Full year results analyst and investor presentation

51

Full year results analyst and investor presentation Tuesday 17 November 2015

Transcript of Full year results analyst and investor presentation

Full year results analyst and investor

presentation

Tuesday 17 November 2015

Introduction

Carolyn McCall

Chief Executive Officer

3 3

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet strategy delivers record results

Profit before tax has increased for the fifth consecutive year

Passengers + 6.0% 69 million

Revenue + 3.5% £4,686m

Profit before tax + 18.1% £686m

PBT margin +1.8ppts 14.6%

EPS + 21.5% 139.1p

Operating cash flow + 12.9% £895m

DPS + 21.6% 55.2p

ROCE + 1.7ppt 22.2%

TSR +28%

3

Financial review

Andrew Findlay

Chief Financial Officer

5 5

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Strong financial performance

5

FY 2015

£ m

FY 2014

£ m

Change

%

Change

% @ CC

Total revenue 4,686 4,527 3.5% 6.5%

Fuel (1,199) (1,251) 4.2% 4.6%

Costs excluding fuel (2,801) (2,695) (3.9%) (8.7%)

Profit before tax 686 581 18.1% 20.2%

Profit before tax margin 14.6% 12.8% 1.8ppt

EBITDAR 940 823 14.1% 16.7%

EBITDAR margin 20.0% 18.2% 1.8ppt

Earnings per share 139.1 114.5 21.5%

Dividend per share 55.2 45.4 21.6%

Return on capital employed 22.2% 20.5% 1.7ppt

6 6

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Profit before tax increased 18%

Profit/(loss) bridge

6

686

12

159

52

600

800

750

700

650

0 FY 2014

698

581

Fuel FY 2015 Other Costs Revenue

(68)

(38)

Crew resilience,

de-icing and disruption

FY 2015 @ CC

686

Fx

7 7

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Revenue performance

7

4.9%

1.5%

7.0%

3.2% 4.7%

-2.8%

4.3%

1.4% 2.9%

3.7%

easyJet capacity growth

RPS growth at constant currency

Q1 Q2 Q3 Q4 FY

£m FY 2015 FY 2014 Change

Passengers (m) 68.6 64.8 6.0%

Load factor (%) 91.5% 90.6% +0.9ppt

Seats flown (m) 75.0 71.5 4.9%

Average sector length (km) 1,118 1,112 0.5%

Total revenue - reported (£m) 4,686 4,527 3.5%

Total revenue - constant currency (£m) 4,821 4,527 6.5%

Total revenue per seat - reported (£) 62.48 63.31 (1.3%)

Total revenue per seat - constant currency (£) 64.28 63.31 1.5%

8 8

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

A strong focus on costs

Total cost per seat bridge

0.360.160.12

0.120.250.58

0.130.43

0.38

Fuel

1.53

De-icing and disruption

Regulated airports inflation

FY 2014 FY 2014 engine deal

Net other cost savings

56.50

1.64

Eurocontrol settlement

Before movement in fuel and

FX

56.71

FX A320 mix

53.33

FY 2015 Crew resilience

Load factor

55.19

Before management

action

Other inflation

Management action

External factors

8

• Cost per seat ex-fuel: -0.9%

• Cost per seat ex-fuel @ constant currency: +3.6%

9 9

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Impact of fuel & currency

9

FY 2015 fuel impact favourable / (adverse) FY 2015 FY 2014

Fuel $ per metric tonne

Market rate 619 973

Effective price 872 977

US dollar rate

Market rate 1.54 1.66

Effective price 1.58 1.59

Actual cost of fuel £ per metric tonne 553 614

FY 2015 currency impact favourable / (adverse) EUR CHF USD Other Total

£m

Revenue (131) (1) 4 (7) (135)

Fuel 0 0 (6) 0 (6)

Costs excluding fuel 127 (3) 5 0 129

Total (4) (4) 3 (7) (12)

(1 cent)

61

Change B/(W)

354

105

(12 cents)

10 10

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Strong cash generation underpins dividend policy and fleet growth

10

16621

92

536

9850

138

688

Net cash Sep 2015

435*

Dividend paid

180

FX Other

615

Net cash before

dividend

Restricted cash

Own shares

CAPEX Tax Net working capital

Depn & amort

Operating profit

Net cash Sep 2014

422*

*Includes money market deposits but excludes restricted cash

11 11

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Strong balance sheet

* Other liabilities (excluding debt) includes unearned revenue of £619m (FY 2014 : £572m) .

** Gearing is defined as (debt + 7 x annual lease payments – cash) divided by (shareholders’ equity + debt + 7 x annual lease payments – cash)

11

£m FY 2015 FY 2014

Goodwill and other intangible assets 492 478

Property, plant and equipment 2,877 2,542

Derivative fiancial instruments (297) (21)

Other assets 348 388

Other liabilities (excluding debt) * (1,606) (1,637)

Capital employed 1,814 1,750

Cash and money market deposits 939 985

Debt (504) (563)

Net cash 435 422

Net assets 2,249 2,172

Gearing ** 14% 17%

12 12

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Future capital investment

FY15 FY16 FY17 FY18 2019-2022

Additional aircraft 55% 58% 73% 53% 37%

Replacement aircraft

18% 14% 4% 29% 43%

Maintenance 27% 28% 23% 18% 20%

Total 100% 100% 100% 100% 100%

Total expected fleet acquisition and overhaul expenditure as a % of easyJet revenue

11% 11% 13% 17% 12%

Fleet acquisition and overhauls will be funded through a combination of debt, easyJet’s strong cash flow and sale and leaseback transactions

2015, based on actual revenue for the 2015 Financial Year Future years based on estimated revenue

12

13 13

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Debt repayment profile

13

Total debt: £504 million

0

50

100

150

200

FY20 FY21

£54m

£74m

£46m

FY16 FY18

£60m

FY17

£182m

£88m

FY19

14 14

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Outlook

Capacity (seats flown)

• H1 c.+8.0% (before disruption )

• FY c.+7% (before disruption)

Revenue per seat (constant currency)

• H1: Slight decline (assuming normal levels of disruption and constant load factors)

Cost per seat including Fuel (constant currency)

• FY c.-1% (assuming normal levels of disruption and constant load factors)

Cost per seat ex fuel (constant currency)

• FY c.+2% (assuming normal levels of disruption and constant load factors)

• Weighted towards first half

FX

• H1: c.£15 million adverse movement from foreign exchange rates

• FY: c.£40 million adverse movement from foreign exchange rates

Fuel

• H1: unit fuel costs £75 million to £85 million favourable

• FY: unit fuel costs £140 million to £160 million favourable

Rates at 13 November 2015 £/USD: 1.522; £/EUR: 1.4106 Unit fuel guidance based on Jet fuel trading range of $450 / metric tonne to $550 / metric tonne

14

15 15

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Initial thoughts and areas of focus

15

Initial Thoughts:

• Great people with passion and commitment to the business

• An enviable customer proposition

• A strategy that continues to deliver sustainable shareholder returns

• Significant opportunities for growth

Areas of focus for me:

• Reinforce our cost focus

• Review of capital structure to balance risk and efficiency whilst maximising returns

Business Review

Carolyn McCall

Chief Executive Officer

17 17

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Continuing to win

• easyJet has delivered another record performance in 2015

• Delivering through the cycle – favourable trends will support strong demand for easyJet

• Future growth and returns drivers

• Network offers significant opportunity

• Best customer proposition and sector-leading digital offering

• Operational excellence to deliver stable margins

• Capital discipline and strong financial footing

• Delivering sustainable shareholder returns

17

18 18

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Favourable economic trends

Source: IMF, Euromonitor, Capital IQ, Bloomberg as at 07-Oct-2015

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

2.5

2000A 2002A 2004A 2006A 2008A 2010A 2012A 2014A 2016E

Co

nsu

me

r C

on

fid

en

ce

In

de

x, s

tan

da

rdis

ed

UK France Spain

Italy Switzerland Germany

Positive outlook across key markets Recovery in consumer confidence

2.7

1.2

2.5

0.5

0.8

1.6

2.3

1.5

2.0

1.1 1.2

1.7

2.2

1.7 1.8

1.1

1.5 1.5

UK France Spain Italy Switzerland Germany

Re

al G

DP

Gro

wth

Yo

Y (

%)

2015 2016 2017

Business model outperforms through the cycle

18

19 19

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

2015 – outperformance in a competitive market

Market capacity increase/(decrease)

easyJet

Sector RASK growth

FY15 easyJet constant currency RASK vs median Sector RASK, year on year change

19

Market capacity growth (%) % rev. change

Note: RASK at constant currency. Sector median RASK includes IAG, LHA, AF-KLM, Ryanair & Norwegian. Note that Ryanair and Norwegian do not report constant currency, therefore reported data used

-0.8

-6

-4

-2

0

2

4

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Q4

2.4

-1.9

Q3

-3.9 -4.8

Q2

1.8

Q1

3.7

-0.7

20 20

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Exciting initiatives underway

20

Embedded (with more to chase)

Launch in FY2016 Launch in FY2017

Revenue - Business passenger - Base openings (Amsterdam,

Naples)

- Base in Venice - New leading edge website - New call centre online - Flight Club launch

- New base openings - Continue RMS and Network

optimisation development

Cost

- AJW maintenance agreement

- Gatwick long term deal - CFM engine deal

- New crew portal - New components supplier - New maintenance hanger - Gatwick consolidation - ADP passenger charges - 1st 186 seat A320

- 1st A320 NEO delivered

Both - Oporto base opening - Mobile platform

- Rome base closure - Barcelona base opening

- Begin retrofit of extra 6 seats - Leading edge commercial

platform

- Based on easyJet financial year, October to September

21 21

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet operates in the right airports and markets

1) Catchment areas defined as population living within 50km of airports within the market and ranked according to GDP for that area; 2) Rank of short haul capacity for the 12 months to September 2015; 3) Manchester catchment includes Liverpool airport; 4) Dusseldorf catchment includes Cologne, Dortmund, Friedrichshafen, Nuremburg and Paderborn; 5) Zurich catchment includes Basel

21

easyJet network

- Number 1 or 2 position in the primary airport in 12 of Europe’s top 25 catchment areas by GDP1

Best Network

22 22

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

LGW GVA MXP LTN SXF CDG AMS BSL BFS BRS

2011 easyJet Capacity 2015 easyJet Capacity

No 1 European network

easyJet No.1

easyJet No.2

Other

% of easyJet capacity currently holding a No.1 , No.2 or other market share position

Airport

Market Share1

Based aircraft

Touching aircraft

LGW 48% 61 61

GVA 40% 14 23

MXP 47% 18 22

LTN 41% 18 18

SXF 58% 9 15

CDG 11% 9 14

AMS 11% 3 14

BSL 54% 9 13

BFS 84% 5 13

EDI 28% 7 11

Positions built over time

No.1 & 2 positions drive returns

easyJet has grown capacity by over 7m seats with a CAGR of c.5% at our top 10 airports over the past 5 years

Strong share at key airports

22

Best Network

+38%

+34% +14%

+16% +23% +4% +32% +68%

+23% +10%

Se

ats

% growth in seats 2011-15

1. easyJet capacity as a % of total short haul capacity at airport

Source: OAG

23 23

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Profitably growing our network

23

easyJet capacity growth

Market capacity growth ROCE

2013 3.3% 1.3% 17.4%

2014 5.1% 4.3% 20.5%

2015 4.9% 5.4% 22.2% Re

turn

s

Routes

CPBH FY13 CPBH FY14 CPBH FY15

12% ROCE

Improving returns in all market conditions

Best Network

24 24

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Progression of returns with increased share over time (base illustration)

Profitably deepening our network

Increasing share drives higher returns1 Adding frequency increases contribution2

Increasing share and frequencies delivers higher returns

24

Best Network

1. Based on performance of 2 easyJet bases through 2015 2. Based on the performance of 2 easyjet routes

-

1,000

2,000

3,000

4,000

5,000

2011 2012 2013 2014 2015

Seat

s [M

illio

ns]

CP

BH

[£

/BH

]

Seats (right axis) CPBH

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2011 2012 2013 2014 2015

Seat

s [M

illio

ns]

CP

BH

[£

/BH

]

Route A

Route B

CP

BH

(£

/BH

)

Market share (%)

2011

2012

2013

2014

2015

25 25

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

We make rational capital allocation decisions

easyJet disciplined allocation of capital delivers higher returns

• 8 Madrid-based aircraft were moved to other bases

• Delivered an incremental network contribution of c.£25m

• We expect a similar outcome from reallocating the aircraft based in Rome FCO

25

8

Madrid Rome

MXP

NAP

Best Network

26 26

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

0

50

100

150

200

250

300

350

400

FY20 easyJet

opportunity

Growth opps

Minimum easyJet

fleet

easyJet case FY20

Maximum easyJet

fleet

Invest in existing network

Natural market growth

Route churn

Current easyJet

fleet

2

3

Much more to go for

50-80

35-50 331-396

25-35 10-20

3

241 227

346

Number of aircraft

- Thickening routes - Join the dots

- New bases - New network points - New routes

- As at 30 September 2015

- Forecast passenger growth on easyJet current markets

335

- Expected churn FY15 – FY20

Range of easyJet FY20 fleet size

26

Significant number of low risk opportunities to pursue

Market share

easyJet share

Other airlines (opportunities to grow)

UK

France

Switzerland

Italy

Germany

Netherlands

Portugal

20%

14%

23%

12%

4%

9%

13%

80%

86%

77%

88%

96%

91%

87%

Best Network

27 27

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Utilising flexibility to take market opportunities

27

241

257

280

303

333

346

359 358

312 335

346 347

239

212 227 221

233

294

304 304 311 311

205

230

255

280

305

330

355

2015 2016 2017 2018 2019 2020 2021 2022

Contracted Max

Base Case

Contracted Min

Previous Base Case

Extra aircraft allows for greater flexibility in fleet planning

4.9% 7.1% 8.7% 7.9% 6.3% 7.9% 6.0% 2.5%

4.9% 7.1% 8.7% 7.5% 5.3% 3.1% 2.1% 2.4%

New base case seat capacity

Old base case seat capacity

Best Network

28 28

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

65

78 74

77 79

86 83

72

82 79

88 87

92 90

68

75 78 79

84 83

88

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014

16-24 25-34 35-44 All

Favourable easyJet customer trends

Source: BLS, Association of National Advertisers, Barkley, SMG, BCG, Yupe, IPG Media Labs, ONS

Purchased Something on the Internet the last 12 Months, UK

Increasing propensity to spend Customers spending more time online

£0

£50

£100

£150

£200

£250

£300

£0

£5,000

£10,000

£15,000

£20,000

£25,000

18 23 28 33 38 43 48 53 58 63 68 73

Avera

ge b

ookin

g v

alu

e

% C

onsu

mer

Ave s

pend b

y a

ge

Consumer Ave spend

easyJet Ave booking value

eas

yjet

Ave

booki

ng

ag

e 2

010

eas

yjet

Ave

booki

ng

ag

e 2

015

easyJet customers have higher propensity to spend

28

Customer proposition

29 29

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Digital Leadership

Best Airline in Mobile

Global Recognition

Best Passenger Assistance

Initiative

Best Mobile Travel & Tourism Winner

Over 500m visits

across platforms in FY15

CRM increases customer value

Value of Mobile YOY Mobile

Revenue

83%

Customers in CRM are of increasing value to easyJet

32%

Innovation in direct

marketing

29

Customer proposition

easyJet Mobile app

14.3m Downloads to date

New website launch in 2016

30 30

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Strengthening our customer relationships

% seats booked by returning customers

Source: Millward Brown brand tracker FY15 vs FY13) Source: easyJet customer database

Brand consideration

Value perceptions 68% 69%

70% 72%

73% 74%

50%

55%

60%

65%

70%

75%

80%

10 11 12 13 14

% f

rom

Re

turn

ing

cu

sto

me

rs

Nu

mb

er

of

sea

ts

New Existing % Existing

30

Growth coming from valuable repeat customers

Customer proposition

30

15

31 31

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Rewarding our loyal customers

31

Customer proposition

FLIGHT CLUB

• Aim to recognise and retain our high frequency and loyal customers

• Simple and low cost to administer

• Will continue to encourage customer loyalty

• Hundreds of thousands of passengers to be part of flight club

32 32

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Business opportunity continuing to develop

32

Increase in business passengers of 25% over next 3 years

TMC GDS sales grew 32% YOY

Business fares grew at 58% YOY

Average 38% Saving on top

Business Routes

Increased focus on FTSE/CAC

& DAX companies

Award winning Business Program

Business Sense Marketing Campaign

Customer proposition

33 33

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Leisure leadership

• Launched almost 60 new leisure routes in 2016

• easyJet holidays revenue per seat increased by 144% in summer 2015

• easyJet has launched around 60 new leisure routes in the 2016 schedule.

33

Customer proposition

34 34

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

1. At the end of the relevant Financial Year 2. Based on fleet plan – base case 3. Maximum fleet does not include the purchase rights

34

61% 52%

47% 39%

32% 29% 28% 28%

39% 44%

19%

3%

33%

53%

51% 47% 46% 45%

8% 18%

24% 26% 26%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22

A319 A320 A320 '186 A320 NEO

Mix

of

fle

et

(%)

71% A320’s

Fleet up-gauging Up-gauging delivering CPS savings

easyJet fleet mix

156 sets 186 seats

Current generation

A319

New generation A320neo

13% -14%

Cost £110m opportunity from up-gauging by 2021

35 35

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet lean – c. £50 million savings in 2016

Short term <1yrs

Medium term 2 – 4 yrs

Long term 4yrs>

Increased pipeline of initiatives

Size of savings per annum

(larger circle means bigger saving opportunity)

Cost

35

• easyJet lean continues to deliver and develop significant cost reductions across

• Maintenance : AJ Walters

• Airports/Handling: deals, automation, structure of charges

• Navigation - SESAR

• Process and efficiency savings enabled by Technology

• Productivity savings enabled by scale in our bases

36 36

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

36

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

1. Network remains robust

2. Gatwick improving

3. Opportunity for step change in operational excellence at Gatwick airport

easyJet network OTP

Building increased resilience Gatwick north terminal consolidation

Cost Operational excellence

37 37

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

What does this mean for our shareholders?

40% annual dividend payout

Stable margins over the cycle

Strong EPS growth

Expected passenger growth of

7% - 8% CAGR

37

38 38

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet is a structural winner

• Europe's best network of primary airports

• Best customer and digital proposition

• Constant innovation to drive demand and loyalty

• Cost discipline, up-gauging will deliver savings of £110

million by 2021

• Strong balance sheet

38

Q & A

appendix

41 41

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Fuel and foreign exchange hedging

Sensitivities – FY16

• $10 per tonne change in fuel price will impact the full year pre-tax result by +/- $3.5 million

• One cent movement in the £/$ will impact the full year pre-tax result by +/- £1.5 million

• One cent movement in the £/€ will impact the full year pre-tax result by +/- £0.7 million

• One cent movement in the £/CHF will impact the full year pre-tax result by +/- £0.4 million

Fuel

requirement US dollar

requirement Euro surplus CHF surplus

Six months ending 31 March 2016

85% at $852 / metric tonne

89% at $1.62/£ 75% at €1.20/£ 69% at CHF1.46/£

Full year ending 30 September 2016

83% at $830 / metric tonne

81% at $1.63/£ 80% at €1.22/£ 67% at CHF1.46/£

Full year ending 30 September 2017

60% at $664 / metric tonne

61% at $1.55/£ 54% at €1.33/£ 51% at CHF1.43/£

As at 13 November 2015

41

42 42

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

H1 forward bookings

% seats sold *

H1 (October 2015 to March 2016) as at 13 November 2015

H1 bookings in line with prior year

42

91%

49%

93%

49%

Oct Nov Dec Jan Feb Mar H1

Winter '15 Winter '16

43 43

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

United Kingdom c. +9%

France c. +6%

Italy c. +3%

Spain c. +4% Switzerland c. +8%

Germany c. +7%

Source : OAG, scheduled data and Internal easyJet projection September 2015. Country capacity growth is based on network touching seats.

Profitably growing our business in 2016

Overall c. 8.0% capacity growth over winter

Netherlands c. +27%

Portugal c. +21%

43

44 44

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyjet

Ryanair

BA

Vueling

Other

Capacity environment H1 2016

Source: Market capacity data from OAG scheduled data, as at 6 September2015 easyJet markets based on internal easyJet definition.

Short-haul market easyJet city to city pairs

7.4% split by carrier

44

5.2%

3.7%

7.7%

6.8% 7.0%

7.8%

6.8%

7.4%

Capacity change totalSH Market

easyJet capacity change Competitors on easyJetmarkets

Capacity ChangeeasyJet markets

Winter 14/15 Winter 15/16

45 45

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Profit after tax

45

£m FY 2015 FY 2014 Change

Profit before tax 686 581 18.1%

Tax charge (138) (131) (5.3%)

Profit after tax 548 450 21.8%

Effective tax rate 20.1% 22.5% 2.4ppt

46 46

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Revenue per seat

46

£ per seat FY 2015 FY 2014 Change

Seat revenue 61.54 62.40 (1.4%)

Non-seat revenue 0.94 0.91 2.2%

Total revenue 62.48 63.31 (1.3%)

47 47

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Revenue, profit and margin growth in H2

47

Reported £m H2 2015 H2 2014 Change

Total revenue 2,919 2,825 3.3%

Fuel (683) (714) 4.3%

Operating costs (excluding fuel) (1,426) (1,352) (5.5%)

EBITDAR 810 759 6.6%

Ownership costs (131) (125) (3.4%)

Pre-tax profit 679 634 7.2%

PBT margin 23.3% 22.4% 0.8ppt

Seats (m) 42.8 40.5 5.9%

Constant currency £ per seat H2 2015 H2 2014 Change

Total revenue 70.35 69.85 0.7%

Fuel (15.68) (17.64) 11.1%

Operating costs (excluding fuel) (34.98) (33.44) (4.6%)

EBITDAR 19.69 18.77 4.9%

Ownership costs (3.14) (3.11) (1.0%)

Pre-tax profit 16.55 15.66 5.6%

48 48

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Cost per seat excluding fuel - key drivers

48

Cost per seat

excluding

fuel

£

Variance at

constant

currency

£

Variance at

constant

currency

%

Weighted variance

at constant

currency

£

Drivers

Airports and ground handling 14.96 (0.37) (2.4%) (1.0%)

• Regulated airport charges

• Impact of higher load factor

• Increase in de-icing costs due to colder weather

• Offset by savings of new contracts

Overhead 5.06 (0.30) (7.3%) (0.7%) • Higher disruption costs including FCO fire

Crew 6.73 (0.25) (3.8%) (0.7%)• Pay increase broadly in line with inflation

• Early recruitment in winter to meet summer

demand

Navigation 4.17 (0.22) (5.1%) (0.6%)• Inflationary increases

• Settlement of the historic Eurocontrol dispute

Maintenance 3.06 (0.11) (3.8%) (0.3%) • One-off benefit of new engine deal in FY 2014

Ownership 3.46 (0.02) (0.4%) (0.0%)• Depreciation on new aircraft purchased

• Offset against decreasing lease costs

37.44 (1.27) (3.4%) (3.3%)

Net Exchange (gains)/losses (0.09) (0.10) 100.0% (0.3%)• Effect of movements in foreign exchange rates

on Balance sheet revaluation

Total CPS excluding fuel 37.35 (1.37) (3.6%) (3.6%)

49 49

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Increasing proportion of A320’s

49

FY 2015 FY 2014 Change

A319 (operating lease) 49 54 (5)

A319 (owned / finance lease) 99 99 0

A319 Total 148 153 (5)

A320 (operating lease) 18 18 0

A320 (owned / finance lease) 75 55 20

A320 Total 93 73 20

Total fleet 241 226 15

Operating lease 28% 32% (4ppt)

Number unencumbered 114 94 20

Percentage of A320s in fleet 39% 32% 7ppt

50 50

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

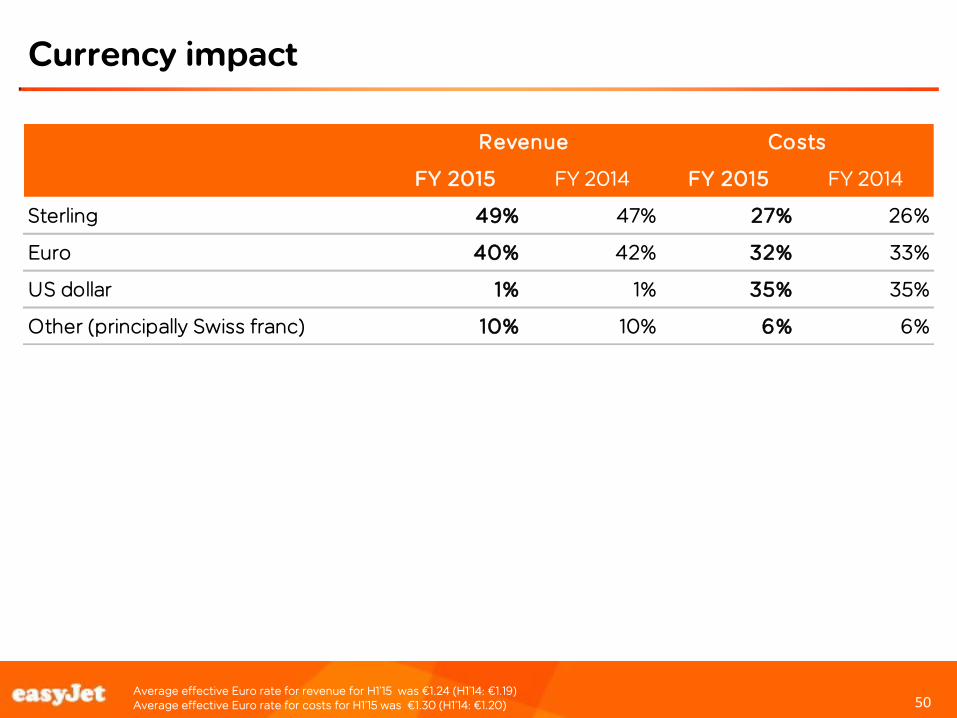

Currency impact

Average effective Euro rate for revenue for H1’15 was €1.24 (H1’14: €1.19) Average effective Euro rate for costs for H1’15 was €1.30 (H1’14: €1.20)

50

FY 2015 FY 2014 FY 2015 FY 2014

Sterling 49% 47% 27% 26%

Euro 40% 42% 32% 33%

US dollar 1% 1% 35% 35%

Other (principally Swiss franc) 10% 10% 6% 6%

Revenue Costs

51 51

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

ROCE calculation – including 7x lease adjustment

Reported £m FY 2015 FY 2014

Earnings before interest and tax – reported 688 581

Interest element of operating lease payments 38 41

Earnings before interest and tax - adjusted 726 622

Tax 20% 21%

Normalised operating profit after tax (NOPAT) 581 491

Average shareholders’ equity – reported 2,211 2,095

Average net cash – reported (429) (490)

Average capitalised leases 833 791

Average capital employed 2,615 2,396

Return on capital employed – 7x basis 22.2% 20.5%

51