From burden to competitive advantageimages.forbes.com/forbesinsights/StudyPDFs/KPMG...Executive...

16

From burden to competitive advantage Regulatory change and transformation in financial services kpmg.com KPMG Transformation Survey

Transcript of From burden to competitive advantageimages.forbes.com/forbesinsights/StudyPDFs/KPMG...Executive...

From burden to competitive advantageRegulatory change and transformation in financial services

kpmg.com

KPMG Transformation Survey

The regulatory environment is rapidly

changing the financial services

industry, both in terms of how it

does business and how it manages

itself. Regulatory triggers are behind

industry consolidation on one hand

and the rising importance of risk

management within firms’

structures on the other. © 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Executive Summary

s KPMG discussed in its March 2014 report,

Evolving Bank Regulation, there is no going back

to the pre-crisis climate of lighter-touch bank

supervision. For financial firms, this is a double

edged sword as compliance with regulatory demands

is quite costly, and the new rules have constrained

revenue growth and profitability options.

The way to overcome these hurdles is to turn

regulatory compliance into a competitive advantage by

transforming the business model through a regulatory

lens. However, results from a recent KPMG survey

of more than 900 senior executives from U.S.-based

multinationals and asset managers revealed that a

large number of financial firms see the regulatory

environment as a burden on transformation. This report

will address steps that need to be taken to turn this

perceived burden into opportunity.

ContentsRegulatory Transformation Ubiquitous in Financial Services . . . . . . . .02

Financial Services Sector Largely Shaped by Regulatory Change . . . . . . . . .04

Overcoming Apprehensions. . . . . . . . . . .06

Toward Competitive Advantage . . . . . . . .07

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . .12

Contributors & Methodology . . . . . . . . . .13

A

93%

U.S.-based multinationals in some phase of changing their business models.

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Regulatory Change and Transformation in Financial Services / 01

Regulatory Transformation Ubiquitous in Financial Services

In the financial services sector, 97 percent of companies are at some stage of a business transformation (Fig. 1). “In this sector, a successful transformation

involves aligning new business models with a risk strategy that complies with the evolving regulatory environment,” says John Ivanoski, partner and national leader for U.S. Financial Services Regulatory Practice at KPMG. “In other words, financial services firms that align their strategies and operating models with the regulatory framework will gain a competitive advantage. Product lines and geographies can be designed to optimize capital and efficiencies.”

The biggest group of firms in the financial services sector (41%) is at the beginning stages of the transformation, either assessing the need for it or planning for it. This is the stage when the regulatory framework needs to be embedded in the operating model. “Substantial steps are being taken to address regulatory transformation in the financial sector,”

says Hugh Kelly, principal, Bank Regulatory Advisory, KPMG. “But it’s a work in progress.”

For companies in the financial services sector, the challenges of the current global regulatory environment are twofold. New regulations are expensive in terms of compliance, as companies need to transform data tracking and gathering systems, reporting functions and, in some cases, their organizational structures. At the same time, these regulations limit revenue growth and profitability by, for example, increasing capital and leverage ratio requirements, or limiting certain products or activities (proprietary trading).

“The entire business model [of the financial services firms] is being challenged right now. They’re having to hold higher capital than before, in a restrained economic environment, which has dampened their earnings and revenue potential,” says Pamela Martin, managing director in the Regulatory Risk Practice at KPMG and of KPMG’s Americas’ Financial

The entire business model is being challenged right now. They’re having to hold higher capital than before, in a restrained economic environment, which has dampened their earnings and revenue potential.

– Pamela Martin Managing Director, Regulatory Risk KPMG

“”

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

02 / Regulatory Change and Transformation in Financial Services

Regulatory Transformation Ubiquitous in Financial Services

Services Regulatory Center of Excellence (CoE). “Before the crisis, the regulatory community was of the mind that the industry had made great strides in improving risk management and being able to diversify risk. That proved not to be the case. [As a result] the regulatory pendulum is as far out as it could possibly go, and it’s likely to stay there. It’s not going to swing back anytime soon.”

Jim Low, Financial Services Audit Partner and Regulatory Center Leader at KPMG: “What we see today in financial services is going to be completely different from what is going to happen in the next couple years.”

Some estimates put the costs of Dodd-Frank compliance for the largest eight U.S. banks alone at up to $34 billion annually.1 The Volcker rule alone could collectively cost the 10 largest U.S. banks up to $10 billion annually.2

The sheer amount of regulations coming at financial services companies can be hard to grasp. It’s not only Dodd-Frank with its Volcker rule and living will plans, but also numerous new rules issued by the Basel Committee and the routine rulemaking of up to eight different federal regulators,3 as well as state regulators.

The regulatory environment is particularly volatile for the global companies that are trying to manage through the multitude of regulators in different jurisdictions, with huge divergences in each market. Understanding the similarities and dissimilarities of U.S. regulation versus other jurisdictions is key to creating a compliance process. Thomson Reuters tracked an average of 110 global regulatory changes every day in the third quarter of 2013, nearly double the daily updates the tool recorded during the same period in 2010. Through September, the number of tracked regulatory alerts has already reached an all-time high of 18,986, according to Thomson Reuters.

1 Standard and Poor’s: Two Years On, Reassessing The Cost Of Dodd-Frank For The Largest U.S. Banks. August 9, 2012.

2 Ibid.

3 Securities & Exchange Commission; Commodity Futures Trading Commission; Federal Reserve System; Federal Deposit Insurance Corporation; Financial Industry Regulatory Authority; Office of the Comptroller of the Currency; National Credit Union Administration; Consumer Financial Protection Bureau.

FIGURE 1. Where is your organization on the transformation continuum?

Does not add up to 100% due to rounding.

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Regulatory Change and Transformation in Financial Services / 03

Capital Markets

Insurance

Banking

Financial Services

All Industries 33%

41%

35%

49%

40%

29%

28%

40%

20%

22%

31%

28%

21%

30%

30%

4%

4%

8%

7%

Assessing/Planning Recently completed one or moreStarted Not considering

While the regulatory environment is perhaps the underlying force driving strategic thinking in the financial sector, industry

consolidation, competition, and customer demand are also primary triggers for transformation (Fig. 2).

The pace of industry consolidation is likely tied to the regulatory environment. As an example, smaller banks that can’t keep up with the pace and cost of regulations are looking to be acquired by larger organizations. While the number of banks in the U.S. has declined from over 9,000 a decade ago to 6,900 today,4 KPMG’s Low estimates that the number of banks may drop to 4,000 over the next decade.

“I can’t think of any companies that wouldn’t say that regulatory credibility, which includes compliance and governance, is a major factor in their strategic planning,” says Kelly. “Achieving that credibility has an impact on their ability to grow. It affects every aspect of their business.”

Global footprint, which is among the top triggers for transformation in the capital markets sector, is also affected by the regulatory environment. Current regulatory changes are leading to subsidiarization. Whereas an investment bank in the past

could have had a single model around the world, it is now breaking up the organizations into subsidiaries where only U.S. customers deal with the U.S. part of that bank. Such a structure requires creating separate back offices, thereby increasing expenses. This, in turn, leads to the reevaluation of a geographic footprint.

The regulatory climate is also changing how companies think about managing themselves. Banks have traditionally managed themselves by lines of business and by geography. Due to the current regulatory environment, they are now also finding it necessary to manage on the basis of their legal entity structure. This is proving quite complex as many large firms have hundreds, if not thousands, of legal entities worldwide.

Balancing growth with shrinking budgets and increased efficiencies, among the top transformation triggers in the financial services sector, is also tied to the regulatory environment. As firms attempt to return to the profitability levels that preceded the financial crisis, they are rethinking their markets and products in the light of new regulatory requirements that put limits on the use of capital.

FIGURE 2. What are the primary triggers for transformation

Financial Services Sector Largely Shaped by Regulatory Change

4 http://www.fdic.gov/bank/statistical/stats/2013sep/industry.pdf

Domestic competitors

Industry consolidation

Customer demandIncreased global footprint

Changes in technology Balance growth with shrinking budgets and increased efficiencies

33%

31%

35%

31%

29%

39%

30%

30%

36%

Banking Capital Markets Insurance

Does not add up to 100% due to rounding.

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

04 / Regulatory Change and Transformation in Financial Services

I can’t think of any companies that wouldn’t say that regulatory credibility, which includes compliance and governance, is a major factor in their strategic planning.

– Hugh Kelly Principal, Bank Regulatory Advisory KPMG

“”

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Regulatory Change and Transformation in Financial Services / 05

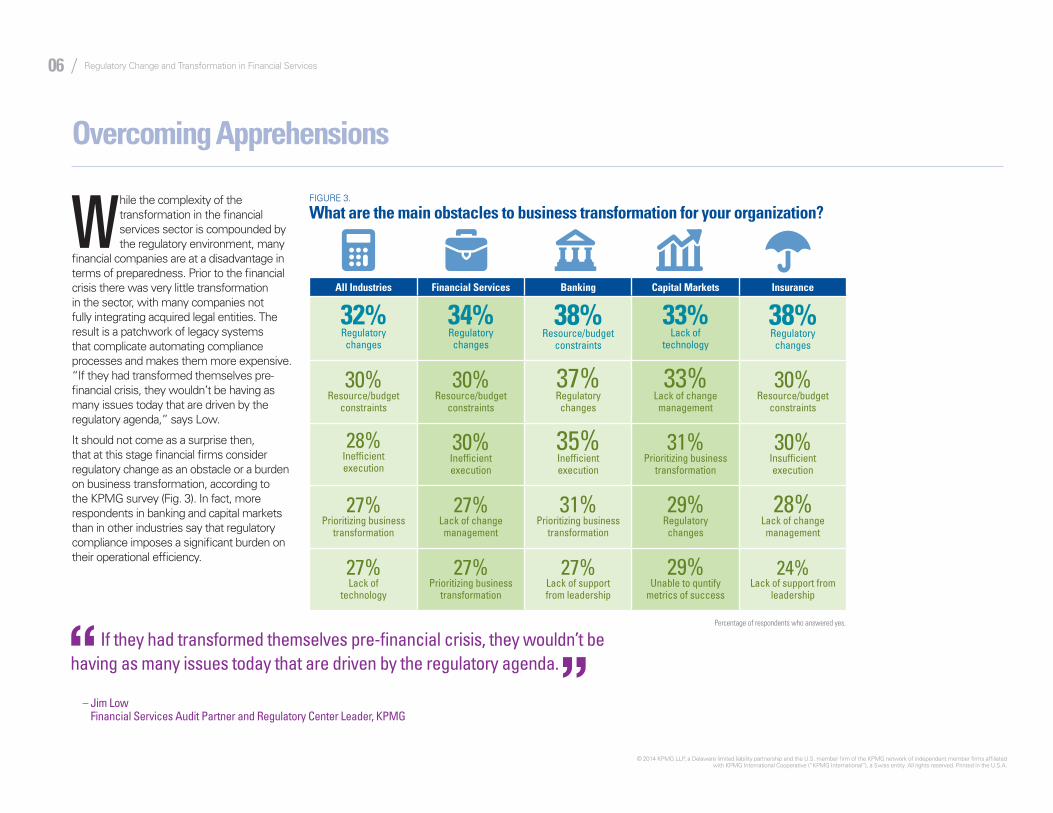

Overcoming Apprehensions

If they had transformed themselves pre-financial crisis, they wouldn’t be having as many issues today that are driven by the regulatory agenda.

– Jim Low Financial Services Audit Partner and Regulatory Center Leader, KPMG

“ ”

FIGURE 3. What are the main obstacles to business transformation for your organization?W

hile the complexity of the transformation in the financial services sector is compounded by the regulatory environment, many

financial companies are at a disadvantage in terms of preparedness. Prior to the financial crisis there was very little transformation in the sector, with many companies not fully integrating acquired legal entities. The result is a patchwork of legacy systems that complicate automating compliance processes and makes them more expensive. “If they had transformed themselves pre-financial crisis, they wouldn’t be having as many issues today that are driven by the regulatory agenda,” says Low.

It should not come as a surprise then, that at this stage financial firms consider regulatory change as an obstacle or a burden on business transformation, according to the KPMG survey (Fig. 3). In fact, more respondents in banking and capital markets than in other industries say that regulatory compliance imposes a significant burden on their operational efficiency.

All Industries Financial Services Banking Capital Markets Insurance

32% Regulatory changes

34% Regulatory changes

38% Resource/budget

constraints

33% Lack of

technology

38% Regulatory changes

30% Resource/budget

constraints

30% Resource/budget

constraints

37% Regulatory changes

33% Lack of change management

30% Resource/budget

constraints

28% Inefficient execution

30% Inefficient execution

35% Inefficient execution

31% Prioritizing business

transformation

30% Insufficient execution

27% Prioritizing business

transformation

27% Lack of change management

31% Prioritizing business

transformation

29% Regulatory changes

28% Lack of change management

27% Lack of

technology

27% Prioritizing business

transformation

27% Lack of support from leadership

29% Unable to quntify

metrics of success

24% Lack of support from

leadership

Percentage of respondents who answered yes.

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

06 / Regulatory Change and Transformation in Financial Services

Toward Competitive Advantage

FIGURE 4. How is transformation defined in your organization?

TARGET OPERATING MODEL

One way to achieve a successful regulatory transformation is by applying KPMG’s Target Operating Model methodology (TOM). TOM lies at the intersection of strategic development and tactical enablement. It looks at the direction where the organization is going and the most effective infrastructure to get it there. It links the “what” with the “how.” TOM is flexible and can be applied either to a regulatory-based transformation, in which the regulatory environment is a primary trigger, or incorporate regulatory changes into another type of transformation (e.g., technology driven).

TOM works for any type of transformation, be it at a business level, an organizational level, or a specific functional area, depending on the issues the organization is trying to address. It is thus applicable to each of the transformation types. The regulatory environment can influence how quickly companies must act, sometimes forcing them to act faster than they may be prepared to and to employ shorter-term solutions to meet compliance deadlines.

The KPMG survey reveals that the majority of financial firms take a strategic approach to transformation by continually aligning their business/

operating models with strategy (52%); the rest are split between those who view transformation as a wholesale turnaround that leads to an overhaul of the business model (enterprise transformation, 21%)

and those who adopt a narrower view, limiting themselves to transforming specific processes, functions, or areas (Fig. 4).

The capital markets sector seems to have a higher-than-average propensity for the wholesale type of transformation, with 27% of survey respondents from this sector selecting this type of transformation.

18%

17%

14%

51%

21%

16%

10%

52%

21%13%

6%

58%

27%

20%

12%

41%

16%

14%

12%

58%

All Industries Financial Services Banking Capital Markets Insurance

Continuous aligning of business/operating models with strategyEnterprise transformation Localized projects Continuously evolving specific areas/processes

Does not add up to 100% due to rounding.

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Regulatory Change and Transformation in Financial Services / 07

STEP ONE: Aligning regulatory transformation with company culture

To be successful, any transformation, and especially any regulatory transformation, needs to be aligned with company culture, be sponsored by all the right stakeholders, and be strengthened by the “tone from the top.” These elements are especially important in the case of regulatory transformation because some new stakeholders, such as Risk and/or compliance executives, have—or should have—bigger roles in the transformation. They may not traditionally have had a seat at the table at other types of business transformations, and their authority helps to smooth the path to acceptance of new roles and spheres of influence.

Pamela Martin believes that financial services firms are in need of a paradigm shift in governance. “One of the key lessons learned from the crisis was that the risk management practices of the financial services industry were too weak, and the regulatory community thinks that they remain weak. A key transformation for the financial services industry would be for everyone at the firm to be responsible for risk management. Not just the risk management group, but every single person at the firm.”

For such a transformation to stick, everybody needs to be on board, starting with the CEO. “Having a successful interaction of risk and compliance units with other units during transformation comes down to the culture and how the organization deals with change,” says KPMG’s Ivanoski.

KPMG’s research reveals that top-down corporate cultures are better suited for business transformations than overly decentralized companies, and that silos are an impediment to business transformation.

In this sense, financial services companies are well positioned for transformation. The KPMG survey reveals that the financial services sector favors using executive committees to prioritize business transformation initiatives, while other industries rely more on a combination of executive committees and working teams. Also, the financial services sector seems more vigilant about monitoring its operating model versus business strategy (e.g., in banking it’s done on a quarterly basis, according to 54 percent of survey respondents, as compared with 34 percent in other industries). ➝

One of the key lessons learned from the crisis was that the risk management practices of the financial services industry were too weak, and the regulatory community thinks that they remain weak. A key transformation for the financial services industry would be for everyone at the firm to be responsible for risk management. Not just the risk management group, but every single person at the firm.

– Pamela Martin Managing Director, Regulatory Risk KPMG

“

”

Toward Competitive Advantage (cont.)

To achieve a successful regulatory transformation there are some important steps that need to be taken:

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

08 / Regulatory Change and Transformation in Financial Services

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Regulatory Change and Transformation in Financial Services / 09

STEP TWO: Establishing regulatory change expectations and standards

Financial services organizations need to establish mechanisms to track all the regulation that affects them and the products they apply to —whether current or under development. KPMG’s Low usually starts by asking clients, “What’s the mechanism by which you’re tracking all the regulation that impacts you? And what about also tracking which products or services they apply to?” The answer he often hears is, “I don’t know.”

Currently, there is no consistent process for tracking regulations. Companies use law firms, in-house legal counsel or consultants to help track it. While bigger organizations have some system in place, smaller ones may not even realize that they are affected, which will lead to issues with regulators down the road.

Toward Competitive Advantage (cont.)

STEP ONE, continued

More respondents than on average believe that their organization’s governance supports business transformation efforts.

However, the financial services sector lags somewhat in terms of having a formal process for prioritizing business transformation initiatives. Having a formal process is correlated with being active in transformation. Fifty-five percent of respondents from all industries say they have a formal process, and just 50 percent from financial services said the same.

In this environment, where there’s pressure on having growth and making sure that costs are managed and optimized, linking how you’re addressing regulatory issues along with the business strategy is incredibly important. That is a differentiator for the companies that get transformation right.

– John Ivanoski Partner and National Leader, U.S. Financial Services Regulatory Practice, KPMG

“

”© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

STEP THREE: Establishing tailored processes for collecting valid information

For many firms, collecting, validating, and reporting information is a manual exercise, at least in year one and two following the implementation of new rules. Such manual processes are susceptible to errors. Automating data gathering, validation, and reporting processes not only reduces risk and improves efficiencies from a regulatory perspective, it also complements business models by keeping compliance cost-effective.

KPMG’s Ivanoski sums up with the big-picture view: “In this environment, where there’s pressure on having growth and making sure that costs are managed and optimized, linking how you’re addressing regulatory issues along with the business strategy is incredibly important. That is a differentiator for the companies that get transformation right.”

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Regulatory Change and Transformation in Financial Services / 11

For companies in the financial services sector, the challenges of the current global regulatory environment are twofold: Regulations are expensive to implement, and they can limit revenue growth and profitability. Thus, to gain competitive advantage through a transformation, financial services firms need to design

strategy and an operating model based on a regulatory framework by:

Recognizing that the regulatory framework is not only a trigger for regulatory transformation, but also underlies transformations aimed at industry consolidation, impacting global footprint and increasing efficiency and profitability.

Embedding the regulatory framework in the operating model early on, when possible, at the beginning stages of transformation. For best results, the regulatory framework should be considered while assessing the need for transformation or planning it.

Empowering compliance and risk executives in the process of transformation, and securing companywide sponsorship for consideration of regulatory issues. The tone from the top should guide every single person in the organization to be conscious of risk management for both compliance and business purposes.

Establishing a system to track applicable regulations and gather data for compliance, and gaining an understanding of how to turn regulations into a competitive advantage.

More information about the current regulatory environment and the key lessons banks need to understand and succeed in this environment is available in KPMG’s March 2014 report, Evolving Bank Regulation.

Conclusion

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

12 / Regulatory Change and Transformation in Financial Services

ContributorsKPMG would like to thank the following executives for sharing their time and expertise:

Robert P. Fisher, Regulatory Risk Partner, KPMG Phone: 804-782-4226 [email protected]

John M. Ivanoski, Partner and National Leader for U.S. Financial Services Regulatory Practice, KPMG Phone: 212-954-2484 [email protected]

Hugh C. Kelly, Principal, Bank Regulatory Advisory, KPMG Phone: 202-533-5200 [email protected]

Jim Low, Financial Services Audit Partner and Regulatory Center Leader, KPMG Phone: 212-872-3205 [email protected]

Pamela A. Martin, Managing Director, Regulatory Risk Practice and Americas’ Financial Services Regulatory Center of Excellence (CoE), KPMG Phone: 202-533-3070 [email protected]

MethodologyThis report is based on a survey of 910 executives at U.S.-based multinationals and banking or asset management firms conducted by Forbes Insights in June and July of 2013. Executives were evenly split among 13 industries/sectors. Out of 709 corporations, 90% of executives came from companies with revenues over $1 billion. Out of 201 banking or asset management firms, all had assets under management of at least $5 billion. Sixty-seven percent of respondents were C-level executives, and the rest were managing director or above. They represented all major corporate functions.

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

Regulatory Change and Transformation in Financial Services / 13

© 2014 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

The information contained herein is of general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Certain of the Advisory services described herein are not permissible to KPMG audit clients and their affiliates.

The views and opinions from the survey findings are those of the survey respondents and do not necessarily represent the views and opinions of KPMG LLP.

Stephen G. Hasty, Jr. Partner, U.S. Innovation Leader for Advisory

Phone: 704-371-5234 [email protected]

Robert T. Vanderwerf Principal, U.S. Transformation Strategy Leader

Phone: 949-885-5580 [email protected]

Brad Sprong Office Managing Partner and Tax Transformation Partner

Phone: 816-802-5270 [email protected]

Mitchell L. Siegel Principal, U.S. Financial Services Transformation Leader

Phone: 678-592-3471 [email protected]

Todd Lohr Managing Director, U.S. Transformation Enablement Leader

Phone: 215-300-4600 [email protected]

Stephen T. Hajdukovic Audit Partner

Phone: 312-665-2415 [email protected]

For further information about this survey, and how KPMG can help your business, please contact:

Kenneth E. Albertazzi Principal, Regulatory Change Management

Phone: 212-954-4904 [email protected]

Greg Matthews Managing Director, Regulatory Change Management

Phone: 212-954-7784 [email protected]