FOCUS: INITIATING COVERAGE ON AFRICAN PETROLEUM CORPORATION · PDF fileOctober 1, 2013 FOCUS:...

45

October 1, 2013 FOCUS: INITIATING COVERAGE ON AFRICAN PETROLEUM CORPORATION LIMITED For more information please contact: Kingsley O. Jibunoh Research Analyst, Institutional Research +44 (0)20 7448 0227 - kojibunoh@firstenergy.com Gerry Donnelly, PhD, B.Eng. Director, Institutional Research +44 (0)20 7448 0214 - gfdonnelly@firstenergy.com London: +44 (0)20 7448 0200 www.firstenergy.com NSX Listed: AOQ AU Price: A$0.12 Opinion: SPECULATIVE BUY 12 Month Target Price: A$0.50 REGULATORY DISCLOSURES: PAGE 41

Transcript of FOCUS: INITIATING COVERAGE ON AFRICAN PETROLEUM CORPORATION · PDF fileOctober 1, 2013 FOCUS:...

October 1, 2013

FOCUS:INITIATING COVERAGE ON AFRICAN PETROLEUM CORPORATION LIMITED

For more information please contact:

Kingsley O. Jibunoh Research Analyst, Institutional Research +44 (0)20 7448 0227 - [email protected]

Gerry Donnelly, PhD, B.Eng. Director, Institutional Research +44 (0)20 7448 0214 - [email protected]

London: +44 (0)20 7448 0200 www.firstenergy.com

NSX Listed: AOQ AU

Price: A$0.12

Opinion: SPECULATIVE BUY

12 Month Target Price: A$0.50

REGULATORY DISCLOSURES: PAGE 41

Table of Contents

FOCUS | FirstEnergy Capital LLP October 1, 2013

For Regulatory Disclosures, Please Go To Our Website: http://www.firstenergy.com/research/regulatory.php or fax us at +1.403.262.0666

Our policy on the dissemination of research can be found at http://www.firstenergy.com/research/regulatory.php

Sources for tabular data and charts are FirstEnergy Capital LLP and Company Reports unless otherwise noted.

This report has not been approved by FirstEnergy Capital LLP for the purposes of section 21 of the Financial Services and Markets Act 2000 as it is being distributed only to persons who are investment professionals within the meaning of article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 is not intended to, and should not be relied upon, by any other person. The information contained herein is for information purposes only and is not to be construed as an offer or solicitation for the sale and purchase of securities. While the accuracy or completeness of the information contained in this document cannot be guaranteed by FirstEnergy Capital Corp., it was obtained from sources believed to be reliable. FirstEnergy Capital Corp. and/or its officers, directors and employees may from time to time acquire, hold or sell positions in the securities mentioned herein as principal or agent. FirstEnergy Capital (USA) Corp., a member of the Financial Industry Regulatory Authority, is a wholly owned subsidiary of FirstEnergy Capital Holdings Corp. and operates as a Broker-Dealer in the United States. FirstEnergy Capital LLP is authorised and regulated by the FCA.

Contents

Highlights and Investment Summary .............................. 3

Asset Overview ........................................................................ 7

Valuation .................................................................................... 13

Risks and Mitigants ................................................................ 15

Financial Estimates ............................................................... 16

Management ............................................................................ 16

Appendix A: Valuation Assumptions................................. 18

Appendix B: Company History ............................................ 19

Appendix C: Asset Description ........................................... 19

Appendix D: Regional Hydrocarbon Sector and Geopolitical Overview ............................................................ 26

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

3

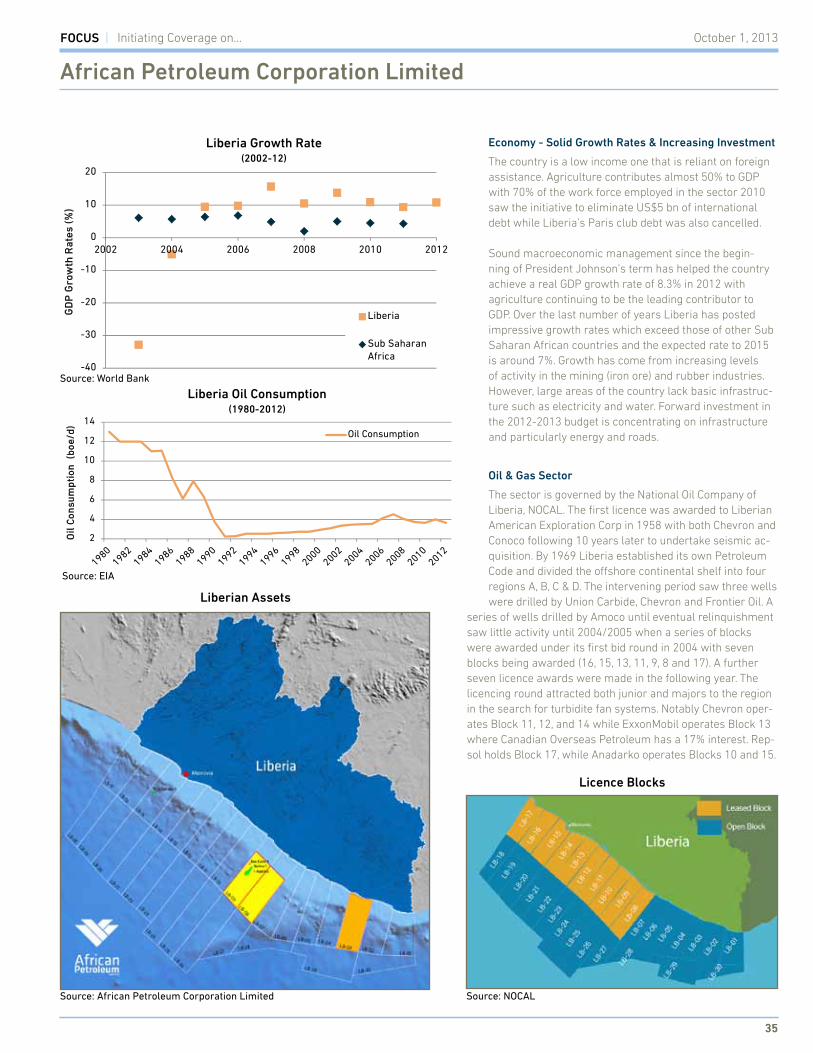

HighlightsWe are initiating coverage on NSX Australia listed African Petroleum Corporation Limited (AOQ AU, c.A$203 mm market capitalization) with a Speculative Buy recommendation and a target price of A$0.50 per share. A recent independently audited resources report, highlights an estimated 5.4 bnbbl of net unrisked mean prospective resources across 12 prospects in the highly prospective West African Transform Margin which has yielded significant discoveries in recent years. We note that African Petroleum has derisked its Liberian acreage with the results of the three wells drilled to date on LB-09.

Few companies offer the size, scale and diversity of plays in African Petroleum’s current portfolio. With one of the largest net acreage positions offshore West Africa, African Petroleum retains the optionality to farm-down its current high working interest positions and reduce its capital expenditure outlay over the next 12-18 months. We highlight that the on-going farm-out process could see the Company potentially drill at least three wells (African Petroleum is proposing up to five wells based on work commitments) in 2014 exposing investors to unrisked upside of c.21x current trading levels.

African Petroleum in our view remains an attractive groundfloor entry point to play a sustained drilling regional campaign of over 38 wells in the near-term across the West African Transform Margin by Majors, Independents and Juniors alike. The proposed migration from Australia’s Junior market to the main board listing on the Australian stock exchange in the near-term will address any historic concerns on transparency and potentially widen the Company’s current blue chip institutional shareholding.

Despite the risk profile of the Company, African Petroleum could potentially become a take-over target given the attractiveness of its acreage holding which is extensively covered with 3D seismic data. Potential acquirers could include Majors, NOCs or large independents that have exist-ing work commitments and access to drilling rigs in the region including Genel, Anadarko, Cairn, Tullow, Vitol, ExxonMobil, Total and LukOil.

Investment SummaryAfrican Petroleum holds equity positions ranging from 60-100% in 10 blocks across Sierra Leone, Liberia, Senegal, the Gambia and Cote d’Ivoire. With anticipated level of drilling activity by African Petroleum and regionally in the next 12-18 months, current trading levels remains an attrac-tive entry point. We put forward a target price of A$0.50 per share and a Speculative Buy recommendation ahead of the Company’s proposed 2014 drilling campaign. Our valuation is predicated on the ability of the Company to complete its ongoing farm-out expeditiously and securing a full or partial well carry to drill a minimum of three wells (maximum of five exploration wells) in 2014.

Extensive Land Position Across the West African Transform Margin

African Petroleum holds attractive acreage positions across the prospective West African Transform Margin (WATM) which in recent years has yielded the Jubilee, TEN and Paradise and Pelican discoveries. We believe the full prospectivity of the WATM is yet to be realised and African Petroleum with its diversified portfolio across five countries and five basins over an areal extent of 31,878 sq km in the region offers an attractive opportunity ahead of high impact regional newsflow in the near-term.

Highlights and Investment Summary

Opportunities- African Petroleum offers exposure to extensive land position in the West

African Transform Margin which has yielded substantial discoveries in recent times such as the Jubilee, TEN, Sankofa, Pecan-1 & Paradise discoveries in Ghana, Jupiter and Venus discoveries in Sierra Leone and discoveries on Blocks CI-401 & CI-103 in Cote d’Ivoire.

- According to a recent independently audited resource report, African Petroleum holds estimated net unrisked mean prospective resources of 5.4 bnbbl across its portfolio (excluding an additional seven to nine prospects and 28 leads identified by APCL).

- Exposure to a potential high impact five well drilling campaign (FCCe: three wells) targeting A$0.31 per share risked (A$1.76 per share unrisked) and extensive near-term drilling activity in the region all the way up to Morocco further North of the Company’s acreage.

- The story is currently trading at A$0.12 per share which implies a c.4x upside to our risked NAV and 21x upside to our unrisked drilling NAV of A$2.53 which is compelling in comparison to peers.

Considerations- There are no guarantees on the Company’s current farm-out process or

timelines to successful completion. Consequently, the Company retains a capital outlay risk with pending work programme obligations and a current cash balance estimated at c.US$20 mm. This could also have an impact on the Company's negotiating position. FirstEnergy assumes an equity raise of c.US$30 mm in 2H13.

- African Petroleum is still an early stage exploration company with no revenues and will be reliant on the capital markets for continued funding of its exploration program.

- Africa Petroleum has drilling work programme commitments due on Block A1 in Gambia by December 31, 2013. We anticipate the Company could potentially secure an extension to be able to complete a well in 2014. Furthermore, we note that drilling commitments are also due in 2014 on Blocks LB-08 in Liberia, and CI-513 in Cote d’Ivoire.

- Despite the extensive technical work undertaken by African Petroleum across its acreage, the Company is yet to make a commercial discovery although it has significantly de-risked the Liberian deep water basin with the Narina-1 discovery.

- The Company's G&A remains high at an estimated US$15 mm per year. We however, believe the Company will seek to bring it down to manageable levels going forward.

- Potential fiscal term changes by the Liberian legislature. However there are no indications that any new petroleum related legislature will affect existing contracts.

Significant Exploration Prospectivity

A recent CPR commissioned by African Petroleum estimates net mean unrisked prospective of 5.4 bnbbl across 12 prospects in the Company’s portfolio. This excludes an additional seven to nine prospects identified by African Petroleum which is expected to be included in a revised CPR in 4Q13. The Company has also identified 28 leads which will be matured over time. African Petroleum internal estimates, based on technical work carried out to date, highlights potential resources in excess of 10 bnbbl unrisked prospective resources. We note that drilling activity carried out by the Company in Liberia has led to better understanding of the offshore Liberian basin and proved the presence of a working petroleum system.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

4

Targeting c.2 bnbbl Unrisked Resources in the Near-term

African Petroleum is proposing to potentially drill up to five exploration wells across its portfolio in 2014 to meet licence obligations. The wells are targeting unrisked prospective resources of c.2 bnbbl (c.1.2 bnbbl assum-ing a three well programme in 2014) which we value at A$1.76 per share (assuming a three well programme in 2014) on an unrisked basis. The Company has opened a dataroom to farm-out some of its acreage ahead of the drilling campaign. We anticipate that the Company will be aiming to secure attractive farm-out terms that will include a well carry obligation as the preferred option given the current cash balance of c.US$20 mm.

High Levels of Regional Interest

The West African Transform Margin, through the Central Atlantic Margin up to Morocco in the North of Africa, will see extensive drilling newsflow in the next 12-18 months. Drilling activity is expected from the Majors, Inde-pendents and NOCs alike. Drilling activity includes wells planned by Tullow on its licence in Guinea in 1H14 across the margin to Cote d’Ivoire where Lukoil is planning a four well campaign and in Ghana where Tullow and its partners are continuously drilling. The recent discoveries in Cote d’Ivoire by Total and Vanco and the discovery by Afren/Lekoil with the Ogo-1 well have potentially extended the prospectivity of the margin further east into

Opportunities- African Petroleum offers exposure to extensive land position in the West

African Transform Margin which has yielded substantial discoveries in recent times such as the Jubilee, TEN, Sankofa, Pecan-1 & Paradise discoveries in Ghana, Jupiter and Venus discoveries in Sierra Leone and discoveries on Blocks CI-401 & CI-103 in Cote d’Ivoire.

- According to a recent independently audited resource report, African Petroleum holds estimated net unrisked mean prospective resources of 5.4 bnbbl across its portfolio (excluding an additional seven to nine prospects and 28 leads identified by APCL).

- Exposure to a potential high impact five well drilling campaign (FCCe: three wells) targeting A$0.31 per share risked (A$1.76 per share unrisked) and extensive near-term drilling activity in the region all the way up to Morocco further North of the Company’s acreage.

- The story is currently trading at A$0.12 per share which implies a c.4x upside to our risked NAV and 21x upside to our unrisked drilling NAV of A$2.53 which is compelling in comparison to peers.

Considerations- There are no guarantees on the Company’s current farm-out process or

timelines to successful completion. Consequently, the Company retains a capital outlay risk with pending work programme obligations and a current cash balance estimated at c.US$20 mm. This could also have an impact on the Company's negotiating position. FirstEnergy assumes an equity raise of c.US$30 mm in 2H13.

- African Petroleum is still an early stage exploration company with no revenues and will be reliant on the capital markets for continued funding of its exploration program.

- Africa Petroleum has drilling work programme commitments due on Block A1 in Gambia by December 31, 2013. We anticipate the Company could potentially secure an extension to be able to complete a well in 2014. Furthermore, we note that drilling commitments are also due in 2014 on Blocks LB-08 in Liberia, and CI-513 in Cote d’Ivoire.

- Despite the extensive technical work undertaken by African Petroleum across its acreage, the Company is yet to make a commercial discovery although it has significantly de-risked the Liberian deep water basin with the Narina-1 discovery.

- The Company's G&A remains high at an estimated US$15 mm per year. We however, believe the Company will seek to bring it down to manageable levels going forward.

- Potential fiscal term changes by the Liberian legislature. However there are no indications that any new petroleum related legislature will affect existing contracts.

the Benin-Dahomey basin. Interest in the region has been on the increase with the entrance of new players such as Cairn/ConocoPhillips going into Senegal and Morocco, Genel’s entry into Cote d’Ivoire and Kosmos Energy’s entry into Mauritania.

Valuation

Our valuation is predicated on the ability of African Petroleum to complete the farm-out process across its portfolio prior to drilling in 2014. Based on a DCF methodology predicated on a potential three well campaign in 2014, we value African Petroleum at A$0.50 per share (12 month view) representing an upside of 4x to current trading levels. Current trading levels exclude the material exploration leverage embedded in the story in the next 12-18 months. We highlight that African Petroleum’s drilling unrisked upside of A$2.53 per share remains compelling and investors who take a position at current levels could see returns in multiples of initial investment in a drilling success scenario. In an upside case comparing African Petroleum to Africa Oil shows the significant torque to valuation achievable with exploration success. Additionally given

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Net

Cas

h

G&

A

Tota

l Cor

e N

AV

Libe

ria

- N

arin

a-1

Libe

ria

- Lo

vebi

rd P

rosp

ect

Libe

ria

- S

unbi

rd T

erra

ceP

rosp

ect

CI-

513-

Aya

me

Tota

l NA

V

Ris

ked

NA

V C

ontr

ibu

tion

(A

$/s

har

e)

Core NAV RENAV

Current Share Price

African Petroleum Valuation Waterfall(October 2013)

Source: FirstEnergy Capital LLP

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

55

Source: FirstEnergy Capital LLP

African Coverage Universe Upside Comparison(October 2013)

the high level of regional newsflow and potential contagion newsflow, current trading levels represent an attractive entry point to play a diversified exploration programme tar-geting oil prospects offshore West Africa in the near-term.

Focusing on the Prospectivity of the Equatorial and Central Atlantic MarginIn recent years oil and gas exploration has been focus-ing on the petroleum prospectivity of conjugate margins integrating high resolution regional seismic data (2D & 3D), plate tectonic modeling and paleographic studies in frontier exploration. One such conjugate margin exploration strat-egy is the South Atlantic and Equatorial Margins campaign which in recent years has yielded significant post salt dis-

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

TLW LN AFR LN HOIL LN CRCL LN ELA LN AOI CN OPHR LN WRL LN AOQ AU

Premium/Discount for FCC Africa Focused E&P Plays

P/Unrisked NAV (12 Mths) P/RENAV (12 Mths)

Early MoverAccess to Acreage

•African Petroleum's strategy has historically involved taking early mover positions in exploration acreages with high working interest positions on attractive entry terms. (Block SL-4A/10)

Seismic Advantage

•African Petroleum has assembled a robust subsurface team and following entry into a new jurisdiction acquires extensive 3D data to evaluate petroleum systems, determine prospectivity and subsequently mature and rank exploration prospects. (Blocks A1 & A4 Gambia, Blocks CI-509 & 513 in Cote d'Ivoire, Blocks LB-08 in Liberia and Blocks SL-03 & 4A-10 in Sierra Leone and Blocks ROP & SOSP in Senegal).

Drilling

•Post technical analysis the Company elects to farm-down equity or commit to drill. African Petroleum has drilled three exploration wells to date in Liberia (LB-09).

Production

•African Petroleum has no commercial discoveries to date. However, the Company will seek to form a JV in any potential commercial projects or farm-out.

Conjugate Margin Play Schematic

coveries in the Jubilee field in Ghana (Equatorial) and the Zaedyus field in French Guiana (South Atlantic). Prior to these significant discoveries, the prospectivity of the region was first realised following the discoveries made by Phillips Petroleum such as the Espoir discovery in Cote d’Ivoire in 1981 and the North Tano discovery in Ghana in 1980. The exploitation of the resources of the region has been made possible by advances in drilling technology which has enabled wells to be drilled beyond the continental shelf.

The Conjugate Margin resource po-tential has been proven to be prolific and a regional approach to explora-tion is widely believed in the industry as the best approach to success. This holistic approach to exploration has been successfully proved by Tullow and has contributed significantly to the transformation of the Company

Source: Tullow Oil Plc

African Petroleum Strategy - High Grading Opportunities

Source: African Petroleum Corporation Limited, FirstEnergy Capital LLP

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

6

from an exploration start-up with the sign-ing of its first licence in Senegal in 1985 to a multibillion E&P Company. The Company has focused on potential areas of major submarine canyon occurrence which could provide an entry point for coarse-grained shallow-water sands onto the continental slope and basin floor. The discoveries to date along the Equatorial Margin are believed to have originated almost exclusively from drift-phase marine sources of Albian-Turonian age although Syn-rift lacustrine and deltaic source rocks are also common. The reservoir targets are mainly turbidite sandstone reservoirs that vary in age from Cenomanian to Maastrichtian.

African Petroleum similar to Tullow has taken a regional approach and focused its explora-tion efforts to date on the Equatorial Margin of West Africa popularly referred to as the West African Transform Margin (WATM) and also in the Central Atlantic Margin. The Company holds one of the most extensive acreage positions in the region currently estimated at 31,878 sq km in 10 licences in Liberia, Sierra Leone, Cote d’Ivoire, the Gambia and Senegal. African Petroleum has successfully drilled three margin play exploration wells with two uncommercial discoveries in the Liberian-Sierra Leone sub-basin with significant potential for commercial

African Petroleum Corporation Ltd | 2013 Corporate Presentation | 14

APCL Portfolio Resources

ERC Equipoise Competent Persons Report (June 2013)

3,046

1,560356

434 5,396

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

Libe

ria

Cot

e d'

Ivoi

re

The

Gam

bia

Sie

rra

Leon

e

Tota

l

Unr

iske

d N

et R

esou

rces

MM

BO

APCL Portfolio by Country (Mean Unrisked MMBO)

473

20953

79 814

-

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

Libe

ria

Cot

e d'

Ivoi

re

The

Gam

bia

Sie

rra

Leon

e

Tota

l

Ris

ked

Net

Res

ourc

es M

MB

O

APCL Portfolio by Country(Mean Risked MMBO)

Source: Africa Petroleum Corporation Limited

African Petroleum Strategy - High Grading Opportunities

Schematic Equatorial, Central & North Atlantic Margin

Source: University of Texas

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

77

recoverable resources as the basin is further de-risked. The Company has also taken an early mover approach by acquiring assets with high working interests providing it with optionality to farm-down following further derisking through technical work.

A recently released CPR undertaken for ERC Equipoise on behalf of African Petroleum ascribes net mean unrisked prospective resources of 5.4 bnbbl (814 mmbbl risked) across the Company’s acreage. African Petroleum internal estimates highlight potential in excess of 10 bnbbl of net unrisked prospective resources (1.7 bnbbl risked).

African Petroleum Portfolio

Source: African Petroleum Corporation Limited, FirstEnergy Capital LLP

African Petroleum: Asset Snapshot

* Negotiations are ongoing with the Gambian government for a licence extensionSource: African Petroleum Corporation Limited

Parameters Liberia Sierra Leone Cote d'Ivoire Gambia Senegal

Blocks LB-08 & LB-09 SL-4A-10 & SL-03 CI-509 & CI-513 A1 & A4 ROP & SOSP

Licence Area (sq km) 5,351 5,855 2,531 2,672 18,277

Working Interest 100% 100% 90% 60% 90%

Award Date June 2005February 2011 & September 2012

December 2011, March 2012 December 2007 November 2011

JV Partner N/A N/A Petroci (10% carried interest)Buried Hill (40%) - carried for

20% Petrosen

Expiry of Initial Exploration Period

June 2012. 1st two year extension expiring on June 30,

2014. Two well commitments on LB-08

SL-4A (September 11, 2015, one contingent well commitment).

SL-03 (1st 2 year extension ends February 22, 2016 with

one well commitment)

CI-509 - March 30, 2015 with one well committment, CI-513 -

December 31, 2014 with one well commitment

*December 31, 2013. (Pending one well commitment)

SOSP - October 25, 2014, ROP - October 25, 2015 with one well

commitment

Asset Overview

Brief Asset OverviewAfrica Petroleum holds equity working interest positions in 10 licences across Liberia, Sierra Leone, Gambia, Senegal and Cote d’Ivoire. The as-sets are extensively covered with 2D and 3D seismic data. African Petroleum has acquired c.19,500 sq km of 3D seismic data across its acreage which has enabled it to map several prospects and leads.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

8

Liberia (Blocks LB-08 & LB-09) - A$0.41 per Share Risked/A$2.18 per Share UnriskedThe Liberian basin evolved as a result of the opening of the Atlantic Ocean. The region is structurally complex and the offshore extents are bound by the Sierra Leone transform system to the north and the St. Paul transform system to the south. However, the upper Cretaceous depositional environments which have yielded discoveries to date in Turbidite sands were less affected by major faulting.

The offshore Liberian continental shelf remains relatively underexplored with intermittent exploratory drilling of nine exploration wells between 1970-1972 and 1984-1985 in shallow water depth of 400 m. Although oil shows were encountered in eight of the wells drilled in the period, ac-cording to data from NOCAL, no commercial discovery was made. However, in recent times sentiment has been turning with the advance in seis-mic and imaging technology which has led to a renewed phase of exploration in the basin. In offshore Sierra Leone, the Venus B-1 discovery well (2009), drilled in 1,800 m water depth encountered 14 m net of hydrocarbon pay in upper Cretaceous deep-water fan sands. This was followed by the Mercury-1 discovery in 2010. Mercury-1 was drilled in 1,600 m water depth and encountered 41 m net of oil pay within the same play.

Location of the Liberian Basin

Source: TGS

Historic Liberia Drilling Results(October 2013)

BlockYear

Drilled Well Name Well Operator StatusNet Pay

(m)Total Depth

(m) Reservoir IntervalCrude Quality

(API)

Block-08 N/A N/A N/A N/A N/A N/A N/A N/ABlock-09 1972 Cestos -1 Frontier Oil & Gas Dry Hole N/A 3,154 N/A N/A

4Q11 Apalis-1 African Petroleum Dry Hole N/A 3,665 N/A N/A1Q12 Narina-1 African Petroleum Commerciality Pending 32 4,850 Turonian, Albian 37-44

1Q13 Bee-Eater-1 African Petroleum Uncommercial Oil Discovery 48 4,100 Turonian, Cenomanian & Albian 37-44

Block-10 1985 S1-1 Amoco Dry Hole N/A 3,043 N/A N/ABlock-11 2Q12 Nighthawk-1 Chevron Liberia Dry Hole N/A 4,785 N/A N/ABlock-12 1985 H2-1 Amoco Dry Hole N/A 3,494 Oil Shows in E/M Albian N/A

2Q12 Carmine Deep Chevron Liberia Uncommercial Oil Discovery N/A 4,693 N/A N/ABlock-13 1970 IIB-1 Chevron Dry Hole N/A 2,930 Immature Oil Show in E/M Albian N/ABlock-14 1985 A2-1 Amoco Dry Hole N/A 3,117 Immature Oil Show in E/M Albian N/ABlock-15 3Q10 Montserrado-1 Anadarko Non Commercial Oil Discovery 8 5,400 Late Cretaceous N/ABlock-16 1971 A1-1 Ashland Exploration Dry Hole N/A 1,288 N/A N/ABlock-17 N/A N/A N/A N/A N/A N/A N/A N/ASource: FirstEnergy Capital LLP, NOCAL

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

99

African Petroleum owns a 100% interest in Block LB-08 and LB-09 in Liberia which lie in water depths ranging from less than 100 m to over 3,000 m. Most of the block lies in water depths greater than 500 m. Both blocks are covered by regional 2D seismic data and a 5,170 sq km 3D seismic survey licenced by African Petroleum from TGS. A recently released CPR ascribes c.3 bnbbl net mean unrisked prospective resources (473 mmbbl risked) across the Company’s acreage in Liberia. This excludes additional prospects and leads identified by African Petroleum on both blocks.

Playing at the MarginTwo petroleum systems have been identified in the offshore Liberian basin in the early Cretaceous and late Cretaceous. Historic shelf drilling show that the early Cretaceous (Aptian to Albian) contains three or more oil-prone marine and lacustrine (Type II/III) source rocks while the late Cretaceous Source rocks are formed by late Cenomanian to Turonian organic-rich (Type II) marine shales. These petroleum systems have encountered significant discoveries in Ghana (Jubilee, TEN, Pelican, Paradise etc) and encouraging results in Liberia, and Sierra Leone. Following recent discoveries, stratigraphic traps are now seen as the most prospective play type in the offshore Liberian basin (and throughout the WATM).

Three wells have been drilled to date on Block-09 with none so far drilled on Block-08. The Apalis-1 was drilled in 2011 and was targeting a four-way-dip-closure. The well encountered traces of hydrocarbons and potential source rock, however reservoir sands were absent and the well was subsequently plugged and abandoned. The second well Narina-1 was drilled in 2012, and encountered 21 m of net pay of c.38 degree API oil in Turonian sandstones and 11 m of net pay in the Albian of c.44 degree API oil. Narina Albian and Turonian oils were sampled in MDTs however no DSTs were run. The well had mixed reservoir quality in the oil bearing Turonian section. The Bee-Eater well was completed in early 2013 and although oil bearing Cenomanian/Turonian sandstone were encountered, reservoir permeabilities over the hydrocarbon section of the well were lower than anticipated. Historic and recent regional drilling has proven the presence of a working petroleum system and the presence of oil in the basin.

Dealing with the Permeability QuestionFollowing the drilling of the Bee-Eater well, African Petroleum has undertaken extensive analysis of the results to develop a better sub marine depositional model. The well is believed to be located in a by-pass zone of sediment transport down slope which is characterised by poorly sorted, cemented and coarse grained sandstone in the Upper Cenomanian in this instance.

Historic drilling activity in the region is believed to have focused on the Basin slope which may account for the observed poor reservoir pa-rameters. Upper slope reservoirs within the mapped fan feeder systems are proving to have reservoir quality challenges due to poor reservoir sorting, cementation and overall poor development due to bypass. Near-term wells are planned by E&P players in Sierra Leone, Liberia and Cote d’Ivoire where the basin floor fan will be tested. This may yield thick, well connected high quality reservoirs analogous to many other worldwide

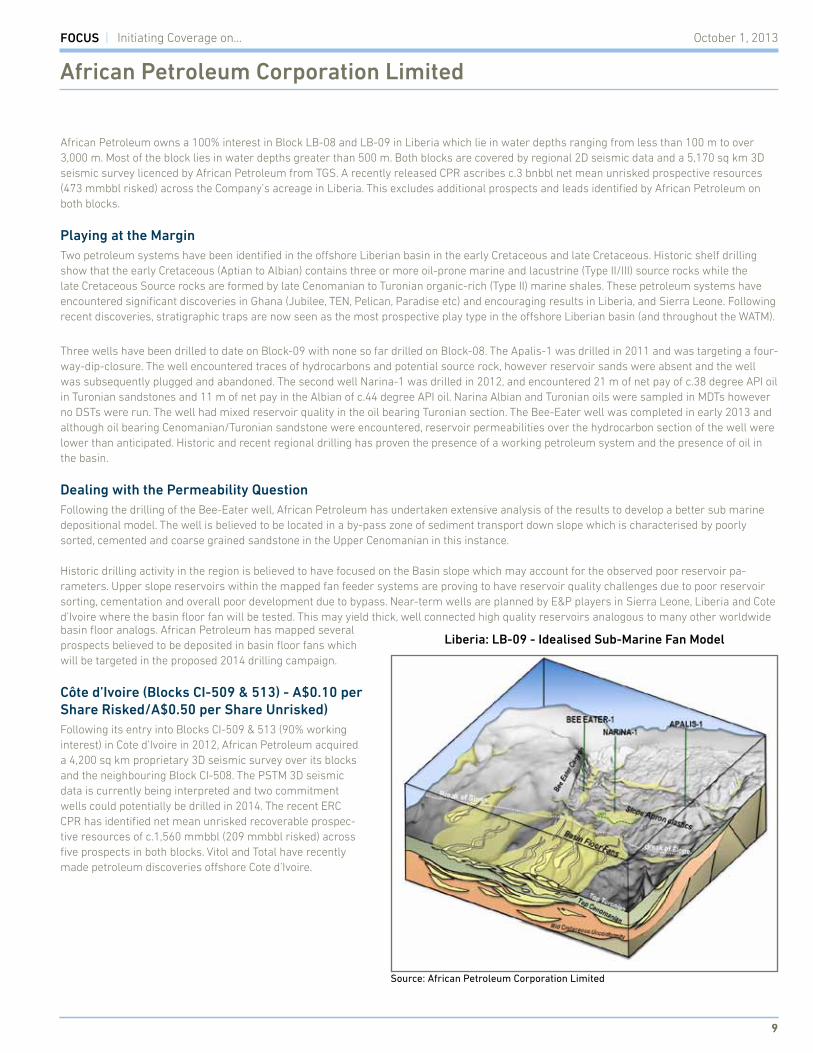

Idealized Sub‐Marine fan Model (Source: African Petroleum) Historic drilling activity in the region is believed to have focused on the Basin slope which may account for the reservoir potential of the sands. Recall from the Introduction section that significant discoveries to date have been from Turbidite sandstone reservoirs from the basin floor. Basin floor sandstone reservoirs are usually characterized by larger grain sizes, lower compaction, better sorting and better porosity and permeability. Approximately 7 ‐10 upcoming wells are scheduled to be drilled to test the down dip potential of the basin floor fans in the northern area of the Liberian basin while a further 11 wells will be drilled in the feeder/slope fan area. African Petroleum has mapped several prospects believed to be deposited in basin floor fans which will be targeted in the proposed 2014 drilling campaign.

Liberia: LB-09 - Idealised Sub-Marine Fan Model

Source: African Petroleum Corporation Limited

basin floor analogs. African Petroleum has mapped several prospects believed to be deposited in basin floor fans which will be targeted in the proposed 2014 drilling campaign.

Côte d’Ivoire (Blocks CI-509 & 513) - A$0.10 per Share Risked/A$0.50 per Share Unrisked)Following its entry into Blocks CI-509 & 513 (90% working interest) in Cote d’Ivoire in 2012, African Petroleum acquired a 4,200 sq km proprietary 3D seismic survey over its blocks and the neighbouring Block CI-508. The PSTM 3D seismic data is currently being interpreted and two commitment wells could potentially be drilled in 2014. The recent ERC CPR has identified net mean unrisked recoverable prospec-tive resources of c.1,560 mmbbl (209 mmbbl risked) across five prospects in both blocks. Vitol and Total have recently made petroleum discoveries offshore Cote d’Ivoire.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

10

Liberia/Sierra Leone Basin Overview

Source: African Petroleum Corporation Limited

Source: African Petroleum Corporation Limited

Cote d’Ivoire Acreage 3D Coverage

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

1111

Gambia Block A1 - Alhamdulilah Prospect

Source: African Petroleum Corporation Limited

Gambia (Blocks A1&A4) - A$0.13 per Share Risked/A$0.17 per Share UnriskedAfrican Petroleum has identified over 30 exploration prospects and leads across five different play types on its Blocks A1 and A4 (60% working interest) in the Gambia based on 3D data enabled subsurface analysis. The Alhamdulilah prospect according to the recent CPR ascribes mean unrisked recoverable prospective resources of c. 527 mmbbl (317 mmbbl risked). An exploration well which is scheduled to be drilled on the structure in 2014 will target stacked four way dip closures across stacked fan complexes.

Rufisque Offshore Profond & Senegal Offshore Sud Profond, Senegal African Petroleum licenced over 10,000 km of 2D seismic data over the Rufisque Offshore Profond (ROP) and Senegal Offshore Sud Profond (SOSP) and has subsequently completed a 3,600 sq km 3D seismic survey over the SOSP Block. Preliminary assessment of the 3D data has identified initial prospects and leads. In addition, 1,500 sq km of 3D seismic data over the ROP Block is currently being reprocessed ready for final interpretation in 3Q/4Q13.

Sierra Leone (Blocks SL-03 & SL-4A-10) The Company acquired a 100% interest of Block SL-4A-10, covering 1,995 sq km offshore Sierra Leone in September 2012, as part of Sierra Leone’s third offshore licencing round. A number of promising prospects have been identified on the licenced 2D seismic data. The Company is currently considering licencing previously acquired 3D seismic survey of Block SL-4A-10 to further analyse these prospects. The Company also holds a 100% interest of Block SL-03, which covers 3,860 sq km offshore Sierra Leone. The Company acquired 2,500 sq km of 3D seismic data over Block SL-03 in September 2011. Several Turonian to Campanian-aged prospective channel systems, located 70-100 km west of the Jupiter, Mercury and Venus discoveries have been identified from the seismic data.

Geared-up for Possible Exploration Success in 2014The Equatorial and Central Atlantic Margin is gearing up for arguably the most significant high impact drilling campaign to date in the region in the next 12-18 months. An estimated 38 wells could be drilled in the region and African Petroleum is proposing to drill up to five high impact exploration wells in 2014.

The Company initiated a farm-out process in February 2013 and remains optimistic that it will be able to farm down part of its high equity posi-tions prior to commencement of drilling in 2014. We anticipate that African Petroleum could potentially successfully execute its ongoing farm-out process on attractive terms.

African Petroleum in 2012 signed a MoU which gave Petrochina an exclusivity period to agree a 20% investment in Liberia block LB-09 and up to 20% in one or more of the Company’s exploration blocks. Although the exclusivity period elapsed in August 2012 without a firm investment, African Petroleum is continuing its discussions with Petrochina in the context of a potential investment.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

12

We highlight the sale of a 40% working interest to Tullow by Hyperdynamics which was completed in December 2012 as a potential benchmark of terms which could be achieved by African Petroleum. As consideration for the 40% working interest farm-out, Hyperdynamics received US$27 mm as reimbursement for past exploration costs and a carry for the Company’s participating interest share of future costs associated with drill-ing an exploration well in the deep water fan area of the concession, up to a gross expenditure cap of US$100 mm. Additionally, Tullow further agreed to pay Hyperdynamics’ proportionate share of costs associated with an appraisal of the initial exploration well in a success case and subject to a gross expenditure cap of US$100 mm.

Furthermore, the entry into Block LB-13 also provides a supplementary datapoint on potential farm-out terms that could be achieved by African Petroleum. ExxonMobil secured an 83% working interest from Canadian Overseas Petroleum in exchange for a well carry up to a maximum of US$120 mm plus the Company’s share of JV costs up to the completion of the first well. We have assumed the Company will be able to complete farm-out processes for all five wells scheduled for 2014 in an optimistic case (for 50% of its current working interest position) and three wells in a conservative scenario.

Source: IHS, Drilling Info & Various Company Websites

West African Transform Margin Drilling 2013/2014

African Petroleum Corporation Ltd | 2013 4

Upcoming Key wells – Catalysts for APCL portfolio

Gambia A1Operator: African Petroleum (60%)Planning to drill in 2013

Potential AOQ 12 Month Drilling Schedule(October 2013)

* We have assumed that African Petroleum could potentially reduce its WI by as much as 50% to secure attractive farm-out terms and well carry of up to 85% of well drilling costs. Source: African Petroleum Corporation Limited, FirstEnergy Capital LLP

Asset

Post Farm-out Net Unrisked Prospective

Resources

Post Farm-out Net Risked Prospective

ResourcesPre-Drill

WI (%)*Post Farm-

out WI (%)

Tentative Drilling

Schedule

Liberia - Lovebird Prospect 210.00 35.00 100 50 1H14Liberia - Sunbird Terrace Prospect 156.00 37.80 100 50 1H14Gambia - Alhamdulilah 95.10 28.08 60 30 2H14CI-509 - Leraba 186.30 14.27 90 45 2H14CI-513 - Ayame 225.90 27.95 90 45 2H14

Total 873.30 143.09

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

1313

Valuation

Risked DCF ApproachWe have used the Discounted Cash Flow (DCF) methodology to derive a US$/bbl metric for a conceptualised field develop-ment across African Petroleum’s assets and we put forward a Speculative Buy recommendation and target price at A$0.50 per share with an unrisked valu-ation of A$2.53 per share. Our valuation is predicated on the Company being able to successfully negotiate a minimum of three multi well carry out of the ongoing farm-out programme across its portfolio. We have elected to be conservative and assumed an equity raise of US$30 mm in 2H13 to hedge against the Company achieving a partial well carry for a mini-mum of three wells.

African Petroleum Asset Valuation

Net Unrisked Resources

(mmbbl)Unrisked

(US$ mm)EMV

(US$ mm)Risked

A$/ShareUnrisked

A$/Share % Total

Net Cash 43 43 0.02 0.02 3.9%G&A -50 -50 -0.02 -0.02 -4.5%

Total Core NAV -7 -7 -0.00 -0.00 -0.7%

Liberia - Narina-1 175 1,846 369 0.15 0.77 33.7%

Liberia - Lovebird Prospect 210 1,734 312 0.13 0.72 28.5%

Liberia - Sunbird Terrace Prospect 156 1,646 296 0.12 0.69 27.0%CI-513-Ayame 226 837 126 0.05 0.35 5.7%

Total Risked Exploration 6,063 1,103 0.46 2.53 100.7%

Total NAV 6,056 1,096 0.46 2.53 100.0%Unrisked NAV 2.53

P/Core NAV x N/A

P/NAV x 15.3%

P/Unrisked NAV x 2.8%

African Petroleum NAV(October 2013)

Source: FirstEnergy Capital LLP and Company Reports

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Net

Cas

h

G&

A

Tota

l Cor

e N

AV

Libe

ria

- N

arin

a-1

Libe

ria

- Lo

vebi

rd P

rosp

ect

Libe

ria

- S

unbi

rd T

erra

ceP

rosp

ect

CI-

513-

Aya

me

Tota

l NA

V

Ris

ked

NA

V C

ontr

ibu

tion

(A

$/s

har

e)

Core NAV RENAV

Current Share Price

African Petroleum Valuation Waterfall(October 2013)

Source: FirstEnergy Capital LLP

African Petroleum doesn’t hold producing, near term production or undeveloped contingent resources and hence the core NAV is insignificant. Our risked NAV is based on prospects we believe will be targeted in the next 12 months. We have used African Petroleum’s development cost estimates in our valuation except in instances where these have been provided by an independent reserves audit.

An outline of the contribution to core NAV and risked exploration is presented herein.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

14

Comparison to PeersWe have compared African Petroleum to the Sub-Saharan focused E&P players in our international coverage universe and the Company screens favorably on a P/ReNAV and P/Unrisked NAV metrics. The Company offers risked and unrisked upside of c.4x and 21x respectively to current trading levels assuming our conservative 2014 drilling programme.

Valuation SensitivityWe present the impact to our target price for changes in the discount rate ranging from 8-20% and also assess the impact of volatil-

(*) Currently negotiating with the Gambian government for extension of commitmentSource: African Petroleum Corporation Limited

Petroleum Fiscal Terms

African Petroleum Corporation Ltd | 2013 Corporate Presentation | 6

Activities & Fiscal Terms of AssetsCountry Block(s) Contract Type Interest in PSC Activities to Date

Cote d’Ivoire CI-509 and CI-513Production Sharing

Contract(PSC)

90%(10% PETROCI)

• APCL was awarded block CI-509 in March 2012 & CI-513 in December 2011 covering 2,537 km2

• Final 3D seismic data delivered June 2013• APCL planning exploration drilling in 2014

The Gambia A1 and A4 Petroleum Agreement with Royalty

60%(40% Buried

Hill)

• APCL farmed-in into A1 and A4 in 2010• Both blocks are covered by 3D seismic data, covering 2,500 km2

• APCL one well commitment by December 2013

Liberia LB-08 and LB-09

Production Sharing Contract(PSC)

First 10 Years Tax Free Holiday

100%

• APCL was awarded Blocks LB-08 and LB-09 in 2005• PSC ratified in 2008• Acquired 5,200 km2 of 3D seismic data on both blocks• APCL drilled Apalis-1, Narina-1 and Bee Eater-1 Wells on LB-09• APCL planning drilling in 2014

Senegal

Rufisque Offshore Profond

andSenegal Offshore

Sud Profond

Production Sharing Contract(PSC)

81%(10% PetroSen)(9% Prestamex)

• APCL was awarded “Rufisque Offshore Profond & Senegal OffshoreSud Profond” blocks in November 2011

• In May 2012 APCL acquired over 3,600 km2 of 3D seismic data• Final 3D seismic was delivered in June 2013

Sierra Leone SL-03 and SL-04A Petroleum Agreement with Royalty 100%

• SL-03 was ratified by the Sierra Leone Parliament in February 2011• SL-04A was ratified by the Sierra Leone Parliament in September 2012• APCL acquired 2,500 km2 of 3D seismic on block SL-03 in September

2011• Currently interpreting 3D seismic data on block SL-03

Source: FirstEnergy Capital LLP

African Coverage Universe Upside Comparison(October 2013)

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

TLW LN AFR LN HOIL LN CRCL LN ELA LN AOI CN OPHR LN WRL LN AOQ AU

Premium/Discount for FCC Africa Focused E&P Plays

P/Unrisked NAV (12 Mths) P/RENAV (12 Mths)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

8.0% 10.0% 12.5% 15.0% 18.0% 20.0%

Ris

ked

NA

V (

A$

/Sh

are)

Risked NAV Sensitivity to Discount Rate and Oil Price

70 80 90 100 110 120

ity in oil price around a price range of between US$60 to US$120 bbl in so far as to determine the extent of the range in US$/bbl NPV metrics.

Petroleum Fiscal Terms Africa Petroleum’s concessions are governed by a mixture of Production Sharing and Tax & Royalty Petroleum agreements. An overview of the terms are highlighted below

Variation in Risked NAV to Variation in Discount Rate & Oil Price (October 2013)

Source: FirstEnergy Capital LLP

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

1515

Capital Raising History, Structure and ShareholdersAfrican Petroleum has approximately 1,695,433,051 outstanding shares in issue and free float is 54%. Options in issue as at July 4, 2013 stood at 39,188,191 with exercise price ranging from A$0.30 - A$1.25 and maturities from 2015 - 2018 (management and board holds c.16 mm options with exercise price ranging from A$0.30 - A$1.00). Current cash position stands at c.US$20 mm.

Despite the strong institutional backing, African Petroleum in the last 12 months has traded an average of c.14.7 mm on a monthly basis (c.0.7 mm shares daily). We attribute this predominantly to the Company’s historic listing on the National Stock Exchange of Australia. Africa Petroleum has signaled its intention to list on the Australian Securities Exchange to address concerns on governance and transparency, gain access to a wider institutional base and improve liquidity. The process is currently ongoing.

We have attempted to capture the extent of exposure to economic, geopolitical, geological and financial risks that the Company may encounter over the mid-near term and offer our views on some factors that may serve to mitigate or negate the impact of the risk.

Security and GeopoliticsAfrican Petroleum is exposed to varying levels of political risks across the five countries where it currently holds acreage. The Gambia has expe-rienced several coups and coup attempts although the incumbent president won his 4th elected term in 2011 in an election that was criticised for legitimacy. Cote d’Ivoire also experienced coups and attempted coups and the country most recently witnessed an election stalemate in 2010 which was subsequently resolved in 2011. Senegal is often regarded as one of the African continent’s stable democracies and has experienced one coup in 1962. Liberia and Sierra Leone have also both undergone coups and wars. Liberia underwent two civil wars in 1989-1996 and 1999-2003 and Sierra Leone went through a decade long civil war from 1991- 2002. It is worth noting that despite the political upheavals the various countries have gone through, the natural resource sector has remained resilient and significantly contributed to its GDP. According to the 2012 Mo Ibrahim Index of African Governance, Senegal scores favorably with a rank of 16th while Cote d’Ivoire, Gambia, Sierra Leone and Liberia rank 46th, 27th, 30th and 34th respectively.

Fiscal and EconomicWith the recent rise in resource nationalism in some African jurisdictions following discovery of petroleum, we highlight that there remains latent fiscal terms risk in some or all of African Petroleum’s assets. The Liberian legislature has in recent year’s been actively involved in the evolution of the Liberian oil & gas industry, proposing a revision of all PSCs granted in the country and adopting a local content law to ensure that local companies participate in the development of the petroleum industry.

Geological The results of African Petroleum’s drilling to date highlights the subsurface risks associated with exploration drilling. Despite the advances in seismic processing and other exploration tools, petroleum exploration remains inherently risky with potential for big pay-offs as well as big losses to deployed capital. However we still view the upside as substantial, particularly in frontier exploration drilling where investor response to well successes or failures can often be disproportionate. We highlight that African Petroleum has assembled a technical team led by Jens Pace (Chief Operating Officer) and Michael Barrett (Exploration Director) who bring significant large cap company experience to the subsurface work for African Petroleum. The Company has to date spent significant amounts of capital acquiring extensive swathes of 3D seismic data which guides the selection of prospects for the proposed exploration programme in the near-term.

Risks and Mitigants

Investor *Shareholding %Directors, Management & Employees 635,660,687 37.5Dundee Corporation 149,602,310 8.8Capital Research Global Investors 125,308,463 7.4M&G Investment Management 113,457,536 6.7Banque Heritage 90,935,679 5.4Baillie Gifford & Co 73,641,946 4.3Private Stakeholders (Cyprus) 52,486,760 3.1Henderson Global Investors 33,106,494 2.0Salida Capital 28,225,722 1.7Goldman Sachs Investment Partners 26,972,136 1.6

Total 1,329,397,733 78.5*As at 30th August, 2013

Date No of Shares (mm) Price/Share (A$)Gross Proceeds

(A$ mm)

May-11 193 (1st Tranche) 1.00 193Jul-11 57 (2nd Tranche) 1.00 57Jul-12 62.693 1.35 85Jun-10 403.63 0.55 222

Total 557.0Source: African Petroleum Corporation Limited

Equity Capital Raise History(August 2013)

Source: African Petroleum Corporation Limited

Top Shareholding(August 2013)

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

16

Management

FinancialAfrica Petroleum’s cash balance as at August 12, 2013 stands at US$20 mm excluding a restricted cash balance of US$12 mm held as security for the drilling work programme in Cote d’Ivoire. The Company, given its current exploration focus, does not have any revenue and will need to access the Equity Capital Markets to continue its drilling campaign. We highlight that this is mitigated by the Company’s high working interest across its portfolio which provides the optionality to farm-down its interest for a potential well carry and reimbursement of past exploration costs.

Financial Estimates

Board and Management

Frank Timis* - Non-Executive Chairman

Mr Timis is the founder of numerous resource companies listed in London, Australia and Toronto. Mr Timis is also Executive Chairman fo African Minerals and a Non-Executive Director with International Petroleum Limited.

Fin&Op’s(October 2013)

Source: FirstEnergy Capital LLP and Company Reports

YEAR END DEC 31, 2012a 2013e 2014e 2015e YEAR END DEC 31, 2012a 2013e 2014e 2015e

PRODUCTION VALUATION

Oil & Liquids Bbl/d 0 0 0 0 Share Price Y/E A$/Share 0.12 0.12 0.12 0.12

Natural Gas mmcf/d 0 0 0 0 Net Asset Value A$/Share 0.00 0.00 0.00 0.00

Total Production Boe/d 0.0 0.0 0.0 0.0 Risked NAV A$/Share 0.46 0.46 0.46 0.46

Production per ShareBoe/Share (000 0.00 0.00 0.00 0.00 Price/Core NAV % N/A N/A N/A N/A

% % N/A N/A N/A N/A Price/Risked NAV % 26.2% 26.2% 26.2% 26.2%

Production per D.A. ShareBoe/Share (000) 0.00 0.00 0.00 0.00 P/CF x N/A N/A N/A N/A% N/A N/A N/A N/A P/E x N/A N/A N/A N/A

DACFM x N/A N/A N/A N/A

Target DACFM x N/A N/A N/A N/ACAPITALIZATION EV per boe/d US$/Boed N/A N/A N/A N/A

Exit Net Debt US$mm (104) (17) (27) (77) Target EV per boe/d US$/Boed N/A N/A N/A N/A

Entry Debt/CF Years N/A N/A N/A N/A EBITDA US$/boe N/A -43 -15 -15

Basic Shares mm 1,695.4 2,135.4 2,135.4 2,325.4 EV/EBITDA US$/boe N/A N/A N/A N/A

Options mm 33.7 39.7 39.7 39.7

Warrants mm 0.0 0.0 0.0 0.0 FINANCIAL PERFORMANCE

Convertible Debentures mm 0.0 0.0 0.0 0.0 Cash Flow

Diluted Shares mm 1,729 2,175 2,175 2,365 Cash Flow US$mm -21.0 -26.4 -14.3 -13.5

Fully Diluted Shares mm 1,735 2,175 2,175 2,365 Cash Flow Netback US$/boe N/A N/A N/A N/A

Market Cap. US$mm 207.5 261.0 261.0 283.8 Cash Flow Per Share US$/share -0.02 -0.01 -0.01 -0.01

Enterprise Value US$mm 103.7 244.1 234.0 206.8 % Change Year-Over-Year % N/A 0.5x 1.1x 0.1xEarnings

YIELD Earnings US$mm -40.3 -46.7 -14.3 -13.5

Dividend US$mm 0.0 0.0 0.0 0.0 Earnings Per Diluted Share US$/share -0.04 -0.02 -0.01 -0.01

Yield % N/A N/A N/A N/A % Change Year-Over-Year Basic N/A 0.6x 2.6x 0.1x

Capital ExpendituresPRICE FORECAST Capex US$mm 212.9 72.1 27.0 30.0

Brent $US 111.68 107.48 100.87 100.00 Capex vs. Cash Flow % N/A N/A N/A N/A

Oil $US wellhd N/A N/A N/A N/A Debt

Natural Gas $US wellhd N/A N/A N/A N/A Total Debt US$mm 0.0 0.0 0.0 0.0

Exchange Rate US$ / A$ 0.94 1.10 1.10 1.10 Exit Net Debt US$mm N/A -16.9 -27.1 -77.1

note: net income must be fixed to mean net income to common

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

1717

Karl Thompson - Executive Director and CEO

Petroleum Explorationist with 28 years of technical, operational and managerial experience in the E&P sector. Previously spent 18 years with Chevron in various capacities.

Mark Ashurst - Executive Director and CFO

Experienced Senior Investment Banker with a broad range of corporate finance and broking skills gained from over 20 years in the City of Lon-don. Previously employed with Hoare Govett and Canaccord Adams.

Jens Pace - Chief Operating Officer

Experienced Geoscientist with over 30 years’ experience in the E&P industry. Previously held senior positions at BP where he worked for over 10 years.

Michael Barrett - Exploration Director

Experienced Explorationist with over 20 years’ spent mostly with Chevron. Most recently employed with Addax/Sinopec International.

Pierre Raillard - Director West Africa

Experienced operational and project management professional with over 20 years’ experience work experience (10+ years in Sub-Saharan Africa).

Non-Executive Board Members

Gibril Bangura

Mr Bangura is an Executive Director of African Minerals Limited and has been a non-executive director of the Company since 2010.

Jeffrey Couch

Mr. Couch has over 15 years of investment banking and capital markets experience and is currently a Managing Director and Head of Investment and Corporate Banking Europe for BMO Capital Markets.

Timothy Turner*

Mr Turner has in excess of 21 years’ experience in new venture, capital raisings and general business consultancy. Mr Turner is currently Non-Executive Director at Cape Lambert Resources, Legacy Iron Limited and International Petroleum Limited.

David King

Dr King is a professional geoscientist and has over 30 years’ experience in oil and gas and other natural resources industries. Dr. King is cur-rently non-executive Chairman of ASX listed Robust Resources Limited and Cellmid Limited.

Anthony Wilson

Mr Wilson was previously Finance Director for BZW Securities and BZW Asset Management over a period of 10 years.

James N. Smith

Mr Smith is a senior oil and gas executive with over 20 years’ experience and a strong geology background.

* - African Petroleum as part of its proposed listed on the ASX will be replacing Frank Timis and Timothy Turner with Charles Matthews and Gordon Grieve on the Board of Directors. Additionally Frank Timis will be appointed as President of the Executive Committee.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

18

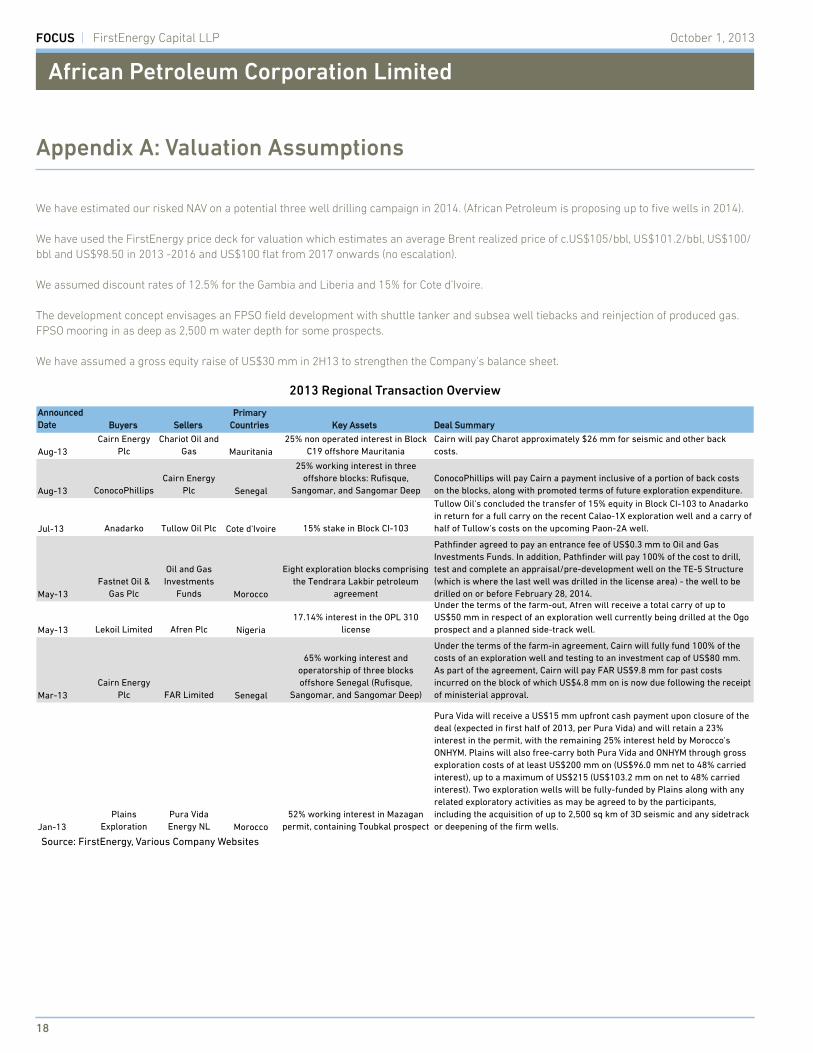

Appendix A: Valuation Assumptions

We have estimated our risked NAV on a potential three well drilling campaign in 2014. (African Petroleum is proposing up to five wells in 2014). We have used the FirstEnergy price deck for valuation which estimates an average Brent realized price of c.US$105/bbl, US$101.2/bbl, US$100/bbl and US$98.50 in 2013 -2016 and US$100 flat from 2017 onwards (no escalation).

We assumed discount rates of 12.5% for the Gambia and Liberia and 15% for Cote d’Ivoire.

The development concept envisages an FPSO field development with shuttle tanker and subsea well tiebacks and reinjection of produced gas. FPSO mooring in as deep as 2,500 m water depth for some prospects.

We have assumed a gross equity raise of US$30 mm in 2H13 to strengthen the Company’s balance sheet.

Announced Date Buyers Sellers

Primary Countries Key Assets Deal Summary

Aug-13Cairn Energy

PlcChariot Oil and

Gas Mauritania25% non operated interest in Block

C19 offshore MauritaniaCairn will pay Charot approximately $26 mm for seismic and other back costs.

Aug-13 ConocoPhillipsCairn Energy

Plc Senegal

25% working interest in three offshore blocks: Rufisque,

Sangomar, and Sangomar DeepConocoPhillips will pay Cairn a payment inclusive of a portion of back costs on the blocks, along with promoted terms of future exploration expenditure.

Jul-13 Anadarko Tullow Oil Plc Cote d'Ivoire 15% stake in Block CI-103

Tullow Oil's concluded the transfer of 15% equity in Block CI-103 to Anadarko in return for a full carry on the recent Calao-1X exploration well and a carry of half of Tullow's costs on the upcoming Paon-2A well.

May-13Fastnet Oil &

Gas Plc

Oil and Gas Investments

Funds Morocco

Eight exploration blocks comprising the Tendrara Lakbir petroleum

agreement

Pathfinder agreed to pay an entrance fee of US$0.3 mm to Oil and Gas Investments Funds. In addition, Pathfinder will pay 100% of the cost to drill, test and complete an appraisal/pre-development well on the TE-5 Structure (which is where the last well was drilled in the license area) - the well to be drilled on or before February 28, 2014.

May-13 Lekoil Limited Afren Plc Nigeria17.14% interest in the OPL 310

license

Under the terms of the farm-out, Afren will receive a total carry of up to US$50 mm in respect of an exploration well currently being drilled at the Ogo prospect and a planned side-track well.

Mar-13Cairn Energy

Plc FAR Limited Senegal

65% working interest and operatorship of three blocks offshore Senegal (Rufisque,

Sangomar, and Sangomar Deep)

Under the terms of the farm-in agreement, Cairn will fully fund 100% of the costs of an exploration well and testing to an investment cap of US$80 mm. As part of the agreement, Cairn will pay FAR US$9.8 mm for past costs incurred on the block of which US$4.8 mm on is now due following the receipt of ministerial approval.

Jan-13Plains

ExplorationPura Vida Energy NL Morocco

52% working interest in Mazagan permit, containing Toubkal prospect

Pura Vida will receive a US$15 mm upfront cash payment upon closure of the deal (expected in first half of 2013, per Pura Vida) and will retain a 23% interest in the permit, with the remaining 25% interest held by Morocco's ONHYM. Plains will also free-carry both Pura Vida and ONHYM through gross exploration costs of at least US$200 mm on (US$96.0 mm net to 48% carried interest), up to a maximum of US$215 (US$103.2 mm on net to 48% carried interest). Two exploration wells will be fully-funded by Plains along with any related exploratory activities as may be agreed to by the participants, including the acquisition of up to 2,500 sq km of 3D seismic and any sidetrack or deepening of the firm wells.

Source: FirstEnergy, Various Company Websites

2013 Regional Transaction Overview

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

1919

Appendix B: Company History

2008 Ratification of Liberia Block LB-08 and LB-09.

2010June – Listed on the National Stock Exchange of Australia (NSX). June – A$222 mm raised in placing.August – Farm-in with Buried Hill, two Blocks offshore The Gambia (A1 and A4).

2011February – Block awarded offshore Sierra Leone (SL-03). June – A$250 mm raised in placing. August – First well spud in Liberia Block, Apalis-1 (LB-09). November – Two Blocks awarded offshore Senegal (Rufisque and Sud Profond).

2012January – Block awarded offshore Côte d’Ivoire (CI-513). February – Significant discovery made at Narina-1 (32m net pay). March – Block awarded offshore Côte d’Ivoire (CI-509). July – A$85 mm raised from placing. September – Block awarded offshore Sierra Leone (SL-4A-10).

2013January – Publication of ERC Equipoise CPRFebruary 2013 – Completion of Bee-Eater Well. Oil discovery although permeability lower than expected.July – Release of ERC Equipoise CPR.

Appendix C: Asset Description

OverviewThe Company’s assets are spread across the West African coast from Senegal to Cote d’Ivoire with exposure to 10 bnbbl of gross unrisked pro-spective resources (1.7 bnbbl risked) according to internal management estimates. The combined acreage covers a total of 31,878 km2 making it among the largest offshore net acreage holders of the West African Transform Margin. The Company benefits from a high degree of optional-ity given the high working interests, in the range of 60% to 100% offering the ability for farm-down to mitigate risk and capital exposure to high impact drilling.

African Petroleum’s assets are located at the very centre within one of the busiest periods of exploration drilling in West Africa that will stretch from Cote d’Ivoire to Mauritania and Morocco. The region is likely to witness multiple high impact catalysts over the coming months with a series of wells drilled offshore Sierra Leon (1 well), Liberia (4 wells), Morocco (1 well), Cote d’Ivoire (1 well). The region has already experienced multiple wells drilled to date that covers Liberia, Cote d’Ivoire, Sierra Leone as well as more frontier regions such as The Gambia.

Liberia The Company holds a 100% working interest in Blocks LB-08 and LB-09 offshore Liberia, the blocks are located within the region of acreage already held by ExxonMobil (XOM US)/Canadian Overseas Petroleum (COPL) (Block LB13) and Anadarko in block LB-10. The Company was awarded the blocks in 2005 with the PSC being ratified in 2008 and following the end of the first exploration phase, incurring a 25% relinquish-ment, the acreage covers a total of 5,351 km2. Play types include a combination of both structural and stratigraphic types presenting a degree of geological diversity. A number of leads and prospects have been established on the acreage that includes both play types.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

20

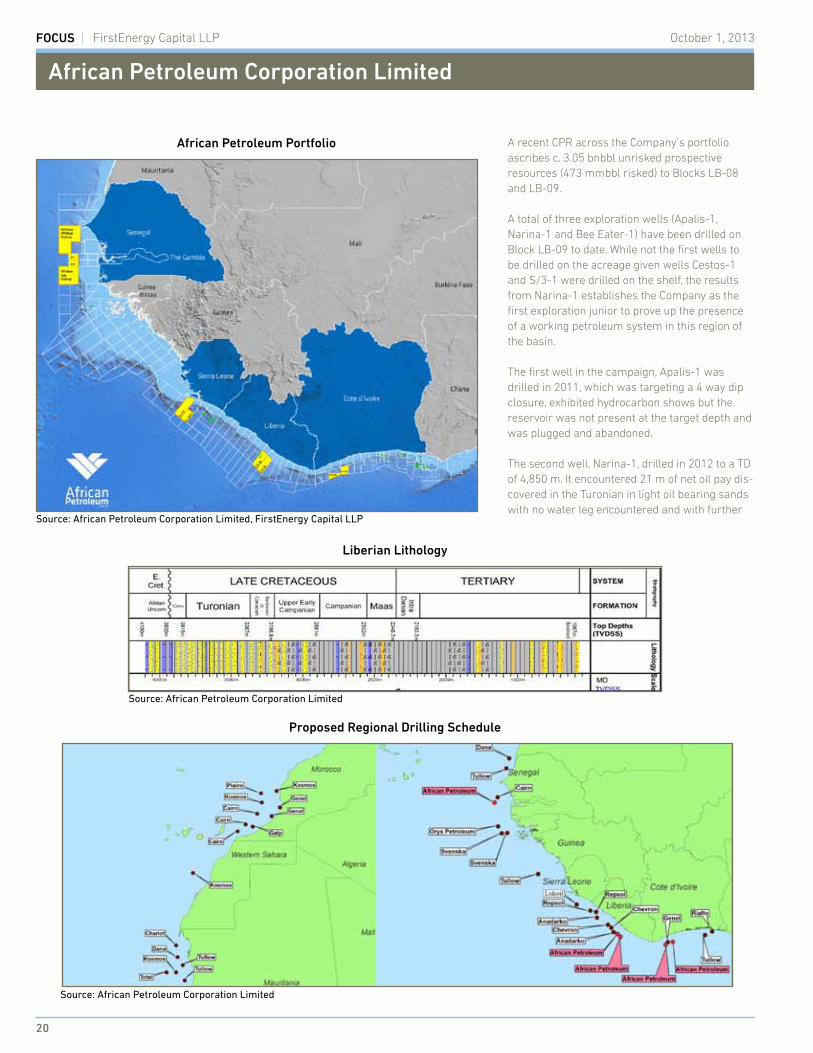

A recent CPR across the Company’s portfolio ascribes c. 3.05 bnbbl unrisked prospective resources (473 mmbbl risked) to Blocks LB-08 and LB-09.

A total of three exploration wells (Apalis-1, Narina-1 and Bee Eater-1) have been drilled on Block LB-09 to date. While not the first wells to be drilled on the acreage given wells Cestos-1 and S/3-1 were drilled on the shelf, the results from Narina-1 establishes the Company as the first exploration junior to prove up the presence of a working petroleum system in this region of the basin.

The first well in the campaign, Apalis-1 was drilled in 2011, which was targeting a 4 way dip closure, exhibited hydrocarbon shows but the reservoir was not present at the target depth and was plugged and abandoned.

The second well, Narina-1, drilled in 2012 to a TD of 4,850 m. It encountered 21 m of net oil pay dis-covered in the Turonian in light oil bearing sands with no water leg encountered and with further

African Petroleum Portfolio

Source: African Petroleum Corporation Limited, FirstEnergy Capital LLP

African Petroleum Corporation Ltd | 2013 Corporate Presentation | 15

West African Transform Margin 2013/2014 Drilling(Anticipated 38 Wells to be drilled)

West-Saharan Africa (16 Wells) Sub-Saharan Africa (22 Wells)

Source: - IHS- Drilling Info- Companies’ Presentation Materials

Proposed Regional Drilling Schedule

Source: African Petroleum Corporation Limited

Liberian Lithology

Source: African Petroleum Corporation Limited

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

2121

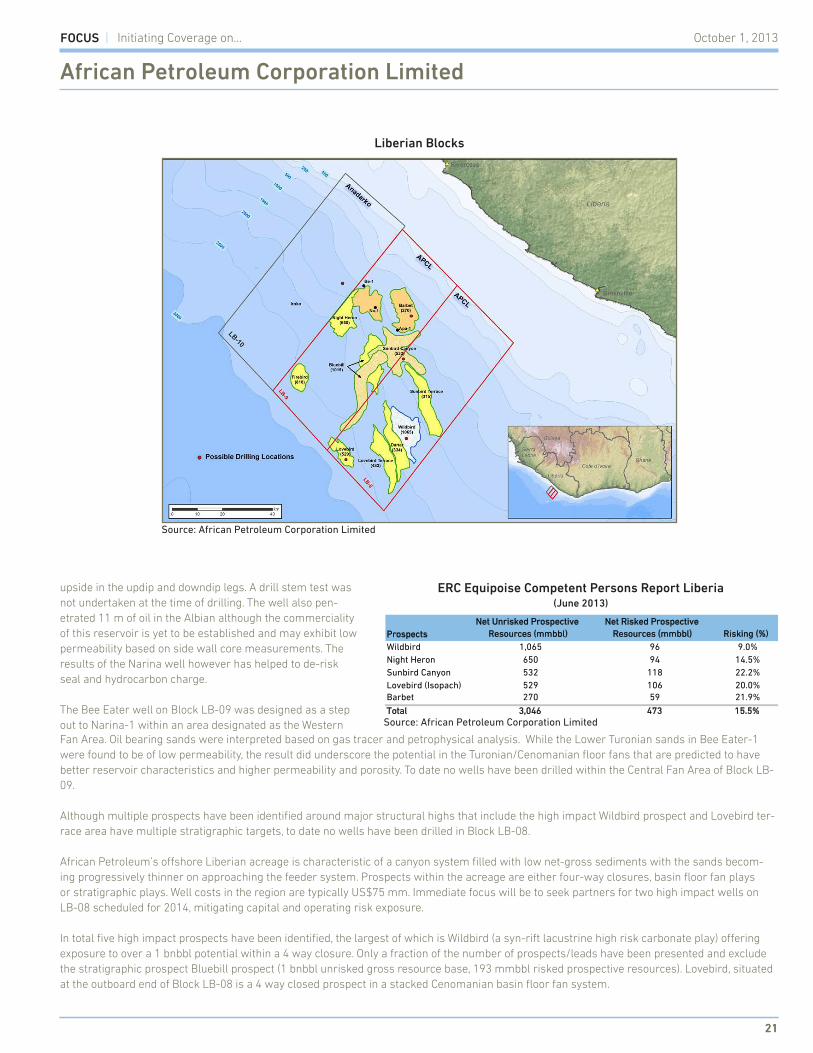

Liberian Blocks

Source: African Petroleum Corporation Limited

upside in the updip and downdip legs. A drill stem test was not undertaken at the time of drilling. The well also pen-etrated 11 m of oil in the Albian although the commerciality of this reservoir is yet to be established and may exhibit low permeability based on side wall core measurements. The results of the Narina well however has helped to de-risk seal and hydrocarbon charge.

The Bee Eater well on Block LB-09 was designed as a step out to Narina-1 within an area designated as the Western

ERC Equipoise Competent Persons Report Liberia(June 2013)

Source: African Petroleum Corporation Limited

ProspectsNet Unrisked Prospective

Resources (mmbbl)Net Risked Prospective

Resources (mmbbl) Risking (%)Wildbird 1,065 96 9.0%Night Heron 650 94 14.5%Sunbird Canyon 532 118 22.2%Lovebird (Isopach) 529 106 20.0%Barbet 270 59 21.9%

Total 3,046 473 15.5%

Fan Area. Oil bearing sands were interpreted based on gas tracer and petrophysical analysis. While the Lower Turonian sands in Bee Eater-1 were found to be of low permeability, the result did underscore the potential in the Turonian/Cenomanian floor fans that are predicted to have better reservoir characteristics and higher permeability and porosity. To date no wells have been drilled within the Central Fan Area of Block LB-09.

Although multiple prospects have been identified around major structural highs that include the high impact Wildbird prospect and Lovebird ter-race area have multiple stratigraphic targets, to date no wells have been drilled in Block LB-08.

African Petroleum’s offshore Liberian acreage is characteristic of a canyon system filled with low net-gross sediments with the sands becom-ing progressively thinner on approaching the feeder system. Prospects within the acreage are either four-way closures, basin floor fan plays or stratigraphic plays. Well costs in the region are typically US$75 mm. Immediate focus will be to seek partners for two high impact wells on LB-08 scheduled for 2014, mitigating capital and operating risk exposure.

In total five high impact prospects have been identified, the largest of which is Wildbird (a syn-rift lacustrine high risk carbonate play) offering exposure to over a 1 bnbbl potential within a 4 way closure. Only a fraction of the number of prospects/leads have been presented and exclude the stratigraphic prospect Bluebill prospect (1 bnbbl unrisked gross resource base, 193 mmbbl risked prospective resources). Lovebird, situated at the outboard end of Block LB-08 is a 4 way closed prospect in a stacked Cenomanian basin floor fan system.

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

22

Sierra LeoneAfrican Petroleum holds a 100% interest in offshore Blocks SL-03 and SL-4A-10. A 3D seismic programme has been acquired on Block SL-03 and is presently under evaluation while a 3D programme has been acquired by PGS on Block SL-4A-10 and African Petroleum is consid-ering purchasing the data. To date SL-03 holds multiple leads and a single prospect, Altair, holding net unrisked prospective resources of 434 mmbbl with a 18% GCoS. Water depth is likely to be greater than 3,000 m. Full stack PSTM has been acquired through the prospect that clearly exhibits a well-defined channel with an underlying syn rift system.

The Company’s acreage is characterised by three large fan play in this acreage with Canyon feeders from the top Albian pushing out into fan systems into the Top Turonian that includes a south trending fault running perpendicular to the main feeder that constitute two of three fan systems.

Approximately 7-10 upcoming wells are scheduled to be drilled to test the down dip potential of the basin floor fans in the northern area of the Liberian basin while a further 11 wells will be drilled in the feeder/slope fan area.

The greatest risk in the Sierra Leone basin is trapping and reservoir quality.

Sierra Leone Licenced Blocks & Prospects

Source: African Petroleum Corporation Limited

Sierra Leone Blocks

Source: African Petroleum Corporation Limited

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

2323

Senegal/The GambiaThe largest drill ready prospects identified to date in The Gambia is that of the Alhamdulilah situated in the northern part of Block A1 along with M prospects offering exposure to a combined 356 mmbbl unrisked prospective resources upside. The Alhamdulilah prospect is a stacked fan complex in the Jurassic, Barremian, Aptian, Albian and Cenomanian. There is however little well control in the region. Within blocks A1 and A4 multiple leads have been mapped that covers a couple of play types that are categorised into channel/fan complexes in deeper water areas and carbonate platform plays. In total five dif-ferent play types have been identified.

The immediate focus will be on the submarine fan systems draped over the prospect with target objectives to include the Cretaceous and Jurassic reservoir systems. It must be noted that only the Jurassic is reflected in the resources estimates. Despite reservoir depths the rig spread rate is understood to be lower due to lack of requirement for multiple drill strings translating into typical well costs in the order of US$75 mm on the proviso of no HP/HT conditions. Drilling activity on the Gambia licence is unlikely any time before mid 2014 and could involve either M or Alhamdulilah prospects.

All first phase seismic data commitments have been met on both blocks. African Petroleum holds a 81% working interest in this acre-age with Senegalese state entity Petrosen holding the balance. On the Rufisque Offshore Profond (ROP), that covers an area of 18,277

Licenced Block (Senagal/The Gambia)

Source: African Petroleum Corporation Limited

Prospects & Leads Mapping

Source: African Petroleum Corporation Limited

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

24

3D Amplitude Extraction of Fan Sand Bodies Offshore The Gambia

Source: African Petroleum Corporation Limited

Source: African Petroleum Corporation Limited

Licence Blocks & Mapped Prospects (Senegal & Gambia)

km2 in water depths of 500 m to 3,500 m there is a commitment to drill one exploration well by October 2015 over a four year exploration licence period. The Senegalese licences have a total exploration period of eight years and a long 25 year development period. The inherent risk is around reservoir quality particularly at increased reservoir depths. A follow up well to the M or Alhamdullilah prospects will likely be drilled on the ROP licence by October 2015.

While the auditor reflected the Cretaceous, Jurassic reservoir systems in the volumetrics estimate, any contribution from the Jurassic interval and repre-sents further potential upside was discounted.

ERC Equipoise Competent Persons Report Senegal(June 2013)

Source: African Petroleum Corporation Limited

ProspectsNet Unrisked Prospective

Resources (mmbbl)Net Risked Prospective

Resources (mmbbl) Risking (%)Alhamdullilah 316 49 15.5%M 40 4 10.0%

Total 356 53 14.9%

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

2525

Cote d’IvoireAfrican Petroleum was awarded the Blocks CI-509 and CI-513 in 2012. The blocks cover a combined area of 2,537 km2 and African Petroleum operates the blocks at a 90% working interest with the balance held by state entity Petroci. A full 3D PSTM data set has been acquired and is

Cote d’Ivoire Prospect Mapping

Source: African Petroleum Corporation Limited

African Petroleum Cote d’Ivoire Blocks

Source: African Petroleum Corporation Limited

currently under interpretation.

A total of two respective exploration wells are scheduled for 2014 across African Petroleum’s block with the target objective being the Upper Creta-ceous submarine fan systems. There is much less play diversification in the Cote d’Ivoire prospects when compared with prospects offshore Liberia or play diversify of The Gambia. The wells are expected to target deep water upper Cretaceous submarine fans (Albian deltaic systems).

FOCUS | FirstEnergy Capital LLP October 1, 2013

African Petroleum Corporation Limited

26

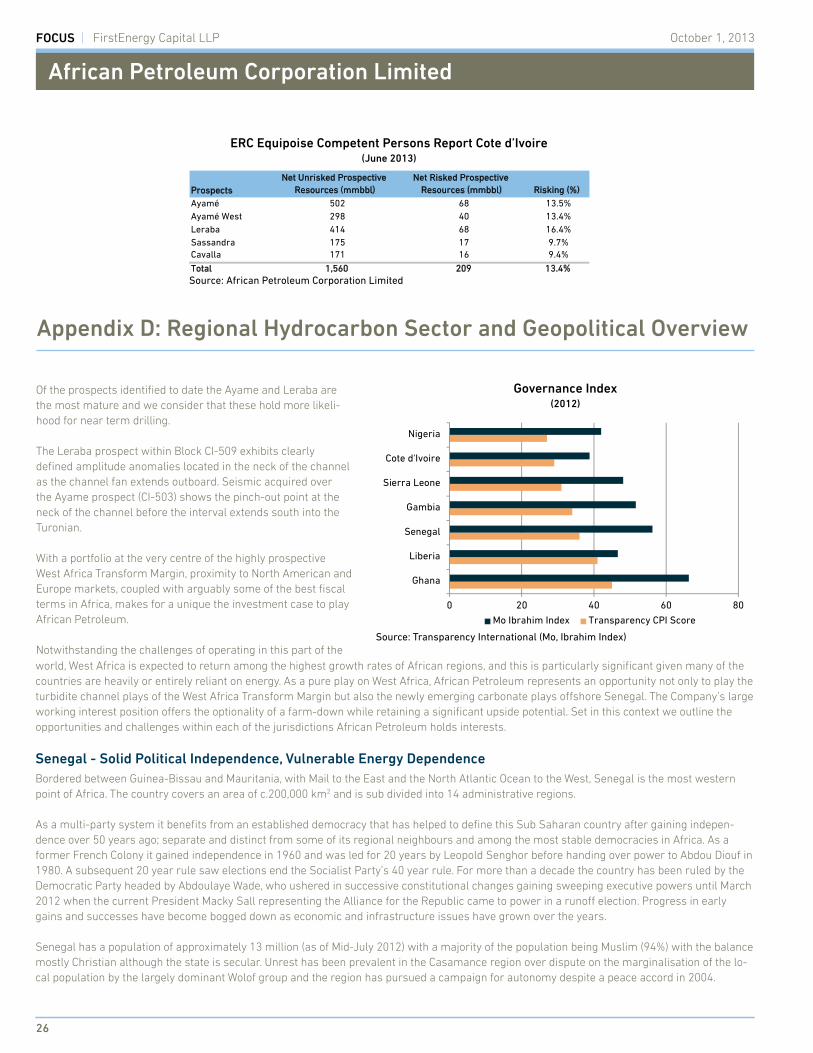

ERC Equipoise Competent Persons Report Cote d’Ivoire(June 2013)

Source: African Petroleum Corporation Limited

Appendix D: Regional Hydrocarbon Sector and Geopolitical Overview

Of the prospects identified to date the Ayame and Leraba are the most mature and we consider that these hold more likeli-hood for near term drilling.

The Leraba prospect within Block CI-509 exhibits clearly defined amplitude anomalies located in the neck of the channel as the channel fan extends outboard. Seismic acquired over the Ayame prospect (CI-503) shows the pinch-out point at the neck of the channel before the interval extends south into the Turonian.

With a portfolio at the very centre of the highly prospective West Africa Transform Margin, proximity to North American and Europe markets, coupled with arguably some of the best fiscal terms in Africa, makes for a unique the investment case to play African Petroleum. Notwithstanding the challenges of operating in this part of the world, West Africa is expected to return among the highest growth rates of African regions, and this is particularly significant given many of the countries are heavily or entirely reliant on energy. As a pure play on West Africa, African Petroleum represents an opportunity not only to play the turbidite channel plays of the West Africa Transform Margin but also the newly emerging carbonate plays offshore Senegal. The Company’s large working interest position offers the optionality of a farm-down while retaining a significant upside potential. Set in this context we outline the opportunities and challenges within each of the jurisdictions African Petroleum holds interests.

Senegal - Solid Political Independence, Vulnerable Energy DependenceBordered between Guinea-Bissau and Mauritania, with Mail to the East and the North Atlantic Ocean to the West, Senegal is the most western point of Africa. The country covers an area of c.200,000 km2 and is sub divided into 14 administrative regions.

As a multi-party system it benefits from an established democracy that has helped to define this Sub Saharan country after gaining indepen-dence over 50 years ago; separate and distinct from some of its regional neighbours and among the most stable democracies in Africa. As a former French Colony it gained independence in 1960 and was led for 20 years by Leopold Senghor before handing over power to Abdou Diouf in 1980. A subsequent 20 year rule saw elections end the Socialist Party’s 40 year rule. For more than a decade the country has been ruled by the Democratic Party headed by Abdoulaye Wade, who ushered in successive constitutional changes gaining sweeping executive powers until March 2012 when the current President Macky Sall representing the Alliance for the Republic came to power in a runoff election. Progress in early gains and successes have become bogged down as economic and infrastructure issues have grown over the years.

Senegal has a population of approximately 13 million (as of Mid-July 2012) with a majority of the population being Muslim (94%) with the balance mostly Christian although the state is secular. Unrest has been prevalent in the Casamance region over dispute on the marginalisation of the lo-cal population by the largely dominant Wolof group and the region has pursued a campaign for autonomy despite a peace accord in 2004.

Governance Index(2012)

0 20 40 60 80

Ghana

Liberia

Senegal

Gambia

Sierra Leone

Cote d'Ivoire

Nigeria

Mo Ibrahim Index Transparency CPI Score

Source: Transparency International (Mo, Ibrahim Index)

ProspectsNet Unrisked Prospective

Resources (mmbbl)Net Risked Prospective

Resources (mmbbl) Risking (%)Ayamé 502 68 13.5%Ayamé West 298 40 13.4%Leraba 414 68 16.4%Sassandra 175 17 9.7%Cavalla 171 16 9.4%

Total 1,560 209 13.4%

African Petroleum Corporation Limited

FOCUS | Initiating Coverage on... October 1, 2013

2727

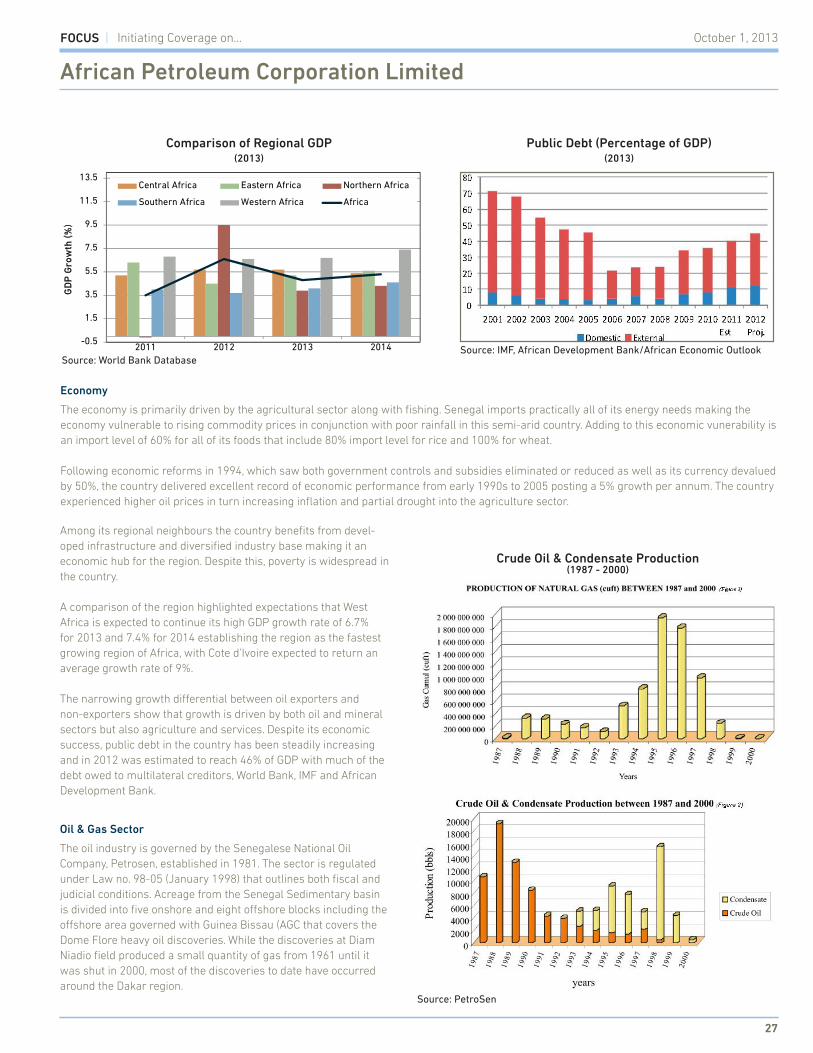

Comparison of Regional GDP(2013)

Economy

The economy is primarily driven by the agricultural sector along with fishing. Senegal imports practically all of its energy needs making the economy vulnerable to rising commodity prices in conjunction with poor rainfall in this semi-arid country. Adding to this economic vunerability is an import level of 60% for all of its foods that include 80% import level for rice and 100% for wheat.

Following economic reforms in 1994, which saw both government controls and subsidies eliminated or reduced as well as its currency devalued by 50%, the country delivered excellent record of economic performance from early 1990s to 2005 posting a 5% growth per annum. The country experienced higher oil prices in turn increasing inflation and partial drought into the agriculture sector.

-0.5

1.5

3.5

5.5

7.5

9.5

11.5

13.5

2011 2012 2013 2014

GD

P G

row

th (

%)

Central Africa Eastern Africa Northern Africa

Southern Africa Western Africa Africa

source : Africa Economic OutlookSource: World Bank Database

Public Debt (Percentage of GDP)(2013)

Source: IMF, African Development Bank/African Economic Outlook

Among its regional neighbours the country benefits from devel-oped infrastructure and diversified industry base making it an economic hub for the region. Despite this, poverty is widespread in the country.