For personal use only - ASX · For personal use only. Date: 21 May, 2013 For personal use only...

13

Shareholder presentation Date: 21 May, 2013 Transaction Solutions International Ltd For personal use only

Transcript of For personal use only - ASX · For personal use only. Date: 21 May, 2013 For personal use only...

Shareholder presentation

Date: 21 May, 2013

Transaction Solutions International Ltd

For

per

sona

l use

onl

y

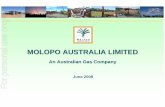

1,300

998

891 866 868

202

62

0

200

400

600

800

1,000

1,200

1,400

USA UK Italy France Brazil China India

Number of ATMs per million people

India is a highly underpenetrated ATM market

1

Developed Economies Other BRICs

Source: IBA

ATM Penetration – India versus Global Peers F

or p

erso

nal u

se o

nly

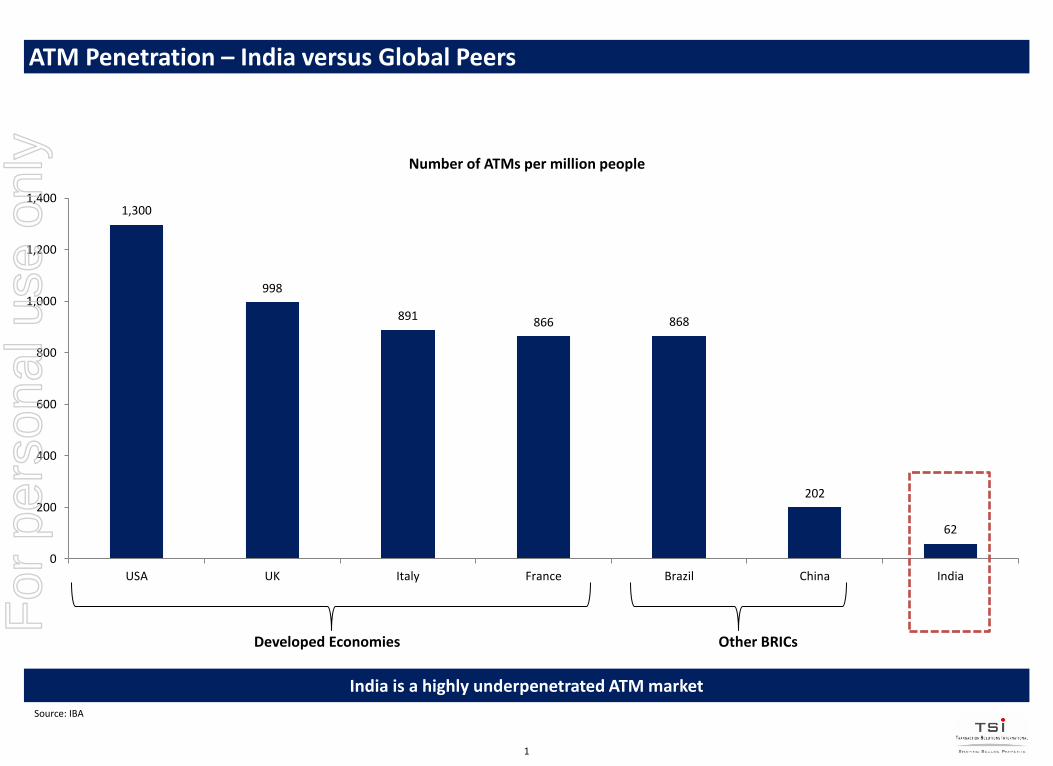

Indian Debit Card Growth

50

102

181

283

407

567

0

100

200

300

400

500

600

FY06 FY08 FY10 FY12E FY14E FY16E

# of debit cards (mm)

Card penetration to result in transaction volume increase

2

Debit card growth: FY06 – FY10 38% CAGR; FY10 – 16 ~3x

Source: RBI

For

per

sona

l use

onl

y

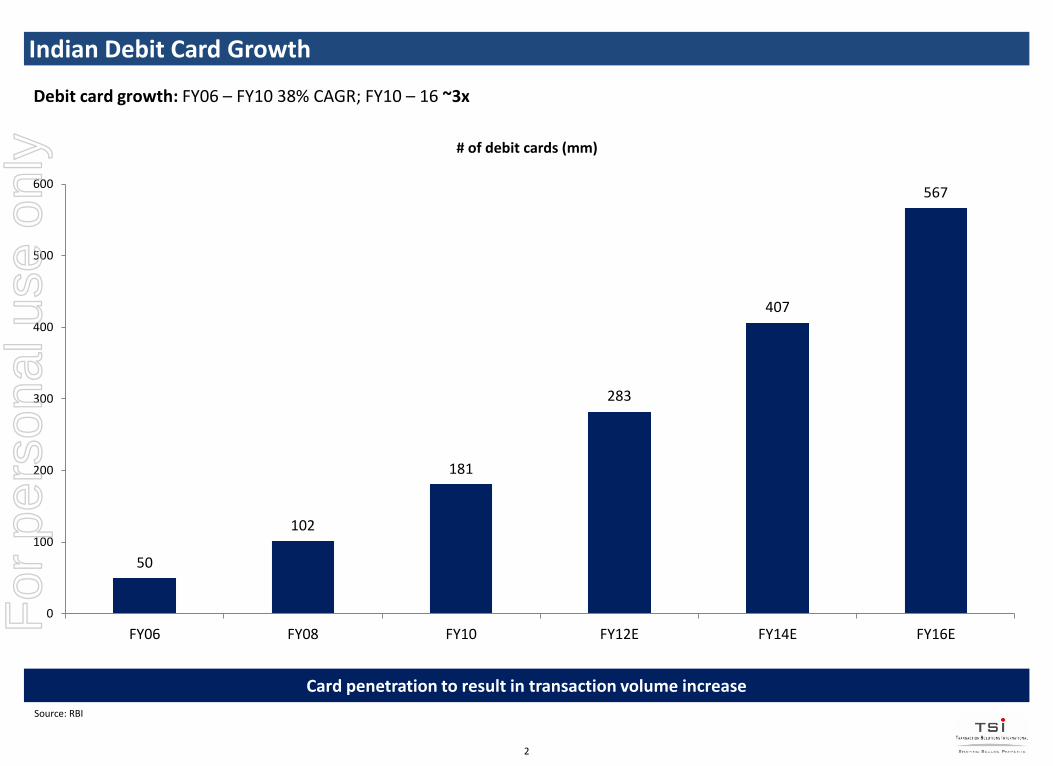

India’s rapid ATM Growth

1,102 2,495 5,489 7,851 11,334

17,642 21,122

25,924

35,057 42,436

60,180

74,743

91,778

112,448

138,557

168,447

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F 2014F 2015F

No of ATMs

Expected demand for ATMs is expected to nearly double from 2012 – 2016

3

Source: RBI

For

per

sona

l use

onl

y

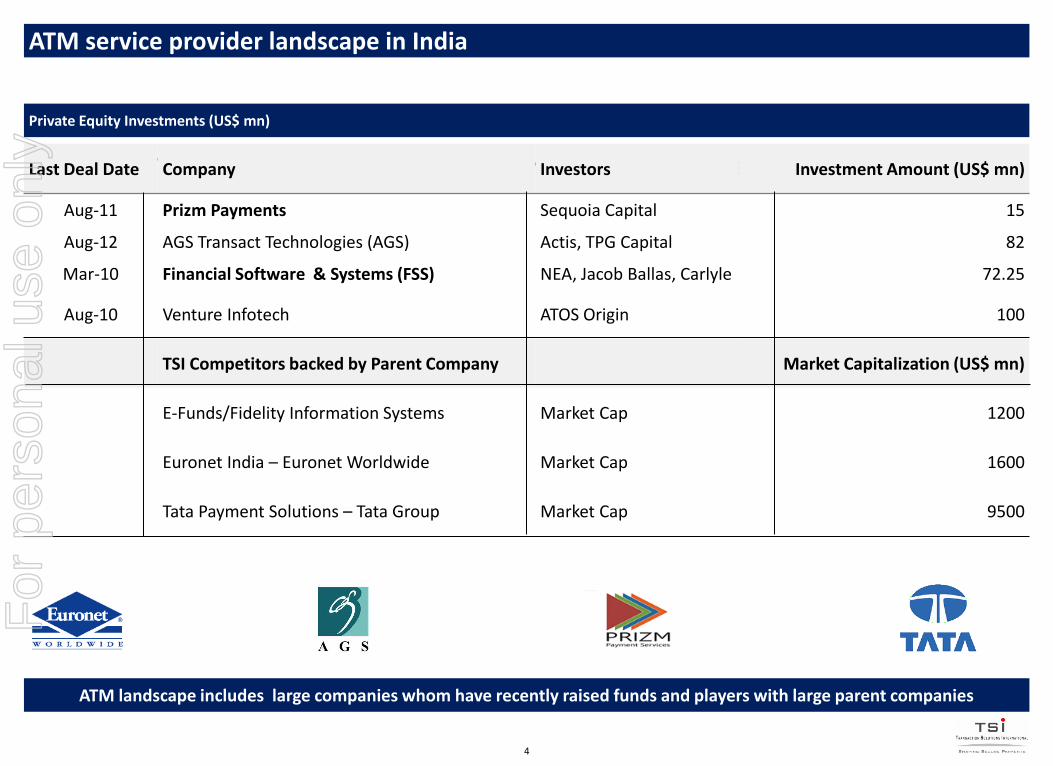

Private Equity Investments (US$ mn)

Corporate Transactions in Indian ATM Outsourcing and Payments Companies

4

Last Deal Date Company Investors Investment Amount (US$ mn)

Aug-11 Prizm Payments Sequoia Capital 15

Aug-12 AGS Transact Technologies (AGS) Actis, TPG Capital 82

Mar-10 Financial Software & Systems (FSS) NEA, Jacob Ballas, Carlyle 72.25

Aug-10 Venture Infotech ATOS Origin 100

TSI Competitors backed by Parent Company Market Capitalization (US$ mn)

E-Funds/Fidelity Information Systems Market Cap 1200

Euronet India – Euronet Worldwide Market Cap 1600

Tata Payment Solutions – Tata Group Market Cap 9500

ATM service provider landscape in India

ATM landscape includes large companies whom have recently raised funds and players with large parent companies

For

per

sona

l use

onl

y

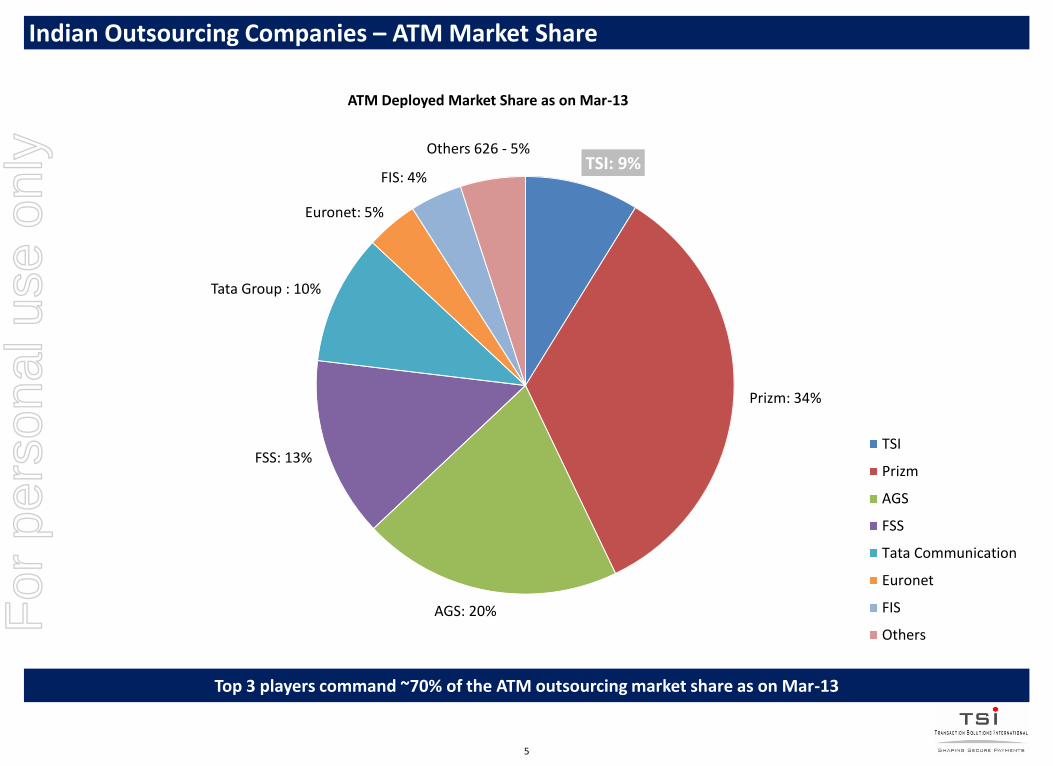

TSI: 9%

Prizm: 34%

AGS: 20%

FSS: 13%

Tata Group : 10%

Euronet: 5%

FIS: 4%

Others 626 - 5%

ATM Deployed Market Share as on Mar-13

TSI

Prizm

AGS

FSS

Tata Communication

Euronet

FIS

Others

Top 3 players command ~70% of the ATM outsourcing market share as on Mar-13

5

Indian Outsourcing Companies – ATM Market Share F

or p

erso

nal u

se o

nly

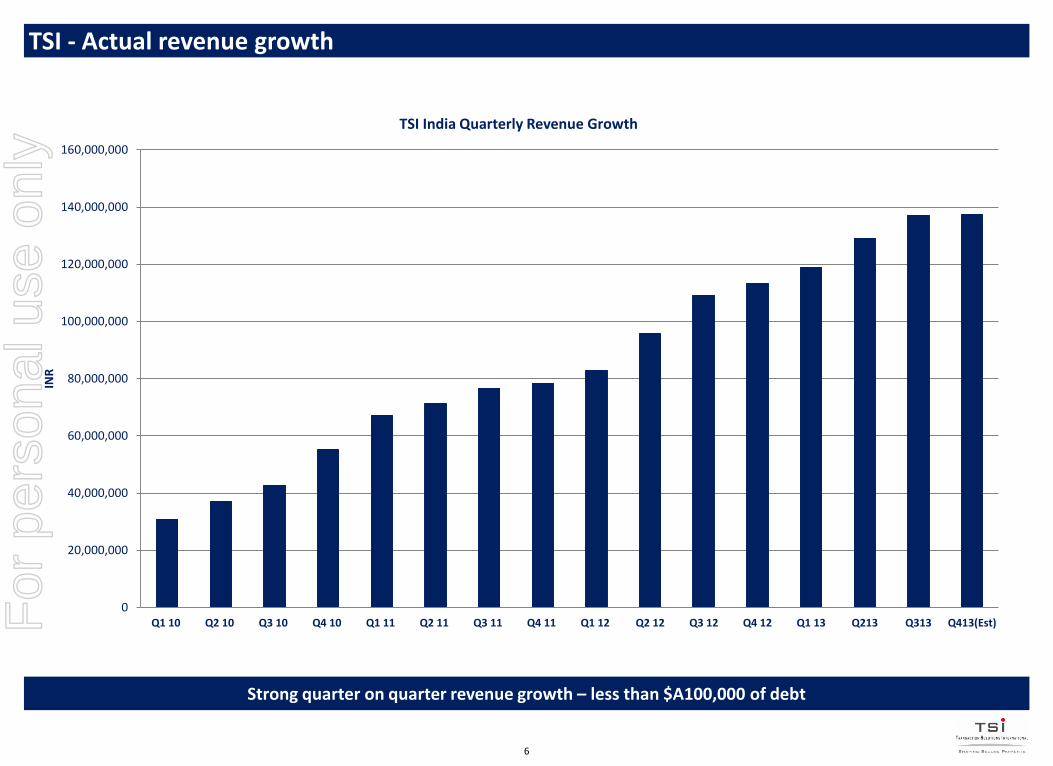

Strong quarter on quarter revenue growth – less than $A100,000 of debt

6

TSI - Actual revenue growth

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q213 Q313 Q413(Est)

INR

TSI India Quarterly Revenue Growth

For

per

sona

l use

onl

y

54.9 54.9 55.1 50.0

47.5 47.1 46.4 43.7

40.3 40.7 41.6

Q1-FY11 Q2-FY11 Q3-FY11 Q4-FY11 Q1-FY12 Q2-FY12 Q3-FY12 Q4-FY12 Q1-FY13 Q2-FY13 Q3-FY13

6,450 6,398 6,360 5,785 5,512 5,302 5,124 4,892

4,550 4,647 4,873

Q1-FY11 Q2-FY11 Q3-FY11 Q4-FY11 Q1-FY12 Q2-FY12 Q3-FY12 Q4-FY12 Q1-FY13 Q2-FY13 Q3-FY13

Transactions / ATM / Month (#)

Revenue / ATM / Month

TSI overall ATM Performance

Performance impacted by large new entrants with a focus on market entry; Per ATM metrics improving in FY13

For

per

sona

l use

onl

y

TSI & CX Partners – The Opportunity in India

8

For

per

sona

l use

onl

y

About CX Partners

Pioneers in Indian Private markets:

Ajay Relan established the Citi Private Equity business in 1995 and built the team / strategy.

The partners have a combined 50+ years of direct experience investing in Indian and global companies.

CX Partners Fund 1 Limited:

The fund raised US$515 million in 2010 and has marquee institutional investors.

Track Record:

The CX team has long and profitable record of investing in financial services sector with prior investments in banks and brokerage houses.

The team has over the years developed a reputation for picking winners and being first movers in identifying durable and actionable investment themes across economic cycles.

Oct, 2009 Jun, 2010 Aug, 2010

Oct, 2010 Dec, 2010 Feb, 2011

Aug, 2011 Sep, 2011

Oct, 2012 Nov, 2012

Sep, 2011

For

per

sona

l use

onl

y

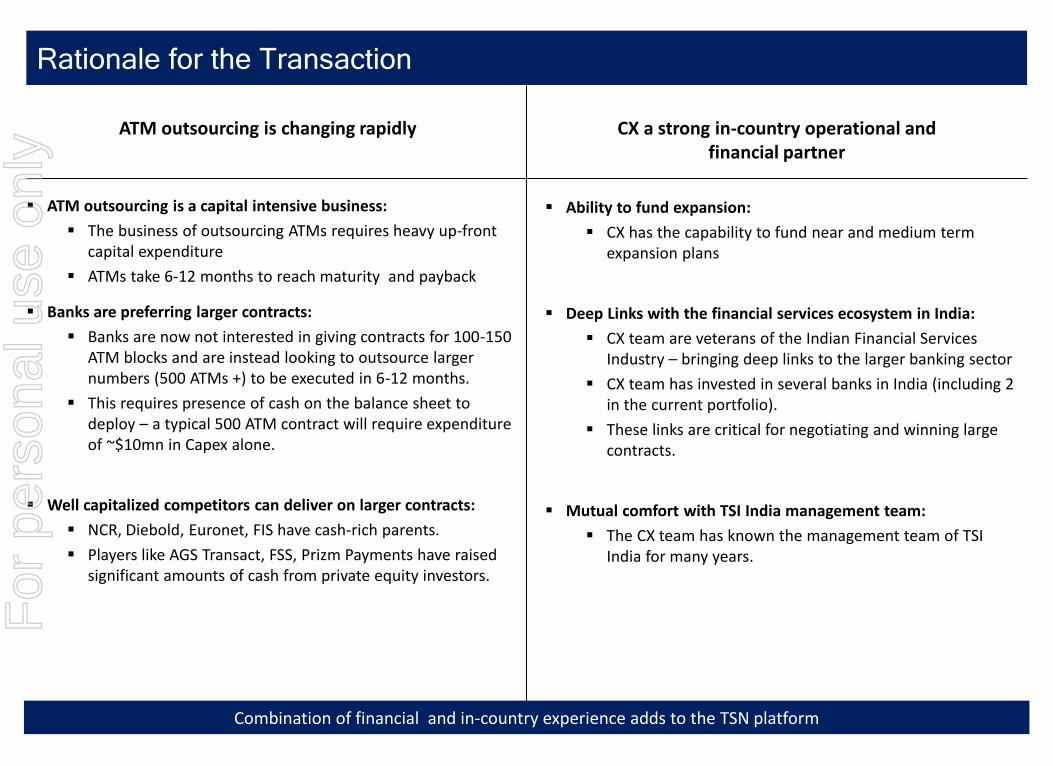

Rationale for the Transaction

ATM outsourcing is a capital intensive business:

The business of outsourcing ATMs requires heavy up-front capital expenditure

ATMs take 6-12 months to reach maturity and payback

Banks are preferring larger contracts:

Banks are now not interested in giving contracts for 100-150 ATM blocks and are instead looking to outsource larger numbers (500 ATMs +) to be executed in 6-12 months.

This requires presence of cash on the balance sheet to deploy – a typical 500 ATM contract will require expenditure of ~$10mn in Capex alone.

Well capitalized competitors can deliver on larger contracts:

NCR, Diebold, Euronet, FIS have cash-rich parents.

Players like AGS Transact, FSS, Prizm Payments have raised significant amounts of cash from private equity investors.

Ability to fund expansion:

CX has the capability to fund near and medium term expansion plans

Deep Links with the financial services ecosystem in India:

CX team are veterans of the Indian Financial Services Industry – bringing deep links to the larger banking sector

CX team has invested in several banks in India (including 2 in the current portfolio).

These links are critical for negotiating and winning large contracts.

Mutual comfort with TSI India management team:

The CX team has known the management team of TSI India for many years.

ATM outsourcing is changing rapidly CX a strong in-country operational and financial partner

Combination of financial and in-country experience adds to the TSN platform

For

per

sona

l use

onl

y

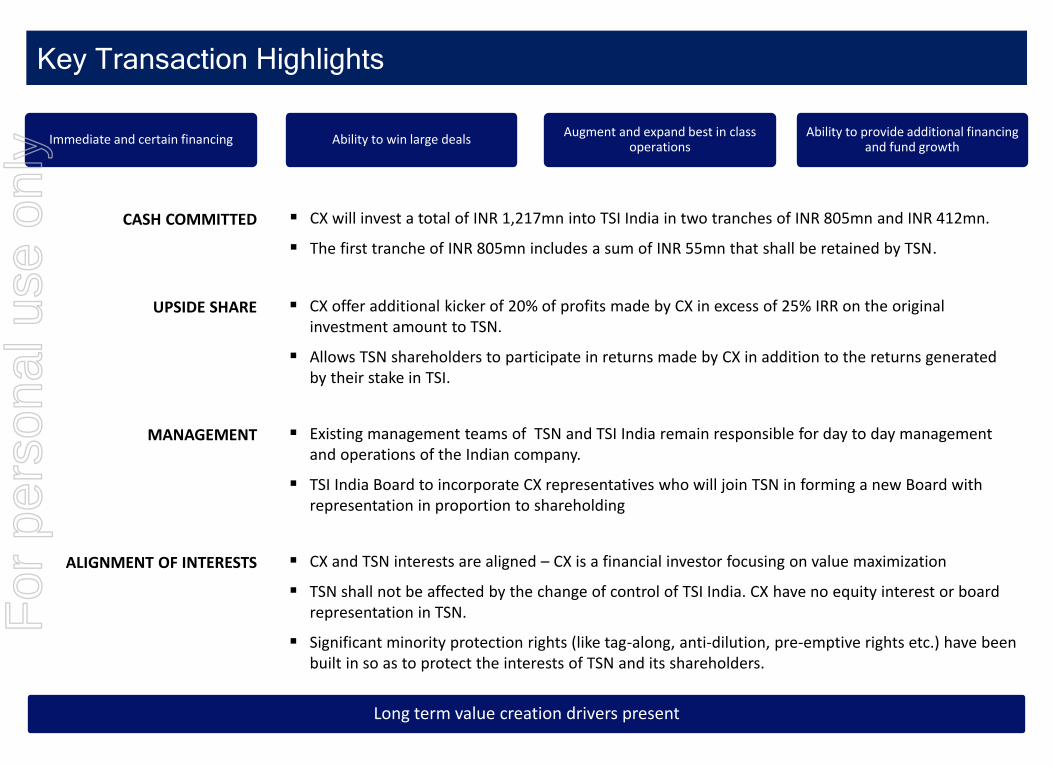

Key Transaction Highlights

CX will invest a total of INR 1,217mn into TSI India in two tranches of INR 805mn and INR 412mn.

The first tranche of INR 805mn includes a sum of INR 55mn that shall be retained by TSN.

CASH COMMITTED

CX offer additional kicker of 20% of profits made by CX in excess of 25% IRR on the original investment amount to TSN.

Allows TSN shareholders to participate in returns made by CX in addition to the returns generated by their stake in TSI.

UPSIDE SHARE

CX and TSN interests are aligned – CX is a financial investor focusing on value maximization

TSN shall not be affected by the change of control of TSI India. CX have no equity interest or board representation in TSN.

Significant minority protection rights (like tag-along, anti-dilution, pre-emptive rights etc.) have been built in so as to protect the interests of TSN and its shareholders.

ALIGNMENT OF INTERESTS

Existing management teams of TSN and TSI India remain responsible for day to day management and operations of the Indian company.

TSI India Board to incorporate CX representatives who will join TSN in forming a new Board with representation in proportion to shareholding

MANAGEMENT

Long term value creation drivers present

Immediate and certain financing Ability to win large deals Augment and expand best in class

operations Ability to provide additional financing

and fund growth

For

per

sona

l use

onl

y

Date: 21 May, 2013

Thank you for your continued support

For

per

sona

l use

onl

y