Sapphire Applications & Market 2015 Report by Yole Developpement

From Technologies to Market

© 2017

Photonique sur silicium: Tendances et perspectives de marché

Eric MOUNIER,

YOLE DEVELOPPEMENT

2

FIELDS OF EXPERTISE

Yole Développement’s 30 analysts operate in the following areas

MEMS & Sensors

LED

Compound

Semi.

Imaging

Photonics

MedTech

Manufacturing

Advanced

Packaging

Batteries / Energy

Management

Power

Electronics

Displays

RF

Devices &

Techno.

3

A GROUP OF COMPANIES

Market,

technology and

strategy

consulting

www.yole.fr

M&A operations

Due diligences

www.yolefinance.com

Innovation and business maker

www.bmorpho.com

Manufacturing costs analysis

Teardown and reverse engineering

Cost simulation tools

www.systemplus.fr

IP analysis

Patent assessment

www.knowmade.fr

5

SILICON PHOTONICS APPLICATIONS – EXAMPLES OF PLAYERS POSITIONING

HPCTelecom

(FTTH, metropolitan)Data Centres

Commercial

productsCommercial

products

High Volumes

Aeronautics/

aerospace

A 110-channel

wavelength selector

developed for the

European Space Agency

(VTT).

Low Volumes

Sensors Autonomous cars

Commercial

products

MIT Lidar using SiPhGenalyte bio sensor.

6

SILICON PHOTONICS LANDSCAPE (NON EXHAUSTIVE)

©2017 | www.yole.fr | Silicon Photonics 2017 report

University labs, research institutes, industrial companies … a whole eco system is setting up.

7

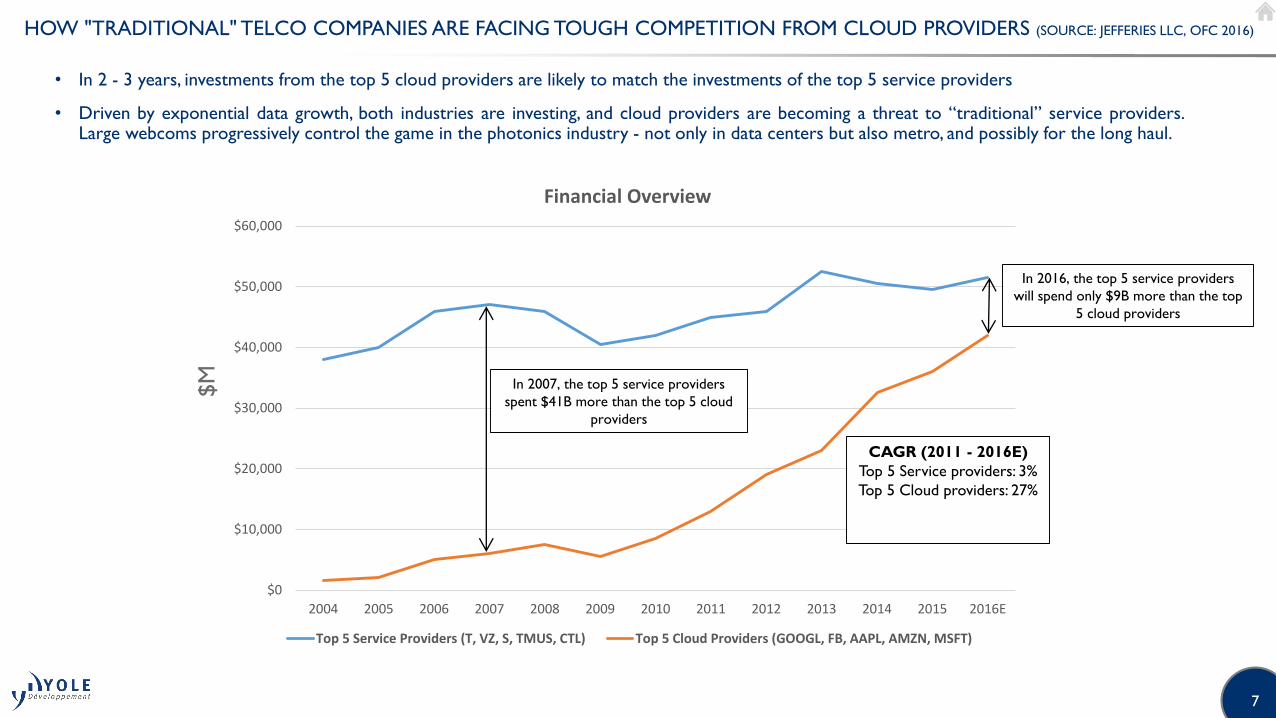

HOW "TRADITIONAL" TELCO COMPANIES ARE FACING TOUGH COMPETITION FROM CLOUD PROVIDERS (SOURCE: JEFFERIES LLC, OFC 2016)

• In 2 - 3 years, investments from the top 5 cloud providers are likely to match the investments of the top 5 service providers

• Driven by exponential data growth, both industries are investing, and cloud providers are becoming a threat to “traditional” service providers.Large webcoms progressively control the game in the photonics industry - not only in data centers but also metro, and possibly for the long haul.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

Financial Overview

Top 5 Service Providers (T, VZ, S, TMUS, CTL) Top 5 Cloud Providers (GOOGL, FB, AAPL, AMZN, MSFT)

In 2007, the top 5 service providers

spent $41B more than the top 5 cloud

providers

In 2016, the top 5 service providers

will spend only $9B more than the top

5 cloud providers

CAGR (2011 - 2016E)

Top 5 Service providers: 3%

Top 5 Cloud providers: 27%

$M

8

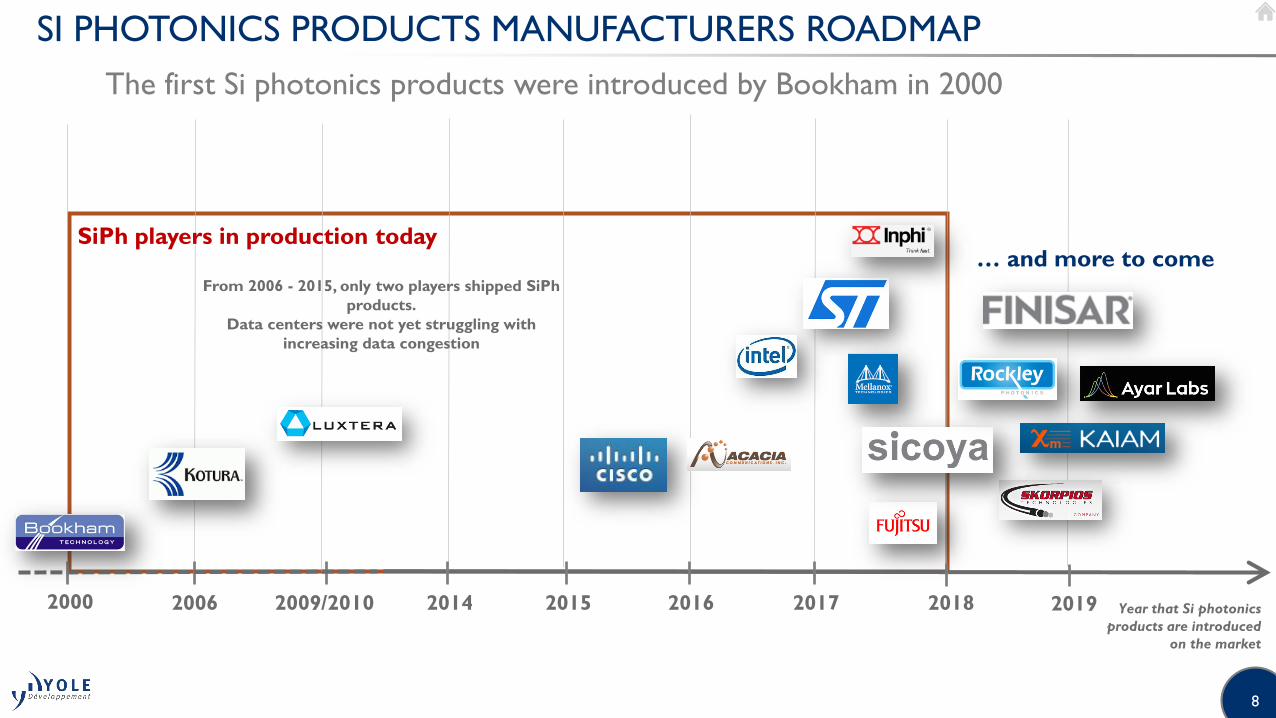

SI PHOTONICS PRODUCTS MANUFACTURERS ROADMAP

The first Si photonics products were introduced by Bookham in 2000

2006 2009/2010 2014 Year that Si photonics

products are introduced

on the market

2015 2016 2017 2018

From 2006 - 2015, only two players shipped SiPh

products.

Data centers were not yet struggling with

increasing data congestion

2000 2019

SiPh players in production today… and more to come

9

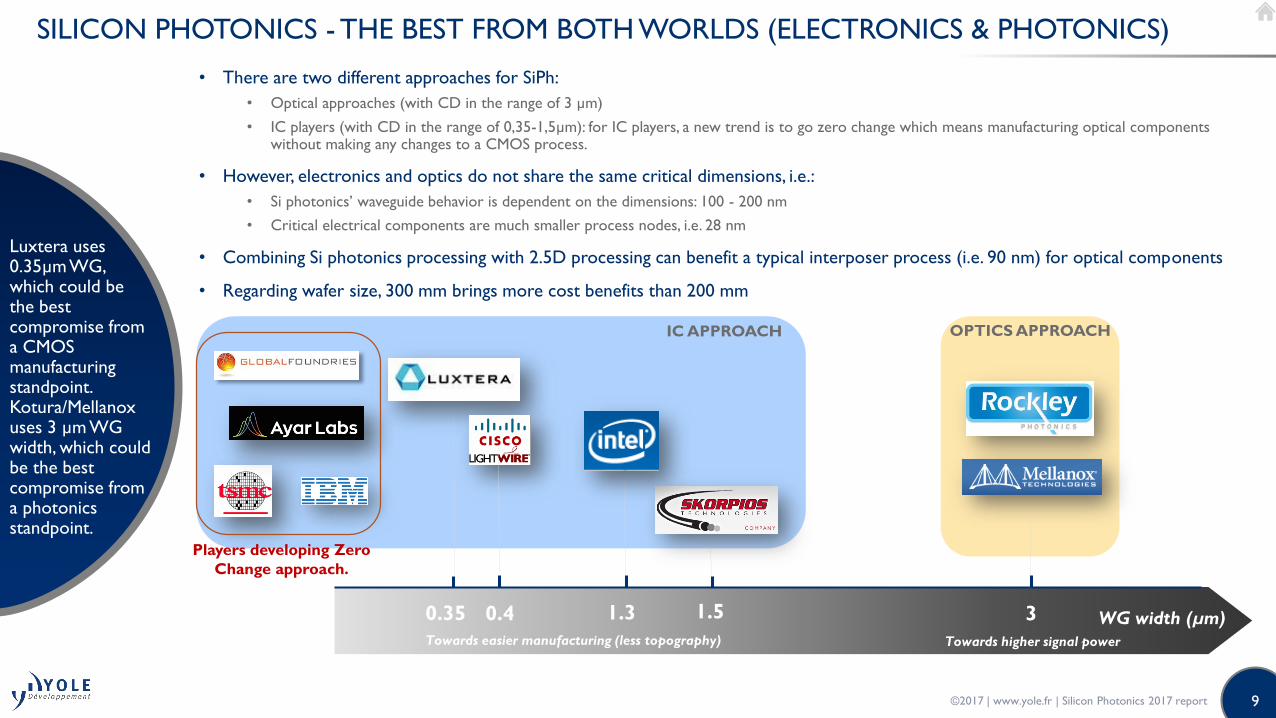

SILICON PHOTONICS - THE BEST FROM BOTH WORLDS (ELECTRONICS & PHOTONICS)

• There are two different approaches for SiPh:

• Optical approaches (with CD in the range of 3 µm)

• IC players (with CD in the range of 0,35-1,5µm): for IC players, a new trend is to go zero change which means manufacturing optical components without making any changes to a CMOS process.

• However, electronics and optics do not share the same critical dimensions, i.e.:

• Si photonics’ waveguide behavior is dependent on the dimensions: 100 - 200 nm

• Critical electrical components are much smaller process nodes, i.e. 28 nm

• Combining Si photonics processing with 2.5D processing can benefit a typical interposer process (i.e. 90 nm) for optical components

• Regarding wafer size, 300 mm brings more cost benefits than 200 mm

Luxtera uses 0.35µm WG, which could be the best compromise from a CMOS manufacturing standpoint. Kotura/Mellanoxuses 3 µm WG width, which could be the best compromise from a photonics standpoint.

©2017 | www.yole.fr | Silicon Photonics 2017 report

30.35 WG width (µm)1.3 1.50.4

Towards higher signal powerTowards easier manufacturing (less topography)

IC APPROACH OPTICS APPROACH

Players developing Zero

Change approach.

10

EXCITEMENT IS HIGH BUT IT IS STILL A MODEST MARKET

• Acacia capitalization exceeded $1.7B (Oct 2016)

• The total of private funding + acquisition total is more than $3B over past 5 years

• But the 2016 Silicon Photonics market value was less than $150M.

2017 Photonics & SiPh

transactions ~$3B

2017 SiPh revenues <

$150M

11

CONCLUSIONS

• Photonics technologies is today driven by GAFAMs.

• Today’s chip market value is still small, but more players are coming:

• After 16 years of development, Intel has successfully penetrated this application

• It shares the current market with Luxtera, leader number 1.

• New startups and more and more products reaching the market.

• Encouraging signs in terms of growing investments from the VC community.

• Si photonics is at the maturity level of the electronics industry in the 80-90s. There are still challenges

to overcome: laser source, packaging, design, supply chain, manufacturability.

• Besides Data Centres, some interesting applications could follow.