Game changer

40

are South Africa’s shale gas hopes built on a house of cards? GAME CHANGER or GAME OVER? KAROO SHALE GAS

-

Upload

jillian-bauer -

Category

Documents

-

view

52 -

download

0

description

or GAME OVER?. Game changer. KAROO SHALE GAS. a re South Africa’s shale gas hopes built on a house of cards?. I am not a scientisT ENGINEER, ECONOMIST, OR LAWYER. KICK-OFF POINT, OBJECTIVE & FOCUS TODAY. - PowerPoint PPT Presentation

Transcript of Game changer

are South Africa’s shale gas hopes built on a house of cards?GAME CHANGER or GAME OVER?

KAROO SHALE GAS

I AM NOT A SCIENTIST ENGINEER, ECONOMIST, OR LAWYER

KICK-OFF POINT, OBJECTIVE & FOCUS TODAY

Global Decisions are being made and energy policy being formed on a foundation of hype, speculation and desperation

Leaders … are convinced technology … US .. answer to energy, jobs, revenue and Co2 problems - (for those who believe in such a thing as climate change)

I’ll spend time touring the US with you. Why? Because it’s stats, promises and hype from US shale gas promoters that have covered our leaders eye’s with wool

I intend to inform South Africa’s leaders via this medium – or in court if we have to

And I present to you the same caveat with which I greeted you last year

LET’S GET STARTED

UNEQUIVOCALLY PRESIDENT BARACK OBAMAJANUARY 25TH 2012

‘We have a supply of natural gas that can last America nearly 100 years, and my administration will take every possible action to safely develop this energy.’

BULLISH: ANC SECRETARY GENERAL GWEDE MANTASHE

ANC tired of talking - OLEBOGENG MOLATLHWA | Times Live 23 July, 2013

The government will forge ahead with contentious projects that it claims will kick-start the stuttering economy - even if it is taken to court.

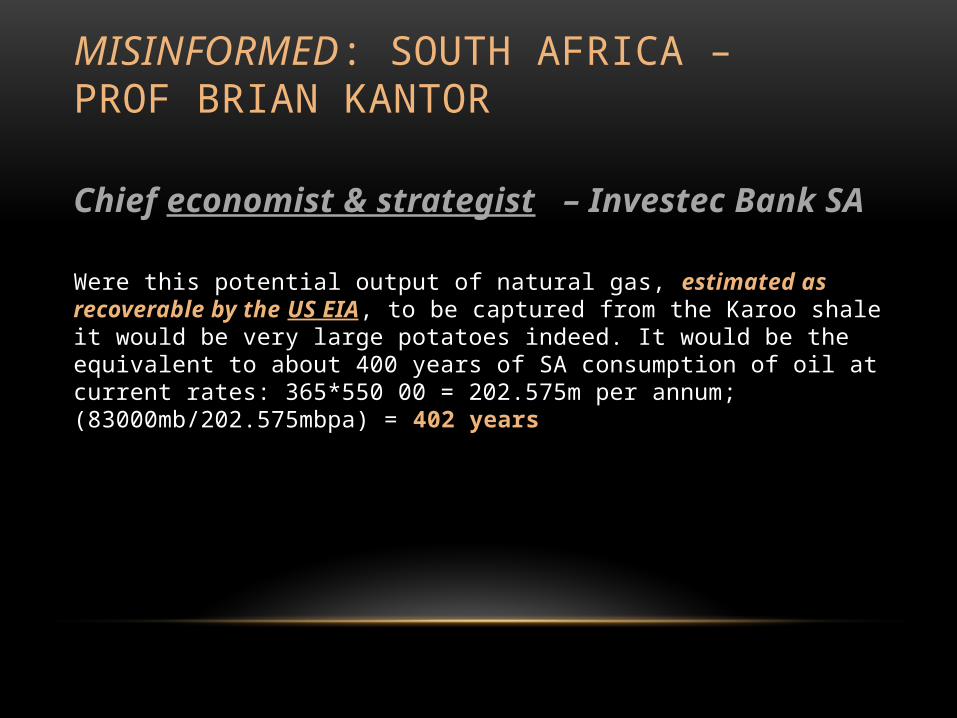

MISINFORMED: SOUTH AFRICA – PROF BRIAN KANTOR

Chief economist & strategist – Investec Bank SA

Were this potential output of natural gas, estimated as recoverable by the US EIA, to be captured from the Karoo shale it would be very large potatoes indeed. It would be the equivalent to about 400 years of SA consumption of oil at current rates: 365*550 00 = 202.575m per annum; (83000mb/202.575mbpa) = 402 years

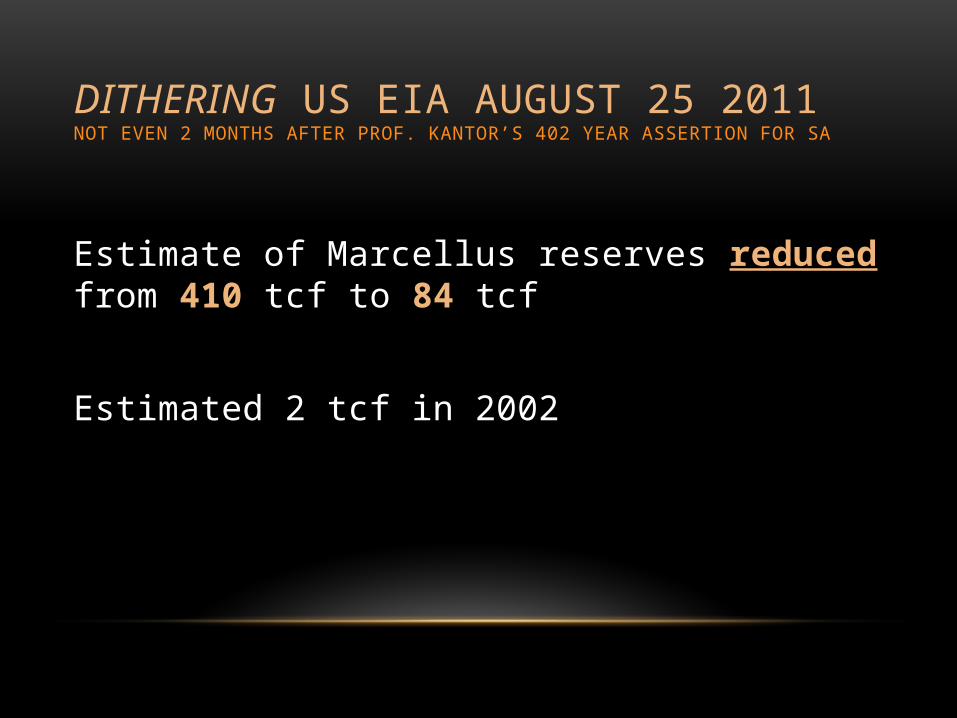

DITHERING US EIA AUGUST 25 2011NOT EVEN 2 MONTHS AFTER PROF. KANTOR’S 402 YEAR ASSERTION FOR SA

Estimate of Marcellus reserves reduced from 410 tcf to 84 tcf

Estimated 2 tcf in 2002

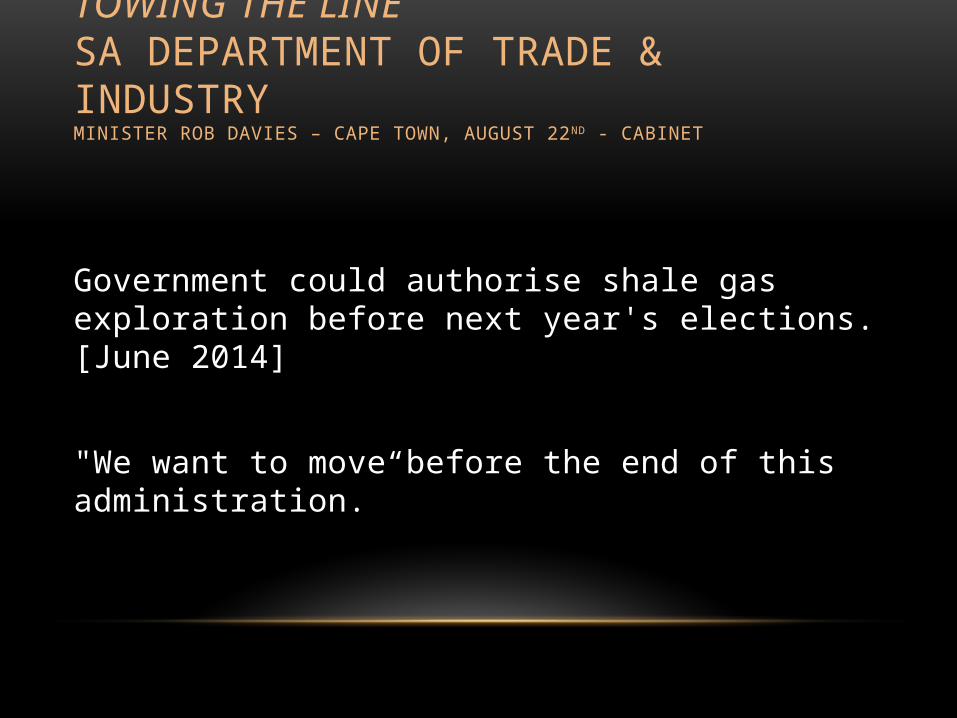

TOWING THE LINESA DEPARTMENT OF TRADE & INDUSTRYMINISTER ROB DAVIES – CAPE TOWN, AUGUST 22ND - CABINET

Government could authorise shale gas exploration before next year's elections. [June 2014]

"We want to move before the end of this administration.”

SO WHO IS BEHIND THIS MISINFORMATION? AND WHY?

THE SHALE GAS PROMOTERS

Aubrey McClendon (ex)CEO – Chesapeake Energy

T. Boone Pickens – Oil and gas billionaire and NGV proponent

Dan Yergin – Chairman IHS CERA (consultants to oil and gas)

Terry Engelder – PhD – Penn State University

Rex Tillerson – CEO Exxon

Tony Hayward (ex)CEO BP

Professors Timothy Considine and Robert Watson – Penn State

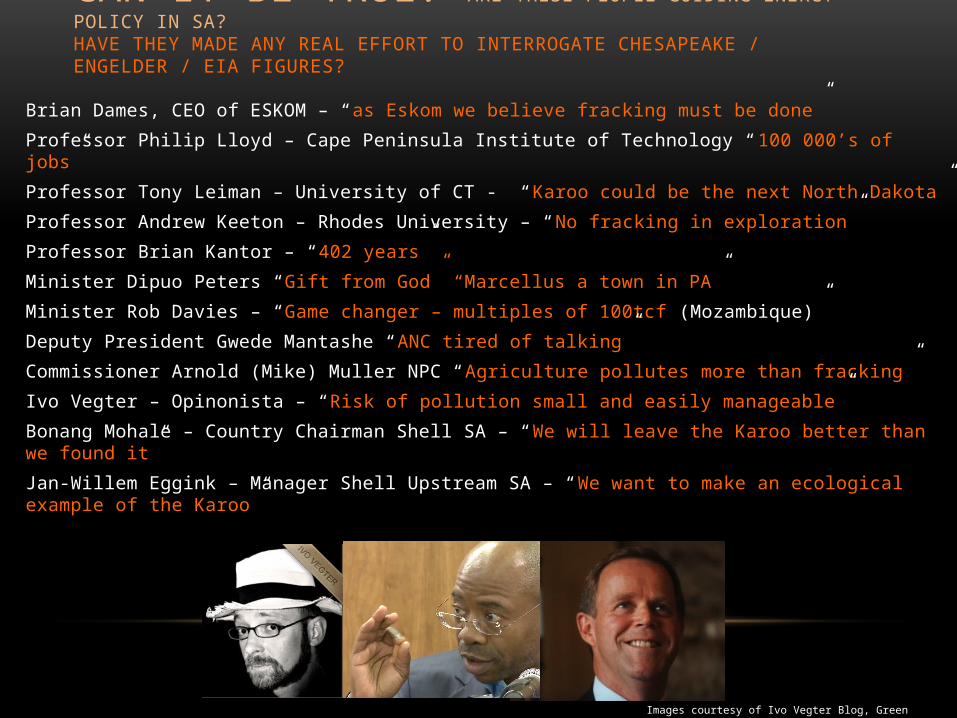

CAN IT BE TRUE? ARE THESE PEOPLE GUIDING ENERGY POLICY IN SA?HAVE THEY MADE ANY REAL EFFORT TO INTERROGATE CHESAPEAKE / ENGELDER / EIA FIGURES?

Brian Dames, CEO of ESKOM – “as Eskom we believe fracking must be done”

Professor Philip Lloyd – Cape Peninsula Institute of Technology “100 000’s of jobs”

Professor Tony Leiman – University of CT - “Karoo could be the next North Dakota”

Professor Andrew Keeton – Rhodes University – “No fracking in exploration”

Professor Brian Kantor – “402 years”

Minister Dipuo Peters “Gift from God” “Marcellus a town in PA”

Minister Rob Davies – “Game changer – multiples of 100tcf (Mozambique)”

Deputy President Gwede Mantashe “ANC tired of talking”

Commissioner Arnold (Mike) Muller NPC “Agriculture pollutes more than fracking”

Ivo Vegter – Opinonista – “Risk of pollution small and easily manageable”

Bonang Mohale – Country Chairman Shell SA – “We will leave the Karoo better than we found it”

Jan-Willem Eggink – Manager Shell Upstream SA – “We want to make an ecological example of the Karoo”

Images courtesy of Ivo Vegter Blog, Green rennaisance, RoyalDutch PLC.com

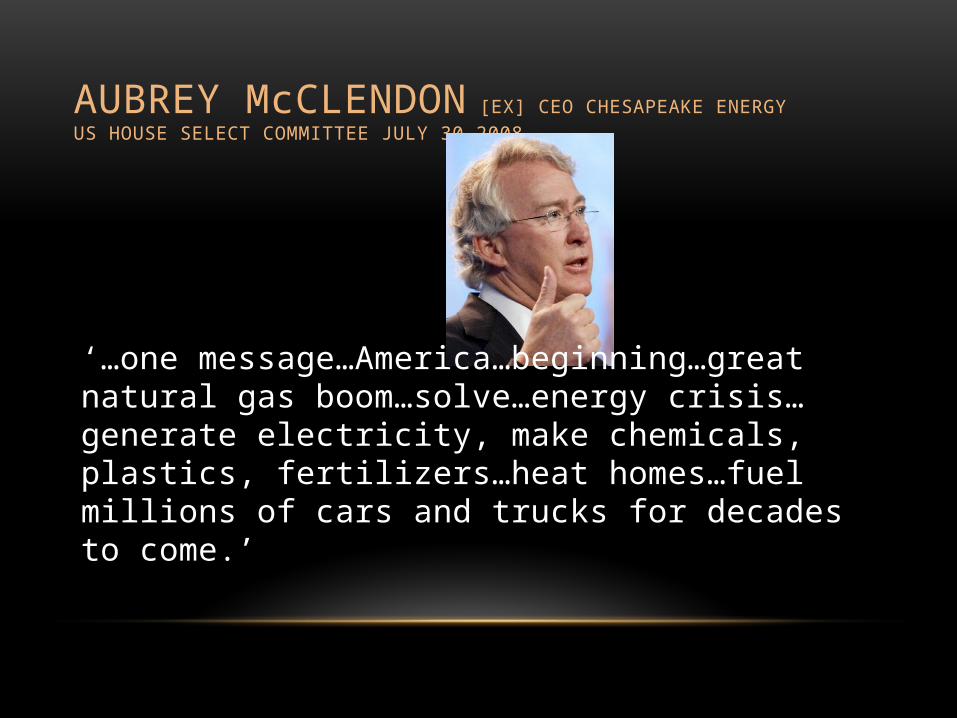

AUBREY McCLENDON [EX] CEO CHESAPEAKE ENERGYUS HOUSE SELECT COMMITTEE JULY 30 2008

‘…one message…America…beginning…great natural gas boom…solve…energy crisis…generate electricity, make chemicals, plastics, fertilizers…heat homes…fuel millions of cars and trucks for decades to come.’

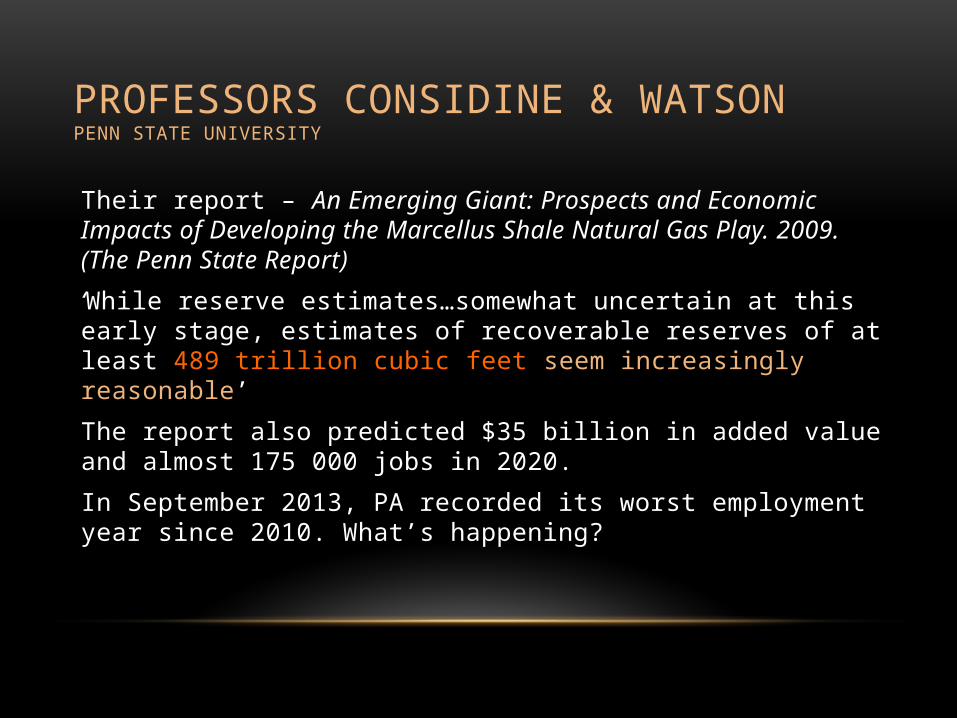

PROFESSORS CONSIDINE & WATSONPENN STATE UNIVERSITY

Their report – An Emerging Giant: Prospects and Economic Impacts of Developing the Marcellus Shale Natural Gas Play. 2009. (The Penn State Report)

‘While reserve estimates…somewhat uncertain at this early stage, estimates of recoverable reserves of at least 489 trillion cubic feet seem increasingly reasonable’

The report also predicted $35 billion in added value and almost 175 000 jobs in 2020.

In September 2013, PA recorded its worst employment year since 2010. What’s happening?

DAN YERGIN – AN INDUSTRY ADVOCATEPULITZER PRIZE WINNER, FORMER HARVARD PROFESSOR AND CHAIRMAN OF IHS CERA

As environmental concerns increasingly threatened multi-billion dollar investments the need for a credible industry advocate became vital. Dan Yergin is that man.

He promotes the ‘shale gale’ as “simply the most significant energy innovation so far this century.”

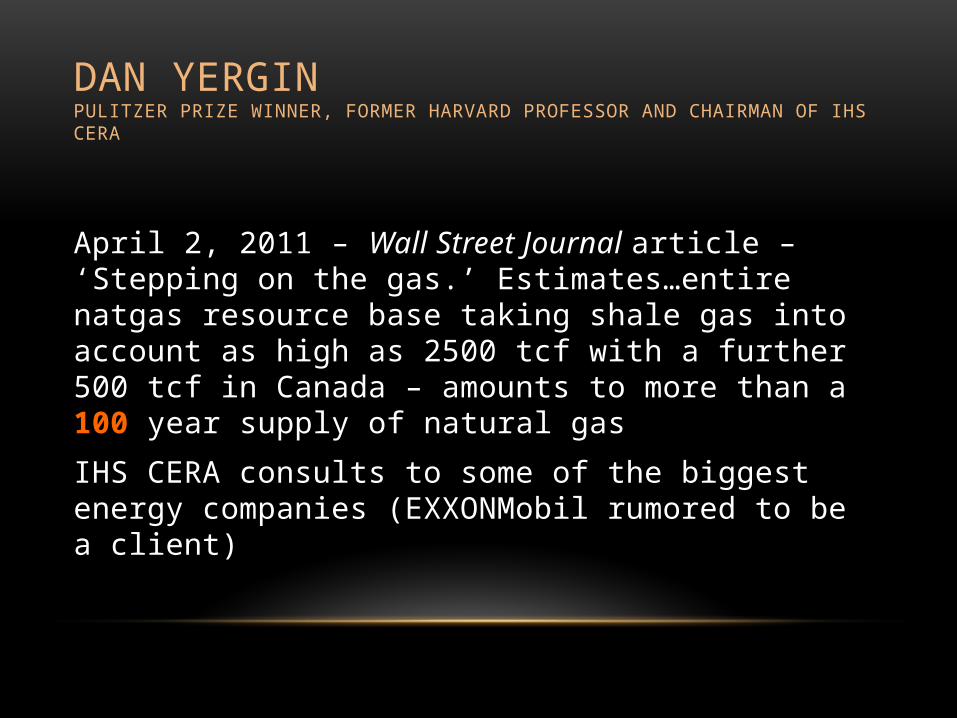

DAN YERGINPULITZER PRIZE WINNER, FORMER HARVARD PROFESSOR AND CHAIRMAN OF IHS CERA

April 2, 2011 – Wall Street Journal article – ‘Stepping on the gas.’ Estimates…entire natgas resource base taking shale gas into account as high as 2500 tcf with a further 500 tcf in Canada – amounts to more than a 100 year supply of natural gas

IHS CERA consults to some of the biggest energy companies (EXXONMobil rumored to be a client)

DAN YERGIN AND CERA IN CONTEXT

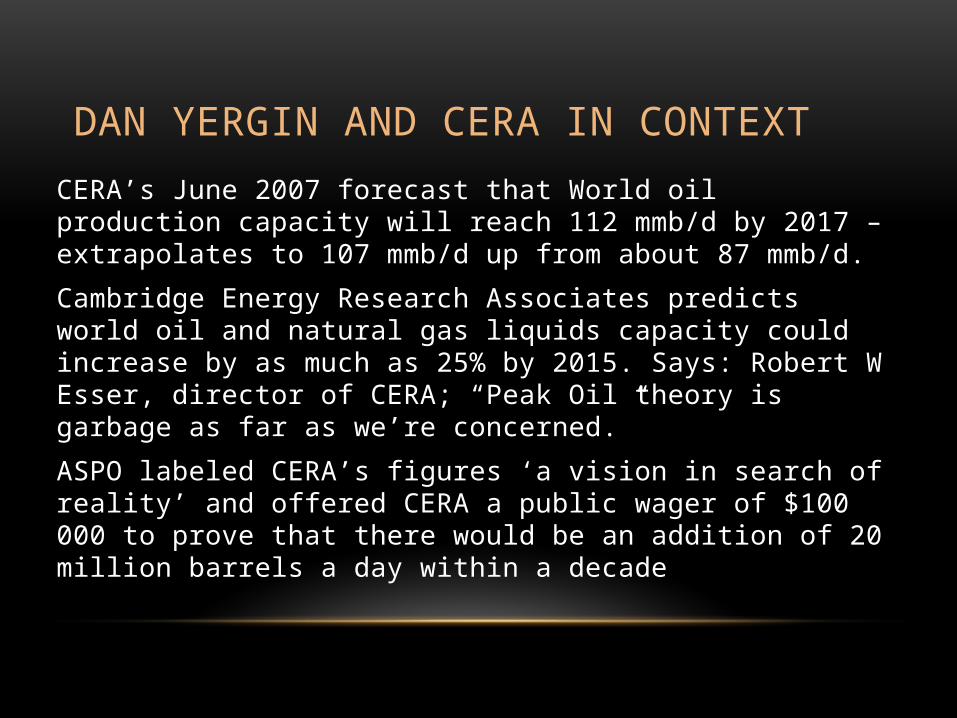

CERA’s June 2007 forecast that World oil production capacity will reach 112 mmb/d by 2017 – extrapolates to 107 mmb/d up from about 87 mmb/d.

Cambridge Energy Research Associates predicts world oil and natural gas liquids capacity could increase by as much as 25% by 2015. Says: Robert W Esser, director of CERA; “Peak Oil theory is garbage as far as we’re concerned.”

ASPO labeled CERA’s figures ‘a vision in search of reality’ and offered CERA a public wager of $100 000 to prove that there would be an addition of 20 million barrels a day within a decade

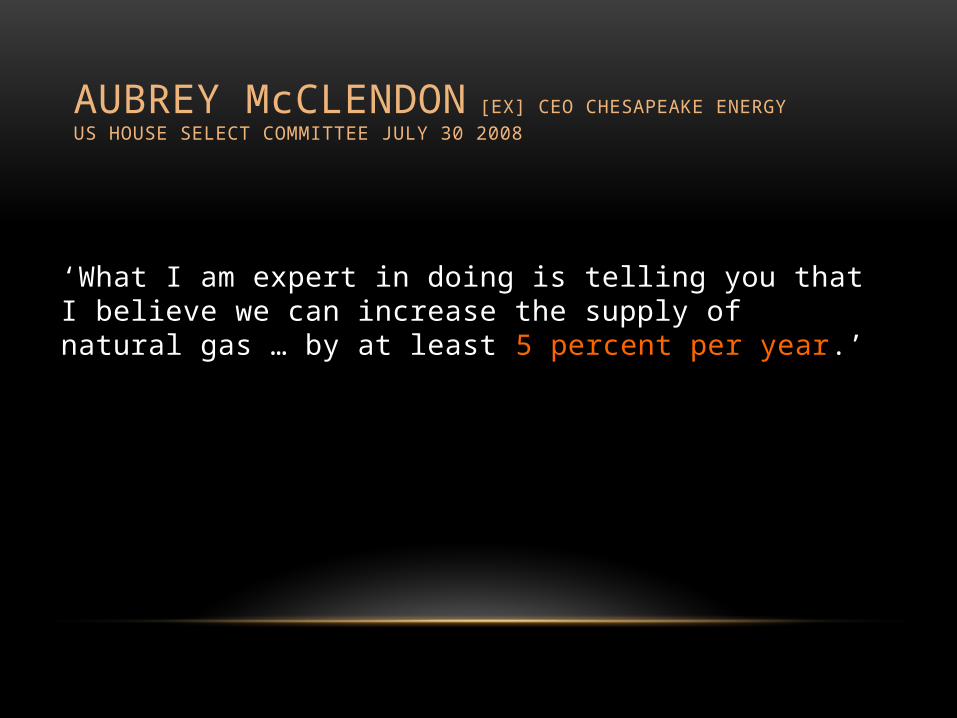

AUBREY McCLENDON [EX] CEO CHESAPEAKE ENERGYUS HOUSE SELECT COMMITTEE JULY 30 2008

‘What I am expert in doing is telling you that I believe we can increase the supply of natural gas … by at least 5 percent per year.’

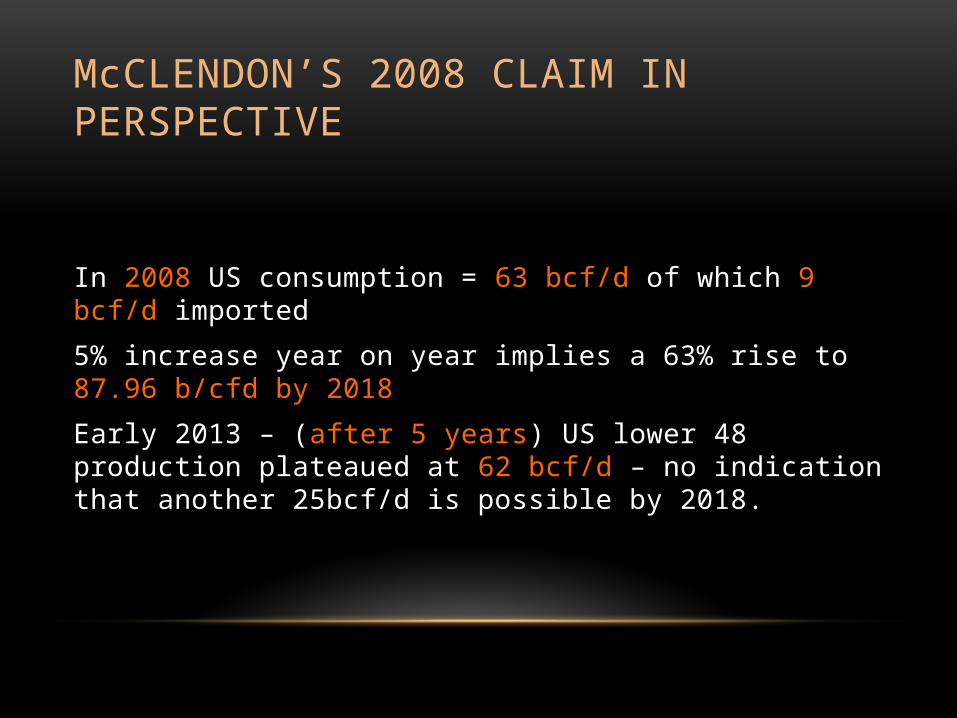

McCLENDON’S 2008 CLAIM IN PERSPECTIVE

In 2008 US consumption = 63 bcf/d of which 9 bcf/d imported

5% increase year on year implies a 63% rise to 87.96 b/cfd by 2018

Early 2013 – (after 5 years) US lower 48 production plateaued at 62 bcf/d – no indication that another 25bcf/d is possible by 2018.

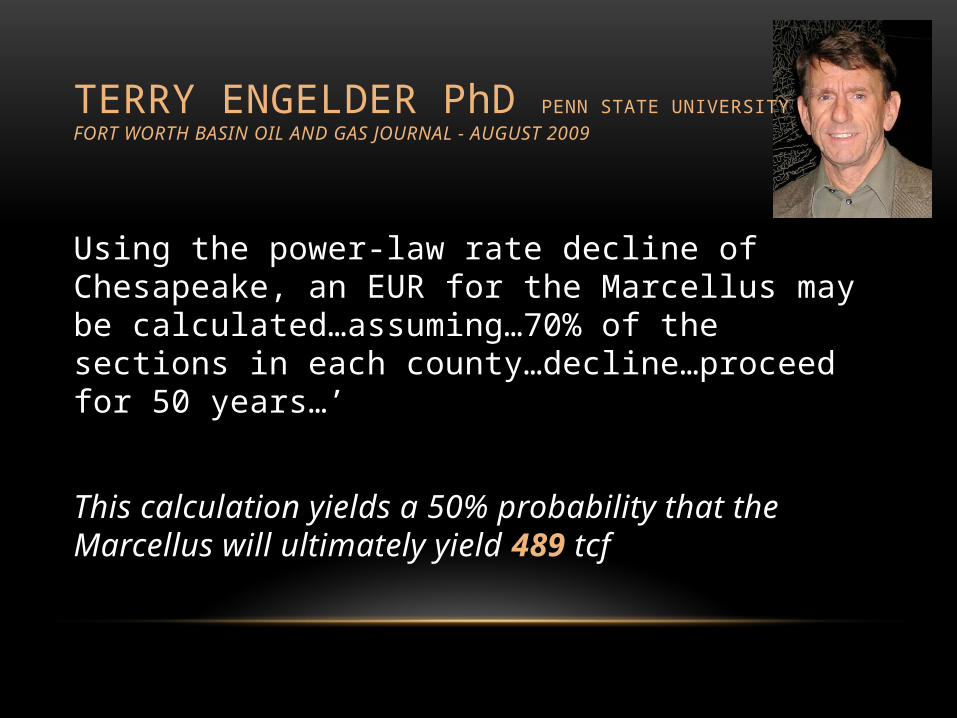

Using the power-law rate decline of Chesapeake, an EUR for the Marcellus may be calculated…assuming…70% of the sections in each county…decline…proceed for 50 years…’

This calculation yields a 50% probability that the Marcellus will ultimately yield 489 tcf

TERRY ENGELDER PhD PENN STATE UNIVERSITYFORT WORTH BASIN OIL AND GAS JOURNAL - AUGUST 2009

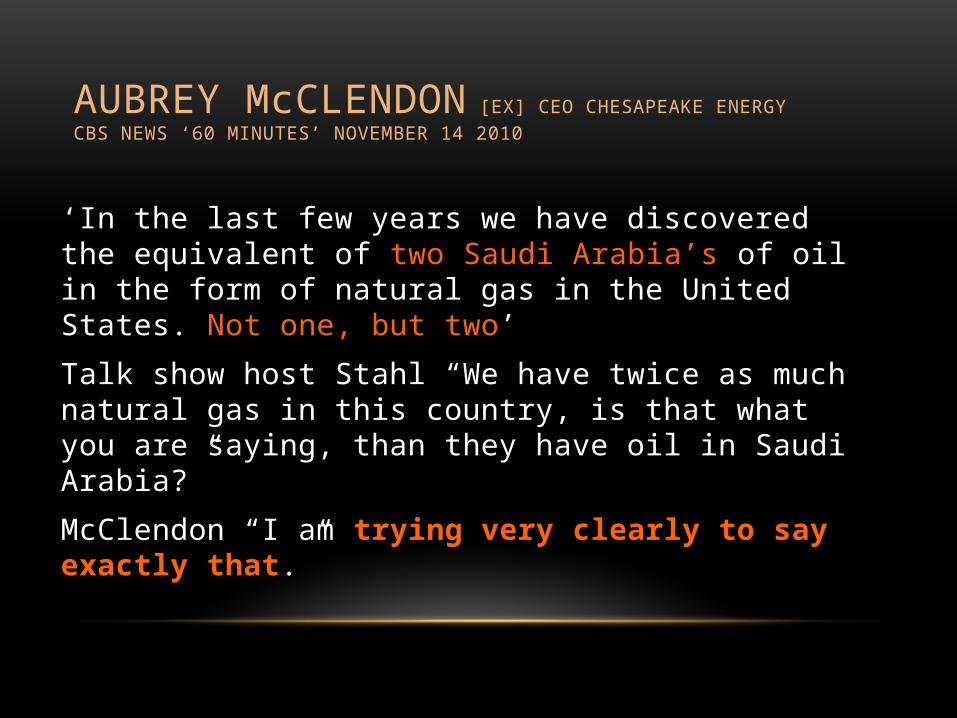

AUBREY McCLENDON [EX] CEO CHESAPEAKE ENERGYCBS NEWS ‘60 MINUTES’ NOVEMBER 14 2010

‘In the last few years we have discovered the equivalent of two Saudi Arabia’s of oil in the form of natural gas in the United States. Not one, but two’

Talk show host Stahl “We have twice as much natural gas in this country, is that what you are saying, than they have oil in Saudi Arabia?”

McClendon “I am trying very clearly to say exactly that.”

McCLENDON’S 2010 CLAIM IN PERSPECTIVE

In 2011 BP Statistical review Saudi Arabia 264.5 billion barrels proven oil reserves at end 2010. Equivalent of 1587 tcf nat gas.

X 2 = 3174 tcf or enough to power the US at its current rate of consumption for approx. 125 years.

T. BOONE PICKENSARCHITECT OF THE PICKENS PLAN

Pickens Plan TV adverts – break stranglehold of foreign oil Actually the Natural Gas Vehicle Actfilled with – tax credits, grants, requires 50% of all new federal Government vehicles to be on gas by Dec 2014Major shareholder in Clean Energy Fuels Corp.

Famous quote on CNBC April 2011 talking about America’s Natural gas Endowment:

You’re there. You’re there. I say you’re going to recover 4000 trillion [tcf]. Which is 700 million barrels.

ARE WE DEVELOPING A PICTURE OF WHY PRESIDENT OBAMA THINKS HE’S GOT MORE THAN A 100 YEARS OF NATURAL GAS?

And if President Obama thinks he’s got 100 years and the same people that told him that, tell President Zuma’s desperate government, that SA is sitting on top of a 400 year treasure trove, who is anyone in SA to argue?

Sooner or later, leaders are going to have to backtrack – I’m intrigued to see how they break the news ….

HOW DID IT PAN OUT FOR THE BIG GUYS?

Between 2006 and 2011, CHK sold whole or partial shale play interests for $17.9 billion.

5 buyers were foreign – Total, BP, Statoil, BHP Billiton

BHP took a $2.84 billion write down

BP took a $2.1 billion write down,

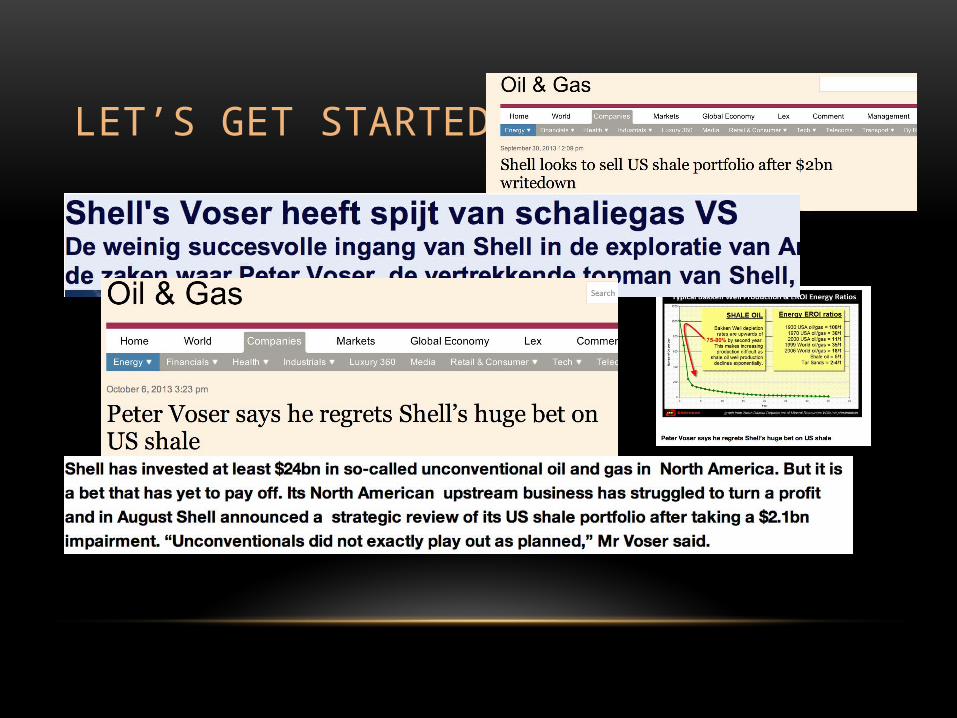

and now (October 2013) Shell is selling up in Colorado and Texas

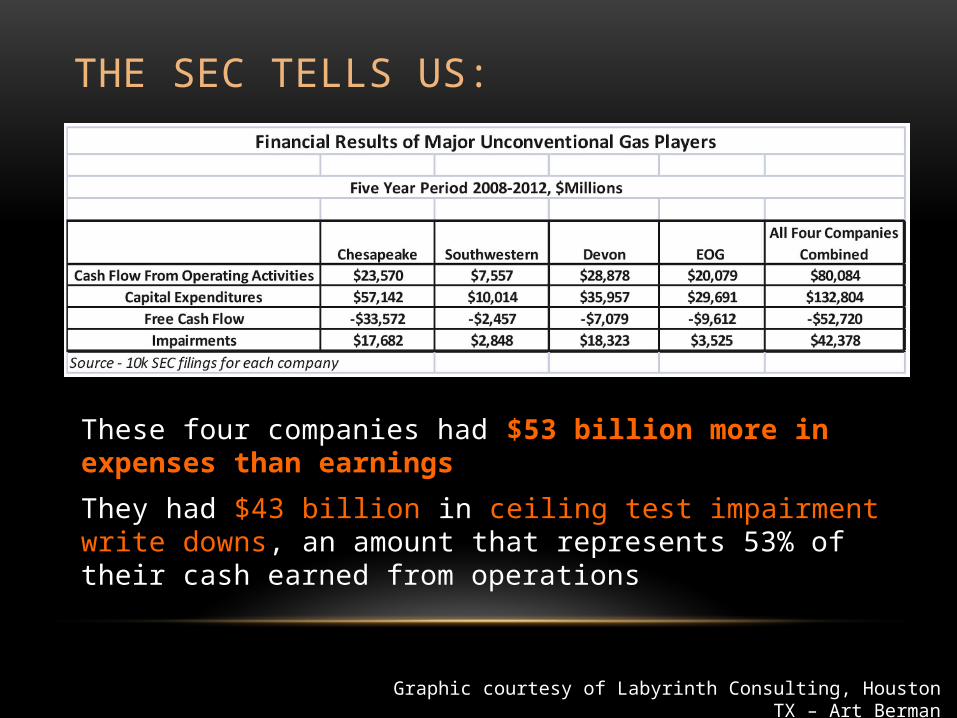

THE SEC TELLS US:

These four companies had $53 billion more in expenses than earnings

They had $43 billion in ceiling test impairment write downs, an amount that represents 53% of their cash earned from operations

Graphic courtesy of Labyrinth Consulting, Houston TX – Art Berman

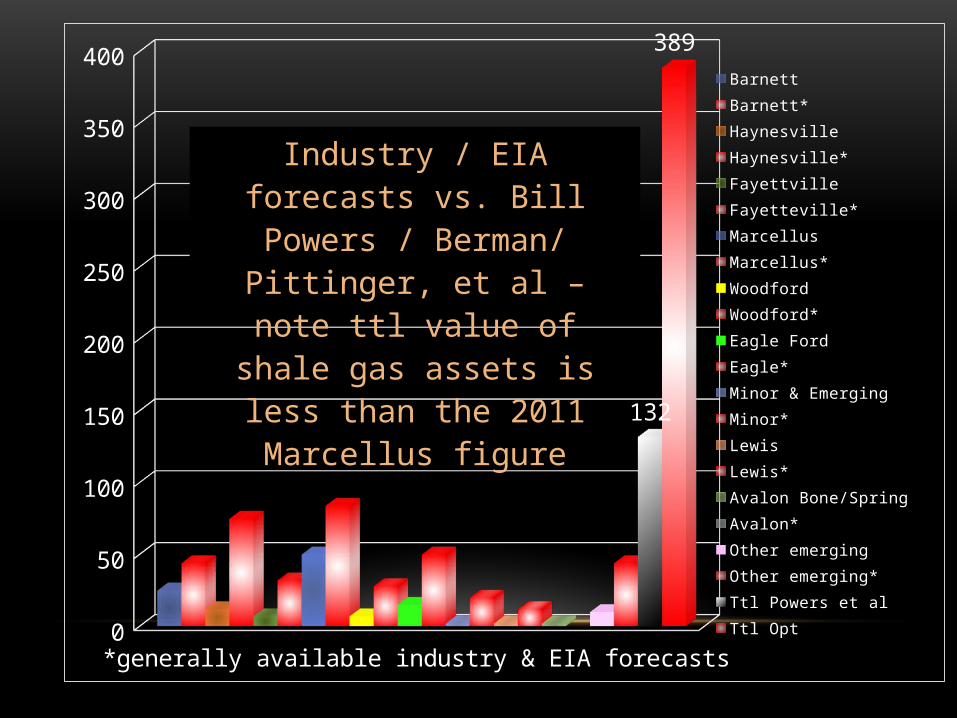

*generally available industry & EIA forecasts0

50

100

150

200

250

300

350

400

132

389

Barnett Barnett*

Haynesville Haynesville*

Fayettville Fayetteville*

Marcellus Marcellus*

Woodford Woodford*

Eagle Ford Eagle*

Minor & Emerging Minor*

Lewis Lewis*

Avalon Bone/Spring Avalon*

Other emerging Other emerging*

Ttl Powers et al Ttl Opt

Industry / EIA forecasts vs. Bill Powers / Berman/ Pittinger, et al – note ttl value of shale gas assets

is less than the 2011 Marcellus figure

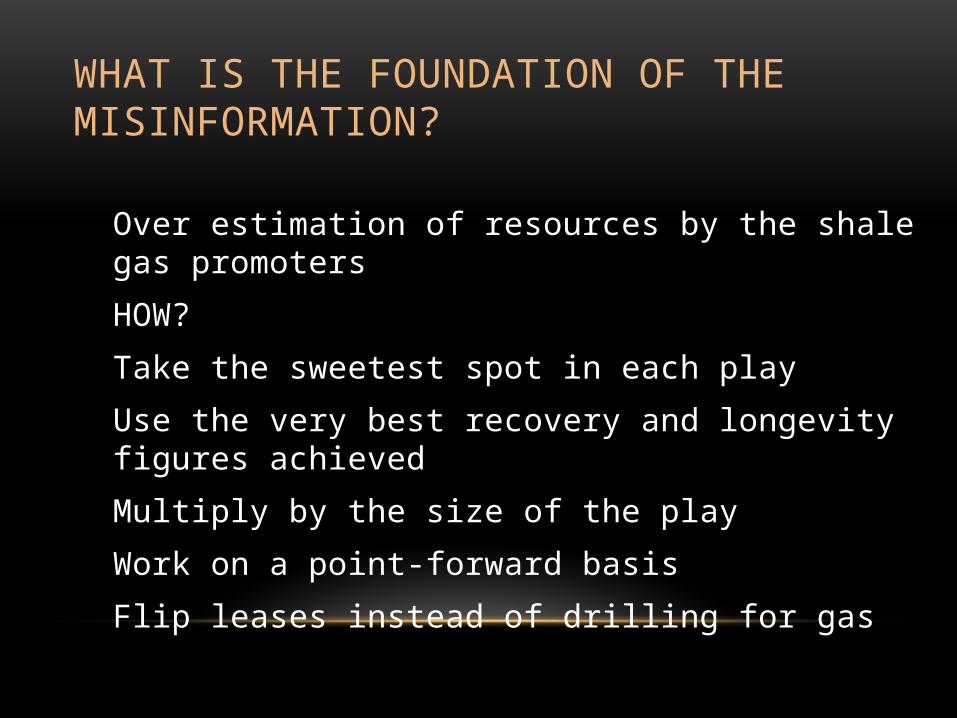

WHAT IS THE FOUNDATION OF THE MISINFORMATION?

Over estimation of resources by the shale gas promoters

HOW?

Take the sweetest spot in each play

Use the very best recovery and longevity figures achieved

Multiply by the size of the play

Work on a point-forward basis

Flip leases instead of drilling for gas

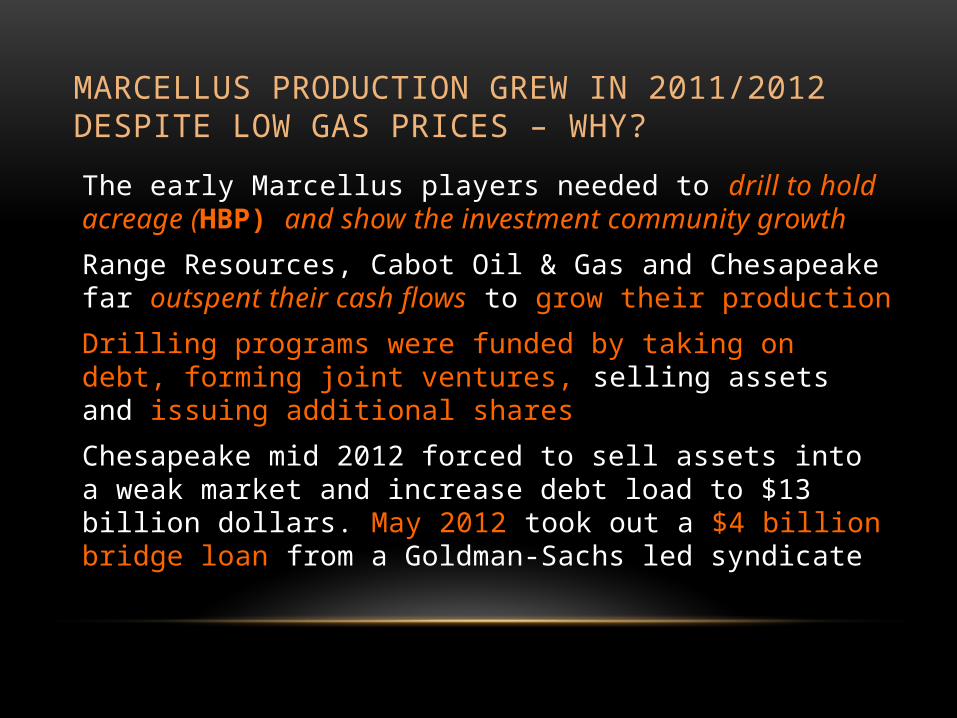

MARCELLUS PRODUCTION GREW IN 2011/2012 DESPITE LOW GAS PRICES – WHY?

The early Marcellus players needed to drill to hold acreage (HBP) and show the investment community growth

Range Resources, Cabot Oil & Gas and Chesapeake far outspent their cash flows to grow their production

Drilling programs were funded by taking on debt, forming joint ventures, selling assets and issuing additional shares

Chesapeake mid 2012 forced to sell assets into a weak market and increase debt load to $13 billion dollars. May 2012 took out a $4 billion bridge loan from a Goldman-Sachs led syndicate

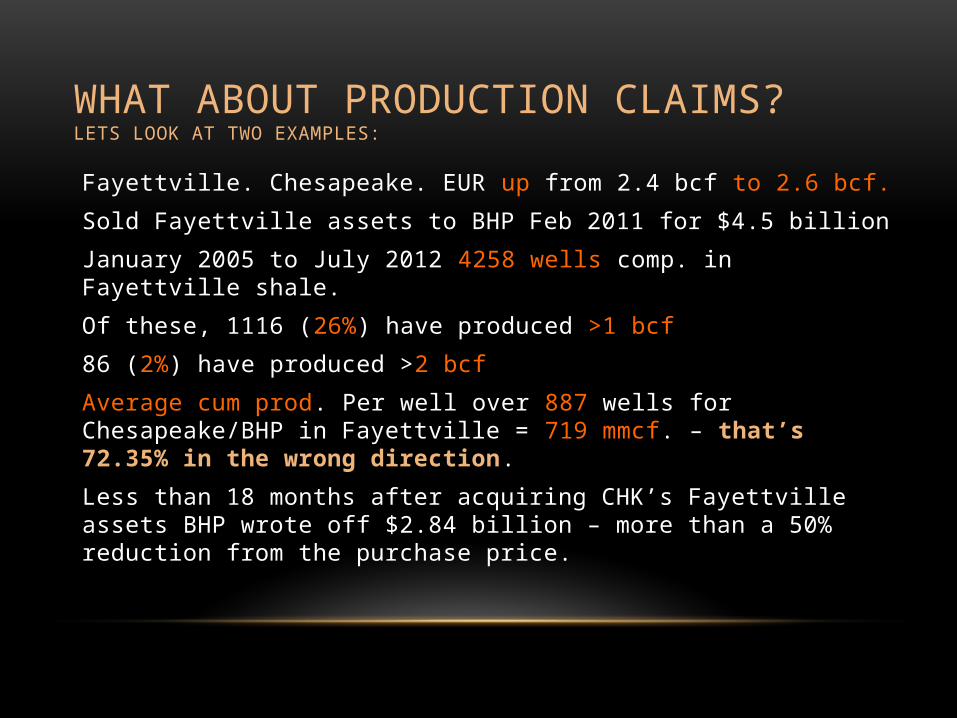

WHAT ABOUT PRODUCTION CLAIMS?LETS LOOK AT TWO EXAMPLES:

Fayettville. Chesapeake. EUR up from 2.4 bcf to 2.6 bcf.

Sold Fayettville assets to BHP Feb 2011 for $4.5 billion

January 2005 to July 2012 4258 wells comp. in Fayettville shale.

Of these, 1116 (26%) have produced >1 bcf

86 (2%) have produced >2 bcf

Average cum prod. Per well over 887 wells for Chesapeake/BHP in Fayettville = 719 mmcf. – that’s 72.35% in the wrong direction.

Less than 18 months after acquiring CHK’s Fayettville assets BHP wrote off $2.84 billion – more than a 50% reduction from the purchase price.

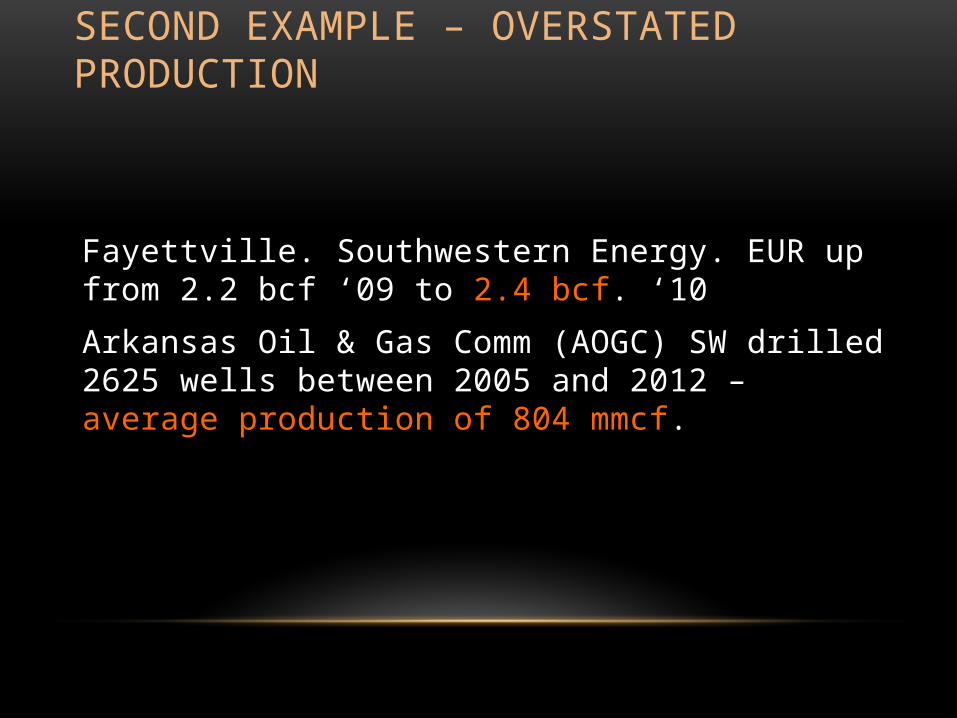

SECOND EXAMPLE – OVERSTATED PRODUCTION

Fayettville. Southwestern Energy. EUR up from 2.2 bcf ‘09 to 2.4 bcf. ‘10

Arkansas Oil & Gas Comm (AOGC) SW drilled 2625 wells between 2005 and 2012 – average production of 804 mmcf.

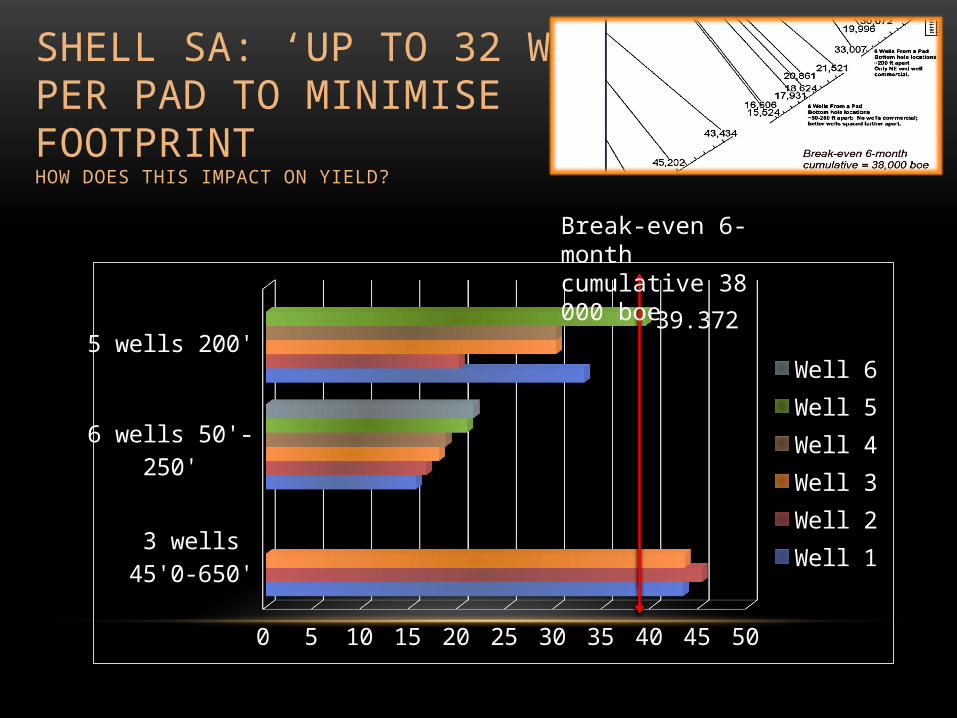

SHELL SA: ‘UP TO 32 WELLSPER PAD TO MINIMISE FOOTPRINTHOW DOES THIS IMPACT ON YIELD?

3 wells 45'0-650'

6 wells 50'-250'

5 wells 200'

0 5 10 15 20 25 30 35 40 45 50

39.372

Well 6Well 5Well 4Well 3Well 2Well 1

Break-even 6-month cumulative 38 000 boe

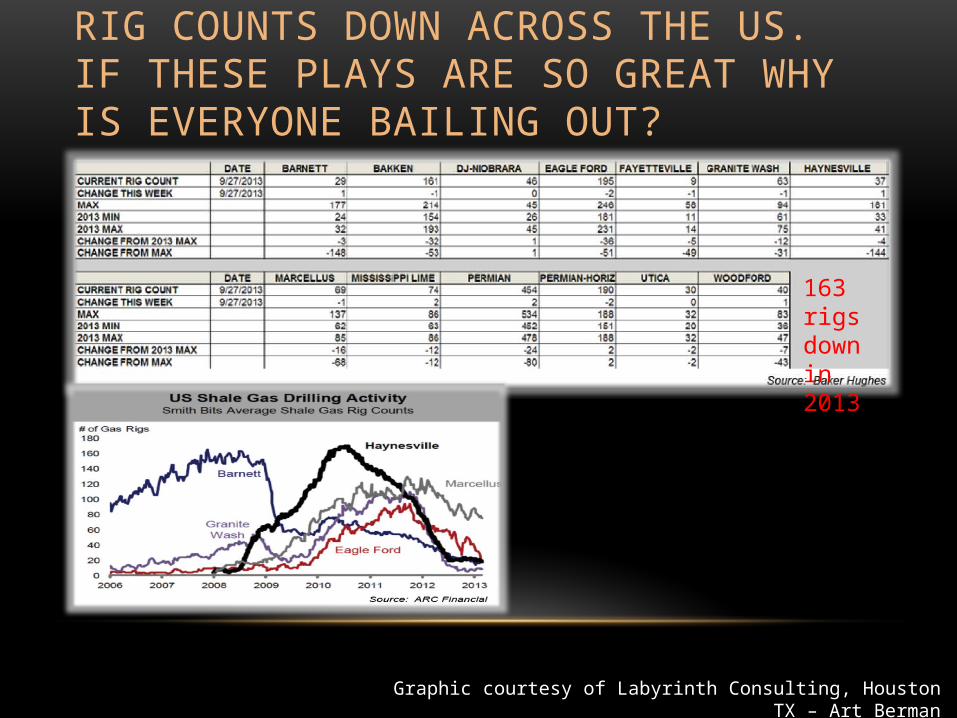

RIG COUNTS DOWN ACROSS THE US. IF THESE PLAYS ARE SO GREAT WHY IS EVERYONE BAILING OUT?

163 rigs down in 2013

Graphic courtesy of Labyrinth Consulting, Houston TX – Art Berman

CAN THE EIA FIGURES EVER BE TRUSTED?

EIA is the nations’s [US] and therefore global source of energy information yet;

EIA has consistently overestimated potential of shale gas

Failed to accurately estimate and shown inability to perform independent analysis that has led to bad policy and bad investment decisions

2011 EIA report ‘US Shale Gas & Oil Plays’ prepared by Intek (private consulting firm)

Instead of collecting real data on wells to determine decline curves and EUR, Intek simply cut and paste out of industry docs, including the 2008 Investor and Analyst meeting of Chesapeake

OR IS SOUTH AFRICA’S ENERGY POLICY ON SHALE GAS IN THE HANDS OF A US CONSULTANCY?

O&G APPROACH IS ‘TRUST US’ BUT THEIR PERFORMANCE SAYS THAT WE SHOULD NOT

At the same time that RoyalDutch Shell is pushing shale gas in South Africa, the company is withdrawing from shale gas assets in Colorado and Texas. (Right now) Why?

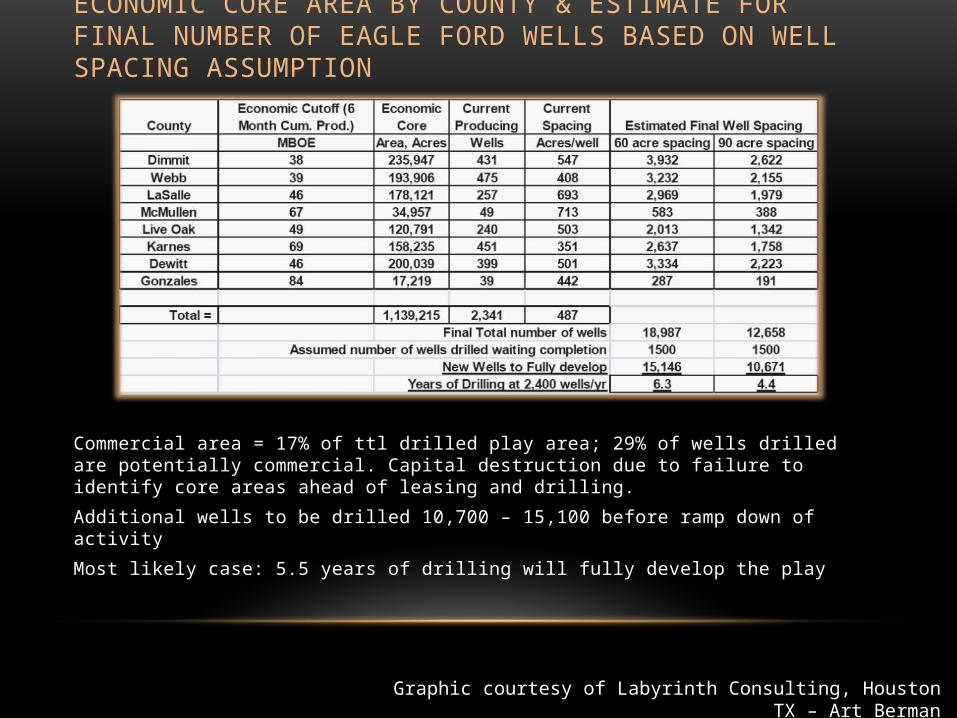

ECONOMIC CORE AREA BY COUNTY & ESTIMATE FOR FINAL NUMBER OF EAGLE FORD WELLS BASED ON WELL SPACING ASSUMPTION

Commercial area = 17% of ttl drilled play area; 29% of wells drilled are potentially commercial. Capital destruction due to failure to identify core areas ahead of leasing and drilling.

Additional wells to be drilled 10,700 – 15,100 before ramp down of activity

Most likely case: 5.5 years of drilling will fully develop the play

Graphic courtesy of Labyrinth Consulting, Houston TX – Art Berman

POINT FORWARD? OR MANIPULATION?What costs are typically excluded from point forward?

entry costs – surveys and finding

land costs 640 acres to a square mile $1k - $20k range

admin, utlities, support staff, interest expense

Typical reference to ‘non-cash items’ because they are in a previous Q.

Does a serious investor look for break-even on point-forward?

Would you invest in a business that brushes these costs under the rug? Consider the risk here especially when reserves and yields are well overstated.

LET’S DO SIMPLE MATH /LOGICSo, if we can buy LNG for $10-$15 per Mcf, why would we commit billions to pipeline, road, medical, law enforcement and legal costs and risk our agriculture, tourism, water, environment to try and extract gas from tight, unyielding shale that depletes so rapidly?

Why would we bank on a resource that may only be ready in 2025 when by 2025 we better be a long long way towards renewables?

Energy Independence? No. For how long and at what cost?

Price? No. If the global price goes up the mining companies will charge the same price for Karoo gas – if we can’t afford it they’ll sell it to China

Jobs? No. Have we forgotten the facts of declining US shale plays?

Cleaner burning? No. Even if this were true (having regard for the fugitive emissions and uncounted EROEI emissions and costs) - our coal would just be burned somewhere else – it remains a global problem

A GAME CHANGER FOR SOUTH AFRICA?

Perhaps, but there are two teams in every game – a winner and a loser.

The promises of RoyalDutch Shell, et al now picked up and echoed by the SA government and those few who will make a lot of money are a fantasy that ignores the decades required for such massive equipment change, infrastructure development and the costs associated therewith.

Fracking. Proudly promoted in South Africa by Royal Dutch Shell and the ANC?

I intend to continue my stand against shale promoters who gamble with South Africa’s future to promote their own.

THANKS FOR YOUR ATTENTION

THIS SLIDE PRESENTATION IS AVAILABLE FROM THE CONFERENCE FACILITATOR OR DIRECT FROM TKAG

LOOK OUT FOR OUR ECONOMIC SYNOPSIS WHICH WILL BE RELEASED TO THE SA MEDIA

AT A PRESS BRIEFING IN CAPE TOWN TOMORROW