FOR OFFICIAL AA/ 3oc'd- ,szoZ - www … · FOR OFFICIAL USE ONLY AA/ 3oc'd- ,szoZ Report No....

84

Documentof The World Bank FOROFFICIAL USE ONLY AA/ 3oc'd- ,szoZ Report No. P-4867-MOR REPORT ANDRECOMMENDATION OF THE PRESIDENT OF THE INTERNATIONAL BANK FOR RECONSTRUCTION ANDDEVELOPMENT TO THE EXECUTIVE DIRECTORS ON A PROPOSED STRUCTURAL ADJUSTMENT LOAN IN AN AMOUNT EQUIVALENT TO US$200 MILLION TO THE KINGDOM OF MOROCCO November 8, 1988 This document bas a resticted ditibution and may be used by recipients only in the perfonnance of their offcial duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

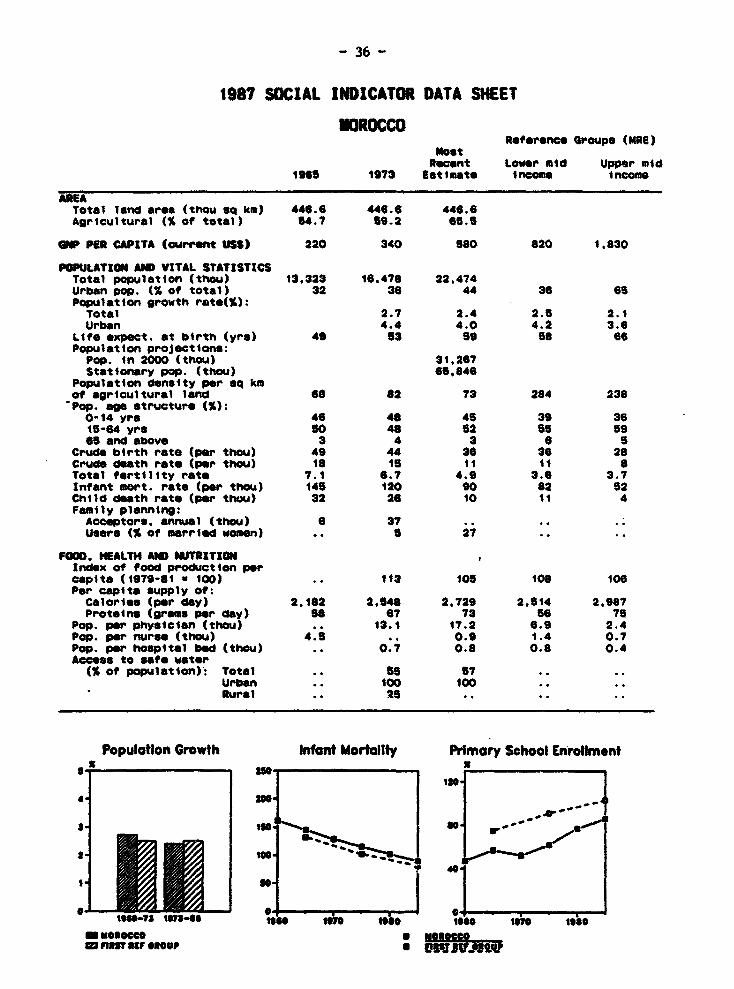

Transcript of FOR OFFICIAL AA/ 3oc'd- ,szoZ - www … · FOR OFFICIAL USE ONLY AA/ 3oc'd- ,szoZ Report No....

Document of

The World Bank

FOR OFFICIAL USE ONLY

AA/ 3oc'd- ,szoZReport No. P-4867-MOR

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

TO THE

EXECUTIVE DIRECTORS

ON A

PROPOSED STRUCTURAL ADJUSTMENT LOAN

IN AN AMOUNT EQUIVALENT TO US$200 MILLION

TO

THE KINGDOM OF MOROCCO

November 8, 1988

This document bas a resticted ditibution and may be used by recipients only in the perfonnance oftheir offcial duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

AverageCalendar 1987 July 1988

Currency Unit = Dirham (DH)1 Dirham (DH) - US$0.1196 0.11861 US Dollar (US$) = DH 8.359 8.432

FISCAL YEAR

January 1 - December 31

ABBREVIATIONS AND ACRONYMS

AfDB: African Development BankASAL: Agricultural Sector LoanBank al-Maghrib: The Central BankCMPE: Centre Marocain pour la Promotion des Exportations

(Center for the Promotion of Moroccan Exports)GFCF: Gross Fixed Capital FormationICB: International Competitive BiddingIGR: Personal Income TaxIHS: International Harmonized SystemITPA: Industrial and Trade Policy Adjustment LoanMLT: Medium and Long TermOCP: Office Cherifien des PhosphatesOECF: Overseas Cooperation Fund (Governmenc of Japan)PAL: Public Administration LoanPGI: General Import ProgramPSN: National Solidarity TaxQR: Quantitative RestrictionSMAEX: Societe Marocaine d'Assurance a 1'Exportation

(Export Insurance Agency)SOE: Statement of ExpensesTIP: Target Investment ProgramTPS: Domestic Sales TaxVAT: Value Added Tax

FOR oFCAL US ONL!

MOROCCO

SrRUCITURAL ADJUSTMENT LOAN

Loan and Pro Sam

Borrower: The Kingdom of Morocco.

Amount: US$2C0 million equivalent.

Terms: 20 years, including 5 years of grace at the standardvariable interest rate.

Description: Morocco's Structural Adjustment Program aims to achieve asustainable increase in the rate of economic growth inorder to ensure employment opportunities and acceptableliving standards for its growing population, while --

enhancing external creditworthiness. The proposed SALwould support the first phase of a program of actioncovering: an increase in the level of public revenues andsavings to finance essential infrastructure and socialinvestment, while reducing the need for public sectorborrowing; further rationalization of trade and industrialpolicy; and the elaboration of an external liabilitymanagement action plan. Specific policy measures wouldhelp raise the overall efficiency of the economy in linewith program. goals.

Bentfits The principal benefits of the adjustment program resultingand Risks: from the acceleration of economic growth through increased

factor productivity would be: a rise in employmentopportunities and living standards for the growingpopulation; the development of an outward-oriented privatesector; and continued improvement in externalcreditworthiness with a view to restoring voluntary accessto commercial borrowing. Program risks concern the timelyimplementation of a comprehensive set of structuralreforms, which will require a cohesive and concertedapproach from those governmental institutions involved inpolicy implementation. Underscoring the Government'scommitment to the adjustment program are strong policydialogue as reflected in a jointly-evolved, medium-termmacroeconomic framework, the implementation of severalbroad reforms in the fiscal area, and the buoyant responseof the economy to the structural measures in place. These,bolstered by a multifaceted program of training andtechnical assistance, all serve to mitigate the risks.

This document has a stricd distrbution and may ' t:u<d by ecipients only in the peformaneof their official duties. Its contents may not otherwi -e be dis m-ed without World Bank authorition.

- ii -

Estimated The proceeds of the proposed loan would be disbursed in twoDisbursements: tranches: US$100 million upon loan effectiveness, bhich is

expected to take place by December 1988, and the remainingUS$100 million after the completion of a number of keyactions upon which success of the program depends. Releaseof the second tranche iP planned for mid-1989.

Appraisal Report: None

Map: IBRD No. 20864

KINGDOM OF MOROCCO

STRUCTURAL ADJUSTlM LOAN

Table of Contents

Page

INTRODUCTION I

PART I: THE ECONOMY 1

Background 1Macroeconomic Developmentssince the Firancial Crisis of 1983 2

Outstanding Development Issues 5Rationale for Continuing Bank Adjustment Lending 6

PART II: THE STRUCTURAL ADJUSTMENT PROGRAM 7

Program Objectives and Policy Tools 7The Policy Framework ofthe First Structural Adjustment Loan 9

Tax Policy and Administration 9The Public Investment Budget 12Trade and Industrial Policy 16External Liability Management 20

Program Benefits, External Financing Requirementsand Social Impact 23fsacroeconomic Outcome of the SAL 23Assessment of Macroeconomic Perfozmance 26Medium-Term External Financing Requirements 27Social Impact of Adjustment 29

PART III: LOAN ADMINISTRATION 30

Procurement and Disbursement 30Accounts and Audits 31Coordination with Other Agencies 31

The OECF 31The AMDB 31

Implementation Risks and Justification 31

PART IV: OTHER BANK OPERATIONS 33

Experience with Past Adjustment Lending 33Project Lending 34

PART V: RECOMMENDATION 35

ANNEXES: I Key Economic Indicators 38II Letter of Development Policy

and Associated Policy Matrices 44III Supplementary Program Data Sheet 62IV Status of Bank Operations in Morocco 65V Institutional Support, Technical Assistance & Training 68VI Progress under Existing Adjustment Operations 70

MAP: IBRD No. 20864

REPORT AND REON OF THE PROF THE ITERNAIONAL BANK FOR RECONSTRUCTON AND DEVELOPMENT

TO THE EXECUTIVE DRECTORSON A PROPOSED STRUCTURAL ADJSIENT LOWAN

IN AN AMOUNT EQUIVALENT TO US$200 MILLONTO THE KINGDOM OF MOROCCO

INTRODUCTION

1. I submit the following report and recommendation on a proposed loanfor the equivalent of US$200 million to the Kingdom of Morocco. The loanwould support the first phase of a structural adjustment program aimed at anacceleration of growth and a strengthening of social services. The programwould be implemented in the context of a macroeconomic framework which ensuresinternal and external equilibria. The loan would have a term of 20 years,including 5 years of grace, at the standard variable interest rate.Cofinancing arrangements with other bilateral and multilateral agencies arebeing actively pursued.

PART I - THE ECONOMY

2. Morocco has a relative abundance of natural resources, including theworld's largest and most easily accessible phosphate reserves, vast areas ofarable land, and an extensive coastline. Its geographical proximity to majorindustrialized markets favors the development of international trade. Thispotential has been exploited in terms of strong manufactured export growth, abooming tourism sector, and the substantial outflow of workers abroad whoseremittances figure prominently in Morocco's balance of payments.

3. Social indicators have improved over time, although differentiallyaccording to income level. The urban-based growth of the 1960s and 1970s, forexample, increased the share of income accruing to the upper 20% of thepopulation, while the poorest levels vitnessed a reduction in their share from181 to 12X. Overall growth was nonetheless sufficiently rapid to diminish theincidence of absolute poverty from almost 50% in 1960 to 372 in 1979. Otheraspects of socioeconomic development have improved since the mid-1960s withlife expectancy at birth rising from 49 to 59 years, infant mortalitydeclining from 145 to 90 per thousand, caloric intake per capita increasingfrom 952 to 119S of the minimum daily standard requirement, and primary schoolenrollment rates growing from 572 to 81S, principally the result of higherfemale participation rates. Although the urban growth rate is twice that ofthe rural sector at present, a significant share of the population continuesto reside in the countryside and is employed in agriculture. In 1986, thepopulation, which is increasing at about 2.61 per annum, reached 22 millionwith a GNP per capita of US$580.

-2 -

4. For nearly two decades after Independence in 1956, Morocco followeda re-atively conservative approach to economic management. A slow rise ininvestment was financed by periodic recourse to external borrowings, whichsupplemented the limited pool of domestic savings. During this period, theeconomy grew at a rate of 4S per anmum. Primary products, principallyphosphates, accounted for 90S of merchandise exports.

5. A boom in phosphate prices during the years 1975-77 injected renewedvigor into the economy and coincided with rising defense expenditures and anunprecedented expansion of the public investment program, signaling the end ofthe circumspect fiscal policies of the past. The sudden reversal in the termsof trade in the late 1970s, as a result of the plunge in phosphate prices andthe second oil shock, prompted Morocco to resort increasingly to externalcapital markets in order to maintain the higher rate of public investment.The viability and expediency of this development strategy were conditioned bythe abundance of foreign financing opportunities on highly attractive terms(interest rates were negative in real terms).

6. During this period, Morocco's external debt grew exponentially fromUS$1.8 billion in 1975 to US$13.9 billion in 1983, at which point itrepresented nearly 1201 of GDP and 3551 of foreign exchange earnings. Thestructure of Moroccan debt changed over this period with 401 of outstandingliabilities owed to conmercial banks compared to nil a decade earlier; morethan 601 of the debt was at non-concessional rates. The unanticipated rise ininternational interest rates in the early 1980s, compounded by the decliningproductivity of public investment and a severe and prolonged drought in1980-84, proved more than Morocco's balance of payments could endure. Bereftof foreign exchange reserves and access to external funds, Morocco was unableto shoulder its debt service burden-the debt service ratio reached 531 in1983, with interest payments alone accounting for 201 of exports.

7. By that time, it ha'd become clear that the solution to Morocco'sfinancial distress lay in a comprehensive program of economic reform. A setof extensive stalb'lisation and adjustment policies was evolved by theGovernment and supported by a series of IMF standby arrangements and WorldBank sectoral adjustment loans. Restrictive fiscal and monetary policies wereemployed tu contain aggregate domestic demand, while structural reforms intrade and industry, agriculture, education, and the public enterprise sectorwere initiated to augment the supply response of the economy. Debt servicepayments to official and comnercial creditors were rescheduled, initiating aprocess that has already spanned five years and is expected to continue wellinto the future.

M b Deveow_ents since the Financial Crss of 1983

8. The challenge of adjustment facing Moroccan policy makers was indeedformidable given the forbidding debt burden, the large financial imbalanceswhich beset the economy, and the relatively limited base of non-traditionalmanufactures. Despite difficult circumstances, Morocco has made much progressin alleviating both internal and external disequilibria since 1983.Stabilization of public finances was achieved through a package ofexpenditure-reducing measures to decrease government absorption. As a result,the overall fiscal deficit as a share of GDP fell from 11.71 in 1983 to 6.11

_3-

in 1987 on a commitment basis. This performa.'ce was all the more remarkablein view of the budgetary claims of national priorItios in the Western Saharaand the sizable interest payments on the public debt, the latter representingnearly one-quarter of total budgetary expenditures. The improvement it thebalance of payments has been even more impressive, as evidenced by the declinein the current account deficit from 12.71 of GDP in 1982 to about 1S (beforedebt rescheduling) in 1987.

9. The substantial reduction in macroeconomic imbalances can beattributed to a combination of favorable external dtvelopments and the pursuitof rigorous policy reforms. The decline in international petroleum pricesserved to strengthen not only the trade balance but the fiscal situation aswell, with the introduction of an oil levy equivalent to 2.7S of GDP(para. 32). Following a period of protracted drought, agricultural productienresponded decidedly to the more auspicious weather conditions, leading to adecline in food prices ana imports. These factors contributed to animprovement in the overall terms of trade when the decrease in import pricesmore than offset the fall in export-prices (para. 10) in 1986, restoring muchof the deterioration that occurred since 1980.

10. Structural policy measures intended to augment the productivecapacity of the economy, however. underlie much of the adjustment that hastaken place sinc6 1983. The sweeping reform of the trade and industrialregime has given rise to productivity gains in labor and capital, averagingover 51 per year, as well as a shift in the structure of external tradeflows-V. Measures introduced to eliminate export barriers, reduce existingdisparitiks between exporting and import-substituting activities, and simplifyadministrative procedures in the area of external trade have led to buoyantexport growth of manufactured goods (para. 60). Increasing at an averageannual rate of 15.5S since 1983, nonphosphate-based manufactures havecompensated both the decline in the price of phosphoric acid and thestagnati=n of world phosphate demand. Nont-aditional manufactured goods nowaccount for over 301 of total merchandise exports, compared to approximately201 in 1983, ~esulting in a more diversified export base and a reduceddependency on natural resource-based manufactures.

11. Appropriate exchange rate management, an important factor underlyingthis impressive performance, served to boost tourism proceeds and workerremittances as well, while containing import demand at sustainable levelsfollowing the reduction of external trade barriers. Despite a 251 nominaldepreciation of the Dirbam since 1983, judicious monetary policies helpedstaunch inflationary pressures, resulting in a 231 decline in the realexchange rate. In line with the objectives of a Bank-supported financialsector reform, the structure of deficit financing changed significantly duringthis period, as the Treasury resorted increasingly to the nonbank privatesector to compensate for reduced borrowing opportunities abroad and limitedaccess to Central Bank funds. This enabled the monetary authorities to eschewinflationary financing and lower the rate of change in prices from 12.5% in1983 to 2.41 in 1987.

1/ The impact of liberalization on trade and industrial adjustment has beenthoroughly documented in report 6714-MOR.

4-

12. The extent of Morocco's adjustment efforts is apparent in theevolution of the non-interest current account balance, which represents themagnitude of the resource transfer between the home country and the rest ofthe world. Before the adjustment program was launched in 1983, Morocco wasreceiving a not resource transfer in excess oL 52 of its GDP. This trend wasreversed after 1985 with Morocco transferring nearly 3% of its GDP abroad in1987, net of debt rescheduling, in line with the narrowing of the currentaccount deficit (para. 8). During this period, the stock of external debtnonetheless continued to rise owing to continuing, albeit decreasing, currentaccount deficits, and increases in the valuation of external liabilitieslinked to real exchange rate movements between the Dirham and internationalcurrencies and amongst the international currencies themselves. By 1987,total debt outstanding and disbursed still represented about 115 of GDP and353X of all foreign exchange earnings.

13. The Bank has given its support to Morocco's adjustment program interms of policy advice, technical assistance, and financing (paras. 109-110).In certain areas, however, progress was not as rapid as expected. Forexample, objectives aiming at the complete repeal of quantitative restrictionson imports by 1989 and the elimination of a stable source of fiscal receiptsin the form of the special import tax (para. 61), as reflected in the ITPAprogram, were not achievable within the given timeframe in light of thelooming threat of world protectionism. the growing opposition of certaindomestic interest groups to further trade liberalization, and the pressingneed to narrow the budget deficit in the face of structural revenueconstraints. In the context of the overall implementation of trade policyreform (paras. 57-61), however, Morocco has arguably become one of the moreliberal trade regimes within the developing world.

14. On balance, the extensive reforms implemented since 1983 haveinitiated a significant transformation of Morocco's underlying economicstructure without unmanageable stress to the social fabric. Themoderately-paced implementation of stabilization measures, the exploitation ofavailable financial capital and restructuring techniques in the form of debtrescheduling, and the adoption of supply-oriented policy reforms have allserved to mitigate the contractionary impact of adjustment. The fall inpurchasing power of salaried employees tollowing the devaluation of the Dirbamwas to some extent limited by the fact that consumer prices increased at aslower rate than producer prices. The social costs of lower real wages,however, were partly compensated by a postive employment effect in themanufacturing sector (7.5% growth per annum since 1983), as the bias towardcapital use was reduced and production shifted to more labor-intensiveexporting activities. In general, the rationalization of the structure ofincentives led to a growing outward-orientation and an increasedcompetitiveness of Moroccan industry which, in turn, enabled firms to exploitexisting productive capacity and avert recessionary pressures. Prescientpolicy-making was evident in the design of a detailed plan, developed inconjunction with the Bank, to target subsidized foodstuffs to the poor topermit a substantial narrowing of generalized consumption subsidies.

-5 -

15. The progress achieved in remedying macroeconomic imbalances since theonset of the adjustment program nevertheless belies certain structuralweaknesses. Although the impact of stabilization policies on economic growthwas relatively restrained, with GDP increasing at an average annual rate of3.3S, per capita consumption stagnated. Moreover, the narrowing of the fiscaldeficit has been achieved, in large part, at the expense of publicinvestment. To this effect, the share of central government gross fixedcapital formation in GDP has fallen by more than half since the early 1980s,representing a modest 2.81 in 1987. While a good deal of budgetary resourceshad previously been channeled to finance premature investments or projects ofquestioneble economic priority, the recent curtailment of developmentexpenditures has been so severe that it has led to the suspension orcancellation of many essential investments in key economic and social sectors,with potentially deleterious effects on future growth and the development ofhuman capital, as well as on income distribution.

16. A less than buoyant fiscal system and the inability to effect therequisite cuts in current expenditures are manifest in the weak public savingseffort, reflected in a 4.51 current budget deficit on average since 1983.kUe discrepancies between budgetary commitments and cash payments have led toa s,ubstantial buildup of domestic payment arrears, which represented 7.31 ofGDp at end-1987. In addition, the virtual depletion of foreign exchangereserves, amounting at times to only several days worth of imports, has givenrise per4!-dically to external payment arrears and protracted delays inobtaining foreign exchange. This has resulted in foregone opportunities orhigher financial charges for those economic agents operating in the foreigntrade sector.

17. T..re are indications that the tendency of the Government to consumebeyond its means may adversely affect private investment demand. For example,real interest rates have risen by approximately 19.5 percentage points sincethe mid-1970. in order to mobilize the private resources necessary tocompensate for the comparative lack of foreign and public savings. Thesignificant rise in the cost of capital and the liquidity problem faced bysome firms as a result of the proliferation of domestic payment arrears, pointto the continuing danger of crowding-out.

18. Finally, Morocco's balance-of-payments' position remains precariousdespite the dramatic improvement in the current account previously noted(pars. 8). At present, debt indicators remain high (para. 74) and constitutea major impediment to mobilizing adequate levels of external financing.Furthermore, the future performance of the current account is predicated, inpart, on the favorable evolution of the external environment. Unlessconstraints on the capital account are eased, Morocco would have to transfereven higher levels of net resources abroad, thereby compromising futureeconomic growth, adjustment efforts, and, ultimately, prospects for improvedcreditworthiness.

- 6 -

FRdl#2fti for g9§*tbig Bo& AdHzsbDFr¢ tMAWn

19. Structural weaknesses in the area of public finance have at timesslowed the pace of reform in sectoral adjustment programs supported by theBank, viz. the inability to reduce budgetary reliance on trade taxation, therecurrence of government arrears, particularly to the public enterprisesector, and the lack of local counterpart funding for public investmentprograms in agriculture, health, and education. As evidenced by thesedevelopments, Morocco's adjustment program is at a critical juncture.Although the vigorous pursuit of policy reforms at the sectoral level has ledto marked increases in output and employment, particularly in export-orientedsectors (para. 14), initial optimism about the timeframe needed to yield thefull benefits of each program is being tempered, as continuing budgetarydifficulties introduce tensions into program execution. Moreover, thefavorable exogenous factors which abetted adjustment efforts cannot be reliedupon to nourish higher rates of economic growth. Finally, Morocco's heavydebt service obligations, which continue to absorb a substantial share ofnational savings, militate in favor of additional structural reforms designedto raise the growth rate above that achieved is the recent past. Indeed, thisorientation is explicitly recognized in the Government's medium-termmacroeconomic framework, which targets a 4.52-51 GDP growth rate. Theviability of a growth-oriented medium-term scenario is conditioned on theextension of structural policy reform to the government budget, required toconsolidate and strengthen the sectoral gains achieved thus far.

20. In view of its ongoing involvement in Morocco's sectoral adjustmentprograms1', the Bank is well placed to assist the Government in deepeningits adjustment efforts through a structural adjustment loan (SAL). Thecompouents of the SAL have been tailored to address the principal difficultiesfacing existing sectoral programs, as well as formulate medium-term approachesto issues addressed hitherto in a short-term perspective. The IMF support tothe Government in furthering the Tmprovement in external and domestic balanceswill continue to be both necessary and desirable. In this context, theestablishment of annual budget and balance-of-payments targets is warranted.Insofar as structural weaknesses in fiscal and investment policy persist, itis apposite that the SAL program pursue the objective of supportinga medium-term framework for roroccan public finances in parallel with the IMFprogram to reduce the budget deficit.

21. Two broad interrelated strategic goals will be pursued throughcontinued adjustment lending. The SAL program would both coalesce with theachievements of past adjustment efforts and address remaining constraints tofurther policy reform, thus effectively helping Morocco to move from aninitial phase of stabilization-cum-liberalization to one of comprehensivestructural adjustment. As the first in a program of two or three similaroperations, the SAL would serve to support Morocco during the transition to apath of higher growth through increased investment, greater productivity,

1/ A description of Bank-supported sectoral adjustment operations and theprogress achieved in meeting specific conditions are addressed inpar"s. 109-111 and Annex VI.

- 7 -

and improved creditworthiness. Concomitantly, a shift in Bank assistancetowards investment lending will be facilitated through continuedliberalixation at the sectoral level, together with the reconstitution of thecountry's development programs for key social sectors and infrastructure. TheBank's continued association with the adj-ustment process through the provisionof quick-disbursing resources is warranted in light of Morocco's limitedaccess to international capital markets, while its catalytic role could betapped to mobilize sources of additional financing (paras. 101-102) in orderto ensure more equitable burden-sharing and limits on exposure.

PART I - THE STRUCTURAFL ADJUSTMENT PROGRAM

PrWIuan Obet vesand PRocn Tools

22. During the past few years, the Moroccan economy has grown at anaverage rate of 3.32 on an annual basis, slightly more than the rate ofincrease in the population. The proposed medium-term adjustment program seeksto reinvigorate the economy through a rise in the growth rate of per capitaincome and to consolidate the structural achievements registered to date,without disrupting macroeconomic atability. Spanning the initial two years ofthe Government's medium-term adjustment program, the SAL is viewed as thefirst in a series of two or three similar operations designed to fully restoreMorocco's access to international financial markets by the mid-1990s, whileenabling the ec-nomy to grow by 4.5S-52 per annum. The adjustment programcontains four sets of policy tools to be used in achieving these goals.

23. Fiscal reform measuree are intended to increase the buoyancy of thetax system, while minimizing distortionary effects on resource allocationdecisions. Measures to be supported under the SAL (paras. 37-42) serve tonarrow fiscal incentives and lower marginal tax rates, leaving exportpromotion to the realm of trade and exchange rate policy. Additional actionin the area of tax administration would improve collection efforts(paras. 43-44).

24. Public investment has taken much of the brunt of the fiscaladjustment in the past. The deteriorating quality of the publ£c capital stockrepresents at present a significant constraint to attaining higher rates ofGDP growth. The increase in the level and efficiency of public investmentexpenditures constitutes a major component of the adju&tment program. To thiseffect, particular attention is being devoted to the identification of atarget public investment program, which would respond to the twin objectivesof complementing private investment and providing for the most urgent socialneeds. The timely execution of the target investment program would besupported by an improvement in budgetary procedures.

25. Trade liberalization efforts have given rise to significantimprovements in the incentive regime governing economic behavior in thetradables sector since 1983, although the pace of structural reform slowedsomewhat in 1986 for fiscal reasons (para. 61). In order to provide economicageats with clear pricing signals for investment and production decisions, aswell as reinforce perceived government credibility in the area of tradereform, the SAL would support continued import liberalization and exportpromotion.

26. External liability management represents a significant challenge inview of the impact of the formidable external debt burden on the Moroccaneconomy. The elaboration of a robust debt management system is clearlywarranted to monitor the complexities of the rescheduling arrangements of thepast, inform policy-makers as to the relative merits of differentrestructuring options, and enable the formulation of a strategy governingexternal debt policy in the future. In this vein, the SAL provides for theinstitutional reforms and technical assistance necessary for theimplementation of such a system.

27. Macro Links to Proaram Components. The interrelationship between thepolicy measures comprising each component of the adjustment progrem and themacroeconomic objectives is an important aspect of the SAL. Growth targetsare predicated on increases in efficiency and investment: the sectoralallocation of incremental capital formation is determinant, however, ifdistorted patterns of growth are to be avoided. To this effect, further tradeliberalization is necessary to provide the private sector with unAmbiguousindications as to the relative profitability of exports, particularly sincecapacity is likely to become an increasing constraint to buoyant export growthin the near future. Tax policy should be designed so as to minimizedistortions regarding the intersectoral allocation of investment. Publicinvestment plays a significant role in the adjustment program in view of itsstrong complementarity to private investment1L7.

28. Finally, policy measures should be internally consistent so as toensure that the processes of fiscal reform, trade liberalization, and raisingpublic investment do not work at cross purposes, with negative repercussionson macroeconomic equilibria. The increase in investment and the process ofimport liberalization could lead to a worsening of the current accountbalance, requiring compensatory action on the exchange rate. Regardingbut' etary balance, both the substitution of quantitative restrictionsby tariffs and the reduction in existing tax incentives will boost Treasuryrevenues. The increase in public investment, however, could exacerbate thebudget deficit, while the mobilization of the required additional financingwill confront the authorities with difficult choices. Whereas excessivereliance on monetary financing would be incompatible with the objective ofprice stability, unbridled recourse to fledgling capital markets could lead toa crowding-out of private investment, either through the cost or theavailability of credit. Furthermore, increasing reliance on non-inflationarysources of domestic finance could jeopardize budgetary equilibria in thefuture by an unsustainable increase in the burden of interest payments. Forexample, a rcenario whereby higher public debt leads to rises in interestrates which, in turn, result in larger interest payments and even higherlevels of public debt, would eventually culminate in an explosion of thebudget deficit.

29. Macroeconomic Consistency Analysis. In order to ensure internalconsistency between the structural measures to be supported under the SAL(Annex II) and the medium-term macroeconomic framework, a macroeconometric

1/ Analysis shows that private investment in Morocco, for example, may besubject to sharp declines in marginal productivity or even not materializeat all in the absence of matching infrastructure-related public investment.

-9-

model of the Mo,-occan economy was constructed. In view of its importance tothe policy dialogue, the model underpinning the macroeconomic analysis wastransferred to Morocco and technical staff trained in its use. These jointefforts served to ensure realism and inject an added degree of rigor in theelaboration of the Government's medium-term macroeconomic framework.Specific, desired outcomes of the SAL program, which have been developed inconsultation with the Bank. are discussed below in paragraphs 82 through 88.

30. The analysis, which has been designed to reflect the mnain objectivesof the adjustment program and aid in the assessment of the ex ting trade-offsand complementarities between policy instruments and targets, las three maincomponents. In the area of external trade, behavioral relationshipscharacterizing the export supply and demand of manufactured goods, as well asdisaggregate import demand decisions, were estimated. Import demand wasanalyxed in the context of a rationed consumer/producer model and, as such,can be used to simulate the impact of trade liberalization policy scenarios.In the area of private expenditure, the relative importance of factorsunderlying consumption and investment decisions was assessed. The privatecapital accumulation decision was found to depend on output, the cost ofcapital, credit availability, and the stock of public capital. While publiccapital is shown to have a strong complementarity effect on privateinvestment, the availability of credit affects only the dynamic adjustment ofinvestment. In the area of Public finance, Treasury revenues were shown to bea function of both income and import levels, with expenditures being set torespect fiscal objectives.

31. Particular emphasis was given to the macroeconomic impact offinancial choices. The amount of monetary financing compatible with a giveninflation target was assessed on the basis of an estimated money demandfunction. Domestic bond financing was determined residually. While recourseto monetary financing is shown to have a decided impact on inflation,exoessive reliance on domestic bond financing could lead to a significantcrowding-out of private investment. The path traced for the fiscal deficit(para. 86) takes these effects into account and is consistent with continuedlow rates of inflation, as well as the targeted levels of private investmentexpenditures.

The Pblicy Framework of the First Structural Adiustment Loan

Tax Policy and Administration

32. Progress to Date. The structural weaknesses in the Moroccan taxsystem have given rise to a steady reduction in tax pressure from 19.01 of GDPin 1983 to 16.8% in 1986. This trend has been mitigated to some extent byincreases in nonfiscal revenues, attributable by and large to the introductionin 1986 of a windfall tax on petroleum. The considerable proceeds from thislevy, which represented 13X of total Treasury revenues in 1986 and 2.72 ofGDP, more than offset the virtual dissipation of dividend payments and profittaxes from OCP (the state-owned phosphate company) to the Government,following the plunge in world phosphate demand.

33. The evolution of overall fiscal receipts nonetheless beliessignificant changes in the structure of revenues since 1983. Direct taxes on

- 10 -

personal income and corporate profits remained relatively stable in relationto GDP during the period 1983-86. The extension of various exemptions grantedunder the* investment and export codes forestalled any rise in the buoyancy ofprofit taxes, particularly since fiscal privileges were directed to the moredynamic sectors of the economy of late, namely agriculture, real estate,tourism, and certain export industries. Revenue from taxes on salaries andwages rose slightly as a proportion of GDP, owing to the progressivity of therate structure and the lack of adjustment of nominal rates in keeping withinflation, resulting in the phenomenon of so-called bracket creep.

34. Indirect taxes have been subject to significant structural reformsleading to wide fluctuations in revenue shares. For example, the reduction inthe special import tax rate (para. 58), as part of the overall efforts toattenuate the bias against exports, led to a decline in overall trade taxrevenues. However, this trend was cushioned to some extent by an increase inthe average effective customs duty rate, coincident with the elimination ofquantitative restrictions on goods at the upper range of the tariff schedule.The aggregate loss of trade tax revenues corresponds tc approximately onepercentage point of GDP.

35. Despite several increases in rates, domestic indirect taxes alsoexperienced a reduction in their share of GDP. On two occasions, the generalrate on the former domestic sales tax (TPS) was raised, from 152 to 17% in1982 and to 192 in 1984. After increasing from 5S in 1980-81 to 62 in1984-85, the ratio of sales tax revenues to GDP subsequently fell to 5.52 in1986. These results can be attributed to: (i) a decline in the tax base,owing to the fact that agriculture and exports, the two fastest growingsectors in the economy, where the incidence of exemption from indirecttaxation is relatively high; and (ii) transitional difficulties regarding thereplacement of the TPS by the value-added tax (VAT) in 1986. Reasons for theshortfall in revenues linked to the introduction of the VAT include: First,the generalization of tax credits were not fully offset by reductions inexemptions or increases in tax rates for certain products. Second, credits onexisting inventories were granted as a condition of the VAT being extended tothe wholesale level. Third, the time period during which tax credits could beclaimed was shortened, engendering a once-and-for-all loss in revenues.Initial revenue losses notwithstanding, the VAT led to a significantrationalization of the rate structure of indirect taxes, as the number ofrates was compressed from eleven to five.

36. Consumption tax proceeds also exhibited a downward trend resultingfrom the failure to adjust upwards most specific tax rates. The only item onwhich revenues increased was tobacco, insofar as government revenues are basedon a percentage of the total sales of the state-owned tobacco monopoly,corresponding in essence to an ad valorem rate. Revenues from all otherexcise taxes and registration fees decreased from 1.4% to 1.0% of GDP duringthe 1983-86 period.

37. Fiscal Reform. The program to be supported under the SAL iscomprised of a series of actions which seeks to: (i) increase the buoyancy ofthe fiscal system by broadening the tax base and reducing marginal rates;(ii) improve the allocative efficiency of the fiscal system, as well as taxincentives for productive investment; (iii) enhance the equity of the tax

- 11 -

structure; and (iv) raise collection rates by strengthening existinginstitutions and rationalizing tax administration efforts.

38. Considerable progress in the fiscal area will be achieved with thepromulgation of the 1988 budgetary law, which contains numerous measures toreform the current tax structure based on the recommendations of jointBank-IMF technical assistance missions. As part of the SAL, the modificationof the existing investment codes (para. 33) will rationalize the incentivesfor productive investment by limiting the duration and rate of existing fiscalexemptions and reducing intersectoral disparities in the tax code. Profit taxexonerations have decreased from ten to five years and the exemption rate from1001 to 50S for all sectors other than export-oriented industries. In thecase of the latter, the ten-year exemption has been curtailed, with the resultthat exporters will now be subject to taxes on half the profits earned fromthe sixth year on. As a result of these reforms, investors in less-developedregions and/or privileged sectors will witness a reduction in tax advantages,both in absolute terms and in relation to other sectors, which have benefitedfrom the reduction in the corporate tax rate (para. 39). Finally, fiscalexemptions on various state-owned banks, including the Central Bank, have beenrepealed.

39. The corporate tax rate on profits earned in 1987 was lowered from 48Sto 451, followed by a further decrease to 40S on all profits earned beginningin 1988 in the context of the SAL program. These reductions in rates havebeen matched by additional measures to broaden the tax base and ensure a moreequitable distribution of the fiscal burden. The minimum corporate taxliability rate, deductible from the actual tax liability of the firm, has beenraised from 4.51 to 81, whereas the national solidarity tax (PSN) rate hasincreased from 101 to 25% for those firms exempted from the corporate tax inaccordance with the privileges previously granted under the investment codes.Finally, the zero-bracket threshold applied to the personal income tax hasbeen raised from DR 6,000 to DH 8,400 in response to the fiscally regressiveimpact of inflation on low-income groups. This measure will result in animprovement in income distribution and an administrative simplification of thepersonal income tax regime in view of the elimination from the tax base of thelarge number of low-income taxpayers.

40. Important measures have also been taken as part of the SAL withrespect to indirect taxation. For example, exemptions from the VAT have beeneliminated on a number of products, leading to a widening of the indirect taxbase. In order to reduce dispersion, rates have been increased on certainitems such as coffee, rice, cattle feed. and transportation services. Excisetaxes, stamp duties, and registration fees have also been adjusted upward witha 7.51 increase in the average price of tobacco products.

41. In order to complete the final phase in the modernization of thefiscal system, the Government has presented the personal income tax reformbill to Parliament for ratification in October 1988 in accordance with theSAL. This reform replaces the current schedular system with a unified incometax schedule, which aggregates all sources of personal income and reduces thehighest marginal tax rates. Multiple taxation of dividends is to becircumscribed, the five existing tax rates on different sources of income areto be consolidated, and the rate structure is to be simplified. As a result

- 12 -

of these modifications, the number of taxpayers will be reduced, therebyfacilitating tax administration. The multiplicity of tax rates according toincome source, which characterized the previous system, was potentiallyregressive in nature and offered numerous possibilities for tax evasion to allbut salaried employees and wage earners. In contrast, the personal income taxreform should lead to a more equitable treatment of the individual taxpayer.

42. On the basis of a disaggregate analysis of these fiscal reform,government revenues are projected to increase significantly. VAT collectionsfrom January to August 1988 are already 232 higher than over the same periodIn the previous year. Wage and corporate tax proceeds should also exhibitgreater buoyancy, as witnessed by the projected increase with respect to GDPof nearly half a percentage point. Globally, fiscal revenues are expected togrow by over 132 in 1988 with the share of total government revenues in GDPrising from 21.91 in 1987 to 22.5S in 1988.

43. Institutional Reform of Tax Administration-'. Important measuresto improve domestic tax administration are being undertaken in parallel to thestructural reform of the fiscal system, so as to realise the expected yieldsof the latter. In order to standardize and strengthen corporate accountingvractices in Morocco, the Government would approve for presentation toParliament a draft law instituting a national chart of accounts to replace theone in effect since 1957, as well as a draft law regulating the accountingprofession. A functional reorganization of the tax department is beingundertaken and a training component formulated to enhance the quality of taxreturn audits, by fully exploiting the potential for cross-checkingdeclarations of VAT and corporate income tax liabilities. The hiring of aminimum of fifty new examiners per year over the period of the SAL programwill lead to an increase in the frequency of audits.

44. A series of actions is presently underway to reduce the potential fortax evasion. The structure of penalties applicable to late payments and taxfraud would be reinforced. Penalty interest will accrue from the time the taxliability originates, rather than at the time the violation is detected as inthe past. A unified taxpayer identification file would be established on thebasis of a national fiscal census, which should aid in tax enforcement. Inorder to simplify administration and reduce lags in tax collection, a study isbeing undertaken to examine the feasibility of advancing the due date for thesecond payment of the corporate income tax and amending the fiscal code, so asto mandAte that commercially-oriented transactions exceeding a certain amountbe settled by check. This will serve to limit the potential for evading VATpayments at the wholesale level.

The Public Investment Budget

45. Proaress to Date. Morocco entered the decade with an ambitious1981-85 Development Plan which targeted an annual GDP growth rate of 6.5%, tobe achieved primarily through a doubling of public investment. In response to

1/ Institutional support, technical assistance, and training programsunderpinning SAL reforms are proposed to be financed under a PublicAdministration Loan (PAL), described in Annex V.

- 13 -

the adverse economic conditions which characterized the early 1980s,government investment was curtailed to the point that real expendituresdeclined by over 501 between 1981 and 1986. While the adjustment andliberalization efforts undertaken by the Government since the 1983 crisissought and obtained a higher share of private investment in total gross fixedcapital formation (GFCF), rising from 12.9% in 1982 to 16.61 in 1986, thelevel of public investment has fallen below the minimum necessary to meet thedevelopment needs of the private sector and the social needs of thepopulation, particularly the economically disadvantaged.

46. The volume of the 1981-85 Plan, together with inappropriate projectselection criteria and the inadequate coordination of planning and budgetingprocesses, resulted in the programming of more public investment than existinginstitutional capacity and resource availability could support. In addition,the Government was unable to contain the growth of annual commitments on theinvestment budget. This led to delays in project execution, a deteriorationof the existing public capital stock, and a substantial buildup of paymentarrears to local contractors.

47. In response to these problems, the Government took a series ofactions beginning in I '5 with a view to realigning expenditures withavailable resources, and thereby improving the budgetary process. Specificmeasures undertaken include: (i) detailed annual reviews of the investmentprogram in consultation with the Bank, resulting in the postponement orelimination of most nonpriority or inadequately prepared projects;(ii) development of the capabilities to undertake sound economic and financialanalysis of investmnt projects, prior to their inclusion in either theDevelopment Plan or the annual budgetary law; and (iii) introduction of anannually modifiable investment plan.

48. The impact of these reforms is evident both in terms of projectselection and efficiency gains achieved in the area of investment budgetingand financial execution. One example of this is the improvement in the ratioof payment orders to authorizations from 301 in 1986 to 501 in 1987.Furthermore, the majority of projects contained in the 1988-92 DevelopmentPlan are of high priority and economically justified.

49. Despite the actions taken during the past few years to rationalizepublic investment expenditures and related budgetary procedures, there remainsome outstanding issues which, unless addressed, could compromise medium-termgrowth objectives. The relative scarcity of fiscal resources and thepersistence of government payment arrears have seriously slowed the completionof ongoing projects and virtually preclude undertaking new investment.Disbursements under externally-financed projects have been hampered for wantof local counterpart funds.

50. The inability to pay contractors in a timely manner for works carriedout has led, moreover, to an increase in project costs. Companies inflatetheir margins on government contracts in order to compensate for anticipatedpayment delays. At times, the situation has deteriorated to such an extentthat certain firms are no longer willing to bid on government contracts.Although the outstanding stock of arrears on the investment budget has beenreduced by over DR 1 billion in 1986-87, principally as a result of the issueof Treasury bonds to public enterprises, payment delays concerning capitalexpenditures now stand at four months.

- 14 -

51. The budgetary practice of cancelling and recommitting those budgetaryallocations which have not given rise to payment orders constitutes asignificant impediment to project execution. While justified in the past whena standardized budgetary nomenclature and computerized management informationsystem were lacking, this procedure has been found to complicate unnecessarilyinvestment planning in the technical ministries. At present, much of the worksundertaken in the previous year must await up to six months of interministerialbudgetary arbitrage before they are recommitted and authorized to continue.Between 50Q and 75% of all payment orders approved in 1987 in health (74.11),housing (65.7X), and education (55.3%) went towards the settlement of arrears;similarly, the share of recommitments in total commitments for these sectorsexhibited comparable rates. In contrast, these same ratios for totalproductive investment across sectors averaged 24.4% and 35.5% respectively.Thus, while the sectoral distribution of budgetary allocations may adequatelyreflect development priorities, budgetary execution has been otherwise.

52. There is presently an urgent need to ensure a level of publicinvestment in priority socioeconomic sectors consistent with overall growthand developmental objectives. In addition, the efficiency of publicinvestment programming and budgeting must be raised to support the timelyexecution of individual projects. In accordance with the growth-oriented,medium-term macroeconomic framework, the Government intends to: (i) maintaina minimum level of central government investment consistent with the targetedincrease in the share of public gross fixed capital formation in GDP from 3.51to 4.21 by 1991-92 (par"s. 27, 84); and (ii) strengthen the processes andprocedures of investment planning and budgeting in order to improve themanagement and efficiency of public investment expenditures. These measuresare expected to ensure both the availability of sufficient resources and thetimely execution of targeted high priority projects in key socioeconomicsectors.

53. The Target Investment Program (TIP). A targeted program of publicinvestment has been formulated by the Government in consultation with Bankstaff, on the basis of growth objectives, sectoral priorities, and identifiedprojects in the Plan. The SAL will focus primarily on projects carried out inthe context of the central budget, insofar as investments of the main publicenterprises and municipalities will be followed under other Bank operations.The annual evolution of the TIP in terms of project execution and financing,as well as changes in the relative share of the TIP with respect to relevantmacroeconomic aggregates, are presented in Table 1. The specific projects orsubsectoral programs contained in the TIP for 1988-89 have been identified andare acceptable to the Bank. Formulation of the annual TIP for the followingyears will take place in October, prior to the presentation of the draftbudgetary law to Parliament. The annual execution of the TIP in terms ofbudgetary commitments and expenditures will be monitored on a quarterly basisunder the SAL.

54. Reform of Budgetary Procedures. A sweeping reform of investmentbudgetary procedures has been initiated based on the recommendations of ajoint Bank-Fund technical assistance mission. Actions already underwayinclude the preparation of a new, harmonized budget nomenclature torationalize the classification of capital expenditures, the simplification ofbudgetary procedures to facilitate investment programming, the strengthening

- 15 -

of project evaluation capabilities in the Department of the Budget, and thecomputerization of budget management a"id control. Overall support for theimprovement of government expenditure policies is expected to be provided forunder the PAL. In contrast, the SAL focuses on those aspects of theinvestment budget and its management which underlie implementation andmonitoring arrangements for the TIP.

Table 1: PROJECTED EVOLUTION OF INVESTMENT(in percentages)

1987 1988 1989 1990 1991

Total Investment/GDP 19.1 19.9 20.5 20.7 21.6

Consolidated GovernmentIuvestment/GDP La 3.5 3.5 4.0 4.1 4.2

Target InvestmentProgram (TIP)/GDP 2.4 2.7 3.1 3.3 3.7

TIP/ConsolidatedGovernment Investment 69.6 77.1 77.5 80.5 88.1

Percentage Share in Cumulative IncreaseTotal TIP 1987-1990

Sectoral Distribution of TIP- Agriculture 32 31 30 30 46S- Public Works 38 39 37 34 41S- Transport 2 2 2 2 24S- Social Sectors /b 28 28 31 34 86%

/a Includes central government, municipalities, and social security./b Includes education, health, and housing.

55. In the context of the 1989 budget law, investment procedures would befurther modified to accelerate the currently protracted arbitrage of budgetaryresources which takes place early in the year between the Ministry of Financeand the spending ministries, so as to expedite project commitments. Inaddition, commitments of the previous year, which have not given rise topayment orders, would no longer require a formal reauthorization prior to thecontinuation of the corresponding works in the following year. To ensure thetimely flow of information between the Ministry of Finance and the spendingministries required for investment planning, the integration of budgetarymanagement systems through computer links to all relevant users would bedesigned in consultation with the Bank. Finally, the present arrangementregarding foreign exchange risk would be reviewed in consultation with the

- 16 -

Bank to mitigate future costs to the Treasury and facilitate financialplanning by beneficiaries and financial intermediaries utilizing foreign loans.

56. These improvements in procedures should give rise to considerableefficiency gains in the budgetary execution of public investments. A set ofperformance ratios in terms of budgetary authorizations, commitments, paymentorders, and disbursements has been established in the context of the SAL. Theadequate execution and financing of the target public investment programshould result in a gradual improvement in these performance ratios and aconcomitant reduction in payment delays from four months in 1987 to one andone-half months in 1989. In order to provide the Bank with the informationrequired for the timely monitoring of the investment budget, aninterministerial working group has been established for all SAL-relateddiscussions of public investment.

Trade and Industrial Policy

57. Progress to Date. A broad reform of the structure of incentives waslaunched in 1983 to correct the deep structural distortions which had hinderedthe performance of the Moroccan eConOmy. This program, supported by twoBank-financed Industrial and Trade Policy Adjustment (ITPA) loans, includedthe liberalization of the trade and industrial regime, the promotion ofexport-oriented activities, the adoption of a more flexible exchange ratepolicy, and the rationalization of domestic capital markets. Specificmeasures were taken in three major areas.

58. First, import restrictions were significantly reduced and theprohibited list of imports abolished, with the result that 89% of total importvalue and 66% of total tariff positions are no longer subject to licensing,compared to 381 and 50S respectively at end-1983. The maximum customs dutyrate was reduced from 4002 in 1983 to 451 in 1987 and the special import tax,an across-the-board, uniform surtax, declined from 151 to 51 over the sameperiod, although the latter was subsequently raised in the interest of fiscalexigencies (para. 61). These measures lowered the unweighted averagecumulative rate of trade taxes (inclusive of the stamp duty) to 35.91, downfrom 58.41, and the maxirum protective rate to 621, down from 466%. Thedispersion of rates was also reduced with the standard deviation decreasingfrom 40.5 to 15.4. Second, the export regime was considerably enhanced. Thetemporary admission scheme, the centerpiece of Morocco's export promotionefforts, was strengthened and extended to include indirect as well as directexporters. Virtually ell export licensing requirements were abolished and allexport taxes repealed. -the export credit scheme was improved by raisingceilings on pre-shipment financing and increasing maturities on post-shipmentfinancing. Fiscal and financial incentives embodied in the industrialinvestment and export codes were rationalized. Third, the simplification ofadministrative procedures has improved the flow of information and relaxedinstitutional constraints with respect to international trade transactions.This has led to a reduction in customs processing time by 501.

59. Analysis of the change in the structure of incentives reveals thatexternal trade flows have increased their share in GDP as a result of thereplacement of quantitative restrictions by tariffs; the decline in nominalprotection following the successive reductions in the tariff ceiling; and thefall in effective protection owing to the high concentration of finished

- 17 -

products in the upper echelons of the tariff range. Liberalization-inducedpolicy reforms have also resulted in a growing proportion of local industrybeing subject to increased competition from abroad. According to aproduction-weighted index of protection, for example, the share of domesticmanufacturing subject to QRs during the period 1983 to 1986 declined from 602to 401 and from 452 to 15S, as a function of tariff line and import valuerespectively. Various export promotion measures served to curtail thefinancial profitability premium of import-substituting activities relative toexports by a factor of nearly three, the premium declining from 501 to 201.The administrative co8sC of external trade also decreased, as illustrated bythe steady increase in the proportion of license requests approved (842 in1986) and the substantial reduction in processing time for applications.

60. The change in incentives has induced a number of significant shiftsin economic benavior since 1983. Buoyant export growth has sustained arelatively higher level of imports, leading to a more open economy asreflected in an increase in the ratio of external trade flows to GDP from 53Sin 1983 to 561 in 1986. The growth in exports could not be attributed to asurge in traditional exports insofar as the decline in the value of phosphaterock was only partially compensated by an increase in the export of phosphoricacid and fertilizer. Rather, robust growth of Moroccan manufactured exportsled to greater market penetration abroad. After stagnating at 1.51 during theperiod 1982-84, Moroccan manufactured exports as a percentage of EEC importsrose to 1.91 in 1986, a strong iadication of improved competitiveness. Therealignment of the wage-rental ratio in keeping with the relative abundance oflabor in the Moroccan economy underlay productivity gains in labor and capitalwhich have taken place in the manufacturing sector. The attenuation ofdistortions in factor prices also contributed to the rapid gains in the exportof labor-intensive goods, particularly once subcontracting activities weretaken into account.

61. Following the closing of ITPA II, the Government continued with thereform of the trade and industrial regime. Licensing requirements wereremoved on 335 tariff positions in August 1987, corresponding to approximately61 of domestic industrial production. Prompted by fiscal considerations, theGovernment replaced the SIT and the relatively distortionary stamp duty by a12.51 uniform import tax in January 1988 to mobilize additional revenues. Theoverall impact of these measures was a rise in the average trade tax rate ofabout two percentage pointa.V, accompanied by a significant compression inthe dispersion of nominal and, by extension, effective rates of protection.

62. Import Liberalization. Although considerable progress has beenachieved in reducing both the level and dispersion of effective prote4%tion,the present structure exhibits certain characteristics which indicate the needfor further reform. An analysis of QR and tariff coverage by end-use showsthat final goods continue to be more highly protected by both instruments thanare inputs, resulting in a cascading structure which reinforces rates of

1/ The average trade tax rate in 1988 (35.7X) is nonetheless significantlylower than that prevailing in 1983 (58.4X) at the onset of theliberalization program.

- 18 -

effective protection. For example, 67.52 of all consumer goods are subject toQRs, compared to 9.52 of intermediates and 17.5% of capital goods. Similarly,intermediates, capital goods, and consumer items had mean tax rates of 27.92,31.72, and 50.12 respectively on an unweighted basis in 1986, and 20.42,21.2%, and 26.52 when weighted by import value.

63. The growth objectives of the medium-term macroeconomic framework arebased, in part, on an increase in the level and marginal efficiency of privatesector capital formation. Whereas existing capacity has been adequate tosustain the manufactured export drive until now, utilization rates arepresently high and new investment is required if export potential is to befully realized in the future. To this effect, further reductions in theremaining quantitative restrictions are necessary to ensure that investmentdecisions, whether in import-substituting or export-oriented sectors, areconditioned by undistorted price signals. Only in this way will resources bechanneled into those productive sectors where Morocco enjoys a comparativeadvantage. A significant share of the latter, however, corresponds toindustries (e.g. textiles) where international trade is regulated on the basisof multilateral agreements.

64. As part of the ITPA program, quantitative restrictions have beeneliminated on product categories corresponding to 602 of domestic industrialproduction, indicating the extent of trade liberalization which has takenplace to date. While the share of domestic production subject to quantitativerestrictions is perhaps the most economically meaningful index of the extentof trade liberalization, Morocco's trade regime appears even more liberalizedin terms of the more traditional measure based on import weights. Subsequentto the ITPA reforms, only 102 of total import value is subject to quantitativecontrols. As part of the SAL, the Government abolished import licensingrequirements on preducts corresponding to 102 of industrial production, inorder to promote efficiency in the industrial sector and reduce the existinganti-export bias. The promulgation of the 1989 and 1990 liberalizationprograms should leave no more than about 152 of domestic production subject toimport licensing requirements, corresponding for the most part to productswhose trade is regulated by international agreement.

65. Safeguard Procedure. Since the onset of the liberalization programin 1983, the shift from quantitative controls to price restrictions has causedconcern among domestic producers and government officials that increasedimport flows could exert excessive pressures on certain industries,particularly in areas exposed to unfair trading practices from abroad. Thishas led to the introduction of reference prices on a limited number of itemswhen the amount of potential protection in the tariff structure was deemedinadequate. Reference prices are set in nominal dirhams and have yet to besubsequently raised on any item. Existing reference prices are limited toapproximately 300 tariff positions (out of 8,057) with concentration ratios of302 in ceramics, 102 in textiles, and less than 52 in paper, chemicals,electrical products, and metal works. The import coverage of reference pricesimposed since 1985 varies from about 952 in ceramics, 202 in textiles, and 52to 72 in paper and metal works. The transitory protection afforded byreference prices has eased adjustment pressures for politically sensitiveindustries and, as such, has served to retain political support for tradeliberalization in general.

- 19 -

66. The Government has recognized the need for a more formal procedurewhich is transparent, nondiscretionary, and reflects the national interestrather than the concerns of onc particular special interest group. Inconsultation with the Bank, the Moroccan authorities are preparing such aprocedure which allows for a limited amount of transitory protection,consistent with the overall national interest, without reintroducing thelevels of protection prevailing in the past. Specific features of thisprocedure are as follows: (i) representation of all concerned parties,including both users of the imported good, be they producers who import theitem as an intermediate input, or final consumers of the good, and producersof the import-competing good. Whereas the producer benefits from theintroduction of transitory protection, users are penalized by the artificialincrease in price; (ii) protection would be granted temporarily, in accordancewith Morocco's international commitments and the national interest; (iii) theinstitution(s) governing this procedure would prepare an annual report on thestate of protection and related costs and benefits to the national economy, inline with continued efforts to rationalize incentives.

67. As part of the SAL, the safeguard procedure will figure prominentlyin the law outlining the general principles of foreign trade activities whichthe Government intends to present to Parliament in 1989. This procedureshould enable trade liberalixation to proceed without jeopardizing theefficient development of the domestic economy. In addition, the adoption ofthe safeguard procedure will supplant the existing practice of referencepricing.

68. Tariff Simplification. An international comparison of Morocco'strade tax structure with those of immediate competitors and comparableeconomies underscores the need for further simplification. Most of the tariffreforms implemented to date have focused on the reduction of rates; however,the Moroccan tariff nomenclature is unduly driven by firm-specificconsiderations. This is particularly evident in the case of such consumergoods as foosd, beverages, tobacco, and textiles. The intricacy of theMoroccan tariff structure seems hardly justified in view of the fact thatother countries manage more complex foreign trade structures with fewer codes.

69. In order to correct these irregularities and induce greaterefficiency in the allocation of productive resources, the Government, in thecontext of the SAL, intends to simplify the existing tariff nomenclature withthe adoption of the International Harmonized System (IHS) on January 1, 1989.Those tariff positions which have not been used during the past five yearswould not automatically be integrated in the new tariff nomenclature. Thenumber of tariff positions would be consolidated at the eight-digit level withthe same rate being applied to like products. An action plan and timetablewill be established in early 1989 to reduce the number of tariff rates and toaggregate product categories from the eight to the six-digit level.

70. Export Promotion and Industrial Developrent. In tandem with the SALprogram, the Government intends to strengthen its efforts in the area ofexport promotion to sustain the impressive performance of exports ofmanufactured goods and services exhibited during the past few years. Theexport insurance agency, S AEX, would be provided with adequate budgetary

- 20 -

resources to cover normal commercial risk and empowered to act on behalf ofthe State in the case of political risk. Budgetary funding for the Center forthe Promotion of Moroccan Exports (CMPE) would be increased with the objectiveof identifying new markets abroad. A study would be carried out to identifyspecific policies and actions in support of industrial expansion and sustainedexport growth. Potential obstacles to external trade flows, identified in thereport of the Committee for the Simplification of Trade Procedures, would beaddressed with the objective of reducing customs processing time by one-half.In order to increase proceeds from tourism, price controls on four- andthree-star hotels were abolislaed in September 1988 and credit ceilings onmedium- and long-term loans to the hotel sector are to be removed beforeend-1988.

71. As part of the SAL, the Government has taken a series of significantmeasures to liberalize the exchange regime to attract both foreign directinvestment and worker remittances from abroad. Virtually all controls havebeen abrogated for resident and nonresident foreign investors ou foreignexchange and stock tranEactions. As such, foreign investors are empowered torepatriate up to the full amount of their initial investment, irrespective ofwhether a guarantee to this effect was granted at the outset. In addition,the purchaser of foreign-owned assets may now settle all foreign-exchangeobligations directly abroad. Prior authorization to repatriate theforeign-exchange equivalent of paid-in capital and profits has been abolishedand commercial banks can now be used to transfer funds directly to nonresidentaliens without going through the Exchange Bureau. Finally, the deregulationof exchange controls has been extended to include Moroccan nationals residingabroad, the latter being authorized to open convertible dirham accounts.

External Liability Management

72. Progress to Date. The rapid rise in Morocco's external indebtednesshas its roots in the late 1970s and largely reflects various adverse externaldevelopments and serious structural problems in the economy. Sharp increasesin oil prices, depressed conditions in the world phosphate market, and risinginternational interest rates undermined Morocco's ability to service itsexternal debt. In addition, an ambitious public investment program and aheavy buildup of defense expenditures were sustained through extensiverecourse to borrowing abroad. As a result, Morocco's total external debtreached about 86t of GDP by 1982, compared to only 371 in 1977. In 1983,Morocco found itself unable to meet its heavy debt service obligations. Inresponse, it sought the assistance of the IMF and the World Bank in puttingtogether a program of macroeconomic stabilization and structural adjustment.This allowed for a series of official and commercial bank debt reschedulings.The amount of payments rescheduled from end-1983 to end-1987 totaledUS$6.5 billion.

73. The profile of Morocco's external debt has improved since 1983,reflecting a slowdown in the contracting of new debt commitments. Inaddition, the compositional structure of new borrowings shifted fromcommercial to official sources which served to soften the average terms ofexternal liabilities. As such, the average interest rate on new commitmentsdeclined from 101 in 1982 to less than 61 in 1987, while the average maturity

- 21 -

increased from 11 years to approximately 20 years. This resulted in anincrease in the grant element from 5% to 282&'.

74. Despite the relief from its creditors, Morocco's total external debtposition remains precarious. At the end of 1987, the total external debtoutstanding and disbursed (DOD) was approximately US$20.6 billion or 11% ofGDP, while debt service payments absorbed 31.6S of exports of goods andservices, inclutiing workers remittances (Table 2). Before debt rescheduling,the debt-service ratio was 60.8%, of which 20.9% of exports accounted forinterest payments alone. In the absence of additional debt relief or anyother form of refinancing, the debt-service ratio would average an estimated47.3S a year during 1988-1990, equivalent to annual debt service payments ofUS$3.8 billion.

Table 2: EXTERNAL DEBT KEY INDICATORS

160t 1981 1982 1C63 194 19o5 194 1967.........................................................................................................

Totol It.nmIt DO (billIon) 1/ 9689.1 10.4 12410.0 139.4 139.0 16696.1 188.6 203.of tiich: PiAlic Odt 6739.1 9615.4 11119.0 12567.4 12707.3 1432.1 1746.6 19466.6

Privte Led" (iltion) 3649. 3694.3 4w23.6 36. 38)6.6 4059.1 48)0.1 4904.4Offietat ewns (bilion) 43.4 M591.1 69A.4 63.0 O6. 1131n.0 1204.4 1452.2

" IXt GofP 59.92 74.31 06.32 118.6S 127.02 134.7S 12212 115.02

Debt tevIce efore Oft (Iitten) 21 1314.7 1423 1S14.2 2063.8 19.3 2361.6 36. 3550.?As I of iSO's net workee rn 30.1$ 34.52 39.42 2.6 S0.6 56.72 7R.7X 60.81

det Service After OC (bmillion) 2V 314.7 143.3 1S14.2 1321.3 653.3 1224.6 1669.4 1166.?A6s X of SINs lnet wrkes r_ 30.12 34.52 39.42 33.71 21.72 29.42 3.43i 31.62

tnt Pewce Sefore St (llitten) 21 68.9 706.6 666.5 7755 79.3 774.1 1063.2 1220.5S X Of GUP 3.63 4.62 4.S2 5.68 6.71 652 7.21 7.32

A S d ofU Mel workers ro 14.9S 17.121 17.32 19.62 20.32 18.62 21.1X 20.92

Int Pwmft Aftor 0t (btlelo) 21 64.9 706.6 6.50 627.5 606.3 576.1 851.2 839.5eof cw 3.62 4.2 4.5 4.71 5.12 4.92 5.1S 5.02

t 2X f We inet Wkes ro 14.92 17.11 1V.32 16.02 15.51 13.62 16.91 14.41

Sacst INIIF. INf aff etimot

1V Inctufts NUL Sahrt-tenu Debt.21 Incltui ILt Debt except military debt.

19B0 1981 196 1910 1984 1985 1966 197T

AMtt ReshWeded a 0 0 742 1134 1135 1769 1704hAMti.tlO 0 0 0 594 945 937 1557 1323Intet0 0 0 148 189 198 212 381

1! During the period 1983-87, Bank lending played a major role in torocco'sadjustment efforts, accounting for about one-fourth of net externalfinancial flows (including int-irest reechedulings).

- 22 -

75. With the steady improvement in the external current account balanceachieved since 1983, Morocco transferred about 3% of its GDP abroad on a netbasis in 1986-87. Net transfers from Morocco are projected to reach between42 and 5% in 1988-89. Notwithstanding these substantial capital outflows andthe underlying repercussions for growth prospects, Morocco still requiressignificant amounts of financing to meet its debt service obligations and toensure an adequate expansion of public investment in key economic and socialsectorsL. Gross capital requirements in 1989-95 would average aboutUS$3 billion per year. More than one-third of this could be covered byrescheduling, although potential amounts forthcoming from conventionalrescheduling do not offer Morocco the relief it needs from its heavy debtburden-it would merely postpone the problem. The rest could be obtainedthrough fresh borrowing, preferably at softer terms, or through exceptionalfinancing in the form of grants. Assuming the necessary financing does notmaterialize from these sources, Morocco could explore other means, includingdebt conversion schemes, exit bonds, or exchange offers, as have beenundertaken by other heavily-indebted countries such as Mexico, Chile, and thePhilippines.

76. Debt Mana8ement System. The debt-servicing problems that continue toloom ahead despite multi-year reschedulings underscore the urgent need for theadoption of a solid debt mAnagement system. The most urgent aspect of debtmanagement consists of an effective system of approving, registering, andmonitoring all external borrowing. This would require institutionalarrangements covering: (i) the legal modalities for authorizing andregulating new borrowings; and (ii) the organization of the flow ofinformation on the contracting and disbursement of loans, and on payments ofprincipal and interest. These structural changes are required before any typeof data computerization is implemented.

77. Recognizing the need to improve the management of its externalindebtedness, the Government of Morocco has committed itself in the context ofthe SAL to the establishment of a debt management system which would allow fora more rigorous and reliable analysis of the country's debt profile. Under aplan of action formulated with Bank support, the Government, through theDepartment of the Treasury, would establish a system of data collection,compilation, and recording of all foreign debt1'. This would serve as thebasis for the Debt Data Computerization Project, which is being undertakenover an 18-month period that began in September 1988 with the support of thePAL.

78. The Department of the Treasury has been effective in monitoringdirect government debt. For public enterprise and publicly-guaranteed debt,however, gaps still exist due to weak control procedures. Privatenonguaranteed debt, though negligible, needs to be added to the system whileit is still within manageable proportions. Most of the necessary informationexists in the Exchange Bureau, but there is no mechanism in place to keeptrack of the evolution and status of private nonguaranteed borrowing.

1/ Detailed projections of external capital requirements in the context ofthe medium-term adjustment program are presented along with a feasiblefinancing plan in paras. 92-93.

2/ Includes public and publicly-guaranteed MLT debt, private nonguaranteedMLT debt, and public short-term debt.

- 23 -