Futuristic Trends in Auto Industry - · PDF file800 1000 1200 1984-85 1988-89 1993-94 1998-99...

40

Futuristic Trends in Auto Futuristic Trends in Auto Industry Industry

Transcript of Futuristic Trends in Auto Industry - · PDF file800 1000 1200 1984-85 1988-89 1993-94 1998-99...

Futuristic Trends in Auto Futuristic Trends in Auto IndustryIndustry

Contents

Auto Industry• Current scenario in India• Trends in Maruti Suzuki• Futuristic Trends• Alignment with Global markets

Plastic Industry• Current trend in plastic Industry• Future Perspective

Indian Automotive Space

India plans to become the Global Small Car Hub.

NORTH

EAST

WEST

SOUTH

MAN

New Hub : Uttarakhand

Bangalore

Sanand

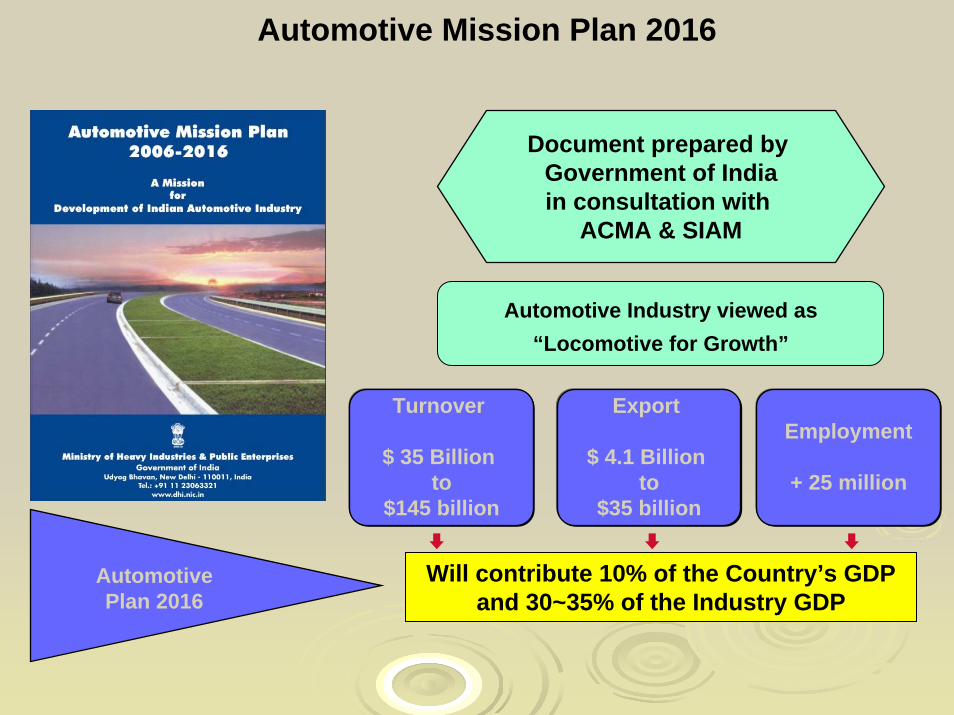

Automotive Mission Plan 2016

Automotive Industry viewed as “Locomotive for Growth”

Turnover

$ 35 Billion to

$145 billion

Automotive Plan 2016

Will contribute 10% of the Country’s GDP and 30~35% of the Industry GDP

Document prepared by Government of Indiain consultation with

ACMA & SIAM

Export

$ 4.1 Billion to

$35 billion

Employment

+ 25 million

Automotive Mission Plan 2016

9X

3X2X

5X

0

5

10

Industry Revenue GDP Share Employment Exports

Automotive Growth Pattern

CAGR 16% CAGR 24%

CAGR 12%

Passenger Car (Mn Units)

0.75

1.7

0.0

0.5

1.0

1.5

2.0

2002 2003 2004 2005 2006 2007

Commercial Vehicles (Mn units)

0.15

0.50

00.1

0.2

0.3

0.4

0.5

0.6

2002 2003 2004 2005 2006 2007

Two Wheelers (Mn units)

4.3

8.5

0.0

2.0

4.0

6.0

8.0

10.0

2002 2003 2004 2005 2006 2007

6Robust growth

Total production 11 Mn vehicles

Automobile Demand Drivers

Car Market Demand Drivers

Favourable govt policies

Availability of Consumer Finance

Household Income Trends

Traffic & InfrastructureVehicle Prices

Product Availability /Access

RAPIDLY EXPANDING CONSUMER BASE

“Rich”CAGR: 15%

“Upper Middle”CAGR: 10%

“Middle Income”CAGR: 2%

“Lower Income”CAGR: -8%

Household Income Class 1995-96 2001-02 2009 (E)

1.2 (7) 2.6 (15) 7.0 (40)

91 (525)46.4 (265)32.5 (186)

85 (490)74.4 (429)54.1 (312.2)

30 (177)57.2 (332)77.0 (444.3)

Number of households** (population), millionsSource : NCAER Upward shift towards affluence

Auto Growth Drivers-Redn Tariff RatesNet Custom Duty

41.26

36.03

30.80

20.00

15.6813.11

10.84 10.84

15

5.445.445.445.44

0.00

10.00

20.00

30.00

40.00

50.00

Mar-01

Mar-02

Mar-03

Mar-04

Mar-05

Mar-06

Mar'07

Mar'08

Auto-Components Steel

Excise Duty on Cars

40

32

24 24 24 24 24 2420

8

1614

12

0

10

20

30

40

50

2001

2002

2003

2004

2005

2006

2007

2008

2009

%

Big Car Small Car

Supportive Trend of Duty Structure

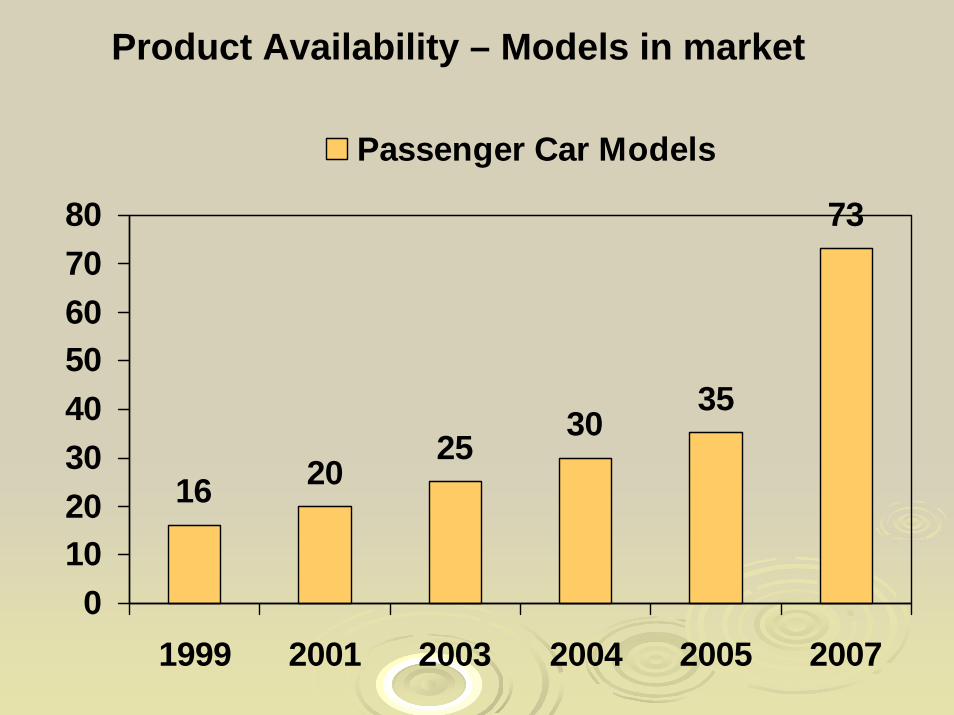

Product Availability – Models in market

16 2025

3035

73

01020304050607080

1999 2001 2003 2004 2005 2007

Passenger Car Models

RISING INDIA: INFRASTRUCTURE GROWTH

Source: N H A I

Seaports

Road Development

NHDP Planned length – 23,646 km

Golden Quadrilateral – Completed 94.77%

Railway East-West Freight Corridor

Total Investment USD 5.5billion.

Total Length 7700km

Two New Deep Ports with special emphasis to Auto Industry

Dhamra , Orissa : USD565 Miln

Sutrapada, Gujrat : USD156 Miln

Up gradation of Major Airports

Total Investment :USD11billion

Delhi-Mumbai Industrial Corridor to attract $90bn, will cover Six states and 450,000sq km(1483kmX300km )area.

Delhi-Mumbai Corridor

Delhi-Mumbai Corridor

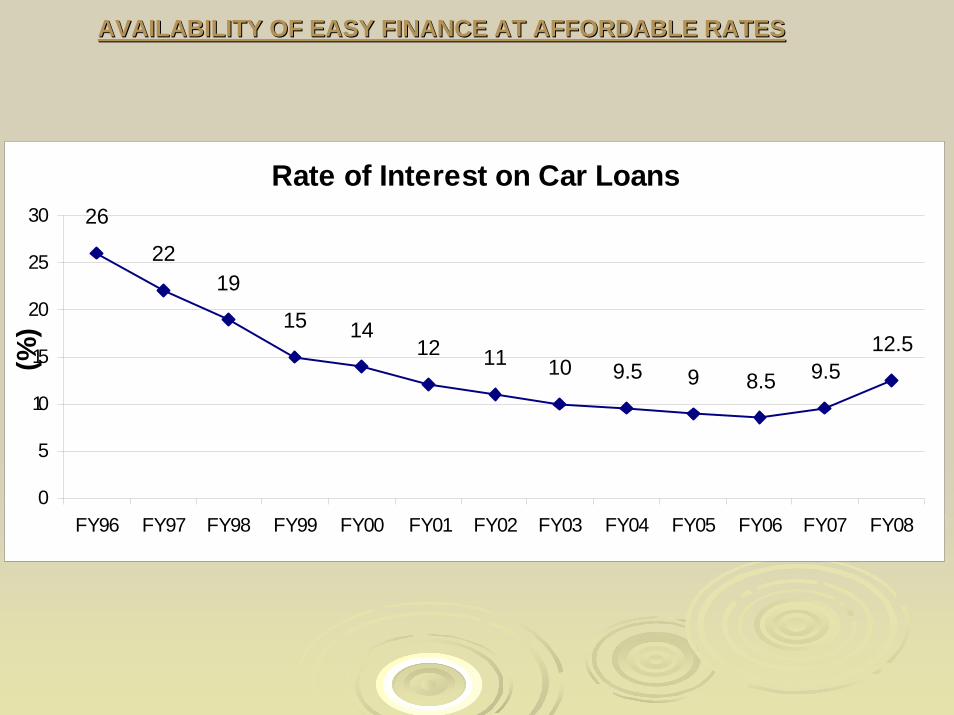

AVAILABILITY OF EASY FINANCE AT AFFORDABLE RATESAVAILABILITY OF EASY FINANCE AT AFFORDABLE RATES

Rate of Interest on Car Loans26

2219

15 1412 11 10 9.5 9 8.5 9.5

12.5

0

5

10

15

20

25

30

FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08

(%)

FAVOURABLE GOVERNMENT POLICIESFAVOURABLE GOVERNMENT POLICIES

WTO compliant policies

No restrictions on import

Tariff levels are being progressively reduced every

year

Conditions of import – to comply with emission and

safety norms as applicable to domestic companies

Increased engagements in Free Trade Agreements

Robust legal system

Passenger Vehicles In India

723,330

989,560

1,209,8761,309,300

1,545,223

1,762,131

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08

CAGR @ 16.35 %

Source: SIAM

Maruti Production Trend Maruti Production Trend -- ConsistentConsistent

22106

158

333 360473

540 572

>1000

667778

0

200

400

600

800

1000

1200

1984-85

1988-89

1993-94

1998-99

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2010-11

Year (Apr-Mar)

Nos

('00

0)

Total Production (in ‘000)

CAGR – 15.75%

CAGR – 16.67%

Indian Auto Component industry trendsIndian Auto Component industry trendsGreat opportunities for organic growth

Increasing domestic demand from all vehicle segments (as well as replacement market)Opportunities for exports increasing manifolds

Global OEMs sourcing from LCCsBig T-1s establishing supplier base in LCCsIndian cos venturing out for acquisitionsInternational Trade liberalization

Global giants gaining ground in India Greenfield ventures e.g., Saint Gobain, Magna Donnely, NTNPartnerships/acquisitions of local players e.g., Bosch(KBX), Mahle (Purolator)

OEMs venturing into components businessTACO, SYSTEC

Component suppliers shifting to module/system suppliers.Focus on design and development capability is continuously increasing.Local sourcing giving way to global sourcing as tariff barriers come down.

MSIL New Model Development Trend

IndiaManufacturing

Market

Design

India Specific & Re-designed

India Manufactured & designed

ab-initio

Globally Manufactured &

designed ab-initio

India

Global

Global

India Global

Suzuki existing model,

modified to suit India

New design,

new/existing platform

New design,

new/existing platform

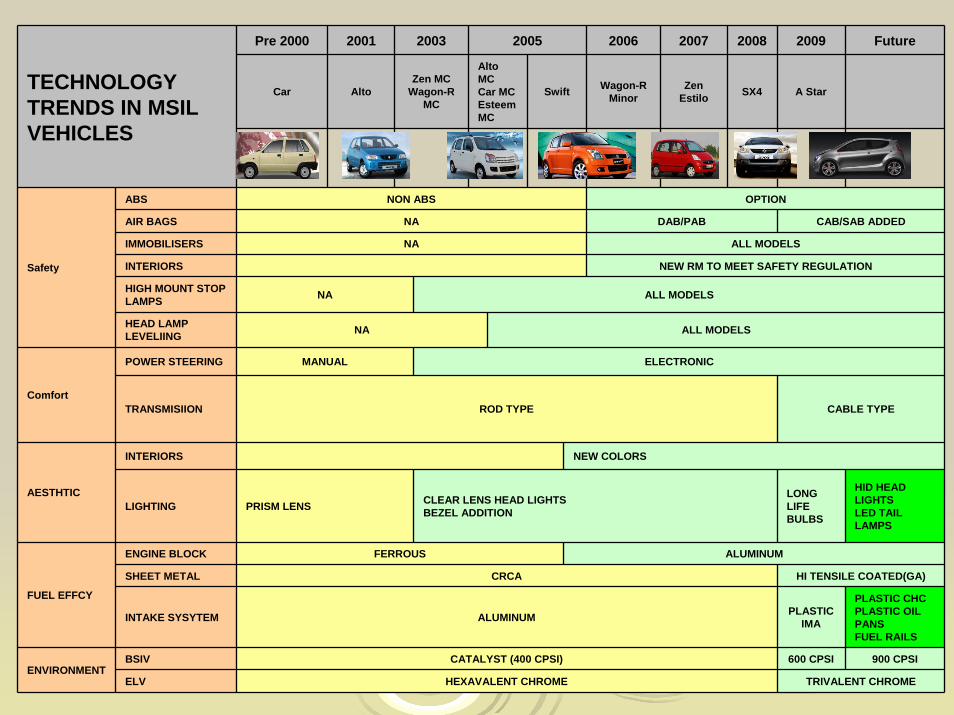

TECHNOLOGY TRENDS

Fuel efficient cars Light weight constructionLower CO2 emissionsHigher accelerationIncreasing emphasis on safetyNVH isolationMore attractive upholsteryMore & more environment regulation compliant (ELV, Asbestos free)Alternate fuels (CNG, LPG, E-10)

GLOBAL TECHNOLOGY TRENDS

Hybrid propulsionPlug in electric vehiclesMove towards Euro – 5 emission normsDrive by wireVoice controlGPS NavigationNight VisionHeads up display

Pre 2000 2001 2003 2005 2006 2007 2008 2009 Future

Car AltoZen MC

Wagon-R MC

Alto MCCar MCEsteem MC

Swift Wagon-R Minor

Zen Estilo SX4 A StarTECHNOLOGY

TRENDS IN MSIL VEHICLES

ABS NON ABS OPTION

AIR BAGS NA DAB/PAB CAB/SAB ADDED

IMMOBILISERS NA ALL MODELS

INTERIORS NEW RM TO MEET SAFETY REGULATION

HIGH MOUNT STOP LAMPS NA ALL MODELS

Safety

HEAD LAMP LEVELIING NA ALL MODELS

POWER STEERING MANUAL ELECTRONIC

ComfortTRANSMISIION ROD TYPE CABLE TYPE

INTERIORS NEW COLORS

AESTHTICLIGHTING PRISM LENS CLEAR LENS HEAD LIGHTS

BEZEL ADDITION

LONG LIFE BULBS

HID HEAD LIGHTSLED TAIL LAMPS

ENGINE BLOCK FERROUS ALUMINUM

SHEET METAL CRCA HI TENSILE COATED(GA)

FUEL EFFCY

INTAKE SYSYTEM ALUMINUM PLASTIC IMA

PLASTIC CHCPLASTIC OIL PANSFUEL RAILS

BSIV CATALYST (400 CPSI) 600 CPSI 900 CPSIENVIRONMENT

ELV HEXAVALENT CHROME TRIVALENT CHROME

Role of Plastics in Automobiles

Plastic Penetration in Passenger Vehicle (Forecast)

60 6777

8697

105

0

20

40

60

80

100

120

.07-08 .08-09 .09-10 .10-11 .11-12 .12-13

Plastic Consumption/Veh (Kg)

Indian Plastics Penetration (Avg) : 60 kg/veh. Global Plastics (Avg) : 120 Kg/veh.

22Increasing Plastic penetration by virtue of metal & other plastic replacement

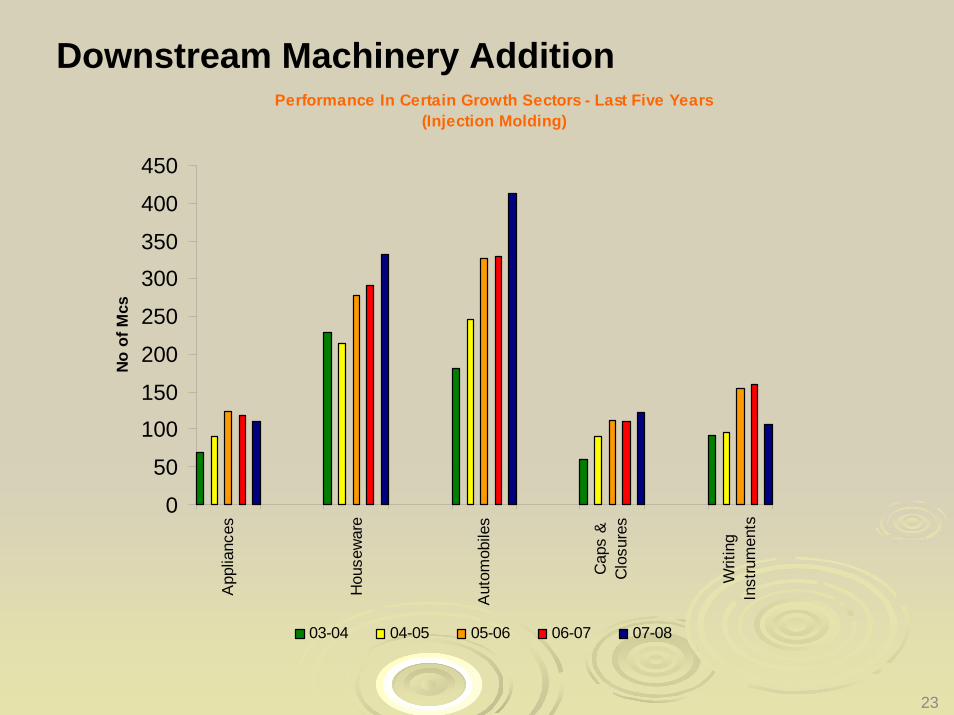

Performance In Certain Growth Sectors - Last Five Years(Injection Molding)

0

50

100

150

200

250

300

350

400

450

App

lianc

es

Hou

sew

are

Aut

omob

iles

Cap

s &

Clo

sure

s

Writ

ing

Inst

rum

ents

No o

f Mcs

03-04 04-05 05-06 06-07 07-08

Downstream Machinery Addition

23

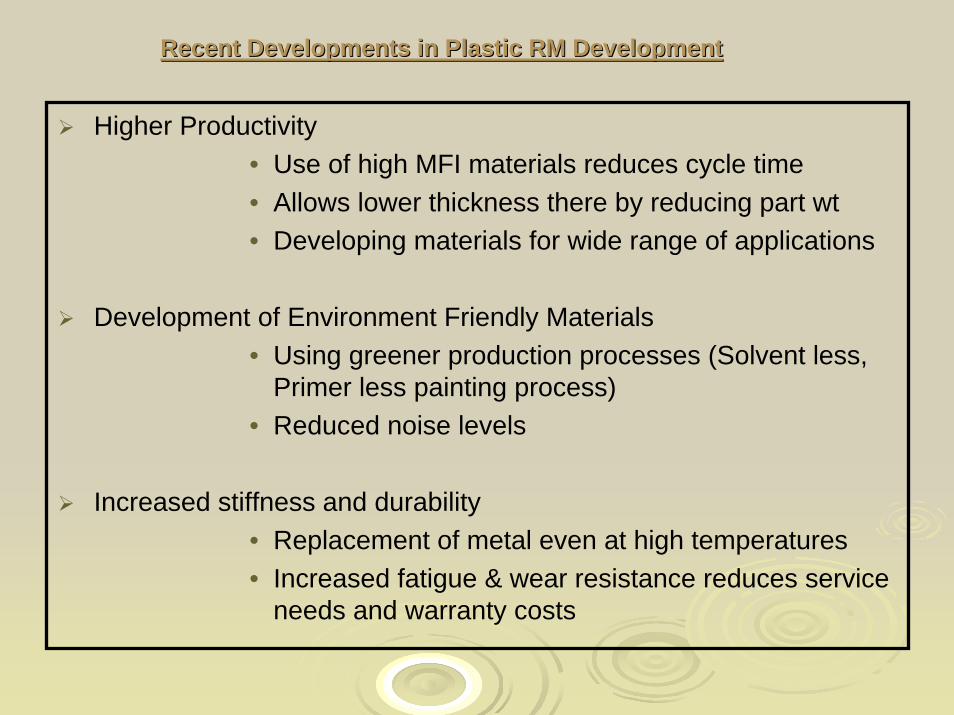

Recent Developments in Plastic RM DevelopmentRecent Developments in Plastic RM Development

Higher Productivity• Use of high MFI materials reduces cycle time• Allows lower thickness there by reducing part wt• Developing materials for wide range of applications

Development of Environment Friendly Materials• Using greener production processes (Solvent less,

Primer less painting process)• Reduced noise levels

Increased stiffness and durability• Replacement of metal even at high temperatures• Increased fatigue & wear resistance reduces service

needs and warranty costs

Application trendsApplication trends

metal substition under the hoodinterior

roof module

structural inserts in thebody in white

FE concepts

functional polymers, mechatronic

outer body parts

Auto Electrical

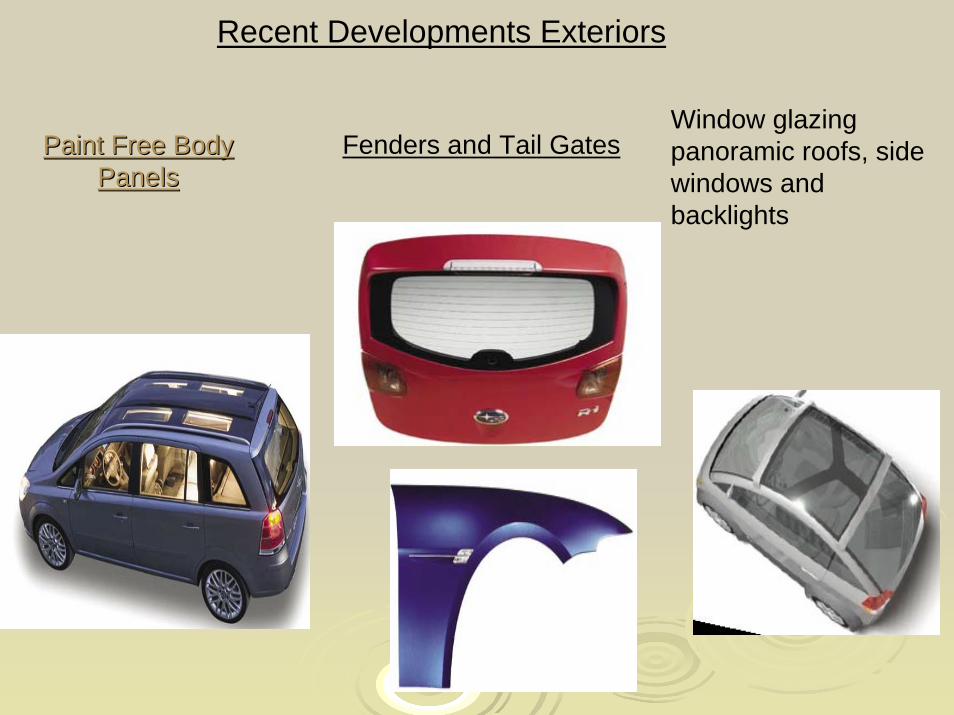

Recent Developments Exteriors

Paint Free Body Paint Free Body PanelsPanels

Fenders and Tail GatesWindow glazing panoramic roofs, side windows and backlights

Recent Developments Advance Safety

Energy AbsorbersEnergy Absorbers Front End Module

Recent Developments in Power Train

Air intake manifold Fuel Rails

Throttle bodyStabilizer clamps

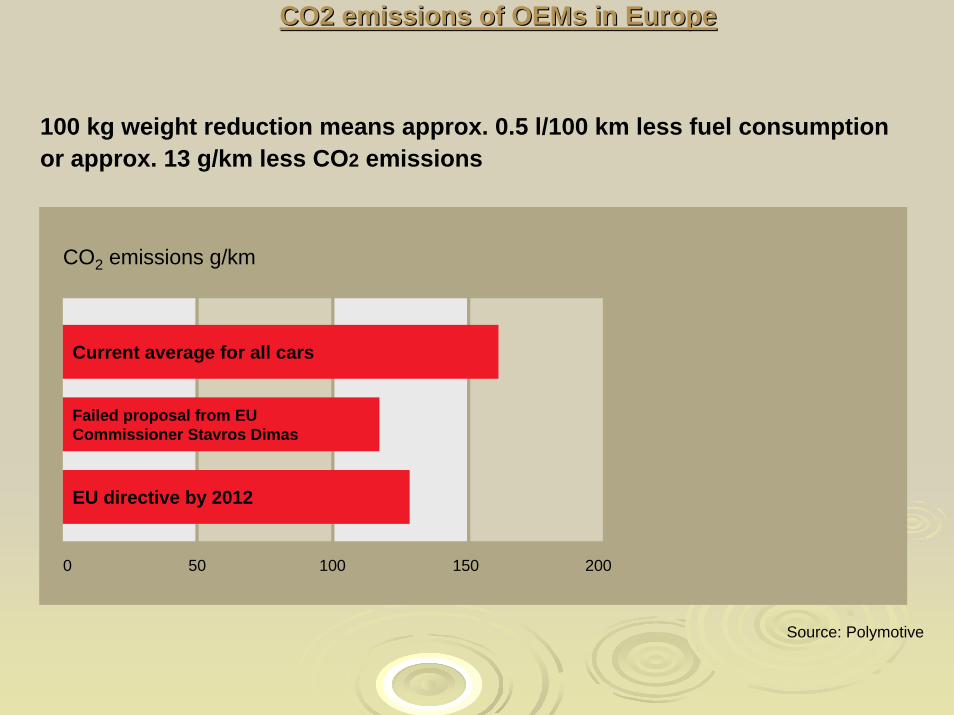

CO2 emissions of OEMs in EuropeCO2 emissions of OEMs in Europe

100 kg weight reduction means approx. 0.5 l/100 km less fuel consumption or approx. 13 g/km less CO2 emissions

CO2 emissions g/km

Current average for all cars

0 50 100 150 200

Failed proposal from EU Commissioner Stavros Dimas

EU directive by 2012

Source: Polymotive

Use of material in modern carsUse of material in modern cars

Plastics approx. 15-18 %

Materials breakdown for the Modern Cars

5%4%3%

53%

6%

14%

13%

2%

Steel

PlasticsTotal 1,429 kg Others

Aluminum

Glass

Elastomers

Fluids

Cast Iron

Source: Polymotive

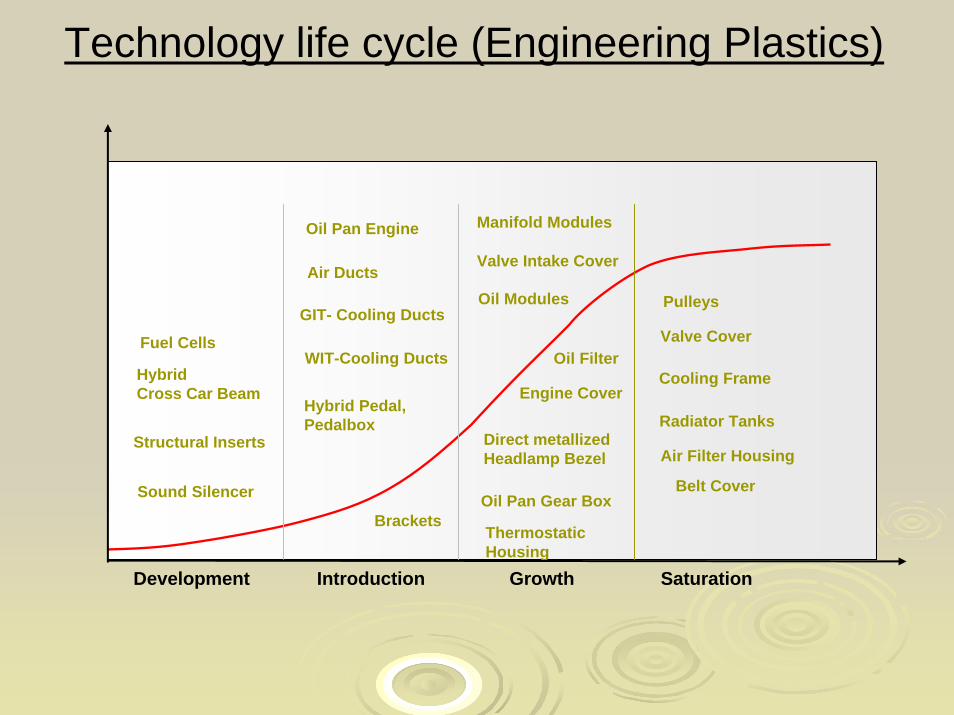

Technology life cycle (Engineering Plastics)

Brackets

Oil Modules

Manifold Modules

Valve Intake Cover

Engine Cover

Radiator Tanks

Belt Cover

Thermostatic Housing

HybridCross Car Beam

Oil Pan Engine

GIT- Cooling Ducts

Sound Silencer

Cooling Frame

Air Filter Housing

Pulleys

WIT-Cooling Ducts

Air Ducts

Oil Filter

Oil Pan Gear Box

Valve Cover

Hybrid Pedal,Pedalbox

Structural Inserts Direct metallized Headlamp Bezel

Fuel Cells

Development Introduction Growth Saturation

Future Challenges for Raw Material SuppliersFuture Challenges for Raw Material Suppliers

1. Response to a globalized auto industryDemand from developing world (footprints required)RM suppliers shall be able to respond globallyMarket specific solution and shorter timing

2. Challenges for improved performance at competitive cost levels in emerging markets.

3. Lower environmental impact and responsible use of energy

Government regulationEmission reductionsEnvironmentally friendlier processesCompliance with ELV & NVH standards

How to face the future

Partnership between all stakeholders involved in the supply chain.Proliferation of knowledge to all stakeholders in the chain.Recruiting and training of more plastic engineers to enhance capabilities.Standardization and availability of engineering data to design engineersMore cost effective solutions for tooling, processing, raw materials etc.

OEM

MOULDER

RM Supplier

Thanks

Automotive Growth DriversAutomotive Growth Drivers

Low vehicle penetrationLow vehicle penetration

Infrastructure Development (Highways) Infrastructure Development (Highways)

Growing middle class buyers (30Growing middle class buyers (30--40million every year)40million every year)

Increased investment by Global PlayersIncreased investment by Global Players

Vehicle & Component Export emerged as a Vehicle & Component Export emerged as a

key factor for growthkey factor for growth

India : A growing Automotive market 35

Learning and Future DirectionLearning and Future Direction

1.1. Future outlook Future outlook •• India: PromisingIndia: Promising•• Global: WeakGlobal: Weak

2. Focus on low cost, fuel efficient cars2. Focus on low cost, fuel efficient cars

3. Stricter environment norms3. Stricter environment norms

4. Advance navigation and safety features4. Advance navigation and safety features

Downstream Development

Processing Capacity (KTA)3.0 MMT Capacity Addition in

next 3 Years

Investment of ~ US $ 160 mn.

with 680 KT capacity in 2007.

Injection Moulding (IM)

Capacity Growth 21 % (2007)

1 MMT Capacity added in IM

Sector in last two years

0.0

3.0

6.0

9.0

2007-08 2010-11

CAGR @17 %

360430

523

2005 2006 2007

IM Capacity Addition (KTA)IM Capacity Addition (KTA)

D/S Growth to Fuel Industry Consumption 37

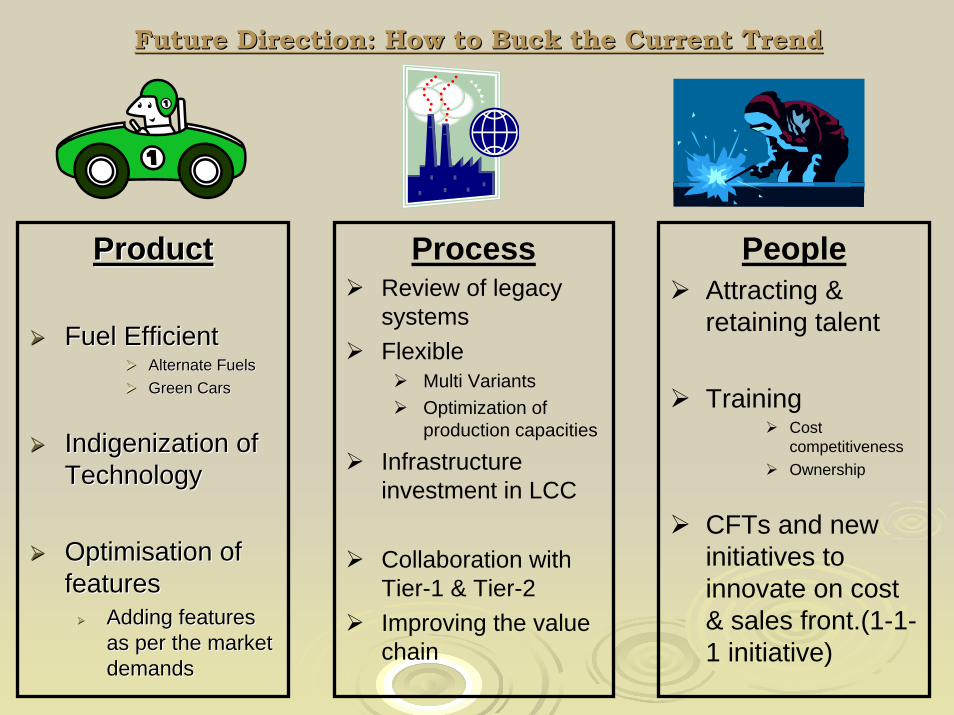

Future Direction: How to Buck the Current TrendFuture Direction: How to Buck the Current Trend

ProcessReview of legacy systemsFlexible

Multi VariantsOptimization of production capacities

Infrastructure investment in LCC

Collaboration with Tier-1 & Tier-2Improving the value chain

PeopleAttracting & retaining talent

TrainingCost competitivenessOwnership

CFTs and new initiatives to innovate on cost & sales front.(1-1-1 initiative)

ProductProduct

Fuel Efficient Fuel Efficient Alternate FuelsAlternate FuelsGreen CarsGreen Cars

Indigenization of Indigenization of TechnologyTechnology

Optimisation of Optimisation of features features

Adding features Adding features as per the market as per the market demandsdemands

Automotive Industry Scenario : 07Automotive Industry Scenario : 07--0808

Turnover : 40 Bn USD Turnover : 40 Bn USD No of Vehicles : 12.5 MillionNo of Vehicles : 12.5 Million

39

1.8

8.9

0.6 0.6 0.3 0.30.01.02.03.04.05.06.07.08.09.0

Pass.

Veh2 W

heeler

s

C.Veh.

3 Whe

elers

Truck/Bus

Tractor

Vehicle Production ( Million)

Income trends : To become 3Income trends : To become 3rdrd Largest Economy, Largest Economy, BUT WITH RELATIVELY LOW PER CAPITA INCOMEBUT WITH RELATIVELY LOW PER CAPITA INCOMEPattern of Growth Not Witnessed By Any Other CountryPattern of Growth Not Witnessed By Any Other Country

GDP vs GDP per capita in 2050GDP vs GDP per capita in 2002GDP (US$ Bn)

GDP per capita (US$)

0

2000

4000

6000

8000

10000

12000

14000

0 10000 20000 30000 40000 50000

GDP (US$ Bn)

GDP per capita (US$)

0

10000

20000

30000

40000

50000

60000

0 20000 40000 60000 80000 100000

US

Japan

ChinaIndia

UK

Germany

ItalyFrance

BrazilRussia

China

US

Brazil

Italy Germany France

Russia

UK

Japan

India

Bubble size corresponds to GDP sizeSource: Goldman Sachs, BCG