Forward-Looking Decision Making - Stanford Universityrehall/Forward Looking Decision Making... ·...

144

Forward-Looking Decision Making Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

-

Upload

phungtuyen -

Category

Documents

-

view

214 -

download

0

Transcript of Forward-Looking Decision Making - Stanford Universityrehall/Forward Looking Decision Making... ·...

Forward-Looking Decision Making

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

The Gorman Lectures in Economics

Series Editor, Richard Blundell

Lawlessness and Economics: Alternative Modes ofGovernance,

Avinash K. Dixit

Rational Decisions,

Ken Binmore

Forward-Looking Decision Making:Dynamic-Programming Models Applied to Health,Risk, Employment, and Financial Stability,

Robert E. Hall

A series statement appears at the back of the book

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Forward-LookingDecision Making

Dynamic-Programming Models Appliedto Health, Risk, Employment, and

Financial Stability

Robert E. Hall

Princeton University Press

Princeton and Oxford

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Copyright © 2010 by Princeton University Press

Published by Princeton University Press,41 William Street, Princeton, New Jersey 08540

In the United Kingdom: Princeton University Press,6 Oxford Street, Woodstock, Oxfordshire OX20 1TW

All Rights Reserved

Library of Congress Cataloging-in-Publication Data

Hall, Robert Ernest, 1943–Forward-looking decision making : dynamicprogramming models applied to health, risk, employment,and financial stability / Robert E. Hall.

p. cm. – (The Gorman lectures in economics)Includes bibliographical references and index.ISBN 978-0-691-14242-5 (alk. paper)1. Households–Decision making–Econometric models.2. Families–Decision making–Econometric models.3. Decision making–Econometric models. I. Title.

HB820.H35 2010330.01′5195–dc22 2009042465

British Library Cataloging-in-Publication Data is available

This book has been composed in LucidaBright using TEXTypeset and copyedited by T&T Productions Ltd, London

Printed on acid-free paper. ©∞press.princeton.edu

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Contents

Foreword vii

Preface ix

1 Basic Analysis of Forward-LookingDecision Making 11.1 The Dynamic Program 11.2 Approximation 51.3 Stationary Case 61.4 Markov Representation 71.5 Distribution of the Stochastic Driving

Force 9

2 Research on Properties of Preferences 102.1 Research Based on Marshallian and

Hicksian Labor Supply Functions 132.2 Risk Aversion 152.3 Intertemporal Substitution 172.4 Frisch Elasticity of Labor Supply 192.5 Consumption–Hours Complementarity 20

3 Health 233.1 The Issues 233.2 Basic Facts 253.3 Basic Model 263.4 The Full Dynamic-Programming Model 313.5 The Health Production Function 35

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

vi Contents

3.6 Preference Parameters 363.7 Solving the Model 373.8 Concluding Remarks 38

4 Insurance 424.1 The Model 434.2 Calibration 454.3 Results 46

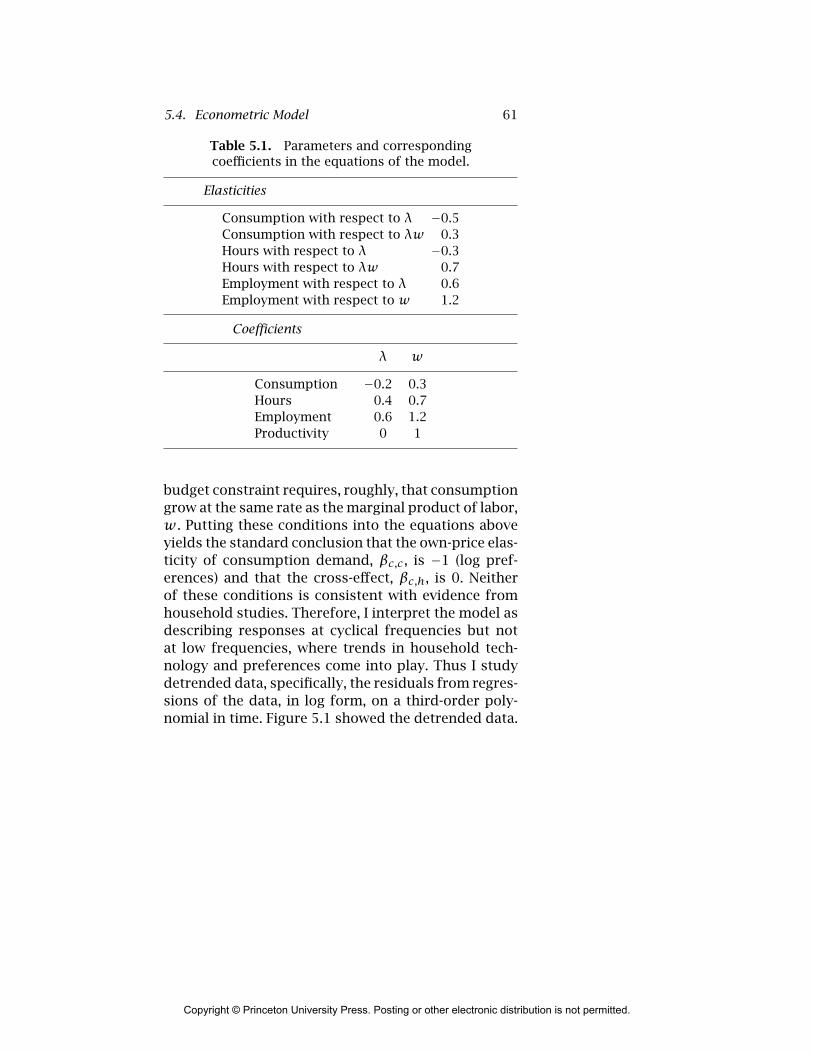

5 Employment 505.1 Insurance 525.2 Dynamic Labor-Market Equilibrium 535.3 The Employment Function 585.4 Econometric Model 595.5 Properties of the Data 645.6 Results 655.7 Concluding Remarks 69

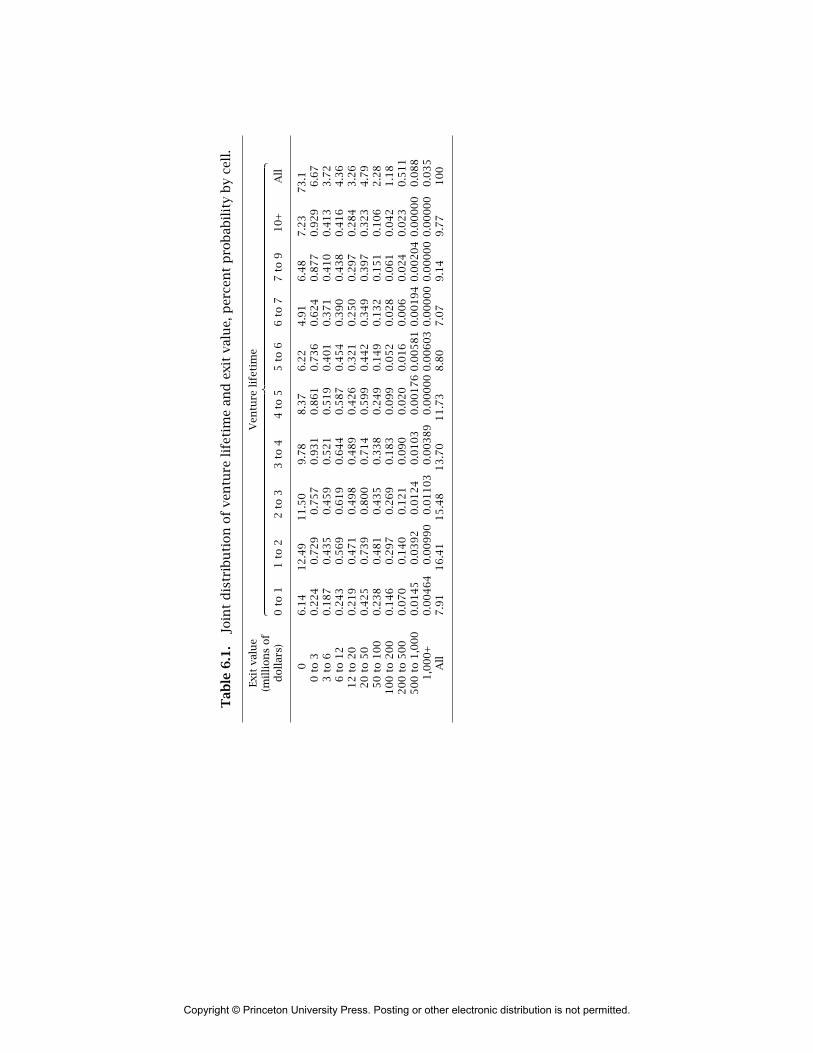

6 Idiosyncratic Risk 706.1 The Joint Distribution of Lifetime and

Exit Value 736.2 Economic Payoffs to Entrepreneurs 746.3 Entrepreneurs in Aging Companies 826.4 Concluding Remarks 85

7 Financial Stability withGovernment-Guaranteed Debt 877.1 Introduction 877.2 Options 927.3 Model 947.4 Calibration 1007.5 Equilibrium 1017.6 Roles of Key Parameters 1137.7 Concluding Remarks 1157.8 Appendix: Value Functions 116

References 119

Index 123

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Foreword

Forward-looking behavior is at the heart of economics.Choices over savings, occupations, earnings, invest-ments, etc., all require forward planning under uncer-tainty. Just how individuals and firms go about doingthis and how, as economists, we should best modelwhat they do are key to our understanding of eco-nomic behavior and are the core concern of this book.Few people have had such an impact on the devel-opment of these aspects of economics as has RobertHall.

This volume makes a compelling case for the useof the dynamic-programming approach to modelingchoices across a wide range of economic decision mak-ing. Not just forward-looking consumption and labormarket decisions, but also health-care choices, wherethe payoff is measured in terms of future quality oflife. Entrepreneurial startup decision making underuncertainty is carefully examined too and a coherentframework for examining moral hazard issues in theprovision of insurance to the risks faced on uncertaininvestments is provided, using this to show the valueof venture investors.

The reader is introduced to the dynamic-program-ming approach to modeling forward-looking behav-ior in an accessible but rigorous way, emphasizingthe relationship to the choices being made by the de-cision maker and the key issues the researcher willface in practical implementation. The key preference

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

viii Foreword

parameters required for modeling choices are de-scribed as well as how to recover them from empir-ical analysis in a fashion that is consistent with theforward decision making framework.

We were extremely fortunate to have Robert Hallpresent these ideas in the Gorman Lecture series andit is wonderful to have them now brought together inone volume.

Richard BlundellUniversity College LondonInstitute for Fiscal Studies

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Preface

When Richard Blundell asked me to give the GormanLectures, I instantly accepted, but it raised the ques-tion of whether there was any common theme in mycurrent research. In addition to my career-long strug-gle to understand fluctuations in the labor market, myrecent work has looked at aggregate health spending,entrepreneurship, and financial instability. It dawnedon me that I had approached this heterogeneous col-lection of subjects with a common analytical core—afamily or personal dynamic program. In all of the mod-els, people balance the present against the future. Sothe unifying feature of the chapters in this volume isa modeling approach.

The first chapter quickly reviews ideas about dy-namic programs, a topic likely to be familiar to manyreaders. I make some suggestions about numericalsolution and the representation of solved models asMarkov processes that may be novel to practition-ers. Chapter 2 surveys recent research of the parame-ters of preferences that often appear in personal dy-namic programs: the intertemporal elasticity of sub-stitution, the Frisch elasticity of labor supply, and theFrisch cross-elasticity, a topic that has gained a lot ofattention recently.

Chapter 3 covers the first substantive model, oneof aggregate health spending, developed jointly withCharles Jones. Here families divide current resourcesbetween consumption and health care; the payoff to

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

x Preface

health care is lowered mortality and increased qual-ity of life. Formulating the dynamic program requiresclose attention to modeling preferences for length oflife. We also use econometric estimates of the rela-tion between health spending and life extension. Weargue that the rise in the share of GDP devoted tohealth is consistent with optimal choice and is not anautomatic sign of waste. The dynamic program has alarge number of state variables, but is analytically be-nign because the value function is linear in the statevariables.

Throughout my work using family dynamic pro-grams, I have been aware that I was part of a largegroup of applied economists using Richard Bellman’suseful tool. We teach dynamic programming to allfirst-year Ph.D. students, and, not surprisingly, theyreach for it to solve many problems of intertemporalchoice. Chapter 4 discusses a fine example of workon an important policy issue by two leading appliedeconomists, Jeffrey Brown and Amy Finkelstein. Theystudy the adverse effects of the availability of pub-lic insurance for nursing home and other long-termcare on the demand for private insurance for that risk.Their dynamic program places a value on the gains tofamilies if private insurance could be used in conjunc-tion with public benefits, a practice currently barredin the United States.

Chapter 5 discusses my current thinking about fluc-tuations in the labor market. The model seeks to ex-plain a finding that has troubled me and many othermacroeconomists: the apparent inefficiency that oc-curs in a recession, when idleness among workersseems to signify a low marginal value of time, butmeasures of the marginal product of labor do not

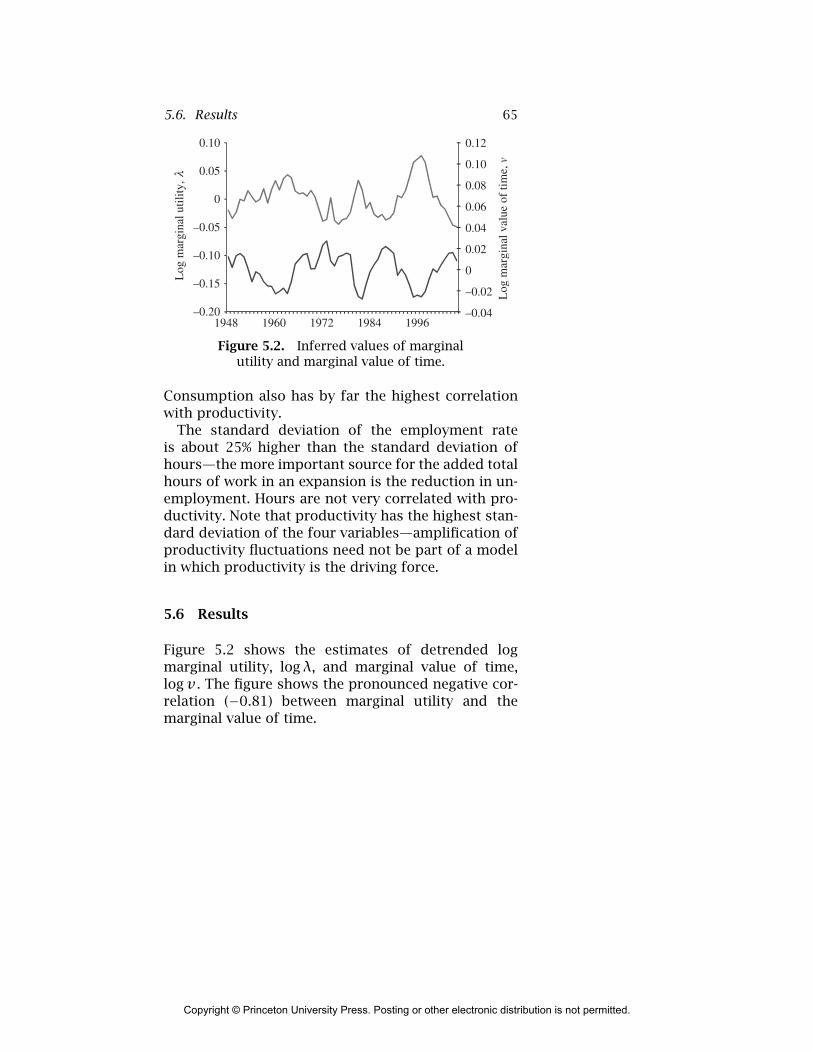

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Preface xi

fall that low. A family dynamic program, using pref-erences from chapter 2, seems to track consump-tion and weekly hours of work quite reasonably, sothe remaining issue is movements in unemployment.Here I incorporate ideas from the recent literature onsearch-and-matching frictions.

Chapter 6 concerns family economics in two senses,because it is joint work with my economist wife,Susan Woodward, who has assembled a rich bodyof data on outcomes for entrepreneurs who are inventure-backed startup companies. The dynamic pro-gram gives a unified treatment to two kinds of risk fac-ing the entrepreneurs—the amount of the eventual fi-nancial reward and the effort needed to achieve the re-ward. Insurance against the risk would be hugely ben-eficial to entrepreneurs but is impractical because ofmoral hazard and adverse selection. Venture investorslimit the payoff to a share of the ultimate value of thecompany to give a powerful incentive to the entrepre-neur and to avoid giving money away to people whodo not have commercially valuable ideas.

Chapter 7 responds to current financial turmoil bylooking at one issue: the potential contribution to in-stability from government guarantees of private debt.The effect of a guarantee is to create a joint incentivefor borrowers and lenders to harvest the guarantee,which enriches the borrower directly and thus influ-ences the terms of the deal between the borrower andlender. When financial institutions are facing substan-tial probabilities of default, families consume more,because the government may bail out their extra con-sumption. The rise in consumption drives down inter-est rates. Some of the features of financial crises mayresult from the factors considered in the model.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

xii Preface

I am pleased to contribute to the activities that re-member and honor Terence Gorman. He was a ma-jor influence on my development as an economist,though I spent little time with him personally. Un-like many of his colleagues, he was not inclined tospend much time touring the colonies. Reading the re-marks at Terence’s memorial in 2003, including thoseof my thesis adviser, Robert Solow, reminded me ofhow thoroughly I was under Terence’s influence. Hisfavorite topics of capital aggregation and duality weremuch in the air when I was a graduate student atMIT in the mid 1960s. My first sole-authored profes-sional publication—in the Review of Economic Studies,naturally—dealt with exactly these topics.

I was lucky enough to spend the amazing years 1967to 1970 at Berkeley, and take part in a revolution inthinking about household and production economics.Dan McFadden taught me modern theory in this area,much under Terence’s influence. Frank Hahn’s remarkat the memorial about Terence’s remaking of con-sumer theory aptly captures what I learned in Berke-ley: “It banished nasty bordered Hessians… it substi-tuted the much deeper and simpler notions of con-cavity and convexity, and made this branch of theoryreally quite beautiful.”

I am grateful to University College London for host-ing me for a week in connection with the lecturesand providing many opportunities to discuss the workwith many of the world’s experts in the areas of myinterests. I thank, as ever, the Hoover Institution forsupporting my research over the past thirty years andCharlotte Pace for running my office and making manyimprovements to the manuscript. The National Bureauof Economic Research provided numerous opportuni-ties to air the work and receive needed criticism.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Preface xiii

My website (Google “Bob Hall”) contains a largeamount of supporting material for the research dis-cussed in this book, including data and Matlab pro-grams.

Chapters 2 and 5 draw from my paper, “Reconcil-ing cyclical movements in the marginal value of timeand the marginal product of labor,” Journal of Po-litical Economy, April 2009, pp. 281–323, used withpermission of the publisher, © 2009 by the Univer-sity of Chicago. Chapter 3 draws from my paperwith Charles I. Jones, “The value of life and the risein health spending,” Quarterly Journal of Economics,February 2007, pp. 39–72, used with permission ofthe publisher, © 2007 by the President and Fellowsof Harvard College and the Massachusetts Instituteof Technology. Figure 4.1 is used with permissionfrom Jeffrey R. Brown and Amy Finkelstein from theirpaper, “The interaction of public and private insur-ance: Medicaid and the long-term care insurance mar-ket,” American Economic Review, September 2008,pp. 1083–102, © 2008 by the American Economic As-sociation. Chapter 6 draws from my paper with SusanWoodward, “The burden of the nondiversifiable risk ofentrepreneurship,” American Economic Review, forth-coming, used with permission of the publisher, © 2009by the American Economic Association.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Forward-Looking Decision Making

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

1Basic Analysis ofForward-LookingDecision Making

Individuals and families make the key decisions thatdetermine the future of the economy. The decisionsinvolve balancing current sacrifice against future ben-efits. People decide how much to invest in healthcare, exercise, and good diet, and so determine theirlongevity and future satisfaction. They make choicesabout jobs that determine employment and unem-ployment levels. Their investment decisions are at theheart of some issues of financial stability.

1.1 The Dynamic Program

Economists have gravitated to the dynamic programas the workhorse model of the way that people bal-ance the present against the future. The dynamic pro-gram is one of the two tools economists tend to reachfor when solving problems of optimization over time.The other is the Euler equation. The two approachesare perfectly equivalent: if a problem is susceptibleto solution by a dynamic program, it is susceptible toan Euler equation solution, and vice versa. The class

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2 1. Basic Analysis

of models suited to either method have the propertythat the trade-off between this year and next year—the marginal rate of substitution—depends only onconsumption this year and next year. Utility functionswith this property are additively separable. They havethe form, ∑

tβtu(xt), (1.1)

where xt is a vector of things the family cares about.In words, the idea of a dynamic program is to sum-

marize the entire future in a value function, whichshows how much lifetime utility the family will enjoystarting next year based on the resources for futurespending left after this year. People makes choicesabout this year by balancing the immediate marginalbenefits from using resources this year against themarginal value of the remaining resources as of nextyear, according to the value function. A dynamic pro-gram uses backward recursion. Start with a known orassumed value function for some distant year. Findthe value function in the previous year by solving theyear-to-year balancing problem for all possible levelsof resources in that year. Keep moving backward intime until you reach a year from now. Finally, solvethis year’s optimization by taking actual resourcesand solving the balancing problem for this year’sutility and next year’s value function. The dynamic-programming approach is conceptually simple andnumerically robust. A famous book by Stokey and Lu-cas (1989) helped persuade economists of the virtuesof dynamic programming for recursive problems.

The Euler equation approach considers a possiblechoice this year and then uses the marginal rate ofsubstitution to map it into a choice next year. Apply

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

1.1. The Dynamic Program 3

this as a forward recursion, to see where the immedi-ate choice leads to at some distant future date. Again,as in the dynamic program, you need to have someconcept of a distant target—for example, the familycannot be deeply in debt at that time. Keep trying outinitial choices to find the one where the family meetsits distant target. Though this approach has some ap-peal in explaining dynamic models, it fails completelyas a way to solve models numerically. The Euler equa-tion is numerically unstable. Good methods exist fordealing with the instability, but are rarely used inmodern dynamic economics because the dynamic pro-gram approach works so well. The instability of theEuler equation creates conceptual confusion as well,because one might fall into the trap of thinking thatthe aberrant paths that do not reach the target mightdescribe actual behavior.

All the models in this book rest on dynamic pro-gramming. At the beginning of the year, the familyinherits some state variables as a result of choicesmade last year and events during that year. Thesecould be wealth, health status, employment status, ordebt. The family picks values of choice variables: con-sumption, health spending, job search, or borrowing.A law of motion shows how the inherited values ofthe state variables, the values of the choice variables,and events during the year map into next year’s val-ues of the state variables. The events include financialreturns, health outcomes, job loss, and fluctuations inearnings.

The Bellman equation describes the condition forrecursive optimization:

Vt(st) = maxxt(ut(st, xt)+ βEt Vt+1(st+1)). (1.2)

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

4 1. Basic Analysis

Here V(s) is the value function, which assigns life-time expected utility based on the state variables, s.The choice variables are in the vector xt . The functionu(s,x) is the period utility that describes the flow ofsatisfaction that the family receives when choosing xgiven s. The general law of motion is

st+1 = ft(st, xt, εt). (1.3)

Here εt describes the random events that occur duringyear t. Anything about year t that is known in advancecan be built into the function ft .

As a simple example, consider the standard life-cycle saving model. The single state variable is wealth,Wt . The only choice variable is current consumption,ct . The Bellman equation is

Ut(Wt) = maxct(u(ct)+ βEεt Ut+1(Wt+1)) (1.4)

and the law of motion for wealth is

Wt+1 = (1+ rt)(Wt − ct +yt + εt). (1.5)

Here rt is the known, time-varying return to savings,yt is the known part of income, and εt is the randompart of income. Although it would be easy to writedown the first-order condition for the maximizationin the Bellman equation, the condition usually doesnot add much to understanding. The best approachis often just to leave the maximization to software(Matlab).

As I noted earlier, to solve for the family’s optimalchoice this year, xt , start with a known value func-tion in some distant year T , VT(sT ), iterate backwardsto find Vt+1, and then solve the Bellman equation forthe optimal xt . Sometimes (but never in this book),the value functions have known functional forms. For

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

1.2. Approximation 5

the great majority of interesting problems, the func-tions need to be represented as well-chosen approx-imations. Judd (1998) discusses this topic at an ad-vanced level. The state variables may be discrete orcontinuous. Discrete variables might tell whether aperson was employed or unemployed, or well or sick.Discrete variables may also describe random outsideevents, even some, such as financial returns, thatmight be considered continuous. Endogenous statevariables such as wealth, that result from choices thatare continuous, need to be treated as continuous. Oneshould avoid the temptation to convert them to dis-crete variables, as the resulting approximation is hardto manage and gives unreliable results.

Handling discrete state variables is straightforward:just subscript the value function by the discrete state.Thus the Bellman equation when st is discrete is

Vst,t = maxxt(ut(st, xt)+ βEt Vst+1,t+1). (1.6)

1.2 Approximation

Many interesting models have only a single continuousstate variable, including all the models in this book.A useful family of approximations in that case is aweighted sum of known functions of s. Let φi(s) de-note these known functions—typically there are sev-eral hundred of them. It is convenient to normalizethem so that they equal 1 at a give value si and 0 atthe points corresponding to other of the functions:

φi(si) = 1 and φj(si) = 0, j ≠ i. (1.7)

The approximation is

Vt(s) =∑iφi(s)Vi,t. (1.8)

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

6 1. Basic Analysis

Under the normalization of the φs, the value Vi,t isthe value of Vt(s) at s = si. The approximation inter-polates between the Vi,t points for intermediate valuesof s. The point defined by an si and Vi pair is called aknot.

A convenient choice for the interpolation functionsis a tent:

φi(s) = 0 if s � si−1

= s − si−1

si − si−1if si−1 < s � si

= si+1 − ssi+1 − si

if si < s � si+1

= 0 if s � si+1. (1.9)

The function Vt(s) is then the linear interpolation be-tween the knots.

Given a set of interpolation functions, the backwardrecursion to find the current knot values is

Vi,t = maxxt(ut(si, xt)+ βEεt Ut+1(ft(si, xt, εt))).

(1.10)For the models in this book, with twenty years of back-ward recursion and 500 knots in the approximation tothe value function, a standard PC, vintage 2008, takesaround half a minute to calculate the value functions.

When calculating the value functions, it is usuallya good idea to store away the choice functions, rep-resented as values xi,t of the optimal choice at timet given state variable value si (these are also calledpolicy functions).

1.3 Stationary Case

Sometimes the stationary value function is interest-ing. Suppose that the decision maker is embedded

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

1.4. Markov Representation 7

in an unchanging environment with the random εsdrawn from an unchanging distribution. Suppose fur-ther that the horizon is infinite. Then the value func-tion becomes stationary, in the sense that it loses itstime subscript. The stationary approximating Bellmanequation is

Vi = maxx(u(si, x)+ βEε V(f(si, x, ε))). (1.11)

To find the values Vi that solve this equation, we cantreat the Bellman equation as a big system of nonlin-ear equations to be solved for the unknowns, Vi. Thismethod is called projection and can be tricky, but whenit works it is usually fast. An alternative, foolproofmethod is value function iteration. Start with arbitraryVi, put them on the right-hand side of the Bellmanequation, and calculate a new set. Iterate this oper-ation to convergence, which is guaranteed (see Judd1998, p. 412). This approach can be slow for biggerproblems (Judd discusses a number of ways to speedit up).

1.4 Markov Representation

The solution to the dynamic program describes theway a decision maker responds to an uncertain en-vironment. From the stochastic driving force ε, themodel generates the decision maker’s stochastic re-sponse, in the sense of the joint distribution of theendogenous variables of the model. Most researchersdescribe the joint distribution by simulation. Theystart at given values of the state variables s, evaluatethe choice functions x(s), draw a random ε from theappropriate distribution, compute the new state vec-tor from the law of motion, and continue for many

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

8 1. Basic Analysis

simulated years. But simulation is extremely ineffi-cient: to drive down the sampling errors from simu-lation, which cause the joint distribution of the sim-ulated data to differ from the true joint distributiongenerated by the model, to acceptable low values, youmay need to simulate for days. Some (but not all) of theaspects of the joint distribution are available with es-sentially perfect accuracy by direct calculation ratherthan simulation.

A recursive model is a Markov process. For givencurrent values of the state variables s, the choice func-tions and the law of motion generate a probability dis-tribution across states in the coming year. If the modelis stationary, the Markov process has constant proba-bilities; otherwise, they vary with time. A Markov pro-cess is fully defined by its transition matrix. Interest-ing aspects of the joint distribution can be calculatedby standard matrix operations applied to the matrix.For example, transition probabilities over more thanone year are powers of the transition matrix and thestationary probabilities of a stationary model can becalculated in no time by matrix inversion.

For a continuous state variable, the true transitionmatrix is infinitely big, so again we need to use an ap-proximation. I treat the model as assuming that thestate variables originate from only the grid of pointsused in the earlier approximation, si. Then I calculatethe transition probability from state si this year to s′inext year as the probability that a person starting fromthe exact point si this year winds up in an interval con-taining si′ next year. The interval runs from halfwaybetween si′−1 and si′ to halfway between si′ and si′+1. Idenote the transition probability as Πi,i′ and calculate

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

1.5. Distribution of the Stochastic Driving Force 9

it as

Πi,i′ = Prob[si′−1 + si′

2� f(si, xi, ε) <

si′ + si′+1

2

].

(1.12)Solve the linear system πΠ = π and

∑i πi = 1 to find

stationary probabilities πi.

1.5 Distribution of the Stochastic Driving Force

The calculation of the Bellman equation requires theevaluation of an expectation over the distribution ofthe random ε. One could imagine assuming a continu-ous distribution of the disturbance with a known func-tional form and performing an analytic or numericalintegration to form the expectation. But it is rare toknow that the disturbance has a particular functionalform and often impossible to do the integration ana-lytically and challenging to do it numerically. It is usu-ally better to use a purely empirical distribution. Forexample, if the disturbance is productivity, one cantake 50 realizations of actual productivity. The inte-gration is replaced by adding up the value functionat 50 values and dividing by 50. Chapter 6 takes thisapproach with 14,000 values of startup companies.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2Research on Properties

of Preferences

The studies in this book use information about pref-erences from research on individual behavior. Con-sider the standard intertemporal consumption–hoursproblem without unemployment,

max Et

∞∑τ=0

δτU(ct+τ, ht+τ), (2.1)

subject to the budget constraint,∞∑τ=0

Rt,τ(wt+τht+τ − ct+τ) = 0. (2.2)

Here Rt,τ is the price at time t of a unit of goodsdelivered at time t + τ .

I let c(λ, λw) be the Frisch consumption demandandh(λ, λw) be the Frisch supply of hours per worker.See Browning et al. (1985) for a complete discussion ofFrisch systems in general. The functions satisfy

Uc(c(λ, λw),h(λ, λw)) = λ (2.3)

andUh(c(λ, λw),h(λ, λw)) = −λw. (2.4)

Here λ is the Lagrange multiplier for the budget con-straint.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2. Research on Properties of Preferences 11

The Frisch functions have symmetric cross-price re-sponses: c2 = −h1. They have three basic first-orderor slope properties:

• Intertemporal substitution in consumption,c1(λ, λw), the response of consumption tochanges in its price.

• Frisch labor-supply response, h2(λ, λw), theresponse of hours to changes in the wage.

• Consumption–hours cross-effect, c2(λ, λw), theresponse of consumption to changes in thewage (and the negative of the response of hoursto the consumption price). The expectedproperty is that the cross-effect is positive,implying substitutability between consumptionand hours of nonwork or complementaritybetween consumption and hours of work.

Consumption and hours are Frisch complements ifconsumption rises when the wage rises (work risesand nonwork falls); see Browning et al. (1985) for adiscussion of the relation between Frisch substitutionand Slutsky–Hicks substitution. People consume morewhen wages are high because they work more and con-sume less leisure. Browning et al. (1985) show thatthe Hessian matrix of the Frisch demand functions isnegative semi-definite. Consequently, the derivativessatisfy the following constraint on the cross-effectcontrolling the strength of the complementarity:

c22 � −c1h2. (2.5)

Each of these responses has generated a body of lit-erature. In addition, in the presence of uncertainty, thecurvature of U controls risk aversion, the subject ofanother literature.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

12 2. Research on Properties of Preferences

To understand the three basic properties of con-sumer–worker behavior listed earlier, I draw primarilyupon research at the household rather than the ag-gregate level. The first property is risk aversion andintertemporal substitution in consumption. With ad-ditively separable preferences across states and timeperiods, the coefficient of relative risk aversion andthe intertemporal elasticity of substitution are recip-rocals of one another. But there is no widely accepteddefinition of measure of substitution between pairs ofcommodities when there are more than two of them.Chetty (2006) discusses two natural measures of riskaversion when hours of work are also included in pref-erences. In one, hours are held constant, while in theother, hours adjust when the random state becomesknown. He notes that risk aversion is always greaterby the first measure than the second. The measuresare the same when consumption and hours are neithercomplements nor substitutes.

The rest of this chapter summarizes the findingsof recent research on the three key properties of theFrisch consumption demand and labor supply sys-tem. The own-elasticities have been studied exten-sively. I believe that a fair conclusion from the re-search is that Frisch elasticity of consumption demandis βc,c = −0.5 and the Frisch elasticity of hours supplyis βh,h = 0.7.

The literature on measurement of the cross-elastici-ty is sparse, but a substantial amount of research hasbeen done on the decline in consumption that occurswhen a person moves from normal hours of work tozero because of unemployment or retirement. The ra-tio of unemployment consumption cu to employmentconsumption ce reflects the same properties of pref-erences as does the Frisch cross-elasticity. I use the

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2.1. Research Based on Labor Supply 13

parametric utility function in Hall and Milgrom (2008)to find the cross-elasticity that corresponds to the con-sumption ratio of 0.85. It is a Frisch cross-elasticity ofβc,h = 0.3.

2.1 Research Based on Marshallian and HicksianLabor Supply Functions

The Marshallian labor supply function gives hours ofwork as a function of the wage and the individual’swealth. The Hicksian labor supply function replaceswealth with utility. The elasticity of the Marshallianfunction with respect to the wage is the uncompen-sated wage elasticity of labor supply and the elastic-ity of the Hicksian function is the compensated wageelasticity. Both are paired with consumption demandfunctions with the same arguments.

For simplicity, I will discuss the relation of the Mar-shallian and Hicksian functions to the Frisch functionsused in chapter 5 with a normalization such that theelasticities are also derivatives. I consider the prop-erties of the functions at a point normalized so thatconsumption, hours, the wage, and marginal utility λare all 1. In this calibration, nonwage wealth is takento be zero; this is not a normalization. The research Iconsider treats wage changes as permanent, in whichcase we can examine a static Marshallian labor sup-ply function where wealth is replaced by permanentincome.

From the budget constraint,

c(λ, λw)−wh(λ,λw) = x, (2.6)

where x is nonwage permanent income, I differentiatewith respect to x, replace the derivatives of the Frisch

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

14 2. Research on Properties of Preferences

functions with the β elasticities, and set x = 0 to findthe Marshallian income effect:

− βh,h − βc,hβh,h − βc,c − 2βc,h

. (2.7)

By a similar calculation, the Marshallian uncompen-sated labor elasticity is

βh,h −(βh,h − βc,h)2 + βh,h − βc,h

βh,h − βc,c − 2βc,h. (2.8)

The Hicksian compensated wage elasticity of laborsupply is the difference between the Marshallian elas-ticity and the income effect:

βh,h −(βh,h − βc,h)2

βh,h − βc,c − 2βc,h. (2.9)

The compensated elasticity is nonnegative.Chetty (2006) takes an approach similar to the one

suggested by these relations, though without explicitreference to the Frisch functions. He shows that thevalue of the coefficient of relative risk aversion (or,though he does not pursue the point, the inverse of theintertemporal elasticity of substitution in consump-tion, −1/βc,c) is implied by a set of other measures.He solves for the consumption curvature parameter bydrawing estimates of responses from the literature onlabor supply. One is consumption–hours complemen-tarity. The others are the compensated wage elasticityof static labor supply and the elasticity of static laborsupply with respect to unearned income.

The following exercise gives results quite similar toChetty’s. From his table 1, reasonable values for theincome elasticity and the compensated wage elastic-ity from labor supply estimates in the Marshallian–Hicksian framework are−0.11 and 0.4. For the income

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2.2. Risk Aversion 15

elasticity, the work of Imbens et al. (2001) is partic-ularly informative. The paper tracks the response ofearnings of winners of significant prizes in lotteries. Itfinds an income elasticity of 0.10. The range of valuesof the Frisch parameters that are consistent with theseresponses is remarkably tight with respect to the wageelasticity βh,h. If the elasticity is 0.45, the complemen-tarity parameter is βc,h = 0, its minimum reasonablevalue, and the own-price elasticity of consumption isβc,c = −3.67, an unreasonable magnitude. The mini-mum compensated wage elasticity is 0.4, in which casethe own-price elasticity of consumption is -0.4 and thecomplementarity parameter is 0.4, at the outer limitof concavity. At βh,h = 0.402, the other elasticities areβc,c = −0.53 and βc,h = 0.38, not too far from the val-ues used in chapter 5 of βh,h = 0.7, βc,c = −0.5, andβc,h = 0.3. The static labor-supply literature is reason-ably consistent with the other research considered inthis chapter. It is completely inconsistent with com-pensated or Frisch elasticities of labor supply in therange of 1 or above.

2.2 Risk Aversion

Research on the value of the coefficient of relative riskaversion (CRRA) falls into several broad categories.In finance, a consistent finding within the frameworkof the consumption capital-asset pricing model isthat the CRRA has high values, in the range from10 to 100 or more. Mehra and Prescott (1985) be-gan this line of research. A key step in its develop-ment was Hansen and Jagannathan’s (1991) demon-stration that the marginal rate of substitution—theuniversal stochastic discounter in the consumption

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

16 2. Research on Properties of Preferences

CAPM—must have extreme volatility to rationalize theequity premium. Models such as that of Campbell andCochrane (1999) generate a highly volatile marginalrate of substitution from the observed low volatil-ity of consumption by subtracting an amount almostequal to consumption before measuring the MRS. I amskeptical about applying this approach in a model ofhousehold consumption.

A second body of research considers experimentaland actual behavior in the face of small risks and gen-erally finds high values of risk aversion. For example,Cohen and Einav (2007) find that the majority of car in-surance purchasers behave as if they were essentiallyrisk neutral in choosing the size of their deductible,but a minority are highly risk averse, so the averagecoefficient of relative risk aversion is about 80. But anyresearch that examines small risks, such as having topay the amount of the deductible or choosing amongthe gambles that an experimenter can offer in the lab-oratory, faces a basic obstacle. Because the stakes aresmall, almost any departure from risk neutrality, wheninflated to its implication for the CRRA, implies a gi-gantic CRRA. The CRRA is the ratio of the percentageprice discount off the actuarial value of a lottery to thepercentage effect of the lottery on consumption. Forexample, consider a lottery with a $20 effect on wealth.At a marginal propensity to consume out of wealth of0.05 per year and a consumption level of $20,000 peryear, winning the lottery results in consumption thatis 0.005% higher than losing. So if an experimental sub-ject reports that the value of the lottery is 1%—say, 10cents—lower than its actuarial value, the experimentconcludes that the subject’s CRRA is 200!

Remarkably little research has investigated theCRRA implied by choices over large risky outcomes.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2.3. Intertemporal Substitution 17

One important contribution is Barsky et al. (1997).This paper finds that almost two thirds of respondentswould reject a new job with a 50% chance of doublingincome and a 50% chance of cutting income by 20%.The cutoff level of the CRRA corresponding to reject-ing the hypothetical new job is 3.8. Only a quarter ofrespondents would accept other jobs correspondingto CRRAs of 2 or less. The authors conclude that mostpeople are highly risk averse. The reliability of thiskind of survey research based on hypothetical choicesis an open question, though hypothetical choices havebeen shown to give reliable results when tied to morespecific and less global choices, say, among differentnew products.

2.3 Intertemporal Substitution

Attanasio et al. (1999) and Attanasio and Weber (1993,1995) are leading contributions to the literature on in-tertemporal substitution in consumption at the house-hold level. These papers examine data on total con-sumption (not food consumption, as in some otherwork). They all estimate the relation between con-sumption growth and expected real returns from sav-ing, using measures of returns available to ordinaryhouseholds. All of these studies find that the elasticityof intertemporal substitution is around 0.7.

Barsky et al. (1997) asked a subset of their respon-dents about choices of the slope of consumption un-der different interest rates. They found evidence ofquite low elasticities, around 0.2.

Guvenen (2006) tackles the conflict between the be-havior of securities markets and evidence from house-holds on intertemporal substitution. With low sub-stitution, interest rates would be much higher than

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

18 2. Research on Properties of Preferences

are observed. The interest rate is bounded from be-low by the rate of consumption growth divided bythe intertemporal elasticity of substitution. Guvenen’sresolution is in heterogeneity of the elasticity andhighly unequal distribution of wealth. Most wealth isin the hands of those with elasticity around 1, whereasmost consumption occurs among those with lowerelasticity.

Finally, Carroll (2001) and Attanasio and Low (2004)have examined estimation issues in Euler equationsusing similar approaches. Both create data from theexact solution to the consumer’s problem and thencalculate the estimated intertemporal elasticity fromthe standard procedure, instrumental-variables es-timation of the slope of the consumption-growth–interest-rate relation. Carroll’s consumers face perma-nent differences in interest rates. When the interestrate is high relative to the rate of impatience, house-holds accumulate more savings and are relieved ofthe tendency that occurs when the interest rate islower to defer consumption for precautionary rea-sons. Permanent differences in interest rates result insmall differences in permanent consumption growthand thus estimation of the intertemporal elasticity inCarroll’s setup has a downward bias. Attanasio andLow solve a different problem, where the interest rateis a mean-reverting stochastic time series. The stan-dard approach works reasonably well in that setting.They conclude that studies based on fairly long time-series data for the interest rate are not seriously bi-ased. My conclusion favors studies with that character,accordingly.

I take the most reasonable value of the Frisch own-price elasticity of consumption demand to be −0.5.Again, I associate the evidence described here about

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2.4. Frisch Elasticity of Labor Supply 19

the intertemporal elasticity of substitution as reveal-ing the Frisch elasticity, even though many of the stud-ies do not consider complementarity of consumptionand hours explicitly.

2.4 Frisch Elasticity of Labor Supply

Pistaferri (2003) is a leading recent contribution to es-timation of the Frisch elasticity of labor supply. Thispaper makes use of data on workers’ personal expecta-tions of wage change, rather than relying on economet-ric inferences, as has been standard in other researchon intertemporal substitution. Pistaferri finds the elas-ticity to be 0.70 with a standard error of 0.09. Thisfigure is somewhat higher than most earlier work inthe Frisch framework or other approaches to measur-ing the intertemporal elasticity of substitution fromthe ratio of future to present wages. Here, too, I pro-ceed on the assumption that these approaches mea-sure the same property of preferences as a practicalmatter. Kimball and Shapiro (2003) survey the earlierwork.

Mulligan (1998) challenges the general consensusamong labor economists about the Frisch elasticityof labor supply with results showing elasticities wellabove 1. My discussion of the paper, published inthe same volume, gives reasons to be skeptical ofthe finding, as it appears to flow from an implausibleidentifying assumption.

Kimball and Shapiro (2003) estimate the Frisch elas-ticity from the decline in hours of work among lotterywinners, based on the assumption that the uncompen-sated elasticity of labor supply is 0. They find the elas-ticity to be about 1. But this finding is only as strongas the identifying condition.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

20 2. Research on Properties of Preferences

Domeij and Floden (2006) present simulation resultsfor standard labor supply estimation specificationssuggesting that the true value of the elasticity maybe double the estimated value as a result of omittingconsideration of borrowing constraints.

Pistaferri studies only men and most of the rest ofthe literature in the Frisch framework focuses on men.Studies of labor supply generally find higher wageelasticities for women.

Rogerson and Wallenius (2009) introduce a distinc-tion between micro and macro estimates of the Frischelasticity, with the conclusion that the two can be quitedifferent. Their vocabulary is different from that ofchapter 5, so their conclusion does not stand in theway of the philosophy employed there, of building amacro model based on micro elasticities. By micro,they refer specifically to estimating the Frisch elastic-ity as the ratio of the slope of the log of hours of workover the life cycle to the slope of log-wages over thelife cycle. They build a life-cycle model where most ofthe effects of wage variation take the form of changesin the age when people enter the labor force and whenthey leave, so the slope while in the labor force seri-ously understates the true Frisch elasticity. A noncon-vex production technology is key to the understate-ment. Although early attempts to measure the Frischelasticity used the approach that Rogerson and Wal-lenius consider, the literature I have cited here usesmore robust sources of variation.

2.5 Consumption–Hours Complementarity

No research that I have found estimates the Frischcross-elasticity directly. A substantial body of work

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

2.5. Consumption–Hours Complementarity 21

has examined what happens to consumption when aperson stops working, either because of unemploy-ment following job loss or because of retirement,which may be the result of job loss. Under some strongassumptions, the decline in consumption identifiesthe cross-elasticity.

Browning and Crossley (2001) appears to be themost useful study of consumption declines during pe-riods of unemployment. Unlike most earlier researchin this area, it measures total consumption, not justfood consumption. They find that the elasticity of afamily member’s consumption with respect to fam-ily income is 56%, for declines in income related tounemployment of that member. The actual decline inconsumption upon unemployment is 14%. Low et al.(2008) confirm Browning and Crossley’s finding in U.S.data from the Survey of Income Program Participation.

A larger body of research deals with the “retire-ment consumption puzzle,” the decline in consump-tion thought to occur upon retirement. Most of this re-search considers food consumption. Aguiar and Hurst(2005) show that, upon retirement, people spend moretime preparing food at home. The change in foodconsumption is thus not a reasonable guide to thechange in total consumption. Hurst (2008) surveys thisresearch.

Banks et al. (1998) use a large British survey of an-nual cross sections to study the relation between re-tirement and consumption of nondurables. They com-pare annual consumption changes in four-year-widecohorts, finding a coefficient of −0.26 on a dummy forhouseholds where the head left the labor market be-tween the two surveys. They use earlier data as instru-ments, so they interpret the finding as measuring theplanned reduction in consumption upon retirement.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

22 2. Research on Properties of Preferences

Miniaci et al. (2003) fit a detailed model to Italiancohort data on nondurable consumption, in a specifi-cation of the level of consumption that distinguishesage effects from retirement effects. The latter are bro-ken down by age of the household head. The pure re-tirement reductions range from 4 to 20%. This studyalso finds pure unemployment reductions in the rangediscussed above.

Fisher et al. (2005) study total consumption changesin the Consumer Expenditure Survey, using cohortanalysis. They find small declines in total consump-tion associated with rising retirement among themembers of a cohort. Because retirement in a cohort isa gradual process and because retirement effects arecombined with time effects on a cohort analysis, it isdifficult to pin down the effect.

In the parametric preferences considered in Halland Milgrom (2008), a difference in consumption be-tween workers and nonworkers of 15% correspondsto a Frisch cross-price elasticity of demand of 0.3, thevalue I adopt.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3Health

3.1 The Issues

In the American health system, families make some ofthe important decisions about health spending. Theydo so directly by some choices about when to seekcare, and more indirectly as voices at their employers,who make choices about insurance coverage, and ascitizens, because the government has a large role infinancing health care for people over 64. In this chap-ter, based on a joint paper with my colleague CharlesJones (Hall and Jones 2007), a family dynamic pro-gram governs the choice between current consump-tion and investment in health. The model helps explainthe growth of GDP spent on health.

Over the past half century, Americans spent a ris-ing share of total economic resources on health andenjoyed substantially longer lives as a result. Debateon health policy often focuses on limiting the growthof health spending. Is the growth of health spending arational response to changing economic conditions—notably the growth of income per person? A dynamic-programming model of family choice about healthspending and consumption suggests that this is in-deed the case. Standard preferences—of the kind used

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

24 3. Health

widely in economics to study consumption, asset pric-ing, and labor supply—imply that health spending isa superior good with an income elasticity well above1. As people get richer and consumption rises, themarginal utility of consumption falls rapidly. Spend-ing on health to extend life allows individuals to pur-chase additional periods of utility. The marginal util-ity of life extension does not decline. As a result,the optimal composition of total spending shifts to-ward health, and the health share grows along withincome. In projections based on the quantitative analy-sis of our model, the optimal health share of spend-ing seems likely to exceed 30% by the middle of thecentury.

The share of health care in total spending was 5.2%in 1950, 9.4% in 1975, and 15.4% in 2000. Over thesame period, health has improved. The life expectancyof an American born in 1950 was 68.2 years, of oneborn in 1975, 72.6 years, and of one born in 2000,76.9 years.

Why has this health share been rising, and what isthe likely time path of the health share for the rest ofthe century? In the model, the key decision is the divi-sion of total resources between health care and non-health consumption. Utility depends on quantity oflife—life expectancy—and quality of life—consump-tion. People value health spending because it allowsthem to live longer and to enjoy better lives.

Standard preferences imply that health is a superiorgood with an income elasticity well above 1. As peoplegrow richer, consumption rises but they devote an in-creasing share of resources to health care. The quanti-tative analysis suggests these effects can be large: pro-jections in our model typically lead to health sharesthat exceed 30% of GDP by the middle of this century.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.2. Basic Facts 25

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 20000.04

0.06

0.08

0.10

0.12

0.14

0.16

Year

Hea

lth s

hare

Figure 3.1. The health share in the United States.

The model abstracts from the complicated institu-tions that shape spending in the United States andasks a more basic question: from a social welfarestandpoint, how much should the nation spend onhealth care, and what is the time path of optimalhealth spending?

3.2 Basic Facts

The appropriate measure of total resources is con-sumption plus government purchases of goods andservices. Investment and net imports are intermedi-ate products. Figure 3.1 shows the fraction of totalspending devoted to health care, according to the U.S.National Income and Product Accounts. The numer-ator is consumption of health services plus govern-ment purchases of health services, and the denomina-tor is consumption plus total government purchasesof goods and services. The fraction has a sharp up-ward trend, but growth is irregular. In particular, the

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

26 3. Health

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 200068

69

70

71

72

73

74

75

76

77

Year

Lif

e ex

pect

ancy

Figure 3.2. Life expectancy in the United States.

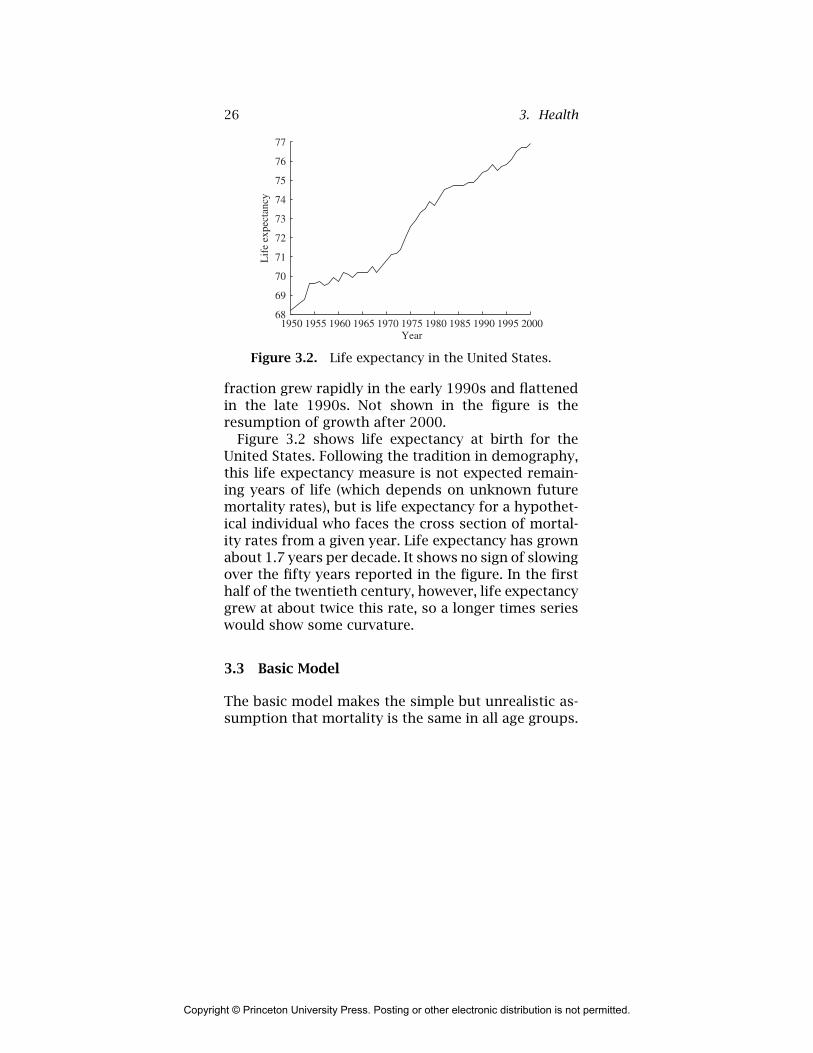

fraction grew rapidly in the early 1990s and flattenedin the late 1990s. Not shown in the figure is theresumption of growth after 2000.

Figure 3.2 shows life expectancy at birth for theUnited States. Following the tradition in demography,this life expectancy measure is not expected remain-ing years of life (which depends on unknown futuremortality rates), but is life expectancy for a hypothet-ical individual who faces the cross section of mortal-ity rates from a given year. Life expectancy has grownabout 1.7 years per decade. It shows no sign of slowingover the fifty years reported in the figure. In the firsthalf of the twentieth century, however, life expectancygrew at about twice this rate, so a longer times serieswould show some curvature.

3.3 Basic Model

The basic model makes the simple but unrealistic as-sumption that mortality is the same in all age groups.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.3. Basic Model 27

Preferences are unchanging over time, and income andproductivity are constant. This model sets the stagefor the full model incorporating age-specific mortalityand productivity growth.

The economy contains people of different ages whoare otherwise identical, grouped in families who makethe economic decisions. All families and all familymembers are identical. Let x denote a person’s healthstatus. The mortality rate of an individual is the in-verse of her health status, 1/x. Because people of allages face this same mortality rate, x is also equalto life expectancy. For simplicity at this stage, timepreference is zero.

In the stationary environment, the family’s valuefunction is a constant V times the number of mem-bers of the family N , which is the only state variable.The family’s dynamic program is

VNt = max(ntu(c)+ VNt+1). (3.1)

The law of motion of family size is

Nt+1 =(

1− 1x

)Nt. (3.2)

Putting the law of motion into the dynamic programand solving for V yields expected lifetime utility perfamily member:

V = xu(c). (3.3)

In this stationary environment, consumption is con-stant so that expected utility is the number of yearsan individual expects to live multiplied by per-periodutility. Period utility depends only on consumption;see Hall and Jones (2007) for a discussion of the exten-sion to making the quality of life depend on health sta-tus. Here and throughout the paper, utility after deathis zero.

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

28 3. Health

Rosen (1988) pointed out the following importantimplication of a specification of utility involving lifeexpectancy. When lifetime utility is per-period utility,u, multiplied by life expectancy, the level of umattersa great deal. In many other settings, adding a constantto u has no effect on consumer choice. Here, addinga constant raises the value the consumer places onlongevity relative to consumption of goods. Negativeutility also creates an anomaly—indifference curveshave the wrong curvature and the first-order condi-tions do not maximize utility. As long as u is positive,preferences are well behaved.

The representative family member receives a con-stant flow of resources y that can be spent on con-sumption or health:

c + h = y. (3.4)

The economy has no physical capital or foreign tradethat permits shifting resources from one period to an-other.

Finally, a health production function governs the in-dividual’s state of health:

x = f(h). (3.5)

The family chooses consumption and health spend-ing to maximize the utility of the individual in equa-tion (3.3) subject to the resource constraint of equa-tion (3.4) and the production function for health statusequation (3.5). That is, the optimal allocation solves

maxc,h

f (h)u(c) s.t. c + h = y. (3.6)

The optimal allocation equates the ratio of healthspending to consumption to the ratio of the elasticities

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.3. Basic Model 29

of the health production function and the flow utilityfunction. With s ≡ h/y , the optimum is

s∗

1− s∗ =h∗

c∗= ηhηc, (3.7)

where

ηh ≡ f ′(h)hx

and ηc ≡ u′(c) cu.Now ignore the fact that income and life expectancy

are taken as constant in this static model and insteadconsider what happens if income grows. The short-cut of using a static model to answer a dynamic ques-tion anticipates the findings of the full dynamic modelquite well.

The response of the health share to rising incomedepends on the movements of the two elasticities inequation (3.7). The crux of the argument is that theconsumption elasticity falls relative to the health elas-ticity as income rises, causing the health share to rise.Health is a superior good because satiation occursmore rapidly in nonhealth consumption.

Why is ηc decreasing in consumption? In mostbranches of applied economics, only marginal utilitymatters. For questions of life and death, however, thisis not the case. The utility associated with death isnormalized at zero in our framework, and how mucha person will pay to live an extra year hinges on thelevel of utility associated with life. In our application,adding a constant to the flow of utility u(c) has a ma-terial effect: it permits the elasticity of utility to varywith consumption. Thus the approach takes the stan-dard constant-elastic specification for marginal utilitybut adds a constant to the level of utility.

What matters for the choice of health spending,however, is not just the elasticity of marginal utility,

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

30 3. Health

but also the elasticity of the flow utility function itself.With the constant term added to a utility function withconstant-elastic marginal utility, the utility elasticitydeclines with consumption for conventional parame-ter values. The resulting specification is then capableof explaining the rising share of health spending.

Period utility is

u(c) = b + c1−γ

1− γ , (3.8)

where γ is the constant elasticity of marginal utility.Based on the evidence in chapter 2, γ > 1 is the likelycase. Accordingly, the second term is negative, so thebase level of utility, b, needs to be positive enough toensure that flow utility is positive over the relevantvalues of c. The flow of utility u(c) is always less thanb, so the elasticity ηc is decreasing in consumption.More generally, any bounded utility function u(c) willdeliver a declining elasticity, at least eventually, as willthe unbounded u(c) = α + β log c. Thus the key tothe explanation of the rising health share—a marginalutility of consumption that falls sufficiently quickly—is obtained by adding a constant to a standard classof utility functions.

A rapidly declining marginal utility of consumptionleads to a rising health share provided the health pro-duction elasticity ηh does not itself fall too rapidly.For example, if the marginal product of health spend-ing in extending life were to fall to zero—say, it wastechnologically impossible to live beyond the age of100—then health spending would cease to rise at thatpoint. Whether or not the health share rises over timeis then an empirical question: there is a race betweendiminishing marginal utility of consumption and thediminishing returns to the production of health. As

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.4. The Full Dynamic-Programming Model 31

discussed later, for the kind of health production func-tions that match the data, the production elasticity de-clines very gradually, and the declining marginal util-ity of consumption does indeed dominate, producinga rising health share.

The simple model develops intuition, but it fallsshort on a number of dimensions. Most importantly,the model assumes constant total resources and con-stant health productivity. This means it is inappropri-ate to use this model to study how a growing incomeleads to a rising health share, the comparative staticresults notwithstanding. Still, the basic intuition for arising health share emerges clearly. The health sharerises over time as income grows if the marginal util-ity of consumption falls sufficiently rapidly relative tothe joy of living an extra year and the ability of healthspending to generate that extra year.

3.4 The Full Dynamic-Programming Model

The full dynamic-programming model has age-specificmortality, growth in total resources, and productivitygrowth in the health sector. All families have the sameage composition.

An individual of age a in period t has an age-specificstate of health, xa,t . As in the basic model, the mor-tality rate for an individual is the inverse of her healthstatus. Therefore, 1−1/xa,t is the per-period survivalprobability of an individual with health xa,t .

An individual’s state of health is produced by spend-ing on health ha,t :

xa,t = f(ha,t ;a, t). (3.9)

In this production function, health status depends onboth age and time. Forces outside the model that vary

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

32 3. Health

with age and time may also influence health status—examples include technological change and education.

The flow utility of the individual is

u(ca,t, xa,t) = b +c1−γa,t

1− γ . (3.10)

The first term is the baseline level of utility discussedearlier. The second is the standard constant-elasticspecification for consumption.

In this environment, consider the allocation of re-sources that would be chosen by a family who placesequal weights on each person alive at a point in timeand who discounts future flows of utility at rate β.Let Na,t denote the number of people of age a aliveat time t. Let Vt(Nt) denote the family’s value func-tion when the age distribution of the population is thevectorNt ≡ (N1,t , N2,t , . . . , Na,t, . . . ). Then the family’sdynamic program is

Vt(Nt)

= max{ha,t ,ca,t}

( ∞∑a=0

Na,t u(ca,t, xa,t)+ βVt+1(Nt+1))

(3.11)

with law of motion

Na+1,t+1 =(

1− 1xa,t

)Na,t, (3.12)

subject to∞∑a=0

Na,t(yt − ca,t − ha,t) = 0, (3.13)

N0,t = N0, (3.14)

xa,t = f(ha,t ;a, t), (3.15)

yt+1 = egyyt. (3.16)

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.4. The Full Dynamic-Programming Model 33

The law of motion for the population assumes alarge enough family so that the number of people ageda + 1 next period can be taken equal to the num-ber aged a today multiplied by the survival proba-bility. This assumption is plainly unrealistic as far asfamily composition. The assumption eliminates theneed to keep track of the distribution of age com-positions across families. General-equilibrium modelsoften make this kind of assumption for tractability.

The first constraint is the family-wide resource con-straint. Note that people of all ages contribute thesame flow of resources, yt . The second constraintspecifies that births are exogenous and constant atN0.The final two constraints are the production functionfor health and the law of motion for resources, whichgrow exogenously at rate gy .

Let λt denote the Lagrange multiplier on the re-source constraint. The optimal allocation satisfies thefollowing first-order conditions for all a:

uc(ca,t) = λt, (3.17)

β∂Vt+1

∂Na+1,t+1

f ′(ha,t)x2a,t

+ux(ca,t)f ′(ha,t) = λt, (3.18)

where f ′(ha,t) represents ∂f(ha,t ;a, t)/∂ha,t . That is,the marginal utility of consumption and the marginalutility of health spending are equated across familymembers and to each other at all times. This condi-tion together with the additive separability of flow util-ity implies that members of all ages have the sameconsumption ct at each point in time, but they havedifferent health expenditures ha,t depending on age.

Normally, a value function with many state variablescreates substantial computational challenges. In thismodel, none arise because the value function is known

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

34 3. Health

to be linear:Vt(Nt) =

∑ava,tNa,t ; (3.19)

va,t is the value of life at age a in units of utility.Combining the two first-order conditions yields

βva+1,t+1

uc+uxx2

a,t

uc=

x2a,t

f ′(ha,t). (3.20)

The optimal allocation sets health spending at eachage to equate the marginal benefit of saving a life to itsmarginal cost. The marginal benefit is the sum of twoterms. The first is the social value of life βva+1,t+1/uc .The second is the additional quality of life enjoyed bypeople as a result of the increase in health status.

Taking the derivative of the value function showsthat the social value of life satisfies the recursiveequation:

va,t = u(ct)+ β(

1− 1xa,t

)va+1,t+1

+ λt(yt − ct − ha,t). (3.21)

The additional social welfare associated with havingan extra person alive at age a is the sum of threeterms. The first is the level of flow utility enjoyed bythat person. The second is the expected social wel-fare associated with having a person of age a+1 alivenext period, where the expectation employs the sur-vival probability 1 − 1/xa,t . Finally, the last term isthe net social resource contribution from a person ofagea, her production less her consumption and healthspending.

The literature on competing risks of mortality sug-gests that a decline in mortality from one cause mayincrease the optimal level of spending on other causes,

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.5. The Health Production Function 35

as discussed by Dow et al. (1999). This property holdsin this model as well. Declines in future mortality willincrease the value of life, va,t , raising the marginalbenefit of health spending at age a.

3.5 The Health Production Function

A period in the model is five years. The data are intwenty five-year age groups, starting at 0–4 and end-ing at 95–99. The historical period has eleven time pe-riods in running from 1950 through 2000. See Hall andJones (2007) for a discussion of data sources.

The inverse of the nonaccident mortality rate (ad-justed health status), xa,t is a Cobb–Douglas functionof health inputs:

xa,t = Aa(ztha,twa,t)θa. (3.22)

In this production function, Aa and θa are parame-ters that depend on age. zt is the efficiency of a unitof output devoted to health care, taken as an exoge-nous trend; it is the additional improvement in theproductivity of health care on top of the general trendin the productivity of goods production. The unob-served variable wa,t captures the effect of all otherdeterminants of mortality, including education andpollution.

Hall and Jones (2007) discusses estimation of theproduction parameters. Figure 3.3 shows the esti-mates of θa, the elasticity of adjusted health status,x, with respect to health inputs, by age category. Thegroups with the largest improvements in health sta-tus over the fifty-year period, the very young andthe middle-aged, have the highest elasticities, rang-ing from 0.25 to 0.40. The fact that the estimates of

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

36 3. Health

0 10 20 30 40 50 60 70 80 90 1000

0.1

0.2

0.3

0.4

0.5

Age

Figure 3.3. Estimated effects ofhealth inputs on health status.

θa generally decline with age, particularly at the olderages, constitutes an additional source of diminishingreturns to health spending as life expectancy rises. Forthe oldest age groups, the elasticity of health statuswith respect to health inputs is only 0.042.

3.6 Preference Parameters

Chapter 2 discussed evidence on the curvature param-eter of the utility function, γ, with the conclusion thatγ = 2 is the most reasonable value. Alternative val-ues range from near-log utility (γ = 1.01) to γ = 2.5.The discount factor, β, is consistent with the choiceof γ and a 6% real return to saving. With consumptiongrowth from the data of 2.08% per year, a standard Eu-ler equation gives an annual discount factor of 0.983,or, for the five-year intervals in the model, 0.918.

The intercept of flow utility b is determined to implya $3 million value of life for 35–39-year-olds in the year

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.7. Solving the Model 37

2000. Hall and Jones (2007) discusses this calculationin detail, including many references to research on thevalue of life.

3.7 Solving the Model

For the historical period 1950–2000, the solution usesresources per person, y , at its actual value. For theprojections into the future, it assumes income contin-ues to grow at its average historical rate of 2.31% peryear. Solution is by value function iteration, startingwith arbitrary values of the coefficients of the valuefunction va,T for a distant horizon T , solving equa-tion (3.20) successively for each earlier period, evalu-ating the v coefficients for the next earlier period, andrepeating back to 1950.

Figure 3.4 shows the calculated share of healthspending over the period 1950 through 2050 for γbetween 1.01 and 2.5. A rising health share is a ro-bust feature of the optimal allocation of resources inthe health model, as long as γ is not too small. Thecurvature of marginal utility, γ, is a key determinantof the slope of optimal health spending over time. Ifmarginal utility declines quickly because γ is high,the optimal health share rises rapidly. This growthin health spending reflects a value of life that growsfaster than income. In fact, in the simple model, thevalue of a year of life is roughly proportional to cγ ,illustrating the role of γ in governing the slope of theoptimal health share over time.

For near-log utility (where γ = 1.01), the optimalhealth share declines. The reason for this is the de-clining elasticity of health status with respect to healthspending in our estimated health production technol-ogy (recall figure 3.3). In this case, the marginal utility

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

38 3. Health

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 20500

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

= 2.5

= 2

= 1.5

= 1.01

Actual

Year

Hea

lth s

hare

s

γ

γ

γ

γ

Figure 3.4. Health share of spending from the modelfor various values of the curvature parameter γ.

of consumption falls sufficiently slowly relative to thediminishing returns in the production of health thatthe optimal health share declines gradually over time.The careful reader might wonder why all of the opti-mal health shares intersect in the same year, around2010. This intersection follows from choosing the util-ity intercept b to match a specific level for the valueof life for 35–39-year-olds and to the fact that ourpreferences feature a constant elasticity of marginalutility.

3.8 Concluding Remarks

A model based on standard economic assumptionsyields a strong prediction for the health share. Pro-vided the marginal utility of consumption falls suf-ficiently rapidly—as it does for an intertemporal

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

3.8. Concluding Remarks 39

elasticity of substitution well under 1—the optimalhealth share rises over time. The rising health shareoccurs as consumption continues to rise, but con-sumption grows more slowly than income. The intu-ition for this result is that in any given period, peoplebecome saturated in nonhealth consumption, drivingits marginal utility to low levels. As people get richer,the most valuable channel for spending is to purchaseadditional years of life. The numerical results suggestthe empirical relevance of this channel: optimal healthspending is predicted to rise to more than 30% of GDPby the year 2050 in most of our simulations, comparedwith the current level of about 15%.

This fundamental mechanism in the model is sup-ported empirically in a number of different ways. First,as discussed earlier, it is consistent with conventionalestimates of the intertemporal elasticity of substitu-tion. Second, the mechanism predicts that the value ofa statistical life should rise faster than income. This isa strong prediction of the model, and a place wherecareful empirical work in the future may be able toshed light on its validity. Costa and Kahn (2004) andHammitt et al. (2000) provide support for this predic-tion, suggesting that the value of life grows roughlytwice as fast as income, consistent with our baselinechoice of γ = 2. Cross-country evidence also suggeststhat health spending rises more than one-for-one withincome; this evidence is summarized by Gerdtham andJonsson (2000).

One source of evidence that runs counter to ourprediction is the micro evidence on health spend-ing and income. At the individual level within theUnited States, for example, income elasticities appearto be substantially less than 1, as discussed by New-house (1992). A serious problem with this existing

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.

40 3. Health

evidence, however, is that health insurance limits thechoices facing individuals, potentially explaining theabsence of income effects. Future empirical work willbe needed to judge this prediction.

As mentioned in the introduction, the recent healthliterature has emphasized the importance of techno-logical change as an explanation for the rising healthshare. In the view developed here, technology changeis a proximate rather than a fundamental explanation.The development of new and expensive medical tech-nologies is surely part of the process of rising healthspending, as the literature suggests; Jones (2004) pro-vides a model along these lines with exogenous tech-nical change. However, a more fundamental analysislooks at the reasons that new technologies are devel-oped. Distortions associated with health insurance inthe United States are probably part of the answer, assuggested by Weisbrod (1991). But the fact that thehealth share is rising in virtually every advanced coun-try in the world—despite wide variation in systemsfor allocating health care—suggests that deeper forcesare at work. A fully worked-out technological storywill need an analysis on the preference side to explainwhy it is useful to invent and use new and expensivemedical technologies. The most obvious explanationis the model here: new and expensive technologies arevalued because of the rising value of life.

Viewed from every angle, the results support theproposition that both historical and future increasesin the health spending share are desirable. The mag-nitude of the future increase depends on parameterswhose values are known with relatively low precision,including the value of life, the curvature of marginalutility, and the fraction of the decline in age-specific

Copyright © Princeton University Press. Posting or other electronic distribution is not permitted.