GBS Market and Maturity Assessment Analysis: Nordic Perspective

59

0 © 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. GBS Market and Maturity Assessment Analysis: Nordic Perspective GBS Roadmap: Driving Value and Performance Don Ryan, KPMG LLP Adrian Baldwin, GSK 28 April 2015

-

Upload

kpmg-sweden -

Category

Business

-

view

161 -

download

3

Transcript of GBS Market and Maturity Assessment Analysis: Nordic Perspective

0© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

GBS Market and

Maturity Assessment

Analysis: Nordic

Perspective

GBS Roadmap: Driving Value and

Performance

Don Ryan, KPMG LLP

Adrian Baldwin, GSK

28 April 2015

1© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Session organization

Breakout #4: Show me the money Financial

Benefits – 30 minutes and Group

Discussion

■ Case examples, dollars amounts, scale

issues – magnitude of returns in relation to

the maturity model

Break out session #5: What moves the

Needle – Drivers and Outcomes – 30

Minutes and Group Exercise

Roundtable #1: Building a better GBS – 60

minutes

■ Four groups: How can GBS support each

business critical objective. Examples of

outcomes and financial benefits.

■ Each group takes 2 categories – but we

can change these depending on what the

group wants. Each group takes 2

categories to discuss.

– Brand Support and Risk Reduction

– M and A support

– Process efficiency (both in GBS and

across retained functions)

– Customer Experience and Interaction

(Overall and as service by GBS)

Breakout #2: GBS Maturity Assessment

Review and Case Example by GSK – 30

minutes

2© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Breakout #2:

Reviewing maturity

assessment results

3© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

It’s a new day

REDUCED COST STRUCTURE

OF OPERATIONS

87%

IMPROVED QUALITY OF

OPERATIONAL DATA TO DRIVE

MANAGEMENT DECISIONS

88%

BETTER USE OF AUTOMATION

TO REDUCE RELIANCE ON

MANUAL LABOR

82%

GREATER SCALABILITY

OF OPERATIONS

84%

IT ENABLED BUSINESS

PROCESSES TO PROVIDE

SOLUTIONS, NOT TECHNOLOGY

80%

Source: HfS research

Organizations say that all these

factors are important or critical to

the success of the GBS program

4© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

What is Global Business Services (GBS)?

An integrated platform to deliver enterprise business services

Drives efficiency and business outcomes

Evolves with the market and company needs

Key Capabilities:

■ Multi-functional business

processes

■ Multi-channel service delivery –

outsourced, shared services and

centers of excellence

■ Process ownership and

management

■ Common information technology

■ Enterprise-wide governance

5© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

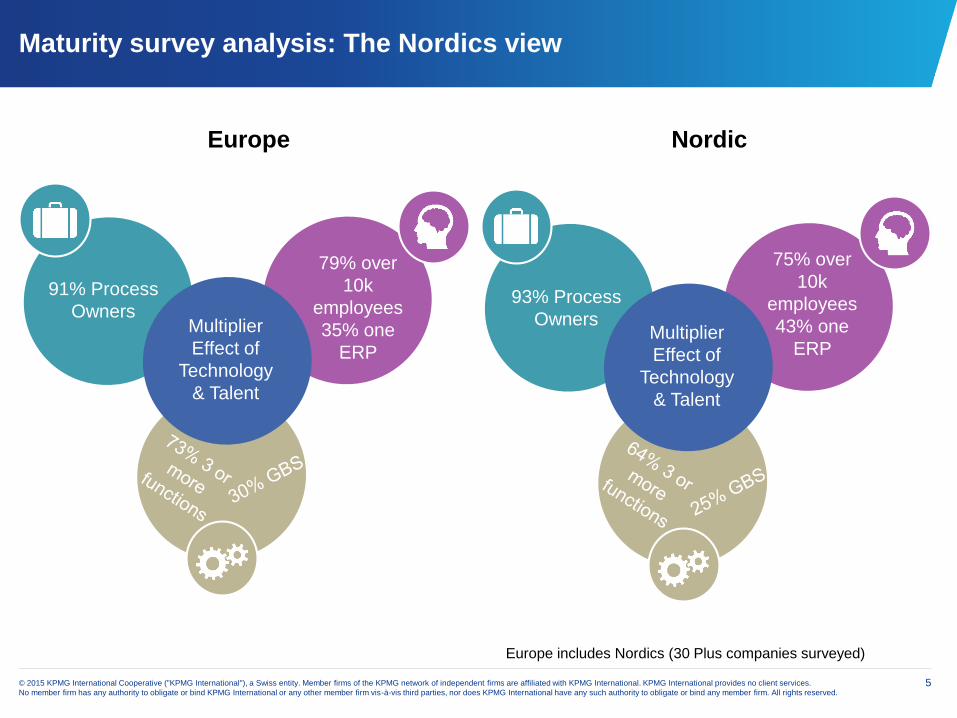

Maturity survey analysis: The Nordics view

Europe includes Nordics (30 Plus companies surveyed)

Europe Nordic

79% over

10k

employees

35% one

ERP

91% Process

OwnersMultiplier

Effect of

Technology

& Talent

75% over

10k

employees

43% one

ERP

93% Process

OwnersMultiplier

Effect of

Technology

& Talent

6© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

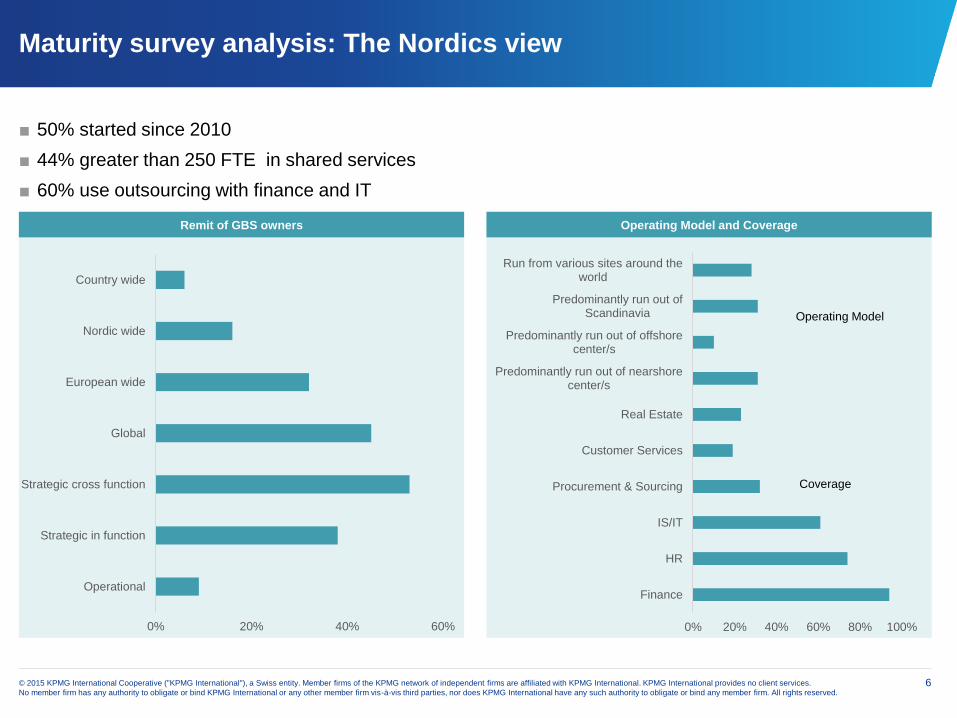

Maturity survey analysis: The Nordics view

■ 50% started since 2010

■ 44% greater than 250 FTE in shared services

■ 60% use outsourcing with finance and IT

Remit of GBS owners Operating Model and Coverage

0% 20% 40% 60%

Operational

Strategic in function

Strategic cross function

Global

European wide

Nordic wide

Country wide

0% 20% 40% 60% 80% 100%

Finance

HR

IS/IT

Procurement & Sourcing

Customer Services

Real Estate

Predominantly run out of nearshorecenter/s

Predominantly run out of offshorecenter/s

Predominantly run out ofScandinavia

Run from various sites around theworld

Operating Model

Coverage

7© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Maturity survey analysis: The Nordics view

Analytics

0% 10% 20% 30% 40% 50%

GBS is not involved in data and analytics services

GBS is currently planning and building a data and analytics reporting service

GBS delivers basic data and analytics reporting (standard packages) and providesperiodic and ad-hoc analysis for customers

GBS delivers advanced data and analytics reporting and diagnostic analysis, andidentifies future operational reporting proactively based on the frequency and

importance of business needs

Analytics

Process Focus

0% 10% 20% 30% 40%

Business processes are managed solely within functionaldelivery teams, discrete to a function

Fragmented process ownership, but with informal peer-to-peer networking

Process owners exist and manage global process forselect processes, applied in functional silos

Functionally oriented process owners exist to managemost global processes

Global process ownership incorporating both the GBS andnon-GBS portion of an end to end process

8© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

What do our clients say

9© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

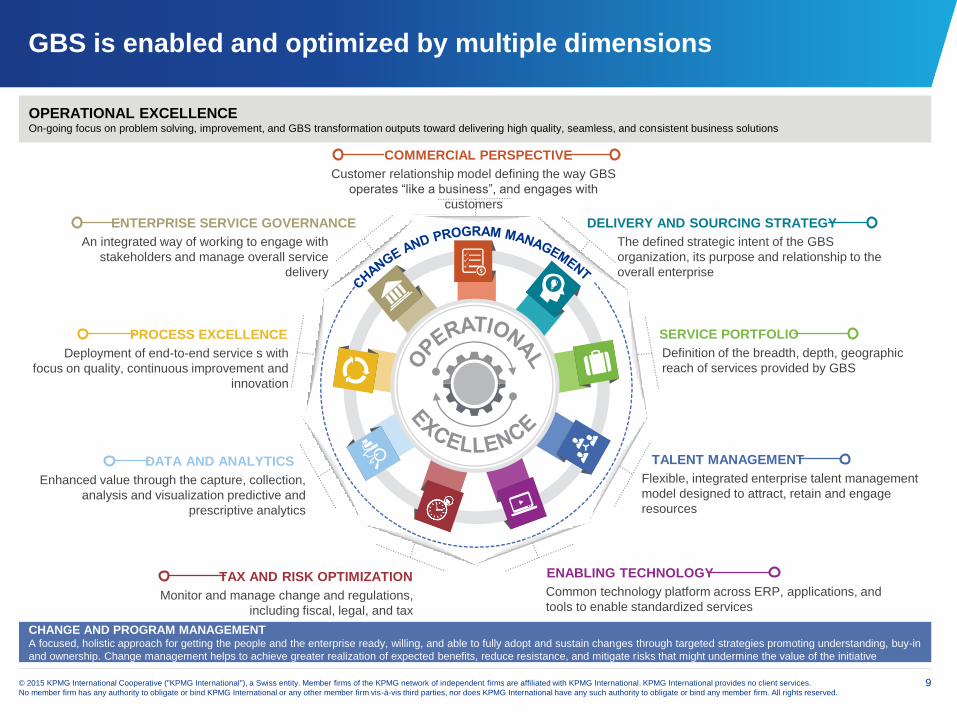

GBS is enabled and optimized by multiple dimensions

CHANGE AND PROGRAM MANAGEMENTA focused, holistic approach for getting the people and the enterprise ready, willing, and able to fully adopt and sustain changes through targeted strategies promoting understanding, buy-in

and ownership. Change management helps to achieve greater realization of expected benefits, reduce resistance, and mitigate risks that might undermine the value of the initiative

OPERATIONAL EXCELLENCEOn-going focus on problem solving, improvement, and GBS transformation outputs toward delivering high quality, seamless, and consistent business solutions

COMMERCIAL PERSPECTIVE

Customer relationship model defining the way GBS

operates “like a business”, and engages with

customers

DELIVERY AND SOURCING STRATEGY

The defined strategic intent of the GBS

organization, its purpose and relationship to the

overall enterprise

SERVICE PORTFOLIO

Definition of the breadth, depth, geographic

reach of services provided by GBS

TALENT MANAGEMENT

Flexible, integrated enterprise talent management

model designed to attract, retain and engage

resources

ENABLING TECHNOLOGY

Common technology platform across ERP, applications, and

tools to enable standardized services

TAX AND RISK OPTIMIZATION

Monitor and manage change and regulations,

including fiscal, legal, and tax

DATA AND ANALYTICS

Enhanced value through the capture, collection,

analysis and visualization predictive and

prescriptive analytics

PROCESS EXCELLENCE

Deployment of end-to-end service s with

focus on quality, continuous improvement and

innovation

ENTERPRISE SERVICE GOVERNANCE

An integrated way of working to engage with

stakeholders and manage overall service

delivery

10© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

GBS maturity survey dimension parameters

Delivery and Sourcing

StrategyLittle or no alignment between GBS and corporate missions,

strategy and planning.

Bi-directional formulation of strategy & planning between GBS,

functional, BU and corporate management

GBS operates on multiple IT systems for each GBS customer.GBS operates on a single instance ERP across enterprise with

standard enabling technologies. Enabling Technology

GBS delivery groups are aligned singularly to functional leadership.

Functions are responsible for all aspects of process development,

performance management and

talent management.

GBS serves as an independent operating unit on par with other

Functions/BUs providing output based services to Functions/BUs

based on policy and requirementsEnterprise Governance

Decentralized service delivery model with single function Multi-functional, multi-channel service delivery modelServices Portfolio

GBS provides transaction processing and staff mix and skills reflect

this narrow focus

Broad talent management practices ensure GBS people and

leaders are recognized for their insight, innovation and customer-

orientation. Talent Management

No formal analysis of service supply-demand.

Formal supply-demand of services is used to optimize

consumption and evaluate service sourcing. Formal analytics in

place. Commercial Orientation

Business processes are managed solely within their delivery teams,

which are discrete to a function and/or geography.

Global process ownership incorporating both the GBS and non-

GBS portion of an end to end process. Process Excellence

Information is created and distributed through a combination of static

reporting and limited ad-hoc requests; analysis is performed on as-

needed basis.

Dynamic reporting, with predictive modeling provide users with

prescriptive analysis of real time data from internal and external

sourcesData & Analytics

Absence of organizational flexibility and senior management

ownership

High degree of management buy-in and formal processes for

driving GBS acceptance in the organizationChange Management

Assurance reporting requirements are not included in service

provider contracts, and no coordination occurs with providers on

assurance related matters

Assurance reporting with impact to the organization's financial

reporting, operational, and compliance objectives with due

diligence occurring for new and existing providersRisk and Tax Optimization

Lo

w

Hig

h

1 3 5

11© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Mapping results against the GBS maturity results: Nordics

SCALED

Functionally oriented

Global shared service model

Variation around processes, tech and governance

standardization

Se

rvic

e D

eli

ve

ry M

an

ag

em

en

t M

atu

rity

Strategic

Multi-functional, multi-channel service delivery model

Provides transactional and analytic services

Managed through integrated, outcome-oriented governance

Synced end-to-end

Integrated

Enterprise wide multi-functional service

delivery platform

Coordinated processes, technology, governance, and multi-

channel delivery for scale and adaptability

SUB-SCALED

Consolidated delivery model

Leverage economies of scale for highly transactional services

Shared services or outsourcing typically on a single-function

FRAGMENTED

Decentralized service delivery model

Duplicative functions, processes, and technology

Little central control and governance over business support

services

Cu

sto

me

r F

oc

us

Levels of Maturity

1

2

3

4

5

Nordic Sector

Aspirational Average 3.8

Current State Aspirational State

# 1

1.8

# 1

NA

# 2

2.2

# 2

NA

# 3

2.9

# 3

3.4

# 4

1.9

# 4

3.0# 5

2.9

# 5

4.2

# 6

1.9

# 6

2.8

# 7

3.4

# 7

3.9

# 8

1.9

# 8

3.4

# 12

4.4

# 9

3.1

# 9

3.6

# 10

1.9

# 10

3.1

# 11

2.7

# 11

3.5

# 12

3.9

Nordic Sector Current

Average 2.8

# 13

3.1

# 13

2.2

# 14

3.6

# 14

2.1

# 15

5.0

# 15

4.0

# 16

3.7

# 16

3.1

# 17

3.3

# 17

2.8

Europe Current

Average 3.0

Europe Aspirational

Average 3.9

12© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

GBS maturity survey results: Europe

Aspirational

LEGEND

Current

Overall.

Average 100

companies

Average Best in

Class

(3 or more

process or gov.)

1 3 5

Data & Analytics

Lo

w

Hig

h3.72.3

Enabling Technology

Lo

w

Hig

h3.0 4.1

Talent Management

Lo

w

Hig

h3.82.7

Services Portfolio

Lo

w

Hig

h3.4

Delivery and Sourcing Strategy

Lo

w

Hig

h4.33.3

Risk and Tax Optimization

Lo

w

Hig

hEnterprise

Governance

Lo

w

Hig

h3.82.9

Process Excellence

Lo

w

Hig

h4.03.0

Commercial Orientation

Lo

w

Hig

h4.03.0

Change Management

Lo

w

Hig

h4.12.9

3.24

.2

3.8

13© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

GBS maturity survey results: Nordics

1 3 5

3.92.7

3.62.4

3.0

4.23.1

2.9

3.72.8

3.2 4.0

3.72.6

3.82.9

3.8Aspirational

LEGEND

Current

Average Best in

Class

Data & Analytics

Lo

w

Enabling Technology

Lo

w

Enterprise

Governance

Lo

w

Talent Management

Lo

w

Process Excellence

Lo

w

Change Management

Lo

w

Services Portfolio

Lo

w

Delivery and Sourcing Strategy

Lo

w

Risk and Tax Optimization

Lo

w

Commercial Orientation

Lo

w

Hig

hH

igh

Hig

hH

igh

Hig

hH

igh

Hig

hH

igh

Hig

hH

igh

2.9

3.6

3.9

Overall.

Average 100

companies

14© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

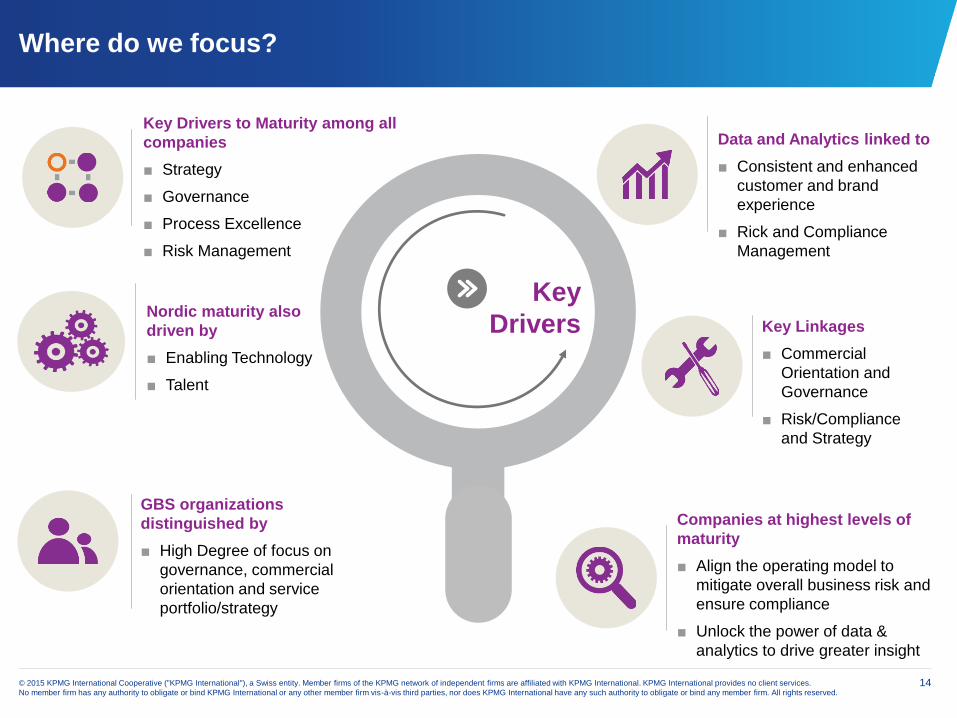

Where do we focus?

Key

Drivers

Key Drivers to Maturity among all

companies

■ Strategy

■ Governance

■ Process Excellence

■ Risk Management

Nordic maturity also

driven by

■ Enabling Technology

■ Talent

Data and Analytics linked to

■ Consistent and enhanced

customer and brand

experience

■ Rick and Compliance

Management

GBS organizations

distinguished by

■ High Degree of focus on

governance, commercial

orientation and service

portfolio/strategy

Key Linkages

■ Commercial

Orientation and

Governance

■ Risk/Compliance

and Strategy

Companies at highest levels of

maturity

■ Align the operating model to

mitigate overall business risk and

ensure compliance

■ Unlock the power of data &

analytics to drive greater insight

15© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

What maturity looks like and how to achieve

Action Plan

Delivery and

Sourcing Strategy

■ Use outsourcing partners to give access to

technology enablers and leading practices

■ Identify a champion at senior level to help gain

alignment with Executive objectives

■ Monitor & report benefits to increase GBS buy-in

■ GBS strategy tied directly to overall

corporate strategy

■ Mix of captive and outsourcing to have the

best labor arbitrage and value delivery

Enabling

Technology

■ Rationalize existing systems

■ Invest in technology led process improvements and

innovations

■ Create dedicated IT organization and/ or CoE to

support GBS

■ One ERP system with 2 or less instances

■ Use of Enterprise Service management for

non-IT governance activities

■ Automation in all possible parts of a process

Governance

■ Formalize, regularize and document all governance

practices

■ Drive an overall functional expansion and

transformation agenda within GBS

■ Single governance structure with head of

GBS reporting to COO or CEO

■ COO or other C-level management are

process owners or sponsors

Services Portfolio

■ Expand functional scope and BU coverage

■ Extend to cross functional end to end process

opportunities

■ OH functions are delivered by GBS; IT is in GBS

■ A large majority of back office operations

are standardized, transactional services

■ GBS provides five or more services

Desired State

16© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

What maturity looks like and how to achieve

Action Plan

Talent

■ Assess workforce capabilities across employee

lifecycle and form clear career paths

■ Enable cross-training and placement across

functions and processes, regular staff rotation

■ Talent management tailored to operations

■ Turnover less than 15% per year

■ Continuous learning and development, robust

training, knowledge management and

collaboration are part of GBS culture

Commercial

Orientation

■ Invest in GBS brand building activities

■ Perform benchmarking on price and performance

against third party providers

■ Measure SLAs that cover more than just

operational/ cost metrics, focus on performance

■ Operate GBS like an independent business

unit with P&L

■ Services as competitive as a third party

provider

Process

Excellence

■ Empower process owners to design and manage

end to end processes; hire black belts

■ Perform process benchmarking with peers

■ Regularly report productivity gains to

demonstrate GBS benefits

■ Process owners with complete ownership

■ At least 5% efficiency improvement YoY

■ Process optimization using lean/six sigma

expertise. Change management and

corporate gov to drive transformation agenda

Data and

Analytics

■ Invest in predictive analytics, state of art tools

■ Talent management tailored to D&A needs

■ Leverage third party services and resources

wherever possible

■ Provide services to GBS and across

functions to help drive better and faster

business decisions leading to better

outcomes

Desired State

Implementing a GBS operating model in GSK

What we do at GSK...

Pharmaceuticals

We develop and make medicines

to treat a range of conditions

including: respiratory diseases,

cancer, heart disease, epilepsy,

bacterial and viral infections

such as HIV and lupus, and

skin conditions like psoriasis.

Consumer Healthcare

We make innovative consumer

products in four categories of

Total Wellness, Skin Health,

Oral Care and Nutrition. Our

portfolio includes well-known

brands such as: Horlicks,

Panadol and Sensodyne.

Vaccines

We research and make

vaccines for children and

adults that protect against

infectious diseases, including:

influenza, rotavirus, cervical

cancer, measles, mumps,

rubella, hepatitis, polio,

tetanus and meningitis.

Implementing a GBS Operating model in GSK18

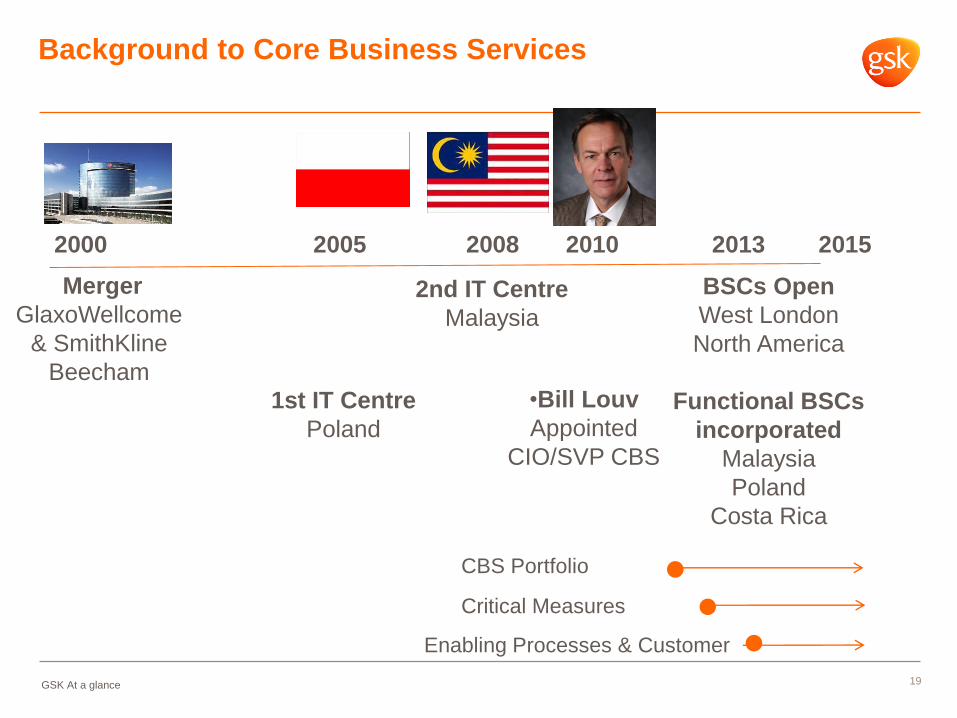

Background to Core Business Services

19GSK At a glance

2000 2005 2008 2010 2013 2015

Merger

GlaxoWellcome

& SmithKline

Beecham

1st IT Centre

Poland

2nd IT Centre

Malaysia

•Bill Louv

Appointed

CIO/SVP CBS

BSCs Open

West London

North America

Functional BSCs

incorporated

Malaysia

Poland

Costa Rica

CBS Portfolio

Critical Measures

Enabling Processes & Customer

Kuala Lumpur

Costa Rica

North Carolina

West LondonPoland

Philadelphia

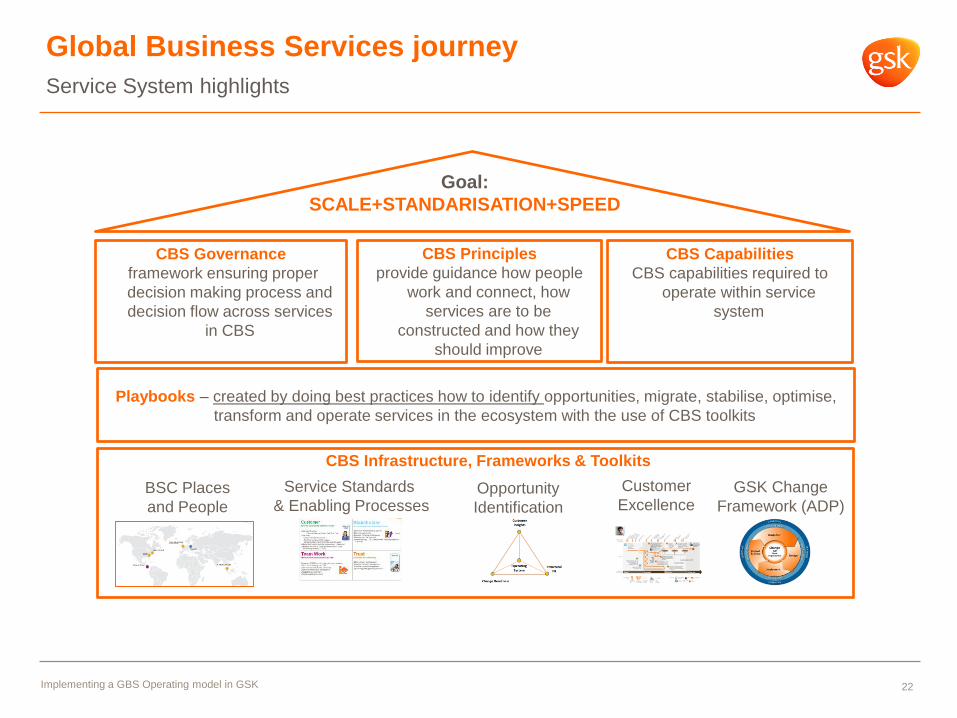

Global Business Services journey

Business

Partners and

Centres of

Excellence

Third Party

Providers

Captive

Business

Service

Centres

CBS – Core Business Services three-tier delivery model captive

Implementing a GBS Operating model in GSK 20

GBS Demographic Assessment

Total number of GBS employees in your company ~ 10000

Total number of GBS Centers 5 BSCs + 2-3 major locations

Regions of OperationsNorth America, Europe,

South America, Asia Pacific

Regions of Opportunity Middle East and Africa

Key Factors - GBS Assessment Industry Best Practices

Number of ERP

system4-5 1 – 3

Number of ERP

system instances>10 1 to 5

Functional areas

within GBS

Finance,

Indirect Procurement,

WREF

IT

>5

Continuing to Roll out global ERP

22

Goal:

SCALE+STANDARISATION+SPEED

CBS Principles

provide guidance how people

work and connect, how

services are to be

constructed and how they

should improve

CBS Governance

framework ensuring proper

decision making process and

decision flow across services

in CBS

CBS Capabilities

CBS capabilities required to

operate within service

system

Playbooks – created by doing best practices how to identify opportunities, migrate, stabilise, optimise,

transform and operate services in the ecosystem with the use of CBS toolkits

BSC Places

and People

Service Standards

& Enabling Processes Opportunity

Identification

GSK Change

Framework (ADP)

Customer

Excellence

CBS Infrastructure, Frameworks & Toolkits

Global Business Services journey

Service System highlights

Implementing a GBS Operating model in GSK

CBS Service Portfolio

Introduction to the CBS Service Portfolio

Purpose : A selection of reasons

Definition

– The CBS Service Portfolio is the agreed single list of services provided by CBS, described and

organised in a way which is meaningful to stakeholders and ultimately customers.

Benefits

– For Customers:

– It populates the Service Gateway with quality Service links for the GSK population.

– For Stakeholders:

– It enables greater visibility of CBS services and ultimately explains which services are

available

– For Service Line Owners and Service Owners:

– Can manage service information in one place within a common framework

– For CBS LT & Governance

– Supports the creation of a common and consistent language and approach for CBS

– Supports the move towards service-orientation and end to end services

– Clear accountability and success measures

CBS Service PortfolioCustomers & Service Owners defined the Portfolio in 2012. Continually Evolving

How many

Services?

How to describe

them?

What to call them?

How to group them?

Who owns what?

Focus Groups

One on One

Surveys

Task “sorting”

June 2012

7 Service Groups

36 Service Lines

280 Services

August 2014

13 Service Groups

49 Service Lines

300 Services

Introduction to the CBS Service Portfolio

Jan 2015

14 Service Groups

56 Service Lines

(10 Not CBS)

300+ Services

Service Portfolio Structure

Service Group - A logical grouping of Service Lines.

Service Line – Has an accountable owner although services

might be across functions.

Represents a logical grouping of like services (usually in the

eye of the Customer) to a significant number of customers

and/or in an area of significant value to GSK that resonates with

senior stakeholders.

Service - Has clear functional accountability

Represents a service provision to a significant

number of customers and is comprised of a

significant variety and volume of processes or tasks

required to deliver the Service based on the

customer needs and value to customers.

Service Gateway Entry : Links to customer

consumable resources. Policies, requests (e.g.

purchasing). Etc. 1000’s of entries exist with

accountable owners

Introduction to the CBS Service Portfolio

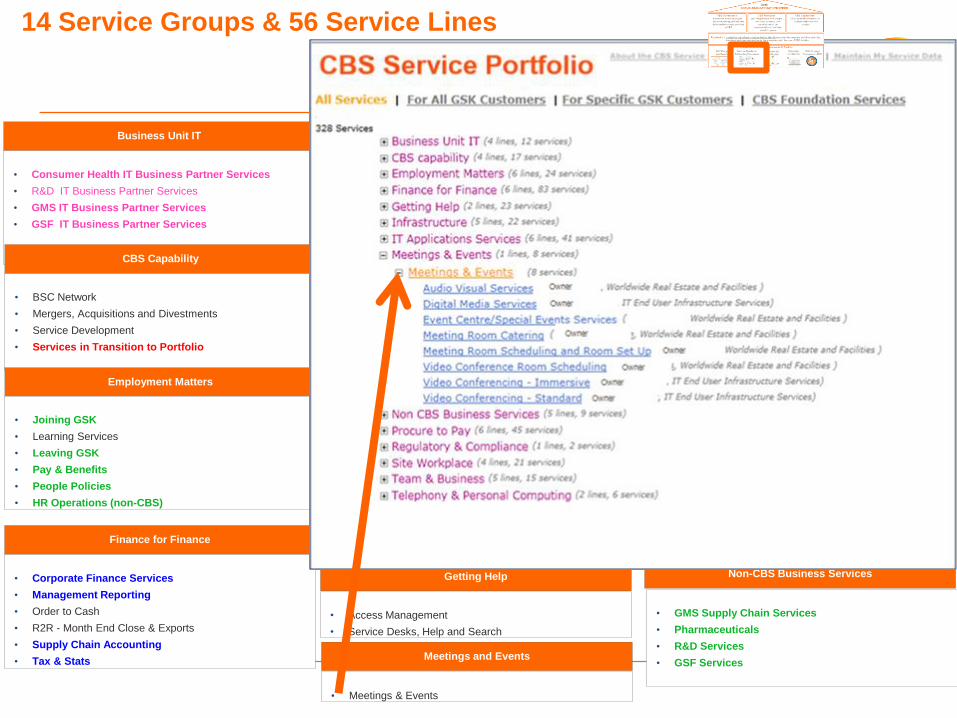

14 Service Groups & 56 Service Lines

• Consumer Health IT Business Partner Services

• R&D IT Business Partner Services

• GMS IT Business Partner Services

• GSF IT Business Partner Services

Business Unit IT

• Access Management

• Service Desks, Help and Search

Getting Help

• BSC Network

• Mergers, Acquisitions and Divestments

• Service Development

• Services in Transition to Portfolio

CBS Capability

• Business Analytics (Draft)

• Collaboration

• Controlled Document Management

• Data Management (Draft)

• Global Digital Services

Team and Business

Employment Matters

• Joining GSK

• Learning Services

• Leaving GSK

• Pay & Benefits

• People Policies

• HR Operations (non-CBS)

• Global ERP

• Global R&D Systems

• Global Support Function Systems

• Make, Test and Move Systems

• Market & Sell Systems

• Middleware/Integration (MW/I)

IT Application Services

• Corporate Finance Services

• Management Reporting

• Order to Cash

• R2R - Month End Close & Exports

• Supply Chain Accounting

• Tax & Stats

Finance for Finance

• Connect to Applications

• Connect to GSK Facilities

• Facilities Infrastructure Services

• IT Hosting Services

• IT System Security

Infrastructure

• Personal Computing & Mobile Devices

• Telephony

Telephony and Personal Computing

• Printing and Scanning

• Real Estate Services

• Scientific Services

• Workplace & Amenity Services

Site Workplace

• Meetings & Events

Meetings and Events

• Invoice to Pay

• Purchase of Goods & Services

• Sourcing Support

• Supplier Diversity

• Supplier Relationship Management

• Third Party Risk Management

Procure to Pay

• Compliance and Control (Assurance) (non-CBS)

Compliance and Assurance

• GMS Supply Chain Services

• Pharmaceuticals

• R&D Services

• GSF Services

Non-CBS Business Services

14 Service Groups & 56 Service Lines

• Consumer Health IT Business Partner Services

• R&D IT Business Partner Services

• GMS IT Business Partner Services

• GSF IT Business Partner Services

Business Unit IT

• Access Management

• Service Desks, Help and Search

Getting Help

• BSC Network

• Mergers, Acquisitions and Divestments

• Service Development

• Services in Transition to Portfolio

CBS Capability

• Business Analytics (Draft)

• Collaboration

• Controlled Document Management

• Data Management (Draft)

• Global Digital Services

Team and Business

Employment Matters

• Joining GSK

• Learning Services

• Leaving GSK

• Pay & Benefits

• People Policies

• HR Operations (non-CBS)

• Global ERP

• Global R&D Systems

• Global Support Function Systems

• Make, Test and Move Systems

• Market & Sell Systems

• Middleware/Integration (MW/I)

IT Application Services

• Corporate Finance Services

• Management Reporting

• Order to Cash

• R2R - Month End Close & Exports

• Supply Chain Accounting

• Tax & Stats

Finance for Finance

• Connect to Applications

• Connect to GSK Facilities

• Facilities Infrastructure Services

• IT Hosting Services

• IT System Security

Infrastructure

• Personal Computing & Mobile Devices

• Telephony

Telephony and Personal Computing

• Printing and Scanning

• Real Estate Services

• Scientific Services

• Workplace & Amenity Services

Site Workplace

• Meetings & Events

Meetings and Events

• Invoice to Pay

• Purchase of Goods & Services

• Sourcing Support

• Supplier Diversity

• Supplier Relationship Management

• Third Party Risk Management

Procure to Pay

• Compliance and Control (Assurance) (non-CBS)

Compliance and Assurance

• GMS Supply Chain Services

• Pharmaceuticals

• R&D Services

• GSF Services

Non-CBS Business Services

Owner

Owner

Owner

Owner

Owner

Owner

Owner

Owner

Selected solutions

28

CLICK

CHAT

CALL

TALK

Enhanced CBS Search

Easier navigation

External and Mobile compatibility

Single point of access

Central place to manage requests,

receive alerts

Service Gateway

Easily accessible via the Service Gateway

External & mobile chat capabilities Real-time help via online chat

Get help while continuing work

‘Live Help’

Live analyst assistance available via ‘Ask

CBS’ Single internal and external phone number

to access all services

‘Single Access Number’

Education on self-help

Provide service improvement feedback Face-to-face service

Get help and advice in person

Access to expert resource

‘Help Lounge’

Customer Experience Highlights

Implementing a GBS Operating model in GSK

Quarterly

Service Board

Monthly Service

Operations

Board

CBS Regional

Service Forums

Summary of CBS Service Governance Model

CBS Regional

Service ForumsCBS Regional

Service Forums

CBS Service Board - will be operated quarterly with

a very clear focus on service strategy and

performance oversight. The board will also look to

ensure we are focusing key ‘intervention’ resources on

the right priorities for CBS

Service Operations Board – will be ran monthly to manage

escalated service operational issues, be proactive around

reviewing the critical measures and act as sound board for

potential changes to the CBS service model i.e. ways of work

and CBS service offerings

SLO Regional Forums - operated where we have a

critical mass of service line owners and service managers.

They will look at ensuring we cross-pollinate best practice

between the services and identify common issues that

should be raised to the Ops Board.

Organisational momentum around Strategy

30

A3 Implement Common Service StandardsI. Performance Gaps and

Targets

IV.This Year’s Action Plan

II. Reflection on Previous

Activities

III. Rationale for This Year’s

Activities

V.Follow Up/Unresolved

Issues

III.Rationale for this year’s activities

V.Follow up / Unresolved Issues

.

II.Reflection on previous activities

I. Performance Gaps and Targets IV.This Year’s Action Plan

CBS?? 2014?? Strategy?? Deployment?? ?? -‐?? Summary?? Pack?? ?? Version?? 1.0?? February?? 2014??

A3: Transform Current

Services

LT Sponsor: Phil Priest

Owner: Neil Serjeant, Esteban Coronado

Contact: George Mitchell

50 % of CBS services in

BSCs - 2014

10 Lean Diagnostics -

2013

SPM deployed with variable

results

45 % of services in

BSCs - 2013

Most Finance

Migrations require

Stabilization

5 Service Lines stabilized, optimized or transformed by

December 2014

2013 2014

Goals Activities D J F M A M J J A S O N D

Creation of Play Books

Identify Opportunities

Assessment &

Prioritization

Migration

Stabilization

Optimization

Identify

opportunities

Stabilize FS Europe

Optimize ES

Opportunity 3 (? EIS)

Opportunity 4

Opportunity 5

= Completed Milestone = Missed Milestone = Future Milestone

2

Return

Date: Oct

13 A3 Transform Current Services

I. Performance Gaps and

Targets

II. Reflection on Previous

Activities

III. Rationale for This Year’s

Activities

IV.This Year’s Action

Plan

V.Follow Up/Unresolved

Issues1. Resourcing and capability for each initiative within A32. Buy in and alignment

a. Within CBS, e.g. SD vs SLO vs GPO.b. Within Service Development, e.g. this A3 vs

Programme Management vs Initiatives.c. Within Service Lines or Functions, e.g. SLOs vs

GPOs vs functional)3. How to design the Transformation Process (Transform Future

Services WIG) - Q2 2014 under an initiative4. How does this Strategic WIG work with the Strategic WIG on Asia

– potential future dependency depending on next two months on Asia

1. Service Lines in the BSCs are delivered at inconsistent levels of performance2. Need to deliver consistent benefits as part of the rationale of creating BSCsLead measures

1) % Services1) Baselined2) Planned3) Delivered

Lag measure1) % of services delivering targeted

improvementBenefits:1) Targeted services stabilized, optimized

and/or transformed.2) Improved Service Development project

alignment, project management and benefits realization

On-Track Target at Risk Target Missed

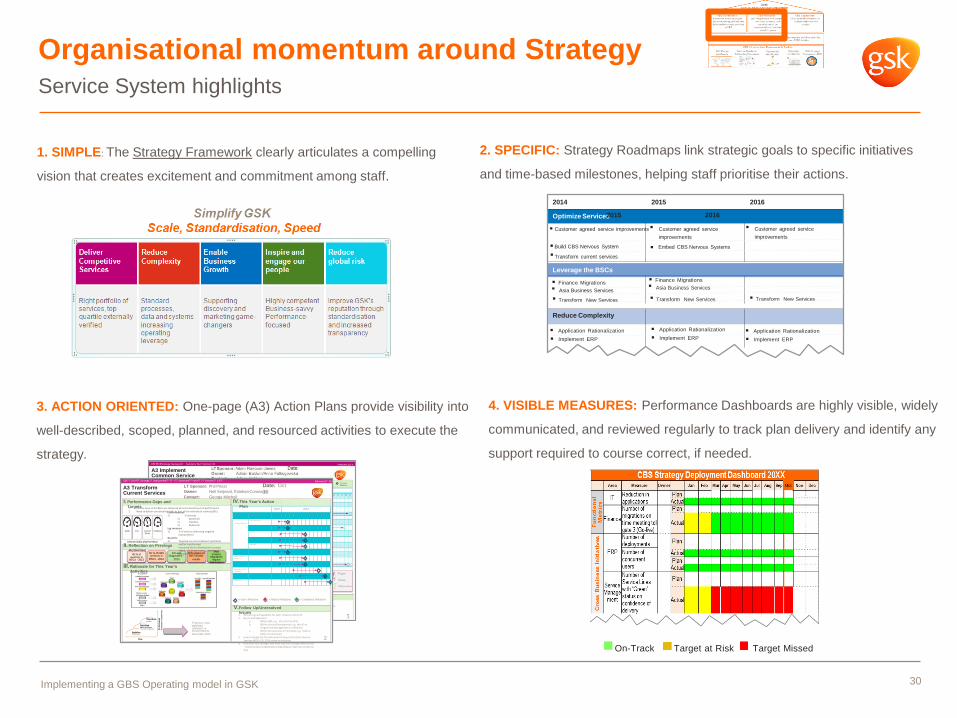

1. SIMPLE: The Strategy Framework clearly articulates a compelling

vision that creates excitement and commitment among staff.

2. SPECIFIC: Strategy Roadmaps link strategic goals to specific initiatives

and time-based milestones, helping staff prioritise their actions.

2014 2015 2016

Optimize Services

Customer agreed service improvements

■ Build CBS Nervous System Embed CBS Nervous Systems

Leverage the BSCs

Asia Business Services

Finance Migrations

Reduce Complexity

■ Customer agreed service

improvements

■ Customer agreed service

improvements

■

■

■ Transform current services

■

■Asia Business Services

Finance Migrations■

■

Transform New Services■ Transform New Services■ Transform New Services■

■ Application Rationalization

■ Implement ERP

■ Application Rationalization

■ Implement ERP

■ Application Rationalization

■ Implement ERP

2015 2016

3. ACTION ORIENTED: One-page (A3) Action Plans provide visibility into

well-described, scoped, planned, and resourced activities to execute the

strategy.

4. VISIBLE MEASURES: Performance Dashboards are highly visible, widely

communicated, and reviewed regularly to track plan delivery and identify any

support required to course correct, if needed.

Service System highlights

Implementing a GBS Operating model in GSK

31© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Breakout #4:

Show me the money:

Quantifying the cost and

value of moving up the

maturity curve

32© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

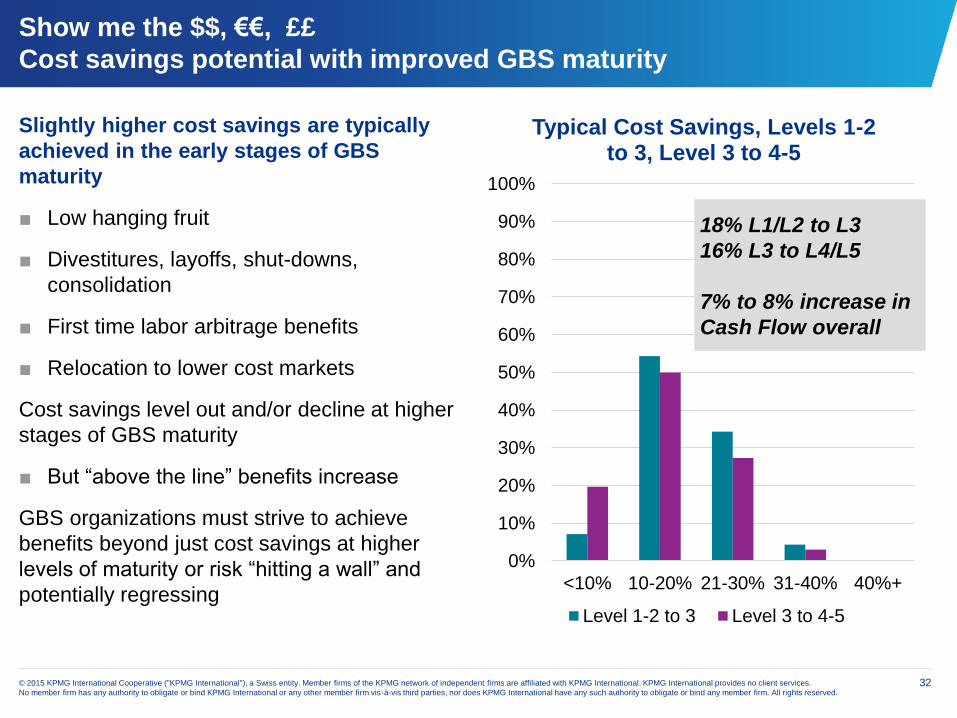

Show me the $$, €€, ££

Cost savings potential with improved GBS maturity

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

<10% 10-20% 21-30% 31-40% 40%+

Typical Cost Savings, Levels 1-2 to 3, Level 3 to 4-5

Level 1-2 to 3 Level 3 to 4-5

Slightly higher cost savings are typically

achieved in the early stages of GBS

maturity

■ Low hanging fruit

■ Divestitures, layoffs, shut-downs,

consolidation

■ First time labor arbitrage benefits

■ Relocation to lower cost markets

Cost savings level out and/or decline at higher

stages of GBS maturity

■ But “above the line” benefits increase

GBS organizations must strive to achieve

benefits beyond just cost savings at higher

levels of maturity or risk “hitting a wall” and

potentially regressing

18% L1/L2 to L3

16% L3 to L4/L5

7% to 8% increase in

Cash Flow overall

33© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Factors that drive cost savings

0% 10% 20% 30%

Labor arbitrage (captive)

Staff mix / spans of control

Rationalization of ERPplatforms

Scale economies

Rationalization of third partyproviders

Standardization &simplification

Labor arbitrage (outsourced)

Implementation of enablingtechnologies

Cross-functional processimplementation

Level 3 to 4-5 Level 1-2 to 3

■ Many factors drive cost savings as

GBS maturity increases

■ Labor arbitrage is predominant driver

for initial cost savings at lower levels

of maturity

■ Cross-functional process

implementation and end-to-end

process ownership drives savings as

organizations become more mature

■ Implementing enabling technologies

also important as maturity increases

34© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Beyond cost: Additional value drivers sought & achieved

1,00 2,00 3,00 4,00 5,00

Improving consistency of the employee experience

Drive improved cash flow or balance sheet performance

Better use and development of talent

Greater infrastructure scalability

Greater organizational flexibility

Improving consistency of the customer experience

Creating platform for innovation & continuous improvement

Increased quality of services provided to business

Transparency & greater control of financial / ops risks

Use of advanced predictive D&A tools to support GBS

Implementation of true end-to-end processes

Stronger governance and compliance

1=Low Importance, Very Unlikely achieved, 5=High importance, Very likely achieved

Importance 3 to 4-5 Importance 1-2 to 3

35© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Possible Case Study – How do we think of Benefits - $10B Firm

OH percentage Impacted

Saving Percentage

due to SS

Information & Technology 3.5%

L1 to L2: 20% to 25%

L4 to L5: 50% to 75%

Penetration by year – 25% up to

100% over 5 years

L1/ L2 to L3: 15% to 25%

……………..

L3 to L4/ L5: 50% + (cumulative)

Finance 1.5%

Human Resources 1.0%

Procurement 1.5%

Facilities 3%

Other indirect Cost 1.5%

$0 $200 000 000 $400 000 000 $600 000 000

Year 1

Year 2

Year 3

Year 4

Below Line Savings

L4 to L5 L3 to L4 L1/2 to L3

36© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Above line benefits can dwarf labor and outsourcing benefits

Above line benefits associated with cash flow increases, revenue growth, acquisition integration

associated with process improvement may more than double any hard core OH cost savings

2015 20192016 2017 2018

Principles: 2015 Critical Service Improvements

(Repeated from 2012, 2013 & 2014)

– Formal agreement of Improvements between CBS Service Line and

Customer/Stakeholder

– Measure/s to be improved

– Clear Targets with timeframes for delivery

– Clear operational measure definitions

– Transparency of progress

CBS and Critical Measures Programme

Voice of Customer Improvements (Customer Satisfaction)

– Mergers Acquisitions & Divestment engagements

– Global Digital services from 50% to 90% Customer Satisfaction

Cost reduction and avoidance

– Printing Services (2013) : 25 % Reduction in Total Cost of Ownership (TCO)

– Windows XP decommissioning accelerated to avoid additional cost of support

– Real Estate Rationalization – Year on Year Savings to CAPEX and OPEX

– 25% Reduction in fees for late Credit Card (Expense) payments

– Lab Services : 20% increase in Chemical Re-use

Service Improvement

– Networks : Reduce High Business Impact Outage hours by 15%

– Multiple examples of reduction in Backlogs (CRs), Cycle times & Issue Volumes

– Joiners & Leavers Right First Time (IT Accounts, Security Badges etc.) – Year on Year Improvements

– % Overdue Debt Reduction & Paid on Time measures

Other

– Site Services : Reduction in CO2 Emissions year on year

Both Effectiveness and Efficiency Measures – A Selection from 2013 & 2014

Presentation title 38

39© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Break out session #5:

What moves the needle:

Drivers and outcomes

What do you do first to

drive maturity and

business value?

40© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Why GBS matters to support corporate goals

■ Companies are looking at growth

again but want to use their cash in a

prudent manner.

■ Cost optimization and moving away

from non-core businesses are

primary business drivers at this time

■ Costs extraction remains a primary

value driver for many organizations,

yet many struggle to identify ways

to continue to optimize and improve

their operating models to deliver

greater benefits

DEALS & DEAL MAKERS

Rising Optimism Fuels Deal

Rebound

At the current pace, M&A volume for the full

year would exceed $3.7 trillion, making it the

second-biggest year in history

By Dana Cimilluca, Dana Mattioli and Shayndi Raice

April 8, 2015 8:18 p.m. ET

Takeovers are booming as companies gain

more confidence about the economy, use

stockpiles of cash to reach for future growth

and get boosts from low interest rates and the

surging stock market.

Source: http://www.wsj.com/articles/rising-optimism-fuels-deal-rebound-1428538721 –

4/9/2015

41© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Cost remains a priority for GBS organizations,

but value and innovation are also expected

42© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Mature strategy and service portfolio can drive GBS development

89% had a strong strategy function

92% had a large service portfolio

Of all GBS

with strong

process

ownership

83% had a strong strategy function

87% had a large service portfolio

Of all GBS

with strong

commercial

orientation

89% had a strong strategy function

86% had a large service portfolio

Of all GBS

with strong

talent

management

92% had a strong strategy function

90% had a large service portfolio

Of all GBS

with strong

governance

processes

43

Transform

Optimise

Continuous improvement

Culture

Collaboration

Equipment &

Safety

Future services –beyond the current scope

Transform end to end service to drive

enterprise value

Embed capabilities and optimise end-to-end

process efficiency to drive business value

Provide expert consultancy on services and

processes to remove variation and complexity

Practicing ADP, innovative, vibrant, service oriented and

rewarding culture

Provide collaborative management support structure,

technologies and tools with smart working setup

Provide necessary office equipment and take additional steps to

ensure safety

Implementing a GBS Operating model in GSK

Business Service Centres offering

Future services –beyond the current scope

44

Business Service Centres as Conversion machineses

Assessment

and

Design

Migrate

Services to

the BSC

Operate

Service

Service

IN

Service

OUT

Convert

Service

Outsource /

Keep it in-

house

Identify which

services for

conversion

Migrate

selected

services /

functions to

the BSCs

Continuous

Improvement

Commoditise,

Standardize,

Simplify,

Eliminate,

Lean it

Prepare

service for

outsourcing

Service Lifecycle

Implementing a GBS Operating model in GSK

45© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Roundtable #1:

Building a better GBS to

Support Higher Level

Objectives – Moving

beyond cost reduction

• Brand Support and Risk

Reduction

• M & A support

• Process efficiency

• Customer Experience and

Interaction

46© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Beyond cost savings

Unlock the Power of

Data & Analytics

■ Increase sophistication and

centralize DA (remove duplicate

systems, add tracking where

needed, one ERP system,

process requests faster, ability to

track process breakdown utilizing

analytics, identify missing process

controls)

■ Common platforms and common

processes and capabilities

Mitigate Overall Business Risk &

Ensure Compliance

■ Proactive vs reactive response to

regulatory demands

■ Global repository of regulatory

requirements (tracking, reporting,

and process driven common

response to regulatory mandates)

Achieve Excellence & Consistency

in Customer Experience

■ Ensure consistent experience to

the customer (uniform and

consistent methods and platforms

to respond to customer requests)

■ Utilize VOC and validate using

internal DA information

■ Implement user satisfaction

Indexes

Build Internal Repository of High

Quality Talent

■ Build professionals within GBS

that can be sourced out to the

other business functions and

train/provide services – source of

internal high quality talent

■ Establish a clearer career path for

GBS professionals

■ Leverage skills & build training

Increase Effectiveness

& Ability to Scale

■ Need to be able to provide

effective services, effective

outcomes. i.e., Integrate project

management to deploy lean six

sigma and continuous

improvement and effectiveness of

delivery goes up due to

centralized leadership of the

different functions

Establish a Consistent Brand

Experience

■ Improve competitive position

■ Support consistency of global

brand experience

Enhance Sophistication &

Collaboration

■ Mind shift in terms of

professionalism. GBS

organizations have much higher

level of expectation in terms of it

being a provider of choice, and a

lever for cost competitiveness

■ Share skills and knowledge

across the organization

■ End to end process

standardization for non

standardized products/services

and business units

■ Process owners identification and

accountability

■ Process controls and continues

process improvement

■ Process automation

Drive Process Excellence

47© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

4

Key value drivers reported

Align the operating model for

efficiency and effectiveness

– Relative Importance –

Drive growth & realize

synergies from acquisitionsHighLow

Drive growth in

emerging markets2Low

Low

Optimize the global

operations footprint

4Low

Connect, collaborate and mine

data to drive greater insightLow 3

Protect the Brand and foster a

common customer experienceLow 2

Drive process excellence

and collaborationLow 4

Build internal repository of

high quality talentLow 3

4

2

2

4

2

4

High

High

High

High

High

High

High

Europe Nordic

3

3

3

48© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

One of the strongest

conclusions from the

research is that ‘top

performers’ – companies

driving the strongest growth

and profitability have cracked

the code on leveraging

technology and talent more

effectively than their peers.

Investments in the right technology and talent contribute

to growth

■ Demonstrate Competitive Differentiation

■ Transform Data into Significant Value

■ Leverage Emerging Technology

■ Accelerate Product Development Cycles

■ Create a ‘Market of One’

■ Create New Roles to Accelerate Growth

■ Maintain a 360˚ View of Competitive Threats

■ Extraordinary Ability to Attract & Retain Talent

How to think of value added benefits:

Factors Driving Growth

49© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Where’s the value in the future?

LABOR ARBITRAGE

CHARACTERISTICS

LABOR AUTOMATION

CHARACTERISTICS

cost take out for relevant functions

40%-75%15%-30%

Model is scalable and is

largely independent of labor growth

Transformative– New way of

doing business

Access to“Rocket Scientists”

who can codify manual processes

Revenue/Profit NOT correlated

to People

cost take out

Model is scalable to the extent

that you can scale labor

Custom/complex, legacy:our mess for less

Access to Low Cost Labor necessary

to provide continuous value

Revenue/Profit correlated

to People

50© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The Four Sectors – Everyone does two

M and A – Tone

• Many industries are

consolidating including Pharma

• GBS as leverage point for time to

benefit

• Increase ROI

• GBS Driving new opportunities –

the art of the possible

Brand and Risk – Don

• GBS as underlying service platform

• How do we quantify brand and risk

benefits

• Importance of standardization across

all geographies

• Underlying importance of data and

analytics in GBS to support brand

Customer Experience and Sales

Support – Joakim

• Marketing and sales will spend

more on technology services

than IT in 2 years

• How does GBS move from back

office to front office

• What services move first

• What are the benefits to overall

customer experience and

marketing strategy

Process Excellence – Lars

• Role of process owners beyond GBS

in driving process excellence

• Benefits of process ownership and

excellence to support retained

function delivery such as product

delivery and development

• Overall corporate reorientation when

GBS drives process ownership

51© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

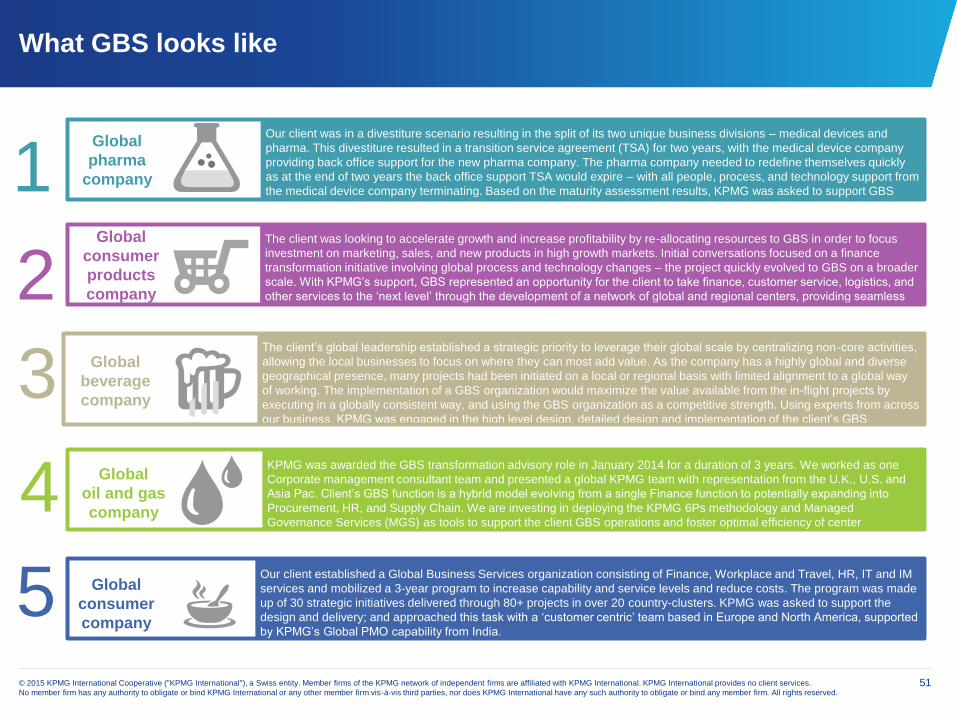

Our client was in a divestiture scenario resulting in the split of its two unique business divisions – medical devices and

pharma. This divestiture resulted in a transition service agreement (TSA) for two years, with the medical device company

providing back office support for the new pharma company. The pharma company needed to redefine themselves quickly

as at the end of two years the back office support TSA would expire – with all people, process, and technology support from

the medical device company terminating. Based on the maturity assessment results, KPMG was asked to support GBS

transformation initiatives across enabling technology, services portfolio, process ownership & optimization, and talent

management.

Global

pharma

company1The client was looking to accelerate growth and increase profitability by re-allocating resources to GBS in order to focus

investment on marketing, sales, and new products in high growth markets. Initial conversations focused on a finance

transformation initiative involving global process and technology changes – the project quickly evolved to GBS on a broader

scale. With KPMG’s support, GBS represented an opportunity for the client to take finance, customer service, logistics, and

other services to the ‘next level’ through the development of a network of global and regional centers, providing seamless

global services to the client’s growing global enterprise.

Global

consumer

products

company2The client’s global leadership established a strategic priority to leverage their global scale by centralizing non-core activities,

allowing the local businesses to focus on where they can most add value. As the company has a highly global and diverse

geographical presence, many projects had been initiated on a local or regional basis with limited alignment to a global way

of working. The implementation of a GBS organization would maximize the value available from the in-flight projects by

executing in a globally consistent way, and using the GBS organization as a competitive strength. Using experts from across

our business, KPMG was engaged in the high level design, detailed design and implementation of the client’s GBS

organization, working on all aspects of the operating model.

Global

beverage

company3KPMG was awarded the GBS transformation advisory role in January 2014 for a duration of 3 years. We worked as one

Corporate management consultant team and presented a global KPMG team with representation from the U.K., U.S. and

Asia Pac. Client’s GBS function is a hybrid model evolving from a single Finance function to potentially expanding into

Procurement, HR, and Supply Chain. We are investing in deploying the KPMG 6Ps methodology and Managed

Governance Services (MGS) as tools to support the client GBS operations and foster optimal efficiency of center

operations.

Global

oil and gas

company4Our client established a Global Business Services organization consisting of Finance, Workplace and Travel, HR, IT and IM

services and mobilized a 3-year program to increase capability and service levels and reduce costs. The program was made

up of 30 strategic initiatives delivered through 80+ projects in over 20 country-clusters. KPMG was asked to support the

design and delivery; and approached this task with a ‘customer centric’ team based in Europe and North America, supported

by KPMG’s Global PMO capability from India.

Global

consumer

company5

What GBS looks like

52© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

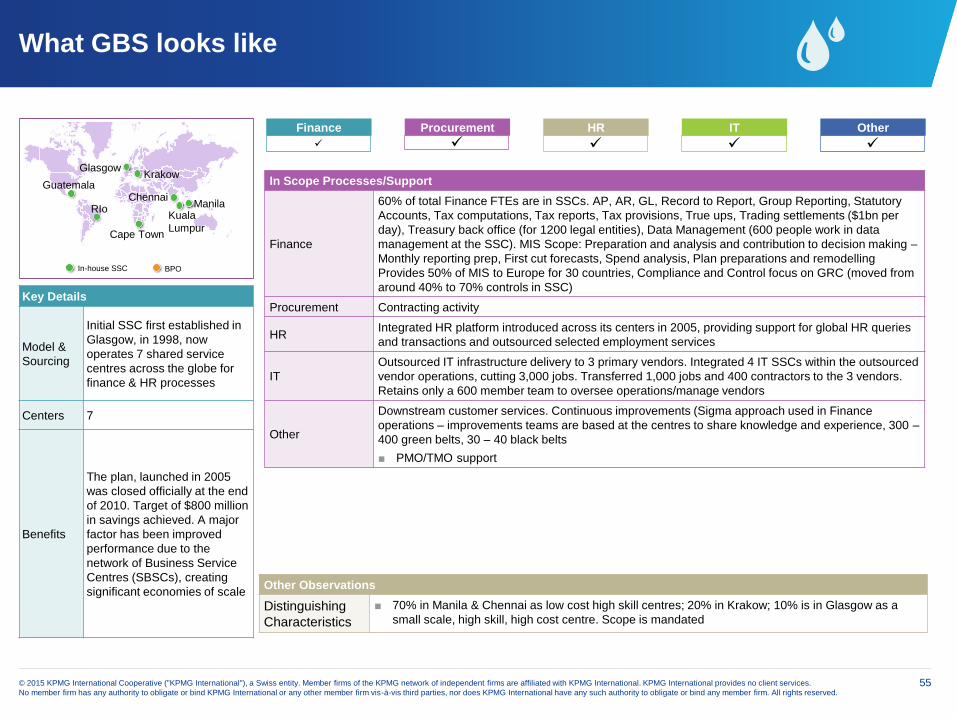

Key Details

Model &

Sourcing

Hybrid model (captive and

outsourced)

Centers5 (BPO – San Jose, Dalian, Naga,

Krakow, COE –Chicago)

Rationale

Developed a Global Finance, HR,

and Ops strategy and supporting

Target Operating Model (TOM) to

support the company as it

transitions away from the existing

TSA support.

Benefits

■ Leading practice operating

model, contracting structure (for

outsourcing), process design

and desktop procedures

■ Deep functional end-to-end

process and training

knowledge.

Themes

Current state environment was

fragmented and disparate highly

decentralized and non-

standardized.

NagaDalian

Procurement

Finance

HR

IT

Other

In Scope Processes/Support

Finance

■ Commercial Finance Strategy & Role/Org. Design

■ Financial Services and COE Deployment

■ Intl. & Fed. Tax, Income/Franchise, GTC CoE Ops.

■ Finance TOM Design and Implementation

■ Outsourcing Governance COE

■ Finance and Ops Training Strategy/Design/ Development

■ Finance COE & Shared Services

Procurement

■ P2P

■ Alignment of people/process/technology within the

procurement function

■ Process design of “direct” and “in-direct”

procurement/standardization/documentation of SOPs

HR■ Strategy/TOM development

■ Organizational realignment and hiring of new FTEs

■ HR/Payroll Change Management

■ HR/Payroll Outsourcing (NgA)/ Implementation

IT

(localization)

■ Application Alignment/Rationalization

■ Concur T&E and Payroll IT Deployment Support

■ Controls Framework

■ Finance/Payroll Application Rationalization &

Deployment Planning

■ Ops TOM/SAP Process Alignment &Documentation

■ Finance TOM/SAP Process Alignment and

Documentation/Technology Support

■ E2E Testing/Simulation/User Readiness

■ SAP Process (US/PR) Documentation

■ New Global ERP System

■ Operations Technology Support

Other

■ Bus. Supp. TOM development/Process Design

■ Outsourcing (IBM)

■ Bus. Supp. Process/ Documentation Governance

■ Bus. Supp. Training Strategy/Design/Development

■ SAP Remediation

■ Bus. Supp. Control Framework

■ E2E Testing, Simulation and User Readiness

■ Implementation PMO/Hypercare

■ Tax Strategy/TOM/Process Development

■ Outsourcing Governance Model Design & Develop

■ Outsourcing COE Design & Deploy

■ Managed Governance Services

■ Ops Strategy/ TOM Development/ Process Design

■ Trade Compliance

■ Regulatory Technology Enablement

■ Regulatory Process Optimization

■ Regulatory Project Management

■ Income/Franchise Tax, Direct/Indirect Tax TOM

■ Deploy centrally managed/leveraged, standard process

via Outsourcing, Shared Services & CoEs across Finance,

Ops and HR

■ User Stability/Process Remediation

Chicago

San Jose

Krakow

Global or Regional Centers Planned Additional Sites

Other Observations

Governance ■ End-to-end design and development of process and outsourcing governance.

Distinguishing

Characteristics

■ 2 year TSA to support technology and process infrastructure with former parent organization created urgency

for implementation.

■ Current state environment was fragmented and disparate (organization, processes, technology platforms),

highly decentralized/non-standardized

What GBS looks like

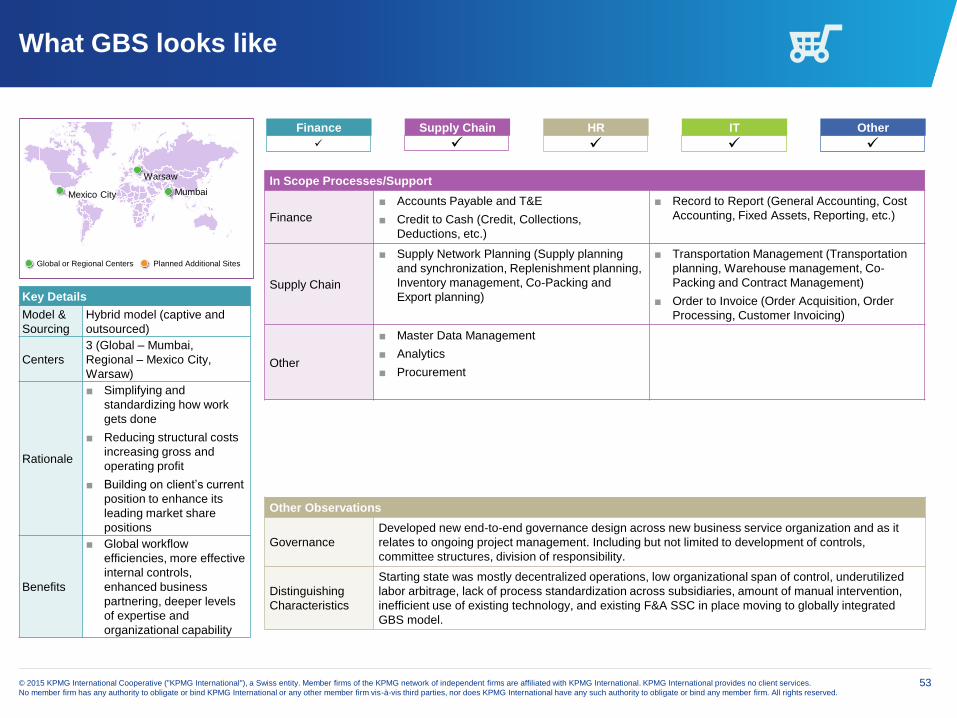

53© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Key Details

Model &

Sourcing

Hybrid model (captive and

outsourced)

Centers

3 (Global – Mumbai,

Regional – Mexico City,

Warsaw)

Rationale

■ Simplifying and

standardizing how work

gets done

■ Reducing structural costs

increasing gross and

operating profit

■ Building on client’s current

position to enhance its

leading market share

positions

Benefits

■ Global workflow

efficiencies, more effective

internal controls,

enhanced business

partnering, deeper levels

of expertise and

organizational capability

Mexico City

Warsaw In Scope Processes/Support

Finance

■ Accounts Payable and T&E

■ Credit to Cash (Credit, Collections,

Deductions, etc.)

■ Record to Report (General Accounting, Cost

Accounting, Fixed Assets, Reporting, etc.)

Supply Chain

■ Supply Network Planning (Supply planning

and synchronization, Replenishment planning,

Inventory management, Co-Packing and

Export planning)

■ Transportation Management (Transportation

planning, Warehouse management, Co-

Packing and Contract Management)

■ Order to Invoice (Order Acquisition, Order

Processing, Customer Invoicing)

Other

■ Master Data Management

■ Analytics

■ Procurement

Other Observations

Governance

Developed new end-to-end governance design across new business service organization and as it

relates to ongoing project management. Including but not limited to development of controls,

committee structures, division of responsibility.

Distinguishing

Characteristics

Starting state was mostly decentralized operations, low organizational span of control, underutilized

labor arbitrage, lack of process standardization across subsidiaries, amount of manual intervention,

inefficient use of existing technology, and existing F&A SSC in place moving to globally integrated

GBS model.

Mumbai

Global or Regional Centers Planned Additional Sites

Supply Chain

Finance

HR

IT

Other

What GBS looks like

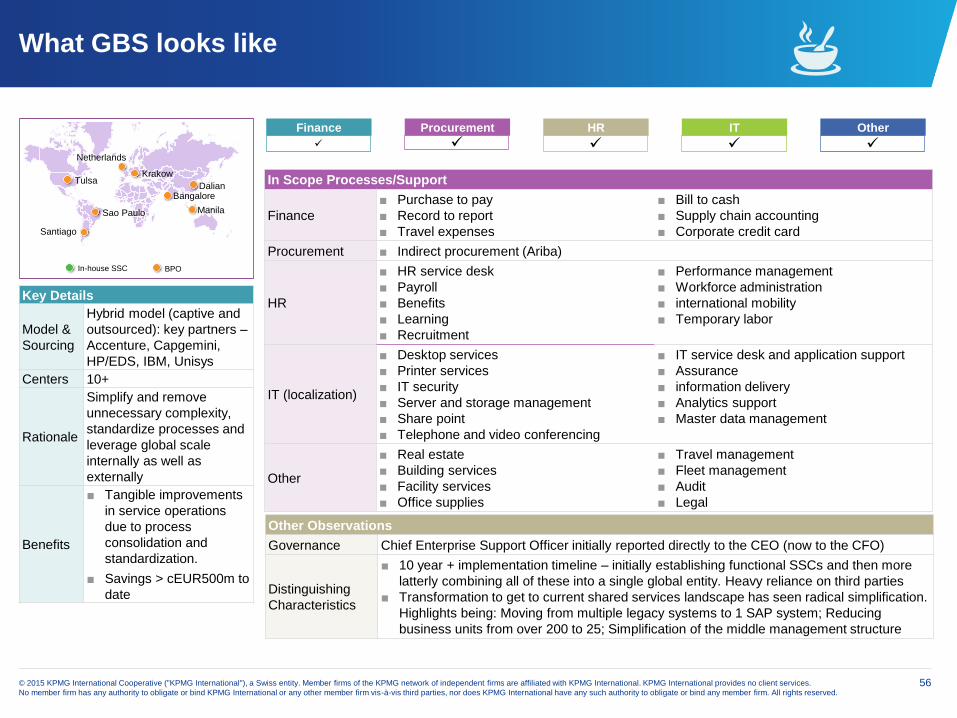

54© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Key Details

Model &

Sourcing

Hybrid model (captive and

outsourced)

Centers 3

Rationale

Development of a GBS

organization as a competitive

strength, with the

implementation of three

centers around the globe.

Benefits

■ Greater focus on

commercial activities by

markets

■ Enhanced information to

support decision making

■ Professional high quality

services

■ New/deeper functional

services

■ Lower cost

and clear transparency

India

Latin America

Europe In Scope Processes/Support

Finance

■ S2P (Finance) e.g., accounts payable, T&E

■ O2C (Finance) e.g., credit management,

collections

■ R2R

■ MDM

Procurement■ S2P (Procurement) e.g., contract and

catalogue management

■ Supply chain

HR

■ Payroll and benefits

■ Recruitment

■ Learning & Development

■ Training

■ Change management

■ Communication plans

IT■ Enabling IT for service delivery

■ Supporting multiple technology initiatives

■ Integrated information technology framework

Other

■ Standardization of E2E processes

■ O2C Front end (e.g., Telesales, Customer

contact)

■ Analytics and insights

■ Service management and governance

■ Support centre (service desk)

■ Business case development