General Explanations of the Administration’s Fiscal … Explanations of the Administration’s...

25

General Explanations of the Administration’s Fiscal Year 2013 Revenue Proposals Department of the Treasury February 2012 This document is available online at: http://www.treasury.gov/resource-center/tax-policy/Documents/General-Explanations-FY2013.pdf

Transcript of General Explanations of the Administration’s Fiscal … Explanations of the Administration’s...

General Explanations

of the Administration’s Fiscal Year 2013

Revenue Proposals

Department of the Treasury February 2012

This document is available online at: http://www.treasury.gov/resource-center/tax-policy/Documents/General-Explanations-FY2013.pdf

1 The Administration’s policy proposals reflect changes from a tax baseline that modifies the Budget Enforcement Act baseline by permanently extending alternative minimum tax relief, freezing the estate tax at 2012 levels, and making permanent the tax cuts enacted in 2001 and 2003. These baseline changes are described in the adjustments to the Budget Enforcement Act Baseline section, below.

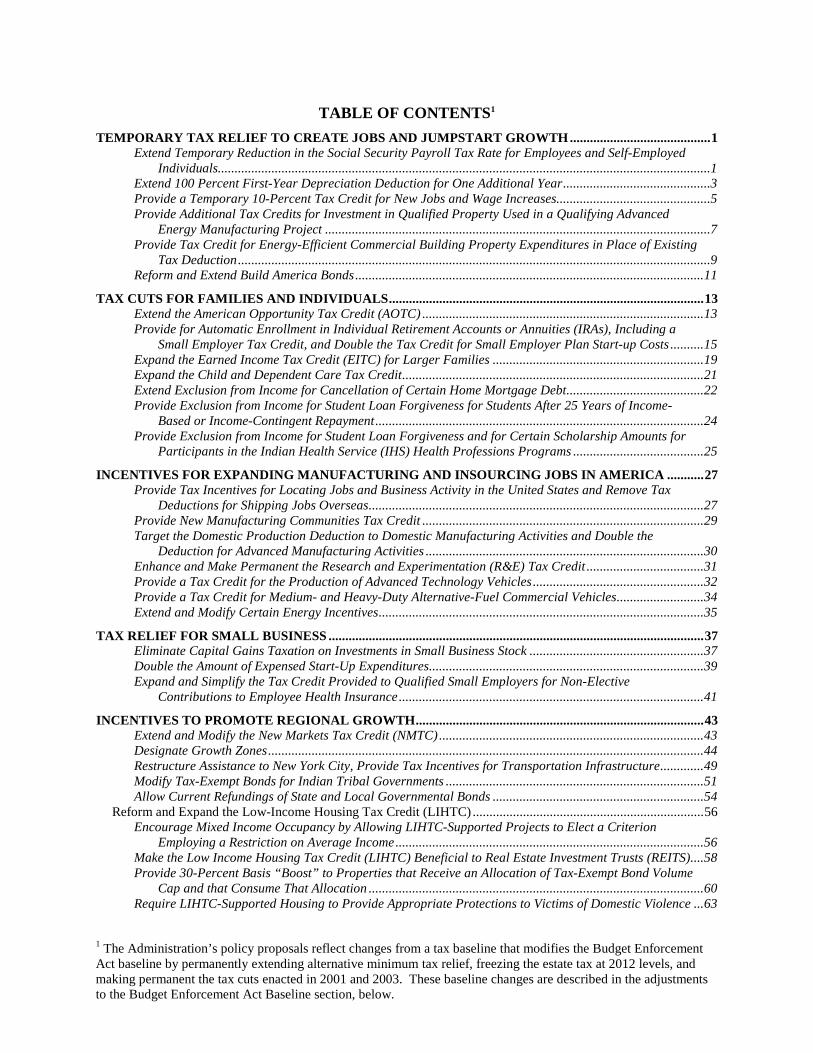

TABLE OF CONTENTS1

TEMPORARY TAX RELIEF TO CREATE JOBS AND JUMPSTART GROWTH .......................................... 1 Extend Temporary Reduction in the Social Security Payroll Tax Rate for Employees and Self-Employed

Individuals...................................................................................................................................................1 Extend 100 Percent First-Year Depreciation Deduction for One Additional Year ............................................3 Provide a Temporary 10-Percent Tax Credit for New Jobs and Wage Increases..............................................5 Provide Additional Tax Credits for Investment in Qualified Property Used in a Qualifying Advanced

Energy Manufacturing Project ...................................................................................................................7 Provide Tax Credit for Energy-Efficient Commercial Building Property Expenditures in Place of Existing

Tax Deduction .............................................................................................................................................9 Reform and Extend Build America Bonds ........................................................................................................ 11

TAX CUTS FOR FAMILIES AND INDIVIDUALS .............................................................................................. 13 Extend the American Opportunity Tax Credit (AOTC) .................................................................................... 13 Provide for Automatic Enrollment in Individual Retirement Accounts or Annuities (IRAs), Including a

Small Employer Tax Credit, and Double the Tax Credit for Small Employer Plan Start-up Costs .......... 15 Expand the Earned Income Tax Credit (EITC) for Larger Families ............................................................... 19 Expand the Child and Dependent Care Tax Credit .......................................................................................... 21 Extend Exclusion from Income for Cancellation of Certain Home Mortgage Debt ......................................... 22 Provide Exclusion from Income for Student Loan Forgiveness for Students After 25 Years of Income-

Based or Income-Contingent Repayment .................................................................................................. 24 Provide Exclusion from Income for Student Loan Forgiveness and for Certain Scholarship Amounts for

Participants in the Indian Health Service (IHS) Health Professions Programs ....................................... 25

INCENTIVES FOR EXPANDING MANUFACTURING AND INSOURCING JOBS IN AMERICA ........... 27 Provide Tax Incentives for Locating Jobs and Business Activity in the United States and Remove Tax

Deductions for Shipping Jobs Overseas .................................................................................................... 27 Provide New Manufacturing Communities Tax Credit .................................................................................... 29 Target the Domestic Production Deduction to Domestic Manufacturing Activities and Double the

Deduction for Advanced Manufacturing Activities ................................................................................... 30 Enhance and Make Permanent the Research and Experimentation (R&E) Tax Credit ................................... 31 Provide a Tax Credit for the Production of Advanced Technology Vehicles ................................................... 32 Provide a Tax Credit for Medium- and Heavy-Duty Alternative-Fuel Commercial Vehicles .......................... 34 Extend and Modify Certain Energy Incentives ................................................................................................. 35

TAX RELIEF FOR SMALL BUSINESS ................................................................................................................ 37 Eliminate Capital Gains Taxation on Investments in Small Business Stock .................................................... 37 Double the Amount of Expensed Start-Up Expenditures .................................................................................. 39 Expand and Simplify the Tax Credit Provided to Qualified Small Employers for Non-Elective

Contributions to Employee Health Insurance ........................................................................................... 41

INCENTIVES TO PROMOTE REGIONAL GROWTH ...................................................................................... 43 Extend and Modify the New Markets Tax Credit (NMTC) ............................................................................... 43 Designate Growth Zones .................................................................................................................................. 44 Restructure Assistance to New York City, Provide Tax Incentives for Transportation Infrastructure ............. 49 Modify Tax-Exempt Bonds for Indian Tribal Governments ............................................................................. 51 Allow Current Refundings of State and Local Governmental Bonds ............................................................... 54

Reform and Expand the Low-Income Housing Tax Credit (LIHTC) ..................................................................... 56 Encourage Mixed Income Occupancy by Allowing LIHTC-Supported Projects to Elect a Criterion

Employing a Restriction on Average Income ............................................................................................ 56 Make the Low Income Housing Tax Credit (LIHTC) Beneficial to Real Estate Investment Trusts (REITS).... 58 Provide 30-Percent Basis “Boost” to Properties that Receive an Allocation of Tax-Exempt Bond Volume

Cap and that Consume That Allocation .................................................................................................... 60 Require LIHTC-Supported Housing to Provide Appropriate Protections to Victims of Domestic Violence ... 63

ii

CONTINUE CERTAIN EXPIRING PROVISIONS THROUGH CALENDAR YEAR 2013 ........................... 65

UPPER-INCOME TAX PROVISIONS .................................................................................................................. 67 Sunset the Bush Tax Cuts for Those with Income in Excess of $250,000 ($200,000 if Single)............................. 67

Reinstate the Limitation on Itemized Deductions for Upper-Income Taxpayers .............................................. 67 Reinstate the Personal Exemption Phase-out for Upper-Income Taxpayers ................................................... 69 Reinstate the 36-Percent and 39.6-Percent Tax Rates for Upper-Income Taxpayers ...................................... 70 Tax Qualified Dividends as Ordinary Income for Upper-Income Taxpayers .................................................. 71 Tax Net Long-Term Capital Gains at a 20-Percent Rate for Upper-Income Taxpayers .................................. 72

Reduce the Value of Certain Tax Expenditures ...................................................................................................... 73 Reduce the Value of Certain Tax Expenditures ................................................................................................ 73

MODIFY ESTATE AND GIFT TAX PROVISIONS ............................................................................................ 75 Restore the Estate, Gift, and Generation-Skipping Transfer Tax Parameters in Effect in 2009 ...................... 75 Require Consistency in Value for Transfer and Income Tax Purposes ............................................................ 77 Modify Rules on Valuation Discounts .............................................................................................................. 79 Require a Minimum Term for Grantor Retained Annuity Trusts (GRATs) ...................................................... 80 Limit Duration of Generation-Skipping Transfer (GST) Tax Exemption ......................................................... 81 Coordinate Certain Income and Transfer Tax Rules Applicable to Grantor Trusts ........................................ 83 Extend the Lien on Estate Tax Deferrals Provided Under Section 6166 of the Internal Revenue Code .......... 84

REFORM U.S. INTERNATIONAL TAX SYSTEM.............................................................................................. 85 Defer Deduction of Interest Expense Related to Deferred Income of Foreign Subsidiaries ............................ 85 Determine the Foreign Tax Credit on a Pooling Basis .................................................................................... 87 Tax Currently Excess Returns Associated with Transfers of Intangibles Offshore .......................................... 88 Limit Shifting of Income Through Intangible Property Transfers .................................................................... 90 Disallow the Deduction for Non-Taxed Reinsurance Premiums Paid to Affiliates .......................................... 91 Limit Earnings Stripping By Expatriated Entities ............................................................................................ 92 Modify Tax Rules for Dual Capacity Taxpayers .............................................................................................. 94 Tax Gain from the Sale of a Partnership Interest on Look-Through Basis ...................................................... 96 Prevent Use of Leveraged Distributions from Related Foreign Corporations to Avoid Dividend Treatment . 98 Extend Section 338(H)(16) to Certain Asset Acquisitions ................................................................................ 99 Remove Foreign Taxes From a Section 902 Corporation’s Foreign Tax Pool When Earnings Are

Eliminated ............................................................................................................................................... 100

REFORM TREATMENT OF FINANCIAL AND INSURANCE INDUSTRY INSTITUTIONS AND PRODUCTS ............................................................................................................................................................. 101

Impose a Financial Crisis Responsibility Fee ................................................................................................ 101 Require Accrual of Income on Forward Sale of Corporate Stock .................................................................. 103 Require Ordinary Treatment of Income from Day-to-Day Dealer Activities for Certain Dealers of Equity

Options and Commodities ....................................................................................................................... 104 Modify the Definition of “Control” for Purposes of Section 249 .................................................................. 105 Modify Rules that Apply to Sales of Life Insurance Contracts ....................................................................... 106 Modify Proration Rules for Life Insurance Company General and Separate Accounts ................................ 107 Expand Pro Rata Interest Expense Disallowance for Corporate-Owned Life Insurance .............................. 109

ELIMINATE FOSSIL FUEL PREFERENCES ................................................................................................... 111 Eliminate Oil and Gas Preferences ....................................................................................................................... 111

Repeal Enhanced Oil Recovery (EOR) Credit ............................................................................................... 111 Repeal Credit for Oil and Gas Produced from Marginal Wells ..................................................................... 112 Repeal Expensing of Intangible Drilling Costs (IDCs) .................................................................................. 113 Repeal Deduction for Tertiary Injectants ....................................................................................................... 115 Repeal Exception to Passive Loss Limitation for Working Interests in Oil and Natural Gas Properties ...... 116 Repeal Percentage Depletion for Oil and Natural Gas Wells ........................................................................ 117 Increase Geological and Geophysical Amortization Period for Independent Producers to Seven Years ...... 119

Eliminate Coal Preferences ................................................................................................................................... 120 Repeal Expensing of Exploration and Development Costs ............................................................................ 120 Repeal Percentage Depletion for Hard Mineral Fossil Fuels........................................................................ 122

iii

Repeal Capital Gains Treatment for Royalties .............................................................................................. 124

OTHER REVENUE CHANGES AND LOOPHOLE CLOSERS ....................................................................... 125 Increase Oil Spill Liability Trust Fund Financing Rate by One Cent and Update the Law to Include Other

Sources of Crudes ................................................................................................................................... 125 Reinstate and Extend Superfund Excise Taxes ............................................................................................... 126 Reinstate Superfund Environmental Income Tax ........................................................................................... 127 Make Unemployment Insurance Surtax Permanent ....................................................................................... 128 Provide Short-Term Tax Relief to Employers and Expand Federal Unemployment Tax Act (FUTA) Base .. 129 Repeal Last-In, First-Out (LIFO) Method of Accounting for Inventories ...................................................... 130 Repeal Lower-Of- Cost-or-Market (LCM) Inventory Accounting Method ..................................................... 131 Eliminate Special Depreciation Rules for Purchases of General Aviation Passenger Aircraft ..................... 132 Repeal Gain Limitation for Dividends Received in Reorganization Exchanges ............................................ 133 Tax Carried (Profits) Interests as Ordinary Income ...................................................................................... 134 Expand the Definition of Substantial Built-In Loss for Purposes of Partnership Loss Transfers .................. 136 Extend Partnership Basis Limitation Rules to Nondeductible Expenditures ................................................. 137 Limit the Importation of Losses under Section 267 ........................................................................................ 138 Deny Deduction for Punitive Damages .......................................................................................................... 139 Eliminate the Deduction for Contributions of Conservation Easements on Golf Courses ............................. 140

REDUCE THE TAX GAP AND MAKE REFORMS .......................................................................................... 141 Expand Information Reporting ............................................................................................................................. 141

Require Information Reporting for Private Separate Accounts of Life Insurance Companies ...................... 141 Require a Certified Taxpayer Identification Number (TIN) from Contractors and Allow Certain

Withholding ............................................................................................................................................. 142 Improve Compliance by Businesses ..................................................................................................................... 143

Require Greater Electronic Filing of Returns ................................................................................................ 143 Authorize the Department of the Treasury to Require Additional Information to be Included in

Electronically Filed Form 5500 Annual Reports .................................................................................... 145 Implement Standards Clarifying When Employee Leasing Companies Can Be Held Liable for Their

Clients’ Federal Employment Taxes ....................................................................................................... 146 Increase Certainty with Respect to Worker Classification ............................................................................. 148 Repeal Special Estimated Tax Payment Provision for Certain Insurance Companies .................................. 151 Eliminate Special Rules Modifying the Amount of Estimated Tax Payments by Corporations ...................... 153

Strengthen Tax Administration ............................................................................................................................. 154 Streamline Audit and Adjustment Procedures for Large Partnerships .......................................................... 154 Revise Offer-in-Compromise Application Rules ............................................................................................ 157 Expand Internal Revenue Service (IRS) Access to Information in the National Directory of New Hires for

Tax Administration Purposes .................................................................................................................. 158 Make Repeated Willful Failure to File a Tax Return a Felony ...................................................................... 159 Facilitate Tax Compliance with Local Jurisdictions ...................................................................................... 160 Extend Statute of Limitations where State Adjustment Affects Federal Tax Liability .................................... 161 Improve Investigative Disclosure Statute ....................................................................................................... 163 Require Taxpayers Who Prepare Their Returns Electronically but File Their Returns on Paper to Print

Their Returns with a 2-D Bar Code ........................................................................................................ 164 Allow the Internal Revenue Service (IRS) to Absorb Credit and Debit Card Processing Fees for Certain

Tax Payments .......................................................................................................................................... 165 Improve and Make Permanent the Provision Authorizing the Internal Revenue Service (IRS) to Disclose

Certain Return Information to Certain Prison Officials ......................................................................... 166 Extend Internal Revenue Service (IRS) Math Error Authority in Certain Circumstances ............................. 168 Impose a Penalty on Failure to Comply with Electronic Filing Requirements .............................................. 170

SIMPLIFY THE TAX SYSTEM ........................................................................................................................... 171 Simplify the Rules for Claiming the Earned Income Tax Credit (EITC) for Workers Without Qualifying

Children .................................................................................................................................................. 171 Eliminate Minimum Required Distribution (MRD) Rules for Individual Retirement Account or Annuity

(IRA) Plan Balances of $75,000 or Less ................................................................................................. 172

iv

Allow All Inherited Plan and Individual Retirement Account or Annuity (IRA) Balances to be Rolled Over Within 60 Days ........................................................................................................................................ 174

Clarify Exception to Recapture Unrecognized Gain on Sale of Stock to an Employee Stock Ownership Plan (ESOP) ............................................................................................................................................ 176

Repeal Non-Qualified Preferred Stock (NQPS) Designation ......................................................................... 177 Repeal Preferential Dividend Rule for Publicly Offered Real Estate Investment Trusts (REITS) ................. 178 Reform Excise Tax Based on Investment Income of Private Foundations ..................................................... 180 Remove Bonding Requirements for Certain Taxpayers Subject to Federal Excise Taxes on Distilled

Spirits, Wine and Beer ............................................................................................................................ 181 Simplify Tax-Exempt Bonds ................................................................................................................................ 183

Simplify Arbitrage Investment Restrictions .................................................................................................... 183 Simplify Single-Family Housing Mortgage Bond Targeting Requirements ................................................... 185 Streamline Private Business Limits on Governmental Bonds ........................................................................ 186

USER FEES ............................................................................................................................................................. 187 Reform Inland Waterways Funding ............................................................................................................... 187

OTHER INITIATIVES ........................................................................................................................................... 189 Allow Offset of Federal Income Tax Refunds to Collect Delinquent State Income Taxes for Out-of-State

Residents ................................................................................................................................................. 189 Authorize the Limited Sharing of Business Tax Return Information to Improve the Accuracy of Important

Measures of Our Economy ...................................................................................................................... 190 Eliminate Certain Reviews Conducted by the U.S. Treasury Inspector General for Tax Administration

(TIGTA). .................................................................................................................................................. 192 Modify Indexing to Prevent Deflationary Adjustments .................................................................................. 193

PROGRAM INTEGRITY INITIATIVES ............................................................................................................ 195 Increase Levy Authority for Payments to Medicare Providers with Delinquent Tax Debt ............................ 195 Implement a Program Integrity Statutory Cap Adjustment for the Internal Revenue Service (IRS) .............. 196

ADJUSTMENTS TO THE BUDGET ENFORCEMENT ACT BASELINE ..................................................... 197

TABLES OF REVENUE ESTIMATES ................................................................................................................ 201

General Explanations of the

Administration’s Fiscal Year 2013 Revenue Proposals

Department of the Treasury February 2012

67

UPPER-INCOME TAX PROVISIONS

Sunset the Bush Tax Cuts for Those with Income in Excess of $250,000 ($200,000 if Single) REINSTATE THE LIMITATION ON ITEMIZED DEDUCTIONS FOR UPPER-INCOME TAXPAYERS Current Law Individual taxpayers may elect to itemize their deductions instead of claiming a standard deduction. Itemized deductions include medical and dental expenses (in excess of 7.5 percent of AGI), 8 State and local property taxes and income taxes,9 interest paid, gifts to charities, casualty and theft losses (in excess of 10 percent of AGI), job expenses and certain miscellaneous expenses (some only in excess of 2 percent of AGI). Prior to the enactment of the Economic Growth and Tax Relief Reconciliation Tax Act (EGTRRA) in 2001, otherwise allowable itemized deductions (other than medical expenses, investment interest, theft and casualty losses, and gambling losses) were reduced by 3 percent of the amount by which AGI exceeded a statutory floor that was indexed annually for inflation, but not by more than 80 percent of the otherwise allowable deductions. EGTRRA temporarily eliminated the itemized deduction limitation and the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (TRUIRJCA) extended this tax relief for two years, through 2012. The baseline for this Budget assumes that relief from this limitation on itemized deductions as provided by EGTRRA and TRUIRJCA is made permanent. For 2012, if it were applicable, the AGI floor for the limitation on itemized deductions would be $173,650 ($86,825 if married filing separately). Reason for Change Limiting the tax benefit of upper-income taxpayers’ itemized deductions would reduce the deficit, make the income tax system more progressive, and distribute the cost of government more fairly among taxpayers of various income levels. Proposal The Administration proposes to reinstate the limitation on itemized deductions for upper-income taxpayers. Itemized deductions (other than medical expenses, investment interest, theft and

8 The AGI floor for medical and dental expenses rises to 10 percent in 2013 for taxpayers under 65 years of age and in 2017 for all other taxpayers. 9 In 2011, taxpayers could elect to deduct State and local general sales taxes instead of State and local income taxes. This Budget includes a proposal to extend that election for two years through 2013.

68

casualty losses, and gambling losses) would be reduced by 3 percent of the amount by which AGI exceeds statutory thresholds, but not by more than 80 percent of the otherwise allowable deductions. The thresholds would be $250,000 for married taxpayers filing joint returns, $225,000 for head-of household taxpayers, $200,000 for single taxpayers, and $125,000 for married taxpayers filing separately. The AGI thresholds are at 2009 levels, and would be indexed for inflation thereafter. The change would be effective for taxable years beginning after December 31, 2012.

69

REINSTATE THE PERSONAL EXEMPTION PHASE-OUT FOR UPPER-INCOME TAXPAYERS Current Law Individual taxpayers generally are entitled to a personal exemption for the taxpayer and for each dependent. The amount of each personal exemption is $3,800 for 2012 and is indexed annually for inflation. Prior to the enactment of the Economic Growth and Tax Relief Reconciliation Tax Act (EGTRRA) in 2001, all personal exemptions were reduced or completely phased out simultaneously for higher-income taxpayers. For a taxpayer with adjusted gross income (AGI) in excess of the threshold amount for the taxpayer’s filing status, the amount of each personal exemption was reduced by 2 percent of the exemption amount for that year for each $2,500 ($1,250 if married filing separately) or fraction thereof by which AGI exceeded that threshold. EGTRRA temporarily eliminated this personal exemption phase-out, and the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (TRUIRJCA) extended this relief for two years through 2012. The baseline for this Budget assumes that relief from the phase-out of personal exemptions as provided by EGTRRA and TRUIRJCA is made permanent. For 2012, if it were applicable, the AGI floor for the personal exemption phase-out would be $260,500 for married taxpayers filing a joint return ($173,650 for single taxpayers). Reason for Change Limiting the tax benefit of upper-income taxpayers’ personal exemptions would reduce the deficit, make the income tax system more progressive, and distribute the cost of government more fairly among taxpayers of various income levels. Proposal The Administration proposes to reinstate the phase-out of personal exemptions for upper-income taxpayers. The proposal would affect taxpayers with AGI above threshold levels that vary by filing status. The thresholds would be $250,000 for married taxpayers filing joint returns, $225,000 for head-of household taxpayers, $200,000 for single taxpayers, and $125,000 for married taxpayers filing separately. The AGI thresholds are at 2009 levels, and would be indexed for inflation thereafter. Under the proposal, the amount of each personal exemption would be reduced (but not below zero) by 2 percent of the exemption amount for that year for each $2,500 ($1,250 if married filing separately) or fraction thereof by which AGI exceeded the threshold. The change would be effective for taxable years beginning after December 31, 2012

70

REINSTATE THE 36-PERCENT AND 39.6-PERCENT TAX RATES FOR UPPER-INCOME TAXPAYERS Current Law Prior to the enactment of the Economic Growth and Tax Relief Reconciliation Act (EGTRRA) in 2001, the two highest individual income tax rates were 36 percent and 39.6 percent. EGTRRA temporarily reduced those tax rate brackets to 33 percent and 35 percent. Under EGTRRA, these tax rate reductions were scheduled to expire after 2010. The lower rates were extended through 2012 by the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010. Under current law they revert to 36 percent and 39.6 percent after December 31, 2012. However, the baseline for this Budget assumes that the 33 percent and 35 percent tax rates as provided by EGTRRA and TRUIRJCA are made permanent. For 2012, the 33 percent rate applies to taxable income over $217,450 for married taxpayers filing a joint return (over $178,650 for single taxpayers). The 35 percent rate applies to taxable income over $388,350 for both married and single filers. Reason for Change Increasing the income tax liability of higher-income taxpayers would reduce the deficit, make the income tax system more progressive, and distribute the cost of government more fairly among taxpayers of various income levels. Proposal The Administration proposes to replace part of the 33 percent and all of the 35 percent tax rate brackets with the prior law tax rate brackets of 36 percent and 39.6 percent. The 36-percent tax rate bracket would begin at taxable income level calculated as the appropriate AGI threshold minus the appropriate standard deduction and one personal exemption (two for married taxpayers filing jointly). The AGI thresholds would be $250,000 for married taxpayers filing joint returns, $225,000 for head-of household taxpayers, $200,000 for single taxpayers, and $125,000 for married taxpayers filing separately. The AGI thresholds are at 2009 levels, and would be indexed for inflation thereafter. The change would be effective for taxable years beginning after December 31, 2012.

71

TAX QUALIFIED DIVIDENDS AS ORDINARY INCOME FOR UPPER-INCOME TAXPAYERS Current Law Under current law, the maximum income tax rate on qualified dividends received by individuals is 15 percent. In addition, any qualified dividends that would otherwise be taxed at a 10- or 15-percent ordinary income tax rate are taxed at a 0-percent rate. The same rates apply for purposes of the alternative minimum tax. The 0- and 15-percent rates for qualified dividends are scheduled to expire for taxable years beginning after December 31, 2012. In 2013, all dividends would be taxed at ordinary individual income tax rates of up to 39.6 percent. The Administration’s revenue baseline assumes that the current 0- and 15-percent tax rates on qualified dividends are permanently extended for all taxpayers. Reasons for Change Restoring the ordinary income tax treatment of qualified dividends for upper-income taxpayers would reduce the deficit and make the tax system more progressive. Taxing qualified dividends at the same rates as other ordinary income would also help simplify the tax code. Proposal The proposal would allow the current reduced tax rates on qualified dividends to expire as scheduled for income that would be taxable in the 36 percent or 39.6 percent brackets. This proposal would be effective for dividends received after December 31, 2012.

72

TAX NET LONG-TERM CAPITAL GAINS AT A 20-PERCENT RATE FOR UPPER-INCOME TAXPAYERS Current Law Under current law, the maximum rate of tax on net long-term capital gains of an individual is 15 percent. In addition, any capital gains that would otherwise be taxed at a 10- or 15-percent ordinary income tax rate are taxed at a 0-percent rate. Gains from recapture of depreciation on certain real estate (section 1250) are taxed at ordinary rates up to 25 percent. Gains from the sale of collectibles are taxed at ordinary rates up to 28 percent. Special provisions also apply to gains from the sale of certain small business stock. The same rates apply for purposes of the alternative minimum tax. Capital losses generally are deductible in full against capital gains. In addition, individual taxpayers may deduct up to $3,000 of capital losses from ordinary income each year. Any remaining unused capital losses may be carried forward indefinitely to a future year. The 0- and 15-percent rates for capital gains are scheduled to expire for taxable years beginning after December 31, 2012. On January 1, 2013, the maximum income tax rate on capital gains would increase to 20 percent (18 percent for assets purchased after December 31, 2000 and held longer than five years). The Administration’s revenue baseline assumes that the current 0- and 15-percent tax rates on net long-term net capital gains are permanently extended for all taxpayers. Reasons for Change Restoring the 20-percent capital gains tax rate for upper-income taxpayers and repealing the reduced tax rates on gains from assets held over five years for would reduce the deficit and make the tax system more progressive. Proposal The proposal would allow the current reduced tax rates on long-term capital gains to expire as scheduled for capital gain income that, in the absence of any preferential treatment of long-term capital gains, would be taxable in the 36 percent or 39.6 percent brackets. It would also repeal the special reduced rate on gains from assets held over five years. Thus, the maximum long-term capital gains tax rate for upper-income taxpayers would be 20 percent. The special rates applying to recapture of depreciation on certain real estate (Section 1250 recapture) and collectibles, and the special provisions applying to the sale of certain small business stock would be retained. This proposal would be effective for long-term capital gains realized after December 31, 2012.

73

Reduce the Value of Certain Tax Expenditures REDUCE THE VALUE OF CERTAIN TAX EXPENDITURES Current Law Under current law, individual taxpayers may reduce their taxable income by excluding certain types or amounts of income, claiming certain deductions in the computation of adjusted gross income (AGI), and claiming either itemized deductions or a standard deduction. The tax reduction from the last dollar excluded or deducted is $1.00 times the taxpayer’s marginal income tax rate (e.g., if the marginal tax rate were 35 percent, tax value of the last dollar deducted would be 35 cents). Certain types of income are excluded permanently or deferred temporarily from income subject to tax. These items include interest on State or local bonds, amounts paid by employers and employees for employer-sponsored health coverage, contributions to health savings accounts and Archer MSAs, amounts paid by employees and employers for defined contribution retirement plans, certain premiums for health insurance for self-employed individuals, certain income attributable to domestic production activities, certain trade and business deductions of employees, moving expenses, interest on education loans, and certain higher education expenses. Individual taxpayers may elect to itemize their deductions instead of claiming a standard deduction. In general, itemized deductions include medical and dental expenses (in excess of 7.5 percent of AGI)10, state and local property taxes and income taxes11, interest paid, gifts to charities, casualty and theft losses (in excess of 10 percent of AGI), job expenses and certain miscellaneous expenses (some only in excess of 2 percent of AGI).

For upper-income taxpayers, otherwise allowable itemized deductions (other than medical expenses, investment interest, theft and casualty losses, and gambling losses) were reduced prior to 2010 if AGI exceeded a statutory floor that was indexed annually for inflation. The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) temporarily eliminated this provision and the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (TRUIRJCA) extended the elimination of the limitation on itemized deductions for two years, through 2012. The baseline for this Budget assumes that relief from this limitation on itemized deductions as provided by EGTRRA and TRUIRJCA is made permanent. However, another proposal in this Budget would reinstate this limitation on itemized deductions beginning in 2013 for upper-income taxpayers only.

10 The AGI floor for medical and dental expenses rises to 10 percent in 2013 for taxpayers under 65 years of age and in 2017 for all other taxpayers. 11 In 2011, taxpayers could elect to deduct state and local general sales taxes instead of state and local income taxes. This Budget includes a proposal to extend that election for two years through 2013.

74

Reasons for Change Increasing the income tax liability of higher-income taxpayers would reduce the deficit, make the income tax system more progressive, and distribute the cost of government more fairly among taxpayers of various income levels. In particular, limiting the value of tax expenditures including itemized deductions, certain exclusions in income subject to tax, and certain deductions in the computation of AGI, would reduce the benefit that high income taxpayers receive from those tax expenditures and help close the gap between the value of these tax expenditures for high-income Americans and the value for middle class Americans. Proposal The proposal would limit the tax value of specified deductions or exclusions from AGI and all itemized deductions. This limitation would reduce the value to 28 percent of the specified exclusions and deductions that would otherwise reduce taxable income in the 36-percent or 39.6-percent tax brackets. A similar limitation also would apply under the alternative minimum tax. The income exclusions and deductions limited by this provision would include any tax-exempt state and local bond interest, employer-sponsored health insurance paid for by employers or with before-tax employee dollars, health insurance costs of self-employed individuals, employee contributions to defined contribution retirement plans and individual retirement arrangements, the deduction for income attributable to domestic production activities, certain trade and business deductions of employees, moving expenses, contributions to health savings accounts and Archer MSAs, interest on education loans, and certain higher education expenses. This proposal would apply to itemized deductions after they have been reduced by the statutory limitation on certain itemized deductions for higher income taxpayers. The proposal would be effective for taxable years beginning after December 31, 2012.

75

MODIFY ESTATE AND GIFT TAX PROVISIONS

RESTORE THE ESTATE, GIFT, AND GENERATION-SKIPPING TRANSFER TAX PARAMETERS IN EFFECT IN 2009 Current Law Until the end of 2012, the current estate, generation-skipping transfer, and gift tax rate is 35 percent, and each individual has a lifetime exclusion for all three types of taxes of $5 million (indexed after 2011 for inflation from 2010). The surviving spouse of a person who dies after December 31, 2010, may be eligible to increase the surviving spouse’s exclusion amount by the portion of the predeceased spouse’s exclusion that remained unused at the predeceased spouse’s death (in other words, the exclusion is “portable”). However, after 2012, the tax rate and tax brackets, the amount of the exclusion, and the law governing these three types of taxes will revert to the law in effect in 2001, as if the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) had never been enacted. Portability of the exemption between spouses for both gift and estate tax purposes, enacted as part of the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010 (TRUIRJCA), also will no longer apply. Prior to the enactment of EGTRRA in 2001, the maximum tax rate was 55 percent, plus a 5-percent surcharge on the amount of the taxable estate between approximately $10 million and $17.2 million (designed to recapture the benefit of the lower rate brackets). The exclusion for estate and gift tax purposes was $675,000 and was scheduled to increase to $1 million by 2006. Under EGTRRA, beginning in 2002, the top tax rate for all three types of taxes was reduced incrementally until it was 45 percent in 2007. In 2004, the exemption for estate taxes (but not for gift taxes) began to increase incrementally until it was $3.5 million in 2009, and the generation-skipping transfer (GST) tax exemption and rate became unified with the estate tax exemption and rate. During this post-EGTRRA period through 2009, the gift tax exemption remained $1 million. Under EGTRRA, for 2010, the estate tax was replaced with carryover basis treatment of bequests, the GST tax was not applicable, and the gift tax remained in effect with a $1 million exclusion and a 35-percent tax rate. The EGTRRA provisions were scheduled to expire at the end of 2010, meaning that the estate tax and GST tax would be inapplicable for only one year. In 2010, TRUIRJCA retroactively changed applicable law for 2010 by providing a top estate tax rate of 35 percent for taxpayers electing estate tax rather than carryover-basis treatment. It also retroactively reinstated the GST tax and unified the exemption for estate, GST, and gift taxes beginning in 2011 with a $5 million total lifetime exclusion for all three taxes (indexed after 2011 for inflation from 2010). The Administration’s FY 2013 baseline assumes that the estate tax provisions in effect in 2012 are permanent. Reasons for Change TRUIRJCA provided a substantial tax cut to the most affluent taxpayers that we cannot afford to continue. We need a permanent estate tax law that provides certainty to taxpayers, is fair, and raises an appropriate amount of revenue.

76

Proposal The proposal would make permanent the estate, GST, and gift tax parameters as they applied during 2009. The top tax rate would be 45 percent and the exclusion amount would be $3.5 million for estate and GST taxes, and $1 million for gift taxes. As reflected in the Administration’s adjusted baseline projection, the portability of unused estate and gift tax exclusion between spouses would be made permanent. The proposal would be effective for the estates of decedents dying, and for transfers made, after December 31, 2012.

77

REQUIRE CONSISTENCY IN VALUE FOR TRANSFER AND INCOME TAX PURPOSES Current Law Section 1014 provides that the basis of property acquired from a decedent generally is the fair market value of the property on the decedent’s date of death. Similarly, property included in the decedent’s gross estate for estate tax purposes generally must be valued at its fair market value on the date of death. Although the same valuation standard applies to both provisions, current law does not explicitly require that the recipient’s basis in that property be the same as the value reported for estate tax purposes. Section 1015 provides that the donee’s basis in property received by gift during the life of the donor generally is the donor’s adjusted basis in the property, increased by gift tax paid on the transfer. If, however, the donor’s basis exceeds the fair market value of the property on the date of the gift, the donee’s basis is limited to that fair market value for purposes of determining any subsequent loss. Section 1022, applicable to the estates of decedents dying during 2010 if a timely election to that effect is made, provides that the basis of property acquired from such a decedent is the lesser of the fair market value of the property on the decedent’s date of death or the decedent’s adjusted basis in that property as increased by the additional basis (if any) allocated to that property by the executor under section 1022. Section 6034A imposes a consistency requirement – specifically, that the recipient of a distribution of income from a trust or estate must report on the recipient’s own income tax return the exact information included on the Schedule K-1 of the trust’s or estate’s income tax return – but this provision applies only for income tax purposes, and the Schedule K-1 does not include basis information. Reasons for Change Taxpayers should be required to take consistent positions in dealing with the Internal Revenue Service. The basis of property acquired from a decedent generally is the fair market value of the property on the decedent’s date of death. Consistency requires that the same value be used by the recipient (unless that value is in excess of the accurate value). In the case of property transferred on death or by gift during life, often the executor of the estate or the donor, respectively, will be in the best position to ensure that the recipient receives the information that will be necessary to accurately determine the recipient’s basis in the transferred property. Proposal This proposal would impose both a consistency and a reporting requirement. The basis of property received by reason of death under section 1014 must equal the value of that property for estate tax purposes. The basis of property received by gift during the life of the donor must equal the donor’s basis determined under section 1015. The basis of property acquired from a decedent to whose

78

estate section 1022 is applicable is the basis of that property, including any additional basis allocated by the executor, as reported on the Form 8939 that the executor filed. This proposal would require that the basis of the property in the hands of the recipient be no greater than the value of that property as determined for estate or gift tax purposes (subject to subsequent adjustments). A reporting requirement would be imposed on the executor of the decedent’s estate and on the donor of a lifetime gift to provide the necessary valuation and basis information to both the recipient and the Internal Revenue Service. A grant of regulatory authority would be included to provide details about the implementation and administration of these requirements, including rules for situations in which no estate tax return is required to be filed or gifts are excluded from gift tax under section 2503, for situations in which the surviving joint tenant or other recipient may have better information than the executor, and for the timing of the required reporting in the event of adjustments to the reported value subsequent to the filing of an estate or gift tax return. The proposal would be effective for transfers on or after the date of enactment.

79

MODIFY RULES ON VALUATION DISCOUNTS Current Law The fair market value of property transferred, whether on the death or during the life of the transferor, generally is subject to estate or gift tax at the time of the transfer. Sections 2701 through 2704 of the Internal Revenue Code were enacted to prevent the reduction of taxes through the use of “estate freezes” and other techniques designed to reduce the value of the transferor’s taxable estate and discount the value of the taxable transfer to the beneficiaries of the transferor without reducing the economic benefit to the beneficiaries. Generally, section 2704(b) provides that certain “applicable restrictions” (that would normally justify discounts in the value of the interests transferred) are to be ignored in valuing interests in family-controlled entities if those interests are transferred (either by gift or on death) to or for the benefit of other family members. The application of these special rules results in an increase in the transfer tax value of those interests above the price that a hypothetical willing buyer would pay a willing seller, because section 2704(b) generally directs an appraiser to ignore the rights and restrictions that otherwise would support significant discounts for lack of marketability and control. Reasons for Change Judicial decisions and the enactment of new statutes in most states, in effect, have made section 2704(b) inapplicable in many situations by recharacterizing restrictions such that they no longer fall within the definition of an “applicable restriction.” In addition, the Internal Revenue Service has identified other arrangements designed to circumvent the application of section 2704. Proposal This proposal would create an additional category of restrictions (“disregarded restrictions”) that would be ignored in valuing an interest in a family-controlled entity transferred to a member of the family if, after the transfer, the restriction will lapse or may be removed by the transferor and/or the transferor’s family. Specifically, the transferred interest would be valued by substituting for the disregarded restrictions certain assumptions to be specified in regulations. Disregarded restrictions would include limitations on a holder’s right to liquidate that holder’s interest that are more restrictive than a standard to be identified in regulations. A disregarded restriction also would include any limitation on a transferee’s ability to be admitted as a full partner or to hold an equity interest in the entity. For purposes of determining whether a restriction may be removed by member(s) of the family after the transfer, certain interests (to be identified in regulations) held by charities or others who are not family members of the transferor would be deemed to be held by the family. Regulatory authority would be granted, including the ability to create safe harbors to permit taxpayers to draft the governing documents of a family-controlled entity so as to avoid the application of section 2704 if certain standards are met. This proposal would make conforming clarifications with regard to the interaction of this proposal with the transfer tax marital and charitable deductions. This proposal would apply to transfers after the date of enactment of property subject to restrictions created after October 8, 1990 (the effective date of section 2704).

80

REQUIRE A MINIMUM TERM FOR GRANTOR RETAINED ANNUITY TRUSTS (GRATS) Current Law Section 2702 provides that, if an interest in a trust is transferred to a family member, the value of any interest retained by the grantor is valued at zero for purposes of determining the transfer tax value of the gift to the family member(s). This rule does not apply if the retained interest is a “qualified interest.” A fixed annuity, such as the annuity interest retained by the grantor of a GRAT, is one form of qualified interest, so the gift of the remainder interest in the GRAT is determined by deducting the present value of the retained annuity during the GRAT term from the fair market value of the property contributed to the trust. Generally, a GRAT is an irrevocable trust funded with assets expected to appreciate in value, in which the grantor retains an annuity interest for a term of years that the grantor expects to survive. At the end of that term, the assets then remaining in the trust are transferred to (or held in further trust for) the beneficiaries, who generally are descendants of the grantor. If the grantor dies during the GRAT term, however, the trust assets (at least the portion needed to produce the retained annuity) are included in the grantor’s gross estate for estate tax purposes. To this extent, although the beneficiaries will own the remaining trust assets, the estate tax benefit of creating the GRAT (specifically, the tax-free transfer of the appreciation during the GRAT term in excess of the annuity payments) is not realized. Reasons for Change GRATs have proven to be a popular and efficient technique for transferring wealth while minimizing the gift tax cost of transfers, providing that the grantor survives the GRAT term and the trust assets do not depreciate in value. The greater the appreciation, the greater the transfer tax benefit achieved. Taxpayers have become adept at maximizing the benefit of this technique, often by minimizing the term of the GRAT (thus reducing the risk of the grantor’s death during the term), in many cases to two years, and by retaining annuity interests significant enough to reduce the gift tax value of the remainder interest to zero or to a number small enough to generate only a minimal gift tax liability. Proposal This proposal would require, in effect, some downside risk in the use of this technique by imposing the requirement that a GRAT have a minimum term of ten years and a maximum term of the life expectancy of the annuitant plus ten years. The proposal also would include a requirement that the remainder interest have a value greater than zero at the time the interest is created and would prohibit any decrease in the annuity during the GRAT term. Although a minimum term would not prevent “zeroing-out” the gift tax value of the remainder interest, it would increase the risk that the grantor fails to outlive the GRAT term and the resulting loss of any anticipated transfer tax benefit. This proposal would apply to trusts created after the date of enactment.

81

LIMIT DURATION OF GENERATION-SKIPPING TRANSFER (GST) TAX EXEMPTION Current Law Generation-skipping transfer tax is imposed on gifts and bequests to transferees who are two or more generations younger than the transferor. The GST tax was enacted to prevent the avoidance of estate and gift taxes through the use of a trust that gives successive life interests to multiple generations of beneficiaries. In such a trust, no estate tax would be incurred as beneficiaries died because their respective life interests would die with them and thus would cause no inclusion of the trust assets in the deceased beneficiary’s gross estate. The GST tax is a flat tax on the value of the transfer at the highest estate tax bracket applicable in that year. Each person has a lifetime GST tax exemption ($5,120,000 in 2012) that can be allocated to transfers made, whether directly or in trust, by that person to a grandchild or other “skip person.” The allocation of GST exemption to a transfer or to a trust excludes from the GST tax not only the amount of the transfer or trust assets equal to the amount of GST exemption allocated, but also all appreciation and income on that amount during the existence of the trust. At the time of the enactment of the GST provisions, the law of most (all but about three) states included the common law Rule Against Perpetuities (RAP) or some statutory version of it. The RAP generally requires that every trust terminate no later than 21 years after the death of a person who was alive (a life in being) at the time of the creation of the trust. Reasons for Change Many states now either have repealed or limited the application of their RAP statutes, with the effect that trusts created subject to the law of those jurisdictions may continue in perpetuity. (A trust may be sitused anywhere; a grantor is not limited to the jurisdiction of the grantor’s domicile for this purpose.) As a result, the transfer tax shield provided by the GST exemption effectively has been expanded from trusts funded with $1 million (the exemption at the time of enactment) and a maximum duration limited by the RAP, to trusts funded with $5,120,000 and continuing (and growing) in perpetuity. Proposal This proposal would provide that, on the 90th anniversary of the creation of a trust, the GST exclusion allocated to the trust would terminate. Specifically, this would be achieved by increasing the inclusion ratio of the trust (as defined in section 2642) to one, thereby rendering no part of the trust exempt from GST tax. Because contributions to a trust from a different grantor are deemed to be held in a separate trust under section 2654(b), each such separate trust would be subject to the same 90-year rule, measured from the date of the first contribution by the grantor of that separate trust. The special rule for pour-over trusts under section 2653(b)(2) would continue to apply to pour-over trusts and to trusts created under a decanting authority, and for purposes of this rule, such trusts will be deemed to have the same date of creation as the initial trust, with one exception, as follows. If, prior to the 90th anniversary of the trust, trust property is distributed to a trust for a beneficiary of the initial trust, and the distributee trust is as described in section 2642(c)(2), the

82

inclusion ratio of the distributee trust will not be changed to one (with regard to the distribution from the initial trust) by reason of this rule. This exception is intended to permit an incapacitated beneficiary’s distribution to continue to be held in trust without incurring GST tax on distributions to the beneficiary as long as that trust is to be used for the sole benefit of that beneficiary and any trust balance remaining on the beneficiary’s death will be included in the beneficiary’s gross estate for Federal estate tax purposes. The other rules of section 2653 also would continue to apply, and would be relevant in determining when a taxable distribution or taxable termination occurs after the 90th anniversary of the trust. An express grant of regulatory authority would be included to facilitate the implementation and administration of this provision. This proposal would apply to trusts created after enactment, and to the portion of a pre-existing trust attributable to additions to such a trust made after that date (subject to rules substantially similar to the grandfather rules currently in effect for additions to trusts created prior to the effective date of the GST tax).

83

COORDINATE CERTAIN INCOME AND TRANSFER TAX RULES APPLICABLE TO GRANTOR TRUSTS Current Law A grantor trust is a trust, whether revocable or irrevocable, of which an individual is treated as the owner for income tax purposes. For income tax purposes, a grantor trust is taxed as if the grantor or another person owns the trust assets directly, and the deemed owner and the trust are treated as the same person. Thus, transactions between the trust and the deemed owner are ignored. For transfer tax purposes, however, the trust and the deemed owner are separate persons, and under certain circumstances the trust is not included in the deemed owner’s gross estate for estate tax purposes at the death of the deemed owner. Reasons for Change The lack of coordination between the income and transfer tax rules applicable to a grantor trust creates opportunities to structure transactions between the deemed owner and the trust that can result in the transfer of significant wealth by the deemed owner without transfer tax consequences. Proposal To the extent that the income tax rules treat a grantor of a trust as an owner of the trust, the proposal would (1) include the assets of that trust in the gross estate of that grantor for estate tax purposes, (2) subject to gift tax any distribution from the trust to one or more beneficiaries during the grantor’s life, and (3) subject to gift tax the remaining trust assets at any time during the grantor’s life if the grantor ceases to be treated as an owner of the trust for income tax purposes. In addition, the proposal would apply to any non-grantor who is deemed to be an owner of the trust and who engages in a sale, exchange, or comparable transaction with the trust that would have been subject to capital gains tax if the person had not been a deemed owner of the trust. In such a case, the proposal would subject to transfer tax the portion of the trust attributable to the property received by the trust in that transaction, including all retained income therefrom, appreciation thereon, and reinvestments thereof, net of the amount of the consideration received by the person in that transaction. The proposal would reduce the amount subject to transfer tax by the value of any taxable gift made to the trust by the deemed owner. The transfer tax imposed by this proposal would be payable from the trust. The proposal would not change the treatment of any trust that is already includable in the grantor’s gross estate under existing provisions of the Internal Revenue Code, including without limitation the following: grantor retained income trusts (GRITs); grantor retained annuity trusts (GRATs); personal residence trusts (PRTs); and qualified personal residence trusts (QPRTs). The proposal would be effective with regard to trusts created on or after the date of enactment and with regard to any portion of a pre-enactment trust attributable to a contribution made on or after the date of enactment. Regulatory authority would be granted, including the ability to create transition relief for certain types of automatic, periodic contributions to existing grantor trusts.

84

EXTEND THE LIEN ON ESTATE TAX DEFERRALS PROVIDED UNDER SECTION 6166 OF THE INTERNAL REVENUE CODE Current Law Section 6166 of the Internal Revenue Code allows the deferral of estate tax on certain closely held business interests for up to fourteen years from the (unextended) due date of the estate tax payment (up to fifteen years and three months from date of death). This provision was enacted to reduce the possibility that the payment of the estate tax liability could force the sale or failure of the business. Section 6324(a)(1) imposes a lien on estate assets generally for the ten-year period immediately following the decedent’s death to secure the full payment of the estate tax. Thus, the estate tax lien under section 6324(a)(1) expires approximately five years before the due date of the final payment of the deferred estate tax under section 6166. Reasons for Change In many cases, the IRS has had difficulty collecting the deferred estate tax, often because of business failures during that tax deferral period. The IRS sometimes requires either an additional lien or some form of security, but these security interests generally are prohibitively expensive and damaging to the day-to-day conduct and financing of the business. In addition, unless these other security measures are put in place toward the beginning of the deferral period, there is a risk that other creditors could have a higher priority interest than the Government. Proposal This proposal would extend the estate tax lien under section 6324(a)(1) throughout the section 6166 deferral period. The proposal would be effective for the estates of all decedents dying on or after the effective date, as well as for all estates of decedents dying before the date of enactment as to which the section 6324(a)(1) lien has not expired on the effective date.