Federation of GCC Chambers Conference on Frameworks for funding industrial projects

GCC Projects Overview

A briefing to MEED Projects Customers

Abu Dhabi, 19 November 2012

Baghdad approves $118bn draft budget for 2013 – MEED 5 Nov

Saudi Arabia's king appoints new interior minister – BBC, 5 Nov

UN: Iran not cooperating on nuclear probe – Daily Star, 5 Nov

Bahrain bomb blasts kill two foreign workers – BBC, 5 Nov

Syria opposition groups hold Qatar meeting – MEED, 4 Nov

UAE approves deficit-free budget for 2013 – MEED, 31 Oct

IMF warns GCC to cut government spending – MEED, 30 Nov

Adviser lined up for NWC privatisation – MEED, 30 Oct

Kuwait awards $2.6bn Subiya Causeway contract – MEED, 29 Oct

Contractors submit bids for Doha Metro Red Line - MEED 16 Oct

Kuwait approves $433m worth of road projects – MEED, 10 Oct

Headlines

• Regionally/globally, outlook is uncertain

• Global outlook worsened, although emerging economies have performed well

• MENA disrupted by upheaval, but high oil prices boost oil exporters

• IMF forecasting MENA growth of 5.3% in 2012, downturn in 2013

• Oil price outlook - $110 barrel in 2012 and $94/barrel in 2013, up from $104/barrel in 2011 and $79/barrel in 2010

• GCC growth = 5.3% in 2012 (3.9.% (oil), 6.4% (non oil))

• MENA oil exporters = 5.5%

• MENA oil importers = 2.2%

• Iraq = 10.2% (14.7% in 2013)

The economic outlook (IMF)

Source: IMF World Economic Outlook, October 2012

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2006 2007 2008 2009 2010 2011 2012 2013

World Advanced economies Emerging economies

MENA GCC MENA oil importers

UAE

Real GDP growth forecast for 2012 and 2013 (%) - IMF

• Lower-than-expected oil prices

• Increase government spending

means that long-term dip in oil

prices will squeeze budgets

raising prospect of fiscal deficits

• Global recession due to

eurozone debt crisis, sluggish

US growth and further shocks

• Lack of growth and subsidy cuts

needed to maintain fiscal

discipline adds to social tensions

• Greater economic divide

• Banking sector problems – credit

remains a challenge

BREAK EVEN OIL PRICES ($/barrel)

2010 2011 2012

Algeria 95 95 105

Bahrain 92 100 115

Iran 70 86 115

Iraq 90 102 110

Kuwait 56 50 50

Libya 55 na na

Oman 58 74 80

Qatar 25 38 40

Saudi Arabia 75 80 75

Sudan 140 na Na

UAE 55 84 80

Yemen 130 150 240

The risks to the outlook (IMF)

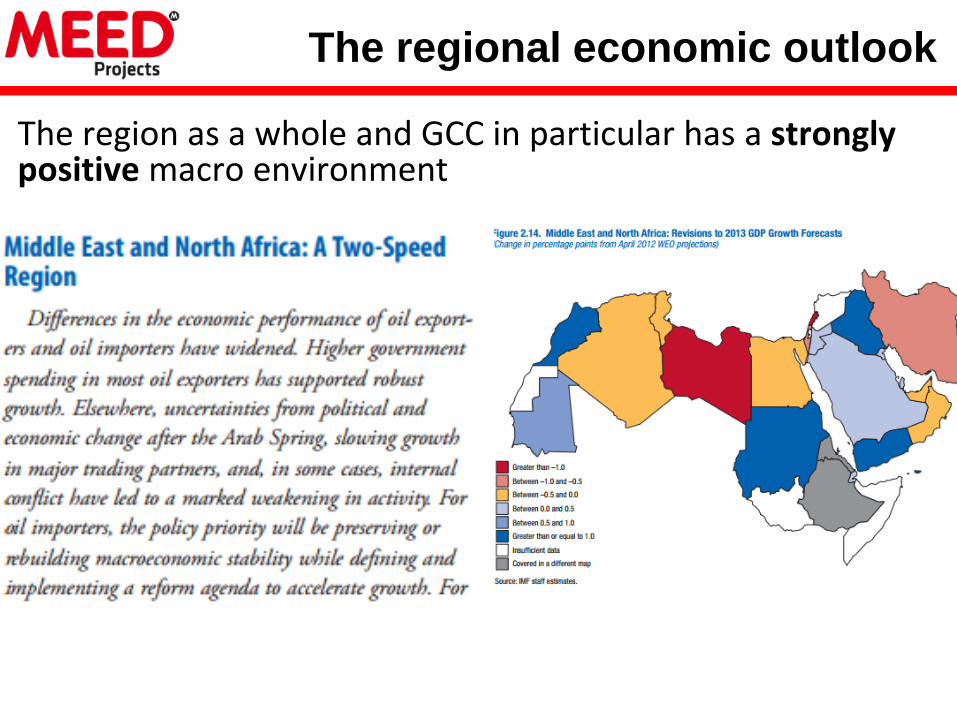

The regional economic outlook

The region as a whole and GCC in particular has a strongly positive macro environment

“The US will overtake Saudi Arabia and Russia to become the world’s largest global oil producer by the

second half of this decade”

“a drop in global oil prices would affect production , since tight oil

requires a high market price to be economic”

“US will be producing 11.1m b/d in 2020 compared with Saudi output

of 10.6m b/d. Saudi Arabia will have regained top spot by 2030 pumping 11.4m b/d compared

with the US’s 10.2m b/d”

Alarming headlines

WEO 2012 – a closer look

WEO 2012 – implications

US oil output growth and softening of US demand means possible drop in oil price

Speed of US oil output growth means oil-exporters only have a 5 year window in which to enjoy high surpluses

Increasing importance of Iraq in the region, economically and probably politically

Universal natural gas demand means hydrocarbons investment focus must shift to gas production

Imperative for reduction in fuel subsidy in GCC/MENA without increase in tariffs, demands energy efficient buildings, transport, industry

Governments must invest while they have surpluses to invest

Governments have a narrow window of opportunity

Iraq to displace Saudi Arabia, UAE, Qatar as biggest projects’ market

Emphasis on previously uneconomic unassociated gas and gas recovery

Public transport, water re-use, green buildings, alternative energy

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Sau

di A

rab

ia

UA

E

Qat

ar

Ku

wai

t

Om

an

Bah

rain

Iran

Iraq

Egyp

t

Alg

eria

Mo

rocc

o

Jord

an

Leb

ano

n

Syri

a

Sud

an

Lib

ya

Tun

isia

Yem

en

$ m

illio

nGCC/MENA: Project markets by value of contracts awarded ($m)

2007 to 2012 (YTD)

Water

Transport

Power

Oil

Industrial

Gas

Construction

Chemical

GCC $776bn)

MENA $358bn

Landscape since 2004 has been dominated by UAE, KSA construction; last 3 years sees UAE contraction and KSA growth

GCC, MENA Projects Market (1)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

Sau

di A

rab

ia

Ku

wai

t

UA

E

Qat

ar

Om

an

Bah

rain

Iraq

Iran

Alg

eria

Egyp

t

Jord

an

Tun

isia

Mo

rocc

o

Yem

en

Leb

ano

n

Sou

th S

ud

an

Lib

ya

Syri

a

Sud

an

$ m

illio

nGCC/MENA: Project markets by budget value of unawarded projects

($m) 2012 to 2017

Water

Transport

Power

Oil

Industrial

Gas

Construction

Chemical

GCC $1,081bn)

MENA $747bn

Big shift in this picture is due entirely to the inclusion of the Saudi nuclear and renewables programme. Iraq has potential to be at least as big as UAE

GCC, MENA Projects Market (2)

GCC – recent history by country

Arrow indicates trend over past 2 years: flat = Bahrain, Kuwait, Oman; growing = Qatar, UAE; slowing = KSA

40% 36% 11% 7% 5% 2%

% of contracts awarded

UAE accounts for 67% of the total number of awarded projects put on hold or cancelled since 2007, equivalent to 74% of the total contract value of those projects

GCC – recent history by country

5% 4% 6% 6% 13% 67%

% of inactive

4% 2% 5% 7% 9% 74%

% of contract

GCC – recent history by sector

Civil Construction (Construction and Transport) consistently the largest sector, except in 2009 (financial crisis)

42% 40%

31%

61%

42% 48%

% contract value of non-Civil projects

GCC – recent history by sector

Civil Construction (Construction and Transport) consistently the largest sector, except in 2009 (financial crisis)

42% 40%

31%

61%

42% 48% 49%

% contract value of non-Civil projects

0

100

200

300

400

500

600

700

800

900

1000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Co

un

t o

f aw

ard

s/co

mp

leti

on

s

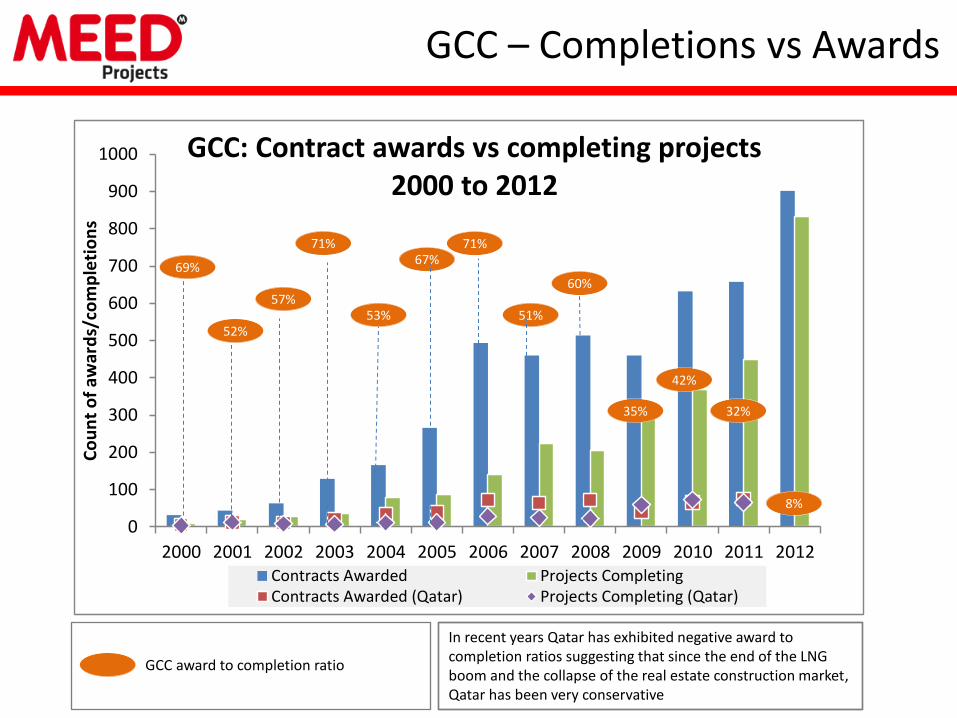

GCC: Contract awards vs completing projects 2000 to 2012

Contracts Awarded Projects CompletingContracts Awarded (Qatar) Projects Completing (Qatar)

69%

71% 67%

71%

51%

60%

35%

42%

32%

8%

57%

52%

GCC award to completion ratio

In recent years Qatar has exhibited negative award to completion ratios suggesting that since the end of the LNG boom and the collapse of the real estate construction market, Qatar has been very conservative

GCC – Completions vs Awards

53%

• KSA awards proportionately more big contracts than GCC

• Count of contract awards actually increased after 2009 but will drop in 2012

• More contracts of $1bn or more were awarded in 2009, 2010, 2011 than in any other year

• Most contracts awarded in 2009, 2010, 2011 were in the $50-$100m band

• Inference: biggest and smallest projects have been the least susceptible to market conditions

• But in 2012, likely that the lowest value bands will see the biggest volume of awards

GCC – Contract awards by value band

7%

7%

% of highest value projects awarded

UAE

GCC

8%

8%

21%

16% 8%

10%

18%

7%

8%

10%

UAE

GCC

GCC

UAE

GCC

UAE

UAE

GCC

UAE

GCC

18 17 10

8 8

18 23 9 10

3

9 19 1 2 4

21 21 9 3

6

23 22 12 4

7

19 17 5

4 6

GCC – Key sectors: Transport

Biggest of the four Key Sectors at $140bn; energy efficient, West-East energy trade, GCC as a hub

Transport cashflow peak is reached in late 2016, but note that this accounts only for known masterplans.

Rail accounts for half of all awards in GCC and roads/rail infrastructure for 80% of transport spending

$139,594m

Cashflow

GCC – Key sectors: Renewables

Despite the early 2011 Fukushima disaster, Riyadh has remained firmly committed to nuclear. As part of its studies, Ka-Care drew up four different scenarios for its deployment, setting out various options for the schedule and size of the programme. The optimised scenario calls for the construction of 11 nuclear reactors with total capacity of 17,600MW by 2030, with the first due to be commissioned in 2020/21. The location of the first reactors will be finalised once Australia’s WorleyParsons completes in the third quarter of 2012 site investigation studies. Once finalised, Riyadh is expected to move swiftly in tendering the first batch of reactors given that it will need to award the initial contracts in 2013 if it is to hit its 2020/21 target.

The kingdom’s solar plans are even more ambitious, especially as it has only limited solar experience and installed capacity of less than 20MW. Ka-Care is targeting 41,000MW of capacity within 19 years of the programme being launched. This, it estimates, would save the kingdom an estimated 523,000 barrels of oil equivalent a day of hydrocarbons.

$89,925m

GCC – Key sectors: Gas

Few viable unassociated fields so investment is necessarily longer term (Khazzan, Dorra, Bab, Hail)

Immediate opportunities in energy capacity building limited to Oil

Qatar North Field moratorium may be lifted in 2015 – new wave of LNG investment?

$48,152m

Cashflow

GCC – Key sectors: Water

Double peak of transmission spending is Qatar (LRDP) and then longer Qatar projects supplemented by Riyadh sewerage

Transmission and treatment of sewage accounts for half of all spending between end 2010 and end 2020

$24,150m

Cashflow

Lack of activity in all sectors caused by political stalemate and uncertainty

Subiya causeway award in October changed the course of the weakest year of awards since 2009

KOC talking about long term plans for the oil sector, to increase output to 4m bpd by 2030 but time running out to meet 2020 clean Fuels deadline

No substantial Refinery projects and no movement yet on Clean Fuels or KNPC Refinery Projects

Volume of awards will be about the same in 2012 vs prior years but top end expectation unlikely to exceed $10.5bn – equivalent to 2010

Subiya causeway award may now give impetus to other urban dev projects in Kuwait City and Subiya itself

Kuwait – 2012 Outlook

Saudi Arabia – 2012 Outlook

Awards in June in Pet-chem and Power, masked lower than expected infra awards in H1 2012, in all but higher ed. 26 of the 148 contracts awarded by public bodies awarded by MOHE

Lack of activity in upstream and midstream sectors (delays to Jizan for instance)

Total value of awards in KSA was $32bn in first 9 months of 2012, compared with $55bn over the equivalent period in 2011

But potential value of infrastructure awards in the Kingdom as a proportion of total potential projects is lower than any other GCC market, even though value of projects is enormous in absolute terms ($80bn)

Big awards = just 6% of total number of contracts awarded in KSA, vs 18% in 2011 and 2011.

Volume of awards will actually increase in 2012 vs prior years but top end expectation unlikely to better 2009 ($59bn) at around $50bn.

0

5

10

15

20

25

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Nu

mb

er

of

Pro

ject

s

Va

lue

($

mil

lio

n)

Qatar: Number and Value of Awarded Contracts and Scheduled Awards 2012

Sum of contract value

Sum of contract value (Aug snapshot)

Count of projects (Aug snapshot)

Count of Projects

ScheduledScheduledAwarded(Sep snaphot)

(Sep snaphot)

Bid deadlines for $5bn worth of packages for Golden Line Tunneling package, Education City/ Msheireb Stations extended into Nov

Bid deadlines for Tunneling worth $6bn (Blue/Green lines) moved to end Oct

August’s analysis $22bn worth of contracts at late bidding scheduled for award Sept to Dec

Overall impact on project volumes/ values in 2012 significant only because full year expected to deliver 100+ contracts, worth in excess of $25bn.

There is still a possibility that the Red Line packages will be awarded on time

Qatar – 2012 Outlook

Volume of awards to drop to between 80 and 90 and top end expectation for 2012 only slightly up on 2011 ($14.5bn) at around $15-19bn.

Volume of awards to increase to between 170 and 190 and top end expectation for 2012 10% up on 2011 ($22.8bn) at around $25bn.

UAE – 2012 Outlook

Dubai led by Civil Construction (buildings and transport); as busy as 2009 (volume/value)

2012 recovery for Abu Dhabi led by award of ADAC midfield terminal award and Takreer carbon black: both $2bn+

Dubai shows almost as much activity but only one award worth more than $1bn (Aviation City)

Abu Dhabi also shows market led by civil, but a more even spread of spending across sectors; no obvious rebound since slump of H2 2012. UZ750 EPC2 still expected in December

Modest value of contract awards in Northern Emirates; Federal government spending accounts for 40%+ of awards including biggest project – Fujairah WDN

GCC – 2013 Outlook

Predicting $112bn full year 2012

Best case: $170bn full year 2013 if KSA rebounds, all scheduled Qatar projects are awarded

Mid case: $137bn full year 2013 if KSA has modest rebound, Qatar delays Gold, Blue and Green Line

Julian Herbert – Director Product Development, MEED

Projects

Abu Dhabi Conference, 18 November 2012

P.O.Box 25960 20th Floor, Al Thuraya Tower 1 Dubai Media City, Dubai, UAE

m: +971 (0) 50 557 4140 t +971 (0) 4 390 0045 d +971 (0) 4 390 0849 f +971(0) 4 368 8025

i www.meedprojects.com