Futures Trading Strategies on SGX - India chapter in AFACT in Singapore

35

AFACT Workshop: Futures Trading Strategies on SGX QuantInsti Nitesh Khandelwal May 23, 2015

-

Upload

quantinsti -

Category

Economy & Finance

-

view

170 -

download

0

Transcript of Futures Trading Strategies on SGX - India chapter in AFACT in Singapore

AFACT Workshop:Futures Trading Strategies on SGX

QuantInstiNitesh KhandelwalMay 23, 2015

2Definitions Statistics Strategies Stat Arb

Agenda

Definition

StatisticalConcepts

TradingStrategies

Stat Arbitrage

3

Quantitative Trading

• Using quantitative techniques to build the tradingmodel and execution. Statistical methods andmathematical computations are extensively used whilecreating the trading model as well as the during theimplementation.

Definitions Statistics Strategies Stat Arb

Quantitative Trading

• Using quantitative techniques to build the tradingmodel and execution. Statistical methods andmathematical computations are extensively used whilecreating the trading model as well as the during theimplementation.

4

Statistical Concepts

• Stationarity• Cointegration• Dickey Fuller test

Definitions Statistics Strategies Stat Arb

Statistical Concepts

• Stationarity• Cointegration• Dickey Fuller test

5

Statistical Concepts: Stationarity

• A stationary time series is one whose statistical properties such as mean,variance, autocorrelation, etc. are all constant over time. Most statisticalforecasting methods are based on the assumption that the time series canbe rendered approximately stationary (i.e., "stationarized") through the useof mathematical transformations.

• A stationarized series is relatively easy to predict: you simply predict that itsstatistical properties will be the same in the future as they have been in thepast! The predictions for the stationarized series can then be"untransformed," by reversing whatever mathematical transformations werepreviously used, to obtain predictions for the original series.

Definitions Statistics Strategies Stat Arb

Statistical Concepts: Stationarity

• A stationary time series is one whose statistical properties such as mean,variance, autocorrelation, etc. are all constant over time. Most statisticalforecasting methods are based on the assumption that the time series canbe rendered approximately stationary (i.e., "stationarized") through the useof mathematical transformations.

• A stationarized series is relatively easy to predict: you simply predict that itsstatistical properties will be the same in the future as they have been in thepast! The predictions for the stationarized series can then be"untransformed," by reversing whatever mathematical transformations werepreviously used, to obtain predictions for the original series.

6

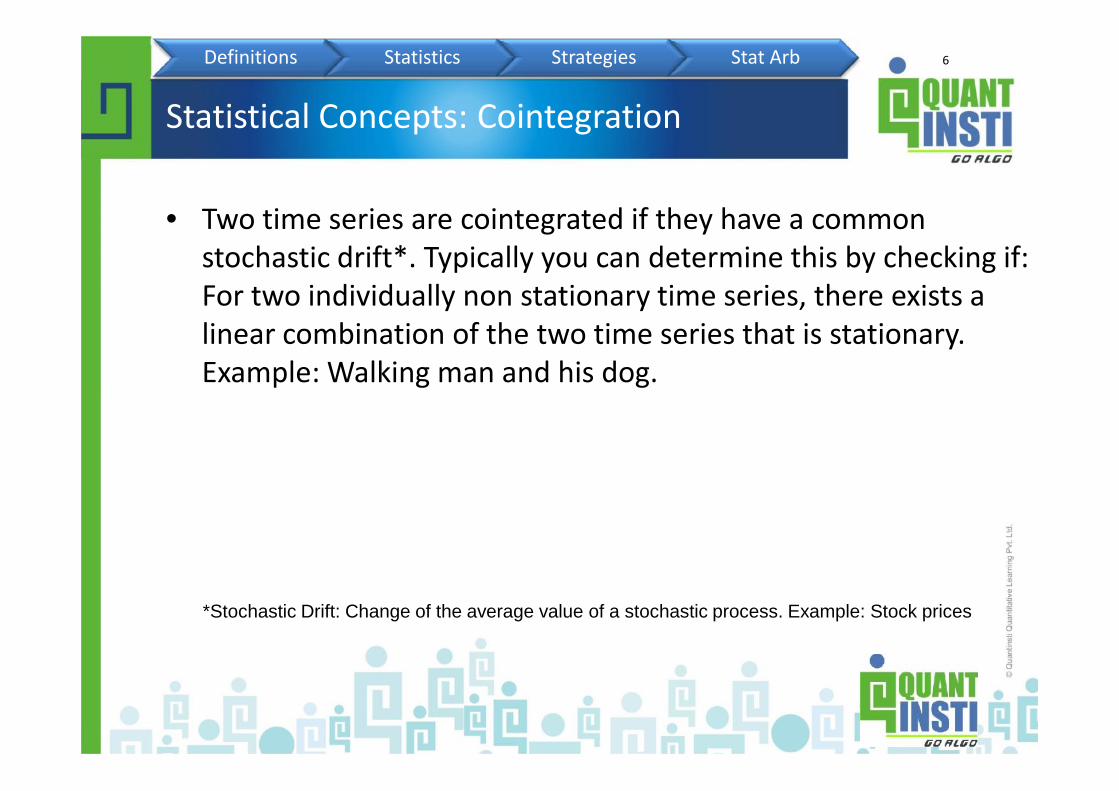

Statistical Concepts: Cointegration

• Two time series are cointegrated if they have a commonstochastic drift*. Typically you can determine this by checking if:For two individually non stationary time series, there exists alinear combination of the two time series that is stationary.Example: Walking man and his dog.

Definitions Statistics Strategies Stat Arb

*Stochastic Drift: Change of the average value of a stochastic process. Example: Stock prices

7

Statistical Concepts: DF Test

It test for the unit root in an autoregressive model.

yt = ρ yt-1 + ut

If |ρ| >= 1, then a unit root is present and the series is nonstationary

Definitions Statistics Strategies Stat Arb

Statistical Concepts: DF Test

It test for the unit root in an autoregressive model.

yt = ρ yt-1 + ut

If |ρ| >= 1, then a unit root is present and the series is nonstationary

8

ETF/Cash - Future Arbitrage:

• Long Cash (or ETF)/ Short Future• Short Cash (or ETF)/ Long Future

• Strategy Notes:– When shorting Cash/ETF, ensure its allowed for Short

selling– Pick stocks with liquid cash market– Spreads become more volatile when close to expiry– Higher interest rates typically indicate higher spreads– Market Sentiment

Futures Trading Strategies

Cash Future

Stat Arbitrage

Definitions Statistics Strategies Stat Arb

ETF/Cash - Future Arbitrage:

• Long Cash (or ETF)/ Short Future• Short Cash (or ETF)/ Long Future

• Strategy Notes:– When shorting Cash/ETF, ensure its allowed for Short

selling– Pick stocks with liquid cash market– Spreads become more volatile when close to expiry– Higher interest rates typically indicate higher spreads– Market Sentiment

Index Arbitrage

Directional

9

Calendar Spreads:• INR May 2015 Vs INR June 2015

Inter Product Spreads:• SGX Nifty Vs SGX MSCI India Futures• SGX Nifty Vs SGX INR Futures

Inter Destinations Spreads:• SGX INR Vs INR NDF• SGX JPY Vs Spot JPY

Futures Trading Strategies

Cash Future

Stat Arbitrage

Definitions Statistics Strategies Stat Arb

Calendar Spreads:• INR May 2015 Vs INR June 2015

Inter Product Spreads:• SGX Nifty Vs SGX MSCI India Futures• SGX Nifty Vs SGX INR Futures

Inter Destinations Spreads:• SGX INR Vs INR NDF• SGX JPY Vs Spot JPY

Index Arbitrage

Directional

10

Futures Trading Strategies

SGX NIFTY MSCI India Future Strategy notes

Product 50 stocks 64 stocks Highly correlated pair (99%correlation)

Lot size 2 times the index 50 times the index MSCI contract size is approx 3.1times the Nifty contract

Tick Size 0.5 index points (USD 1) 0.2 index points (USD 10) Correct rounding

Daily Price Range 10/15/20% 10/15/20% Same ‘mostly’

Definitions Statistics Strategies Stat Arb

Contract Months 2 nearest months and 4quarterly months

2 nearest months and 4months on yearly cycle

Near month is most liquid

Trading Hours 9am to 6:10pm, 7:15pmto 2am

9am to 6:10pm, 7:15pm to2am

Same

Last Trading Day Last Thursday of themonth

Last Thursday of themonth

They expire at their respectiveindex values

Settlement Cash Cash Same

11

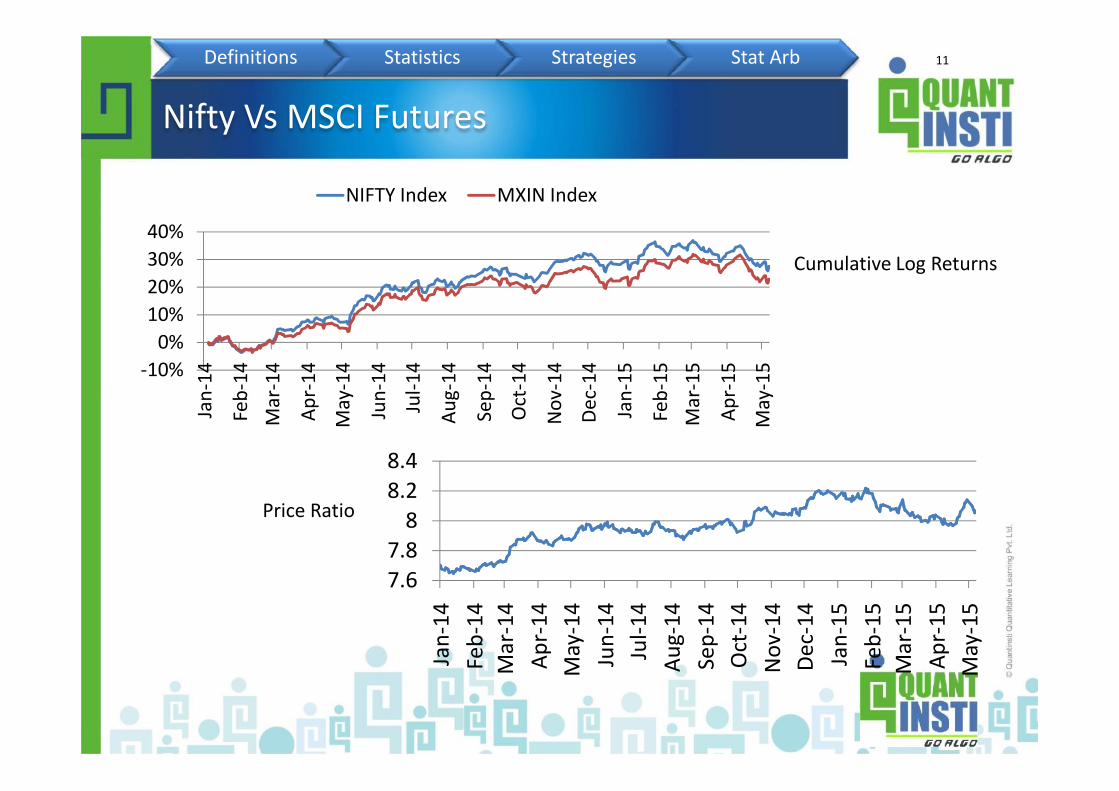

Nifty Vs MSCI Futures

-10%0%

10%20%30%40%

Jan-

14

Feb-

14M

ar-1

4

Apr-

14

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct

-14

Nov

-14

Dec-

14

Jan-

15

Feb-

15M

ar-1

5

Apr-

15

May

-15

NIFTY Index MXIN Index

Cumulative Log Returns

Definitions Statistics Strategies Stat Arb

Jan-

14

Feb-

14M

ar-1

4

Apr-

14

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct

-14

Nov

-14

Dec-

14

Jan-

15

Feb-

15M

ar-1

5

Apr-

15

May

-15

7.67.8

88.28.4

Jan-

14Fe

b-14

Mar

-14

Apr-

14M

ay-1

4Ju

n-14

Jul-1

4Au

g-14

Sep-

14O

ct-1

4N

ov-1

4De

c-14

Jan-

15Fe

b-15

Mar

-15

Apr-

15M

ay-1

5

Price Ratio

12

Correlation• 99% correlation

– More importantly, they are cointegrated!

Spread Margin Benefit• 70% margin credit for 3 lots of Nifty against

1 lot of MSCI India Future

Nifty Vs MSCI Futures

Cash Future

Stat Arbitrage

Definitions Statistics Strategies Stat Arb

Correlation• 99% correlation

– More importantly, they are cointegrated!

Spread Margin Benefit• 70% margin credit for 3 lots of Nifty against

1 lot of MSCI India FutureIndex Arbitrage

Directional

13

Futures Trading Strategies

Cash Future

Stat Arbitrage

Index Arbitrage:

• Long Nifty Future/ Short ConstituentStocks/Futures

• Short Nifty Future/ Long ConstituentStocks/Futures

• Strategy Notes:– When shorting Cash, ensure its allowed for Short selling– Approximate Index replication– Trade Size– Transaction Cost

– Index Future with Cash Stock + Stock Future

Definitions Statistics Strategies Stat Arb

Index Arbitrage

Directional

Index Arbitrage:

• Long Nifty Future/ Short ConstituentStocks/Futures

• Short Nifty Future/ Long ConstituentStocks/Futures

• Strategy Notes:– When shorting Cash, ensure its allowed for Short selling– Approximate Index replication– Trade Size– Transaction Cost

– Index Future with Cash Stock + Stock Future

14

Futures Trading Strategies

Cash Future

Stat Arbitrage

Directional Trading Strategies:

• Trading Strategies based on indicators/quantitative analysis

StrategyIdeation

Definitions Statistics Strategies Stat Arb

Index Arbitrage

Directional

Directional Trading Strategies:

• Trading Strategies based on indicators/quantitative analysis

StrategyModeling

Back TestingParameterOptimization

Implementation

RiskManagement

15

Ideation & Validation• Check for cointegration

Modeling• Create a mean reverting index and model the strategy

– Key inputs: Signal generation parameters, SL, TP, Order quantity

Back-testing• Calculate the key outputs

– Net profit, average profit, drawdown, returns, ratios

Implementation• Causality & exceptions

Stat Arb Example: Strategy Building Process

Definitions Statistics Strategies Stat Arb

Ideation & Validation• Check for cointegration

Modeling• Create a mean reverting index and model the strategy

– Key inputs: Signal generation parameters, SL, TP, Order quantity

Back-testing• Calculate the key outputs

– Net profit, average profit, drawdown, returns, ratios

Implementation• Causality & exceptions

16

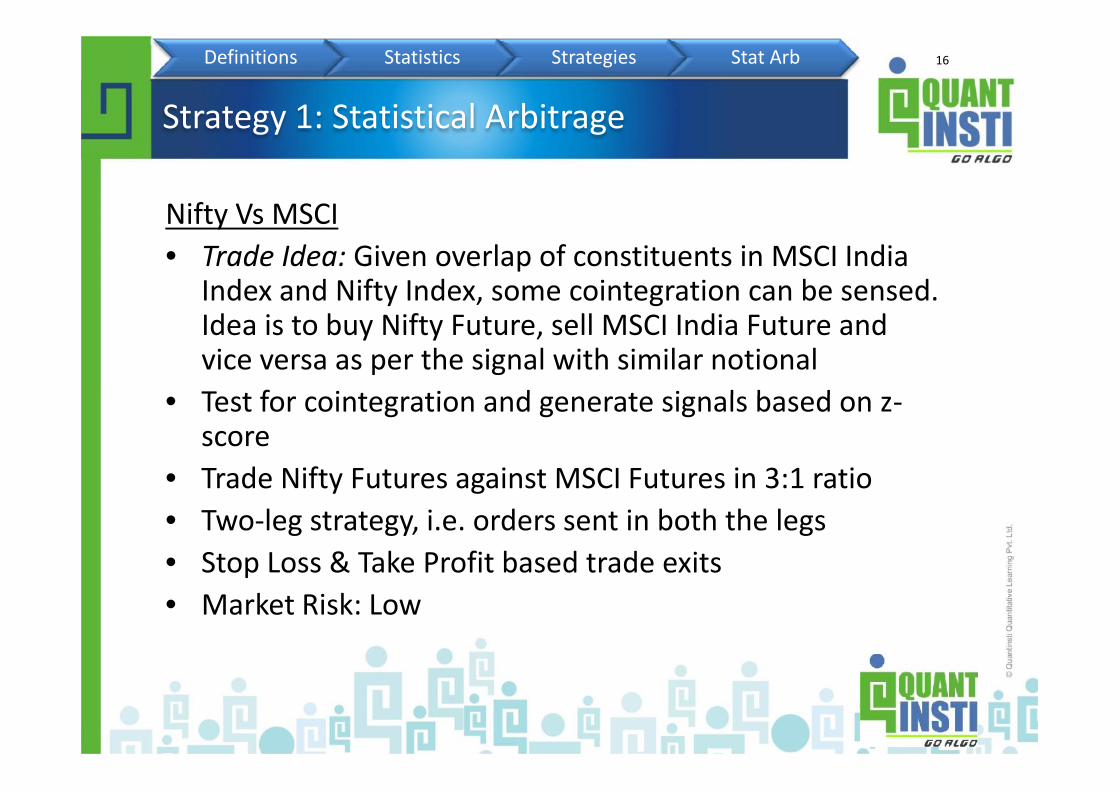

Nifty Vs MSCI• Trade Idea: Given overlap of constituents in MSCI India

Index and Nifty Index, some cointegration can be sensed.Idea is to buy Nifty Future, sell MSCI India Future andvice versa as per the signal with similar notional

• Test for cointegration and generate signals based on z-score

• Trade Nifty Futures against MSCI Futures in 3:1 ratio• Two-leg strategy, i.e. orders sent in both the legs• Stop Loss & Take Profit based trade exits• Market Risk: Low

Strategy 1: Statistical Arbitrage

Definitions Statistics Strategies Stat Arb

Nifty Vs MSCI• Trade Idea: Given overlap of constituents in MSCI India

Index and Nifty Index, some cointegration can be sensed.Idea is to buy Nifty Future, sell MSCI India Future andvice versa as per the signal with similar notional

• Test for cointegration and generate signals based on z-score

• Trade Nifty Futures against MSCI Futures in 3:1 ratio• Two-leg strategy, i.e. orders sent in both the legs• Stop Loss & Take Profit based trade exits• Market Risk: Low

17

MSCI ETF Vs MSCI Future• Trade Idea: ETF assumed as the lead indicator (ideally to

be tested through Granger Causality or other Causalitymodels). If the ETF returns are exceeding Future’sreturn, take a short term naked position in MSCI Future.

• Trade MSCI Futures based on ETF Returns• Single leg strategy, i.e. orders sent only in MSCI Futues

but ETF data used as well.• Trade exit: When signal on the opposite side is

generated• Market Risk: Medium

Strategy 2: Trading Causality

Definitions Statistics Strategies Stat Arb

MSCI ETF Vs MSCI Future• Trade Idea: ETF assumed as the lead indicator (ideally to

be tested through Granger Causality or other Causalitymodels). If the ETF returns are exceeding Future’sreturn, take a short term naked position in MSCI Future.

• Trade MSCI Futures based on ETF Returns• Single leg strategy, i.e. orders sent only in MSCI Futues

but ETF data used as well.• Trade exit: When signal on the opposite side is

generated• Market Risk: Medium

18

INR Futures• Trade Idea: To ride on the short term trend of the INR

futures with exits based on Stop Loss and Take Profit.• Trend Following model• Trading signal generated when current closing price goes

above or below (buy or sell respectively) max/min ofprevious ‘x’ days closing price

• Single leg strategy, i.e. orders sent only in INR Futures• Trade exit: When Stop Loss or Take Profit is triggered.• Market Risk: High

Strategy 3: Trend Following Strategy

Definitions Statistics Strategies Stat Arb

INR Futures• Trade Idea: To ride on the short term trend of the INR

futures with exits based on Stop Loss and Take Profit.• Trend Following model• Trading signal generated when current closing price goes

above or below (buy or sell respectively) max/min ofprevious ‘x’ days closing price

• Single leg strategy, i.e. orders sent only in INR Futures• Trade exit: When Stop Loss or Take Profit is triggered.• Market Risk: High

19

Thank YouMerci

DankeGracias

TerimaKasihXieXie

GraziShukriya

[email protected]/ +91–9920–44-88–77 / +65–6221–3654

GoAlgo! Join QI’s E-PAT (Executive Program on Algorithmic Trading)

Next batch starts: June 20, 2015. Visitwww.quantinsti.comfor more information

Question & Answers

Definitions Statistics Strategies Stat Arb

Thank YouMerci

DankeGracias

TerimaKasihXieXie

GraziShukriya

[email protected]/ +91–9920–44-88–77 / +65–6221–3654

GoAlgo! Join QI’s E-PAT (Executive Program on Algorithmic Trading)

Next batch starts: June 20, 2015. Visitwww.quantinsti.comfor more information

20

APPENDIXAPPENDIX

21

Definitions

• Financial Derivative is a financial instrument whose price isderived from the price of some other financial instrument.

• Futures & Forwards:– Future: Standardized contracts for the purchase and sale of financial

instruments or physical commodities for future delivery on a regulatedexchange.

– Forward: A private over the counter (OTC) agreement between abuyer and seller for the future delivery of a commodity or a financialinstrument, at an agreed upon price. In contrast to futurescontracts, forward contracts are not standardized and are non-transferable.

Definitions Fundaments Pricing

Definitions

• Financial Derivative is a financial instrument whose price isderived from the price of some other financial instrument.

• Futures & Forwards:– Future: Standardized contracts for the purchase and sale of financial

instruments or physical commodities for future delivery on a regulatedexchange.

– Forward: A private over the counter (OTC) agreement between abuyer and seller for the future delivery of a commodity or a financialinstrument, at an agreed upon price. In contrast to futurescontracts, forward contracts are not standardized and are non-transferable.

22

Futures

• Financial Derivative is a financial instrument whose price isderived from the price of some other financial instrument.

• Futures & Forwards:– Future: Standardized contracts for the purchase and sale of financial

instruments or physical commodities for future delivery on a regulatedexchange.

– Forward: A private over the counter (OTC) agreement between abuyer and seller for the future delivery of a commodity or a financialinstrument, at an agreed upon price. In contrast to futurescontracts, forward contracts are not standardized and are non-transferable.

Definitions Fundaments Pricing

Futures

• Financial Derivative is a financial instrument whose price isderived from the price of some other financial instrument.

• Futures & Forwards:– Future: Standardized contracts for the purchase and sale of financial

instruments or physical commodities for future delivery on a regulatedexchange.

– Forward: A private over the counter (OTC) agreement between abuyer and seller for the future delivery of a commodity or a financialinstrument, at an agreed upon price. In contrast to futurescontracts, forward contracts are not standardized and are non-transferable.

23

Market Participants

• Hedgers: Use futures to manage the price risk• Arbitrageurs: Profit from pricing mismatch• Speculators: Take price risk to generate profits

Definitions Fundaments Pricing

24

Key Characteristics

• Spot Price• Contract/Lot Size• Expiry Date• Margin• Settlement• Delivery

Definitions Fundaments Pricing

Key Characteristics

• Spot Price• Contract/Lot Size• Expiry Date• Margin• Settlement• Delivery

25

Benefits of Trading Futures

• Capital efficiency: Higher leverage• More strategies: Different instrument from Cash• Better liquidity: Bigger notional values• Price Discovery: Fair and Transparent Price Discovery

Definitions Fundaments Pricing

Benefits of Trading Futures

• Capital efficiency: Higher leverage• More strategies: Different instrument from Cash• Better liquidity: Bigger notional values• Price Discovery: Fair and Transparent Price Discovery

26

Futures Pricing

• Pricing depends on key characteristics of instrument– Spot Price– Date of Expiry– Risk free rate of return– Storage & Delivery Cost– Convenience Yield

Definitions Fundaments Pricing

Futures Pricing

• Pricing depends on key characteristics of instrument– Spot Price– Date of Expiry– Risk free rate of return– Storage & Delivery Cost– Convenience Yield

27

Futures Pricing: The Math

• For Equity Futures:

F(t, T) = S(t)*er(T-t)

where:– F (t, T) = Price of the future at time t with expiry on time T– S(t) = Spot Price at time T– r = Risk free rate of return– T = Expiry date– t = Current date

Definitions Fundaments Pricing

Futures Pricing: The Math

• For Equity Futures:

F(t, T) = S(t)*er(T-t)

where:– F (t, T) = Price of the future at time t with expiry on time T– S(t) = Spot Price at time T– r = Risk free rate of return– T = Expiry date– t = Current date

28

Futures Pricing: The Math

• For Commodity Futures:

F(t, T) = S(t)*e(r+s-c)(T-t)

where:– F = Price of the future– S = Spot Price– R = Risk free rate of return– T = Expiry date– t = Current date– s = Storage cost– c = Convenience Yield

Definitions Fundaments Pricing

Futures Pricing: The Math

• For Commodity Futures:

F(t, T) = S(t)*e(r+s-c)(T-t)

where:– F = Price of the future– S = Spot Price– R = Risk free rate of return– T = Expiry date– t = Current date– s = Storage cost– c = Convenience Yield

29

Executive Programme in AlgorithmicTrading (E-PAT)

Executive Programme in AlgorithmicTrading (E-PAT)

30

E-PAT

Statistics andEconometrics

Financial Computing &Technology

QI’s E-PAT course

E-PAT Financial Computing &Technology

Algorithmic &Quantitative Trading

31

E-PAT

Statistics andEconometrics

Financial Computing &Technology

E-PAT course structure - module I

Basic Statistics

Advanced Statistics

Probability and Distribution Statistical Inference Linear Regression

Correlation vs. Co-integration ARIMA, ARCH-GARCH Models Multiple Regression

E-PAT Financial Computing &Technology

Algorithmic &Quantitative Trading Time Series Analysis

Correlation vs. Co-integration ARIMA, ARCH-GARCH Models Multiple Regression

Stochastic Math Causality Forecasting

32

E-PAT

Statistics andEconometrics

Financial Computing &Technology

E-PAT course structure - module II

Programming

Technology for AlgorithmicTrading

Intro to ProgrammingLanguage(s)

Programming on AlgorithmicTrading Platforms

System Architecture Understanding an Algorithmic

Trading Platform Handling HFT Data

E-PAT Financial Computing &Technology

Algorithmic &Quantitative Trading Statistical Tools

System Architecture Understanding an Algorithmic

Trading Platform Handling HFT Data

Excel & VBA Financial Modeling using R Using R & Excel for Back-testing

33

E-PAT

Statistics andEconometrics

Financial Computing &Technology

E-PAT course structure - module IIITrading Strategies

Derivatives & MarketMicrostructure

Statistical Arbitrage Market Making Strategies Execution Strategies Forecasting & AI Based Strategies Pair Trading Strategies Trend following Strategies

Option Pricing Model Dispersion Trading Risk Management using Higher

Order Greeks Option Portfolio Management Order Book Dynamics Market Microstructure

Algorithmic &Quantitative Trading

Managing Algo Operations

Option Pricing Model Dispersion Trading Risk Management using Higher

Order Greeks Option Portfolio Management Order Book Dynamics Market Microstructure

Hardware & Network Regulatory Framework Exchange Infrastructure &

Financial Planning (Costing) Risk Management in Automated

systems Performance Evaluation &

Portfolio Management

34

E-PAT

Statistics andEconometrics

Financial Computing &Technology Project work

E-PAT course structure - project

E-PAT Financial Computing &Technology

Algorithmic &Quantitative Trading

35

Thank YouMerci

DankeGracias

TerimaKasihXieXie

GraziShukriya

[email protected]/ +91–9920–44-88–77 / +65–6221–3654

GoAlgo! Join QI’s E-PAT (Executive Program on Algorithmic Trading)

Next batch starts: June 20, 2015. Visitwww.quantinsti.comfor more information

Question & Answers

Thank YouMerci

DankeGracias

TerimaKasihXieXie

GraziShukriya

[email protected]/ +91–9920–44-88–77 / +65–6221–3654

GoAlgo! Join QI’s E-PAT (Executive Program on Algorithmic Trading)

Next batch starts: June 20, 2015. Visitwww.quantinsti.comfor more information