FOR INTERNAL CIRCULATION

13

FOR INTERNAL CIRCULATION Grievances Redressal Policy Birla Sun Life Insurance Aaft^

Transcript of FOR INTERNAL CIRCULATION

FOR INTERNAL CIRCULATION

Grievances Redressal Policy

Birla Sun LifeInsurance

Aaft^

BSLI Grievances Redressal Policy

Complaints are an opportunity for an organization to understand or identify gaps in theprocess, product or communication and work towards process improvements and cementthe Company's relationship with dissatisfied customers . Complaint handling process is partof the customer care initiative:,

Regulation 5 of the Insurance Regulatory and Development Authority (Protection ofPolicyholders' Interests ) Regulations , 2002 prescribes that every insurer shall have in placeproper procedures and effective mechanism to address complaints /grievances ofpolicyholders efficiently and with speed.

The purpose of this Grievance Redressal Policy (hereafter referred to as the 'Policy') is to setforth the policies and procedures to be followed in receiving, handling and responding toany complaint against BSLI ("the Company"). This process encompasses complaints relatingto all products issued by the Company and/or solicited by its agents or independentbrokers. Products in this Policy will be referred to as "policies", which encompasses all lifeinsurance policies sold by the Company.

Further, it is the Company's guiding principle to provide prompt and fair resolution ofcustomer complaints in accordance with all legal and regulatory guidelines. It is imperativethat the policies and procedures outlined in this Policy be fully understood and diligentlyfollowed by all employees, agents, independent brokers, and managerial personnel engagedin the Company's customer complaint handling process.

Phis Policy will be updated periodically . Any questions concerning this Policy should bedirected to:

Compliance

Birla Sun Life Insurance CompanyOne India Bulls Centre, Tower 1, 15th Floor,Jupiter Mill Compound, Elphinstone Road,Mumbai - 400 013

.Uarclr 2010 Prepared by BSLI

I er.cirur ,i /

BSLI Grievances Rcdlressal I'olirv

DUINIT1ONS

Complaint

Includes any documented verbal or written statement (including a-mails and faxes) from a

client or any person acting on behalf of a client which alleges a grievance involving thedesign, performance, underwriting, administration, claim settlement of a BSLI product or

the activities of any employee/agent/broker of the Company in connection with theirsolicitation or execution of any transaction or disposition of a client's funds. A complaint is

an unpleasant customer experience with any of BSLI's touch points leading todissatisfaction.

Complaints can be classified as:

1. Functional : Direct Sales Force, Group Business , Third Party Distribution , Underwriting,Client Services, Actuarial, Finance and Planning, etc.

2. Internal:

• Complaints received fromo Insurance Advisor (IA)o Corporate Agent (CA)o Broker

• The complaint could be regarding some dissatisfaction about sales practice(s) of theCompany, delay/wrong commission received by the IA/CA/Broker, allegedrebating by another IA/CA/Broker, misconduct or fraudulent act by the medicalexaminer/laboratories/any sales intermediary and/or any other market misconduct

3. External:• Complaints received from:

ooo

Prospects / policyholdersRegulatory/ statutory body / OmbudsmanMedia/ advertising forum/ policyholder forum

• Includes cases pertaining to any delay in delivery/ non-receipt of policy documents,delay in resolving queries/ complaints, delays/ repudiation of claims , non-adherenceto service standards , misconduct of IA/CA /Broker, etc.

Insurance advisorAs per Section 2(10) of the Insurance Act, 1938, an "Insurance Advisor" means any personlicensed under Section 42 of the said Act to solicit and procure insurance business, includingbusiness relating to the continuance, renewal or revival of policies of insurance, and receivesremuneration by way of commission or other remuneration for the business thus solicited orprocured

March 20/0 Prepared by BSLI 3I'ersion .,/

BSLI Grievances Redressal Policy

Intermediary and Insurance IntermediarySection 2(1013) of the Insurance Act, 1938, read with Section 2(1)(f) of the InsuranceRegulatory & Development Authority Act, 1999, states that "intermediary and insuranceintermediary" includes insurance brokers, reinsurance brokers, insurance consultants,surveyors and loss assessors

Corporate Agent

Regulation 2(t) read with Regulation 2(k) of the Insurance Regulatory and DevelopmentAuthority (Licensing of Corporate Agents) Regulations, 2002, defines a "Corporate Agent" asany person licensed to act as such;"Person" means a:

• Firm; or

• Company formed under the Companies Act, 1956, and includes a banking company asdefined in Section 2(4A) of the above Act; or

• Corresponding new bank as defined under Clause 5(1)(d)(a) of the Banking RegulationAct, 1949 (X of 1949); or

• Regional Rural Bank established under the Regional Rural Bank Act, 1976; or• Cooperative society, including a cooperative bank or a co-operative federation, registered

under the Co-operative Societies Act, 1912, or under the laws applicable in the respective

State; or

• Panchayat or local authority

Corporate Insurance ExecutiveAs per Regulation 2(g) of the Insurance Regulatory and Development Authority (Licensingof Corporate Agents) Regulations, 2002, a "Corporate Insurance Advisor" in case of acompany or a partnership firm means any director or a partner or one or more of itsofficers/employees so designated by it, and, in case of any other person, the chief executive(by any name called) or any of the employee(s) designated by him who have the requisiteknowledge & training & have passed the exam as required under Section 42 of the InsuranceAct, 1938

BrokersAs per Regulation 2(1)(i) of Insurance Regulatory and Development Authority (Insurance

Brokers) Regulations, 2002, "Insurance brokers" means a person who for a remunerationarranges insurance contracts with insurance/ reinsurance companies on behalf of clients and

to whom a license has been granted by the Authority under Regulation 11 of the said

Regulations to act as an insurance broker

Ilu, r!, 'n l u Prepared by BSLI 4

BSLI Grievances Redressal Policy

rJ&

There is a thin line between a customer complaint and an inquiry/request.

'Inquiry ' is defined as any communication from a customer for the primary purpose ofrequesting for information.

'Request ' is any communication from a customer soliciting a change/ modification in thepolicy.

'Complaint'• Is a communication or expression of dissatisfaction• May be received either verbally or in writing• Expresses a grievance from or on behalf of a customer• Could be against any business practice followed by the Company or sales conduct of its

agents/representatives/insurance intermediaries• Is reviewed and dealt with at least one level 'higher' than the level which routinely

handles and makes operational decisions about the subject matter of a complaint• Can encompass anything that does not fall in either Inquiry or Request

'Complaint' versus 'Inquiry'/'Request'A 'complaint' needs to be clearly differentiated from 'inquirv'/'request'. Not every contactby a customer/ policyholder questioning an action of the Company will constitute acomplaint. Differentiating a complaint from an inquiry/request involves a reasonableapplication of judgment. The distinguishing factor should be the tone of the communicationand it reasonable interpretation of it. If the tone is critical and the customer sounds unhappyor displeased about something, the communication should be treated as a'complaint'.

A complaint includes allegations of some form of mis-selling, non-delivery of the policy,churning/twisting, failure to properly advise, misrepresentation or unsuitability of theproduct, delays in processing any client request like address change/premiumpayment/change in policy features, etc.

or,

The various types of complaints are -1. Reportable complaints2. Multiple complaints

3. Creeping complaints

;Ilarclt 2010 Prepared by BSI.I

I crsiotr ri /

BSLI Grievances Redressal I'olicv

As,

3. 'Creeping complaint'• Means a complaint repeatedly reported by the same complainant and where the

primary issue remains unchanged• Complaints re-lodged by the same complainant for a matter that has been resolved

and closed can also be termed as a creeping complaint• I'hese complaints are to be reported only once in the complaints database

COUftA 7'S CAN U R .'DRDID AT W1. Call Centre2. Customer can call at 1-800-270-7000 between 9:00am to 9:00pm (Monday to Friday) and

register their complaints. The call centre executive are also trained to resolve complaintsover the phone by themselves

3. Website4. BSLI website www.birlasunlife.com provides an option to the customer to log his

Grievance on the internet5. Branch6. BSLI has 600 plus branches spread across pan India. The customer can visit and register

his complaint at any of these branches7. Advisor

8. Customer gives his complaint to his servicing Advisor for resolution9. Corporate Agents10. Customer registers his complaint with his Corporate Agent for resolution11. Regulatory Bodies (Ombudsman/ IRDA)12. In-case if the customer does not receive a satisfactory or a timely response from BSLI;

customer has the option to report his complaint with the Regulators

The above list is only illustrative and not comprehensive

MODE OF R TS3 Letters.

3 Emails,

3 Telephonic Calls

3 Facsimile (Fax)

3 Walk-ins

11arch 20/0I *ersian /

Prepared by BSLI

BSLI Grievances Redressal Policy

1`,

SCOPE, OF GRIEVANCE REDR I„ Ic

1) Complaints that would be required to be immediately reported to Compliance are asfollows:• Complaints pertaining to the sales conduct of agents, brokers and other sales

intermediaries such as -o Missellingo Misrepresentationo Rebatingo Misappropriation of fundso Fraudo Forgeryo Lack of serviceo Thefto Commission schemes/sharingo Fictitious policies

• Employee fraud• Vendor fraud• Administration, control, coordination and reporting of customer complaints received

through Regulatory agencies• Allegations of financial irregularities by any person who has a responsibility within

the Company and that involves money, credit or any other property of the Companyor its clients

• Any complaint where there is a stated or implied threat of litigation• Any other matter as may be defined by Compliance from time to time

2) Compliance will also be responsible for the following:• Ensuring the recording & maintenance of the above complaints• Reporting of the above complaints to the Company's Management (Audit

Committee/Regulatory Committee) and the JV partner Sun Life• Maintenance of & responding to IRDA inquiries requesting information on

brokers/sales practices• Statistical customer complaint analysis

Please Note:

1) Compliance function should be sent a copy of all complaints involving any salesintermediary (like Agent, Broker, etc.) as well as an employee

2) The BSLI Compliance team investigates fraud and irregularities by any associate, agentor independent broker that falls within the above points

Alarch 2(1I0 Prepared by BSLI

l'er.vion r^ I

BSLI Grievances Redressal Policy

Complaints which are handled by Customer Service are primarily where thecustomer has expressed his dissatisfaction towards the services provided by BSLI

Listed are a few complaints which are received by Customer Service(below is not an exhaustive list)

.

Changes in not affected in the policy contractPolicy contract not received

Error in policy contract

Surrender amount not received

Revival of policy not affected

Nomination not affected

TT'T`LbS INVOLVED

Resolution of complaints requires involvement of each function, branch and corporate agentto support with investigations & follow-ups for complaints received against them andprovide satisfactory and timely resolution to the customer

Resolution of the complaints are informed to the customer by means of written (letter or e-mail)

9Alarch 1010 Prepared by BSLI

I "erstoo r /

BSLI Grievances Redressal Policy

SINCIFIC GUlDIEUNES

1) Media

• In the event or any probability of a complaint being reported in the media, the FCC orthe Functional I lead (Marketing & Communication) as well as Compliance should beinformed by the concerned FCC/person within 1 day

2) Complaints to Senior Company Officials

• Complaints alleging theft and complaints directly addressed to the senior companyofficials have to be directly sent to the Compliance Function

• The Compliance Function would decide on the appropriate course of action i.e. eitheran investigation or handing over the responsibility of resolving the complaint to therespective function

0., I 3) Market Conduct issues

• Complaints alleging theft , fraud or any other type of market misconduct should beinvestigated from a market conduct perspective and under utmost confidentiality

• Such complaints should be intimated to Compliance Function within 1 day ofreceiving the same

• Compliance Function shall ensure that the alleged misconduct of IA/CA/ Broker isinvestigated fully through the concerned function

4) Regulatory/Forum complaints

• Complaints received from regulatory/ statutory authority(ies) or from anymedia/ advertising/ policyholder forums should be forwarded to Compliance within

one working day of receiving the same, as given under the 'Workflow of Complaints'mentioned above.

5) Policyholder Grievance Redressal Committee (PGRC)

• l'GRC is a Committee (chaired by an independent consultant) formed to address thegrievances of policyholders in the following scenarios:o Misselling/ Misrepresentationo Lapse in BSLI process(es)o Out of Free Look Caseso Alleged fraud/ forgery/misappropriation /rebating complaints on a case to case

basiso Anv other case at the discretion of Compliance

• Please refer to the latest version of the PGRC Process Note for more details

Alurch 21110 Prepared by BSLI /0

1 'ersion '^ /

BSLI Grievances Redressal Policy

6) Policyholder's Protection Committee (I'PC)

• As per Corporate Governance Guidelines, dated 05th August 2009, issued by theInsurance Regulatory and Development Authority [IRDA] constitution of"Policyholders' Protection Committee" (PI'C) is mandatory.

• Hence, BSI.I has constituted the PPC vide the Secretarial Department's PPC Charter.• The Compliance team may contribute to the Agenda of the 1'PC meetings as & when

required. Similarly, the Compliance team will also have access to the PPC minutes.

REVIEW OF GRIEVANCE RFURR AL MUCY

The review of the Grievance Redressal policy will be conducted:• Atleast annually• As & when necessitated due to requirements under any regulatory/ governmental

authority or JV partners or BSLI Management.

OTHER REMEAIEAE ARSE AVAILAItLE UNDER THE LAW

1) Redressal of Public Grievances Rules, 1998 : Insurance Ombudsman

Every complainant has the right to complain/appeal against anyrecommendation/ resolution of BSLI to a higher external authority hereinafter referred toas the 'ombudsman'.

Any person who has a grievance against an insurer may himself or through his legalheirs make a complaint in writing to the Ombudsman within whose jurisdiction thebranch or office of the insurer complained against is located or to the Ombudsmanwithin whose jurisdiction the complainant resides, at the option of the complainant.

Activities of the Ombudsman are governed by the Redressal of Public Grievances Rules,1998 and modifications made thereto from time to time. A list of Offices of InsuranceOmbudsman, as specified by the Governing Body of Insurance Council (GBIC) inDecember 2009 attached herewith as Annexure 2.

No complaint to the Ombudsman shall lie unless:• The complainant had before making a complaint to the Ombudsman made a written

representation to the insurer named in the complaint and the insurer had:o Rejected the complaint, oro Complainant had not received any reply within one month after the insurer

concerned received his representation; oro The complainant is not satisfied with the reply given to him by the insurer

• The complaint is made not later than one year after the Insurer had rejected therepresentation or sent his final reply on the representation of the complainant;

I Larch 2010 Prepared by BSLI I II 'rrsioT :11

BSLI Grievances Redressal Policy

• The complaint is not on the same subject matter for which any proceedings beforeany Court or Consumer Forum or Arbitrator is pending or was so earlier.

The Ombudsman has the power to hear the following type of complaints:1) Any partial/ total repudiation of claims by an insurer2) Dispute pertaining to the premium paid / payable in terms of the policy3) Disputes concerning the legal construction of polities in claims related cases4) Delay in claim settlement5) Non- issuance of policy document to clients after receipt of premiums

2) The Consumer Protection Act, 1986

The Consumer Protection Act, 1986, is also applicable to the insurance sector. Aconsumer or any beneficiary of insurance can file a 'complaint ' under The ConsumerProtection Act, 1986, in case the service provided to him by the insuranceadvisor/ corporate agents/broker/ insurer suffers from deficiencies in any respect.

Consumer Disputes Redressal Agencies:

1) District Forum:

• Established by the respective State Government in each district of the State• Jurisdiction: complaints where value of services and compensation, if any,

claimed does not exceed rupees twenty lakhs2) State Commission:

• Established in each state• Jurisdiction:

o Complaints where value of services and compensation, if any, claimed exceedsrupees twenty lakhs but does not exceed rupees one crore;

o Appeals against the orders of any District Forum within the State; ando Where it appears to the State Commission that any District Forum within the

State has exercised its jurisdiction illegally or with material irregularity in anyconsumer dispute which is pending or has been decided by that DistrictForum

3) National Commission:• Established at the national level• Jurisdiction:

o Complaints where value of services and compensation, if any, claimed exceedsrupees one crore;

o Appeals against the orders of any State Commissiono Where it appears to the National Commission that any State Commission has

exercised its jurisdiction illegally or with material irregularity in any consumerdispute which is pending or has been decided by that State Commission

Please Note: All appeals against the orders of the National Commission to befiled with the Supreme Court

I/arch 20/0 Prepared by BS1.1 12

'crsion 71 /

BSLI Grievances Redress al Policy

The client or his legal heirs need to follow the hierarchy of escalations for complaints asgiven below:

Consumer Disputes Redressal Agencies

State Commission

Prepared by BSLI 13March 2010I'cr.ciun --/

BSLI Grievances Redressal I'olicv

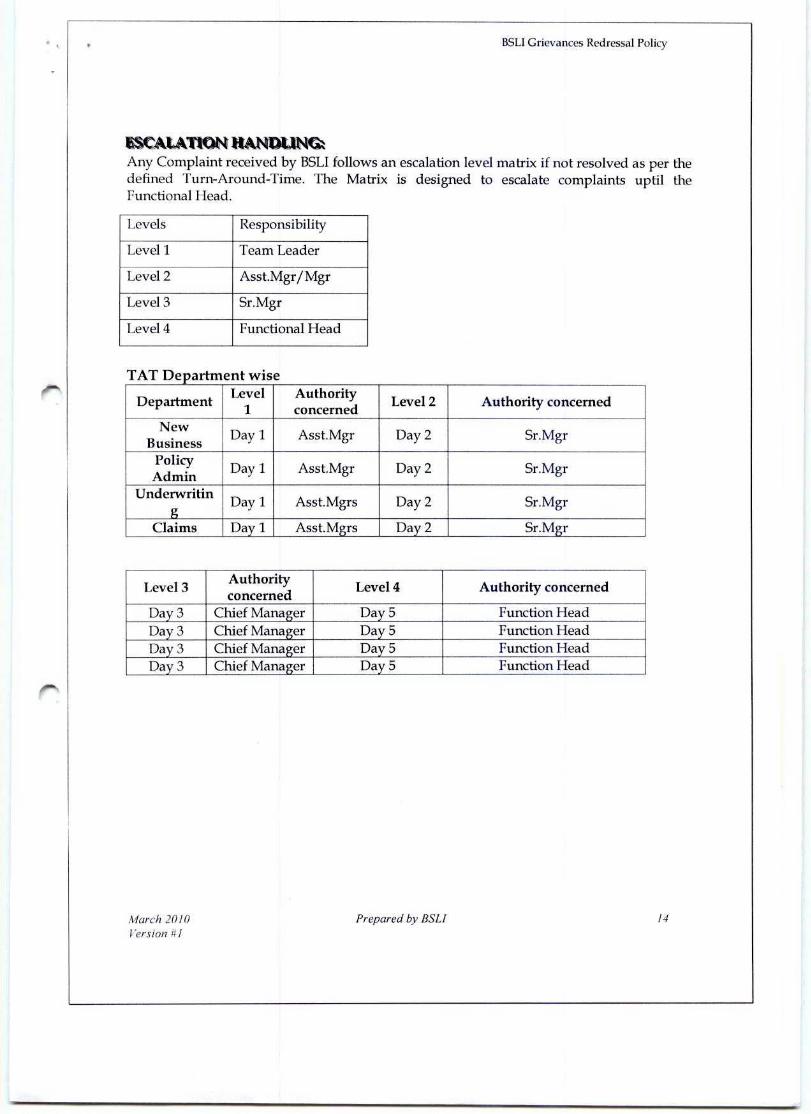

LAT NDUAny Complaint received by BSLI follows an escalation level matrix if not resolved as per thedefined Turn-Around-Time. The Matrix is designed to escalate complaints uptil theFunctional Head.

Levels Responsibility

Level 1

Level 2

Team Leader

Asst. Mgr/Mgr

Level 3 Sr.Mgr

Level 4 Functional Head

TAT Department wise

Department Level1

Authority

concernedLevel 2 Authority concerned

NewBusiness

Day 1 Asst.Mgr Day 2 Sr.Mgr

PolicyAdmin

Day 1 Asst.Mgr Day 2 Sr.Mgr

UnderwritinDay I Asst.Mgrs Day 2 Sr.Mgr

$_Claims Day 1 Asst.Mgrs Day 2 Sr.Mgr

Level 3Authorityconcerned

Level 4 Authority concerned

Day 3 Chief Manager Day 5 Function HeadDay3 Chief Manager Day 5 Function I lead _Day 3 Chief Manager Day 5 Function Head

Day 3 Chief Manager Day 5 Function I lead

Prepared by 13SLI 14Alarch 2010

I ersion +:1