FYI June 12, 2015 Jeff Ammerman, Director of Technical Assistance,...

33

-

Upload

ambrose-ward -

Category

Documents

-

view

216 -

download

1

Transcript of FYI June 12, 2015 Jeff Ammerman, Director of Technical Assistance,...

• Listen to audio over your computer speakers. If you are not able to listen via the Internet, you can dial-in by phone using the numbers shown on your screen.

• If you disconnect, simply repeat instructions to reconnect to the program.• If listening to audio by phone, you can adjust the volume by pressing *4.• To submit a question, type in the chat window and click “Enter” to send. • CPE and CEU Credits are NOT available for this forum.

Thanks for Joining Us!

• Our Intent and Purpose– Strategic Plan Outreach and Mentorship Effort

for New and Newer PASBO Members in all aspects of School Business Management

– Use PASBO Experts to Help New Entrants– Continuing Series

• Time shift to 2nd Thursday of the Month at 1:30 pm• Taking the summer off• Next one will be Thursday, September 10 at 1:30 pm

3

Today’s Agenda

1. What's Due– Calendar of State and Federal Reports

2. PASBO Tools You Can Use– Resources to Help You

3. Audits an Auditor Preparation

4. Your Questions Answered– An Open Forum for Your Questions About Topics Covered and

Uncovered!4

Before We Start• The due dates on the calendar

are intended as a guide not as absolute deadline dates.

• The calendar is a work in progress and will be modified throughout the year.

• This is not an “official” calendar although it has been reviewed by PDE.

5

Sources of Filing and Reporting Info

• PIMS Data Collection Calendar http://www.portal.state.pa.us/portal/server.pt/community/pims-

pennsylvania_information_management_system/8959

• Comptroller Forms http://www.portal.state.pa.us/portal/server.pt/community/forms

_and_procedures/13472

• Food Service Calendar http://www.portal.state.pa.us/portal/server.pt/community/natio

nal_school_lunch/7487/activity_calendar/964588

6

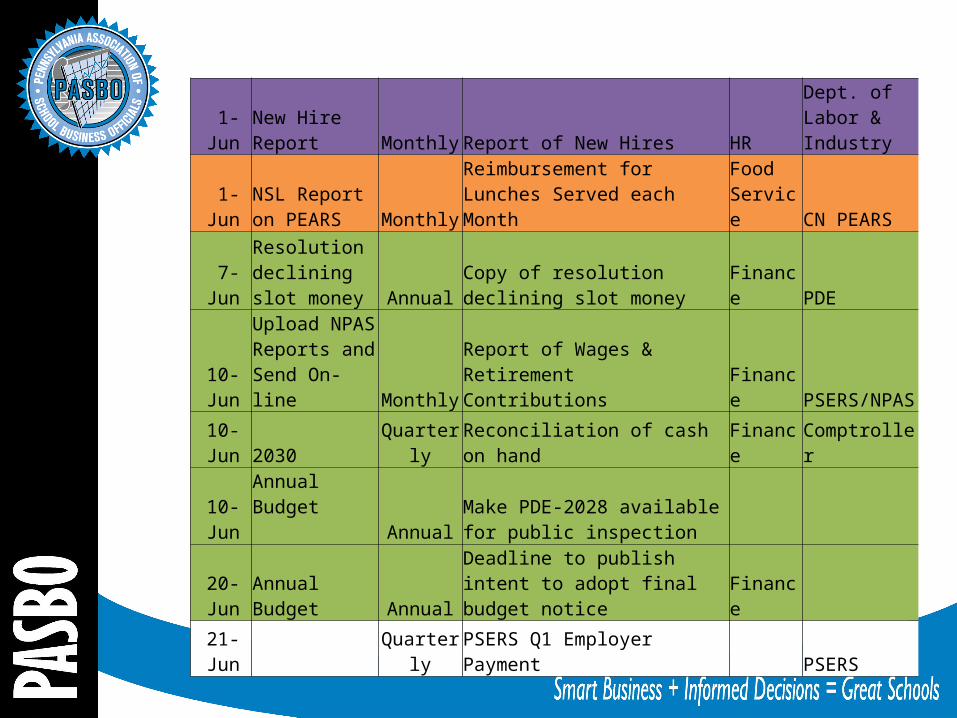

1-JunNew Hire Report Monthly Report of New Hires HR

Dept. of Labor & Industry

1-JunNSL Report on PEARS Monthly

Reimbursement for Lunches Served each Month

Food Service CN PEARS

7-Jun

Resolution declining slot money Annual

Copy of resolution declining slot money Finance PDE

10-Jun

Upload NPAS Reports and Send On-line Monthly

Report of Wages & Retirement Contributions Finance PSERS/NPAS

10-Jun 2030 Quarterly Reconciliation of cash on hand Finance Comptroller

10-Jun

Annual Budget Annual

Make PDE-2028 available for public inspection

20-Jun Annual Budget Annual

Deadline to publish intent to adopt final budget notice Finance

21-Jun Quarterly PSERS Q1 Employer Payment PSERS

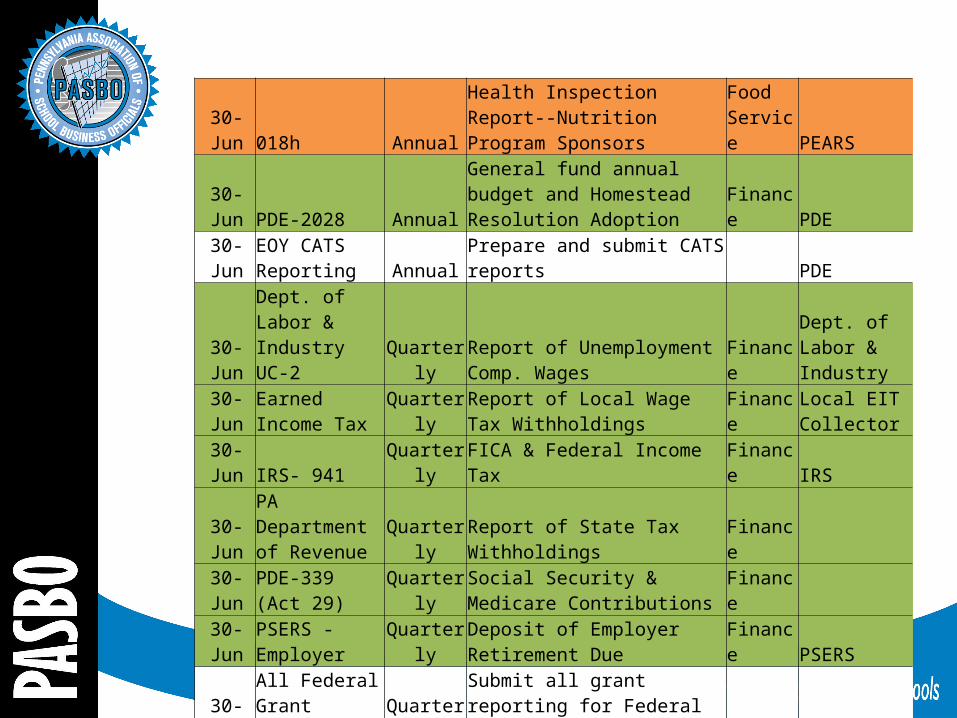

30-Jun 018h Annual

Health Inspection Report--Nutrition Program Sponsors

Food Service PEARS

30-Jun PDE-2028 Annual

General fund annual budget and Homestead Resolution Adoption Finance PDE

30-Jun

EOY CATS Reporting Annual Prepare and submit CATS reports PDE

30-Jun

Dept. of Labor & Industry UC-2 Quarterly

Report of Unemployment Comp. Wages Finance

Dept. of Labor & Industry

30-Jun

Earned Income Tax Quarterly

Report of Local Wage Tax Withholdings Finance

Local EIT Collector

30-Jun IRS- 941 Quarterly FICA & Federal Income Tax Finance IRS30-Jun

PA Department of Revenue Quarterly Report of State Tax Withholdings Finance

30-Jun PDE-339 (Act 29) Quarterly

Social Security & Medicare Contributions Finance

30-Jun

PSERS - Employer Quarterly

Deposit of Employer Retirement Due Finance PSERS

30-Jun

All Federal Grant reporting Quarterly

Submit all grant reporting for Federal programs. FAI

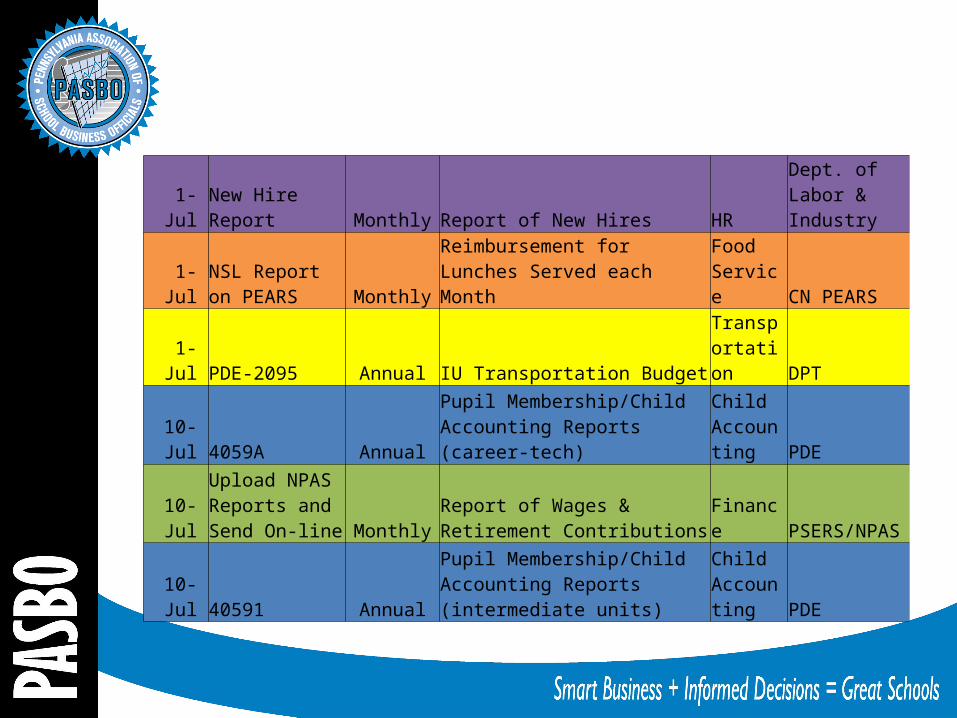

1-Jul New Hire Report Monthly Report of New Hires HRDept. of Labor & Industry

1-JulNSL Report on PEARS Monthly

Reimbursement for Lunches Served each Month

Food Service CN PEARS

1-Jul PDE-2095 Annual IU Transportation BudgetTransportation DPT

10-Jul 4059A AnnualPupil Membership/Child Accounting Reports (career-tech)

Child Accounting PDE

10-Jul

Upload NPAS Reports and Send On-line Monthly

Report of Wages & Retirement Contributions Finance PSERS/NPAS

10-Jul 40591 Annual

Pupil Membership/Child Accounting Reports (intermediate units)

Child Accounting PDE

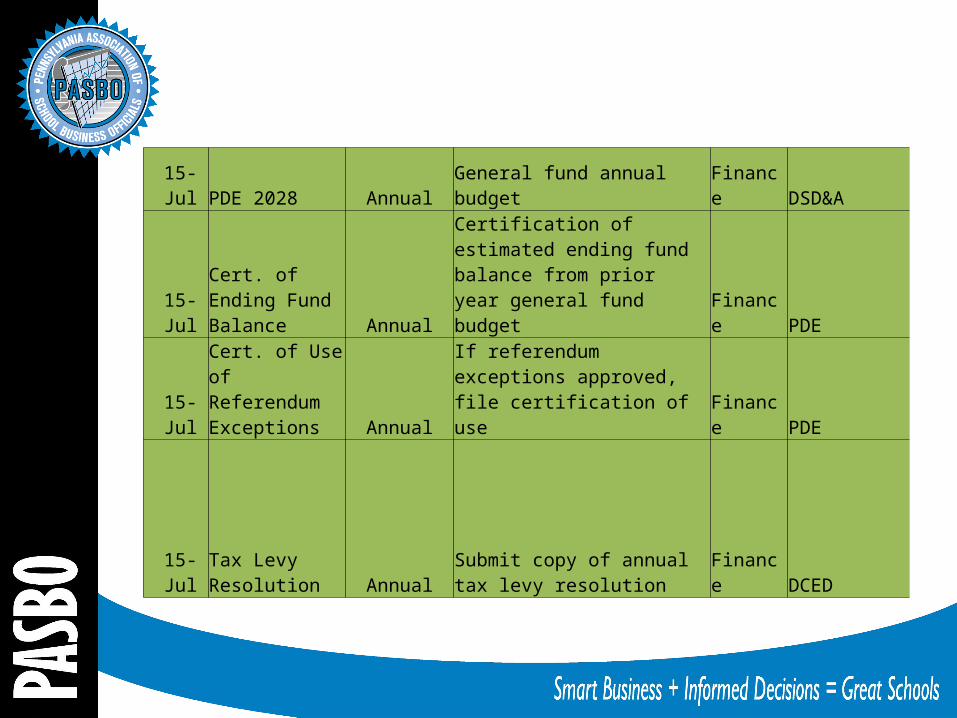

15-Jul PDE 2028 Annual General fund annual budget Finance DSD&A

15-JulCert. of Ending Fund Balance Annual

Certification of estimated ending fund balance from prior year general fund budget Finance PDE

15-Jul

Cert. of Use of Referendum Exceptions Annual

If referendum exceptions approved, file certification of use Finance PDE

15-JulTax Levy Resolution Annual

Submit copy of annual tax levy resolution Finance DCED

A “must attend” for all people new to a position in school business.

School Operations AcademyJuly 30-31, 2015Penn State Conference CenterState College, PA

Tracks in Business, Facilities, Food Service and Transportation will help you to: - learn proven techniques from experienced practitioners - gain ideas to create efficiencies and reduce costs- exchange challenges and solutions with your peers- build a network of contacts across the state

There’s a doc for that…

Delivering Best Practices and Good Ideas

www.pasboerc.org

at the Electronic Resource Center

Follow PASBOtwitter.com/pasbo_org Like PASBO

Add PASBO to your social networks

The Budget Blog• Invitation only site related to the State Budget• If you have not yet signed up, please send an

email to [email protected]• Sign-up is easy

What is an Audit?

• Provides an independent assessment of and reasonable assurance about whether an entity's reported financial condition, results, and use of resources are presented fairly.

Planning is the Key!!!

• “He who fails to plan, plans to fail” • “

Planning is bringing the future into the present so that you can do something about it now”

• “Expect the best, plan for the worst, and prepare to be surprised.”

Planning

Generally accepted auditing standards require auditors to use information gathered about the entity and its environment to :– Identify and assess the risks of material

misstatement.

– Determine the nature, timing, and extent of further audit procedures needed to respond to those risks.

Planning

During the planning process, the auditor gains sufficient knowledge of the client to:

– Identify risky audit areas.

– Determine the procedures necessary to address identified risks.

Planning

– For lower-risk areas, the auditor determines what limited procedures will be necessary.

– The additional time spent applying risk assessment during the planning process may be more than offset by efficiencies gained from limiting procedures in lower-risk areas.

– Because the auditor is focusing his or her efforts on higher-risk areas, the audit approach is more effective.

Planning

Entrance Meeting- items to consider

• Discuss blocks of vacation or illness time. • Inform staff of the impending audit.

• Explain the audit process and timing to staff.

• Designate key contact personnel.

• Review and sign the engagement letter.

Planning

Suggested Procedures– Review the general ledger for any journal entries that need to

be posted.– Examine the balance sheet for any uncollected receivables – Update the capital asset inventory.– Update the District's accrued sick and vacation liability.– Review prior year audit findings and ensure that corrective

action was taken.– Assemble a central file of audit information.– Ensure that receipts and expenditures are posted to the

correct general ledger accounts.

Planning

Information Request List • Review the information request list and

determine if the items requested are available.

• Inform the auditor if any of the items requested are not available.

Fieldwork

• SAS No. 110 states that “the auditor should design and perform further audit procedures whose nature, timing, and extent are responsive to the assessed risks of material misstatement at the relevant assertion level.”

• The auditor must develop an audit plan in which the auditor documents the audit procedures to be used that, when performed, are expected to reduce audit risk to an acceptably low level.

Fieldwork

AICPA Fieldwork Standards:– The auditor must adequately plan the work and must

properly supervise any assistants.

– The auditor must obtain a sufficient understanding of the entity and its environment, including its internal control, to assess the risk of material misstatement of the financial statements and to design the nature, timing, and extent of further audit procedures.

– The auditor must obtain sufficient appropriate audit evidence by performing audit procedures to afford a reasonable basis for an opinion regarding the financial statements under audit.

Fieldwork

• By leveraging the knowledge gained through the auditing process, an auditor may also make suggestions to management on ways to improve internal controls to ensure accurate reporting and guard against fraudulent activities.

MD&A

• Management Discussion and Analysis (MD&A)

Section• Usually written by the Business Manager for

the LEA• MD&A should introduce the basic financial

statements and provide an analytical overview of the government’s financial activities.

• Required to present MD&A before the basic financial statements

More on MD&A

• Present financial information for the current and prior fiscal years, and management’s analysis is geared toward explaining how finances changed from year to year and why they changed

• Intended to bring to the financial report user’s attention key issues that affected or will affect an LEA’s financial health

Financial Statements

• Review the draft of the final audit report. • Review each section thoroughly • Ensure each section is accurate and complete. • Make revisions, if needed, to convey the

appropriate wording and tone.• Discuss the draft report with your senior

management.

Financial Statements

During Reporting• Ensure the auditor makes all proposed

revisions the report draft. • If no further revisions are required, a

final audit report is issued. • Share the final audit report with your

staff so they are informed about the results of the audit.

Final Communication

Management Letters • Address and resolve issues proactively

– Ensure the facts are correct. – Discuss the issue with the auditor and provide any

information that may be critical to understanding the full scope of the issue.

– Obtain supporting documentation to clear or resolve a potential finding.

Final Communication

Management Letter

• Keep your senior management apprised of the audit and any issues that arise.

• Discuss the planned corrective action plan.

• Prepare a written response.

Time for Questions!

Send text questions using the “Chat” function at the left side of your screen.

Type message in box and click “Enter” to send.

CPE and CEU Credits are not available for this forum.

Thank you for your participation!