FUTURE BUSINESS PLAN FEASIBILITY REPORT - Sajjad · FUTURE BUSINESS PLAN FEASIBILITY REPORT . ......

21

SAJJAD TEXTILE MILLS LIMITED Page 1 SAJJAD TEXTILE MILLS LIMITED FUTURE BUSINESS PLAN FEASIBILITY REPORT

Transcript of FUTURE BUSINESS PLAN FEASIBILITY REPORT - Sajjad · FUTURE BUSINESS PLAN FEASIBILITY REPORT . ......

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 1

SAJJAD TEXTILE MILLS LIMITED

FUTURE BUSINESS PLAN

FEASIBILITY REPORT

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 2

TABLE OF CONTENTS

1. Executive Summary 4

2. Introduction 5

3. Certifications 5

4. Proposed Management Structure 5

5. Future Business Plan 7

6. Operational Plans 8

7. Multi-Dimensional Marketing Strategy 9

8. Investment In Pakistan Stock Exchange Limited 10

9. Market and Competition Analysis 13

10. SWOT Analysis 13

11. Industry Trends 16

12. Exports 17

13. Import of Spinning Machinery 19

14. Product / Service Description 20

15. Financial Projections 21

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 3

Mission Statement The Mission of Sajjad Textile Mills Limited is to be the finest

organization, and to conduct business responsibly

and in a straight forward way.

Our basic aim is to benefit the customers, employees

and shareholders and to fulfill our commitments to the society.

Our hallmark is honesty, innovation, teamwork of our people

and our ability to respond effectively to change in all aspects

of life including technology, culture and environment.

We will create a work environment, which motivates, recognizes

and rewards achievements at all levels of the organization because

In Allah We Believe & In People We Trust We will always conduct ourselves with integrity

and strive to be the best

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 4

EXECUTIVE SUMMARY

OBJECTIVES OF REPORT

The broad objective of this report is to provide an overview on trading and marketing of yarn and fibres and restructure Sajjad Textile Mills from yarn manufacturing to trading of yarn, fibre and investment in listed securities through proposed disposal of its Land, Building and other assets and its viability.

COMPANY OVERVIEW

Textile spinning industry in Pakistan continues to struggle through a global economic downturn. Weak export market has caused many units to sell their product locally which has added immense downward pressure on yarn prices within Pakistan. Inadequate and costly power supply led to reduced capacity utilization which augmented to additional losses. Moreover, import of Indian yarn has further added to this pressure and is causing serious issues for spinner in the country. Many spinning units have shut down their operations as production viability remains very low. In addition to the numerous adversities being faced by the industry, there has been a serious mismatch in cost of raw material prices as compared to yarn prices. Yarn prices of natural fiber, man-made fiber and blended fiber remained depressed the entire year. The macro-economic environment in the last couple of years has played a significant role and affected the textile industry on the whole. The inability of Government to take appropriate steps to encourage the most important sector of the economy rendered the textile industry to either close or to continue running in losses ultimately unable to keep-up with their debt obligations. The Government also failed to take notice of high lending rates, reduction in punitive duties and refusal of banks to show flexibility towards textile industry. The combined effect of all the factors have resulted in disaster for such industries.

The Company had already suspended its manufacturing operations since September 22, 2016 due to shortage of working capital, unfavorable market conditions and continuous losses. At the balance sheet date, the Company’s accumulated losses stood at Rs. 499.010 million. In view of aforesaid, the Management has proposed to dispose of the Land, Building and other assets to partially settle the pressing liabilities of the Company and to initiate trading activities as allowed by Memorandum of Association of the Company.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 5

INTRODUCTION

Sajjad Textile Mills Limited (the Company) was incorporated as a public limited company in Pakistan

under the Companies Ordinance 1984 and is listed on Pakistan Stock Exchange Limited. The company was

incorporated on 12th June 1988 and obtained certificate of commencement of business on 20th March

1989. The company is being managed by a family whose three generations are in the textile business for

over four decades. The Directors, Sponsors and Associates hold around 94% shareholding of the Company.

CERTIFICATIONS

BUREAU VERITAS has certified Sajjad Textile Mills Limited for UKAS Quality Management, ISO 9001

Certification.

PROPOSED MANAGEMENT STRUCTURE

Sajjad Textile Mills Limited as a trading concern will be managed by its Chief Executive Officer Mr.

Muhammad Asim Sajjad, its Chief Operating Officer Mr. Sajjad Aslam and its Director Finance Mr.

Salman Muhammad Aslam

Mr. Muhammad Asim Sajjad is a seasoned businessman, completed his graduation from United

Kingdom in 2001 and started working as Chief Executive since June 2006. He bears good knowledge

of the textile industry including hands on experience in production activities.

Mr. Sajjad Aslam, a graduate from Punjab University, has a vast and diversified experience of nearly

45 years in the textile sector. He has hands on experience with all the contours of management,

manufacturing and trading processes.

Mr. Salman Muhammad Aslam is a business management graduate from Bentley University-USA

and has been looking after the financial and commercial activities of the Company since 2006. He

also handles sales and promotional activities and has a very competent and active personality in

Company’s management.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 6

RESTRUCTURING METHODLOGY

After a careful financial analysis of Sajjad Textile Mills Limited and finances available with the

company in the form of sale proceeds of Land, Building and other assets after payments of its certain

liabilities, the following restructuring proposal has been developed. The restructuring will be in two

phases:

1. Sale of Land, Building and other assets of the company and settlement of certain liabilities.

2. Initiation of trading of yarn, natural/man-made fibre and investment in listed securities.

The management has sought approval from its members to dispose of the Land, Building and other assets

and to start trading of yarn, fibre and/or allied products and investment in listed securities keeping in view

the prevailing circumstances.

The company intends to enter in trading of different varieties of yarn, fibre and/or allied products, the first

target for the management is to maintain its recent clientele in yarn market of Pakistan and

international market. After its recent clientele is maintained, company intends to enter in trading of

different and specialized varieties of these products, and the plan includes in getting exclusive selling,

distribution and branding rights to some of the renowned brands in the textile industry.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 7

FUTURE BUSINESS PLAN TRADING PORTFOLIO - YARN, FIBRE AND/OR ALLIED PRODUCTS

The global export patterns are changing fast as a result of reduction in trade barriers and technological advancements that have led to gains in productivity and change in comparative advantage patterns in world economies. Asian economies such as China and India are enjoying a notable growth in changing circumstances across the world. Pakistan also has great potential for higher growth however the political threats, socio economic environment and lack of updated technologies are obstruction in the way of progress. Some sectors of Pakistan economy have shown a good performance in terms of turnover volumes and exports. Due to the current economic situation in Pakistan surrounding large-scale manufacturing and the importance of textile industry in the country, management of Sajjad Textile Mills Limited has decided to take approval from its members to change its primary business from manufacturing of yarn to trading of different varieties and counts of yarn, fibre and/or allied products and investment in listed securities.

Keeping in sight the future outlook of Pakistan’s economy and capital position in post CPEC era, management has planned for the company to enter yarn, fibre and allied products trading business. While running as a yarn manufacturing business, Sajjad Textile Mills Limited had a lot of limitation in terms of the variety of its products, as switching from one count to another, one fiber to another or between different blends had a lot of cost and investment attached to it, while manufacturing other varieties of yarn was not possible without capital investment in new machinery and building. In the trading business, these switching costs are minimized and it is possible for the company to start trading in different varieties of yarn, fibre and/or allied products.

Company senior management is already in contact with different local and international buyers/sellers/agents in order to make a steadfast entry in this field. Although actual business can only be started once capital investment is available by selling off its land, building and other assets as proposed in the EOGM notice. The management has started engaging company’s recent clientele while looking for new business partners as well. Some of yarn counts and fibres company has planned to include in its business are:

1. NE 08/1-80/1 Cotton Carded Yarn 2. NE 10/1-80/1 Cotton Combed Weaving 3. NE 16/1-65/1 Polyester Viscose Blended Yarn 4. NE 20/1-70/1 Polyester Cotton Blended Yarn 5. Viscose, Tencil and Polyester Fibre 6. Different varieties of specialized yarn.

Non-exhaustive list, and product range might change from time to time depending on prevailing market conditions.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 8

OPERATIONAL PLANS

Management of Sajjad Textile Mills Limited is in contact with both recent clientele and also with new potential trading partners in this field. This includes both local and foreign partners. Following are some of international textile companies being considered in this regard focusing mainly on China and Indonesia:

1. Xiamen C & D Light Industry Co., Ltd. China 2. Formosa Chemicals & Fibre Corporation (FCFC) 3. South Pacific Viscose (SPV) 4. Birla Fibres Co., Ltd. 5. Wuhu Fuchun dye & weave co., Ltd. China 6. Zhejiang Twin Lantern Home Textiles Co., Ltd. China 7. Hickman International N.T. Hong Kong 8. Tai Zeus International Corporation Taiwan 9. Jinfang Cotton Technology Co., Ltd. China 10. Hangzhou Fuchun dye & weave co., Ltd. China 11. Tai Zeus International Corporation Taiwan

Management is in contact with these firms regarding import/export of different variety of yarn and fibre to Pakistan, which also includes exclusive selling and branding rights to some of the renowned textile brands in the world. Additionally, the Management is also in contact with number of local companies/agents who are willing to extend their full cooperation in the future business of the company.

TARGET MARKET

First focus of management in terms of target market or customers will be to at least maintain company’s recent clientele by providing quality yarn, fibre and/or allied products to them at best possible prices. Efforts have already been made in this regard and management has received a very positive response.

After maintaining its customer base, management plans on introducing specialized yarn, fibre and/or allied products in the local industry, which include Acrylic and other varieties. These products required specialized machinery and are not widely manufactured by the local industry, while have a reasonable demand.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 9

MULTI-DIMENTIONAL MARKETING STRATEGY

Given the nature of our product and the variety we plan on introducing, we will have a multi-dimensional marketing strategy. This would include marketing through our salaried distribution team, commission agents and making use of the growing e-B2B environment in the industry.

i. SALES TEAM

To keep our current clientele engaged and to specifically target the organized sectors of the industry, we would have a suitably sized sales team.

ii. COMMISSION AGENTS

Commission agents provide a large number of services and act as a bridge for both contracting parties. Khan & Khan’s (2010) research emphasizes on their importance in Pakistan’s textile sector. As further depicted by Nordas (2004), services of intermediaries include getting the contract signed by both parties; these contracts contain conditions about product quality, quantity, packing, delivery time, shipping company and other related clauses.

In Pakistani textile industry, commission agents provide services of finding buyers, negotiating the deal, and giving credit to buyers. Their role is very important for exploring new markets, as not only the agents cut down the risk by buying on cash and providing credit to their clients but also they buy in large quantities and supply to smaller customers.

iii. E-B2B FORUMS

Electronic business to business (e-b2b) forums are a growing trend in textile industry of Pakistan, but majority of the players in the industry lack awareness on high to reap full benefits of such services. ICT can play a significant role in reducing transaction costs; it can be seen as a direct alternative to the traditional intermediaries (Christiaanse, et al., 2001, pp.464). As Chong et al (2010) argues that the intermediary cost can be eliminated if buyers view the products directly over the Internet and then contacts the supplier directly. Thus, with the increased use of Internet amongst various industrial suppliers and buyers, the traditional role of intermediaries becomes questionable (Tay and Chelliah, 2011, pp.217). Alibaba, tradekey, yarn.com, fabric.com and other such websites already account for huge transactions in the textile industry.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 10

INVESTMENT IN PAKISTAN STOCK EXCHANGE

Although decades of internal political disputes and low levels of foreign investment have led to slow growth and underdevelopment in Pakistan — which has a nominal GDP of $270 billion and a per capita income of $5,000 — the embattled country has succeeded in attracting very positive reviews in the recent times from numerous Western media houses, the World Bank and the globally-acclaimed credit rating agencies like Moody’s, etc.

For example, the recent report of the Indian edition of Quartz, a digital global business news publication, which was initially sponsored by internationally known firms like Messrs Credit Suisse, Boeing, Chevron and Cadillac, etc, has revealed that Pakistan has beaten major Asian economies this year in stock market performance as the country’s benchmark equity index, the Pakistan Stock Exchange, has been the fifth best performing throughout the world.

Quartz India, which is viewed by over half a million unique visitors every month, has stated: “The Brazil, Russia, India, China and South Africa (BRICS) grouping is passe and the top emerging markets are losing sheen. The British exit (Brexit) has battered stocks the world over and currencies across economies are weakening. In times like these, guess what’s working for the global equity markets? Pakistan. The South Asian nation, mostly in the news for terrorism and political violence, has beaten major Asian economies this year in stock market performance. In 2016, Pakistan’s benchmark equity index, the PSX, has been one of Asia’s best performing. In fact, it is the fifth-best performing stock index globally. Bloomberg even referred to Pakistan as an Asian ‘tiger,’ in a report.”

The eminent media outlet, which is run by 175 staffers pulled from prominent journalism brands like Bloomberg, the New York Times, the Economist and the Wall Street Journal, etc, has added: “The Karachi Stock Exchange (KSE) — also known as the Pakistan Stock Exchange—has stood out in recent years, despite a troubled political and security environment. But not all its listed companies are traded on it — in fact, less than a fourth were actively traded in 2014. Nonetheless, improving political and financial stability is helping revive Pakistan’s stock markets. There’s also been some support from a 2012 government amnesty programme, which allowed investors to pour money into shares until June 2014 without their source of funds being questioned. This doubled the average traded volume on the KSE.”

Quartz has maintained: “Launched in 1988, the Morgan Stanley Capital International (MSCI) emerging markets index first included Pakistan in 1994. In 2002, the KSE was shut down due to a stock market crash. Six years later, in 2008, it was temporarily closed following the global financial crisis. Faced with such shutdowns, MSCI dropped Pakistan out of the emerging markets index till this year. Over time, investors have regained confidence in the country’s equity markets. Investment in infrastructure, coupled with aggressive government spending, is making Pakistani markets attractive to investors. Further stability in politics will only help. Meanwhile, the Chinese have announced large investments in the country. When China’s $46-billion investment to build a China-Pakistan Economic Corridor actually happens, it will boost trade and make critical infrastructure, such as power, easily available to individuals and industries alike.”

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 11

An April 27, 2016 report of the Moody’s Corporation, which had reported revenue of $3.5 billion in 2015 and employs approximately 10,800 people in 36 countries, had said: “Pakistan’s B3 issuer rating balances strengthening growth and progress on structural reforms against a relatively high government debt burden and political risks. Moody’s assessment of Pakistan’s “Moderate” economic strength encompasses the sovereign’s very low per capita incomes and the large size of its economy. Economic output, previously anemic, has picked up over recent years and is now rising at a relatively healthy pace. GDP growth has edged up to average 4.1 per cent year-on-year since FY2014, from 3.4 per cent between FY2010-13. The implementation of the China-Pakistan Economic Corridor will likely support activity further, and in concert with energy sector reforms will improve the operating environment for investment.”

The US credit rating agency had held: “Moody’s assessment of institutional strength as Very Low reflects Pakistan’s weak but improving rankings on governance survey indices, specifically the World Bank’s Worldwide Governance Indicators. It also takes into account the central bank’s management of inflation and monetary policy, and progress on reforms under the ongoing IMF programme. Moody’s ‘Very Low (-)’ assessment of Pakistan’s fiscal strength reflects the country’s moderately large debt burden and weak revenue base, which lower debt affordability relative to peers. The share of foreign currency debt to total general government debt has considerably declined in the last five years. But such borrowing still comprises about a third of total public debt, leaving government finances exposed in the event of exchange rate depreciation or financial market volatility.”

The report had observed: “Moody’s assessment of Pakistan’s vulnerability to event risks as High is driven by political risks, both domestic and geopolitical. The government’s relatively large annual borrowing needs, in particular owing to large rollover requirements, are also a constraint. However, recent efforts to lengthen the maturities of domestic debt will likely contain these risks in the future. At the same time, modest external financing needs limit external vulnerability risks.”

Meanwhile, a July 14, 2016 report of a renowned American media house Bloomberg had termed the Pakistan Stock Exchange (PSX) the best of the Asian markets. The Bloomberg report had contended: “Pakistan has regained the ‘tiger’ status in the region with 15 per cent rise and increasing rate of annual growth.”

The report had stated that the Pakistani economy was moving ahead to even stronger points with stable output. Bloomberg had further noted: “Reforms in the privatization programme and better relations with the International Monetary Fund (IMF) have strengthened Pakistan’s economy.” According to the report, inclusion of Pakistan in countries with emerging markets status will increase foreign investment significantly. “Meanwhile, foreign investors are looking at the rewarding outlook in Pakistan after Chinese investment of $46 billion under the CPEC project.”

The American media house had said that transnational investors were considering Pakistan the best market for gains after reduced performance of the Chinese economy and interest rates in the United States.

The report had read: “Pakistan was downgraded to frontier status in December 2008; four months after the Karachi Stock Exchange imposed a rule that caused near total paralysis of market activity for more than three months. The Morgan Stanley Capital International’s Frontier Markets Index currently features 16 Pakistani companies that make up about 9 per cent of the gauge. The Karachi Stock Exchange KSE-100 Index has gained 15 per cent this year, making it the best performer in Asia. The country averted an external payments crisis in 2013 through a loan programme of the IMF and is dedicated to boosting economy to its fastest pace of the decade,” according to the report.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 12

Last but not the least, in February 10, 2016, the World Bank President Jim Yong Kim had opined that Pakistan was on the path of increased economic growth and prosperity. He said Pakistan had an opportunity to become more ambitious in reforming its economy and reducing poverty in the country. At the meeting with the prime minister, the WB chief had highlighted the importance of pressing forward with economic reforms, stating that his institution for the Dasu hydropower project and Tarbela-IV extension project would help the government in improving the energy mix and reduce dependence on expensive fuels.

In view of aforesaid, management of Sajjad Textile Mills Limited has decided to maintain a portfolio in the equity market keeping in view the prevailing circumstances. Company intends to engage suitable financial analysts and maintain a reasonable portfolio, purely based on fundamentals.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 13

MARKET AND COMPETITION ANALYSIS

MARKET ANALYSIS Textile industry in Pakistan, in its widest concatenation is the largest and most important industrial sector in the national economy and occupied a major position in the world Textile Industry in terms of production and exports the demand for cotton/ P.C. yarn in export market has been increasing and this trend is expected to continue in future. At the same time with the introduction of high speed shut less, air jet and other frames of looms in Pakistan, there is rapid growth in the domestic weaving industry. The knitting and power loom industry have also registered a similar increase in demand of cotton yarn. These trends indicated consistently increasing demand for cotton yarn in both export and domestic market.

SWOT ANALYSIS

STRENGTHS - BUILD UPON HOME DEMAN

• Pakistan is a sub-tropical country with mean temperature on the higher side which makes cotton an ideal clothing material for the prevalent climate. Owing to the facility of ample supply of cotton, Pakistan has an innate opportunity to capitalize on this resource endowment as the fourth largest producer of the commodity. The country has the third largest spinning capacity which establishes a strong foothold for further value addition in the sector.

• Given the climatic conditions and culturally rich society, there is an innate demand for cotton clothing. The country is home to people from different ethnicities and cultures with a strong preference towards specific clothing. Furthermore, the recent hype of branded lawn clothing has tapped on a market that promises healthy returns. As is the norm of the industry, customers from lower and middle income strata hoard replicas of the branded products. This trend in clothing is anticipated to stay and ensures a loyal customer base; evidence of the same can be seen in the recent launch of multiple clothing brands over the last three years.

WEAKNESSES – TRAILING IN VALUE ADDED CHAIN

• Minimal and low value-added products dominate exports, constituting over 50% of the exported value. Cotton cloth, cotton yarn, bed sheets and knitwear remain major export generators. Over the last five years, the composition has not undergone any major change except minimal improvement in the share of readymade garments at 18% in FY16 compared to 13% in FY11, leaving significant upside potential untapped.

• Pakistan’s product mix of natural to synthetic fiber (80:20) does not correspond to the international standards (60:40). The latter enhances the usability of raw material as synthetic fiber offers greater flexibility as opposed to natural fiber.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 14

• Lack of developed infrastructure facilities has hindered the growth of textile sector. The country wide energy crisis has adversely affected the textile sector and led to closure and transfer of units to Bangladesh, Turkey and other countries. The facilities installed require up-gradation but the sector is facing dearth of investment as neither local bodies nor foreigners are willing to invest.

OPPURTUNITIES – UNEXPLORED FRONTIERS AND PRODUCTS

• Under Generalized System of Preferences (GSP) plus Status, valid from 2014 till 2017, 70% of Pakistan’s exports are allowed preferential tariffs and partial duty free access. In the face of an energy crisis and depleting foreign exchange reserves, this privileged access to European markets presents an opportunity to capitalize on markets. Previously, Pakistan was allotted this status in 2001 but it did not capitalize upon this opportunity unlike other beneficiaries like Bangladesh, who did not have the edge of sufficient raw material. Out of a total of 6,000 products that are allowed duty free access, Pakistan only exports 150 clearly indicative of the need to diversify.

• Pakistan’s textile trade is heavily tilted towards China. However, other markets like Africa and Russia can be explored, which will not only broaden the export market but facilitate the enhancement of Pakistan’s exports to suit the customer.

• With the facility of abundant good quality raw material at its disposal, Pakistan can alter its product line from low to high value added items. Countries import raw material from Pakistan, process it and sell it with a high mark up which reflects the significant impact of value addition. Given the growth in the world-wide fashion industry, the resources can be redirected to produce items that cater to international tastes specifically. Sales are driven primarily through the “brand name”. Through in-depth research and effective marketing efforts, Pakistan can either launch its own new brands or partner with existing ones to enter new markets. Though such high-end consumers are a niche in Pakistan, the presence of international brands in the local retail market is indicative of the potential this segment offers. Moreover, by emphasizing on the end product, the entire value chain benefits.

THREATS – NOT GETTING INTO NEW TRADE ALLIANCES

• Declining international cotton prices have adversely impacted the local market as well. The ginners have excess bales of cotton and spinners have limited their production.

• As per the International Cotton Advisory Committee (ICAC), world consumption of cotton is expected to remain stable at 23.9mt, post FY16. The reduction can be attributed to lower demand on account of reduced prices of polyester, an alternate man-made fibre. Also, China’s dismissal of the stockpiling policy will take its toll on Pakistan’s balance of payments. For over 5 years, more than 60% of Pakistan’s cotton yarn has been exported to China. Not only had the country generated foreign exchange but the demand had been providing an incentive to local manufacturers to produce more.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 15

• Since the start of 2014, the Euro has devalued considerably. Compared to Chinese yuan and Indian rupee, the effect of devaluation is less pronounced compared to the Pakistani rupee. This makes the Pakistani rupee overvalued compared to other currencies. As Pakistan’s products become more expensive abroad, they become less competitive, translating into decline in exports. This results in lower profitability for local companies.

• As per the Trans Pacific Partnership, member countries will be allowed duty free import of goods. Pakistan’s major markets like EU, USA and Canada are signatories to this agreement which would extend the preferential access to all the members and provide a level playing field, posing a threat to Pakistan’s exports. Vietnam, as the third largest garment exporter, and other countries like Malaysia and Mexico are expected to dent Pakistan’s exports share.

• As part and parcel of GSP Plus Status, Pakistan is required to adhere to the conventions of the United Nations, which primarily pertain to human rights. Given the lax implementation of these conventions in Pakistan, any instance of non-compliance can result in suspension of the status as has been the case with Sri Lanka.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 16

INDUSTRY TRENDS We are in the midst of cotton season in Pakistan, but sadly there is no cotton crop management policy or then perhaps, no real functional government at a time that holds the key in determining the textile sector’s performance over the next twelve months – everyone seems preoccupied with the Panama case instead of dispensing actual governance. Amidst the ongoing high political drama, what we forget is that there is a country to be run! Textile constitutes the largest sector in Pakistan’s exports and the country is faced with a serious current account deficit situation at a time when both our overall exports and textile exports have been declining for more than 3 years now. The irony though is that our finance minister is just not worried, or even worse, he simply does not care. In his opinion, we in Pakistan unnecessarily worry about textiles by giving it more than its due importance, whereas, there are many other areas that require far more focus and attention. Not surprisingly, our competitors do not share his mindset on a sector that almost everyone regards as any developing economy’s potentially largest exporting and employment-generating engine. India, for example, announces its comprehensive cotton crop policy as early as April every year, which is based on its national vision on targeted crop size, farmers’ security, sector’s raw cotton export targets, manufacturing competitiveness, employment safety, effects on allied industry, and safeguarding of national textile made-ups’ exports while side-by-side endeavouring to enhance value addition. Bangladesh, even though it is not a raw cotton producer/grower, also announces a similar policy framework every year to ensure that in the coming year its textile exports remain on track.

As Pakistan slowly emerges from a long-term power crisis, its once booming textile sector is scrambling to find its feet ─ but high energy costs and a decade lost to competitors mean recovery is far from assured. Energy production was severely depressed for more than 10 years due to chronic under-investment, inefficiencies in the power network and an inability to collect sufficient revenue to cover costs. The result was crippling for manufacturers and in particular the textile sector, which employs 30 per cent of the working population. Pakistan is the world's fourth largest cotton producing country but interminable power and gas cuts have stopped exporters from producing their export orders on time.

The recently released textile export numbers paint a bleak picture of the sector. Even though there was an increase of 24 percent and 30 percent on a year-on-year and month-on-month basis respectively in June-17; overall textile exports remained almost stagnant showing a measly increase of 0.4 percent for FY17 over the previous year.

More alarming is the fact that the FY17 figure of $12.45 billion is 6 percent lower than the previous 3 year average number of $13.2 billion. The slide continues as all the prescriptive advice falls on deaf ears in policymaking quarters.

The value added garments sector and bed wear were the only areas that registered positive growth while cotton yarn, cotton cloth, knitwear, towels as well as the others segment registered negative or stagnant growth. The garments sector registered an increase in exports of 6 percent for FY17 on year-on-year basis.

The All Pakistan Textile Mills Association (APTMA) revealed in a recent presentation that Pakistan has lost its global textile export share by 23 percent which poses serious risks to the future sustainability and viability of the textile industry in the country.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 17

It was also of the view that implementation of the PM’s export package is yet to be implemented in letter and spirit. For despite a shortfall of cotton there has been re-imposition of a 4 percent customs duty coupled with a 5 percent sales tax.

The entire textile industry has been desperately asking for the release of pending refunds, implementation of the export package, continuation of zero-rating regime and lowering of energy tariffs –the major issues that have sank the industry. But there has been little progress on these fronts and with every passing day the country loses out on more international markets. It seems for now the slide will continue given the political turmoil the government is in, improving textile exports will surely be on the back-burner.

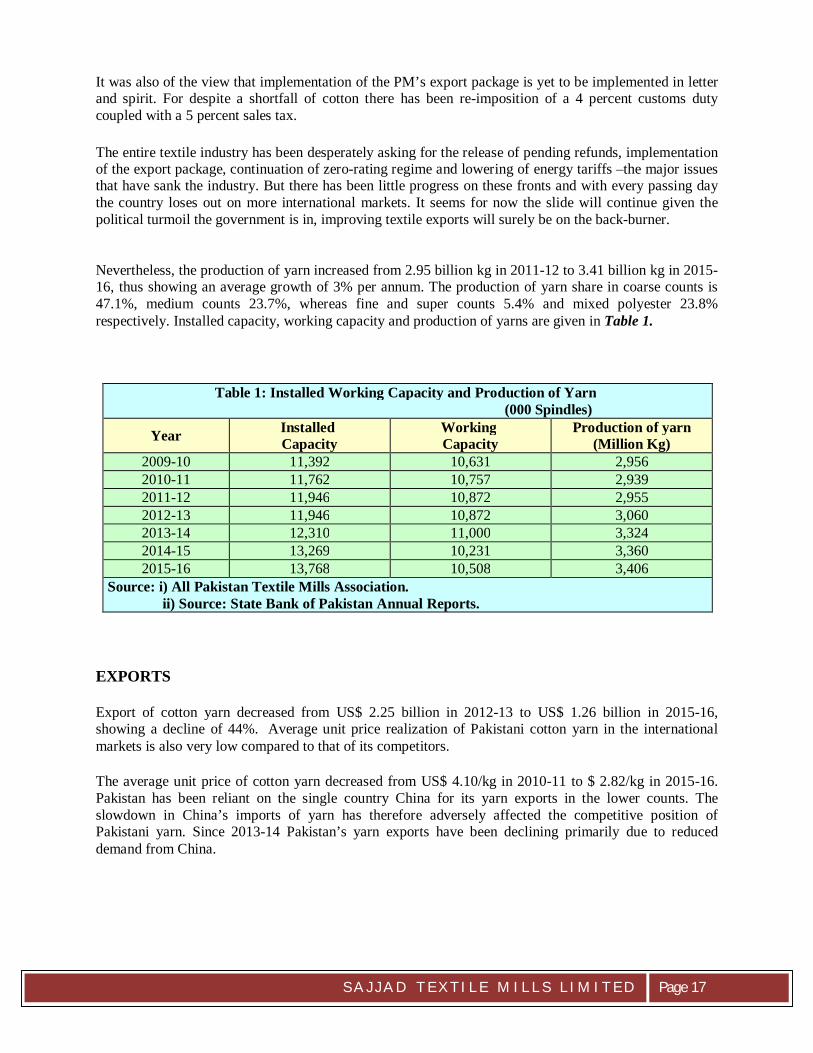

Nevertheless, the production of yarn increased from 2.95 billion kg in 2011-12 to 3.41 billion kg in 2015-16, thus showing an average growth of 3% per annum. The production of yarn share in coarse counts is 47.1%, medium counts 23.7%, whereas fine and super counts 5.4% and mixed polyester 23.8% respectively. Installed capacity, working capacity and production of yarns are given in Table 1.

Table 1: Installed Working Capacity and Production of Yarn (000 Spindles)

Year Installed Capacity

Working Capacity

Production of yarn (Million Kg)

2009-10 11,392 10,631 2,956 2010-11 11,762 10,757 2,939 2011-12 11,946 10,872 2,955 2012-13 11,946 10,872 3,060 2013-14 12,310 11,000 3,324 2014-15 13,269 10,231 3,360 2015-16 13,768 10,508 3,406

Source: i) All Pakistan Textile Mills Association. ii) Source: State Bank of Pakistan Annual Reports.

EXPORTS

Export of cotton yarn decreased from US$ 2.25 billion in 2012-13 to US$ 1.26 billion in 2015-16, showing a decline of 44%. Average unit price realization of Pakistani cotton yarn in the international markets is also very low compared to that of its competitors.

The average unit price of cotton yarn decreased from US$ 4.10/kg in 2010-11 to $ 2.82/kg in 2015-16. Pakistan has been reliant on the single country China for its yarn exports in the lower counts. The slowdown in China’s imports of yarn has therefore adversely affected the competitive position of Pakistani yarn. Since 2013-14 Pakistan’s yarn exports have been declining primarily due to reduced demand from China.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 18

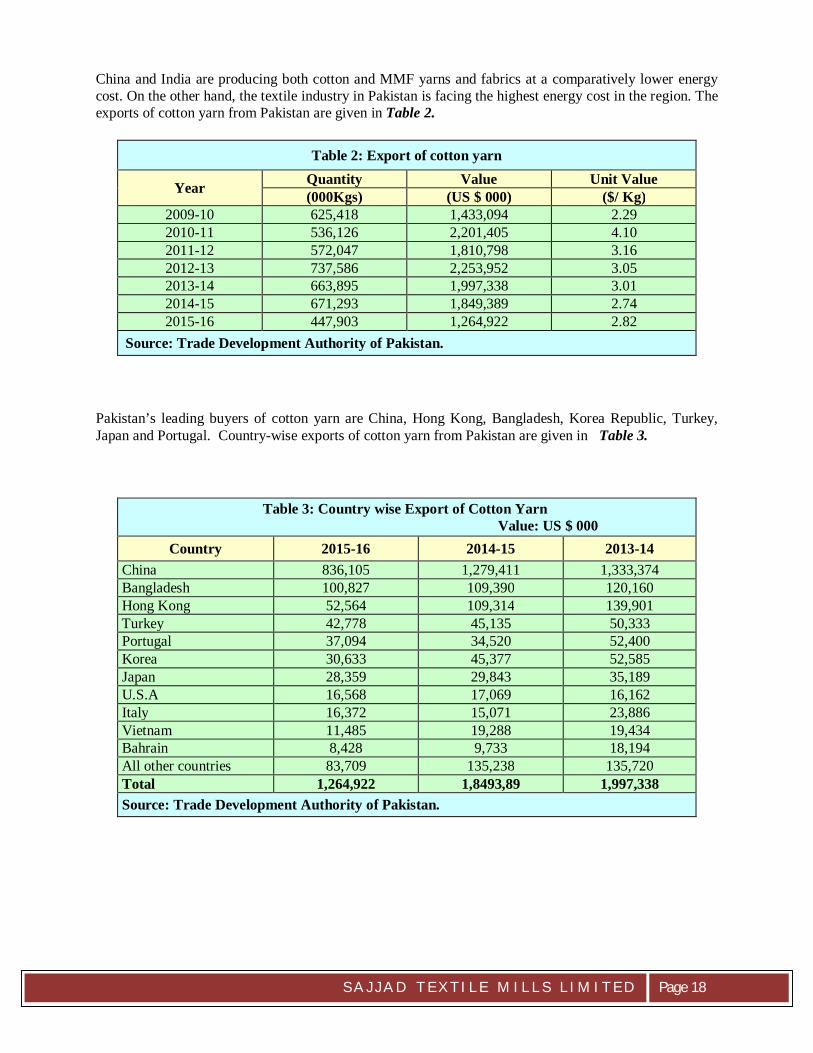

China and India are producing both cotton and MMF yarns and fabrics at a comparatively lower energy cost. On the other hand, the textile industry in Pakistan is facing the highest energy cost in the region. The exports of cotton yarn from Pakistan are given in Table 2.

Table 2: Export of cotton yarn

Year Quantity Value Unit Value (000Kgs) (US $ 000) ($/ Kg)

2009-10 625,418 1,433,094 2.29 2010-11 536,126 2,201,405 4.10 2011-12 572,047 1,810,798 3.16 2012-13 737,586 2,253,952 3.05 2013-14 663,895 1,997,338 3.01 2014-15 671,293 1,849,389 2.74 2015-16 447,903 1,264,922 2.82

Source: Trade Development Authority of Pakistan.

Pakistan’s leading buyers of cotton yarn are China, Hong Kong, Bangladesh, Korea Republic, Turkey, Japan and Portugal. Country-wise exports of cotton yarn from Pakistan are given in Table 3.

Table 3: Country wise Export of Cotton Yarn Value: US $ 000

Country 2015-16 2014-15 2013-14 China 836,105 1,279,411 1,333,374 Bangladesh 100,827 109,390 120,160 Hong Kong 52,564 109,314 139,901 Turkey 42,778 45,135 50,333 Portugal 37,094 34,520 52,400 Korea 30,633 45,377 52,585 Japan 28,359 29,843 35,189 U.S.A 16,568 17,069 16,162 Italy 16,372 15,071 23,886 Vietnam 11,485 19,288 19,434 Bahrain 8,428 9,733 18,194 All other countries 83,709 135,238 135,720 Total 1,264,922 1,8493,89 1,997,338 Source: Trade Development Authority of Pakistan.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 19

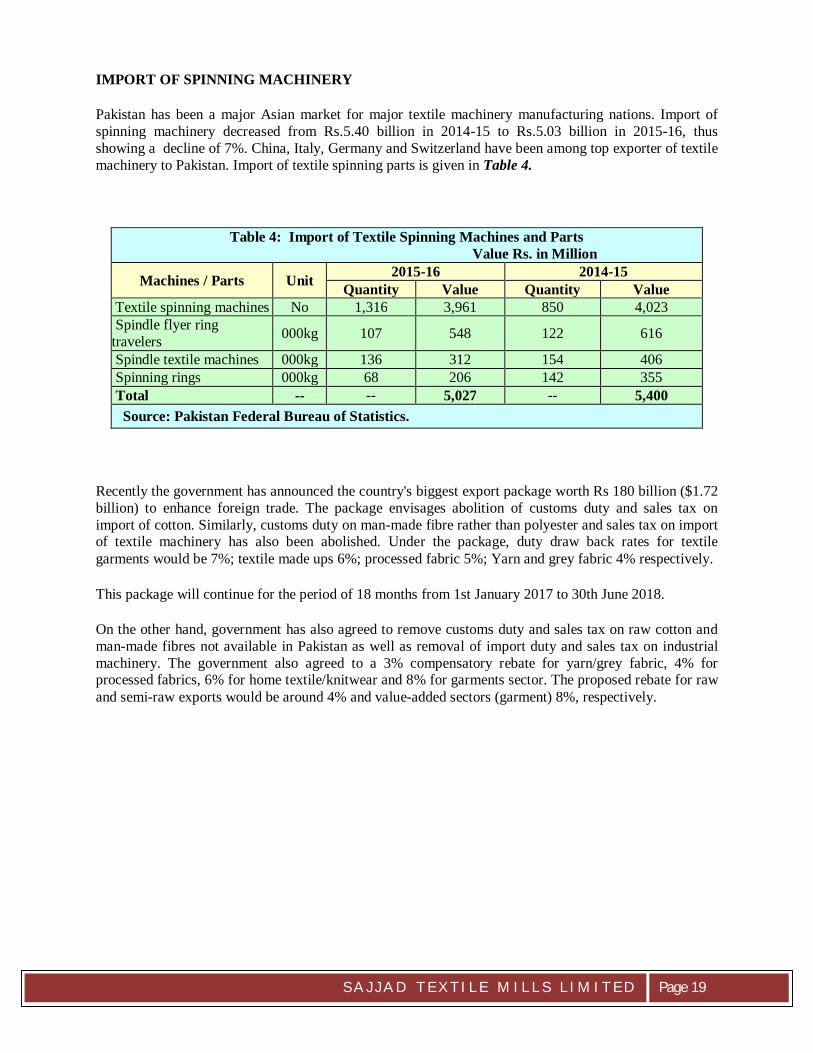

IMPORT OF SPINNING MACHINERY

Pakistan has been a major Asian market for major textile machinery manufacturing nations. Import of spinning machinery decreased from Rs.5.40 billion in 2014-15 to Rs.5.03 billion in 2015-16, thus showing a decline of 7%. China, Italy, Germany and Switzerland have been among top exporter of textile machinery to Pakistan. Import of textile spinning parts is given in Table 4.

Table 4: Import of Textile Spinning Machines and Parts Value Rs. in Million

Machines / Parts Unit 2015-16 2014-15 Quantity Value Quantity Value

Textile spinning machines No 1,316 3,961 850 4,023 Spindle flyer ring travelers 000kg 107 548 122 616

Spindle textile machines 000kg 136 312 154 406 Spinning rings 000kg 68 206 142 355 Total -- -- 5,027 -- 5,400 Source: Pakistan Federal Bureau of Statistics.

Recently the government has announced the country's biggest export package worth Rs 180 billion ($1.72 billion) to enhance foreign trade. The package envisages abolition of customs duty and sales tax on import of cotton. Similarly, customs duty on man-made fibre rather than polyester and sales tax on import of textile machinery has also been abolished. Under the package, duty draw back rates for textile garments would be 7%; textile made ups 6%; processed fabric 5%; Yarn and grey fabric 4% respectively.

This package will continue for the period of 18 months from 1st January 2017 to 30th June 2018.

On the other hand, government has also agreed to remove customs duty and sales tax on raw cotton and man-made fibres not available in Pakistan as well as removal of import duty and sales tax on industrial machinery. The government also agreed to a 3% compensatory rebate for yarn/grey fabric, 4% for processed fabrics, 6% for home textile/knitwear and 8% for garments sector. The proposed rebate for raw and semi-raw exports would be around 4% and value-added sectors (garment) 8%, respectively.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 20

PRODUCT / SERVICE DESCRIPTION

The business line of the company will be trading of yarn and/or natural/man-made fibres in local and/or international market and investment in listed securities under the prevailing circumstances.

Some of yarn counts and fibres company has planned to include in its business are:

1. NE 08/1-80/1 Cotton Carded Yarn 2. NE 10/1-80/1 Cotton Combed Weaving 3. NE 16/1-65/1 Polyester Viscose Blended Yarn 4. NE 20/1-70/1 Polyester Cotton Blended Yarn 5. Viscose ,Tenciland Polyester Fibre 6. Different varieties of specialized yarn.

Non-exhaustive list and product range might change from time to time depending on prevailing market conditions.

S A J J A D T E X T I L E M I L L S L I M I T E D

Page 21

FINANCIAL PROJECTIONS

(Annexed to Notice of Extra-ordinary General Meeting)

Disclaimer: Financial Projections included in this report are based on prevailing circumstances and

underlying assumptions and departures therefrom may affect the projections.