Future Trade Policy Scenarios Group 3 - GTAP · 2019-04-14 · Center for Global Trade Analysis...

33

Center for Global Trade Analysis Department of Agricultural Economics, Purdue University 403 West State Street, West Lafayette, IN 47907-2056 USA Global Trade Analysis Project Stay Connected with GTAP! www.gtap.agecon.purdue.edu Future Trade Policy Scenarios Group 3

Transcript of Future Trade Policy Scenarios Group 3 - GTAP · 2019-04-14 · Center for Global Trade Analysis...

Center for Global Trade AnalysisDepartment of Agricultural Economics, Purdue University403 West State Street, West Lafayette, IN 47907-2056 USA

Global Trade Analysis Project

Stay Connected with GTAP!www.gtap.agecon.purdue.edu

Future Trade Policy ScenariosGroup 3

Center for Global Trade AnalysisDepartment of Agricultural Economics, Purdue University403 West State Street, West Lafayette, IN 47907-2056 USA

Global Trade Analysis Project

Stay Connected with GTAP!www.gtap.agecon.purdue.edu

Joining Uncle-Sam in a very different kind of war

Disclaimer: The views represented in this presentation do not represent official positions or policy of any presenter’s respective university, agency, or government.

Let us imagine the (scary) world where the USA convinces its major allies to join the trade war with China…!

The battleThe provocation The allies increase tariffs by 10ppt on all Chinese goodsThe response China matches the tariffs on each ally

Fortifying their positionsThe sweetener Allies reduce NTMs within their bloc (based on empirical FTA estimates) Scenario 1 & 2The defense China puts in place internal measures to keep investment high Scenario 2

Four considerations• What happens for North America• What happens for east Asia• What happens for the rest of OECD• Who are the big winners & losers in the developing world

SYNTHESIS

3

Who joins the war USA | Mex & Can | EU & UK | Aus & NZ | Japan

Our implementationBaseline: exogenous = SSP2 assumptions for population, GDP growth & labour supply

closure = CPTPP closure

Policy shock (S1): exogenous = SSP2 population closure = CP-TPP closure, with GDP endogenous

Policy shock (S2): exogenous = as per Scenario 1closure = exogenise total Chinese investment (qinv)

by freeing up Chinese rate of return (cgdslack)

Timeframe2011 no difference to 2018

trade measures introduced gradually from 2019 over 5yr simulation to 2026

SYNTHESIS

4Disclaimer: {Optional -Use this text box to absolve your home institution of any attachment to the views and findings of your presentation}

Commodities affected by the tariffs (allies vs. China) Oilseed crops | Wheat | other agriculture, Forestry & Fishing Energy resources | other resource extraction Energy products | Iron & Steel | Other metals | Non-metal minerals

| Chemicals | other heavy manuf Textiles | Vehicles | Electronics | Machinery | Other light manufacturing

Services affected by the NTM reductions (within the block of allies) Power & Utilities | Transport | Communications | Financial services | Other services

Regional aggregation no change to WTO scenarios

SYNTHESIS

5Disclaimer: {Optional -Use this text box to absolve your home institution of any attachment to the views and findings of your presentation}

Global Macroeconomic Results

6

globalcgds

pcgdswld

pxwwld

qxwwld

-3

-2

-1

0

1

2

3

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Perc

enta

ge D

evia

tion

from

Bas

elin

e

Impact on China: GDP & Investment

7

-2.5

-2

-1.5

-1

-0.5

02019 2020 2021 2022 2023 2024 2025 2026

China-S1 China-S2

• China’s reaction offset the negative effects of GDP on 0.02~1.24 percentage point from 2019-2026.

-8

-7

-6

-5

-4

-3

-2

-1

02019 2020 2021 2022 2023 2024 2025 2026

China-Inv-S1 China-Inv-S2

• Investment 1.2~6.82 ppt.

Impact on China: rate of return

8

(5.00)

(4.00)

(3.00)

(2.00)

(1.00)

-2019 2020 2021 2022 2023 2024 2025 2026

Current rate of return

China-S1 China-S2

(5.00) (4.00) (3.00) (2.00) (1.00)

- 1.00 2.00 3.00

2019 2020 2021 2022 2023 2024 2025 2026

Expected rate of return

China-S1 China-S2

Impact on China: GDP expenditures

9

• China’s reaction offset the negative effects:• Priv. Cons. 0.13~1.18 ppt.• Gov. Cons. 0.11~1.22 ppt.

-2.5

-2

-1.5

-1

-0.5

02019 2020 2021 2022 2023 2024 2025 2026

China-Gov-S1 China-Gov-S2

-3

-2.5

-2

-1.5

-1

-0.5

02019 2020 2021 2022 2023 2024 2025 2026

China-Hou-S1 China-Hou-S2

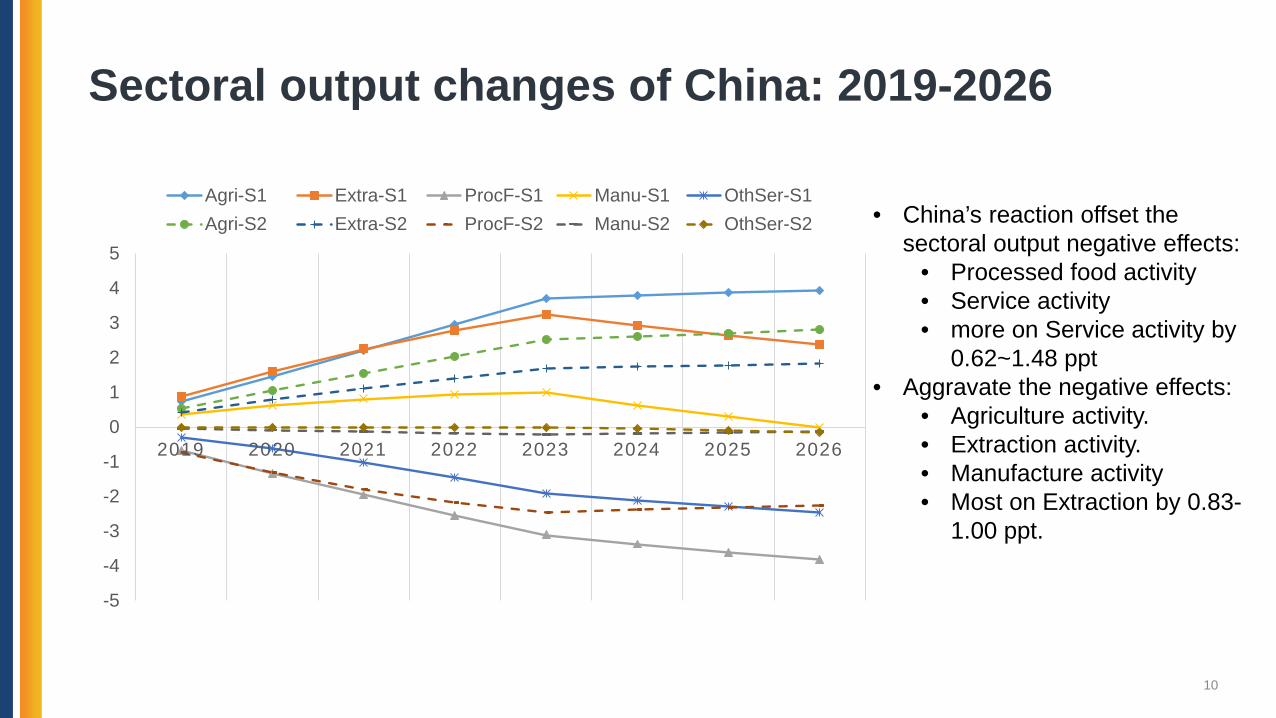

Sectoral output changes of China: 2019-2026

10

• China’s reaction offset the sectoral output negative effects:

• Processed food activity• Service activity• more on Service activity by

0.62~1.48 ppt• Aggravate the negative effects:

• Agriculture activity.• Extraction activity.• Manufacture activity• Most on Extraction by 0.83-

1.00 ppt.

-5

-4

-3

-2

-1

0

1

2

3

4

5

2019 2020 2021 2022 2023 2024 2025 2026

Agri-S1 Extra-S1 ProcF-S1 Manu-S1 OthSer-S1Agri-S2 Extra-S2 ProcF-S2 Manu-S2 OthSer-S2

China import from others: 2019-2026

11

• China’s reaction offset the negative effects on import:

• Import increase especially from neutral regions, i.e. which don’t isolation China

• Korea: 0.67~3.5 ppt• US: 0.82~2.34 ppt• World: 0.47~2.26 ppt

-60.00%

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

2019 2020 2021 2022 2023 2024 2025 2026

Korea-S1 JPN-S1 USA-S1 EU27-S1 World-S1Korea-S2 JPN-S2 USA-S2 EU27-S2 World-S2

China export to others: 2019-2026

12

• China’s reaction aggravate the negative effects on export, export decrease:

• World: 1.29~5.38~3.73 ppt• Korea: 1.05~4.6~3.01 ppt• US: 1.26~4.74~3.27 ppt

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

2019 2020 2021 2022 2023 2024 2025 2026

Korea-S1 JPN-S1 USA-S1 EU27-S1 World-S1Korea-S2 JPN-S2 USA-S2 EU27-S2 World-S2

• China’s reaction• Decreases China’s total trade surplus: $554.18bn~$2671.12bn• Increases China’s trade deficit with Korea: $30.33bn~$161.03bn• Decrease China’s trade surplus with Japan : $46.55bn~$161.05bn• Decrease China’s trade surplus with US : $109.45bn~$397.74bn• Decrease China’s trade surplus with EU : $107.12bn~$402.4bn

Impact on China: Trade balance

13

Impact on North America:GDP & Investment

14

USA

Canada

Mexico

0

0.5

1

1.5

2

2.5

3

3.5

4

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Perc

enta

ge D

evia

tion

from

Bas

elin

e

GDP

USA

Canada

Mexico

0

1

2

3

4

5

6

7

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Perc

enta

ge D

evia

tion

from

Bas

elin

e

Investment

Impact on North America:Trade

15

USA

Canada

Mexico

0

2

4

6

8

10

12

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026Pe

rcen

tage

Dev

iatio

n fro

m B

asel

ine

Imports

USA

Canada

Mexico

0

2

4

6

8

10

12

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Perc

enta

ge D

evia

tion

from

Bas

elin

e

Exports

• Positive GDP and investment impacts – becomes muted when China reacts (particularly investment)

• U.S. manufacturing and agriculture sectors adversely impacted• U.S. services sectors expand

• U.S. exports increase, imports increase even more• Reduced U.S.-China exports down 38% (36%), imports down 20% (24%)• Increased Intra-North America trade

• US exports up 10% (10-11%) with Canada & Mexico• US imports up 14%-16% (14-17%) with Canada & Mexico

• U.S. Trade Deficit – gets even worse

16

Impact on North America:Summary

-2

-1

0

1

2

3

4

5

2019 2020 2021 2022 2023 2024 2025 2026

2 China 3 Korea5 BRN 6 MYS7 SGP 8 VNM9 REA 10 India14 Argentina 15 Brazil18 TUR 19 RUS21 CHL 22 PER23 ROW

% (Cumulative, difference from base case)

17

Expected GDP Change(difference from base case)

-2

-1

0

1

2

3

4

5

2019 2020 2021 2022 2023 2024 2025 2026

1 AUS 4 JPN 11 USA12 CAN 13 MEX 16 EU2717 GBR 20 NZL

% (Cumulative, difference from base case)

allied countries other countries

Japan

-4

-2

0

2

4

6

8

10

12

14

16

2019 2020 2021 2022 2023 2024 2025 2026

2 China 3 Korea5 BRN 6 MYS7 SGP 8 VNM9 REA 10 India14 Argentina 15 Brazil18 TUR 19 RUS

% (Cumulative, difference from base case)

-4

-2

0

2

4

6

8

10

12

14

16

2019 2020 2021 2022 2023 2024 2025 2026

1 AUS 4 JPN 11 USA

12 CAN 13 MEX 16 EU27

17 GBR 20 NZL

% (Cumulative, difference from base case)

18

Expected Export Change(difference from base case)

allied countries other countries

-15

-10

-5

0

5

10

15

2019 2020 2021 2022 2023 2024 2025 2026

2 China 3 Korea 5 BRN6 MYS 7 SGP 8 VNM9 REA 10 India 14 Argentina15 Brazil 18 TUR 19 RUS21 CHL 22 PER 23 ROW

% (Cumulative, difference from base case)

-15

-10

-5

0

5

10

15

2019 2020 2021 2022 2023 2024 2025 2026

1 AUS 4 JPN11 USA 12 CAN13 MEX 16 EU2717 GBR 20 NZL

% (Cumulative, difference from base case)

19

Expected Import Change(difference from base case)

allied countries other countries

-15

-10

-5

0

5

10

15

2019 2020 2021 2022 2023 2024 2025 2026

1 AUS 4 JPN11 USA 12 CAN13 MEX 16 EU2717 GBR 20 NZL

% (Cumulative, difference from base case)

-15

-10

-5

0

5

10

15

2019 2020 2021 2022 2023 2024 2025 2026

2 China 3 Korea 5 BRN6 MYS 7 SGP 8 VNM9 REA 10 India 14 Argentina15 Brazil 18 TUR 19 RUS21 CHL 22 PER 23 ROW

% (Cumulative, difference from base case)

20

Expected Investment Change(difference from base case)

allied countries other countries

21

Expected Export Change from Japan by Countries(difference from base case)

-1200

-1000

-800

-600

-400

-200

0

2019 2020 2021 2022 2023 2024 2025 2026

2 China 3 Korea 5 BRN6 MYS 7 SGP 8 VNM9 REA 10 India 14 Argentina15 Brazil 18 TUR 19 RUS21 CHL 22 PER 23 ROW

% (Cumulative, difference from base case)

allied countries other countries

(40)

(20)

0

20

40

60

80

100

120

140

2019 2020 2021 2022 2023 2024 2025 20261 OtherAgri 2 Wheat 3 OilSeeds4 EnergyExt 5 OtherExt 6 TextWapp7 LightMnfc 8 PetroCoalPro 9 Chemicals10 MineralPro 11 IronSteel 12 OtherMetals13 MetalPro 14 Motor 15 OtherTrans16 Elecronics 17 Machinery 18 Util_Cons19 Transport 20 Communicate 21 Financial22 OthServices

(20)

(10)

0

10

20

30

40

50

2019 2020 2021 2022 2023 2024 2025 2026

Agriculture MiningLight Manu PetroChemiIron/Metals Motor/TransportMachinery/Electronics Service

22

Expected Export Change from Japan by Commodities(difference from base case)

Goods classified in the model Composite Goods

% %

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2019

2020

2021

2022

2023

2024

2025

2026

1 AUS 2 China 3 Korea 4 JPN 5 BRN6 MYS 7 SGP 8 VNM 9 REA 10 India11 USA 12 CAN 13 MEX 14 Argentina 15 Brazil16 EU27 17 GBR 18 TUR 19 RUS 20 NZL21 CHL 22 PER 23 ROW

23

Share by partner countries of Metal Products Export from Japan (difference from base case)

Impact on Korea:GDP & Investment

24

Korea

China

Japan

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

Perc

enta

ge D

evia

tion

from

Bas

elin

e

GDP

Korea

China

Japan

-8

-7

-6

-5

-4

-3

-2

-1

0

1Investment

Impact on Korea:Trade

25

Korea

China

Japan

-10

-8

-6

-4

-2

0

2

4Exports

Korea

China

Japan

-20

-15

-10

-5

0

5

10

Imports

Impact on Korea:Trade

26

Korea

China

Japan

-150000

-100000

-50000

0

50000

100000

150000

200000

Trade Balance

• Negative GDP and investment impacts• GDP impact becomes muted, but investment impact becomes

worse when China reacts• Korea’s agriculture and manufacturing sectors adversely impacted• Korea’s electronics, machinery and services sectors expand

• Korea’s exports increase, no change in imports, imports but increase a lot when China reacts

• Korea’s trade surplus increase, but trade surplus in recession

27

Impact on Korea:Summary

The Impact of EU GDP

28

EU

00.5

11.5

22.5

33.5

44.5

5

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

GDP

China isolation has resulted in the increase of EU GDP, but the reaction from China will reduce somewhat the amount of GDP increase in EU

EU: Investment is declining, when China reacts to the isolation

29

EU

0123456789

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

InvestmentAs global capital inflows will come into China, as the returns in China is increasing

EU: Trade of EU is increasing

30

EU

0

1

2

3

4

5

6

7

8

9

10

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Exports

EU

0123456789

10

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Imports

Trade Balance of EU is decreasing due to Trade Creation and Diversion Effects

31

-350000

-300000

-250000

-200000

-150000

-100000

-50000

0

50000

100000

2019 2020 2021 2022 2023 2024 2025 2026

Sectoral Output is declining, but some promising to textile and light manufacturing

32-14

-12

-10

-8

-6

-4

-2

0

2

4

6

1 O

ther

Agr

i

2 W

heat

3 O

ilSee

ds

4 En

ergy

Ext

5 O

ther

Ext

6 Te

xtW

app

7 Li

ghtM

nfc

8 Pe

troC

oalP

ro

9 C

hem

ical

s

10 M

iner

alPr

o

11 Ir

onSt

eel

12 O

ther

Met

als

13 M

etal

Pro

14 M

otor

15 O

ther

Tran

s

16 E

lecr

onic

s

17 M

achi

nery

18 U

til_C

ons

19 T

rans

port

20 C

omm

unic

ate

21 F

inan

cial

22 O

thSe

rvic

es

23 o

sg

24 d

we

EU

Center for Global Trade AnalysisDepartment of Agricultural Economics, Purdue University403 West State Street, West Lafayette, IN 47907-2056 USA

Global Trade Analysis Project

Stay Connected with GTAP!www.gtap.agecon.purdue.edu

Questions?