Fractal Forecasting of Financial Markets with Fraclet Algorithm

33

Fraclet Predictor Overview Presented by Quant Trade Technologies, Inc.

-

Upload

bzinchenko -

Category

Economy & Finance

-

view

172 -

download

4

Transcript of Fractal Forecasting of Financial Markets with Fraclet Algorithm

Fraclet Predictor Overview

Presented byQuant Trade Technologies, Inc.

2

Contents

Introduction/Motivation

Survey and Lag Plots

Exact Problem Formulation

Proposed Method› Fractal Dimensions Background› Our method

Results

Conclusions

3

General Problem Definition

Given a time series {xt

}, predict its future course, that is, xt+1

, xt+2

, ...

Time

Value?

4

Motivation

• Financial data analysis

• Physiological data, elderly care

• Weather, environmental studies

Traditional fields

Sensor Networks (MEMS, “SmartDust”)• Long / “infinite”

series

• No human intervention “black box”

5

Traditional Forecasting Methods

ARIMA but linearity assumption

Neural Networks but large number of parameters and long training times

Hidden Markov Models O(N2) in number of nodes N; also fixing N is a problem

Lag Plots

6

Lag Plots

xt-1

xxtt

4-NNNew Point

Interpolate these…

To get the final prediction

Q0: Interpolation Method

Q1: Lag = ?

Q2: K = ?

7

Q0: Interpolation

Using SVD (state of the art)

Xt-1

xt

8

Why Lag Plots?› Based on the “Takens’ Theorem”

[Takens/1981]› which says that delay vectors can be

used for predictive purposes

9

Inside Theory

Example: Lotka-Volterra

equations

ΔH/Δt = rH

–

aH*P ΔP/Δt = bH*P –

mP

H is density of prey P is density of predators

Suppose only H(t) is observed. Internal state is (H,P).

10

Problem at hand

Given {x1 , x2 , …, xN }

Automatically set parameters

- L(opt) (from Q1) - k(opt) (from Q2)

in Linear time on N

to minimise Normalized Mean Squared Error (NMSE) of forecasting

11

Transform Data

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

x(t)

x(t-1)

Logistic Parabola

X(t-1)

X(t)

The Logistic Parabola xt

= axt-1

(1-xt-1

) + noise

time

x(t)

Intrinsic Dimensionality

≈

Degrees of Freedom

≈

Information about Xt

given Xt-1

CIKM 2002Your logo here 12

Cube the Data

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

x(t)

x(t-1)

Logistic Parabola

x(t-1)

x(t)

x(t-2)

x(t)

x(t)

x(t-2)

x(t-2) x(t-1)

x(t-1)

x(t-1)

x(t)

13

How Much Data is Enough?

To find L(opt):› Go further back in time (ie., consider Xt-2 , Xt-3

and so on)› Till there is no more information gained

about Xt

14

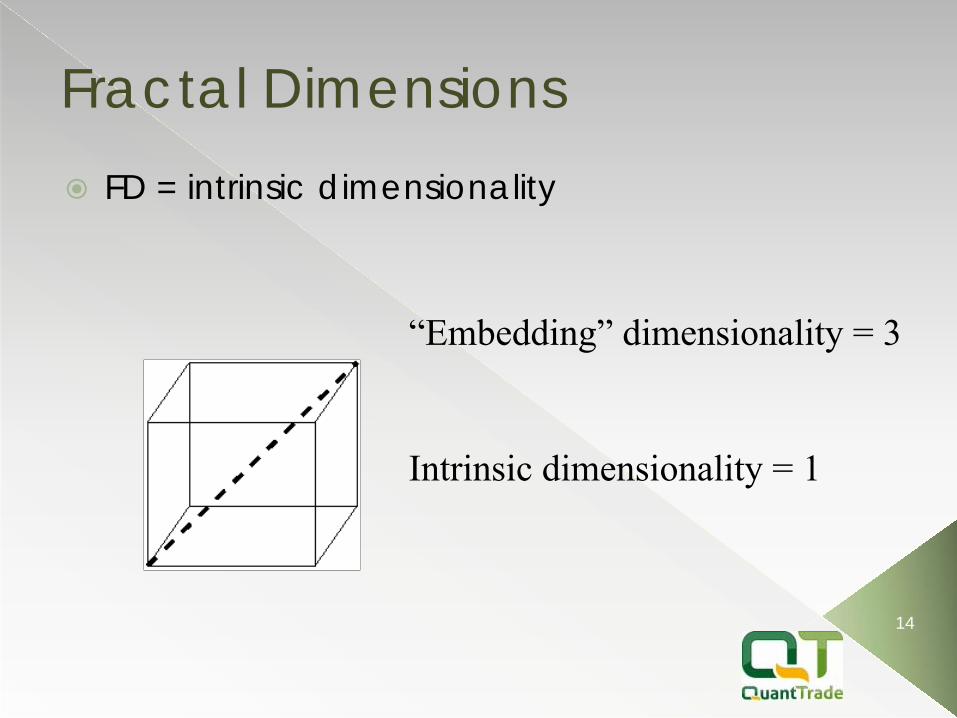

Fractal Dimensions

FD = intrinsic dimensionality

“Embedding”

dimensionality = 3

Intrinsic dimensionality = 1

15

Fractal Dimensions

FD = intrinsic dimensionality [Belussi/1995]

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 1.8 2

Y a

xis

X axis

Sierpinsky

7

8

9

10

11

12

13

14

15

16

-7 -6 -5 -4 -3 -2 -1 0 1 2

log

(# p

airs

with

in r

)

log(r)

FD plot

= 1.56

log(r)

log( # pairs)

Points to note:

• FD can be a non-integer

•

There are fast methods to compute it

16

Q1: Finding L(opt)

Use Fractal Dimensions to find the optimal lag length L(opt)

Lag (L)

Frac

tal D

imen

sion

epsilon

L(opt)

f

17

Q2: Finding k(opt)

To find k(opt)

• Conjecture: k(opt) ~ O(f)

We choose k(opt) =

2*f + 1

18

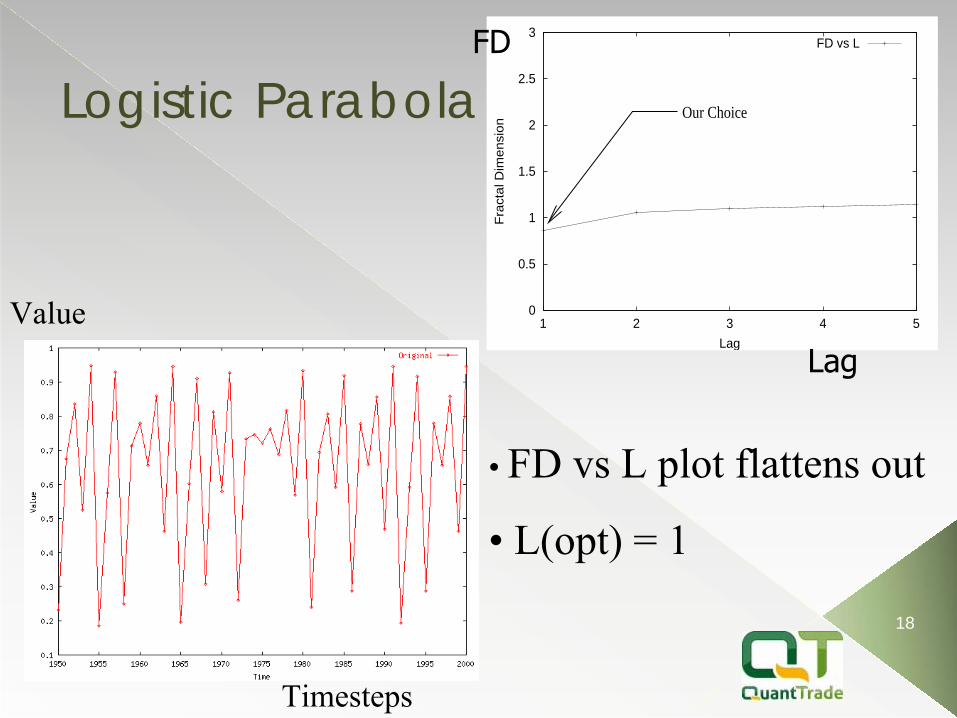

Logistic Parabola

0

0.5

1

1.5

2

2.5

3

1 2 3 4 5

Fra

ctal D

imensi

on

Lag

FD vs L

Our Choice

• FD vs

L plot flattens out

• L(opt) = 1

Timesteps

ValueLag

FD

19

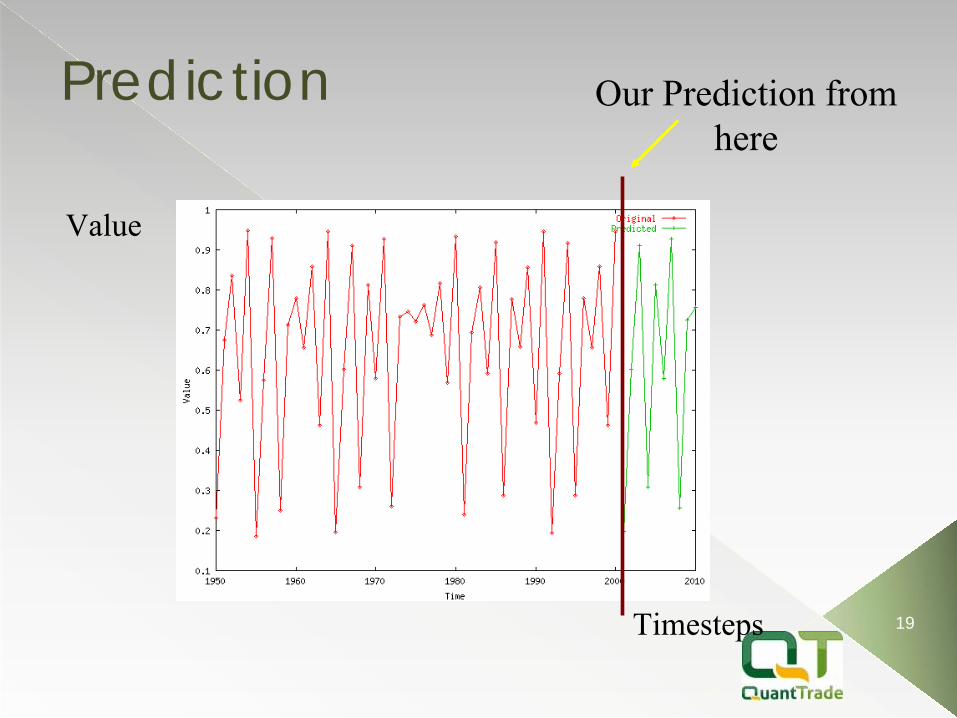

Prediction

Timesteps

Value

Our Prediction from here

20

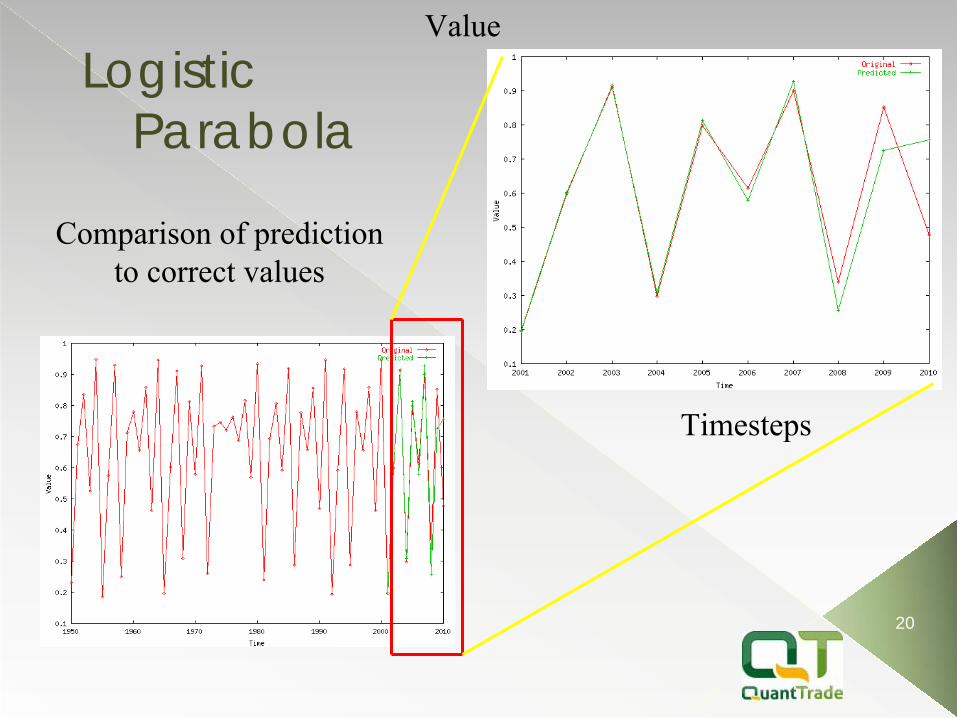

Logistic Parabola

Timesteps

Value

Comparison of prediction to correct values

21

Logistic Parabola

0

0.5

1

1.5

2

2.5

3

1 2 3 4 5

Fra

ctal

Dim

ensi

on

Lag

FD vs L

Our Choice

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

1 2 3 4 5 6

NM

SE

Lag

NMSE vs Lag

Our Choice

Our L(opt) = 1, which exactly minimizes NMSE

Lag

NM

SE

FD

22

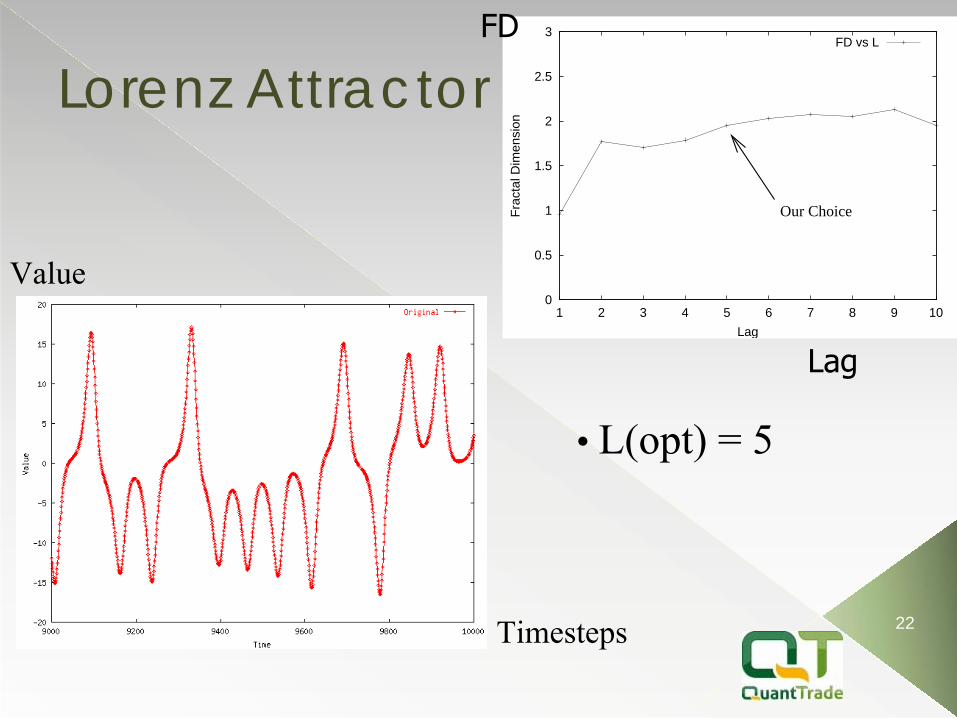

Lorenz Attractor

0

0.5

1

1.5

2

2.5

3

1 2 3 4 5 6 7 8 9 10

Fra

ctal

Dim

ensi

on

Lag

FD vs L

Our Choice

• L(opt) = 5

Timesteps

Value

Lag

FD

23

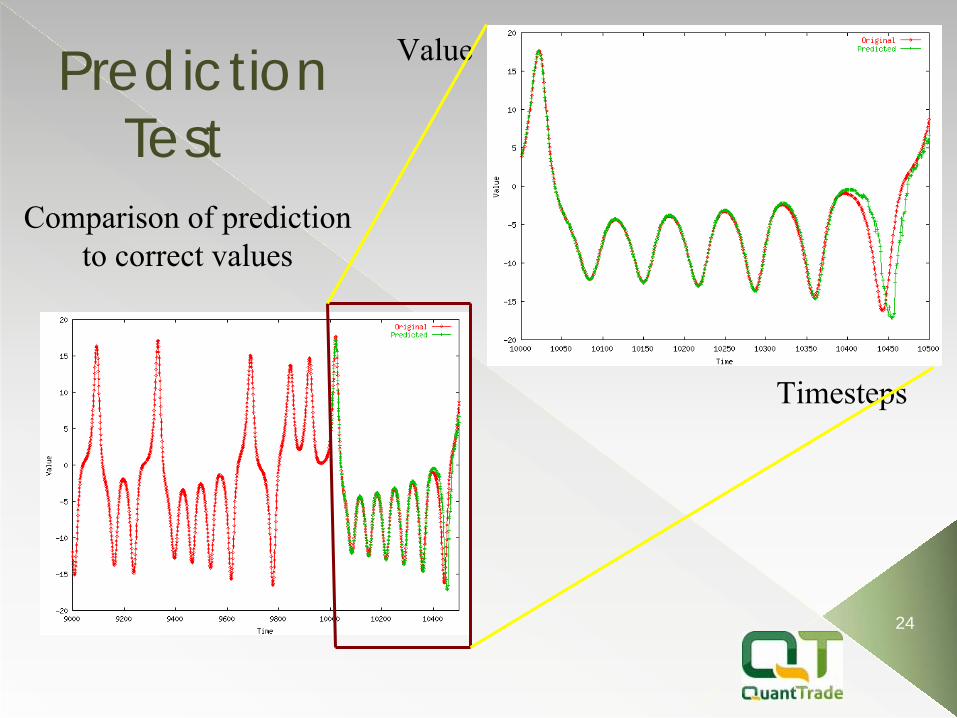

Lorenz Attractor Prediction

Value

Timesteps

Our Prediction from here

24

Prediction Test

Timesteps

Value

Comparison of prediction to correct values

25

Optimal Prediction

0

0.5

1

1.5

2

2.5

3

1 2 3 4 5 6 7 8 9 10

Fra

ctal

Dim

ensi

on

Lag

FD vs L

Our Choice

L(opt) = 5

Also NMSE is optimal at Lag = 5

0

0.2

0.4

0.6

0.8

1

0 2 4 6 8 10 12

NM

SE

Lag

NMSE vs Lag

Our Choice

Lag

NM

SE

FD

26

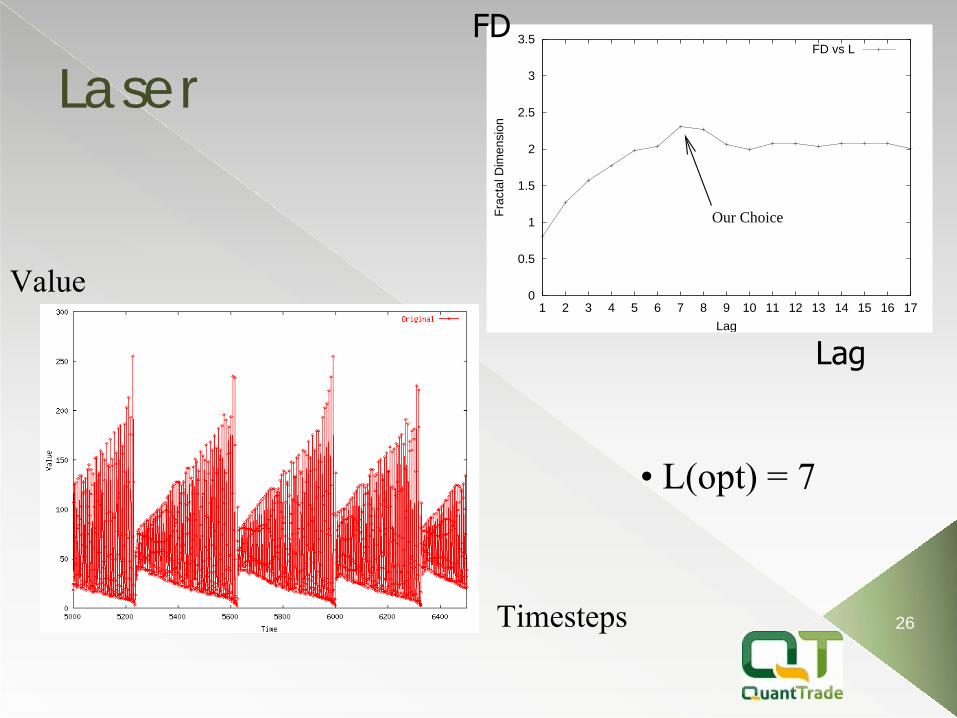

Laser

0

0.5

1

1.5

2

2.5

3

3.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Fra

ctal

Dim

ensi

on

Lag

FD vs L

Our Choice

• L(opt) = 7

Timesteps

Value

Lag

FD

27

Prediction

Timesteps

Value

Our Prediction starts here

28

Prediction Test

Timesteps

Value

Comparison of prediction to correct values

29

Optimal Prediction

0

0.5

1

1.5

2

2.5

3

3.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Frac

tal D

imen

sion

Lag

FD vs L

Our Choice

0

0.5

1

1.5

2

2.5

3

3.5

1 2 3 4 5 6 7 8 9 10 11 12 13

NM

SE

Lag

NMSE vs L

Our Choice

L(opt) = 7

Corresponding NMSE is close to optimal

Lag

NM

SE

FD

30

Speed and Scalability

Preprocessing is linear in N

Proportional to time taken to calculate FD

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2000 4000 6000 8000 100001200014000160001800020000

Pre

pro

cess

ing

Tim

e

Number of points (N)

Time vs N

31

The Fraclet Way

Our Method:

Automatically set parameters

L(opt) (answers Q1)

k(opt) (answers Q2)

In linear time on N

32

Conclusions

Black-box non-linear time series forecasting

Fractal Dimensions give a fast, automated method to set all parameters

So, given any time series, we can automatically build a prediction system

Useful in a sensor network setting

33

Pioneers in the fractal exploration of financial markets

Trading futures and options involves the risk of loss. You should consider carefully whether futures or options are appropriate to your financial situation. You must review the customer account agreement and risk disclosure prior to establishing an account. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of futures results. The risk of loss in trading futures or options can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition. Information contained, viewed, sent or attached is considered a solicitation for business.

Quant Trade, LLC has been a Commodity Futures Trading Commission (CFTC) registered Commodity Trading Advisor (CTA) since September 4, 2007 and a member of the National Futures Association (NFA).

Copyright @ 2012 Quant Trade, LLC. All rights reserved. No part of the materials including graphics or logos, available in this Web site may be copied, reproduced, translated or reduced to any electronic medium or machine- readable form, in whole or in part without written permission.

2 N Riverside PlazaSuite 2325Chicago, Illinois 60606Quant Trade LLC(872) 225-2110