G.C.E.(A.L.) Support Seminar - 2014 - Education...

18

Questoion No. Answer Questoion No. Answer (1) 3 (21) 2 (2) 4 (22) 4 (3) 1 (23) 4 (4) 5 (24) 3 (5) 5 (25) 2 (6) 3 (26) 4 (7) 5 (27) 3 (8) 5 (28) 2 (9) 4 (29) 4 (10) 2 (30) 5 (11) 3 (12) 2 (13) 5 (14) 4 (15) 4 (16) 2 (17) 2 (18) 3 (19) 5 (20) 5 [ see page 2 Accounting - Paper I Answer Guide G.C.E.(A.L.) Support Seminar - 2014

Transcript of G.C.E.(A.L.) Support Seminar - 2014 - Education...

Questoion No. Answer Questoion No. Answer

(1) 3 (21) 2

(2) 4 (22) 4

(3) 1 (23) 4

(4) 5 (24) 3

(5) 5 (25) 2

(6) 3 (26) 4

(7) 5 (27) 3

(8) 5 (28) 2

(9) 4 (29) 4

(10) 2 (30) 5

(11) 3

(12) 2

(13) 5

(14) 4

(15) 4

(16) 2

(17) 2

(18) 3

(19) 5

(20) 5

[ see page 2

Accounting - Paper I Answer Guide

G.C.E.(A.L.) Support Seminar - 2014

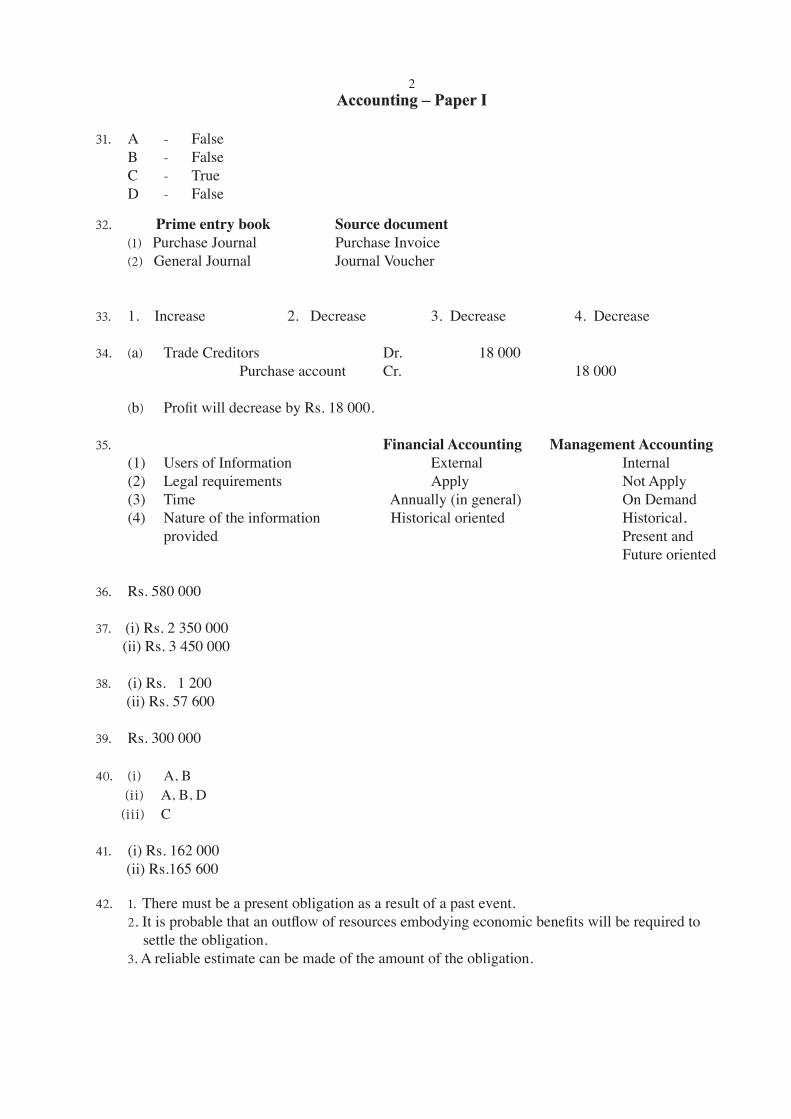

2Accounting – Paper I

31' A - False

B -False C - True

D - False

32' Prime entry book Source document ^1&Purchase Journal Purchase Invoice ^2&General Journal Journal Voucher

33' 1. Increase 2. Decrease 3. Decrease 4. Decrease

34' ^a& Trade Creditors Dr. 18 000 Purchase account Cr. 18 000

^b& Profit will decrease by Rs. 18 000.

35' Financial Accounting Management Accounting (1) Users of Information External Internal (2) Legal requirements Apply Not Apply (3) Time Annually (in general) On Demand (4) Nature of the information Historical oriented Historical, provided Present and Future oriented

36' Rs. 580 000

37'(i) Rs. 2 350 000 (ii) Rs. 3 450 000

38' (i) Rs. 1 200 (ii) Rs. 57 600

39' Rs. 300 000

40' ^⁄& A, B ^⁄⁄&A, B, D ^⁄⁄⁄& C

41' (i) Rs. 162 000 (ii) Rs.165 600

42' 1'There must be a present obligation as a result of a past event. 2. It is probable that an outflow of resources embodying economic benefits will be required to settle the obligation. 3. A reliable estimate can be made of the amount of the obligation.

343' Net cash flows generated from operational activities Rs.5 140 000 Option:-

Draft profit for the period

Add:- Provision for income tax Depreciation of assets Deduct:- Profit on sale of motor vehicles Income tax paid Increase in inventoriesNet cash flows generated from operational activities

360100

200 300

20

5 200

460

5 660

(520)

5 140

(Rs. '000)

44' A Transfer of Rs. 200 000 to the general reserve. B Issue of shares of Rs. 500 000 by capitalising the reserves. C Issue of Ordinary shares for Rs. 500 000. D Transfer of Rs. 300 000 to revaluation reserve, and Rs. 500 000 to retained earnings, out of the total comprehensive income of Rs.800 000.

45' Only C.

46' Rs.125 000

47' ^⁄& Purchasing department should be informed by the stores department on the required quantity of goods to be purchased. ^⁄⁄& Obtain quotations from the approved suppliers. (Purchasing department will send to suppliers)^⁄⁄⁄&Recording the receipts, issues and balances of the stocks and keeping them at the racks will enable to check the balances of stocks at the stores at any given time ^⁄¤& Register maintained to record the material receipts, issues and balances including the value.

48' ^⁄& Economic Order Quantity – 2 000 units ^⁄⁄& Optimum number of orders to place – 125 orders

49' ^⁄& 2014.03.31 Accumulated Fund Rs. 36 0002013.03.31 Accumulated Fund Rs. 31 000Surplus Rs. 5 000

^⁄⁄& 2014.03.31 Accumulated Fund – Rs. 36 000

50' 1.Prime cost 2. Prime cost 3. Production overhead cost 4. Production overhead cost

4Accounting – Paper II

Question No. 01

^1& Net Profit Adjustment Statement

Drafted ProfitAdd:- Building revaluation Provision for doubtful debts Interest Income Deductions:- Depreciation - Building Depreciation -Machinery Lease interest Bad debts Write off of inventories Long term loan interest Expenses of issue of shares Provision for income taxes

2002

30

80604040152050

135

580

232812

(440)372

(Rs. '000)

^2& Kanishaka (Pvt) Ltd. Statement of Financial Position as at 31.03.2014

Non-Current AssetsProperty Plant and EquipmentFixed Deposit - 15%

Current AssetsInventoriesTrade debtors 260Provision for doubtful debts (13)Interest receivable Cash & cash equivalents

Stated Capital

Ordinary SharesNon redeemable preference shares

ReservesRevaluation reserveGeneral reserveRetained earnings

Long-term liabilities Long term loan @12% Lease creditors

Current liabilitiesTrade creditorsLoan interest payableLease creditorsIncome tax payablesDividends payablesBank overdraft

160

24730

1 125

3 8001 500

1 280800342

4002095

200100185

7 1801 200

1 5629 942

5 300

2 422

1 000220

1 0009 942

(Rs. '000)

5^3& Kanishaka (Pvt) Ltd.

Changes in equity statement for the year ended 31.03.2014

(Rs. '000)

Balance 01.04.2013Capitalization of reservesGeneral reserveTotal comprehensive income Right issue of shares Dividends:- Preference shares Ordinary sharesBalance 31.03.2014

Ordinaryshares

Preferenceshares

Revaluation reserve

General reserve

Retained earnings

Total

2 500800

--

500

--

3 800

1 500----

--

1 500

1 000(600)

-880

-

--

1 280

800(200)

200--

--

800

450-

(200)372

-

(180)(100)

342

6 250--

1 252500

(180)(100)7 722

^4& Disclosures

(1) The inventories has been valued at Rs.160 000 which is the lower of cost of the inventories and its net realizable value.

(2) Rs. 100 000 worth of inventories has been pledged to the bank as a security for the bank overdraft obtained.

Workings :

AssetBalance

01.04.2013Additions/

RevaluationsDisposals/ Transfers

Balance31.03.2014

8 600

^1 420&

7 180

LandBuildingsOffice EquipmentMachinery

4 4002 0001 800 400

----

----

4 4002 0001 800 400

DepreciationBalance

01.04.2013Additions Deductions

Balance31.03.2013

BuildingsOffice EquipmentMachinery

-680

-

400280 60

---

400960 60

(Rs. '000)

Revaluation Reserve (Rs.)Bal b/f Land 400^Equity& Buildings 680Bal c/d

1 080 1 080

Building Account (Rs.)Bal b/f 1 600 Accumulated 280Revaluation DepreciationReserve Bal c/d 2 000 2 280 2 280

680200

880

6Question No. 02

02' ^a& ^1&

Profit and Loss Appropriation Account (Rs.'000)Net profit

Interest on capital:DisaGayaSachi

Salaries :Sachi

Profit Shares :DisaGayaSachi

100

85

50

165

110

55

740

^235&

^175&

^330&

-

Dissa Gaya Sachi Dissa Gaya Sachi

Drawings Drawings

Balance c/d

20030

535765

22035

240495

14020

125285

Balance b/f Salaries Interest on capital Profit share Interest for loan

500-

100165

-765

300-

85110

-495

-17550555

285

(Rs.'000) Current Accounts

Dissa Gaya Sachi Dissa Gaya SachiGoodwill

Balance c/d

150

1 0001 150

100

850950

50

500550

Balance b/fSalariesGoodwill

1 000-

1501 150

800-

150950

-550

-550

(Rs.' 000)Capital Accounts

ÚGoodwill also can be treated by debiting Sachi Rs.50 and crediting Gaya Rs.50.

7^a&

Equity and LiabilitiesCapital Accounts : Dissa Gaya SachiCurrent Accounts : Dissa Gaya SachiNon Current Liabilities : Loan from SachiCurrent Liabilities : Loan from Sachi

1 000850500

535240125

2 350

900

325

603 635

(Rs.'000)Extracts of statement of Financial Position as at 31.03.2014

Workings:

Calculation of Adjusted profit Rs.’000Profit before adjustments (120+180+360) 660Add – Drawings (30+35+20) 85Deductions – Loan interest 400 × 5/100 × ¼ (5) 740

Total Goodwill 50 × 6 = 300

^b& ^1&

1/1 InventoryRaw material purchases3/31 InventoryCost of materials consumedProduction salariesPrime CostProduction overhead costOverhead expensesDepreciation on machineryTotal production cost

10 00066 000(8 800)

15 80010 000

67 20062 000

129 200

25 800155 000

(Rs. '000)

Suranji Manufacturing Enterprise Manufacturing account for the quarter ended 31.03.2014

^2& Revenue generated from sales of flower pots 1650 × 150 = Rs. 247 500

8

Workings:

Number of flower pots produced

1/1 Timber stock ( Sq.fts) 50Purchases 300 3/31 Closing stock (8 800 / 220) (40) 310 No. of flower pots 310 × 5 = 1 550Production salaries 1 550 × 40 = Rs. 62 000

Number of Flower pots sold

Opening No. of flower pots 200Production during the quarter 1 500Closing stock (100) 1 650

Question No. 03

^3& ^a& ^1&

(Rs. '000)Assets

Liabilities EquityMotor Vehicles

Furniture & fittings Stocks Trade

Debtors Bank

1 500 95 43 270 137 355 1 690 +40 -40 +125 +125 +90 -90 -65 30 +50 +15 -270 +265 -5 -35 -5 -30 -8 -8

-25 -251 475 135 60 30 412 350 1 762

^⁄&

Bal B/f

^⁄⁄&

^⁄⁄⁄&

^⁄¤&

^¤&

^¤⁄&

^¤⁄⁄&

^¤⁄⁄⁄&

^2& All numbers are in rupees thousand

Net profit/ loss = Closing net assets – Opening net assets + Drawings - Additional capital introduced

= 1 762 – 1 690 + 8 - 125 Net Loss = Rs. 45

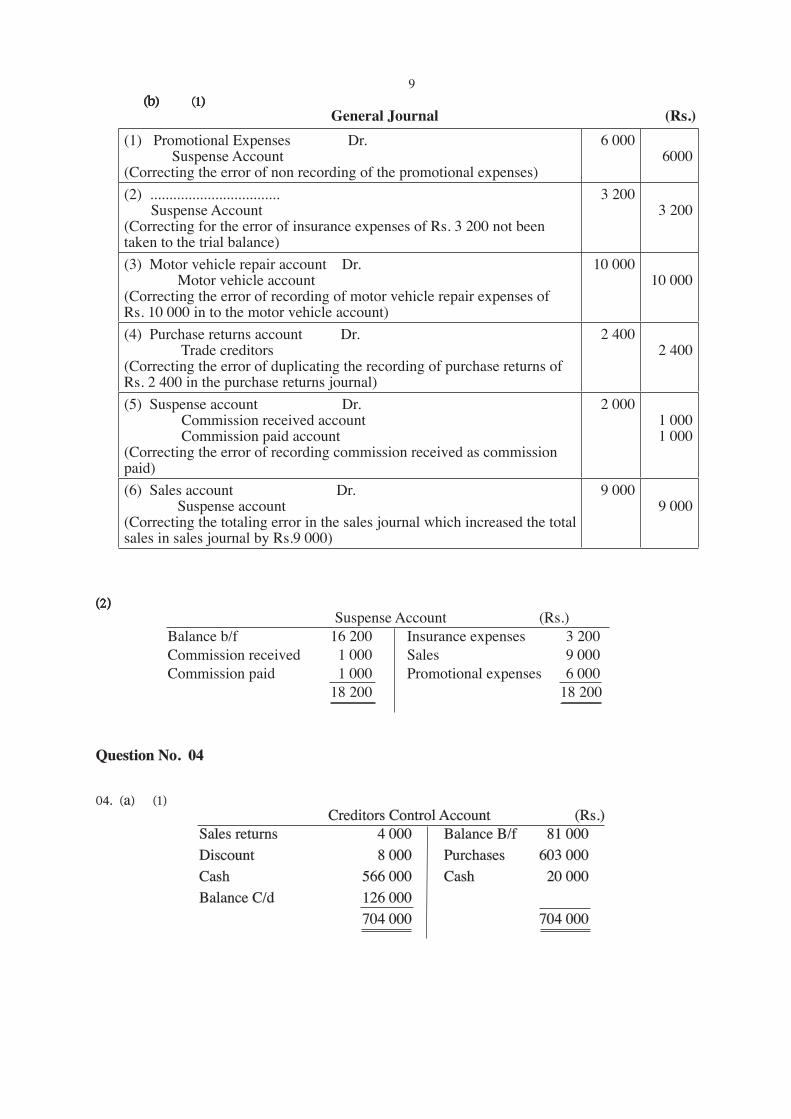

9 ^b& ^1&

(1) Promotional Expenses Dr. Suspense Account(Correcting the error of non recording of the promotional expenses)

6 0006000

(2) .................................. Suspense Account(Correcting for the error of insurance expenses of Rs. 3 200 not been taken to the trial balance)

3 2003 200

(3) Motor vehicle repair account Dr. Motor vehicle account(Correcting the error of recording of motor vehicle repair expenses of Rs. 10 000 in to the motor vehicle account)

10 00010 000

(4) Purchase returns account Dr. Trade creditors(Correcting the error of duplicating the recording of purchase returns of Rs. 2 400 in the purchase returns journal)

2 4002 400

(5) Suspense account Dr. Commission received account Commission paid account (Correcting the error of recording commission received as commission paid)

2 0001 0001 000

(6) Sales account Dr. Suspense account (Correcting the totaling error in the sales journal which increased the total sales in sales journal by Rs.9 000)

9 0009 000

General Journal (Rs.)

^2&

Suspense Account (Rs.)Balance b/f 16 200 Insurance expenses 3 200Commission received 1 000 Sales 9 000Commission paid 1 000 Promotional expenses 6 000 18 200 18 200

Question No. 04

04'^a& ^1&

Creditors Control Account (Rs.)Sales returns 4 000 Balance B/f 81 000Discount 8 000 Purchases 603 000Cash 566 000 Cash 20 000Balance C/d 126 000 704 000 704 000

10^2& Rs. 145 000

Balance as per creditor accountAdd: Unrecorded PurchasesPurchases being recorded at a lower amountLess: SalesBalance in the creditor account

12 00027 000

126 000

39 000165 000(20 000)145 000

(Rs.)

Option:

Creditors Control Account (Rs.) Sales 20 000 Balance B/f 126 000 Purchases 27 000 (recorded at a lesser value) Balance C/d 145 000 Purchases 12 000 165 000 165 000

^3&

Creditor Reconciliation Statement (Rs.)Balance as per creditors control

Add: Discount - Asith Unrecorded discount

Deductions: Unrecorded purchases Total of trade creditor ledger

3 0004 000

145 000

7 000152 000

(12 000)140 000

^b& ^1&

Bank Reconciliation Statement as at 31.03.2014 (Rs.)Bank overdraft as per bank statementAdd : Unrealized cheques

Less : Cheques issued but not presentedBalance as per bank account

^8 000&

25 00017 000

^18 000&

^1 000&

11

Bank Account (Rs.)Returned cheque 15 000 Balance B/f 13 750(Rent) Bank charges 500 Cheque book charges 350Balance C/d 1 000 Insurance expenses 1 400 16 000 16 000

^2&Bank account balance (over draft) before the adjustments are made is Rs.13 750

Question No. 05

05' ^a& ^1&

(1) Machinery transfer account Dr. Machinery account

(Transferring the cost of the machine to the machinery transfer account)

130 000130 000

(2) Accumulated depreciation for machineryMachinery transfer account

(Transferring the accumulated depreciation of the transferring machinery to the Machinery transfer account )

32 50032 500

(3) Machinery accountMachinery transfer accountCash account

(Completing the transaction by transferring the old machine and settling the balance by cash)

120 000100 00020 000

(4) Machinery transfer account Profit & Loss/ Income statement

(Recognizing the profit of machinery transfer)

2 5002 500

General Ledger (Rs.)

^2&

Decrease in profit if not for machinery transfer (Machinery depreciation) = Rs. 10 000

Decrease in profit as a result of transfer (Depreciation – 7 500+ 3 000) = Rs. 10 500Increase in profit due to the profit obtained in machine transfer = Rs. 2 500 Rs. 8 000

Increase in profit 10 000 - 8 000 = Rs. 2 000

12Workings:

Accumulated profit up to the date of transfer (Rs.)

Year ended = 8 00031.03.2011

Year ended = 8 00031.03.2012

Year ended = 4 00031.03.2013 = 5 000

Depreciation

up to 01.01.2014 = 7 500 32 500

Depreciation for the = 2014.01.01 to 1/1 to 3/31 = 7 500year ended 31.03.2014 = 3 000 10 500

8 000×12

10 000×34

90 000 - 10 000 10}

}}

90 000 + 40 000 - 10 000 - 20 000

10 × 1

2

120 000 1104

×

05' ^b&

Statement of Affairs (Rs.)Capital250 250Noncurrent assets 150 000 Cash 80 000 Trade debtors15 250Trade creditors 30 000 Stocks 35 000 280 250 280 250

Cash account (Rs.)Bal b/f 80 000 Salaries 19 000Receipts from 223 000 Operational expenses 18 000trade debtors Drawings 5 000Cash sales 54 000 Trade creditors 280 000 Bal c/d 35 000 357 000 357 000

}

Debtors Control Account (Rs.)Bal b/f 15 250 Cash 223 000Sales 264 750 Discount given 7 000 Bal c/d 50 000 280 000 280 000

Creditors Control Account (Rs.)Cash 280 000 Bal b/f 30 000Discount 4 000 Purchases 268 000received Bal c/d 14 000 298 000 298 000

}

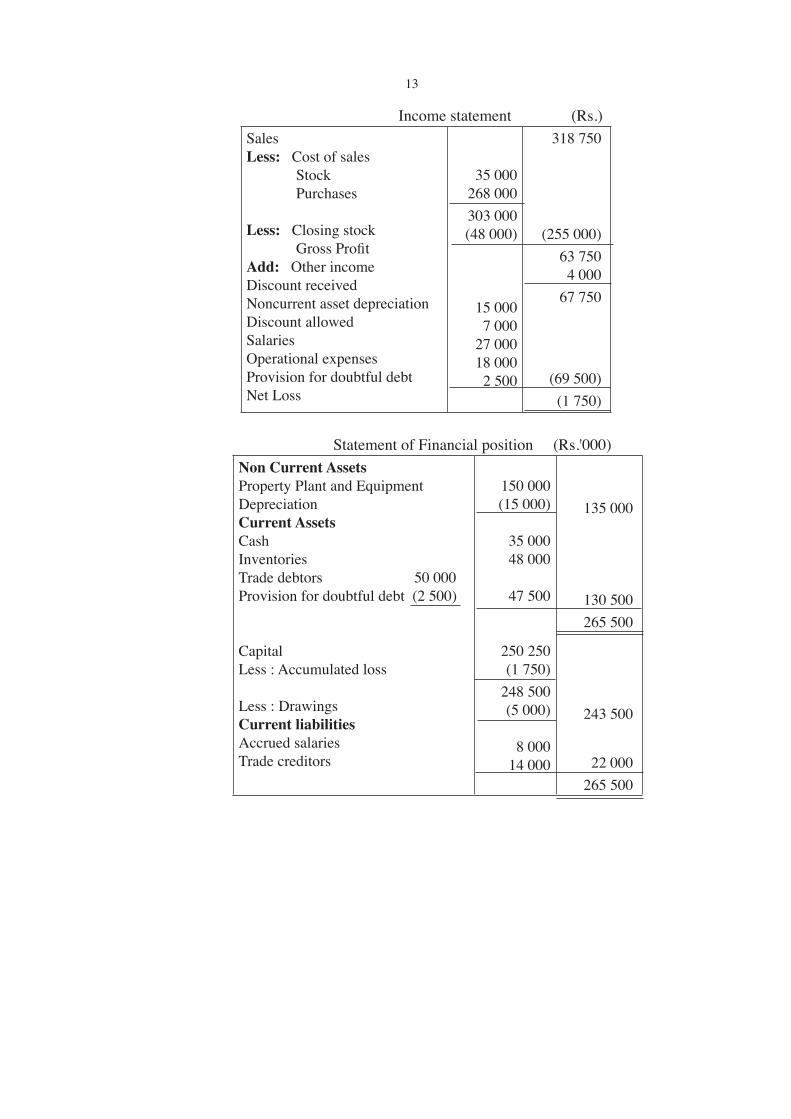

13

Income statement (Rs.)SalesLess: Cost of sales Stock Purchases Less: Closing stock Gross ProfitAdd: Other incomeDiscount receivedNoncurrent asset depreciationDiscount allowedSalariesOperational expensesProvision for doubtful debtNet Loss

35 000268 000303 000(48 000)

15 0007 000

27 00018 0002 500

318 750

(255 000)63 7504 000

67 750

(69 500)(1 750)

Statement of Financial position (Rs.'000)Non Current AssetsProperty Plant and EquipmentDepreciationCurrent AssetsCashInventoriesTrade debtors 50 000Provision for doubtful debt (2 500)

CapitalLess : Accumulated loss Less : DrawingsCurrent liabilitiesAccrued salariesTrade creditors

150 000(15 000)

35 00048 000

47 500

250 250(1 750)

248 500(5 000)

8 00014 000

135 000

130 500265 500

243 500

22 000265 500

14Question No. 06

^6& ^a& ^1&

Statement of Affairs as at 31.03.2013 (Rs. ' 000)Accumulated Fund 550 Noncurrent assets Noncurrent Liabilities Sports complex 500 Life membership fund 500 Gym equipment 800 Gym Equipment fund 300 800 Current Liabilities Current Assets Subscription received 125 Subscription receivable 50 in advance Bank balance 125Advance received 40 165 Cash 40 215 1 515 1 515

}

Income and Expenditure Account for the year ended 31.03.2014 ^Rs. ' 000&Salaries 120 Subscription fees 550Other Expenses 250 Daily fees 520Promotional expenses 80 Rental income 120Maintenance 75 Depreciation - Sports complex 25 Depreciation -Gym equipment 160 Surplus 480 1 190 1 190

}

Statement of Financial Position as at 31.03.2014 (Rs. ' 000)Accumulated Fund 550 Noncurrent assets Add : Surplus 480 Sports complex 475 Noncurrent Liabilities Gym equipment 640 1 115 Life time membership fund 450 Gym Equipment fund 300 750 Current Liabilities Subscription received 100 Current Assetsin advance Subscription receivable 100Advance received 70 Bank balance 745Rent received in advance 60 230 Cash 50 895 2 010 2 010

15

Workings: Subscription Account (Rs. ' 000)Balance B/f 50 Balance B/f 125Income expenditure 550 Cash 425Balance c/d 100 Life member fees 50 Balance c/d 100 700 700

Cash Account (Rs. ' 000)Balance B/f 40 Salaries 120Subscription 425 Other expenses 250Income from daily charges 550 Promotional expenses 80Rental income 180 Maintenance 75 Bank 620 Balance c/d 50 1 195 1 195

^b&

Total variable cost = Rs. 300 Contribution = 800 - 300 = 500

Total Fixed Cost Vehicle expenses = 125 000Other = 25 000Salaries = 12 500 162 500

(1) Number of items to be sold = 162500 / 500 = 325

(2) In order to obtain a profit of Rs. 150 000 = (162500+150 000)/500 = 625

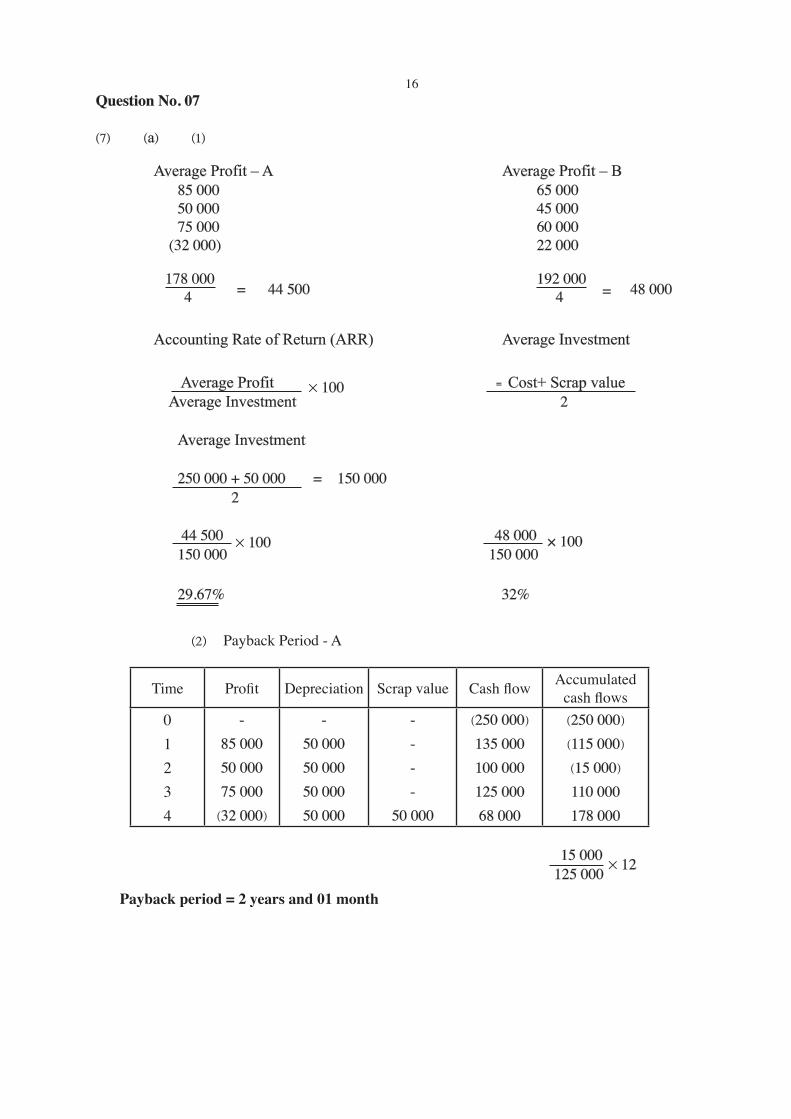

16Question No. 07

^7& ^a& ^1&

Average Profit – A Average Profit – B 85 000 65 000 50 000 45 000 75 000 60 000 (32 000) 22 000

178 000 4

= 44 500

192 000 4

= 48 000

Accounting Rate of Return (ARR) Average Investment

Average Profit }Cost+ Scrap value Average Investment 2

Average Investment

250 000 + 50 000 = 150 000 2

44 500 48 000 150 000 150 000

29.67% 32%

× 100

× 100 × 100

^2&Payback Period - A

Time Profit Depreciation Scrap value Cash flow Accumulated cash flows

01234

-85 00050 00075 000^32 000&

-50 00050 00050 00050 000

----

50 000

^250 000&

135 000100 000125 00068 000

^250 000&

^115 000&

^15 000&

110 000178 000

15 000

125 000× 12

Payback period = 2 years and 01 month

17 Payback Period - B

Time Profit Depreciation Scrap value Cash flow Accumulated cash flows

01234

-65 00045 00060 00022 000

-50 00050 00050 00050 000

----

50 000

^250 000&

115 00095 000110 000122 000

^250 000&

^135 000&

^40 000&

70 000192 000

40 000

110 000× 12

Payback period – 2 years and 04 months

^3&

A (Rs.)

01234

Discounting factor at 15% Cash Flows Present Value 1

'87'76'66'57

^250 000&

135 000100 000125 00068 000

^250 000&

117 45076 00082 50038 760

Net Present Value 64 710

B (Rs.)

01234

Discounting factor @ 15% Cash Flows Present Value

1'87'76'66'57

^250 000&

115 00095 000110 000122 000

^250 000&

100 05072 20072 60069 540

Net Present Value 64 390

^4& As per Accounting Rate of Return (ARR) A B Option to select 29.67% 32% B

As per Payback Period A B Option to select 2 years and 01 month 2 years and 04 months A

As per Net Present Value A B Option to select 64 710 64 390 A

(5) Machine A

18^7& ^b&

(1) Average Consumption = 3 000 + 10 000 – 1 000 – 1 200 = 10 800 = 10 800 / 3 = 3 600

(2) Re order level = Maximum consumption × Maximum lead time = 800 × 15 = 12 000 units

(3) Re- order quantity = 15 000 units

^4&

Unit price (Rs.) 2014.03.01 Balance 3 000 10.00 30 000 Purchases 15 000 12.00 180 000 18 000 11.67 210 000 Issues (10 000) (116 700) 8 000 93 300 Sales returns 1 000 12.00 12 000 9 000 11.70 105 300 Purchases 15 000 15.00 225 000 24 000 13.76 330 300 Purchase returns (2 000) 15.00 (30 000) Balance 22 000 13.65 300 300

Value of stock as at 31.03.2014 is Rs. 300 300