For personal use only - ASX · 3/25/2015 · Imerys, the china clay operator in Devon and Cornwall...

29

Wolf Minerals ASX:WLF|AIM:WLFE Level 3, 22 Railway Road, Subiaco, Western Australia 6008 P: +61 8 6364 3776 www.wolfminerals.com.au Investor Presentation 25 March 2015 Russell Clark, Managing Director For personal use only

Transcript of For personal use only - ASX · 3/25/2015 · Imerys, the china clay operator in Devon and Cornwall...

Wolf Minerals ASX:WLF|AIM:WLFE

Level 3, 22 Railway Road, Subiaco,

Western Australia 6008 P: +61 8 6364 3776

www.wolfminerals.com.au

Investor Presentation 25 March 2015

Russell Clark, Managing Director

For

per

sona

l use

onl

y

The information contained in this document has been prepared based upon information supplied by Wolf Minerals Limited (the Company). This Document does not constitute an offer or invitation to any person to subscribe for or apply for any securities in the Company.

While the information contained in this Document has been prepared in good faith, neither the Company nor any of its shareholders, directors, officers, agents, employees or advisers give any representations or warranties (express or implied) as to the accuracy, reliability or completeness of the information in this Document, or of any other written or oral information made or to be made available to any interested party or its advisers (all such information being referred to as Information) and liability therefore is expressly disclaimed.

Accordingly, to the full extent permitted by law, neither the Company nor any of its shareholders, directors, officers, agents, employees or advisers take any responsibility for, or will accept any liability whether direct or indirect, express or implied, contractual, tortious, statutory or otherwise, in respect of, the accuracy or completeness of the Information or for any of the opinions contained in this Document or for any errors, omissions or misstatements or for any loss, howsoever arising, from the use of this Document. Neither the issue of this Document nor any part of its contents is to be taken as any form of commitment on the part of the Company to proceed with any transaction and the right is reserved to terminate any discussions or negotiations with any person. In no circumstances will the Company be responsible for any costs, losses or expenses incurred in connection with any appraisal or investigation of the Company. In furnishing this Document, the Company does not undertake or agree to any obligation to provide the recipient with access to any additional information or to update this Document or to correct any inaccuracies in, or omissions from, this Document which may become apparent.

This Document should not be considered as the giving of investment advice by the Company or any of its shareholders, directors, officers, agents, employees or advisers. Each party to whom this Document is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. In particular, any estimates or projections or opinions contained in this Document necessarily involve significant elements of subjective judgment, analysis and assumptions and each recipient should satisfy itself in relation to such matters.

This Document may include certain statements that may be deemed forward-looking statements. All statements in this discussion, other than statements of historical facts, that address future activities and events or developments that the Company expects, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. The Company, its shareholders, directors, officers, agents, employees or advisers, do not represent, warrant or guarantee, expressly or impliedly, that the information in this Document is complete or accurate. To the maximum extent permitted by law, the Company disclaims any responsibility to inform any recipient of this Document of any matter that subsequently comes to its notice which may affect any of the information contained in this Document. Factors that could cause actual results to differ materially from those in forward-looking statements include market prices, continued availability of capital and financing, and general economic, market or business conditions. Investors are cautioned that any forward-looking statements are not guarantees of future performance and that actual results or developments may differ materially from those projected in forward-looking statements.

Disclaimer

2

For

per

sona

l use

onl

y

• Wolf is currently developing a world class tungsten mine in the UK

• Wolf will specialise in Tungsten and other specialty metals

• Wolf exists to deliver superior returns to shareholders

• Wolf is actively reviewing organic and step out growth opportunities

Wolf Minerals Limited Focused on delivering returns to shareholders

3

For

per

sona

l use

onl

y

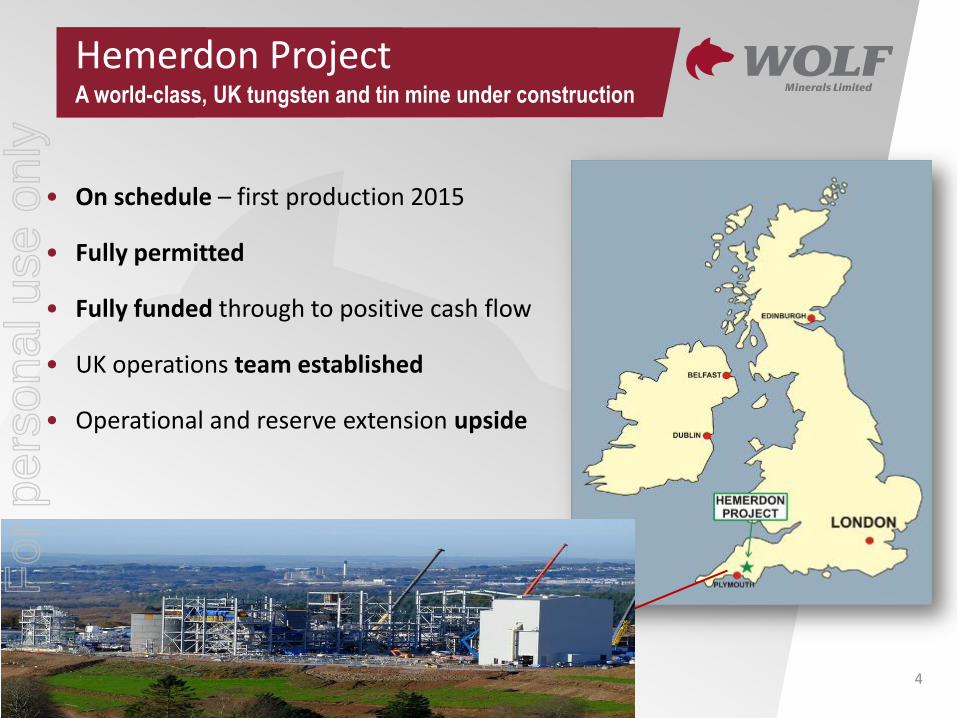

• On schedule – first production 2015

• Fully permitted

• Fully funded through to positive cash flow

• UK operations team established

• Operational and reserve extension upside

Hemerdon Project A world-class, UK tungsten and tin mine under construction

4

For

per

sona

l use

onl

y

• Hard • Heavy • High Melting Point • Non Corrosive • No Substitutes • Critical & Strategic – China has majority of reserves • Demand follows GDP growth • Expected extra demand – 4-5,000 tpa • Supply? • Current APT (Ammonium Paratungstate) price US$260-

300/mtu Market needs at least one “Hemerdon” coming on line each year to meet demand

Tungsten Critical to industrial, mining and agricultural production – no

substitutes

5

For

per

sona

l use

onl

y

The Tungsten Market Structural supply deficit – higher prices

6

Supply • Tungsten production dominated by China:

– Chinese restrictions on production and export of concentrates

– Declining grades from existing Chinese producers – China holds 60% of known tungsten reserves (USGS)

and accounts for +60% of demand and +80% of supply

– China net importer of concentrates in 2013, and continues to import

• Existing stockpiles close to depletion and producers don’t have the capacity to increase production.

• Most significant tungsten projects are at least 18 months to 2 years away from commercial production.

Demand • Forecast demand growth of 4.0 – 5.5% pa to 2018. • New capacity required to meet global demand. • Hemerdon Project will produce about 3.5% of

forecast world demand in 2016. Data Source: Tungsten Market Research Ltd (January 2014)

APT Price: Probability weighted average of low, base and high forecasts; in $Real 2012

Supply Risk

• In the past 5 years only one major tungsten project has been developed (Nui Phao in Vietnam).

• The supply forecast below includes the successful development and commissioning of 14 tungsten projects by 2018 of which 9 are located in Australia and Canada.

• Hemerdon (UK) is the only project in development, the rest don’t have development funding solutions in place and many have incomplete feasibility studies – significant supply risk

• Limited supply to push tungsten prices above US$450/mtu

0

100

200

300

400

500

600

0

20,000

40,000

60,000

80,000

100,000

120,000

2012 2013 2014 2015 2016 2017 2018

AP

T P

rice

(U

S$/m

tu)

Tun

gste

n S

up

ply

& D

eman

d (

tW)

China Vietnam UK

Canada Russia Australia

Spain Other Demand

Price

For

per

sona

l use

onl

y

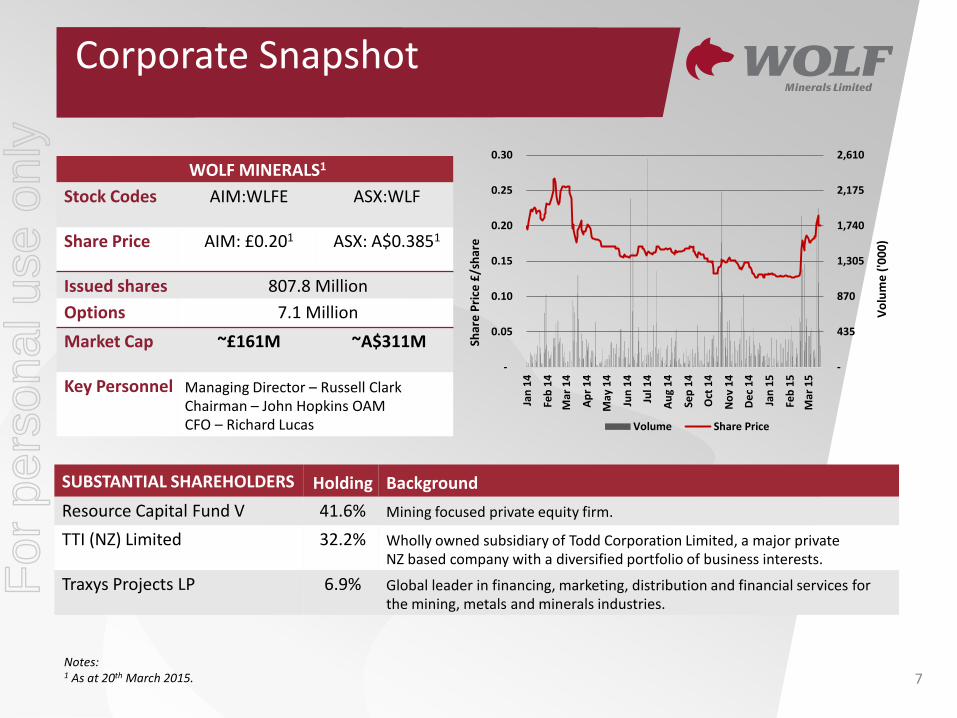

Corporate Snapshot

Notes: 1 As at 20th March 2015. 7

WOLF MINERALS1

Stock Codes AIM:WLFE ASX:WLF

Share Price AIM: £0.201 ASX: A$0.3851

Issued shares 807.8 Million

Options 7.1 Million

Market Cap ~£161M ~A$311M

Key Personnel Managing Director – Russell Clark Chairman – John Hopkins OAM CFO – Richard Lucas

SUBSTANTIAL SHAREHOLDERS Holding Background

Resource Capital Fund V 41.6% Mining focused private equity firm.

TTI (NZ) Limited 32.2% Wholly owned subsidiary of Todd Corporation Limited, a major private NZ based company with a diversified portfolio of business interests.

Traxys Projects LP 6.9% Global leader in financing, marketing, distribution and financial services for the mining, metals and minerals industries.

-

435

870

1,305

1,740

2,175

2,610

-

0.05

0.10

0.15

0.20

0.25

0.30

Jan

14

Feb

14

Mar

14

Ap

r 1

4

May

14

Jun

14

Jul 1

4

Au

g 1

4

Sep

14

Oct

14

No

v 1

4

De

c 1

4

Jan

15

Feb

15

Mar

15

Vo

lum

e (

'00

0)

Shar

e P

rice

£/s

har

e

Volume Share Price

For

per

sona

l use

onl

y

Experienced Board

8

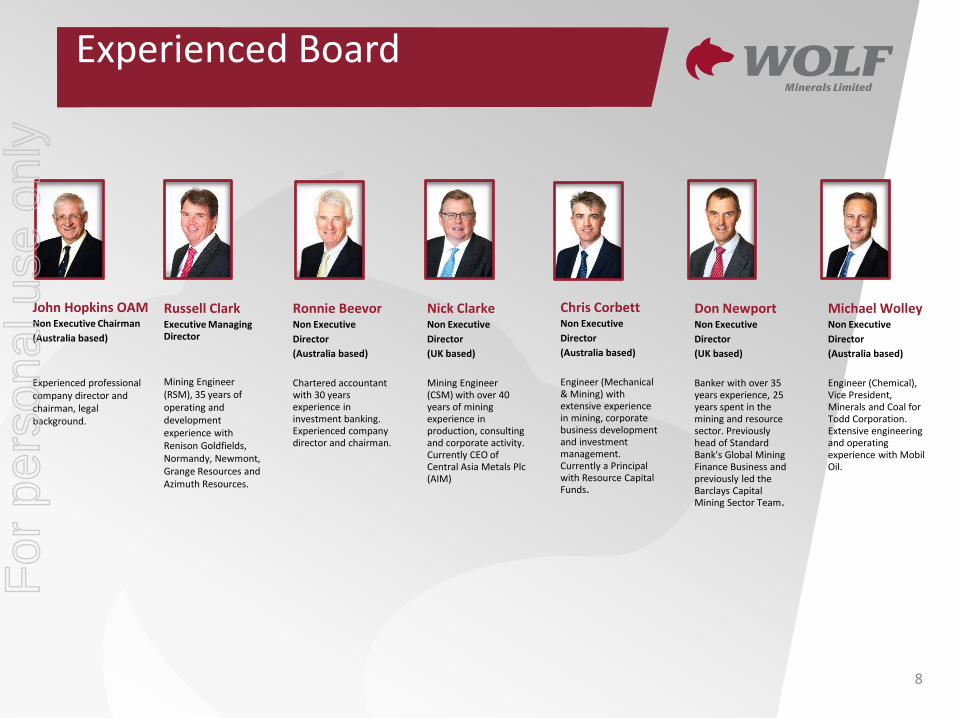

Russell Clark Executive Managing Director

Mining Engineer (RSM), 35 years of operating and development experience with Renison Goldfields, Normandy, Newmont, Grange Resources and Azimuth Resources.

John Hopkins OAM Non Executive Chairman

(Australia based)

Experienced professional company director and chairman, legal background.

Ronnie Beevor Non Executive

Director

(Australia based)

Chartered accountant with 30 years experience in investment banking. Experienced company director and chairman.

Nick Clarke Non Executive

Director

(UK based)

Mining Engineer (CSM) with over 40 years of mining experience in production, consulting and corporate activity. Currently CEO of Central Asia Metals Plc (AIM)

Chris Corbett Non Executive

Director

(Australia based)

Engineer (Mechanical & Mining) with extensive experience in mining, corporate business development and investment management. Currently a Principal with Resource Capital Funds.

Don Newport Non Executive

Director

(UK based)

Banker with over 35 years experience, 25 years spent in the mining and resource sector. Previously head of Standard Bank's Global Mining Finance Business and previously led the Barclays Capital Mining Sector Team.

Michael Wolley Non Executive

Director

(Australia based)

Engineer (Chemical), Vice President, Minerals and Coal for Todd Corporation. Extensive engineering and operating experience with Mobil Oil.

For

per

sona

l use

onl

y

Executive Management Team

9

Russell Clark Executive Managing Director

Mining Engineer (RSM), 35 years of operating and development experience with Renison Goldfields, Normandy, Newmont, Grange Resources and Azimuth Resources. Previously MD and CEO of Grange Resources and Azimuth Resources. FAICD

Richard Lucas Chief Financial Officer and Joint Company Secretary (Australia based)

Chartered Accountant. Previously a Director at PWC. Commercial Manager at Lihir Gold and CFO of the Geotech Group.

Rupert McCracken Project Manager (UK based)

Mechanical Engineer with over 25 years of global experience in the development, construction and commissioning of mineral processing projects. Previously an engineer with Bechtel, Transfield & Minproc Engineers, and a project manager for Comet Resources, Ticor South Africa, BHP Billiton and Resolute Mining.

Jeff Harrison Operations Manager (UK based)

Mining Engineer (Nottingham, RSM) with over 35 years of global mining and mineral processing experience. Has been a senior manager for Imerys, the china clay operator in Devon and Cornwall and is well known to the local Plymouth community. He is a Chartered Engineer, a Fellow of the AusIMM and a member of the Institute of Quarrying.

Andy Bond Mine Manager (UK based)

Geologist/Mining Engineer (Camborne) with over 29 years of mining industry experience in Devon and Cornwall.

Charlie Northfield Process Manager (UK based)

Metallurgist (Camborne) with over 30 years of experience including managing process plants recovering tungsten and tin in Thailand and Zimbabwe.

For

per

sona

l use

onl

y

10

Hemerdon Project F

or p

erso

nal u

se o

nly

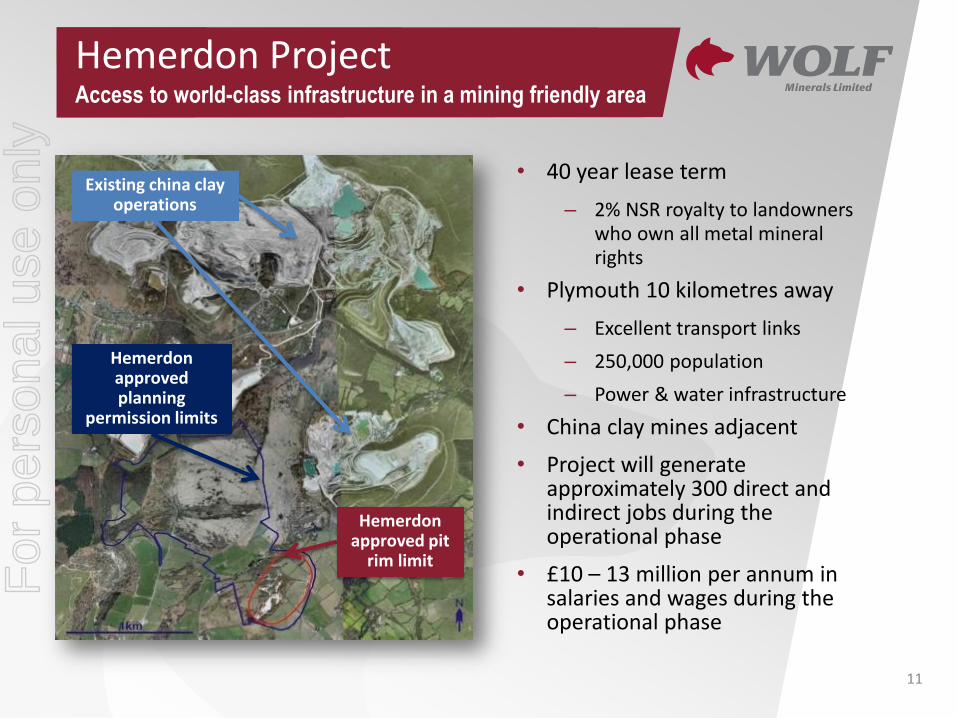

• 40 year lease term

– 2% NSR royalty to landowners who own all metal mineral rights

• Plymouth 10 kilometres away

– Excellent transport links

– 250,000 population

– Power & water infrastructure

• China clay mines adjacent

• Project will generate approximately 300 direct and indirect jobs during the operational phase

• £10 – 13 million per annum in salaries and wages during the operational phase

Hemerdon Project Access to world-class infrastructure in a mining friendly area

11

Existing china clay operations

Hemerdon approved planning

permission limits

Hemerdon approved pit

rim limit

For

per

sona

l use

onl

y

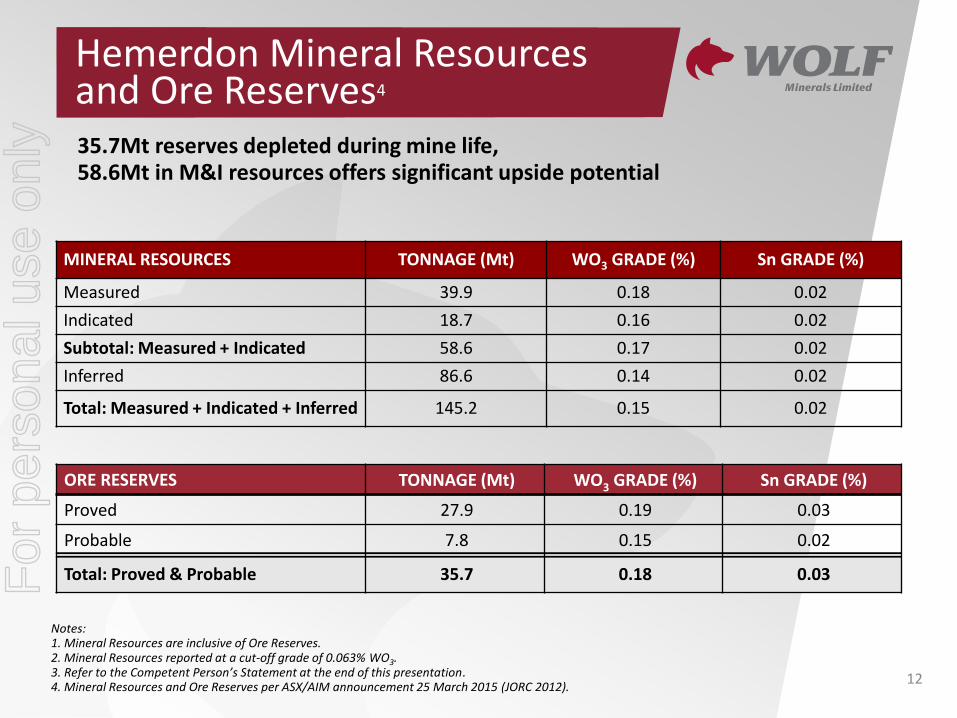

Hemerdon Mineral Resources and Ore Reserves4

12

Notes: 1. Mineral Resources are inclusive of Ore Reserves. 2. Mineral Resources reported at a cut-off grade of 0.063% WO3. 3. Refer to the Competent Person’s Statement at the end of this presentation. 4. Mineral Resources and Ore Reserves per ASX/AIM announcement 25 March 2015 (JORC 2012).

ORE RESERVES TONNAGE (Mt) WO3 GRADE (%) Sn GRADE (%)

Proved 27.9 0.19 0.03

Probable 7.8 0.15 0.02

Total: Proved & Probable 35.7 0.18 0.03

35.7Mt reserves depleted during mine life, 58.6Mt in M&I resources offers significant upside potential

MINERAL RESOURCES TONNAGE (Mt) WO3 GRADE (%) Sn GRADE (%)

Measured 39.9 0.18 0.02

Indicated 18.7 0.16 0.02

Subtotal: Measured + Indicated 58.6 0.17 0.02

Inferred 86.6 0.14 0.02

Total: Measured + Indicated + Inferred 145.2 0.15 0.02

For

per

sona

l use

onl

y

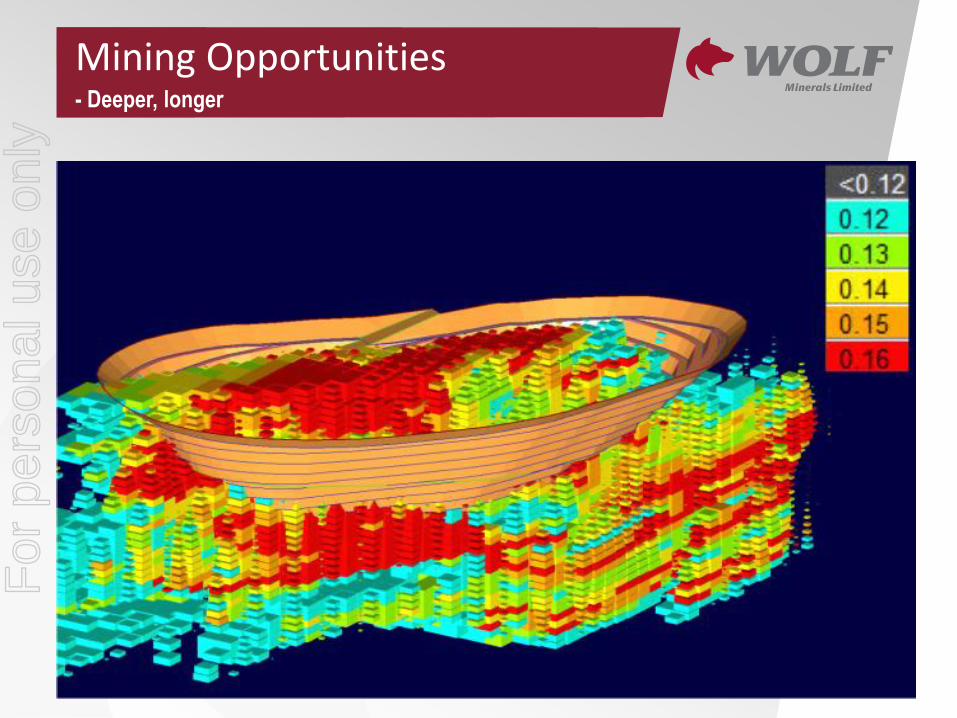

• Open pit mining, 10 year mine life1

• Pit 800m long x 400m wide x 260m deep

• Low life of mine strip ratio

• 3Mt of ore mined per annum1

• Open at depth and along strike

Mine Design Open pit mine, low strip ratio, extension potential

1 Assumes extension of current planning permissions beyond 2021 and 5.5 days per week operation 13

• Drilling indicates mineralisation is open at depth to +400m below surface, ~140m below final pit bottom

• New drill holes planned to test depth extension

Hemerdon Ore Body Cross-Section

For

per

sona

l use

onl

y

Geotechnical Program Completed - Steeper wall slopes now possible

14

New pit design results in 34% more ore reserve1

1 per ASX/AIM announcement 25 March 2015

Soft Granite

Hard Granite

2015 redesigned pit

2011 DFS pit

-65m RL

5m RL

For

per

sona

l use

onl

y

15

Mining Opportunities - Deeper, longer

For

per

sona

l use

onl

y

• Proven technology

• Gravity circuit using DMS, tables, spirals

• Initial fines removal and DMS upgrades headgrade from 0.19% WO3 to ~1% WO3

• Throughput of 3 Mtpa – Tungsten recovery ~66%

• Production: – ~3,450 tpa WO3 in concentrate1 – ~460 tpa tin in concentrate1

• Product shipped by container ~100 tonnes per week1

Processing Simple gravity circuit using proven technology

16

PRIMARY &

SECONDARY

SCRUBBING &

SCREENING

DENSE MEDIA

SEPARATION

REGRIND MILL

REDUCTION KILN

MAGENETIC

SEPARATORS

ROM BIN

TUNGSTEN

CONCENTRATE

TERTIARY

CRUSHING

SPIRAL

CONCENTRATORS

SHAKING TABLES

SHAKING TABLES

TIN

CONCENTRATE1 Assumes 5.5 days per week operation

For

per

sona

l use

onl

y

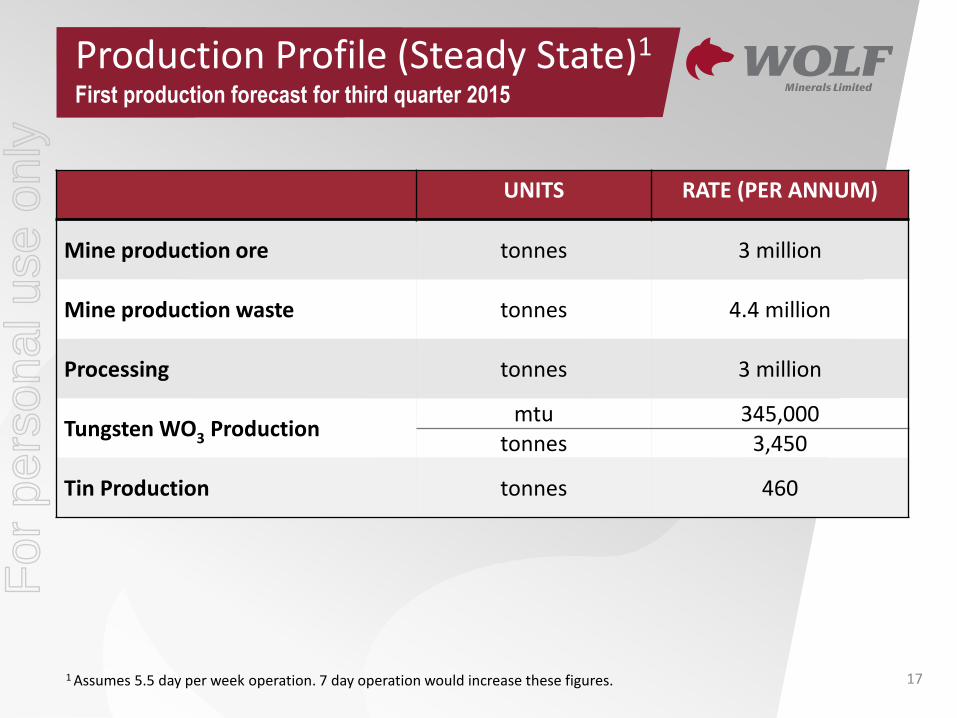

Production Profile (Steady State)1 First production forecast for third quarter 2015

UNITS RATE (PER ANNUM)

Mine production ore tonnes 3 million

Mine production waste tonnes 4.4 million

Processing tonnes 3 million

Tungsten WO3 Production mtu 345,000

tonnes 3,450

Tin Production tonnes 460

17 1 Assumes 5.5 day per week operation. 7 day operation would increase these figures.

For

per

sona

l use

onl

y

Mine Life

• Additional mine life potential through: – Steepening walls, mining deeper - – Known extensions to the south – Ore body is open at depth - underground potential

Processing

• Increased production through: – Improved WO₃ recoveries – currently 66% – Greater plant availability – Trial 7 day operation approved, March 2015

– Sale of aggregate

Financial

• Significant leverage if APT prices higher than forecast

• Processing upside opportunities may result in increased production with no additional Capex

Opportunities – Being Realised

18

DFS Ore Reserve increased by 34%, March 2015

Note: Subject to confirmatory studies and extension of planning permission where appropriate

For

per

sona

l use

onl

y

19

Community & Social Responsibility F

or p

erso

nal u

se o

nly

• £75 million Engineering Procurement & Construction (EPC) contract

• Globally experienced firm in EPC project execution

• Solid reputation for on time, on budget delivery

• Commissioning and performance guarantees included

• Completion scheduled for 3rd quarter 2015

EPC contract to GR Engineering Fixed term, fixed price EPC with globally experienced firm

20

Hemerdon processing facility GR Engineering

Interactive 3D Design Model

For

per

sona

l use

onl

y

• 80% of tungsten concentrate off-take with GTP & Wolfram Bergbau und Hutten

• Five year delivery schedule

• Partial guarantee for senior debt, along with German Government under UFK scheme

• Tin marketing agreement with Traxys

Strategic Off-taker Support Fixed term, fixed volume, floating price

Wolfram Bergbau und Hutten (Sandvik)

21

Global Tungsten & Powders (Plansee)

For

per

sona

l use

onl

y

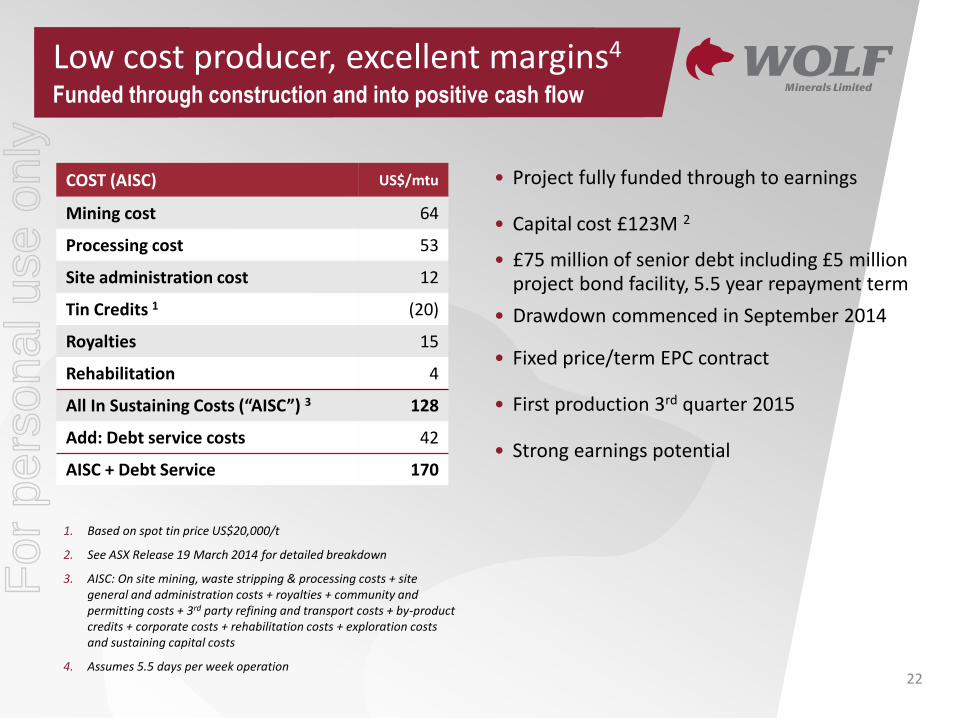

Low cost producer, excellent margins4 Funded through construction and into positive cash flow

COST (AISC) US$/mtu

Mining cost 64

Processing cost 53

Site administration cost 12

Tin Credits 1 (20)

Royalties 15

Rehabilitation 4

All In Sustaining Costs (“AISC”) 3 128

Add: Debt service costs 42

AISC + Debt Service 170

• Project fully funded through to earnings

• Capital cost £123M 2

• £75 million of senior debt including £5 million project bond facility, 5.5 year repayment term

• Drawdown commenced in September 2014

• Fixed price/term EPC contract

• First production 3rd quarter 2015

• Strong earnings potential

22

1. Based on spot tin price US$20,000/t

2. See ASX Release 19 March 2014 for detailed breakdown

3. AISC: On site mining, waste stripping & processing costs + site general and administration costs + royalties + community and permitting costs + 3rd party refining and transport costs + by-product credits + corporate costs + rehabilitation costs + exploration costs and sustaining capital costs

4. Assumes 5.5 days per week operation

For

per

sona

l use

onl

y

Live photos and streaming video @

23

http://www.wolfminerals.com.au/irm/content/live-streaming-video.aspx?RID=326

For

per

sona

l use

onl

y

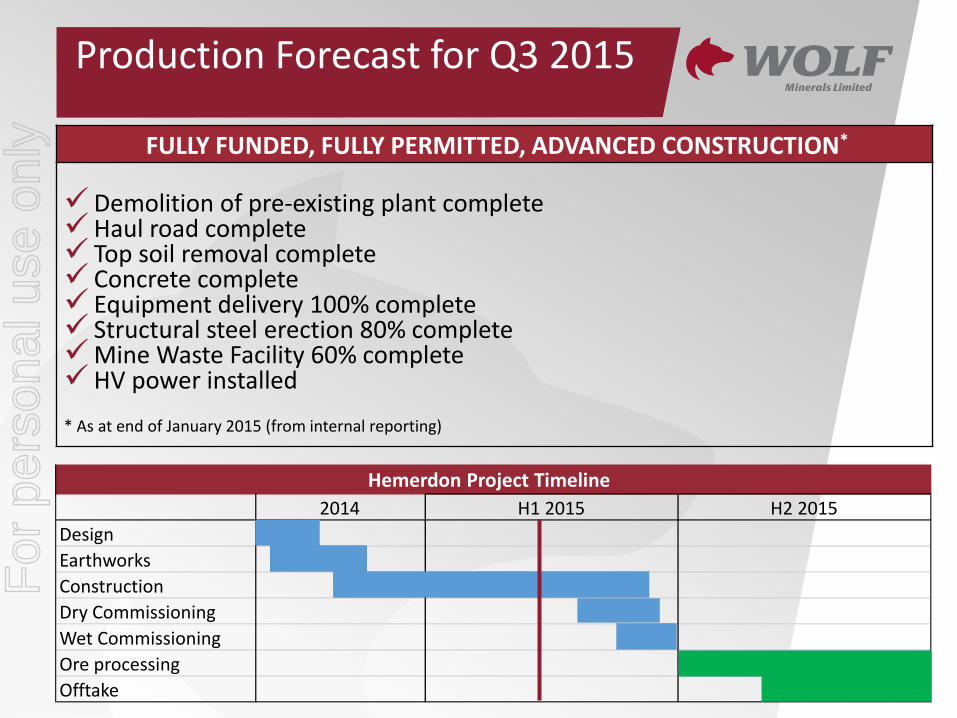

FULLY FUNDED, FULLY PERMITTED, ADVANCED CONSTRUCTION* Demolition of pre-existing plant complete Haul road complete Top soil removal complete Concrete complete Equipment delivery 100% complete Structural steel erection 80% complete Mine Waste Facility 60% complete HV power installed

* As at end of January 2015 (from internal reporting)

Production Forecast for Q3 2015

24

2014

Design

Earthworks

Construction

Dry Commissioning

Wet Commissioning

Ore processing

Offtake

H1 2015 H2 2015

Hemerdon Project Timeline

For

per

sona

l use

onl

y

25

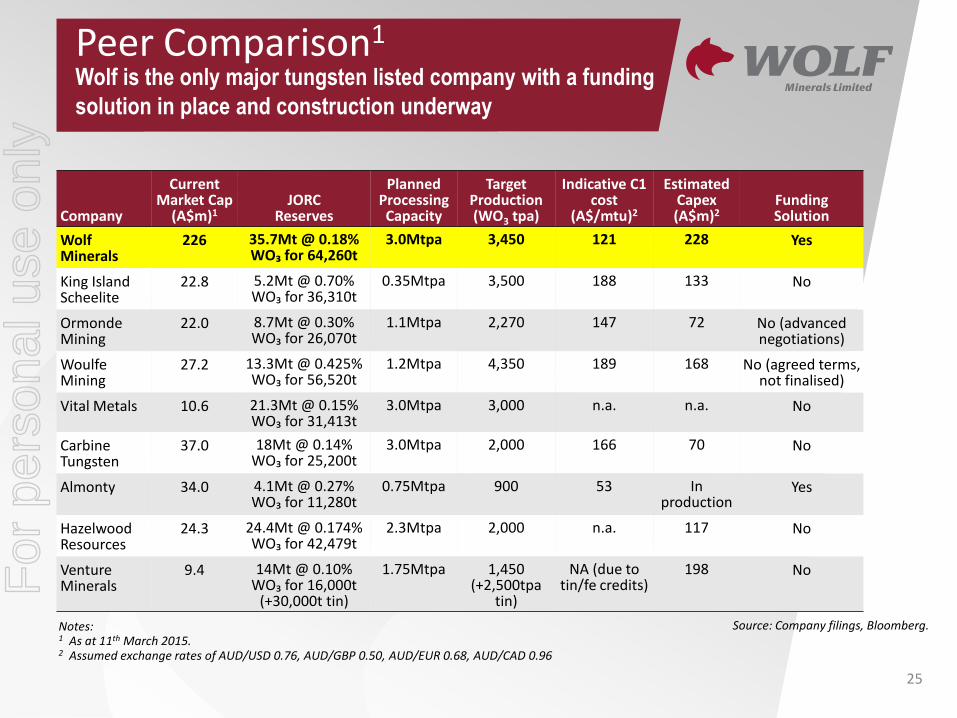

Company

Current Market Cap

(A$m)1 JORC

Reserves

Planned Processing Capacity

Target Production (WO3 tpa)

Indicative C1 cost

(A$/mtu)2

Estimated Capex (A$m)2

Funding Solution

Wolf Minerals

226 35.7Mt @ 0.18% WO₃ for 64,260t

3.0Mtpa 3,450 121 228 Yes

King Island Scheelite

22.8 5.2Mt @ 0.70% WO₃ for 36,310t

0.35Mtpa 3,500 188 133 No

Ormonde Mining

22.0 8.7Mt @ 0.30% WO₃ for 26,070t

1.1Mtpa 2,270 147 72 No (advanced negotiations)

Woulfe Mining

27.2 13.3Mt @ 0.425% WO₃ for 56,520t

1.2Mtpa 4,350 189 168 No (agreed terms, not finalised)

Vital Metals 10.6 21.3Mt @ 0.15% WO₃ for 31,413t

3.0Mtpa 3,000 n.a. n.a. No

Carbine Tungsten

37.0 18Mt @ 0.14% WO₃ for 25,200t

3.0Mtpa 2,000 166 70 No

Almonty 34.0 4.1Mt @ 0.27% WO₃ for 11,280t

0.75Mtpa 900 53 In production

Yes

Hazelwood Resources

24.3 24.4Mt @ 0.174% WO₃ for 42,479t

2.3Mtpa 2,000 n.a. 117 No

Venture Minerals

9.4 14Mt @ 0.10% WO₃ for 16,000t

(+30,000t tin)

1.75Mtpa 1,450 (+2,500tpa

tin)

NA (due to tin/fe credits)

198 No

Notes: 1 As at 11th March 2015. 2 Assumed exchange rates of AUD/USD 0.76, AUD/GBP 0.50, AUD/EUR 0.68, AUD/CAD 0.96

Source: Company filings, Bloomberg.

Peer Comparison1 Wolf is the only major tungsten listed company with a funding

solution in place and construction underway

For

per

sona

l use

onl

y

• First new metal mine in England for over 40 years

• Globally significant deposit of a strategic metal - Ore Reserve increase 34% March 2015

• One of the largest western world tungsten mines

• Experienced management team

• Fully permitted and funded to positive cashflows

• Strong local and regional support for project

• Strong strategic and institutional shareholder base

• Construction approaching completion – production forecast for Q3 2015

• Tungsten offtake agreements with two of world’s largest end-users

• Significant potential to increase production and mine life - Trial for 24/7 operation given the go ahead in March 2015

• Tungsten price forecast to rise (Argus Tungsten Monthly Outlook - January 2015)

Summary Hemerdon Project

26

For

per

sona

l use

onl

y

Wolf Minerals Limited (ASX: WLF, AIM: WLFE) (“Wolf” or “the Company”) wishes to clarify where

production forecasts for its Hemerdon Tungsten and Tin project released in its presentations are sourced.

On 16th May 2011, Wolf Minerals issued an ASX announcement “Hemerdon Tungsten and Tin Project

Definitive Feasibility Study Results” in which the Minerals Resources and Reserves were stated. In

addition the mining method and associated assumptions, and the concentrator flow sheet, tin and

tungsten recoveries and resultant annual production figures for tin and tungsten were also stated. These

continue to form the basis of the production forecasts included in the company’s presentations.

Following the 16th May 2011 announcement, capital and operating costs and the project time line were

re-assessed.

On 20th January 2014, Wolf Minerals issued an ASX announcement “Hemerdon Tungsten Project Pre-

Construction Update” in which it updated DFS estimates of the project timetable, the capital costs of the

project and the operating costs associated with the project. These continue to form the basis of the

project capital expenditure forecasts and the project timeline that are included in the company’s

presentations.

On 25th March 2015, Wolf Minerals issued an ASX announcement “Wolf Minerals Announces 34%

Increase in Ore Reserves at Hemerdon Tungsten and Tin Project” in which it announced a Mineral

Resource Estimate compliant to the JORC code 2012, and an Ore Reserve which had been revised

following a successful geotechnical drilling program which resulted in steeper pit slope design and

increased ore reserves.

Clarification of production and capital cost forecast

assumptions stated in this presentation

27

For

per

sona

l use

onl

y

The Mineral Resource Estimate reported is above a 0.05% W (0.063% WO3) cut-off and is based on work done by Mr Daniel Guibal, who is a Chartered Professional Fellow of The Australasian Institute of Mining and Metallurgy. Mr Guibal is employed by SRK Consulting and takes responsibility for the Mineral Resource Estimate. He has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the "Australasian Code for reporting of Exploration Results, Mineral Resources and Ore Reserves" (JORC, 2012). Mr Guibal consents to the inclusion of the Mineral Resource Estimate based on his information in the form and context in which it appears.

The 2015 Ore Reserve is based on work done by Mr Rick Taylor, who is a Chartered Professional Member of

The Australasian Institute of Mining and Metallurgy. Mr Taylor is a full time employee of Wolf Minerals

Limited, and takes responsibility for the Ore Reserves. He has sufficient experience which is relevant to the

style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to

qualify as a Competent Person as defined in the 2012 Edition of the "Australasian Code for reporting of

Exploration Results, Mineral Resources and Ore Reserves" (JORC, 2012). Mr Taylor consents to the inclusion

of the Ore Reserve based on his information in the form and context in which it appears.

Competent Persons Statement

28

For

per

sona

l use

onl

y

Wolf Minerals ASX:WLF|AIM:WLFE

Level 3, 22 Railway Road, Subiaco,

Western Australia 6008 P: +61 8 6364 3776

www.wolfminerals.com.au

FURTHER INFORMATION:

Russell Clark - Managing Director

Or

Tim Thompson / Adam Lloyd

+44 (0) 207 653 9850 / [email protected]

James Moses

+61 (0) 420 991 574/[email protected]

For

per

sona

l use

onl

y