FUTURE CHALLENGE IN ISLAMIC INSURANCE (TAKAFUL) IN BANGLADESH · PDF fileFUTURE CHALLENGE IN...

12

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016 69 FUTURE CHALLENGE IN ISLAMIC INSURANCE (TAKAFUL) IN BANGLADESH Mohammed Jabed Sarwar Research and Product Development Unit, Al Zara Consulting Ltd., Chittagong, Bangladesh ABSTRACT In the last few decades Takaful (Islamic Insurance) has become very popular in Bangladesh as well as other Muslim countries. But the business of takaful did not flourish up to the mark in Bangladesh. The takaful industry was started its journey in Bangladesh in 1999. Now there are six full-fledged takaful operators and thirteen window operation of conventional operators. The takaful industry refers to carry out financial transactions that are compliant with the creed of Islamic principles or laws, by and large called as Sharia. These paper aims to examine the experience, challenges and key drives for the growth of the latest progress of Takaful industry in Bangladesh. The main focal point of this paper will be human capital development. The Islamic insurance services industry has become an even more important agenda to ensure that its growth and development is supported by the necessary skills and capabilities. This is particularly important for Islamic insurance given that it has become the most rapidly growing segment in world financial system. To make broad discussion, we examine six biggest takaful operators in Bangladesh. Currently there is a lack of Islamic finance knowledge among the financial and non-financial industries that still needs to be improved. Keywords: Training and Development, Islamic insurance, Human Capital Development, Bangladesh Corresponding author’s e-mail: [email protected] INTRODUCTION Islamic insurance would be successful in Bangladesh, thanks to the local phenomenon of the flourishing Islamic banks as well as the success of Islamic economy globally. "Islamic economy is gaining momentum. Takaful has already been successful in different Muslim countries like Sudan and Malaysia, even in non-Islamic countries like the USA. This has been an incentive for us. Now, in Bangladesh 39 insurance companies are engaged in insurance businesses of various types. Among them 18companies are life insurance companies including the state owned Jiban Bima Corporation. In 2000, Sarah based life insurance business was introduced in the country by Fareast Islami Life Insurance Co. Ltd. They incepted their business on 29th May 2000. After that another two companies- Prime Islami Life Insurance Ltd and Padma Islami Life Insurance Co. Ltd began their business operation. At present most of the life insurance companies of the country have introduced an Islamic life insurance wing to fulfill customers demand. So, the application of Islamic management is essential in these organizations for the proper operation of the Islamic insurance system. The present paper highlights the above matters and tries to point out the aspects for proper implementation of Islamic management system development in the life insurance companies. Compared to the conventional insurance sector in Bangladesh, Islamic insurance is like how David was to Goliath. While conventional insurance has been doing business in this South-Asian country for over 50 years, Islamic insurance only made its appearance as late as December 1999. There are about 43 conventional insurance companies operating in the country with a large network of branches and yet more are applying for license each year. Islamic insurance, on the other hand, operates through seven companies. However, the good news is that Islamic insurance can explore a hitherto untapped market to do swinging business. While the future may look bleak for conventional insurance companies, given the socio-economic conditions in Bangladesh, Islamic insurance is set to sweep the market. Islami Bank Bangladesh Limited (IBBL), the first Islamic bank in the country, for establishing the concept of Islamic finance. This, they say, has gone a long way in helping other Islamic banks and Islamic insurance companies gain a foothold. IBBL is one of the leading banks in the country, inspiring four other Islamic banks to come up as well as encouraging conventional banks to start Islamic branches and another to open Islamic counter. The success of Islamic banking made people start thinking about Islamic insurance as well. 43 general insurance companies already operating in Bangladesh, the market is somewhat saturated. Their business volume is also not increasing that much yearly, with the amount of premiums coming in every year standing more or less static at Taka 400-500 crore."

Transcript of FUTURE CHALLENGE IN ISLAMIC INSURANCE (TAKAFUL) IN BANGLADESH · PDF fileFUTURE CHALLENGE IN...

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

69

FUTURE CHALLENGE IN ISLAMIC INSURANCE

(TAKAFUL) IN BANGLADESH

Mohammed Jabed Sarwar

Research and Product Development Unit, Al Zara Consulting Ltd., Chittagong, Bangladesh

ABSTRACT

In the last few decades Takaful (Islamic Insurance) has become very popular in Bangladesh as well as other

Muslim countries. But the business of takaful did not flourish up to the mark in Bangladesh. The takaful

industry was started its journey in Bangladesh in 1999. Now there are six full-fledged takaful operators and

thirteen window operation of conventional operators. The takaful industry refers to carry out financial

transactions that are compliant with the creed of Islamic principles or laws, by and large called as Sharia. These

paper aims to examine the experience, challenges and key drives for the growth of the latest progress of Takaful

industry in Bangladesh. The main focal point of this paper will be human capital development. The Islamic

insurance services industry has become an even more important agenda to ensure that its growth and

development is supported by the necessary skills and capabilities. This is particularly important for Islamic

insurance given that it has become the most rapidly growing segment in world financial system. To make broad

discussion, we examine six biggest takaful operators in Bangladesh. Currently there is a lack of Islamic finance

knowledge among the financial and non-financial industries that still needs to be improved.

Keywords: Training and Development, Islamic insurance, Human Capital Development, Bangladesh

Corresponding author’s e-mail: [email protected]

INTRODUCTION

Islamic insurance would be successful in Bangladesh, thanks to the local phenomenon of the

flourishing Islamic banks as well as the success of Islamic economy globally. "Islamic economy is gaining

momentum. Takaful has already been successful in different Muslim countries like Sudan and Malaysia, even in

non-Islamic countries like the USA. This has been an incentive for us. Now, in Bangladesh 39 insurance

companies are engaged in insurance businesses of various types. Among them 18companies are life insurance

companies including the state owned Jiban Bima Corporation. In 2000, Sarah based life insurance business was

introduced in the country by Fareast Islami Life Insurance Co. Ltd. They incepted their business on 29th May

2000. After that another two companies- Prime Islami Life Insurance Ltd and Padma Islami Life Insurance Co.

Ltd began their business operation. At present most of the life insurance companies of the country have

introduced an Islamic life insurance wing to fulfill customers demand. So, the application of Islamic

management is essential in these organizations for the proper operation of the Islamic insurance system. The

present paper highlights the above matters and tries to point out the aspects for proper implementation of Islamic

management system development in the life insurance companies.

Compared to the conventional insurance sector in Bangladesh, Islamic insurance is like how David was

to Goliath. While conventional insurance has been doing business in this South-Asian country for over 50 years,

Islamic insurance only made its appearance as late as December 1999. There are about 43 conventional

insurance companies operating in the country with a large network of branches and yet more are applying for

license each year. Islamic insurance, on the other hand, operates through seven companies. However, the good

news is that Islamic insurance can explore a hitherto untapped market to do swinging business. While the future

may look bleak for conventional insurance companies, given the socio-economic conditions in Bangladesh,

Islamic insurance is set to sweep the market.

Islami Bank Bangladesh Limited (IBBL), the first Islamic bank in the country, for establishing the

concept of Islamic finance. This, they say, has gone a long way in helping other Islamic banks and Islamic

insurance companies gain a foothold. IBBL is one of the leading banks in the country, inspiring four other

Islamic banks to come up as well as encouraging conventional banks to start Islamic branches and another to

open Islamic counter. The success of Islamic banking made people start thinking about Islamic insurance as

well. 43 general insurance companies already operating in Bangladesh, the market is somewhat saturated. Their

business volume is also not increasing that much yearly, with the amount of premiums coming in every year

standing more or less static at Taka 400-500 crore."

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

70

Against this bleak backdrop, the religious sentiments of Bangladesh nationals have become the trump card of

Islamic insurance companies. "Nearly 85percent of our population is Muslim," of this, at least 30-40 percent

does not go in for any kind of insurance at all, fearing it will be tainted with riba. If you consider life insurance,

more specifically, we would say only three to five percent of the populations covered by this type of insurance.

So here is this virtually virgin market waiting to be tapped. Not only will be able to capture a large segment that

has gone uninsured so far, we would also be able to wean away Islamic-minded people from conventional

insurance firms to which they have gone to in the absence of takaful companies in the country."

In Bangladesh, insurance is a must for any kind of export-import business. Companies who take loans

from banks have to be insured. We expect the bulk of our business, therefore, to come from Islamic banks. With

this, both takaful companies as well as Islamic banks will help one another generate income. Islamic insurance

companies will come across the problem of riba. As it is, the takaful companies are forced to invest some of

their money in interest-bearing bonds. Also, in the absence of any re-takaful organizations in the country, and

due to existing legal requirements, all insurance companies have to reinsure at least 50 percent of their business

with the state-owned Sadharan Bima Corporation, a conventional insurance company.

The government has been trying to help Islamic finance further by floating a Mudharaba bonds that

would enable Islamic banks to keep their statutory liquid reserves invested in it and avoid riba. It is therefore

expected that the government would do the same for Islamic insurance as well. The only thing is, it will take

some time. Islami Bank Bangladesh Limited was founded with the major objective of establishing Islamic

economy or balanced economic growth by ensuring reduction of rural-urban disparity and equitable distribution

of income. Islami Bank Bangladesh Limited (IBBL), the largest private bank in the country is the only

commercial bank that offers Grameen styled retail microcredit to a large number of borrowers. The microcredit

program known as ‘Rural Development Scheme’ was launched in 1995 as pilot program styled after the

Grameen Bank model except that the scheme used Islamic modes of investment.

Finally, it may be mentioned that if the Islamic financial system, is to become truly liquid and efficient

it must develop more standardized and universally (or at least widely) tradable financial instruments. The

development of a secondary financial market for Islamic financial products is crucial if the industry is to achieve

true comparison with the conventional system. It must also work hard to develop more transparency in

financial reporting and accounting and ideally - a form of Islamic GAAP. Development if the whole sale and

especially inter-bank and money markets, will be the key to Islamic finance growing outside its current little

sphere of influence, and becoming a truly national invigorating force.

METHODOLOGY

The information of this paper is mainly based on primary and secondary data. Primary data has been collected

through questionnaires. Other than the information from the questionnaires, rest of the data has been collected

from secondary sources. All the required information of questionnaire has been collected by direct interviews

and discussion with executives of various life and non-life Islamic insurance and expert personnel’s of Islamic

and Takaful insurance. Some of the policy holders of Islamic insurance provided some insight into the problems

and issues of the study. All the secondary information is collected from various books, financial papers,

documents, articles and annual report related with Islamic finance, Islamic Insurance and banking and provision

of Sharia. The collected data and information have been tabulated, processed and analyzed carefully. During our

research period, we tried our best to get acquainted with all the rules and regulations, policy and Sharia

compliance. Annual reports of Islamic Life and non-life Insurance in Bangladesh provided us with valuable

information about growth and portability i.e. Return on Net profit after tax as the percentage of total assets and

net revenue as the percentage of total assets. The data acquired by questionnaire helped us to make a test named

X2 (Chi Square test). It helped us to find out, whether the education on Islamic Finance is significantly needed

to keep the present growth in Islamic Insurance (both life and non-life) or not? To prepare this report I also

followed some guidelines provided by some key personals of Islamic Insurance and Finance in Bangladesh.

LITERATURE REVIEW

Insurance is a risk-sharing arrangement between two parties. In this arrangement, one party (the insurer) agrees

to indemnify another party (the insured) against certain losses specified by a contract (the policy). Insurance is

an economic device by which individuals and organizations can transfer pure risks (that is, uncertainty about

financial losses) to others. (Obaidullah, 2005). In other words, insurance is basically a mutual-help where people

intend to help each other. However, we have to underline, that insurance here is to transfer a risk from one party

to another party, which risk itself is pure risk and not speculative risk. Pure risk is different with speculative

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

71

risk, where the outcome for the pure risk is only loss not gain. On the other hand, speculative risk is where there

is probability to gain.

One may say that insurance is not really needed due to people can be self-insured. In contrast, it can be

accepted since people must be having an emergency fund for the loss which can be suddenly occurred. How

about if the loss is too great? Or else the emergency fund is less than the loss, and we have to borrow some

money and have to pay it back. As the result, people come out with the idea of insurance which they can

mutually-insured. Technically, insurance reduces risk, when individuals transfer risk to insurer they exchange a

risk to the premium. After risk is transferred to the premium, there is no need to set up an emergency-fund

anymore. In the insurer side, after receiving a risk as an exchange of the premium, risk will be summed up in

one pool in which other people have transferred similar loss exposures to the insurer. If any loss occurs and the

insured make a claim, then that claim will be taken from the pool in which with an assumption that not everyone

who has joined into the pool not make a claim. How about if everyone makes a claim? Insurer has thought

about it, insurer will invest the money which has been collected from the pool into another tools of investment

so that loss could be covered plus make some profit in which according to Islam is prohibited and will be

explained further.

LEGAL RULING OF ISLAMIC INSURANCE IN BANGLADESH

In Bangladesh, Takaful (Islamic insurance) has been defined in the Insurance Act, but no rules/regulations have

been made so far. Sharia scholars have to come forward with their suggestions so as to decide finally as to what

Sharia compliant is and what is not. A risk based approach along with well thought out rules based regulations

may be appropriate. An important decision for the Sharia people and the regulators is whether to allow Takaful

windows. There are several other issues where consensus is required and need regulatory support. Regulatory

support is a key factor for the continued development and growth of Takaful. A good example is Malaysia

which has become the biggest Takaful market worldwide. This is due to the comprehensive Takaful regulations

and continuous support by the Regulator Bank Negara Malaysia. In Indonesia, the regulator allows conventional

insurers to set up Takaful windows. Recently, Pakistan's regulator SECP issued new Takaful rules allowing

conventional insurers to set up Takaful windows. In Bangladesh, Insurance Act 2010 allows conventional life

insurance companies to open Takaful windows but non-life conventional companies are barred from opening

Takaful windows.

In Takaful, the shareholders are expected to provide the initial capital, but ultimately the participants

(policyholders) are expected to build up the necessary solvency capital. The challenge of setting solvency

standard for Takaful operators needs to be handled very carefully by the Regulator. The International Financial

Services Board (IFSB) has set a standard with regard to solvency requirements for Takaful. The standard

envisages separate ring fenced shareholders' and policyholders' funds, where each fund would need to have

sufficient assets to meet the solvency obligations. It has been assumed that the shareholders would be obliged to

extend interest-free loan to the policyholders' fund when it is needed. The standard is silent on how Takaful

products will be priced and what happens to the contributing policyholders, if the fund created by them is used

to finance future policyholders. The regulators need to introduce creative solutions to these issues. Besides the

legal and regulatory issues, there are a number of practical challenges that also need to be addressed in order to

ensure the success of this nascent industry. For example there is a great need to educate the general public about

insurance and Takaful.

Although the Takaful industry has seen double digit growth since 2010, it still suffers from a lack of

penetration in supposedly vibrant markets, and is still performing at what is considered to be lackluster levels.

Many within the industry have admitted to a gamut of issues which need to be addressed urgently and

effectively in order to allow the industry to perform at its best; particularly in the investment space, where

Takaful companies are suffering from a dearth of long term investment opportunities to suit their risk and

investment profiles. Another issue stems from the lack of risk based capital, where there is a mismatch between

the companies' assets and liabilities, and the universal issue of lack of talent and understanding of Sharia-based

insurance products.

We take a closer look at the fundamentals of the Takaful industry, its issues from a macro and micro

perspective, and what needs to be done to mitigate these problems in order to prevent a stagnation of growth

within a sector which is ultimately brimming with potential. Strong competition, evolving regulations and

shortage of Takaful expertise are identified as key risks in both the GCC and Southeast Asia. While most

operators agree that the new regulations are a positive development, they are concerned over increased variances

in regulatory regimes across jurisdictions. Such variances make it difficult for Takaful operators to function

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

72

across regions and also lead to confusion for customers and multinational insurers. Ultimately, industry

consolidation would allow Takaful operators to compete effectively with larger, more established conventional

insurers and also reduce unhealthy price wars.

THE PROBITION OF CONVENTIONAL INSURANCE UNDER ISLAMIC LAW

Initially, conventional insurance contains three elements that contradict the sharia (Islamic law).

Uncertainty (Gharar)

Any transaction entered into should be free from excessive uncertainty. The purpose of this prohibition is to

avoid fraud, injustice and exploitation. In a conventional insurance, uncertainty arises when insured pays a

premium but does not know whether he is going to make a clam in the future. And the amount of financial

benefit to be received is not known as well. Similarly, the insurer does not know whether he is going to be called

upon to pay claims under the policy, nor the amount to be paid to the insured.

Gambling (Maisir)

Gambling is obviously not permissible under Islamic law. In a game of gambling, one party is always hoping for

a gain as a cost of losing for another party. In the context of insurance, the policyholder hopes (bet) to gain a

large sum from his small amount of contribution. What the policyholder actually hopes is that the claim will

exceed his contribution. In this case, the company would probably be in deficit. However, the policyholder

would loss the money paid for premium if the insured event does not occur. Here, the gambling is playing its

role. When the policyholder does not make any claim during the period, the insurance operator may obtain all

the profit while the policyholder may not obtain any profit at all. The loss of premiums on abolition of contract

by the policyholder will only be burden to the policyholder. Furthermore, only a proportional refund would be

made if any termination of contract done by the insurance company.

Interest (Riba)

An insurance contract wherein the policyholder expects to obtain a fix amount of profit that is greater than what

he has contributed is considered as riba. Hence, the conventional insurance is prohibited under Islamic law.

Furthermore, the investment of premiums usually involves prohibited elements such as riba and maisir.

THE DISTINCTION BETWEEN CONVENTIONAL AND ISLAMIC INSURANCE

Different views have been expressed about the conventional insurance from the point of view of Islam (Ali

Khan, 2004). It is said that conventional insurance is prohibited due to the elements of Riba (interest), Gharar

(uncertainty) and Maisir (gambling). However, insurance is permissible in Islam when undertaken in the

framework of takaful or mutual guarantee and ta’awun or mutual cooperation. It is not like conventional

insurance where a party offers and sells protection and the other party accepts and buys the service at a certain

cost or price. Rather, it is an agreement by a group of people with common interests to protect of guarantee each

other from a certain misfortune. It is based on sincerity and willingness of the group to help anyone among

them. Essentially, the concept of takaful is based on solidarity, responsibility and brotherhood among

participants (Obaidullah, 2005). These are the main points of different between takaful and conventional

insurance:

Conventional insurance is a buy-sell contract in which the insurance company offers and sells

protection and the participants (policyholders) accepts and buys the premium at a certain price. In case of

Islamic insurance, the participants give up individual rights to attain collective rights over contribution and

benefits along with the takaful operator as the one who manage the fund. The contract under Islamic insurance is

usually involves the concepts of tabarru, mudaraba and wakala.

In case of conventional insurance, insurer’s profits include underwriting surplus, which is the

difference between total premiums received from and total claims and benefits paid to policyholders.

Essentially, profit comprises underwriting surplus plus investment income. The distribution of profits or surplus

is a managerial decision taken by the management of the insurer. As a result there is a conflict of interest

between shareholders of the insurer company and the policyholders. In case of Islamic insurance, on the other

hand, the operator has no claims in underwriting surplus. Further, it is the takaful contract, not the management

of the operator company that specifies in advance how and when profit will be distributed. There is little room

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

73

for conflict between interests of shareholders of the operator company and the policyholders. This point is

further elaborated in the subsequent chapter dealing with alternative models of Islamic insurance (Obaidullah,

2005).

Conventional insurance is based on profit-motive and its goal is to maximize revenue to shareholder.

The business of insurance is owned by shareholder. Islamic insurance, in contrast, is based on the motive of

community welfare and protection. The nature of business is non-profit oriented. The one who manage the

operation is called takaful operator. At this point, the takaful operator only received a fair compensation as being

an agent for the policyholder and through a share in returns on investment of funds. In case of conventional

insurance, when there is no claim during the period agreed, the policyholder will lose his premium that has been

paid to the insurer. In Islamic insurance, however, when there is no claim being made during the period agreed,

the underwriting surplus is given back to the policyholder, or donated to charity.

In a life insurance policy, where the risk occurs, the beneficiary(s) shall have the right to claim whole

amount named in policy. But, if in case the risk does not occur, the insured shall have the right to claim the

policy value at maturity together with the interest if any. In a life takaful policy, on the other hand, if the risk

occurs the beneficiary(s) shall have the right to claim the policy value from the PSA (Participant’s Special

Account) besides the accumulated entire amount from the PA (Participant’s Account). But, if in this category of

policy, the participant survives at the maturity of the policy, his/her claim shall be confined within the amount

available in the PA (Ma’sum Billah & Patel, 2003). In conventional insurance the investment of premiums is

completely at the judgment of the insurer with no involvement by policyholder. As such investment usually

involves prohibited elements of riba and maisir. In contrast, the takaful contract specifies how and where the

premiums would be invested. Usually, the takaful operator will invest the premiums in shari’ah compliant areas.

The Islamic insurance company has an additional obligation to pay annual zakat while in conventional

insurance, there is no such obligation.

FINDINGS

Findings from Secondary Data

Islamic insurance (Takaful) means the act of group of people reciprocally granting each commercial profit

sharing contract between the providers of funds for a business venture and the entrepreneurs who actually

conduct the business. In other words, the Takaful business conducted by the company and the individual

members of a group of participants who desire to reciprocally guarantee certain loss or damage that may be

inflicted upon any one of them. An overview of the growth in the Islamic Insurance practice, in Bangladesh, is

discussed below.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

74

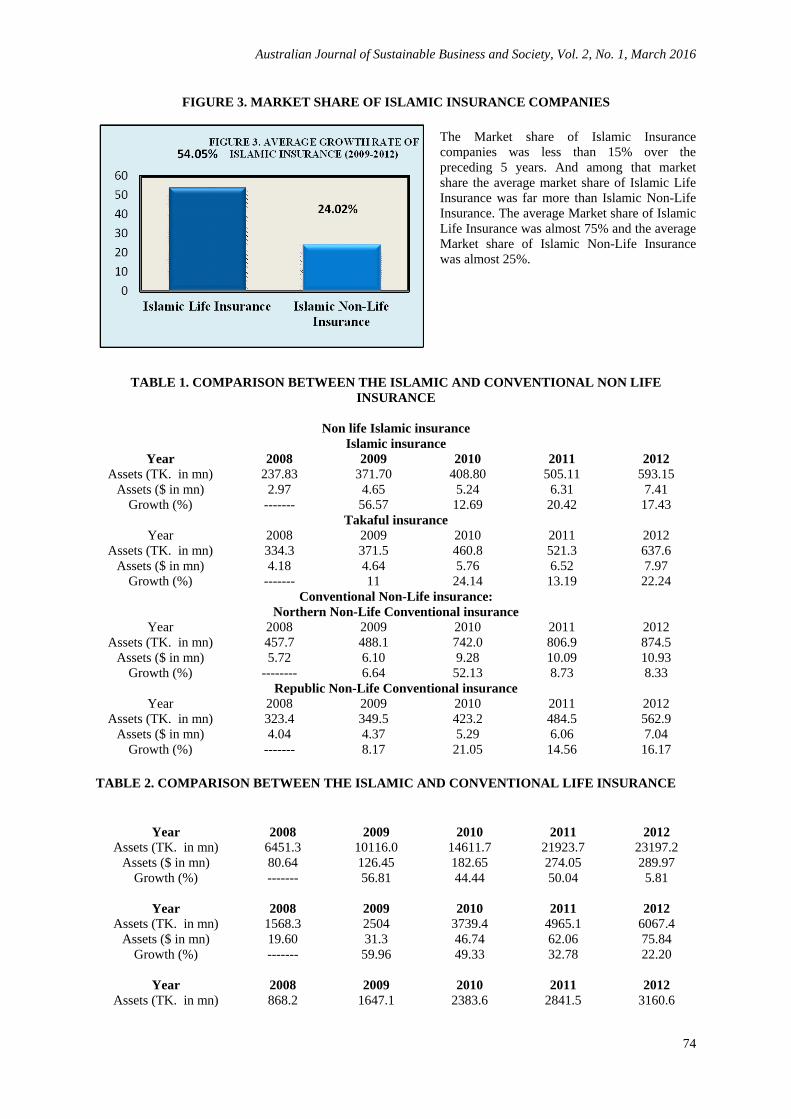

FIGURE 3. MARKET SHARE OF ISLAMIC INSURANCE COMPANIES

The Market share of Islamic Insurance

companies was less than 15% over the

preceding 5 years. And among that market

share the average market share of Islamic Life

Insurance was far more than Islamic Non-Life

Insurance. The average Market share of Islamic

Life Insurance was almost 75% and the average

Market share of Islamic Non-Life Insurance

was almost 25%.

TABLE 1. COMPARISON BETWEEN THE ISLAMIC AND CONVENTIONAL NON LIFE

INSURANCE

Non life Islamic insurance

Islamic insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 237.83 371.70 408.80 505.11 593.15

Assets ($ in mn) 2.97 4.65 5.24 6.31 7.41

Growth (%) ------- 56.57 12.69 20.42 17.43

Takaful insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 334.3 371.5 460.8 521.3 637.6

Assets ($ in mn) 4.18 4.64 5.76 6.52 7.97

Growth (%) ------- 11 24.14 13.19 22.24

Conventional Non-Life insurance:

Northern Non-Life Conventional insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 457.7 488.1 742.0 806.9 874.5

Assets ($ in mn) 5.72 6.10 9.28 10.09 10.93

Growth (%) -------- 6.64 52.13 8.73 8.33

Republic Non-Life Conventional insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 323.4 349.5 423.2 484.5 562.9

Assets ($ in mn) 4.04 4.37 5.29 6.06 7.04

Growth (%) ------- 8.17 21.05 14.56 16.17

TABLE 2. COMPARISON BETWEEN THE ISLAMIC AND CONVENTIONAL LIFE INSURANCE

Fareast Islamic life insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 6451.3 10116.0 14611.7 21923.7 23197.2

Assets ($ in mn) 80.64 126.45 182.65 274.05 289.97

Growth (%) ------- 56.81 44.44 50.04 5.81

Prime Islamic life insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 1568.3 2504 3739.4 4965.1 6067.4

Assets ($ in mn) 19.60 31.3 46.74 62.06 75.84

Growth (%) ------- 59.96 49.33 32.78 22.20

Padma Islamic life insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 868.2 1647.1 2383.6 2841.5 3160.6

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

75

Assets ($ in mn) 1.85 20.59 29.80 35.52 39.51

Growth (%) ------- 89.77 44.73 19.19 11.23

Conventional Life insurance:

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 1253.6 1737.6 2587 2840.5 3181.3

Assets ($ in mn) 15.67 21.72 32.34 35.51 9.80

Growth (%) -------- 38.61 48.90 39.77 12

National Life insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 13141.0 16286.0 20422.5 23823.8 27919.9

Assets ($ in mn) 164.26 203.58 253.28 297.81 349

Growth (%) -------- 13.94 25.40 16.66 17.19

Popular Life insurance

Year 2008 2009 2010 2011 2012

Assets (TK. in mn) 6300.8 9479.6 13216.9 16722.8 21235.9

Assets ($ in mn) 78.76 118.50 165.21 209.04 265.45

Growth (%) -------- 50.46 39.42 26.53 26.99

The average growth rate of both the Islamic Life insurance & Conventional Life insurance had been

following an increasing trend. But from the chart, it can be identified that the average growth rate of the Islamic

life insurance is much higher than the Conventional Life insurance. At the same time it can be noticed that,

though the growth rate of Islamic life insurance is higher, but the amount of increase in the assets is much less

compared to the Conventional Life insurance.

This scenario indicates that the

confidence of the people, in Bangladesh, is

increasing on the policies of Islamic life

insurance. But at the same time majority of

the people still rely more on the practice of

Conventional Life insurance. But with

such an impressive growth rate the Islamic

Life insurance might dominate the market

in the near future.

GROWTH RATE OF ISLAMIC LIFE

INSURANCE ON THE BASIS OF

ASSETS

Average Growth rate of Islamic Life Insurance

According to the chart, the average growth rate of Islamic Life Insurance companies from 2009 to 2012 had

been quite impressive. It brings forward the fact that the general people have got aware and attracted to the

policies and practice of Islamic Life Insurance. From this a conclusion can be drawn that in 2012, more people

rely on the Islamic Life Insurance, compared to 2009.

Average growth rate of Islamic Non-Life Insurance:

The average growth rate of Islamic Non-Life Insurance has increased since 2009. People of Bangladesh have

got acquainted with and has also adopted the policies of Islamic Insurance. Now they rely on this practice to

secure their important belongings with much encouragement, than they used to do till 2009.

Comparison of growth rate between Islamic Life and Non-Life Insurance

Though the growth rate of both the Islamic Life Insurance and Islamic Non-Life Insurance has increased, but the

increase rate of Islamic Life Insurance is much higher than the Islamic Non-Life Insurance. It suggests that the

people of Bangladesh rely on Islamic Insurance for their lives compared to their belongings.

Probability of Islamic Life Insurance

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

76

To calculate profitability we have considered ROTA (Return on Total Assets). Increase of Islamic non-life

insurance return means Net profit after tax and in case of Islamic life insurance return means balance of revenue

showed in balance sheet.

Return on total assets indicates that

how much return or revenue an organization

is generating by utilizing its assets. A higher

rate indicates better utilization of the

organization’s assets.

According to the chart, the current

position of the organizations of Islamic Life

Insurance indicates an impressive scenario.

It brings forward the fact that an average of

84.83% revenue is generated by utilizing the

total assets of the organization.

The data of Islamic Non-Life

Insurance indicates that by utilizing the

assets, the organizations are generating an

average of 7.29% Net profit after tax. It

indicates that the organizations are quite

efficient in utilizing its assets.

FINDINGS FROM QUESTIONNAIRE SURVEY

The total number of respondents in our

questionnaire survey was 30 employees from

the field of Islamic Insurance. Among them 12

are high level executives, 14 are mid-level

Executives and the rest 4 are Sharia expertise.

All the respondents are post graduated and

among them 20 of the respondents are male and

the rest 10 are females. Among the respondents

9 are fresh new comers in the industry through

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

77

their current job and the rest 21 respondents came

into this industry from other work fields.

We have collected a lot of information

from the employees of different Islamic Insurance

Organizations, regarding their viewpoints towards

the existing image of Islamic Insurance sector in

Bangladesh. They have pointed out several factors

that influence the growth, development and present

condition of the Islamic Insurance sector in our

economy.

Difference

According to the 60% respondents of our survey

business operations of Islamic Insurance is

different from Conventional Insurance in various

aspects. According to them the information system

of Islamic Insurance, in terms of interest, premium

and policies, are quite transparent and clear

compared to the Conventional Insurance.

Another very significant difference

between Islamic and Conventional Insurance is that

when someone buy a Conventional Insurance

policy they cannot claim their premium after

maturity if they do not face the mentioned

difficulties in the policy. But in case of Islamic

Insurance the premiums are being distributed to the

clients on maturity, even if the mentioned occurrence does not take place.

Employees enter the Conventional Insurance sector by having some basic knowledge about it since a

part of it is present in our education system. But the employees who enter the Islamic Insurance sector, enters as

a clean slate. So it takes a lot of time for the new entrants of this industry to get acknowledged with their job.

Satisfaction Level

In our survey it came forward that 80% of the

employees are satisfied with their working

condition in the Islamic Insurance organizations.

According to them they are proud to work for

their organization and its causes. However, the

rest 20% respondents do not consider their

working condition very impressive. According

to tem, the working condition of an organization

is formed by the employees and technologies

with which they complete their work. And both

the factors of working condition in these

organizations are not enough efficient.

According to them the employees are untrained

and the technologies used are not enough up to

dated. And until measures are not being taken to

improve these factors the working condition will

remain unsatisfactory for them.

Training

In terms of training a huge lacking is being brought forward by the respondents. According to them, they do not

get the opportunity to acquire adequate training regarding their job before or after they take entrance in this

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

78

particular job field. This drawback does not

only hold back the performance of the

employees but also become an obstacle for

the growth of the organization as well as for

the growth of the industry.

According to the survey, 90% of the

respondents believe that a mandatory

training program should be introduced for

the new comers in this industry. They

believe that different seminars should be

organized in order to inform the existing

employees, regarding the correct form of

performing their tasks. This will help to

boost up the efficiency of the employees and

result in a further development of this

industry as a whole.

The survey suggests that 80% of the respondents think that expatriates from other countries should be invited in

the organizations to train the existing employees. They believe that the ideas and work strategies shared by the

expatriates will help them to acquire an international view point regarding this field. Those ideas can be taken as

guidelines and followed accordingly to achieve the desired success in the long run.

Investment Restrictions

Another factor that restrains the expansion of Islamic Finance is the lack in investment in this sector. One of the

reasons for this might be the limited number of products available for making a potential investment. Since

Islamic Insurance sector is quite new in Bangladesh,

only a small number of products are available in the

market in the present period.

Unawareness of the people regarding the

practice and policies of this sector can also be a reason

for the inadequate amount of investment in this sector.

According to the survey, 90% of the respondents

consider that the Islamic Insurance organizations should

take necessary and cautious measures in order to

aware the people of Bangladesh about their

existence and policies. They should come forward

and try to attract the general population towards

buying their policies. With this the organizations

can even encourage the investors to step forward

and make investments in this sector.

Challenges

The growth and development of the Islamic Insurance sector is being held back by a number of factors. First of

all, there is a very minimum amount of Regulatory framework towards the sector of Islamic Insurance. An

increased number of government policies and government intervention in this sector can be proved as very

beneficial for its growth and development. A lack of education concerning this sector also proves to be a very

vital drawback for the Islamic Insurance sector. According to the respondents of our survey subjects regarding

Islamic Finance should be introduced in our education system in the graduation and post-graduation level. It

could have been proved as a very good suggestion if put to practice.

90%

10%

FIGURE 8. RESPONDENTS' VIEW TOWARDS

TAKING MEASURES FOR ATTRACTING PEOPLE

Measures

required to

attract people

No measures

required to

attract people

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

79

There is also a lack of training and knowledge regarding this sector in our economy. As a result the

employees working in this sector faces ignorance in various stages of their work field. Some training must be

provided to the new entrants of this sector so that they can get well identified with their future duties and

responsibilities while performing their job. A very small amount of technologies are being introduced by the

practitioners of the Islamic Insurance. New technologies are very much required for the development of every

sector and especially for a developing sector such as Islamic Insurance. But before putting the technologies to

practice, the employees should be trained by the expert technicians so that the employees do not find any

difficulties while coping with the changes.

Future prospects

The growth rate and development of Islamic Insurance sector in Bangladesh is currently following an increasing

trend. But it is also inevitable that without proper training and knowledge the growth will not be able to be

sustained. The scenario might even get reversed. To sustain this growth rate and for further development it is

necessary to arrange different training and education programs. The government and Islamic Insurance

organizations should come together and provide such opportunities to the existing and upcoming employees of

this sector. The organizations of Islamic Insurance should take policies and measures to aware and attract

common people towards their products. They should make attempt to build a strong marketing department for

the Islamic Insurance sector, and make innovations in their existing products to encourage people to come

towards this sector.

According to my survey 80% of the respondents believe that Islamic Insurance sector has high

potential in Bangladesh. But this potential needs proper nourishment from both the organizations and regulatory

body. The government should take some major steps for the betterment of this sector. The government itself can

establish an Islamic Insurance organization to improve the faith of people in this sector. This will also encourage

people to get more aware of the products and scopes of Islamic Insurance sector. This will drastically improve

the condition of Islamic Insurance sector in Bangladesh. More regulatory framework should also be developed,

by the government, in favor of this sector.

CONCLUSION

In the field of the Islamic insurance, the impact of global acceptability may reflect in the day to day

enhancement in the field of financial industry of Bangladesh due to its enormous growth rapidly around the

globe. Helping industry in terms of development of more mature Islamic insurance products and better controls

and risk mechanisms is by having the appropriate education and knowledge of the field is un-discretionary

allows the career to progress eventually. The fact is that based on the level of knowledge and understanding of

Islamic finance that every individual holds is the foundation of Islamic insurances.

The growth rate of Islamic Banking and Finance itself have not augmented with the demands for

learning centres, education providers and training module which creates the gap of practical and theoretical

aspects of Islamic insurance. The level of Sharia compliance will be questioned and resultants can be

significantly drastic if no solutions found. The Islamic insurance industries have to take initiative to launch a

professional Certification of Islamic insurance with the support of skilled working people and with the market

needs. In Bangladesh, there's is no such institutions/universities which offer professional certificate courses in

insurance that enable seeker to be recognized. More challenging approach and experience of external club that

lead towards in acquiring divergent viewpoint is significant to increase the knowledge base through external

courses for professional growth.

In Islamic insurance and finance, we must explore the opportunities which are detrimental to the

economy and to be able to safeguard the future of our children from an unfavourable interest based system. To

motivate current market players and to attract prospective investors, the government needs to develop a sound

regulatory and legal framework for the Islamic financial industry in which a dedicated research and steps are

required to all stakeholders. To increase the growth of this sector in Bangladesh all stakeholders should play a

role to develop an economic system truly reflective of the true sacred principles.

REFERENCE

Ahmad M. S. (2007). Takaful in Southeast Asia: The growing pains and challenges? Kuala Lumpur, Malaysia:

ICMIF Takaful.

Ali, K. M. M. (2006). Basis And Models of Takaful: The need for Ijtihad. ICMIF Takaful.

Australian Journal of Sustainable Business and Society, Vol. 2, No. 1, March 2016

80

Ali, K. M. M. Introduction to Islamic Insurance. Dhaka.

Ali, K. M. M. PresentScenario and Future Potentials of Takaful.

Aziz, F. A., & Lian, T. K. (2006). NTUC Income’s Experience in Developing Takaful Insurance. Kuala Lumpur,

Malaysia: ICMIF Takaful.

Bakarudin, I. (2007). Establishing A Robust Legal and Regulatory Framework For Takaful. Financial

Regulators Forum in Islamic Finance, 29 March.

Billah, M. M., & Patel, S. (2003). An Opportunity for ICMIF members to provide Islamic insurance (Takaful)

products. Kuala Lumpur, Malaysia: ICMIF Takaful.

Dingwall, S., & Griffiths, F. (2006). The United Kingdom: Regulatory approach to takaful. Kuala Lumpur,

Malaysia: ICMIF Takaful.

Fisher, O. (2009). HistoricalReview, Importance, and an Introduction to insurable Risk. In A.R. Yousri Ahmed

(Ed).Principles of Takaful.Manama, Kingdom of Bahrain: BIBF, 11-26.

http://www.islamicfinancenews.com/get.php?file=V7i5.pdf

Ishak, B. (2007). Establishing a Robust Legal and Regulatory Framework for Takaful. Financial Regulators

Forum in Islamic Finance, 29 March.

Khan, A. A. (2003). Difference between Islamic and Conventional Insurance. Insurance Journal.

Khan, L. A. (2005). How does takaful differ from insurance. Maybank Annual Report, 2009.

Obaidullah, M. (2005). Islamic financial services. Jeddah, Saudi Arabia.

Stagg-Macey, C. (2007). An overview of Islamic insurance. Kuala Lumpur: ICMIF Takaful.

Syarikat Takaful Malaysia Annual Report, 2009.

Taylor, D. Y. (2005). Takafulin the New Millennium. Kuala Lumpur, Malaysia: ICMIF Takaful.

Taylor, D. Y. (2005). Ten-Year Master Plan for the Islamic Financial Industry (Takaful).

Tolefat, A. (2006). Mixed model is best approach. Kuala Lumpur, Malaysia: ICMIF Takaful.