FS_ALGO_1401_VWAP Customizations - Order Logic on Best Quantities (No names)

17

FS_ALGO#1401 VWAP Customizations - Order Logic on Best Quantities FS Number FS ALGO#1401 Client BROKER DU Business Analyst Milton Ko Date 10/12/2014 Internal Enhancement Reference(s) Page 1 of 17

Transcript of FS_ALGO_1401_VWAP Customizations - Order Logic on Best Quantities (No names)

FS_ALGO#1401 VWAP Customizations - Order Logic on Best Quantities

FS Number FS ALGO#1401

Client BROKER

DU Business Analyst Milton Ko

Date 10/12/2014Internal Enhancement

Reference(s)

Page 1 of 17

Revision history

Version Date Description By

0.1 10/12/2014 Initial version Milton Ko

0.2 19/12/2014

Corrected some typos and added page

numbers Milton Ko

0.3 29/12/2014

Modified the definition of A’ and B’ in 1.3.1,

added section 1.3.2, and inserted scenarios

1(f), 1(g), 3(f) and 3(g) Milton Ko

Page 2 of 17

Contents

1 Business Requirements.................................................................................................................... 4

1.1 Background and Objective............................................................................................................4

1.2 Scopes.......................................................................................................................................... 4

1.3 Details and Definitions of the New Logic.......................................................................................4

1.3.1 The Logic of Order Placement................................................................................................5

1.3.2 The Maximum Possible Quantities A’ and B’..........................................................................6

1.4 Business Requirements................................................................................................................6

1.4.1 Requirement Catalogue..........................................................................................................7

1.4.2 Detailed Requirements and Scenarios...................................................................................7

1.4.2.1 Req001 – Add “Order Quantity Factor” and “Aggressive Time” for Input for Start-up......71.4.2.2 Req002 – Implement the Logic Stated in 1.3 as a Logic of Order Placement of VWAP...7 71.4.2.3 Req003 – VWAP Control Center Customization............................................................15

1.4.2.3.1 The Aggressive Time...............................................................................................151.4.2.3.2 Mode Button............................................................................................................151.4.2.3.3 Order Quantity Factor..............................................................................................151.4.2.3.4 Scenarios Induced by VWAP Control Center..........................................................15

2 Authorization of Business Requirement.......................................................................................17

Page 3 of 17

1 Business Requirements

1.1 Background and Objective

The algorithm VWAP in the automated trading platform of DECIDE aims at assisting traders to break down large size orders into small trading orders and execute. The model used for breaking size orders bases on historical data. The first VWAP version on the production of BROKER is 2.0.8, whose Go-Live date was in April 2014. After over half a year of experience working with VWAP, BROKER has decided to add in a customized trading logic regarding the order placement. This document means to specify this logic and related definitions in a precise and closed way.

1.2 Scopes

The logic of order placement in the recent VWAP (referred as original logic hereafter) is logically closed (including responses for all scenarios). The logic specified in this document (referred as new logic hereafter) is an add-on to that. Any situation not described by the new logic will follow the original logic.

The scope of the customizations specified in this document includes:

1. the add-on logic described in Section 1.3;

2. the GUI requirements specified in Section 1.4.2.3 ;

Anything not included in the above 2 items is out of scope.

1.3 Details and Definitions of the New Logic

VWAP works on both buy and sell size orders. The new logic applies to both. Indeed, the new logic on buy size orders is just the “reverse” of that on sell size orders. For the new logic, we need to introduce 2 new parameters entered by users:

1. Order Quantity Factor, denoted by c, a positive number;

2. Aggressive Time, denoted by T, with format HH:MM:SS (for example, 15:30:00).

There are a few more notations that we will need for the description of the logic.

3. the maximum quantity allowed for order placement by VWAP, denoted by M, set up in VWAP Control Center.

4. the price at one tick below best ask, denoted by Pa. (In case when ask side is empty, Pa is the best bid)

Page 4 of 17

5. the price at one tick above best bid, denoted by Pb. (In case when bid side is empty, Pb is the best ask)

6. the quantity at the best ask and best bid, denoted by A and B respectively. (In case ask side is empty, A = 0; in case bid side is empty, B = 0)

7. the maximum possible quantity in front of our VWAP order in the queue lining up at the price Pa for buy size orders, and or at Pb for sell size orders, denoted by A’ and B’ respectively. The estimation logic will be described in Section 1.3.2

8. the quantity of the order placed by VWAP at a moment, denoted by Q.

1.3.1 The Logic of Order Placement

Let us now describe the logic on buy size orders first. When the market is empty, no order is placed, as the recent VWAP does. Suppose now the market depth is non-empty and a running VWAP places a buy order, and the following logic is applied only when the current time is before time T, and the order is up at the price Pa.:

(B1) When A<Q, the placed order stays at Pa and wait until any of the following is true:

(a) Someone fills the best ask with more quantities such that A ≥ Q. Then if (B2) is NOT true, VWAP converges the order up to match at the best ask price; otherwise, follow the consequences of (B2);

(b) Someone executes this order partially at Pa, and Q decreases so that A ≥ Q. Then if (B2) is NOT true, VWAP converges the partially matched order up to match at the best ask price.

(c) Someone fully executes the order at Pa.

(B2) When A' + Q ≤ cM, the placed order stays at Pa and wait until any of the following is true:

(a) Someone fully executes the order at Pa.

(b) The best ask increases, which means Pa increases. Then VWAP converges the order, either unmatched or partially matched, up at the new Pa and repeat the same logic, (B1) and (B2), again.

Similarly, we describe the logic on sell size orders. Suppose now the market depth is non-empty and a running VWAP places a sell order, and the following logic is applied only when the current time is before time T, and the order is down at the price Pb.:

(S1) When B<Q, the placed order stays at Pb and wait until any of the following is true:

(a) Someone fills the best bid with more quantities such that B ≥ Q. Then if (S2) is NOT true, VWAP converges the order down to match at the best bid price; otherwise, follow the consequences of (S2);

(b) Someone executes this order partially at Pb, and Q decreases so that B ≥ Q. Then if (S2) is NOT true, VWAP converges the partially matched order down to match at the best bid price.

(c) Someone fully executes the order at Pb.

(S2) When B' + Q ≤ cM, the placed order stays at Pb and wait until any of the following is true:

Page 5 of 17

(a) Someone fully executes the order at Pb.

(b) The best bid decreases, which means Pb decreases. Then VWAP converges the order, either unmatched or partially matched, down at the new Pb and repeat the same logic, (S1) and (S2), again.

It is emphasized that the above logics, (B1) and (B2), or (S1) and (S2), are applied only when the current time is before time T, the aggressive time. After time T, VWAP enters the so called Aggressive Mode1, defined as the mode in which logic (B1) and (B2), or (S1) and (S2), would be suppressed, and VWAP follows the original logic on the placement of orders. Moreover, this aggressive mode can be turned on by a button in VWAP Control Center, supposed to be implemented upon the graphical user interface (GUI) requirement stated in this document. We will describe more about this button in 1.4.2.3 for GUI requirement.

1.3.2 The Maximum Possible Quantities A’ and B’

The estimation of A’ by VWAP follows the following logic. Suppose now VWAP is running on a buy size order. Right after VWAP places a buy order at the price Pa, VWAP detects the total volume at this level, denoted by Va, and put A’ = Va – Q. Then A’ is the number of shares in front of our order at this moment, and will be updated immediately only after the occurrence of any of the following:

(i) There is a transaction at the price Pa. Then A’ will be deducted by the transaction quantity.(ii) When Va, the total volume at Pa, is updated, and A’ > Va – Q, VWAP will set A’ = Va – Q.(iii) When Va is updated and A’ < 0, VWAP will set A’ = 0.(iv) When the order is partially executed, VWAP will set A’ = 0.

Please be noted that in the case when there are cancellations of some order at the price Pa, it is not possible to know if the cancelled orders were in front of our order or behind. In this case, VWAP will not update A’ (unless (ii) and (iii) is true), and this makes A’ the maximum possible quantity in front of our order instead of exact. In other words, the estimation by the above logic always gives an upper bound of the quantity in front of our order.

We have the same estimation logic of B’ for sell VWAP. Suppose now VWAP is running on a sell size order. Right after VWAP places a sell order at the price Pb, VWAP detects the total volume at this level, denoted by Vb, and put B’ = Vb – Q. Then B’ is the number of shares in front of our order at this moment, and will be updated immediately only after the occurrence of any of the following:

(v) There is a transaction at the price Pb. Then B’ will be deducted by the transaction quantity.(vi) When Vb, the total volume at Pb, is updated, and B’ > Vb – Q, VWAP will set B’ = Vb – Q.(vii) When Vb is updated and B’ < 0, VWAP will set B’ = 0.(viii) When the order is partially executed, VWAP will set B’ = 0.

Scenarios for illustrating the above logic will be stated in 1.4.2.2.

1.4 Business Requirements

1 The motivation of having this aggressive time and mode is to avoid incomplete execution. Imagine for a buy VWAP, if logic (B2) is true, an order stays at Pa and the market depth keeps unchanged until the end time comes, that order would never be executed. Therefore, time T should be set as a time a short duration before the end time of a VWAP job, say 30 minutes. After this time, VWAP execute orders in a more aggressive manner by following the original logic.

Page 6 of 17

1.4.1 Requirement Catalogue

Req ID UseCaseID

Requirement Description: Comments /Explanation /Details

RQ001 - Add 2 parameter inputs in the start-up frame of VWAP: Order Quantity Factor and Aggressive Time

Order Quantity Factor is used in logic (B2) and (S2); Aggressive Time defines the time when VWAP enters the aggressive mode

RQ002 - VWAP follow the logic stated in section 1.3

This is the most important requirement of this document

RQ003 - VWAP Control Center has (a) a field showing the aggressive time for users to modify it(b) a button for users to switch on and off the aggressive mode(c) a field showing the Order Quantity Factor for users to modify it

1.4.2 Detailed Requirements and Scenarios

In this section, unless otherwise specified, VWAP refers to the VWAP algorithm with the customized logic stated in 1.3.

1.4.2.1 Req001 – Add “Order Quantity Factor” and “Aggressive Time” for

Input for Start-up

When VWAP is started, in the startup frame, it is required that the parameters “Order Quantity Factor” and “Aggressive Time” can be set. If “Order Quantity Factor” is left empty, it is default 1; if “Aggressive Time” is left empty, it is default 30 minutes before the end time of this VWAP job.

1.4.2.2 Req002 – Implement the Logic Stated in 1.3 as a Logic of Order

Placement of VWAP

We will illustrate the logic stated in 1.3 by the following scenarios. These scenarios will be used as test cases for the implemented solution. Let us employ the term “non-aggressive mode” for referring to the mode when VWAP is not on aggressive mode (for definition please refer to the last paragraph of 1.3), and call a VWAP job a buy VWAP if it works on a buy size order and a sell VWAP if it works on a sell size order. We will use the notations defined in 1.3. Moreover, in the subsections we always assume that the parameters set by users are as follow: M = 20000, c = 1.5.

In scenario 1 and 2, we assume the underlying buy size order has limit 253. This means that VWAP will not place any buy order with limit greater than 253, no matter what happens. Similarly, in scenario 3 and 4, we assume the underlying sell size order has limit 248. This means that VWAP will not place any sell order with limit less than 248.

Page 7 of 17

Scenario 1: A Buy VWAP on Non-Aggressive Mode with Insufficient Supply at Best Ask

(a) The market depth at this moment is as follows:

Bid AskQuantity Price Price Quantity

200000 250 251 5000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Pa = 250, one tick below the best ask. Suppose now VWAP places a buy order with quantity 8000. Hence Q = 8000. The order then converges up at price 250 and the market depth becomes as follow:

Bid AskQuantity Price Price Quantity

208000 250 251 5000250000 249 252 150000220000 248 253 180000300000 247 254 160000

At this moment, A = 5000 < Q, thus (B1) is true. VWAP then keeps the order at this price, standing by for the update of the market depth.

(b) Continuing from (a), assume someone places a sell order at 251 with quantity 5000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

208000 250 251 10000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 8000 < A = 10000. Moreover A’ + Q = 208000 ≥ 1.5 × 20000 = 30000, (B2) is not true. Hence VWAP converges the order up to 251 and fully executes it.

(c) Continuing from (a), assume someone places a sell order at 250 with quantity 202000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

6000 250 251 5000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 6000 > 5000 = A. Hence according to (B1), still VWAP keeps the order at 250.

(d) Continuing from (a), assume someone places a sell order at 250 with quantity 204000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

Page 8 of 17

4000 250 251 5000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 4000 < 5000 = A. Hence according to (a) of (B1), we check also (B2). And now A’ = 0, and A’ + Q = 4000 < 30000. VWAP keeps the order at 250 and waits for execution.

(e) Continuing from (a), assume someone places a buy order at 250 with quantity 200000, and another places a sell order at 250 with quantity 204000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

204000 250 251 5000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 4000 < 5000 = A. Hence according to (a) of (B1), we check also (B2). And now A’ = 0, and A’ + Q = 4000 < 30000. VWAP keeps the order at 250 and wait for execution.

(f) Continuing from (a), assume someone places a buy order at 250 with quantity 200000, and the 200000 shares in front of our order got cancelled. Yet, VWAP can only tell there is a cancellation of 200000 shares but cannot tell if that is in front of us or not. Thus A’ = 200000 (refer to 1.3.2). Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

208000 250 251 5000250000 249 252 150000220000 248 253 180000300000 247 254 160000

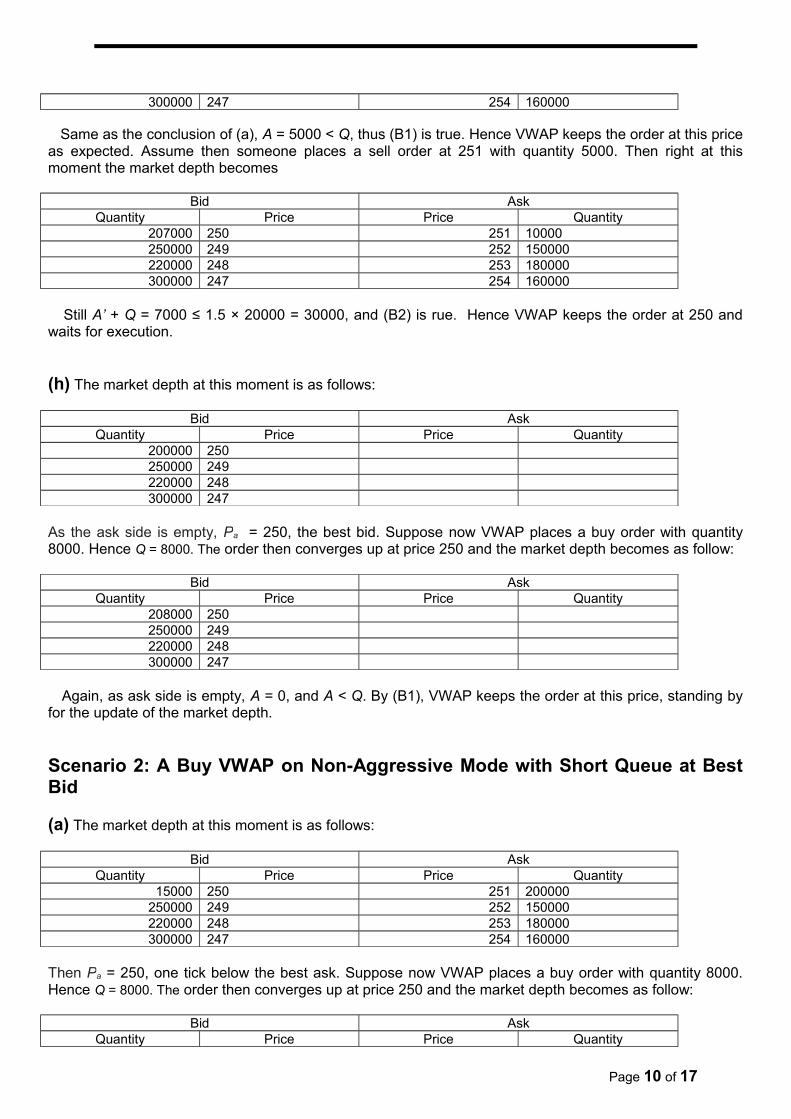

Same as the conclusion of (a), A = 5000 < Q, thus (B1) is true. Hence VWAP keeps the order at this price as expected. Assume then someone places a sell order at 251 with quantity 5000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

208000 250 251 10000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Still A’ + Q = 208000 ≥ 1.5 × 20000 = 30000, and (B2) is not true. Hence VWAP converges the order up to 251 and fully executes it.

(g) Continuing from (a), assume someone places a buy order at 250 with quantity 200000, and the 200000 shares in front of our order got cancelled. Moreover, someone places a sell order at 250 with quantity 1000 and our order is partially executed. The remaining quantity of our order Q becomes 7000. Thus A’ = 0 (refer to (iv) under 1.3.2). Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

207000 250 251 5000250000 249 252 150000220000 248 253 180000

Page 9 of 17

300000 247 254 160000

Same as the conclusion of (a), A = 5000 < Q, thus (B1) is true. Hence VWAP keeps the order at this price as expected. Assume then someone places a sell order at 251 with quantity 5000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

207000 250 251 10000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Still A’ + Q = 7000 ≤ 1.5 × 20000 = 30000, and (B2) is rue. Hence VWAP keeps the order at 250 and waits for execution.

(h) The market depth at this moment is as follows:

Bid AskQuantity Price Price Quantity

200000 250250000 249220000 248300000 247

As the ask side is empty, Pa = 250, the best bid. Suppose now VWAP places a buy order with quantity 8000. Hence Q = 8000. The order then converges up at price 250 and the market depth becomes as follow:

Bid AskQuantity Price Price Quantity

208000 250250000 249220000 248300000 247

Again, as ask side is empty, A = 0, and A < Q. By (B1), VWAP keeps the order at this price, standing by for the update of the market depth.

Scenario 2: A Buy VWAP on Non-Aggressive Mode with Short Queue at Best Bid

(a) The market depth at this moment is as follows:

Bid AskQuantity Price Price Quantity

15000 250 251 200000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Pa = 250, one tick below the best ask. Suppose now VWAP places a buy order with quantity 8000. Hence Q = 8000. The order then converges up at price 250 and the market depth becomes as follow:

Bid AskQuantity Price Price Quantity

Page 10 of 17

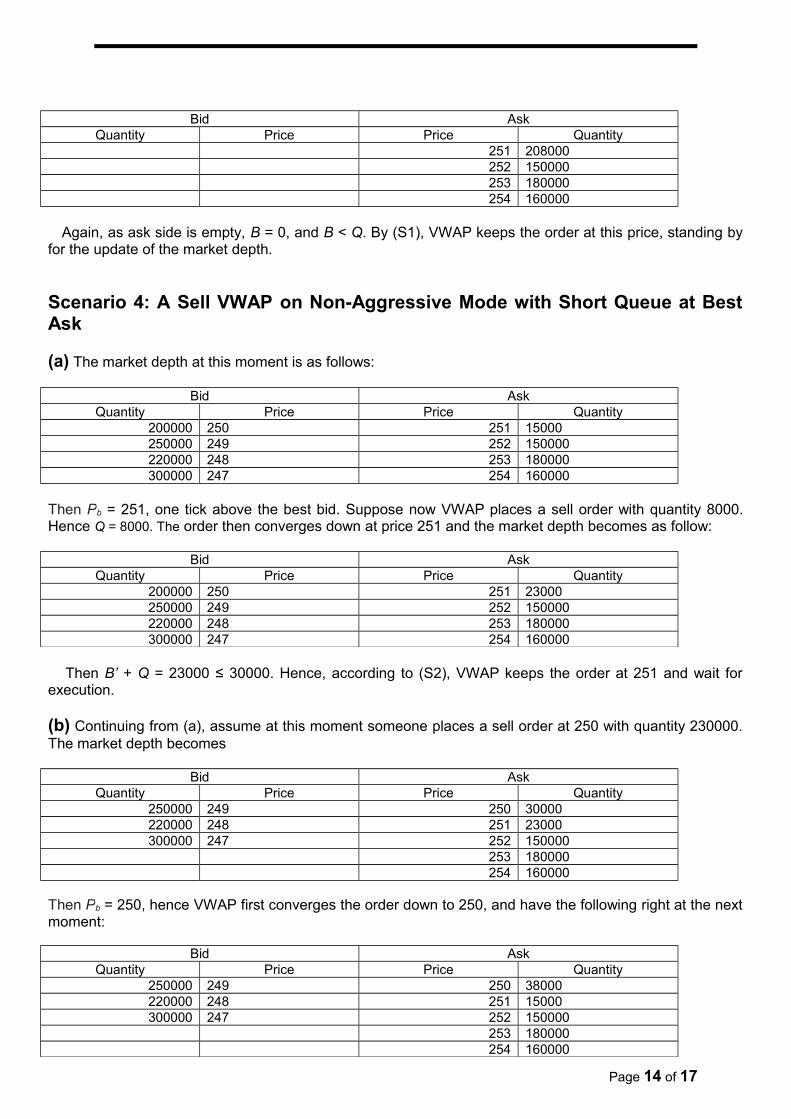

23000 250 251 200000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then A’ + Q = 23000 ≤ 30000. Hence, according to (B2), VWAP keeps the order at 250 and wait for execution.

(b) Continuing from (a), assume at this moment someone places a buy order at 251 with quantity 230000. The market depth becomes

Bid AskQuantity Price Price Quantity

30000 251 252 15000023000 250 253 180000

250000 249 254 160000220000 248300000 247

Then Pa = 251, hence VWAP first converges the order up to 251, and have the following right at the next moment:

Bid AskQuantity Price Price Quantity

38000 251 252 15000015000 250 253 180000

250000 249 254 160000220000 248300000 247

Now Q = 8000 < 150000 = A, and A’ = 30000 hence A’ + Q = 38000 ≥ 30000. Hence (B1) and (B2) are not true, and VWAP converges the order up at 252 and execute it.

Scenario 3: A Sell VWAP on Non-Aggressive Mode with Insufficient Supply at Best Bid

(a) The market depth at this moment is as follows:

Bid AskQuantity Price Price Quantity

5000 250 251 200000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Pb = 251, one tick above the best bid. Suppose now VWAP places a sell order with quantity 8000. Hence Q = 8000. The order then converges down at price 251 and the market depth becomes as follow:

Bid AskQuantity Price Price Quantity

5000 250 251 208000250000 249 252 150000220000 248 253 180000300000 247 254 160000

At this moment, B = 5000 < Q, and thus (S1) is true. VWAP then keeps the order at this price, standing by for the update of the market depth.

Page 11 of 17

(b) Continuing from (a), assume someone places a buy order at 250 with quantity 5000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

10000 250 251 208000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 8000 < B = 10000. Moreover B’ + Q = 208000 ≥ 1.5 × 20000 = 30000, (S2) is not true. Hence VWAP converges the order down to 250 and fully executes it.

(c) Continuing from (a), assume someone places a buy order at 251 with quantity 202000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

5000 250 251 6000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 6000 > 5000 = B. Hence according to (S1), still VWAP keeps the order at 251.

(d) Continuing from (a), assume someone places a buy order at 251 with quantity 204000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

5000 250 251 4000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 4000 < 5000 = B. Hence according to (a) of (S1), we check also (S2). And now B’ = 0, and B’ + Q = 4000 < 30000. VWAP keeps the order at 251 and wait for execution.

(e) Continuing from (a), assume someone places a sell order at 251 with quantity 200000, and another places a buy order at 251 with quantity 204000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

5000 250 251 204000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Q = 4000 < 5000 = A. Hence according to (a) of (S1), we check also (S2). And now B’ = 0, and B’ + Q = 4000 < 30000. VWAP keeps the order at 251 and wait for execution.

(f) Continuing from (a), assume someone places a sell order at 251 with quantity 200000, and the 200000 shares in front of our order got cancelled. Yet, VWAP can only tell there is a cancellation of 200000 shares but cannot tell if that is in front of us or not. Thus B’ = 200000 (refer to 1.3.2). Then right at this moment the market depth becomes

Bid Ask

Page 12 of 17

Quantity Price Price Quantity5000 250 251 208000

250000 249 252 150000220000 248 253 180000300000 247 254 160000

Same as the conclusion of (a), B = 5000 < Q, thus (S1) is true. Hence VWAP keeps the order at this price as expected. Assume then someone places a buy order at 250 with quantity 5000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

10000 250 251 208000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Still B’ + Q = 208000 ≥ 1.5 × 20000 = 30000, and (S2) is not true. Hence VWAP converges the order down to 250 and fully executes it.

(g) Continuing from (a), assume someone places a sell order at 251 with quantity 200000, and the 200000 shares in front of our order got cancelled. Moreover, someone places a buy order at 251 with quantity 1000 and our order is partially executed. The remaining quantity of our order Q becomes 7000. Thus B’ = 0 (refer to (viii) under 1.3.2). Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

5000 250 251 207000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Same as the conclusion of (a), B = 5000 < Q, thus (S1) is true. Hence VWAP keeps the order at this price as expected. Assume then someone places a buy order at 250 with quantity 5000. Then right at this moment the market depth becomes

Bid AskQuantity Price Price Quantity

10000 250 251 207000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Still B’ + Q = 7000 ≤ 1.5 × 20000 = 30000, and (S2) is rue. Hence VWAP keeps the order at 251 and waits for execution.

(h) The market depth at this moment is as follows:

Bid AskQuantity Price Price Quantity

251 200000252 150000253 180000254 160000

As the bid side is empty, Pb = 251, the best ask. Suppose now VWAP places a buy order with quantity 8000. Hence Q = 8000. The order then converges down at price 251 and the market depth becomes as follow:

Page 13 of 17

Bid AskQuantity Price Price Quantity

251 208000252 150000253 180000254 160000

Again, as ask side is empty, B = 0, and B < Q. By (S1), VWAP keeps the order at this price, standing by for the update of the market depth.

Scenario 4: A Sell VWAP on Non-Aggressive Mode with Short Queue at Best Ask

(a) The market depth at this moment is as follows:

Bid AskQuantity Price Price Quantity

200000 250 251 15000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then Pb = 251, one tick above the best bid. Suppose now VWAP places a sell order with quantity 8000. Hence Q = 8000. The order then converges down at price 251 and the market depth becomes as follow:

Bid AskQuantity Price Price Quantity

200000 250 251 23000250000 249 252 150000220000 248 253 180000300000 247 254 160000

Then B’ + Q = 23000 ≤ 30000. Hence, according to (S2), VWAP keeps the order at 251 and wait for execution.

(b) Continuing from (a), assume at this moment someone places a sell order at 250 with quantity 230000. The market depth becomes

Bid AskQuantity Price Price Quantity

250000 249 250 30000220000 248 251 23000300000 247 252 150000

253 180000254 160000

Then Pb = 250, hence VWAP first converges the order down to 250, and have the following right at the next moment:

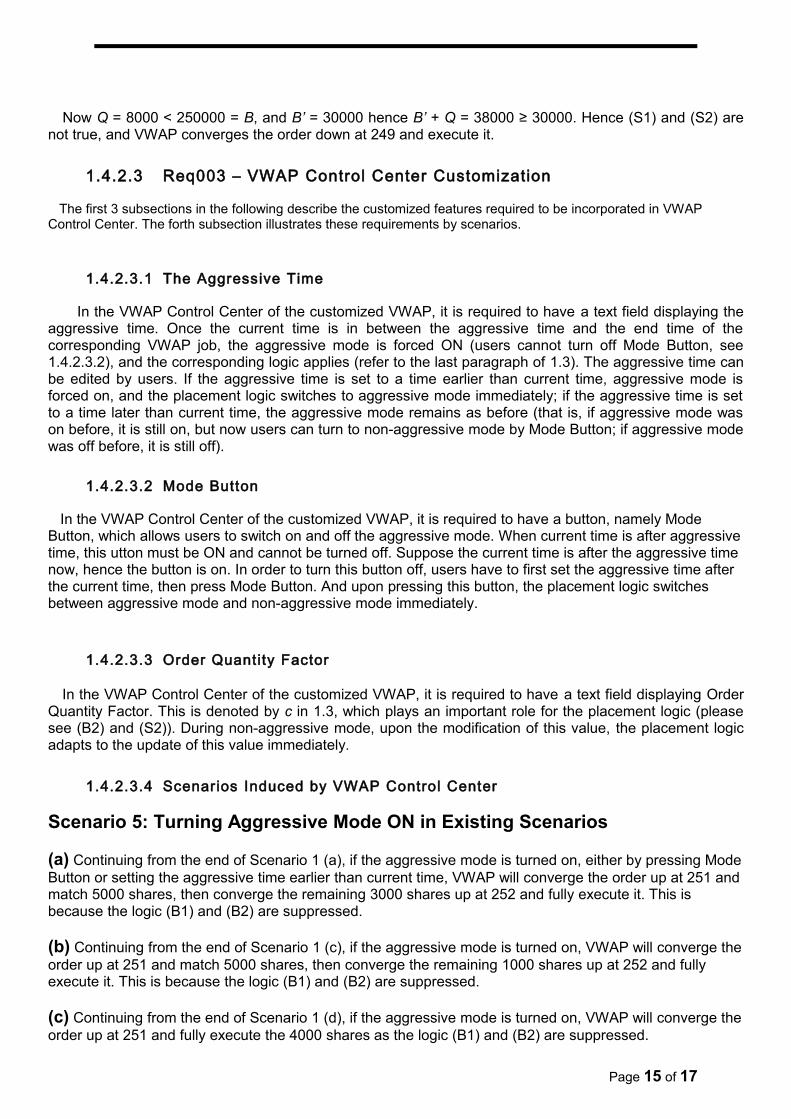

Bid AskQuantity Price Price Quantity

250000 249 250 38000220000 248 251 15000300000 247 252 150000

253 180000254 160000

Page 14 of 17

Now Q = 8000 < 250000 = B, and B’ = 30000 hence B’ + Q = 38000 ≥ 30000. Hence (S1) and (S2) are not true, and VWAP converges the order down at 249 and execute it.

1.4.2.3 Req003 – VWAP Control Center Customization

The first 3 subsections in the following describe the customized features required to be incorporated in VWAP Control Center. The forth subsection illustrates these requirements by scenarios.

1.4.2.3.1 The Aggressive Time

In the VWAP Control Center of the customized VWAP, it is required to have a text field displaying the aggressive time. Once the current time is in between the aggressive time and the end time of the corresponding VWAP job, the aggressive mode is forced ON (users cannot turn off Mode Button, see 1.4.2.3.2), and the corresponding logic applies (refer to the last paragraph of 1.3). The aggressive time can be edited by users. If the aggressive time is set to a time earlier than current time, aggressive mode is forced on, and the placement logic switches to aggressive mode immediately; if the aggressive time is set to a time later than current time, the aggressive mode remains as before (that is, if aggressive mode was on before, it is still on, but now users can turn to non-aggressive mode by Mode Button; if aggressive mode was off before, it is still off).

1.4.2.3.2 Mode Button

In the VWAP Control Center of the customized VWAP, it is required to have a button, namely Mode Button, which allows users to switch on and off the aggressive mode. When current time is after aggressive time, this utton must be ON and cannot be turned off. Suppose the current time is after the aggressive time now, hence the button is on. In order to turn this button off, users have to first set the aggressive time after the current time, then press Mode Button. And upon pressing this button, the placement logic switches between aggressive mode and non-aggressive mode immediately.

1.4.2.3.3 Order Quantity Factor

In the VWAP Control Center of the customized VWAP, it is required to have a text field displaying Order Quantity Factor. This is denoted by c in 1.3, which plays an important role for the placement logic (please see (B2) and (S2)). During non-aggressive mode, upon the modification of this value, the placement logic adapts to the update of this value immediately.

1.4.2.3.4 Scenarios Induced by VWAP Control Center

Scenario 5: Turning Aggressive Mode ON in Existing Scenarios

(a) Continuing from the end of Scenario 1 (a), if the aggressive mode is turned on, either by pressing Mode Button or setting the aggressive time earlier than current time, VWAP will converge the order up at 251 and match 5000 shares, then converge the remaining 3000 shares up at 252 and fully execute it. This is because the logic (B1) and (B2) are suppressed.

(b) Continuing from the end of Scenario 1 (c), if the aggressive mode is turned on, VWAP will converge the order up at 251 and match 5000 shares, then converge the remaining 1000 shares up at 252 and fully execute it. This is because the logic (B1) and (B2) are suppressed.

(c) Continuing from the end of Scenario 1 (d), if the aggressive mode is turned on, VWAP will converge the order up at 251 and fully execute the 4000 shares as the logic (B1) and (B2) are suppressed.

Page 15 of 17

(d) Continuing from the end of Scenario 1 (e), if the aggressive mode is turned on, VWAP will converge the order up at 251 and fully execute the 4000 shares as the logic (B1) and (B2) are suppressed.

(e) Continuing from the end of Scenario 2 (a), if the aggressive mode is turned on, VWAP will converge the order up at 251 and fully execute the 8000 shares as the logic (B1) and (B2) are suppressed.

(f) Continuing from the end of Scenario 3 (a), if the aggressive mode is turned on, VWAP will converge the order down at 250 and match 5000 shares, then converge the remaining 3000 shares up at 249 and fully execute it. This is because the logic (S1) and (S2) are suppressed.

(g) Continuing from the end of Scenario 3 (c), if the aggressive mode is turned on, VWAP will converge the order down at 250 and match 5000 shares, then converge the remaining 1000 shares up at 249 and fully execute it. This is because the logic (S1) and (S2) are suppressed.

(h) Continuing from the end of Scenario 3 (d), if the aggressive mode is turned on, VWAP will converge the order down at 250 and fully execute 4000 shares as the logic (S1) and (S2) are suppressed.

(i) Continuing from the end of Scenario 3 (e), if the aggressive mode is turned on, VWAP will converge the order down at 250 and fully execute 4000 shares as the logic (S1) and (S2) are suppressed.

(j) Continuing from the end of Scenario 4 (a), if the aggressive mode is turned on, VWAP will converge the order down at 250 and fully execute 8000 shares as the logic (S1) and (S2) are suppressed.

Scenario 6: Modifying Order Quantity Factor c in Existing Scenarios

(a) Continuing from the end of Scenario 1 (d), suppose Order Quantity Factor c is modified to 0.1. Then checking (B2), A’ + Q = 4000 > 2000 = 0.1 × 20000. VWAP will converge the order up at 251 and fully execute the 4000 shares.

(b) Continuing from the end of Scenario 1 (e), suppose Order Quantity Factor c is modified to 0.1. Then checking (B2), A’ + Q = 4000 > 2000 = 0.1 × 20000. VWAP will converge the order up at 251 and fully execute 4000 shares.

(c) Continuing from the end of Scenario 2 (a), suppose Order Quantity Factor c is modified to 1. Then checking (B2), A’ + Q = 23000 > 20000 = 1 × 20000. VWAP will converge the order up at 251 and fully execute 8000 shares.

(d) Continuing from the end of Scenario 3 (d), suppose Order Quantity Factor c is modified to 0.1. Then checking (S2), B’ + Q = 4000 > 2000 = 0.1 × 20000. VWAP will converge the order down at 250 and fully execute 4000 shares.

(e) Continuing from the end of Scenario 3 (e), suppose Order Quantity Factor c is modified to 0.1. Then checking (S2), B’ + Q = 4000 > 2000 = 0.1 × 20000. VWAP will converge the order down at 250 and fully execute 4000 shares.

(f) Continuing from the end of Scenario 4 (a), suppose Order Quantity Factor c is modified to 1. Then checking (B2), A’ + Q = 23000 > 20000 = 1 × 20000. VWAP will converge the order up at 251 and fully execute 8000 shares.

Page 16 of 17

2 Authorization of Business Requirement

By signing at the space below, BROKER agrees that the requirements and the corresponding logic stated in this document, FS_ALGO_1401_VWAP Customizations - Order Logic on Best Quantities v0.3, fulfil the customization requirement on the recent version of VWAP.

For the Client:

Name:

Position:

Date:

Signature:

For the Supplier:

Name:

Position:

Date:

Signature:

For the Client:

Name:

Position:

Date:

Signature:

For the Supplier:

Name:

Position:

Date:

Signature:

For the Client:

Name:

Position:

Date:

Signature:

For the Supplier:

Name:

Position:

Date:

Signature:

Page 17 of 17