Fomc 20071031 Material

20

Appendix 1: Materials used by Mr. Dudley October 30-31, 2007 143 of 162 Authorized for Public Release

-

Upload

fraser-federal-reserve-archive -

Category

Documents

-

view

214 -

download

0

Transcript of Fomc 20071031 Material

Appendix 1: Materials used by Mr. Dudley

October 30-31, 2007 143 of 162Authorized for Public Release

0

20

40

60

80

100

120

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

Price

0

20

40

60

80

100

120Price

BBB-

BBB

A

AA

AAA

S&P Ratings Downgrade: 10/17 and 10/19

ABX P rices for 07-01 Tranches

Source: JP Morgan

(1) Lower Rated ABX Tranches Keep Falling January 1, 2007 – October 26, 2007

800850900950

10001050110011501200

Jan-07 Feb-07 Mar-07 Apr-07 May-07 Jun-07 Aug-07 Sep-07 Oct-07

$ Billions

4.504.755.005.255.505.756.006.256.50

Percent

Total Outstanding Volume (LHS)Average 30-Day Rate (RHS)Average Overnight Rate (RHS)

FOM C Rate Cut: 9/18

Source: Federal Reserve Board

(2) Outstanding ABCP Volume Contraction Slows January 1, 2007 – October 24, 2007

-200

20406080

100120140160

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

BPS

-20020406080100120140160BPS

Secured CP - Unsecured CP

Secured CP - One Month OIS

(3) Secured CP Rate Spreads Narrow January 1, 2007 – October 26, 2007

Source: Federal Reserve Board

Class II FOMC – Restricted FR Page 1 of 10

October 30-31, 2007 144 of 162Authorized for Public Release

0

5

10

15

20

25

30

35

1/5 1/26 2/16 3/9 3/30 4/20 5/11 6/1 6/22 7/13 8/3 8/24 9/14 10/5 10/26Week Ending

$ Billions

Investment Grade

High-Yield

(4) High Yield Issuance Recovering January 2007 – October 2007

Source: Bloomberg

0

10

20

30

40

50

Jan-06 Mar-06 May-06 Jul-06 Sep-06 Nov-06 Jan-07 Mar-07 May-07 Jul-07 Sep-07

60$ Billions

CLOCDO

Source: Merrill Lynch

(5) CLO Issuance Picks Up, While CDO Issuance Remains Depressed January 2006 – October 2007

Class II FOMC – Restricted FR

5.50

5.75

6.00

6.25

6.50

6.75

7.00

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/075.50

5.75

6.00

6.25

6.50

6.75

7.00

7.25Percent

7.25Percent

Jumbo Mortgage Rates

Conforming Mortgage Rates

FOM C Rate Cut:

9/18

Source: Bloomberg

(6) Spread between Jumbo and Conforming Mortgage Rates Has Narrowed Somewhat January 1, 2007 – October 26, 2007

*Data for October 2007 includes issuance until 10/22/2007

Page 2 of 10

October 30-31, 2007 145 of 162Authorized for Public Release

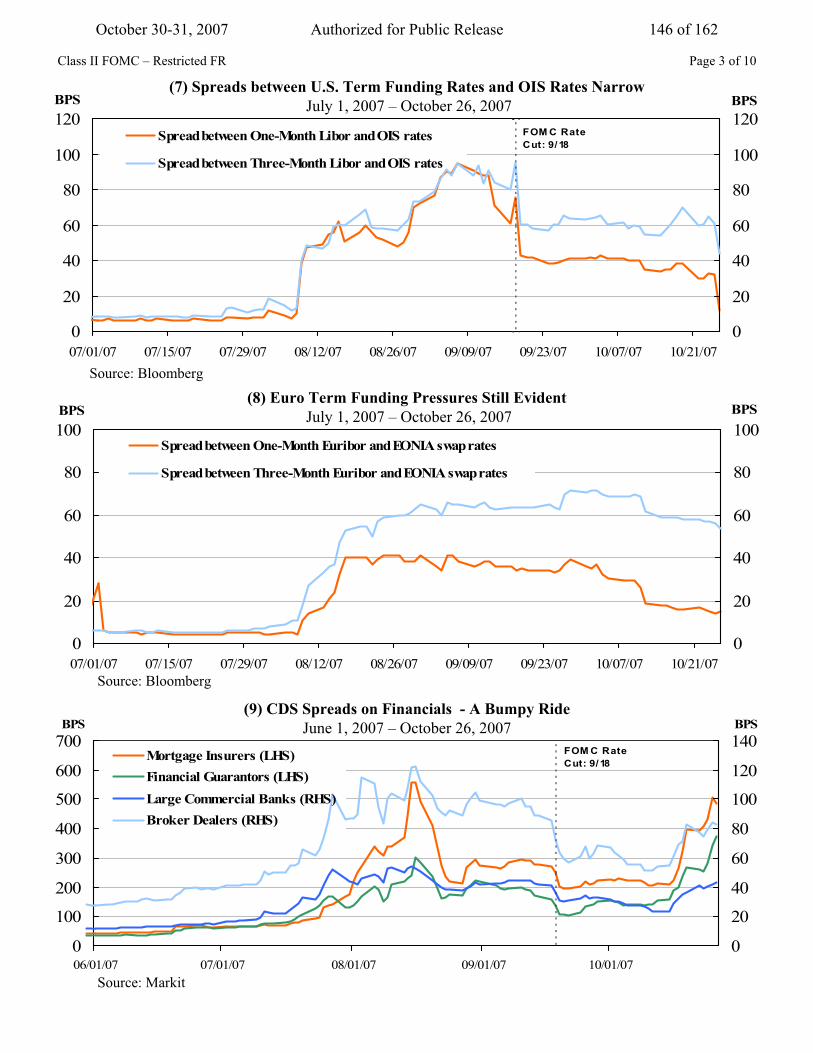

0

100

200

300

400

500

600

700

06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

BPS

0

20

40

60

80

100

120

140BPS

Mortgage Insurers (LHS)Financial Guarantors (LHS)Large Commercial Banks (RHS)Broker Dealers (RHS)

FOM C Rate Cut: 9/18

(9) CDS Spreads on Financials - A Bumpy RideJune 1, 2007 – October 26, 2007

Source: Markit

Class II FOMC – Restricted FR Page 3 of 10

0

20

40

60

80

100

120

07/01/07 07/15/07 07/29/07 08/12/07 08/26/07 09/09/07 09/23/07 10/07/07 10/21/07

BPS

0

20

40

60

80

100

120BPS

Spread between One-Month Libor and OIS rates

Spread between Three-Month Libor and OIS rates

FOM C Rate Cut: 9/18

(7) Spreads between U.S. Term Funding Rates and OIS Rates NarrowJuly 1, 2007 – October 26, 2007

Source: Bloomberg

0

20

40

60

80

100

07/01/07 07/15/07 07/29/07 08/12/07 08/26/07 09/09/07 09/23/07 10/07/07 10/21/07

BPS

0

20

40

60

80

100BPS

Spread between One-Month Euribor and EONIA swap rates

Spread between Three-Month Euribor and EONIA swap rates

(8) Euro Term Funding Pressures Still Evident July 1, 2007 – October 26, 2007

Source: Bloomberg

October 30-31, 2007 146 of 162Authorized for Public Release

100

200

300

400

500

600

03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

BPS

100

200

300

400

500

600BPS

ITRAXX Crossover Series 7

LCDX

FOM C Rate Cut: 9/18

(10) Global Credit Default Swap SpreadsMarch 1, 2007 – October 26, 2007

Source: Bloomberg

95

100

105

110

115

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/0795

100

105

110

115

120Index to 100 on 1/1

120 Index to 100 on 1/1

S&P 500NasdaqRussell 2000

FOM C Rate Cut: 9/18

Source: Bloomberg

(11) U.S. Equity Indices Reverse Sharp DeclineJanuary 1, 2007 – October 26, 2007

Class II FOMC – Restricted FR

56789

10111213

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

Percent

5678910111213

Percent

S&P 500: Bottom-Up Equity Analyst Forecasts for 2007

S&P 500: Bottom-UpEquity Analyst Forecasts for 2008

(12) Equity Earnings ExpectationsJanuary 1, 2007 – October 19, 2007

Source: Thompson Financial

Page 4 of 10

October 30-31, 2007 147 of 162Authorized for Public Release

0.000.020.040.060.080.100.120.140.16

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

Skew

0.000.020.040.060.080.100.120.140.16Skew

Put - Call Equity Risk Reversal

(13) Demand for Downside Protection on S&P 500 Has FallenJanuary 1, 2007 – October 25, 2007

Source: OptionMetrics

Class II FOMC – Restricted FR

(14) Correlation of Daily Price/Yield ChangesAugust 7, 2007 – September 17, 2007

Blue boxes denote correlations greater than 0.50 or less than -0.50Source: Bloomberg and JP Morgan

Blue boxes denote correlations greater than 0.50 or less than -0.50Source: Bloomberg and JP Morgan

(15) Correlation of Daily Price/Yield ChangesSeptember 18, 2007 – October 26, 2007

Variables 2YR Yield10YR Yield S&P USD/JPY

Swap Spreads VIX CDX IG

2YR Yield10YR Yield 0.89S&P 0.75 0.75USD/JPY 0.80 0.77 0.71Swap Spreads -0.55 -0.35 -0.53 -0.37VIX -0.62 -0.51 -0.81 -0.64 0.56CDX IG 0.62 0.63 0.71 0.48 -0.58 -0.58Merrill-HY -0.84 -0.78 -0.57 -0.78 0.54 0.47 -0.56

Page 5 of 10

Variables 2YR Yield10YR Yield S&P USD/JPY

Swap Spreads VIX CDX IG

2YR Yield10YR Yield 0.77S&P 0.22 0.28USD/JPY 0.18 0.05 0.62Swap Spreads 0.37 0.27 -0.53 -0.53VIX -0.13 -0.26 -0.91 -0.52 0.47CDX IG 0.49 0.51 0.78 0.58 -0.37 -0.74Merrill-HY -0.67 -0.70 -0.40 -0.41 0.08 0.28 -0.65

October 30-31, 2007 148 of 162Authorized for Public Release

0

5

10

15

20

25

30

35

01/01/05 05/01/05 09/01/05 01/01/06 05/01/06 09/01/06 01/01/07 05/01/07 09/01/07

$ Price

0

5

10

15

20

25

30

35 $ Price

Average Spread Since Jan '05

(16) Oil Refining Crack Spread Near Lows January 1, 2005 – October 26, 2007

Source: Bloomberg

Class II FOMC – Restricted FR

92949698

100102

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/0792949698100102

Euro vs. Dollar: Index as of Jan07

as of Jan07

104106108110Index to 100

104106108110

Index to 100

Yen vs. Dollar: Index

(17) Dollar Stays on Gradual Downtrend January 1, 2007 – October 26, 2007

Dol

lar

Dep

reci

atio

n

Dol

lar

App

reci

atio

n

Broad Trade-Weighted Dollar: Index as of Jan97

Source: Bloomberg and Federal Reserve Board

-200

20406080

100120140

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

BPS1.281.301.321.341.361.381.401.421.44

$/Euro

Eurodollar-Euribor (LHS)

$/EUR (RHS)

Source: Bloomberg

(18) Dollar Tracks Interest Rate Differentials January 1, 2007 – October 26, 2007

Page 6 of 10

October 30-31, 2007 149 of 162Authorized for Public Release

3.0

3.5

4.0

4.5

5.0

5.5

6.0Percent

Survey Response -size indicates freq

September Average Forecast

Market Rates as of 9/10

(21) Distribution of Expected Policy Target Among Primary Dealers Prior to September 18 FOMC Meeting

Source: Dealer Policy Survey Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008

3.0

3.5

4.0

4.5

5.0

5.5

6.0Percent

Survey Response -size indicates freq

May Average Forecast

Market Rates as of 10/23

(20) Distribution of Expected Policy Target Among Primary Dealers Prior to October 31 FOMC Meeting

Source: Dealer Policy Survey

Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008

01020304050607080

9/18/2007 9/21/2007 9/26/2007 10/1/2007 10/4/2007 10/10/2007 10/15/2007 10/18/2007 10/23/2007 10/26/2007

Percent

4.25 Target Rate4.50 Target Rate4.75 Target Rate

Sept. Nonfarm Payrolls: 10/5

Sept. Housing Starts: 10/17

(19) Probabilities on Policy Rate Expectations for October FOMC MeetingSeptember 18, 2007 – October 26, 2007

Source: Cleveland Fed

Class II FOMC – Restricted FR Page 7 of 10

October 30-31, 2007 150 of 162Authorized for Public Release

2.20

2.40

2.60

2.80

3.00

06/01/06 09/01/06 12/01/06 03/01/07 06/01/07 09/01/07

Percent

2.20

2.40

2.60

2.80

3.00 Percent

Barclays

Federal Reserve Board

FOM C Rate Cut: 9/18

(22) TIPS Implied Inflation: 5-10 Year HorizonJune 1, 2006 – October 26, 2007

Source: Federal Reserve Board and Barclays Capital

Class II FOMC – Restricted FR

4.25

4.50

4.75

5.00

5.25

5.50

5.75

07/01/07 08/01/07 09/01/07 10/01/07

Percent

4.25

4.50

4.75

5.00

5.25

5.50

5.75 Percent

Effective Rate Target Rate

(24) Effective versus Target Fed Funds RateJuly 1, 2006 – October 26, 2007

Source: Federal Reserve Bank of New York

Page 8 of 10

4.70

4.72

4.74

4.76

4.78

4.80

4.82

4.84

09/18/07 09/25/07 10/02/07 10/09/07 10/16/07 10/23/07

Percent

4.70

4.72

4.74

4.76

4.78

4.80

4.82

4.84 Percent

Rolling Cumulative Effective Rate Since 9/19

Target Fed Funds Rate

(23) While Day-to Day Effective Rate Remain Volatile, Cumulative Effective Rate at TargetSeptember 18, 2007 – October 26, 2007

Source: Federal Reserve Bank of New York

October 30-31, 2007 151 of 162Authorized for Public Release

3.50

3.75

4.00

4.25

4.50

4.75

5.00

5.25

Years to Maturity

Percent

3.50

3.75

4.00

4.25

4.50

4.75

5.00

5.25 Percent

8/7/2007 9/17/2007 10/26/2007

(27) Treasury Yield Curve Shifts Lower and Continues to Steepen

Source: Bloomberg1-Year 2-Year 3-Year 5-Year 7-Year 10-Year

4.00

4.25

4.50

4.75

5.00

5.25

Dec-07 Mar-08 Jun-08 Sep-08 Dec-08Eurodollar Futures Contracts

Percent

4.00

4.25

4.50

4.75

5.00

5.25 Percent

8/7/2007 9/17/2007 10/26/2007

Source: Bloomberg

(25) Eurodollar Futures Curve Shifts Lower

Class II FOMC – Restricted FR APPENDIX: Reference Exhibits

0

4

8

12

16

20

1.75 2.00 2.25 2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 4.50 4.75 5.00 5.25 5.50 5.75 6.00 6.25 6.50

Percent

0

4

8

12

16

20Percent

10/26/2007

9/17/2007

(26) Probability Distribution on Eurodollar Futures Contract 300 Days Forward

Source: CME Option

Page 9 of 10

October 30-31, 2007 152 of 162Authorized for Public Release

0

100

200

300

400

500

03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07

BPS

0

100

200

300

400

500BPS

FOM C Rate Cut: 9/18

B

Ba

BaaA

Aa Aaa

S&P Rating Downgrades: 10/17 and

10/19

Source: Bloomberg

(29) US Corporate Option-Adjusted Debt Spread by RatingMarch 1, 2007 – October 26, 2007

0

20

40

60

80

100

120

140Percent

0

5

10

15

20

25

30

35 Percent

VIX (RHS)

1-Month Dollar-Yen Vol (RHS)

1-Month Euro-Dollar Vol (RHS)

SMOVE (LHS)

FOM C Rate Cut: 9/18

(28) Implied Volatility Increases in Recent Days January 1, 2007 – October 26, 2007

Page 10 of 10Class II FOMC – Restricted FR

01/01/07 02/01/07 03/01/07 04/01/07 05/01/07 06/01/07 07/01/07 08/01/07 09/01/07 10/01/07Source: Bloomberg

October 30-31, 2007 153 of 162Authorized for Public Release

Appendix 2: Materials used by Mr. Madigan

October 30-31, 2007 154 of 162Authorized for Public Release

Class I FOMC – Restricted Controlled (FR)

Material for FOMC Briefing on October Projections

Brian Madigan October 30, 2007

October 30-31, 2007 155 of 162Authorized for Public Release

2007 2008 2009 2010Central Tendencies

Real GDP Growth 2.2 to 2.3 1.8 to 2.5 2.3 to 2.7 2.5 to 2.6June projections 2-1/4 to 2-1/2 2-1/2 to 2-3/4

Unemployment Rate 4.7 to 4.8 4.8 to 5.0 4.8 to 5.0 4.7 to 4.9June projections 4-1/2 to 4-3/4 about 4-3/4

PCE Inflation 2.9 to 3.0 1.8 to 2.1 1.7 to 2.0 1.6 to 1.9

Core PCE Inflation 1.8 to 1.9 1.7 to 1.9 1.7 to 1.9 1.6 to 1.9June projections 2 to 2-1/4 1-3/4 to 2

RangesReal GDP Growth 2.2 to 2.5 1.6 to 2.6 2.0 to 2.8 2.2 to 2.7

June projections 2 to 2-3/4 2-1/2 to 3

Unemployment Rate 4.7 to 4.8 4.6 to 5.0 4.6 to 5.0 4.6 to 5.0June projections 4-1/2 to 4-3/4 4-1/2 to 5

PCE Inflation 2.7 to 3.2 1.7 to 2.3 1.5 to 2.2 1.5 to 2.0

Core PCE Inflation 1.8 to 2.1 1.7 to 2.0 1.5 to 2.0 1.5 to 2.0June projections 2 to 2-1/4 1-3/4 to 2

1. Projections of real GDP growth, PCE inflation and core PCE inflation are fourth-quarter-to-fourth-quarter growth rates, i.e. percentage changes from the fourth quarter of the prior year to the fourth quarter of the indicated year. PCE inflation and core PCE inflation are the percentage rates of change in the price index for personal consumption expenditures and the price index for personal consumption expenditures excluding food and energy, respectively. Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of each year. Each participant's projections are based on his or her assessment of appropriate monetary policy. The range for each variable in a given year includes all participants' projections, from lowest to highest, for that variable in the given year; the central tendencies exclude the three highest and three lowest projections for each variable in each year.

Table 1: Economic Projections of Federal Reserve Governors and Reserve Bank Presidents 1

October 30-31, 2007 156 of 162Authorized for Public Release

Appendix 3: Materials used by Mr. Stockton

October 30-31, 2007 157 of 162Authorized for Public Release

2007-Q2Final Greenbook Advance

Real GDP 3.8 3.3 3.9

Final Sales 3.6 3.6 3.5 Personal Consumption 1.4 3.2 3.0 Durables 1.7 2.8 4.4 Nondurables -0.5 2.9 2.7 Services 2.3 3.4 2.9 Business Fixed Investment 11.0 6.2 7.9 Nonresidential Structures 26.2 3.7 12.3 Equipment and Software 4.7 7.4 5.9 Residential Investment -11.8 -22.4 -20.1 Government 4.1 3.2 3.7 Federal 6.0 5.8 6.8 State and Local 3.0 1.8 2.0 Exports 7.5 16.9 16.2 Imports -2.7 3.5 5.2

Level in chained 2000 dollars:

Change in nonfarm business inventories 1.3 -4.2 12.4Change in farm inventories 3.6 1.0 2.9Net Exports -573.9 -535.9 -546.2

Price Indexes:

Total PCE Chain Price Index 4.3 1.5 1.7 Core PCE Chain Price Index 1.4 1.6 1.8

Gross Domestic Product(percent change at an annual rate)

2007-Q3

Page 1 of 1

October 30-31, 2007 158 of 162Authorized for Public Release

Appendix 4: Materials used by Mr. Madigan

October 30-31, 2007 159 of 162Authorized for Public Release

Class I FOMC – Restricted Controlled (FR)

Material for FOMC Briefing on Monetary Policy Alternatives Brian Madigan October 31, 2007

October 30-31, 2007 160 of 162Authorized for Public Release

Class I FOMC – Restricted Controlled (FR) Table 1: Alternative Language for the October 2007 FOMC Announcement Bluebook version

September FOMC Alternative A Alternative B Alternative C

Policy Decision

1. The Federal Open Market Committee decided today to lower its target for the federal funds rate 50 basis points to 4-3/4 percent.

The Federal Open Market Committee decided today to lower its target for the federal funds rate 25 basis points to 4-1/2 percent.

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 4-3/4 percent.

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 4-3/4 percent.

2. Economic growth was moderate during the first half of the year, but the tightening of credit conditions has the potential to intensify the housing correction and to restrain economic growth more generally. Today’s action is intended to help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and to promote moderate growth over time.

Economic growth was solid in the third quarter, and strains in financial markets have eased somewhat on balance. However, the pace of economic expansion will likely slow somewhat in the near term, partly reflecting the intensification of the housing correction. Today’s action, combined with the policy action taken in September, should help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and promote moderate growth over time.

Economic growth was solid in the third quarter, and strains in financial markets have eased somewhat on balance. The pace of economic expansion will likely slow somewhat in the near term, partly reflecting the intensification of the housing correction. But, to date, other sectors of the economy have proven resilient and the global economy remains strong. The Committee anticipates that the economic expansion will return to a moderate pace over time, but sees continuing risks to growth, notably the potential impact of the tightening of credit conditions for some households and businesses.

Economic growth was solid in the third quarter despite an intensification of the housing correction. Strains in financial markets have eased somewhat on balance, reducing the downside risks to growth. Though incoming indicators point to some near-term slowing in the pace of economic expansion, the recent easing of monetary policy should help promote moderate growth over time.

Rationale

3. Readings on core inflation have improved modestly this year. However, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year. However, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year. However, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year, but the high level of resource utilization and recent increases in energy prices may put renewed upward pressures on overall and core inflation.

Assessment of Risk

4. Developments in financial markets since the Committee’s last regular meeting have increased the uncertainty surrounding the economic outlook. The Committee will continue to assess the effects of these and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

The Committee judges that the upside risks to inflation roughly balance the downside risks to growth. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

On balance, the Committee views downside risks to growth as the greater policy concern. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

The Committee judges that the upside risks to inflation roughly balance the downside risks to growth. Future policy adjustments will depend on the outlook for both inflation and economic growth, as implied by incoming information.

October 30-31, 2007 161 of 162Authorized for Public Release

Class I FOMC – Restricted Controlled (FR) Table 1: Alternative Language for the October 2007 FOMC Announcement Revised: October 31, 2007

September FOMC Alternative A Alternative B Alternative C

Policy Decision

1. The Federal Open Market Committee decided today to lower its target for the federal funds rate 50 basis points to 4-3/4 percent.

The Federal Open Market Committee decided today to lower its target for the federal funds rate 25 basis points to 4-1/2 percent.

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 4-3/4 percent.

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 4-3/4 percent.

2. Economic growth was moderate during the first half of the year, but the tightening of credit conditions has the potential to intensify the housing correction and to restrain economic growth more generally. Today’s action is intended to help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and to promote moderate growth over time.

Economic growth was solid in the third quarter, and strains in financial markets have eased somewhat on balance. However, the pace of economic expansion will likely slow in the near term, partly reflecting the intensification of the housing correction. Today’s action, combined with the policy action taken in September, should help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and promote moderate growth over time.

Economic growth was solid in the third quarter, and strains in financial markets have eased somewhat on balance. The pace of economic expansion will likely slow in the near term, partly reflecting the intensification of the housing correction. But, to date, other sectors of the economy have proven resilient and the global economy remains strong. The Committee anticipates that the economic expansion will return to a moderate pace over time, but sees continuing risks to growth, notably the potential impact of the tightening of credit conditions for some households and businesses.

Economic growth was solid in the third quarter despite an intensification of the housing correction. Strains in financial markets have eased somewhat on balance, reducing the downside risks to growth. Though incoming indicators point to some near-term slowing in the pace of economic expansion, the recent easing of monetary policy should help promote moderate growth over time.

Rationale

3. Readings on core inflation have improved modestly this year. However, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year, but recent increases in energy and commodity prices, among other factors, may put renewed upward pressure on inflation. In this context, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year. However, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Readings on core inflation have improved modestly this year, but recent increases in energy and commodity prices, among other factors, may put renewed upward pressure on inflation. In this context, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

Assessment of Risk

4. Developments in financial markets since the Committee’s last regular meeting have increased the uncertainty surrounding the economic outlook. The Committee will continue to assess the effects of these and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

The Committee judges that, after this action, the upside risks to inflation roughly balance the downside risks to growth. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

On balance, the Committee views downside risks to growth as the greater policy concern. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

The Committee judges that the upside risks to inflation roughly balance the downside risks to growth. Future policy adjustments will depend on the outlook for both inflation and economic growth, as implied by incoming information.

October 30-31, 2007 162 of 162Authorized for Public Release