporters 1414.4 Breaking up floating cartels could help developing countries 142

Boxes1.1 Is Latin America going against the rising tide? 81.2 Integration pays off where policies are supportive 121.3 The terrorist attacks of September 11, 2001 had an economic impact 161.4 Consumption in low- and middle-income countries is smoothed over

the business cycle 271.5 Is the World Bank overestimating global poverty? 311.6 Technological progress is an important determinant of growth 342.1 Intra-firm trade increases worldwide 593.1 Trade restrictions shield MNCs from competitive forces at enormous cost:

the case of Argentina 893.2 Competition policy and competition law share similar objectives

across countries 1023.3 Does public investment “crowd out” or “crowd in”

private investment? 104

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

vi

gep_fm.qxd 12/5/02 4:17 PM Page vi

4.1 What is a BIT? 1204.2 The Multilateral Agreement on Investment (MAI) 1224.3 South-South flows: who invests and who receives? 1254.4 Do BITs increase investment flows? Only a bit 1294.5 Disciplines on corporations can also improve the investment climate 1324.6 The lysine cartel, 1995–2001 1394.7 International cooperation aids competition policy 144

C O N T E N T S

vii

gep_fm.qxd 12/5/02 4:17 PM Page vii

gep_fm.qxd 12/5/02 4:17 PM Page viii

Foreword

ix

Productivity increases and efficient investment are essential conditions for rapid growth andpoverty reduction. The key to accelerating technological improvement and increasing in-vestment is improving the “investment climate.” In the broadest sense, this term encom-

passes the policy and institutional environment that fosters entrepreneurship, learning, and pro-ductive investment.

In this report, we argue that the investment climate for developing countries has both a globaldimension and a national dimension. The global investment climate, although less amenable topolicy initiatives of developing countries, nonetheless presents opportunities, risks, and at timesobstacles for developing countries. In this report, we focus on two aspects of the global invest-ment climate: the current state of the world economy as it affects developing countries’ financialoutlook, exports, and growth prospects (chapter 1) and the organization of global business,notably the proliferation of multinational companies and associated production networks (chap-ter 2). In previous reports we have studied other aspects of the global investment climate, in-cluding the world trading system (Global Economic Prospects 2002) and aspects of the globalfinancial system (Global Development Finance 2002).

The national dimension of the investment climate for developing countries is discussed inchapter 3. This dimension is composed of the policy and institutional environment that fostersentrepreneurship—and that strongly influences the pace of productivity growth and the rate ofinvestment. Differences in national policies help explain why some countries grow rapidly andothers do not, even though all operate within the same international investment climate. In short,policymakers have considerable scope for choosing policies that influence the amount and pro-ductivity of investment.

For the purposes of this report, we focus on two types of national policies that affect howcountries use globalization to grow. The first type is investment policies—for example, tax in-centives, tariffs, subsidies, and policies to channel investment into particular activities, as well aspublic investment. The second type is policies that promote or limit competition—for example,tariffs, entry restrictions, and state monopolies as well as conventionally defined competitionpolicy.

We chose these policy areas for three reasons. First, these policy areas directly link the do-mestic policy dimensions of the investment climate with the global economy. Second—in contrastto macroeconomic policies, property rights, and other institutional features that primarily affectthe quantity of investment—policies fostering investment and competition work instead throughmicroeconomic incentives to influence the quality of investment (as measured by its productivity).Finally, these policies are at the center of global debate, figuring prominently in discussions of the

gep_fm.qxd 12/5/02 4:17 PM Page ix

Doha Development Agenda launched at the World Trade Organization (WTO) Ministerial Meet-ing in November 2001.

To inform that debate, the final chapter of this report asks how the international communitycan support developing countries in their quest for better investment climates, both global andnational. The chapter focuses on synergies that can emerge from developing countries’ participa-tion in international agreements on investment and competition policies, topics that are not onlycentral to the WTO Doha Development Agenda but that also figure prominently in manyregional trade negotiations around the world.

Nicholas SternChief Economist and Senior Vice PresidentThe World Bank

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

x

gep_fm.qxd 12/5/02 4:17 PM Page x

Acknowledgments

xi

This report was prepared by the Development Prospects Group in the World Bank, draw-ing on resources throughout the Development Economics Vice Presidency and the WorldBank’s operational units. Richard Newfarmer was the lead author and manager of the

report, under the direction of Uri Dadush. The principal chapter authors were Hans Timmer(chapter 1), William Shaw (chapter 2), Jeffrey Lewis and Scott Wallsten (chapter 3), and RichardNewfarmer and Pierre Sauvé (chapter 4). We are grateful for the ideas and insights of BernardHoekman, Michael Klein, and Theodore Moran (Georgetown University). The report was pre-pared under the general guidance of Nicholas Stern.

Many staff from inside and outside the World Bank contributed to the report. In chapter 1,Caroline Farah, Himmat Kalsi, Robert Keyfitz, Annette I. De Kleine, Robert Lynn, FernandoMartel Garcia, Mick Riordan, and Bert Wolfe contributed to the global trends; Dominique Vander Mensbrugghe provided the long-term analysis; and Shaohua Chen and Martin Ravallioncontributed to the poverty analysis; Kathleen Rollins was the staff assistant. Chapter 2 benefitedfrom background papers and other inputs from Gary Gereffi, Mary Hallward-Driemeier, ShafiqIslam, Frances Ng, Matthew Slaughter, Lawrence White, and Yong Zhang. Similarly, in chapter 3,Claudio Frischtak, Rughvir Khemani, Kamal Saggi, Luis Villela, and Alberto Barreix as wellas Mary Hallward-Driemeier provided background papers that became building blocks for thesections on incentives, investment, competition, and foreign investment, and Denis Medvedevprovided valuable written inputs and research assistance. Chapter 4 was based on backgroundpapers by Simon Evenett and Benno Ferrarini (competition), Bijit Bora (performance require-ments), and Mary Hallward-Driemeier (bilateral investment treaties and investor protections) aswell as inputs from Aaditya Mattoo and Shweta Bagai (various). Beata Smarzynska and JacquesMorisset provided helpful guidance and comments on various aspects of the report. The regionalappendixes benefited from the written inputs of the Regional Chief Economists around the Bankand their staff. John Baffes, Betty Dow, Donald Mitchell, and Shane Streifel prepared the com-modity appendix. The staff assistant for the report was Awatif Abuzeid. Mark Feige provided ed-itorial assistance. Yinne Yu and Yong Zhang as well as Jonathan Koh provided valuable researchassistance at various stages of the report’s preparation. Dorota Nowak coordinated publicationand dissemination activities.

Several experts provided written comments that immeasurably improved the quality of the re-port at various stages: Pierre-Richard Agenor, Robert Anderson, Milan Brahmbhatt, Jean-JacquesDethier, Simeon Djankov, Richard Eglin, Antonio Estache, Shahrokh Fardoust, Alan Gelb,Coralie Gevers, Ian Goldin, Rughvir Khemani, Aart Kraay, Ernesto May, Mustapha Nabli, Anne

gep_fm.qxd 12/5/02 4:17 PM Page xi

McGuirk, Ashoka Mody, Ijaz Nabi, John Panzer, Guillermo Perry, Guy Pfeffermann, KarlSauvant, Todd Schneider, Mark Sundberg, and Roberto Zagha.

We are also grateful for the many substantive comments we received from governmentsaround the world through their Executive Directors on the World Bank’s Board.

Melissa Edeburn, Susan Graham, and Ilma Kramer managed the production for the WorldBank’s Office of the Publisher.

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

xii

gep_fm.qxd 12/5/02 4:17 PM Page xii

Summary

xiii

The global recovery is fragile, becauseinvestment spending is insufficient tounderpin continuing growth—Strong cyclical dynamics, together with aneasing of macroeconomic policies in theUnited States and elsewhere, have boostedlarge parts of the global economy into the ini-tial phase of a recovery in 2002. The drivingforces behind the initial phase of the recoverywere strong, but they have proved short-livedbecause inventory and high-tech cycles areshort and appear to have peaked. Thoughconsumption spending has held firm, this isprecisely the time when investment demandshould pick up and boost recovery onto ahigher trajectory. So far it has not. Financialimbalances, evident in different formsthroughout the world economy, seem to beweighing down growth. Wide-ranging uncer-tainty in financial markets may jeopardize theneeded rebound in fixed investment and maythus diminish prospects for projecting theglobal recovery into the future. Falling andvolatile stock markets, accounting scandals,accumulated debts (domestic and foreign, pri-vate and public), and reassessments of long-run profitability keep investors cautious, ifnot jittery, throughout the world. For thesereasons, growth in 2003 seems certain to beweaker for almost all developing regions thanwe anticipated as recently as six months ago.

Analysis of long-term trends indicates thatthe investment cycle as a determinant of over-all cyclical behavior is as important in low-

and middle-income countries as it is in high-income countries. But the volatility of invest-ment is greater in developing countries than inrich countries. Countries with sound invest-ment climates experience far less volatilitythan countries with deficient policies andinstitutions.

Capital flows to developing countries haveproved to be procyclical. But the direction ofcausality between investment and capital in-flow appears to differ significantly betweenrich and poor countries. In rich countries, aboom in domestic fixed investment tends toattract foreign capital, while in middle-incomecountries it is the acceleration of capitalinflows that typically stimulates domesticinvestment. Similarly, a fall in rich countries’investment tends to reduce net capital inflows,while for middle-income countries reduced netcapital inflows (or increased capital outflows)are the driving forces behind contractions indomestic investment. This dependence on cap-ital flows makes the middle-income countriesespecially vulnerable to tensions in global fi-nancial markets. Low-income countries, withgreater reliance on official aid and with lim-ited access to private capital markets, do notexhibit either of these patterns.

—but long-term prospects remainpromisingOver the long run, new opportunities fortechnological advances (often driven byglobalization), together with more stable

gep_fm.qxd 12/5/02 4:17 PM Page xiii

macroeconomic policies and an improvedbusiness climate, have the potential to acceler-ate growth and to increase investment ratiosin developing countries that currently lagbehind. The outlook for reductions in globalpoverty, while generally positive and of thesame order of magnitude as in our previousreport, is marginally dimmer because of theabsence of a robust recovery today.

At the same time, demographics are likelyto alter existing savings and investment pat-terns and will tend to push countries to be-come more interdependent through capitalflows. Major demographically driven shifts incurrent account balances—particularly inJapan, which is moving toward reduced sur-plus, and in middle-income countries, whichare moving toward increased surplus—arelikely to accelerate financial integration.Underneath large swings in net flows are evenlarger movements of gross capital flows, asforeign direct investment (FDI) expands intogrowing markets in developing countries andas financial agents in developing countriesseek to diversify their portfolios in rich coun-tries. However, because international financialflows have at times fluctuated widely, theyhave sometimes proved damaging to growthand poverty reduction. The international com-munity and developing countries have tosearch for mechanisms to provide greater sta-bility in integration. Developing countries cando much on their own. Improving the domes-tic investment climate, particularly throughsound macroeconomic policies and gover-nance, can reduce the volatility of capitalflows and attract less-volatile FDI.

Global competition is creating newopportunities for developing countriesCross-border trade and direct investment haveexpanded rapidly over the past three decades.Global exports of goods and services in-creased from 14 percent of output in the early1970s to 23 percent by the late 1990s, whileglobal FDI flows have more than doubled rel-ative to the gross domestic product (GDP).The surge in FDI flows accelerated in the late

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

xiv

1990s, rising from $331 billion in 1995 to$1.3 trillion in 2000, before falling off to anestimated $725 billion in 2001. Most of theseflows are destined to rich countries.

FDI flows to developing countries areabout $160 billion. This amount is still rela-tively small compared with all domestic in-vestment in developing countries, now about$1 trillion. Nonetheless, in virtually every re-gion, FDI is a driving force of globalizationand has risen relative to total capital expen-ditures during the 1990s. It has doubled inmiddle-income countries and has tripled inlow-income countries. However, recently FDIflows have fallen. They peaked in 1999 at$184 billion and are experiencing their mostsustained fall since the global recession of1981–83.

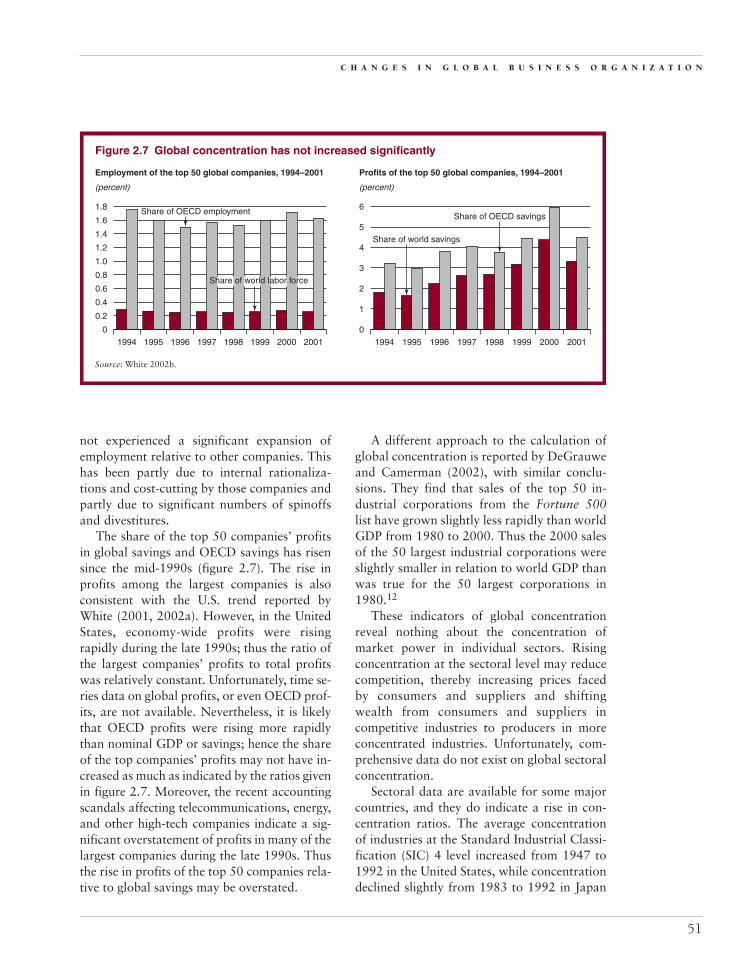

These trends over the past decade have in-creased competition in most markets aroundthe world. Despite a sharp increase in mergersand acquisitions, the share of global economicactivity accounted for by the largest compa-nies does not appear to have risen over the1990s. The profits of the top 50 companies ac-counted for 0.8 percent of world GDP in2001. Although their share of aggregate prof-its amounted to 3.3 percent of global savingsin 2000, up from 1.8 percent in 1994, this in-crease is likely to be the result of the boom inthe United States and the overstatement ofearnings of some large U.S. corporations.These factors point to a pattern of stabilityrather than a trend of increases. Similar pat-terns exist for the largest 500 companies.

Four changes in the organization of busi-ness are particularly important for developingcountries. First, the rise of foreign investmentin services is creating a new source of compe-tition—and potential productivity gains—indeveloping countries, where staid state com-panies have often monopolized production fordecades. Recent efforts to privatize these com-panies and to open industries to competitionhave allowed some developing countries toharness this competition for gains. In manydeveloping countries, restrictions on servicesstill remain high, because some countries have

gep_fm.qxd 12/5/02 4:17 PM Page xiv

privatized only slowly and others have priva-tized badly, creating private monopolies stillinsulated from competition.

Second, production networks that span theglobe, once barely a dot on the horizon of in-ternational business, have now become a cen-tral feature. That so many large firms havechosen to outsource production of parts andequipment or to otherwise locate productionfacilities offshore offers new opportunitiesfor developing countries. Firms choosing to“deverticalize” production through outsourc-ing create new opportunities for suppliers andcreate a foundation for a steady increase intrade for participating developing countries.The downside is that this production and theassociated high rates of export growth arehighly concentrated geographically, and sothis door into a greater share of the globaleconomy has, to date, opened only for rela-tively few countries. Taking advantage ofnetworks requires a strong policy environ-ment that fosters private investment and pro-vides complementary public investments (seebelow).

Third, with growing concerns about risk,investors are becoming increasingly sensitiveto investment climates in developing coun-tries, and the result is that money is moving tothe countries with large, rapidly growing, andrelatively stable economic environments.Countries such as China, the Republic ofKorea, and Mexico benefited from the largestinflows in 2000. As a share of domestic in-vestment, however, small-market countries areproving they can keep pace—provided thatthey protect property rights, have stablemacroeconomic environments, and have goodinstitutions. Poor countries that fall short onpolicies and institutions compound the disad-vantages they already experience from havingsmall markets. Hence, they may be virtuallyshut out from foreign investment flows in anysector other than natural resources.

Finally, long-term private investment fi-nancing for infrastructure has fallen off tolevels that may prove persistent. This retrench-ment has two origins. First, the post-1997 rise

S U M M A R Y

xv

in global risk premiums has reduced investors’appetite for risk and for projects with long ges-tations. Adversity to such projects is reflectednot only in the average spreads over U.S. Trea-sury interest rates that developing countriesmust pay to their bondholders in the EmergingMarket Bond Index (even excluding country“outliers” in crisis) but also more generally inspreads of high-risk corporate bonds in theUnited States. Both have more than doubledfrom under 500 basis points to more than1,000. The recent collapse of the telecommu-nications sector, as well as difficulties experi-enced by major power companies associatedwith the Enron scandal, has diminished thenumber of players and enthusiasm amongpotential long-term financiers. Second, manyprojects have suffered payment problemsbecause of the inability of contracts to weathersharp contractions in demands. FromArgentina to Indonesia, the string of defaultsassociated with infrastructure projects and re-structurings has left in its wake a severe re-trenchment. Thus, governments throughoutthe developing world will have to do more tooffset this risk—principally through betterpolicies, and perhaps through a slowing of theretreat from government financing of infra-structure that has occurred under the bannerof privatization.

Harnessing globalization requiresreducing barriers to competition—To raise the productivity of both foreign anddomestic investment, developing countrieshave to harness the full force of competitioninherent in globalization. Too often they havenot done so. In many countries, policy barri-ers to competition—whether they are im-pediments to trade, restrictions on incomingforeign investment, administrative barriers tocompetition, or monopolies granted to stateenterprises—have channeled domestic as wellas foreign investment into less-productiveactivities that dampen productivity improve-ment and hobble growth. Import competition,for example, can limit what would otherwisebe the shared monopoly pricing of a few local

gep_fm.qxd 12/5/02 4:17 PM Page xv

producers. In a wide sample of developingcountries, decreasing imports in concentratedindustries from 25 percent of domestic sales tozero is associated with increases of 8 percentin oligopolistic markups on sales.

Competition-impeding regulations in re-cently privatized industries have underminedpotential benefits from privatization and haveinsulated new owners—frequently foreigncompanies—from efficiency-improving com-petition; the result has been slow growth andresource misallocation. In Africa, for example,telephone services in countries with privatemonopolies have expanded growth only one-third as fast as telephone services in countrieswith competitive networks.

Over time, firms in countries with lowerbarriers to trade and to investment competi-tion tend, as a general rule, to enjoy signifi-cantly higher productivity of investment, bothforeign and domestic, and with it more rapidgrowth. This fact does not imply a single pre-scription for all countries irrespective of theirstage of development. As the experience ofChina—among others—has shown, reformshave to be tailored to country circumstancesand integrated into sustainable developmentstrategies. The analysis does imply, however,that countries wishing to increase their oppor-tunities from globalization would do well tolook first at the incentive features of theirinvestment climate, with special attention tobarriers that impede competition.

—and using targeted interventions with care—Governments may hope to make up for anunfriendly investment environment through in-centive mechanisms. But while there are clearlyexamples in which targeted interventions—such as fiscal incentives, export processingzones (EPZs), or support for economic clus-ters—may indeed lead to higher investmentlevels (and the jobs and related spillovers thatgo along with them), there is, unfortunately,little evidence that such initiatives can besystematically successful. Instead, they tend towork best when they work in support of

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

xvi

broader reform packages, either to catalyzesupport for emerging opportunities (such asclusters) or to create transitional mechanismsand initial constituencies for reform that canbe progressively expanded (such as EPZs). Butmore broadly, investment incentives will gen-erally not make up for serious deficienciesin the investment environment or generatesustained growth. To encourage productiveinvestment and benefit from globalization,governments must tackle the challenges ofpromoting competition and entrepreneurshipand of undertaking complementarily pro-ductive public investment in areas such aseducation.

—and therefore sound public investmentsare essentialPublic investment also plays a crucial role inenhancing growth. Some countries get boththe levels and the composition of investmentright, and their growth rates are high. Othercountries invest too much through the publicsector and crowd out private investment.Because these effects are also associated withinvestments in state enterprises that enjoy mo-nopoly positions protected from competition,the composition effects of public investmentare negative. Other countries invest too littlethrough the public sector. This problem is usu-ally manifested in poor education, poor in-frastructure, and poor public institutionsgenerally—all of which reduce profitable in-vestment opportunities for both domestic andforeign companies. Investing in effective pub-lic institutions has an especially high return.

International agreements on investmentand competition policies can providebenefits through reciprocity—Countries get most of the positive growthstimulus from domestic unilateral reformstailored to local strategy and conditions, andthese reforms should not be held hostage tointernational agreements. Nonetheless, re-forming governments may be able to obtainadditional benefits from international agree-ments. Benefits can take several forms. For

gep_fm.qxd 12/5/02 4:17 PM Page xvi

investment policies, participating in interna-tional agreements that are linked to greatermarket access may elicit more investment bysignaling to investors that changes are perma-nent. Also, participating in international nego-tiations may strengthen the hand of domesticreformers by holding out the prospect of mar-ket access abroad in exchange for new domes-tic policies; simultaneously, negotiations canprompt reciprocal reforms among partnersthat would not otherwise occur. For competi-tion policy, international agreements may leadto the removal of restraints that inhibit com-petition, thereby unleashing new price compe-tition that benefits all countries.

—but agreements on investment policy arelikely to have strong development effectsonly if they deal with the big issues facingdeveloping countries—The purposes of coordinating investmentpolicy are to expand the flow of investmentaround the world, to minimize policy exter-nalities that hurt neighbors, and to helpimprove economic performance. Agreementsmight contribute to achieving these goalsthrough three main channels: protectinginvestors’ rights, which increases incentives toinvest; liberalizing investment flows, whichpermits enhanced access and competition; andcurbing policies that may distort investmentflows and trade at the expense of neighbors.

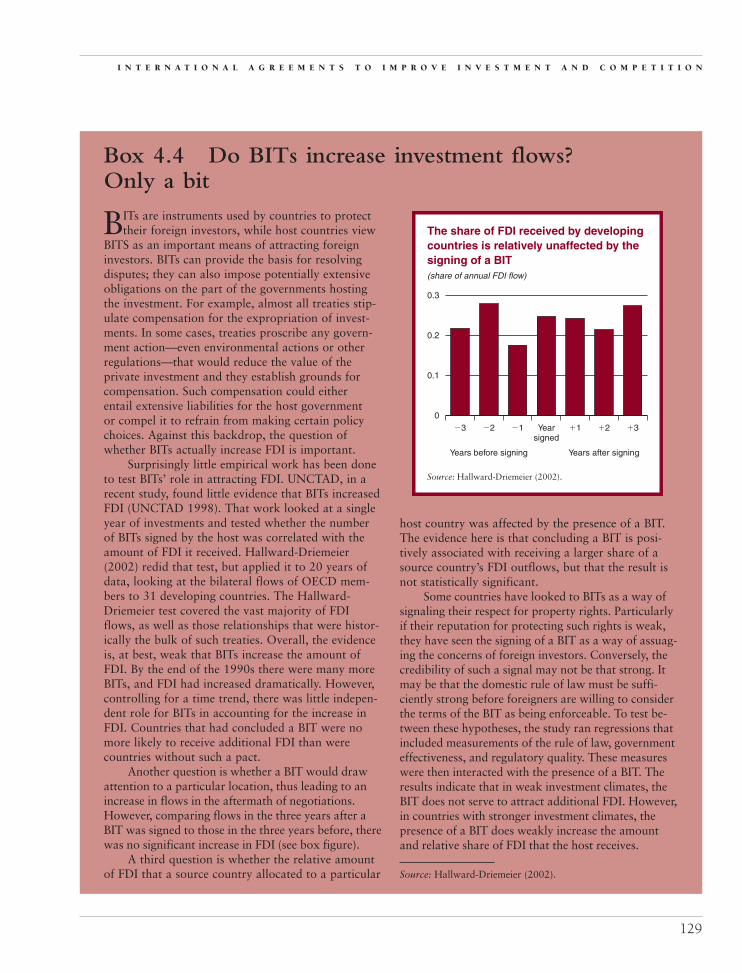

International agreements that focus on es-tablishing protections for investors cannot beexpected to expand markedly the flow of in-vestment to new signatory countries. This isbecause many protections are already con-tained in bilateral investment treaties (BITs).Even the relatively strong protections in BITsdo not seem to have increased flows of in-vestment to signatory developing countries.These facts suggest that expectations for newflows associated with protections emergingfrom any multilateral agreement should bekept low.

International agreements that allow coun-tries to negotiate reciprocal market liberaliza-tion and to promote nondiscrimination can

S U M M A R Y

xvii

reinforce sound domestic policies and cancontribute to better performance. Since mostof the remaining restrictions are on services,governments around the world can increasemarket access by using the existing multilat-eral framework rather than creating a newone. The General Agreement on Trade in Ser-vices (GATS) provides an as-yet-underutilizedarrangement to negotiate reciprocal marketaccess in services. To date, the coverage ofcommitments for a large number of countriesis limited. About two-thirds of the WorldTrade Organization membership has sched-uled 60 or fewer sectors (of the 160 or so spec-ified in the GATS list). Moreover, in manycases, commitments do not reflect the actualdegree of openness. Finally, in some countries,the commitments that have been made serveonly to protect the privileged position of in-cumbents rather than enhance the contestabil-ity of markets. To remedy these problems,governments must take greater advantage ofthe opportunity offered by the GATS to lendcredibility to reform programs by committingto maintain current levels of openness or byprecommitting to greater levels of futureopenness. To advance the process of servicesreforms beyond levels undertaken indepen-dently and to lead to more balanced outcomesfrom the developing-country point of view,countries could better harness the power ofreciprocity by devising negotiating formulasthat widen the scope for tradeoffs across sec-tors (both in goods and in services) and acrossmodes of delivery, particularly the temporarymovement of workers. While difficult, such ef-forts may prove easier than designing a wholenew international investment arrangement.

Similarly, curbing policy externalities that“beggar thy neighbor” can benefit developingcountries, especially if the countries focuson two critical issues. The first is to reduceinvestment-distorting trade barriers. By de-priving developing countries of market accessand by discouraging their exports, many tradebarriers also lessen the attractiveness of oppor-tunities to invest in developing countries’ ex-port industries for both foreign and domestic

gep_fm.qxd 12/5/02 4:17 PM Page xvii

investors. In Canada, the European Union(EU), Japan, and the United States, average advalorem–equivalent tariffs for manufacturesare roughly twice as high for developing coun-tries as they are for members of the Organisa-tion for Economic Co-operation and Develop-ment. The ad valorem–equivalent tariffs onagriculture (to say nothing of subsidies) inthose countries are also more than three timeshigher than such tariffs on manufactures. Re-ducing trade barriers among developing coun-tries themselves is as important as reducingtrade barriers in rich countries. Developingcountries import from each other at average advalorem–equivalent rates comparable to EUrates for imports from developing countries.This level of protection dampens investment—both domestic and foreign—in affected exportindustries, and removal of these barrierswould have significant development effects.

The second critical issue is to curb theemerging competition among countries to lureforeign investment through investment incen-tives. Unfortunately, information on the ex-tent of investment incentives is inadequate toassess their effects, and so a high priority forinternational collaboration is to systematicallycompile this information.

Finally, participation in international agree-ments on investment may also have benefitsover and above unilateral reforms if the agree-ments include reciprocal market access inareas of importance to developing countries.These benefits can become clear only in thecourse of negotiation.

—and thus competition agreements shouldfocus on restraints to competition thathurt developing countriesGreater competition is associated with morerapid development, and lowering policy barri-ers to trade and foreign investment in devel-oping countries, as shown in chapter 3, is apowerful procompetitive force. Beyond unilat-eral actions, international agreements on com-petition policy might also bring benefits, pro-vided they address the major restrictions thatadversely affect developing countries.

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

xviii

Restrictions on competition in the globalmarketplace that most hurt development takethree forms. The first form consists of policybarriers in markets abroad that limit competi-tion among developing countries in thesemarkets. These barriers, like those discussedabove, discourage investment and create ob-stacles to competition. Particularly harmfulare the $311 billion in agricultural subsidiesand textile quotas, as well as the correspond-ing high border protection, tariff distortions(that is, tariff peaks and escalation), and pro-tectionist use of antidumping. These practicesare only too common in all countries, rich andpoor alike. All of these trade restrictions limitthe ability of exporters in developing countriesto compete in international markets.

Second, private restraints on competitioncan adversely affect prices for consumers andproducers in developing countries—much asthey can in industrial countries. For example,cartel practices among companies based inhigh-income countries taxed consumers indeveloping countries by up to $7 billion in the1990s. Actions that facilitate prosecution ofcartels should be high on the priority list. Suchactions can range from developing more sys-tematic arrangements to exchange informa-tion among competition agencies, to grantingstanding for developing countries to sue underforeign antitrust laws when their trade is ad-versely affected. Indeed, both developing andindustrial countries would benefit from muchgreater efforts to identify and document re-strictive business practices that adversely af-fect prices of their trade.

Third, many governments in high-incomecountries officially sanction trade restraintsthrough antitrust exemptions for their compa-nies in domestic law. For example, many gov-ernments permit their companies to cartelizeexports. Shrouded in the secrecy of governmentregistries, these national export cartels maywell raise prices to developing countries. Ef-forts should be made to make information onnational export cartels transparent. Everyonewould benefit from a decrease in cartels thathave damaging price effects. Similarly, antitrust

gep_fm.qxd 12/5/02 4:17 PM Page xviii

exemptions for ocean transport have given riseto price-fixing arrangements that systematicallyhurt consumers everywhere, including those indeveloping countries. These restraints are esti-mated to cost developing countries more than$2 billion per year and entail similar costs toconsumers in industrial economies.

Finally, competition policies in developingcountries themselves can in many cases beimproved through increased transparency,nondiscrimination, and procedural fairness.However, international cooperation in thiscomplex area of regulation has to recognizethat countries have different capacities andinstitutional settings, warranting caution inrecommending—much less in mandating—across-the-board policies. In this area, volun-tary programs that facilitate the learning and

S U M M A R Y

xix

adoption of best practices in developing coun-tries can pay high dividends.

Unlocking global opportunities begins withthe efforts of developing countries to improvetheir investment climates. Deployed well, in-vestment policies and policies to unleash com-petition can accelerate economic growth andreduce poverty. This report offers a generalframework and lessons, but each country hasto formulate its own development strategy.Nonetheless, the international community,working together, can help through develop-ment assistance, voluntary collaboration, andwell-conceived international agreements. Forthese efforts to have greatest effect, they haveto tackle the most pressing investment andcompetition problems—and that is the chal-lenge ahead.

gep_fm.qxd 12/5/02 4:17 PM Page xix

Abbreviations and Data Notes

xxi

ADB Asian Development Bank

ASCM Agreement on Subsidies and Countervailing Measures

BITs Bilateral Investment Treaties

EPZ Export processing zone

EU European Union

FDI Foreign direct investment

FSAP Financial Sector Assessment Program

GATS General Agreement on Trade in Services

GPA Government Procurement Agreement

HIV/AIDS Human immunodeficiency virus/acquired immune deficiency syndrome

ICC International Chamber of Commerce

ICN International Competition Network

ICSID International Center for Settlement of Investment Disputes

IMF International Monetary Fund

ITO International Trade Organization

LDC Least developed countries

M&A Mergers and acquisitions

MAI Multilateral Agreement on Investment

MERCUSOR Latin America Southern Cone trade bloc (Argentina, Brazil, Paraguay, andUruguay)

MFN Most favored nation

MNCs Multinational corporations

NAFTA North American Free Trade Agreement

NGO Nongovernmental organization

OAS Organization of American States

OECD Organisation for Economic Co-operation and Development

ROSC Reports on the Observance of Standards and Codes

SOEs State-owned enterprises

gep_fm.qxd 12/5/02 4:17 PM Page xxi

TNCs Transnational corporations

TRIMs Trade-Related Investment Measures

TRIPS Trade-Related Aspects of Intellectual Property Rights

U.S. BEA U.S. Bureau of Economic Analysis

UNCITRAL United Nations Commission on International Trade Law

UNCTAD United Nations Conference for Trade and Development

UNDP United Nations Development Programme

USAID U.S. Agency for International Development

WTO World Trade Organization

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

xxii

Data notesThe “classification of economies” tables atthe end of this volume classify economies byincome, region, export category, and indebt-edness. Unless otherwise indicated, the term

“developing countries” as used in this vol-ume covers all low- and middle-income coun-tries, including countries with transitioneconomies.

gep_fm.qxd 12/5/02 4:17 PM Page xxii

Developments in early 2002 showed acyclical rebound—Macroeconomic stimulus, a rebound from arecord trough in the high-tech sectors anda bottoming-out of inventory cycles, broughtlarge parts of the global economy onto a re-covery path at the end of 2001. Lower interestrates helped keep consumers’ demand fordurable goods strong. Together with fiscal eas-ing, that demand provided support for therebound in the United States and, to a lesserextent, in some East Asian and Europeancountries. High-tech markets—in which tech-nologies quickly become obsolete—returnedto strong growth by creating replacements forold products. Inventory selloffs ceased, therebycontributing to an acceleration of gross do-mestic product (GDP) growth in early 2002.

The driving forces behind the initial phaseof the recovery were strong, but short-lived, asbusiness confidence remained weak. Inventoryand high-tech cycles typically are short, andboth appear to have peaked toward the middleof 2002. The effects of fiscal stimulus andmonetary easing can also, under current cir-cumstances, dissipate quickly.

—but uncertainty in financial markets hassapped momentum In the second phase of a typical recovery, theupturn spreads to other sectors and otherregions, and the driving force shifts from in-ventory dynamics to accumulation of fixedinvestment. In the current upswing, however,

the second phase is in jeopardy because of ten-sions in financial markets, which reflect accu-mulated financial imbalances and significantuncertainties. These pressures have made therecovery in 2002 less uniform, and they arelikely to moderate growth in 2003.

In Japan, deflation and high and rapidlygrowing government debt have placed severelimits on both monetary and fiscal stimuli.Combined with the fragility of the bankingsector, which is burdened by bad loans anddiminishing capital caused by lower equityvalues, financial uncertainty prevents thespread of recovery from export sectors tothose that produce for the domestic market.The accounting scandals in the United Stateshave undermined the trust in reporting sys-tems. Investors, who have come to rely oncontinuously rising equity prices, now find itdifficult to assess the profitability of firms.That difficulty sharply pushed up risk premi-ums in equity markets. European financial in-stitutions were forced to adjust their balancesheets in the wake of large-scale defaults,notably by Argentina and several majorU.S. firms, which probably played a role insuppressing a nascent recovery in Europeaneconomies. In Europe and elsewhere, telecom-munication sectors still suffer from overin-vestment and high debt burdens, making aspeedy recovery of capital spending in thosesectors unlikely.

Uncertainty is keeping investors cautious,if not skittish, throughout the world. While

1

1The International Economy andProspects for Developing Countries

1

gep_ch01.qxd 12/5/02 4:15 PM Page 1

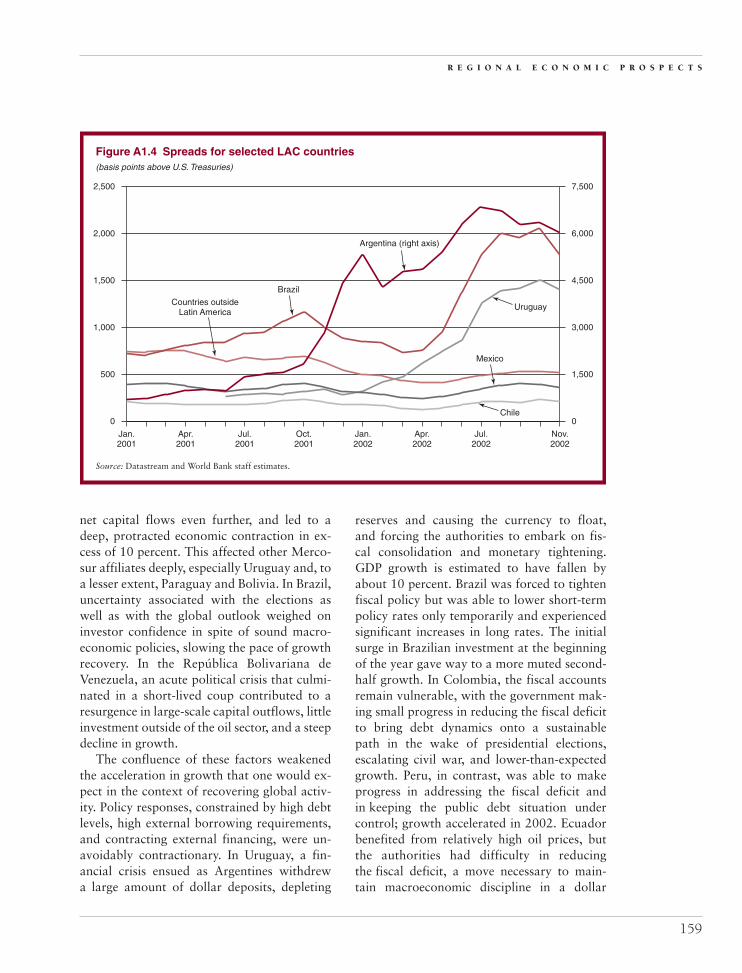

investors in high-income countries take theirlosses and replenish their reserves, they limittheir exposure to developing countries andconcentrate their assets in investment-gradeborrowing countries.1 Capital flows into largeparts of Latin America dropped sharply, re-flecting the aftermath of Argentina’s defaultand the vicious combination of global uncer-tainty, domestic problems in some large coun-tries, and intra-regional contagion. The reversalof capital flows—with the accompanying risein spreads and depreciation of currencies—when combined with vulnerable balance-sheet characteristics triggered a dangerousworsening of debt dynamics in some LatinAmerican countries. In such an environment,average per capita income in Latin Americahas fallen in 2002 for the second year insuccession.

The rebound in 2002 was less uniformthan anticipated—Rapid recovery in the beginning of 2002,driven in part by sharp increases in the U.S.government’s expenditure in the aftermath ofterrorist attacks, has resulted in upward revi-sions of 2002 growth for the United States,East Asia, and Japan, relative to forecastsprepared in February (table 1.1). At the otherextreme, growth in Latin America has beenlowered by 1.6 percentage points for theyear. This decrease reflects not only the crisisin Argentina, but also the major contrac-tions of GDP in Uruguay and the RepúblicaBolivariana de Venezuela, plus slow growthin Brazil, Chile, and Mexico. Those eventsmade the 2001–02 period the worst for theregion since the debt crisis of the early 1980s.Consistent with higher-than-anticipatedglobal growth, non-oil commodity prices in2002 have risen more than anticipated.Nonetheless, the present rebound in com-modity prices is modest from an historicalperspective, thus highlighting the continuingdownward pressures on prices tied to struc-tural factors. Higher commodity prices havesupported modestly improved performance inSub-Saharan Africa.

—and the outlook for 2003 is for tepid growth Reflecting financial uncertainty and the dis-appointing recovery of business confidence,projected growth for 2003 has been markeddown for almost all developing regions, be-cause a robust rebound in industrial coun-try growth—driven by strong advances ininvestment—has become less likely. In linewith these revisions, inflation, interest rates,and non-oil commodity prices are also likelyto be lower. The sole exception to this patternis the Middle East and North Africa region,where oil exporters have benefited from highoil prices during 2002. Several of these coun-tries are seeing increased government expendi-ture, financed by rapidly mounting surplusesof oil revenues.

Investment cycles in developing countriesare more volatile than in rich countriesWith the sharp fall in global investment in2001 and the uncertainty surrounding a re-bound in capital expenditure, investmentbehavior has become a key element of theoutlook. A closer look at investment cycles indeveloping countries suggests the followingconclusions:

• Investment behavior in low- and middle-income countries is a determinant ofoverall volatility that is even moreimportant than it is in high-incomecountries.

• Those developing countries with astronger policy environment exhibitlower volatility in investment.

• Although in rich countries domesticfixed investment tends to drive foreigncapital inflows, in middle-income coun-tries the opposite tends to occur (that is,capital inflows typically drive domesticinvestment).

These conclusions imply that the middle-income countries are especially vulnerable tothe current jitters in financial markets. Suchcountries are exposed to sudden reversals in

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

2

gep_ch01.qxd 12/5/02 4:15 PM Page 2

T H E I N T E R N A T I O N A L E C O N O M Y A N D P R O S P E C T S F O R D E V E L O P I N G C O U N T R I E S

3

Table 1.1 Global conditions affecting growth in developing countries and world GDP growth(percentage change from previous year, except interest rates and oil price)

Global DevelopmentCurrent estimate Current forecasts Finance 2002 forecasts

2000 2001 2002 2003 2004 2002 2003

Global conditionsWorld trade (volume) 13.1 �0.5 2.9 7.0 8.0 1.8 8.3

Inflation (consumer prices)G-7 OECD countriesa,b 1.9 1.7 0.9 1.2 1.5 0.9 1.6United States 3.4 2.8 1.5 2.1 2.3 1.5 2.4

Commodity prices (nominal $)Commodity prices, except oil ($) �1.3 �9.1 5.0 5.8 4.4 1.3 7.3Oil price ($, weighted average), $/bbl 28.2 24.4 25.0 23.0 20.0 20.0 21.0Oil price (% change) 56.2 �13.7 2.7 �8.0 �13.0 �17.9 5.0Manufactures export unit value ($)c �2.1 �1.4 0.5 3.0 2.2 �0.5 3.6

Interest ratesLIBOR, 6 months (US$, percent) 6.6 3.6 1.8 1.5 3.1 2.3 4.0EURIBOR, 6 months (euro, percent) 4.5 4.2 3.4 3.2 3.8 3.0 4.0

GDP (growth)d

World 3.8 1.1 1.7 2.5 3.1 1.3 3.6Memo item: World GDP (ppp)e 4.5 2.1 2.8 3.4 4.0 2.4 4.3

High-income countries 3.5 0.7 1.5 2.1 2.7 0.9 3.3OECD countriesf 3.4 0.8 1.4 2.1 2.6 0.8 3.1

United States 3.8 0.3 2.3 2.6 3.1 1.3 3.7Japan 2.1 �0.3 0.0 0.8 1.3 �1.5 1.7Euro Area 3.7 1.5 0.8 1.8 2.6 1.2 3.3

Non-OECD countries 6.8 �0.7 2.3 3.7 5.3 2.7 5.3

Developing countries 5.2 2.9 2.8 3.9 4.7 3.1 4.9East Asia and Pacificf 7.0 5.5 6.3 6.1 6.4 5.6 7.1Europe and Central Asia 6.6 2.3 3.6 3.4 3.6 3.2 4.3

Transition countries 6.4 4.6 3.5 3.3 3.5 3.4 4.0Latin America and the Caribbean 3.7 0.4 �1.1 1.8 3.7 0.5 3.8

Excluding Argentina 4.5 1.2 0.7 1.9 3.6 2.1 4.3Middle East and North Africa 4.2 3.2 2.5 3.5 3.7 2.7 3.3

Oil exporters 3.6 2.4 2.4 3.7 3.6 2.2 2.8Diversified economies 3.7 4.3 2.2 2.7 3.6 3.1 4.4

South Asia 4.8 4.4 4.6 5.4 5.8 4.9 5.3Sub-Saharan Africa 3.2 2.9 2.5 3.2 3.8 2.6 3.6

Memorandum items

Developing countriesExcluding the transition countries 5.0 2.6 2.7 4.0 4.9 3.1 5.1Excluding China and India 4.6 1.7 1.5 2.8 3.8 2.0 4.1

Note: OECD � Organization for Economic Co-operation and Development, bbl � barrel, EURIBOR � European interbank offered rate, LIBOR � Londoninterbank offered rate, ppp � purchasing power parity.a. Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.b. In local currency, aggregated using 1995 GDP weights.c. Unit value index of manufactures exports from the G-5 countries to developing countries, expressed in U.S. dollars.d. GDP in 1995 constant dollars: 1995 prices and market exchange rates.e. GDP measured at 1995 purchasing power parity (international dollar) weights.f. Republic of Korea income classification changed from middle to high income (July 2002). Both forecasts were adjusted for this revision.Source: World Bank, November 2002 and Global Development Finance 2002 projections of February 2002.

gep_ch01.qxd 12/5/02 4:15 PM Page 3

capital flows, which can dampen investmentsharply and can undermine growth momen-tum. Countries with strong policy environ-ments are more likely to avoid or smoothlyabsorb potential external financial shocks.

In the long term, faster growth can be achieved in most developing regionsMarket reforms and trade liberalization dur-ing the 1990s have opened opportunities foraccelerating technological advances through-out the developing world for the next 15 years.An exception is emerging East Asia, wheresome moderation of technological progressis anticipated, reflecting in part the extra-ordinarily rapid catching-up that occurred dur-ing the 1980s and 1990s. The acceleration ofgrowth in many of the other regions is likelyto coincide with increasing savings and invest-ment rates. Demographic transitions are anti-cipated to boost saving rates in developingcountries, while reducing them in high-incomecountries.

On balance, the declining availability ofsavings in the aging populations of high-incomecountries and the increased savings in thedeveloping world—set against investmentpatterns needed to accommodate potentialgrowth—imply that more and more develop-ing countries will move toward surplus on thecurrent account and that the recent shift fromdebt accumulation to debt reduction is likelyto continue. As long as domestic credit mar-kets continue to mature and public savingsdo not deteriorate, domestic savings can beexpected to rise, and the required reduction indebt levels will not conflict with the requiredinvestment.

A recovery constrained by major risks

During the summer of 2002, investor riskperceptions increased and market senti-

ment deteriorated across large parts of theworld’s economy, thereby jeopardizing theglobal recovery that had started in the fourth

quarter of 2001. Accumulated financial im-balances that had built up during the 1990semerged as a critical factor that clouded theeconomic outlook. In the United States, thebursting of the equity bubble and cumulatedprivate sector debt kept investors cautious andresulted in a continuous flight to quality,which moved the yield on government bondsto a 40-year low while hampering the recoveryin private investment. In Japan, banking prob-lems and the lack of scope for monetary eas-ing and fiscal stimulus limited the spilloverfrom an export-driven recovery to a reboundin domestic investment. In Europe, weaknesswas concentrated in the highly indebtedtelecommunications sector and in financialsectors that had to absorb sharp devaluationsof their assets.

Bankruptcies and reductions in investmentduring the global downturn of 2001 and thesubsequent first phase of recovery in early2002 had not reduced corporate debt nor re-stored profitability sufficiently. In a number ofcases, the downturn has generated new imbal-ances. Throughout the world, fiscal balancesdeteriorated and balance sheets of financialinstitutions weakened. Continued tension infinancial markets made the recovery less uni-form in 2002—as well as probably less robustin 2003—than would have been the caseunder more normal circumstances. Vulnerabil-ity to adverse shocks has increased, and eventhe potential for a “double-dip” recession sce-nario in the industrial countries cannot—atthis juncture—be entirely ruled out.

Three distinct phases characterize recentdevelopments. The first phase portrays thedriving forces behind the initial phase of therecovery that started in late 2001, a recoverythat was more robust in the United States andEast Asia. These forces range from the end ofinventory adjustment, monetary easing, andfiscal stimulus to a technical rebound in thehigh-tech industrial sectors. This picture nor-mally would be characterized as a favorableenvironment for developing countries. Thatenvironment includes low inflation and inter-est rates, plus a significant recovery in global

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

4

gep_ch01.qxd 12/5/02 4:15 PM Page 4

trade and commodity prices, albeit a recoveryfrom low levels. During the second phase, arecovery typically broadens to other regionsand other sectors. Therefore, a recovery ofprofits and strong growth in fixed investmentbecomes the driving force that sustains or evenaccelerates growth. In the absence of suchbroadening and deepening, driving forces thatunderpin the initial phase would suddenlyappear to become short lived, which is thesituation today. Finally in the third phase—typically the shift from “recovery” to eco-nomic expansion—implications of the set ofopposing forces (cyclical rebound and finan-cial turbulence) for the medium-term globaloutlook (2003–04) are analyzed. The lack ofuniformity in growth performance during2002, following an almost synchronized slow-ing of growth across regions in 2001, is par-ticularly notable. The growth projections for2003 are more uniform across regions, butare distinctly weaker than would have beenanticipated in a strong, synchronized globalrecovery.

The first phase of the global recovery was driven by policy stimulus—In the wake of the terrorist attacks in Septem-ber 2001, forceful monetary easing in theUnited States—and to a lesser extent inEurope—helped prevent a deepening of theglobal downturn. U.S. consumers benefitedfrom historically low interest rates to boosttheir purchases of durable goods. Combinedwith double-digit growth in governmentspending—mainly driven by security, defense,and reconstruction efforts—the stimulus wassufficient to turn U.S. GDP growth positive, to2.7 percent (annualized), in the fourth quarterof 2001. One quarter later, Japan, which suf-fered steep output declines for three quartersin succession, and Europe, having experiencedonly a modest fall in GDP, broke away fromnegative growth rates as well.

The importance of U.S. domestic demandin this recovery is striking. During the firsthalf of 2002, GDP advanced at a 3 percent

annual rate, despite a drag of nearly 1.5 per-centage points stemming from a deteriorationof net exports. In contrast, output in Japan in-creased by 2.5 percent, of which foreign tradecontributed 1.8 percentage points, while in theEuro Area, GDP growth of 1.6 percent wassupported by almost 1 percentage point frompositive net exports contributions.

—inventory dynamics—Inventory dynamics played a pivotal role inthe recovery, thus complementing macro-economic stimulus efforts. The same reductionin the inventory stock that led to a negativecontribution of stock building to GDP growthin 2001 implied a positive contribution ofstock building to GDP growth in 2002. Oncethe lower level of desired inventories wasachieved, stock building shifted from sharplynegative to close to zero. The slowing of inven-tory liquidation significantly shifted the con-tribution to GDP growth from the second halfof 2001 to the first half of 2002: that shiftadded 1.2 percentage points to the accelera-tion of GDP growth in both Japan and theEuro Area, and a full 2.2 percentage points inthe United States (figure 1.1).

—a high-tech rebound—Recovery in global high-tech markets was anequally powerful stimulant. After demand forsemiconductors and related equipment plum-meted during 2001, markets were anticipatedto rebound sharply, but the scope of recoveryexceeded expectations. There are severalnatural limits to declines at rates of up to50 percent. The nature of the product—thetechnology of which becomes obsoletequickly—warrants a periodic return to highgrowth, as old products are replaced by newones and as the introduction of advancedtechnologies generates new and growing mar-kets. Defense- and security-related spending inthe United States also played a role in bolster-ing demand (U.S. manufacturing orders forcomputers and communications equipmentratcheted to annual rates of 40 and 90 per-cent, respectively, in early 2002). As the

T H E I N T E R N A T I O N A L E C O N O M Y A N D P R O S P E C T S F O R D E V E L O P I N G C O U N T R I E S

5

gep_ch01.qxd 12/5/02 4:15 PM Page 5

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

6

�3

�4

�5

�6

�2

�1

0

1

2

3

4

5

Q22002

Q32001

Q42001

Q12002

Q22002

Q32001

Q42001

Q12002

Q22002

Q12002

Q42001

Q32001

United States

Japan

Euro Area

Source: U.S. Department of Commerce; Japan Economic Statistics and Research Institute (ESRI) and Eurostat.

Figure 1.1 The recovery was initiated in a typical fashion(growth in percent)

GDP growth

Stock contribution

�20

�15

�10

�5

0

5

10

15

20

Jan.2000

May2000

Sep.2000

Jan.2001

May2001

Sep.2001

Jan.2002

Sep.2002

May2002

Note: 3m/3m saar refers to 3-month/3-month seasonallyadjusted annualized rate.Source: Datastream.

Figure 1.2 A brief rebound in industrialcountries was underway

Manufacturing production

(percent change, 3m/3m saar)

EU-15

Japan

United States�50

�25

0

25

50

75

100

125

�20

�10

0

10

20

30

40

50

Jan.2000

Jul.2000

Jan.2001

Jul.2001

Jan.2002

Jul.2002

Figure 1.3 Rebound in industrialcountries boosted production in EastAsia

Semiconductor dollar sales and industrialproduction*

(percent change, 3m/3m saar)

Note: Through July 2002. *Republic of Korea, Malaysia,Singapore, and Taiwan, China.Source: Semiconductor Industry Association (SIA) andnational sources through Datastream, World Bank staffestimates.

Semiconductor sales(left axis)

Industrial production(right axis)

rebound intensified, a strong boost was givento manufacturing output in industrial coun-tries, and especially to production and exportsfrom East Asia (figures 1.2 and 1.3).

Macroeconomic stimuli, inventory dynam-ics, and a powerful turnaround in high-techmarkets in the industrial countries set the stage

for a broader global recovery through thetraditional channels of international transmis-sion. With world trade increasing, commodityprices firming, and interest rates—fostered bylow inflation—standing at historically low

gep_ch01.qxd 12/5/02 4:15 PM Page 6

levels, developing countries faced a broadlyfavorable environment during the early part of2002.

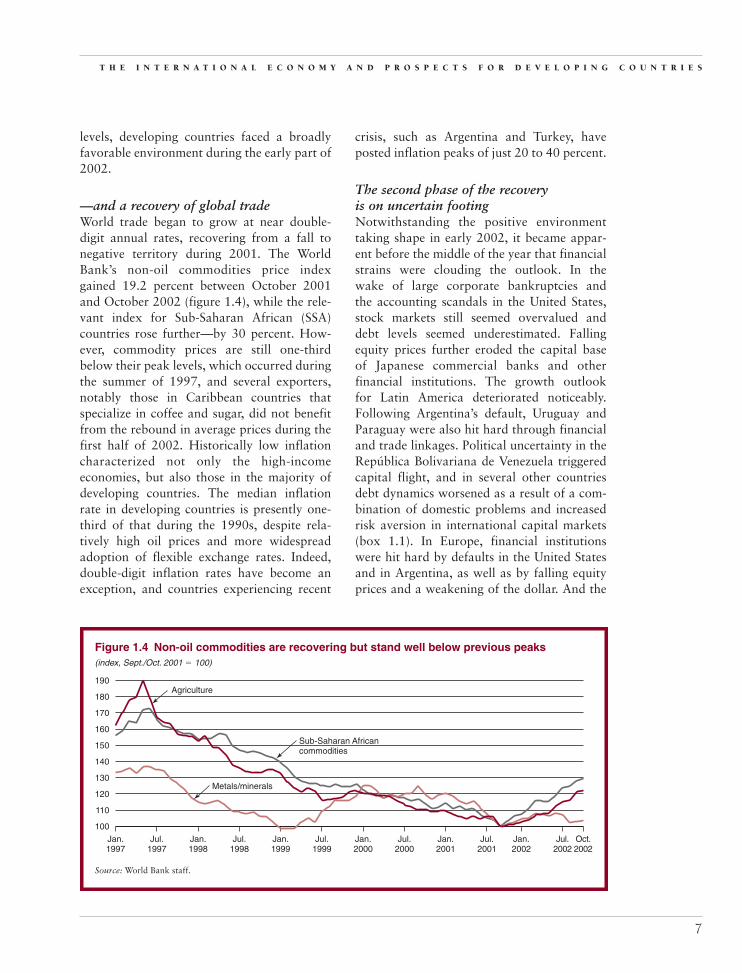

—and a recovery of global tradeWorld trade began to grow at near double-digit annual rates, recovering from a fall tonegative territory during 2001. The WorldBank’s non-oil commodities price indexgained 19.2 percent between October 2001and October 2002 (figure 1.4), while the rele-vant index for Sub-Saharan African (SSA)countries rose further—by 30 percent. How-ever, commodity prices are still one-thirdbelow their peak levels, which occurred duringthe summer of 1997, and several exporters,notably those in Caribbean countries thatspecialize in coffee and sugar, did not benefitfrom the rebound in average prices during thefirst half of 2002. Historically low inflationcharacterized not only the high-incomeeconomies, but also those in the majority ofdeveloping countries. The median inflationrate in developing countries is presently one-third of that during the 1990s, despite rela-tively high oil prices and more widespreadadoption of flexible exchange rates. Indeed,double-digit inflation rates have become anexception, and countries experiencing recent

crisis, such as Argentina and Turkey, haveposted inflation peaks of just 20 to 40 percent.

The second phase of the recovery is on uncertain footingNotwithstanding the positive environmenttaking shape in early 2002, it became appar-ent before the middle of the year that financialstrains were clouding the outlook. In thewake of large corporate bankruptcies andthe accounting scandals in the United States,stock markets still seemed overvalued anddebt levels seemed underestimated. Fallingequity prices further eroded the capital baseof Japanese commercial banks and otherfinancial institutions. The growth outlookfor Latin America deteriorated noticeably.Following Argentina’s default, Uruguay andParaguay were also hit hard through financialand trade linkages. Political uncertainty in theRepública Bolivariana de Venezuela triggeredcapital flight, and in several other countriesdebt dynamics worsened as a result of a com-bination of domestic problems and increasedrisk aversion in international capital markets(box 1.1). In Europe, financial institutionswere hit hard by defaults in the United Statesand in Argentina, as well as by falling equityprices and a weakening of the dollar. And the

T H E I N T E R N A T I O N A L E C O N O M Y A N D P R O S P E C T S F O R D E V E L O P I N G C O U N T R I E S

7

Source: World Bank staff.

Jan.2002

Jul.2001

Jan.2001

Oct.2002

Jul.2000

Jan.2000

Jul.2002

Jul.1999

Jan.1999

Jul.1998

Jan.1998

Jul.1997

Jan.1997

100

110

120

130

140

150

160

170

180

190

Figure 1.4 Non-oil commodities are recovering but stand well below previous peaks(index, Sept./Oct. 2001 � 100)

Sub-Saharan Africancommodities

Metals/minerals

Agriculture

gep_ch01.qxd 12/5/02 4:15 PM Page 7

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

8

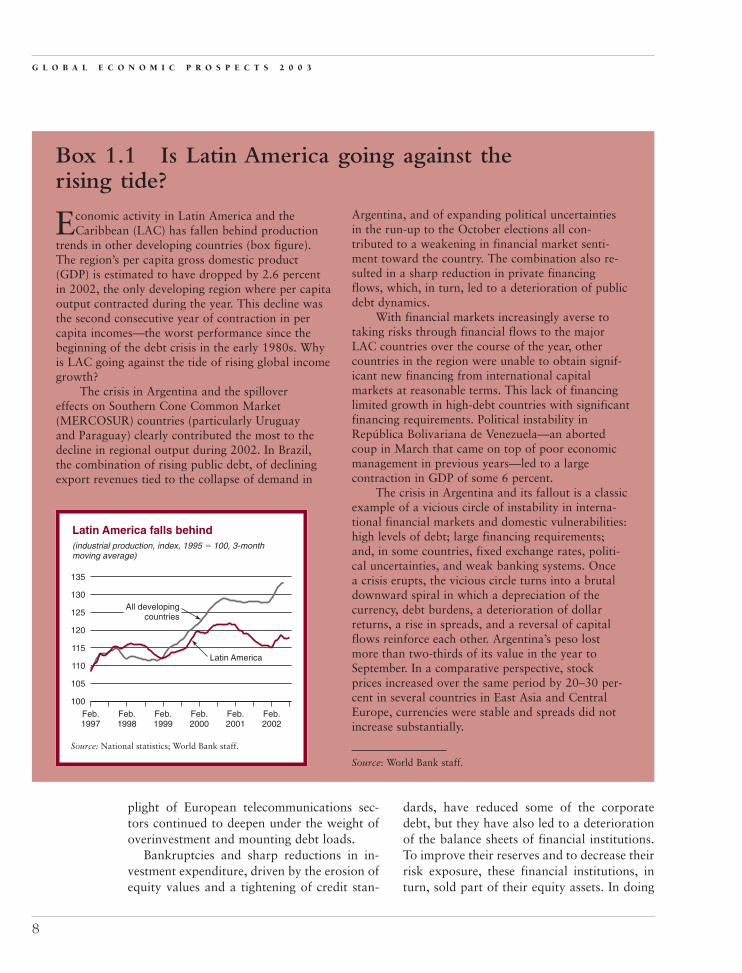

Economic activity in Latin America and theCaribbean (LAC) has fallen behind production

trends in other developing countries (box figure).The region’s per capita gross domestic product(GDP) is estimated to have dropped by 2.6 percentin 2002, the only developing region where per capitaoutput contracted during the year. This decline wasthe second consecutive year of contraction in percapita incomes—the worst performance since thebeginning of the debt crisis in the early 1980s. Whyis LAC going against the tide of rising global incomegrowth?

The crisis in Argentina and the spillovereffects on Southern Cone Common Market(MERCOSUR) countries (particularly Uruguayand Paraguay) clearly contributed the most to thedecline in regional output during 2002. In Brazil,the combination of rising public debt, of decliningexport revenues tied to the collapse of demand in

Box 1.1 Is Latin America going against therising tide?

Argentina, and of expanding political uncertaintiesin the run-up to the October elections all con-tributed to a weakening in financial market senti-ment toward the country. The combination also re-sulted in a sharp reduction in private financingflows, which, in turn, led to a deterioration of publicdebt dynamics.

With financial markets increasingly averse totaking risks through financial flows to the majorLAC countries over the course of the year, othercountries in the region were unable to obtain signif-icant new financing from international capitalmarkets at reasonable terms. This lack of financinglimited growth in high-debt countries with significantfinancing requirements. Political instability inRepública Bolivariana de Venezuela—an abortedcoup in March that came on top of poor economicmanagement in previous years—led to a largecontraction in GDP of some 6 percent.

The crisis in Argentina and its fallout is a classicexample of a vicious circle of instability in interna-tional financial markets and domestic vulnerabilities:high levels of debt; large financing requirements;and, in some countries, fixed exchange rates, politi-cal uncertainties, and weak banking systems. Oncea crisis erupts, the vicious circle turns into a brutaldownward spiral in which a depreciation of thecurrency, debt burdens, a deterioration of dollarreturns, a rise in spreads, and a reversal of capitalflows reinforce each other. Argentina’s peso lostmore than two-thirds of its value in the year toSeptember. In a comparative perspective, stockprices increased over the same period by 20–30 per-cent in several countries in East Asia and CentralEurope, currencies were stable and spreads did notincrease substantially.

Source: World Bank staff.

Feb.1997

Feb.1998

Feb.1999

Feb.2000

Feb.2001

Feb.2002

Source: National statistics; World Bank staff.

100

105

110

115

120

125

130

135

Latin America

All developingcountries

Latin America falls behind(industrial production, index, 1995 � 100, 3-monthmoving average)

plight of European telecommunications sec-tors continued to deepen under the weight ofoverinvestment and mounting debt loads.

Bankruptcies and sharp reductions in in-vestment expenditure, driven by the erosion ofequity values and a tightening of credit stan-

dards, have reduced some of the corporatedebt, but they have also led to a deteriorationof the balance sheets of financial institutions.To improve their reserves and to decrease theirrisk exposure, these financial institutions, inturn, sold part of their equity assets. In doing

gep_ch01.qxd 12/5/02 4:15 PM Page 8

T H E I N T E R N A T I O N A L E C O N O M Y A N D P R O S P E C T S F O R D E V E L O P I N G C O U N T R I E S

9

so, they further fueled the fall in stock pricesand amplified new imbalances. Similarly,the drop in capital flows has increased debtproblems in several vulnerable middle-incomecountries.

Another example of new or deterioratingimbalances is the public sector deficit acrossthe industrial countries. The U.S. general gov-ernment deficit deteriorated from a surplusposition of 2.3 percent of GDP in calendaryear 2000 to a deficit of 2.5 percent in 2002,with 2.5 percentage points of that shift attrib-uted to structural deterioration. In turn, theUnited States has not taken advantage of therecession to narrow its deficit on current ac-count. Despite increases in the household sav-ings rate and declines in the private investmentrate, the current account deficit widened toa watershed mark of 5 percent of GDP as ofthe second quarter of 2002.

In the Euro Area as well, fiscal deficits havedeteriorated from a 0.9 percent surplus to a likelevel of deficit, though this deterioration re-flects mainly the work of automatic stabilizers.Unlike the U.S. fiscal deficit, it is not a struc-tural deterioration. France, Germany, Italy,and Portugal are now approaching the currentlimits of a 3 percent of GDP deficit, limitsthat were imposed by the European MonetaryUnion Growth and Stability Pact. The originalplan to eliminate deficits by 2004 has beenabandoned and replaced by an agreement toreduce structural deficits by at least 0.5 per-centage points per annum over the comingyears. Japanese fiscal deficits remain extra-ordinarily high, at levels above 7 percent ofGDP. And East Asian emerging economies, onaverage, continue to run relatively high deficitlevels—above 4 percent of GDP—contrastedwith a deficit of 1 percent before the 1997 crisis.In other parts of the developing world, primarysurpluses are increasing, but improvement ofthe overall deficit remains difficult to achieve,given the burden of debt service.

Deteriorated government deficits, com-bined with low nominal interest rates, haveleft little room for further fiscal stimulus ormonetary easing, although some lowering of

interest rates seems still likely, especially inthe Euro Area. The limited scope for macro-economic policy makes the risks surroundingthe recovery even more severe. Policy solutionsin the industrial world may best be focusedon eliminating bad debts and restoring in-vestor’s sentiment by strengthening institu-tional oversight.

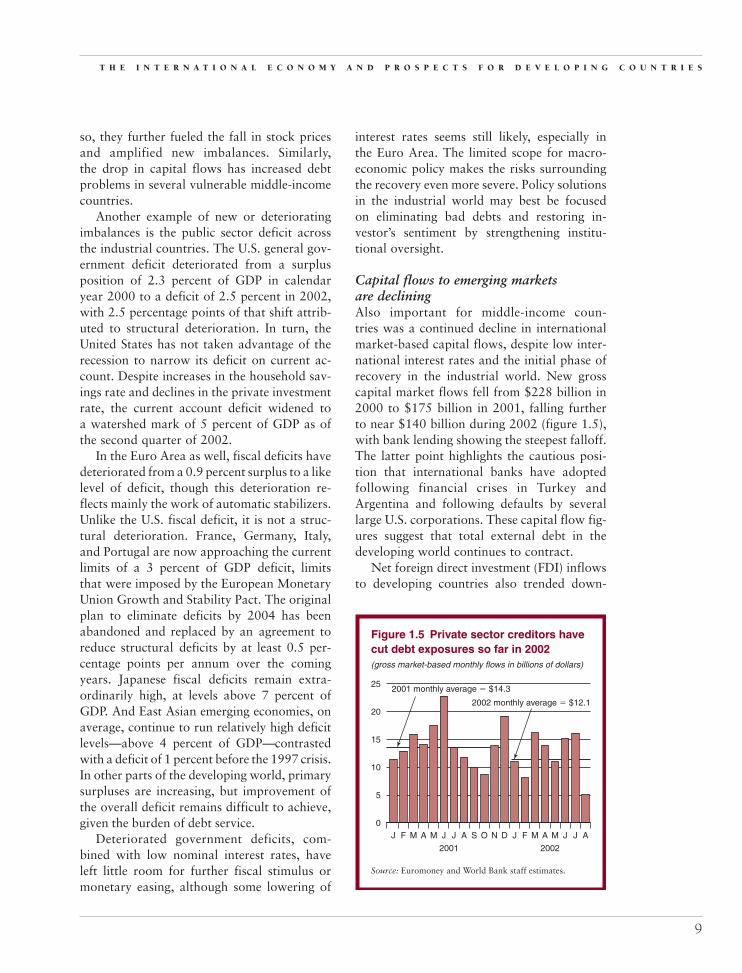

Capital flows to emerging markets are decliningAlso important for middle-income coun-tries was a continued decline in internationalmarket-based capital flows, despite low inter-national interest rates and the initial phase ofrecovery in the industrial world. New grosscapital market flows fell from $228 billion in2000 to $175 billion in 2001, falling furtherto near $140 billion during 2002 (figure 1.5),with bank lending showing the steepest falloff.The latter point highlights the cautious posi-tion that international banks have adoptedfollowing financial crises in Turkey andArgentina and following defaults by severallarge U.S. corporations. These capital flow fig-ures suggest that total external debt in thedeveloping world continues to contract.

Net foreign direct investment (FDI) inflowsto developing countries also trended down-

Source: Euromoney and World Bank staff estimates.

AJJMAMFJ

2001 2002

DNOSAJJMAMFJ

25

20

15

10

5

0

2001 monthly average � $14.3

2002 monthly average � $12.1

Figure 1.5 Private sector creditors havecut debt exposures so far in 2002(gross market-based monthly flows in billions of dollars)

gep_ch01.qxd 12/5/02 4:15 PM Page 9

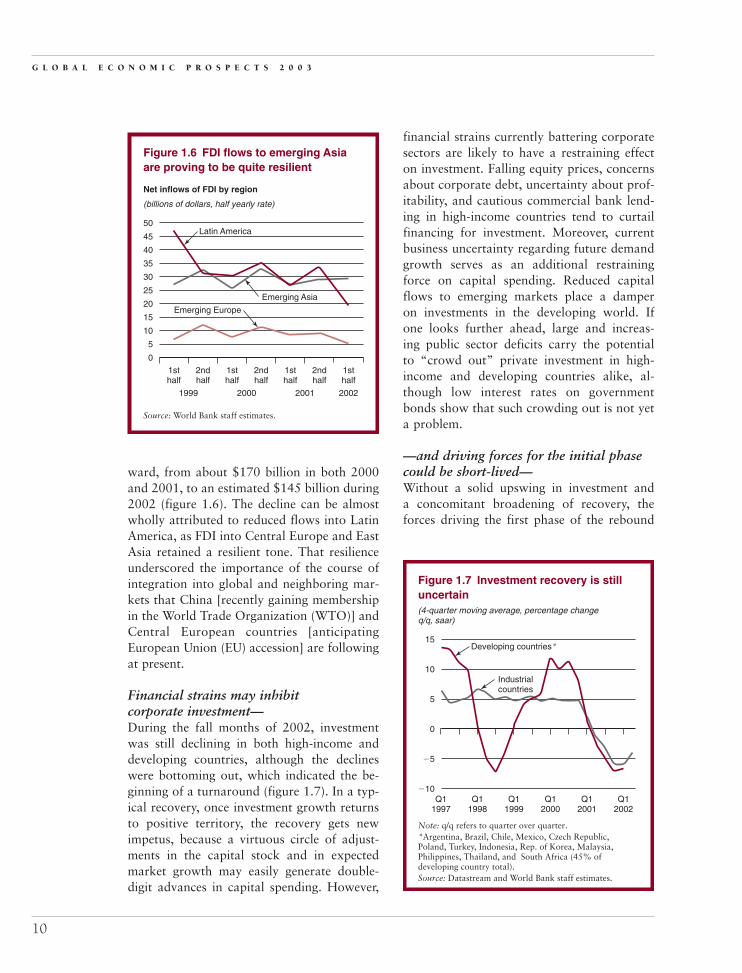

ward, from about $170 billion in both 2000and 2001, to an estimated $145 billion during2002 (figure 1.6). The decline can be almostwholly attributed to reduced flows into LatinAmerica, as FDI into Central Europe and EastAsia retained a resilient tone. That resilienceunderscored the importance of the course ofintegration into global and neighboring mar-kets that China [recently gaining membershipin the World Trade Organization (WTO)] andCentral European countries [anticipatingEuropean Union (EU) accession] are followingat present.

Financial strains may inhibit corporate investment—During the fall months of 2002, investmentwas still declining in both high-income anddeveloping countries, although the declineswere bottoming out, which indicated the be-ginning of a turnaround (figure 1.7). In a typ-ical recovery, once investment growth returnsto positive territory, the recovery gets newimpetus, because a virtuous circle of adjust-ments in the capital stock and in expectedmarket growth may easily generate double-digit advances in capital spending. However,

financial strains currently battering corporatesectors are likely to have a restraining effecton investment. Falling equity prices, concernsabout corporate debt, uncertainty about prof-itability, and cautious commercial bank lend-ing in high-income countries tend to curtailfinancing for investment. Moreover, currentbusiness uncertainty regarding future demandgrowth serves as an additional restrainingforce on capital spending. Reduced capitalflows to emerging markets place a damperon investments in the developing world. Ifone looks further ahead, large and increas-ing public sector deficits carry the potentialto “crowd out” private investment in high-income and developing countries alike, al-though low interest rates on governmentbonds show that such crowding out is not yeta problem.

—and driving forces for the initial phasecould be short-lived—Without a solid upswing in investment anda concomitant broadening of recovery, theforces driving the first phase of the rebound

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 3

10

Q11997

Q11998

Q11999

Q12000

Q12001

Q12002

Note: q/q refers to quarter over quarter. *Argentina, Brazil, Chile, Mexico, Czech Republic,Poland, Turkey, Indonesia, Rep. of Korea, Malaysia,Philippines, Thailand, and South Africa (45% ofdeveloping country total).Source: Datastream and World Bank staff estimates.

0

5

10

15

�10

�5

Figure 1.7 Investment recovery is stilluncertain(4-quarter moving average, percentage changeq/q, saar)

Developing countries*

Industrialcountries

Source: World Bank staff estimates.

0

10

5

20

15

30

25

35

45

40

50

1sthalf