Geeves Track Preliminary Business Case · 2.2 The Southwest Tasmanian Wild Tourism ... At present...

81

GEEVES TRACK PRELIMINARY BUSINESS CASE FINAL Prepared for SEPTEMBER 2017 The Geeves Effect

Transcript of Geeves Track Preliminary Business Case · 2.2 The Southwest Tasmanian Wild Tourism ... At present...

GEEVES TRACK PRELIMINARY BUSINESS CASE

FINAL Prepared for

SEPTEMBER 2017 The Geeves Effect

© SGS Economics and Planning Pty Ltd 2017

This report has been prepared for The Geeves Effect. SGS Economics and Planning has taken all due care in the preparation of this report. However, SGS and its associated consultants are not liable to any person or entity for any damage or loss that has occurred, or may occur, in relation to that person or entity taking or not taking action in respect of any representation, statement, opinion or advice referred to herein.

SGS Economics and Planning Pty Ltd ACN 007 437 729 www.sgsep.com.au Offices in Canberra, Hobart, Melbourne, Sydney

Geeves Track Preliminary Business Case i

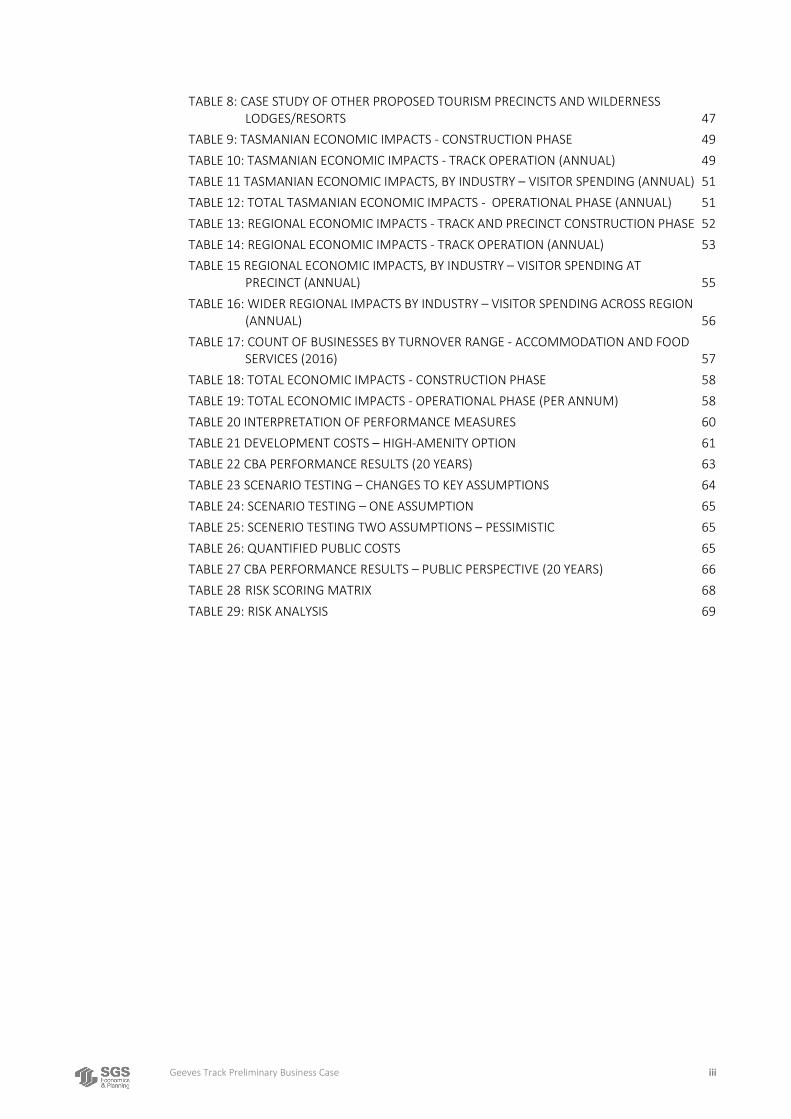

TABLE OF CONTENTS

1. INTRODUCTION 1

1.1 Project Background 1

1.2 The Project 1

1.3 Study Area 2

2. THE PROPOSED TRAIL AND PRECINCT 3

2.1 The Track 3

2.2 The Southwest Tasmanian Wild Tourism Precinct 3

3. INVESTMENT NEED AND POLICY CONTEXT 5

3.1 Socio-economic profile 5

3.2 The current tourism industry 12

3.3 Policy context 19

3.4 Environmental context 21

3.5 Consultation findings 23

3.6 Popularity of other destinations 24

3.7 Summary of investment need 25

4. DEMAND ASSESSMENT 26

4.1 Method for demand study 26

4.2 Case studies 26

4.3 Consultation findings 32

4.4 Visitor analysis 32

4.5 Track demand forecast 34

4.6 Tourism precinct forecast 39

4.7 Summary of demand 42

5. PROPOSAL COSTING 43

5.1 The Geeves Track 43

5.2 Accommodation along track 44

5.3 Operation costs of track and nodes 44

6. ECONOMIC IMPACT ASSESSMENT 46

6.1 Introduction 46

6.2 Economic stimuli (direct impacts) 46

6.3 The Input-Output (I-O) Model 47

6.4 Assessed economic impacts 47

6.5 Distributional analysis – economic stimulus for the Region 52

6.6 Other regional impacts 58

Geeves Track Preliminary Business Case ii

6.7 Limitations of EIA 58

7. COST BENEFIT ANALYSIS 60

7.1 The CBA Analysis 60

7.2 The Geeves Effect CBA 60

7.3 The Geeves Effect CBA – Government (public) cost perspective 65

8. RISK ANALYSIS 67

9. FINDINGS 72

APPENDIX 74

LIST OF FIGURES

FIGURE 1: STUDY AREA 2

FIGURE 2: MEDIAN AGE OF RESIDENTS 5

FIGURE 3: AGE PROFILE OF HUON VALLEY LGA COMPARED TO TASMANIA 6

FIGURE 4: MEDIAN PERSONAL INCOME ($ WEEK) 7

FIGURE 5 IRSD SCORES FOR SOUTHERN TASMANIA BY SA2 8

FIGURE 6: LQ ANALYSIS OF REGION 10

FIGURE 7: CONCENTRATION OF INDUSTRIES (BASED ON EMPLOYMENT) OVER TIME (2001-2011) 11

FIGURE 8: HUON VALLEY UNEMPLOYMENT RATE COMPARED TO NEARBY LGAS (2010-2017) 12

FIGURE 9: GROWTH IN ANNUAL VISITORS TO TASMANIA (2014-17) 13

FIGURE 10: EXISTING ATTRACTIONS IN STUDY AREA (NON-FOOD AND BEVERAGE RELATED) 14

FIGURE 11: EXISTING FOOD AND BEVERAGE ATTRACTIONS 16

FIGURE 12: EXISTING ACCOMMODATION PROVIDERS IN STUDY AREA 17

FIGURE 13: PLACES VISITED BY TOURISTS AND WHETHER THEY PASS THROUGH, STOP OR STAY (2016/17*) 18

FIGURE 14 METHOD FOR DEMAND STUDY 26

FIGURE 15 CHARACTERISTICS AND DEMAND 31

FIGURE 16: LENGTH OF TIME SPENT IN TASMANIA BY SEGMENT 33

FIGURE 17: OVERNIGHT BUSHWALKERS VISITING TASMANIA - HOUSEHOLD INCOME 37

LIST OF TABLES

TABLE 1: ESTIMATED VISITOR NUMBERS TO ATTRACTIONS (APRIL 2016-MARCH 2017) 15

TABLE 2: TASMANIAN VISITOR ANALYSIS (2016/17) 33

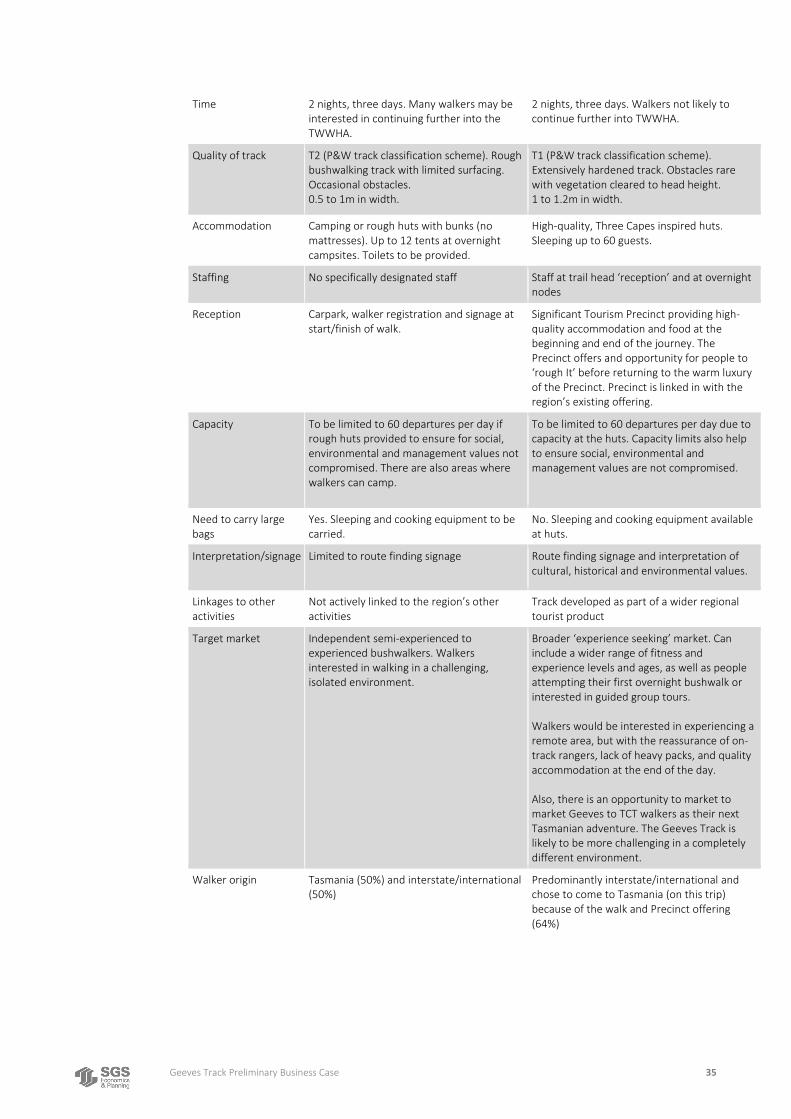

TABLE 3: CONSIDERATION OF TWO BROAD TRACK OPTIONS 34

TABLE 4: SOTH ISLAND NEW ZEALAND OVERNIGHT BUSHWALKS 39

TABLE 5: ESTABLSHMENTS WITH 15 OR MORE ROOMS BY REGION (2016) 40

TABLE 6: DEMAND FOR WILDERNESS LODGES 40

TABLE 7: DEMAND SUMMARY (OPTION 2) 42

Geeves Track Preliminary Business Case iii

TABLE 8: CASE STUDY OF OTHER PROPOSED TOURISM PRECINCTS AND WILDERNESS LODGES/RESORTS 47

TABLE 9: TASMANIAN ECONOMIC IMPACTS - CONSTRUCTION PHASE 49

TABLE 10: TASMANIAN ECONOMIC IMPACTS - TRACK OPERATION (ANNUAL) 49

TABLE 11 TASMANIAN ECONOMIC IMPACTS, BY INDUSTRY – VISITOR SPENDING (ANNUAL) 51

TABLE 12: TOTAL TASMANIAN ECONOMIC IMPACTS - OPERATIONAL PHASE (ANNUAL) 51

TABLE 13: REGIONAL ECONOMIC IMPACTS - TRACK AND PRECINCT CONSTRUCTION PHASE 52

TABLE 14: REGIONAL ECONOMIC IMPACTS - TRACK OPERATION (ANNUAL) 53

TABLE 15 REGIONAL ECONOMIC IMPACTS, BY INDUSTRY – VISITOR SPENDING AT PRECINCT (ANNUAL) 55

TABLE 16: WIDER REGIONAL IMPACTS BY INDUSTRY – VISITOR SPENDING ACROSS REGION (ANNUAL) 56

TABLE 17: COUNT OF BUSINESSES BY TURNOVER RANGE - ACCOMMODATION AND FOOD SERVICES (2016) 57

TABLE 18: TOTAL ECONOMIC IMPACTS - CONSTRUCTION PHASE 58

TABLE 19: TOTAL ECONOMIC IMPACTS - OPERATIONAL PHASE (PER ANNUM) 58

TABLE 20 INTERPRETATION OF PERFORMANCE MEASURES 60

TABLE 21 DEVELOPMENT COSTS – HIGH-AMENITY OPTION 61

TABLE 22 CBA PERFORMANCE RESULTS (20 YEARS) 63

TABLE 23 SCENARIO TESTING – CHANGES TO KEY ASSUMPTIONS 64

TABLE 24: SCENARIO TESTING – ONE ASSUMPTION 65

TABLE 25: SCENERIO TESTING TWO ASSUMPTIONS – PESSIMISTIC 65

TABLE 26: QUANTIFIED PUBLIC COSTS 65

TABLE 27 CBA PERFORMANCE RESULTS – PUBLIC PERSPECTIVE (20 YEARS) 66

TABLE 28 RISK SCORING MATRIX 68

TABLE 29: RISK ANALYSIS 69

Geeves Track Preliminary Business Case 1

1. INTRODUCTION

The Lake Geeves Track and Accommodation Precinct is a proposed project in Tasmania’s South West. This report provides an overview of the project, the key attributes of the local area, an estimate of potential visitation, a high-level cost estimate, and an assessment of its overall the potential benefits the project could deliver.

1.1 Project Background The Geeves Effect have identified the opportunity to upgrade and extend an existing walking track near Lake Geeves in south western Tasmania.

The group have developed a concept and identified a number of opportunities associated with the track including attracting further tourism investment in to the region, and linking together a number of existing tourism attractions in the region. An accommodation and tourism precinct is also proposed, to provide a location for track walkers to stay before and after their walk, and also to attract additional tourism to the region, including overnight and day trip visitors.

The purpose of this project is to develop a ‘proof of concept’ for the project; to identify the high-level costs and potential benefits and to identify if, and how, the project should proceed. It includes refinement of the opportunities and characteristics to be provided by the Project (such as the nature and configuration of accommodation along the track and at the Precinct). The report will provide a preliminary view of the benefits (and costs/risks) of the proposal, and concludes with an indication as to whether further planning and investigations should proceed.

1.2 The Project The project considered in this report comprises an upgraded trail, allowing walkers to access Lake Geeves and Federation Peak. Huts located on the track would provide overnight accommodation as part of the walk. The project also incorporate investment in a range of tourist infrastructure at the trail head– close to the town of Geeveston.

The Track

Lake Geeves is located in the south west of Tasmania, near the town of Geeveston and at the foot of the Federation Peak. Although a number of walking tracks currently provide access to Federation Peak, the Lake (at the base of Federation Peak) is currently inaccessible on foot. In order to provide access to the unique and spectacular landscape views of the Federation Peak and Lake, 17.5km of the existing Eastern Arthur Range Traverse Track requires upgrading, and the environmentally sensitive construction of an additional 2.5km of track would be required (the Track).

The terrain that this ~20km of track covers is particularly rugged, and as such would not be traversable as a day trip. Overnight accommodation along the track is therefore a crucial component of the project.

The upgrading and extension of the track would create a significant tourism drawcard for the region. The track would provide unique vistas and views of Federation Peak, and would enable a broader range of visitors to visit what is currently a difficult area to access.

Geeves Track Preliminary Business Case 2

The new Management Plan for the TWWHA (2016) allows for an increased opportunity for the use of built infrastructure both for management purposes and for commercial tourism operations. In particular, the prohibition on built infrastructure within the Southwest National Park has been lifted. However, for the Geeves Track to be approved a change of zoning along the proposed route will be required.

It is anticipated that the track would also provide access to a range of other, existing tracks including Federation Peak, Moss Ridge; Eastern Arthurs, Western Arthurs and Lake Pedder; The Huon Track; YoYo Track.

To further support the development of the tourism offer in the region, and the accessibility of the Track, an Accommodation and Wilderness Experience Precinct is also proposed.

The Precinct

The Precinct would operate as a ‘launching pad’ for those seeking to use the trail, providing accommodation and access to other nearby outdoor/ adventure activities. The precinct is also envisaged to provide a range of other activities and attractions, including food and beverage offering/s, retail and visitor information.

The precinct would capitalise on growing demand for ecotourism in Tasmania, positioning itself as a premium destination for those seeking an immersive wilderness experience. In developing the precinct there would be a need to be cognisant of the existence of the nearby Tahune Airwalk, and offer experiences and services that complement, rather than compete with, the services offered there.

The precinct would leverage the fact that there is a lack of overnight accommodation and other tourist infrastructure in the region to the south of Hobart, in spite of the region’s popularity among daytrippers.

1.3 Study Area The proposed Track and Precinct are located in the Huon Valley LGA. This is the ‘study area’ or the ‘region’ and is the area that will capture flow on demand to other attractions and businesses, the economic impact, and wider social benefits that will flow. It is shown in Figure 1.

FIGURE 1: STUDY AREA

Geeves Track Preliminary Business Case 3

2. THE PROPOSED TRAIL AND PRECINCT

The ‘Project’ comprises the Track (including Track accommodation) and Tourist Precinct. This section provides additional detail regarding the proposed Project and its context.

2.1 The Track Lake Geeves is located 670m below the iconic destination of Federation Peak in the wilderness of the Eastern Arthurs Ranges. Views of Federation Peak are possible from the Lake.

At present there is a rough, overgrown track into the area, with the last 2.5 km into Lake Geeves not passable. The proposal is to provide a year-round walking track from Farmhouse Creek to Lake Geeves. This involves the upgrading 17.5 km of the existing Eastern Arthur Range Traverse Track and the environmentally sensitive construction of an additional 2.5km of track to reach Lake Geeves. The track is in the Tasmanian Wilderness World Heritage Area (TWWHA).

Accommodation along the Track is also required, given the time required to traverse the track. Two accommodation locations are proposed at different locations along the track; it is assumed that walkers would walk to the first accommodation on Day 1, and stay there overnight. On Day 2, walkers would visit the Lake to view the Peak, before returning to the second accommodation pod. On Day 3, walkers would return to the beginning of the track. The location of the accommodation pods would be planned to enable a second attempt at walking to view the Peak, should weather conditions on Day 1 not provide a view of the Peak.

2.2 The Southwest Tasmanian Wild Tourism Precinct A Tourism Precinct incorporating a range of functions is also proposed. It could include:

Accommodation, including a large scale eco-facility which could accommodate at least a tour bus sized group of people, providing pre or post walk accommodation for walkers and operating as a Track welcome and reception

A visitor information centre providing information, promotion of the region’s tourism offering, and context and history of the region.

Retail and food/ beverage outlets, particularly linked to local produce and goods launching place for other wilderness activities (e.g. bike riding, rafting, wildlife tours) Access to nearby short walks Gallery or other arts component

The private sector would be provided with opportunities to identify the specific activities and design the layout of the precinct, consistent with the concept of an ‘Immersive wilderness experience’.

It is anticipated the Precinct designed in this way would be an attraction its own right, generating demand for overnight and day visits, distinct from the Track. To enable this, the layout, structure and activities within the precinct would require further consideration and design. The development of an ‘eco/ wilderness’ destination is anticipated to have the potential to attract a much wider audience to the area and region.

Geeves Track Preliminary Business Case 4

A location has been identified nearby the head of the proposed Track, but outside of the Tasmanian Wilderness World Heritage Area (TWWHA), for the tourism precinct.

Geeves Track Preliminary Business Case 5

3. INVESTMENT NEED AND POLICY CONTEXT

This chapter provides a socio-economic analysis of Region, an overview of the consultation undertaken with relevant stakeholders; and a review of relevant policy documents, to establish the project context in more detail.

3.1 Socio-economic profile A socio-economic profile of the Region has been collated to understand the context of the Project.

Population and income

The population of the Region has grown steadily over the past decade (2006 to 2016) – rising from 14,000 to around 16,200. This represents an increase of 2,200 residents equating to an average annual growth rate (AAGR) of 1.5%. This AAGR is significantly higher than the state average over the same period. While population growth is a component of a region’s economic vitality, other population factors including age profile are also important.

Error! Reference source not found. shows the change in median age of the Region, with the neighbouring Kingborough and Hobart, and Tasmania as a whole included for comparison. The figure shows that while the population of the state as a whole is ageing, though the median age of the population of the Huon Valley has grown even more rapidly. Driven by the popularity of the region as a location for retirement-age residents, the median age across the region has grown from 39 to 45 in only ten years.

FIGURE 2: MEDIAN AGE OF RESIDENTS

Source: ABS Census of Population and Housing

25

30

35

40

45

2006 2011 2016

HUON VALLEY LGA HOBART LGA KINGBOROUGH LGA TASMANIA

Geeves Track Preliminary Business Case 6

Figure 3 also considers this aging demographic. It shows that compared to Tasmania as a whole, the proportion of people aged 15-39 in the Huon Valley is lower than for the state as a whole. Conversely the portion of the population aged 45-74 in the Huon Valley is higher than for the state of Tasmania. This reflects the fact that young people tend leave the region in their late teens and early twenties in search of employment and education opportunities. It also further confirms the popularity of the region among retirement age cohorts. The lack of working age residents represents a substantial risk to the regional economy. As such, creation of sustainable employment opportunities for young people in the region should be treated as a priority.

FIGURE 3: AGE PROFILE OF HUON VALLEY LGA COMPARED TO TASMANIA

Source: ABS Census of Population and Housing

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0-4

5-9

10

-14

15

-19

20

-24

25

-29

30

-34

35

-39

40

-44

45

-49

50

-54

55

-59

60

-64

65

-69

70

-74

75

-79

80

-84

85

yea

rs +

SHA

RE

OF

PO

PU

LATI

ON

IN A

GE

RA

NG

E

AGE RANGE

Huon Valley LGA Tasmania

Geeves Track Preliminary Business Case 7

The median total personal income in the Region has also grown, though at a substantially lower rate than the rest of Tasmania. The table shows nominal incomes increased by 42 per cent over ten years. Adjusting for inflation1, the real increase in median income was substantially less (17 per cent). Low incomes in comparison to the rest of Tasmania reflect a relative lack of skilled service sector jobs in the region, and relatedly, a relatively low number of skilled, highly-educated local workers.

The ABS Index of Relative Socio-economic Disadvantage (IRSD) provides a measure of the economic and social status of regional populations. The index produces a score that facilitates comparisons between areas at a given time, incorporating a range of variables such as educational attainment, employment status and income.

Figure 5 shows the spatial element of disadvantage across south eastern Tasmania, with the study area comprised of the Huonville-Franklin, Cygnet, and Geeveston-Dover SA2s. The most heavily disadvantaged regions have a score of 1, indicating that they are in the lowest decile for SEIFA (i.e. they are among the 10 per cent of Australia’s most disadvantaged SA2s). The most disadvantaged regions are situated to the north of Hobart and in parts of the Eastern Shore, with most of the Hobart metropolitan area shown to experience relatively little disadvantage.

The Geeveston-Dover area receives a low score (3) indicating that it is among the 30 per cent of most disadvantaged SA2s in Australia. The limited number of jobs available within a short travel time amplifies this disadvantage.

1 Using the ABS CPI for Hobart

200

300

400

500

600

700

800

2006 2011 2016

INC

OM

E P

ER W

EEK

($

)

HUON VALLEY LGA HOBART LGA KINGBOROUGH LGA TASMANIA

FIGURE 4: MEDIAN PERSONAL INCOME ($ WEEK)

Geeves Track Preliminary Business Case 8

FIGURE 5 IRSD SCORES FOR SOUTHERN TASMANIA BY SA2

Source: ABS Census of Population and Housing: Socio-Economic Indexes for Areas (SEIFA), Australia, 2011 *A score of 1 is an area that is considered the most disadvantaged, in comparison to the rest of Tasmania. *A score of 10 is an area with little disadvantage compared to the rest of Tasmania

Industry and employment

This section considers the performance of a range of industries across the region.

Location quotient analysis (LQ)

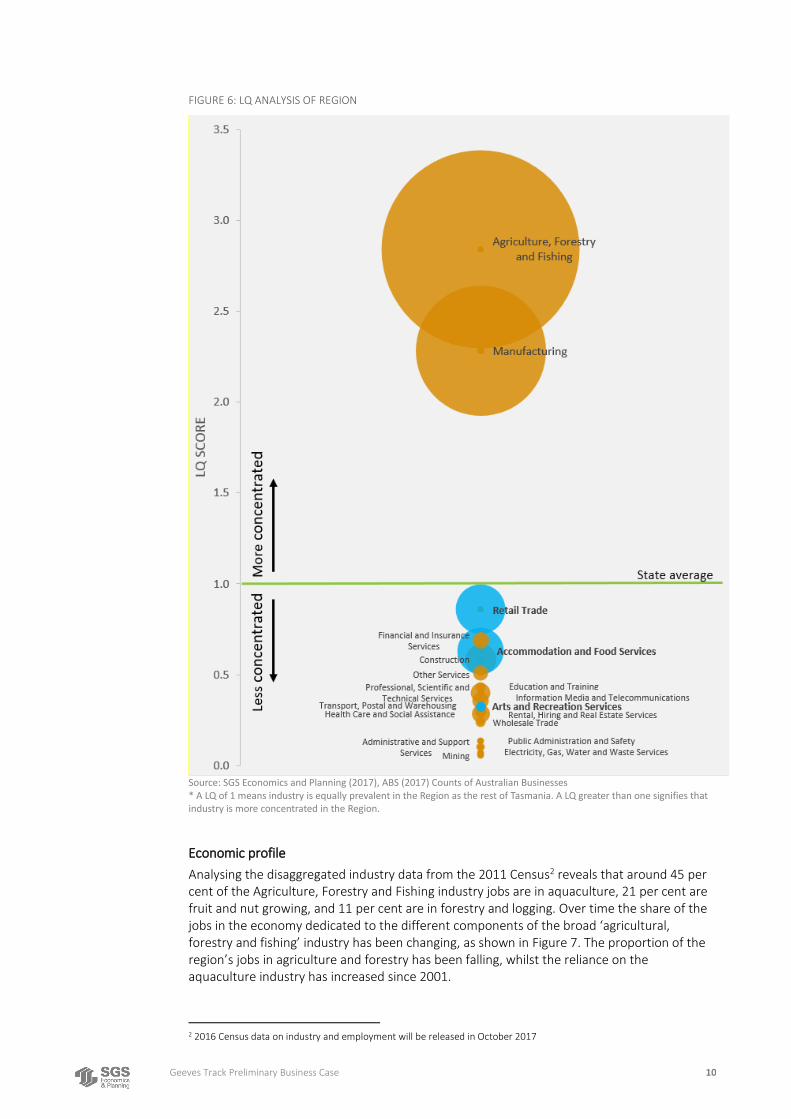

A location quotient (LQ) analysis is a valuable tool for quantifying how concentrated a particular industry group is in a region as compared to a broader region (e.g. a state or a nation). It can reveal what makes a particular region ’unique’ in comparison to the broader regional average.

Geeves Track Preliminary Business Case 9

Regions, due to their physical, technological and intellectual characteristics, can have cost, productivity and other strategic advantages relative to other economies. Comparative strategic advantages are widely considered to be one of the origins of international trade, and in an increasingly global economy they can be considered the key drivers of regional economic growth. The theory of comparative advantage can be applied at the national, state, regional and local level.

Comparative strategic advantages result in high levels of employment in industries that benefit from these advantages, and this is revealed through the LQ analysis. When the LQ value is greater than one it is an indication that a region is fairly specialised and has a competitive advantage in that field of industry over other regions. Generally speaking, a region is a net exporter if the location quotient is high (that is >1), and a net importer if the location quotient is low (that is <1).

An LQ analysis of the Region reveals that there are two industries that have a higher concentration in the Huon valley than in Tasmania as a whole, as shown in Figure 6. These industries are agriculture, forestry & fishing (LQ of 2.8) and manufacturing (LQ of 2.3). An LQ greater than one signifies that industry type is more concentrated than it is across Tasmania, and the higher the LQ the more concentrated that industry is. In Figure 6 the size of the circles represent the number of people employed in that industry.

The economy of the Region is dominated by agriculture, forestry and fishing, and manufacturing. It is also evident that industries related to tourism; accommodation & food services, retail trade, and arts & recreation (the blue circles) are underrepresented in the Region in comparison to the rest of the State.

Geeves Track Preliminary Business Case 10

FIGURE 6: LQ ANALYSIS OF REGION

Source: SGS Economics and Planning (2017), ABS (2017) Counts of Australian Businesses * A LQ of 1 means industry is equally prevalent in the Region as the rest of Tasmania. A LQ greater than one signifies that industry is more concentrated in the Region.

Economic profile

Analysing the disaggregated industry data from the 2011 Census2 reveals that around 45 per cent of the Agriculture, Forestry and Fishing industry jobs are in aquaculture, 21 per cent are fruit and nut growing, and 11 per cent are in forestry and logging. Over time the share of the jobs in the economy dedicated to the different components of the broad ‘agricultural, forestry and fishing’ industry has been changing, as shown in Figure 7. The proportion of the region’s jobs in agriculture and forestry has been falling, whilst the reliance on the aquaculture industry has increased since 2001.

2 2016 Census data on industry and employment will be released in October 2017

Geeves Track Preliminary Business Case 11

This reflects the region’s current reliance on aquaculture (the salmon industry specifically). While this industry has grown significantly recently, and it makes a significant contribution to the local economy, the reliance on a single sector can limit a regions resilience and capacity to respond to future economic or environmental changes.

FIGURE 7: CONCENTRATION OF INDUSTRIES (BASED ON EMPLOYMENT) OVER TIME (2001-2011)

In terms of manufacturing, 25 per cent of the manufacturing industry in the Region is related to wood products, and 19 per cent is related to food products (largely seafood processing and bakery products). The manufacturing sector is strongly related to the agricultural, forestry and aquaculture industries in the region and together comprise the main economic drivers of the region.

While the Tasmanian forestry industry retains a role in the local economy, it has been through a process of major structural transformation brought about by changing markets and the influence of changes in government policy. This resulted in significant reductions in employment and economic opportunities, and eroded regional communities’ confidence in their future3. The effects of this are still felt in many communities in Tasmania, including the Huon Valley. From 2008, the downturn in industry activity resulted in large job losses. Between 2008 and 2011, employment in forest industry jobs declined by around 50%, or 3,500 jobs across Tasmania; 139 of these jobs were lost in the Huon Valley4.

The further development of the tourism industry presents an opportunity to diversify the region’s economy. This would limit the impact of economic downturns in key industries and an important step in securing the ongoing sustainability and vitality of regional communities.

3 West et al (2012). Diversifying Tasmania’s Economy: Analysis and Options. Australian Innovation Research Centre 4 Jacki Schirmer, Caroline Dunn, Edwina Loxton (2014). Socio-economic impacts of forest industry change - Tasmanian forest industry employment and production, 2012-13

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Agriculture Forestry and Logging Aquaculture

2001 2011

Geeves Track Preliminary Business Case 12

Unemployment

The Region has been experiencing high rates of unemployment in recent years, with unemployment relatively high (see Figure 8). This chronic shortage of jobs presents a major challenge for the Region, with a need to create economic activity (and employment) to support and enhance the quality of life of residents.

FIGURE 8: HUON VALLEY UNEMPLOYMENT RATE COMPARED TO NEARBY LGAS (2010-2017)

Source: SGS Economics and Planning (2017), Australian Department of Employment (2017) Small Area Labour Markets — March quarter 2017

3.2 The current tourism industry

State level tourism trends

Tourism is an important contributor to the sustainable development of regional areas around Australia. It is often advocated as a means to diversify economic conditions in rural and regional areas by providing alternative sources of employment and income generation in times of downturn in traditional industries such as agriculture and forestry.5

Tasmania has a well-established and recognised ‘tourism brand’ and the Australian Innovation Research Centre (AIRC) recently prepared a report for the Commonwealth Department of Infrastructure and Regional Development that identified six main areas of opportunity for Tasmania, including tourism generally, and more specifically ‘experiential’ tourism, i.e. tourism related to the island’s wilderness and consumption of gourmet products.

The Saffire resort, the Museum of Old and New Art and the development of new trails including a new iconic wilderness walk on the Tasman Peninsula, lend weight to the sector’s growth prospects.6

This is reflected in the growth of visitor nights in the State, which have increased by 19% between March 2014 and March 2017. While this growth in tourism was initially centred on Hobart, visitor numbers are now growing in regions across the State. Visitation has been

5 Carmen Cox & Meredith Wray (2011) Best Practice Marketing for Regional Tourism Destinations, Journal of Travel & Tourism Marketing, 28:5, 524-540 6 RDA Tasmania Regional Plan (2015)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

HUON VALLEY LGA HOBART LGA KINGBOROUGH LGA

Geeves Track Preliminary Business Case 13

growing at six per cent in the South, 11 per cent on the East Coast, four per cent in the North and five per cent on the Cradle Coast7.

Figure 9 shows the overall growth in visitor numbers, as well as specific segments which are growing, which includes:

Outdoor and other activities Bushwalking Visiting national parks Overnight bushwalking

FIGURE 9: GROWTH IN ANNUAL VISITORS TO TASMANIA (2014-17)

The rapidly increasing number of overnight bushwalkers visiting the State since 2015 has been credited to being mostly due to the establishment of the Three Capes Track8.

The following sections provide an overview of the current tourism offer in the region.

Existing Regional attractions

The existing attractions in the Region are identified in Figure 10. It indicates that there are a number of tourism attractions in the region, including adventure based outdoor activities, galleries, museums, and sites of interest.

7 Tasmanian Government – Jobs and Economic Plan 2016 Update 8 Gramenz, E. (2017). Three Capes Track helping drive Tasmania’a record tourist numbers. ABC News, Sun 19 March 2017

Bushwalk overnight or longer (AAGR = 28%)

Visit National Parks (AAGR = 12%)

Outdoor and other activities (AAGR = 9%)

Bushwalk - not overnight (AAGR = 10%)

Total visitors (AAGR = 6'%)

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Mar-14 Mar-15 Mar-16 Mar-17

Nu

mb

er o

fan

nu

al v

isit

ors

Geeves Track Preliminary Business Case 14

FIGURE 10: EXISTING ATTRACTIONS IN STUDY AREA (NON-FOOD AND BEVERAGE RELATED)

Source: SGS Economics and Planning (2017), Tasmanian Government (2015) LIST Points of Interest dataset.

The region is home to a number of relatively well-known bushwalking trails; these include those in the Hartz Mountain National Park, Adamson’s Peak and the South Coast Track. The South Coast Track is designated as one of Tasmania’s ‘Great Bushwalks’9 and consists of a challenging 85 kilometres of remote wilderness walk, typically popular among experienced bushwalkers. The track is currently undergoing a $2 million upgrade to ensure it remains a quality walking experience capable of delivering ongoing economic benefits to the broader region10. The South Coast Track attracts about 1,200 to 1,300 walkers per year.

Other tracks include Lake Espereance Track; Lake Osbourne Track; Huon Track; Big Tree Walk; Mt Picton; Tahune short walks. Many of these tracks are in poor condition and consequently are not utilised by many walkers.

Table 1 provides an overview of visitation levels at major regional and Tasmanian tourist attractors. It indicates that whilst there are a number of attractions which support visitation to the region, including several significant attractions (the Tahune Airwalk and Hastings Caves)

9 Tasmanian Parks and Wildlife Service 10 State Government Media Release (2016). Upgrading the South Coast Track

Geeves Track Preliminary Business Case 15

the level of visitation they generate is considerably lower than other well-known, iconic attractions in other parts of Tasmania.

TABLE 1: ESTIMATED VISITOR NUMBERS TO ATTRACTIONS (APRIL 2016-MARCH 2017)

Major Huon Region Attractions Estimated visitors AAGR (2014-2017)

Tahune Forest Airwalk 71,385 2.8%

Hastings Caves/Thermal Springs 34,962 14.0%

Signature Tasmanian Attractions

Salamanca Market 427,334 5.6%

MONA - Museum of Old and New Art 341,578 4.9%

Mount Wellington 321,654 10.3%

Port Arthur Historic Site 275,253 8.3%

Freycinet National Park 249,960 12.1%

Cradle Mountain 236,842 12.1%

Cataract Gorge 225,992 1.6%

Source: Toursim Tasmania (2017). Tourism Visitor Survey

*AAGR = Average Annual Growth Rate

Table 1 also reveals that nature based attractions have experienced strong growth over the past three years (Cradle Mountain and the Freycinet National Park in particular). This may be indicative of a broader shift in preferences among tourists for nature-based holiday experiences.

Existing food and beverage attractions

Figure 11 shows the existing food and beverage attractions in the Region. The quality of the hospitality offer in a region is crucial in attracting visitation in particular segments; the availability of ‘local’ produce and a range of hospitality choices is particularly beneficial and can complement the development of the track and precinct.

Geeves Track Preliminary Business Case 16

FIGURE 11: EXISTING FOOD AND BEVERAGE ATTRACTIONS

Source: SGS Economics and Planning (2017), Tasmanian Government (2015) LIST Points of Interest dataset.

The existing supply and distribution of food and beverage attractions in the region reflects the local agricultural sector, which includes ciders, cherries, apples and wine. The availability of local produce is an important consideration for the tourism context.

Existing accommodation supply

Figure 12 provides an overview and location of existing accommodation in the region. Most of this accommodation comprises small holiday units or guest houses.

Geeves Track Preliminary Business Case 17

FIGURE 12: EXISTING ACCOMMODATION PROVIDERS IN STUDY AREA

Source: Source: SGS Economics and Planning (2017), Tasmanian Government (2015) LIST Points of Interest dataset.

Although the map suggests that the supply of accommodation across the region is relatively widespread, in terms of overall accommodation capacity, options are relatively limited with the majority of facilities being holiday units/houses or bed and breakfasts alongside a few small hotels and camping grounds. A further 152 options are listed on AirBnB.

The capacity of the region to accommodate large groups (e.g. those arriving in a tour bus) in a single location is limited. This is likely to mean that fewer tourists stay overnight in the region than would otherwise be the case. This is reflected in visitor data (as shown in Figure 13) which reveals that for the four prominent towns in the Region (Dover, Geeveston, Cygnet and Huonville) nearly 50 per cent of visitors on average across the four simply pass through without stopping. In terms of attracting tourists to stay overnight, only 10 per cent of tourists to Geeveston stay overnight, rising to 19 per cent at Dover.

Coles Bay and Cradle Mountain have been included in the chart for context11; these locations are significant nature based tourist attractions and experience a much higher percentage of

11 There are a range of factors which could influence the proportion of visitors who stay overnight compared to passing through or just stopping; this includes distance from a major city and whether the town is located at the end of a route. Both Cradle Mountain and Coles Bay are further away from a major city than the towns in the region, and are located at

Geeves Track Preliminary Business Case 18

overnight visitors and tourists who stop, in comparison to the four towns in the study Region. This is likely a result of their relative distance from major population centres making them relatively unattractive as day trip destinations.

FIGURE 13: PLACES VISITED BY TOURISTS AND WHETHER THEY PASS THROUGH, STOP OR STAY (2016/17*)

Source: Tourism Tasmania (2017) Tasmanian Visitor survey

*Data for Geeveston from 2013/14

Summary and implications

The current tourism industry in the region comprises a range of attractions, accommodation, and food and beverage facilities. The TWWHA is a major asset, and there is a significant range of gourmet food and beverage suppliers. There are several small-scale attractors in the regions, such as the Tahune Airwalk, Hartz Mountain and Hastings Cave.

the end of a road instead of being part of a ‘route’. These factors are likely to increase the propensity of tourists to stay the night – however the difference is still stark.

Geeves Track Preliminary Business Case 19

There is however, no major flagship attraction or large-scale accommodation and the LQ analysis in Figure 6, indicates that the tourism industry is less prominent in the Region than across Tasmania as a whole, with the three sectors most closely associated with tourism (i.e. accommodation & food services, retail trade, and arts & recreation services) having an LQ below one.

Analysis of major nature based attractions elsewhere in Tasmania indicates they are experiencing growth, suggesting there is significant demand for such activities in the State.

3.3 Policy context

Tasmanian State Government – EOI Program

The Tasmanian Government is undertaking an expressions of interest (EOI) program for tourism investment opportunities in the TWWHA, National Parks and Reserves, to unlock the natural areas to new tourism experiences. The EOI process provides opportunities within Tasmania’s natural areas for new tourism experiences that also contribute to the conservation of the natural environment. The Tasmanian Government’s EOI Process invites investors with ideas for tourism ideas to pitch them to the Government. The Government is looking for developments that broaden the range of experiences on offer, improve access for tourists, complemented by sensitive and appropriate tourism infrastructure, while maintaining the integrity of natural and cultural heritage.

The EOI process demonstrates the State Government’s support for appropriate tourism developments in the TWWHA. The Tasmanian Government recognises the importance of managing the TWWHA in a way that is genuinely respectful of its natural and cultural heritage values. It also recognises that “the TWWHA is an area to be experienced, celebrated and shared with the world. The Tasmanian Government is supportive of sensitive and appropriate use of the TWWHA for recreational and tourism purposes and acknowledges the important role tourism plays in contributing to the economic wellbeing of the Tasmanian community12”.

Tasmanian State Government – Jobs and Economic Plan (2016 update)

Economic growth and job creation are the Hodgman Liberal Government’s ‘greatest priorities’. The Government wishes to support Tasmania’s competitive strengths to drive Tasmania’s economy and build confidence. The current Hodgman State Government has a target of reducing Tasmania’s unemployment rate to at least the national average.

Tourism 21

Tourism is supported by many institutions including Tourism Tasmania, the Department of State Growth, Tourism Industry Council Tasmania, four Regional Tourism Organisations, the 29 Local Government Areas, many Local Tourism Associations and the Tasmania Visitor Information Network.

Their collective strategy is Tourism 21 which aims to bring 1.5 million visitors per annum to Tasmania by 2020. A priority for the strategy is to:

“Invest in quality visitor infrastructure Investment in private and public infrastructure is the backbone for growing the visitor economy. For Tasmania to achieve 1.5 million visitors a year by 2020 requires the ongoing development of exciting new visitor experiences to drive interest in Tasmania, stimulate visitor demand and encourage travel within the state.”

Tasmanian Visitor Engagement Strategy

The Tasmanian Visitor Engagement Strategy is a key action of T21 and sets out the guiding principles, elements and actions that the State Government will undertake with industry to rethink and strengthen the State’s approach to visitor engagement.

12 TWWHA Management Plan – Minister’s Forward

Geeves Track Preliminary Business Case 20

The following principles were developed to guide the future of visitor engagement in Tasmania:

Provide a landscape where visitors engage in meaningful experiences rather than skimming the surface of the destination.

Encourage greater interaction between locals and visitors. Help visitors connect with the rich stories that set Tasmania apart. Inspire visitors to create and share unique itineraries that meet their special interests and

get off the beaten track. Let the landscape, culture and people of Tasmania lead the story through seamless and,

where possible unobtrusive visitor engagement.

Destination Management Plan – Destination Southern Tasmania (2014)

With record levels of visitation to Hobart, the key priorities for Destination Southern Tasmania are to provide a better experience to extend the length of stay and yield, (or encourage frequent, repeat visits), and to achieve wider regional dispersal - as opposed to attracting significantly increased visitor numbers.

The Management Plan argues that successful regional dispersal has only occurred with the bundling of attractive, market-led experiences and accommodation – the success of Bruny Island being a key example. Accommodation occupancy rates in Southern Tasmania currently sit at more than 85%, however this figure is largely driven by the exceptionally high occupancies in central Hobart. Beyond this core tourism precinct, many accommodation operators are struggling with occupancies closer to 35-40% in regional areas.

“Despite the optimism around the latest visitor data, the reality remains that regional Tasmania is not experiencing a corresponding growth. This is a key factor in considering Hobart vis-à-vis the broader Southern region. The current situation reflects a ‘two-speed’ visitor economy.”

Further, the DMP argues that product development and investment is paramount is the Southern Region. This is necessary to capitalise on the record visitor numbers to the immediate Hobart area, and to encourage regional dispersal. This investment should cover both the development of new and existing products and infrastructure. These investments, such as the development of accommodation in ‘wilderness’ areas, revamped visitor centres, food and beverage tours, tasting centres and improved tourism signage, to name a few will have cross-over impacts and meet a range of objectives; well-focused investments leverage further opportunities.

Reimagining the Visitor Experience of Tasmania’s Wilderness World Heritage Area: Ecotourism Investment Profile

The Reimagining project aims to establish a new vision for growing and enhancing visitor experiences to the TWWHA. This Ecotourism Investment Profile aims to guide and facilitate growth in ecotourism through a strategic approach, following consultation with key stakeholders, investors, industry, and regional tourism stakeholders.

A broad vision for tourism in the Tasmanian Wilderness World Heritage Area was identified. The vision decided upon was “To deliver the most contemporary wilderness World Heritage Area experience offering shared, life changing, moments.” It was argued that the focus for the future of the TWWHA is on growing the value of the place at a low volume, and aims at attracting visitors who are willing to pay for high value experiences.

Analysis in the Investment Profile found that while the importance of the World Heritage Area is without question, its pulling power for domestic and international visitors has waned, and that while the wilderness is seen as a core attraction, the TWWHA region has not seen the levels of innovation, or created the new attractions or experiences needed to maintain a competitive advantage over the last decade.

Geeves Track Preliminary Business Case 21

A consideration of relevant tourism trends found that increasingly, the trends in wilderness tourism are towards both adventure and comfort, resulting in booms elsewhere of investment in the following:

‘Glamping’ and luxury tents in spectacular locations Reuse of industrial and heritage sites for modern luxury Ziplines, via ferrata, high ropes/flying fox and tubing Overnight mountain-biking, hiking and skiing trails Heli-touring, jet boating and other rapid transport

In terms of accommodation opportunities, it was argued that there is significant opportunity for more, new, low-impact, environmentally sensitive wilderness accommodation to be developed inside and around the edges of the TWWHA, in order to deliver more immersive World Heritage wilderness experiences for visitors – and provide greater accommodation capacity for visitors to the TWWHA. New and innovative commercial, wilderness accommodation in and around the TWWHA – with associated food and wine experiences, guided tours and more – would provide greater opportunities for visitors to experience, learn about, and become advocates for unique wilderness destinations, which they may otherwise have not been able to visit. Investment in small-scale wilderness accommodation will make the TWWHA more attractive for new, higher-yield markets; in response the Investment Profile identifies identifying suitable precincts for eco-lodge accommodation developments as a priority project.

In terms of new trails in the TWWHA the Investment Profile reads that whilst there continues to be high demand for the Overland Track, international and national trends suggest that there is a growing demand for shorter walks, including one and two night soft adventure experiences. In response it was recommended that there is an opportunity to develop an additional ‘iconic’ walk in the TWWHA at Cradle Mountain – a two day-one night commercial, guided walking experience.

3.4 Environmental context The proposed hut-based Geeves Track is in the Tasmania Wilderness World Heritage Area, meaning that the area has very-high natural values to drive demand, but also that special approvals are required to develop in the TWWHA, including a change to the zoning under the Management Plan.

The TWWHA Management Plan

The Management Plan sets out what uses may occur within the TWWHA, where they may occur and under what circumstances.

A range of proclamations are made in the Management Plan which are relevant to the Geeves Track component of the Geeves Effect. In regard to:

Tourism in the TWWHA - “There is considerable demand for commercial adventure tourism, immersive experiences and a variety of accommodation; from the rustic lodgings of Mount Field’s Government Huts, to the luxury standard at Pumphouse Point at Lake St Clair. Activities include wildlife viewing, walking, camping, rafting, climbing, canyoning and yachting.”

Scope for development - “There is considerable scope to increase the contribution the TWWHA make to Tasmania (social and economic) while “continuing to protect the TWWHA’s natural and cultural values, particularly through the fostering of greater private investment as an accepted component of future management.”

Development of infrastructure - “creation of appropriate commercial opportunities and provision of opportunities for self-reliant recreation must all be prioritised where visitor demand is highest or there are gaps in presentation opportunities.”

Geeves Track Preliminary Business Case 22

Presentation is a key requirement of the World Heritage Convention. Management of presentation covers all aspects of the visitor experience, including information, interpretation, recreation opportunities, management presence and facilities

Regional economies - “will benefit from strategies that boost visitation in the TWWHA. It is vital that presentation of the area evolves to ensure that it continues to play an important role in the overall tourism sector in Tasmania, and for Tasmanians and visitors alike to continue to experience the values of the TWWHA”

Access - is a “fundamental aspect of the visitor experience. However, it requires careful management practices that are consistent with the protection of the TWWHA’s natural and cultural values.”

Use and potential development in the TWWHA are primarily regulated and controlled through a system of four Management Zones. The Management Zones (Visitor Services, Recreation, Self-Reliant Recreation and Wilderness) reflect the spectrum of current and anticipated use and their associated levels of infrastructure.

The Management Plan does allow for new track developments in the TWWHA, but for the Geeves Track the trail to Federation Peak will need to be rezoned from Self-Reliant Recreation Zone to Recreation zone (the same as the overland track) and the new section from the Federation Peak Track into Geeves Lake will need to be rezoned from Wilderness to Recreation. The current zones that overlay the Track do not allow for significant Tracks or new tracks.

Community access to natural heritage

The TWWHA Management Plan explicitly acknowledges the importance of the TWWHA to local communities and the connections that many people have with it. Community involvement in its management is a key objective and the plan also recognises that the TWWHA should play an important role in the social and economic life of local communities.

Allowing greater access to world heritage wilderness for people does not need to compromise the value of the area. Other regions in the world are successfully managing their world heritage assets whilst still allowing locals and tourists to experience and connect with the heritage on offer.

For example, Iceland has seen a rapid increase in visitation built of the countries natural heritage. The Þingvellir National Park is located in the southwest region of Iceland, and was designated a World Heritage site in 2004.

The Management Plan for the Park has a Vision that reads that “as many people as possible should be able to enjoy what the national park has to offer, without affecting its quality. Emphasis is placed upon visitors enjoying the park in diverse ways, and restrictive management is applied only where it clearly serves the interests of conservation in accord with this management plan13”.

In Norway, the managers of their natural heritage sites have changed their approach in the past decade regarding the way heritage is protected. The changes come from a desire to incorporate human rights and culture into their heritage and environmental management plans. It is argued that when the universal values associated with World Heritage listed places are applied, this can override (or imped) the individual, local and traditional connection to the land.

The key task in Norway when managing to protect the environmental heritage is about bridging the divide of culture and heritage, as they believe it is culture that applies significance to a heritage site. Generally, this applies to indigenous people and their biocultural connection to the land, however in Norway the recognition of connections between people and nature applies to all of society. A benefit of this approach is that it is

13 Þingvellir National Park Management Plan 2004-2024, page 27.

Geeves Track Preliminary Business Case 23

believed that by allowing and building these connections between society and nature, people will care for and respect for the natural heritage, and act as custodians.

3.5 Consultation findings Targeted consultation was undertaken with a number of stakeholders, including:

Local business and tourism industry:

local business owners the Apple Shed Tahune Airwalk Destination Southern Tasmania / Key individual for development of Three Capes

Track

Data and information contacts:

CEO Destination Southern Tasmania Tourism Tasmania Huon Valley Council Parks and Wildlife Service

Others:

Hanny Allston (member of National Parks and Wildlife Advisory Council)

The key messages relating to the need for investment include:

While the region is relatively close to Hobart, there is a lack of a ‘signature’ tourist product in the Huon Valley, and the overall ‘brand’ of the region is limited.

The region’s economic growth and employment growth is limited, and growth in the tourism sector could potentially support economic development. It can have widespread benefits.

While the salmon industry is important for the local economy, it’s not enough. For the Geeves Track proposal to be successful it needs to be more than just a

bushwalk; it needs to allow for a sophisticated experience. The Tahune Airwalk was designed and built with the intention that it become the

signature attraction and experience for the region. Initial visitation was encouraging but has tapered off of late. Existing attractions, including The Airwalk stand to benefit from the development of a flagship tourism attractor. The operators of the Tahune Airwalk are fully supportive of the project and see the potential of the Geeves Track increasing the appeal of the region and drawing more people in. The Airwalk is currently expanding and offering lodge accommodation.

The development of a number of other ‘day trip’ experiences both in Hobart and nearby (e.g. MONA, Pennicott tours, Bruny Island) has developed competition for the Tahune Airwalk and may have contributed to its limited growth.

There is limited accommodation in the region. While there are some existing B&B and pubs, there is nowhere that accommodates a group (small or large) overnight.

There is no wilderness accommodation or significant hotels in the Region. Although the regions of the Tasman Peninsula and the Huon Valley are not directly

comparable (the Peninsula already had a tourism market prior to the Three Capes Track due to the Port Arthur Historic Site); anecdotally the Track has benefited the Tasman Peninsula community. Real Estate prices in Nubeena have increased for example, with local real estate agents putting this down to the influence of the Three Capes Track. There has also have been a range of new small investments in tourism infrastructure and businesses that is anecdotally linked to the presence of the Three Capes Track being in the region.

The local tourism industry very seasonal; sales drop for 4-5 months of the year. This has implications for business confidence and employment.

Geeves Track Preliminary Business Case 24

The quality of accommodation along the track is an important consideration. No one wants to see Hastings Cave in winter, but Geeves Track can be rugged.

Tasmania has promoted itself as a ‘Clean and Green’ state and the Geeves project is consistent with this.

The area to which the Geeves Track will provide access is currently inaccessible, the track would open it up for all types of people who normally wouldn’t have access to the wilderness.

Existing community support

The Geeves Effect Inc has already presented to a wide range of groups and individuals with an overwhelming indication of support, including:

Huon Valley business community, via a meeting at Port Huon with over 100 local business owners in attendance

Huon Valley Economic Development Committee (who made a unanimous recommendation to Council to support the Project)

Huon Valley Council and councillors (who provided unanimous support) Huon Valley Kingborough Tourism Association Far South Tourism Association Huon Valley Kingborough Business Association Huon Valley Council Commissioner, General Manager and senior managers Huon Valley Liberal Party The Huon Valley Rotary Kingborough Rotary Huon Eldercare Kingborough Senior Citizens organisation Huon Resource Development Group Inc, Numerous State and Federal politicians Previous Federal Tourism Minister (which lead to the securing of funding for the

demand study) Destination Southern Tasmania Previous Director Parks and Wildlife Service Tasmania Numerous public servants from Department of Premier and Cabinet and Department

of State Growth, The Office of the Coordinator General The Premier of Tasmania.

The Geeves Effect Inc has also participated in extended interviews on ABC Radio broadcasting state-wide to inform the public of the proposal.

The feedback from this consultation has been positive, with the vast majority of groups very supportive of the project. Specific consultation with Parks and Wildlife indicated that due to the current status of the track in the World Heritage Precinct, they are unable to support the project however all other groups indicated support.

3.6 Popularity of other destinations Some of Tasmania’s iconic natural attractions and destinations appear to be experiencing high levels of crowding and activity. While this reflects a positive outcome for local economies, it also suggests that there is increasing demand for Tasmania’s tourism assets and latent demand for hiking trails in Tasmania.

Developing a new, regionally significant, attraction in a currently under visited region of the State can provide additional choices for visitors and encourage total capacity in visitors to increase.

This is supported by an Australian study by Cox & Wray (2011) which considered the regional marketing efforts of 21 regional destinations in Australia. From this the authors identified a

Geeves Track Preliminary Business Case 25

range of approaches that allow for best practice regional marketing to occur. Identification of new product development opportunities and visitor experiences was seen as important. Importantly developing new products in peripheral parts of a region was found to be highly effective to disperse visitors more broadly through a region, often having the secondary benefits of avoiding over-visitation of key icon attractions and also extending the guests’ overall length of stay14.

3.7 Summary of investment need Tasmania’s economy has undergone significant change as a result of changes to the timber industry, and this has had major impacts on some communities, including Huonville. While some other industries have emerged (including salmon fishing) and some manufacturing associated with the timber and agriculture industry remains, the region retains a relatively narrow economic base. This is a key risk for the future of the region.

The region also accommodates a small tourism sector including some attractions leveraging its natural assets, agriculture and some accommodation. Visitor numbers to Tasmania are growing, reflecting demand for the State’s natural assets and tourism offer. The region does not, however, have a major attractor or drawcard.

There is also a lack of accommodation capacity, with limited opportunities to accommodate large numbers of tourists. The number of visitor nights in the region is low, representing a missed opportunity to capture visitor expenditure.

The natural advantages are well placed to support ‘experiential tourism’ in the region, and the tourism sector represents an opportunity for economic and employment growth. Failure to respond to these challenges is likely to lead to lower levels of economic activity, fewer jobs, and increasing levels of social and economic disadvantage.

The development of tourism infrastructure in the World Heritage area needs to be done carefully, but this would enable more people to experience Tasmania’s natural beauty and environment.

These conclusions were broadly supported by stakeholder consultation. The consultation further uncovered a belief among stakeholders that investment is required to attract more visitors. A lack of appropriate accommodation was also identified as a key issue.

In summary:

The region’s economy was significantly affected by changes to the timber industry. While some industries are growing, the region retains a narrow economic base. Unemployment remains high compared to neighbouring areas

The population is ageing and there is a lack of opportunities for young people in the region

Tasmania’s tourism economy is growing. There is some tourism activity in the region however

It is not coordinated and there is no central ‘precinct’ which draws visitors by providing an ‘experience’

There is a lack of flagship attraction precinct There is limited accommodation in the region

There is policy support for additional tourism activity in the region and in the TWWHA from State Government, as well as strong community support.

14 Carmen Cox & Meredith Wray (2011) Best Practice Marketing for Regional Tourism Destinations, Journal of Travel & Tourism Marketing, 28:5, 524-540

Geeves Track Preliminary Business Case 26

4. DEMAND ASSESSMENT

This section provides a demand analysis to understand current and future demand for the Geeves Track and Tourist Precinct and assess their potential market appeal.

4.1 Method for demand study The following chart provides an overview of the method used for the Demand Study.

FIGURE 14 METHOD FOR DEMAND STUDY

4.2 Case studies Strategic investment by the State Government and by investor-developers has contributed significantly to creating demand for Tasmania’s tourism products. The following review identifies how trail developments (both hiking and mountain bike) can provide positive outcomes, particularly in rural and regional settings. It will also identify usage of the trails in Tasmanian context, to help establish likely demand for the Geeves Track and Tourist Precinct.

Three Capes Track and surrounds

The Three Capes Track (3CT) was planned, developed and then constructed over a period of ten years. The track was officially opened in November of 2015. The development of Three Capes included major upgrading of existing track and the creation of new track, plus the construction of three accommodation complexes on the route. The development allowed for

1) Review of similar

offerings

•Review current multi-day bushwalks in Tasmania via a case study review

•Current demand for iconic trails in Tasmania

•Consultation with the Toursim industry

2) Visitor analysis

•Visatation to Tasmania by market segment

•Visitation growth forecasts

3) Competitive market

assessment

•Qualitative assessment of likely market appeal

•Market strengths of the proposal

4) Demand assessment

•Establish likely demand of Track and Precinct

•Likely flow-on deamnd to businesses and other attractions

Geeves Track Preliminary Business Case 27

a wider demographic to experience the area; walkers no longer have to be experienced, be able to set up their own camp, or carry heavy backpacks.

The construction of the track included 47 kilometres of formed track (either gravel or pine boards) and three huts, providing walkers a safe, short and not-overly taxing alternative to other iconic experiences in Tasmania, such as the Overland Track.

The walk is an ‘easy to moderate’ point to point walk, with three hut locations along the track providing walking unique experiences each day. The huts collect rainwater for drinking, washing and cooking provide solar power for lighting and USB charging stations and pellet fires for heating.

Walkers book their departure day online, and pay a track fee of $495 per adult which includes:

Site entry, car parking and secure lockers at Port Arthur Historic Site Pennicott Wilderness Journey cruise, departing Port Arthur at 11.30am and 2pm daily Three nights accommodation in cabins on the track Bus transfer from Fortescue Bay back to Port Arthur Historic Site Guide book with maps

During planning, it was argued that the Track would increase the profile of the Tasman Peninsula’s natural values which would help transform the Tasman from a day destination to an overnight one. It was estimated that the track would attract 10,000 walkers per year (60 departures per day) with 90% of walkers being from interstate. The 10,000 walkers per annum was met in the first year of operation, not after ten years as envisioned.

It was estimated that this would generate spending of $3.1 million per year and the creation of 70 jobs for the region. It was also predicted that more than 55 jobs would be created for the construction phase, at least ten of which would be traineeship or similar positions. At a state level, it was projected that the development of the Three Capes Track would generate $19.7 million spending within Tasmania annually creating an additional 334 jobs in Tasmania.

Since opening the Track has been a success with visitation meeting and exceeding predictions, and the track has won prestigious industry awards including the 2016 Gold for new tourism business at the Australian Tourism Awards. This has led to increasing confidence in the project with extensions to the Track supported by the State Government, and private investment to construct two further on-track, premium eco-lodges.

The investment in the 3CT by the State Government has proven to be very fruitful with a very high return on investment15. Annual revenues from walker fees alone in the near future (after construction of privately operated huts) will equal the total investment made by the State Government ($17 million). Revenues received on the Track are set to reach $4.5 million in the 2017/18 financial year16. The Track has been credited with making a significant economic contribution to the Tasman Peninsula, with the PWS employing 13 FTE staff to run and manage the Track, with a further7 FTE staff at Pennicot Wilderness Journeys and the Port Arthur Historic site17. During the construction phase 93% of the construction expenditure was spent with-in Tasmanian18

The identification in the planning stage of the need to provide a high-quality track and accommodation experience, without the need for walkers to carry heavy packs, has proven to be accurate leading to strong market appeal. The tourism market is increasingly expecting a high-quality, sophisticated, unique, experience based attractions and leisure activities; a key reason for the success of the Three Capes Track is that it tapped into a large, new market of potential visitors19. Three Capes didn’t market itself purely at the small bushwalking market,

15 Information from consultation with Destination Southern Tasmania - Stuart Lennox 16 Groom, M (2017). Iconic tracks hike up revenues. Press release from Minister for Environment and Parks 17 Groom, M (2017). Iconic tracks hike up revenues. Press release from Minister for Environment and Parks 18 Clark, B (2017). 2017 National and International Trail Awards, Tasmania’s Three Capes Track 19 Information from consultation with Destination Southern Tasmania - Stuart Lennox

Geeves Track Preliminary Business Case 28

but instead the wider experiential tourist market, i.e. it was aimed at people who want an experience, not people purely interested in bushwalking. The 3CT experience includes boat rides, art works, interpretation via a guide book, and knowledgeable resident park ranges. This access to a new market segment is seen as crucial to the Three Capes Tracks success.

Destination Southern Tasmania, with support from the Department of State Growth, has recently developed the Tasman Destination Action Plan 2016–2018. The Plan aims to leverage the signature experiences of the Three Capes Track. Key opportunities for the Tasman region identified in the Plan generated by the growing tourism industry in the region include:

Converting day visitors to overnight visitors Leverage Three Capes Track to grow market – be seen as a premium walking

destination, day and overnight Converting visitation to population growth, including business investment Product development for high yield visitors including food and beverage

opportunities and niche experiences including game fishing and surfing

Regarding access to the Capes for bushwalkers not wanting to stay in huts and avoid the walking fee, they cannot walk the entire 3CT circuit. However, walkers can access Cape Pillar via a two day walk on the old Cape Pillar track from Fortescue Bay. A formal campsite is provided with tent platforms, toilet and rainwater tank. Walkers can return via Mt Fortescue and Cape Hauy.

Implication for Geeves Track: A well-considered, planned and delivered track, combined with successful brand growth/ marketing, can support increased visitation and tourism activity. The identification of the appropriate visitor segment, carefully planned accommodation and track activation strategies are crucial to deliver an integrated and compelling tourism product.

Overland Track

The Overland Track is a world-famous, six-day walk through the mountains, alpine meadows, glacial landscapes and temperate rainforests of the Tasmanian Wilderness World Heritage Area (TWWHA). The walk begins at Cradle Mountain and extends 65 kilometres to Lake St Clair. The walk can be undertaken as an independent walker, a member of a large group (13 max) e.g. a school or community group, or as a member of a commercial group (Cradle Mountain Huts) staying in private huts.

Public accommodation along the Track is provided by six overnight nodes to accommodate walkers. Each overnight node has basic facilities with accommodation options including:

Huts with bunks (no mattresses), tables and bench seats, and heating. No lighting or cooking facilities are provided.

Tent platforms for campers (platforms protect vegetation) Toilets (composting toilets – all waste is flown out by helicopter) Water supplied by rainwater tanks

The Overland Track Report for 2015/16 reported that walker numbers were up by 17.5 per cent on the previous year. During 2015/16 a total of 8,265 walkers departed Cradle Mountain to walk the Overland Track; the months of December to March were almost fully booked, with fewer bookings in the shoulder months of October, November, April and May. No bookings are required in June through September.

The Overland Track has been a significant part of the Tasmanian tourism brand for many years, but it is also making an important contribution to regional economic development and the broader Tasmanian economy. A recent report, The Socio-economic Impact of the Overland Track, identified the value of direct and indirect tourism expenditure from the track for 2012- 2013 at $16.36 million and estimated the business supports the equivalent of 85 full-time jobs. The track has a direct benefit to the many businesses that are associated with it through providing guided walks or transport for walkers to and from the track. Other businesses supply the Parks and Wildlife Services with materials and/or services including

Geeves Track Preliminary Business Case 29

track materials, products and services for the huts and toilets, energy supplies and helicopter services.

In 2015/16 the Parks and Wildlife Service Business Enterprise that operates the Overland Track generated $1.1 million in revenue. This revenue was generated through walker fees, commercial licences/leases, and merchandise. The Overland Track generates an economic return to the Parks and Wildlife Service which is reinvested to maintain and improve services.

Implication for Geeves Track: Successful tracks can generate revenue which can be re-invested to support track operations and maintenance. Selecting an appropriate price point for the walk is crucial, to avoid dampening demand via high price, but to also recoup costs and support track maintenance and operation of the walk.

Cradle Mountain Village

Located just outside the TWWHA, the Cradle Mountain Village connects visitors to a wide choice of wilderness experiences. Experiences include well-known bushwalks such as the summit of Cradle Mountain and the six-kilometre Dove Lake circuit, and the Devil Sanctuary and Wildlife Park. Of an evening, activities include dinner at accommodation and nocturnal wildlife walks.

Cradle Mountain is considered the primary gateway to the TWWHA, and is the beginning point for the Overland Track.

Accommodation options at the village include camping and huts, budget rooms and five-star luxury lodges and hotels. Accommodation is located within two-to-five minutes of the Cradle Mountain Visitor Centre.

The Cradle Mountain Visitor Centre and visitor experience with-in the Park are set to be upgraded. The proposal includes a cable-car to transport visitors into the park and significant upgrade to the Visitor Centre. Economic modelling performed by Inspired by Marketing as part of the Master Plan (2016) reveals that the upgrade will lead to increased tourism expenditure in Tasmania due to attracting more visitors. The redevelopment is forecast to attract an additional:

58,600 visitors 102,100 visitor nights $29.2m in incremental expenditure

Implications for Geeves Track: Investments in visitor infrastructure on the boundary of the TWWHA can generate economic benefits for the surrounding region.

Freycinet National Park and Peninsula Circuit

The Freycinet National Park is Tasmania’s most visited Park, attracting around 270,000 visitors per annum. Freycinet Peninsula encompasses the Freycinet National Park and adjacent Coles Bay and Swanwick townships. It is receiving unprecedented visitation with growth to Freycinet National Park increasing 61% from 186,000 visitors in 2011 – 2012 to an expected 300,000 in 2017-2018.

There are several options for walking and experiencing the Freycinet Peninsula. Bushwalkers can walk Freycinet Peninsula Circuit, taking two to three days. No huts are provided and walkers carry their own tent and sleeping gear, cooking equipment, water and food; the track is grade T2, Narrow but distinct tracks, which can be muddy in some place. Costs for independent bushwalkers completing the Freycinet Circuit are the cost of access to the National Park (parks pass) and bookings are not required.

At Freycinet there is also the award-winning Freycinet Experience Walk; a four-day privately operated guided tour along the Freycinet Peninsula. The Experience includes bus transfers to and from Hobart with stops at attractions along the way, two sea cruises, fishing, swimming and daily bushwalks throughout the Freycinet Peninsula. The experience is limited to 10

Geeves Track Preliminary Business Case 30

guests and two guides at a time. Accommodation is provided at the high-quality Friendly Beaches Lodge, purposely designed to be eco-friendly, and located deep with-in the National Park. The cost for the Experience Walk is $2,400 per person for the summer season.

The Freycinet Lodge is also located with-in the Parks boundaries and has close to 100 per cent occupancy over summer and 90% in the shoulder seasons20; the Lodge has recently gained council approval to expand, with-in its existing footprint. Camping in the Freycinet National Park is also very popular with campsites, including powered sites, allocated via a ballot system over summer due to the demand. Hotel, motel, backpacker and cabin accommodation are available outside the Park in the nearby town of Coles Bay, including the international award winning, 5 star, Saffire Resort.

The success of Tourism at Freycinet and along-the East Coast more generally, alongside the decline of primary industries such as farming fishing and forestry, has seen the tourism industry become the largest industry for the region over the past decade21. The East Coast Regional Tourist Organisation22 is targeting that by 2020 the East Coast’s tourism industry will employ 1,100 people, attract 1.9 million room nights and be worth $200 Million.

However there has been some recent concern that Freycinet is reaching capacity with some commentators and groups calling visitation caps to be put in place. The region’s tourism body highlights that the ongoing success has highlighted some infrastructure pressure – especially around the Freycinet area. Some of the antiquated sewerage systems are struggling with the peak loads and the Wineglass Bay Walk car park overflows most days during the peak times which can negatively impact on the Visitor Experience23. Large increases in visitor numbers at any national park or reserve can place pressure on natural values, services, visitor experience and amenity.

In response to crowding the State Government has announced funding to provide for 80 new car parks at the National Park to alleviate parking issues. It is argued that the current situation is at a critical point and if allowed to degrade further could significantly threaten the ongoing success of the Peninsula as a regional and state tourism drawcard and become a detriment of the Tasmanian brand

Implications for Geeves Track: Very high-quality offerings, such as the Freycinet Experience and Saffire Resort, can be offered in tandem with more general Park entry.

The Park is reaching capacity and attracting visitors to other regions of the State could limit the impact on the natural environment, and possibly Tasmania’s brand, at the National Park.

Blue Derby Trails and Pods Ride Experience

The Dorset Council established the 80km of mountain-bike trails with funding from the Tasmanian Forest Agreement. Since then an unprecedented era of visitation, exposure and opportunity has occurred in the area. The Blue Derby forest reserves attracts riders from all over the state, across the country and around the globe and hosted a multi-day Trail Running event over the long weekend in 2016 and 2017. Economist Saul Eslake reports close to a 250 per cent increase in visitation to the Derby region since 2015, “reflecting the region’s success in attracting mountain bike riders to the newly developed trails”.24

The wider trails network has been a huge success. The two local councils, Dorset and Break O’Day, estimated during planning that the trails might attract 5,000 riders a year; the councils now expect up to 50,000 people to use the trails over the next 12 to 18-month period, with 70 per cent of users coming from interstate25. Unemployment was high in Dorset before the

20 http://www.themercury.com.au/lifestyle/ract-pod-project-at-freycinet-national -park-approved-by-glamorgan-spring-bay-council/news-story/6938a4a46a42070db4442accf51b2a30 21 Geografia et al. (2014) Planning for Sustainable Tourism on Tasmania’s East Coast - Sustainable Tourism Options Report 22 East Coast Regional Tourist Organisation (2016) Annual Report 23 East Coast Regional Tourist Organisation (2016) Annual Report 24 The Mercury (2017). No Point Turning Back Now. 25 Bearup, G. (2017). It’s pedalicious: Blue Derby Pods Ride. The Australian.

Geeves Track Preliminary Business Case 31

construction of the tracks, but since work began on the tracks the number of cafes in Derby is set to double and tourist accommodation is to be tripled26. Land and housing prices have also increased rapidly with many houses being converted to Airbnbs.

The Blue Derby Pods Ride adds to the experience by providing a high-end, multi-day riding option. Accommodation consists of high amenity, architecturally designed ‘pods’ set in the natural environment. The pods include solar panels, composting toilets and manually pumped showers in an effort to reduce their environmental impact. Prices for the pod ride experience start at $1,750 per person in winter, $1,950 at shoulder times and $2,150 at peak for two nights, three days. The price includes bikes and helmets, all food and drinks, pod accommodation, mountain biking instruction and flora and fauna descriptions.

The pods alone are estimated to create 16 full-time jobs, and accommodate up to 1,000 visitors a year.

Implications for Geeves Track: There are opportunities to be gained through delivering new, high-yield eco-tourism attractions in the protected area network.

Case study summary and findings

FIGURE 15 CHARACTERISTICS AND DEMAND

Three Capes Track Overland Track Cradle Mountain Village