From big bang to a galaxy of stars - alfi.lu · 10 BIG BANG TO GALAXY OF STARS “Ucits gave new...

72

From big bang to a galaxy of stars An assessment of Ucits after 30 years of evolution 30

Transcript of From big bang to a galaxy of stars - alfi.lu · 10 BIG BANG TO GALAXY OF STARS “Ucits gave new...

From big bang to a galaxy of stars An assessment of Ucits after 30 years of evolution

30

Important notice

This document was produced by, and the opinions expressed are those of, Broadridge Analytics Solutions Ltd (BASL), as of the date of writing. It has been prepared solely for information purposes and for the use of BASL’s client. The information and analysis contained in this publication have been compiled or arrived at from sources believed to be reliable but BASL cannot guarantee their accuracy or interpretation. This document does not constitute any kind of advice including investment advice and should not be acted on as such. BASL does not accept liability for any loss arising from any use of such publication. This publication is not intended to be a substitute for detailed research or the exercise of professional judgement.

Copyright © 2018 Broadridge Analytics Solutions Ltd

Published by Broadridge Analytics Solutions Ltd

Suite 501 Salisbury House

London Wall

London EC2M 5QQ

All rights reserved. No part of this publication may be reproduced, stored in any

retrieval system, or transmitted in any form or by any means, electronic, mechani-

cal, photocopying, recording or otherwise, without the prior permission of the

publishers.

Foreword Denise Voss, Chairman of ALFI

Thirty years ago, few would have foreseen the phenomenal success that Europe’s Ucits has become. ‘Undertakings for Collective Investment in Transferable Securities’ was an unlikely candidate to be a brand in its own

right, however today it is one of the EU’s most recognised financial exports, held by investors resident in over 70 countries around the globe. As the premier global investment fund, nearly two out of three Ucits distributed on a cross-border basis are from Luxembourg, and assets under management in Luxembourg Ucits continue to grow, recently reaching a new record of €3.6trn. We expect this trend to continue given the sound regulatory framework and reputation of Ucits, and the depth of global capability embedded in the structure.

All is not rosy, however. A new technological world faces the industry; savers who are looking for engaging, easy to use, customisable and, crucially, mobile solutions. Fund industry actors must now appeal to this demographic group. But, to make investing ‘on the go’ successful, they must also contribute to developing the sound financial knowledge these savers need to make smart choices with or without financial advice. This report highlights the opportunity but investor education is a critical component. ALFI’s recent relaunch of www.understandinginvesting.org, reflects our belief that investor education is essential both for the economic well-being of individuals and the global economy.

Internationally, ALFI is as active as ever with an intense promotional agenda to showcase the Grand Duchy’s investment fund ecosystem. In Latin America, Luxembourg Ucits are now among the preferred investment solutions for local pension funds and in Asia, we will continue to nurture the close relationships we maintain with the many fund markets in the region.

For 30 years ALFI has been committed to advancing Luxembourg’s position as the international fund centre of reference. We now look forward to another 30 years of commitment to achieving the full potential of Luxembourg Ucits and other funds in serving the financial health of investors and the economy.

Introduction Diana Mackay

The Big Bang for asset managers occurred 30 years ago when the European Parliament passed a directive giving Undertakings for Collective Investments in Transferable Securities the passport to access all retail

investors in what was then known as the European Community. This strange beast, now more commonly known as the Ucits Directive, triggered a period of explosive growth, turning an industry that was nascent in some countries and non-existent in others into a global brand boasting fund assets of nearly €10trn. The Big Bang caused a collection of just 5,500 funds to explode into a universe of 32,000 stars, many with sales appeal in markets beyond the gaze of the European rule makers.

Luxembourg was the first European country to seize the opportunity and the first to implement the Directive in 1988. And in this year that saw the birth of Alfi, action was taken that culminated in the smallest member of the European Community becoming the largest domicile for European funds, and the beating heart of the global fund market. European Ucits have become an accepted regulatory standard for retail funds in markets all over the world. They are an important export story with non-European markets accounting for 24% of Ucits’ assets. In terms of net sales in 2017, their share was even higher at 31%.

The 30-year history of Ucits has sometimes seemed a crooked path but proof of its resilience is clear from its ability to survive and thrive through market corrections and serious financial storms. I am privileged to have been in a position to track this regulatory success from its birth, and to have witnessed, and been able to measure, the extent of its global reach. This report represents the accumulated wisdom and data of the many stakeholders that have contributed to the past growth of Ucits. It also sets the scene for those that will guide its health for investors in the next thirty years.

5

Contents

Foreword 3

Introduction 4

Executive summary 6

Route to the top – a short history of Ucits 8

1 Three decades of exploration 11

2 European constellation 23

3 Into the wider universe 35

4 Distribution power 49

5 Future horizons 59

Appendices

1 Contributors & acknowledgements 67

2 Notes to sources 68

Executive summary

■ Ucits assets have the potential to grow at a compound rate of 5% in the next three decades: This growth rate would quadruple their asset base to over €42trn by the year 2048. This model suggests that average annual net sales flows would rise from €201bn in 2017 to €860bn in thirty years.

■ Consolidation may lead to a contraction in the number of Ucits available in the next 30 years. At the current rate of decline Ucits will number 17,500 in 2048 but their average size will be €2.4bn.

■ The Ucits Directive gave investment funds regulatory credibility: Its launch made offshore funds acceptable vehicles for retail investors thereby kick starting a period of explosive growth that took assets in long-term Ucits from €300bn to nearly €10trn in their first three decades of life. AIFMD has added a further €6trn of assets.

■ Luxembourg’s decision to be the first country to implement Ucits set the Grand Duchy on the fast track in attracting groups looking for a suitable domicile for their cross-border initiatives. Luxembourg now houses 36% of assets invested in Ucits.

■ In its brief history Ucits has proved resilient to market crises: Ucits has enjoyed periods of strong market growth and endured two significant crashes. Each market crisis has ultimately resulted in new investors appreciating the regulatory benefits of the structure.

■ Cross-border distribution is now no longer a dream but an integral feature of the regime: Pure cross-border groups are now amongst Europe’s ten largest asset management brands. Cross-border groups now account for 51% of all European long-term fund assets.

■ Ucits has made Europe a honey pot for fund groups worldwide: Groups from EU countries manage 56% of assets with US groups accounting for 30%.

6 B I G B A N G T O G A L A X Y O F S T A R S

■ Cross-border groups source 77% of their assets from Europe: Within this European portion, five countries account for 70% of assets. Italy has been the most successful market for these groups, followed by Switzerland and Germany.

■ Although designed for European investors Ucits has also proved to be a successful export: Asian markets account for 13% of cross-border assets, with Latin American markets contributing 3%. Hong Kong represents the largest market for Ucits in Asia, followed by Taiwan and Singapore.

■ China is seen to be the big prize for foreign managers: Few groups, however, have managed to compete with the local players for assets that remain focussed on domestic strategies. Plans to lift capital controls and grow third pillar pension provision could provide opportunity for the future.

■ Despite its success, it has been tough for pure-play cross-border groups to gather net new money: The average group has generated just €1bn of annual net sales from Europe and to achieve this each group has had to generate around €12bn of gross sales.

■ Mifid 2 has been a game changer disrupting the traditional value chain: The impact has been increased transparency and pricing pressure, leading to a new focus on low-cost passives. The wealth management segment, particularly those that were fee-based are least affected. They represent 43% of the European asset pool that is accessible to third party providers.

■ The CMU and local initiatives to enhance long term savings to meet severe demographic challenges will encourage future growth in Europe: Outside Europe regulators are likely to wish to protect their own markets but the Ucits brand means that the Ucits structure is most likely to be the adopted vehicle.

E X E C U T I V E S U M M A R Y 7

8 B I G B A N G T O G A L A X Y O F S T A R S

Decade 32007

2017

Route to the top A short history of Ucits

€1.8trn

1988

1987

€6.1trn

€9.7trn

2001

Global financial crisis

2007-2008

2011

Luxembourgbecomes first

country to implement

Ucits

Birth of Ucits

Ucits 3 adopted

Dotcom crash

Error 404

1997-2000

2002

Ucits AUM by

year

2004

new 10

countries join the EU

Decade 21997

Decade 1

1987

Ucits 4 & AIFMD adopted

The

is adopted

E U R O

2013

Taper tantrum

Ucits 5 adopted

2016

T H R E E D E C A D E S O F G R O W T H 9

Decade 32007

2017

Route to the top A short history of Ucits

€1.8trn

1988

1987

€6.1trn

€9.7trn

2001

Global financial crisis

2007-2008

2011

Luxembourgbecomes first

country to implement

Ucits

Birth of Ucits

Ucits 3 adopted

Dotcom crash

Error 404

1997-2000

2002

Ucits AUM by

year

2004

new 10

countries join the EU

Decade 21997

Decade 1

1987

Ucits 4 & AIFMD adopted

The

is adopted

E U R O

2013

Taper tantrum

Ucits 5 adopted

2016

10 B I G B A N G T O G A L A X Y O F S T A R S

“ Ucits gave new life to Luxembourg but the

relationship has been symbiotic and ...

Luxembourg has breathed new life into Ucits.

By providing a fund centre that is dedicated

to the asset management industry it has

offered a home that is ... attractive to those

looking to develop a long-term presence in the

European savings’ market. This is at the root

of Luxembourg’s success but it is also a critical

factor in the evolution of Ucits and the single

market dream”— Symbiosis in the Evolution of Ucits, Lipper, 2008

T H R E E D E C A D E S O F G R O W T H 11

1 Three decades of exploration

The stated goal of the European policy machine in launching Ucits was to create a passporting structure for fund sales within the European Community. Thus a fund legally created in one European domicile, assuming it met specified criteria, could be registered for sale in another. The limited ambitions of the European Commission at the time was the creation of a ‘level playing field’ for funds across Europe, but it established Europe as the global hub for fund investment and opened a door for retail savers to access the services of expert portfolio managers regardless of their location.

Prior to the Ucits Directive, the concept of cross-border business in the retail world was more or less non-existent, at least in Continental Europe. There was some interaction between Belgian investors buying coupon funds

based in Luxembourg but it was really only in the UK that cross-border business thrived and this was in the form of so-called offshore activity. For much of the 1970s and 1980s the offshore market was largely the province of British fund managers offering offshore funds to domestic investors, expatriates and other high net worth ‘third country’ nationals through low-cost tax centres in the Channel Islands, the Caribbean, Switzerland and Hong Kong. In many Continental European markets the concept of ‘offshore’ was decidedly negative and, indeed, until the mid-1980’s French investors were restricted from investing abroad. Investment in foreign funds was regarded as dangerous.

Decade 1: pan-European expansion

The Ucits Directive changed all this by giving funds, regardless of their domicile, regulatory credibility. In so doing it kick-started three decades of remarkable expansion of long-term investment for retail savers. Its development in the first decade was initially slow and in some ways unexpected. A single market of funds

11

12 B I G B A N G T O G A L A X Y O F S T A R S

that was agnostic to fund domicile and the residence of the end investor was a laudable dream but initial practicalities and market preferences made complete freedom of movement unrealistic. Luxembourg’s move to become the first country to implement the Directive paved the way for this central, multi-lingual private banking centre to become a host domicile to the early movers looking to take advantage of the opportunities that Ucits presented.

Luxembourg takes the lead

Luxembourg’s early implementation of Ucits in March 1988 put it more than a year ahead of Dublin, which formed its International Financial Services Centre and implemented the Directive in 1989. Five years later, about 75% of the 992 funds based in Luxembourg identified themselves as Ucits and were registered for sale in at least one other EC jurisdiction. Early implementation of the Directive in Luxembourg resulted in a wave of product launches there by the leading Continental European banks, thereby converting the country from a quiet banking backwater into a European fund centre with back office capabilities that enabled funds from any neighbouring nation to match the local offerings.

The historical importance of Ucits to Continental banks in this first phase of Ucits development cannot be overestimated. Belgium had historical ties with Luxembourg and the new regime further strengthened the ties. For other countries, the Grand Duchy offered the convenience of a single location with all the language and technical skills to establish funds that not only carried the imprimatur of the European Community, but also looked local. French and German banks could now use their extensive branch networks to market regulated savings products to retail investors alongside

their locally-based funds. For the Swiss, market access was the critical factor. Having voted against joining the European club, Luxembourg became a vital conduit for Swiss groups to access their private clients across Europe. The early cross-border pioneers also saw Luxembourg as a viable central hub from which they could more easily explore the Continental European markets, but in this first decade they were the minority.

0

2,0004,0006,0008,000

10,00012,00014,000

16,00018,00020,000

0

200400600800

1,0001,2001,400

1,6001,8002,000

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Fig 1.1: Growth of AUM (€bn) and # funds in 1st decade

Total net assets Lux AUM Number of funds

Source: Efama, Alfi, ICI

T H R E E D E C A D E S O F G R O W T H 13

Round-tripping

The first decade of Ucits was pan-European rather than cross-border in its orientation. It was an opportunity for the indigenous banks to move beyond their role as deposit-takers and, for the first time, flex their muscles in the more lucrative

Fig 2: Early advantages of Luxembourg for development of Ucits

Drivers of growth in initial adoption phase

Belgium

Strong historical and cultural ties with Luxembourg, and no local fund

infrastructure meant that Luxembourg Ucits filled an immediate demand

gap. Luxembourg funds offered a coupon allowing Belgian nationals

to manage complex inheritance taxes so the implementation of laws

enabling the launch of local Ucits meant a slow start for the domestic fund

industry.

Germany

Processing advantages – a fund based in Luxembourg could be launched

faster than an equivalent German-based fund. German groups discovered

the convenience and flexibility of being able to offer Luxembourg funds to

their local clients and owning a Luxembourg fund became fashionable!

SwitzerlandAn international client base and a position outside the EU made an

alternative home in Luxembourg an essential recourse for Swiss banks.

France

Luxembourg was less important to French providers, which thrived

on a large domestic market. Luxembourg Ucits offered no immediate

attraction to French investors over their local funds but a small number

of institutions found the large umbrella structures attractive for the

switching opportunities they allowed. Umbrella structures were not

available in France.

UK

For UK groups the Ucits opportunity was one of access to Continental

European investors but finding suitable distributors in these bank-

dominated countries proved challenging.

14 B I G B A N G T O G A L A X Y O F S T A R S

By 1993 round-trip

funds represented

58% of all

Luxembourg Ucits

provision of long-term savings products, which also introduced many to foreign exchange and other investment banking activities. These banks entered a pan-Europe phase of acquisition activity looking to develop equivalent domestic franchises in other European countries. For these organisations Luxembourg became a convenient domicile for funds destined for consumption by their home-market investors and insofar as they acquired or established entities in other countries, their aim was to manage local (or Luxembourg) funds for local investors.

The phrase ‘round-tripping’ was coined to describe the local sales focus of these early adopters of Ucits in Luxembourg. By the end of 1993 round-trip funds represented 58% of all Luxembourg Ucits. And, by linguistic extension the term ‘reverse round-trip’ also became a feature linked to funds that were launched in Luxembourg and notified for sale only in Luxembourg. These funds, predominately managed by German banks enabled clients to buy either Luxembourg or German funds through a single Luxembourg account. In this year more than half of all Luxembourg Ucits were sold into just one market. A mere 8% of Luxembourg-based Ucits were notified for sale in more than four markets and of all Ucits selling into this number of countries, Luxembourg Ucits accounted for 92%.

Decade 2: from boom to bust, and boom again

After a sluggish start the fund industry under the Ucits Directive boomed. By the end of its first decade the number of Ucits in Europe had exploded from 5,500 with €307bn of assets under management to over 17,000 with assets of €1.8trn1. The drivers were complex but essentially distilled into two areas:

▪ Interest rates reductions encouraging a long-term move out of cash and money market funds, into fixed income funds mainly investing in government bonds. Banks were the principle beneficiaries of this shift, which also kick-started the vibrant Italian fund industry.

▪ Rising appetite for equity funds, which culminated in the dot.com bubble of 1999 and, ultimately, in the crash that followed in 2000.

The dot.com bubble marked the end of the first decade for Ucits but also its first crisis of confidence. 1999 was the pivotal year when European investors piled into

1 Efama

T H R E E D E C A D E S O F G R O W T H 15

equity funds, specifically those investing in internet and technology stock. No pan-European sales data exists for this heady period but extrapolation from such data as was available at the time suggests that over €200bn of new money was invested in equity funds in 1999, with a further €143bn in 2000, of which €129bn was invested by Italians alone. The scale of this bubble can only really be appreciated by looking at subsequent equity flows, which have never since reached the 1999 volumes. Their best subsequent year was, in fact, 2017 when European funds registered €164bn of new money but, in contrast with 1999, this latest peak saw 65% of net inflow going into passively managed funds.

Shock waves from the dot.com crash

The crash came in the Spring of 2000 and with it collapsed the allfinanz ambitions of many European banks to dominate both the manufacture and distribution of funds. Their heavy involvement in encouraging savers into high-risk technology stocks, managed internally, rocked the confidence of their clients, many of whom saw the value of their holdings plummet by 50%-70%. On the plus side, they chose, or were persuaded to avoid, crystallising losses and although the new money tap was turned back to just a dribble, equity funds remained in positive territory until the financial crisis weighed in.

Source: Broadridge, latest data date – June 2018 Author estimates for 1999 and 2001 based on BVI and Assogestioni data for Germany and Italy.

(150)

(100)

(50)

0

50

100

150

200

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Fig 1.2: Net sales of Equity funds from dot.com bubble to current date

16 B I G B A N G T O G A L A X Y O F S T A R S

European expansion and new growth

Meanwhile, the newly-launched Eurozone in 2000, and the subsequent widening of the European Union to embrace many Eastern European nations in 2004 led, to a rapid expansion of interest in European and Eurozone stock funds. This time, though, it was the cross-border groups that were the main beneficiaries. Mainstream retail investors, the core constituents of the banks, remained on the sidelines nursing their tech-stock losses, but wealth managers and third party distributors in search of performance sought the investment skills on offer from the pure-play fund houses. This was also a period of open- or guided-

architecture growth when banks saw advantage in using third party manufacturers to offset earlier disappointment in their own equity skills. Many banks shifted their strategies from allfinanz to distribution and fund selection strength.

Ucits 3 and inclusion of derivatives as eligible assets

At the start of this second decade of Ucits evolution, the European Commission published its proposals for Ucits 3 (1998), having failed to get agreement for Ucits 2. Ucits 3 was adopted in 2001 and expanded the range of investments permitted by Ucits funds to money market funds and funds of funds. Critically, the list of eligible assets included, for the first time, certain derivatives and hedge fund strategies aimed at sophisticated investors. ‘Newcits’ became the buzz word for these strategies to distinguish them from traditional products, that were all subsumed under the Ucits 3 umbrella. On the plus side, retail investors gained access to some regulated hedge fund strategies and, of these, absolute return strategies have become the most prolific.

These initiatives reinvigorated Ucits and fund industry fortunes leaving the dot.com crash a memory that could quickly be forgotten. By 2005 net sales of long-term funds had risen to a new high point of €371bn with bond funds enjoying their best year on record. Rising interest rates put an end to the bond boom in 2006 but equities continued to shine until the first rumblings of the financial crisis slammed the door to the second decade of Ucits.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Fig 1.3: Growth of AUM (€bn) and # funds in 2nd decade

Total net assets Lux AUM Number of funds

Source: Efama, Alfi

T H R E E D E C A D E S O F G R O W T H 17

Decade 3: promises delivered or dashed?

The third decade of Ucits had an inauspicious start. With the financial markets seemingly spiralling out of control, investors sold out of every asset class with the sole exception of safe-haven money market funds. This was a year of unparalleled redemptions for long-term funds, which rose to €390bn by the year end. It was undoubtedly a painful period for fund groups but withdrawals in 2008 – the depth of the crisis – represented less than 10% of the €4.5trn then invested in funds. Crippled market performance, though, had a much greater impact on industry fortunes, wiping out more than a quarter of long-term fund assets.

Fears of the destruction of the Ucits brand and loss of trust amongst retail savers were rife. Ironically, though, although mainstream savers retreated to cash, others saw the benefits of the regulatory protection of Ucits and the period of pain was surprisingly brief. By 2010 assets had recovered to their 2007 peak and fund groups enjoyed two years of sales volumes that came close to €250bn a year. In a period of extraordinary distress that had many in the industry questioning how investor trust could be restored, some investors were benefiting from the unprecedented decline in market values. The regulatory protection offered by Ucits proved to be a draw for institutions and wealth managers who had previously viewed the vehicle as too expensive, at least for exposure in plain vanilla securities.

Post-Financial Crisis drivers of growth

The rebound could be distilled down to the following drivers:

▪ Record low interest rates, resulting from central bank policies to steer global economies from collapse.

“There is a high risk of investors losing confidence and the industry as a whole should be aware that the trust needed to build the culture of long-term savings, which is so indispensable to the future economic health of the European Community, may have been challenged.”

– John Baptiste de Franssu Building Long-Term Savings in Europe, 2009

18 B I G B A N G T O G A L A X Y O F S T A R S

▪ Wealth managers, quick to spot the capacity of emerging markets to recover earlier than the developed countries, and to take advantage of stock market rises fuelled by the proprietary trading that followed government quantitative easing strategies. Of €113bn that was redeemed from equities in 2008, €112bn returned in 2009.

▪ The chase for yield against the backdrop of low interest rates had the wealthy and some mainstream investors backing investment grade debt and other higher yielding bond funds.

▪ A new-found appreciation of the regulated status of Ucits, which compounded as Europe entered its debt crisis. Funds were seen to be safer than unregulated hedge funds and the ability to access hedge strategies in Ucits form seemed a better option for many. Meanwhile, interest rates were crumbling and cash deposits were vulnerable to being snatched by creditors in advance of a state bail out.

▪ Accommodative Central Bank policies in the form of quantitative easing created enormous opportunities for more sophisticated investors to front run the well-broadcast initiatives.

Expanding appetite and new opportunities

Amongst the wider retail franchise this was the decade of risk aversion and restraint. Fearful savers with the willing encouragement from their cash-strapped banks retreated to cash. Some banks sold off their asset management arms either willingly or under orders from European regulators – the price of rescue during the Eurozone credit crunch – leaving local and cross-border independents the space to innovate and expand.

In this decade of turmoil and opportunity the competitive landscape changed again, from one that was dominated by the large Continental

captive banks to one where independent houses, both local and cross-border, stepped into the spotlight. At the start of 2007 Europe’s ranking of largest managers of long-term funds was led by UBS and included just two cross-border groups. A decade later the number of pure-play cross-border groups had doubled, whilst those

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fig 1.4: Growth of AUM (€bn) and # funds in 3rd decade

Total net assets Lux AUM Number of funds

Source: Efama, Alfi

T H R E E D E C A D E S O F G R O W T H 19

with a mixed franchise had expanded. Importantly, BlackRock, powered by its ETF business, had leapfrogged bank and independent competitors alike to become Europe’s largest asset management brand.

Incorporating alternatives into the passporting regime

During this period Ucits 4 and 5 were implemented, further facilitating cross-border expansion with the introduction of the management group passport, the launch of the simplified prospectus (which became the Key Investor Information Document or Kiid), and provisions to encourage efficiencies through pooling of assets (via master feeder funds) and fund mergers. Finally, within Ucits 5 were numerous provisions to increase the security of the depositary provisions and implement a remuneration regime for key staff that aligned their interests more closely with investors. As well as enhancing existing Ucits provisions the European Parliament also approved a further important expansion of the passport to include a number of so-called alternative products in the form of the Alternative Investment Fund Manager’s Directive (AIFMD) in 2011.

Fig 1.5: Market leaders – Dec 2006 (€bn)

Name Provenance AUM

1 UBS AG CH/X-Border 179

2 Crédit Agricole FR 179

3 Unicredit IT 150

4 DWS DE/X-Border 130

5 Fidelity X-Border 114

6 AXA Group FR/X-Border 100

7 JPMorgan X-Border 95

8 Eurizon IT 89

9 Union DE 86

10 Allianz GI DE 83

Total AUM – Top 10 1,202

Total AUM – All groups 4,443

Market share of top 10 groups 27%

Fig 1.6: Market leaders – Dec 2016 (€bn)

Name Provenance AUM

1 BlackRock X-Border 519

2 UBS AG CH/X-Border 231

3 DWS DE/X-Border 226

4 Intesa SP IT 160

5 Amundi FR/X-Border 151

6 JPMorgan X-Border 144

7 Union DE 144

8 AXA FR/X-Border 142

9 Fidelity X-Border 139

10 Schroders X-Border 138

Total AUM – Top 10 1,994

Total AUM – All groups 7,559

Market share of top 10 groups 26%

Source: Broadridge. Note: Data excludes money market funds and funds of funds.

20 B I G B A N G T O G A L A X Y O F S T A R S

The new category of Alternative Investment Funds (AIFs) introduced a sizeable new segment of investment activity embracing closed-ended investment funds, private equity and venture capital funds, real estate funds and hedge funds. The European trade association, Efama, show assets of funds now categorised as AIFs to have had €1.9trn of assets in 2007. By the end of 2017, this volume had expanded to reach nearly €6trn of which the bulk (27%) was invested in multi-asset products.

Although still a junior partner to Ucits, their growth has once again proven the power of regulation in facilitating market expansion. Demand for alternative products is rising, particularly in the current more volatile market climate. However, there remains some suspicion of the complex structures involved in some products, particularly hedge funds. Increasingly, asset managers find easier acceptance if the strategy can be brought within a Ucits wrapper. Some selectors specifically

include only Ucits into their selection criteria because their target market effectively excludes AIFs under the Mifid 2 rules. This, of course, will act as a break on the appeal of AIFs because although many AIF products are of interest to selectors, such as private equity, they want these products within a Ucits wrapper.

Into the next decade

The decade that began in the depths of the global financial crisis ultimately resulted in an accelerated expansion of Ucits and a wider regulatory framework for alternatives. It also resulted in the realisation of the cross-border dream for those early pioneers that made use of the facilities offered by Luxembourg and Dublin to access the European markets with a single range of funds. By the beginning of the fourth decade of Ucits, assets under management were on the cusp of breaching the €10trn mark with AIFs adding a further €6trn to the universe. More than a third of funds domiciled in Europe are sourcing assets from multiple European and global markets and, of these, 64% are based in Luxembourg, and a further 25% in Dublin. Ironically, the decision made by the US regulators three decades ago to

0.01.02.03.04.05.06.07.08.09.0

10.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Fig 1.7: AUM in Ucits v AIFs (€trn)

Ucits AIFs

Source: Efama Fact Book 2018, Alfi

‘I’m seeing an increased focus on Ucits-compliant non-directional strategies, including long/short equity’Discretionary Portfolio Manager | Sweden

‘We only accept Ucits funds, no AIFs on our shortlist.’Retail bank | Austria

T H R E E D E C A D E S O F G R O W T H 21

forego reciprocal access for Ucits into the US and SEC-registered funds into Europe, resulted in Europe becoming the central hub of cross-border fund traffic, and Ucits becoming the commonly accepted regulatory standard for funds around the world.

This important footprint will bode well for Ucits in the coming decade as populations in many of the newer markets are encouraged by their governments to take on the mantle of pension provision. Regulators in most non-European countries will wish to build a local fund franchise but the regulatory structures they use are most likely to be based on Ucits, which will ultimately facilitate access for European Ucits when doors begin to open.

In Europe the next decade will see the launch of the Capital Markets Union, an EU initiative that could be as important to the future growth of Ucits as the original Directive. At the core of this action plan is a desire to increase investment and the choices available to retail and institutional investors. Ultimately, the EU is seeking to deepen the capital markets by migrating some of the vast pool of deposit savings into managed investments. This is a multi-tentacled initiative but over the next decade we can expect Ucits to be a key beneficiary.

Europe2018: 74%2013: 77%

North America2018: 4%2013: 5% Asia

2018: 12%2013: 11%

La�n America2018: 3%2013: 3%

Fig 1.8: Global appeal of cross-border funds, by region

Bubble size repre-sents fund market AUM

Propor�on of cross-border AUM by region, 2018 vs 2013, %.

MEA2018: 1%2013: 1%

Source: Broadridge

22 B I G B A N G T O G A L A X Y O F S T A R S

“ When we choose a provider, we look at

minimum fund sizes of at least €100m as a

rule of thumb to safeguard consistency.

We also need UCITS-compliant funds. ”— Insurance fund selector | Germany

E U R O P E A N C O N S T E L L A T I O N 23

2 European constellation

The Ucits Directive created the regulatory energy that sparked a spectacular growth of long-term savings through funds in Europe. From a near-standing start of €307bn, the European industry has exploded into a constellation of over 32,000 Ucits with assets of nearly €10trn in long-term funds1. Although in its initial development phase it was the local European industries that were powered up, as the new century dawned the dream of the cross-border passport became a visible reality. Cross-border funds2 now account for nearly a third of all long-term Ucits, and 51% of assets3. The bulk of this business is sourced from European investors but an unintended consequence of this regulatory initiative was its early acceptance by investors in wider global markets.

The intention of the original architects of Ucits was to create a harmonised landscape for marketing funds across Europe. Discussions of some wider reciprocal agreements between the US and Europe rumbled along in the

background during the early phase of Ucits’ inception but the idea of opening up the US market to funds domiciled in Europe, and visa versa, proved to be an industry fantasy that arose out of the optimistic naivety of business strategists looking at market opportunity with little understanding of local cultures, savings preferences and competitive forces. To American eyes at that time Europe was seen to be a huge opportunity. It was a single market with 360 million or so consumers – a third larger than the US – with savings predominately committed to cash deposits. This status quo has changed very little in the first 30 years of Ucits; 40% of European household savings remains in cash and deposits, according to Central Bank statistics, with just 11.4% committed to investment funds4.

1 Efama2 Defined by Broadridge as funds that source less than 80% of their assets from one single country. 3 Broadridge, long-term funds, excluding funds of funds, June 2018 4 Efama Factbook, 2018

23

24 B I G B A N G T O G A L A X Y O F S T A R S

With no reciprocal trade agreement forthcoming between Europe and the USA, any group wanting a stake in the Ucits opportunity was forced to establish funds in the European Union and although some US groups were already present, the launch of Ucits resulted in multiple waves of newcomers from the US and elsewhere, establishing funds in either Luxembourg and Dublin to take advantage of this unique passport. Today, asset managers from some 48 non-EU countries take advantage of the Ucits Directive by basing funds in the EU and, of these, groups with a US provenance have the largest presence with fund assets of nearly €3trn, or 30% of the

entire European Ucits total5. Similar proportions can be seen in Europe’s largest host domicile, Luxembourg. However, the presence of US groups in Europe’s second host centre, Dublin, is all-powerful. Here they account for 72% of Irish-domiciled assets.

Territorial expansion

Although the Ucits Directive promised the so-called single market for funds, the ability of a single family of funds to sell into multiple markets was slow to emerge. Indeed, the early cross-border pioneers found it hard to track down distributors that were willing to sell their funds. They were unknown entities and treated with suspicion; banks were a closed door and their all-embracing presence left little room for newcomers. In these early days (1994) just 269 funds were registered for sale in five countries or more6. Today, there are 12,607 cross-border funds, each one registered to sell in an average of just over eight countries7.

By the end of 2016 cross-border activity had reached a pivotal point in its gestation, with assets finally overtaking those of Europe’s domestic players. This trend continued in 2017 when the assets of cross-border groups accounted for 51% of long-term funds (Fig 2.2). The power of the Ucits franchise is even more obvious when looking at the average volume of assets in cross-border funds, compared with their domestic

5 Broadridge, data at 30 June 2018. Data excludes funds of funds to avoid double counting.6 Lipper Analytical Strategy Report – Cross-Border Marketing 19957 Global Fund Distribution 2018, Alfi, data sourced from Lipper and PWC

Australasia1%

Carribean0%

EU56%

LatAm0%

MEA1%

N America30%

Wider Europe12%

Fig 2.1: Share of assets by group provenance

Source: Broadridge

0

1,000

2,000

3,000

4,000

5,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Fig 2.2: Growth of Cross-Border Fund AUM (€bn)

Domestic Cross-border

Source: Broadridge

E U R O P E A N C O N S T E L L A T I O N 25

counterparts. This analysis (Fig 2.3) shows cross-border funds to have overtaken domestic funds in the aftermath of the dot.com bubble, highlighting one of many factors encouraging the growth of cross-border strategies over the last two decades.

Drivers of cross-border opportunities

The Ucits framework provided the structure for cross-border development, but it was external market drivers that created the opportunities. The most important of these were:

▪ Increased consumer scepticism in the allfinanz banking model following the bursting of the dot.com bubble. The consumer shock that came from overselling practices at that time led to greater retail appetite for product choice that went beyond the in-house range.

▪ Introduction of D2C supermarket platforms and discount brokerages in the late 1990s, that encouraged greater consumer awareness of the wider choices of products that were available. Fund performance data was embedded in these sites and enabled cross-border providers to profile the superior performance of relevant funds in a period of equity bull markets. Although none of these D2C providers became significant distributors, they nonetheless played an important educational role.

▪ The global financial crisis, which served to highlight the security of regulated products making them increasingly attractive to wealth advisers who previously regarded funds as an expensive option for exposure to securities that they could easily access directly. At a time when developed markets were sinking into oblivion, the search for uncorrelated options such as emerging markets and absolute return strategies, further enhanced the use of funds because they were cheaper to access in this form, and they were regulated.

▪ An institutional drift towards funds for the regulatory comfort they offered, supported by asset managers, which launched, in particular, tracker products for their clients. The most recent iteration of this development is the growth of fund activity from fiduciaries and institutional gatekeepers like Mercers who are now enabling institutions to access their advisory/asset allocation strategies via Ucits funds.

0

50

100

150

200

250

300

350

400

450

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Fig 2.3: Growth of ave fund AUM (€bn)

Domestic Cross-border

Source: Broadridge

26 B I G B A N G T O G A L A X Y O F S T A R S

▪ Communication and particularly the dissemination of information via the internet, which created greater visibility of funds from other markets that might not otherwise have been spotted. In this way sight of successful local funds from boutiques now creates external demand and encourages the managers of such funds to expand their franchise. The huge success of Carmignac’s Patrimoine fund in 2009-2010 is an example of this dynamic at play.

Sales expansion

Net sales totals over the same period show even more energy, in part from the steady influx of new players, but also from new investors – sophisticated and institutional – that increased their commitment to funds. Rising interest in ETFs, a switch away from plain vanilla funds towards more complex solutions, and the delivery of greater choice, has helped the cross-border segment to accelerate. The slower pace of development from domestic groups was really linked to the bank franchise, which

suffered more acutely from the financial crisis and, mirroring the risk aversion of their retail clients, took much longer to recover.

The game has changed in the last few years and banks are now looking to increase profitability rather than boost cash buffers. Their captive clients, weary of impoverished interest rates are ready to consider more lucrative savings options even with some risk attached. These local players have therefore begun to recover some market share. It is worth noting here the growing importance of local boutiques as contributors to the domestic sales totals in some markets. Their role remains small but they are increasingly in the sights of fund selectors in their countries of operation.

Global passport success

The Ucits success story and its rapidly expanding reach into multiple global markets can be mapped through the registrations that Ucits funds have achieved over the years. However, the real test of their accomplishment is in the assets derived from these countries. These assets are invested in European Ucits but are sourced from investors both within and beyond Europe. According to Broadridge SalesWatch1 data, based on data declared by 67 of Europe’s leading cross-border groups, just

(300)

(200)

(100)

0

100

200

300

400

500

600

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Fig 2.4: Net sales of Cross-Border v domestic funds (€bn)

Domestic Cross-border

Source: Broadridge

E U R O P E A N C O N S T E L L A T I O N 27

under a quarter of assets invested in their European Ucits are sourced from outside Europe, principally Asian and Latin American markets (see Chapter 3 for further details on these markets). The split of assets has changed very little over time although the overall volume of assets represented by the contributing groups have more than doubled since 2010. These groups registered assets of €2.6trn at the end of 2017.

Focus on Europe

Within Europe the asset split is weighted heavily towards five key markets, which represent 70% of the €1.9trn of assets booked by investors in Europe. The data set reveals assets sourced from nearly 40 countries in the wider European region, including Russia and Turkey. However, the majority of these markets are very small and only 14 contribute long-term assets of more than €10bn. Fig 2.6 illustrates the split and highlights those markets in which foreign or cross-border Ucits have enjoyed most traction. These are also the markets that have generated the largest sales volumes in recent years (see Market Dashboard below for a full profile of Europe’s top five markets).

With retail investor attention increasingly favouring products offered by the cross-border investment specialists, and more local players entering the cross-border arena, how successful have these expansionist strategies been in gathering new assets from European retail investors? Fig 2.4 shows a strong growth dynamic but this data also includes ETFs, Asian and other non-European inflows, as well net sales from institutions. A deep-dive into the sales activities of the Broadridge SalesWatch8 groups, which better reflect the appetite of third party retail buyers, reveals a more nuanced picture of a maturing industry where increasingly weighty gross sales volumes are necessary to maintain positive net sales traction. This is particularly the case for the largest and longest-standing cross-border groups that have built up sizeable pools of legacy assets that inevitably become vulnerable to redemption as investors shift

8 See Appendix 1 for detailed definition of this data

Asia-Pacific13%

Europe77%

LatAm3%

Other7%

Fig 2.5: Regional split of European Ucits by asset source

Source: Broadridge SalesWatch1 Data: Split based on assets of €2.6trn at 31 Dec 2017. Data excludes ETFs, Funds of Funds, SIFs and money market funds.

Italy23%

Switzerland17%

Germany12%

UK11%

Spain7%

Rest30%

Fig 2.6: Source of AUM from European investors in cross-border funds

Source: Broadridge SalesWatch1 Data: Split based on assets of €1.9trn at 31 Dec 2017. Data excludes ETFs, Funds of Funds, SIFs and money market funds.

28 B I G B A N G T O G A L A X Y O F S T A R S

their allocations in response to the changing waves of product demand. ETFs will be also a factor in the widening gap that has developed, almost uninterrupted, between gross and net sales totals since 2012. During this period, the steady take-up of ETFs, which predominately wear a Ucits hat, have eaten into the assets of certain core sectors, particularly in the equity arena.

The fact remains, though, that aspiring managers looking to penetrate the European markets, need to be aware that despite the large sales numbers that are thrown around in the public domain, the average pure-play cross-border group has historically generated

just under €1bn of annual net sales receipts from the European markets9. And, to achieve this volume, it was necessary for each group to achieve around €12bn of gross sales. The average obviously masks much bigger numbers from the largest contributing brands, but it highlights the amount of sales activity required to support the rising asset trend. Nonetheless, at the asset level, growth over the last decade of turmoil more or less matches that of the wider European universe where assets have risen by a factor of 1:8 with market performance and net sales contributing in more or less equal proportions.

There is much still to do to fully realise the single market dream in Europe but, after three decades of evolution, the playing field for cross-border and domestic groups is now more or less level. Cross-border funds have proved their ability to capture new business from all the European markets, and in some, they have built a sizeable market share.

9 Broadridge SalesWatch – calculated over the 10-year period to Dec 2017

(4,000)(2,000)

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018 a

nnualis

ed

Fig 2.7: Gross and net sales over time -per group average (€m)

Gross sales Net sales Linear (Gross sales) Linear (Net sales)

Source: Broadridge SalesWatch

29M A R K E T D A S H B O A R D

ITALYKey metrics – long-term funds (€bn) 2017

AUM CAGR (10 yr) Net sales

Domestic 475 2% 34

Cross-border 456 21% 68

TOTAL 931 8% 102

Foreign market share 49% 67%

Product focus (€bn) 2017

Domestic Net sales

1. Mixed Asset - Target Mat 6.3

2. Bond Global Currency 6.1

3. Asset Allocation 5.9

4. Mixed Asset Conservative 5.6

5. Bond Emerging Markets 5.1

Cross-border Net sales*

1. Mixed Asset Income --

2. Bond Global Currency --

3. Asset Allocation --

4. Bond Emerging Markets --

5. Bond Flexible --

% of passives in client portfolios: 19%

Bond45%

Equity27%

Mixed26%

Other2%

Cross-border AUM by investment type

(80,000)

(60,000)

(40,000)

(20,000)

0

20,000

40,000

60,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net sales history – 3-yr moving average (€m)

Domestic Cross-border

Broadridge. Data at 31 Dec 2017 with CAGR calculated from 2007. Data excludes ETFs, Money Market funds (incl Enhanced). Funds of Funds also excluded except in sector table. Cross-border data sourced from confidential data contributions from 67 groups to Broadridge SalesWatch service.

The Italian market has been the most

successful target for cross-border groups,

which have built up a market share of

nearly 50%. Bond funds are a strong

favourite but mixed asset funds are now

enjoying stronger growth. There is very little

difference in appetite between domestic

and cross-border sectors, although local

players dominate the Target Maturity space.

* Net sales data unavailable for reasons of confidentiality..

30 M A R K E T D A S H B O A R D

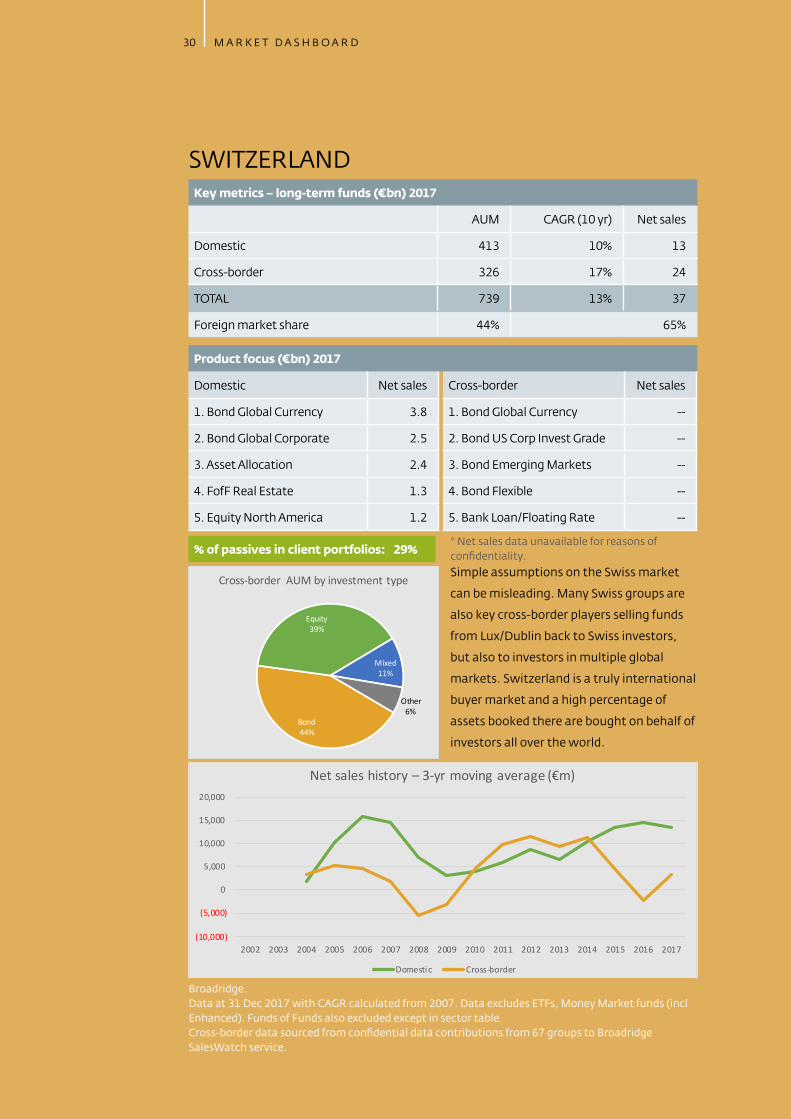

SWITZERLANDKey metrics – long-term funds (€bn) 2017

AUM CAGR (10 yr) Net sales

Domestic 413 10% 13

Cross-border 326 17% 24

TOTAL 739 13% 37

Foreign market share 44% 65%

Product focus (€bn) 2017

Domestic Net sales

1. Bond Global Currency 3.8

2. Bond Global Corporate 2.5

3. Asset Allocation 2.4

4. FofF Real Estate 1.3

5. Equity North America 1.2

Cross-border Net sales

1. Bond Global Currency --

2. Bond US Corp Invest Grade --

3. Bond Emerging Markets --

4. Bond Flexible --

5. Bank Loan/Floating Rate --

* Net sales data unavailable for reasons of confidentiality.. % of passives in client portfolios: 29%

Bond44%

Equity39%

Mixed11%

Other6%

Cross-border AUM by investment typeSimple assumptions on the Swiss market

can be misleading. Many Swiss groups are

also key cross-border players selling funds

from Lux/Dublin back to Swiss investors,

but also to investors in multiple global

markets. Switzerland is a truly international

buyer market and a high percentage of

assets booked there are bought on behalf of

investors all over the world.

(10,000)

(5,000)

0

5,000

10,000

15,000

20,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net sales history – 3-yr moving average (€m)

Domestic Cross-border

Broadridge. Data at 31 Dec 2017 with CAGR calculated from 2007. Data excludes ETFs, Money Market funds (incl Enhanced). Funds of Funds also excluded except in sector table. Cross-border data sourced from confidential data contributions from 67 groups to Broadridge SalesWatch service.

31M A R K E T D A S H B O A R D

GERMANYKey metrics – long-term funds (€bn) 2017

AUM CAGR (10 yr) Net sales

Domestic 590 3% 28

Cross-border 240 12% 15

TOTAL 830 4% 43

Foreign market share 29% 35%

Product focus (€bn) 2017

Domestic Net sales

1. Mixed Asset Conservative 6.1

2. Asset Allocation Alternative 4.8

3. Bank Loan/Floating Rate 3.4

4. Equity Global Income 2.3

5. FofF Asset Allocation 2.2

Cross-border Net sales

1. Bank Loan/Floating Rate --

2. Asset Allocation Alternative --

3. Mixed Asset Income --

4. Bond Global Currency --

5. Bond Flexible --

* Net sales data unavailable for reasons of confidentiality.. % of passives in client portfolios: 23%

Bond36%

Equity40% Mixed

19%

Other5%

Cross-border AUM by investment type One of the first markets to become truly

accessible to cross-border Ucits, Germany

remains a key target for cross-border Ucits

although the pace of sales was curtailed

by the financial crisis and has only recently

recovered to its earlier form. Mixed asset

funds have been the product of choice but

competition from local providers is stiff.

(15,000)

(10,000)

(5,000)

0

5,000

10,000

15,000

20,000

25,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net sales history – 3-yr moving average (€m)

Domestic Cross-border

Broadridge. Data at 31 Dec 2017 with CAGR calculated from 2007. Data excludes ETFs, Money Market funds (incl Enhanced). Funds of Funds also excluded except in sector table. Cross-border data sourced from confidential data contributions from 67 groups to Broadridge SalesWatch service.

32 M A R K E T D A S H B O A R D

UKKey metrics – long-term funds (€bn) 2017

AUM CAGR (10 yr) Net sales

Domestic 1,182 7% 63

Cross-border 219 24% 10

TOTAL 1,401 8% 73

Foreign market share 16% 14%

Product focus (€bn) 2017

Domestic Net sales

1. Equity Global 27.4

2. FofF Balanced 5.6

3. Bond Target Maturity 4.7

4. Equity Europe ex UK 4.4

5. FofF Dynamic 3.6

Cross-border Net sales

1. Bond Global Currency --

2. Bond Global Corporates --

3. Bond Emerging Markets --

4. Equities Europe ex UK --

5. Bonds Emerging Markets --

* Net sales data unavailable for reasons of confidentiality.. % of passives in client portfolios: 24%

Bond52%

Equity37%

Mixed10%

Other1%

Cross-border AUM by investment typeThe UK market is Europe’s most open in

terms of distribution structures, but also

one of the least accessible. Headline data

suggests huge potential but most of the

cross-border groups that are winning

assets are groups with a strong domestic

presence. The Brexit factor is affecting

appetite, shifting investor focus from UK

equities to global stock funds.

(10,000)

0

10,000

20,000

30,000

40,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net sales history – 3-yr moving average (€m)

Domestic Cross-border

Broadridge. Data at 31 Dec 2017 with CAGR calculated from 2007. Data excludes ETFs, Money Market funds (incl Enhanced). Funds of Funds also excluded except in sector table. Cross-border data sourced from confidential data contributions from 67 groups to Broadridge SalesWatch service.

33M A R K E T D A S H B O A R D

SPAINKey metrics – long-term funds (€bn) 2017

AUM CAGR (10 yr) Net sales

Domestic 181 -2% 10

Cross-border 143 19% 27

TOTAL 324 3% 37

Foreign market share 44% 73%

Product focus (€bn) 2017

Domestic Net sales

1. FofF Bond Europe Currency 5.2

2. Asset Allocation 3.7

3. FofF Balanced 3.3

4. FofF Asset Allocation 3.2

5. Bond EUR Short Term 2.6

Cross-border Net sales

1. Bond EUR Short Term --

2. Bond Flexible --

3. Bond Global Currency --

4. Bank Loan/Floating Rate --

5. Mixed Asset Income --

* Net sales data unavailable for reasons of confidentiality.. % of passives in client portfolios: 16%

Bond46%

Equity38%

Mixed15%

Other1%

Cross-border AUM by investment typeThe recent success of cross-border groups

in Spain is linked to the Spanish banks’

strategy of using funds of funds for

their client investments. These are open

architecture products that feed heavily on

cross-border Ucits. The exclusion of funds

of funds from the headline data therefore

contributes to the stalled asset growth from

the local fund groups.

(30,000)

(20,000)

(10,000)

0

10,000

20,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net sales history – 3-yr moving average (€m)

Domestic Cross-border

Broadridge. Data at 31 Dec 2017 with CAGR calculated from 2007. Data excludes ETFs, Money Market funds (incl Enhanced). Funds of Funds also excluded except in sector table. Cross-border data sourced from confidential data contributions from 67 groups to Broadridge SalesWatch service.

34 B I G B A N G T O G A L A X Y O F S T A R S

“ The industry is proving more successful

than we originally thought at capturing the

assets of HNWIs – many of them in emerging

markets”— PWC Asset Management 2020: Taking Stock, June 2017

I N T O T H E W I D E R U N I V E R S E 35

3 Into the wider universe

Durability and brand recognition continue to underpin the sales success of Ucits outside Europe. However, alongside emergent sales opportunities headwinds are forming, raising questions about the long-term growth outlook for one of the region’s most successful exports. Whether developing a Ucits footprint in Asia, Latin America or the Middle East, competition is stiff and local regulations are complex so cross-border fund groups must adapt their business models and hone their product offering to compete with increasingly sophisticated domestic providers.

With 30 years under its belt the Ucits framework has withstood financial crises and adapted to new regulations and shifting investor demands. Its acceptance as a regulatory standard outside Europe was unexpected

in its early days, but subsequently extolled as an important European success story. Its path has not been smooth; the inclusion of derivatives under the Ucits 3 Directive caused consternation amongst non-European regulators who feared the entry of complex products that had the potential to undermine the Ucits brand, and investor confidence. It survived and non-European investors now account for 23% of assets invested in European Ucits. Nonetheless, while many markets continue to open their doors to Ucits, protectionist moves in some of the fastest growing wealth management centres have the potential to challenge the distribution muscle and resilience of all but the largest and most visible product providers.

Asia Pacific region

Growing wealth in the Asian Pacific region (Apac) is a huge draw card for international asset managers. According to the latest Cap Gemini Global Wealth Report1, Apac and North America powered the growth in numbers of the world’s

1 Published June 2018

35

36 B I G B A N G T O G A L A X Y O F S T A R S

wealthiest investors, accounting for 75% of the increase in the global high net worth population in 2017 and 69% of the rise in HNWI wealth2. The report also notes that Asia Pacific region maintained its growth momentum and expanded its lead over North America, reaching a record 6.2 million HNWIs with $21.6tn in financial wealth. As a relatively sophisticated client base this wealth community clearly represents a growing opportunity for international product providers as they look to diversify and gain access to niche asset classes.

The importance of the mass affluent and mass retail investors should also be considered since over 70% of total Apac wealth is held by these segments. While financial literacy remains low, opportunities are likely to increase as lower interest rates and the downward trend in investment returns means more initiatives will have to be introduced to promote pensions savings. While money market funds account

for the majority of new flows in Apac, the current impetus to mobilise savings and invest in riskier assets is only going to get more intense, even in ultra-conservative countries such as Japan.

Hong Kong, Singapore and Taiwan

Notwithstanding the significant opportunity that these developments represent, the constituent Apac markets are at varying stages of sophistication and addressability. Fig 3.3 shows the countries that are most open to third-party foreign asset managers and cross-border Ucits funds are Hong Kong, Singapore and Taiwan3 where cross-border market share represented 46%, 66% and 54% of their respective investment fund industries in June 2018. Offshore funds or sub-advised funds form a significant proportion of assets under management in these markets.

2 A total of 1.2 million new HNWIs accounting for $4.6trn in new wealth3 Broadridge SalesWatch data – see Appendix 1

0500

1,0001,500

2,000

2,5003,000

3,5004,000

2013 2018

Fig 3.1: Apac AUM by Domicile (€m)

Cross Border Domestic

Source: Broadridge3

(100,000)

0

100,000

200,000

300,000

400,000

500,000

600,000

2010 2011 2012 2013 2014 2015 2016 2017 H1 2018

Fig 3.2: Apac net sales by domicile (€m)

Domestic Cross-border

Source: Broadridge3

I N T O T H E W I D E R U N I V E R S E 37

Taiwan is something of an anomaly and merits a special mention. Curbs on offshore fund launches resulted in significant outflows from Ucits products in 2015 and 2016, but sales have dramatically recovered as more asset managers have taken advantage of an incentive scheme that rewards offshore providers for boosting their local presence. The Taiwanese authorities are clearly keen to expand the domestic market, but the carrot and stick approach adopted has, paradoxically, lifted offshore fund business in the country.

South Korea, Japan and Thailand

In other markets such as South Korea, Japan and Thailand, international managers must work with local partners to access the domestic wealth pools. In Korea, for example, it is currently more costly to invest directly in an offshore fund than it is to invest locally due to tax and regulatory issues. The same holds true for Australia. Unsurprisingly, observers says that regulators are more likely to look favourably on foreign managers who show a demonstrable commitment to establishing a sustained local presence. It is notable that in January 2017, the South Korean FSC announced that it will revise asset management regulations to further open the sector. Under the proposed new rules, foreign asset managers will be allowed to sell to a wider group of professionals. However, product partnerships and distribution tie-ups will be increasingly the norm as foreign managers look for a cost efficient means of expansion. It is worth pointing out that Japan’s offshore assets as a percentage of onshore assets can be deceptive as sub-advised assets are significant in this country and not always visible.

India

India is one of the most challenging markets to penetrate as is evidenced by the number of managers that have exited the country in recent years. Offshore funds have yet to gain traction in the country and the majority of onshore funds invest locally. However, India’s asset management space is growing as a result of government support and an increasingly professional wealth management industry. Broadridge forecasts double digit growth in mutual funds and ETFs from 2016-2021.

0

50

100

150

200

250

2013 2018 2013 2018 2013 2018

Hong Kong Singapore Taiwan

Fig 3.3: Apac AUM growth by market (€m)

Cross Border Domestic

Source: Broadridge3

38 B I G B A N G T O G A L A X Y O F S T A R S

China

China is seen by most foreign managers as the main prize and foreign funds can be distributed via a foreign bank or local wealth manager using their overseas investment quota (QDII). However, it is domestic focused strategies that are in demand and currently few international fund houses have made inroads here. That said, managers should keep an eye on developments in China, as plans to lift capital controls on outbound investments and grow the country’s third pillar pension segment will likely create opportunities to launch retail pension funds via fund of funds structures.

Apac investor appetite

The bulk of mutual fund assets sourced from Apac investors lie in fixed income and equities. Two notable exceptions are China and South Korea where money market funds dominate. Weaning investors off money market funds in these countries will be a challenge, though Chinese investors are starting to diversify and multi-asset funds along with fixed income funds will likely gain market share over the next three years.

Equities Apac, thematic equities and mixed asset funds have enjoyed the strongest sales flows across the region over the past three quarters, though every market has its own nuances. In Taiwan, for example, fixed income funds dominate but more money is starting to be diverted into mixed funds, which will benefit foreign asset management firms more than local players. The multi-asset segment has grown in popularity in several Apac countries as it provides a means to access diversified investment strategies and suits the more conservative mind-set of many Asian

investors. Those that come with income components remain popular across the region, particularly in South East Asia where demand has been relatively untapped. Managers need to keep mixed asset funds simple in order for investors to understand and feel comfortable with these products.

Social responsibility and ESG

There has been a lot of talk about the need for managers to adapt their product offerings to include an ESG component. While support for ethically invested

multi-asset along with

fixed income funds are

expected to grow

market share over the

next three years

I N T O T H E W I D E R U N I V E R S E 39

funds has gained significant traction in Europe and North America, they are only now making an impact in Apac. A number of global managers are registering and promoting their ESG strategies by leveraging on the success they have built in other regions. Whilst just four of the largest 20 international ESG funds are passively managed, seven passive funds made the top 20 list by net new flows at the end of 2017. Examples of global managers importing these strategies include HSBC, launching two funds with a lower carbon investment strategy targeted at Hong Kong retail investors in April 2018 and Natixis Asset Management rolling out a green bond fund and a sustainable equity fund through its boutique asset management unit (Mirova). Both funds are for sale in Hong Kong and Singapore.

Passives and ETFs

ETFs have been steadily making inroads in Apac and it is likely that ETF Connect – the planned trading link between Hong Kong and mainland China’s two stock exchanges – will give the sector a much needed boost. Currently, Apac institutions are increasing and broadening ETF usage, but the bulk of flows have been directed to US and European exchanges. Retail penetration, on the other hand, remains low and requires a more favourable regulatory framework to improve uptake. While Japan will remain the largest ETF market in Apac, we expect China (and Hong Kong due to ETF connect) to be the two fastest growing markets in the region. Nearly 70% of the projected growth is expected to come from new flows and ETF assets in the region are expected to reach $1.9trn by 20254.

Passport threat

Observers have suggested that the most significant threat to Ucits in Asia comes from recent passporting initiatives looking to emulate and, arguably, to replace Ucits. These include:

▪ The China mainland/Hong Kong Mutual Recognition of funds (MRF) scheme,

4 Broadridge forecasts

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2013 2018

Fig 3.4: Growth of AUM in mutual fund vs ETF (€bn)

ETFs

Mutual Funds

Source: Broadridge3

40 B I G B A N G T O G A L A X Y O F S T A R S

▪ The Asean Collective Investment scheme (CIS) between Singapore, Malaysia, Thailand,

▪ The Asia Region Fund Passport (ARPF) between Australia, New Zealand, Singapore, Thailand, Korea and Japan.

Like Ucits these schemes allow approved funds that are domiciled in one country to be distributed in another participating country and vice versa. While Hong Kong investors have shown a moderate interest in buying China mutual funds and the CIS has attracted a modest number of participating funds, asset volumes remain low. Many observers believes ARPF could be equally disappointing. The main drawback is the problems posed by the different tax rules in each jurisdiction, which will be very difficult to align. Further measures will need to be taken in order to provide real impetus to these regional schemes.

Forward view on Asia

With so much wealth being generated throughout Apac, and as the needs of investors continue to evolve, Ucits will continue to play an important role because they facilitate economies of scale, allow the central management of product strategies and are firmly embedded in the investment culture of the region. International managers can succeed if they focus on a limited range of products and choose their markets wisely – a scatter gun approach can never work in Apac. Beyond the most addressable markets, a local presence is required and attention to detail is key. Managers have learnt to their cost that applying the same marketing and distribution strategies across disparate markets rarely works and parachuting sales staff in from Europe without the requisite language skills and cultural training can prove to be a costly and unproductive strategy.

Latin America

International managers have traditionally approached Latin America through the region’s pension schemes (AFPs and Afores) because of their size, transparency, growth outlook and addressability. According to Broadridge data5, total professionally managed pension scheme assets reached $850bn at the end of 2017, of which $309bn was managed by third party asset managers.

5 Broadridge Money in Motion

I N T O T H E W I D E R U N I V E R S E 41

Appetite for cross border Ucits products remained robust throughout 2017 as pension scheme administrators sought expertise in emerging market debt, European, Asian and North American equities. And while the global share of LatAm Ucits remains tiny at just 2%, regulatory changes to the region’s pensions systems and shifting dynamics in the region’s wealth management sector are enticing new entrants to its shores. However, this view needs to be treated with caution because the perceived opportunities presented by the pension systems can be deceptive.

As Fig 4 shows, addressable pension assets are fairly evenly split within the private (DB & DC) and the public Cap AFP Afores systems. Cap is the largest component with 44% or $150bn of the total addressable pool, followed by defined benefit with $100bn or 35% of the addressable assets.

Andean markets

With their similar regulations and ease of access, the Andean markets (Chile, Colombia and Peru) present the greatest opportunity for international managers. While Chile is the most established market for both local and international managers, other Cap systems modelled on Chile represent a growing opportunity due to their favourable demographics and appetite for mutual funds rather than mandates.

Fig 4: LatAm addressable institutional assets, €bn

Total

institutional AUM

Addressable

AUM

Addressable

%

DBPrivate 170 101 59%

Public 64 1 2%

DC Private 98 59 61%

CAP

Chile 208 82 39%

Mexico 161 22 14%

Columbia 86 20 23%

Peru 48 10 21%

Costa Rica 10 1 8%

846 296 35%

Source: Broadridge.

Brazil accounts for 90% of this segment, which, due to regulatory restrictions, can only be accessed by means of local players.

Mexico CAP system, Afores, is only accessible through ETFs listed on the local stockmarket or via pension mandates. From Jan investment in Ucits is possible

The Andean market (Chile, Colombia, & Peru) presents the greatest opportunity for foreign managers, thanks to similar regulations and single point of contact from abroad or through third-party representatives.

1

1

2

2

3

3

42 B I G B A N G T O G A L A X Y O F S T A R S

Total institutional asset management in Chile reached $208bn at the end of 2017 with the addressable component representing $82bn. This compares to $86bn of AUM in Colombia’s Cap public DC scheme of which $20bn is addressable, and $48bn in Peru’s public pension scheme of which $10bn is addressable. It is worth noting that some of Chile’s largest AFPs, such as Provida, typically have between 40%-45% of their assets in foreign vehicles.

Mexico

While Mexico is one of the largest pension markets in the region with assets of $161bn and an addressable asset pool of $22bn, until recently the Cap system was only accessible through ETFs listed on a local stock exchange or through mandates given by one of the pension managers. However, Consar, the local pension regulator, introduced new guidelines in January allowing pension funds to invest in mutual funds with 20% allocation to overseas Ucits. These guidelines require further clarification, but international managers are confident that they are well placed to win assets as pension scheme administrators are eager to access international securities via foreign mutual fund structures because they are less expensive and more accessible than mandates – this is especially true for smaller schemes.

Brazil

On the face of it Brazil appears a compelling opportunity, accounting for 90% of private and public DB and private DC assets6. However, until recently it was impractical to target the Brazilian pension schemes. While pension funds could, in

6 Broadridge, Money in Motion

0

200

400

600

800

1,000

2013 2018

Fig 3.5: LatAm AUM by Domicile (€bn)

Cross Border Domestic

Source: Broadridge

(10,000)

0

10,000

20,00030,000

40,000

50,000

60,00070,000

80,000

2010 2011 2012 2013 2014 2015 2016 2017 H1 2018

Fig 3.6: LatAm net sales by domicile (€m)

Domestic Cross-border

Source: Broadridge

0

20

40

60

80

100

2013 2018 2013 2018 2013 2018

Chile Colombia Peru

Fig 3.7: LatAm AUM growth by market (€m)

Cross Border Domestic

Source: Broadridge3

I N T O T H E W I D E R U N I V E R S E 43

theory, invest 10% of assets overseas, few rarely took advantage of this option. The process was cumbersome and domestic fixed income offered better risk-adjusted returns due to the relatively high interest rates in the country. With the recent fall in interest rates, however, pension administrators are looking overseas for yield. That said the home bias for local and high local rates still exists. Managers need to have a truly differentiated story or a huge brand to lean on as local fund pickers prefer to go with what they know.

LatAm investor appetite