Functional Foods and Health Benefits

36

Health Benefits: Looking at the Next Big Functional Foods

-

Upload

frost-sullivan -

Category

Health & Medicine

-

view

4.916 -

download

0

Transcript of Functional Foods and Health Benefits

Health Benefits: Looking at the Next Big Functional Foods

2

Industry Backdrop

History

Predicting the Future

Top 5 Functional Ingredients

Highlights

Source: Frost & Sullivan.Source: Frost & Sullivan.

Geography

Scientific

Maths

3

Nutraceuticals – Industry Backdrop

4

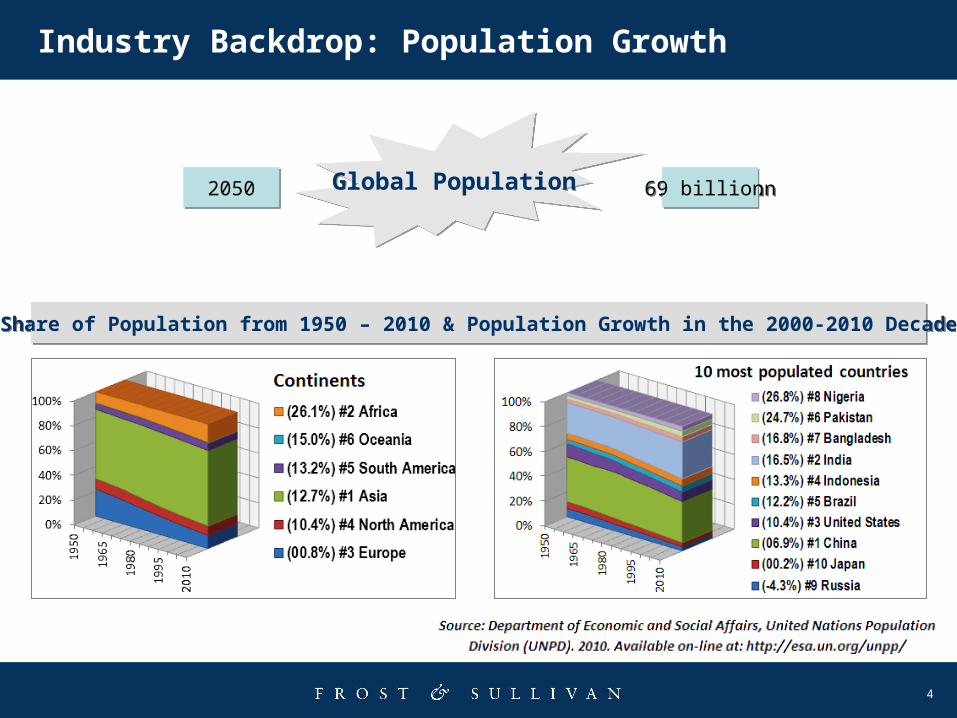

Industry Backdrop: Population Growth

Global PopulationGlobal Population20102010 6.8 billion6.8 billion20502050 9 billion9 billion

Share of Population from 1950 – 2010 & Population Growth in the 2000-2010 DecadeShare of Population from 1950 – 2010 & Population Growth in the 2000-2010 Decade

5

Industry Backdrop: Industry Challenges

Production efficiency

Sustainability

Quality & Safety

Nutrition & Health

Production efficiency

Sustainability

Quality & Safety

Nutrition & Health

Dietary SupplementsFunctional BeveragesFunctional Foods

Nutraceuticals

+ +

Source: Frost & Sullivan.Source: Frost & Sullivan.

6

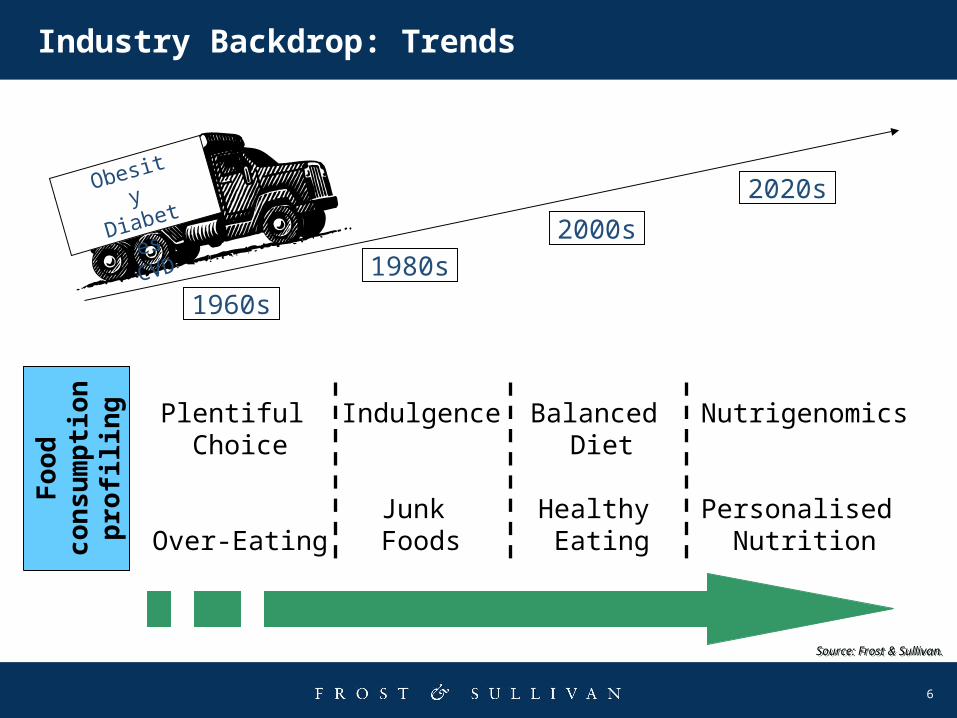

Plentiful Choice

Over-Eating

Food

con

su

mp

tio

n p

rofi

lin

g Indulgence

Junk Foods

Balanced Diet

Healthy Eating

Nutrigenomics

Personalised Nutrition

1960s

2020s

2000s1980s

Obesity

Diabete

sCVD

Industry Backdrop: Trends

Source: Frost & Sullivan.Source: Frost & Sullivan.

7

Nutraceuticals – Predicting the Future

8

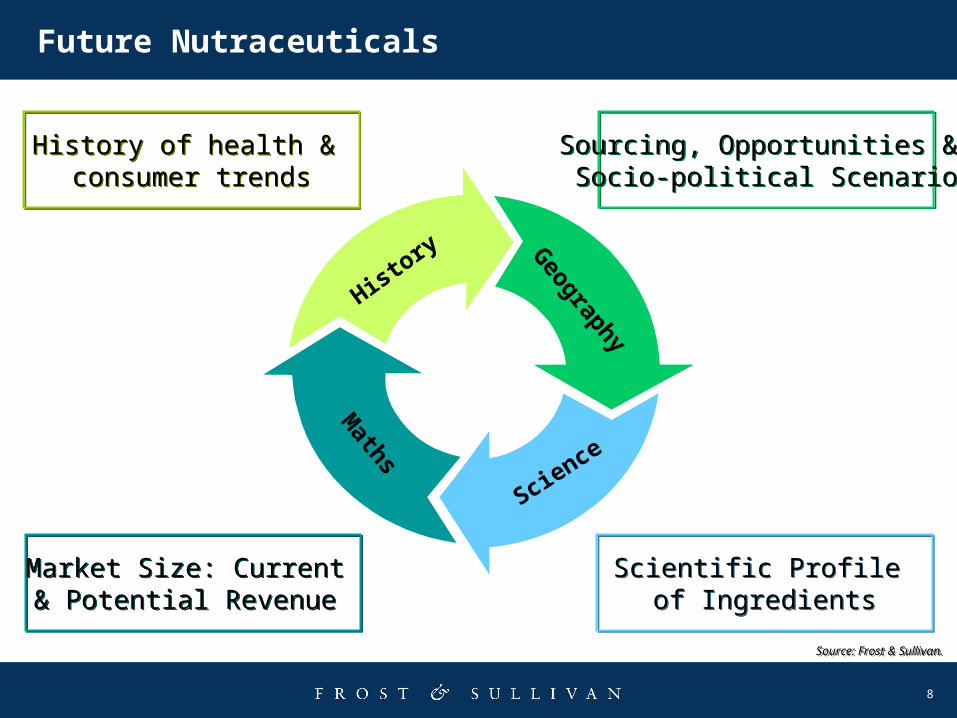

Future Nutraceuticals

History

Geography

Science

Maths

History of health & consumer trends

History of health & consumer trends

Sourcing, Opportunities & Socio-political Scenario

Sourcing, Opportunities & Socio-political Scenario

Market Size: Current & Potential Revenue Market Size: Current & Potential Revenue

Scientific Profile of Ingredients

Scientific Profile of Ingredients

Source: Frost & Sullivan.Source: Frost & Sullivan.

9

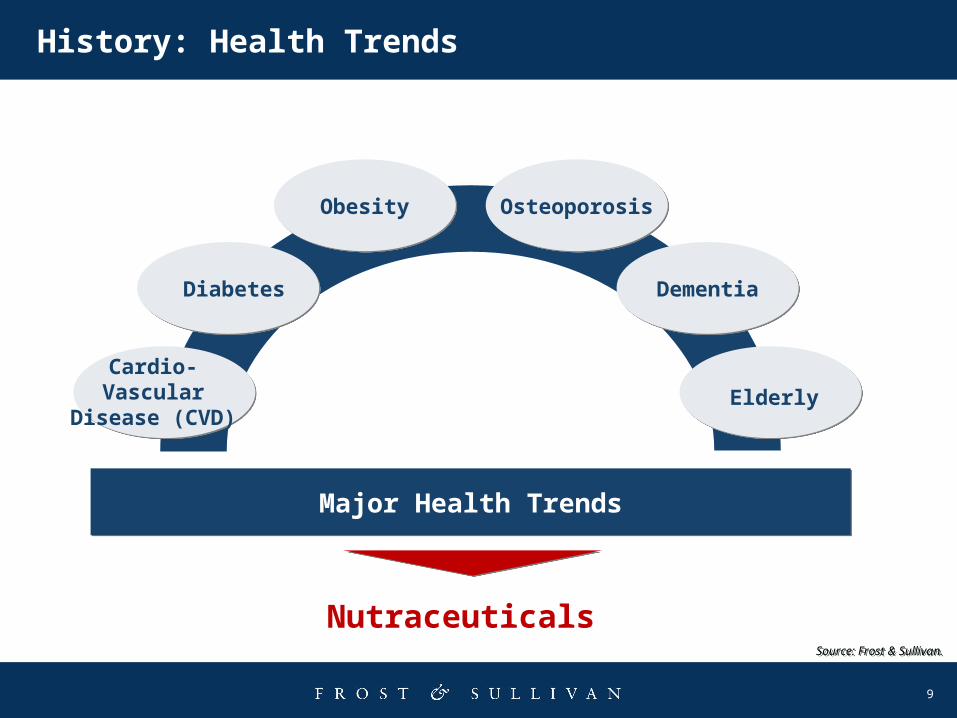

History: Health Trends

Cardio-Vascular

Disease (CVD)

Diabetes

Obesity

Elderly

Dementia

Osteoporosis

Major Health TrendsMajor Health Trends

NutraceuticalsSource: Frost & Sullivan.Source: Frost & Sullivan.

10

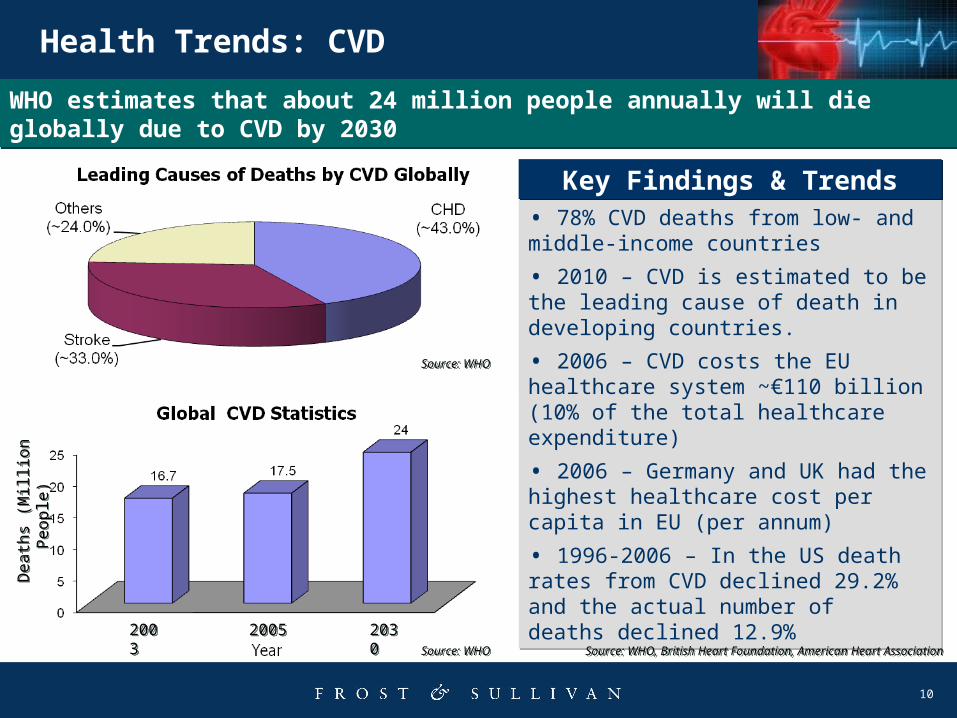

Health Trends: CVD

WHO estimates that about 24 million people annually will die globally due to CVD by 2030WHO estimates that about 24 million people annually will die globally due to CVD by 2030

• 78% CVD deaths from low- and middle-income countries

• 2010 – CVD is estimated to be the leading cause of death in developing countries.

• 2006 – CVD costs the EU healthcare system ~€110 billion (10% of the total healthcare expenditure)

• 2006 – Germany and UK had the highest healthcare cost per capita in EU (per annum)

• 1996-2006 – In the US death rates from CVD declined 29.2% and the actual number of deaths declined 12.9%

• 78% CVD deaths from low- and middle-income countries

• 2010 – CVD is estimated to be the leading cause of death in developing countries.

• 2006 – CVD costs the EU healthcare system ~€110 billion (10% of the total healthcare expenditure)

• 2006 – Germany and UK had the highest healthcare cost per capita in EU (per annum)

• 1996-2006 – In the US death rates from CVD declined 29.2% and the actual number of deaths declined 12.9%

Key Findings & TrendsKey Findings & Trends

Source: WHOSource: WHO

Source: WHO, British Heart Foundation, American Heart AssociationSource: WHO, British Heart Foundation, American Heart AssociationSource: WHOSource: WHO

Death

s (M

illio

n P

eople

) D

eath

s (M

illio

n P

eople

)

20032003

20052005 20302030

11

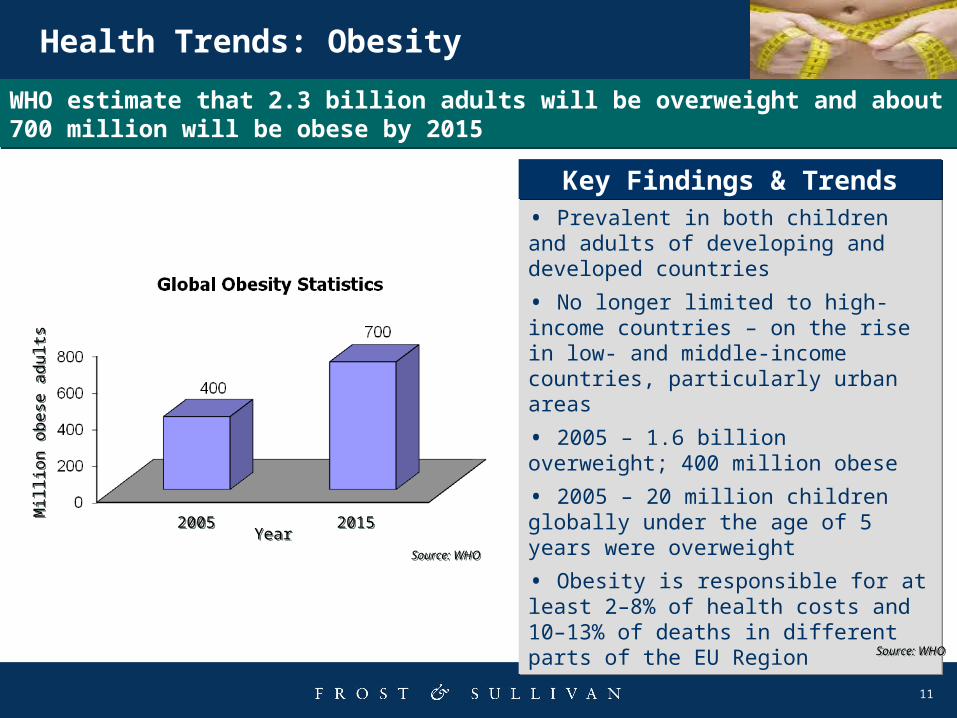

Health Trends: Obesity

• Prevalent in both children and adults of developing and developed countries

• No longer limited to high-income countries – on the rise in low- and middle-income countries, particularly urban areas

• 2005 – 1.6 billion overweight; 400 million obese

• 2005 – 20 million children globally under the age of 5 years were overweight

• Obesity is responsible for at least 2–8% of health costs and 10–13% of deaths in different parts of the EU Region

• Prevalent in both children and adults of developing and developed countries

• No longer limited to high-income countries – on the rise in low- and middle-income countries, particularly urban areas

• 2005 – 1.6 billion overweight; 400 million obese

• 2005 – 20 million children globally under the age of 5 years were overweight

• Obesity is responsible for at least 2–8% of health costs and 10–13% of deaths in different parts of the EU Region

WHO estimate that 2.3 billion adults will be overweight and about 700 million will be obese by 2015WHO estimate that 2.3 billion adults will be overweight and about 700 million will be obese by 2015

Key Findings & TrendsKey Findings & Trends

Mill

ion

ob

ese

ad

ults

Mill

ion

ob

ese

ad

ults

20052005 20152015YearYear

Source: WHOSource: WHO

Source: WHOSource: WHO

12

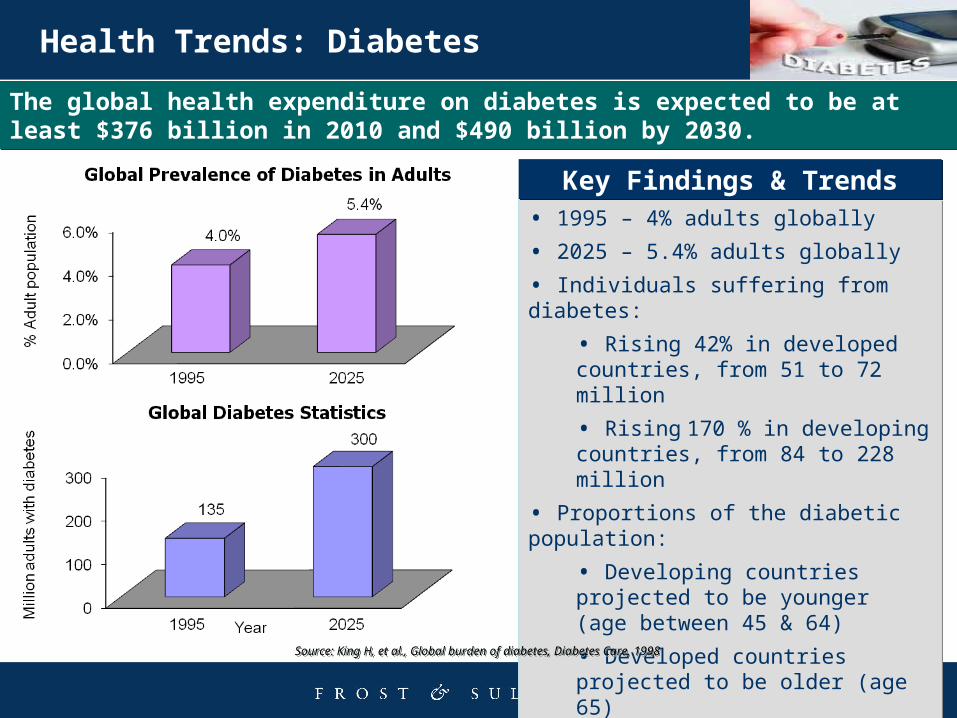

Health Trends: Diabetes

• 1995 – 4% adults globally

• 2025 – 5.4% adults globally

• Individuals suffering from diabetes:

• Rising 42% in developed countries, from 51 to 72 million

• Rising 170 % in developing countries, from 84 to 228 million

• Proportions of the diabetic population:

• Developing countries projected to be younger (age between 45 & 64)

• Developed countries projected to be older (age 65)

• 1995 – 4% adults globally

• 2025 – 5.4% adults globally

• Individuals suffering from diabetes:

• Rising 42% in developed countries, from 51 to 72 million

• Rising 170 % in developing countries, from 84 to 228 million

• Proportions of the diabetic population:

• Developing countries projected to be younger (age between 45 & 64)

• Developed countries projected to be older (age 65)

The global health expenditure on diabetes is expected to be at least $376 billion in 2010 and $490 billion by 2030. The global health expenditure on diabetes is expected to be at least $376 billion in 2010 and $490 billion by 2030.

Key Findings & TrendsKey Findings & Trends

Source: King H, et al., Global burden of diabetes, Diabetes Care. 1998Source: King H, et al., Global burden of diabetes, Diabetes Care. 1998

13

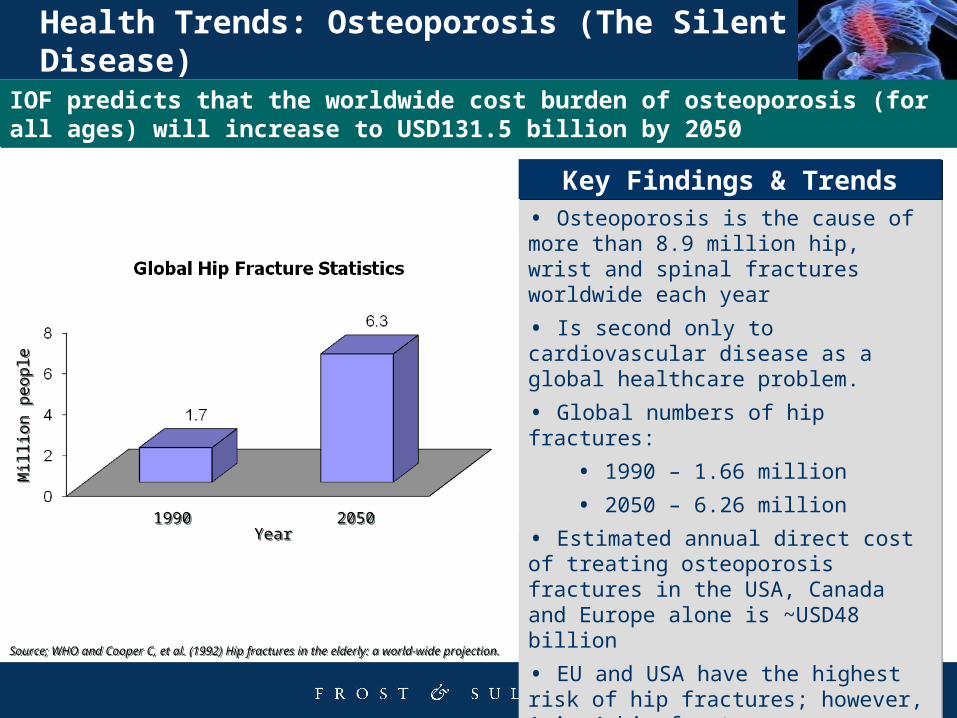

• Osteoporosis is the cause of more than 8.9 million hip, wrist and spinal fractures worldwide each year

• Is second only to cardiovascular disease as a global healthcare problem.

• Global numbers of hip fractures:

• 1990 – 1.66 million

• 2050 – 6.26 million

• Estimated annual direct cost of treating osteoporosis fractures in the USA, Canada and Europe alone is ~USD48 billion

• EU and USA have the highest risk of hip fractures; however, 1 in 4 hip fractures now occur in Asia and Latin America. This is set to increase to 1 in 2 by 2050

• Osteoporosis is the cause of more than 8.9 million hip, wrist and spinal fractures worldwide each year

• Is second only to cardiovascular disease as a global healthcare problem.

• Global numbers of hip fractures:

• 1990 – 1.66 million

• 2050 – 6.26 million

• Estimated annual direct cost of treating osteoporosis fractures in the USA, Canada and Europe alone is ~USD48 billion

• EU and USA have the highest risk of hip fractures; however, 1 in 4 hip fractures now occur in Asia and Latin America. This is set to increase to 1 in 2 by 2050

Health Trends: Osteoporosis (The Silent Disease)

IOF predicts that the worldwide cost burden of osteoporosis (for all ages) will increase to USD131.5 billion by 2050IOF predicts that the worldwide cost burden of osteoporosis (for all ages) will increase to USD131.5 billion by 2050

Key Findings & TrendsKey Findings & Trends

Source; WHO and Cooper C, et al. (1992) Hip fractures in the elderly: a world-wide projection.Source; WHO and Cooper C, et al. (1992) Hip fractures in the elderly: a world-wide projection.

Mill

ion

pe

op

leM

illio

n p

eo

ple

19901990 20502050YearYear

14

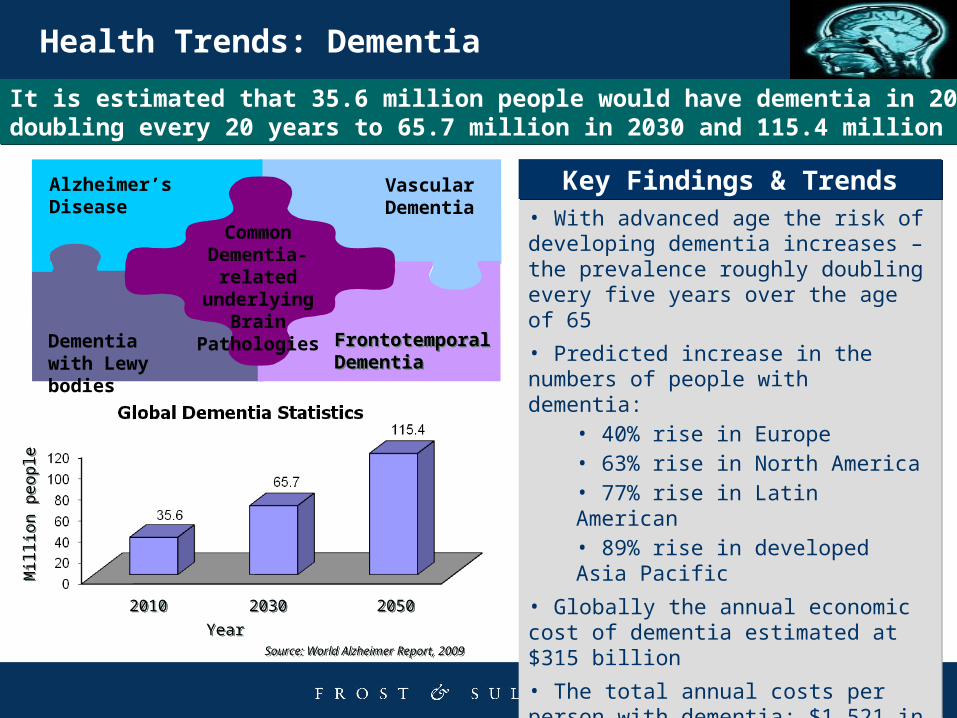

Health Trends: Dementia

• With advanced age the risk of developing dementia increases – the prevalence roughly doubling every five years over the age of 65

• Predicted increase in the numbers of people with dementia:

• 40% rise in Europe• 63% rise in North America• 77% rise in Latin American • 89% rise in developed Asia Pacific

• Globally the annual economic cost of dementia estimated at $315 billion

• The total annual costs per person with dementia; $1,521 in a low income countries and up to $17,964 in high income countries.

• With advanced age the risk of developing dementia increases – the prevalence roughly doubling every five years over the age of 65

• Predicted increase in the numbers of people with dementia:

• 40% rise in Europe• 63% rise in North America• 77% rise in Latin American • 89% rise in developed Asia Pacific

• Globally the annual economic cost of dementia estimated at $315 billion

• The total annual costs per person with dementia; $1,521 in a low income countries and up to $17,964 in high income countries.

Alzheimer’s Disease

Dementia with Lewy bodies

Vascular Dementia

Frontotemporal DementiaFrontotemporal Dementia

CommonDementia-related underlying Brain

Pathologies

It is estimated that 35.6 million people would have dementia in 2010, nearly doubling every 20 years to 65.7 million in 2030 and 115.4 million in 2050. It is estimated that 35.6 million people would have dementia in 2010, nearly doubling every 20 years to 65.7 million in 2030 and 115.4 million in 2050.

Key Findings & TrendsKey Findings & Trends

Source: World Alzheimer Report, 2009Source: World Alzheimer Report, 2009

Mill

ion

pe

op

leM

illio

n p

eo

ple

20102010 20502050

YearYear

20302030

15

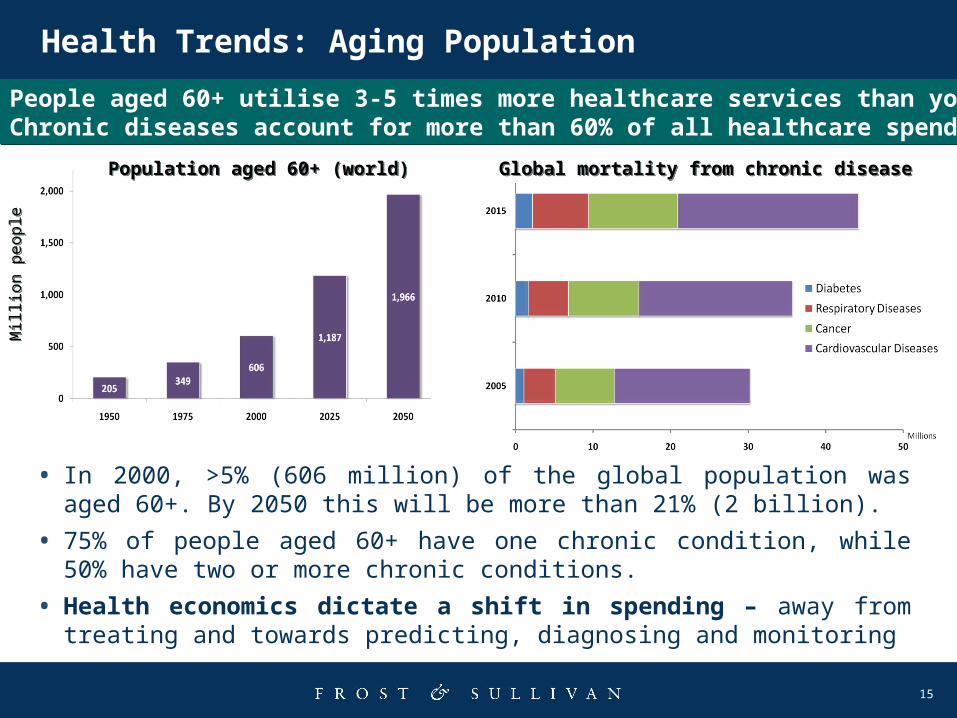

• In 2000, >5% (606 million) of the global population was aged 60+. By 2050 this will be more than 21% (2 billion).

• 75% of people aged 60+ have one chronic condition, while 50% have two or more chronic conditions.

• Health economics dictate a shift in spending – away from treating and towards predicting, diagnosing and monitoring

Health Trends: Aging Population

People aged 60+ utilise 3-5 times more healthcare services than younger peopleChronic diseases account for more than 60% of all healthcare spendingPeople aged 60+ utilise 3-5 times more healthcare services than younger peopleChronic diseases account for more than 60% of all healthcare spending

Mill

ion

pe

op

leM

illio

n p

eo

ple

Population aged 60+ (world)Population aged 60+ (world) Global mortality from chronic diseaseGlobal mortality from chronic disease

16

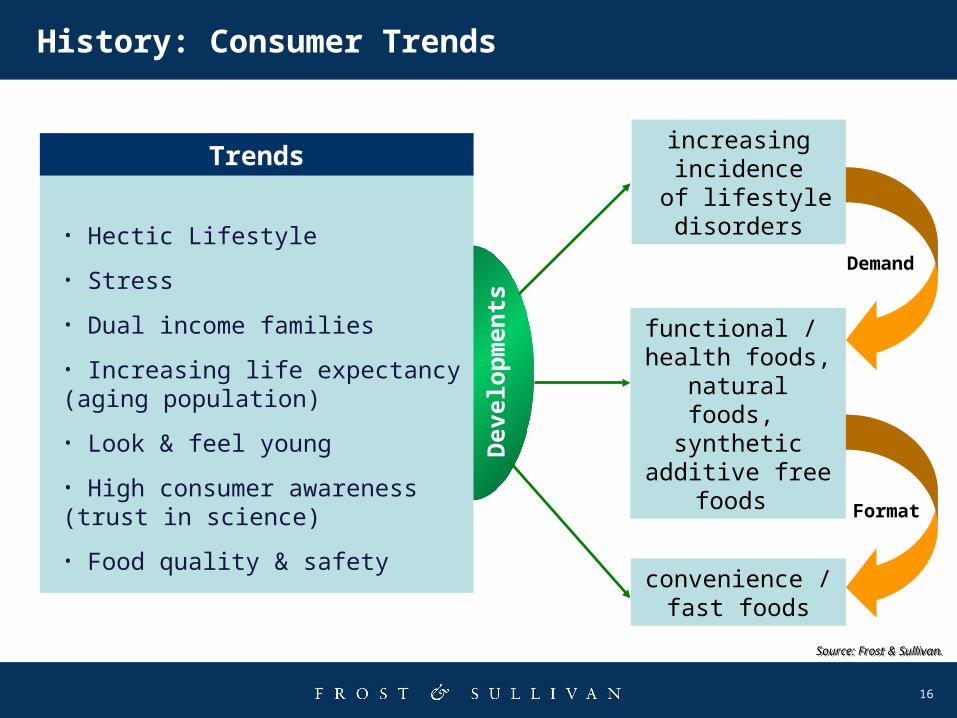

History: Consumer Trends

Source: Frost & Sullivan.Source: Frost & Sullivan.

• Hectic Lifestyle

• Stress

• Dual income families

• Increasing life expectancy (aging population)

• Look & feel young

• High consumer awareness (trust in science)

• Food quality & safetyconvenience /

fast foods

increasing incidence of lifestyle disorders

functional / health foods,

natural foods, synthetic additive

free foods Dev

elo

pm

ents

Trends

Demand

Format

17

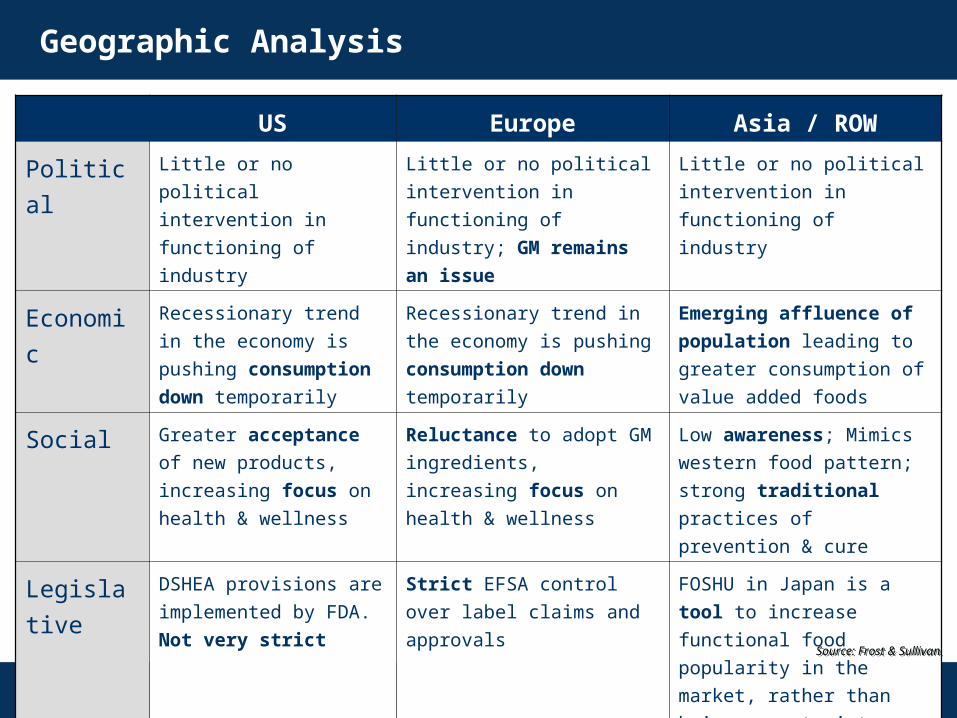

Geographic Analysis

US Europe Asia / ROW

Political Little or no political

intervention in

functioning of industry

Little or no political

intervention in functioning

of industry; GM remains

an issue

Little or no political

intervention in functioning

of industry

Economi

c

Recessionary trend in

the economy is pushing

consumption down

temporarily

Recessionary trend in the

economy is pushing

consumption down

temporarily

Emerging affluence of

population leading to

greater consumption of

value added foods

Social Greater acceptance of

new products,

increasing focus on

health & wellness

Reluctance to adopt GM

ingredients, increasing

focus on health &

wellness

Low awareness; Mimics

western food pattern;

strong traditional

practices of prevention &

cure

Legislativ

e

DSHEA provisions are

implemented by FDA.

Not very strict

Strict EFSA control over

label claims and approvals

FOSHU in Japan is a tool

to increase functional food

popularity in the market,

rather than being a

restraint.Source: Frost & Sullivan.Source: Frost & Sullivan.

18

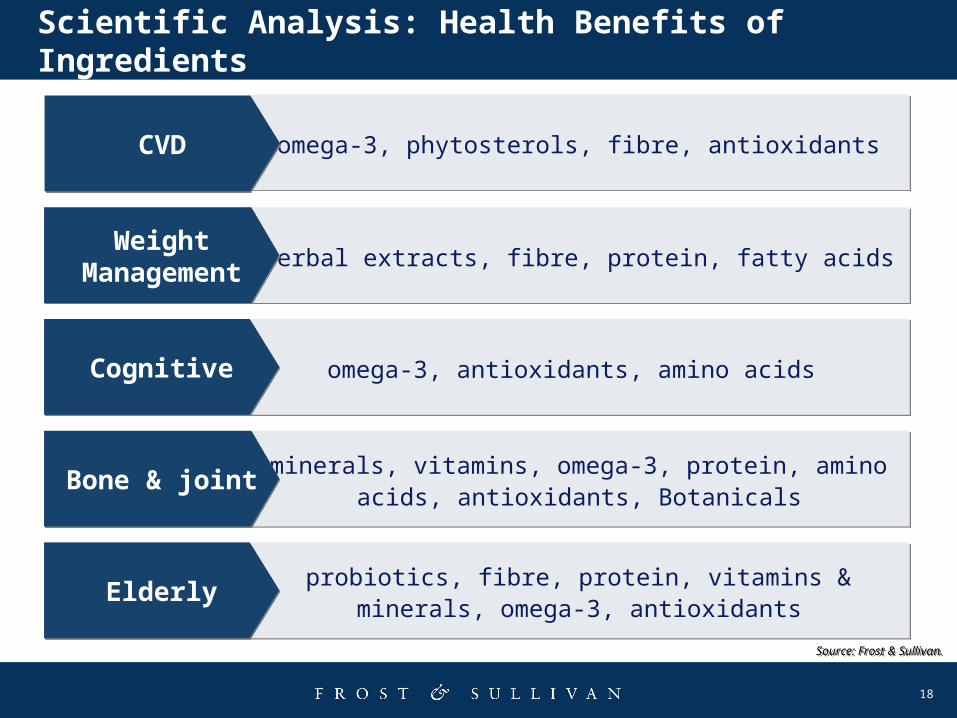

omega-3, phytosterols, fibre, antioxidantsomega-3, phytosterols, fibre, antioxidants

herbal extracts, fibre, protein, fatty acidsherbal extracts, fibre, protein, fatty acids

omega-3, antioxidants, amino acids omega-3, antioxidants, amino acids

CVDCVD

Weight Management

Weight Management

CognitiveCognitive

Scientific Analysis: Health Benefits of Ingredients

probiotics, fibre, protein, vitamins & minerals, omega-3, antioxidants

probiotics, fibre, protein, vitamins & minerals, omega-3, antioxidants

ElderlyElderly

minerals, vitamins, omega-3, protein, amino acids, antioxidants, Botanicals

minerals, vitamins, omega-3, protein, amino acids, antioxidants, Botanicals

Bone & jointBone & joint

Source: Frost & Sullivan.Source: Frost & Sullivan.

19

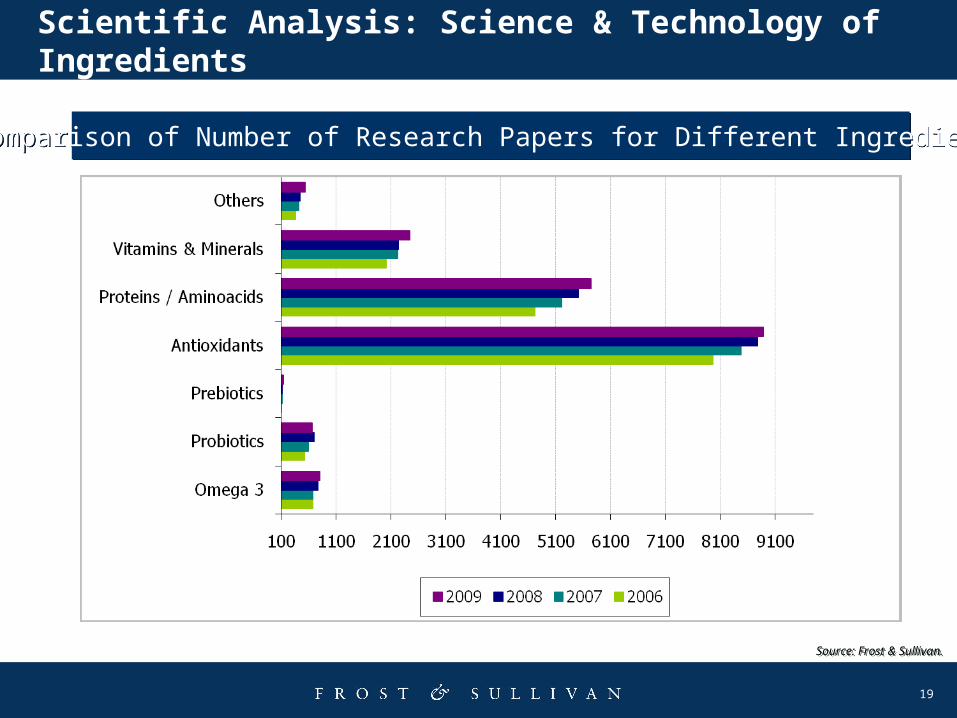

Scientific Analysis: Science & Technology of Ingredients

Comparison of Number of Research Papers for Different IngredientsComparison of Number of Research Papers for Different Ingredients

Source: Frost & Sullivan.Source: Frost & Sullivan.

20

Scientific Analysis: Ingredient Profile

Ingredients Omega 3Probiotic

sFibre /

PrebioticsAntioxidant

s

Proteins / Amino acids

Vitamins &

MineralsBotanical

s

Ranking on a Scale of 1- 10

6.9 6.4 5.6 6.8 7.0 7.1 6.4

Future Nutraceutical Ingredients RankingFuture Nutraceutical Ingredients Ranking

1. Research Profile 6. New Product Introduction

2. Health Claim - Regulatory 7. Consumer Marketing

3. Health Positioning 8. Current Market Size

4. Application Profile 9. Sustainability

5. Consumer Awareness 10. Market Growth rate

Top 10 Parameters Used to Assess Future Nutraceutical Ingredients Top 10 Parameters Used to Assess Future Nutraceutical Ingredients

Source: Frost & Sullivan.Source: Frost & Sullivan.

21

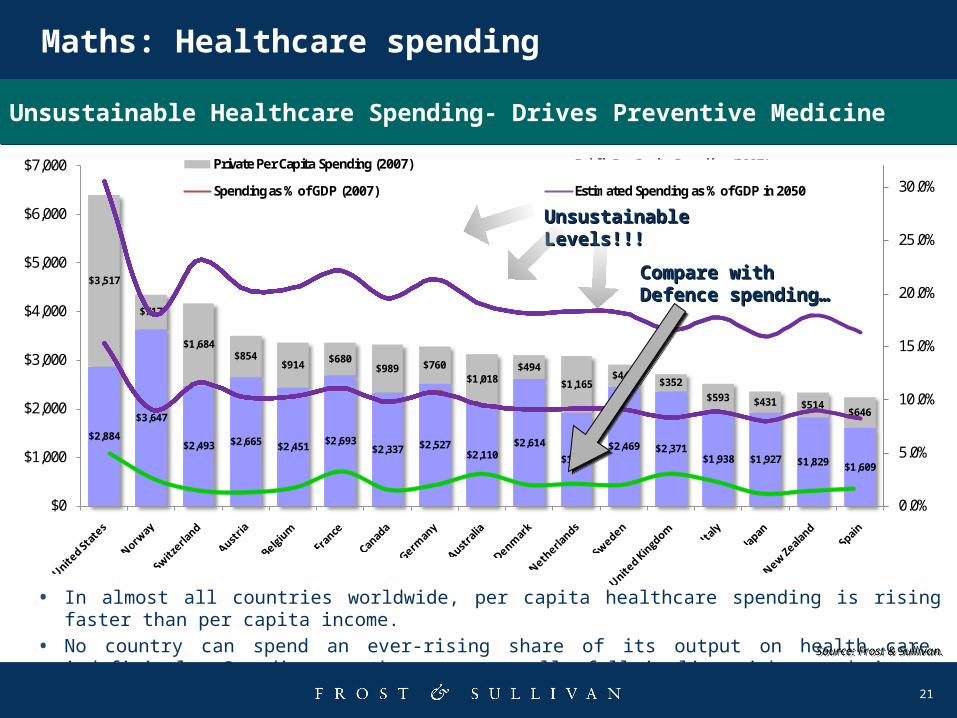

• In almost all countries worldwide, per capita healthcare spending is rising faster than per capita income.

• No country can spend an ever-rising share of its output on health care, indefinitely. Spending growth must eventually fall in line with growth in per capita income.

$2,884

$3,647

$2,493 $2,665 $2,451 $2,693$2,337 $2,527

$2,110$2,614

$1,927$2,469 $2,371

$1,938 $1,927 $1,829 $1,609

$3,517

$717

$1,684$854

$914 $680$989 $760

$1,018$494

$1,165$449

$352$593 $431 $514

$646

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$2,884

$3,647

$2,493 $2,665 $2,451 $2,693$2,337 $2,527

$2,110$2,614

$1,927$2,469 $2,371

$1,938 $1,927 $1,829 $1,609

$3,517

$717

$1,684$854

$914 $680$989 $760

$1,018$494

$1,165$449

$352$593 $431 $514

$646

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

Private Per Capita Spending (2007) Public Per Capita Spending (2007)

Spending as % of GDP (2007) Estimated Spending as % of GDP in 2050

$1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009 $1,009

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

Unsustainable Unsustainable Levels!!!Levels!!!

Compare with Compare with Defence spending…Defence spending…

Maths: Healthcare spending

Unsustainable Healthcare Spending- Drives Preventive Medicine Unsustainable Healthcare Spending- Drives Preventive Medicine

Source: Frost & Sullivan.Source: Frost & Sullivan.

22

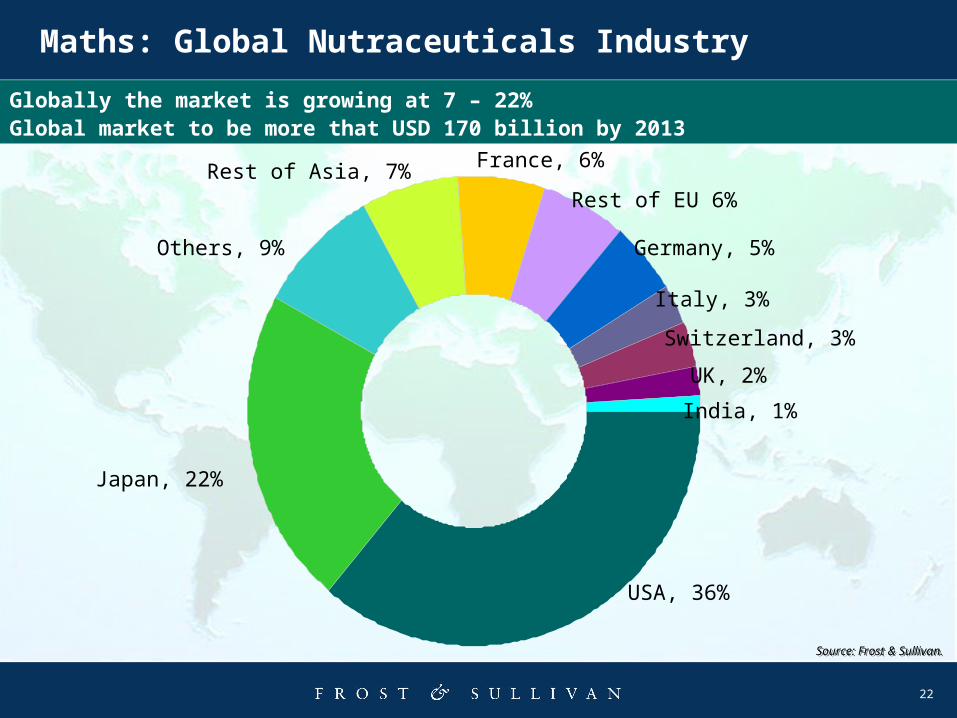

Maths: Global Nutraceuticals Industry

USA, 36%

Japan, 22%

Others, 9%

Rest of Asia, 7% France, 6%

Italy, 3%

Rest of EU 6%

Germany, 5%

Switzerland, 3%

UK, 2%

India, 1%

Globally the market is growing at 7 – 22% Global market to be more that USD 170 billion by 2013

Source: Frost & Sullivan.Source: Frost & Sullivan.

23

Nutraceuticals – Top 5 Functional Ingredients

24

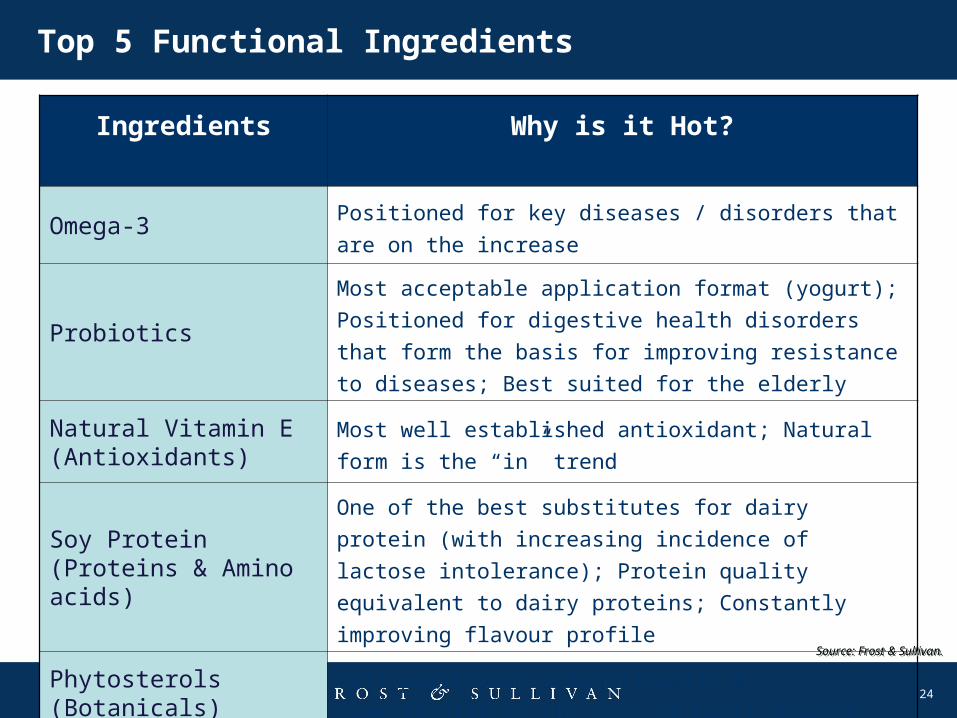

Top 5 Functional Ingredients

Ingredients Why is it Hot?

Omega-3 Positioned for key diseases / disorders that are on

the increase

Probiotics

Most acceptable application format (yogurt);

Positioned for digestive health disorders that form

the basis for improving resistance to diseases; Best

suited for the elderly

Natural Vitamin E (Antioxidants)

Most well established antioxidant; Natural form is the

“in” trend

Soy Protein (Proteins & Amino acids)

One of the best substitutes for dairy protein (with

increasing incidence of lactose intolerance); Protein

quality equivalent to dairy proteins; Constantly

improving flavour profile

Phytosterols (Botanicals)

Well positioned scientifically & commercially in the

area of heart diseaseSource: Frost & Sullivan.Source: Frost & Sullivan.

25

Top 5 Functional Ingredients: Omega-3 Ingredients

• Well-positioned for cognitive & heart health

• New research areas include immune & bone & joint health

• Most important challenge is the flavour profile that decelerates penetration into

many food applications

•Marine Oil Key Players: Pronova BioPharma ASA, EPAX AS, ONC; Algal Oil Key Player:

Martek & Lonza

• Sources under development include: flax, soy

Revenue: $323.0 Million(CAGR – 10.2%)

Volume Market Share by Application, (2009)

Volume Market Share by Application, (2009)

Source: Frost & Sullivan.Source: Frost & Sullivan.

26

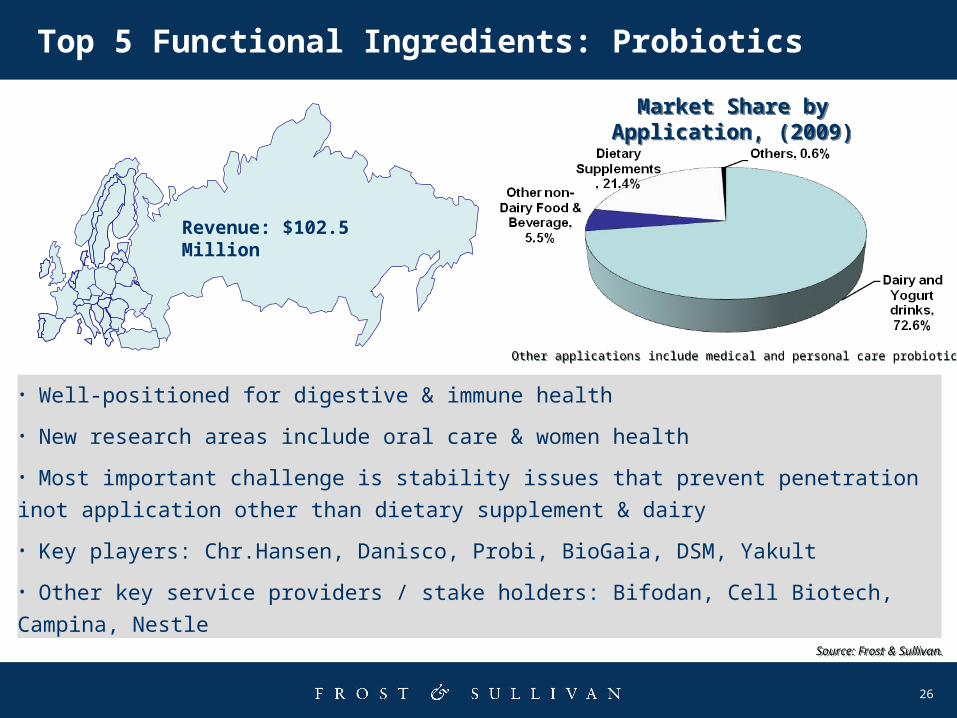

Top 5 Functional Ingredients: Probiotics

• Well-positioned for digestive & immune health

• New research areas include oral care & women health

• Most important challenge is stability issues that prevent penetration inot

application other than dietary supplement & dairy

• Key players: Chr.Hansen, Danisco, Probi, BioGaia, DSM, Yakult

• Other key service providers / stake holders: Bifodan, Cell Biotech, Campina,

Nestle

Other applications include medical and personal care probioticsOther applications include medical and personal care probiotics

Market Share by Application, (2009)Market Share by

Application, (2009)

Source: Frost & Sullivan.Source: Frost & Sullivan.

Revenue: $102.5 Million

27

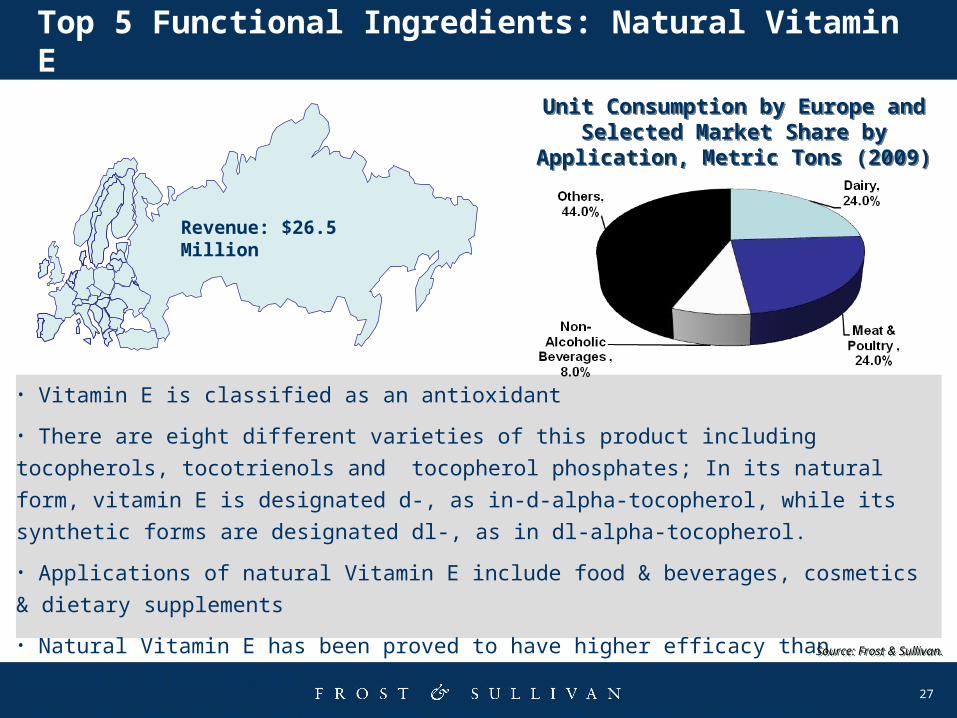

Top 5 Functional Ingredients: Natural Vitamin E

• Vitamin E is classified as an antioxidant

• There are eight different varieties of this product including tocopherols, tocotrienols

and tocopherol phosphates; In its natural form, vitamin E is designated d-, as in-d-

alpha-tocopherol, while its synthetic forms are designated dl-, as in dl-alpha-

tocopherol.

• Applications of natural Vitamin E include food & beverages, cosmetics & dietary

supplements

• Natural Vitamin E has been proved to have higher efficacy than synthetic

alternatives.

• Key players/Stake Holders: DSM, Cognis, ADM, Shenjian Medical

Unit Consumption by Europe and Selected Market Share by

Application, Metric Tons (2009)

Unit Consumption by Europe and Selected Market Share by

Application, Metric Tons (2009)

Source: Frost & Sullivan.Source: Frost & Sullivan.

Revenue: $26.5 Million

28

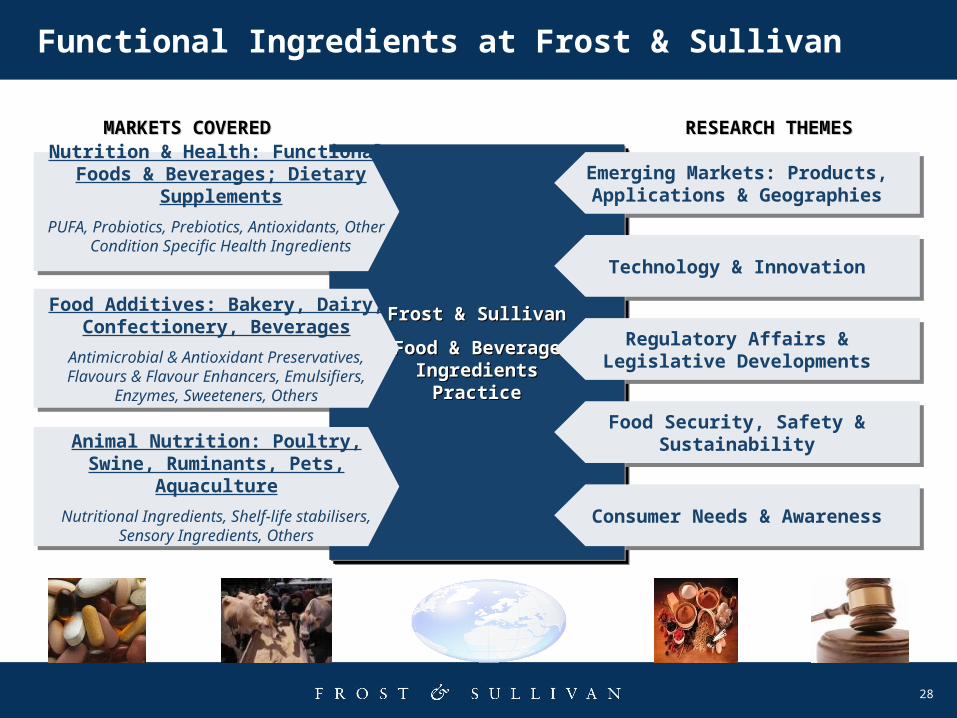

Functional Ingredients at Frost & Sullivan

Frost & SullivanFrost & Sullivan

Food & BeverageFood & BeverageIngredientsIngredients

PracticePractice

Frost & SullivanFrost & Sullivan

Food & BeverageFood & BeverageIngredientsIngredients

PracticePractice

Nutrition & Health: Functional Foods & Beverages; Dietary Supplements

PUFA, Probiotics, Prebiotics, Antioxidants, Other Condition Specific Health Ingredients

Food Additives: Bakery, Dairy, Confectionery, Beverages

Antimicrobial & Antioxidant Preservatives, Flavours & Flavour Enhancers, Emulsifiers,

Enzymes, Sweeteners, Others

Animal Nutrition: Poultry, Swine, Ruminants, Pets, Aquaculture

Nutritional Ingredients, Shelf-life stabilisers, Sensory Ingredients, Others Consumer Needs & Awareness

Technology & Innovation

Emerging Markets: Products, Applications & Geographies

MARKETS COVEREDMARKETS COVERED RESEARCH THEMESRESEARCH THEMES

Regulatory Affairs & Legislative Developments

Food Security, Safety & Sustainability

29

Where the future lies: Growth and Opportunities

Histor

y

Geograph

y

Science

Maths

+ =

Source: Frost & Sullivan.Source: Frost & Sullivan.

30

Frost & Sullivan - Information

31

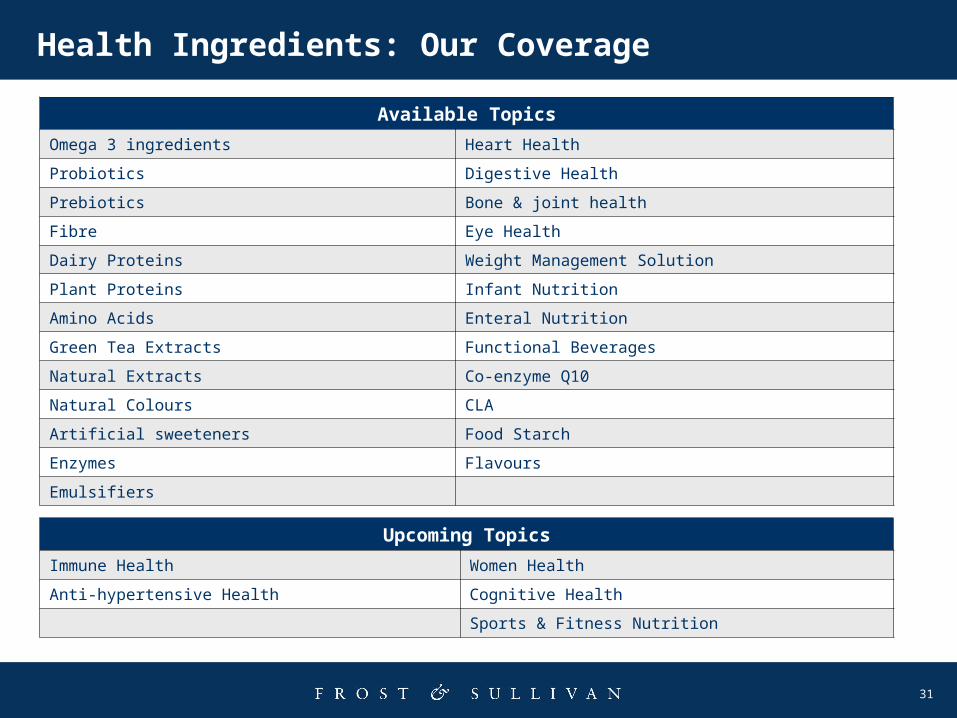

Health Ingredients: Our Coverage

Available Topics

Omega 3 ingredients Heart Health

Probiotics Digestive Health

Prebiotics Bone & joint health

Fibre Eye Health

Dairy Proteins Weight Management Solution

Plant Proteins Infant Nutrition

Amino Acids Enteral Nutrition

Green Tea Extracts Functional Beverages

Natural Extracts Co-enzyme Q10

Natural Colours CLA

Artificial sweeteners Food Starch

Enzymes Flavours

Emulsifiers

Upcoming Topics

Immune Health Women Health

Anti-hypertensive Health Cognitive Health

Sports & Fitness Nutrition

32

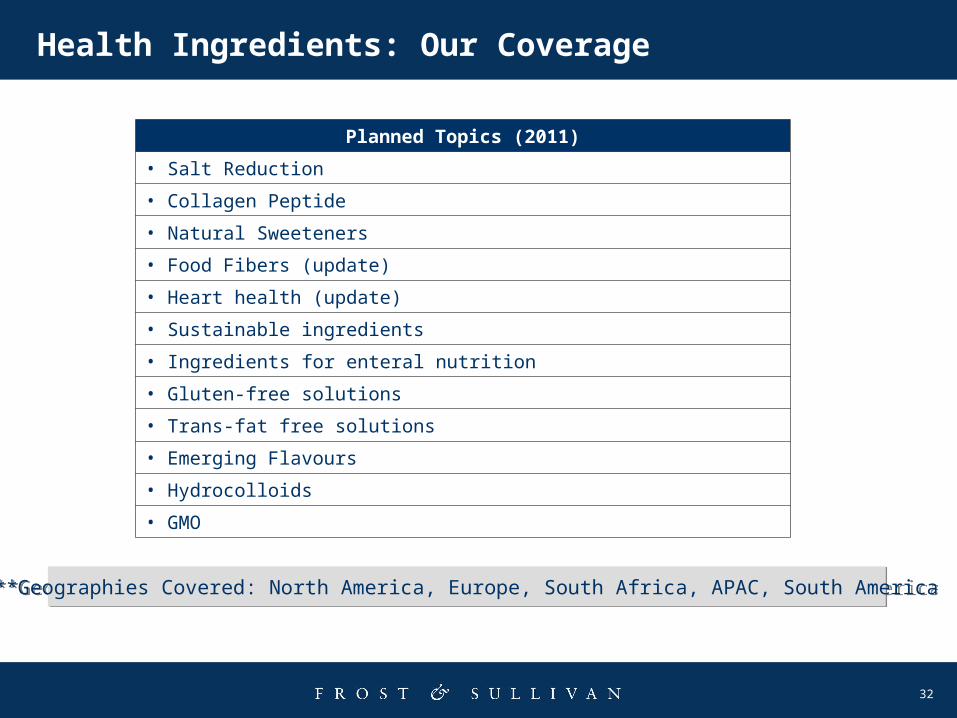

Health Ingredients: Our Coverage

Planned Topics (2011)

• Salt Reduction

• Collagen Peptide

• Natural Sweeteners

• Food Fibers (update)

• Heart health (update)

• Sustainable ingredients

• Ingredients for enteral nutrition

• Gluten-free solutions

• Trans-fat free solutions

• Emerging Flavours

• Hydrocolloids

• GMO

**Geographies Covered: North America, Europe, South Africa, APAC, South America**Geographies Covered: North America, Europe, South Africa, APAC, South America

33

What Makes Us Unique

Exclusively Focused on Growth

Global thought leader exclusively focused on addressing client growth strategies and plans – Team actively engaged in researching and developing of growth models that enable clients to achieve aggressive growth objectives.

Industry Breadth

Cover the broad spectrum of industries and technologies to provide clients with the ability to look outside the box and discover new and innovative ideas.

Global Perspective

32 global offices ensure that clients receive a global coverage/perspective based on regional expertise.

360o Perspective

Proprietary T.E.A.M.TM

Methodology integrates all 6 critical research methodologies to significantly enhance the accuracy of decision making and lower the risk of implementing growth strategies.

Growth Monitoring

Continuously monitor changing technology, markets and economics and proactively address clients growth initiatives and position.

Trusted Partner

Working closely with client Growth Teams – helping them generate new growth initiatives and leverage all of Frost & Sullivan assets to accelerate their growth.

34

T.E.A.M. Methodology

Frost & Sullivan’s proprietary T.E.A.M. methodology, ensures that clients have complete “360 Degree

Perspective” from which to drive decision-making. Technical, Econometric, Application, and Market

information ensures that clients have a comprehensive view of industries, markets and technology.

Technical Real-time intelligence on technology, including emerging technologies, new

R&D breakthroughs, technology forecasting, impact analysis, groundbreaking

research, and licensing opportunities.

Econometric In-depth qualitative and quantitative research focused on timely and critical

global, regional, and country specific trends, including the political,

demographic, and socioeconomic landscapes.

Application Insightful strategies, networking opportunities, and best practices that can be

applied for enhanced market growth; interactions between the client, peers, and

Frost & Sullivan representatives that result in added value and effectiveness.

Market Global and regional market analysis, including drivers and restraints, market

trends, regulatory changes, competitive insights, growth forecasts, industry

challenges, strategic recommendations, and end-user perspectives.

35

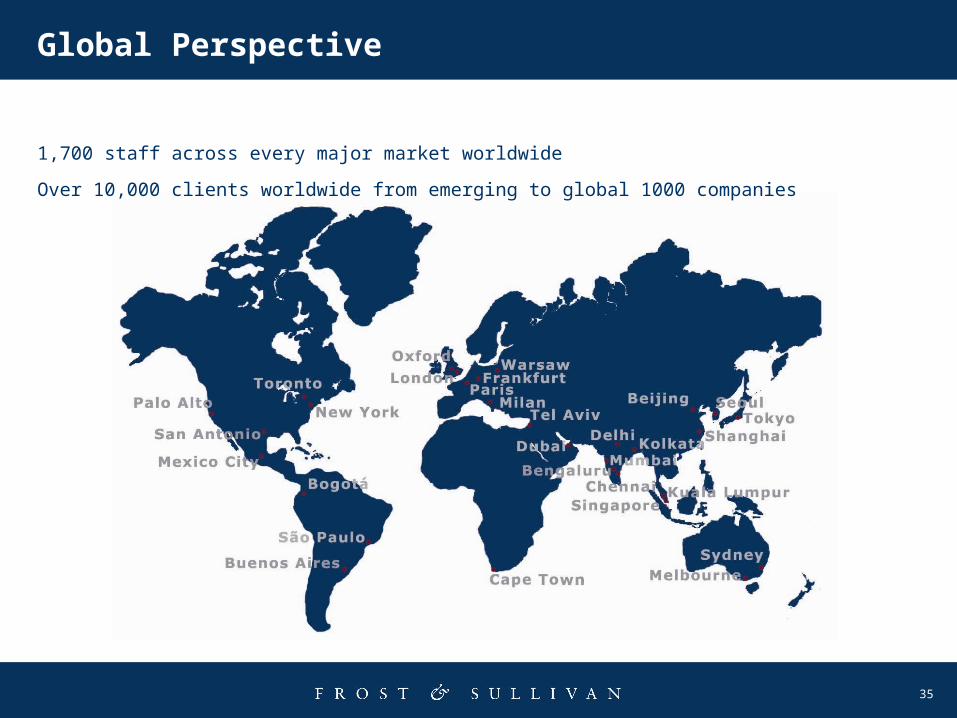

Global Perspective

1,700 staff across every major market worldwide

Over 10,000 clients worldwide from emerging to global 1000 companies