Focus group discussion on national railways master plan, jakarta, 6 may 2010

17

6 May 2010 National Railway Master Plan Focus Group Developing Rail Freight Services on Java: What is Recommended for the Railway Master Plan?

-

Upload

indonesia-infrastructure-initiative -

Category

Business

-

view

2.194 -

download

0

Transcript of Focus group discussion on national railways master plan, jakarta, 6 may 2010

6 May 2010

National Railway Master Plan Focus Group Developing Rail Freight Services on Java:

What is Recommended for the Railway Master Plan?

Page 2

Objectives of the National Railways Master Plan

• Rapidly expand railway capacity to meet

Indonesia’s growing passenger and freight transport

needs.

• Implement railway structural reforms, including– increasing role of sub-national railway operations – increasing separation of infrastructure and above

rail operations.

• To – encourage public and private sector investment– increase competition in the railway sector and

increase transport efficiency.

Page 3

Key Demand Drivers on Java

Economic growth is driving rapid growth of transport demands for both passengers and freight

High density of population strongly favors railway passenger services.

But, the economic geography of Java – short distances between markets and – near proximity of lower-cost water transport for minerals &

other bulky goods

limits the normal role of railway freight services.

Page 4

Key Driving Forces

The economic geography– short distances between markets and near proximity of lower-cost water transport for minerals & other bulky goods– limits the normal role of railway freight services.

=> but expansion of transport capacity, especially in the highways sector, is constrained by difficulties in acquisition of rights of way.

=> Capacity constraints and congestion will increasingly impinge on economic growth, unless railway capacity and service quality can be enhanced.

Page 5

Key Driving Forces

The economic geography limits the normal role of railway freight services=> but expansion of capacity in the highways sector is constrained by acquisition of rights of way.

High density of population strongly favors railway passenger services.

=> Technological modernization of railways to meet large increases in demand for passenger services also creates important economies of scope for expanding capacity and improving railway freight services at very low cost

Page 6

Regulatory Environment Is an Important Element of the Plan

• Law 23/2007 requires that private freight operations have equal and fair access to the national railway infrastructure

• This will require separation of infrastructure from direct control of PT KA and development of an access regime that provides fair access and access pricing for all operators

• It also requires regulation governing licensing of private rail operators and chartering of new railway lines

Page 7

Development of Rail Freight Services Capabilities is an Important Part of the Railway Master Plan

• Rail freight market shares have been declining for decades

– Passenger services dominate railway traffic

– Limited available capacity– Difficult relationships with PTKA

• The existing infrastructure is unfriendly to freight transport

– Low axle loads– Antique rolling stock– Inadequate services

• The Railway Master Plan addresses each of these issues

Freight Traffic

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mill

ion

To

ns

JavaSumatra

Freight Ton-kilometers

0

1,000

2,000

3,000

4,000

5,000

6,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

bil

lion

s

Java

Sumatra

Page 8

Separation of Infrastructure Is a Significant Change

• When fully implemented, one entity will be responsible for building,

maintaining and operating existing national railways• Allows for private operators and regulated infrastructure pricing• Allows private ownership of railways

Sub-ballas t

Drainage

B allast Shoulders

Railway R

ight-of-W

ay

Sleepers FasteningsRails

Clearance Envelope

Sub-grade

Page 9

Regulatory Changes are Insufficient to Grow Freight Traffic – New Investment is Needed

Item New Price Units Cost to Replace

Locomotives $2,500,000 340 $850,000,000

Coaches $1,800,000 1,547 $2,784,600,000

EMUs $2,200,000 408 $897,600,000

DMUs $2,500,000 106 $265,000,000

Wagons $80,000 4,200 $336,000,000

Total $5,133,200,000

Source: DGR; HWTSK analysis

• Replacement cost for the existing freight wagon fleet is more than US$330 million

• Replacement cost for the existing locomotive fleet is about US$850 million

• Total rail equipment replacement costs are more than US$5 billion

• Much of the existing fleet is obsolete and needs replacement in the next decade

Page 10

The Current Infrastructure is Inadequate for Freight Services

Axle loadings are limited to a maximum of 18 tons – providing a maximum of 50 tons of lading per wagon

Many lines have lower axle loadings – 13 tons or less – providing a maximum net load of 30 tons or less per freight wagon

These limitations also extend to the locomotive fleet – limiting the power of locomotives and the maximum sizes of trains

The current infrastructure constrains the development of the Java rail freight market – trains don’t carry much more than trucks, sometimes less

Page 11

Jakarta

Cikampek

CirebonTegal

Prupuk

Purwokerto

Sukabumi

Suralaya

Bandung

Banjar

Yogyakarta

Solo

Semarang

Gambringan

Madiun

Kertosono

Malang

Bangil

Bali

Madura

Java

Surabaya

Panarukan

Banyuwangi

Gundih

Kroya

Padalarang

Bogor

Moving axle loads to 25 tons on the main lines – wagon carrying capacity to 77 tons

Increasing physical clearances to 6.1 meters eventually

Recommended Infrastructure Standards Include:– R60 continuously welded rail– Concrete sleepers at 1,660/kilometer– 300 mm hard rock ballast– Electronic signaling– Bridges sufficient for 25 tons/axle loading at track speed

Infrastructure Enhancement is a Major Recommendation for the Rail Master Plan

Page 12

Proposed Infrastructure Enhancements Will Transform Rail Operations

• High-Speed passenger trains proposed on the north island coast line

– 150-kph max speed services– Hourly departures, half-hourly in peak periods

• Higher-speed passenger services on the Bandung – Yogyakarta line – perhaps using tilt-trains

– Increased frequency– Bi-level equipment for greater capacity

• Capacity enhancements will allow more, larger, heavier, and faster freight services

Page 13

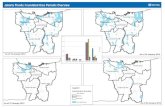

Freight Success May Depend on Specialized Terminals

Specialized terminals for warehousing and logistics services include– Containers– Oil and bulk liquids– Steel, other industrial materials– Coal terminals– Manufacturing, automobiles

Jakarta

Cikampek

CirebonTegal

Prupuk

Purwokerto

Sukabum i

Suralaya

Bandung

Banjar

Yogyakarta

Solo

Semarang

Gambringan

Madiun

Kertosono

Malang

Bangil

Bali

Madura

Java

Surabaya

Panarukan

Banyuwangi

Gundih

Kroya

Padalarang

Bogor

CM

M

M

M

O

SS

O Oil

M Manufacturing

S Steel

C

C ContainersC

C

C

C

C

C

Page 14

Specialized Terminals and Freight Rolling Stock Increasingly Private Sector Responsibility

• High capital needs for infrastructure and passenger services

• Means a larger role for private investment in railway facilities

• New law allows and encourages private investment in rail sector– Freight wagons– Specialized terminals and terminal operations– Rail operators using PT KA locos, drivers– Warehousing and logistics services– Rail operations role possible in the future

Page 15

PT KA Will Also be Transformed• PT KA must implement accounting separation of railway

services and infrastructure accounts• More rigorous accounting standards to identify

infrastructure, passenger, and freight operating costs• PT KA likely to separate into at least two divisions

– Infrastructure Services Unit: Maintain and operate railway infrastructure, including day-to-day maintenance, dispatching, under contract with DGR

– Rail Operations Unit: To assemble and operate trains, operate stations and terminals, provide locomotives, drivers, and operations management infrastructure

– Rail Operations Unit may further separate into freight and passenger divisions

• PT KA will no longer have monopoly on operations but will be able to provide operations services to private railways

Page 16

Possible Rail Sector Structure in Indonesia

Transport Policy

Economic regulation Accident Investigation

Technical Regulation& Standards, PSO,Access Charges

Access terms (networkstatement, capacity allocation)

Page 17

TerimaKasih