Frost & Sullivan North American Mobile Crm Analyst Briefing

21

North American Mobile CRM Market: Investment Themes Driving the Mobile CRM Space Swarna Pasupathi, Research Analyst Business and Financial Services Information and Communication Technology September 30, 2008

-

Upload

frost-sullivan -

Category

Technology

-

view

3.745 -

download

0

Transcript of Frost & Sullivan North American Mobile Crm Analyst Briefing

North American Mobile CRM Market:Investment Themes Driving the Mobile CRM Space

Swarna Pasupathi, Research Analyst

Business and Financial Services

Information and Communication Technology

September 30, 2008

2

Focus Points

� Introduction

� Market Overview

� Investment Analysis

� Scorecards

� Question and Answers

3

• Frost & Sullivan’s Financial Research team has recently completed an extensive review of

investment opportunities in the North American Mobile CRM market.

• The study highlights the growth segments in the North American Mobile CRM market, and

identifies specific investment themes and opportunities within the market.

• It includes a comprehensive overview and in-depth financial analysis of the North American

Mobile CRM universe covered by Frost & Sullivan.

Introduction

4

Focus Points

� Introduction

� Market Overview

� Market Segmentation

� Industry Economics

� Investment Analysis

� Investment Themes

� Growth Monitor

� Scorecards

� Sector Scorecard

� Mergers & Acquisitions Analysis

� Venture Capital Score Card

� Venture Opportunity Score Card

� Question and Answers

5

Market Overview - Segmentation

Segments Focussed

• Mobile Sales Force Automation (SFA)

• Mobile Field Service Management (FSM)

Major Industry Participants

• COGNOS

• Oracle (PeopleSoft and Siebel)

• Salesforce.com

• SAP AG

• Maximizer Software

• Vettro

• Dexterra

• SAGE

• Sybase – iAnywhere Solutions

6

Market Overview

• Enterprise inclination towards mobility platform is on the rise.

• Growth: CRM spending is growing at 11.8% CAGR

• Opportunity: Mid-market is still under-penetrated; only 20% of SMBs use mobile CRM

and the rest of firms are in decision-making cycle to adopt mobile platform during the

period 2008-2012.

Despite an economic slowdown SMB’s will continue to invest in mobile solutions :

• Competitive Advantage

• Increases Productivity with less staff

• Increases Customer Satisfaction

Market Overview Market Segmentation Industry Economics

7

ENHANCERS

INHIBITORS

�Increases Productivity and ROI

�The concept of mobile-commuting

in the workforce offers flexibility thereby

increasing the overall productivity of the

team.

�The is an increase in the number of

vendors offering of Mobile-CRM

integration applications.

�Steady tariff plans from Mobile

Network Service Provider

�Subsidized mobile device

prices have reduced the deployment

cost for organizations.

�Availability of varieties of high

powered mobile devices has created

a robust platform for mobile application.

�Lack of justifying the total

cost of ownership (TCO)

�Non-Acceptance of Technology

�Security and Integration issues on

mobile devices stunt growth in the

SMB segment

�Increase in Number of Vendors

�Information Lag

�Slow rollout and adoption of next

generation networks

Industry Economics

8

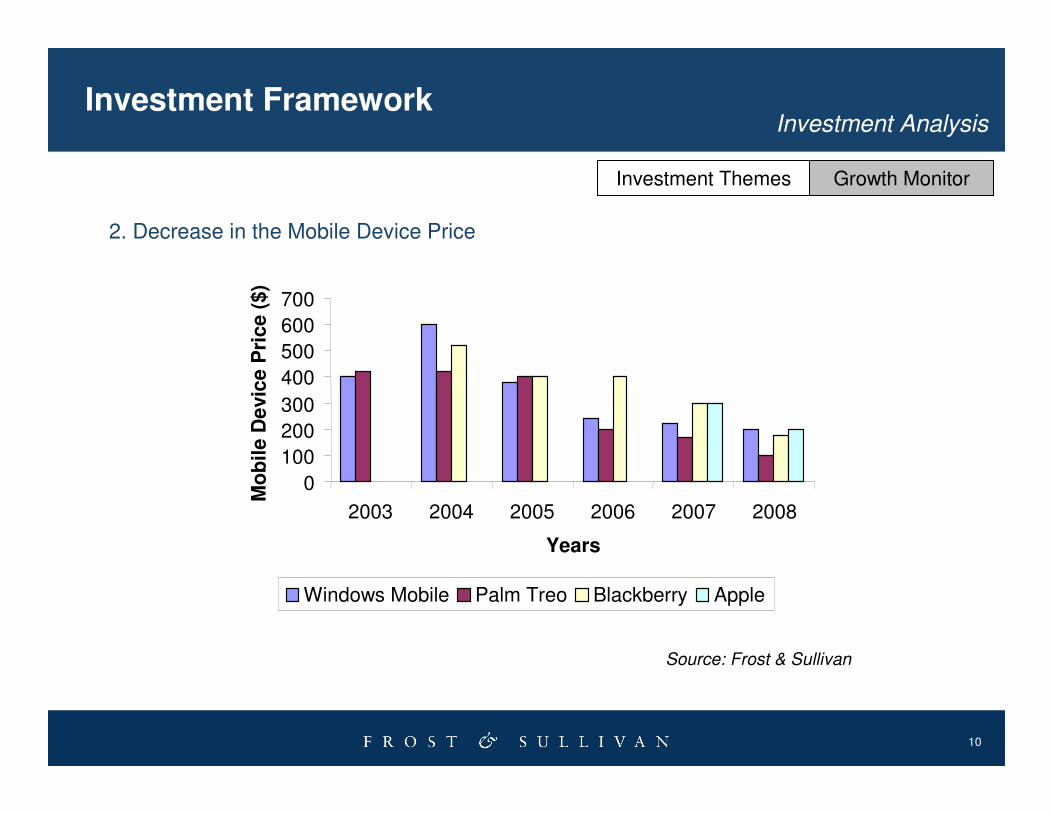

Investment FrameworkInvestment Analysis

1. Standardization of Mobile Network Operator’s Tariff Plans

2. Decrease in the Mobile Device Price

3. Immense Increase in Smartphone Shipment Worldwide

Investment Themes Growth Monitor

9

Investment FrameworkInvestment Analysis

Source: Frost & Sullivan

1. Standardization of Mobile Network Operators Tariff Plans

Investment Themes Growth Monitor

0

20

40

60

80

100

120

300 600 900 1500

Anytime Minutes

Netw

ork

Serv

ice C

ost

($)

Verizon T mobile AT & T Sprint

10

Investment FrameworkInvestment Analysis

Source: Frost & Sullivan

2. Decrease in the Mobile Device Price

Investment Themes Growth Monitor

0

100

200

300

400

500

600

700

2003 2004 2005 2006 2007 2008

Years

Mo

bil

e D

evic

e P

ric

e (

$)

Windows Mobile Palm Treo Blackberry Apple

11

Investment FrameworkInvestment Analysis

3. Increase in Smart Phone Shipment Worldwide

Source: Frost & Sullivan

Investment Themes Growth Monitor

0

20

40

60

80

100

120

2004 2005 2006 2007

Year

Un

its

Sh

ipp

ed

(M

illio

n)

Shipment in Smartphone Devices Worldwide

12

Investment FrameworkInvestment Analysis

Source: Frost & Sullivan

40.060.015.0-20.024.44,064.0SAP AG

20.080.015.0-20.043.0557.9Salesforce.com

35.065.015.0-20.047.09,460.0ORACLE

100020.0-25.01.320.4ASTEA

15.020.6Segment CAGR (2007-2012)

FSM

(%)

MSFA

(%)

Growth Rank

(%)

NA Mobile CRM Revenues in 2007

($ Million)

Company’s Total NA Revenues in 2007

($ Million)

Company

Investment Themes Growth Monitor

13

Focus Points

� Introduction

� Market Overview

� Market Segmentation

� Industry Economics

� Investment Analysis

� Investment Themes

� Growth Monitor

� Scorecards

� Sector Scorecard

� Mergers & Acquisitions Analysis

� Venture Capital Scorecard

� Venture Opportunity Scorecard

� Question and Answers

14

Segment Opportunity Scorecard

Venture OpportunityMergers & Acquisitions Venture CapitalSector Score Card

Sector Average Company

Size

Number of Companies

Revenues ($ Million)

CAGR %

(2007 – 2012)

Sector Consolidation

Attractiveness to Venture

Capital Partners

Small < 15 25.3 Low-Medium High

Medium < 10 46.8 Medium–High Medium MSFA

Large < 5 132.9

15.0

High Low

Small < 30 19.8 Low–Medium High

Medium <10 56.9 Medium Medium MFSM

Large < 5 210.9

20.6

High Low

Small < 10 19.0 Low High

Medium <10 42.6 Medium–High Medium MSFA and MFSM

Large < 5 160.2

15.0 – 17.5

High Low

Source: Frost & Sullivan

15

Segment Growth – SFA & FSM

Source: Frost & Sullivan

Venture OpportunityMergers & Acquisitions Venture CapitalSector Score Card

0.0

200.0

400.0

600.0

800.0

1000.0

2007 2008 2009 2010 2011 2012

Years

Gro

wth

$ M

illio

n

SFA FSM

16

Venture OpportunityMergers & Acquisitions Venture CapitalSector Scorecard

Source: Frost & Sullivan

Mergers and Acquisition Analysis

1005.3949.05,000.0Business

IntelligenceCOGNOSIBM12-Nov-07

1005.078.8394.0Business Analytics

Visual Sciences

Omniture Inc

25-Oct-07

1005.41,250.06,780.0Enterprise

Software

Business

Objects

SA

SAP AG7-Oct-07

%OwnedAfter

Transaction

Revenue Multiple

Target Revenue ($ Million)

Deal Size

($ Million)

Business Acquired

Target Company

Acquiring Company

Date Announced

17

Venture OpportunityMergers & Acquisitions Venture CapitalSegment Opportunity

Source: Frost & Sullivan

Venture Capital ScorecardFinancial Analysis

C and D14.0 + 5.5Experienced

IT, Biotech,

and Clean

Energy

1985New

Enterprise Associates

17-Oct-

05, 07-

Feb-08

A and B2.0 + 5.75ExperiencedIT and

Healthcare 1978

Draper

Fisher Jurvetson

01-Aug-

04 and

01-Feb-

05

CRMSugar CRM

ExperiencedDiversified1998Thoma

Cressey

N/A0

ExperiencedIT1983Battery

VenturesSince

2003CRMOnyx

Funding Round

Funded Amount ($

Million)

Relevant Experience

of Management

Team

Field of Investment

Year of Establishment

Venture Partners

Date of Funding

SegmentCompany

18

Venture Opportunity Scorecard

Source: Frost & Sullivan

Venture OpportunityMergers & Acquisitions Venture CapitalSegment Opportunity

Financial Analysis

Medium-HighMediumMediumHigh86.5MSFA

&

MFSM

Dexterra

Medium-HighHighMediumHigh45.5

MSFA

&

MFSM

Antenna

Software

MediumMediumMediumMedium50MSFA

&

MFSM

Metrix

Overall Attractiveness

Clients and Reputation

Technology Innovation

Application Catering to Mobile Devices

Company’s Funding Till

Date($ Million)

SegmentCompany

19

Future Roadmap

• Increased adoption to mobility platform by SMB segment

• The roll out of Apple iPhone and Goggle Android phone

• Emerging Platforms and possible alliances in the future

• Mobile Applications vs. Mobile Network Service Providers vs. Mobile Device

Manufacturers vs. Internet Community vs. Customers

• Innovative, patentable and interoperable mobile application will attract future

investments.

20

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

21

For Additional Information

• To leave a comment, ask the analyst a question, or receive the

free audio segment that accompanies this presentation, please contact Stephanie Ochoa, Social Media Manager at (210) 247-

2421, via email, [email protected], or on Twitter at

http://twitter.com/stephanieochoa.