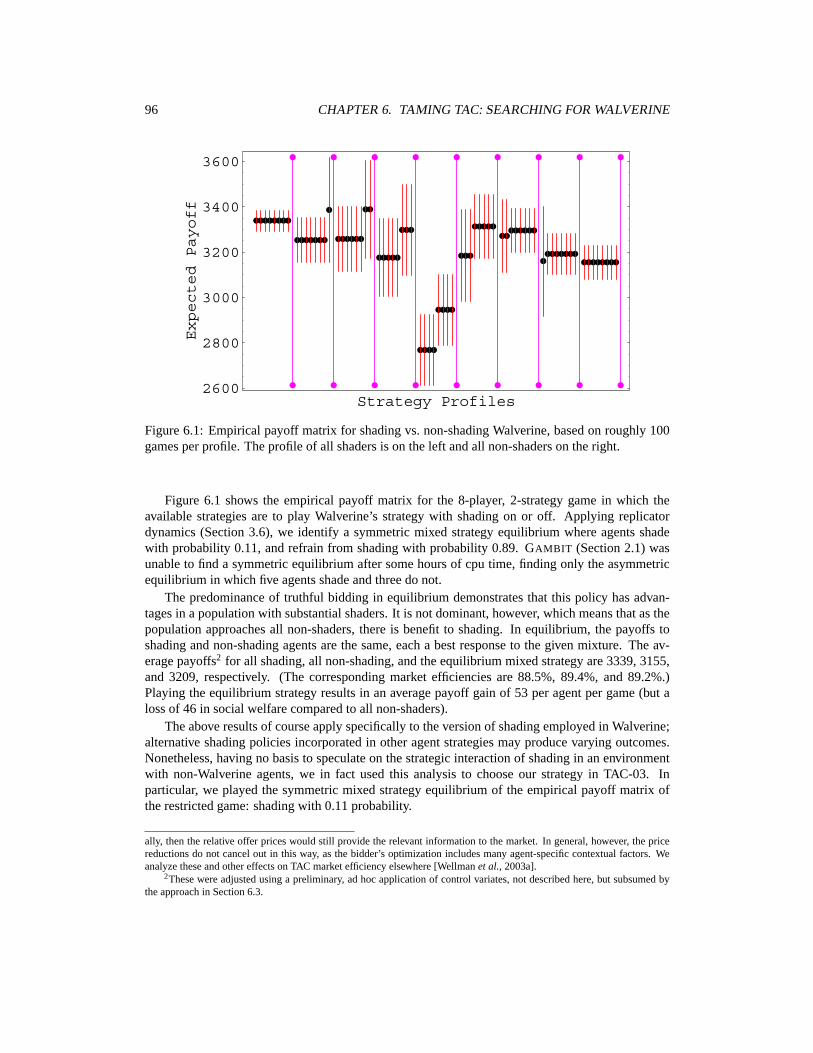

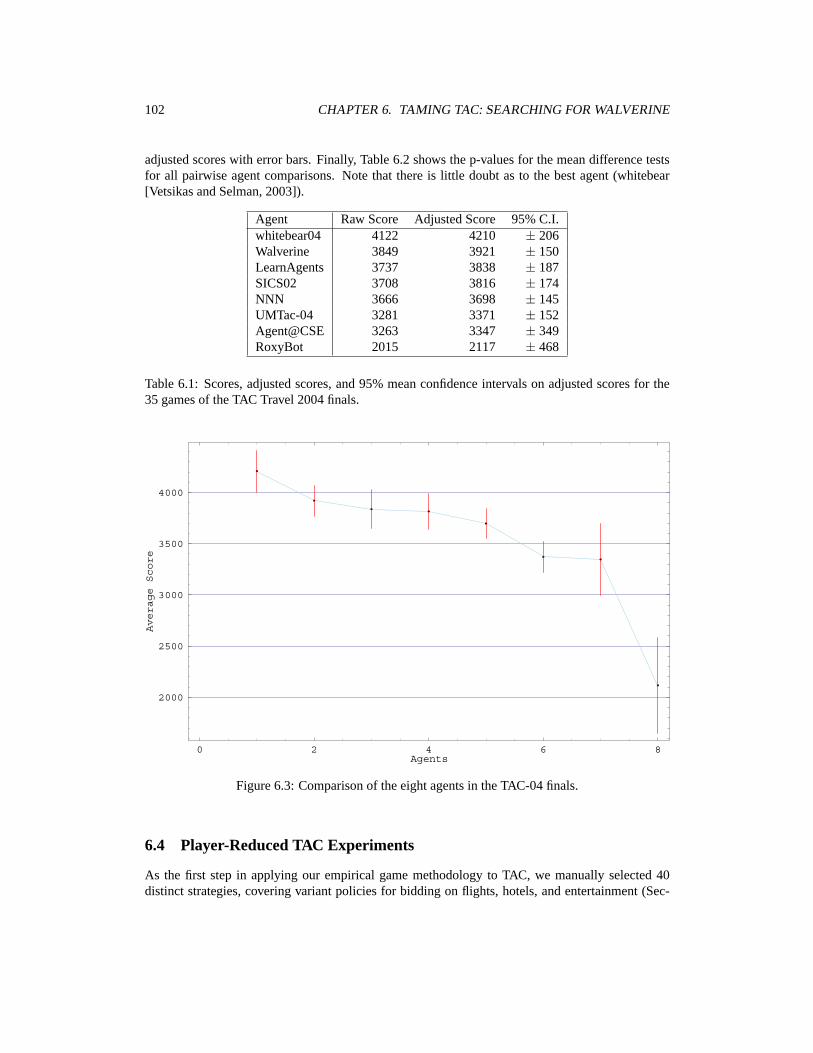

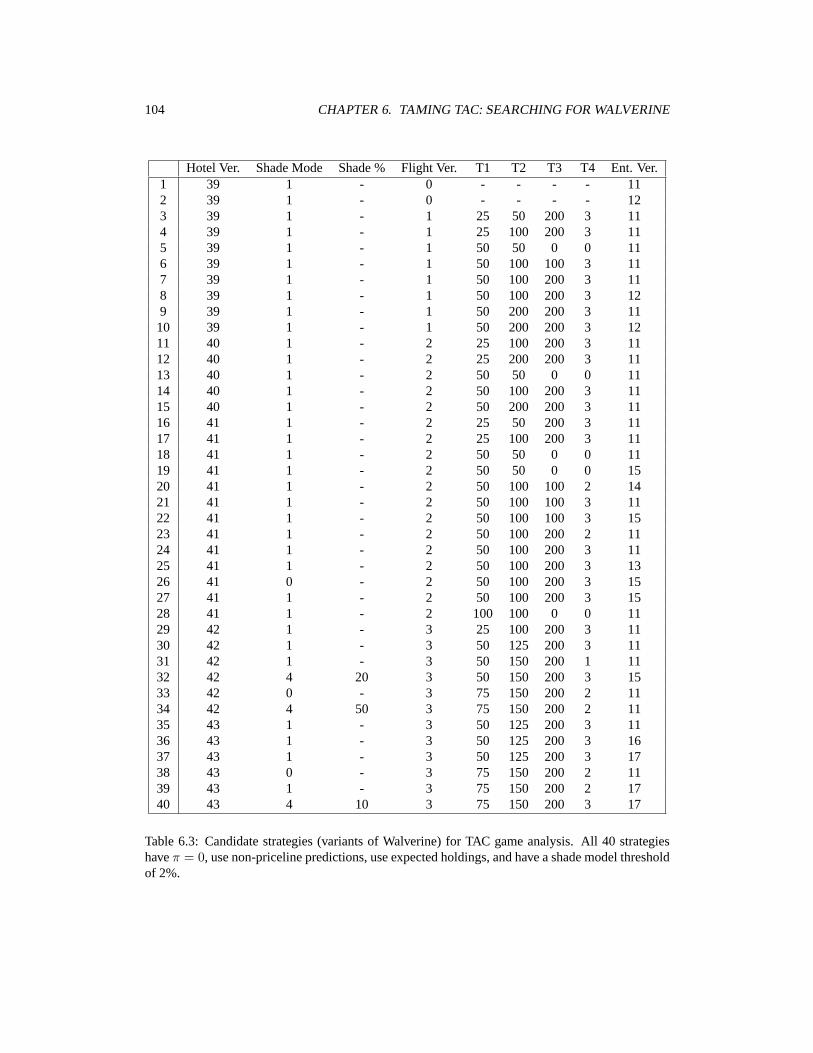

![PEP Web - The Analytic Third: Working with Intersubjective ... … · analytic third'. This third subjectivity, the intersubjective analytic third Green's [1975] 'analytic object'),](https://static.fdocuments.us/doc/165x107/6099619e2d4b51336024f694/pep-web-the-analytic-third-working-with-intersubjective-analytic-third.jpg)

Generating Trading Agent Strategies: Analytic and ...

165

Generating Trading Agent Strategies: Analytic and Empirical Methods for Infinite and Large Games by Daniel M. Reeves A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy (Computer Science and Engineering) in The University of Michigan 2005 Doctoral Committee: Professor Michael P. Wellman, Chair Professor Jeffrey K. MacKie-Mason Professor Scott E. Page Associate Professor Satinder Singh Baveja

Transcript of Generating Trading Agent Strategies: Analytic and ...

Generating Trading Agent Strategies:Analytic and Empirical Methods

for Infinite and Large Games

by

Daniel M. Reeves

A dissertation submitted in partial fulfillmentof the requirements for the degree of

Doctor of Philosophy(Computer Science and Engineering)

in The University of Michigan2005

Doctoral Committee:Professor Michael P. Wellman, ChairProfessor Jeffrey K. MacKie-MasonProfessor Scott E. PageAssociate Professor Satinder Singh Baveja

First edition

c© 2005 by Daniel M. Reeves

Artificial Intelligence LaboratoryUniversity of Michigan1101 Beal AvenueAnn Arbor, Michigan, 48109USA

http://ai.eecs.umich.edu/people/dreeves

To my parents, Laurie Kalkman Reeves and Martin Reeves.

Abstract

A Strategy Generation Engine is a system that reads a description of a game or market mechanismand outputs strategies for participants. Ideally, this means a game solver—an algorithm to computeNash equilibria. This is a well-studied problem and very general solutions exist, but they can onlybe applied to small, finite games. This thesis presents methods for finding or approximating Nashequilibria for infinite games, and for intractably large finite games.

First, I define a broad class of one-shot, two-player infinite games of incomplete information.I present an algorithm for computing best-response strategies in this class and show that for manyparticular games the algorithm can be iterated to compute Nash equilibria. Many results from thegame theory literature are reproduced—automatically—using this method, as well as novel resultsfor new games.

Next, I address the problem of finding strategies in games that, even if finite, are larger than whatany exact solution method can address. Our solution involves (1) generating a small set of candidatestrategies, (2) constructing via simulation an approximate payoff matrix for the simplification of thegame restricted to the candidate strategies, (3) analyzing the empirical game, and (4) assessingthe quality of solutions with respect to the underlying full game. I leave methods for generatingcandidate strategies domain-specific and focus on methods for taming the computational cost ofempirical game generation. I do this by employing Monte Carlo variance reduction techniques andintroducing a technique for approximating many-player games by reducing the number of players.We are additionally able to solve much larger payoff matrices than the current state-of-the-art solverby exploiting symmetry in games.

I test these methods in small games with known solutions and then apply them to two realisticmarket scenarios: Simultaneous Ascending Auctions (SAA) and the Trading Agent Competition(TAC) travel-shopping game. For these domains I focus on two key price prediction approachesfor generating candidate strategies for empirical analysis: self-confirming price predictions andWalrasian equilibrium prices. We find that these are highly effective strategies in SAA and TAC,respectively.

v

Acknowledgments

This thesis includes joint work with Michael Wellman, Jeffrey MacKie-Mason, Anna Osepayshvili,Kevin Lochner, Shih-Fen Cheng, Rahul Suri, Yevgeniy Vorobeychik, and Maxim Rytin. In Sec-tion 1.4 I outline this thesis in relation to previously published work with the above coauthors. Mycollaboration with Maxim Rytin, though, is published here for the first time as the proofs of keytheorems in Chapter 3. Kevin O’Malley was instrumental in the development of our entry in theTrading Agent Competition, which is the subject of Chapter 6. Finally, William Walsh collaboratedon the proofs of theorems related to the supply-chain game in Chapter 2.

I’m grateful to my thesis committee—Michael Wellman, Jeffrey MacKie-Mason, Scott Page,and Satinder Singh Baveja—for their careful reading, insightful comments, and cutting questions.This thesis is definitively improved due to their input. As early as my proposal defense, Satinderhelped shape the course of this research by proposing what led to our epsilon metric, defined inChapter 3. Similarly, Scott has proposed myriad improvements and helped clarify the contributionin Chapter 2 by asking hard questions about the generality of my approach. Even before Scott cameto Michigan, he provided invaluable guidance at the Computational Economics Workshop at theSanta Fe Institute in 2000, when I first got excited about strategy generation in auctions. Jeff, ofcourse, is much more than a committee member. As a coauthor of most of the material in Chapters 3,4, and 5, it’s thanks in no small part to his vision and hard work that this thesis is where it is.

This brings me to Mike. Perhaps it’s filial bias but I am convinced there is no better researchadvisor in all of academia. Mike’s research and thesis advising is nothing short of a graduatestudent’s dream. He is an academic role model in every way, and I just can’t thank him enoughfor his guidance and patience. Guidance doesn’t capture it—he was a full collaborator (includingwriting code, running experiments, and proving theorems) on everything in this thesis. Patience islikewise an understatement; if he was ever frustrated by my almost explicit goal of stretching mygraduate school career out as long as possible, he didn’t let on. I also won’t forget how kind he waswhen I was ill in 2002.

Others who I would like to thank for their help, support, or guidance include Terence Kelly, An-drzej Kozlowski, Daniel Lichtblau, Ted Turocy, Benjamin Grosof, David Reiley, Leslie Fine, Kay-yut Chen, Jaap Suermondt, Evan Kirshenbaum, Kemal Guler, John Miller, Annie Noone, BethanySoule, Dave Morris, Chris Kapusky, Karen Conneely, Sarah Nuss-Warren, Rachel Rose, Rob Felty,Michelle Sternthal, Doug Bryan, Brian Renaud, Marie Eguchi, and finally, my family.

vii

Contents

1 Introduction: Games, Strategies, and Nash Equilibria 11.1 Games of Incomplete Information and Normal-Form Representation . . . . . . . . 11.2 Symmetric Games . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.3 Summary and Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.4 Overview of Thesis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2 Generating Best-Response Strategies in Infinite Games of Incomplete Information 72.1 Finite Game Approximations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72.2 Infinite Games and Bayes-Nash Equilibria . . . . . . . . . . . . . . . . . . . . . . 82.3 Existence and Computation of Piecewise Linear Best-Response Strategies . . . . . 112.4 Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.5 Related Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3 Empirical Game Methodology 213.1 Measuring Solution Quality: The ε Metric . . . . . . . . . . . . . . . . . . . . . . 223.2 Restricting the Strategy Space . . . . . . . . . . . . . . . . . . . . . . . . . . . . 233.3 Game Simulators and Brute-Force Estimation of Games . . . . . . . . . . . . . . . 263.4 Variance Reduction in Monte Carlo Sampling . . . . . . . . . . . . . . . . . . . . 283.5 Reducing the Number of Players . . . . . . . . . . . . . . . . . . . . . . . . . . . 323.6 Analyzing Empirical Games . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 373.7 Interleaving Analysis and Estimation . . . . . . . . . . . . . . . . . . . . . . . . . 403.8 Sensitivity Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 413.9 Related Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4 Price Prediction for Strategy Generation in Complex Market Mechanisms 474.1 Interdependent Auctions: TAC and SAA . . . . . . . . . . . . . . . . . . . . . . . 474.2 Walrasian Price Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 484.3 The Simultaneous Ascending Auctions (SAA) Domain . . . . . . . . . . . . . . . 504.4 Strategies for SAA: Straightforward Bidding and Variations . . . . . . . . . . . . . 514.5 Price Prediction Strategies for SAA . . . . . . . . . . . . . . . . . . . . . . . . . 544.6 Methods for Predicting Prices in SAA . . . . . . . . . . . . . . . . . . . . . . . . 574.7 The Trading Agent Competition (TAC) Domain . . . . . . . . . . . . . . . . . . . 594.8 Price Prediction in TAC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 614.9 Walrasian Price Equilibrium in the TAC Market . . . . . . . . . . . . . . . . . . . 614.10 Bidding Strategy using Price Predictions in TAC . . . . . . . . . . . . . . . . . . . 664.11 Evaluating Prediction Quality in TAC . . . . . . . . . . . . . . . . . . . . . . . . 68

ix

x CONTENTS

4.12 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

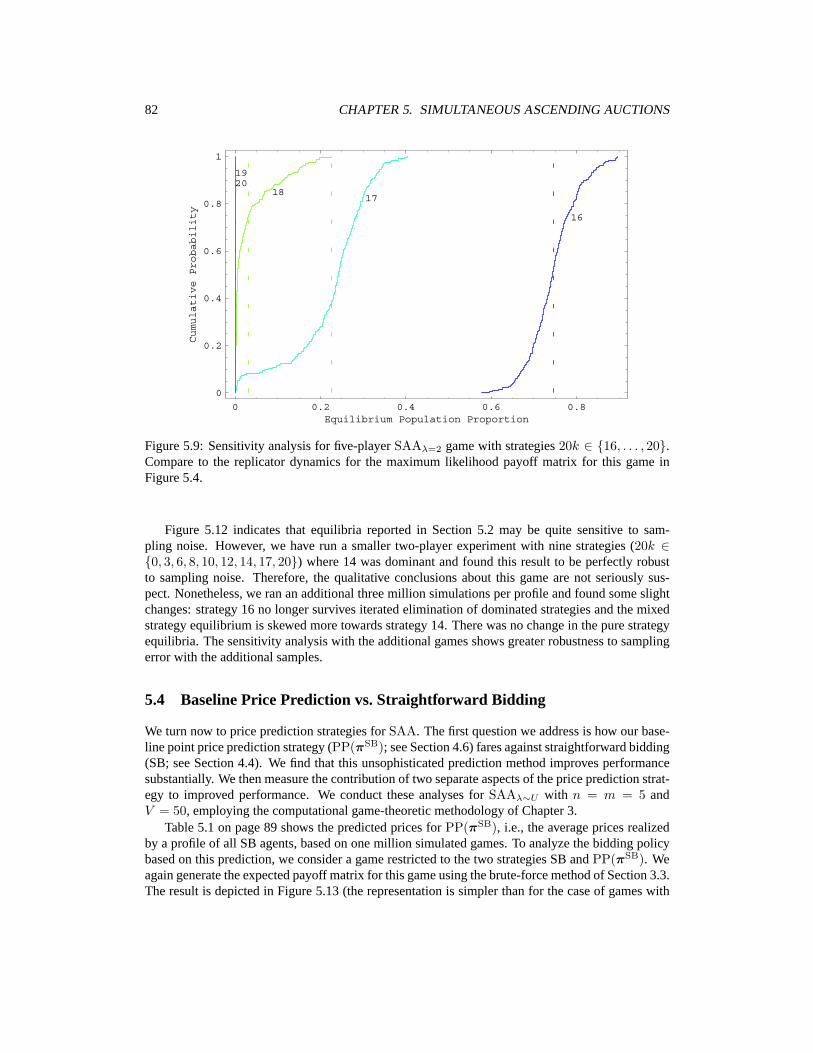

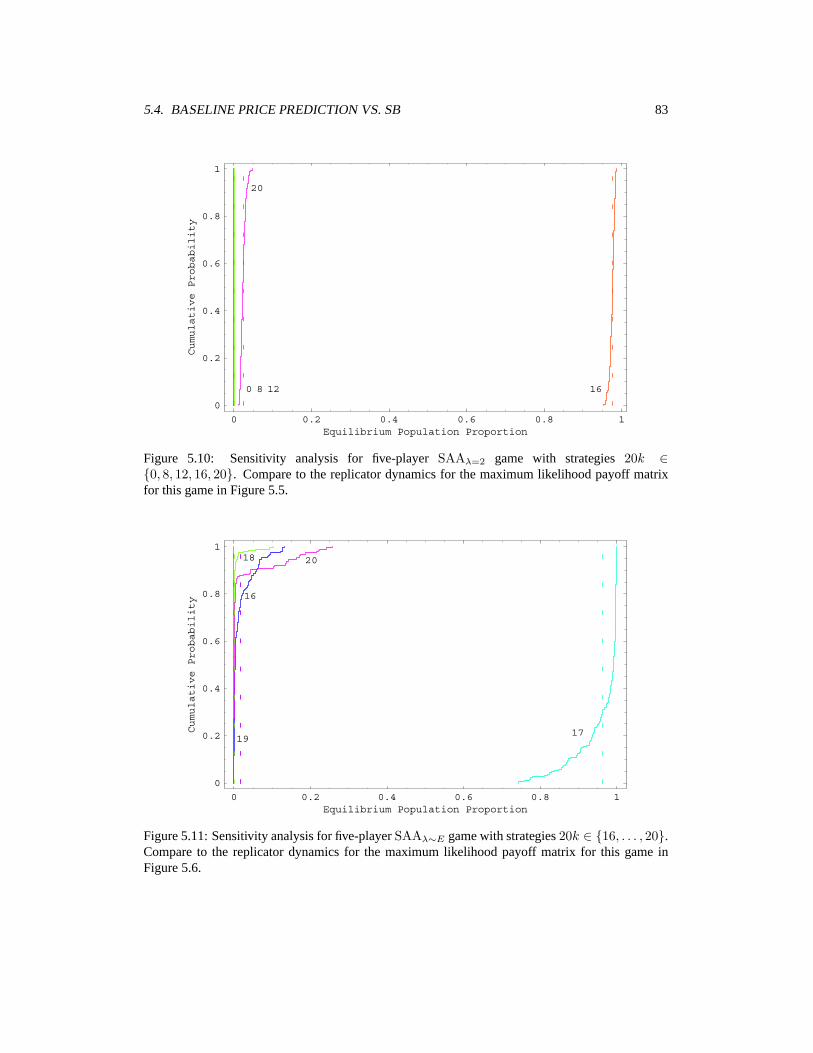

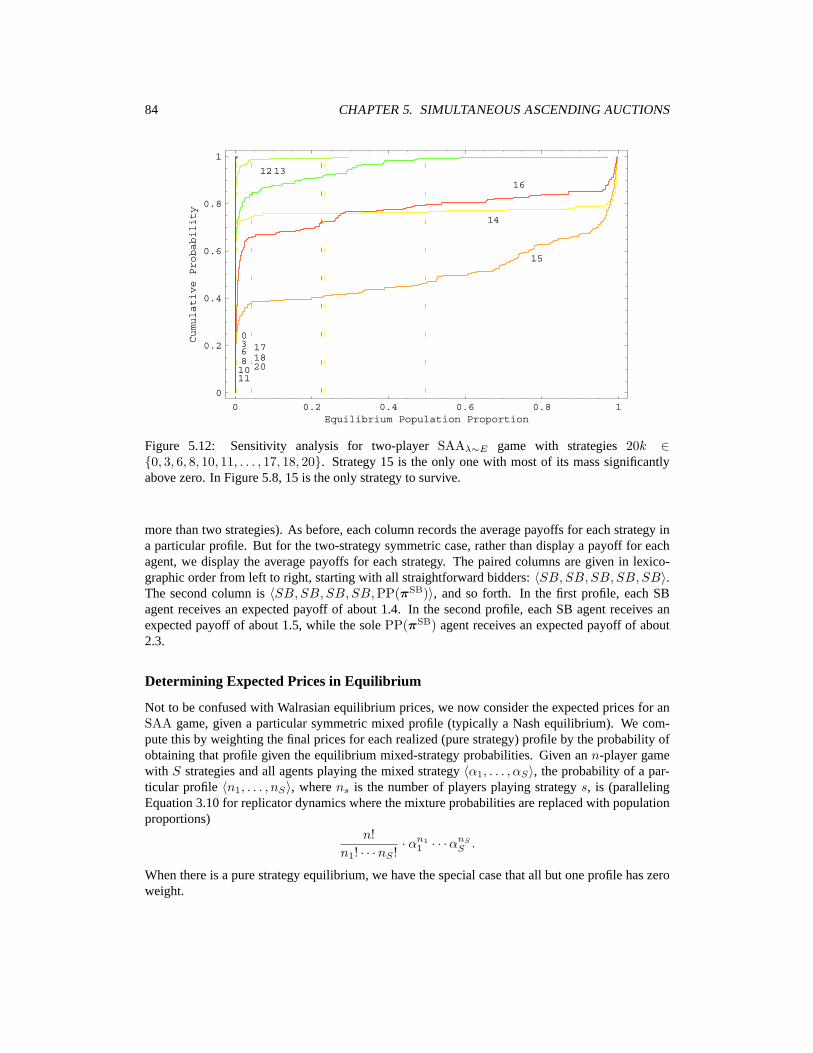

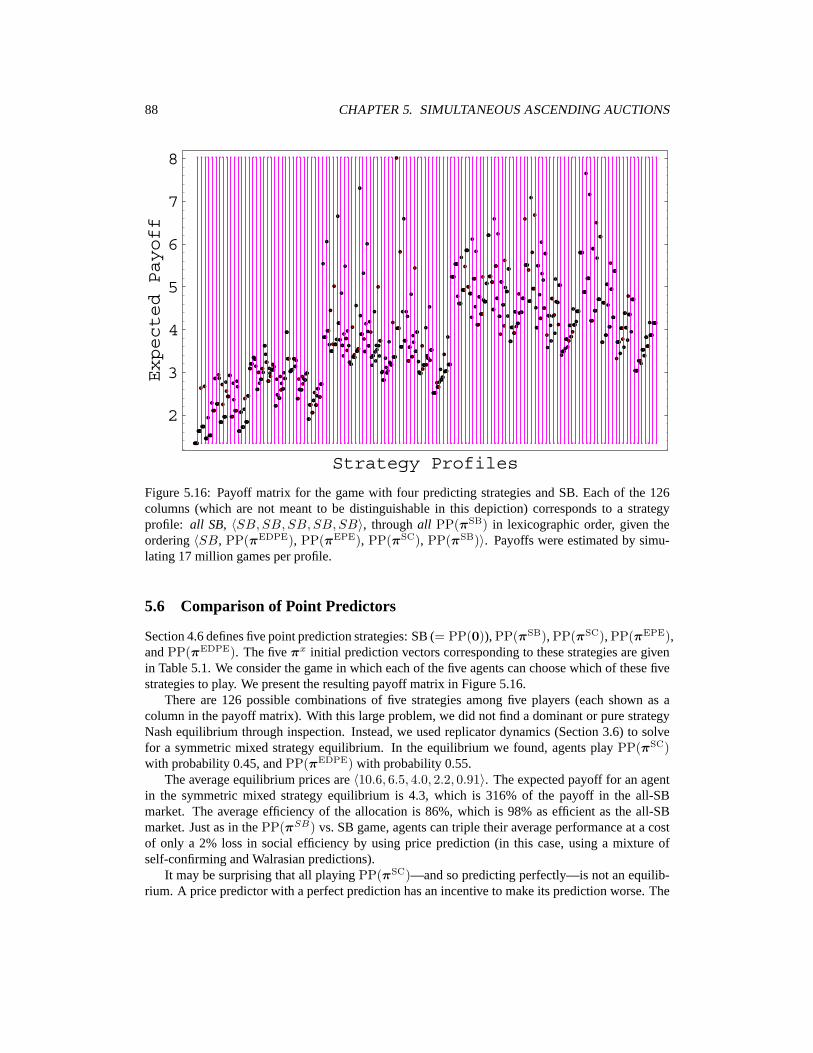

5 Empirical Game Analysis for Simultaneous Ascending Auctions 735.1 Type Distributions for SAA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 735.2 Experiments in Sunk-Awareness . . . . . . . . . . . . . . . . . . . . . . . . . . . 755.3 Sensitivity Analysis for Sunk-Awareness Results . . . . . . . . . . . . . . . . . . 815.4 Baseline Price Prediction vs. Straightforward Bidding . . . . . . . . . . . . . . . . 825.5 How Does Price Prediction Help? . . . . . . . . . . . . . . . . . . . . . . . . . . 865.6 Comparison of Point Predictors . . . . . . . . . . . . . . . . . . . . . . . . . . . . 885.7 Self-Confirming Distribution Predictors . . . . . . . . . . . . . . . . . . . . . . . 895.8 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

6 Taming TAC: Searching for Walverine 956.1 Preliminary Strategic Analysis: Shading vs. Non-Shading . . . . . . . . . . . . . . 956.2 Walverine Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 976.3 Control Variates for the TAC Game . . . . . . . . . . . . . . . . . . . . . . . . . . 1006.4 Player-Reduced TAC Experiments . . . . . . . . . . . . . . . . . . . . . . . . . . 1026.5 Finding Walverine 2005 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1116.6 TAC 2005 Outcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1126.7 Related Work: Strategic Interactions in TAC Travel . . . . . . . . . . . . . . . . . 114

7 Conclusion 1177.1 Summary of Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1177.2 Future Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

A Proofs and Derivations 121A.1 CDF of a Piecewise Uniform Distribution . . . . . . . . . . . . . . . . . . . . . . 121A.2 Proof of Theorem 2.3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121A.3 Proof of Theorem 2.4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122A.4 Proof of Theorem 2.5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124A.5 Proof of Theorem 3.4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124A.6 Proof of Theorem 3.5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126A.7 Proof of Lemma 3.7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127A.8 Proof of Theorem 3.10 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129A.9 Proof of Lemma 3.11 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130A.10 Proof of Theorem 3.12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131A.11 Proof of Theorem 3.13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

B Monte Carlo Best-Response Estimation 133

C Notes on Equilibria in Symmetric Games 135

D Strategies for SAA Experiments 139D.1 Price Predicting Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139D.2 53-Strategy Game For 5×5 Uniform Environment . . . . . . . . . . . . . . . . . . 143D.3 Strategies For Alternative Environments . . . . . . . . . . . . . . . . . . . . . . . 144

Bibliography 147

Chapter 1

Introduction: Games, Strategies, and NashEquilibria

IN WHICH we define terms like “game” and “strategy” and introduce the problem ofgenerating strategies for games.

When a human is faced with a new game they digest the rules, consider the motives and ca-pabilities of the other players, and formulate a strategy for playing. This thesis takes steps towardautomating that process. A Strategy Generation Engine is a system that advises on how to play agame given a formal description of the possible interactions of the players. In the absence of otherplayers, a strategy generation engine is just an optimization routine. That is, it would answer, deci-sion theoretically, the question: What actions maximize my (expected) utility? In the next section,we see how, by way of a cursory introduction to some foundational concepts of game theory, thestrategy generation concept can be generalized to the case of multiple agents: a game.

1.1 Games of Incomplete Information and Normal-Form Representation

Game theory was founded by von Neumann and Morgenstern [1947] to study situations in whichmultiple agents (players) interact in order to each maximize an objective (payoff) function deter-mined not only by their own actions but also the actions of other players. Agents always knowtheir own payoff function—i.e., their utility function—but may not know those of the other agents.To capture this, we redefine an agent’s payoff to be a function not only of its own and others’ ac-tions, but also of private information. Thus it is without loss of generality to consider all the payofffunctions (or, equivalently, the single multidimensional payoff function) as known by all the agents.

An agent’s private information is known more succinctly as its type, or sometimes as its pref-erences. The term “type” is used because it is exactly this private information that formally distin-guishes the agents. The term “preferences” reflects the fact that the private information determinesthe agent’s utility, given all the agents’ actions. For example, in poker an agent’s hand constitutes itstype. In an auction, the analogous information is how much the agent values the goods being sold.

The agents’ types are drawn from a probability distribution, called the type distribution. Tocapture randomness in the game, we introduce a special player, Nature, with type dictated, as forany other player, by the type distribution. But Nature has no payoff function and its action is simplyits type. In this way Nature could, for example, represent the roll of dice, affecting any or all

1

2 CHAPTER 1. INTRODUCTION

other players’ payoffs. We assume that the possible actions, payoff function, and type distributionare common knowledge.1 The special case that all agents have exactly one possible type is calledcomplete information. In this thesis, I consider the general case: games of incomplete information.

Nash Equilibrium

In the case of a single agent, the optimal policy is straightforward: choose the action that maximizespayoff (utility). If payoff depends on Nature’s action, the agent simply maximizes its expectedpayoff given the type distribution. In the case of multiple agents, Nash [1951] proposed a solutionconcept now known as the Nash equilibrium and proved that for finite games (as long as agents canplay mixed strategies, i.e., randomize among actions) such an equilibrium always exists. A Nashequilibrium that does not employ mixed strategies—called a pure-strategy Nash equilibrium—is aprofile of actions such that each action is a best response to the rest of the profile. That is, eachagent maximizes its own utility given the actions played by the others. The generalization to mixed-strategy equilibria entails maximizing expected utility given the distribution of agent actions.

Although the limitations of the Nash equilibrium as a solution concept have been well studied,particularly the problem of what agents will do in the face of multiple equilibria [van Damme, 1983],finding Nash equilibria remains fundamental to the analysis of games. In fact, for many practicalapplications, it suffices to find one of many possible Nash equilibria. That equilibrium, by virtueof being the one found by a given solver, becomes focal and the equilibrium selection problemis moot. For example, if agent software is distributed that implements an equilibrium policy fora game, no recipient has an incentive to modify the software unless they imagine that others arealso modifying it in a certain way, which they would have no incentive to do. Practically, this isreasonable assurance the found equilibrium will actually be played.

Bayes-Nash Equilibrium

The notion of Nash equilibrium needs to be generalized slightly for the case of incomplete in-formation games. We first define an agent’s strategy as a mapping from its information—privateinformation (type) as well as information revealed during the game—to actions. Another seminalgame theorist, Harsanyi2 [1967], first introduced the concept of agent types and used it to define aBayesian game. A Bayesian game is specified by a set of types T , a set of actions A, a probabilitydistribution F over types, and a payoff function P . Harsanyi defines a Bayes-Nash equilibrium(sometimes known as a Bayesian equilibrium) as the simple Nash equilibrium of the non-Bayesiangame with set of actions being the set of strategies (functions from T to A), and the payoff functionbeing the expectation of P with respect to F . In this thesis I use “Nash equilibrium” or “equilib-rium” interchangeably with “Bayes-Nash equilibrium” when appropriate.

The idea of a normal (or strategic) form representation is to ignore the actions and define thegame in terms of the strategies. In other words, per Harsanyi’s insight, an agent’s set of strategies isequivalent to its set of actions.

Definition 1.1 (Normal-form Game) Γ = 〈n, {Si}, {ui()}〉 is an n-player normal-form game,with strategy set Si the available strategies for player i (with typical element si), and the payoff

1A fact is common knowledge [Fagin et al., 1995] if everyone knows it, everyone knows that everyone knows it, adinfinitum.

2Harsanyi, along with Selten, shared the 1994 Nobel Prize in economics with Nash “for their pioneering analysis ofequilibria in the theory of non-cooperative games.”

1.2. SYMMETRIC GAMES 3

function ui(s1, . . . , sn) giving the utility accruing to player i when players choose the strategyprofile (s1, . . . , sn).

In contrast, extensive form is a more compact representation in which payoffs are given for se-quences of actions but only implicitly for combinations of agent strategies (mappings from infor-mation to actions).

1.2 Symmetric Games

With the exception of the bargaining game in Section 2.4, every game I examine in this thesis issymmetric. A game in normal form is symmetric if all agents have the same strategy set, and thepayoff to playing a given strategy depends only on the strategies being played, not on who playsthem. In other words, a game is symmetric if there are no distinct player roles or identities (asidefrom Nature). I define this concept formally as follows:

Definition 1.2 (Symmetric Game) A normal-form game is symmetric if the players have identicalstrategy spaces (S1 = . . . = Sn = S) and ui(si, s−i) = uj(sj , s−j), for si = sj and s−i = s−j

for all i, j ∈ {1, . . . , n}.3 Thus we can write u(t, s) for the payoff to any player playing strategy twhen the remaining players play profile s. We denote a symmetric game by the tuple 〈n, S, u()〉. (Ioverload S to refer to the number of strategies as well as the set of strategies.)

A strategy profile with all players playing the same strategy is a symmetric profile, or, if such aprofile is a Nash equilibrium, a symmetric equilibrium.

Many well-known games are symmetric, for example the Prisoners’ Dilemma, Chicken, andRock-Paper-Scissors, as well as standard game-theoretic auction models. Symmetric games maynaturally arise from models of automated-agent interactions, since in these environments the agentsmay possess, by design, identical circumstances, capabilities, and perspectives. But these are en-compassed in the agent types so even if they differ it is often accurate to model them as drawnfrom identical distributions, restoring symmetry. Designers often impose symmetry in artificial en-vironments constructed to test research ideas—for example, the Trading Agent Competition (TAC)[Wellman et al., 2001b] market games—since an objective of the model structure is to facilitateinteragent comparisons.

The relevance of symmetry in games stems in large part from the opportunity to exploit thisproperty for computational advantage, as I do throughout this thesis. Symmetry immediately sup-ports more compact representation. The number of distinct profiles in an n-player, S-strategysymmetric game is

(n+S−1

n

), as opposed to Sn for the nonsymmetric counterpart. Furthermore,

symmetry enables solution methods specific to this structure.Given a symmetric environment, we typically prefer to identify symmetric equilibria, as asym-

metric behavior seems relatively unintuitive [Kreps, 1990], and difficult to explain in a one-shotinteraction. Rosenschein and Zlotkin [1994] argue that symmetric equilibria may be especially de-sirable for automated agents, since programmers can then publish and disseminate strategies forcopying, without need for secrecy.

1.3 Summary and Motivation

This thesis concerns the generation and selection of strategies, in particular for trading agents par-ticipating in various market mechanisms. Games that trading agents face typically involve private

3s−i denotes the length n− 1 profile s with the ith element removed.

4 CHAPTER 1. INTRODUCTION

information, such as an agent’s valuation for a good being bought or sold, and fine-grained actionspaces, such as bids of arbitrary amounts of money. Such games are well modeled as infinite gamesof incomplete information. Generating trading agent strategies means creating a system that canread the description of such a mechanism and output strategies for participating agents.

To make this more concrete, consider an extremely simple auction mechanism, which I useas a running example throughout this thesis: a First-Price Sealed-Bid Auction (FPSB). This is agame in which each agent has one piece of private information: its valuation for an indivisible goodbeing auctioned (in the simplest case we take the common-knowledge type distribution to be i.i.d.U [0, 1]). Each agent also has a continuum of possible actions: its bid amount. The payoff to anagent is its valuation minus its bid if its bid is highest, and zero otherwise (with ties broken by faircoin toss). We have developed an algorithm that can solve this game. That is, it takes the gamedescription—for the two-player case—and outputs the unique symmetric Bayes-Nash equilibrium.(In this case, for an agent with valuation v, the equilibrium strategy is to bid v/2.) Of course, theNash equilibrium strategy for the particular case of FPSB was identified by auction theorists beforecomputational game solvers existed [Vickrey, 1961; McAfee and McMillan, 1987]. Our algorithmapplies to a class of games that includes the above example.

The above method is tractable only for quite simple games. For example, mechanisms thatinvolve iterated bidding and multiple auctions are not likely to be amenable to analytic approaches.For such games, I present an empirical game methodology comprising the following broad phases:

1. Generate a small set of candidate strategies. For many domains this must be done semi-manually.

2. Construct via simulation a (partial, approximate) empirical payoff matrix for the simplifica-tion of the game restricted to the candidate strategies.

3. Analyze (ideally, solve) the empirical game.

4. Assess the quality of the solutions with respect to the underlying full game.

I discuss approaches for step 1, present techniques for speeding up step 2, compare existing tech-niques for step 3 in the context of symmetry, and give procedures for achieving step 4. We use smallgames with known equilibria such as FPSB to test these methods.

We then apply the methodology to two much larger and more realistic market games: Simul-taneous Ascending Auctions (SAA), and the Trading Agent Competition (TAC) travel-shoppinggame [Wellman et al., 2001b]. TAC was created by our research group and first held in 2000. It washeld for the sixth time in August 2005 in Edinburgh. The domain involves travel agents shopping fortravel packages for a group of hypothetical clients with varying preferences over length of trip, hotelquality, and entertainment options. The shopping involves participating in dozens of simultaneousauctions of various kinds. For example, hotels are sold in multi-unit English ascending auctionswhile entertainment tickets are bought and sold in continuous double auctions (like the stock mar-ket). An agent’s payoff is the total utility it achieves for its clients, minus its net expenditure.

SAA is a far simpler model that still captures a core strategic issue in TAC: bidding for com-plementary goods in concurrent auctions. To apply step 1 to SAA and TAC, I present classes ofstrategies based on market price prediction. In particular we consider self-confirming price predic-tions and Walrasian equilibrium prices. Given a set of candidate strategies in SAA or TAC, we applythe subsequent steps of our empirical game methodology to recommend effective strategies in thesedomains.

1.4. OVERVIEW OF THESIS 5

1.4 Overview of Thesis

Much of this thesis consists of derivatives of and extensions to published papers with many coau-thors. Chapter 2 is based largely on a paper published in 2004 [Reeves and Wellman], with exten-sions to analyze and discuss additional games amenable to our approach. Chapter 2 is distinct fromthe rest of the thesis in that it takes an analytic approach to computing strategies in a class of simple,one-shot, infinite games.

Chapter 3 presents our empirical game methodology, the germinal ideas of which we publishedin the context of market-based scheduling [Wellman et al., 2003c]. We extended the approachlater [Reeves et al., 2005], also adding the core ideas for sensitivity analysis, i.e., evaluating thequality of solutions in approximate games. Our approach evolved further in subsequent papers onmarket-based scheduling, and simultaneous ascending auctions (SAA) in general [MacKie-Masonet al., 2004; Osepayshvili et al., 2005]. We also collected and revised our descriptions of the gamesolution techniques we employed [Cheng et al., 2004]. That paper presents a collection of theoremsabout symmetric games which we include here in Appendix C. The player reduction approach togame approximation in Chapter 3 was introduced in the context of TAC and local-effect games[Wellman et al., 2005b]. Other results in Chapter 3, including the proofs of key theorems and manyof the experiments with first-price sealed-bid auctions (FPSB) are new to this thesis.

Chapter 4 draws from our work in SAA [MacKie-Mason et al., 2004; Osepayshvili et al., 2005]and TAC [Wellman et al., 2004; Cheng et al., 2005] to present price prediction as a general approachfor strategies in games involving simultaneous interdependent auctions. The strategic approachesdiscussed in Chapter 4 are used to generate the candidate strategies to which we apply our empiricalgame methodology (Chapter 3) in Chapters 5 and 6.

Chapter 5 coalesces our results from a series of papers on SAA starting with a simple varia-tion on the well-studied straightforward bidding (SB) strategy, called sunk-awareness [Reeves etal., 2005]. We next considered price prediction, showing that even a naive implementation of thisapproach results in a far superior strategy [MacKie-Mason et al., 2004]. We later generalized the ap-proach to predict price distributions and concluded that a special case of this—self-confirming pricedistribution prediction—constitutes a robust strategy in a range of SAA environments [Osepayshviliet al., 2005].

In Chapter 6 we use the approach of Chapter 3 in TAC to choose the strategy for our entry inthe 2005 competition. We also report on preliminary strategic analysis of TAC in which we derivean equilibrium mixed strategy of shading hotel bids with small probability [Wellman et al., 2003a].Following the preliminary shading analysis, much of Chapter 6 is based on a preliminary report inwhich we introduce our approach to choosing our agent strategy for 2005 [Wellman et al., 2005c].New to this thesis is an analysis of the results of the 2005 competition, vindicating our strategychoice.

Chapter 2

Generating Best-Response Strategies inInfinite Games of Incomplete Information

IN WHICH we generate strategies for sealed-bid auctions and other one-shot, two-player, infinite games of incomplete information.

In a one-shot game1 an agent immediately receives a payoff after choosing a single action basedonly on knowledge of its own type, the payoff function, and the distribution from which types aredrawn. By infinite game, we mean that the action spaces are continuous. In this chapter we considerone-shot, two-player, infinite games of incomplete information. Furthermore, we restrict agent typesto a subset of the reals. A strategy in this context is a one-dimensional function (R → R) from theset of types to the set of actions. The case where the set of types and actions are finite (and especiallywhen there are no types—complete information) has been well studied in the computational gametheory literature. In the next section we discuss the state-of-the-art finite game solver, GAMBIT.But for incomplete information games with a continuum of actions available to the agents we knowof no available algorithms, though many particular infinite games of incomplete information havebeen solved in the literature.

In this chapter we define a broad class of games and present an algorithm for computing exactbest-response strategies.2 The definition of Nash equilibrium (each agent playing a best responseto the other strategies) invites an obvious algorithm for solving a game: start with a profile of seedstrategies and iteratively compute best-response profiles until a fixed-point is reached. This process(when it converges) yields a profile that is a best response to itself and thus a Nash equilibrium.After presenting our class of games (Section 2.2) and our algorithm (Section 2.3) we show examplesof iterating the best-response computation to automatically solve various new and existing games(Section 2.4).

2.1 Finite Game Approximations

GAMBIT [McKelvey et al., 1992] is a software package incorporating several algorithms for solv-ing finite games [McKelvey and McLennan, 1996]. The original 1992 implementation of GAMBIT

1Fudenberg and Tirole [1991] call them one-stage games.2The solutions are exact as long as the inputs are rational since all calculations are done in the rational field.

7

8 CHAPTER 2. BEST-RESPONSE STRATEGIES IN INFINITE GAMES

was limited to normal-form games (Definition 1.1). GALA [Koller and Pfeffer, 1997] introducedconstructs for schematic specification of extensive-form games, with a solver exploiting recent al-gorithmic advances [Koller et al., 1996]. GAMBIT subsequently incorporated these GALA features,and currently stands as the standard in general finite game solvers.

We employ a standard first-price sealed-bid auction (FPSB) to compare our approach for thefull infinite game to a discretized version amenable to finite game solvers. Consider a discretizationof (FPSB) with two players, nine types, and nine actions. Both players have a randomly (uniform)determined valuation (t) from the set {0, . . . , 8} and the available actions (a) are to bid an integer inthe set {0, . . . , 8}. Let [p, a; a′] denote the mixed strategy of performing action a with probabilityp, and a′ with probability 1− p. (There happened never to be mixed strategies with more than twoactions.) GAMBIT solves this game exactly, finding the following Bayes-Nash equilibrium:

t : 0 1 2 3 4 5 6 7 8a(t) : 0 0 1 1 2 [.455, 2; 3] 3 3 [.727, 3; 4]

This result is indeed close to the unique symmetric Bayes-Nash equilibrium, a(t) = t/2, of thecorresponding infinite game (see Section 2.4) despite varying asymmetrically—an artifact of thediscretization. However, the calculation took 90 minutes of cpu time and 17MB of memory.3 When2 additional types and actions are added to the discretization, a similar equilibrium results, requiring23 hours of cpu time and 34MB of memory.

GAMBIT’s algorithm [Koller et al., 1996] is worst-case exponential in the size of the game treewhich is itself size O(n4) in the size of the type/action spaces. Based on this complexity and ourtiming results, we conclude that (regardless of hardware advances) we are near the limit of whatGAMBIT’s algorithm can compute. In Section 2.4 we show how our method immediately finds thesolution to the full infinite FPSB game. And in Chapter 3, we present better approaches to discreteapproximations, for when it is necessary to employ them.

2.2 Infinite Games and Bayes-Nash Equilibria

We consider a class of two-player games, defined by a payoff structure that is analytically restrictive,yet captures many well-known games of interest. Let t denote the subject agent’s type and a itsaction, and t′ and a′ the type and action of the other agent.4 We assume that types are scalars drawnfrom piecewise-uniform probability distributions, and payoff functions take the following form:

u(t, a, t′, a′) =

⎧⎪⎪⎪⎪⎪⎪⎨⎪⎪⎪⎪⎪⎪⎩

θ1t+ ρ1a+ θ′1t′ + ρ′1a

′ + φ1 if −∞ < a+ αa′ < β2

θ2t+ ρ2a+ θ′2t′ + ρ′2a

′ + φ2 if β2 ≤ a+ αa′ ≤ β3

· · ·θI−1t+ ρI−1a+ θ′I−1t

′ + ρ′I−1a′ + φI−1 if βI−1 < a+ αa′ < βI

θIt+ ρIa+ θ′It′ + ρ′Ia

′ + φI if βI ≤ a+ αa′ ≤ +∞.

(2.1)

Our class comprises games with payoffs that are linear5 functions from own type and action, con-ditional on a linear comparison between own and other agent action. The form is parameterized

3The machine had four 450MHz Pentium 2 processors and 2.5GB RAM, running Linux kernel 2.4.18.4Following convention, we often call the other agent the “opponent” even though the term is less apt for non-zero-sum

games.5Functions with constant terms are technically affine rather than linear but we ignore that distinction from here on.

2.2. INFINITE GAMES AND BAYES-NASH EQUILIBRIA 9

by α, βi, θi, ρi, θ′i, ρ′i, and φi, where i ∈ {1, . . . , I} indexes the comparison case. (We define

β1 ≡ −∞ and βI+1 ≡ +∞ for notational convenience in our algorithm description below.) Theβi, βi+1 regions alternate between open and closed intervals as this is without loss of generality forarbitrary specification of boundary types (‘<’ vs. ‘≤’) on the regions6 and in particular allows theimplementation of common tie-breaking rules for sealed-bid auctions.

This parameterized payoff function captures many known mechanisms. Table 2.1 shows theparameter settings for many such games, plus new ones we introduce in Section 2.4. Given a gamedescription in this form, we search for Bayes-Nash equilibria through a straightforward iterativeprocess. Starting with a seed strategy profile (typically based on a myopic or naive strategy such astruthful bidding), we repeatedly compute best-response profiles until reaching a fixed-point or cycle.A strategy profile that is a best response to itself is, by definition, a Bayes-Nash equilibrium. Weshow that this process is effective at finding equilibria for certain games in our class. For all gamesin our class, the best-response algorithm can be used to verify candidate equilibria or ε-equilibriafound by alternate means.

Our method considers only pure strategies. Although mixed strategies are generally requiredfor infinite as well as finite games, there are broad classes of infinite games for which pure-strategyequilibria are known to exist. For example, Debreu [1952] shows that equilibria in pure strategiesexist for infinite games of complete information with action spaces that are compact, convex subsetsof a Euclidean space R

n, and payoffs that are continuous and quasiconcave in the actions. However,games in our class may have discontinuous payoff functions (most auctions do). Furthermore, ouraction space—being the set of piecewise linear functions on the unit interval—is not a compactsubset of R

n. Athey [2001] proves the existence of pure-strategy Nash equilibria for games ofincomplete information satisfying a property called the single-crossing condition (SCC). Theseresults encompass many familiar games of economic relevance, including auction games such asFPSB. Our class includes games violating SCC, for which search in the space of pure strategiesmay not be sufficient. Nevertheless, an ability to compute best responses for the broadest possibleclass of games is useful in itself.

The best-response algorithm takes as input a piecewise linear strategy with K pieces (K − 1piece boundaries),

s(t) =

⎧⎪⎪⎪⎪⎨⎪⎪⎪⎪⎩

m1t+ b1 if −∞ < t ≤ c2m2t+ b2 if c2 < t ≤ c3. . .mK−1t+ bK−1 if cK−1 < t ≤ cKmKt+ bK if cK < t ≤ +∞,

(2.2)

represented by the vectors c, m, and b. The piecewise-linear strategy class is sufficiently flexibleto approximate any strategy, although of course the complexity of the strategy or quality of theapproximation suffers as nonlinearity increases.

A two-player game is symmetric (Definition 1.2) if both players face the same payoff function.For symmetric games we start with a single seed strategy, to be repeatedly replaced with the strategythat responds best to it.7 Most of the examples presented in this chapter are symmetric and havesymmetric pure equilibria. For asymmetric games, we start with a pair of seed strategies, on every

6For example, to specify u1 in (−∞, a], u2 in (a, b], u3 in (b, c), u4 at c, and u5 in (c,∞), translate to the alternatingopen/closed specification: u1 in (−∞, a − ε), u1 in [a − ε, a], u2 in (a, b), u2 in [b, b], u3 in (b, c), u4 in [c, c], u5 in(c,∞).

7It can be shown that symmetric games must have symmetric equilibria, although there are some symmetric games withonly asymmetric pure equilibria (see Appendix C).

10 CHAPTER 2. BEST-RESPONSE STRATEGIES IN INFINITE GAMES

Gam

eθ

ρθ

′ρ

′φ

βα

FPSB0,1/2,1

0,−1/2,−

10,0,0

0,0,00,0,0

0,0−

1V

ickreyA

uction0,1/2,1

0,0,00,0,0

0,−1/2,−

10,0,0

0,0−

1V

iciousV

ickreyA

uction0,

1−k

2,1−

kk,k/2,0

−k,−k/2,0

0,k−

12,k−

10,0,0

0,0−

1Supply

Chain

Gam

e−

1,−1,0

1,1,00,0,0

0,0,00,0,0

v,v

1B

argainingG

ame

(seller)−

1,−1,0

1−k,1−

k,0

0,0,0k,k,0

0,0,00,0

−1

(buyer)0,1,1

0,−k,−k

0,0,00,1−

k,1−

k0,0,0

0,0−

1A

ll-PayA

uction0,1/2,1

−1,−

1,−1

0,0,00,0,0

0,0,00,0

−1

War

ofA

ttrition0,1/2,1

−1,−

1/2,00,0,0

0,−1/2,−

10,0,0

0,0−

1*

Shared-Good

Auction

0,1/2,10,−

1/4,−1/2

0,0,01/2,1/4,0

0,0,00,0

−1

*JointPurchase

Auction

0,10,−

1/20,0

0,1/20,−

C/2

C1

SubscriptionG

ame

0,10,−

10,0

0,00,0

C1

Contribution

Gam

e0,1

−1,−

10,0

0,00,0

C1

Table2.1:

Various

mechanism

sas

specialcasesof

theparam

eterizedpayoff

functionin

Equation

2.1.Starredgam

esare

newly

definedin

thisthesis.

Note

thatthebargaining

game,being

asymm

etric,isdescribed

bytw

opayoff

functions.T

hesegam

esare

discussedin

Section2.4.

2.3. BEST-RESPONSE ALGORITHM 11

iteration computing a best response to each to get the new pair. We may also find asymmetricequilibria when iterating from a single strategy (equivalently, a symmetric profile). In this case, acycle of length two (given our restriction to two-player games, but regardless of whether the gameis symmetric) constitutes an asymmetric equilibrium.

2.3 Existence and Computation of Piecewise Linear Best-ResponseStrategies

Here we present our algorithm to compute the best response to a given strategy by way of a con-structive proof that in our class of games, best responses to piecewise linear strategies are them-selves piecewise linear. Intuitively, the proof proceeds by first deriving an algebraic expression forexpected utility against the given strategy in terms of the payoff parameters, the distribution pa-rameters, the opponent strategy parameters, own type, and own action. By appropriate partitioningof the action space, the expected utility is expressed as a piecewise polynomial in the agent’s ac-tion. We then show that the action maximizing that expression (the best response) is a piecewiselinear expression of the agent’s type. Finally, we establish a bound for the number of pieces in thebest-response strategy.

Theorem 2.1 Given a payoff function with I regions as in Equation 2.1, an opponent type distribu-tion with cdf F that is piecewise uniform with J pieces and J − 1 piece boundaries {d2, . . . , dJ},and a piecewise linear strategy function withK pieces as in Equation 2.2, the best-response strategyis itself a piecewise linear function with no more than 2(I − 1)(J +K − 2) piece boundaries.

Proof. Finding the best response strategy means maximizing expected utility over the other agent’stype distribution. Let T be the random variable denoting the other agent’s type.

First, redefine s(t) to include additional redundant boundary points {d2, . . . , dJ} so there arenow J +K − 2 boundary points of s(t), {c2, . . . , cJ+K−1}, and

s(t) =

⎧⎨⎩

m1t+ b1 if −∞ < t ≤ c2. . .mJ+K−1t+ bJ+K−1 if cJ+K−1 < t ≤ +∞.

We now express the expected utility, factored over the pieces of s() and u(), as

EU(t, a) = ET [u(t, a, T, s(T ))] =I∑

i=1

J+K−1∑j=1

E[(θit+ ρia+ θ′iT + ρ′i(mjT + bj) + φi

∣∣cj < T ≤ cj+1, βi <.. a+ α(mjT + bj) <.. βi+1

]·Pr(cj < T ≤ cj+1, βi <.. a+ α(mjT + bj) <.. βi+1).

(We use the notation “xi <.. y” to denote xi < y if i is odd and xi ≤ y if i is even.)If αmj = 0 then the summand reduces to⎧⎪⎨⎪⎩

(θit+ ρia+ (θ′i + ρ′imj)cj + cj+1

2+ ρ′ibj + φi)

·(F (cj+1)− F (cj)) if βi − αbj <.. a <.. βi+1 − αbj0 otherwise.

12 CHAPTER 2. BEST-RESPONSE STRATEGIES IN INFINITE GAMES

(The derivation of the cdf F () of a piecewise uniform distribution is in Appendix A.1.)For the case of αmj = 0, first define

xij(a) ≡ βi − αbj − aαmj

and

yij(a) ≡ βi+1 − αbj − aαmj

with x and y swapped if αmj < 0. We also introduce mm(a, b, x) ≡ min(b,max(a, x)).We consider first the probability term in the summand, rewriting it as

pij(a) ≡Pr (βi <.. a+ α · (mjT + bj) <.. βi+1 & cj < T ≤ cj+1)= Pr (xij(a) <.. T <.. yij(a) & cj < T ≤ cj+1)=F (mm(cj , cj+1, yij(a)))− F (mm(cj , cj+1, xij(a))).

For the expectation term in the summand, we first define

xyij(a) ≡E[T | mm(cj , cj+1, xij(a)) <.. T <.. mm(cj , cj+1, yij(a))]

=mm(cj , cj+1, xij(a)) +mm(cj , cj+1, yij(a))

2.

We can now express the expected utility, EU(t, a), as

I∑i=1

J+K−1∑j=1

(θit+ ρia+ (θ′i + ρ′imj)xyij(a) + ρ′ibj + φi) · pij(a). (2.3)

This expression is a piecewise second degree polynomial in a and simply linear in t. Treating itas a function of a, parameterized by t, we can find the boundaries for the polynomial pieces (whichwill be expressions of t). This is done by setting the arguments of the maxes and mins equal andsolving for a, yielding the following four action boundaries for each region {βi, βi+1} in u() andeach region {cj , cj+1} in s():

cj+1 = yij(a) =⇒ a = βi+1 − α · (mjcj+1 + bj)cj = yij(a) =⇒ a = βi+1 − α · (mjcj + bj)

cj+1 = xij(a) =⇒ a = βi − α · (mjcj+1 + bj)cj = xij(a) =⇒ a = βi − α · (mjcj + bj).

This yields a total of at most 2(I−1)(J+K−2) unique action boundaries. So expected utility is nowexpressible as a piecewise polynomial in a (parameterized by t) with at most 2(I−1)(J+K−2)+1pieces.

For arbitrary t, we can find the action a that maximizes EU(t, a) by evaluating at each of theboundaries above and wherever the derivative (of each piece) with respect to a is zero. This yieldsup to 2(I − 1)(J + K − 2) + 1 critical points, all simple linear functions of t. Call this set ofcandidate actions C and the corresponding set of expected utilities EU(t, C). The best-responsefunction can then be expressed, for given t, as arg maxC(EU(t, C)). This is a piecewise max ofthe linear functions in C, and so it is piecewise linear.

2.4. EXAMPLES 13

It remains to establish an upper bound on the resulting number of distinct ranges for t. We claimthe size of C, 2(I − 1)(J + K − 2) + 1, is such an upper bound. To see this, first note that thepiecewise max of a set of linear functions must be convex (since, inductively, the max of a line andconvex function is convex). It is now sufficient to show that at most one new t range can be addedby taking the max of a linear function of t and a piecewise linear convex function of t. Supposethe opposite, that the addition of one line adds two pieces. They cannot be contiguous else theywould be one piece. So there must be a piece of the convex function between the two pieces of theline. This means the convex function goes below, then above, then below the line and this violatesconvexity. Therefore, each line in C adds at most one piece to the piecewise max of C and thereforethe piecewise linear best response to s() has at most 2(I − 1)(J + K − 2) + 1 pieces and thus2(I − 1)(J +K − 2) type boundaries. �

Our algorithm for finding a best response follows this constructive proof. Finding C takestime O(IJK). To actually find the piecewise linear function, arg maxC(EU(t, C)), we employa brute force approach that requires O((IJK)2) time. First, we find all possible piece boundariesby taking all pairs in C, setting them equal, and solving for t. For each t range we then computearg maxC(EU(t, C)) and merge whenever contiguous ranges have the same argmax. As the proofshows, this will yield at most 2(I − 1)(J + K − 2) type boundaries. Thus, we have shown howto find the piecewise linear best response to a piecewise linear strategy in polynomial time. Theresulting function is converted to the same strategy representation (c, m, b) that the algorithm takesas a seed for the opponent strategy.

2.4 Examples

Here we consider existing and new games and show that our method for finding best responses canconfirm or rediscover known results as well as find equilibria in new games. Refer to Table 2.1 onpage 10 for how these and other games are encoded per Equation 2.1.

There are many games not analyzed here to which our approach is amenable, such as the All-Pay auction (both winner and loser pay their bids; can be used to model activities like lobbying), theWar of Attrition (both winner and loser pay the second-highest price) [Krishna and Morgan, 1997],incomplete information versions of Cournot or Bertrand games [Fudenberg and Tirole, 1991, p.215], and various voluntary participation games in which agents choose an amount to contributefor a joint good and receive utility based on the sum of the contributions. There is a large body ofliterature on such games, also referred to as private provision of public goods. In one variant, thesubscription game, agents specify their contributions but their money is refunded if the sum is notsufficient to acquire the good. The contribution game is the same but with no refund. Until Menezeset al. [2001], only complete information versions of these games were considered in the literature.We additionally define in Table 2.1 a new variant called the joint purchase auction which is like thesubscription game except that any surplus money collected is split evenly among the participants.8

We do not analyze this game here but have found that it has a Nash equilibrium similar to that ofthe bargaining game analyzed in Section 2.4.

Our approach is not needed for incentive compatible mechanisms such as the Vickrey auction,but, reassuringly, our algorithm returns the dominant strategy of truthful bidding [Vickrey, 1961] asa best response to any other strategy in that domain.

8An arguably fairer version of the game in which the surplus is divided proportionally to the contributions is unfortu-nately not in the class of games defined by Equation 2.1.

14 CHAPTER 2. BEST-RESPONSE STRATEGIES IN INFINITE GAMES

Figure 2.1: Supply Chain game with two producers in series.

First-Price Sealed-Bid Auction

We consider the first-price sealed-bid auction (FPSB) with types that are drawn from U [0, 1] andthe following payoff function:

u(t, a, a′) =

⎧⎪⎪⎪⎪⎪⎨⎪⎪⎪⎪⎪⎩

t− a if a > a′

t− a2

if a = a′

0 otherwise.

(2.4)

In words, two agents have private valuations for a good and they submit sealed bids expressing theirwillingness to pay. The agent with the higher bid wins the good and pays its bid, thus receivinga surplus of its valuation minus its bid. The losing agent gets zero payoff. In the case of a tie, awinner is chosen randomly, so the expected utility is the average of the winning and losing utility.

This game can be given to our solver by setting the payoff parameters as in Table 2.1. Thealgorithm also needs a seed strategy, for which we can use the default strategy of truthful bidding(always bidding one’s true valuation: a(t) = t for t ∈ [0, 1]). This strategy is encoded as c = 〈0, 1〉,m = 〈0, 1, 0〉, and b = 〈0, 0, 0〉 per Equation 2.2. Note that the first and last elements of m andb are irrelevant as they correspond to type ranges that occur with zero probability. After a singleiteration (a fraction of a second of cpu time), our solver returns the strategy a(t) = t/2 for t ∈ [0, 1]which is the known Bayes-Nash equilibrium for this game (see Theorem 3.1). We find that in factwe reach this fixed point in one or two iterations from a variety of seed strategies—specifically,strategies a(t) = mt for m > 0. We approach the fixed point asymptotically (within 0.001 in teniterations) for seed strategies a(t) = mt+ b with b > 0.

Supply-Chain Game

This example derives from our work in mechanisms for supply chain formation [Walsh et al., 2000;Walsh, 2001, Chapter 6]. Consider a supply chain with two producers in series, and one consumer(see Figure 2.1). Producer 1 has output g1 and no input. Producer 2 has input g1 and output g2.The consumer—which is not an agent in this model—wants good g2. The producer costs, t1 andt2, are chosen randomly from U [0, 1]. A producer knows its own cost with certainty, but not theother producer’s cost—only the distribution (which is common knowledge). The consumer’s value,v ≥ 1, for good g2 is also common knowledge.

The producers place bids a1 and a2. If a1 + a2 ≤ v, then all agents win their bids in the auctionand the surplus of producer i is ai − ti. Otherwise, all agents receive zero surplus. In other words,the two producers each ask for a portion of the available surplus, v, and get what they ask minustheir costs if the sum of their bids is less than v.9

9Thus the expected efficiency obtained with any set of bidding policies is equal to the probability that the solution iscomputed by the auction.

2.4. EXAMPLES 15

0 0.2 0.4 0.6 0.8 1Type

0.6

0.7

0.8

0.9

1

1.1Action

Figure 2.2: Hand-coded strategy for the Supply Chain game of Section 2.4, along with best responseand empirical verification of best response (the error bars for the empirically estimated strategy areexplained in Appendix B).

Walsh et al. [2000] propose a strategy for supply-chain games defined on general graphs. In themore general setting, it is the best known strategy (for lack of any other proposed strategies in theliterature). For the particular instance of Figure 2.1, the strategy works out to:

a(t) ={t/2 + (v/2− 1/4) if 0 ≤ t < v − 13t/4 + v/4 otherwise.

Our best-response finder proves that this strategy is not a Nash equilibrium and shows how to opti-mally exploit agents who are playing it.

Figure 2.2 shows this strategy for the game with v = (10−√5)/5 ≈ 1.55 (chosen so that thereis a 0.9 probability of positive available surplus) along with the best response, as determined by ouralgorithm and confirmed by Monte Carlo simulation.

When we perform further best-response iterations it eventually falls into a cycle of period twoconsisting of the following strategies (where x = 3/4):

a1(t1) ={x if t1 ≤ xv otherwise

(2.5)

a2(t2) ={v − x if t2 ≤ v − xv otherwise.

(2.6)

The following theorem confirms that we have found an equilibrium, and follows an analogousresult [Nash, 1953] for the similar (complete information) Nash demand game.

Theorem 2.2 Equations 2.5 and 2.6 constitute an asymmetric Bayes-Nash equilibrium for thesupply-chain game, for any x ∈ [0, v].

16 CHAPTER 2. BEST-RESPONSE STRATEGIES IN INFINITE GAMES

Proof. Assume producer 2 bids according to Equation 2.6. Since producer 1 cannot improve itschance of winning with a bid below x, and can never win with a bid above x, producer 1 effectivelyhas the choice of winning with a bid of x or getting nothing. Producer 1 would choose to win at xprecisely when t1 ≤ x. Hence, (2.5) is a best response by producer 1. By a similar argument, (2.6)is a best response by producer 2, if producer 1 follows Equation 2.5. �

Following is a more interesting equilibrium, which our solver did not find but we were able toderive manually and our best-response finder confirms.

Theorem 2.3 When v ∈ [3/2, 3], the following strategy is a symmetric Bayes-Nash equilibrium forthe Supply Chain game:

a(t) ={

2v/3− 1/2 if t ≤ 2v/3− 1t/2 + v/3 otherwise.

Appendix A.2 contains the proof which is essentially an application of our best-response algorithmto the particular game and strategy above. When this strategy is used as the seed strategy for oursolver with any particular v, the same strategy is output, thus confirming that it is a Bayes-Nashequilibrium.

Bargaining Game

The supply chain game is similar to a two-player sealed-bid double auction, or bargaining game. Inthis game there is a buyer with value v′ and a seller with cost c′, each drawn from distributions thatare common knowledge. The buyer and seller place bids and if the buyer’s is greater than the seller’s,they exchange the good at a price that is some linear combination of the two bids. In the supply-chain example, we can model the seller as producer 1, with c′ = t1. Because the consumer reportsits true value, which is common knowledge, we can model the buyer as the combination of theconsumer and producer 2, with v′ = v− t2. However, to make the double auction game isomorphicto our supply-chain example, we need to alter the game so that excess surplus is thrown away insteadof shared. The bargaining game as defined above has been well studied in the literature [Chatterjeeand Samuelson, 1983; Leininger et al., 1989; Satterthwaite and Williams, 1989]. We consider thespecial case of the bargaining game where the sale price is halfway between the buy and sell offers,and the valuations are U [0, 1]. The payoff function for this game is encoded in Table 2.1.

The following is a known equilibrium [Chatterjee and Samuelson, 1983] for a seller (1) andbuyer (2):

a1(t1) = 2t1/3 + 1/4a2(t2) = 2t2/3 + 1/12.

Our solver finds this equilibrium after several iterations (with tolerance 0.001) when seeded withtruthful bidding.

Shared-Good Auction

Consider two agents who jointly own an inherently unsharable good and seek a mechanism todecide who should buy the other out and at what price. (For example, two roommates could use this

2.4. EXAMPLES 17

0 0.2 0.4 0.6 0.8 1Type

0

0.2

0.4

0.6

0.8

1

Action

Figure 2.3: a(t) = 2t/3 is a best response to truthful bidding in the shared-good auction with[A,B] = [0, 1]. This strategy is in turn a best response to itself, thus confirming the equilibrium.

mechanism to decide who gets the better bedroom.10) Assume that it is common knowledge thatthe agents’ valuations (types) are drawn from U [A,B]. We propose the mechanism

u(t, a, a′) ={t− a/2 if a > a′

a′/2 otherwise

which we chose because it has the property that if players bid their true valuations, the mechanismwould allocate the good to the agent who valued it most and split the surplus evenly between thetwo (each agent would get a payoff of t/2 where t is the larger of the two valuations). The followingBayes-Nash equilibrium also allocates the good to the agent who values it most, but that agent getsup to twice as much surplus as the other agent, depending on the minimum valuation A.

Theorem 2.4 The following is a Bayes-Nash equilibrium for the shared-good auction game whenvaluations are drawn from U [A,B]:

a(t) =2t+A

3.

Appendix A.3 contains the proof.Our solver finds this equilibrium exactly (for any specific [A,B]) in one iteration from truthful

bidding. We confirm the result via simulation as shown in Figure 2.3.

10Thanks to Kevin Lochner who both inspired the need for and helped define this mechanism.

18 CHAPTER 2. BEST-RESPONSE STRATEGIES IN INFINITE GAMES

Vicious Vickrey Auction

Brandt and Weiß [2001] introduce the following auction game:

u(t, a, t′, a′) =

⎧⎪⎪⎪⎪⎪⎨⎪⎪⎪⎪⎪⎩

(1− k)(t− a′) if a > a′

(1− k)(t− a′)− k(t′ − a)2

if a = a′

−k(t′ − a) otherwise.

(2.7)

It is a Vickrey auction generalized by the parameter k which allows agents to be spiteful in the senseof getting disutility from the other agent’s utility. For example, this might be the case for businessesthat are competitors.

Brandt and Weiß derive an equilibrium for a complete information version of this game. Ourgame solver can address the incomplete information setting.

Theorem 2.5 The following is a Bayes-Nash equilibrium for the Vicious Vickrey auction game whenvaluations are drawn from U [0, 1]:

a(t) =k + t

k + 1.

Appendix A.4 contains the proof. Our solver finds this equilibrium (for various specific values ofk) within several iterations from a variety of seed strategies.

In recent work, Morgan et al. [2003] and Brandt et al. [2005] have independently (from eachother as well as from this work) investigated incomplete-information versions of the Vicious Vickreyauction. Morgan et al. as well as Brandt et al. report the equilibrium for Vicious Vickrey given inTheorem 2.5, and in fact do so for the more general case of arbitrary type distributions and numberof agents. Morgan et al. use a payoff function rescaled from (2.7) by a factor of 1

1−k and with a

slightly different parameter, α, which is k1−k in our formulation. Interestingly, the equilibrium does

not depend on the number of agents.

2.5 Related Work

The seminal works on game theory are von Neumann and Morgenstern [1947] and Nash [1951].There are several modern general texts [Aumann and Hart, 1992; Fudenberg and Tirole, 1991; Mas-Colell et al., 1995] that analyze many of the games in Section 2.4. Algorithms for solving finitegames include the classic Lemke-Howson algorithm [Lemke and Howson, Jr., 1964] for solvingbimatrix games (two-agent finite games of complete information). In addition to the algorithmsdiscussed in connection with GAMBIT (Section 2.1), there has been recent work [La Mura, 2000;Kearns et al., 2001; Bhat and Leyton-Brown, 2004] in algorithms for computing Nash equilibria infinite games by exploiting compact representations. Govindan and Wilson [2003, 2002] have re-cently found new algorithms for searching for equilibria in normal-form and extensive-form gamesthat are faster than any algorithm implemented in GAMBIT. Blum et al. [2003] have extendedand implemented these algorithms in a package called GAMETRACER. Singh et al. [2004] adaptgraphical-game algorithms for the incomplete information case, including a class of games withcontinuous type ranges and discrete actions.

2.5. RELATED WORK 19

The approach of finding Nash equilibria by iterated best-response, sometimes termed best-replydynamics, dates back to Cournot [1838]. A similar approach known as fictitious play was intro-duced by Robinson [1951] and Brown [1951] in the early days of modern game theory. Fictitiousplay employs a best response, not to the single strategy from the last iteration, but a compositestrategy formed by mixing the strategies encountered in previous iterations according to their his-torical frequency. This method generally has better convergence properties than best-response, butShapley [1964] showed that fictitious play need not converge in general. Milgrom and Roberts[1991] cast both of these iterative methods as special cases of what they term adaptive learning andshow that in a class of games of complete information, all adaptive learning methods converge tothe unique Nash equilibrium. Fudenberg and Levine [1998] provide a good general text on itera-tive solution methods (i.e., learning) for finite games. Hon-Snir et al. [1998] apply this approachto a particular auction game with complete information. The relaxation algorithm [Uryasev andRubinstein, 1994], applicable to infinite games, but only complete information games, is a gener-alization of best-response dynamics that has been shown to converge for some classes of games.Finally, Turocy [2001] presents a Monte Carlo “stochastic approximation” approach to estimatingbest responses in a very broad class of auction games and proposes iterating the procedure to findequilibria.

The literature is rife with examples of analytically computed equilibria for particular auctiongames. For example, Milgrom and Weber [1982] derive equilibria for first- and second-price auc-tions with affiliated signals, Gordy [1998] finds closed-form equilibria in certain common-valueauctions given particular signal distributions, and Menezes et al. [2001] find equilibria for the sub-scription and contribution games. Additionally, as discussed in Section 2.4, Brandt et al. [2005] andMorgan et al. [2003] have independently derived the same symmetric Bayes-Nash equilibrium forthe more general case of the incomplete-information Vicious Vickrey auction with arbitrary typedistribution and number of agents.

Chapter 3

Empirical Game Methodology

IN WHICH we lay out a collection of techniques for generating strategies in games toobig to solve exactly, and show experimental evidence that they work.

The previous chapter describes a class of games for which we can find best-response strategiesand in many cases Nash equilibria. The strategy generation in that case is fully automated, yieldinga profile of strategies from only the description of the game. But the solution methods described inChapter 2 will simply not scale to games with several players with multidimensional types whereinformation is revealed dynamically during the game. Consider, for example, bidding in concurrentauctions for related goods (a problem I address in detail in subsequent chapters). Such a gamewould be defined by (1) a distribution over agents’ value functions defined over all subsets of a setof goods, (2) a strategy space mapping valuations crossed with all possible quote histories to a bidvector for the auctions, and (3) a payoff function incorporating the auction rules that assigns payoffsbased on valuations and bidding actions. The game size is astronomical with no game-theoreticsolution in sight.1

There are many realistic multi-player, multi-round games that we cannot literally solve (i.e.,find Nash equilibria for). Can we provide any strategic guidance at all? This chapter presents amethodology for doing so. In Section 3.2 we describe the first step: identifying a space of candi-date strategies. From there we describe the process of generating, through simulation, an empiricalestimate of an expected payoff matrix for the reduced game in which only the generated candidatestrategies are available. The process of empirically estimating the payoff matrix is very compu-tationally expensive, and we present new and existing techniques for getting better estimates withless simulation time. These include Monte Carlo variance reduction methods and ways to avoidestimating every cell in the payoff matrix. Given an empirical estimate of a game, we discuss howwe solve it using solution techniques for finite games. Finally, since the game being analyzed in thisstep is an empirical estimate, we present methods for assessing the confidence we can have in thesolutions with respect to the underlying game we care about.

We use a First-Price Sealed-Bid Auction (FPSB) as a starting point to illustrate and provideevidence for many of the techniques in this chapter. Section 2.4 describes FPSB with two players.

1Compare to chess which has been considered for half a century to be game-theoretically unsolvable [Shannon, 1950].The market games studied in this thesis have similar—in some ways more complicated—dynamic information revelation. Itis in fact the lack of such dynamics in the one-shot games of Chapter 2 that allows for the analytic solutions there, despitethe games’ infinite action and type spaces.

21

22 CHAPTER 3. EMPIRICAL GAME METHODOLOGY

In this chapter we consider the natural n-player generalization of the 2-player game defined byEquation 2.4. We now include the following theorem from the auction theory literature2 givingthe unique symmetric Nash equilibrium of FPSB. This serves as the gold standard for all of ourapproximation techniques.

Theorem 3.1 (McAfee and McMillan, 1987, p. 709) The unique symmetric Nash equilibrium forFPSB with n players having types i.i.d. with cdf F , and a lowest possible type A is

a(t) = t−

∫ t

A

F (x)n−1 dx

F (t)n−1.

For U [A,B] types this isA+ n− 1

n· t, and for U [0, 1]:3

n− 1n· t.

3.1 Measuring Solution Quality: The ε Metric

Since our techniques are based on approximations to underlying games of interest, we need a wayto assess solution quality. There are three broad sources of inaccuracy for our solutions: (1) weconsider restricted strategy spaces and could miss better strategies (even if they are in the restrictedspace since we may incompletely explore it), (2) our simulation-based payoff estimates can beriddled with sampling error (especially when the simulations take minutes per game), and (3) weintroduce other approximations, such as reducing the number of players (Section 3.5). For thesereasons, the equilibria we derive will often not correspond to equilibria in the underlying game.In light of this, we need a measure of the quality of the strategies we find when they are not inequilibrium.

Suppose that, using some approximation Γ to a game Γ, we find an equilibrium profile s∗ ofΓ. We want to determine how closely s∗ approximates an equilibrium in Γ. If we could find anequilibrium s∗ of Γ we could compare s∗ and s∗ directly. Of course, if we could do that then therewas no need to approximate Γ in the first place. Also, the comparison between s∗ and s∗ is notnecessarily meaningful if there is more than one equilibrium in Γ.

A more natural way to answer the question is to measure the potential gain to deviating froms∗ in Γ. Ideally the answer is zero and s∗ is an equilibrium for Γ as well as Γ. In that case, Γis a perfect substitute for Γ for the purpose of finding an equilibrium profile. More generally, thesmaller the gain from deviating from s∗ in Γ, the more faithful an approximation is Γ. To this end,we define the ε of a profile, following Turocy’s [2001] usage.

Definition 3.2 (Epsilon of a Profile) For a symmetric game Γ = 〈n, S, u()〉 and strategy profiles (typically an equilibrium in some approximation of Γ), we denote by εΓ(s) the potential gain to

2Krishna [2002] provides a textbook treatment.3Kagel and Levin [1993] generalize the result for the U [0, 1] case to mth-price, single-good, sealed-bid auctions:

n− 1

n + 1−m· t, (3.1)

yielding the familiar truthful bidding result for the first and second price case [Vickrey, 1961].

3.2. RESTRICTING THE STRATEGY SPACE 23

deviating from s in Γ:

εΓ(s) ≡ maxs′∈S

u(s′, s)− u(s, s).

Alternatively, we can express ε as a percentage:

ε%Γ(s) ≡ εΓ(s)u(s, s)

· 100.

This definition follows the standard notion of approximate equilibrium. Profile s is an εΓ(s)-Nash equilibrium of Γ, and εΓ(s) = 0 if and only if s is a Nash (i.e., a 0-Nash) equilibrium of Γ.Henceforth, we drop the game subscript when understood in context.

A propitious feature of the ε metric is that εΓ(s) can be evaluated even when we know only avanishing fraction of the payoff function of Γ. In particular, we only need to know the payoffs for theunilateral deviations from s. In a symmetric n-player game with S strategies, this means evaluatingfewer than nS cells of the payoff matrix out of

(n+S−1

n

), or Sn in the case of a nonsymmetric game.

3.2 Restricting the Strategy Space

A strategy is a mapping from an agent’s private information (type), and the information revealedduring the game, to an action. In the one-shot games considered in Chapter 2 there is no infor-mation revelation (by definition of a one-shot game) and the private information and actions areone-dimensional (real numbers). So strategies in that context are one-dimensional functions fromtype to action.

The first step in our methodology for empirically analyzing games is to restrict the game byconstructing a finite set of candidate strategies. In FPSB, the strategy space is the set of functionsfrom the reals to the reals (type to action). One restriction of this strategy space is to consideronly strategies of the form a(t) = kt for specific values of k.4 This is a natural parameterizationfor FPSB, generalizing truthful bidding (a(t) = t) with a bid shading factor, k. To restrict thestrategy space less severely, we could add a translational parameter b to allow affine linear strategies(kt + b). In fact, by introducing 3K − 1 parameters, we can allow piecewise linear strategies ofup to K pieces per Equation 2.2. For one-shot games with one-dimensional types (e.g., the gamesin Chapter 2 and their generalizations to more than two players) such piecewise linear strategyparameterizations will tend to suffice. Such parameterizations are appealing because they entail nodomain knowledge—the parameters can be chosen automatically. For more complicated games, thestrategy space will be too large to parameterize so naively and we rely on the manual construction ofa strategy parameterization. This may be done by starting with a baseline strategy and generalizingit via parameters. The baseline strategy may be utterly simplistic, naive, and perform miserably.But as long as the space of strategies allowed by the parameterization includes smarter strategies(and they need not be identifiable as such a priori) then our methodology has hope of finding them.For FPSB, the baseline strategy of truthful bidding is as bad as not participating, guaranteeing zeroutility. But introducing a simple shading parameter (without knowing a good setting for it) allowsour methodology to approximate the unique symmetric Nash equilibrium of the underlying game.5

The next section shows how.

4Selten and Buchta [1994] dub this ray bidding.5There are other asymmetric equilibria [Milgrom and Weber, 1985].

24 CHAPTER 3. EMPIRICAL GAME METHODOLOGY

In Chapter 4 we apply this method of generating candidate strategies to the Simultaneous As-cending Auctions domain, and in Chapter 6 we apply it to the Trading Agent Competition travel-shopping domain. Following is the definition of the restricted form of FPSB that we use throughoutthis chapter.

Definition 3.3 (FPSBn) In the n-player first-price sealed-bid auction, player i has a private valueti, decides to bid ai, and obtains payoff ti − ai if its bid is highest and zero otherwise.6 FPSBnis the special case where ti are i.i.d. U [0, 1], and agents are restricted to parameterized strategies,bidding ai(ti) = kiti for ki ∈ [0, 1], for all i ∈ {1, . . . , n}. We denote strategies in FPSBn by theparameter k.

We now establish theoretical results to which we can compare the empirical methods in the restof this chapter.

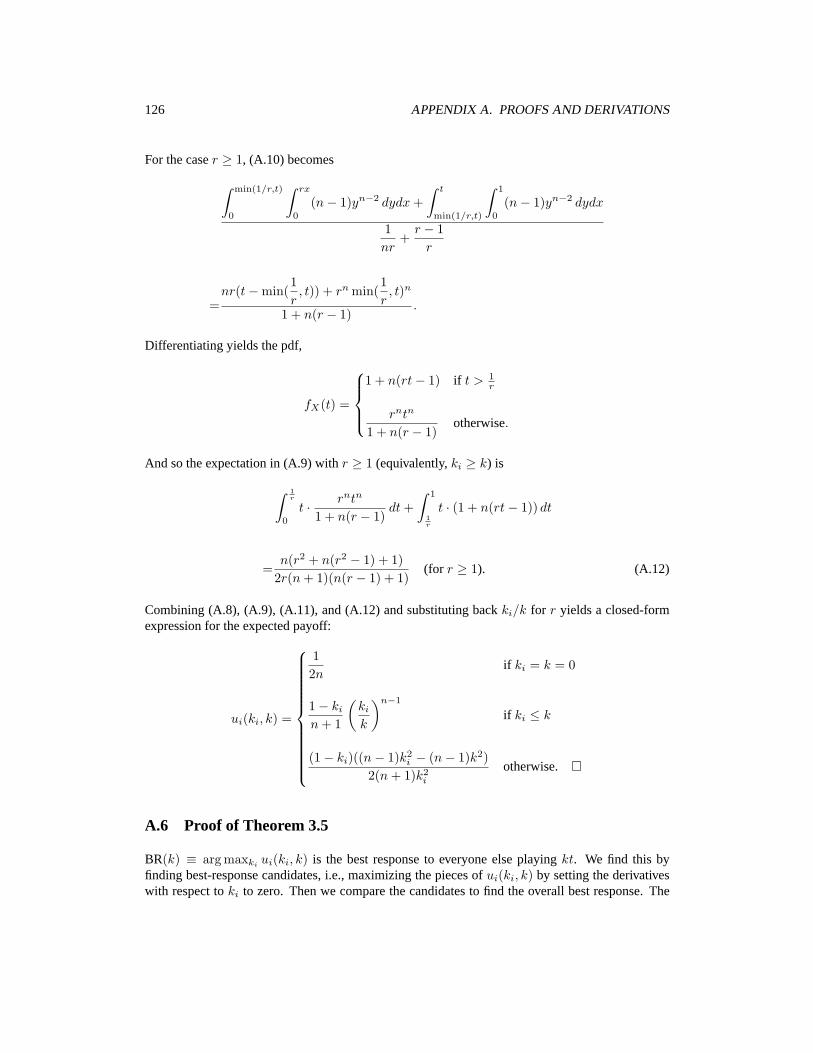

Theorem 3.4 The expected payoff for an agent playing ki against everyone else playing k in FPSBnis:

ui(ki, k) =

⎧⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎨⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎩

12n

if ki = k = 0

1− ki

n+ 1

(ki

k

)n−1

if ki ≤ k

(1− ki)((n− 1)k2i − (n− 1)k2)

2(n+ 1)k2i

otherwise.

Appendix A.5 contains the proof.

Theorem 3.5 The best response to everyone else playing k in FPSBn is:

BR(k) ≡ arg maxki

ui(ki, k) =

⎧⎪⎪⎪⎪⎪⎪⎪⎪⎨⎪⎪⎪⎪⎪⎪⎪⎪⎩

undefined if k = 0

ξ if k <n− 1n

n− 1n

if k ≥ n− 1n

,

(3.3)

where ξ ≡3√

3(k2(n2 − 1

) (9n+

√3(n+ 1) ((n− 1)k2 + 27(n+ 1)) + 9

))2/3

− 32/3k2(n2 − 1

)3(n+ 1) 3

√k2(n− 1)

(9n2 + 18n+ (n+ 1)3/2

√3(n− 1)k2 + 81(n+ 1) + 9

) .

6In the case of ties (though these happen with probability zero in the infinite game with nondegenerate strategies), oneof the bidders with the highest bid is chosen with equal probability (and thus in expectation each high bidder i receives(ti − ai)/k in a k-way tie). Formally, the full payoff function is:

ui(t, a) =

8>><>>:

ti − ai

|{x ∈ a | x = max(a)}| if ai = max(a)

0 otherwise.

(3.2)

3.2. RESTRICTING THE STRATEGY SPACE 25

Appendix A.6 contains the proof. For the special case of n = 3, Selten and Buchta [1994] point outthe third case of (3.3), that the best response to playing k greater than the equilibrium of 2/3 is toplay 2/3. Turocy [2001] generalizes this result to arbitrary n and formth-price, single-good, sealed-bid auctions: when all other agents are playing k greater than the equilibrium (see Equation 3.1) thebest response is to bid the equilibrium k. This result yields the third case of (3.3) as a special case(m = 1). Additionally, Turocy derives the second case, ξ, for the special case n = 2, albeit with atypo. The following is the best response to k ∈ (0, n−1

n ) for n = 2:

ξ =k2

3 3√√

k6 + 81k4 − 9k2− 1

33√√

k6 + 81k4 − 9k2.

Turocy [2001, p. 107] also gives the plot of (3.3) for n = 2.Interestingly, the unrestricted best response, i.e., the best response to k in the unrestricted FPSB,

is conceptually much simpler despite being nonlinear: a(t) = min(n−1n t, k) for k > 0. (We found

this using the best-response algorithm in Chapter 2 for the 2-player case, and inferred/verified it viaMonte Carlo estimation (Appendix B) for more than two players.)

Corollary 3.6 The ε of a symmetric profile in FPSBn, εFPSBn(k), is:

maxx

(ui(x, k))− ui(k, k) =

⎧⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎨⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎪⎩

12− 1

2nif k = 0

(k − ξ) (ξ2 − kξ + ξ + k + (ξ − 1)(ξ + k)n)

2ξ2(n+ 1)if k <

n− 1n

1− n+ k

((n− 1kn

)n

+ n− 1)

n2 − 1otherwise.

Proof. Having closed-form solutions for ui(ki, k) and BR(k)—Theorems 3.4 and 3.5—a closed-form solution for ε follows almost immediately. Since ui(x, 0) has no maximum, we take the supre-mum to be implied, i.e., lim

x→0ui(x, 0) = E[Ti] = 1/2. Otherwise, max

x(ui(x, k)) = ui(BR(k), k).

�

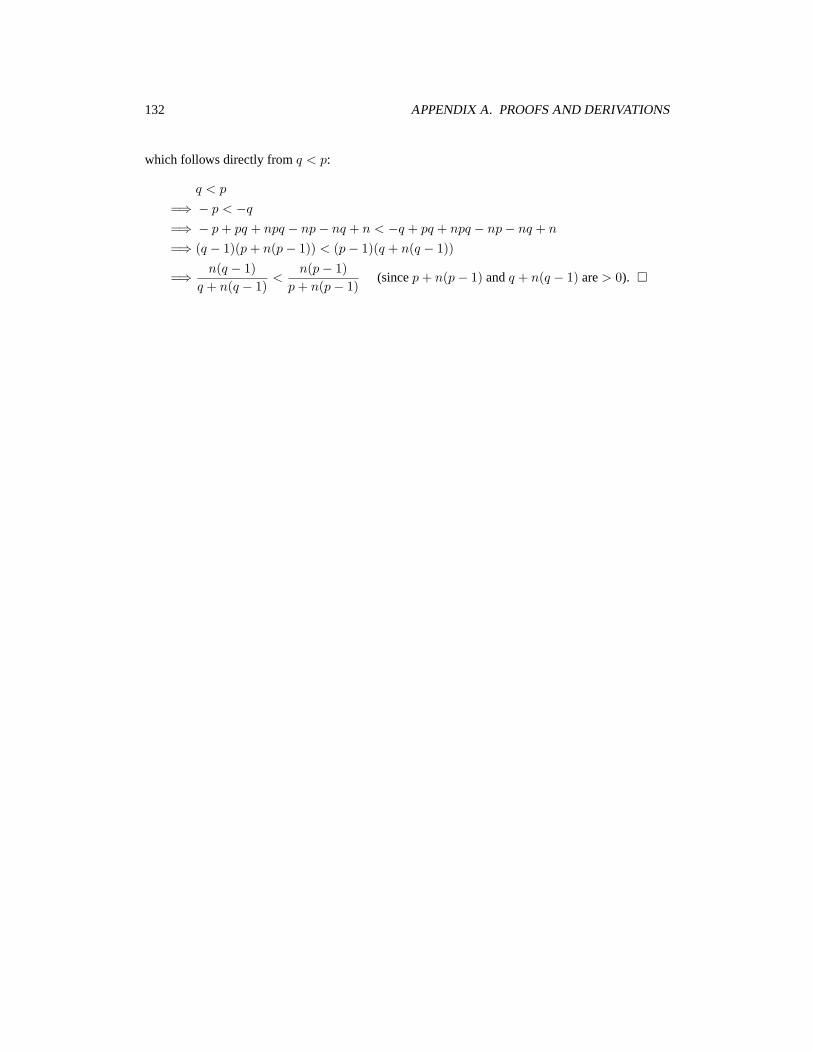

The following lemma allows us to establish the unique symmetric equilibrium of FPSBn and isalso needed for the theorems in Section 3.5.

Lemma 3.7 Let f be the function in the second case of εFPSBn(k),

f(k) ≡ (k − ξ) (ξ2 − kξ + ξ + k + (ξ − 1)(ξ + k)n)

2ξ2(n+ 1).

Then f

(n− 1n

)= 0 and f has no other positive roots.

Appendix A.7 contains the proof. That n−1n is a symmetric equilibrium of FPSBn is already implied

by the fact that it is an equilibrium in unrestricted FPSB with U [0, 1] types (Theorem 3.1) sinceFPSBn is the same game as FPSB but with a subset of the actions). But this does not establishuniqueness.

26 CHAPTER 3. EMPIRICAL GAME METHODOLOGY

Theorem 3.8n− 1n

is the unique symmetric equilibrium of FPSBn.

Proof. The theorem is trivially true for n = 1. Consider the n > 1 case. That n−1n is an equilibrium

follows directly from Theorem 3.5 (alternatively, from Theorem 3.1). For uniqueness it suffices toshow that for no other k is BR(k) = k. Theorem 3.5 rules out k = 0 and Lemma 3.7 establishes

that ε(k) = 0 for k ∈ (0,n− 1n

). �

3.3 Game Simulators and Brute-Force Estimationof Games

So far, we have taken a baseline strategy (truthful bidding) for FPSB and generalized it with a naturalparameterization (bid shading fraction). We solve this restricted form of FPSB in the previoussection, showing that the restriction does not change the unique symmetric equilibrium. Still, FPSBnis an infinite game so we further restrict the strategy space by discretizing the parameters. We nowshow how to approximate a normal form version of the game via simulation. The closed-formexpressions in the previous section allow us to compare with the limiting case of infinite simulationtime and continuous parameters.

The first step in estimating the empirical game is to write a game simulator.7 A game simulatoris a function that takes as input the agent types and the agent strategies and outputs payoffs. Forexample, a game simulator for FPSBn can be written as a straightforward extension to the payofffunction in Definition 3.3 as follows:8