Forensic Accounting – the Missing Link in Education and Practice

66

2012/65

Transcript of Forensic Accounting – the Missing Link in Education and Practice

2012/65

33

Nataša Petrović1, Alfred Snider2, Marko Ćirović1, Nemanja Milenković1

1University of Belgrade, Faculty of Organizational Sciences, Serbia2University of Vermont, United States of America

Management Journal for Theory and Practice Management 2012/65

Debate in Education for Sustainable DevelopmentUDC: 378.147:[502/504(497.11) ; 005.6:502.131.1DOI: 10.7595/management.fon.2012.0031

1. Introduction

“It is not the strongest of the species that survives, or the most intelligent, but the one most respon-sive to change.”

Charles Darwin

Industrialization and population growth cause pollution, erosion, habitat fragmentation, and wasteful con-sumption, consequently endangering the integrity of global ecosystems. Ecosystem management programsthat focus on patches or categories, such as forestry management and wildlife management, are not enoughto counter the growing damage inflicted upon our finite natural resources.

Sustainable development was developed to fulfil that need. Sustainable development is a global develop-ment management philosophy that aims to conserve the integrity of the Earth’s ecosystems while support-ing economic growth and social welfare. It was developed by the Brundtland Commission during the WorldCommission on Environment and Development in 1987 (WCED, 1987). Its primary purpose was to reducethe resistance to the conservation of the environment while raising awareness of the importance of theEarth’s natural resources, both for those who need them today and those who will need them tomorrow.

Sustainable Development has become a popular management philosophy in many countries throughout theworld. Its popularity can be partially attributed to reports of global climate change and the declining stabil-ity of global ecosystems. However, its initiation can also be attributed to the efforts of the United Nations (UN),which has encouraged all countries to develop their own national sustainable development strategies. Today,countries on all five continents have developed and are in the process of implementing national sustainabledevelopment strategies.

Further on, sustainability is defined as “development that meets the needs and aspirations of the presentwithout compromising the ability of future generations to meet their own needs” (West, 2008) and, therefore,is generally linked to ongoing economic growth and development (Petrović et al, 2011).

2. The prism of sustainability

The Prism of Sustainability (Fig. 1) is an extension of The Three Pillars of Sustainability Theory with the ad-dition of institutions. Otherwise The Three pillars of Sustainability is a very common depiction of sustainabledevelopment. Represented are the three primary pillars upholding three essential elements of sustainabledevelopment: economic development, social development, and environmental conservation (UN, 2002).

There is no doubt that higher education should contribute significantly to education for sustainable develop-ment. Given the need to develop new approaches to improve students’ environmental awareness, knowledgeand understanding of environmental issues and sustainability topics, the implementation of debating in clas-rooms has been presented in this paper, as an aditional educational tool, at the course of Environmental Man-agement at the Faculty of Organizational Sciences.

Keywords: debate, education, sustainable development, education for sustainable development

Institutions are large organizations that are influential in a community such as Government Organizations,Non-Government Organizations, Universities, and Hospitals. The development of institutions is not enough;achieving enough cooperation and coordination to successfully implement sustainable development re-quires institutional, social, and financial strength. Strong institutions are necessary to develop, implement,enforce, and evaluate policies and regulations. Social vigour is also important, meaning that the society hasthe knowledge, technical, and social capacity to adhere to rules and regulations and to participate in newinitiatives. Support from the lowest levels of society is essential for the success of sustainable development(Ghai & Vivian, 1995).

However, for the lowest levels of society to provide support from the bottom up they must first obtain liveli-hood security (food, water, and basic necessities) to make sustainable choices as well as the financial powerto pay for them. Without these components, sustainable development, as defined by the Brundtland Com-mission, cannot be achieved (WCED, 1987).

Education and public outreach programs, like Agenda 21 (1992) have been developed to increase the localpublic understanding and support of the concept of sustainability.

Figure 1: The Prism of Sustainability

3. Education for sustainable development

The United Nations Decade of Education for Sustainable Development (DESD, 2005-2015), offers an oppor-tunity to rethink the manner in which we approach global environmental and sustainable challenges (DESD,2009). Apart from the regional and national launches, progress has been achieved in both institutional andprogrammatic areas at international, regional and national levels. The Decade of Education for SustainableDevelopment comes at a time when the economic, social, environmental and cultural realms of global soci-ety are faced with daunting challenges. The obligation of higher education is work in a way of mobilizing fur-ther political support in countries where Education for Sustainable Development (ESD) is not yet a priority.Today, more than ever before, the need for a holistic approach to learning and teaching becomes both vitaland urgent. If its potential to contribute to the paradigm shift in thinking, learning and teaching for a sustain-able world is to be realized, Education for Sustainable Development has to move to the political centre-stage.

Sustainable development needs to be added to an already overcrowded curriculum of foundation subjectsthat must teach the basics of reading, writing and arithmetic (UNCED, 1992). At the same time it can beseen as an integrative, cross-curricular theme that can bring together many of the single issues that schoolsare already expected to address. Education for Sustainable Development learning goals include: acting withrespect for others, acting with responsibility locally and globally, critical thinking, understanding complex-ity, the capacity to imagine the future, understanding inter-disciplinary relations, responsible behaviour andthe ability to identify and clarify environmental values (DESD, 2009).

The main thrusts of Education for Sustainable Development, originally identified in Chapter 36 of Agenda 21,have been expanded upon in the Work Programme of the UN Commission of Sustainable Development –CSD, reports of the major UN Conferences of the 1990’s:

34

2012/65Management Journal for Theory and Practice Management

1. Public understanding of the principles behind sustainability. ESD has a major role in furthering the dis-cussion of sustainability itself and the evolution of the concept from a vision to its practical application inculturally appropriate and locally relevant forms.

2. Mainstreaming ESD. This social process needs to be mainstreamed into all sectors including business,agriculture, tourism, natural resource management, local government and mass media, adding value toprogram development and implementation.

3. Lifelong learning for all. The quality life – long education and learning opportunities are required for all peo-ples regardless of their occupation or circumstances.

4. ESD is relevant to all nations. The realization that it is our most highly educated countries that createsome of the greatest threats to a sustainable future for the planet, the reorienting of existing educationprograms in all nations to address the social, environmental, and economic knowledge, skills, perspec-tives, and values inherent in sustainability is also a major thrust of ESD.

5. Specialized Training Programs. The development of specialized training programs to ensure that all sec-tors of society have the skills necessary to perform their world in a sustainable manner (UNCED, 1992).

The nature of Education for Sustainable Development demands new perspectives on matters such as cur-riculum, teaching and learning. Education for Sustainable Development and Education Sustainable Devel-opment tend to focus on connections, feedback loops, relationships and interaction. Yet the dominanteducational structures are based on fragmentation rather than on connections and synergy. Another ob-servation is that the search for a more sustainable world requires the full and democratic involvement of allmembers of society which should also have implications for teaching and learning (Petrović et al, 2011b).

Education for Sustainable Development calls for new kinds of learning that are not so much of a transmis-sive nature (i.e. learning as reproduction) but rather of a transformative nature (i.e. learning as change)(DESD, 2009).

This kind of education implies four descriptors - educational policy and practice which is sustaining, tenable,healthy and durable:• Sustaining: it helps sustain people, communities and ecosystems.• Tenable: it is ethically defensible, working with integrity, justice, respect and inclusiveness.• Healthy: it is itself a viable system, embodying and nurturing healthy relationships and emergence at dif-

ferent system levels.• Durable: it works well enough in practice to be able to keep doing it.

4. Effective teaching environmental topics and sustainable issues

Education for Sustainable Development allows every human being to acquire the knowledge, skills, atti-tudes and values necessary to shape a sustainable future. Education for Sustainable Development meansincluding key sustainable development issues into teaching and learning; for example, climate change, dis-aster risk reduction, biodiversity, poverty reduction, and sustainable consumption. It also requires partici-patory teaching and learning methods that motivate and empower learners to change their behaviours andtake action for sustainable development. Education for Sustainable Development consequently promotescompetencies like critical thinking, imagining future scenarios and making decisions in a collaborative way.Education for Sustainable Development requires far-reaching changes in the way education is often prac-ticed today (UNESCO, 2012).

Strategies to teach environmental and sustainable topics, particularly controversial ones, without coming upagainst affective barriers to learning are:• Teaching the science first: presenting the science objectively, using data and relevant examples; next, dis-

cussing issues related to this topic. By setting the stage deliberately, learners are more likely to be recep-tive to the information.

• Teaching with data: presenting the topic without emotional statements and consequent emotional re-sponses in learners.

• Using active learning techniques: learners learn better when they can learn for themselves. Environmen-tal issues lend themselves to teaching techniques like using local examples, gathering data from the field,using role-playing or debates, or participating in environmental projects.

• Leading by example: the goal is to promote environmentally-favourable behaviour in learners, consider ahands-on project that will challenge them to consider the environmental impacts of their own actions.

35

Management Journal for Theory and Practice Management 2012/65

5. Debate

A debate is an equitably structured communication event about some topic of interest, with opposing ad-vocates alternating before a decision-making body (Snider & Schnurer, 2006).

This definition implies a number of principles for a debate. A debate should be equitably designed. All des-ignated “sides” should be given an equal opportunity to present their views. A debate should be structured,with established communication periods and patterns with a beginning and an end. This structure allows forpreparation and strategy.

A debate is a communication event where the mode of operation is oral or written communication (a text de-bate) and serves as performance as well as a method of transmitting ideas and arguments. Every debatehas a topic, allowing the debate process to be more directed than a normal conversation. The topic itselfshould be of some importance and interest to the participants and any audience that may observe the de-bate. A debate is composed of two or more sides of an issue where the advocacy positions are identified inadvance.

For example, a debate might be held on the issue of creating a national death penalty for certain crimes, oneside is in favour of death penalty (thus they may be called “pro,” “affirmative,” “proposition,” or “government”;in this text we favour affirmative) and one side will be against death penalty (thus they may be called “con,”“negative,” or “opposition”; we favour negative). This sense of “opposing sides” is critical to the probinganalysis of the topic to be debated because debaters will bring the strongest arguments to back their sideand be prepared to challenge the ideas of the other side. Presentations in a debate should alternate betweenthe sides, creating a pulse of critical communication in opposition to previous and subsequent pulses.

During the debate the advocates will be asking other participants and observers to agree with their point ofview and, in the end, call for a “decision” by those present, either publicly or privately (Snider & Schnurer,2006).

Participation in academic debating creates numerous benefits for the students:• Data analysis is an essential debating tool. Debaters must learn how to find the relevant information on the

topic when they are researching possible motions for a tournament analysis and save or remember theirresults. After debating for some time, debaters collect a lot of information, but they will always encounternew topics, where they will have to quickly utilize the data they know in a new problem.

• Presentation of knowledge is required from debaters in a limited time frame. Debaters learn how to pres-ent vast amounts of knowledge briefly, effectively and to the point.

• Critical thinking is forced onto debaters, and debaters quickly adopt it. Sides are randomly assigned in adebate, therefore debaters must know how to argue, analyze and assess opposing sides of any argument.

• Knowledge of the world problems is necessary in the international debating scene, as the topics must bedrawn from a pool of issues which are equally important to all the countries that are participating.

• Finding the right information is important because facts count in debate. Most global debates have com-peting schools of thought, often with competing information. Debaters need to know how to weigh au-thorities, how to compare sources and spot when information is biased.

• Intercultural communication is developed and trained in debate, as judges come from different culturalbackgrounds, as well as the opposition teams. That means debaters train to be understood, as well as tounderstand.

• Persuasion is a peripheral skill for debaters. In theory, debates should be judged by completely objectivejudges. As this cannot be the case, advance debating classes cover persuasion methods as a manner ofgaining that last bit of competitive edge (Snider, 2011).

6. Introduction of the concepts of academic educational debating in environmental management course – case study

On the other hand, a number of courses in higher environmental education and a number of initiatives to in-tegrate environmental issues into university curricula have been launched in the past decade worldwide.However, to satisfy the specific needs of this kind of education implementing, innovative methods of deliv-ering such knowledge for sustainability are needed (Petrović et al, 2011b).

36

2012/65Management Journal for Theory and Practice Management

Higher environmental education has to be learner-cantered, providing learners with opportunities to constructtheir own understandings through hands-on, minds on investigations (Petrović & Milićević, 2006; Petrović

& Milićević, 2007; Kostova, 1998). Having this in mind, we selected Environmental management course, be-cause it is based on a wide range of scientific and practical knowledge of environmental science and sus-tainable development. Thus this course represents a good benchmark for an adequate improvement ofstudents’ environmental awareness and knowledge about sustainability.

In the spring semester of 2012 school year, just over 200 students enrolled the Environmental Managementcourse at their third year of study at University of Belgrade, Faculty of Organizational Sciences. The courseclasses consisted of two hours of lectures and two hours of exercise each week during a 13-week semes-ter. The course has sections on ecology, environmental issues and protection, conservation of natural re-sources, environmental management and sustainable development. The course program is based on astrong methodology, requiring participants to turn their environmental and management knowledge andunderstanding into appropriate environmental actions.

The introduction of educational innovations in the classroom develops the students’ independence andgives them the capacity to be self-confident as well as self-reliable in striving to fulfil their goals and aspira-tions (Kostova & Atasoy, 2008). Having that in mind, we wanted to work on students’ analytical skills throughtheir participation in contemporary environmental debates.

A framework for the introduction of the concepts of academic educational debating in Environmental Man-agement course development consisted of:• Introduction and overview of the course content. A review of major environmental topics and sustainable

issues, and the role of various actors in addressing environmental problems.• About environmental debates. Identifying major themes in environmental discourse. E.g. Anthropocen-

trism vs. Biocentrism, Sovereignty vs. Global Commons, Resource use/Development vs. Conservation.• Motion 1 - The Climate Change Debate.• Motion 2 - Alternative Energy Sources. • Motion 3 - Nuclear energy• Motion 4 - Animal rights• Motion 5 - Environmental protection Vs. Economic growth • Motion 6 - Energy consumption limits• Motion 7 – Zero growth• Motion 8 – Vegetarianism

Students enrolled at the course were introduced to and familiarized with the concepts of academic educa-tional debating. Students, encouraged to voluntarily participate in debating, worked on their skills in: or-ganization, research, delivery, refutation, and argumentation. These students were trained to participate inclassroom practice environmental debates.

Assignment values were as follows: participation, practice speech (5 extra credits), practice debates (10extra credits), winning tournament (20 extra credits).

Each practice debate simulated the British parliamentary format of debating. This format is one of the mostcommonly and widely used debate formats currently. Students were divided into 4 teams, each team con-sisting of 2 members hence all of the practice debates had 8 students actively participating. When the de-bate was done, group discussion and an elaborate feedback from the educator followed.

After the students successfully completed the course and were graded, the students who participated in thedebates took part in a short preliminary research. The research was conducted at the University of Belgrade,Faculty of Organizational Sciences. The number of students that participated in it was 51.When these students were asked whether or not participating in the debates helped them evaluate specificenvironmental problems - 27 of them strongly agreed and 21 of them partially agreed that it helped. Thatgives us the total of 94.12% of analysed students that strongly or partially believe that the debate helped themwhen approaching specific environmental problems, while only 5.88% partially disagreed with that statement.

When the same group was asked to express their attitude towards the statement “the debate helped me crit-ically analyse all sides of the given environmental problem”, 90.19% strongly or partially agreed, while 9.2%partially disagreed with it.

37

Management Journal for Theory and Practice Management 2012/65

38

2012/65Management Journal for Theory and Practice Management

Conslusion

The introduction of debate in higher education helps students articulate and appreciate alternative arguments about crit-ical environmental issues even if they disagree with some of them. Understanding and articulating opposing points of vieware a hallmark of a strong advocacy and good literature, because respectful, informed, responsible discourse is neces-sary to address difficult environmental topics and sustainable issues. Further, critical examination of major environmentalproblems reveals numberless competing interests, priorities and perspectives.

Likewise, by using debate, Environmental Management course utilized these additional teaching methods:1. Lectures about debating and debate theory. In this way, students are introduced with information about debate con-

cepts, practices, and vocabulary.2. Class discussions. Class discussions provided environmental topics for debating, argumentative concepts, and on var-

ious debate methods and practices.3. Practice speeches. Students had a task to give short, unprepared speeches about ideas in order to gain training in de-

livery, organization, and argumentative concepts.4. Practice debates. Students were engaged in debates against each other in teams. These debates were supplemented

by research done by students as well as by additional material supplied by the educator. 5. Debate tournaments. Students were engaged in debates against each other. They would simulate all the elements that

are present at the university debate tournaments held in British parliamentary format. That would include motion analy-sis, data preparing, organizing, structuring and labelling their speeches and speech delivery.

6. Research. Students were engaged in primary research on given environmental topic which was the motion and thetheme of the debate.

The preliminary research given in this paper and high percentages of students satisfied with debates at the course of En-vironmental Management have encouraged us to proceed with this method and this research, and to involve other envi-ronmental courses at the faculty.

Based on this, we would highly recomend others to explore the use of debating in clasrooms as a supplement to traditionallearning. Our data suggest that students would use debating as a good tool not only for a broader engagement in theproces of learning but also as a way to develop a way of critical thinking and engaging in environmental transparency.

LITERATURE

[1] Agenda 21 (1992). http://www.un.org/esa/dsd/agenda21/[2] Ghai, D., & Vivian, J. (1995). “Grassroots Environmental Action: People’s Participation in Sustainable De-

velopment.” Rutledge, London.[3] Kostova, Z. (1998). How to Learn Successfully. Sofia: Pedagog 6.[4] Kostova, Z., & Atasoy, E. (2008). Methods of successful learning in environmental education. Journal of

Theory and Practice in Education, 4(1), 49-78.[5] Petrović N., Jeremić, V., & Išljamović, S. (2011a). Going green: cloud computing and sustainability. 9th

International conference: Strategic Management and its support by information systems. Celadna, Os-trava, Czech Republic.

[6] Petrović, N., Drakulić, M., Išljamović, S., Jeremić, V., & Drakulić, R. (2011b). Novi okviri ekološkog obra-zovanja u visokoškolskom obrazovanju. Management, 16(60), 11-17.

[7] Petrović, N., & Milićević, M. (2006). Education For Sustainable Development, Collection of Works, 9th

”Toulon – Verona” Conference, Paisley, Scotland.[8] Petrović, N., & Milićević, M. (2007). Higher good Environmental Education, Collection of Works, 10th

”Toulon – Verona” Conference, Thessaloniki, Greece.[9] Snider, A.C., & Schnurer, M. (2006). Many sides: debate across the curriculum, IDEBATE Press, New

York, USA.[10] Snider, A.C. (2011). Debate: Important for Everyone, University of Vermont, Vermont, USA.[11] UN (2002). Report of the World Summit on Sustainable Development: Johannesburg, South Africa, 26

August-4 September 2002. A/CONF.199/20 and A/CONF. 199/20/Corr.1.[12] UNCED (1992). Agenda 21: Programme of Action for Sustainable Development, Rio Declaration on En-

vironment and Development. N.Y.: United Nations.

[13] UNESCO (2012). Education for Sustainable Development. .[14] United Nations Decade of Education for Sustainable Development (2009). Review of Contexts and Struc-

tures for Education for Sustainable Development, Learning for a sustainable world.[15) WCED (1987). “Our Common Future” The Bruntdland Report. Oxford University Press.[16] West, J. E. (2008). The green grid’s datacenter metrics – Experience from the field. HPCwire. .

Receieved: August 2012.Accepted: October 2012.

Nataša PetrovićUniversity of Belgrade, Faculty of Organizational Sciences

petrovicn@fon,bg.ac.rs

Nataša Petrović graduated from the Faculty of Organizational Sciencesin 1991, got her mastersdegree in 1999, and a Ph. D. in 2002. She currently works as an associate professor at the

University of Belgrade - Faculty of Organizational Sciences. The area of her scientific researchincludes: environmental management, sustainable development, environmental education, eco

marketing, design for environment, public participation in environmental protection.

Alfred SniderUniversity of Vermont, United States of America

Alfred Snider is the Edwin W. Lawrence Professor of Forensics at the University of Vermont. Heteaches courses in Speech Communication, most often Argumentation, Persuasion, Debate,

Campaign Rhetoric, Issues in Public Address, and related subjects. He is also the Director of theLawrence Debate Union, an endowed co-curricular program that trains students to debate and

then sponsors their intercollegiate debate competition globally. He received a “LifetimeAchievement” award from the Cross Examination Debate Association in 2001, the “Humanitarian

Award” from the National Forensic League in 2008 as well as a number of other honors.

Marko ĆirovićUniversity of Belgrade, Faculty of OrganizationalSciences

Marko Ćirović works as a teaching associate at the Faculty of Organizational Sciences, Universityof Belgrade. He graduated from this Faculty in management in 2010, and got his masters degree in

2012. He is currently enrolled in doctorial studies at the Faculty of Organizational Sciences. Hisarea of interest includes: environmental management, eco-marketing, environmental education and

debate as a method of education.

Nemanja MilenkovićUniversity of Belgrade,Faculty of Organizational Sciences

Nemanja Milenkovic graduated from the Faculty of Organizational Sciences in 2010. He receivedhis M.Sc. degree in 2012 in the scientific field of computational statistics. His area of interest

includes probability theory, statistics and linear-statistical models. He is a member of The StatisticalSociety of Serbia.

39

Management Journal for Theory and Practice Management 2012/65

About the Author

41

Miloš Mitrić¹, Aleksandra Stanković², Andrijana Lakićević³ ¹University of Kragujevac, Faculty of Hotel Management and Tourism²University of Kragujevac, Faculty of Hotel Management and Tourism

³University of Belgrade, Faculty of Organizational Sciences

Forensic Accounting – the Missing Link in Education and Practice UDC: 343.53:657.632 ; 657.632DOI: 10.7595/management.fon.2012.0032

1. Introduction

Requirements for accounting information, both within and without the company, have led to a gradual divi-sion of accounting into two subsystems, namely: financial accounting and management accounting. Withregard to the accounting division, both subsystems can be said to represent the socio-professional activities.

Forensic accounting, as a set of socio-professional activities, is aimed at protecting companies, and thus rep-resents the implementation of legal, economic, social and political functions. In this sense, forensic ac-counting is a discipline that combines accounting, auditing and law. The law reflects the government’s abilityto establish, manage and develop social, economic and political order. Forensic accounting, as a separatebranch of accounting, deals with the control of legal and professional recordkeeping [12].

The present paper shall discuss important aspects of forensic accounting, in both theory and practice, andresearch opportunities and trends towards a wider inclusion of this discipline into academic and practicalcourses.

Management Journal for Theory and Practice Management 2012/65

Financial scams and fraud appear to be a global problem. Although research related to financial fraud and em-bezzlement varies slightly from region to region, fraud schemes and perpetrator characteristics are pretty sim-ilar. In Serbia in particular, forensic accounting is an underdeveloped area in education and practice, and isthus often replaced by and considered to be an audit, even in academic circles, whereas forensic accountantsare viewed as auditors.The correlation between auditing and forensic accounting is a dynamic process that changes over time due topolitical, social and cultural events, and the auditors themselves are expected to have, at least, adequate knowl-edge and skills to recognize a financial fraud. However, detailed disclosure of financial fraud and embezzlementis the matter forensic accountants are dealing with. These experts have the skill sets in many areas and are ableto apply their skills and abilities in one area, while working in another. Forensic scientists need to be familiar withnot only financial accounting, but also with tax and business law, criminology, psychology, etc.The aim of this paper is to show the incidence of financial fraud and embezzlement, indicating the conse-quences they bear and to explore the extent to which forensic accounting is represented in academic institu-tions and practice in the Republic of Serbia. It also explains the general concepts of services in the field offorensic accounting. As a research method in this paper the content analysis method is applied. With respect to the consequences of financial fraud and embezzlement it carries, and lessons learned fromrecent financial scandals in the world and in Serbia in particular, we can conclude that the development offorensic accounting in education and practice is of utmost importance. Although this process is neither easynor cheap, the benefits it provides are invaluable.The present research topic should be given more attention, given a large number of fraudulent acts in the finan-cial statements that characterized the operations of a substantial number of Serbian companies. A higher educa-tion is being proposed in the area of forensic accounting, both at the academic level and in the accounting practice.

Keywords: financial fraud, forensic accounting, auditing, forensic accountants

2. Definition of Forensic Accounting

The area that deals with the study of financial fraud and malfeasance is called forensic accounting. Certainforms of forensic accounting date back to 1817 and refer to court decisions, i.e. rulings on declaration ofbankruptcy. Then the Scottish accountants pooled their knowledge and expertise in addressing this specificissue in the form of opinions in support of arbitration proceedings in 1820’s, followed by articles examiningexpert testimonies and evidence on arbitration that began to appear in the late 1800’s and early 1900’s.Maurice E. Peloubet, a partner in the accounting firm in New York, is probably the first to publish the phrase“forensic accounting” in his article in 1946 [3].

In the accounting literature itself, there is no single definition of forensic accounting. Out of the vast array ofdefinitions that can be found in the literature, the most acceptable one, according to ACFE (Association ofCertified Fraud Examiners), is the one defining forensic accounting as a set of skills to use in potential oractual civil or criminal cases, including generally accepted accounting and auditing ones; determining lossof profits, revenue, property or damage, assessment of internal controls, fraud and everything else that leadsto the applying of accounting knowledge to the legal system.

The concept of forensic accounting is a thorough and complex setting in which an accountant, in his pro-fessional independent judgement, forms a presentation at such a high level of reliability, that it can qualifyas evidence in legal proceedings conducted [15].

In order to complete the required tasks, it is essential that forensic accountants demonstrate substantialknowledge of accounting and auditing, oral and written communication skills, strong detail-spotting skills anda good use of information and communication technology [6]. Forensic accounting, sometimes referred toas an investigative accounting, is an area that, in addition to accounting knowledge, requires a good use ofinformation technology [16]. The complex structure of the knowledge forensic accountants are equippedwith, in addition to the above knowledge, mostly relies on laws and regulations [12]. In his work, one mustdemonstrate sufficiently broad business and organizational know-how and experience, must be competentand morally reliable (no complaints), so that his professional opinion (judgement) on the operations and re-lated fraud or other illegal acts is convincing enough [7]. Forensic accountants are expected to demon-strate a high degree of independence and objectivity, which is in accordance with the Code of Ethics forProfessional Accountants. A forensic accountant shall be considered independent if he is intellectually hon-est and ready for impartial decisions. Independence is usually considered to be a prerequisite of objectiv-ity. The key feature that a forensic accountant should possess is objectivity, which is difficult to achieve dueto the many factors which might affect the assessment and expectations [5]. A forensic accountant, then, isthe creator of independent and unbiased, objective information on the economic truth.

The task of a forensic accountant is to analyze, interpret and present interconnected business and financialpositions, so that they can be properly understood and appropriately supported. In the course of their work,a forensic accountant often participates in the following activities:

• Research and analysis of evidence of fraud committed,• Developing applications using information and communication technologies used in the analysis and

presentation,• Presentation of research results, and• Participation in legal proceedings (usually as a witness in court, as an expert in forensic accounting) [10].

It is estimated that in the years to come, in developed market economies, a forensic accountant is likely tobe one of the 20 most wanted professions.

3. Forensic Accounting and Related Services

Forensic Accounting is the application of accounting principles, theories and disciplines to facts or hy-potheses in a legal dispute and encompasses every branch of accounting knowledge. Forensic accountingis comprised of two major components: (1) litigation support services in proceedings that recognize therole of forensic scientists as experts or consultants, and (2) investigative services that may or may not leadto testimony in court. Forensic Accounting may involve application of special skills in accounting, auditing,finance, quantitative methods, certain parts of the law and research, and investigative skills to collect, ana-

42

2012/65Management Journal for Theory and Practice Management

lyze and evaluate evidence, interpret them, and communicate findings within reports. Forensic Accountingis either based on certification services or on advisory services [8].

Fraud Examination or Forensic Investigation of Financial Frauds is a methodology for exposing financialfrauds and involves obtaining evidence, interviewing people, writing reports and testimonies. Certified FraudExaminer is a license added by the ACFE Association (Association of Certified Fraud Examiners based in theUnited States) [2]. Such an investigation is conducted on the basis of fraud indicators, such as cash short-age or other evidence being investigated, in order to determine the extent of loss, i.e. damage and the iden-tity of the perpetrator.

Fraud Deterrence or Financial Fraud Deterrence is related to creating an environment where people are dis-couraged to commit fraud, although it can be done. Deterrence from financial fraud is usually achievedthrough a number of efforts related to internal controls and ethics programs that create integrity and stimu-late employees to report potential abuse. Such actions increase the likelihood that the fraudulent act per-ceived will be detected and reported accordingly. Financial fraud deterrence can be achieved using softwaremonitoring tools, triggered once the perception of detection is present and potential perpetrators becomeaware that they will certainly be punished if caught.

Financial Fraud Detection refers to the process of detecting the presence or existence of fraud. Financialfraud detection can be accomplished by means of well-designed internal control, supervision and monitor-ing systems, as well as by actively seeking evidence of potential fraud.

Fraud Remediation or Financial Fraud Remediation refers to rehabilitation, i.e. loss recovery through insurance,legal system or other means, modifications within operational processes and procedures, including internalcontrol system modifications in order to reduce or prevent the recurrence of similar frauds in the future.

4. Interrelationship between Audit, Financial Fraud and Forensic Accounting

Effective stress management delivers direct obligations and responsibilities, which in turn also add certaincost [9]. Stress is a psychophysical condition a man falls into in difficult circumstances and situations [11].Auditing companies and their employees are required to a much greater extent to invest time, financial re-sources and expertise in creating quality working environments that are seen as potential sources of stress.An auditor is responsible for forming and expressing his opinion on financial statements whereas the com-petent Audit Authority is in charge of their preparation and presentation (auditing does not diminish the re-sponsibility of the Audit Authority).

Numerous financial frauds occurred in the past, as well as at the beginning of this century, had disruptedthe trust of a large number of users of the financial information contained in financial statements. Financialreporting and accounting and auditing professions are often blamed for the occurrence of frauds and lossof confidence in the reliability of financial information by a number of users and decision-makers. Therehave always been some accounting frauds happening followed by financial collapses, to a much greater ex-tent recently, and with more serious consequences to all of us.

Generally speaking, a fraud can be divided into four basic elements:• Misrepresentation of Material Fact. (Materiality in the context of legal standards that vary from jurisdiction

to jurisdiction),• Awareness that interpretation is erroneous or a negligent disregard of the truth,• Confidence - a person who receives an interpretation is reasonable and justified in relying on it.• Damage - financial damage caused by all of the above mentioned [13].

There have been numerous scientific debates arguing that the two factors should be taken into accountwhen analyzing psychology and personality of the fraud perpetrator:• Biological characteristics of the individual, which vary widely and influence behavior, including social be-

havior and• Social characteristics of the individual, which are derived from the way the individual behaves, i.e. inter-

acts with other people.

43

Management Journal for Theory and Practice Management 2012/65

Two basic types of financial fraud perpetrators have been identified on the basis of these psychology studies:• Calculated criminals - who want to compete and prove themselves and• Criminals depending on the situation - those who are willing to do anything to save themselves, their fam-

ily or their company from disaster. [13]

Fraud detection (Figure 1) is an interactive process that includes:• Corporate control system establishment,• Investigation and problem solving,• Process testing and transaction, • Transaction control level.

Figure 1: Fraud Detection Process [4]

Interrelationship between audit, fraud and forensic accounting is a dynamic process that changes over timedue to political, social and cultural events. The work of external auditors is greatly influenced by the Sar-banes-Oxley Act, according to which an auditor is expected to demonstrate, at least, an adequate knowl-edge and skills in the area of forensic accounting and fraud in order to identify financial frauds [4].

However, auditors are not obliged to plan and perform audits to detect errors that are not material to the fi-nancial statements, regardless of whether the error is unintentional or related to financial fraud or malfea-sance. However, if the auditor encounters evidence of financial fraud and embezzlement during the audit,he shall notify the competent body.

Organizations tend to rely too heavily on external audit as a quality control mechanism to detect financialfraud and embezzlement. Societies, subjects to external audits, are the most common victims of financialfrauds. External audits are extremely important and can have a strong deterrent effect on the prevention offinancial fraud, but are not solely relied upon to detect fraud.

Detecting financial fraud and embezzlement falls within the scope of activities dealt with by forensic ac-countants who demonstrate skill sets in different domains (financial accounting, tax and business law, crim-inology, psychology, etc.) and who are thus able to apply their skills and abilities in one area while workingin another.

5. Facts and Statistics on Financial Fraud and Embezzlement

Financial fraud and embezzlement, although different in terms of patterns they follow, have many featuresin common. Monitoring and analyzing the resulting abuse and information associated with them have amajor role in discovering the new ones. Therefore, it is useful to know the following facts.

Employees holding high-ranking positions generally cause the greatest damage to their organizations. Stud-ies show that the fraud committed by owners or executives causes three times more damage than the fraudcommitted by ordinary managers, and more than nine times greater damage compared to the frauds com-mitted by general staff. Frauds committed by managers or owners, take more time to be discovered.

44

2012/65Management Journal for Theory and Practice Management

More than 77% of financial frauds were committed by individuals in one of six departments: accounting, op-erations, sales, executive management, customer service and procurement departments. More than 87% offraud perpetrators had never been charged or convicted of any fraudulent practices [14].

Fraud perpetrators often display warning signs that they are likely to engage in illegal activities. The mostcommon signs imply living beyond their means (36% of cases) and experiencing financial difficulties (27%of cases) [14].

Small organizations are more often victims of financial fraud. In contrast to larger organizations, small or-ganizations often lack control activities that combat and prevent financial fraud, making the scope for fi-nancial fraud and embezzlement larger.

It has been observed that most of the frauds are committed in banking and financial services, governmentand public administration and in the manufacturing sector. Also, according to research results, it may be con-cluded that nearly half of organizations, the fraud victims, never recover from losses caused by fraud.

ACFE published research findings covering 1388 fraud cases. The analysis of fraud types and changes inthe median loss (Figure 2) indicates increased manifolds over the period from 2008 to 2012 in the medianfraud loss, whereas financial statement frauds are the most common type of fraud in the U.S., entailing there-fore the greatest average loss at the organizational level.

Figure 2: Occupational Frauds by Categoryin U.S. and Median Loss [14]

the analysis of changes in the losses resulting from fraudulent activities by number of employees in theUnited States (Figure 3) demonstrates the lowest average loss in organizations with 1000 to 9999 employ-ees and also the lowest average loss incurred within organizations in 2012 compared to 2010 and 2008.

45

Management Journal for Theory and Practice Management 2012/65

Figure 3: Size of Victim Organization Loss arisenfrom fraud by number of employees in U.S. [14]

ACFE research results show that tips are among the most common forms of fraud detection in the UnitedStates (Figure 4), followed by management review (management control), internal audit and random checks.

Figure 4: Methods of detecting fraud in U.S. [14]

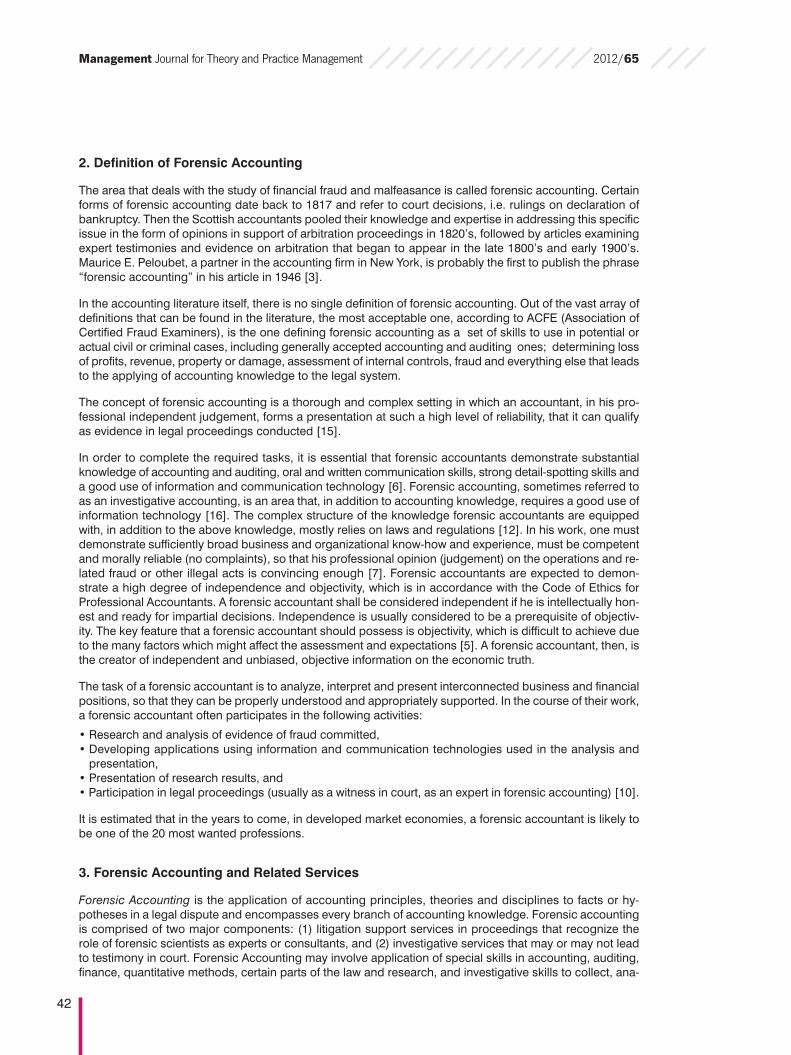

Research findings also show that it usually takes 18 months on average before financial frauds get detected(Figure 5). Also, it is noteworthy that most fraud reports come from employees operating within the victimorganizations.

46

2012/65Management Journal for Theory and Practice Management

Figure 5: Duration of fraud on the basis of fraudtype in the U.S. [14]

Financial frauds and scams make a global problem. Although research related to financial fraud and em-bezzlement varies slightly from region to region, most of the trends in fraud schemes, perpetrator charac-teristics, and controls to combat fraud are similar regardless of where the actual frauds occur.

Studies show that a typical organization loses 5% of its annual revenue due to fraud and financial irregular-ities. If this percentage is applied to the gross world product in 2011, we reach the potential global loss ex-ceeding $ 3.5 billion [1]. Nearly one-fifth of the financial frauds committed involve losses exceeding $ 1million.

Astonishing data are obtained from a survey conducted by the ACFE, indicating losses amounting to around$ 994 billion in U.S. companies during 2008 due to fraud and abuse. The perpetrators were primarily em-ployed in the accounting sector, 29% and 18% were related directly to the management [13].

The highest-profile financial frauds in recent history occurred in corporations with capital weighing billionsof dollars, such as “Tyco International”, “WorldCom” and “Enron“. These financial frauds caused massivewidespread damage, and their leading executives were convicted and sentenced to long prison terms. Thereare many privatizations in Serbia, conducted in the past decade brought into question.

6. Study and Application of Forensic Accounting Concept

In the United States business schools, forensic accounting exists as a subject at the undergraduate level,and is even mandatory as required in most of the cases. There are also a great number of academic insti-tutions and interest organizations that provide education in the domain of forensic accounting and, faced withthe questions regarding nature, scope and format of the curriculum to be introduced in undergraduate busi-ness education, they invest huge resources. Training in these areas is funded by the government, compa-nies, audit firms and nonprofit organizations.

47

Management Journal for Theory and Practice Management 2012/65

In Croatia, at the University of Split, there is a University Center for Forensic Sciences within which students,among the rest, can attend lectures at the Financial and Accounting Forensics Department which offerssubjects called “Forensic Accounting I” and “Forensic Accounting II.”

In contrast, forensic accounting is new and insufficiently known in Serbia as a term and is still associatedwith audits exclusively. There are a great number of professional bodies dealing with education in this area1,whereas this subject is not available in undergraduate programs. Academic achievements in this field arenegligible.

Such shortcomings in education and practice leave ample room and opportunity for potential perpetratorsof financial fraud and embezzlement. In this context, the Faculty of Organizational Sciences is quite recog-nizable owing to its Cyber Forensics and ‘Forensic Accounting’ available as a study subject within this Mas-ter’s Degree program.

7. Tips for Combating Financial Fraud

It cannot go unnoticed that many people are trying to understand how it is possible that there are so manyfrauds, who is responsible for them, and who is in charge of their detection and investigation; whether it isa question of the system, attitude, aggressive internal policies, stricter regulations or all of the above; whichis the best system for their prevention, etc. There appear to be more questions than answers. Althoughforensic accounting investigation has gained its significance in large organizations and in public in general,there is still a lot to be learned about this relatively new discipline [13].

It is important not to rely on external audit as the only way of detecting fraud. Although it may play an im-portant preventive role in potential fraud detection, its options are limited.

Employee education programs are the foundation of preventing and detecting financial frauds. Employeesare an organization’s most effective method for financial fraud detection. Staff must be trained in these mat-ters as to what constitutes fraud, in what way it concerns the entire society and how to report any suspiciousactivity. What available data show is that not only were most of the frauds discovered by the council, but alsothe losses organizations with training programs for managers and workers for combating financial frauds suf-fer due to misuse and fraud are considerably lower. [1]

Unannounced audits are an effective, but an underutilized tool in the fight against fraud. Although unan-nounced audits may be useful in financial fraud and malfeasance detection, their most important benefitlies in preventing fraud by creating the perception of fraud detection. Generally speaking, fraud perpetratorswill make an abuse only if they believe that they will not be caught. The threat of unannounced audits in-creases the perception of fraud detection having thus a strong deterrent effect on potential fraudsters.

Improvement of the internal control system is useful, but internal controls alone are not sufficient to fully pre-vent financial fraud and embezzlement. While it is important for organizations to have the strategic plan tocombat fraud through an internal control system, it will not always detect financial fraud in the making.

48

2012/65Management Journal for Theory and Practice Management

1The exception is the Serbian Association of Accountants and Auditors, providing professional education and publishing a variety of publica-tions in this field.

REFERENCES

[1] ACFE Report to the Nation on Occupational Fraud & Abuse, Association of Certified Fraud Examiners.(2012). pp. 10-39.

[2] Adapted from Association of Certified Fraud Examiners, Fraud Examiners Manual, Austin: Associationof Certified Fraud Examiners. (2005).

[3] Crumbley L. (2001). Forensic Accounting: Older Than You Think, Journal of Forensic Accounting. Vol.2.pp. 181-202.

[4] Golden T.W., Skalak S.L., Clayton M.I. (2006). A Guide to forensic accounting investigation, John&WileySons, Inc.

[5] Kleinman G., Anandarajan A. (2011). Inattentional blindness and its relevance to teaching forensicaccounting and auditing, Jounal of Accounting Education. 29. pp. 37–49. doi:

[6] Krstić J. (2009). Uloga forenzičkih računovođa u otkrivanju prevara u finansijskim izveštajima, Factauniversitatis - series: Economics and Organization. 6(3). p. 295-302.

[7] Kolar I. (2010). Je li forenzičko računovodstvo pravi put za otklanjanje privrednog kriminala, ActaEconomica, 12, p. 81-103.

[8] Larry D., HeitgerL., Smith S.. (2005). Forensic and Investigative Accounting, Chicago: CCH Incorporated.[9] Mellor N., Mackay C., Packham C., Jones R., Palferman D., Webster S., Kelly P. (2011). “‘Management

Standards’ and work-related stress in Great Britain: Progress on their implementation“. Safety Science49 (7). pp. 1040–1046. doi:

[10] Novajlija S.. (2011). Forenzičko računovodstvo i uticaj kreativnog računovodstva na finansijske izveštaje.Druga međunarodna naučna konferencija ‚‚Ekonomija integracija”. Tuzla. pp.567 – 585.

[11] Ong L., Linden W., Young S. (2004). „Stress management, What is it? “. Journal of PsychosomaticResearch 56 (1). pp. 133–137. doi:

[12] Renzhou D. (2011). Research on Legal Procedural Functions of Forensic Accounting, Energy Procedia5. pp. 2147–2151. doi:

[13] Skalak S.L., Golden T. W., Clayton M. I., Pill A. S.. (2011). A Guide to Forensic Accounting Investigation,John Wiley & Sons, Inc, Hoboken. New Jersey.

[14] Association of Certified Fraud Examiners. (2012). Retrieved from [15] Zysman B.C.A, Forensinc Accounting. (2012). Retrieved from [16] What is Forensic Accounting? (2012). Retrieved from

Receieved: September 2012. Accepted: October 2012.

49

Management Journal for Theory and Practice Management 2012/65

Conslusion

Fraud is a possible future for any company in the world, regardless of size, location or industry.Forensic accounting and professional forensic accountants close the gap between accountants, auditors, inspectors andother government and court officials, which lack the specific knowledge and skills to prevent, detect and prove criminaland other illegal activities in establishment, operation and closure of companies.

On the global level, forensic accounting is one of the highest paid and most sought after business services, and the fieldfull of challenges when it comes to science. In Serbia, forensic accounting is quite rare. Given the fact that we want to catchup with the world, and that financial fraud and embezzlement are not something we are not familiar with, we would haveto work on the development of forensic accounting, both in education and in practice.

In Serbia, forensic accounting is often replaced by and considered to be an audit, even in academic circles, whereasforensic accountants are viewed as auditors, even though the two disciplines have quite different motives.

With regard to the consequences of financial fraud and embezzlement, based on the lessons learnt from recent financialscandals, throughout the world and in Serbia as well, we can conclude that it is extremely important to work on the de-velopment of forensic accounting, both in education and in practice. Even though this process is neither simple nor cheap,the benefits it provides are invaluable, for both business entities and the society as a whole.

50

2012/65Management Journal for Theory and Practice Management

Miloš MitrićUniversity of Kragujevac, Faculty of Hotel Management and Touris

E-mail: [email protected]

Mr Mitrić is Audit Director of LeitnerLeitner in Serbia and a team leader for audit, forensic servicesand advisory engagements. His expertise includes audit, due diligence, forensic accounting, fraud

examinations, valuations and various consultancy services. Before joining LeitnerLeitner, hepracticed audit at Deloitte & Touche in the USA and BDO in Serbia. Mr. Mitrić is a holder of CPA

qualification and a Member of the American Institute of Certified Public Accountants, and is aCertified Auditor in Serbia. He is also a Certified Fraud Examiner (CFE) and Credited Forensic

Accountant (Cr. FA). Mr. Mitric has an MBA from Villanova University, USA, and is a PhD candidateat Belgrade University Faculty of Economics.

Aleksandra StankovićUniversity of Kragujevac, Faculty of Hotel Management and Touris

Aleksandra Stankovic works as a Teaching Assistant at the Faculty of Hotel Management and Tourism in Vrnjačka Banja, University of Kragujevac. She completed her Bachelor Studies in

Accounting and Corporate Finance as well as her Master studies at the Faculty of Economics in Kragujevac. The fields of her scientific and professional interests are related

to Accounting and Finance.

Andrijana LakićevićUnivesity of Belgrade,Faculty of Organizational Sciences

Andrijana Lakićević was born in Belgrade. She graduated from the Faculty of Economics inBelgrade. Holds an MBA degree (Master of Business Administration) from the Texas A&M

University-Commerce in cooperation with the Faculty of Economics in Belgrade. Has several yearsof work experience in the industry sector. Areas of interest: Finance, Accounting, Banking,

Management and Environmental protection. Currently working at the Faculty of OrganizationalSciences in Belgrade, Department of Financial Management.

About the Author

51

Zohar LasloSCE –Shamoon College of Engineering

The Adjustment of Locus of Influence and Organizational Forms Towards Better ProjectPortfolio’s Performance UDC: 005.72:005.74 ; 005.83DOI: 10.7595/management.fon.2012.0030

XIII International Symposium SymOrg 2012, 05 - 09 June 2012, Zlatibor, Serbia

1. Introduction

The matrix structure has become the popular organizational framework for managing the development ofnew products and services (Perham, 1970) and the primary organizational means for maintaining an efficientflow of resources in project portfolios. This structure operates through a two-dimensional system of control:a projectline chain of command and a functional chain of command (Lawrence et al., 1982). Within the ma-trix, each chain of command keeps its traditional role and takes responsibility for goals as in the two earlierhierarchical forms of organization (Lawrence &Lorsch, 1967). Project managers retain responsibility for de-veloping products, while functional managers concentrate on the organization’s capability to make use ofup-to-date technical knowledge. In order to complete a job, functional managers must address different ob-jectives and priorities than project managers. The different objectives are based on functional managers’focus on long-term effectiveness, while project managers concentrate on more immediate accomplishments(Allen et al., 1988; Project Management Institute, 1997). The matrix organization attempts to combine the ad-vantages of functional structures with product-oriented structures so as to create synergism by a shared re-sponsibility between project and functional management. A balance between these often opposing forcesin an organization was presumed to lead to an optimum balance between product completion and techni-cal excellence (Katz & Allen, 1985). In matrix organizations, both lateral and hierarchical dimensions of ma-trices depend on one another and neither stands alone (Joyce, 1985). Organizations using matrix structureswere expected to keep up with new technologies while obtaining savings in a more efficient assignment ofhuman and physical resources.

Important issues that loom high in the management of R&D projects are those of uncertainty, ambiguity,and complexity (Pich et al., 2002). To survive, high-tech companies must cope with the effects these issuesmay produce. Burton &Obel, (1998) recommend the matrix configuration for high uncertainty environ-ments,because matrix management allows for a greater ease in loaning an employee to another project

Management Journal for Theory and Practice Management 2012/65

Project managers support the idea that successful projects occur when the resources necessary for their workare obtained. Functional managers support the idea that resources should be made available based on theoverall needs of the organization. In fact, organizations are much more complex entities as different projectgroups compete for scarce resources. One successful project may divert essential resources from other proj-ects and thereby prevent the organization from achieving an overall successful performance. Thus, in contrastto the customary emphasis on the needs of individual projects when thinking about matrix forms, effective im-plementation calls for an ‘optimized’ equilibrium between the satisfaction of goals of the different organizationalunits. The paper introduces some insights about the implementation of matrix forms in high-tech project port-folios where uncertainty, ambiguity, and complexity are looming.

Keywords: project portfolio, matrix forms, locus of influence, flow of resources, purchase policy, setting pri-orities, low-tech environment, system dynamics model.

without making the change permanent. In any event, it is easier to accomplish work objectives in an orga-nizational structure such as matrix, where task loads are shifting rapidly between departments.

While the matrix enjoyed widespread popularity in the 1970s, discord about the effectiveness of the conceptsurfaced in the 1980s. Shortcomings in the matrix form of organization became evident as functional andproject managers were found to compete detrimentally for organizational resources (Peters & Waterman,1984). Project managers seek to obtain resources to meet any unanticipated circumstance by either ex-panding existing capacities or contracting for services from external suppliers. In contrast, functional man-agers oppose indiscriminate accumulation of assets by a project; they usually reject attempts to outsourcework because of possible underemployment of firm personnel. A project portfolio adds another set of dis-agreements when project managers compete against each other for the allocation of scarce resources (Platjeet al., 1994; Payne, 1995). These disagreements may be destructive according to evidence that high inten-sity conflicts revolve around items such as scheduling, priorities, and manpower (Thamhain&Wilemon, 1974).

Critics of the matrix, however, describe an inherent propensity for conflict among managers, which substan-tially limits its effectiveness. Although conflicts may actually encourage more effective information exchangethat can improve decision making (Stasser& Titus,1985), this positive effect breaks down quickly when con-flict becomes more intense (De Dreu&Weingart, 2003). Larson &Gobeli (1987) argued that even when con-flict in the matrix was kept to a low level, shared decisionmaking caused slow reaction times and made itdifficult to evaluate responsibility. Moreover, the strife reduces job satisfaction for functional managers (Turneret al., 1998) and results in contradictory policies that lead to a misallocation of resources and reductions inorganizational effectiveness (Martin,1994; Cardullo, 1996). However, high intensity conflicts and an unbal-anced power of influence are the most substantive failures of matrix implementation (Davis & Lawrence,1977). High-tech companies, however, must survive in a dynamic environment and the matrix retains its pop-ularity as the solution for rapidly changing marketplaces and technologies (Grinnell & Apple, 1975).

This paper surveys research carried out over a decade in which implementations of matrices seeking improvedproject portfolio performance have been investigated. This research has introduced new paradigms for matriximplementations due to the increased complexity of projects, especially those relative to uncertainty. A systemdynamics model was developed and implemented for such complex high-tech environment, a milieu with highuncertainty in meeting project deadlines and with intensive competition over scarce resources.

2. The low-tech case

The first category in organizational classification is the low-tech case—an environment not involving scarceresources of unique specialization. Total shared resource capacity is not a constraint, because a shortageof internal resources can be reinforced through the import of external capacities that can be provided by sub-contractors in a fairly rapid response time.In this environment the matrices can be classified into the follow-ing fundamental types (Laslo & Goldberg,2008):

1. Project matrices, so-called ‘profit and cost centres’.

2. Functional matrices, so-called ‘megaprojects’.

In project matrices power is given to project managers. The common configuration of these matrices isbased on the following basic principles:

1. The project manager has full control over a project budget and is authorized to take independent make-buy decisions.

2. The functional unit manager allocates resource capacity without discrimination among projects (the sameprice, no project preferences, or project priorities).

The second principle is relevant for a high-tech case but not for a low-tech case,because in the latter envi-ronment each project manager is permitted to achieve full satisfaction of needed resources from externalsources (outsourcing).

52

2012/65Management Journal for Theory and Practice Management

In functional matrices power is given to functional managers. The functional managers do not allocate re-sources to the projects, but rather, the resources are directly allocated to project activities, taking their crit-icality into consideration. The common configuration of these matrices is based on the following basicprinciples:1. The functional manager allocates resources according to present or future internal capacity, and agrees

to take external buy decisions only when this does not threaten the future employment of organizationalresources.

2. The functional manager allocates internal resource capacity without discrimination (the same price, nopreferences or priorities).

In the low-tech case, the principle of allocating internal resource capacity without discrimination is commonto both project and functional matrices; the difference between these fundamental forms derives only fromthe ‘make internally’ or ‘buy externally’ policy (see Table 1).

It is clear that project managers will prefer matrices where they have full control of the budget and where theyare authorized to take independent make-buy decisions. Project matrices provide freedom to obtain all re-sources seen as needed to implement programs.

For the functional manager, the project matrices can be seen as a disaster. These matrices prevent reason-able planning for future employment of the organization’s capacities. Functional managers seek functionalmatrices so they can control when and how projects are given additional resources, often on the basis ofoutsourcing.

The different preferences of the matrices in a low-tech environment are shown in Table 2.

The traditional description of confrontations occurring within a matrix organization is shown in Figure 1.

53

Management Journal for Theory and Practice Management 2012/65

Tab.1: Fundamental matrices associated with the lowtech case Make or Buy Policy MatrixForm Full satisfaction of projects’ needs Project matrices Partial satisfaction of projects’ needs Functional matrices

Tab. 2: The lowtech case: Preferences of matrices Matrices From the Aspect of …

ProjectMatrices FunctionalMatrices

The project manager (P) Best matrices Worst matrices The functional manager (F) Worst matrices Best matrices

FUNCTIONAL MATRICES

PROJECT MATRICES

P

F

Fig. 1: The lowtech case: Single front of confrontation

The implementation of project matrices by an organization is never acceptable to functional managers (F)who pursue functional matrices. This aspiration by functional managers will be opposed by a coalition of proj-ect managers (P) involved with both favoured and unfavoured projects. In contrast, functional managerswill do everything to prevent moves to project matrices.

This confrontation is intrinsic to the nature of the managerial positions. Davis & Lawrence (1978) suggest thatbecause power struggles occur when managers share authority, organizations should seek ways to preventconflict from reaching destructive heights.

3. The high-tech case

Laslo & Goldberg (2008) consider the high-tech case as one where organizational technological special-ization causes difficulties in achieving additional resource capacities in a rapid response time, although re-inforcement by external capacities is legitimate. The allocated capacities of scarce resources are constraintsthat determine progress in the implementation of a project.In this environment the matrices can be classi-fied into three fundamental types:• Project matrices.• Balanced matrices (prioritized resource allocations).• Functional matrices.

Project matrices are the same in both the high-tech and low-tech environments. Moreover, the basic princi-ples of these matrices remain the same. In contrast to the low-tech situation, however, in the high-tech situ-ation, resource allocation without discrimination becomes a real decision alternative. When the organizationmaintains a monopoly over scarce resources, it would have difficulty supplementing those resources throughexternal purchase. In both low-tech and high-tech environments, functional matrices are based on the sameprinciples.The balanced matrices are unique to the high-tech environment. Where scarce resources are in-volved, an organization’s readiness and ability to purchase those resources externally cannot satisfy the re-source needs of the projects—external resource unavailability trumps both readiness and ability topay.Limited capacities must be shared somehow between favoured and unfavoured projects.

In the balanced matrices, greater power goes to favoured project managers and to functional managerswho deal with unfavoured project managers. The configuration of these matrices is based on two principles:1. The functional manager allocates organizational resource capacity according to directed priorities - usu-

ally to the favoured projects, while unfavoured projects have to manage with the remaining resources.2. The make-buy policy is usually differential and determined by a project’s priority.

With the virtual impossibility of a differential make-buy policy because of an inability to obtain further scarceresources, instead of two fundamental matrices involving differential project treatment, we define only onefundamental form. So, the high-tech case can be described through three fundamental matrices based ontwo dimensions: the make-buy policy and the priority policy (see Table 3).

A two dimensional definition of fundamental resource policies in the high-tech environment brings about aconsideration of more complicated decision preferences (see Table 4).

54

2012/65Management Journal for Theory and Practice Management

Tab. 3 Fundamental matrices associated with the hightech case Priority Policy Make or Buy Policy

Equal Resource Allocations

Prioritized Resource Allocations

Full satisfaction of projects’ needs Project matrices Partial satisfaction of projects’ needs Functional matrices

Balanced matrices

Tab. 4 The hightech case: Preferences of matrices Matrices

From the Aspect of … ProjectMatrices BalancedMatrices FunctionalMatrices

The favoured project manager (H) Fair matrices Best matrices Worst matrices The unfavoured project manager (L) Best matrices Worst matrices Fair matrices The functional manager (F) Worst matrices Fair matrices Best matrices

In this case, competition between projects on resource allocations, especially concerning scarce resources,breaks the traditional coalition between project managers, and brings about unexpected agreement be-tween functional managers and project managers.

In a high-tech situation, scarce resource capacities are constraints. These constraints reduce the attrac-tiveness of project matrices among managers of favoured projects. Project matrices offer unlimited resourcecapacities for normal resources, but competition occurs for scarce resources with unfavoured projects. Bal-anced matrices create an option for favoured projects to obtain scarce resources. Therefore balanced ma-trices should be the preferred choice for favoured project managers. Functional matrices, on the other hand,mean favoured projects face a rationing of resources, and give favoured project managers a good reasonto reject such matrices.

Project matrices are the favourite matrices for managers of unfavoured projects. These matrices guaranteethem a share of all resources, in contrast to balanced matrices that leave unfavoured projects with a low prob-ability of receiving scarce resources and could lead to their failure. Despite the fact that functional matricesalso aim at rationing resources, unfavoured projects prefer them over balanced matrices, because they havea better chance of receiving resources.

The functional managers’ objective, because it is directed at the optimized use of available resources, makesthe functional matrices the most attractive. For the same reason, functional managers reject the project ma-trices, matrices that prevent resource allocation planning. Balanced matrices, however, can be a compro-mise for functional managers. Project managers, however, disagree on the worth of balanced matrices,because favoured projects are not limited by the need to allocate resources to internal development, whileunfavoured projects, most of which are internal ventures, face difficulties as resources are pulled from themto be given to the favoured, mostly sponsored, projects.

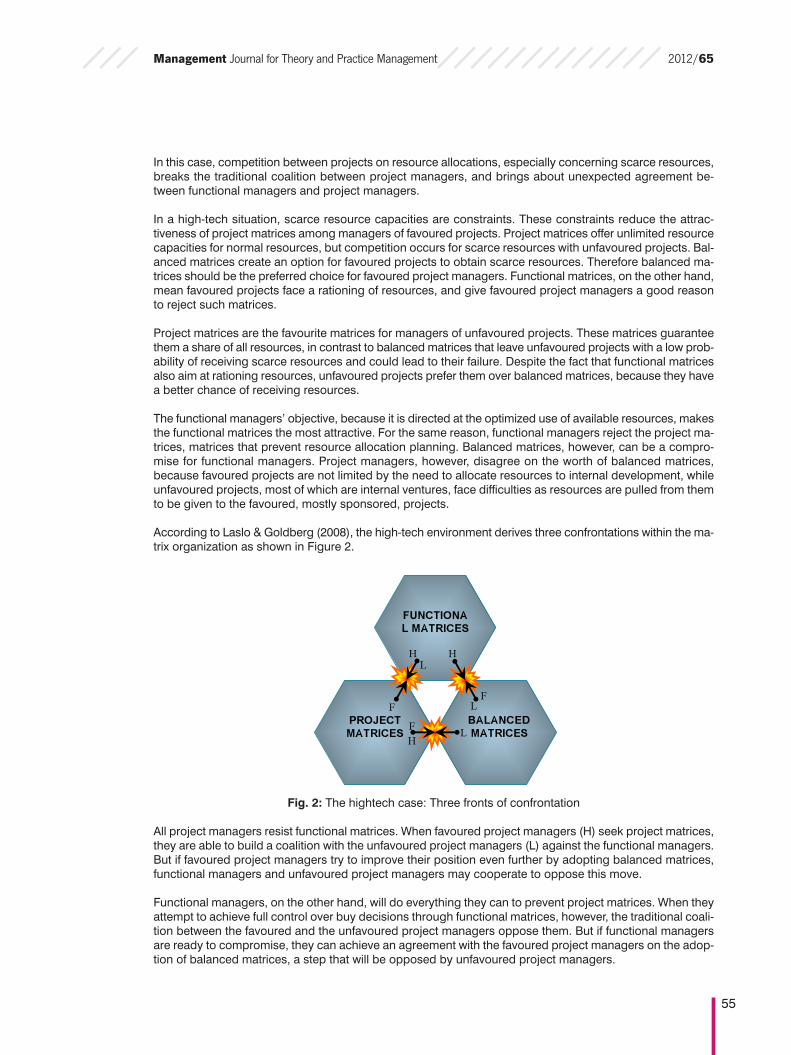

According to Laslo & Goldberg (2008), the high-tech environment derives three confrontations within the ma-trix organization as shown in Figure 2.

Fig. 2: The hightech case: Three fronts of confrontation

All project managers resist functional matrices. When favoured project managers (H) seek project matrices,they are able to build a coalition with the unfavoured project managers (L) against the functional managers.But if favoured project managers try to improve their position even further by adopting balanced matrices,functional managers and unfavoured project managers may cooperate to oppose this move.

Functional managers, on the other hand, will do everything they can to prevent project matrices. When theyattempt to achieve full control over buy decisions through functional matrices, however, the traditional coali-tion between the favoured and the unfavoured project managers oppose them. But if functional managersare ready to compromise, they can achieve an agreement with the favoured project managers on the adop-tion of balanced matrices, a step that will be opposed by unfavoured project managers.

55

Management Journal for Theory and Practice Management 2012/65

FUNCTIONAL MATRICES

PROJECT MATRICES

BALANCED MATRICES

L H

F F

LH F

L

H

Balanced matrices are the preferred policies for favoured projects, but a disaster for unfavoured projects.Managers of unfavoured projects can partner with functional managers if they agree to improve their posi-tion by moving toward the functional matrices, a step that will be opposed by favoured project managers.The efforts of unfavoured project managers to go farther, and to obtain project matrices, will be confrontedby an unexpected coalition of favoured project managers and functional managers.

4. The system dynamics model of a project portfolio’s flow of resources

A model describing a dynamic flow of resources in a project portfolio can be used to evaluate the impact ofalternative matrices on the performances of the project portfolio, of its functional units, and of each of its in-dividual projects.Under uncertainty, these expected performances are difficult to investigate empirically be-cause all the variables are an integral part of a complex nonlinear organizational system where it would beimpossible to obtain an adequate variety of situations. When it is infeasible or impossible to compute an exactresult with a , the Monte Carlo method tends to be used (Metropolis &Ulam (1949). Contrary to determinis-tic modeling using best guess single-point estimates, the Monte Carlo method considers samples of randomvariables as model inputs to produce a large number of probabilistic outcome occurrences (Vose, 2000).Monte Carlo simulations can quantify the effects of uncertainty in project schedules and budgets, providingthe project manager with statistical indicators of project performance, such as target project completiondate and cost. The Monte Carlo method has also been widely used for decades to simulate various mathe-matical and scientific situations, and it is frequently referred to in project management curricula and stan-dards, such as A Guide to the Project Management Body of Knowledge (Project Management Institute,2004). Broad Monte Carlo simulations allow a limitless number of comparisons, where a real organizationwould resist intervention because of its possible consequences. Hence, many more variables are controlledthan would be possible in a study of real organizations.

Forrester’s ‘system dynamics’ theory provides a means to understand the payoff outcomes of each player’sactions in such a complex and uncertain system (Forrester, 1980). What makes using system dynamics dif-ferent from other approaches to studying systems is the use of feedback loops. In its simplest sense, sys-tem dynamics focuses on information that is transmitted and returned throughout the progress of a process,and the system behaviours over time that result from those flows. The feedback loops create the nonlinearityfound so frequently in complex dynamic problems. Running ‘what if?’ simulations to test certain matrix formson such a model enables us to study reinforcing processes—feedback flows that generate exponentialgrowth or collapse—and balancing processes—feedback flows that help a system maintain stability.