Gabrielle Gauthey Presentation

19

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED. THE IMPACT OF OTT ON TRADITIONAL NATIONAL NETWORKS AND MEDIA Gabrielle Gauthey September 2012

-

Upload

citi-columbia -

Category

Documents

-

view

222 -

download

0

description

Gabrielle Gauthey Presentation

Transcript of Gabrielle Gauthey Presentation

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

THE IMPACT OF OTT ON TRADITIONAL NATIONAL NETWORKS AND MEDIA

Gabrielle Gauthey September 2012

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

2

AGENDA

1. DATA EXPLOSION, INVESTMENTS AND MODELS AROUND THE WORLD

2. TELCOS, OTT, MEDIA: WHICH TECHNOLOGICAL AND BUSINESS MODELS EVOLUTIONS?

3. THE CASE OF EUROPE

4. NEED FOR INNOVATIVE INVESTMENT MODELS?

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

3

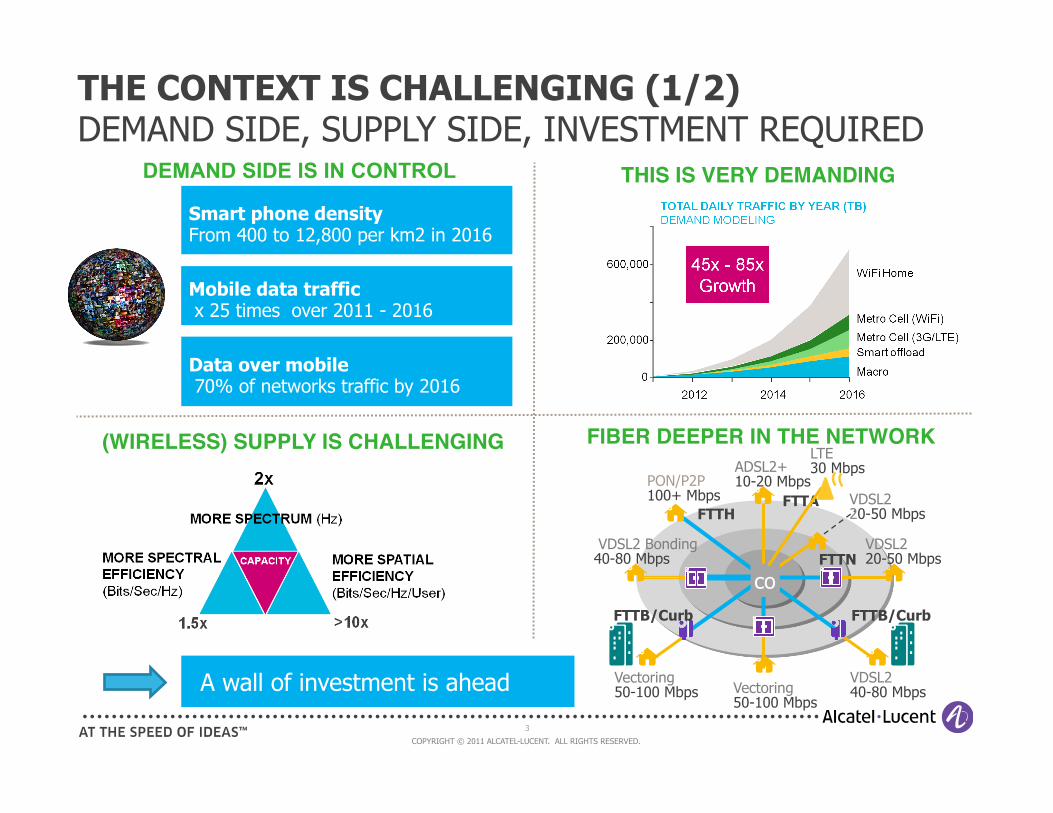

THE CONTEXT IS CHALLENGING (1/2) DEMAND SIDE, SUPPLY SIDE, INVESTMENT REQUIRED

DEMAND SIDE IS IN CONTROL THIS IS VERY DEMANDING!

(WIRELESS) SUPPLY IS CHALLENGING!

A wall of investment is ahead

Smart phone density From 400 to 12,800 per km2 in 2016

Mobile data traffic x 25 times over 2011 - 2016

Data over mobile 70% of networks traffic by 2016

FIBER DEEPER IN THE NETWORK!

FTTN

FTTB/Curb

FTTH VDSL2 20-50 Mbps

ADSL2+ 10-20 Mbps

VDSL2 Bonding 40-80 Mbps

VDSL2 20-50 Mbps

VDSL2 40-80 Mbps

Vectoring 50-100 Mbps

PON/P2P 100+ Mbps

Vectoring 50-100 Mbps

co FTTB/Curb

FTTA

LTE 30 Mbps

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

4

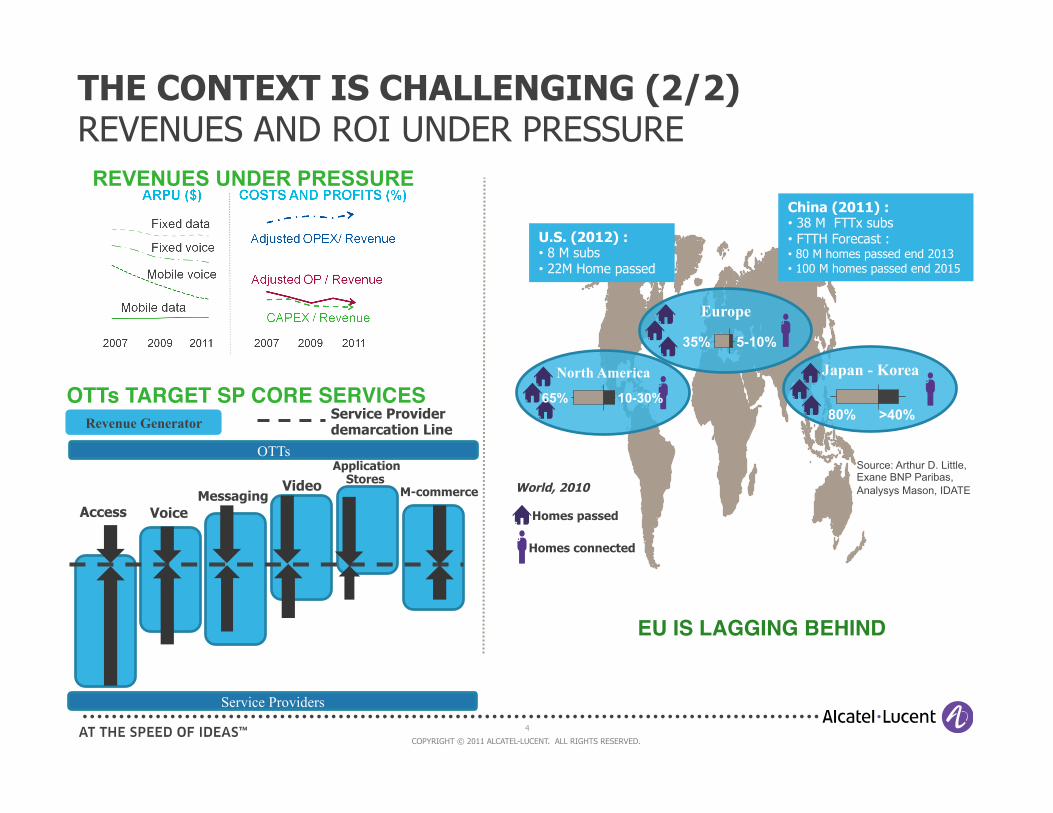

THE CONTEXT IS CHALLENGING (2/2) REVENUES AND ROI UNDER PRESSURE

REVENUES UNDER PRESSURE

OTTs TARGET SP CORE SERVICES!

Source: Arthur D. Little, Exane BNP Paribas, Analysys Mason, IDATE

Homes passed

Homes connected

World, 2010

U.S. (2012) : • 8 M subs • 22M Home passed

China (2011) : • 38 M FTTx subs • FTTH Forecast : • 80 M homes passed end 2013 • 100 M homes passed end 2015

EU IS LAGGING BEHIND!

North America

65% 10-30%

Europe

35% 5-10%

Japan - Korea

80% >40%

Access Voice Messaging

Video Application

Stores M-commerce

OTTs

Revenue Generator Service Provider demarcation Line

Service Providers

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

5

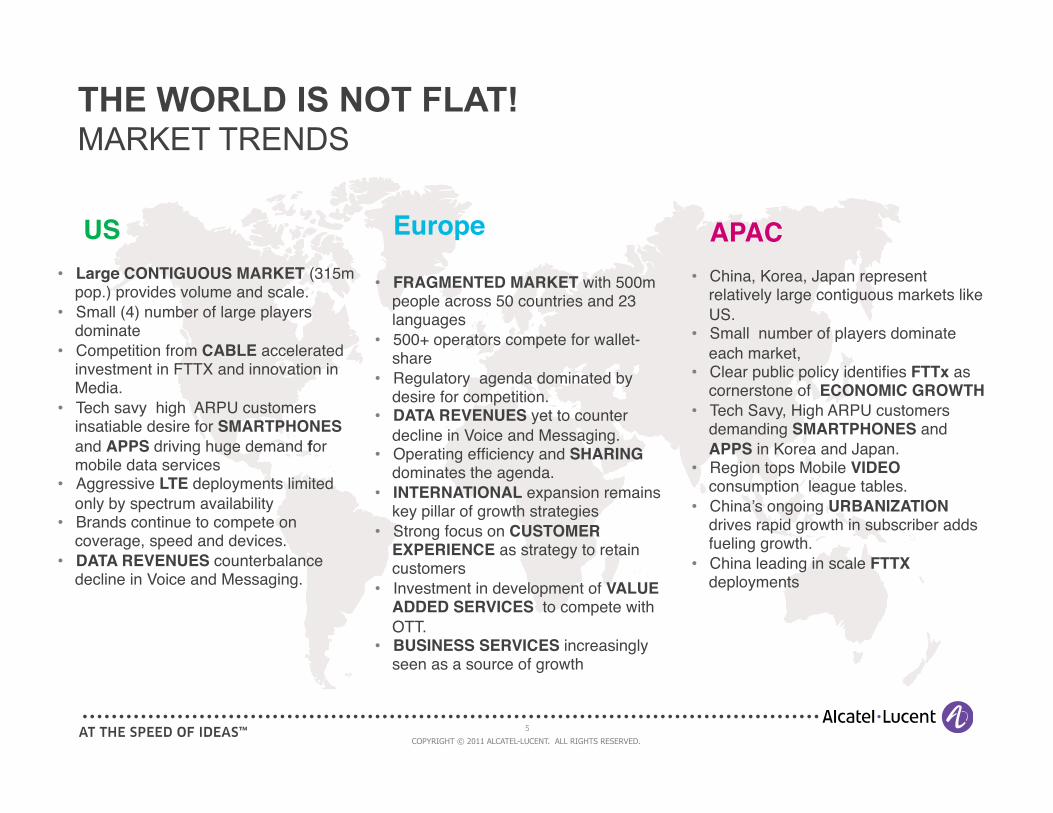

THE WORLD IS NOT FLAT! MARKET TRENDS

! US!!• Large CONTIGUOUS MARKET (315m

pop.) provides volume and scale."• Small (4) number of large players

dominate"• Competition from CABLE accelerated

investment in FTTX and innovation in Media."

• Tech savy high ARPU customers insatiable desire for SMARTPHONES and APPS driving huge demand for mobile data services"

• Aggressive LTE deployments limited only by spectrum availability"

• Brands continue to compete on coverage, speed and devices. "

• DATA REVENUES counterbalance decline in Voice and Messaging."

!APAC"• China, Korea, Japan represent

relatively large contiguous markets like US."

• Small number of players dominate each market,"

• Clear public policy identifies FTTx as cornerstone of ECONOMIC GROWTH!

• Tech Savy, High ARPU customers demanding SMARTPHONES and APPS in Korea and Japan."

• Region tops Mobile VIDEO consumption league tables."

• China’s ongoing URBANIZATION drives rapid growth in subscriber adds fueling growth."

• China leading in scale FTTX deployments"

!Europe!"• FRAGMENTED MARKET with 500m

people across 50 countries and 23 languages"

• 500+ operators compete for wallet-share"

• Regulatory agenda dominated by desire for competition. "

• DATA REVENUES yet to counter decline in Voice and Messaging."

• Operating efficiency and SHARING dominates the agenda. "

• INTERNATIONAL expansion remains key pillar of growth strategies!

• Strong focus on CUSTOMER EXPERIENCE as strategy to retain customers"

• Investment in development of VALUE ADDED SERVICES to compete with OTT."

• BUSINESS SERVICES increasingly seen as a source of growth"

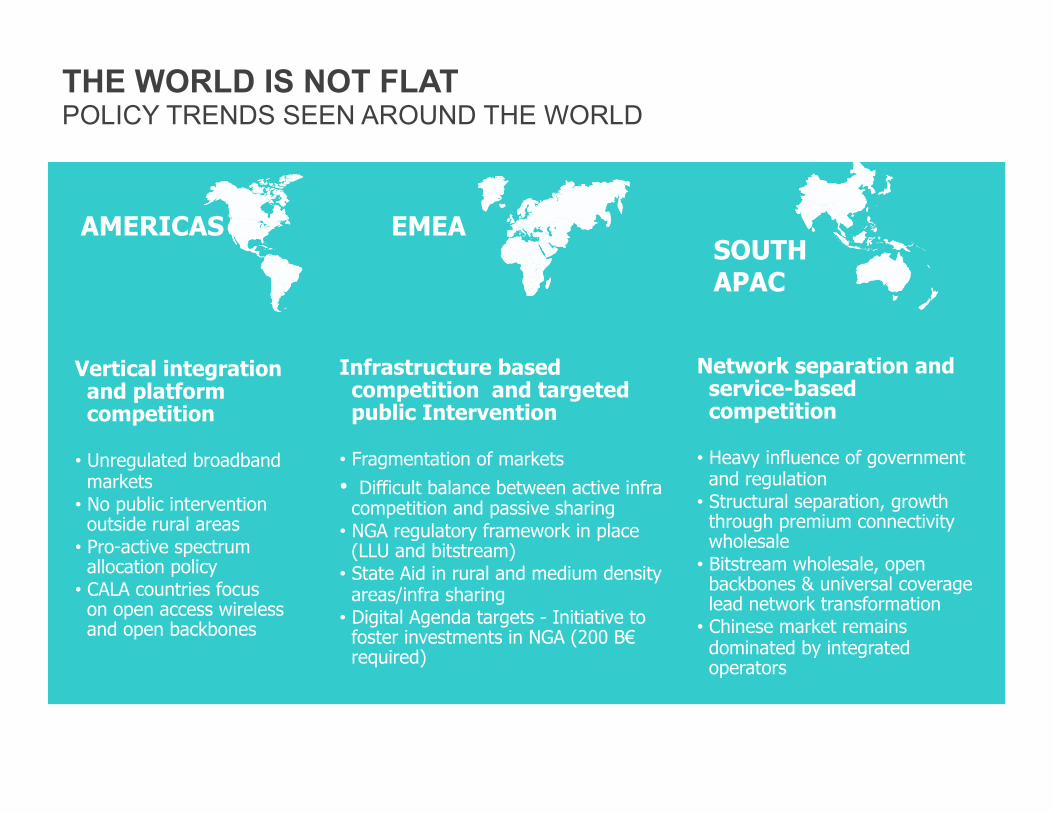

THE WORLD IS NOT FLAT POLICY TRENDS SEEN AROUND THE WORLD

Vertical integration and platform competition

• Unregulated broadband markets

• No public intervention outside rural areas

• Pro-active spectrum allocation policy

• CALA countries focus on open access wireless and open backbones

Network separation and service-based competition

• Heavy influence of government and regulation

• Structural separation, growth through premium connectivity wholesale

• Bitstream wholesale, open backbones & universal coverage lead network transformation

• Chinese market remains dominated by integrated operators

Infrastructure based competition and targeted public Intervention

• Fragmentation of markets • Difficult balance between active infra

competition and passive sharing • NGA regulatory framework in place

(LLU and bitstream) • State Aid in rural and medium density

areas/infra sharing • Digital Agenda targets - Initiative to

foster investments in NGA (200 B€ required)

EMEA SOUTH APAC

AMERICAS

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

7

AGENDA

1. DATA EXPLOSION, INVESTMENTS AND MODELS AROUND THE WORLD

2. TELCOS, OTT, MEDIA: WHICH TECHNOLOGICAL AND BUSINESS MODELS EVOLUTIONS?

3. THE CASE OF EUROPE

4. NEED FOR INNOVATIVE INVESTMENT MODELS?

8

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

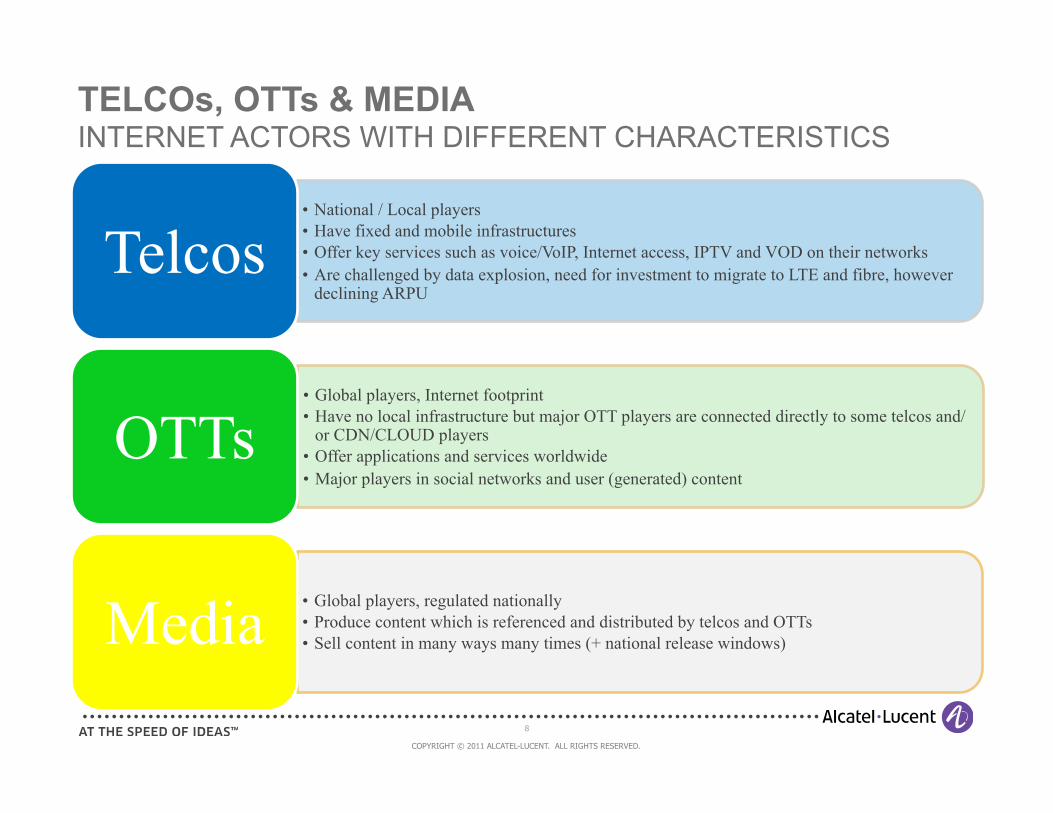

TELCOs, OTTs & MEDIA INTERNET ACTORS WITH DIFFERENT CHARACTERISTICS

• National / Local players • Have fixed and mobile infrastructures • Offer key services such as voice/VoIP, Internet access, IPTV and VOD on their networks • Are challenged by data explosion, need for investment to migrate to LTE and fibre, however

declining ARPU Telcos

• Global players, Internet footprint • Have no local infrastructure but major OTT players are connected directly to some telcos and/

or CDN/CLOUD players • Offer applications and services worldwide • Major players in social networks and user (generated) content

OTTs

• Global players, regulated nationally • Produce content which is referenced and distributed by telcos and OTTs • Sell content in many ways many times (+ national release windows) Media

9

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

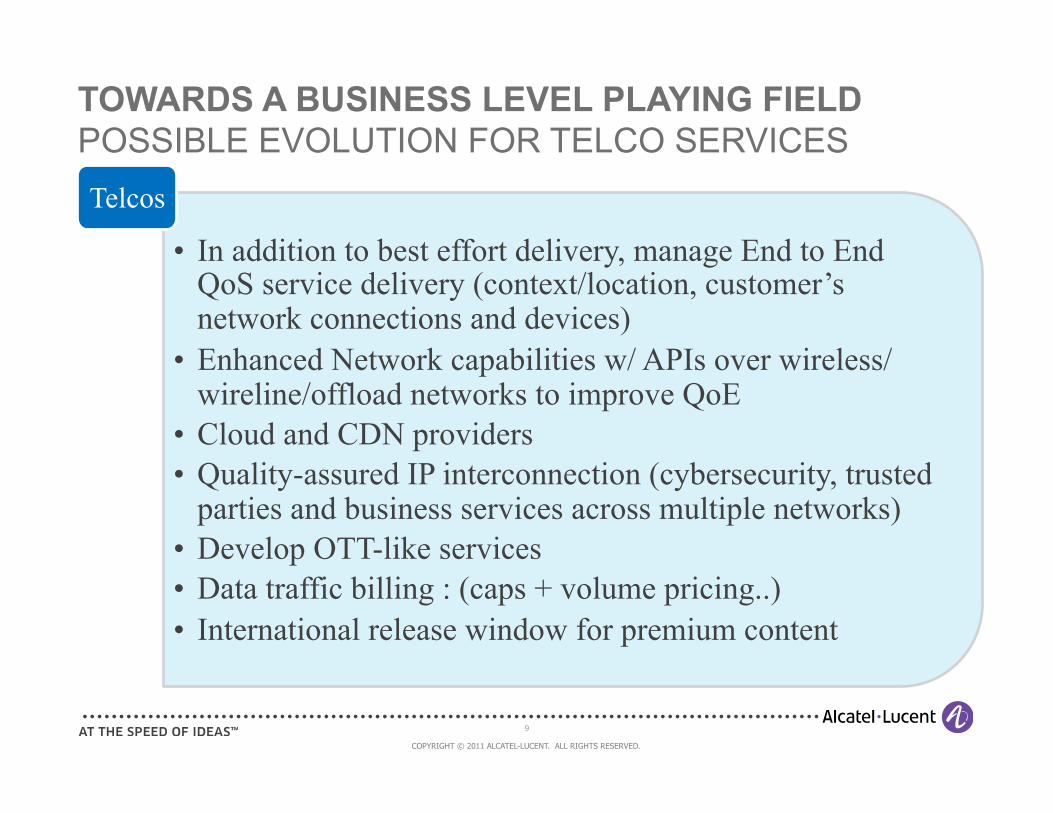

TOWARDS A BUSINESS LEVEL PLAYING FIELD POSSIBLE EVOLUTION FOR TELCO SERVICES

• In addition to best effort delivery, manage End to End QoS service delivery (context/location, customer’s network connections and devices)

• Enhanced Network capabilities w/ APIs over wireless/wireline/offload networks to improve QoE

• Cloud and CDN providers • Quality-assured IP interconnection (cybersecurity, trusted

parties and business services across multiple networks) • Develop OTT-like services • Data traffic billing : (caps + volume pricing..) • International release window for premium content

Telcos

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

10

AGENDA

1. DATA EXPLOSION, INVESTMENTS AND MODELS AROUND THE WORLD

2. TELCOS, OTT, MEDIA: WHICH TECHNOLOGICAL AND BUSINESS MODELS EVOLUTIONS?

3. THE CASE OF EUROPE

4. NEED FOR INNOVATIVE INVESTMENT MODEL?

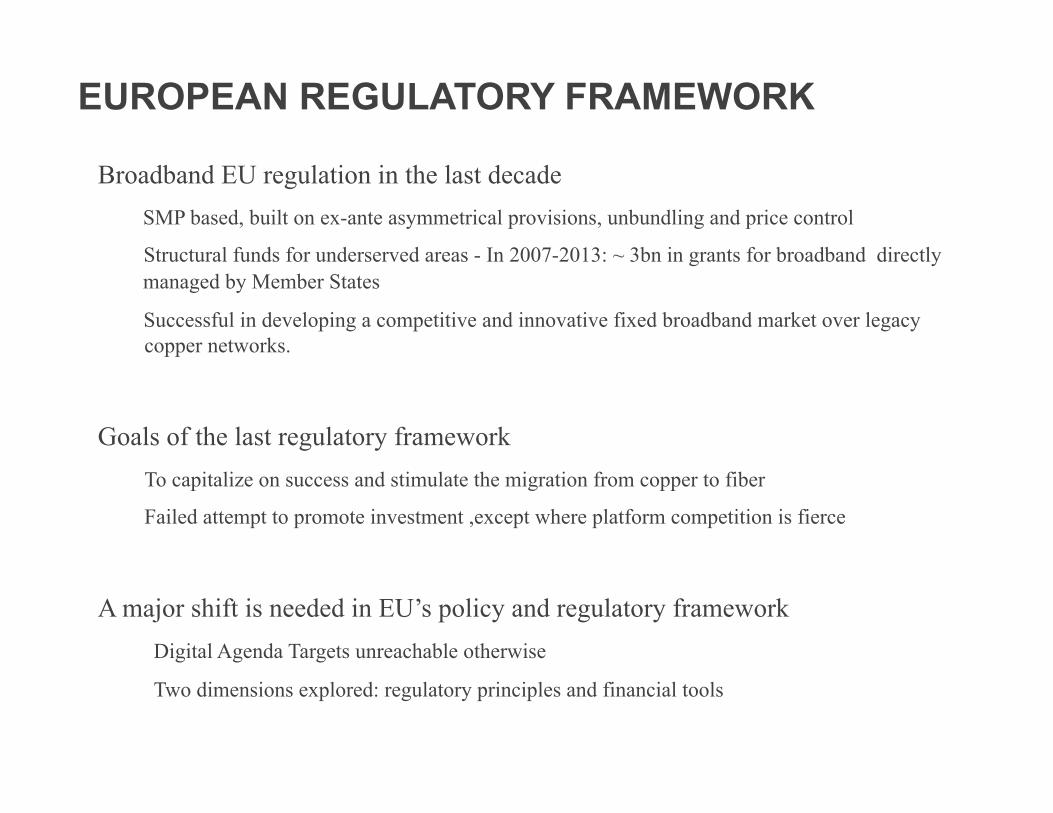

Broadband EU regulation in the last decade SMP based, built on ex-ante asymmetrical provisions, unbundling and price control

Structural funds for underserved areas - In 2007-2013: ~ 3bn in grants for broadband directly managed by Member States

Successful in developing a competitive and innovative fixed broadband market over legacy copper networks.

Goals of the last regulatory framework To capitalize on success and stimulate the migration from copper to fiber

Failed attempt to promote investment ,except where platform competition is fierce

A major shift is needed in EU’s policy and regulatory framework Digital Agenda Targets unreachable otherwise

Two dimensions explored: regulatory principles and financial tools

EUROPEAN REGULATORY FRAMEWORK

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

12

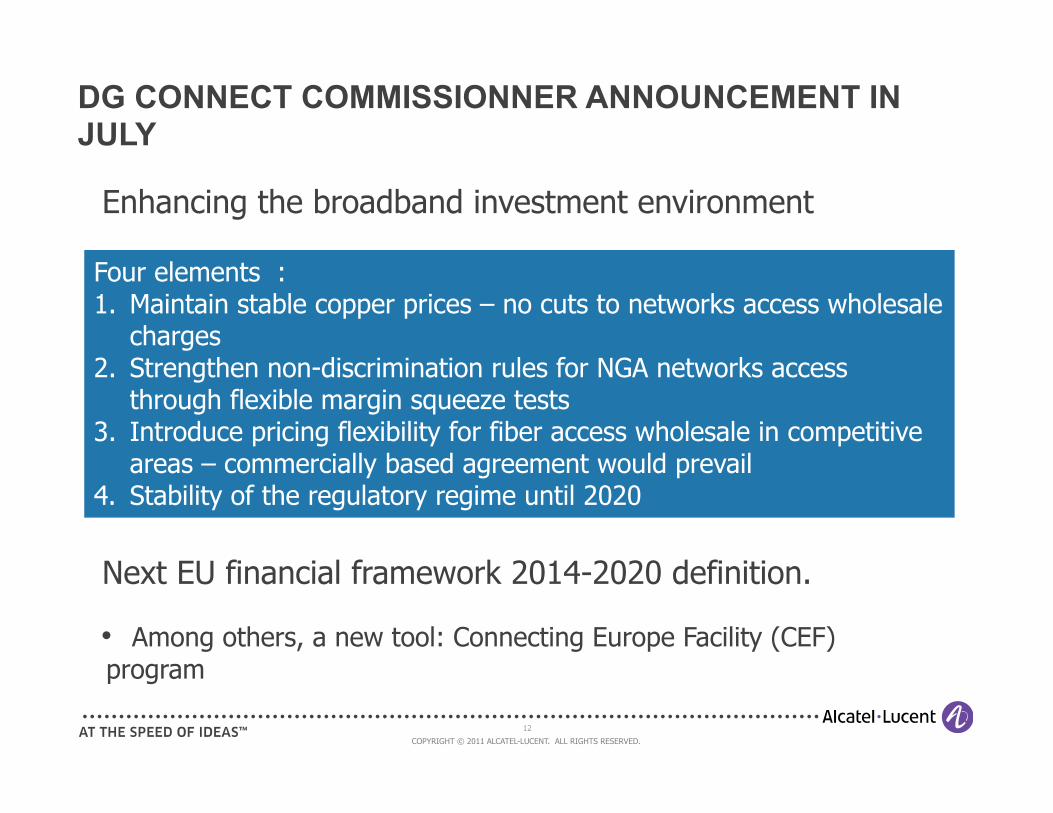

DG CONNECT COMMISSIONNER ANNOUNCEMENT IN JULY

Enhancing the broadband investment environment

Next EU financial framework 2014-2020 definition.

• Among others, a new tool: Connecting Europe Facility (CEF) program

Four elements : 1. Maintain stable copper prices – no cuts to networks access wholesale

charges 2. Strengthen non-discrimination rules for NGA networks access

through flexible margin squeeze tests 3. Introduce pricing flexibility for fiber access wholesale in competitive

areas – commercially based agreement would prevail 4. Stability of the regulatory regime until 2020

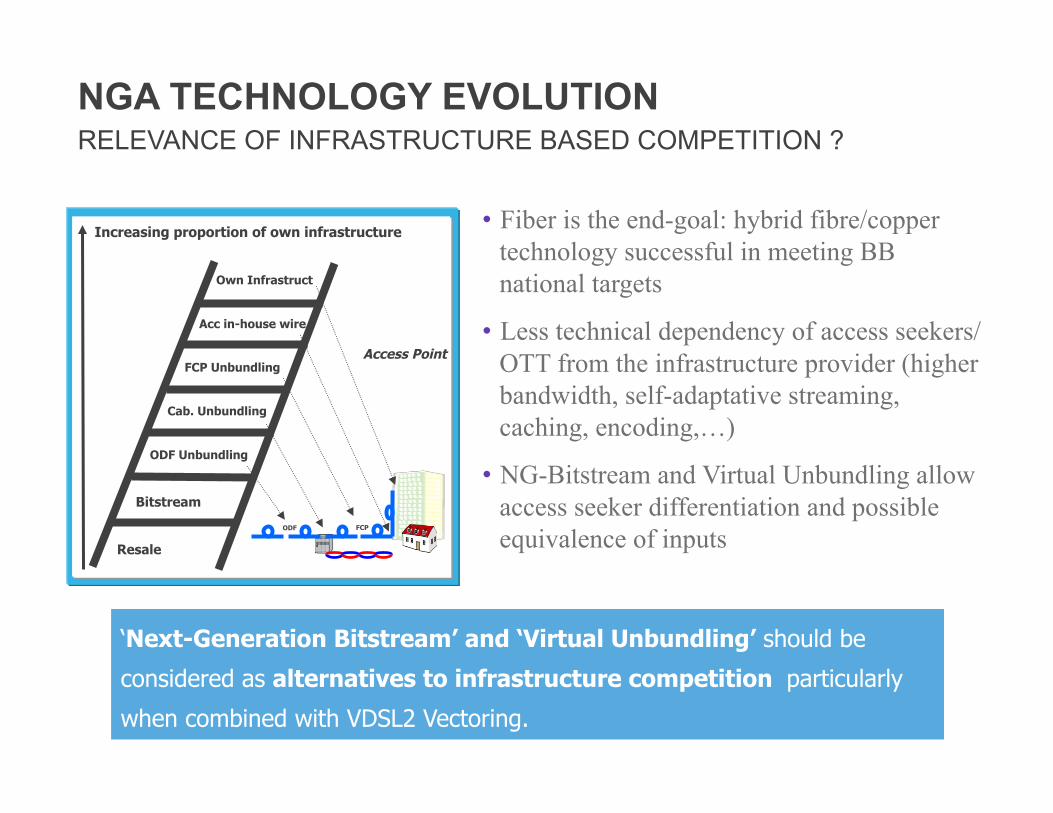

• Fiber is the end-goal: hybrid fibre/copper technology successful in meeting BB national targets

• Less technical dependency of access seekers/OTT from the infrastructure provider (higher bandwidth, self-adaptative streaming, caching, encoding,…)

• NG-Bitstream and Virtual Unbundling allow access seeker differentiation and possible equivalence of inputs

NGA TECHNOLOGY EVOLUTION RELEVANCE OF INFRASTRUCTURE BASED COMPETITION ?

‘Next-Generation Bitstream’ and ‘Virtual Unbundling’ should be

considered as alternatives to infrastructure competition particularly

when combined with VDSL2 Vectoring.

Resale

Bitstream

ODF Unbundling

Cab. Unbundling

FCP Unbundling

Acc in-house wire

Own Infrastruct

Increasing proportion of own infrastructure

Access Point

FCP ODF

• Local and contextual circumstances will prevail for NGA roll-out • In many areas, a single common passive infrastructure will be deployed.

• Solutions should not only be built on geographic segmentation but also along a layered approach, allowing co-investing models – and use of financial instruments to de-risk investments

• In policy-driven areas, public intervention will be required

• In all areas, Mobile demand is also driving progressive migration towards fibre backhauling

INFRASTRUCTURE SHARING: INEVITABLE ESPECIALLY OUTSIDE DENSE AREAS

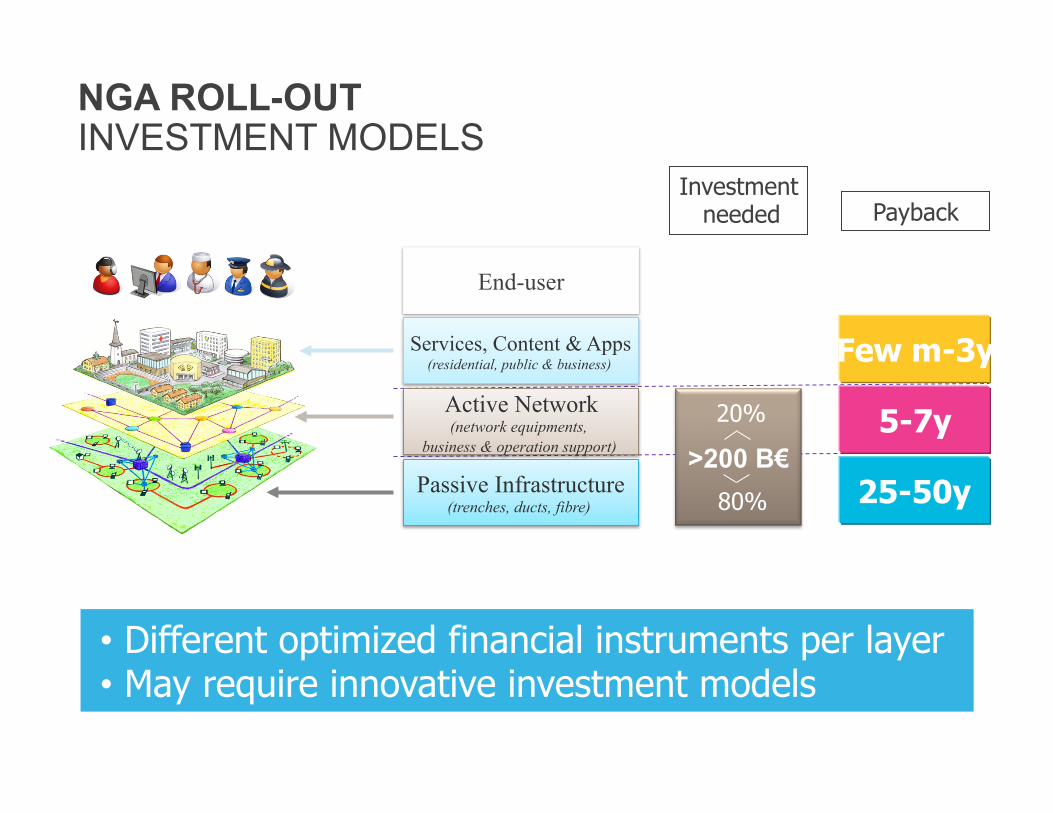

NGA ROLL-OUT INVESTMENT MODELS

• Different optimized financial instruments per layer • May require innovative investment models

Services, Content & Apps (residential, public & business)

Active Network (network equipments,

business & operation support)

Passive Infrastructure (trenches, ducts, fibre)

End-user

>200 B€

Investment needed Payback

Few m-3y

5-7y

25-50y

20%

80%

ROI

Risk NGA roll out

Lack of investment in NGA networks

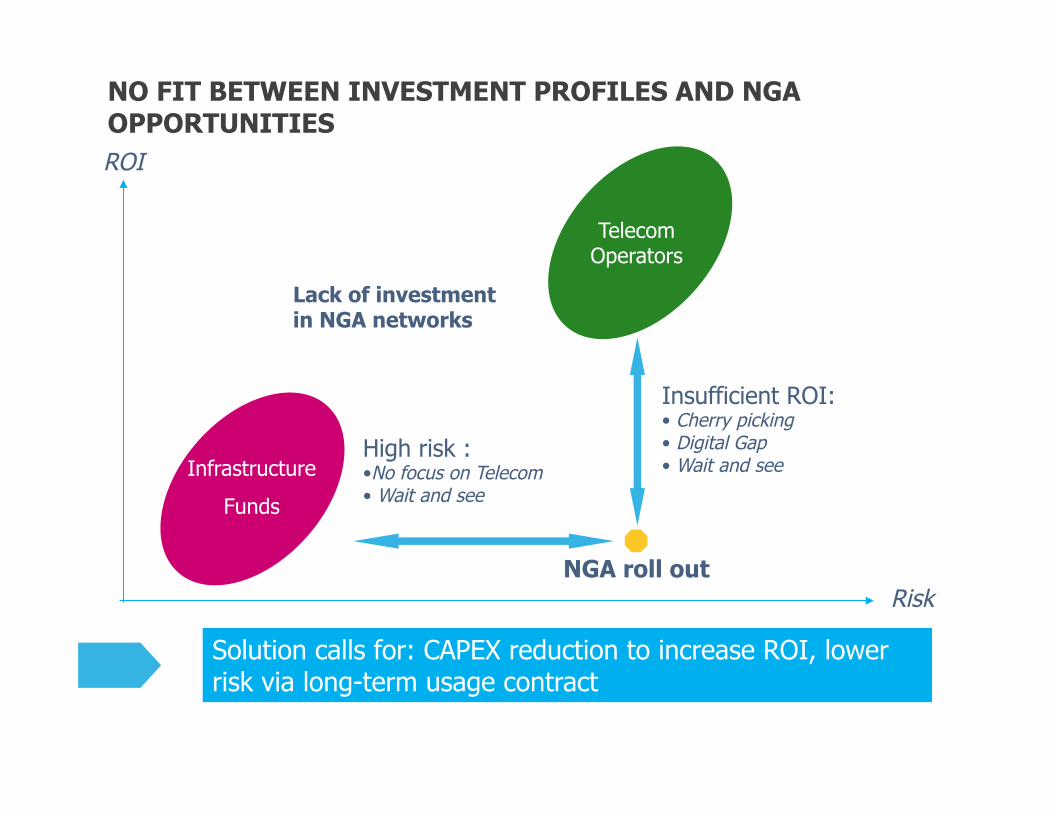

NO FIT BETWEEN INVESTMENT PROFILES AND NGA OPPORTUNITIES

Infrastructure

Funds

Telecom Operators

Insufficient ROI: • Cherry picking • Digital Gap • Wait and see

High risk : • No focus on Telecom • Wait and see

Solution calls for: CAPEX reduction to increase ROI, lower risk via long-term usage contract

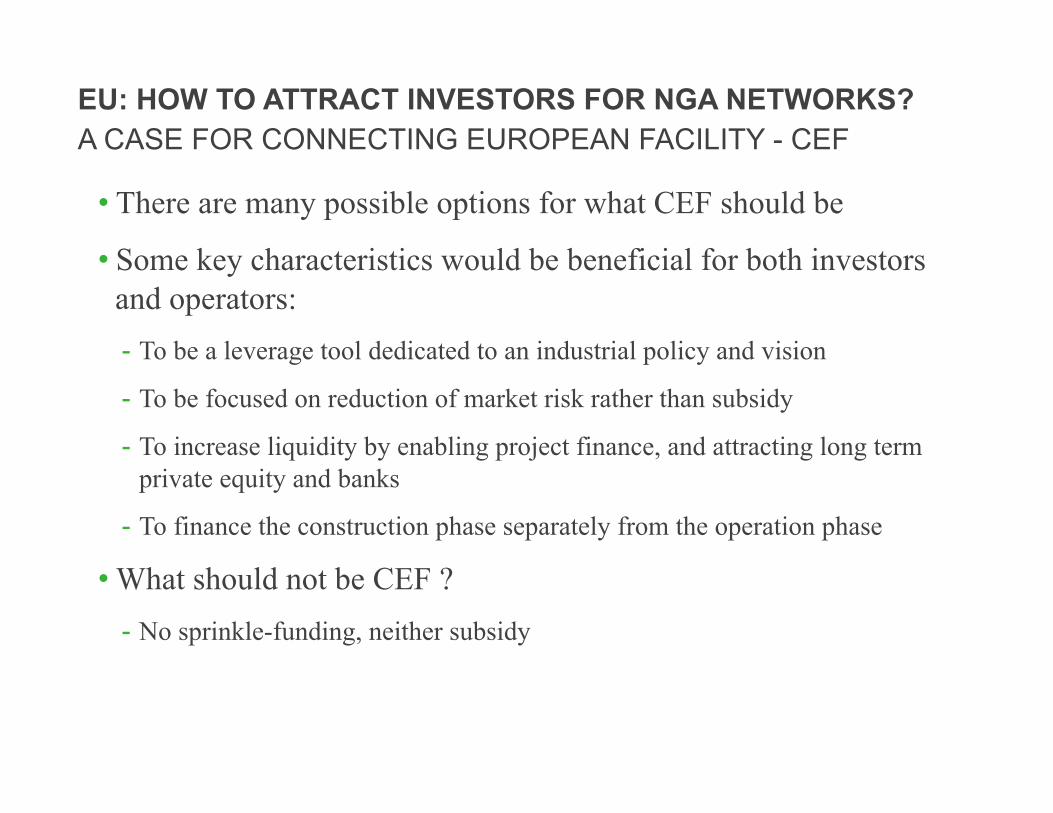

• There are many possible options for what CEF should be

• Some key characteristics would be beneficial for both investors and operators: - To be a leverage tool dedicated to an industrial policy and vision

- To be focused on reduction of market risk rather than subsidy

- To increase liquidity by enabling project finance, and attracting long term private equity and banks

- To finance the construction phase separately from the operation phase

• What should not be CEF ? - No sprinkle-funding, neither subsidy

EU: HOW TO ATTRACT INVESTORS FOR NGA NETWORKS? A CASE FOR CONNECTING EUROPEAN FACILITY - CEF

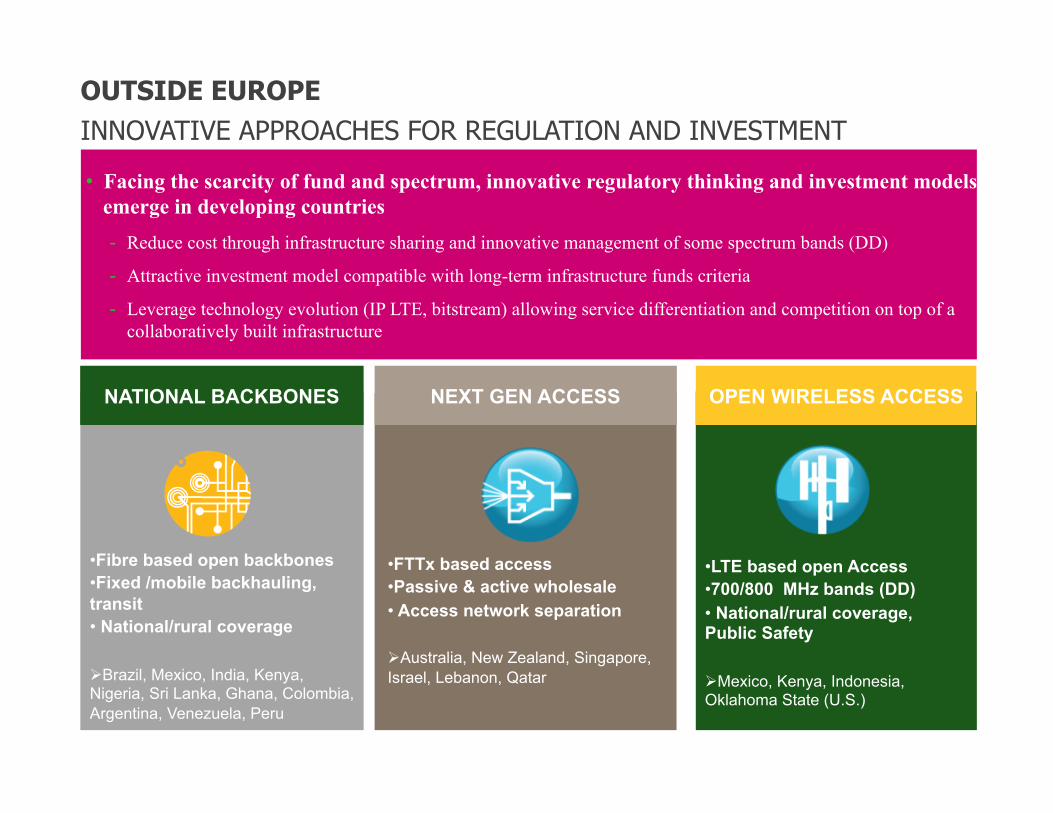

• Facing the scarcity of fund and spectrum, innovative regulatory thinking and investment models emerge in developing countries - Reduce cost through infrastructure sharing and innovative management of some spectrum bands (DD)

- Attractive investment model compatible with long-term infrastructure funds criteria

- Leverage technology evolution (IP LTE, bitstream) allowing service differentiation and competition on top of a collaboratively built infrastructure

OUTSIDE EUROPE INNOVATIVE APPROACHES FOR REGULATION AND INVESTMENT

• FTTx based access • Passive & active wholesale • Access network separation

Ø Australia, New Zealand, Singapore, Israel, Lebanon, Qatar

NEXT GEN ACCESS

• LTE based open Access • 700/800 MHz bands (DD) • National/rural coverage, Public Safety

Ø Mexico, Kenya, Indonesia, Oklahoma State (U.S.)

OPEN WIRELESS ACCESS

• Fibre based open backbones • Fixed /mobile backhauling, transit • National/rural coverage

Ø Brazil, Mexico, India, Kenya, Nigeria, Sri Lanka, Ghana, Colombia, Argentina, Venezuela, Peru

NATIONAL BACKBONES

• NGA roll-out is not an evolution but more the building of a new

essential infrastructure for the 40 years to come.

• The achievement of the ‘EC digital agenda targets’ requires innovative and flexible NGA solutions

• New investment models, new regulatory thinking will be needed

for NGA roll-out to attract long term investors

IN A NUTSHELL,