Francis Clark Budget Seminar March 2015

67

2015 FRANCIS CLARK BUDGET SEMINAR

-

Upload

francis-clark-llp -

Category

Business

-

view

269 -

download

1

Transcript of Francis Clark Budget Seminar March 2015

2015

FRANCIS CLARK

BUDGET SEMINAR

Budget 2015

Private client issues

www.francisclark.co.uk

Timetable – where are we?

• Autumn Statement – some measures with immediate effect from

December; some for Finance Bill

• Finance Bill to be published Tuesday 24 March

• Parliament dissolved Monday 30 March

• Which measures will be passed by then?

• Election and second Budget

• …and a third?

www.francisclark.co.uk

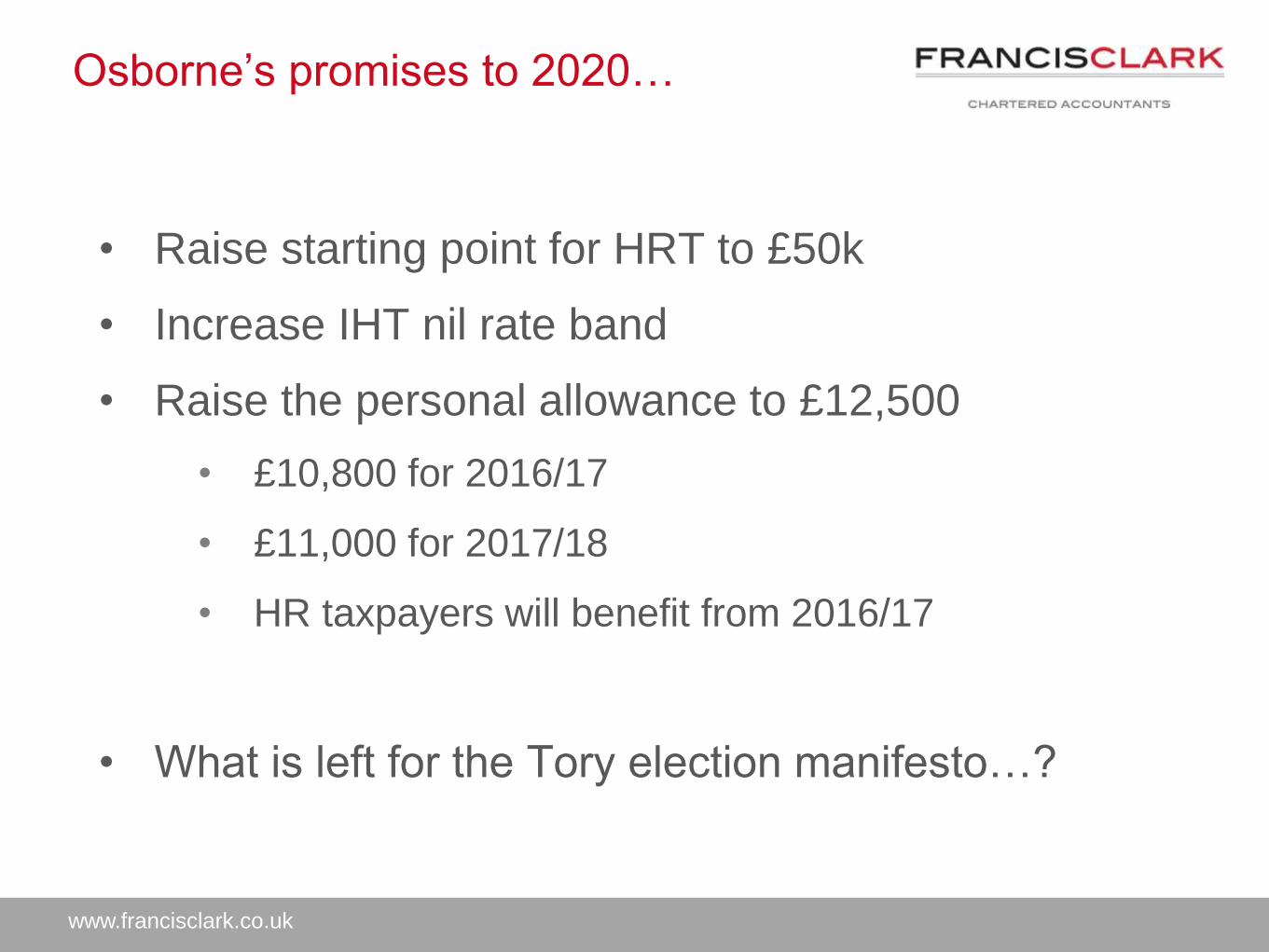

Osborne’s promises to 2020…

• Raise starting point for HRT to £50k

• Increase IHT nil rate band

• Raise the personal allowance to £12,500

• £10,800 for 2016/17

• £11,000 for 2017/18

• HR taxpayers will benefit from 2016/17

• What is left for the Tory election manifesto…?

www.francisclark.co.uk

Since May 2010

• Rich have gained from a 10% cut (50% - 45%)

• Millions escape tax completely

• Meanwhile ‘middle England’…

• means tested child benefit (£50k)

• lowering of start point for higher rate tax (£42k)

www.francisclark.co.uk

Rates and allowances – income tax

Allowances – 2015/16 tax year

£

Personal allowance 10,600

Higher rate band 31,785

Additional rate band 150,000

Personal allowance abated £1 for £2 at 100,000

Personal allowance lost at 121,200

(60% effective tax rate)

www.francisclark.co.uk

Personal allowances – tax free

-

2,000

4,000

6,000

8,000

10,000

12,000

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

www.francisclark.co.uk

Rates and allowances – income tax

Rates – 2015/16 tax year

Basic rate 20%

Higher rate 40%

Additional rate 45%

Rate for trusts 45%

Effective dividend rate (HR) 25%

Effective dividend rate (AR) 30.6%

No rate

changes

www.francisclark.co.uk

Rates and allowances – NIC

Lower earnings limit (LEL) 112

Primary threshold (PT) 155

Upper earnings limit (UEL) 815

Upper profits limit 42,385

Under 21s lower threshold/secondary threshold (ST) 156

Under 21s upper threshold 815

Lower profits limit 8,060

Small profits threshold/small earnings exemption (SPT) 5,965

Employees - PT to UEL 12%

Employees - Above UEL 2%

Employer - Above ST 13.8%

Class 4 LPL - UPL 9%

Class 4 above UPL 2%

Class 2 £2.80 per week

www.francisclark.co.uk

NIC update

Class 2 NIC

• Move to collection via Self Assessment in 2015/16

• Plan to abolish class 2 NIC by end of next Parliament

Class 4 NIC

• Consultation on reforms in next Parliament

www.francisclark.co.uk

High income child benefit charge

• Earnings > £50k

• At £60k - 100% claw-back

• Election not to receive

• Consider income planning

• Pension/Gift Aid contributions pre-5 April?

• 2014/15 charge is £1,770 for a two child family

www.francisclark.co.uk

Savings rate – changes

• Currently 10% on £2,880

• April 2015 – 0% on £5,000

• Linda, who is 65, has pension income of £9,800 and savings

income of £4,600 in 2015/16. She will have no tax liability. The

liability in 2014/15 would have been £592.

• Budget announcement – from April 2016 – “personal savings

allowance”

• no tax on first £1,000 of interest (basic rate taxpayers)

• £500 allowance for 40% taxpayers

• Banks & building societies will stop automatically deducting interest

www.francisclark.co.uk

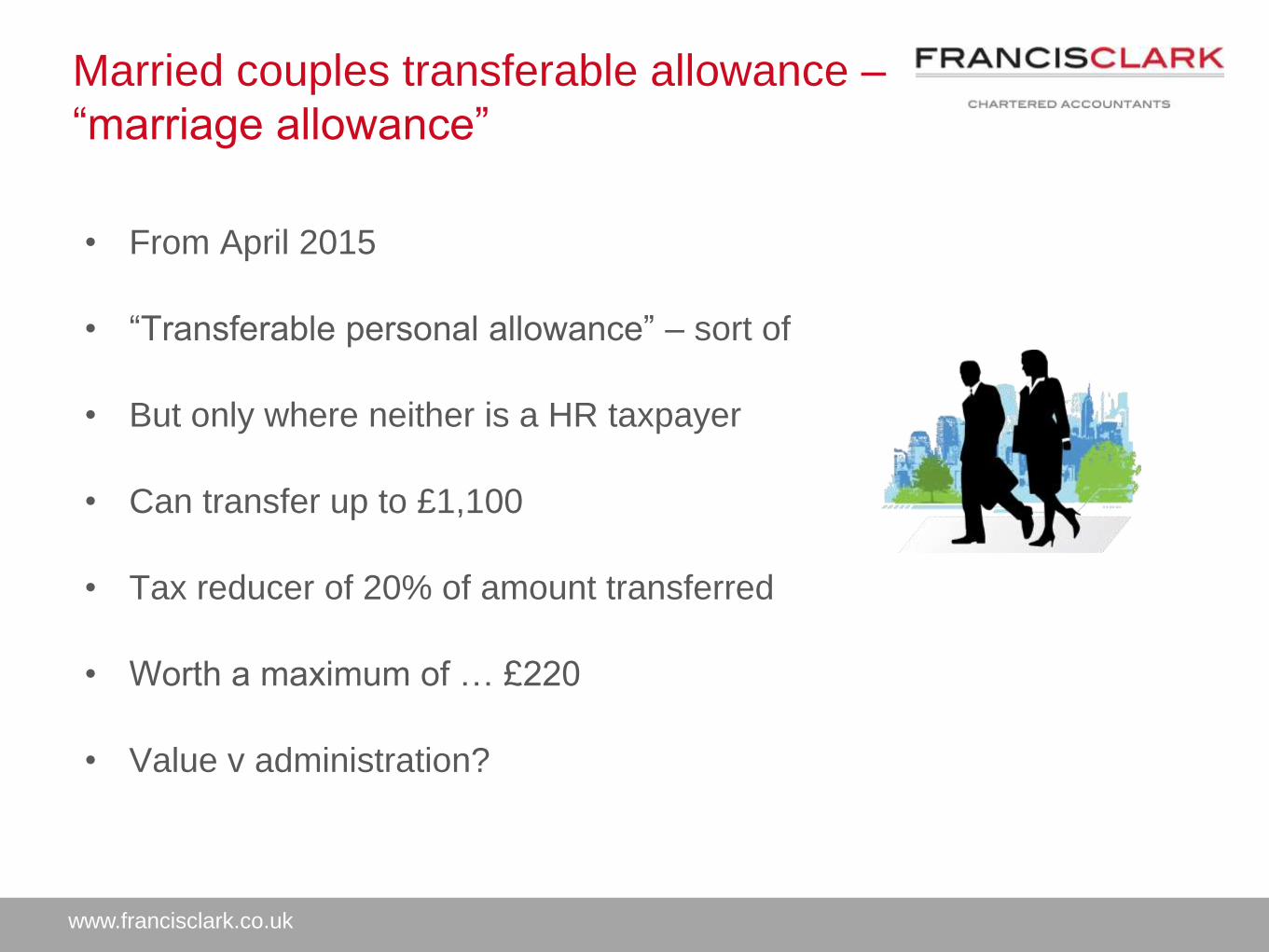

Married couples transferable allowance –

“marriage allowance”

• From April 2015

• “Transferable personal allowance” – sort of

• But only where neither is a HR taxpayer

• Can transfer up to £1,100

• Tax reducer of 20% of amount transferred

• Worth a maximum of … £220

• Value v administration?

www.francisclark.co.uk

“The death of annual tax returns”

• Plan = to replace with “digital tax accounts”

• Automatic receipt of information from various sources – increased

risk of errors?

• Will still need to input accounts and other tax information

• Expected to be in place by 2020

www.francisclark.co.uk

Rates and allowances – CGT

• Annual exemption 2015/16 £11,100

• Capital gain treated as top slice of income

• 18% if basic rate

• 28% if higher or additional rate

• Entrepreneurs’ relief taxes first £10m of ‘business’ gains at 10%

• Some ‘tweaks’ in Autumn Statement - incorporation

• Changes in Budget yesterday – joint ventures & associated disposals

• Post election changes?

www.francisclark.co.uk

Entrepreneurs Relief – future changes?

• Mr X and his wife Mrs Y looking to retire.

• Disposal in 31 March 2015. CGT payable at 10% on proceeds.

• If ER limit slashed by next government and/or CGT rates increased then tax

payable could increase substantially.

• Consider planning to ‘bank’ the £10m lifetime limit.

www.francisclark.co.uk

Non-residents CGT

• From 6 April 2015

• Disposal of UK residential property

• Individuals, trust and close companies

• To be paid with 30 days (or by normal self assessment if relevant)

www.francisclark.co.uk

PPR – main residence relief

• Consultation over summer suggested loss of ability to elect for all

taxpayers – now dropped

• From 6 April 2015 non-residents cannot claim PPR relief unless 90

midnights spent at the property

• UK residents cannot claim PPR relief on overseas property unless

spent 90 midnights there

www.francisclark.co.uk

SDLT – residential property

• Changes to SDLT effective 4 December 2014 – marginal system

• For residential purchases only

• Average family home price of £275,000 would save £4,500

• A £2.1m purchase would carry £18,750 more stamp duty

compared with the old system.

Residential £

£0 - £125,000 0%

£125,000 - £250,000 2%

£250000 - £925,000 5%

£925,000 - £1,500,000 10%

£1,500,000+ 12%

www.francisclark.co.uk

Remittance basis for non-doms

• Current regime

• Consultation on minimum claim period (3 years?)

• Proposed changes

• Remittance basis charges to increase:

Current From 6 April 2015

7 out of 9 years 30,000 30,000

12 out of 14 years 50,000 60,000

17 out of 20 years 90,000

www.francisclark.co.uk

Inheritance tax

• 16,000 estates paid IHT in 2010, now 35,000 +

• NRB frozen until 2019 at £325,000

• Life-time planning might now be easier?

• Use of trusts

• PETs

• Gifts out of income

• £3,000 exemption (!)

• Deeds of variation – under review – per Budget

www.francisclark.co.uk

Year End Tax Planning - Individuals

Income Tax and Capital Gains Tax (CGT)

• Pension Contributions/Gift Aid

• Utilise CGT Annual Exemption

• Equalising income between spouses

• Taxable gains – accelerate or postpone?

• SEIS / EIS / VCT investments

• Utilise ISA allowance

Budget 2015

Business tax

www.francisclark.co.uk

Corporation Tax

• Relatively quiet Budget

• Corporation tax rate 20% (regardless of associates)

• Associated companies still applicable under certain circumstances

• E.g. quarterly instalment payments

• Corporate partner arrangements have been attacked - unless

commercial

• Diverted profits tax (“Google tax”) – 25% from 1 April 2015

www.francisclark.co.uk

Goodwill – Entrepreneurs’ Relief

• Where a business is transferred from a sole trade/partnership to

company

• Goodwill transferred as part of the disposal

• Taxpayer would pay 10% tax on the gain

• Blocked for transfers to related company from 3 December 2014

• Deduction for the amortisation of the acquired goodwill?

• Not where transfer is to a related party from 3 December 2014

www.francisclark.co.uk

Budget – Entrepreneurs’ Relief changes

Associated disposals

• “Associated disposal” rules tightened

• Disposal of personally owned asset associated with

• a disposal of shares or

• reduction in partnership share

• In the past – what minimum reduction is acceptable?

• New rule = 5% minimum reduction = “meaningful disposal”

• Rules also tightened for joint ventures

www.francisclark.co.uk

Venture capital – EIS, SEIS, VCT & SITR

• Gains on disposals on or after 3 December 2014 eligible for ER

after deferral under EIS or SITR

• SITR to be extended to community energy generation

• 30% Income Tax relief

• No tax on dividends received or disposal of shares

• Energy generation removed from EIS, SEIS and VCT

www.francisclark.co.uk

Research & Development

• “Above the line” credit 11% (previously 10%)

• SME R&D rate: 230% deduction (previously 225%)

• Restriction if material used in product that this sold

• Increased access to R&D = aim

• Voluntary advanced assurances

• Raise awareness & guidance for small companies

www.francisclark.co.uk

Capital allowances

Annual Investment Allowance

• 100% deduction

• £250k limit until 1/4/2014

• Then £500k!

• Original plan = back to £25k from 1/1/16

• Chancellor has consulted with industry – to be increased to a

‘much more generous amount’

www.francisclark.co.uk

Farmers – changes to averaging

• Currently allowed to “average” profits over 2 tax years

• Assist where substantial fluctuations in profits – often out of control

of the farmer (e.g. weather)

• Consultation re extending from 2 years to 5 years from April 2016

www.francisclark.co.uk

NIC & employing staff

• Abolition of employer contributions for apprentices under 25 up to

UEL from 6 April 2016

• No employers NIC for under 21s from 6 April 2015

• Employment allowance of £2,000 to reduce employers NIC liability

• extended to staff for personal family or household affairs e.g. nannies,

gardeners, housekeepers from 6 April 2015

• National Minimum Wage - £6.70 from October 2015

www.francisclark.co.uk

Changes to benefits in kind

From April 2016

• Abolition of £8,500 threshold for benefits in kind

• Dispensations will be removed – replaced with exemption or

alternatively a scale rate

• Employers can voluntarily payroll car, fuel, medical insurance and

subscriptions

From April 2015

• Statutory exemption for trivial BIKs (worth <£50 in the tax year)

www.francisclark.co.uk

Budget 2015 – VAT

• VAT registration threshold £82,000 from 1 April 2015

(currently £81,000)

• Deregistration threshold £80,000 from 1 April 2015

(currently £79,000)

• No changes to Fuel Scale Charges

www.francisclark.co.uk

Budget 2015 – VAT

• VAT Refund Scheme from 1 April 2015 for Charities

• Hospices

• Search and Rescue and Air Ambulance

• Blood Bikes

• Prompt Payment Discount – changes from 1 April 2015

• Reminder – MOSS introduced from 1 January 2015

• No VAT on Severn River Toll from 2018

www.francisclark.co.uk

Budget 2015 – Other Indirect Taxes

• 2% reduction in alcohol duty rates from 23 March for spirits, sparkling cider,

perry, beer, wine (for each for certain ABVs)

• 2% increase all tobacco products from 6pm on 18 March 2015

• Gaming duty – new (increased) bandings for accounting periods starting on or

after 1 April 2015

• Landfill tax – increase in rates from 1 April 2016

• Vehicle Excise Duty – increase in rates in line with RPI - April 2015

• VED for HGVs frozen for 2015/16

• Fuel duty - planned increase for September 2015 has been cancelled

www.francisclark.co.uk

Miscellaneous

• Business rates review on-going

• Bad debt relief on peer to peer lending to allow offset of bad debts

against interest on loans made from 6 April 2015

• Charities – small donations gift aid (without needing paperwork) –

increase from £5,000 to £8,000 a year

The Budget;

The Financial Planning view

March 2015

www.fcfp.co.uk Twitter.com/francisclarkifa

The Budget

Agenda

• What changed

Anything we weren’t expecting? (the headlines)

Investments

Pensions

• What does it all mean?

Placing the changes in context

• Case Study

www.fcfp.co.uk Twitter.com/francisclarkifa

What Changed

Anything we weren’t expecting? – (the headlines)

• Yes!

• Annuity buy-backs introduced

(with a few days notice, thanks George)

• Pension Lifetime allowance cut to £1m

• Help-to-buy ISAs

• More flexible-ISAs

• Pension reforms

Plus the things we already knew come in to force

www.fcfp.co.uk Twitter.com/francisclarkifa

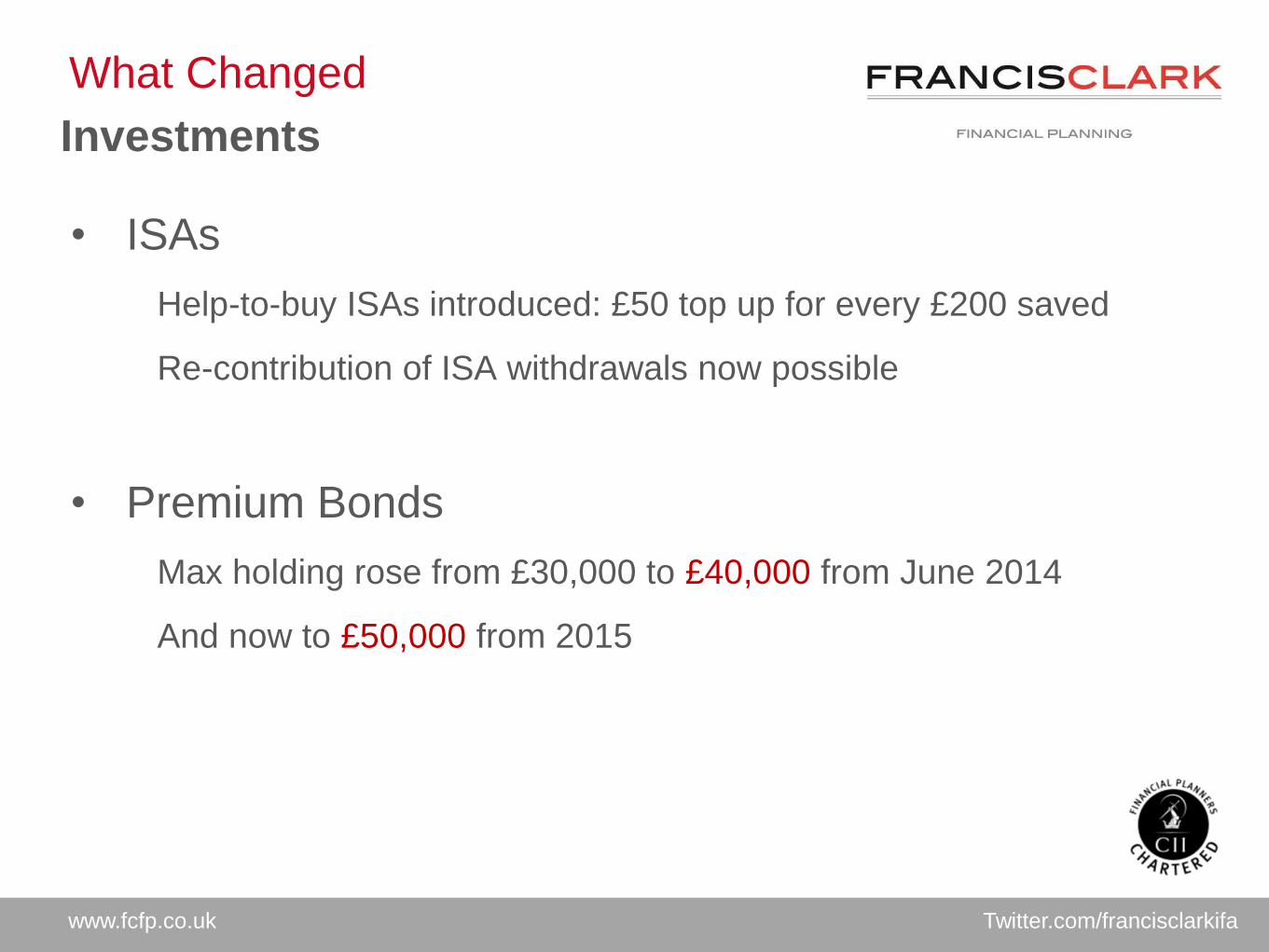

What Changed

Investments

• ISAs

Help-to-buy ISAs introduced: £50 top up for every £200 saved

Re-contribution of ISA withdrawals now possible

• Premium Bonds

Max holding rose from £30,000 to £40,000 from June 2014

And now to £50,000 from 2015

www.fcfp.co.uk Twitter.com/francisclarkifa

What Changed

Investments

• Pensioner Bonds

Enhanced saving bonds for over 65s from January 2015 – sold

out in 3 weeks!

Cap scrapped – pensioners have until 15 May 2015

• SEIS/EIS/VCT

No changes

• Investment Bonds (onshore & offshore)

No changes

www.fcfp.co.uk Twitter.com/francisclarkifa

What Changed

Pensions

• Lifetime Allowance

Reduced to £1m from £1.25m

(Was £1.8m as recently as 2011/12)

• Annuity buy-backs

Pensioners now have the ability to exchange their guaranteed

annuity income for a lump sum.

• Other changes

As already announced.

So what does it all mean?

www.fcfp.co.uk Twitter.com/francisclarkifa

What does it all mean?

Annuity buy-backs

• Raises many more questions…

• But, in short….

www.fcfp.co.uk Twitter.com/francisclarkifa

Re-cap

Budget 2014: Death of the annuity

www.fcfp.co.uk Twitter.com/francisclarkifa

Wait!

• Short term annuities

• Decreasing annuities introduced

Maybe annuities aren't dead?

Re-cap

www.fcfp.co.uk Twitter.com/francisclarkifa

What now?

Budget 2015: No, annuities are dead again

www.fcfp.co.uk Twitter.com/francisclarkifa

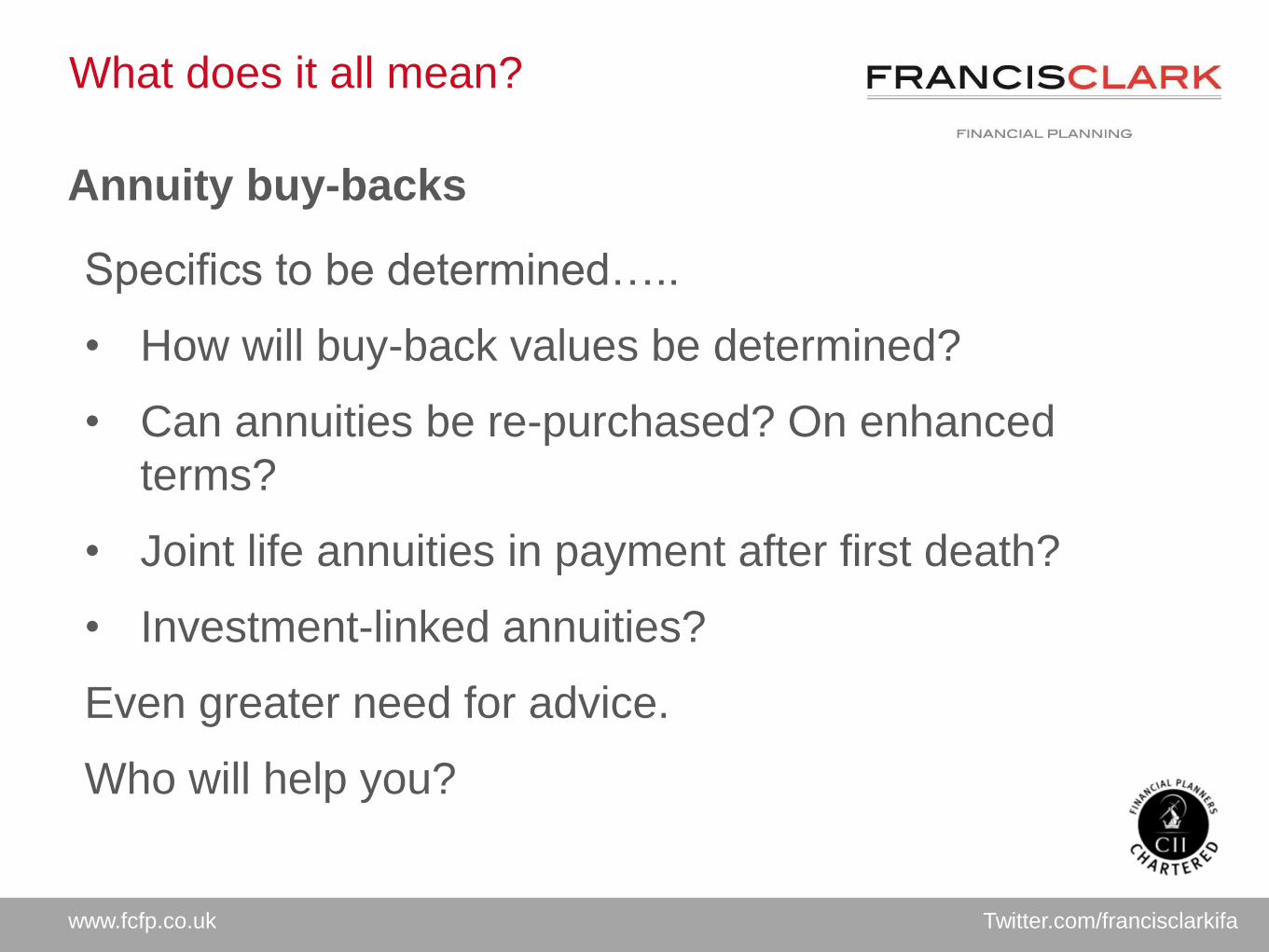

What does it all mean?

Annuity buy-backs

Specifics to be determined…..

• How will buy-back values be determined?

• Can annuities be re-purchased? On enhanced

terms?

• Joint life annuities in payment after first death?

• Investment-linked annuities?

Even greater need for advice.

Who will help you?

www.fcfp.co.uk Twitter.com/francisclarkifa

What does it all mean?

Pensions; Right to advice

• 2014: Everyone retiring from a DC scheme offered

“free, impartial, face-to-face advice”

www.fcfp.co.uk Twitter.com/francisclarkifa

What does it all mean?

Pensions; Right to advice

• “Guidance”

• Citizens advice bureau to provide face-to-face

guidance

• TPAS offering telephone service

• The Money Advice Service will be building the

online part of the service and developing material

after Treasury Select Committee “concerns”1

1 - FTAdviser 20/10/2014

www.fcfp.co.uk Twitter.com/francisclarkifa

What does it all mean?

• Displeased with your annuity?

• Situation changed?

• This is an unexpected second chance

• Don’t get it wrong twice (definition of madness, anyone?)

• Seek independent advice before taking action

Annuity buy-backs

www.fcfp.co.uk Twitter.com/francisclarkifa

What does it all mean?

• Well, more pensions actually…

• Really? Why’s that then?

Anything else?

www.fcfp.co.uk Twitter.com/francisclarkifa

What does it all mean?

www.fcfp.co.uk Twitter.com/francisclarkifa

What does it all mean?

• Will not affect the majority of savers

• Individual Protection 2014 still available

• However, will catch those with large(ish) defined benefit

entitlement

• Those in control of their pension funding – business

owners – can manage their position with proper planning.

…….and advice?

What about the reduced lifetime allowance?

Case Study –

Mr Ant E Pensions

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study

• Aged 60

• Business owner, higher rate tax payer

• Wants to phase retirement…go PT…wind down slowly

• Never liked pensions – has no provision

• Except an old works pension from years ago; worth £2.50

Background

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study

Never liked pensions…..

• “Can’t get my hands on the money”

• “Forced to buy a meaningless annuity”

• “Can’t control my investment”

• “Can’t pass it on to my family”

• “Taxed unfairly on my death”

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study

Now I do like Pensions. I changed my mind. OK.

• Entire pension pot available as a lump sum

• Punitive 55% tax charge removed

• First 25% of pension pot still tax-free

• On death, pensions can be passed on as a lump

sum without charge (pre-age 75)

• Or at recipient's marginal rate (post age 75)

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study

Pension funding

• Anthony pays £90,000 in to a pension this year –

using his allowance for 2014/15 and 2011/12

• Further funding of £90,000 next year (2015/16 and

2012/13)

• And £90,000 the year after (2016/17 and 2012/13)

• £270,000 in. Tax saving £108,000. Net cost £162,000

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study

Pension withdrawal

• Age 63. Fund now £300,000

• Stops working

• Withdraws £75,000 tax free.

• And £40,000 income. Net income = £34,000

(no national insurance!)

www.fcfp.co.uk Twitter.com/francisclarkifa

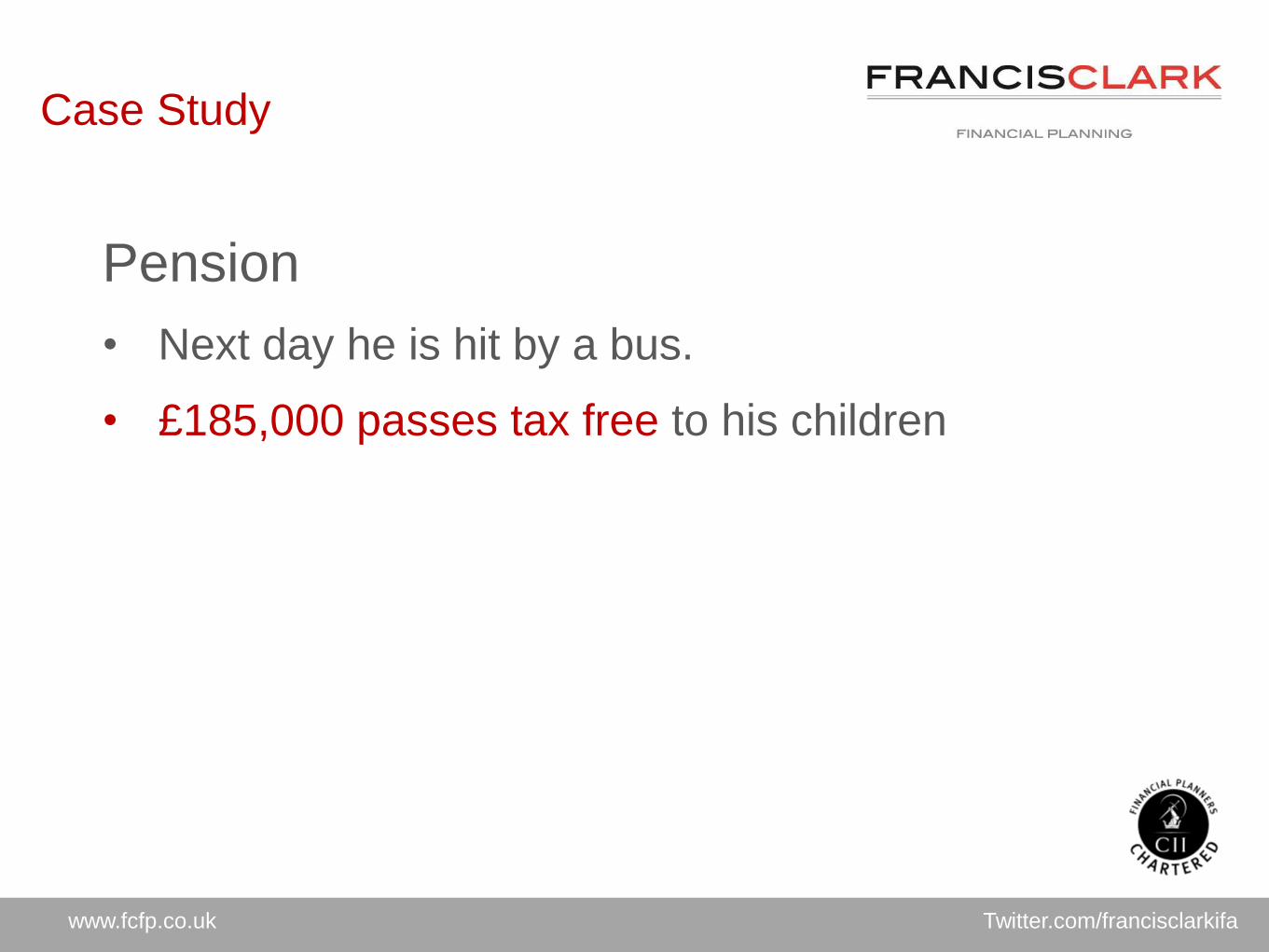

Case Study

Pension

• Next day he is hit by a bus.

• £185,000 passes tax free to his children

www.fcfp.co.uk Twitter.com/francisclarkifa

Case Study

Pension – summary position

*assumes CGT @28% saved on growth, and 20%

income tax saved on tax free lump sum.

www.fcfp.co.uk Twitter.com/francisclarkifa

Questions

?

www.fcfp.co.uk

No responsibility can be accepted for any action taken as a result of information contained in this

presentation. We therefore strongly recommend that no action should be taken before obtaining

detailed professional advice.

Past performance is not a guide to future returns and the value of investments and income from

them may go down as well as up and an investor may not get back the amount invested.

Francis Clark Financial Planning is a trading style for Francis Clark Financial Planning Limited,

which is authorised and regulated by the Financial Services Authority.

Registered Office: Sigma House, Oak View Close, Edginswell Park, Torquay, TQ2 7FF.

Registered in England No. 05413603

Exeter Plymouth Salisbury Taunton Tavistock Torquay Truro

This PowerPoint presentation is for general information only and is not intended to constitute professional advice.

Though Francis Clark Financial Planning Ltd is confident on its accuracy, no duty of care is assumed to any direct Recipient of this presentation and no liability is accepted for any

omission or inaccuracy.

Important Statement

Twitter.com/francisclarkifa

The Budget;

The Financial Planning view

March 2015

Thank you

www.francisclark.co.uk

(c) copyright Francis Clark LLP, 2015

You shall not copy, make available, retransmit, reproduce, sell, disseminate, separate, licence, distribute, store electronically, publish, broadcast or otherwise circulate either within

your business or for public or commercial purposes any of (or any part of) these materials and / or any services provided by Francis Clark LLP in any format whatsoever unless you

have obtained prior written consent from Francis Clark LLP to do so and entered into a licence.

To the maximum extent permitted by applicable law Francis Clark LLP excludes all representations, warranties and conditions (including, without limitation, the conditions implied

by law) in respect of these materials and /or any services provided by Francis Clark LLP.

These materials and /or any services provided by Francis Clark LLP are designed solely for the benefit of delegates of Francis Clark LLP. The content of these materials and / or

any services provided by Francis Clark LLP does not constitute advice and whilst Francis Clark LLP endeavours to ensure that the materials and / or any services provided by

Francis Clark LLP are correct, we do not warrant the completeness or accuracy of the materials and /or any services provided by Francis Clark LLP; nor do we commit to ensuring

that these materials and / or any services provided by Francis Clark LLP are up-to-date or error or omission-free.

Where indicated, these materials are subject to Crown copyright protection. Re-use of any such Crown copyright-protected material is subject to current law and related regulations

on the re-use of Crown copyright extracts in England and Wales.

These materials and / or any services provided by Francis Clark LLP are subject to our terms and conditions of business as amended from time to time, a copy of which is available

on request.

Our liability is limited and to the maximum extent permitted under applicable law Francis Clark LLP will not be liable for any direct, indirect or consequential loss or damage arising

in connection with these materials and / or any services provided by Francis Clark LLP, whether arising in tort, contract, or otherwise, including, without limitation, any loss of profit,

contracts, business, goodwill, data, income or revenue. Please note however, that our liability for fraud, for death or personal injury caused by our negligence, or for any other

liability is not excluded or limited.

Disclaimer & copyright