FY 2013 RESULTS ANALYST BRIEFING - listed company · This presentation is not and does not...

26

FY 2013 RESULTS ANALYST BRIEFING 27 February 2014

Transcript of FY 2013 RESULTS ANALYST BRIEFING - listed company · This presentation is not and does not...

FY 2013 RESULTS

ANALYST BRIEFING

27 February 2014

This presentation is not and does not constitute an offer, invitation, solicitation or recommendation to subscribe for, or purchase, any securities

and neither this presentation nor anything contained in it shall form the basis of, or be relied on in connection with any contract or commitment or

investment decision.

This presentation has been prepared solely for use at this presentation. By your continued attendance at this presentation, you are deemed to

have agreed and confirmed to Telekom Malaysia Berhad (the “Company”) that: (a) you agree not to trade in any securities of the Company or its

respective affiliates until the public disclosure of the information contained herein; and (b) you agree to maintain absolute confidentiality

regarding the information disclosed in this presentation until the public disclosure of such information, or unless you have been otherwise

notified by the Company.

Reliance should not be placed on the information or opinions contained in this presentation or on its completeness. This presentation does not

take into consideration the investment objectives, financial situation or particular needs of any particular investor.

No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information,

opinions and conclusions contained in this presentation. None of the Company and its affiliates and related bodies corporate, and their

respective officers, directors, employees and agents disclaim any liability (including, without limitation, any liability arising from fault or

negligence) for any loss arising from any use of this presentation or its contents or otherwise arising in connection with it.

This presentation contains projections and “forward-looking statements” relating to the Company’s business and the sectors in which the

Company operates. These forward-looking statements include statements relating to the Company’s performance. These statements reflect the

current views of the Company with respect to future events and are subject to certain risks, uncertainties and assumptions. It is important to note

that actual results could differ materially from those anticipated in these forward looking statements. The Company does not undertake to inform

you of any matters or information which may come to light or be brought to the Company’s attention after the date hereof.

The forecasts and other forward-looking statements set out in this presentation are based on a number of estimates and assumptions that are

subject to business, economic and competitive uncertainties and contingencies, with respect to future business decisions, which are subject to

change and in many cases outside the control of the Company. The directors and officers of the Company believe that they have prepared the

forecasts with due care and attention and consider all best estimates and assumptions when taken as a whole to be reasonable at the time of

preparing the presentation. However, the Company’s forecasts presented in this presentation may vary from actual financial results, and these

variations may be material and, accordingly, neither the Company nor its directors or officers can give any assurance that the forecast

performance in the forecasts or any forward-looking statement contained in this presentation will be achieved. Details of the forecasts and the

assumptions on which they are based are set out in the presentation.

This presentation may not be copied or otherwise reproduced without the written consent of TM.

Disclaimer

Performance Overview

Financial review

Operating highlights

Concluding remarks

3

Key Highlights

• Revenue growth in line with Headline KPI •Stronger Normalised EBIT Growth • Higher Customer Satisfaction Index 72

FY2013 Headline KPI

FY2013 Achievement

6%

3%

6.4%

18.2%

> 72

Broadband leadership: • 7.2% growth in total broadband customers

•41% of total customers are on high speed broadband (4Mbps and above)

•Positive growth driven by Data and Internet revenue •Normalised PATAMI grew by 17.9% to RM1.04bn • Total Capex/Revenue ratio from 25.5% to 17.5%

4

Achieved all headline KPI – 4th consecutive year

• Final dividend of 16.3 sen per share

•Total dividend payout of 26.1 sen per share or RM933.7mn

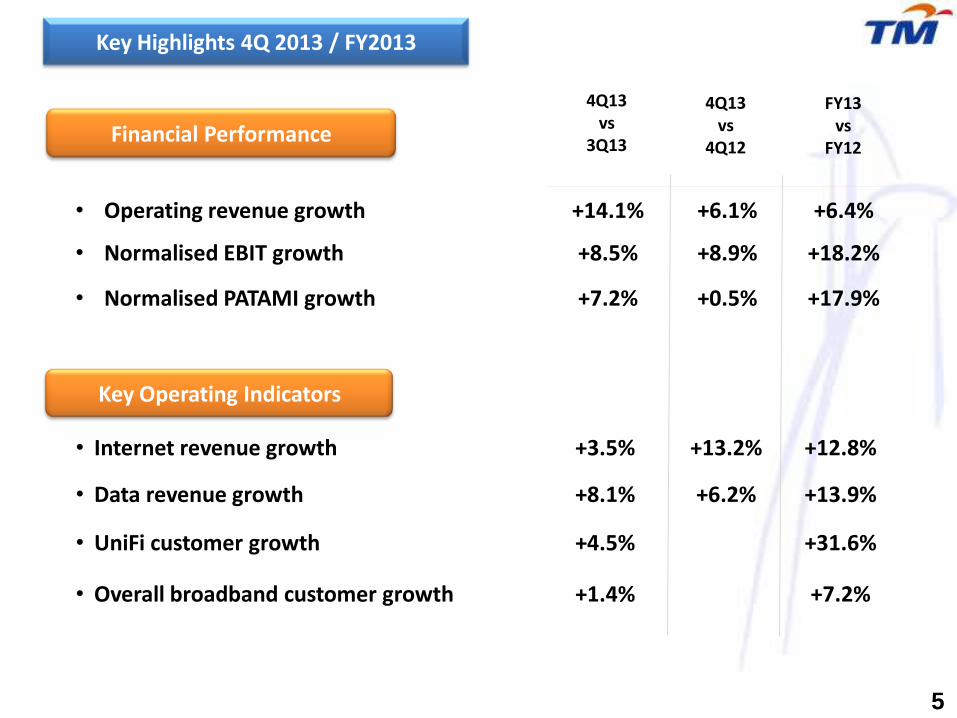

• Operating revenue growth +14.1% +6.1% +6.4%

• Normalised EBIT growth +8.5% +8.9% +18.2%

• Normalised PATAMI growth +7.2% +0.5% +17.9%

Key Operating Indicators

Key Highlights 4Q 2013 / FY2013

Financial Performance

5

• Internet revenue growth +3.5% +13.2% +12.8%

• Data revenue growth +8.1% +6.2% +13.9%

• UniFi customer growth +4.5% +31.6%

• Overall broadband customer growth +1.4% +7.2%

4Q13 vs

3Q13

4Q13 vs

4Q12

FY13 vs

FY12

Performance Overview Financial review Operating highlights

Concluding remarks

6

Group Results FY 2013 & 4Q2013

7

RMmn

Reported

4Q13 3Q13 % Change

QoQ 4Q12**

% Change YoY

FY13 FY12** % Change

FY13 vs FY12

Revenue 2,979.8 2,610.5 +14.1 2,809.3 +6.1 10,628.7 9,993.5 +6.4

Other Operating Income

35.8 32.5 +10.2 74.2 -51.8 121.5 165.4 -26.5

EBITDA 958.0 906.3 +5.7 901.8 +6.2 3,531.6 3,233.3 +9.2

Depn & Amort. 578.8 541.4 +6.9 508.0 +13.9 2,159.7 2,046.4 +5.5

EBIT 379.2 364.9 +3.9 393.8 -3.7 1,371.9 1,186.9 +15.6

Net Finance Cost* 60.8 59.5 +2.2 54.7 +11.2 226.3 191.9 +17.9

FX (Gain) / Loss 8.7 43.8 -80.1 (5.4) ->100.0 105.2 (73.4) ->100.0

Profit Before Tax (PBT) 309.7 264.9 +16.9 346.2 -10.5 1,046.0 1,069.6 -2.2

PATAMI 344.2 240.9 +42.9 363.2 -5.2 1,012.2 1,263.7 -19.9

Normalised PATAMI 289.7 270.3 +7.2 288.4 +0.5 1,038.5 881.0 +17.9

Note: For Normalised EBIT and Normalised PATAMI refer Slides 8 and 9 •Excludes FX (Gain )/Loss ** Restated due to adoption of MFRS 116 in 2013

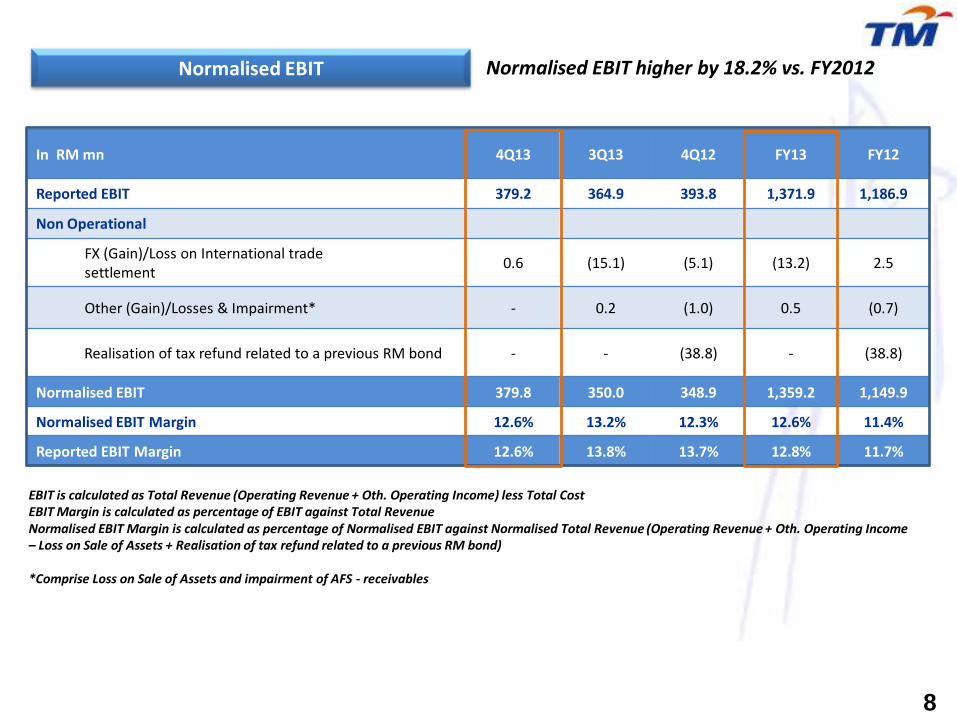

Revenue exceeded RM10bn and Normalised PATAMI exceeded RM1bn

Normalised EBIT Normalised EBIT higher by 18.2% vs. FY2012

In RM mn 4Q13 3Q13 4Q12 FY13 FY12

Reported EBIT 379.2 364.9 393.8 1,371.9 1,186.9

Non Operational

FX (Gain)/Loss on International trade settlement 0.6 (15.1) (5.1) (13.2) 2.5

Other (Gain)/Losses & Impairment* - 0.2 (1.0) 0.5 (0.7)

Realisation of tax refund related to a previous RM bond - - (38.8) - (38.8)

Normalised EBIT 379.8 350.0 348.9 1,359.2 1,149.9

Normalised EBIT Margin 12.6% 13.2% 12.3% 12.6% 11.4%

Reported EBIT Margin 12.6% 13.8% 13.7% 12.8% 11.7%

EBIT is calculated as Total Revenue (Operating Revenue + Oth. Operating Income) less Total Cost EBIT Margin is calculated as percentage of EBIT against Total Revenue Normalised EBIT Margin is calculated as percentage of Normalised EBIT against Normalised Total Revenue (Operating Revenue + Oth. Operating Income – Loss on Sale of Assets + Realisation of tax refund related to a previous RM bond) *Comprise Loss on Sale of Assets and impairment of AFS - receivables

8

Normalised PATAMI

9

Normalised PATAMI 17.9% higher vs. FY2012

In RM mn 4Q13 3Q13 4Q12 FY13 FY12

Reported PATAMI 344.2 240.9 363.2 1,012.2 1,263.7

Non Operational

FX (Gain)/Loss on International trade Settlement 0.6 (15.1) (5.1) (13.2) 2.5

Realisation of tax refund related to a previous RM bond - - (38.8) - (38.8)

Other (Gain)/Losses & Impairment* 0.7 0.7 (1.5) (1.2) (1.0)

Unrealised FX (Gain)/Loss on Long Term Loans

8.7 43.8 (5.4) 105.2 (73.4)

Tax Incentives** (29.5) - (53.4) (29.5) (301.4)

S108 impact from utilisation of tax incentives - - 29.4 - 29.4

Impact of tax rate changes (35.0) - - (35.0) -

Normalised PATAMI** 289.7 270.3 288.4 1,038.5 881.0

*Comprise fair value (FV) changes of FVTPL (FV through P&L) investment gain/loss on disposal for AFS (available for sale) investments, Loss on Sale of Assets and impairment of AFS - receivables

**Current year tax incentives: FY13: RM162.8mil (HSBB), FY12: RM188.4mil [RM56.0mil (last mile), RM132.4mil (HSBB)]

Cost % of Revenue1

Note: The classification of cost is as per financial reporting

(Please refer to Appendix for quarterly details & breakdown)

Healthier total cost/revenue ratio despite higher manpower & content cost

FY 2013 vs. FY 2012 •Higher Direct cost due to higher

content cost, USP cost, leased charges and domestic outpayment •Higher Manpower cost due to higher salaries and staff benefits •Lower Maintenance cost due to lower customer projects •Lower Marketing cost due to lower A&P activities

10

20.1 20.1

17.0 17.2

19.9 21.0

11.6 10.9

8.5 7.1

6.3 6.4

4.2 3.7 0.6 0.8

FY12 FY13

Bad debt

Marketing expenses

Supplies & material

Maintenance cost

Other operating cost

Manpower cost

Direct cost

Dep & Amortisation

Revenue = Operating Revenue + Other Operating Income 1

RM mn RM mn

Total Cost / Revenue ( %)

RM8,972.0

88.3%

RM9,378.3

87.2%

% of Revenue

781 479

645

516

228

171

0

500

1000

1500

2000

FY12 FY13

Access Core Network Support System*

338 269

278

129

276

299

0

200

400

600

800

1000

FY12 FY13 Access Core Network Support System*

1,119 748

923

645

504

470

0

500

1,000

1,500

2,000

2,500

3,000

FY12 FY13

Access Core Network Support System*

Lower capex/revenue ratio Group Capital Expenditure

** Gross capex to be shared with Government equally up to RM4.8bn (fully paid as at July 2012) Note: Government coinvestment treated as deferred income, to be amortised progressively to match against the depreciation of assets

*Include Application, Support System & Others (building, land improvement, moveable plants, application & other assets)

HSBB Capex**

Note : BAU – Business As Usual

RM mn

2,546

1,654

25.5

BAU Capex

892

8.9

Capex / Revenue ( %)

1,166

697

6.6

1,863

17.5

11.0 16.6

Total Capex

11

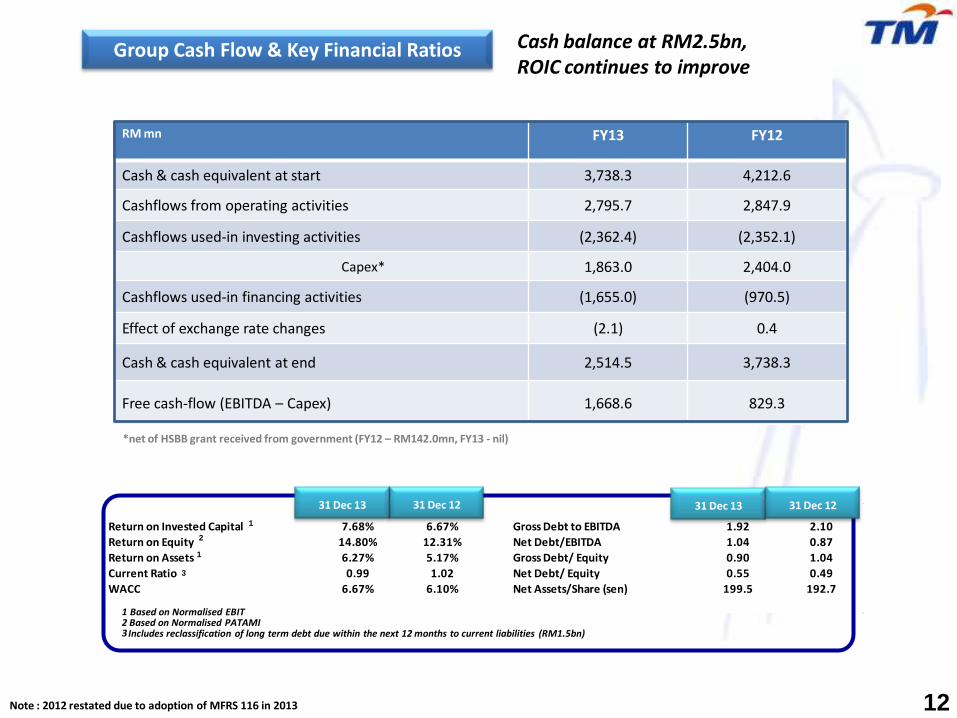

Group Cash Flow & Key Financial Ratios

12

Cash balance at RM2.5bn, ROIC continues to improve

31 Dec 13 31 Dec 12 31 Dec 13 31 Dec 12Return on Invested Capital 7.68% 6.67% Gross Debt to EBITDA 1.92 2.10

Return on Equity 14.80% 12.31% Net Debt/EBITDA 1.04 0.87

Return on Assets 6.27% 5.17% Gross Debt/ Equity 0.90 1.04

Current Ratio 0.99 1.02 Net Debt/ Equity 0.55 0.49

WACC 6.67% 6.10% Net Assets/Share (sen) 199.5 192.7

31 Dec 13 31 Dec 12

RM mn FY13 FY12

Cash & cash equivalent at start 3,738.3 4,212.6

Cashflows from operating activities 2,795.7 2,847.9

Cashflows used-in investing activities (2,362.4) (2,352.1)

Capex* 1,863.0 2,404.0

Cashflows used-in financing activities (1,655.0) (970.5)

Effect of exchange rate changes (2.1) 0.4

Cash & cash equivalent at end 2,514.5 3,738.3

Free cash-flow (EBITDA – Capex) 1,668.6 829.3

31 Dec 12 31 Dec 13

*net of HSBB grant received from government (FY12 – RM142.0mn, FY13 - nil)

3

3 Includes reclassification of long term debt due within the next 12 months to current liabilities (RM1.5bn)

Based on Normalised EBIT Based on Normalised PATAMI

1

1

2

2 1

Note : 2012 restated due to adoption of MFRS 116 in 2013

Performance Overview

Financial review

Operating highlights

Concluding remarks

13

Voice 37%

Data 22%

Internet 24%

Other 17%

Voice 34%

Data 24%

Internet 25%

Other 17%

630 398

673 1,711 1,823

4Q12 3Q13 4Q13 FY12 FY13

626 686 709 2,372 2,676

4Q12 3Q13 4Q13 FY12 FY13

907 892 911 3,706 3,618

4Q12 3Q13 4Q13 FY12 FY13

Group Total Revenue by Product

Data

RM mn

RM mn RM mn

Voice*

Others**

Internet* FY13

FY12

RM mn RM mn

RM mn

RM10,629mn

RM9,994mn

* Reclassification between Voice and Internet of RM30mn in 2Q13 **Others comprise other telco and non-telco services (i.e ICT-BPO, MMU tuition fees, customer projects)

+0.5%

+2.1%

Revenue growth driven by Internet and Data

-2.4% +13.2%

+3.5%

+12.8%

+6.2%

+8.1%

+13.9% +6.7%

+69.2%

+6.5%

14

646 635 687 2,205 2,512

4Q12 3Q13 4Q13 FY12 FY13

Positive growth across all segments

15

Group Total Revenue by Line of Business

* Others comprise revenue from VADS, Property Development, TM R&D, TMIM, UTSB and MKL

2,035 1,947 2,207

7,454 7,965

4Q12 3Q13 4Q13 FY12 FY13

Global & Wholesale

FY13 FY12 RM10,629mn RM9,994mn

Retail

RM mn RM mn RM mn

Others*

Retail (C+S+E+G): 75% Retail (C+S+E+G): 74%

+8.5%

+13.4%

+6.9% +4.6%

+8.1%

+3.4% -7.5%

+32.4%

+7.6%

318 222

294

890 958

4Q12 3Q13 4Q13 FY12 FY13

457 442 478

1,650 1,706

4Q12 3Q13 4Q13 FY12 FY13

Retail 75%

Global & Wholesale

16%

Others 9%

Retail 74%

Global & Wholesale

17%

Others 9%

2,390 2,364 2,337 2,317 2,296

1,486 1,474 1,463 1,453 1,442

483 532 577 607 635

4Q12 1Q13 2Q13 3Q13 4Q13

Fixed Line Residential Fixed Line Business UniFi

406 448 484 509 530

77 84

93 98 105

4Q12 1Q13 2Q13 3Q13 4Q13

UniFi Residential UniFi Business

1,296 1,292 1,291 1,290 1,292

287 285 285 287 288

483 532 577 607 635

4Q12 1Q13 2Q13 3Q13 4Q13

Streamyx Residential Streamyx Business UniFi

Net adds (in thousand)

In thousand

In thousand

+7.2%

+1.4%

Physical Highlights

Broadband Customer Growth

Fixed Line Customer Growth

+43

4,370

2,109

Net adds (in thousand)

532

UniFi

+49

Healthy broadband growth and higher ARPU across products

2,066

483

4,359

16

*Call Usage Only ** Streamyx Net ARPU *** Blended ARPU

ARPU (RM) 4Q12 1Q13 2Q13 3Q13 4Q13

Fixed Line (DEL)* 32 31 32 31 33

Streamyx Broadband** 81 80 82 83 85

UniFi*** 181 178 180 183 185

ARPU

577

+45

+44

2,153

4,377

In thousand

+30

607 2,184

+31

4,377

2,215

+31 +28

635

4,373

+31.6%

+4.5%

+0.3%

-0.1%

Performance Overview

Financial review

Operating highlights

Concluding remarks

17

Key Takeaways

Financial Performance

Broadband Champion

• Achieved all Headline KPI’s 6.4% revenue growth, driven by Internet and Data Normalised EBIT growth 18.2%

• Normalised PATAMI grew by 17.9% • Sustained capital and cost efficiency: Cost/Revenue ratio

improved to 87.2%

• Total broadband customer base grown to 2.2mn • Increasing number of customers on high speed broadband

41% of total broadband customers on 4Mbps and above >650,000 Unifi customers to date; 43% takeup rate

Shareholder Value

Customer-centricity

• Commitment to create shareholder value • Total dividend payout of 26.1 sen per share or RM933.7mn

(including interim dividend of 9.8 sen per share or RM350.6mn paid in September 2013)

• Successful implementation of improvement initiatives • Achieved TRI*M Index score of >72

18

Outlook 2014

19

MALAYSIA’S BROADBAND CHAMPION

Enabling a digital lifestyle – Life Made Easier, Business Made Easier Innovative offerings across segments with enhanced customer service Expansion of broadband services in under-served areas Complement TM’s existing suite of fixed broadband services

INFORMATION & INNOVATION EXCHANGE

Integrated ICT player for Managed Accounts Beyond Connectivity - providing more end-to-end

and value-added services, Managed Services, cloud services and BPO

Content and Applications Drive

PERFORMANCE IMPROVEMENT PROGRAM 3.0

Continued growth Fundamental productivity shift Institutional health drivers

20

Headline KPI

2014 2016

Revenue Growth

EBIT Growth

Customer Satisfaction Measure

5.0-5.5% 6%

5% 8%

72 72

1 Using TRiM index measuring end to end customer experience at all touch points. TRiM (Measuring, Managing and Monitoring) is a standardized indicator system. It analyzes, measures and portrays stakeholder relationships on the basis of standardized indicators. The TRI*M Index is an indicator of the status quo of a particular relationship. The index is made up of four points of view on the stakeholder relationship, e.g. for customer loyalty: overall rating, recommendation, repeat purchasing of product/services, and a company's competitive advantage. The information is based on surveys/interviews on a sample customer base.”

Appendices

Normalised EBITDA Normalised EBITDA higher by 10.1% vs. FY2012

22

In RM mn 4Q13 3Q13 4Q12 FY13 FY12

Reported EBITDA 958.0 906.3 901.8 3,531.6 3,233.3

Non Operational

FX (Gain)/Loss on International trade settlement 0.6 (15.1) (5.1) (13.2) 2.5

Other (Gain)/Losses & Impairment* - 0.2 (1.0) 0.5 (0.7)

Realisation of tax refund related to a previous RM bond - - (38.8) - (38.8)

Normalised EBITDA 958.6 891.4 856.9 3,518.9 3,196.3

Normalised EBITDA Margin 31.8% 33.7% 30.1% 32.7% 31.6%

Reported EBITDA Margin 31.8% 34.3% 31.3% 32.9% 31.8%

EBITDA is calculated as Total Revenue (Operating Revenue + Oth. Operating Income) less Operating Cost (Exc. Depreciation, Amortisation & Impairment). EBITDA Margin is calculated as percentage of EBITDA against Total Revenue Normalised EBITDA Margin is calculated as percentage of Normalised EBITDA against Normalised Total Revenue (Operating Revenue + Oth. Operating Income – Loss on Sale of Assets + Realisation of tax refund related to a previous bond) *Comprise Loss on Sale of Assets and impairment of AFS - receivables

Cost % of Revenue

23

4Q13 3Q13 4Q12 FY13 FY12

Comments (FY2013 vs. FY2012)

Operating Revenue (RM mil) 2,979.8 2,610.5 2,809.3 10,628.7 9,993.5 -

Other Operating Income (RM mil)

35.8 32.5 74.2 121.5 165.4 -

Direct Costs % 17.1 18.4 15.5 17.2 17.0 Higher due to content cost, leased charges and USP cost RM mil. 516.9 485.5 447.4 1,850.3 1,729.7

Manpower % 20.4 20.3 21.0 21.0 19.9 Higher due to salaries and staff benefits RM mil. 614.3 536.7 604.7 2,260.3 2,024.5

Supplies & Materials % 7.0 6.3 6.8 6.4 6.3 Higher due to customer projects

RM mil. 211.9 167.5 195.9 692.8 644.6

Bad & Doubtful Debts % 0.9 0.8 (0.1) 0.8 0.6 Higher due to impairment of trade receivables RM mil. 27.2 21.6 (4.0) 89.9 63.7

Marketing Expenses % 4.2 3.2 3.9 3.7 4.2 Lower A&P activities

RM mil. 125.7 84.4 112.3 394.1 422.3

Maintenance Cost % 8.4 6.5 9.3 7.1 8.5 Lower customer projects at TM Government RM mil. 254.8 172.6 266.9 763.4 860.6

Other Operating Costs % 10.2 10.2 12.4 10.9 11.6 Lower property development cost

RM mil. 306.8 268.4 358.5 1,167.8 1,180.2

Depreciation & Amortisation % 19.2 20.5 17.6 20.1 20.1 Higher absolute cost due to accelerated depreciation of CDMA and USP assets RM mil. 578.8 541.4 508.0 2,159.7 2,046.4

Total (RM mil) 2,636.4 2,278.1 2,489.7 9,378.3 8,972.0 -

Total (%) 87.4 86.2 86.3 87.2 88.3 -

Group Balance Sheet

24

6,894.8

165.2

8,513.7

5,130.2

1,202.6

2,129.4

51.5

-

15,573.7

6,724.7

1,740.9

466.1

3,738.7

779.0

6,622.2

3,545.5

2,010.2

1,066.5

102.5

14,721.7

749.5

15,573.7

As at 31 Dec 2012**

7,136.7

162.6

8,076.7

4,865.0

1,151.0

1,999.5

51.4

9.8

15,376.0

5,722.2

1,847.7

440.9

2,514.9

918.7

5,770.5

3,172.8

1,590.2

1,007.5

(48.3)

14,572.0

852.3

15,376.0

Shareholders’ Funds

Non-Controlling Interests

Deferred & Long Term Liabilities

Long Term Borrowings

Deferred Tax

Deferred Income

Derivative financial liabilities

Long Term Employee Benefit

Current Assets

Trade Receivables

Other Receivables

Cash & Bank Balances

Others

Current Liabilities

Trade and Other Payables

Short Term Borrowings

Others

Net Current (Liabilities)/Assets*

Property Plant & Equipment

Other Non-Current Assets

RM Million As at 31 Dec 2013

*Due to reclassification of long term debt due within the next 12 months to current liability (RM1.5bn) **Restated due to adoption of MFRS 116 in 2013

RETAIL

25

737 730 754 3,010 2,985 392 385 390

1,356 1,546 625 684 706

2,359 2,671

286 156 373

765 808

4Q12 3Q13 4Q13 FY12 FY13

Others

Internet

Data

Voice

RM mn +13.4%

+8.5%

2,207 1,947 2,035

Revenue by Product

7,965 7,454

+6.9%

RM mn

Revenue by Product

182 164 155 719 636

311 307 340

1,048 1,160 22 28 29

91 108

4Q12 3Q13 4Q13 FY12 FY13

Others

Data

Voice

Others : Include internet

Note: Total revenue is after inter-co elimination. Revenue of product is before inter-co elimination

457 442 478

1,649 1,706

+8.1%

+4.6% +3.5%

GLOBAL & WHOLESALE

THANK YOU Any queries please email to : [email protected]

•Investor Relations • Level 11 (South Wing) •Menara TM •JlnPantaiBharu •50672 Kuala Lumpur, Malaysia • Tel (603) 2240 4848/ 7366 / 7388