Forensic Interview Techniques for Fraud Examiners and … · Forensic Interview Techniques for...

160

© 2013 Association of Certified Fraud Examiners, Inc. Forensic Interview Techniques for Fraud Examiners and Auditors 20th November 2013

Transcript of Forensic Interview Techniques for Fraud Examiners and … · Forensic Interview Techniques for...

© 2013 Association of Certified Fraud Examiners, Inc.

Forensic Interview Techniques for Fraud Examiners and Auditors

20th November 2013

© 2013 Association of Certified Fraud Examiners, Inc. 2 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 3 of 160

Aim:

To provide the delegates with the knowledge, understanding, and skills to

enable them to professionally plan, conduct, and evaluate investigative

interviews with witnesses and suspects

Objectives:

By the end of this course the delegates will be able to:

• Describe how to make investigative decisions and record the rationale

• Understand and apply the PEACE interview framework

• Demonstrate how to conduct an investigative interview

• Evaluate the conduct and content of an investigative interview of a

witness and a suspect

© 2013 Association of Certified Fraud Examiners, Inc. 4 of 160

Investigative Interviewing

Background and General Principles of

Investigative Interviewing – P.E.A.C.E

Conversation Management (CM)

© 2013 Association of Certified Fraud Examiners, Inc. 5 of 160

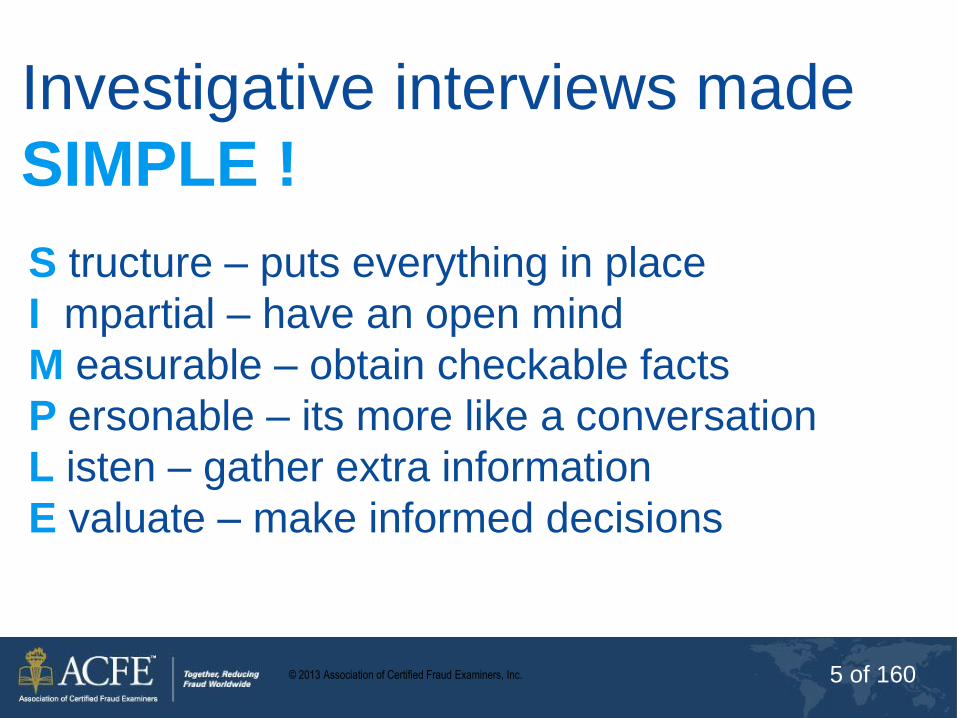

Investigative interviews made

SIMPLE !

S tructure – puts everything in place

I mpartial – have an open mind

M easurable – obtain checkable facts

P ersonable – its more like a conversation

L isten – gather extra information

E valuate – make informed decisions

© 2013 Association of Certified Fraud Examiners, Inc. 6 of 160

Know Your Audience!

© 2013 Association of Certified Fraud Examiners, Inc. 7 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 8 of 160

Why do we need

interview training?

© 2013 Association of Certified Fraud Examiners, Inc. 9 of 160

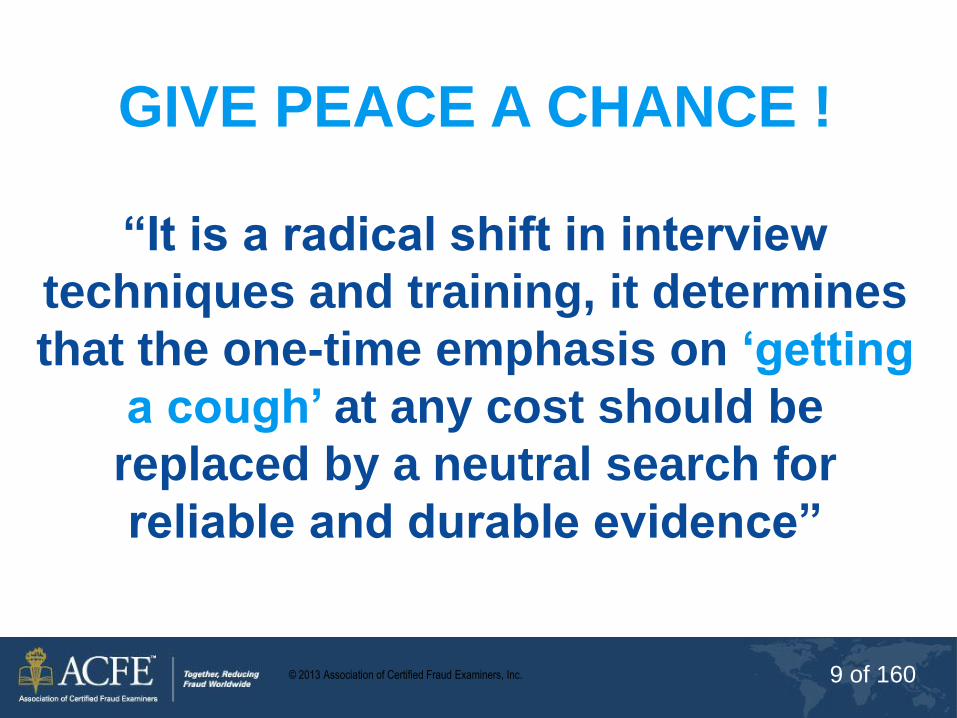

GIVE PEACE A CHANCE !

“It is a radical shift in interview

techniques and training, it determines

that the one-time emphasis on ‘getting

a cough’ at any cost should be

replaced by a neutral search for

reliable and durable evidence”

© 2013 Association of Certified Fraud Examiners, Inc. 10 of 160

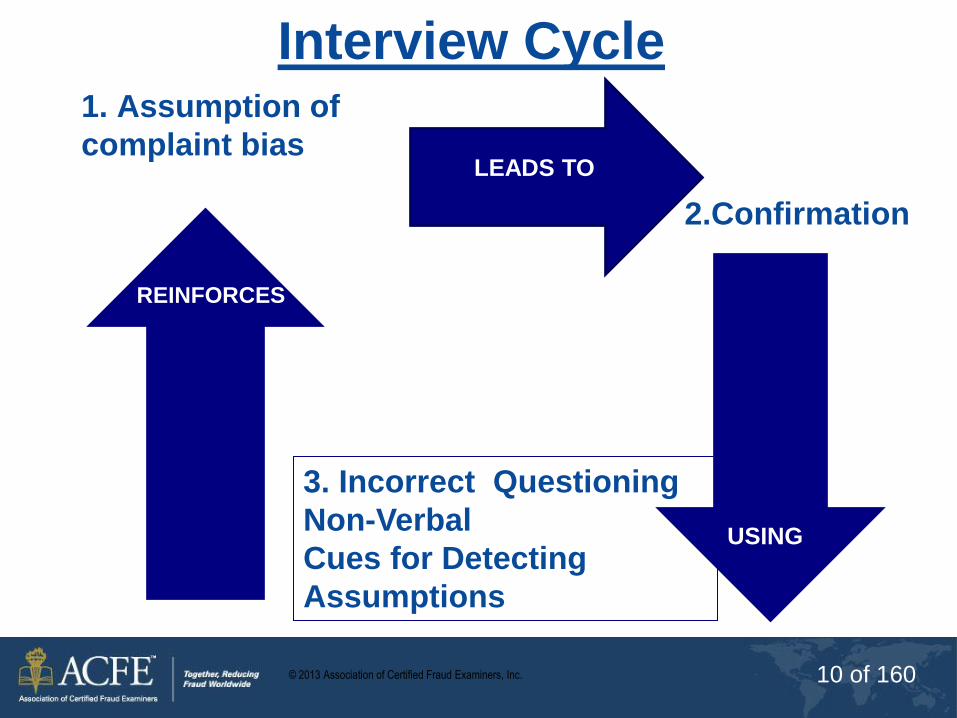

1. Assumption of

complaint bias

LEADS TO

USING

REINFORCES

Interview Cycle

2.Confirmation

3. Incorrect Questioning

Non-Verbal

Cues for Detecting

Assumptions

© 2013 Association of Certified Fraud Examiners, Inc. 11 of 160

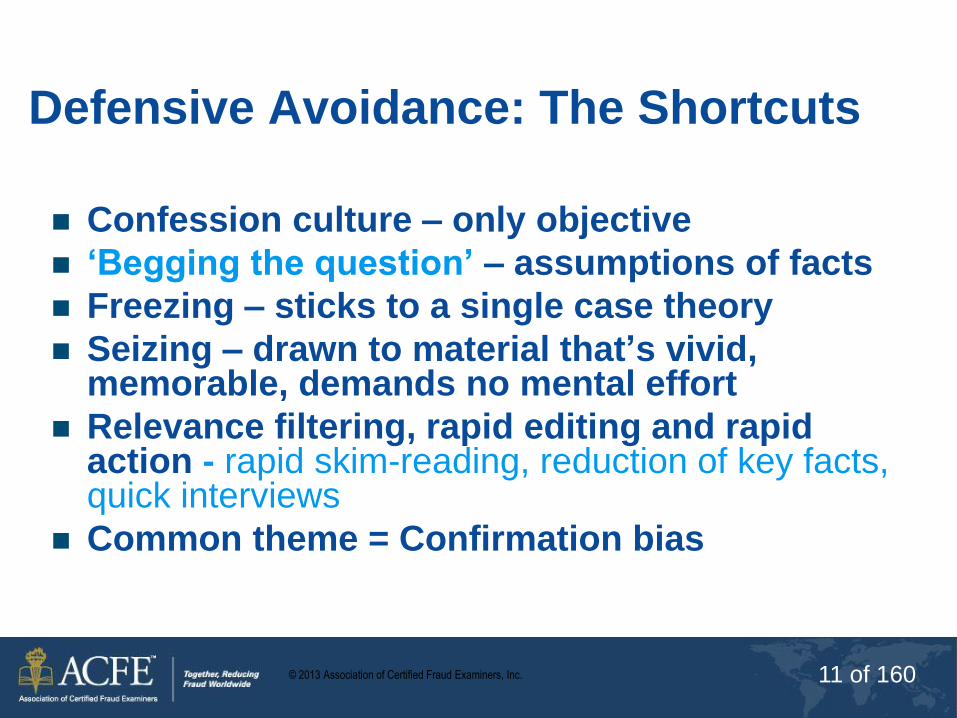

Defensive Avoidance: The Shortcuts

Confession culture – only objective

‘Begging the question’ – assumptions of facts

Freezing – sticks to a single case theory

Seizing – drawn to material that’s vivid, memorable, demands no mental effort

Relevance filtering, rapid editing and rapid action - rapid skim-reading, reduction of key facts, quick interviews

Common theme = Confirmation bias

© 2013 Association of Certified Fraud Examiners, Inc. 12 of 160

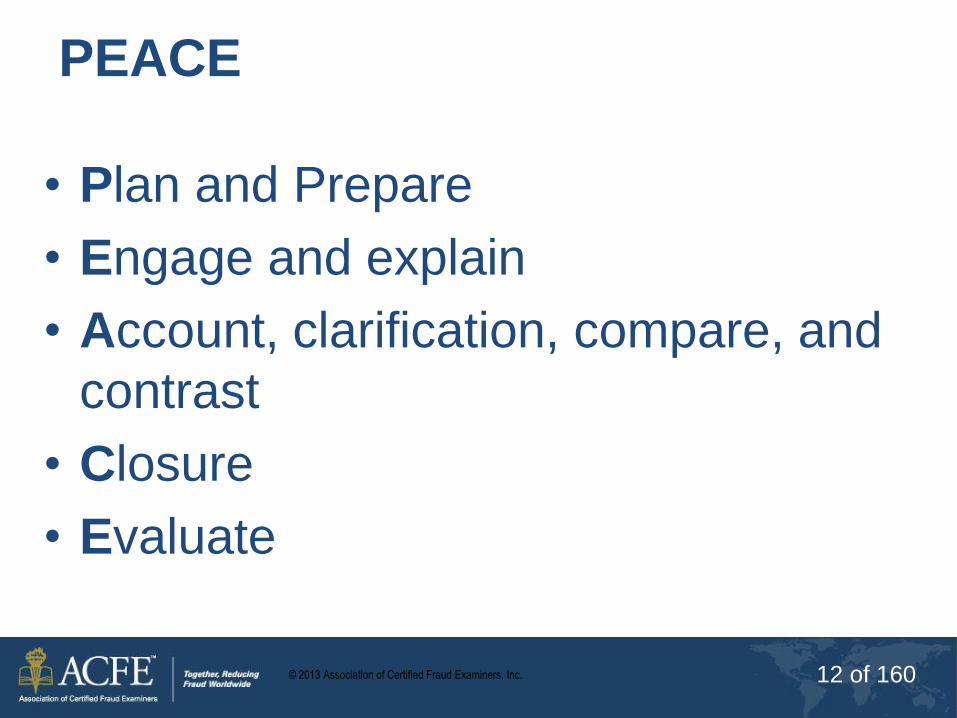

PEACE

• Plan and Prepare

• Engage and explain

• Account, clarification, compare, and

contrast

• Closure

• Evaluate

© 2013 Association of Certified Fraud Examiners, Inc. 13 of 160

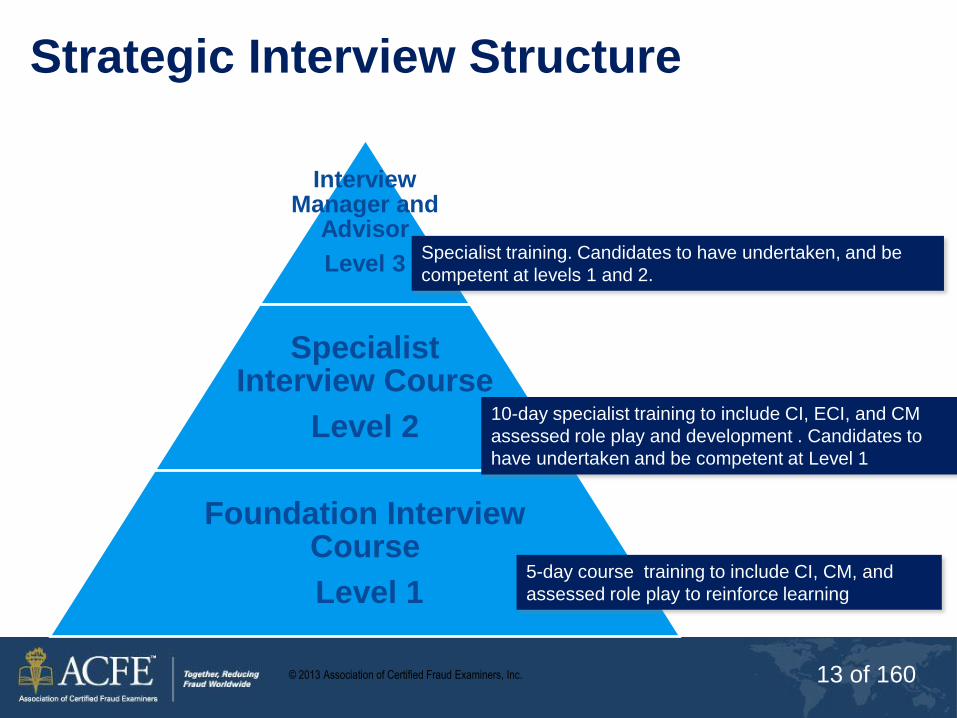

Strategic Interview Structure

Interview Manager and

Advisor

Level 3

Specialist Interview Course

Level 2

Foundation Interview Course

Level 1 5-day course training to include CI, CM, and

assessed role play to reinforce learning

10-day specialist training to include CI, ECI, and CM

assessed role play and development . Candidates to

have undertaken and be competent at Level 1

Specialist training. Candidates to have undertaken, and be

competent at levels 1 and 2.

© 2013 Association of Certified Fraud Examiners, Inc. 14 of 160

BENEFITS OF PEACE

© 2013 Association of Certified Fraud Examiners, Inc. 15 of 160

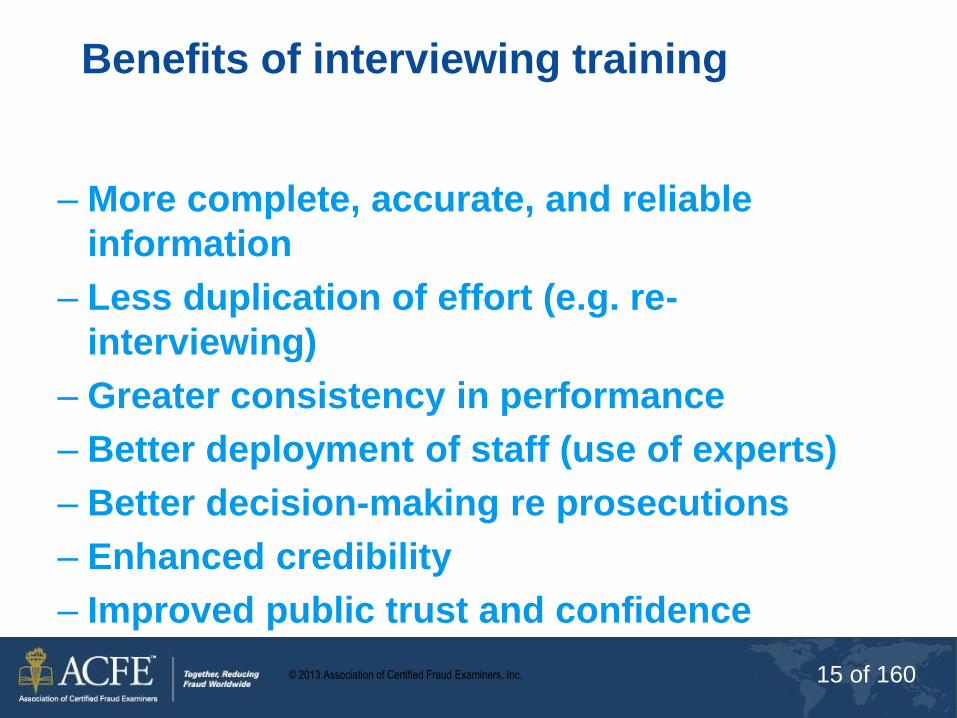

Benefits of interviewing training

– More complete, accurate, and reliable

information

– Less duplication of effort (e.g. re-

interviewing)

– Greater consistency in performance

– Better deployment of staff (use of experts)

– Better decision-making re prosecutions

– Enhanced credibility

– Improved public trust and confidence

© 2013 Association of Certified Fraud Examiners, Inc. 16 of 160

MEMORY: INNER EDITOR

© 2013 Association of Certified Fraud Examiners, Inc. 17 of 160

Aim:

To develop understanding regarding memory, retention,

and how people can fabricate accounts

Objectives:

a) Explain how they retain information and record

information verbally given to them themselves.

b) Identify best practise regarding information retention and

recording of such and reasons why.

c) Explain how to recognise truthful / untruthful accounts.

MEMORY

© 2013 Association of Certified Fraud Examiners, Inc. 18 of 160

Why do interviewers need to

know about memory?

To understand memory is fragile

Memory can be influenced by the interviewer

Interviewees’ can be assisted to remember

© 2013 Association of Certified Fraud Examiners, Inc. 19 of 160

‘Generation Game’

© 2013 Association of Certified Fraud Examiners, Inc.

© 2013 Association of Certified Fraud Examiners, Inc.

© 2013 Association of Certified Fraud Examiners, Inc. 22 of 160

© 2013 Association of Certified Fraud Examiners, Inc.

© 2013 Association of Certified Fraud Examiners, Inc.

© 2013 Association of Certified Fraud Examiners, Inc.

© 2013 Association of Certified Fraud Examiners, Inc. 26 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 27 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 28 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 29 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 30 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 31 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 32 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 33 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 34 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 35 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 36 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 37 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 38 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 39 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 40 of 160

‘End’

© 2013 Association of Certified Fraud Examiners, Inc. 41 of 160

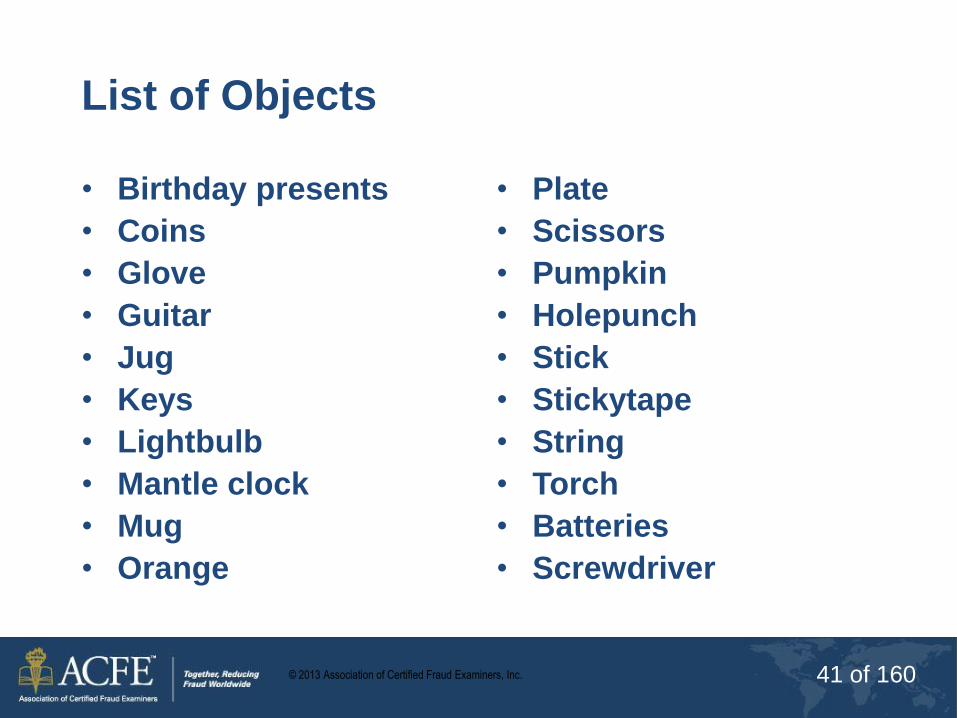

List of Objects

• Birthday presents

• Coins

• Glove

• Guitar

• Jug

• Keys

• Lightbulb

• Mantle clock

• Mug

• Orange

• Plate

• Scissors

• Pumpkin

• Holepunch

• Stick

• Stickytape

• String

• Torch

• Batteries

• Screwdriver

© 2013 Association of Certified Fraud Examiners, Inc. 42 of 160

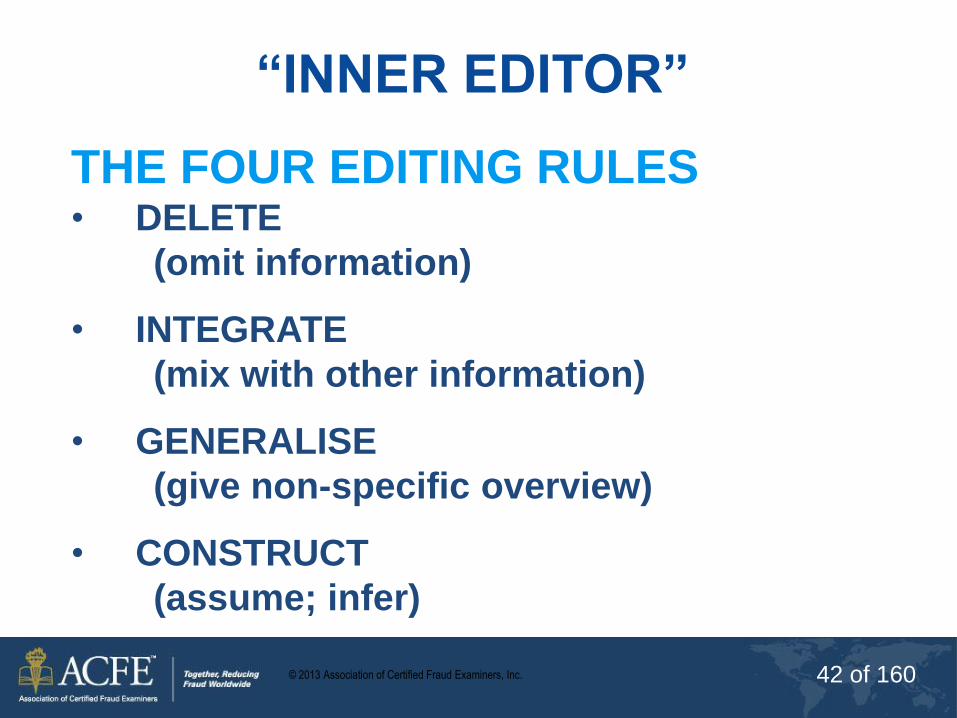

“INNER EDITOR”

THE FOUR EDITING RULES • DELETE

(omit information)

• INTEGRATE

(mix with other information)

• GENERALISE

(give non-specific overview)

• CONSTRUCT

(assume; infer)

© 2013 Association of Certified Fraud Examiners, Inc. 43 of 160

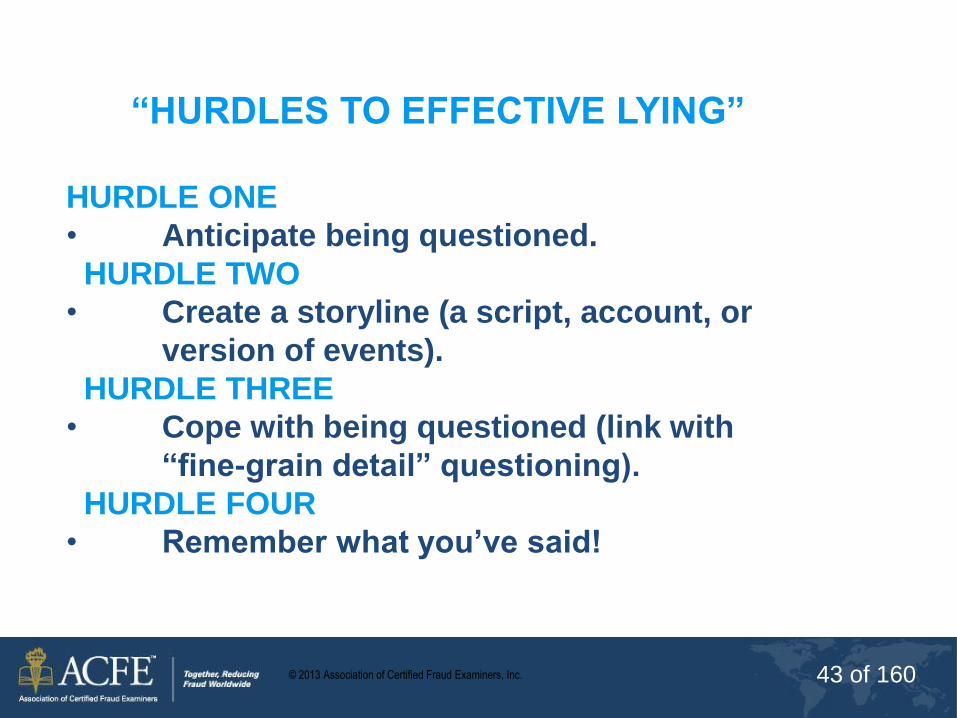

“HURDLES TO EFFECTIVE LYING”

HURDLE ONE

• Anticipate being questioned.

HURDLE TWO

• Create a storyline (a script, account, or

version of events).

HURDLE THREE

• Cope with being questioned (link with

“fine-grain detail” questioning).

HURDLE FOUR

• Remember what you’ve said!

© 2013 Association of Certified Fraud Examiners, Inc. 44 of 160

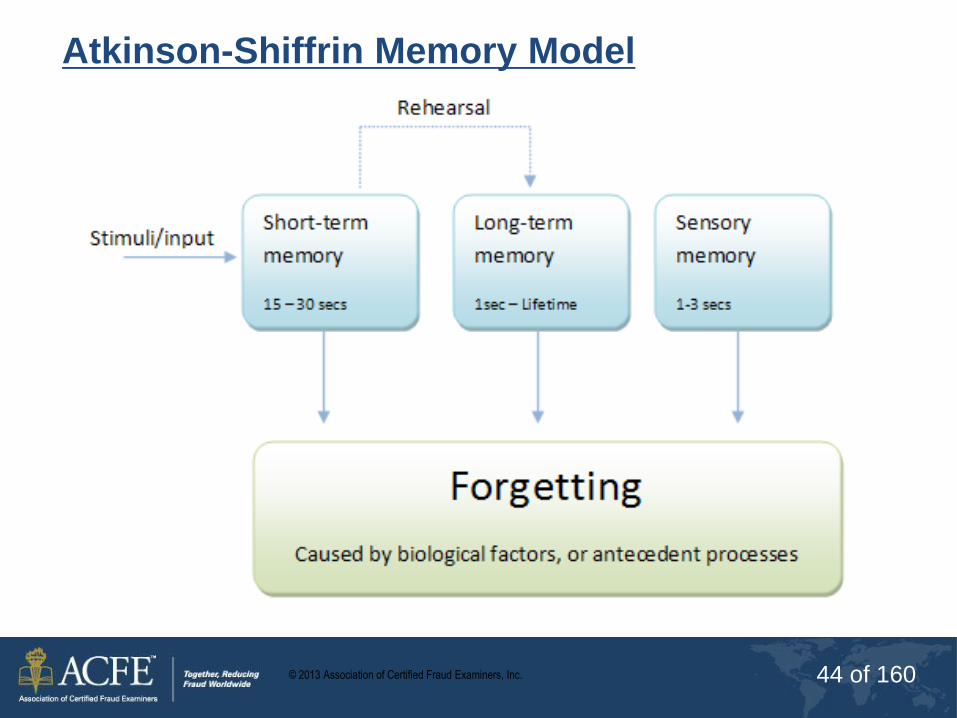

Atkinson-Shiffrin Memory Model

© 2013 Association of Certified Fraud Examiners, Inc. 45 of 160

Storage • Short-term

memory only has limited capacity

• Summarising can commit to long-term memory.

© 2013 Association of Certified Fraud Examiners, Inc. 46 of 160

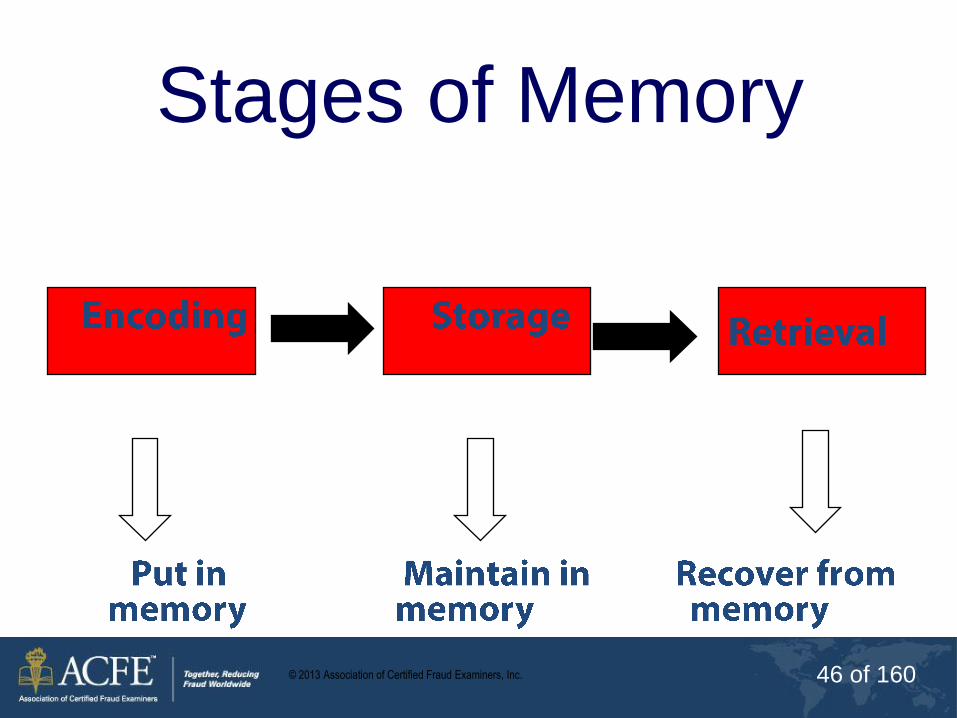

Stages of Memory

© 2013 Association of Certified Fraud Examiners, Inc. 47 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 48 of 160

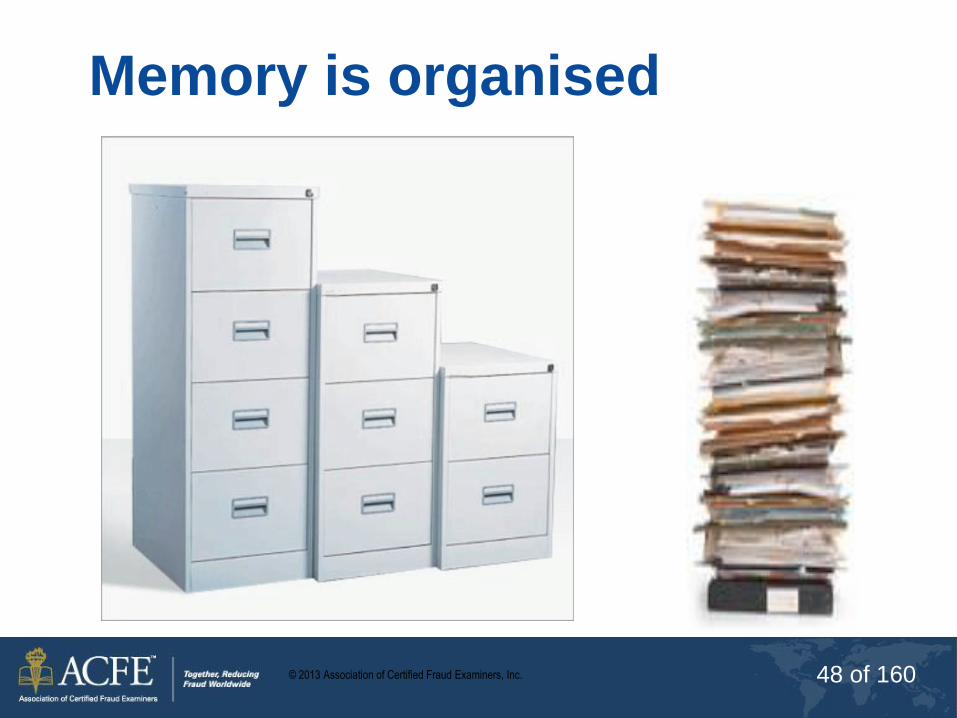

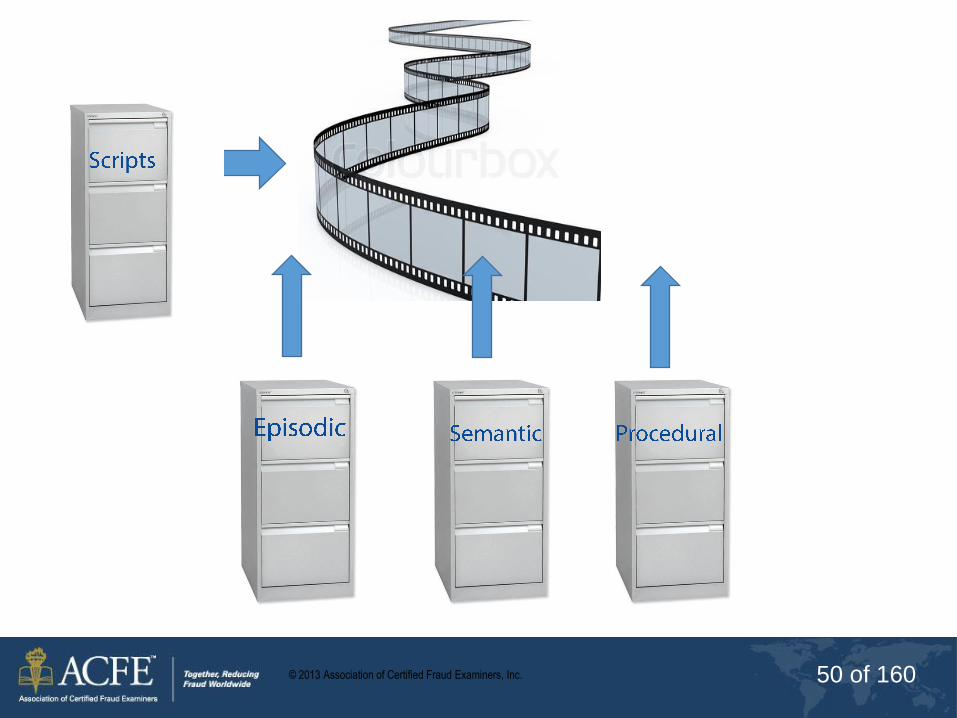

Memory is organised

© 2013 Association of Certified Fraud Examiners, Inc. 49 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 50 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 51 of 160

Aim:

To develop understanding regarding memory, retention,

and how people can fabricate accounts

Objectives:

a) Explain how they retain information and record

information verbally given to them themselves.

b) Identify best practise regarding information retention and

recording of such and reasons why.

c) Explain how to recognise truthful / untruthful accounts.

MEMORY

© 2013 Association of Certified Fraud Examiners, Inc. 52 of 160

APPROPRIATE

QUESTIONS

© 2013 Association of Certified Fraud Examiners, Inc. 53 of 160

Aim:

To enable delegates to gain knowledge of the various

questioning styles, the effects of each and identify the

correct questioning style to use in order to interview

any interviewee.

Objectives:

a)Define the various questioning styles.

b)Explain the positive/negative effects the various

styles have on a interviewee.

c)Demonstrate the correct questioning style required.

QUESTIONING STYLE

© 2013 Association of Certified Fraud Examiners, Inc. 54 of 160

Your ability to question

• Your ability to construct appropriate questions prior to and during an investigative interview is vital to:

– Obtaining complete, accurate and reliable information

– Maximising the amount of relevant reliable information

– Ensuring the information gained is admissible

– Maintaining the trust and confidence of the public

© 2013 Association of Certified Fraud Examiners, Inc. 55 of 160

Best kind of question for

information gathering

Answers to open questions are

more elaborate and more

accurate

OPEN QUESTIONS

© 2013 Association of Certified Fraud Examiners, Inc. 56 of 160

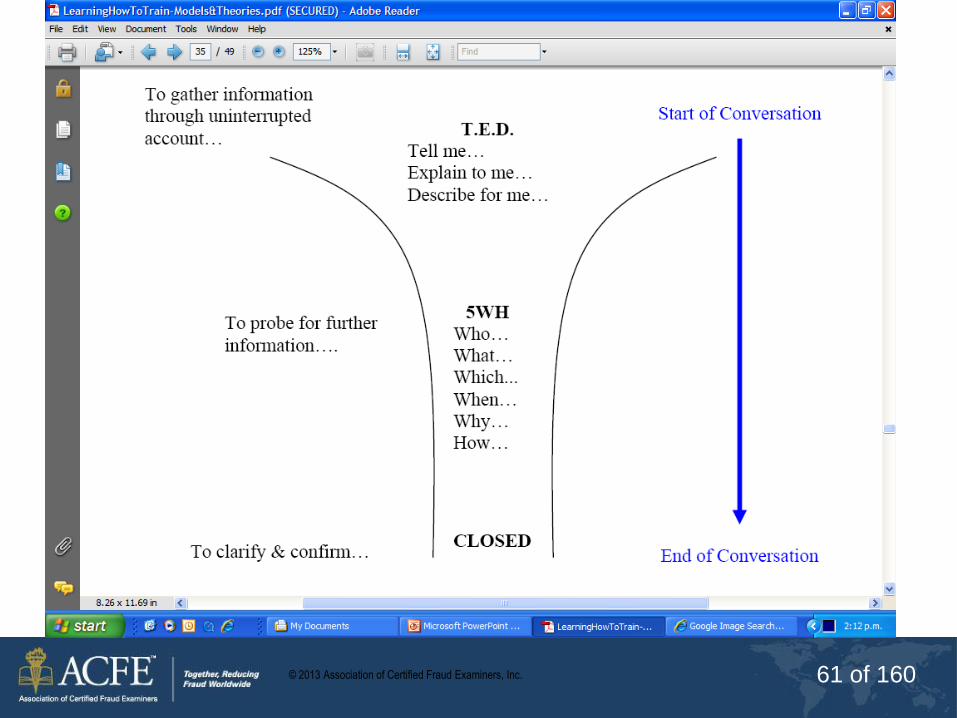

T.E.D.S.

Tell, Explain, Describe,

Show (Take, Guide)

5WH

Who, Why, What, Where,

When, and How (Which)

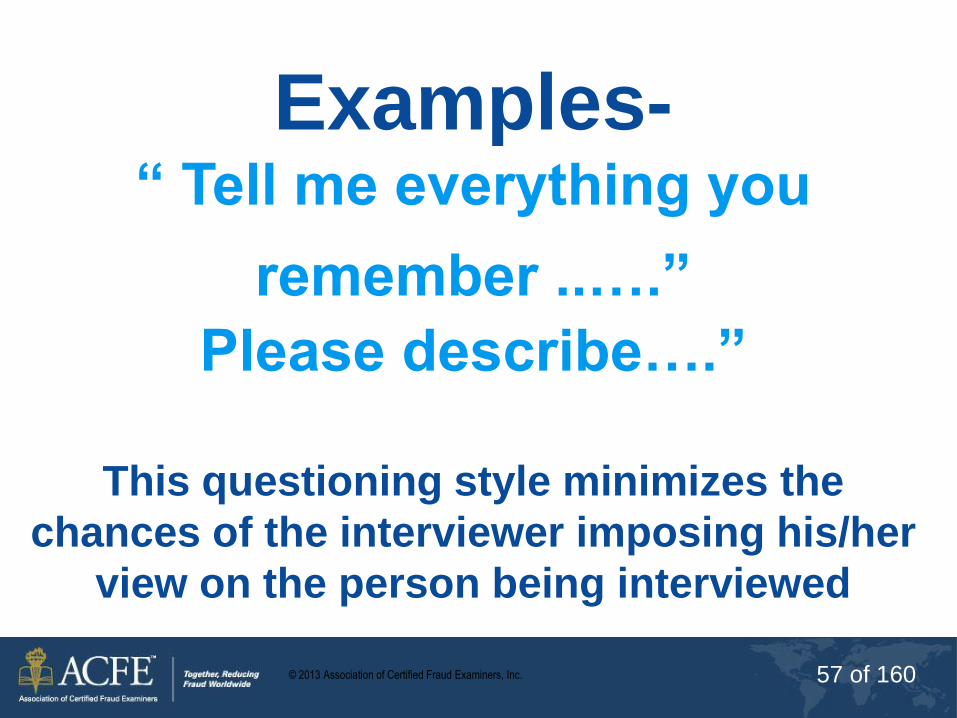

© 2013 Association of Certified Fraud Examiners, Inc. 57 of 160

Examples- “ Tell me everything you

remember ..….” Please describe….”

This questioning style minimizes the

chances of the interviewer imposing his/her

view on the person being interviewed

© 2013 Association of Certified Fraud Examiners, Inc. 58 of 160

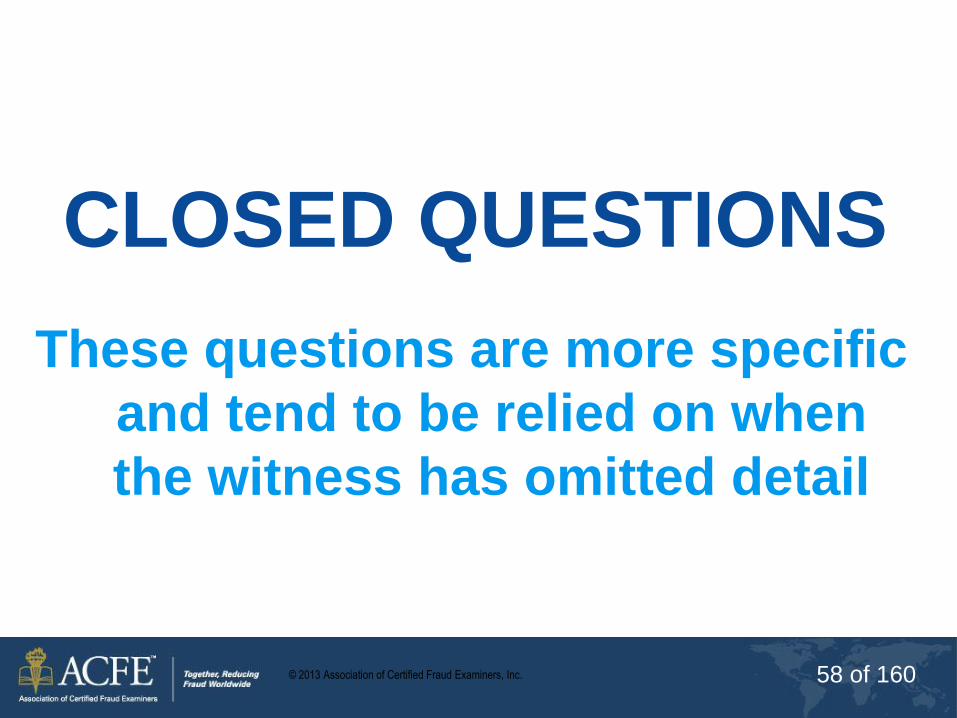

CLOSED QUESTIONS

These questions are more specific

and tend to be relied on when

the witness has omitted detail

© 2013 Association of Certified Fraud Examiners, Inc. 59 of 160

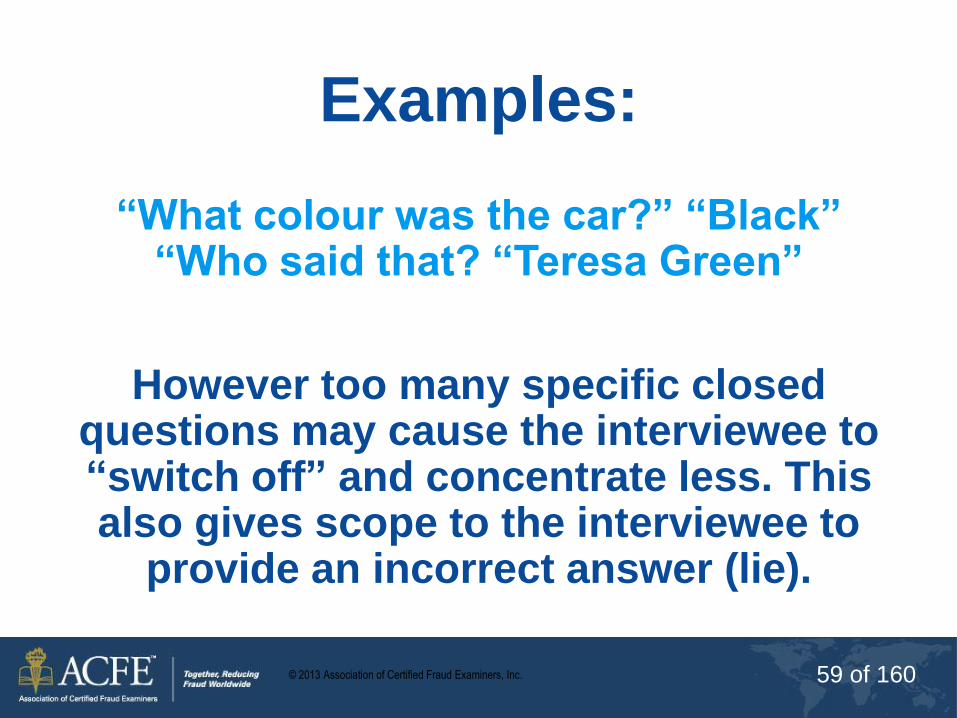

Examples:

“What colour was the car?” “Black” “Who said that? “Teresa Green”

However too many specific closed

questions may cause the interviewee to “switch off” and concentrate less. This also gives scope to the interviewee to

provide an incorrect answer (lie).

© 2013 Association of Certified Fraud Examiners, Inc. 60 of 160

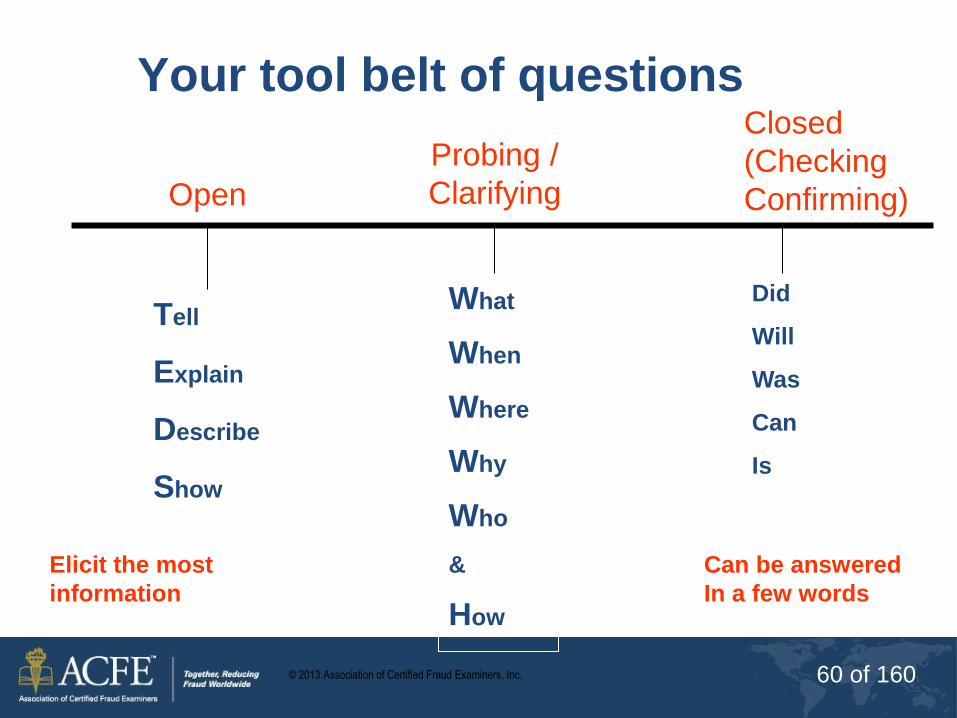

Your tool belt of questions

Can be answered

In a few words

Elicit the most

information

Tell

Explain

Describe

Show

What

When

Where

Why

Who

&

How

Did

Will

Was

Can

Is

Open

Probing /

Clarifying

Closed

(Checking

Confirming)

© 2013 Association of Certified Fraud Examiners, Inc. 61 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 62 of 160

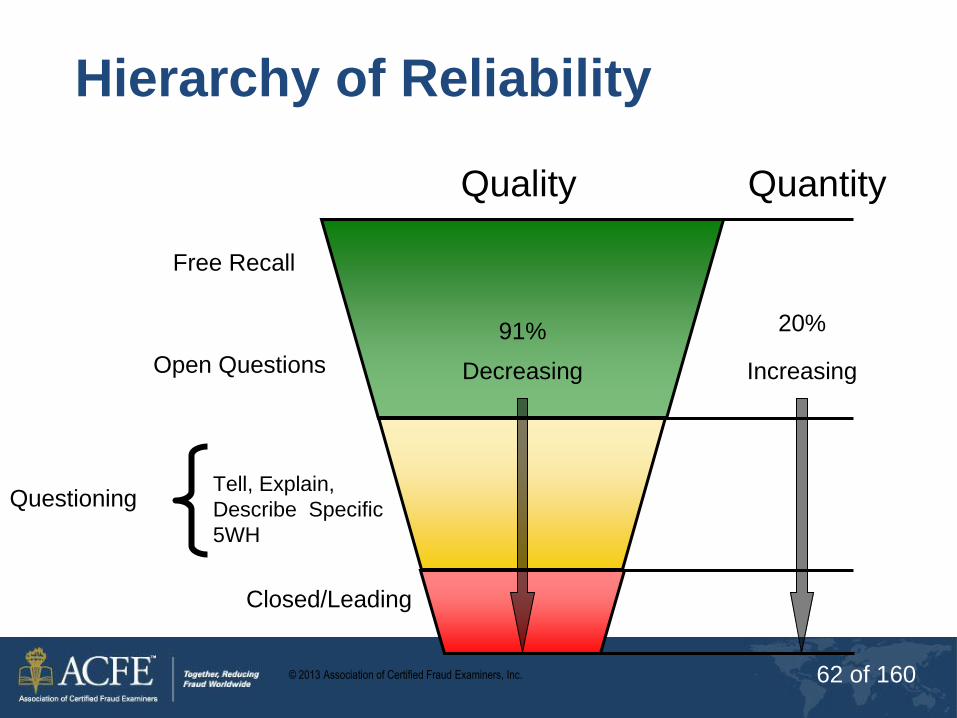

Hierarchy of Reliability

Quality Quantity

Free Recall

Open Questions

Closed/Leading

Increasing

20%

Questioning Tell, Explain,

Describe Specific

5WH

Decreasing

91%

© 2013 Association of Certified Fraud Examiners, Inc. 63 of 160

Active Listening

© 2013 Association of Certified Fraud Examiners, Inc. 64 of 160

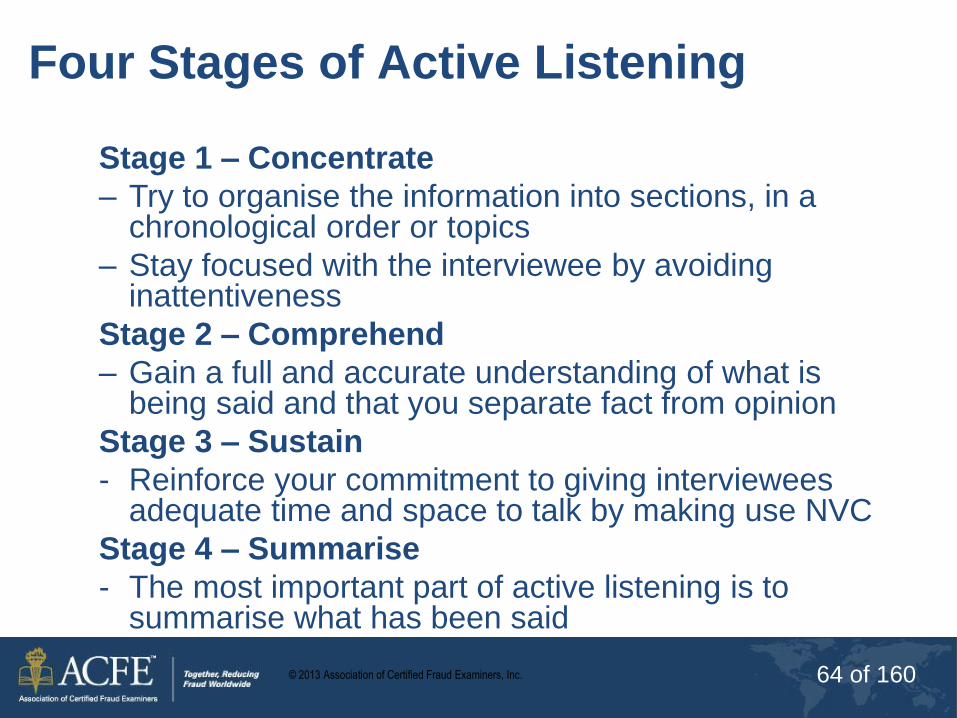

Four Stages of Active Listening

Stage 1 – Concentrate

– Try to organise the information into sections, in a chronological order or topics

– Stay focused with the interviewee by avoiding inattentiveness

Stage 2 – Comprehend

– Gain a full and accurate understanding of what is being said and that you separate fact from opinion

Stage 3 – Sustain

- Reinforce your commitment to giving interviewees adequate time and space to talk by making use NVC

Stage 4 – Summarise

- The most important part of active listening is to summarise what has been said

© 2013 Association of Certified Fraud Examiners, Inc. 65 of 160

SUMMARISE ACCURATELY

This demonstrates you are actively

LISTENING to the witness – The art of

a good Interviewer !!!!

© 2013 Association of Certified Fraud Examiners, Inc. 66 of 160

QUESTIONING TIPS

© 2013 Association of Certified Fraud Examiners, Inc. 67 of 160

EFFECTIVE LISTENING -

GUGGLING

© 2013 Association of Certified Fraud Examiners, Inc. 68 of 160

ECHO PROBE

“ the forms were duplicated”

“Duplicated?”

MIRROR PROBE

“she blamed you?”

“Blamed you?”

© 2013 Association of Certified Fraud Examiners, Inc. 69 of 160

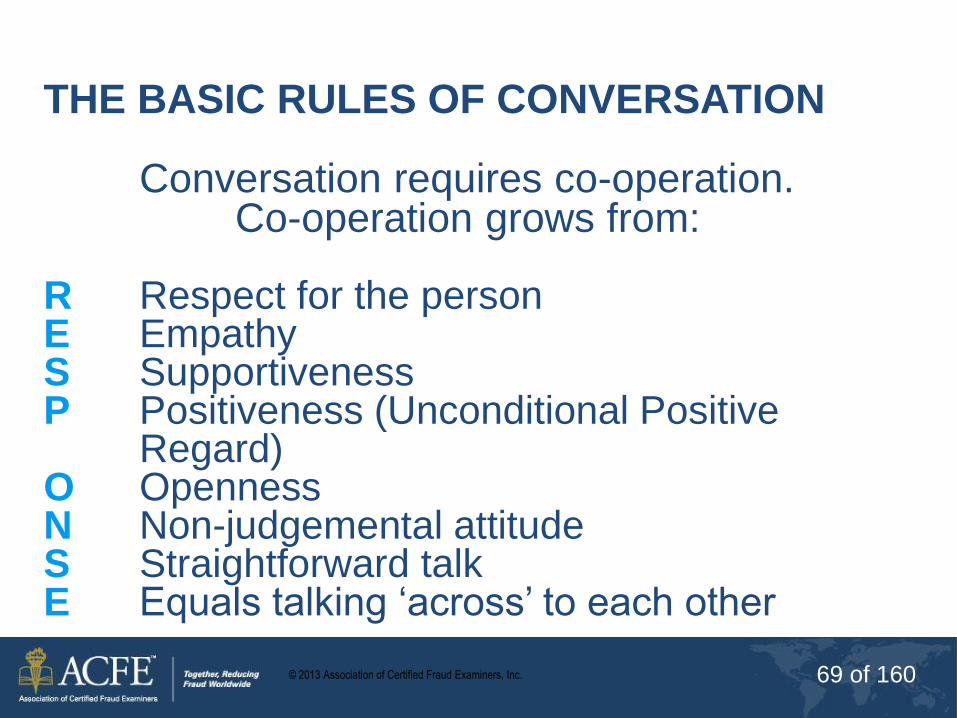

THE BASIC RULES OF CONVERSATION Conversation requires co-operation. Co-operation grows from: R Respect for the person E Empathy S Supportiveness P Positiveness (Unconditional Positive Regard) O Openness N Non-judgemental attitude S Straightforward talk E Equals talking ‘across’ to each other

© 2013 Association of Certified Fraud Examiners, Inc. 70 of 160

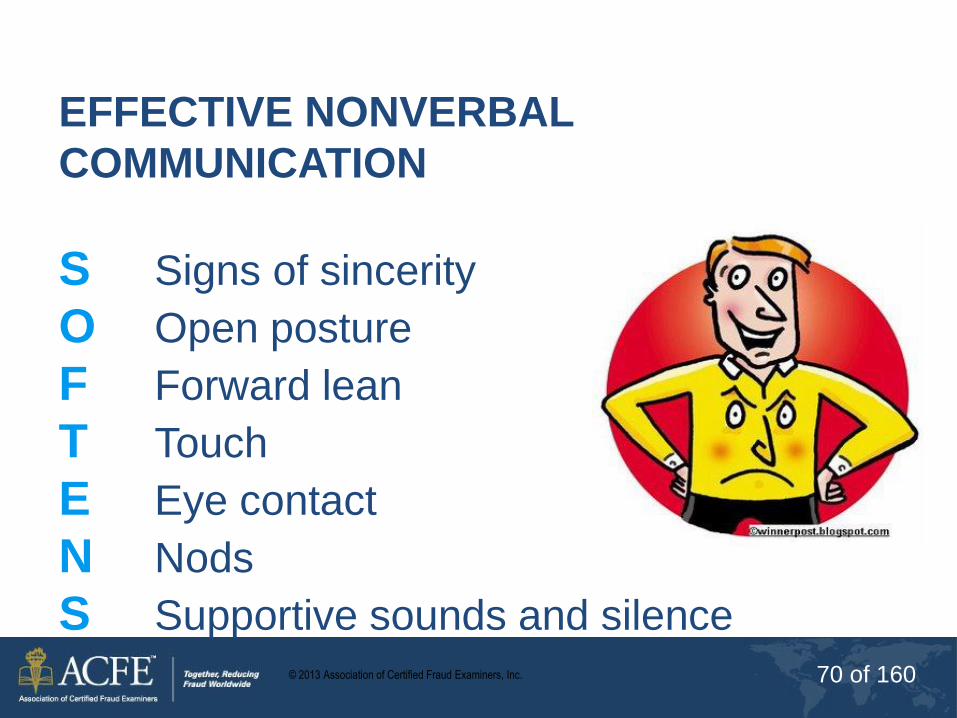

EFFECTIVE NONVERBAL

COMMUNICATION

S Signs of sincerity

O Open posture

F Forward lean

T Touch

E Eye contact

N Nods

S Supportive sounds and silence

© 2013 Association of Certified Fraud Examiners, Inc. 71 of 160

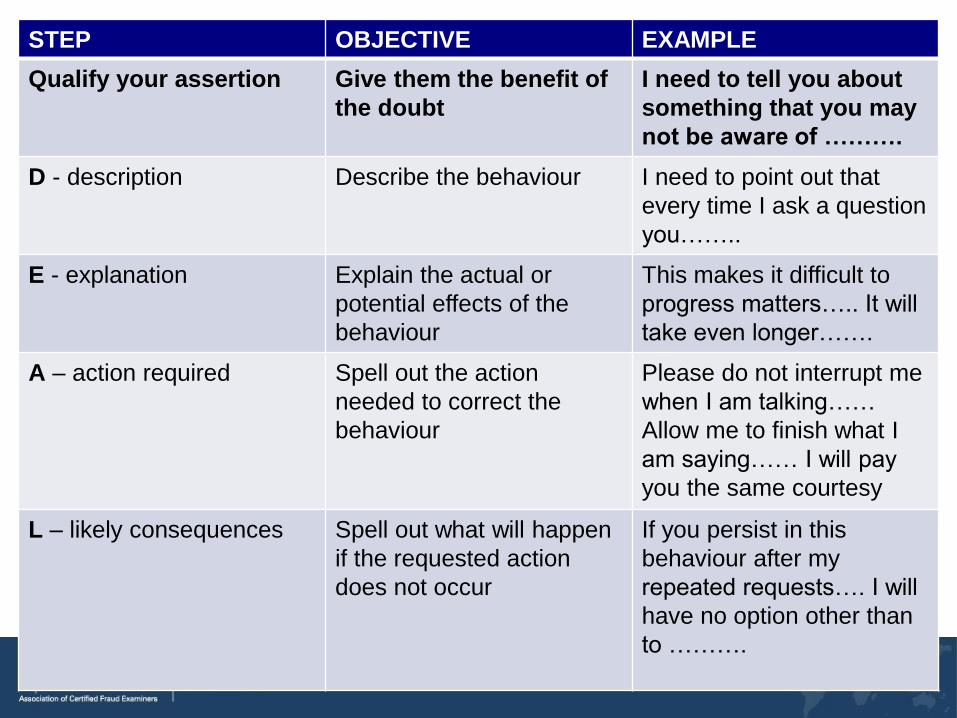

DEAL: A technique for

countering disruptive behaviour

© 2013 Association of Certified Fraud Examiners, Inc. 72 of 160

STEP OBJECTIVE EXAMPLE

Qualify your assertion Give them the benefit of

the doubt

I need to tell you about

something that you may

not be aware of ……….

D - description Describe the behaviour I need to point out that

every time I ask a question

you……..

E - explanation Explain the actual or

potential effects of the

behaviour

This makes it difficult to

progress matters….. It will

take even longer…….

A – action required Spell out the action

needed to correct the

behaviour

Please do not interrupt me

when I am talking……

Allow me to finish what I

am saying…… I will pay

you the same courtesy

L – likely consequences Spell out what will happen

if the requested action

does not occur

If you persist in this

behaviour after my

repeated requests…. I will

have no option other than

to ……….

© 2013 Association of Certified Fraud Examiners, Inc. 73 of 160

DECEPTIVE

DISCLOSURE

© 2013 Association of Certified Fraud Examiners, Inc. 74 of 160

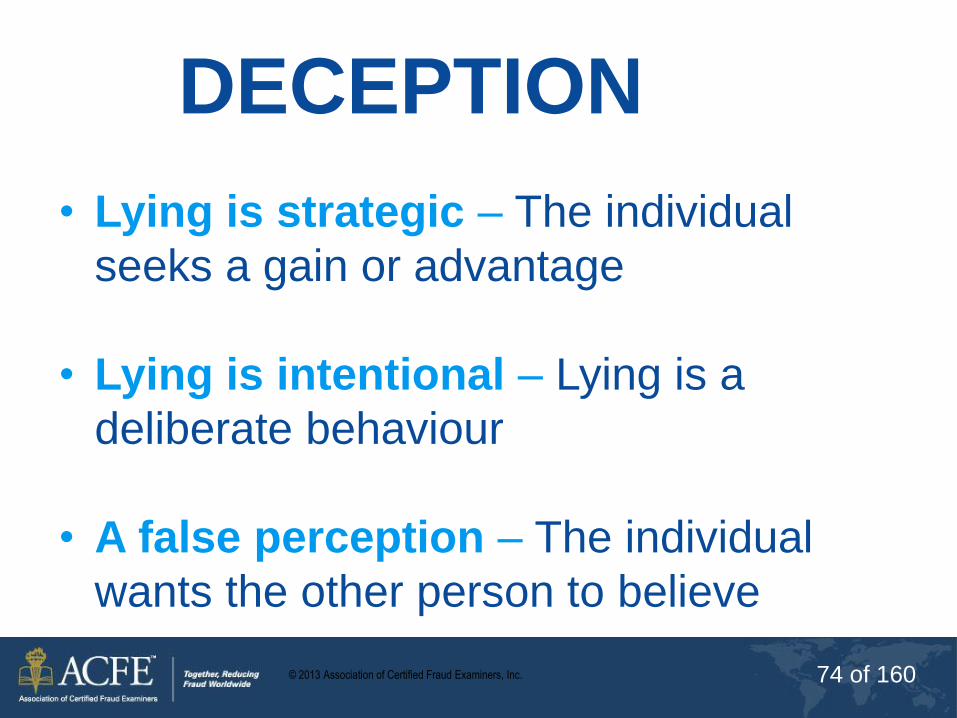

DECEPTION

• Lying is strategic – The individual

seeks a gain or advantage

• Lying is intentional – Lying is a

deliberate behaviour

• A false perception – The individual

wants the other person to believe

© 2013 Association of Certified Fraud Examiners, Inc. 75 of 160

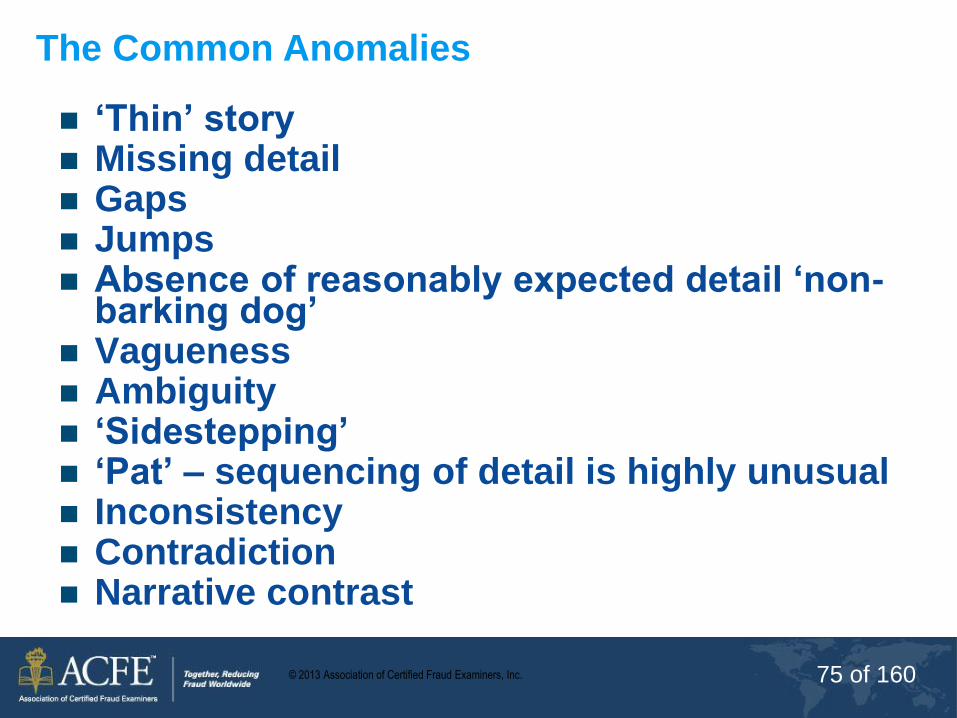

‘Thin’ story Missing detail Gaps Jumps Absence of reasonably expected detail ‘non-

barking dog’ Vagueness Ambiguity ‘Sidestepping’ ‘Pat’ – sequencing of detail is highly unusual Inconsistency Contradiction Narrative contrast

The Common Anomalies

© 2013 Association of Certified Fraud Examiners, Inc. 76 of 160

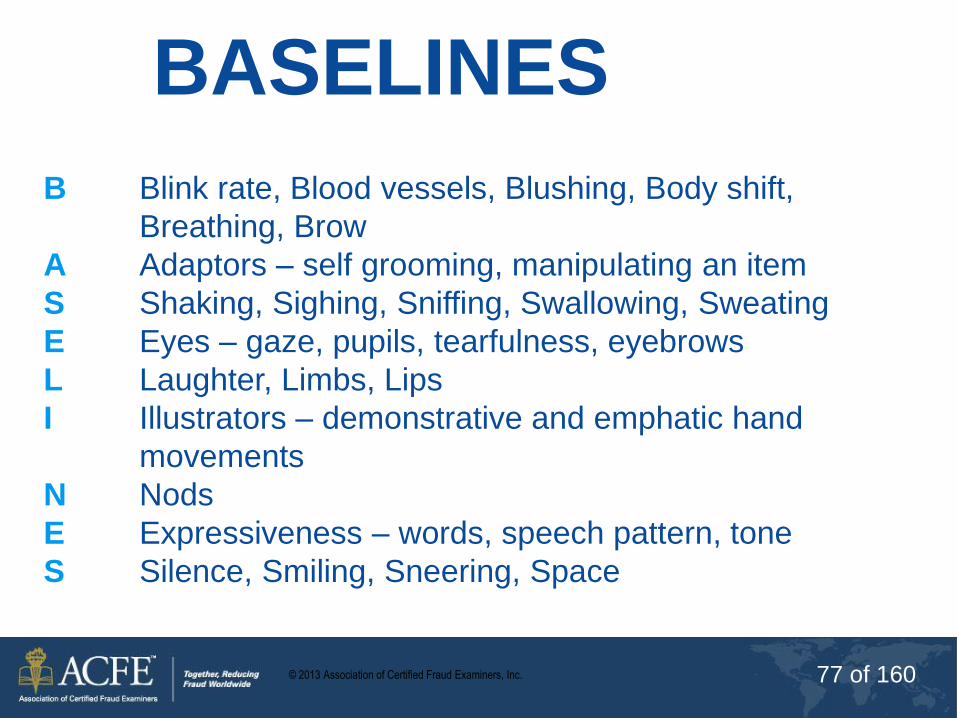

BASELINES

© 2013 Association of Certified Fraud Examiners, Inc. 77 of 160

B Blink rate, Blood vessels, Blushing, Body shift,

Breathing, Brow

A Adaptors – self grooming, manipulating an item

S Shaking, Sighing, Sniffing, Swallowing, Sweating

E Eyes – gaze, pupils, tearfulness, eyebrows

L Laughter, Limbs, Lips

I Illustrators – demonstrative and emphatic hand

movements

N Nods

E Expressiveness – words, speech pattern, tone

S Silence, Smiling, Sneering, Space

BASELINES

© 2013 Association of Certified Fraud Examiners, Inc. 78 of 160

INAPPROPRIATE

QUESTIONS

© 2013 Association of Certified Fraud Examiners, Inc. 79 of 160

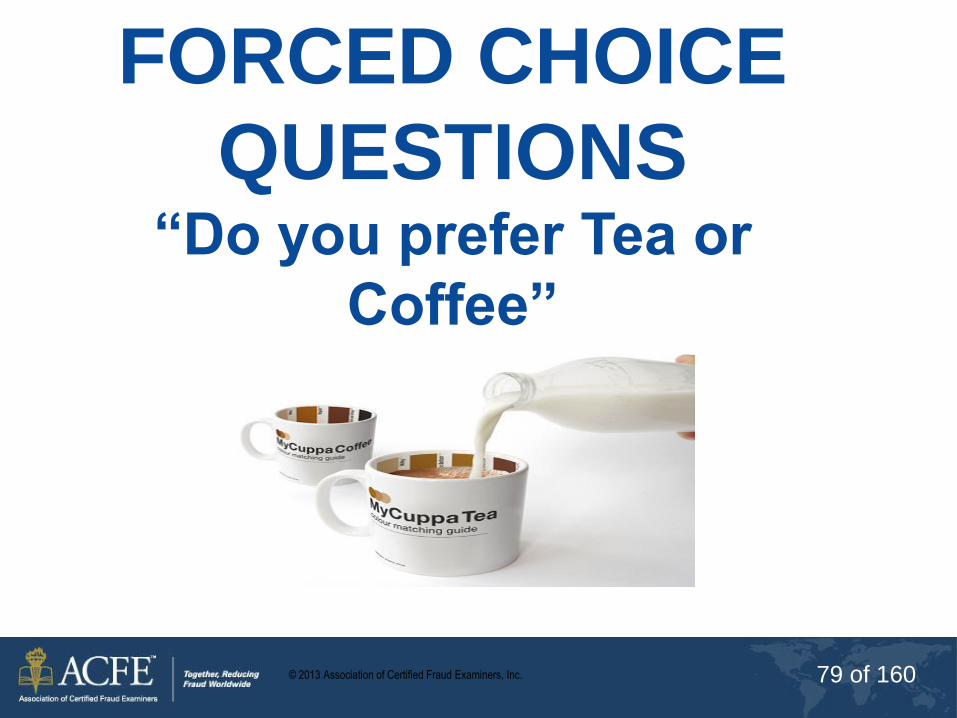

FORCED CHOICE

QUESTIONS “Do you prefer Tea or

Coffee”

© 2013 Association of Certified Fraud Examiners, Inc. 80 of 160

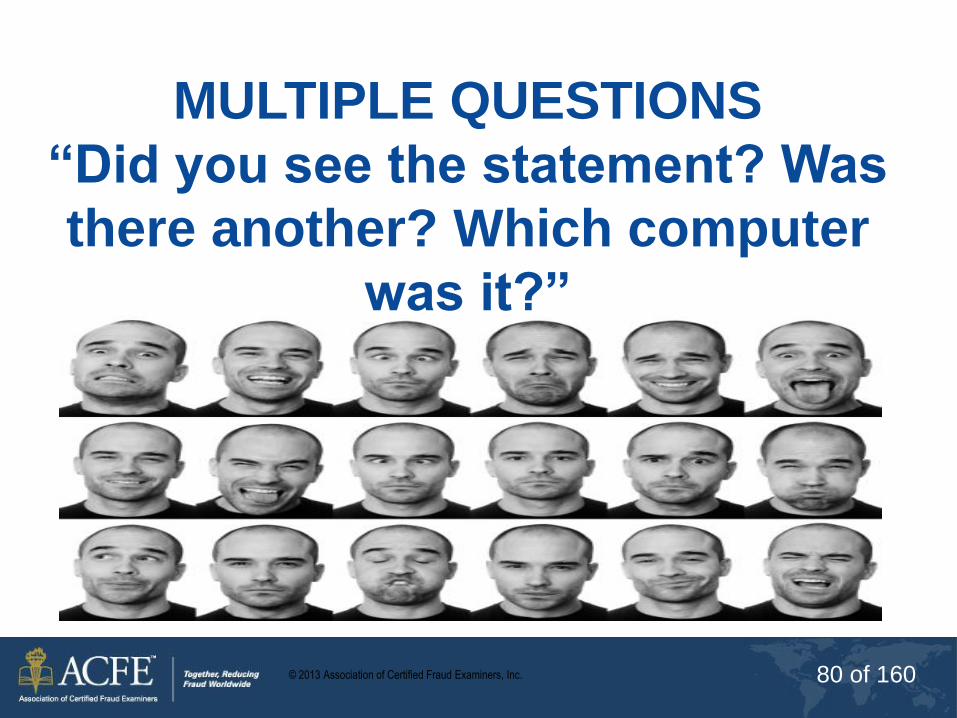

MULTIPLE QUESTIONS

“Did you see the statement? Was

there another? Which computer

was it?”

© 2013 Association of Certified Fraud Examiners, Inc. 81 of 160

LEADING AND

MISLEADING

QUESTIONS

© 2013 Association of Certified Fraud Examiners, Inc. 82 of 160

The distinction between a

Leading and Misleading

questions concerns the nature of

the implied response.

The first leads the interviewee to

a correct response whereas the

second leads the interviewee to

an incorrect response

© 2013 Association of Certified Fraud Examiners, Inc. 83 of 160

Leading questions and misleading questions introduce information to the interviewee and imply it is the correct or incorrect response

- Was his jacket black? - And was the car a Ford? - Did you go straight home?

© 2013 Association of Certified Fraud Examiners, Inc. 84 of 160

COMPLEX QUESTIONS

Complex questions occur when the question is not well thought out by the interviewer:

‘You said that you’ve never been there before but I think that you did go there, and that you said you’ve never been there because you know you would get into trouble for being there because you know that place was unsafe. Isn’t that so?’

© 2013 Association of Certified Fraud Examiners, Inc. 85 of 160

Questions to avoid

• Statement / Opinion type questions are those that attempt to impose the interviewers thoughts and ideas on the interviewee.

– We’ve spoken to the witness and she’s telling the truth. (No evidence.)

– You’re lying, I know you are!

– Are you sure you don’t know what happened .....

© 2013 Association of Certified Fraud Examiners, Inc. 86 of 160

• Negative phrasing occurs when a

question begins with a negative statement

and seeks the interviewee’s agreement

– You’re not qualified, are you?

– You didn’t see it, did you?

– You don’t work here, yes?

© 2013 Association of Certified Fraud Examiners, Inc. 87 of 160

• Hypothetical questions are suggestive questions about things that may not have actually happened (i.e., the ‘what if’ factor).

– You say you didn’t transfer the funds, but

if you did transfer the funds would you have benefited from them?

– If you were the manger what do you think you would have done?

– Would you recognise this person if you saw them again?

© 2013 Association of Certified Fraud Examiners, Inc. 88 of 160

ASSUMPTIONS

Do not assume anything. Seek

clarification from the interviewee. If they

don’t know, tell them that its is okay to

say so.

© 2013 Association of Certified Fraud Examiners, Inc. 89 of 160

REMEMBER –

The way in which interviewers structure

questions can have a marked influence

on the responses given by the witness or

suspects.

Thus, it is imperative to understand the

nature of questioning in order to conduct

the most effective and non-biasing

conversation in order to obtain quality

evidence.

© 2013 Association of Certified Fraud Examiners, Inc. 90 of 160

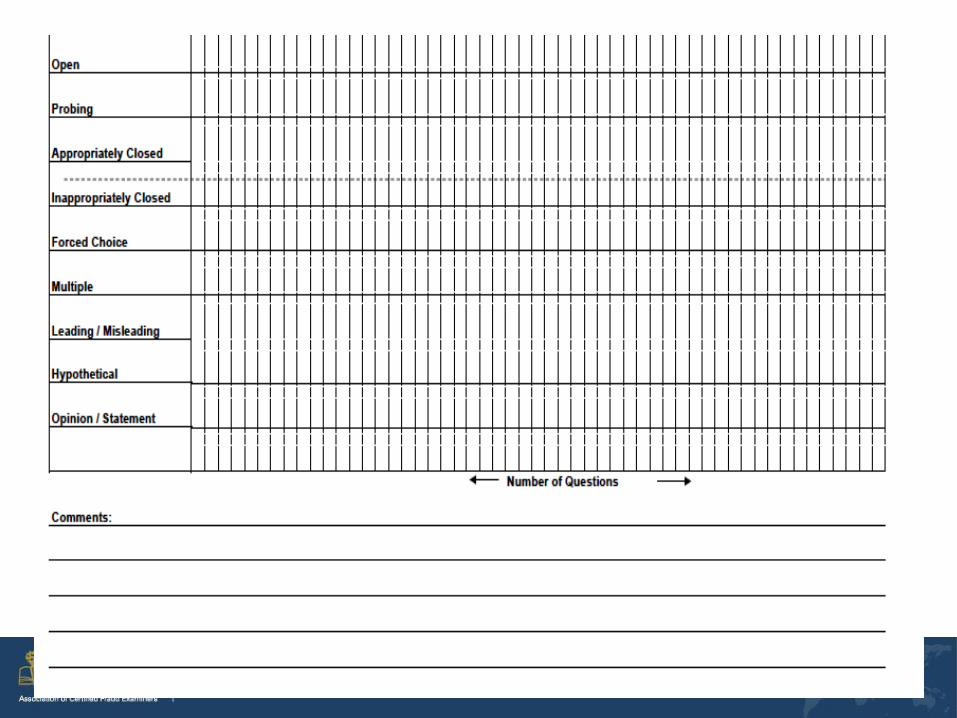

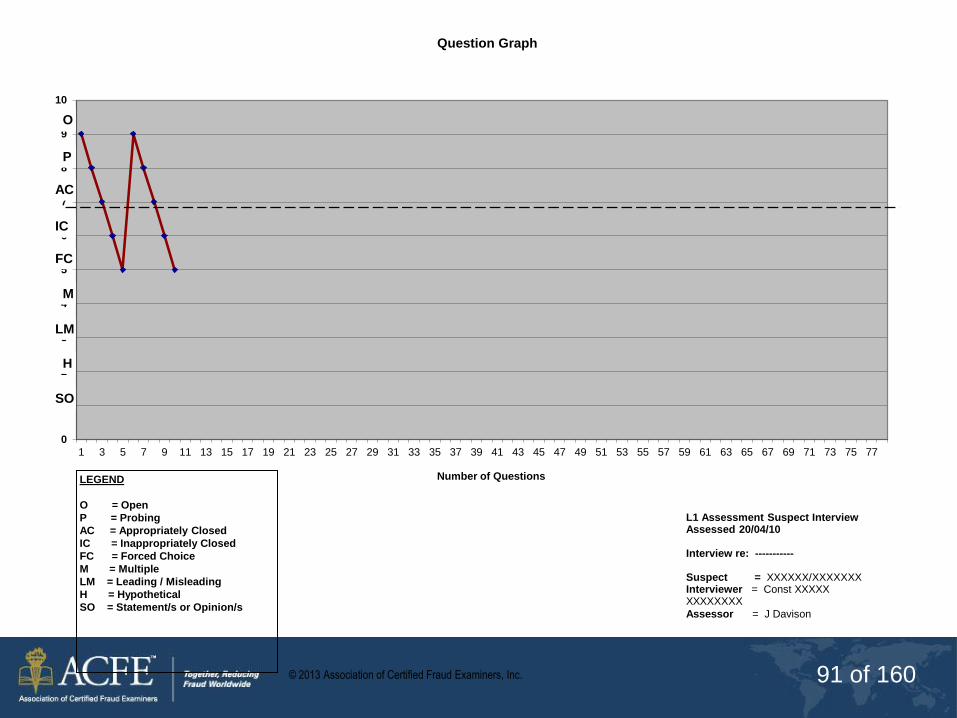

© 2013 Association of Certified Fraud Examiners, Inc. 91 of 160

0

1

2

3

4

5

6

7

8

9

10

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77

Number of Questions

Question Graph

LEGEND

O = Open

P = Probing

AC = Appropriately Closed

IC = Inappropriately Closed

FC = Forced Choice

M = Multiple

LM = Leading / Misleading

H = Hypothetical

SO = Statement/s or Opinion/s

L1 Assessment Suspect Interview Assessed 20/04/10 Interview re: ----------- Suspect = XXXXXX/XXXXXXX Interviewer = Const XXXXX XXXXXXXX

Assessor = J Davison

O

P

AC

IC

FC

M

LM

H

SO

© 2013 Association of Certified Fraud Examiners, Inc. 92 of 160

POLICE

INTERVIEW

TECHNIQUES

© 2013 Association of Certified Fraud Examiners, Inc. 93 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 94 of 160

Aim:

To enable delegates to gain knowledge of the various

questioning styles, the effects of each and identify the

correct questioning style to use in order to interview

any interviewee.

Objectives:

a)Define the various questioning styles.

b)Explain the positive/negative effects the various

styles have on a interviewee.

c)Demonstrate the correct questioning style required.

QUESTIONING STYLE

© 2013 Association of Certified Fraud Examiners, Inc. 95 of 160

CONVERSATION

MANAGEMENT (CM)

© 2013 Association of Certified Fraud Examiners, Inc. 96 of 160

Aim To provide staff with the necessary skills to competently interview

a compliant and non compliant suspect using the conversation

management (CM) model of interviewing.

Objectives

Understand the importance of the caution, and it’s meaning.

Understand the importance of adverse inference

Apply conversation management (CM) in a simulated interview

(compliant and non-compliant)

Evaluate their own and other staff interviews.

© 2013 Association of Certified Fraud Examiners, Inc. 97 of 160

PEACE • Plan and Prepare

• Engage and explain

• Account, clarification, compare,

and contrast

• Closure

• Evaluate

© 2013 Association of Certified Fraud Examiners, Inc. 98 of 160

Plan & Preparation

Planning;

“the mental process of getting

ready to interview…”

Preparation;

“considering what needs to be

made ready..”

© 2013 Association of Certified Fraud Examiners, Inc. 99 of 160

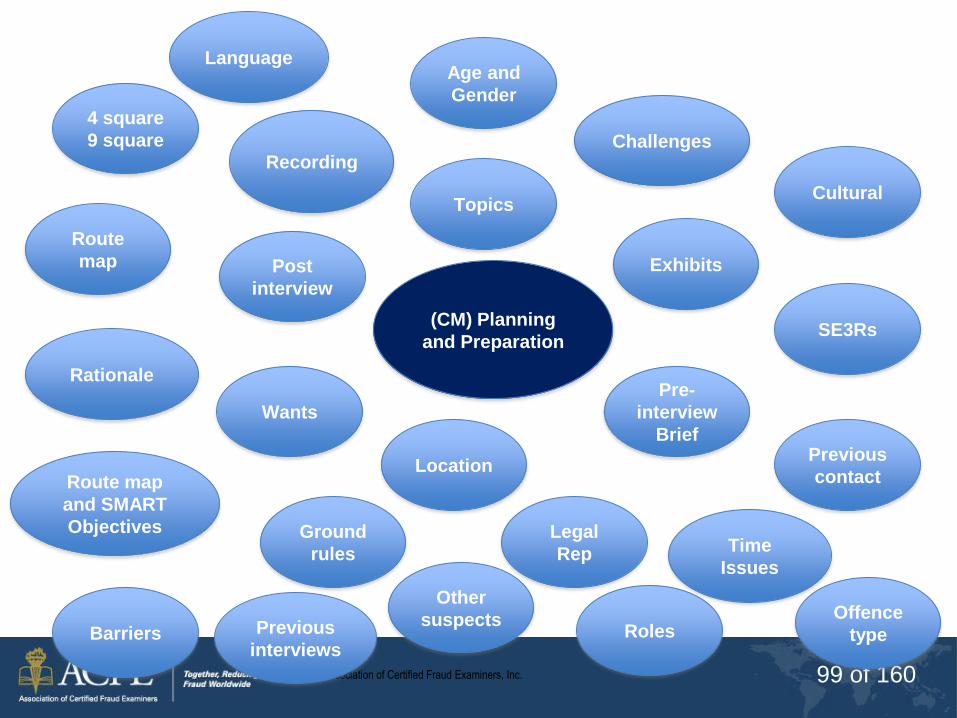

(CM) Planning

and Preparation

Topics

Post

interview

Location

Route

map

Rationale

Route map

and SMART

Objectives

Barriers

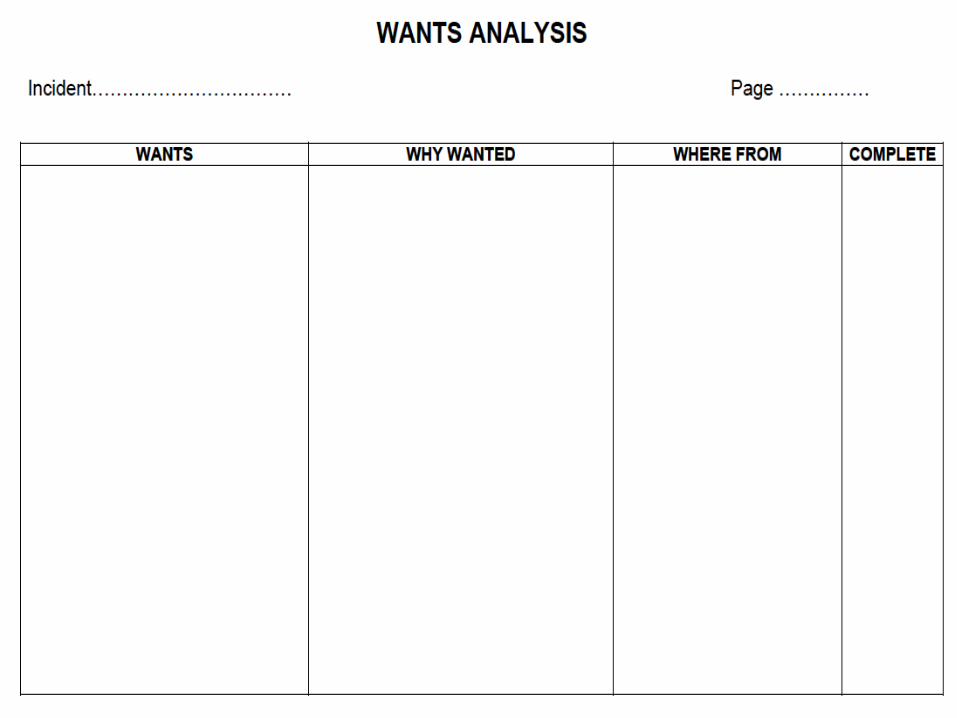

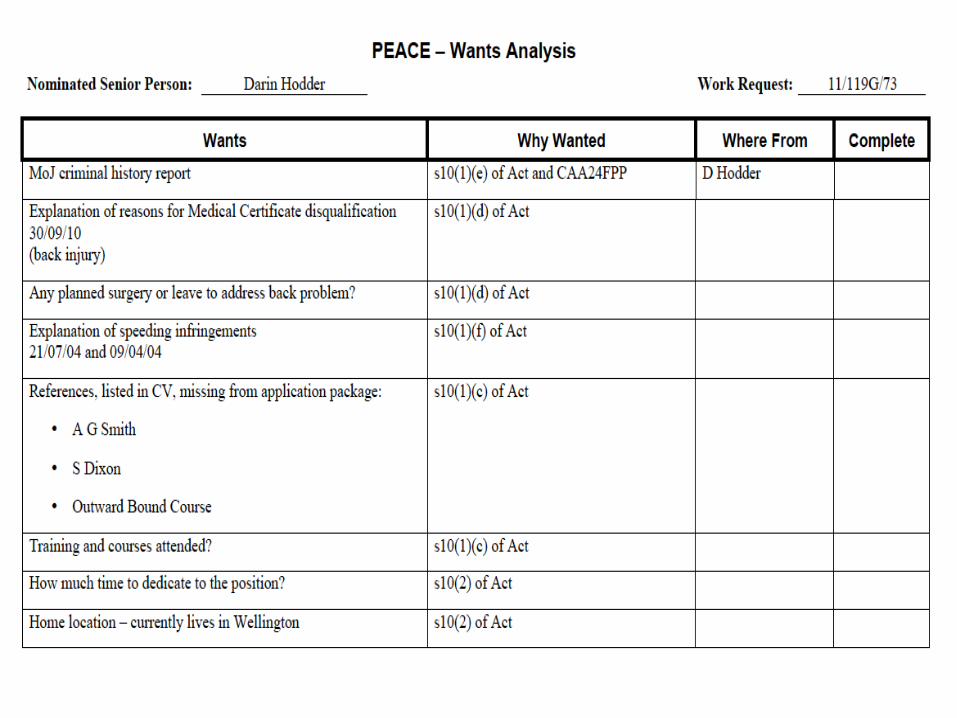

Wants

Ground

rules

Previous

interviews

Other

suspects

Legal

Rep

Roles

Time

Issues

Offence

type

Previous

contact

Pre-

interview

Brief

Exhibits

Cultural

Language

SE3Rs

Challenges

Age and

Gender

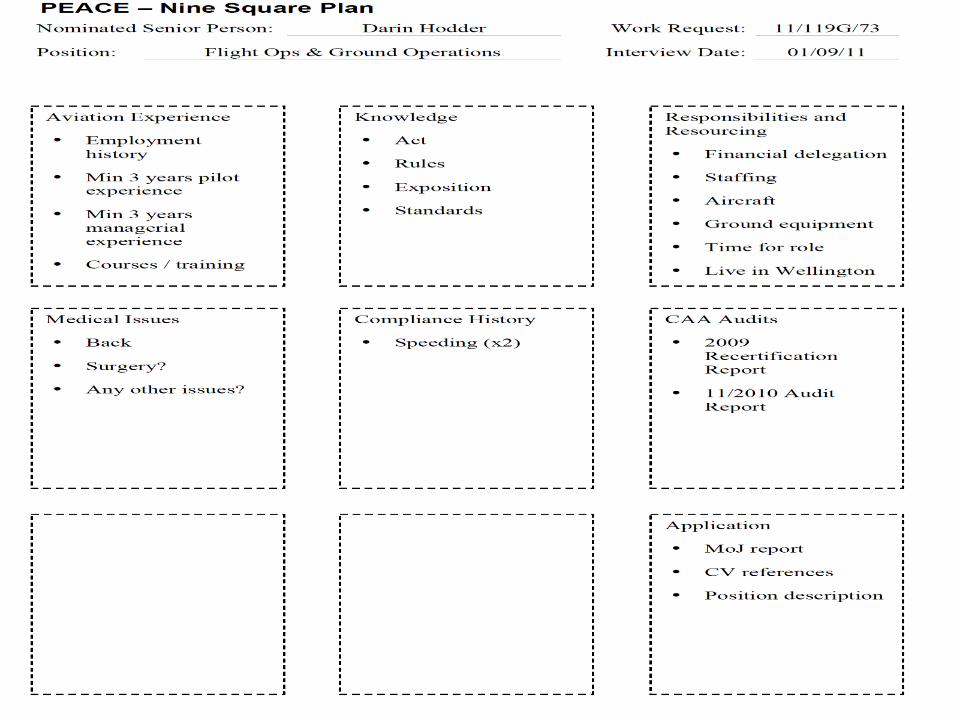

4 square

9 square Recording

© 2013 Association of Certified Fraud Examiners, Inc. 100 of 160

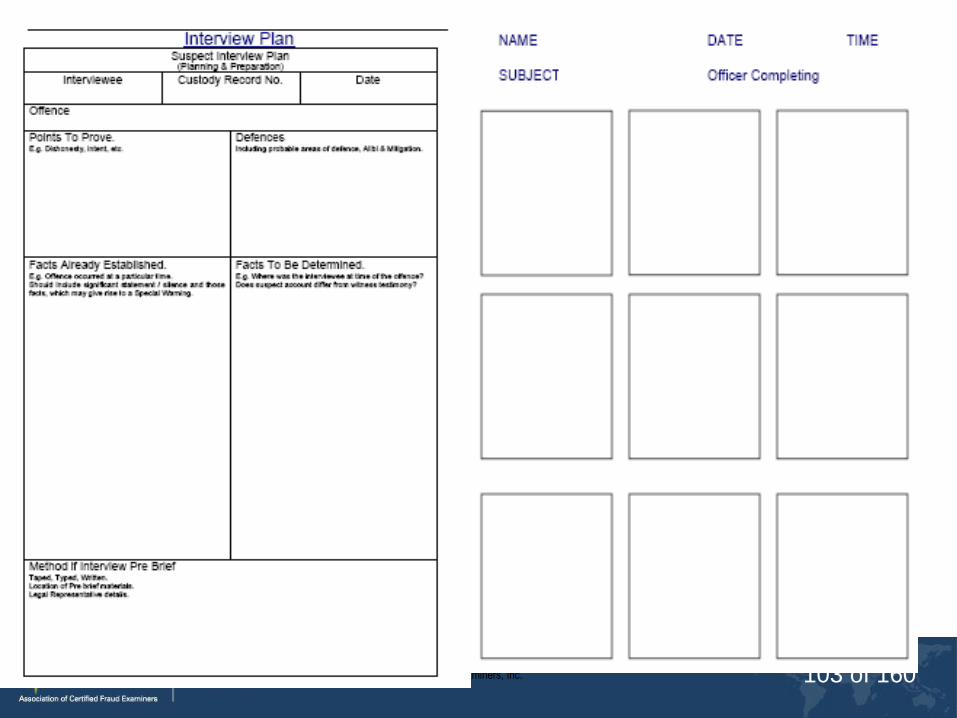

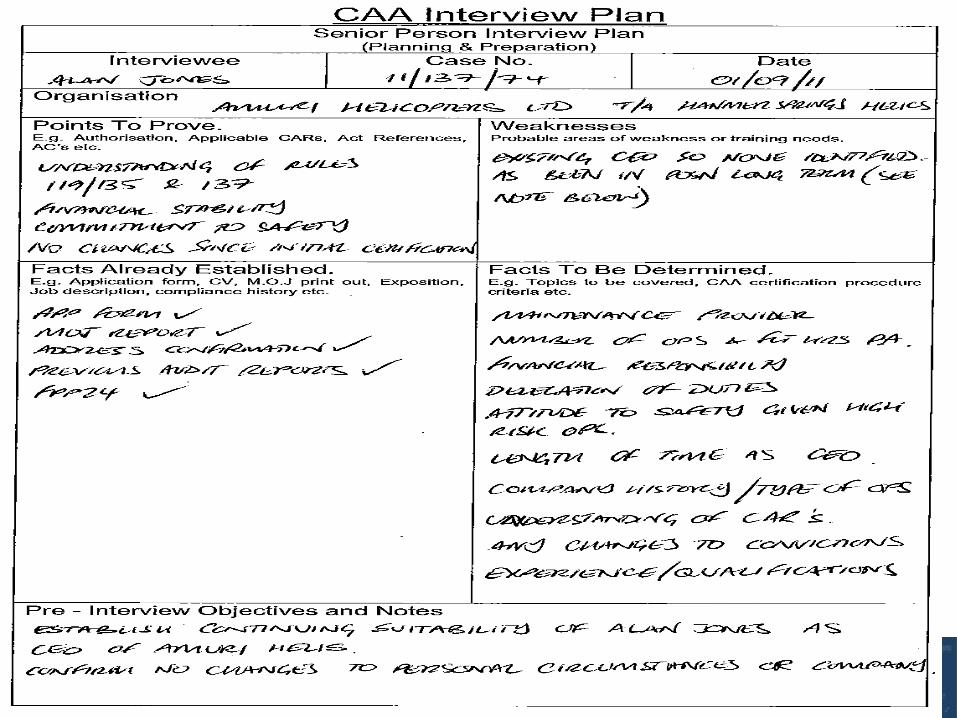

Planning templates

© 2013 Association of Certified Fraud Examiners, Inc. 101 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 102 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 103 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 104 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 105 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 106 of 160

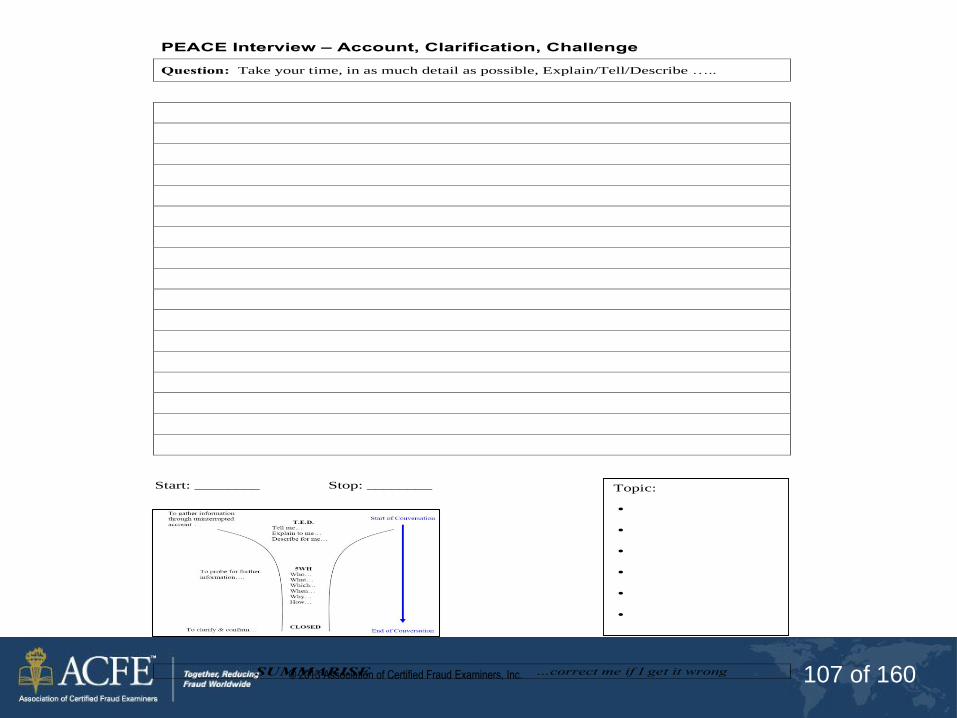

© 2013 Association of Certified Fraud Examiners, Inc. 107 of 160 SUMMARISE …correct me if I get it wrong

PEACE Interview – Account, Clarification, Challenge

Question: Take your time, in as much detail as possible, Explain/Tell/Describe …..

Topic:

·

·

·

·

·

·

Start: ________ Stop: ________

© 2013 Association of Certified Fraud Examiners, Inc. 108 of 160

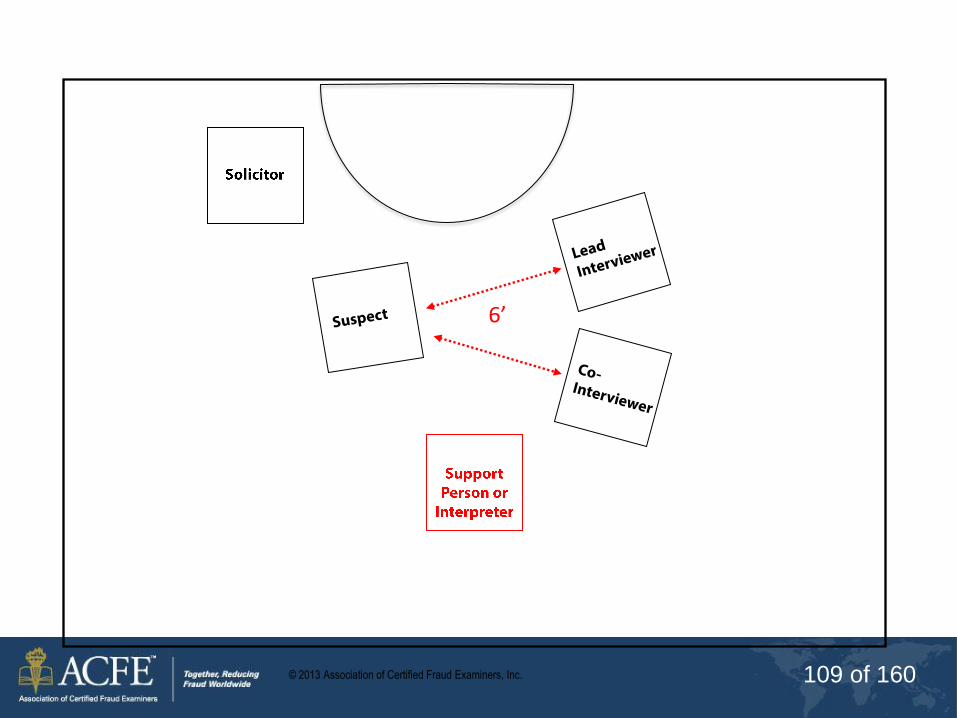

© 2013 Association of Certified Fraud Examiners, Inc. 109 of 160

6’

© 2013 Association of Certified Fraud Examiners, Inc. 110 of 160

Pre-Interview Briefings

• A practical guide

© 2013 Association of Certified Fraud Examiners, Inc. 111 of 160

Pre-interview briefings

Aim • To present and develop knowledge with regard to ‘pre-

interview briefings’.

Objectives

• Recognise the reasons for conducting ‘Pre-interview

briefings’.

• Identify facts for use in a ‘pre-interview briefing’.

• Construct a written ‘pre-interview briefing’ document.

• Analyse a written ‘pre-interview briefing’ document.

© 2013 Association of Certified Fraud Examiners, Inc. 112 of 160

What are they?

• Facts you are willing to disclose to the legal advisor or suspect prior to a suspect interview.

• Why disclose any facts?

• To support the Disclosure Acts.

© 2013 Association of Certified Fraud Examiners, Inc. 113 of 160

What evidence do you

have to disclose? • You do not have to disclose any evidence,……

however

• Giving nothing, will more than likely result in no

adverse inference being drawn at court.

• Ref: Regina v Nottle February 2004

© 2013 Association of Certified Fraud Examiners, Inc. 114 of 160

Who decides what

evidence to disclose?

• You do … although this may be a joint decision

when working as part of a team.

• Look at each case on an individual basis.

• Decide what to give and what not to give and

record your rationale behind this.

© 2013 Association of Certified Fraud Examiners, Inc. 115 of 160

How do we disclose

the information? • A typed written document should be prepared.

• A formal pre-interview briefing should be held with the legal advisor or suspect.

• The pre-interview briefing conversation should be recorded on audio tape

© 2013 Association of Certified Fraud Examiners, Inc. 116 of 160

The briefing • Hand the legal advisor/suspect a copy of the

written ‘pre-interview’ briefing document.

• Read it aloud (it’s on tape!).

• Invite questions.

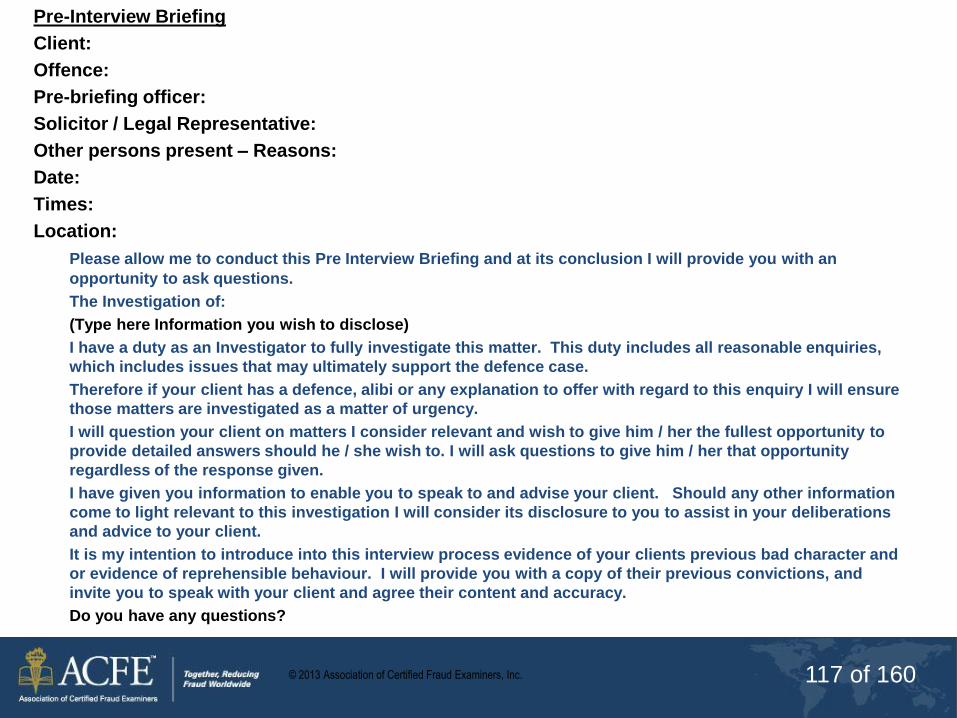

© 2013 Association of Certified Fraud Examiners, Inc. 117 of 160

Pre-Interview Briefing

Client:

Offence:

Pre-briefing officer:

Solicitor / Legal Representative:

Other persons present – Reasons:

Date:

Times:

Location:

Please allow me to conduct this Pre Interview Briefing and at its conclusion I will provide you with an

opportunity to ask questions.

The Investigation of:

(Type here Information you wish to disclose)

I have a duty as an Investigator to fully investigate this matter. This duty includes all reasonable enquiries,

which includes issues that may ultimately support the defence case.

Therefore if your client has a defence, alibi or any explanation to offer with regard to this enquiry I will ensure

those matters are investigated as a matter of urgency.

I will question your client on matters I consider relevant and wish to give him / her the fullest opportunity to

provide detailed answers should he / she wish to. I will ask questions to give him / her that opportunity

regardless of the response given.

I have given you information to enable you to speak to and advise your client. Should any other information

come to light relevant to this investigation I will consider its disclosure to you to assist in your deliberations

and advice to your client.

It is my intention to introduce into this interview process evidence of your clients previous bad character and

or evidence of reprehensible behaviour. I will provide you with a copy of their previous convictions, and

invite you to speak with your client and agree their content and accuracy.

Do you have any questions?

© 2013 Association of Certified Fraud Examiners, Inc. 118 of 160

Do you have to

answer the questions? • You should acknowledge the questions.

• Decide if you want to expand on all, or aspects

of the written document.

• Answer appropriately, for example “I’m not

prepared to enhance on that as I’m looking for

an untainted account from your client”

• Record any further information disclosed.

© 2013 Association of Certified Fraud Examiners, Inc. 119 of 160

Can they

have the copy? • Yes……let them keep their copy to

write on, and for reference.

• Get them to sign your copy, e.g. ‘Copy

received by…………………..’

© 2013 Association of Certified Fraud Examiners, Inc. 120 of 160

Scenario • Investment company has set up a Ponzi

scheme.

• An investor has provided a statement.

• There are documents which display that the

company has manipulated the products and

listed them incorrectly.

© 2013 Association of Certified Fraud Examiners, Inc. 121 of 160

Modus Operandi

• The company has set up a

fraudulent investment

operation.

© 2013 Association of Certified Fraud Examiners, Inc. 122 of 160

Evidence • Investor statement giving details of how

they were directed to invest in this scheme

• Further evidence from other employees and other companies

• Numerous documents (e.g., bank statements, invoices, company letters, emails)

© 2013 Association of Certified Fraud Examiners, Inc. 123 of 160

The suspect awaits

interview • What facts/evidence do you

disclose?

It’s your decision!

© 2013 Association of Certified Fraud Examiners, Inc. 124 of 160

Have you disclosed

enough or too much?

• What affect could your disclosure

have on the……

• …interview and……

• …any subsequent inferences at

court?

© 2013 Association of Certified Fraud Examiners, Inc. 125 of 160

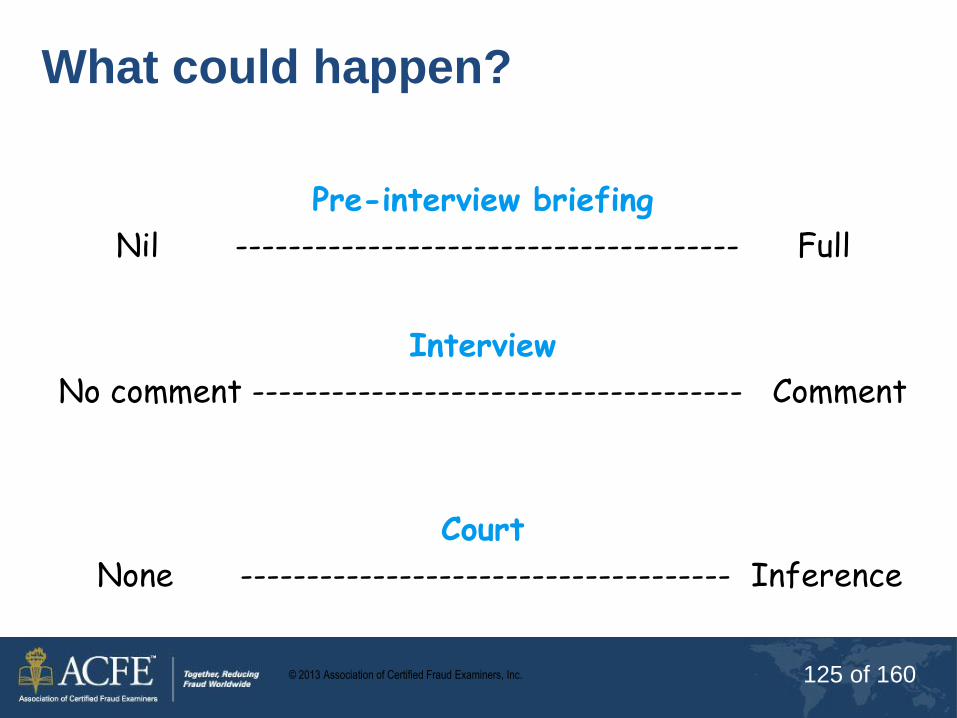

What could happen?

Pre-interview briefing

Nil -------------------------------------- Full

Interview

No comment ------------------------------------- Comment

Court

None ------------------------------------- Inference

© 2013 Association of Certified Fraud Examiners, Inc. 126 of 160

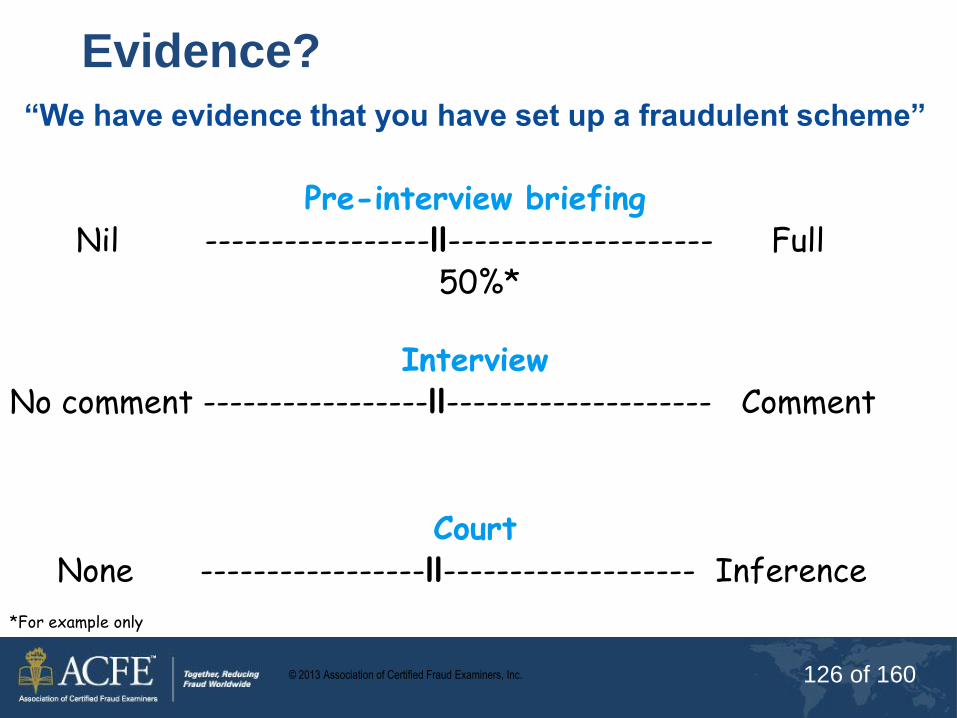

Evidence?

“We have evidence that you have set up a fraudulent scheme”

Pre-interview briefing

Nil -----------------ll-------------------- Full 50%*

Interview No comment -----------------ll-------------------- Comment

Court None -----------------ll------------------- Inference *For example only

© 2013 Association of Certified Fraud Examiners, Inc. 127 of 160

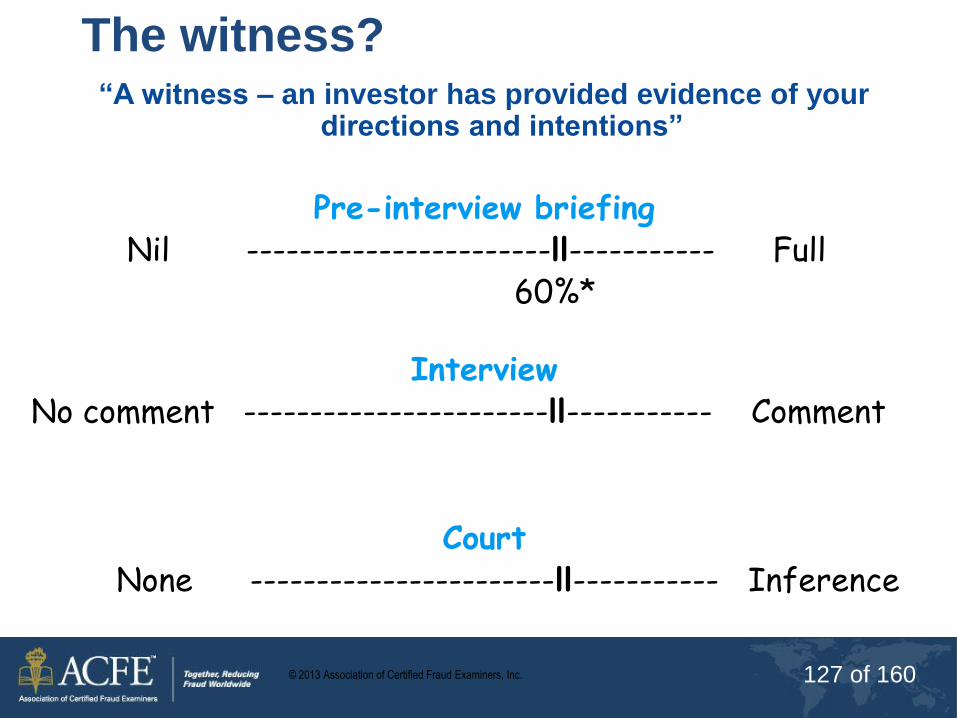

The witness? “A witness – an investor has provided evidence of your

directions and intentions”

Pre-interview briefing

Nil -----------------------ll----------- Full 60%*

Interview No comment -----------------------ll----------- Comment

Court None -----------------------ll----------- Inference

© 2013 Association of Certified Fraud Examiners, Inc. 128 of 160

Think before you disclose?

• What account do I want from the suspect at

this stage?

• How can I best achieve it through the pre-

interview briefing?

© 2013 Association of Certified Fraud Examiners, Inc. 129 of 160

Phased or staged

pre-interview briefings

• What are they?

• Information/facts given to the legal

advisor/suspect at different phases/stages of

the interview process.

• You decide when and

what to disclose.

© 2013 Association of Certified Fraud Examiners, Inc. 130 of 160

Pre-interview briefings

Aim • To present and develop knowledge with regard to ‘pre-

interview briefings’.

Objectives

• Recognise the reasons for conducting ‘Pre-interview

briefings’.

• Identify facts for use in a ‘pre-interview briefing’.

• Construct a written ‘pre-interview briefing’ document.

• Analyse a written ‘pre-interview briefing’ document.

© 2013 Association of Certified Fraud Examiners, Inc. 131 of 160

Plan & Preparation

Engage & Explain

Rapport Reason Routines Route Map

© 2013 Association of Certified Fraud Examiners, Inc. 132 of 160

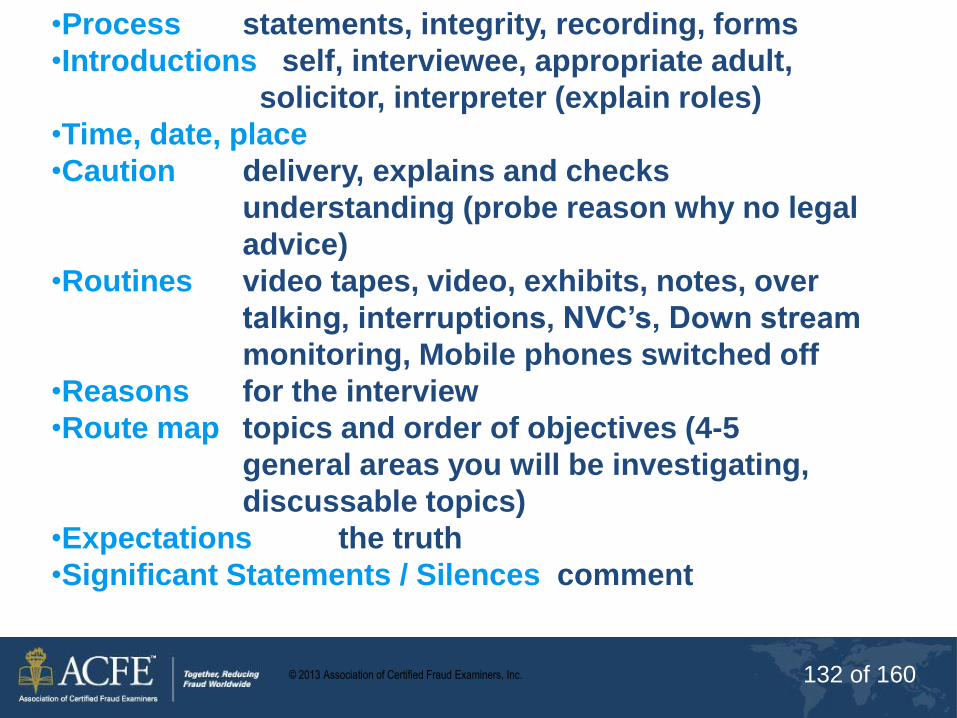

Introduction to Participant Interview Tapes Get the tapes recording at the earliest opportunity Intro This should include the details of all the persons present, the place of the interview, the date and time the interview commenced. F.I.L.A. Explain to the Participant their entitlement to free and independent legal advice (even if Legal Rep. present at interview or not). Caution 1. Deliver the caution in conversational style 2. Explain the 3 parts of the caution to the Participant. 3. Ask the Participant to explain their understanding of the caution so that you can check that they DO have an understanding of it. Routines As part of your routines, you should explain other aspects in the interview room. e.g. V video cameras in the room (if applicable) E exhibits in the room and their use in the interview N notes that you will be taking T what will happen to the interview tapes (Include remote monitoring if applicable

•Process statements, integrity, recording, forms

•Introductions self, interviewee, appropriate adult,

solicitor, interpreter (explain roles)

•Time, date, place

•Caution delivery, explains and checks

understanding (probe reason why no legal

advice)

•Routines video tapes, video, exhibits, notes, over

talking, interruptions, NVC’s, Down stream

monitoring, Mobile phones switched off

•Reasons for the interview

•Route map topics and order of objectives (4-5

general areas you will be investigating,

discussable topics)

•Expectations the truth

•Significant Statements / Silences comment

© 2013 Association of Certified Fraud Examiners, Inc. 133 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 134 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 135 of 160

1st Account

Engage & Explain

Plan & Prep

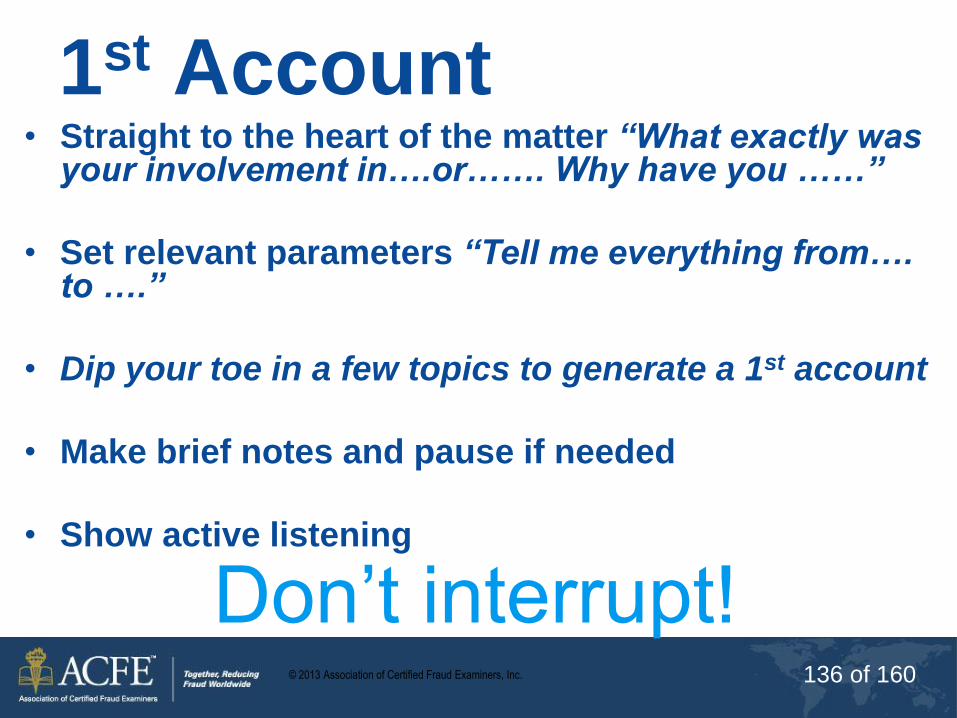

© 2013 Association of Certified Fraud Examiners, Inc. 136 of 160

1st Account • Straight to the heart of the matter “What exactly was

your involvement in….or……. Why have you ……”

• Set relevant parameters “Tell me everything from…. to ….”

• Dip your toe in a few topics to generate a 1st account

• Make brief notes and pause if needed

• Show active listening

Don’t interrupt!

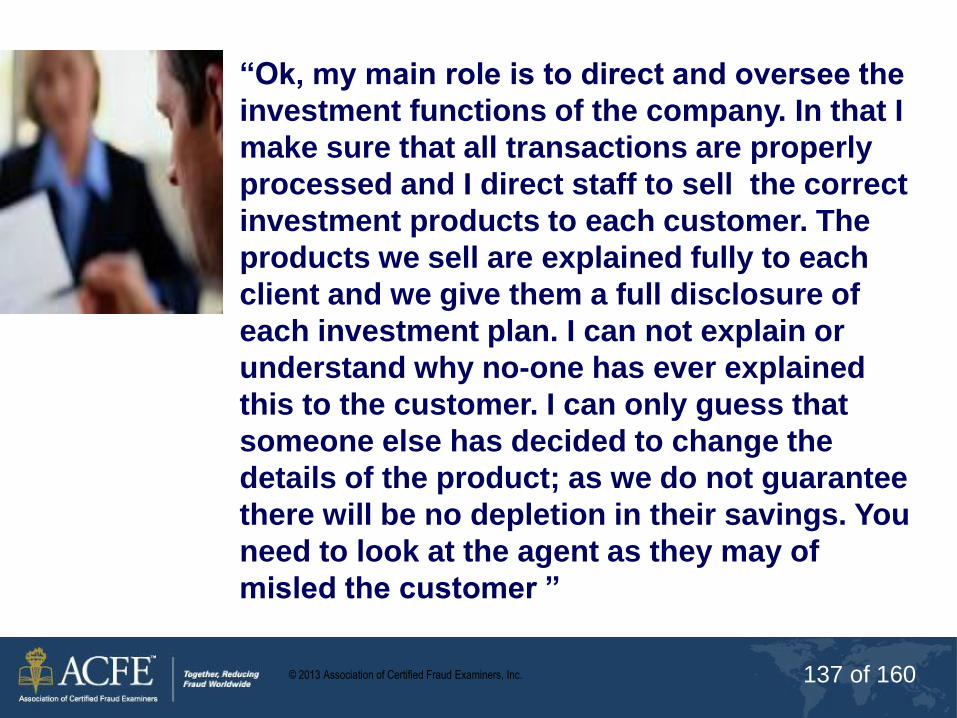

© 2013 Association of Certified Fraud Examiners, Inc. 137 of 160

“Ok, my main role is to direct and oversee the

investment functions of the company. In that I

make sure that all transactions are properly

processed and I direct staff to sell the correct

investment products to each customer. The

products we sell are explained fully to each

client and we give them a full disclosure of

each investment plan. I can not explain or

understand why no-one has ever explained

this to the customer. I can only guess that

someone else has decided to change the

details of the product; as we do not guarantee

there will be no depletion in their savings. You

need to look at the agent as they may of

misled the customer ”

© 2013 Association of Certified Fraud Examiners, Inc. 138 of 160

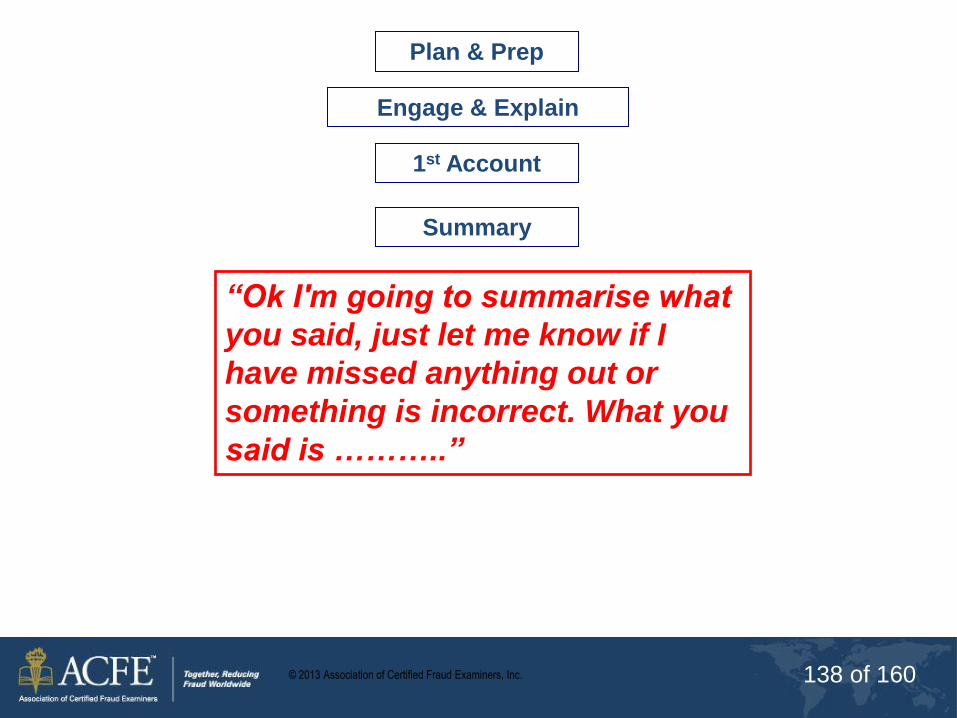

Summary

1st Account

Engage & Explain

Plan & Prep

“Ok I'm going to summarise what

you said, just let me know if I

have missed anything out or

something is incorrect. What you

said is ………..”

© 2013 Association of Certified Fraud Examiners, Inc. 139 of 160

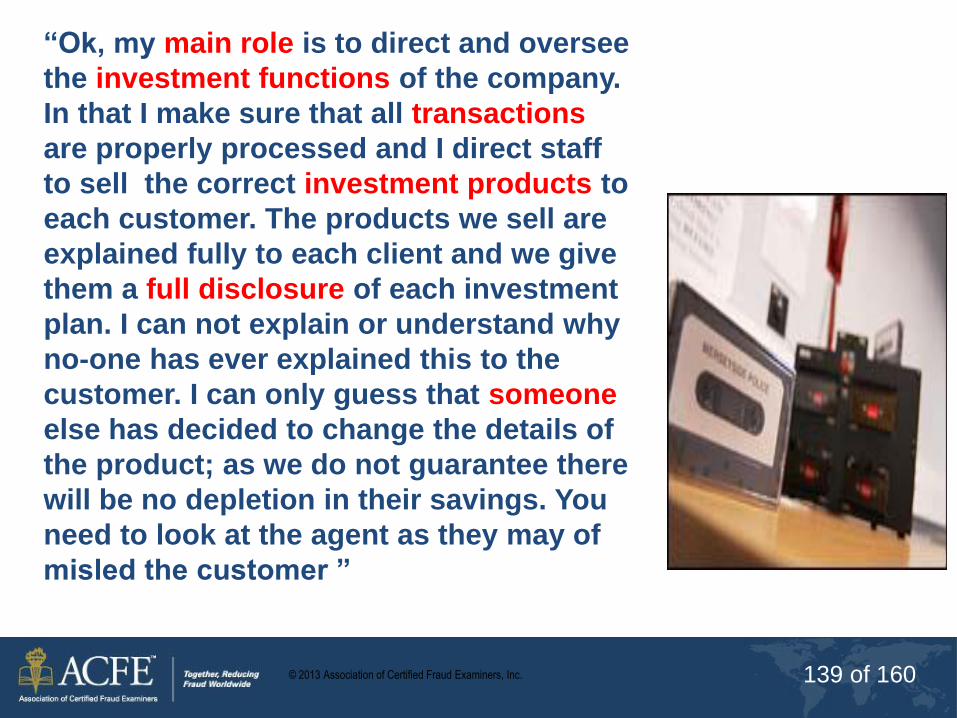

“Ok, my main role is to direct and oversee

the investment functions of the company.

In that I make sure that all transactions

are properly processed and I direct staff

to sell the correct investment products to

each customer. The products we sell are

explained fully to each client and we give

them a full disclosure of each investment

plan. I can not explain or understand why

no-one has ever explained this to the

customer. I can only guess that someone

else has decided to change the details of

the product; as we do not guarantee there

will be no depletion in their savings. You

need to look at the agent as they may of

misled the customer ”

© 2013 Association of Certified Fraud Examiners, Inc. 140 of 160

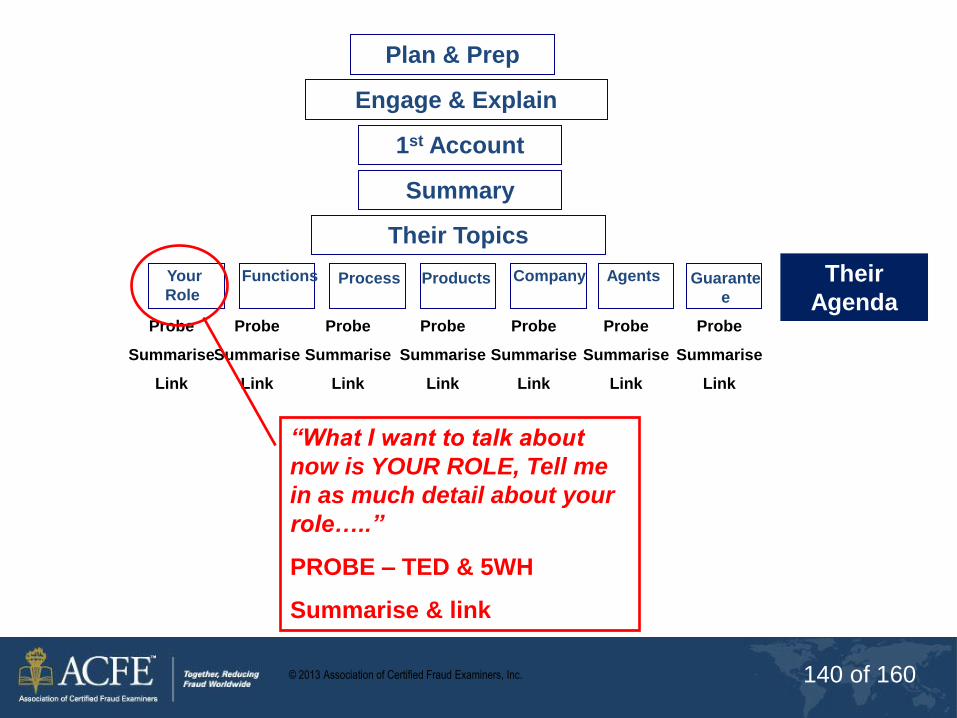

Summary

1st Account

Engage & Explain

Plan & Prep

Probe

Summarise

Link

Their Topics

Your

Role

Functions Process Products

Company Agents Guarante

e

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

“What I want to talk about

now is YOUR ROLE, Tell me

in as much detail about your

role…..”

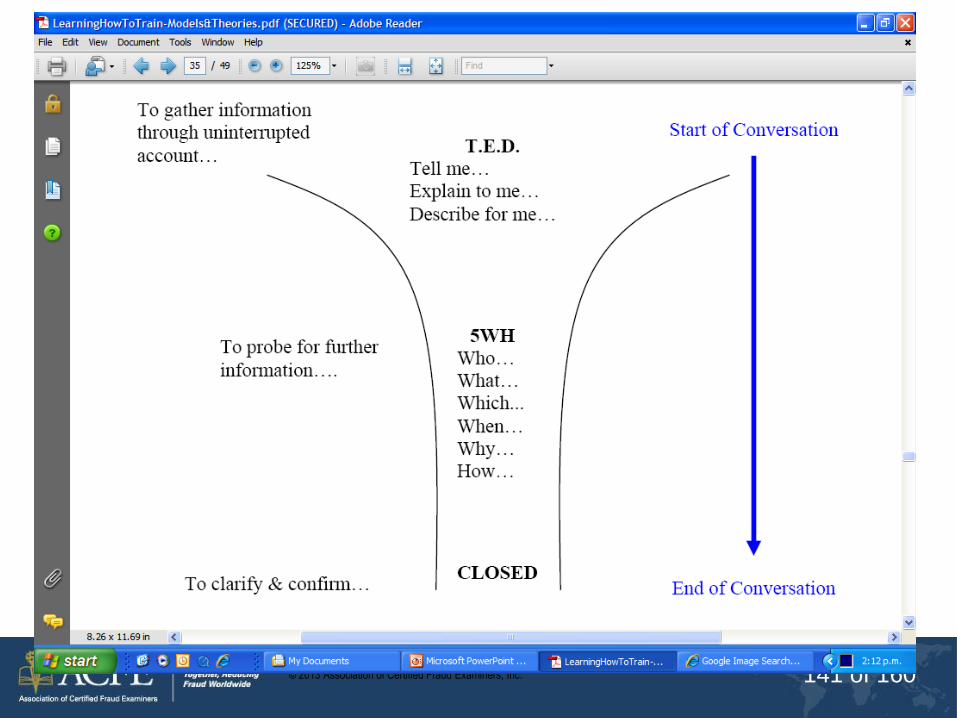

PROBE – TED & 5WH

Summarise & link

Their

Agenda

© 2013 Association of Certified Fraud Examiners, Inc. 141 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 142 of 160

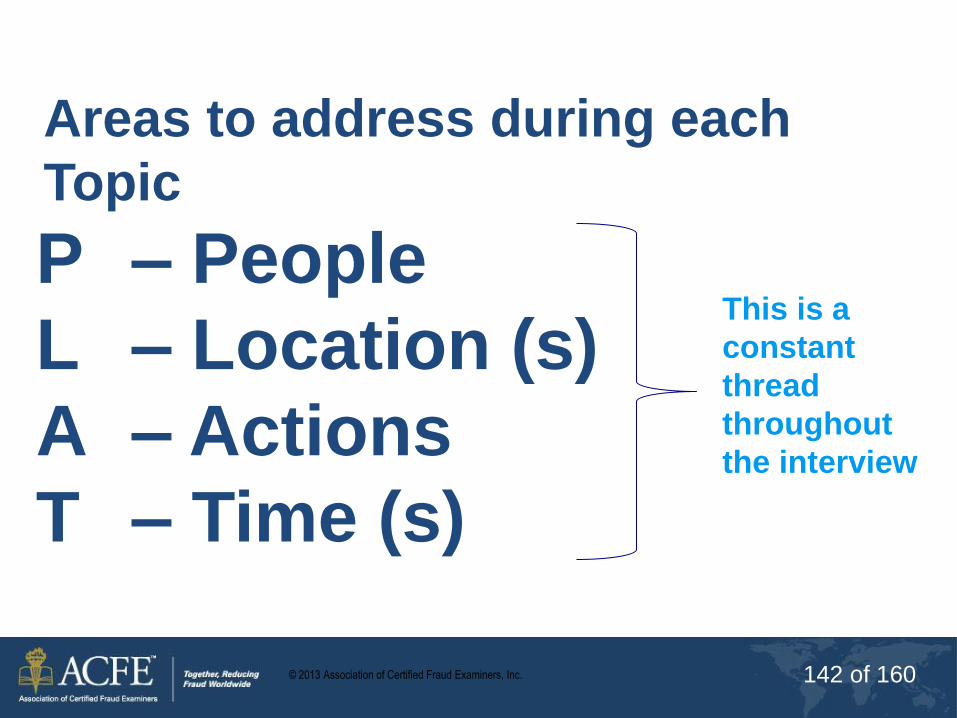

Areas to address during each

Topic

P – People

L – Location (s)

A – Actions

T – Time (s)

This is a

constant

thread

throughout

the interview

© 2013 Association of Certified Fraud Examiners, Inc. 143 of 160

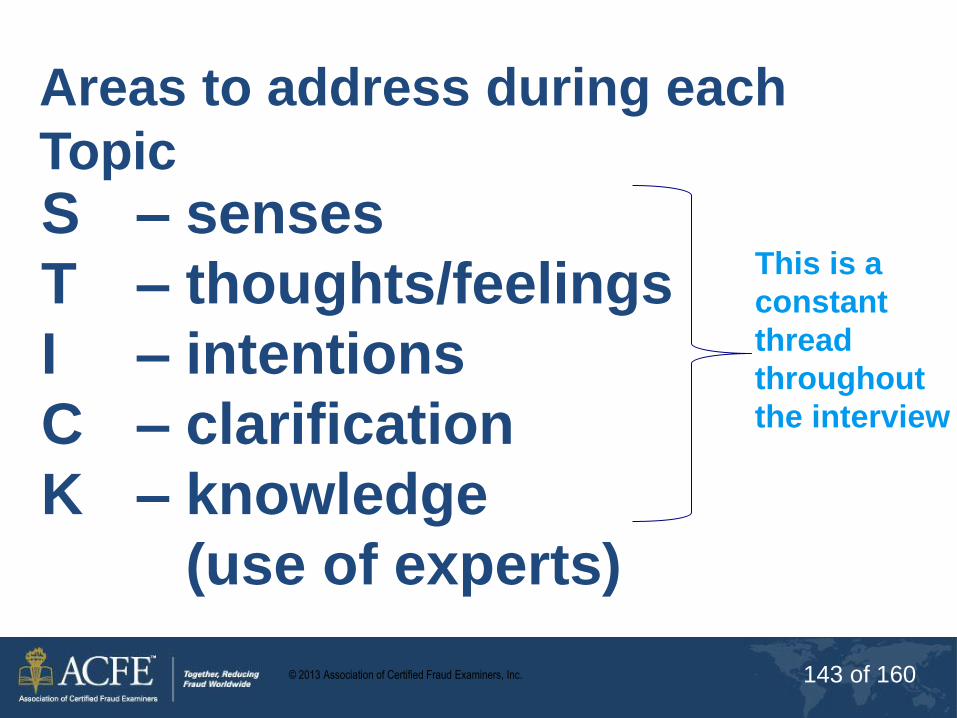

Areas to address during each

Topic

S – senses

T – thoughts/feelings

I – intentions

C – clarification

K – knowledge

(use of experts)

This is a

constant

thread

throughout

the interview

© 2013 Association of Certified Fraud Examiners, Inc. 144 of 160

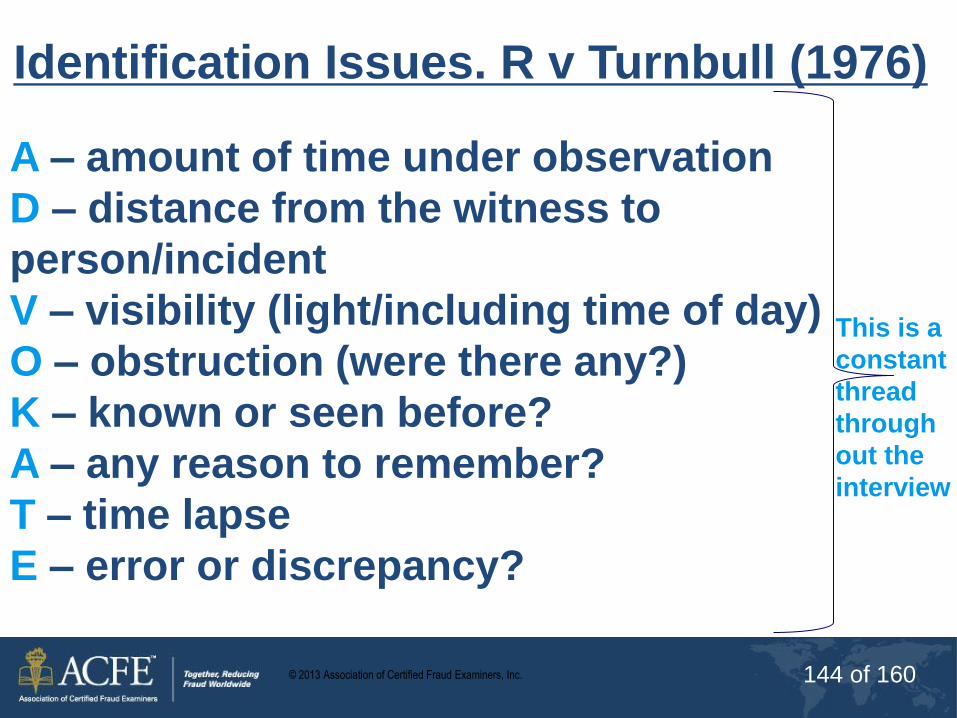

Identification Issues. R v Turnbull (1976)

A – amount of time under observation

D – distance from the witness to

person/incident

V – visibility (light/including time of day)

O – obstruction (were there any?)

K – known or seen before?

A – any reason to remember?

T – time lapse

E – error or discrepancy?

This is a

constant

thread

through

out the

interview

© 2013 Association of Certified Fraud Examiners, Inc. 145 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 146 of 160

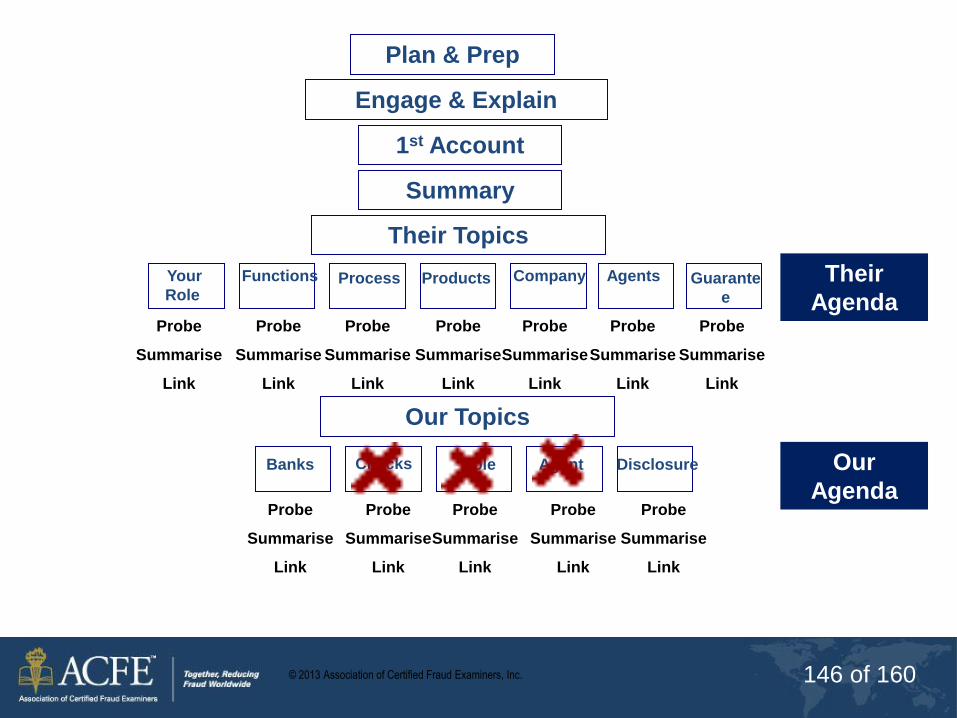

Summary

1st Account

Engage & Explain

Plan & Prep

Probe

Summarise

Link

Their Topics

Your

Role

Functions Process Products

Company Agents Guarante

e

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Their

Agenda

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Role

Our Topics

Banks Checks Agent

Disclosure Our

Agenda

© 2013 Association of Certified Fraud Examiners, Inc. 147 of 160

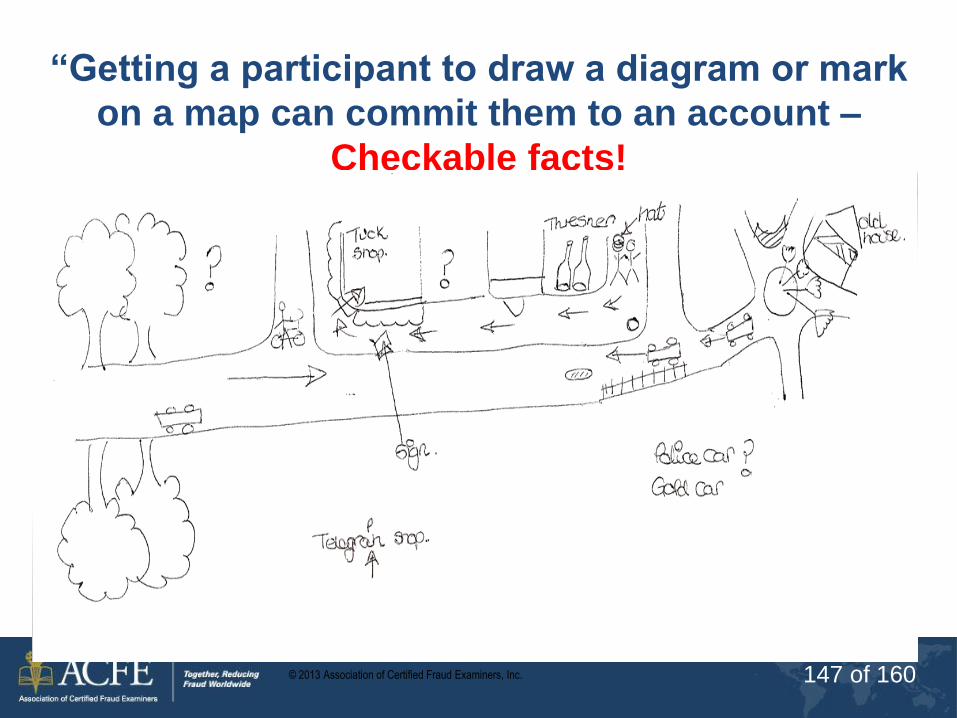

“Getting a participant to draw a diagram or mark

on a map can commit them to an account –

Checkable facts!

© 2013 Association of Certified Fraud Examiners, Inc. 148 of 160

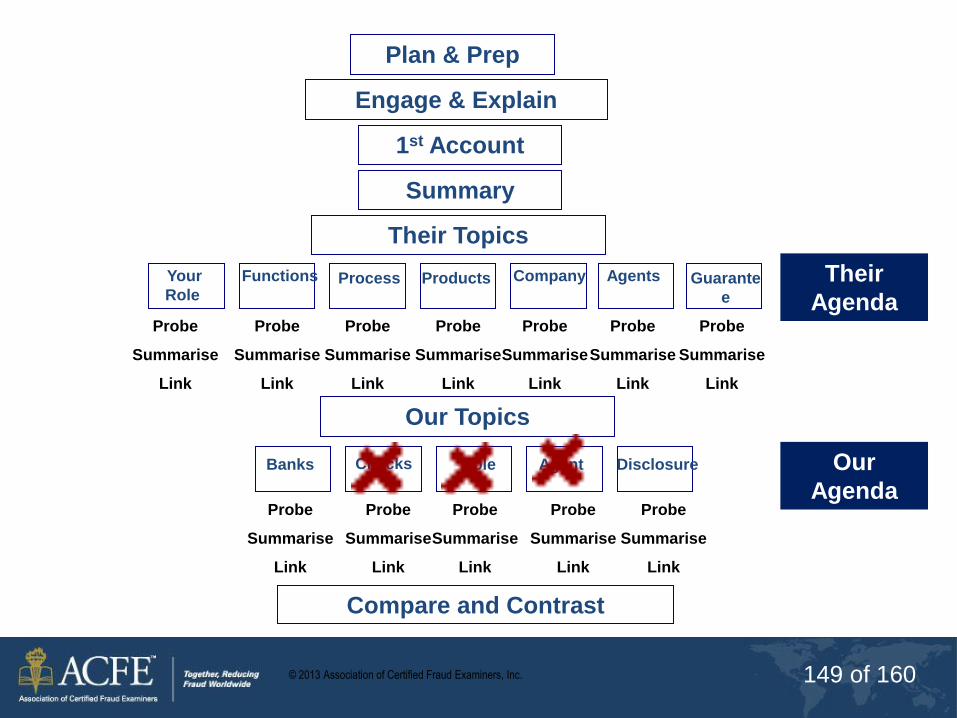

Probe, Summarise, & Link

• Questioning spiral

• Fine grain detail in important topic areas

• Obstacles to lying, provable lies, “flush out the truth”

• Keep it conversational

• Don’t be tempted to challenge

• Summarise – commits to memory, shows effective listening and commits the Participant to an account.

• Don’t repeat topics already covered

© 2013 Association of Certified Fraud Examiners, Inc. 149 of 160

Summary

1st Account

Engage & Explain

Plan & Prep

Probe

Summarise

Link

Their Topics

Your

Role

Functions Process Products

Company Agents Guarante

e

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Their

Agenda

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Role

Our Topics

Banks Checks Agent

Disclosure Our

Agenda

Compare and Contrast

© 2013 Association of Certified Fraud Examiners, Inc. 150 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 151 of 160

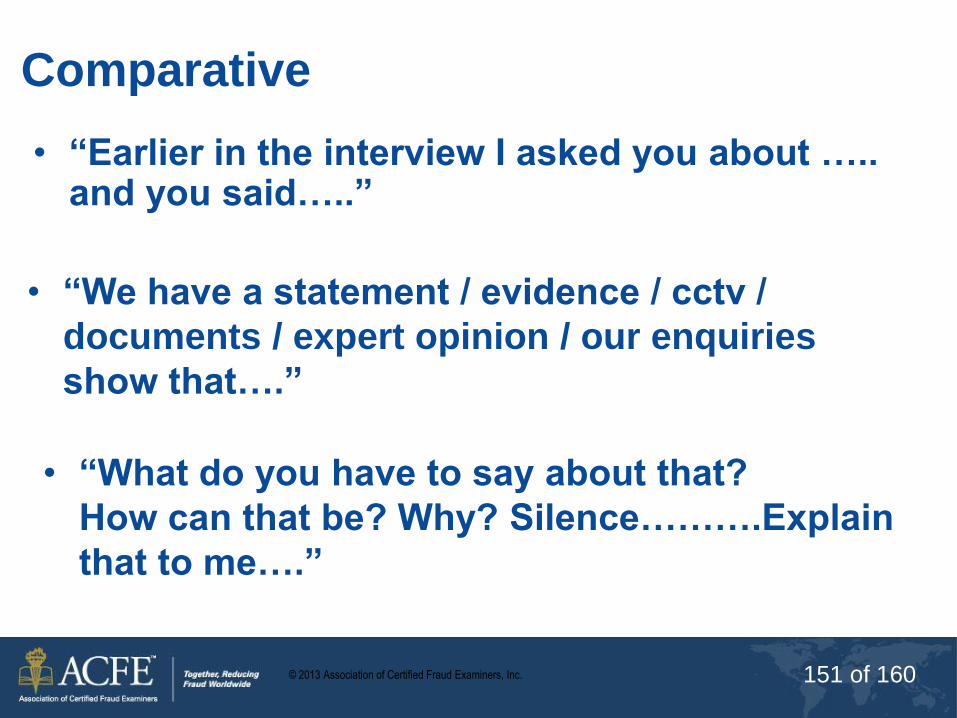

Comparative

• “Earlier in the interview I asked you about ….. and you said…..”

• “We have a statement / evidence / cctv /

documents / expert opinion / our enquiries

show that….”

• “What do you have to say about that?

How can that be? Why? Silence……….Explain

that to me….”

© 2013 Association of Certified Fraud Examiners, Inc. 152 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 153 of 160

© 2013 Association of Certified Fraud Examiners, Inc. 154 of 160

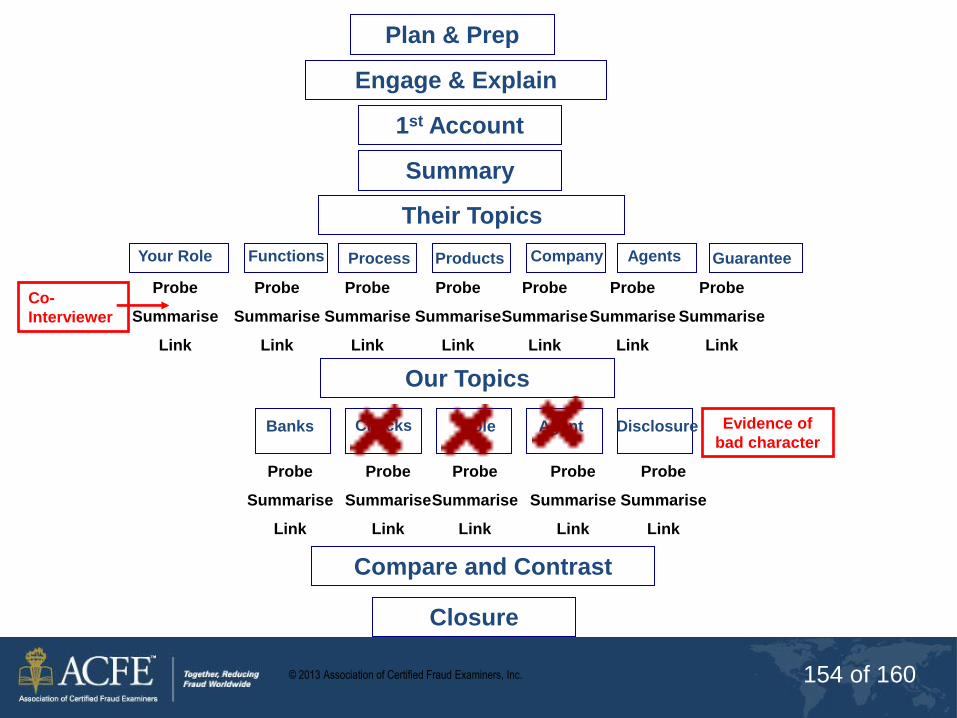

Summary

1st Account

Engage & Explain

Plan & Prep

Probe

Summarise

Link

Their Topics

Your Role Functions Process Products

Company Agents Guarantee

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Probe

Summarise

Link

Role

Our Topics

Banks Checks Agent

Disclosure

Compare and Contrast

Co-

Interviewer

Evidence of

bad character

Closure

© 2013 Association of Certified Fraud Examiners, Inc. 155 of 160

Closure

• Polite – “Thanks for telling me that”

• Positive – “What I’m going to do now is…”

• Prospective – “This is what will happen…”

You may have to interview this person again!

© 2013 Association of Certified Fraud Examiners, Inc. 156 of 160

Evaluate

© 2013 Association of Certified Fraud Examiners, Inc. 157 of 160

ANY QUESTIONS

© 2013 Association of Certified Fraud Examiners, Inc. 158 of 160

Investigative Interviewing

Background and General Principles of

Investigative Interviewing – P.E.A.C.E

Conversation Management (CM)

© 2013 Association of Certified Fraud Examiners, Inc. 159 of 160

Aim:

To provide the delegates with the knowledge, understanding, and

skills to enable them to professionally plan, conduct, and evaluate

investigative interviews with witnesses and suspects

Objectives:

By the end of this course the delegates will be able to:

• Describe how to make investigative decisions and record the

rationale

• Understand and apply the PEACE interview framework

• Demonstrate how to conduct an investigative interview

• Evaluate the conduct and content of an investigative interview of a

witness and a suspect

© 2013 Association of Certified Fraud Examiners, Inc. 160 of 160

Contact

www.forensicinterviewsolutions.c

om

+64 889 4200