Gender and Choosing Sector for Digital Wallet: Is there ...

13

Amity Journal of Commerce and Financial Review Laxmi Rani Gender and Choosing Sector for Digital Wallet: Is there any Association with Education? Laxmi Rani 1 Abstract Digital wallet is a modern payment system-based software system by using any electronic device with internet that permit people to perform electronic transactions. These transactions can be purchasing items on-line with the help of computer, laptop or mobile etc. and making payment for the purchase. This research has been conducted to check whether there is any association between gender and sector for digital wallet with layer of education. Primary data is used by collecting responses from 208 users. The results showed that association between gender and choosing sector for digital wallets was found. Cramer’s V shows strength of association between gender and choosing the sector which shows the association is week. Further research can be done on other factors than gender and education. Keywords: digital wallets, education 1. Introduction Now-a-days e- banking and mobile banking uses are increasing day by day but a new concept of digital wallet has changed the scenario in digital India. Digital wallet is a modern payment system based software system by using any electronic device with internet that permit people to perform electronic transactions. These transactions can be purchasing items on-line with the help of computer, laptop or mobile etc. and making payment for the purchase. A customer bank account can also be linked to the digital wallet with full safety. They might also have their driver’s license, health care, loyalty card(s) and other ID documents stored on the phone. So digital wallets are being used not only for basic financial transactions but also to authenticate and verify the holder's credentials. For example, digital wallet can be used to verify the age of the purchaser to the store while purchasing malt. Digital wallets have 1 Research Scholar, APJ Abdul Kalam University, Madhya Pradesh

Transcript of Gender and Choosing Sector for Digital Wallet: Is there ...

Amity Journal of Commerce and Financial Review Laxmi Rani

Gender and Choosing Sector for Digital Wallet:

Is there any Association with Education?

Laxmi Rani1

Abstract

Digital wallet is a modern payment system-based software system by using any

electronic device with internet that permit people to perform electronic transactions.

These transactions can be purchasing items on-line with the help of computer, laptop

or mobile etc. and making payment for the purchase. This research has been

conducted to check whether there is any association between gender and sector for

digital wallet with layer of education. Primary data is used by collecting responses

from 208 users. The results showed that association between gender and choosing

sector for digital wallets was found. Cramer’s V shows strength of association

between gender and choosing the sector which shows the association is week. Further

research can be done on other factors than gender and education.

Keywords: digital wallets, education

1. Introduction

Now-a-days e- banking and mobile banking uses are increasing day by day but

a new concept of digital wallet has changed the scenario in digital India.

Digital wallet is a modern payment system based software system by using

any electronic device with internet that permit people to perform electronic

transactions. These transactions can be purchasing items on-line with the help

of computer, laptop or mobile etc. and making payment for the purchase. A

customer bank account can also be linked to the digital wallet with full safety.

They might also have their driver’s license, health care, loyalty card(s) and

other ID documents stored on the phone. So digital wallets are being used not

only for basic financial transactions but also to authenticate and verify the

holder's credentials. For example, digital wallet can be used to verify the age

of the purchaser to the store while purchasing malt. Digital wallets have

1 Research Scholar, APJ Abdul Kalam University, Madhya Pradesh

Amity Journal of Commerce and Financial Review Laxmi Rani

become very popular in Japan. Digital wallets are also called "wallet mobiles".

Digital wallet includes both a software and information component. The

software component is responsible for security and encryption of the user’s

personal information and for the actual transaction taking place. Usually,

digital wallets are stored on the client side and can be managed easily by

client. Digital wallets are also compatible with most e-commerce Web sites. A

server-side digital wallet is also known as a thin wallet. Thin wallet is one that

an organization creates for and about you and maintains on its servers. Digital

wallets are becoming very popular among most of the retailers now due to its

security, efficiency, and added utility features. Digital wallets increase the

customer satisfaction of their online purchase experience.

Various digital wallets like Paytm, Mobikwik etc. are available in the market.

These available wallets in the market have changed the payment habits of

people. People prefer payment through digital wallet because these are easy

and convenient to use while making payment. Besides this, digital wallets have

more features in comparison to traditional wallets. To use digital wallets, we

need an electronic device like a computer or smart phone and internet

connection. So digital wallets don’t require so many resources because smart

phone and internet is the necessity now a day and most of the people have

internet and smart phone. So by using digital wallets, payer can pay online to

the payee, payer doesn’t need to go to bank for making payments and payee

doesn’t need to go to the bank for receiving the payment. But this changing

pattern of making and receiving payment has some issues. Some people treat

digital wallets as risky and they think that there can be mismanagement of

fund, fraud may happen, network problem may slow the process or duplication

of transactions may occur. So this system is not risk proof; there may be

technical, infrastructural and service issues. So solutions to different issues

must be considered by the digital wallet companies. Each working and non-

working person have equal opportunity to use digital wallets but if they find

that these are not safe, they will not use digital wallets. Security issues, less

knowledge of computer or other electronic devices, less knowledge about

digital wallets and unavailability of internet in many places are still a major

limitation for major users of digital wallets in India.

Amity Journal of Commerce and Financial Review Laxmi Rani

The paper is organized into four different sections. Section 2 includes detailed

review literature followed by research methodology in section 3. Section 4 and

5 discuss about result and finding and conclusion.

2. Literature Review

Prasad Yadav and Arora (2019) concluded that there is a positive association

between customer satisfaction and solutions in digital wallets and negative

association between customer satisfaction and problems in using digital

wallets.

Arora et al (2019) try to find out the relationship between occupation of people

and instinct in use of digital wallets on customer satisfaction and various

factors that are responsible for various types of risks in use of digital payments

and to recommend measures for minimizing these risks. Findings show a

significant variance in overall satisfaction of digital wallets and various

occupations.

Singh and Arora (2014) conducted a study to know the association between

demographic variables and use of mobile banking in selected public, private

and foreign banks. Significant mean differences were found in solutions in

mobile banking and marital status of respondents. No association was found

between education levels and problems in mobile banking. It is also suggested

that various security measures associated with mobile banking like SMS, PIN,

privacy policies etc. should be communicated to the users to enhance the use

of mobile banking because people are not very much aware about these

security measures. It is also suggested that customers should choose difficult

or secured password that cannot be break.

Education is one of the most crucial activities for any nation (Arora M (2012).

Human Resources are an indispensable but often neglected S Singh, S

Chaudhary, Arora M (2014). Staff in education has found challenge. Private

institutes are in societies but in real Sole proprietorship which means when

there is single ownership in business. S Singh, S Chaudhary, M Arora (2014).

Arora, M. (2019) conducted a study based on multiple comparisons on average

agreement on different variables like customer satisfaction, infrastructure risk,

service quality risk, security risk, boost up of technological risk solutions,

boost up of financial risk solutions and boost up of service quality risk

solutions. The results show that graduates has greater agreement on

Amity Journal of Commerce and Financial Review Laxmi Rani

infrastructure risk Ph.D. respondents, post-graduates has greater agreement on

infrastructure risk than Ph.D. respondents, undergraduates have lower

agreement on boost up of technological risk solutions than graduate

respondents, undergraduate respondents have lower agreement on boost up of

technological risk solutions than post-graduates, graduates have higher

agreement on boost up of technological risk solutions than Ph. D. ,

undergraduates have higher agreement on boost up of technological risk

solutions than graduates.

Arora, M. and Lochab, A. (2018) conducted a study to know the impact of

education on the customer satisfaction while using mobile banking and various

factors responsible for risks associated with mobile banking in the selected

banks and to recommend various suggestions for improving risk solutions.

Research findings conclude there is a significant difference in different level

of education and customer satisfaction associated with mobile banking. It is

also concluded that graduate respondents have greater agreement on

infrastructure risk than post graduate. So mobile banking should be the part of

syllabus of the graduation.

Arora, M., Lochab, A. and Khurana, P. (2019) research findings conclude that

respondents of public sector banks find implementation of security measures

as security risk solution at most than those of private sector banks and foreign

banks. Present research is being conducted to check whether there is any

association between gender and sector for digital wallet with layer of

education

3. Objectives

Objective of this paper is to check the association between gender and

education sector with respect to digital wallet.

4. Research Methodology

Study is exploratory. Primary data is used for data collection from users of

digital wallets. Questionnaire based on five point Likert scale is used.

Secondary data is based on earlier published literature review.

Amity Journal of Commerce and Financial Review Laxmi Rani

Non-parametric Chi-square test is used whether there is relationship between

Gender ad choosing sector for digital wallet. Two categorical variables are

male and female categories in Gender. Private sector wallet users and public

sector wallet users in Sector.

5. Data Analysis

Following contingency table is used to assess whether an association exists between

gender and choice of sector by comparing the observed frequency of responses in the

cells to the expected frequency. Both variables are truly independent to each other.

Table 1: Association between Education and Bank Choice

Education Bank Type Observed / Expected Gender

Male Female Total

Under - Graduate

Public

Observed 17 28 45

Expected 21.38 23.63 45

% within row 37.8 % 62.2 % 100.0 %

% within column 44.7 % 66.7 % 56.3 %

% of total 21.3 % 35.0 % 56.3 %

Private

Observed 17 9 26

Expected 12.35 13.65 26

% within row 65.4 % 34.6 % 100.0 %

% within column 44.7 % 21.4 % 32.5 %

% of total 21.3 % 11.3 % 32.5 %

Foreign

Observed 4 5 9

Expected 4.28 4.72 9

% within row 44.4 % 55.6 % 100.0 %

% within column 10.5 % 11.9 % 11.3 %

% of total 5.0 % 6.3 % 11.3 %

Total

Observed 38 42 80

Expected 38 42 80

% within row 47.5 % 52.5 % 100.0 %

% within column 100.0 % 100.0 % 100.0 %

% of total 47.5 % 52.5 % 100.0 %

Observed 16 18 34

Amity Journal of Commerce and Financial Review Laxmi Rani

Education Bank Type Observed / Expected Gender

Male Female Total

Graduate

Public Expected 18.55 15.45 34

% within row 47.1 % 52.9 % 100.0 %

% within column 53.3 % 72.0 % 61.8 %

% of total 29.1 % 32.7 % 61.8 %

Private

Observed 8 4 12

Expected 6.55 5.45 12

% within row 66.7 % 33.3 % 100.0 %

% within column 26.7 % 16.0 % 21.8 %

% of total 14.5 % 7.3 % 21.8 %

Foreign

Observed 6 3 9

Expected 4.91 4.09 9

% within row 66.7 % 33.3 % 100.0 %

% within column 20.0 % 12.0 % 16.4 %

% of total 10.9 % 5.5 % 16.4 %

Total Observed 30 25 55

Expected 30 25 55

% within row 54.5 % 45.5 % 100.0 %

% within column 100.0 % 100.0 % 100.0 %

% of total 54.5 % 45.5 % 100.0 %

Post-Graduate

Public

Observed 12 11 23

Expected 12.71 10.29 23

% within row 52.2 % 47.8 % 100.0 %

% within column 57.1 % 64.7 % 60.5 %

% of total 31.6 % 28.9 % 60.5 %

Private

Observed 5 3 8

Expected 4.42 3.58 8

% within row 62.5 % 37.5 % 100.0 %

% within column 23.8 % 17.6 % 21.1 %

% of total 13.2 % 7.9 % 21.1 %

Foreign Observed 4 3 7

Expected 3.87 3.13 7

% within row 57.1 % 42.9 % 100.0 %

Amity Journal of Commerce and Financial Review Laxmi Rani

Education Bank Type Observed / Expected Gender

Male Female Total

% within column 19.0 % 17.6 % 18.4 %

% of total 10.5 % 7.9 % 18.4 %

Total

Observed 21 17 38

Expected 21 17 38

% within row 55.3 % 44.7 % 100.0 %

% within column 100.0 % 100.0 % 100.0 %

% of total 55.3 % 44.7 % 100.0 %

Ph.D.

Public

Observed 4 12 16

Expected 7.31 8.69 16

% within row 25.0 % 75.0 % 100.0 %

% within column 25.0 % 63.2 % 45.7 %

% of total 11.4 % 34.3 % 45.7 %

Private

Observed 7 4 11

Expected 5.03 5.97 11

% within row 63.6 % 36.4 % 100.0 %

% within column 43.8 % 21.1 % 31.4 %

% of total 20.0 % 11.4 % 31.4 %

Foreign

Observed 5 3 8

Expected 3.66 4.34 8

% within row 62.5 % 37.5 % 100.0 %

% within column 31.3 % 15.8 % 22.9 %

% of total 14.3 % 8.6 % 22.9 %

Total

Observed 16 19 35

Expected 16 19 35

% within row 45.7 % 54.3 % 100.0 %

% within column 100.0 % 100.0 % 100.0 %

% of total 45.7 % 54.3 % 100.0 %

Public

Observed 49 69 118

Expected 59.57 58.43 118

% within row 41.5 % 58.5 % 100.0 %

% within column 46.7 % 67.0 % 56.7 %

% of total 23.6 % 33.2 % 56.7 %

Amity Journal of Commerce and Financial Review Laxmi Rani

Education Bank Type Observed / Expected Gender

Male Female Total

Total

Private

Observed 37 20 57

Expected 28.77 28.23 57

% within row 64.9 % 35.1 % 100.0 %

% within column 35.2 % 19.4 % 27.4 %

% of total 17.8 % 9.6 % 27.4 %

Foreign

Observed 19 14 33

Expected 16.66 16.34 33

% within row 57.6 % 42.4 % 100.0 %

% within column 18.1 % 13.6 % 15.9 %

% of total 9.1 % 6.7 % 15.9 %

Total

Observed 105 103 208

Expected 105 103 208

% within row 50.5 % 49.5 % 100.0 %

% within column 100.0 % 100.0 % 100.0 %

% of total 50.5 % 49.5 % 100.0 %

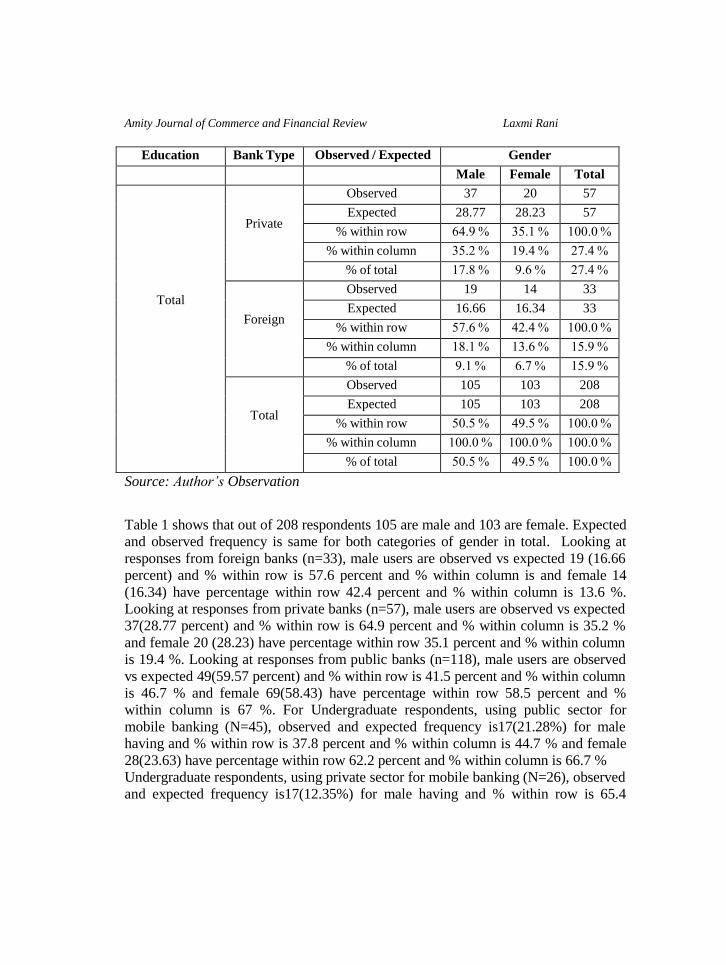

Source: Author’s Observation

Table 1 shows that out of 208 respondents 105 are male and 103 are female. Expected

and observed frequency is same for both categories of gender in total. Looking at

responses from foreign banks (n=33), male users are observed vs expected 19 (16.66

percent) and % within row is 57.6 percent and % within column is and female 14

(16.34) have percentage within row 42.4 percent and % within column is 13.6 %.

Looking at responses from private banks (n=57), male users are observed vs expected

37(28.77 percent) and % within row is 64.9 percent and % within column is 35.2 %

and female 20 (28.23) have percentage within row 35.1 percent and % within column

is 19.4 %. Looking at responses from public banks (n=118), male users are observed

vs expected 49(59.57 percent) and % within row is 41.5 percent and % within column

is 46.7 % and female 69(58.43) have percentage within row 58.5 percent and %

within column is 67 %. For Undergraduate respondents, using public sector for

mobile banking (N=45), observed and expected frequency is17(21.28%) for male

having and % within row is 37.8 percent and % within column is 44.7 % and female

28(23.63) have percentage within row 62.2 percent and % within column is 66.7 %

Undergraduate respondents, using private sector for mobile banking (N=26), observed

and expected frequency is17(12.35%) for male having and % within row is 65.4

Amity Journal of Commerce and Financial Review Laxmi Rani

percent and % within column is 44.7 % and female 9(13.65) have percentage within

row 34.6 percent and % within column is 21.4 %. These crosstabs are further

explained in Table 2 as χ² Tests

Table 2: χ² Tests for Gender and Choosing Bank type with Stage of Education

Education Value Df p- value

Under

Graduate χ² 5.074

2 0.079

χ²

continuity

correction

5.074

2

0.079

Likelihood

ratio 5.13

2 0.077

Fisher's

exact test NaN ᵃ

N 80

Graduate χ² 2.013 2 0.365

χ²

continuity

correction

2.013

2

0.365

Likelihood

ratio 2.041

2 0.36

Fisher's

exact test NaN ᵃ

N 55

Post

Graduate χ² 0.268

2 0.874

χ²

continuity

correction

0.268

2

0.874

Likelihood

ratio 0.27

2 0.874

Fisher's

exact test NaN ᵃ

N 38

Ph. D. χ² 5.098 2 0.078

Amity Journal of Commerce and Financial Review Laxmi Rani

Education Value Df p- value

χ²

continuity

correction

5.098

2

0.078

Likelihood

ratio 5.263

2 0.072

Fisher's

exact test NaN ᵃ

N 35

Total χ² 9.199 2 0.01

χ²

continuity

correction

9.199

2

0.01

Likelihood

ratio 9.296

2 0.01

Fisher's

exact test NaN ᵃ

N 208

ᵃ Available for 2x2 tables only

Source: Author’s Calculation

As per table 2 χ² value for undergraduates is 5.074 at degree of freedom 2, p value

(0.07) is significant at 10 percent level but not at 5 percent. Results can be considered

reliable as χ² continuity correction is also same. Also, χ² value for graduates is 2.013

at degree of freedom 2, p value (0.365) is not significant at 10 percent level as well as

not at 5 percent. Results can be considered reliable as χ² continuity correction is also

same. χ² value for postgraduates is .268 at degree of freedom 2, p-value (.874) is

neither significant at 10 percent level nor at 5 percent. Results can be considered

reliable as χ² continuity correction is also same. But χ² value for Ph.D. is 5.098 at

degree of freedom 2, p value (0.078) is significant at 10 percent level but not at 5

percent. Results can be considered reliable as χ² continuity correction is also same.

Amity Journal of Commerce and Financial Review Laxmi Rani

Table 3: Nominal Cramer's V

Education

Value

Under-

Graduate Phi-coefficient NaN

Cramer's V 0.2518

Graduate Phi-coefficient NaN

Cramer's V 0.1913

Post -

Graduate Phi-coefficient NaN

Cramer's V 0.084

Ph.D. Phi-coefficient NaN

Cramer's V 0.3817

Total Phi-coefficient NaN

Cramer's V 0.2103

Nominal Cramer's V shows the strength of association of Gender and choosing sector

for digital wallet: is any Association with layer of education, for undergraduates it is

0.2518, association exists but is week, for graduates it is 0.1913 but for post graduates

it is only 0.0840 and for Ph.D. it is 0.3817. Overall, for Ph.D. it is highest and for

postgraduates, it is lowest.

6.0 Findings and Conclusion

The table shows that out of 208 respondents 105 are male and 103 are female. So,

number of male and female observations is almost equal. Expected and observed

frequency is same for both categories of gender in total. χ² value for undergraduates is

significant at 10 percent level but not at 5 percent. Results can be considered reliable

as χ² continuity correction is also same. χ² value for graduates is not significant at 10

percent level as well as not at 5 percent. Results can be considered reliable as χ²

continuity correction is also same. χ² value for postgraduates is neither significant at

Amity Journal of Commerce and Financial Review Laxmi Rani

10 percent level nor at 5 percent. Results can be considered reliable as χ² continuity

correction is also same. But χ² value for Ph.D. is significant at 10 percent level but not

at 5 percent. Results can be considered reliable as χ² continuity correction is also

same. Nominal Cramer's V shows the strength of association of Gender and choosing

sector for digital wallet: is any Association with layer of education, for

undergraduates it is 0.2518, association exists but is week for graduates it is 0.1913

but for post graduates it is only 0.0840 and for Ph.D. it is 0.3817. Overall, for Ph.D. it

is highest and for postgraduates, it is lowest.

Mobile banking has become necessity of common man, especially due to covid-19

situation. Present research is being conducted to check whether there is any

association between gender and sector for digital wallet with layer of education. 5

point Likert scale questionnaire based data is used by collecting responses. Chi-square

results showed that association between Gender and choosing sector for digital

wallets was found. Cramer’s V shows strength of association between Gender and

choosing the sector which shows the association is week. Further research can be

done on other factors than gender and education. Limitation of the study is there may

be some other factors which may be significant.

References

Arora et al. (2019), “Influence of Occupation on The Outlook of Digital Wallets”,

Vivekananda Journal of Research, Vol. 8, Issue 2, 131-148.

Arora M (2012), Human Resource Accounting for academics, International Journal of

Advanced Research in Management and Social Sciences,1(3), 209-215

Arora M, Yadav M and Mishra (2019), Random walk hypothesis Evidence from the

top ten stock exchanges using the variance Ratio Test, Advances in Management

Research 1, 178-183

Arora, M. (2019), “Post hoc test of customers' perception towards mobile banking,

Managing strategies and issues in finance: LAMBERT, 239-250.

Arora, M. and Lochab, A. (2018), “A Study on Post Hoc Analysis on Education Level

in Mobile Banking”, Effulgence-A Management Journal, Vol. 16.

Arora, M., Lochab, A. and Khurana, P. (2019), “An empirical research on

reinforcement of mobile banking services”, Bloomsbury, 43-51.

Amity Journal of Commerce and Financial Review Laxmi Rani

13 | P a g e

Volume 3, Issue 2, 2021

Meyer, D., Zeileis, A., Hornik, K., Gerber, F., & Friendly, M. (2017). vcd: Visualizing

Categorical Data. [R package]. Retrieved from https://cran.r- project.org/package=vcd.

Prasad Yadav, Miklesh and Arora, Madhu, Study on Impact on Customer Satisfaction for E-Wallet

Using Path Analysis Model (April 10, 2019). International Journal of Information Systems &

Management Science, Vol. 2, No. 1, 2019, Available at SSRN: https://ssrn.com/abstract=3369651

R Core Team (2018). R: A Language and environment for statistical computing. [Computer

software]. Retrieved from https://cran.r-project.org/.

S Singh, S Chaudhary, Arora M (2014), Business Ethics and Human Resource Accounting,

International Journal of Management and Social Sciences Research, 3(5), 2319-4421

Sultan, S. and Arora M. (2014), “Demographic perception towards mobile banking in

India”, International journal of Management, IT and Engineering, 4(7):251-259. The jamovi project (2019). jamovi. (Version 1.1) [Computer Software]. Retrieved from

https://www.jamovi.org.