For Investment Professionals only Investment case · 1 Investment case: The UK private rented...

4

1 1 Investment case: The UK private rented sector (PRS) Demographics and demand Demographic trends suggest that demand for housing will continue to rise. The UK population is expected to expand by around 0.5% per annum in the medium term (2017-2026) 2 – much faster than the European Union average of just 0.2%. 3 London is growing even faster. At the same time, household size is continuing to fall, with more people living alone. The government estimates that some 300,000 new homes need to be built annually. However, supply is lagging behind, with 217,350 homes built in the 2016/17 financial year. The resulting supply/demand imbalance means upwards pressure on house prices over the long run. Barriers to home ownership remain high, with significant affordability constraints (particularly in London). This is likely to fuel demand for rented accommodation – a sector which was dominated by private landlords. The PRS has been growing over the past decade, and – at 4.5 million households – now represents 20% of the English market, 4 up from 10% in 2001. In addition, a significant proportion now see themselves as permanent renters, with the 2015-16 English Housing Survey suggesting that only 60% of the PRS households surveyed expect to move into owner-occupation, with most only expecting to do so after five years or more. The rising demand for private rentals in the UK contrasts with the situation in continental Europe, where in many countries the sector is now fully mature and has stopped growing or is even shrinking. Indeed, in a report by the London School of Economics and the University of Cambridge, the UK was the only European country out of 11 studied where the general trend pointed to ongoing PRS growth. The value of an investment and the income from it can fall as well as rise and you may not get back the amount you originally invested. The UK PRS has doubled in size in the past decade and is increasingly attracting the attention of institutions including pension funds and insurers. There are now 95,918 Build-to-Rent homes complete, under construction or in planning across the UK. 1 We expect this figure to grow thanks to the sector's potential to generate a strong, stable income stream and proven diversification benefits. Our research suggests that the investment case for UK PRS is backed by: • Low correlations with commercial real estate, equities and bonds • Defensive characteristics with improved capital preservation • PRS is the fastest growing tenure type • A long-standing supply/demand imbalance in the UK housing market backed by strong population growth • Scope for professional investors to add value through active management and economies of scale 200 250 300 Housing need 150 100 50 0 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 20202021 Private enterprise Housing associations Local authorities Forecast completions Housing completions, England (’000s) Source: Department for Communities and Local Government (March 2017), JLL (November 2017), Autumn Budget 2017. Housing supply in England 1 Savills, British Property Federation. 2 ONS. 3 Eurostat. 4 English Housing Survey 2015-16. 80 70 60 50 40 30 20 10 0 1918 1928 1938 1948 1958 1968 1978 1988 1998 2008 2015-6 Tenure as a percentage of all households (%) Private renting Owner occupied Social renting Tenure over time (England) Source: English Housing Survey. For Investment Professionals only

Transcript of For Investment Professionals only Investment case · 1 Investment case: The UK private rented...

11

Investment case:The UK private rented sector (PRS)

Demographics and demand

Demographic trends suggest that demand for housing will continue to rise. The UK population is expected to expand by around 0.5% per annum in the medium term (2017-2026)2 – much faster than the European Union average of just 0.2%.3 London is growing even faster. At the same time, household size is continuing to fall, with more people living alone.

The government estimates that some 300,000 new homes need to be built annually. However, supply is lagging behind, with 217,350 homes built in the 2016/17 financial year.

The resulting supply/demand imbalance means upwards pressure on house prices over the long run. Barriers to home ownership remain high, with significant affordability constraints (particularly in London). This

is likely to fuel demand for rented accommodation – a sector which was dominated by private landlords.

The PRS has been growing over the past decade, and – at 4.5 million households – now represents 20% of the English market,4 up from 10% in 2001. In addition, a significant proportion now see themselves as permanent renters, with the 2015-16 English Housing Survey suggesting that only 60% of the PRS households surveyed expect to move into owner-occupation, with most only expecting to do so after five years or more.

The rising demand for private rentals in the UK contrasts with the situation in continental Europe, where in many countries the sector is now fully mature and has stopped growing or is even shrinking. Indeed, in a report by the London School of Economics and the University of Cambridge, the UK was the only European country out of 11 studied where the general trend pointed to ongoing PRS growth.

The value of an investment and the income from it can fall as well as rise and you may not get back the amount you originally invested.

The UK PRS has doubled in size in the past decade and is increasingly attracting the attention of institutions including pension funds and insurers.

There are now 95,918 Build-to-Rent homes complete, under construction or in planning across the UK.1 We expect this figure to grow thanks to the sector's potential to generate a strong, stable income stream and proven diversification benefits. Our research suggests that the investment case for UK PRS is backed by:

• Low correlations with commercial real estate, equities and bonds

• Defensive characteristics with improved capital preservation

• PRS is the fastest growing tenure type

• A long-standing supply/demand imbalance in the UK housing market backed by strong population growth

• Scope for professional investors to add value through active management and economies of scale

200

250

300 Housing need

150

100

50

02000 2002 2004 2006 2008 2010 2012 2014 2016 2018 20202021

Private enterprise Housing associations

Local authorities Forecast completions

Hou

sing

com

plet

ions

, Eng

land

(’00

0s)

Source: Department for Communities and Local Government (March 2017), JLL (November 2017), Autumn Budget 2017.

Housing supply in England

1Savills, British Property Federation. 2ONS. 3Eurostat. 4English Housing Survey 2015-16.

80

70

60

50

40

30

20

10

01918 1928 1938 1948 1958 1968 1978 1988 1998 2008 2015-6

Tenu

re a

s a p

erce

ntag

e of

all

hous

ehol

ds (%

)

Private renting Owner occupied Social renting

Tenure over time (England)

Source: English Housing Survey.

For Investment Professionals only

2

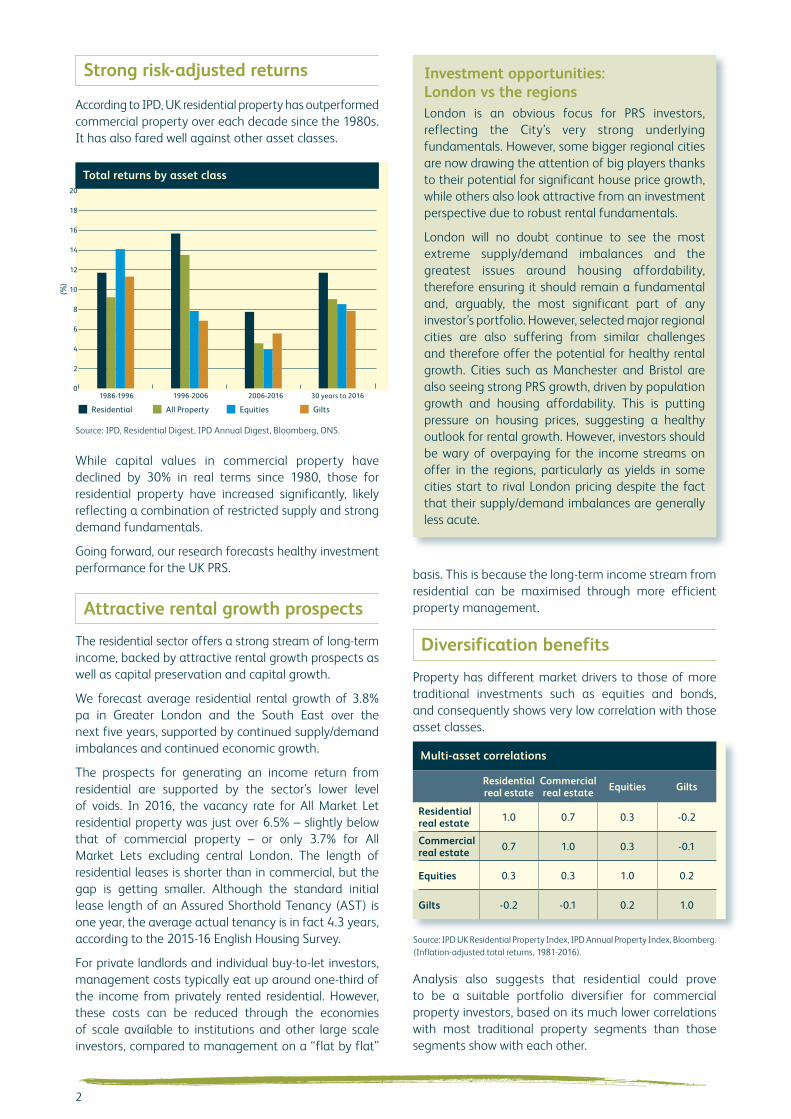

Strong risk-adjusted returns

According to IPD, UK residential property has outperformed commercial property over each decade since the 1980s. It has also fared well against other asset classes.

While capital values in commercial property have declined by 30% in real terms since 1980, those for residential property have increased significantly, likely reflecting a combination of restricted supply and strong demand fundamentals.

Going forward, our research forecasts healthy investment performance for the UK PRS.

Attractive rental growth prospects

The residential sector offers a strong stream of long-term income, backed by attractive rental growth prospects as well as capital preservation and capital growth.

We forecast average residential rental growth of 3.8% pa in Greater London and the South East over the next five years, supported by continued supply/demand imbalances and continued economic growth.

The prospects for generating an income return from residential are supported by the sector’s lower level of voids. In 2016, the vacancy rate for All Market Let residential property was just over 6.5% – slightly below that of commercial property – or only 3.7% for All Market Lets excluding central London. The length of residential leases is shorter than in commercial, but the gap is getting smaller. Although the standard initial lease length of an Assured Shorthold Tenancy (AST) is one year, the average actual tenancy is in fact 4.3 years, according to the 2015-16 English Housing Survey.

For private landlords and individual buy-to-let investors, management costs typically eat up around one-third of the income from privately rented residential. However, these costs can be reduced through the economies of scale available to institutions and other large scale investors, compared to management on a “flat by flat”

20

12

14

16

18

10

6

8

2

4

030 years to 20162006-20161996-20061986-1996

Residential All Property Equities Gilts

(%)

Source: IPD, Residential Digest, IPD Annual Digest, Bloomberg, ONS.

Total returns by asset class

Investment opportunities: London vs the regionsLondon is an obvious focus for PRS investors, reflecting the City’s very strong underlying fundamentals. However, some bigger regional cities are now drawing the attention of big players thanks to their potential for significant house price growth, while others also look attractive from an investment perspective due to robust rental fundamentals.

London will no doubt continue to see the most extreme supply/demand imbalances and the greatest issues around housing affordability, therefore ensuring it should remain a fundamental and, arguably, the most significant part of any investor’s portfolio. However, selected major regional cities are also suffering from similar challenges and therefore offer the potential for healthy rental growth. Cities such as Manchester and Bristol are also seeing strong PRS growth, driven by population growth and housing affordability. This is putting pressure on housing prices, suggesting a healthy outlook for rental growth. However, investors should be wary of overpaying for the income streams on offer in the regions, particularly as yields in some cities start to rival London pricing despite the fact that their supply/demand imbalances are generally less acute.

basis. This is because the long-term income stream from residential can be maximised through more efficient property management.

Diversification benefits

Property has different market drivers to those of more traditional investments such as equities and bonds, and consequently shows very low correlation with those asset classes.

Source: IPD UK Residential Property Index, IPD Annual Property Index, Bloomberg.(Inflation-adjusted total returns, 1981-2016).

Multi-asset correlations

Residential real estate

Commercial real estate Equities Gilts

Residential real estate 1.0 0.7 0.3 -0.2

Commercial real estate 0.7 1.0 0.3 -0.1

Equities 0.3 0.3 1.0 0.2

Gilts -0.2 -0.1 0.2 1.0

Analysis also suggests that residential could prove to be a suitable portfolio diversifier for commercial property investors, based on its much lower correlations with most traditional property segments than those segments show with each other.

3

Source: IPD UK Residential Property Index, IPD UK Annual Property Index.(Inflation-adjusted total returns, 1981-2016).

Intra-property correlations

Residential Retail Office Industrial

Residential 1.0 0.6 0.7 0.5

Retail 0.6 1.0 0.8 0.8

Office 0.7 0.8 1.0 0.9

Industrial 0.5 0.8 0.9 1.0

Adding residential property into a multi-asset or commercial property portfolio would therefore be expected to improve risk-adjusted returns.

Defensive characteristics

People always need somewhere to live. Therefore, if there is a downturn in the economy, the robust nature of the rental market is demonstrated as it counteracts the sales market when the economic environment encourages, or even obliges, people to rent. This potentially lessens capital decline for rented accommodation investments.

The statistical volatility of the commercial and residential property types has been similar over the past 30 years, which mainly reflects the upside volatility of residential property. However, when looking just at downside volatility (in this case, the risk of negative total returns), residential has actually shown a much lower level of risk than commercial. During the steep market downturns of the 1990s and 2000s, residential property recorded a smaller capital decline than commercial and also recovered its initial value faster.

Government support

In its White Paper, the government first signalled its growing awareness of the importance of the PRS as a tenure type and of Build to Rent (BTR) specifically, as opposed to traditional buy-to-let, as a way of creating better-quality, professionally-managed rented stock on a large scale. This shift away to a more multi-tenured view should help provide the impetus to boost housing supply in aggregate.

In the recent Budget, housing supply continued to be a high priority for the government and it built on foundations laid out by the Housing White Paper. A number of measures and solutions were announced to drive housing supply to an ambitious target of 300,000 homes per annum. Measures include extra funds to increase activity among small and medium housebuilders, unlock development opportunities through the provision of infrastructure, and for Help to Buy.

In particular, the government sought to proactively support BTR with £8 billion of new financial guarantees to drive private housebuilding in the sector. This should

both raise the profile and viability of BTR and institutional PRS in the short to medium term.

Purpose-built, efficient stockAchieving the necessary scale to make institutional investment viable is one of the prevailing barriers to entry for the PRS. While the equivalent US sector (known as multifamily) is mature, this took time to develop.

Brexit and the PRSAs Brexit negotiations are ongoing, the impact of exiting the EU on the economy and the property market is still far from certain, but this may benefit the PRS, in the short term at least. Since the referendum, housing transaction volumes have fallen (although they remain well above pre-Financial Crisis levels), as uncertainty deters households from making life-changing decisions, such as moving into owner-occupation.

With 29 March 2019 as the official date Britain is expected to exit the EU, further uncertainty is likely to persist. Ongoing lack of clarity over the future of the UK-EU relationship means the housing sales market will likely remain subdued for some time. Households will therefore likely stay in the PRS for longer than anticipated, underpinning rental growth.

The PRS is the key tenure for new and short-term migrants, so any fall in EU migration would subdue rental demand. However, 51% of migratory inflows come from outside of the EU and are unlikely to be affected by Brexit. Indeed, restrictions on the number of EU citizens who can work here may result in pressure to increase the number of non-EU international immigrants as UK employers seek to fill vacant roles. Moreover, the critical importance of EU migrants to the labour market should ensure that immigration will be allowed to continue, albeit to a lesser extent.

Any restriction on migration would be unlikely to cancel out the supply/demand imbalance, especially as lower housing demand would likely spark a similar reduction in activity from housing developers. So, while rental growth prospects may be relatively weaker post Brexit, the persistent supply-demand imbalance and the high levels of house prices relative to incomes will position the PRS as a key, and growing, tenure.

Forward-funding and forward-purchase offer an attractive route for large-scale investment in the sector, with housebuilders and developers increasingly open to such transactions. This is illustrated by the partnerships between M&G Real Estate and Crest Nicholson, and M&G Real Estate and Telford Homes, which have created much-needed PRS units across the UK.

By focusing on blocks and units designed specifically for rent and taking an active interest in the development of

For Investment Professionals only. This document is for investment professionals only and should not be passed to anyone else as further distribution might be restricted or illegal in certain jurisdictions. The distribution of this document does not constitute an offer or solicitation. Past performance is not a guide to future performance. The value of investments can fall as well as rise. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and you should ensure you understand the risk profile of the products or services you plan to purchase. This document is issued by M&G Investment Management Limited (except if noted otherwise below). The services and products provided by M&G Investment Management Limited are available only to investors who come within the category of the Professional Client as defined in the Financial Conduct Authority’s Handbook. They are not available to individual investors, who should not rely on this communication. Information given in this document has been obtained from, or based upon, sources believed by us to be reliable and accurate although M&G does not accept liability for the accuracy of the contents. M&G does not offer investment advice or make recommendations regarding investments. Opinions are subject to change without notice. In Australia, M&G Investment Management Limited does not hold an Australian financial services licence and is exempt from the requirement to hold one for the financial services it provides. M&G Investment Management Limited is regulated by the Financial Conduct Authority under the laws of the UK which differ from Australian laws. In Singapore, this document is issued by M&G Real Estate Asia Pte Ltd. This document may not be circulated or distributed, whether directly or indirectly, to persons in Singapore other than (i) an institutional investor pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “SFA”) or (ii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. M&G Investments and M&G Real Estate are business names of M&G Investment Management Limited and are used by other companies within the Prudential Group. M&G Investment Management Limited is registered in England and Wales under numbers 936683 with its registered office at Laurence Pountney Hill, London EC4R 0HH. M&G Investment Management Limited is authorised and regulated by the Financial Conduct Authority. M&G Real Estate Limited is registered in England and Wales under number 3852763 with its registered office at Laurence Pountney Hill, London EC4R 0HH. M&G Real Estate Limited forms part of the M&G Group of companies. M&G Investment Management Limited and M&G Real Estate Limited are indirect subsidiaries of Prudential plc of the United Kingdom. Prudential plc and its affiliated companies constitute one of the world’s leading financial services groups and is not affiliated in any manner with Prudential Financial, Inc, a company whose principal place of business is in the United States of America. NOV 17 / 246811

www.mandgrealestate.com

these products, experienced professional investors can ensure greater efficiencies for operation, energy and maintenance. Similarly, by ensuring consistency across developments, they can maximise economies of scale to reduce costs of repairs and enhance overall returns through greater customer satisfaction, which impacts occupancy.

The forward-funding route also offers greater tax efficiency than purchasing existing properties as the stamp duty land tax (SDLT) is based on the lower, pre-development land value.

Growth prospects in the institutional PRS are supported by the trends seen in the student accommodation sector. This has only very recently become a truly institutional market as developers started to provide the kind of stock investors want to add to their portfolios. As a result, the student accommodation sector saw investment volumes of c. £3 billion in 2016 alone according to Cushman & Wakefield. It is not hard to imagine a similar future for the PRS in the years to come.

Liquidity advantage

Liquidity is another potential advantage for residential property over its commercial counterpart. In commercial property, the only exit route is to sell a building to another investor. In a downturn where the large-scale investor interest falls away, it may therefore not be possible to sell a building (at least for a reasonable price) until market confidence returns, potentially years down the line.

Although the same problems may apply to selling a whole block of flats at some points in the economic cycle, residential property benefits from the potential to sell flats individually to smaller buy-to-let investors or owner-occupiers. This potential pool of investors likely far outweighs the number of institutions in any market.

Moreover, when selling to owner-occupiers, investors do not have to sell at investment value as they would to another investor, potentially enabling them to secure a higher price and thus boosting investment returns. This double exit route makes the PRS increasingly attractive as an investment as a result.

Conclusion

Overall, our research suggests that the investment case for UK residential is supported by the favourable demographic trends, the supply/demand imbalance in the housing market, and attractive rental growth prospects. The sector also offers diversification versus other asset classes and other real estate sectors, defensive characteristics and strong returns. Professional investors have the scope to further optimise returns through economies of scale and greater efficiency. Taken together, this makes a compelling case for investing in the UK PRS.

For more informationLucy WilliamsDirector, Institutional Business UK and Europe, Real Estate

+44 (0)20 7548 6585

Christopher Andrews, CFAHead of Client Relationships and Marketing, Real Estate

+65 6436 5331

Stefan CornelissenDirector, Institutional Business Benelux, Nordics and Switzerland

+31 (0)20 799 7680

Rehearsal Rooms, North Acton, London

![[On-Demand Webinar] Dual Income Investment Opportunities](https://static.fdocuments.us/doc/165x107/58ed28111a28ab440e8b4611/on-demand-webinar-dual-income-investment-opportunities.jpg)