Fraud Corruption Powerpoint Presentation

22

CORNERSTONE TRAINING INSTITUTE

-

Upload

nathan-m-francis -

Category

Documents

-

view

28 -

download

1

description

Detecting a fraud in an organization is essential to make it healthier all the time

Transcript of Fraud Corruption Powerpoint Presentation

CORNERSTONE

TRAINING INSTITUTE

PRESENTATION DURING THE

AUDIT TRAINING

PROGRAMME 13TH – 17TH

FEBRUARY, 2012

About the Presenter

Kennedy BichangaBcom, Mcom, DCMAExecutive Chairman CTIMember of ACCA, IIA, KIM, ACFE

Sacco Fraud

THEME

INTRODUCTION TO FRAUD:

Background:•The Sacco's business is money, using money to generate more money.

•People want money to meet their real and perceived needs using either prudent (lawful) and /or illegal dishonest means.

•Those who uses fraudulent has remained the biggest nightmares for financial institutions and economy at large.•These category of persons are perfecting their art everyday to avoid ,delay and evade detection ,which makes fraud so much alive.It changes faces as soon as the scheme is discovered.WHY DO THINK FRAUDSTERS SUCCEED?•Fraudsters are able to achieve their schemes primarily through collusion with members of staff, weak internal controls and lack of clear fraud policy, and dishonest members of staff.

Definition

• Fraud is a deliberate misrepresentation of a fact which causes another person or an Institution to suffer damages, usually monetary losses. • Most people consider the act of lying to be fraudulent but in a legal sense, lying in only one small element of actual fraud. There must be a deliberate misrepresentation of the product's condition and actual monetary damages.

Commercial fraud topologies Q1 2010

1 Cheque Fraud 16 23 13 1,66,210,399.5

31,9 87,002.00

2 Forgery cheating

5 5 13 54,507,123.54 9,865,264.00

3 Credit card fraud 6 11 8 3,062,455.00 48,143,600.00

4 transfers 1 5 4 116,492,933.00

48,143,600.00

5 Computer fraud 0 0 1 248,149.90 248,149.90

6 Counterfeiting 1 0 0 5,00.00 5,000.00

7 Identity theft 2 0 1 2,601,00.00 0.00

8 Theft by Directors

1 0 0 491,000.00 0.00

9 Forex Fraud 0 1 0 328,366.00 328,386.00

10 embezzlement 1 2 2 26,559,880.80 0.0011 Loan fraud 1 1 0 600,000.00 260,000.00

12 conveyancing 0 0 0 0.00 0.0013 Stock/commer cial

paper fraud0 0 0 0.00 0.00

14 Investment scam 0 0 0 0.00 0.0015 Pension Fund Fraud 0 0 0 0.00 0.00

Totals 371,106,327.7

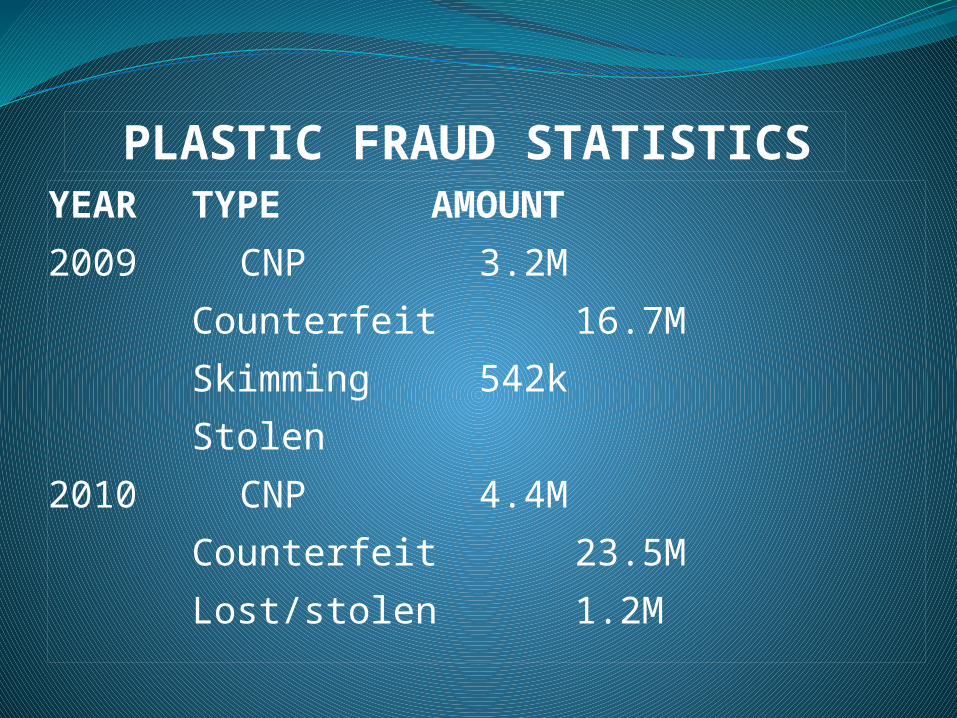

YEAR TYPE AMOUNT

2009 CNP 3.2M

Counterfeit16.7M

Skimming 542k

Stolen

2010 CNP 4.4M

Counterfeit23.5M

Lost/stolen 1.2M

PLASTIC FRAUD STATISTICS

Emerging Fraud Trend•Increased usage of spacious or parallel cheques• Disputed•ATM transactions• Identify Theft•Cheque fraud•Staff defalcation•Fraudulent application of loans•Forged customers instructions•Fraudulent transfer of funds•Credit card frauds

What are the most common frauds in Saccos?

•Payment of recycled cheques.•Payment of fraudulently endorsed

cheques•Failure to affect loan repayment

(suppression of loan repayments)•Fraudulently guarantee LNs.•Irregular approval of loans• Disbursement of ghost loans

Frauds Unique to Sacco's

Key changes There are a number of key factors in the financial sector that has seen them come with increased cases of fraud.

1 Business system models2 Delivery channels with minimum human

supervision(ATM,EFTS, Electronic cards internet banking)

3 Staff. 4 Politics

5 Regulations6 Technology, increased competition,

economic environment etc. All these create challenges.

What should the Saccos do?

What are the Saccos doing?•Faced with such challenges the banks forged a

common front to deal with the following:•Fraud and security Policies•Operational challenges•Governance & regulatory issues.•Any other emerging risk within the industry•There exists various sub committees handling various issues . In the USA, we have such committee known as Sacco fraud and security committee.

• Staff complicity and conclusion• Technological advancement• Weak controls or overrides• Insufficient policies and procedures• Reluctance to share information and non

cooperation• Customer negligence

Reasons for increase in fraud

1.Sophistication in modus operandi in perpetration of funds

2. Inability to handle investigations thus leading to poor quality

3. Inability to detect frauds timely due to lack of automated fraud detection system

4.Lack of an industry fraud management framework that will clearly set out the legal and operational provisions that will enable saccos share

information and collaborate 5.Lack of information/data on fraud trends

Challenges

1.Pressure the evidence 2.Escalate to the appropriate authority apply the need to know rule 3.Review and understand the process 4.Carry out an in-depth audit trail 5.Recommend controls that will mitigate future occurrence 6.Where applicable involve the police for further investigations.

Action when fraud is detected

1) Develop effective/relevant internal controls 2) Develop a culture of respect internal control 3) Enforce controls beyond regulations requirements

4) Develop Anti-fraud policy specific to each Institution with derived score and ownership

5) Train staff on the anti fraud policy

Way forward:

4) Communicate what needs to be done and the consequences. Develop raising concern policy-Thus normally acts deterrent to fraud

5) Build ethics and integrity in the institution .Enforce code of conduct and avoid conflict of interest .Educate & involve staffs

6) Enforce corporate governance Share intelligence to counter fraud

QUESTION

THANK YOU