FNFG: A Story of goodwill - Columbia Universityme2417/FNFG - A Story of Goodwill.pdfThis premium was...

18

FNFG: A STORY OF GOODWILL BY: MICHAEL ELIAS (SEAS ’15) Stock: FNFG – Buy at $8.72, 3-Year Target Price: $12.17 Margin of Safety: 40% Thesis: First Niagara Financial Group is a regional bank that over- expanded in the landscape of the post-financial crisis to the effect of diluting shareholder value. Despite this over-expansion, there has been a greater overreaction on the part of shareholders, dumping the stock well below its intrinsic value. However, this value was not diluted, it was merely transferred to the “intangible” Goodwill account. When included in the tangible book value, the Bank trades at a 30% discount to its asset value. When conservative estimates of earnings are used over three years, the Bank trades at a 40% discount to its Intrinsic Value Michael Elias 2920 Broadway 2207 Lerner Hall Tel: 347-967-7550 Email: [email protected]

Transcript of FNFG: A Story of goodwill - Columbia Universityme2417/FNFG - A Story of Goodwill.pdfThis premium was...

FNFG: A STORY OF GOODWILL BY: MICHAEL ELIAS (SEAS ’15)

Stock: FNFG – Buy at $8.72, 3-Year Target Price: $12.17

Margin of Safety: 40%

Thesis: First Niagara Financial Group is a regional bank that over-

expanded in the landscape of the post-financial crisis to the effect of diluting

shareholder value. Despite this over-expansion, there has been a greater

overreaction on the part of shareholders, dumping the stock well below its

intrinsic value. However, this value was not diluted, it was merely

transferred to the “intangible” Goodwill account. When included in the

tangible book value, the Bank trades at a 30% discount to its asset value.

When conservative estimates of earnings are used over three years, the

Bank trades at a 40% discount to its Intrinsic Value

Michael Elias

2920 Broadway 2207 Lerner Hall

Tel: 347-967-7550

Email: [email protected]

TABLE OF CONTENTS

Table of Contents

Business Overview _______________________________________________________________________________________ 1

Commercial & Retail Banking ____________________________________________________________________________________1

Growth By Acquisition ____________________________________________________________________________________________1

Strong Core Deposits and Customer Relationships _____________________________________________________________1

High Quality Loan Portfolios _____________________________________________________________________________________1

Industry Overview _______________________________________________________________________________________ 2

The Pain of 2008 __________________________________________________________________________________________________2

Regulatory Reform ________________________________________________________________________________________________2

Nature Of Competition ____________________________________________________________________________________________2

Investment Thesis _______________________________________________________________________________________ 3

Aggressive Expansion Did Not Dilute Value; It Concealed Value _______________________________________________3

Goodwill: Is It Good At All? _______________________________________________________________________________________3

Value of Goodwill __________________________________________________________________________________________________3

Adjusted Tangible Book Value is Greater Than The Current Share Price by 30% ____________________________4

Three Year Price Target Price: $12.17 ___________________________________________________________________________4

Asset Reproduction Value _______________________________________________________________________________ 5

Analyzing The Reproduction Cost Of FNFG’s Assets ____________________________________________________________5

Cash _____________________________________________________________________________________________________________5

Commercial Loan Portfolio ____________________________________________________________________________________5

Consumer Loan Portfolio ______________________________________________________________________________________5

Inventory _______________________________________________________________________________________________________5

Plant, Property, and Equipment (PPE) ________________________________________________________________________5

Investment Securities __________________________________________________________________________________________6

Advances ________________________________________________________________________________________________________6

Goodwill ________________________________________________________________________________________________________6

Deposits & Other Assets _______________________________________________________________________________________7

Intangibles ______________________________________________________________________________________________________7

Liabilities _______________________________________________________________________________________________________7

TABLE OF CONTENTS

Summary ___________________________________________________________________________________________________________8

Earning Power Value ____________________________________________________________________________________ 9

Establishishing The Value of Expected Future Cash Flows _____________________________________________________9

Net Income ______________________________________________________________________________________________________9

Future Dividends _______________________________________________________________________________________________9

Present Value of Future Cash Flows ________________________________________________________________________ 10

Catalysts for Growth ____________________________________________________________________________________ 11

Improving Net Interest Margin _________________________________________________________________________________ 11

Improving Macro Outlook ______________________________________________________________________________________ 11

Insider Buying ___________________________________________________________________________________________________ 11

Higher Core Deposits Responsible for Greater Revenue _____________________________________________________ 11

Summary ________________________________________________________________________________________________ 12

Misunderstood __________________________________________________________________________________________________ 12

Undervalued _____________________________________________________________________________________________________ 12

Out of Favor ______________________________________________________________________________________________________ 12

Appendix ________________________________________________________________________________________________ 14

Goodwill Analysis: Acquisition _________________________________________________________________________________ 14

Goodwill Analysis: Sales and Divestitures _____________________________________________________________________ 15

FIRST NIAGARA FINANCIAL GROUP

Page 1

Business Overview

COMMERCIAL & RETAIL BANKING

First Niagara Financial Group, Inc. is a regional bank holding company operating in the Mid-Atlantic, with a

geographic footprint reaching across New York, Pennsylvania, Connecticut, and Western Massachusetts.

Through FNFG’s wholly-owned bank subsidiary, First Niagara Bank, N.A. (‘the Bank’ from henceforth), the

Bank provides a range of retail and commercial banking, as well as other financial services. The Bank provides

its retail consumer and business customers with banking services, including residential and commercial real

estate loans, commercial business loans, consumer loans, wealth management products, as well as retail and

commercial deposit products. As of December 31, 2013, the Bank had $26.7 billion of deposits, $37.6 billion

dollars in assets held throughout 421 full service branches.

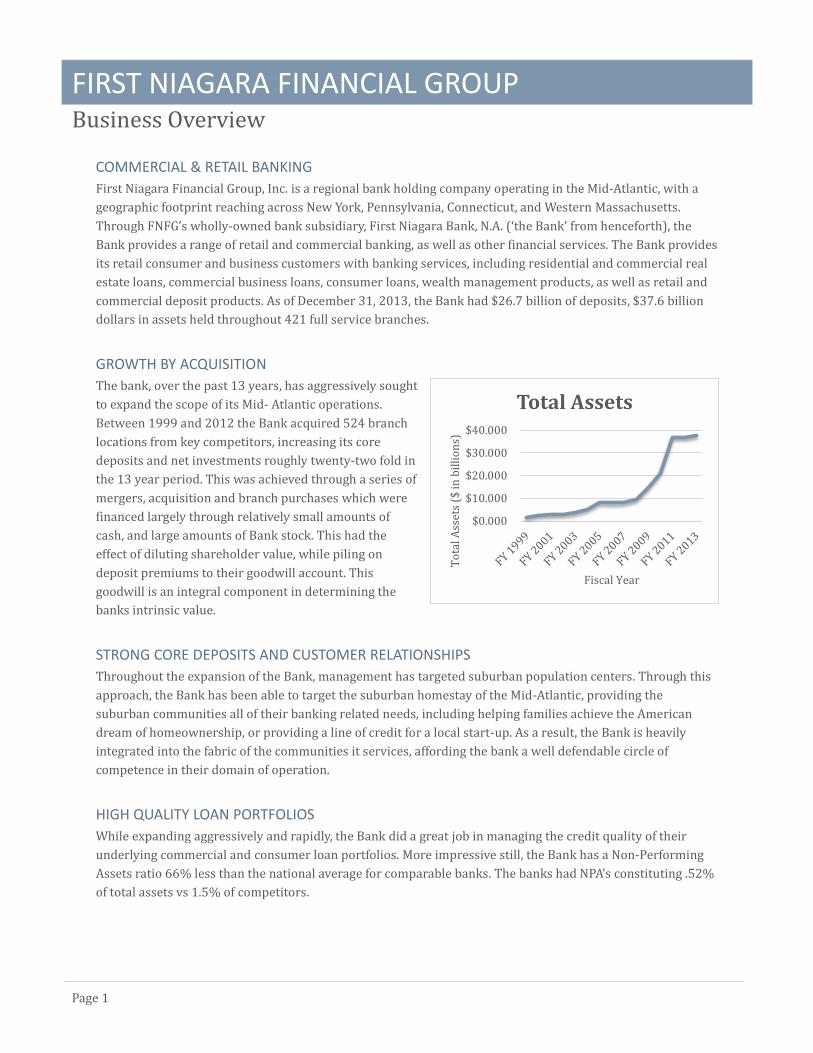

GROWTH BY ACQUISITION

The bank, over the past 13 years, has aggressively sought

to expand the scope of its Mid- Atlantic operations.

Between 1999 and 2012 the Bank acquired 524 branch

locations from key competitors, increasing its core

deposits and net investments roughly twenty-two fold in

the 13 year period. This was achieved through a series of

mergers, acquisition and branch purchases which were

financed largely through relatively small amounts of

cash, and large amounts of Bank stock. This had the

effect of diluting shareholder value, while piling on

deposit premiums to their goodwill account. This

goodwill is an integral component in determining the

banks intrinsic value.

STRONG CORE DEPOSITS AND CUSTOMER RELATIONSHIPS

Throughout the expansion of the Bank, management has targeted suburban population centers. Through this

approach, the Bank has been able to target the suburban homestay of the Mid-Atlantic, providing the

suburban communities all of their banking related needs, including helping families achieve the American

dream of homeownership, or providing a line of credit for a local start-up. As a result, the Bank is heavily

integrated into the fabric of the communities it services, affording the bank a well defendable circle of

competence in their domain of operation.

HIGH QUALITY LOAN PORTFOLIOS

While expanding aggressively and rapidly, the Bank did a great job in managing the credit quality of their

underlying commercial and consumer loan portfolios. More impressive still, the Bank has a Non-Performing

Assets ratio 66% less than the national average for comparable banks. The banks had NPA’s constituting .52%

of total assets vs 1.5% of competitors.

$0.000

$10.000

$20.000

$30.000

$40.000

To

tal A

sset

s ($

in b

illi

on

s)

Fiscal Year

Total Assets

FIRST NIAGARA FINANCIAL GROUP

Page 2

Industry Overview

THE PAIN OF 2008

In the aftermath of the undoubted malfeasance on the part of bankers and underwriters that caused the

Financial Crisis of 2008, many investors have been turned off from banks, having taken excruciating losses on

their positions. Others, including with mainstream America, have persecuted the banks for their greed and

lack of remorse. When juxtaposed, these truths have the effect of leaving many financial institutions

undervalued in the absence of investors. If there is anything we learn in the aftermath of 2008, it is that a

healthy banking system, which properly facilitates the flow of credit, is the cornerstone of the market

economy. The absence of which leads to the breakdown of life as we know it. As a result, the undervaluation of

a sector that is essential to life as we know it represents an opportunity to finding value.

REGULATORY REFORM

One reason why the banking sector has remained undervalued since the financial crisis, has been uncertainty

regarding the future earning power of financial institutions as consequence of the regulatory reform imposed

since the financial crisis. The Dodd–Frank Wall Street Reform and Consumer Protection Act, has enacted

innumerous regulations on the way that banks conduct business, most directly relating to what depository

banks can and cannot do. For this reason, there is a great potential for income streams once treasured by

banks to disappear. The bulk of these rules relate to “Systemically Important Financial Institutions”,

constituting banks with over $50 billion in assets. First Niagara, with $37 billion dollars in assets, has been

spared from any material changes to their business as a result of the new regulations. For this reason, we can

assume with a relative degree of certainty that that the earnings of the bank will remain materially unchanged

until the $50 billion mark is reached.

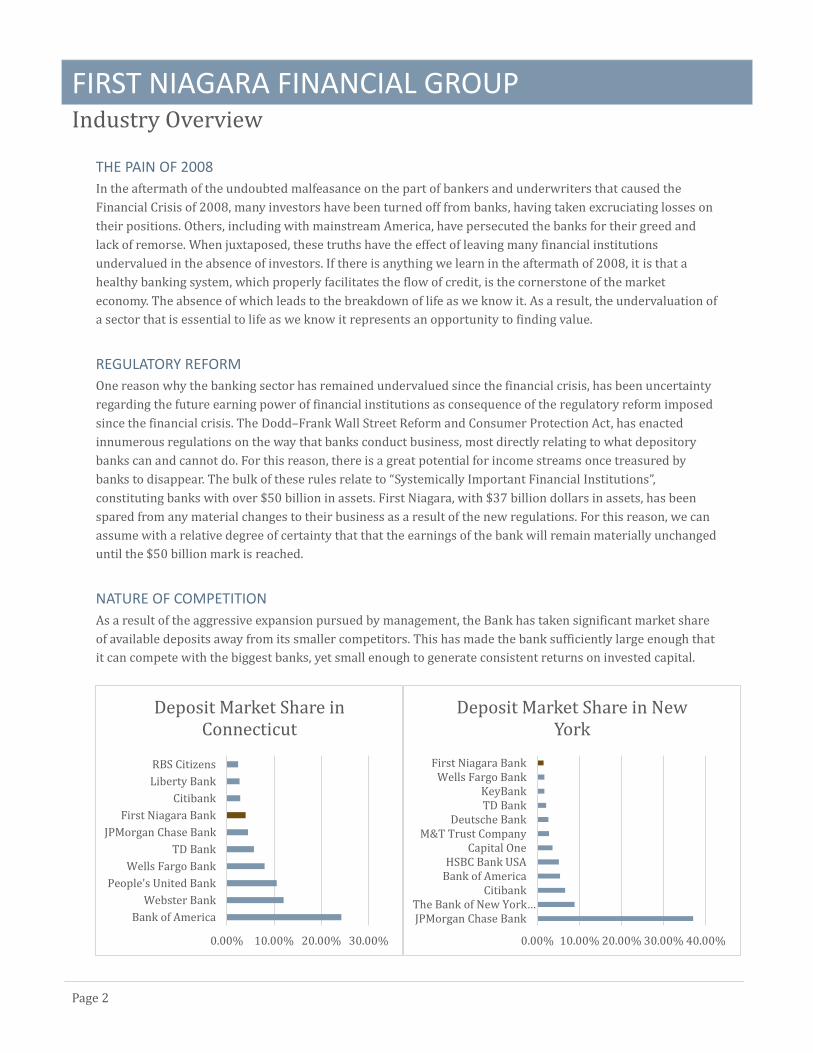

NATURE OF COMPETITION

As a result of the aggressive expansion pursued by management, the Bank has taken significant market share

of available deposits away from its smaller competitors. This has made the bank sufficiently large enough that

it can compete with the biggest banks, yet small enough to generate consistent returns on invested capital.

0.00% 10.00% 20.00% 30.00% 40.00%

JPMorgan Chase BankThe Bank of New York…

CitibankBank of AmericaHSBC Bank USA

Capital OneM&T Trust Company

Deutsche BankTD BankKeyBank

Wells Fargo BankFirst Niagara Bank

Deposit Market Share in New York

0.00% 10.00% 20.00% 30.00%

Bank of America

Webster Bank

People's United Bank

Wells Fargo Bank

TD Bank

JPMorgan Chase Bank

First Niagara Bank

Citibank

Liberty Bank

RBS Citizens

Deposit Market Share in Connecticut

FIRST NIAGARA FINANCIAL GROUP

Page 3

Investment Thesis

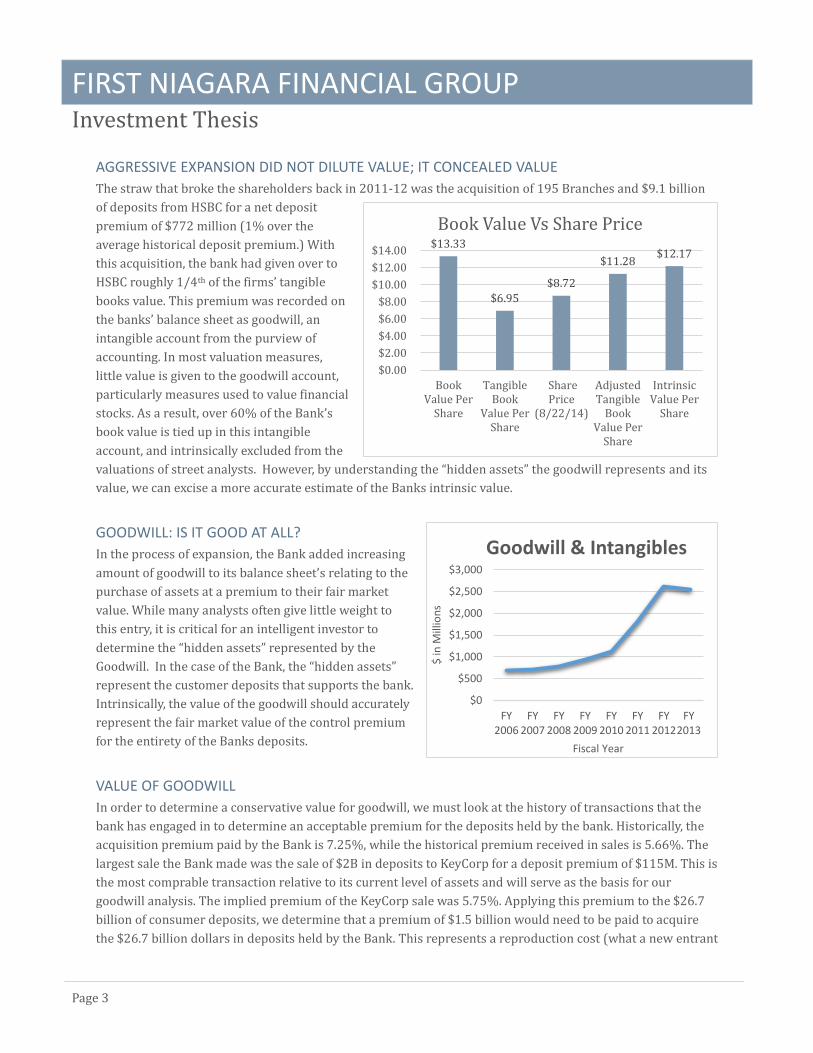

AGGRESSIVE EXPANSION DID NOT DILUTE VALUE; IT CONCEALED VALUE

The straw that broke the shareholders back in 2011-12 was the acquisition of 195 Branches and $9.1 billion

of deposits from HSBC for a net deposit

premium of $772 million (1% over the

average historical deposit premium.) With

this acquisition, the bank had given over to

HSBC roughly 1/4th of the firms’ tangible

books value. This premium was recorded on

the banks’ balance sheet as goodwill, an

intangible account from the purview of

accounting. In most valuation measures,

little value is given to the goodwill account,

particularly measures used to value financial

stocks. As a result, over 60% of the Bank’s

book value is tied up in this intangible

account, and intrinsically excluded from the

valuations of street analysts. However, by understanding the “hidden assets” the goodwill represents and its

value, we can excise a more accurate estimate of the Banks intrinsic value.

GOODWILL: IS IT GOOD AT ALL?

In the process of expansion, the Bank added increasing

amount of goodwill to its balance sheet’s relating to the

purchase of assets at a premium to their fair market

value. While many analysts often give little weight to

this entry, it is critical for an intelligent investor to

determine the “hidden assets” represented by the

Goodwill. In the case of the Bank, the “hidden assets”

represent the customer deposits that supports the bank.

Intrinsically, the value of the goodwill should accurately

represent the fair market value of the control premium

for the entirety of the Banks deposits.

VALUE OF GOODWILL

In order to determine a conservative value for goodwill, we must look at the history of transactions that the

bank has engaged in to determine an acceptable premium for the deposits held by the bank. Historically, the

acquisition premium paid by the Bank is 7.25%, while the historical premium received in sales is 5.66%. The

largest sale the Bank made was the sale of $2B in deposits to KeyCorp for a deposit premium of $115M. This is

the most comprable transaction relative to its current level of assets and will serve as the basis for our

goodwill analysis. The implied premium of the KeyCorp sale was 5.75%. Applying this premium to the $26.7

billion of consumer deposits, we determine that a premium of $1.5 billion would need to be paid to acquire

the $26.7 billion dollars in deposits held by the Bank. This represents a reproduction cost (what a new entrant

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

FY2006

FY2007

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

$ in

Mill

ion

s

Fiscal Year

Goodwill & Intangibles

$13.33

$6.95

$8.72

$11.28$12.17

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

BookValue Per

Share

TangibleBook

Value PerShare

SharePrice

(8/22/14)

AdjustedTangible

BookValue Per

Share

IntrinsicValue Per

Share

Book Value Vs Share Price

FIRST NIAGARA FINANCIAL GROUP

Page 4

would have to pay to replicate the Bank’s current business) of roughly 61.7% of the goodwill account. This

value must be added back to the tangible book value of assets in order to more accurately determine the value

of shareholder equity.

ADJUSTED TANGIBLE BOOK VALUE IS GREATER THAN THE CURRENT SHARE PRICE BY 30%

After determining the reproduction costs of both the assets and liabilities of the Bank, we see the Bank trades

at a 30% discount to its asset value. In the graph below, you can see that the Bank has been trading below its

adjusted tangible book value. This provides an investor the opportunity to get cheap access to a bank

operating 1% below its long-term profitability as a result of historical low interest rates.

THREE YEAR PRICE TARGET PRICE: $12.17

Once we have determined the asset value, the next step is determining the value of the earnings. In order to

remain conservative in our valuation, we assume the revenue stream remains constant and operating margins

remain about the same. This is to prevent wild ambition on the part of future, uncertain earnings.

Understanding that the money the Bank returns to its shareholders come primarily in the form of dividends,

we can conservatively project the present value of expected future dividends. Over a three year holding

period, we would hold the Banks shares until the full adjusted tangible book value is realized, while

accumulating dividends along the way for our patience. In addition to the catalyst for growth on the part of an

improving net interest margin, the Bank represents a value opportunity hidden in plain sight, ready to return

to its historic price of $12-15 per share.

FY2013 FY2014* FY2015* FY2016*

Net Income Growth 75.18% 1.02% 1.02% 1.02%

Net Income $295.00 $299.77 $304.41 $309.12

Dividend Payout Ratio (Common Shares) 38.37% 38.37% 38.37% 38.37%

Dividend Payments (Common Shares) $113.20 $115.03 $116.81 $118.62

Present Value of Future Dividends N/A $108.52 $103.96 $99.59

Discount Rate 6%

Present Value of Future Dividends $312.08

Adjusted Tangible Book Value $3,975.61

ATBV + Expected Future Dividends $4,287.69

Shares Outstanding 352.4

Intrinsic Value Per Share $12.17

FIRST NIAGARA FINANCIAL GROUP

Page 5

Asset Reproduction Value

ANALYZING THE REPRODUCTION COST OF FNFG’S ASSETS

To determine an appropriate value for the net assets of First Niagara Financial Group, we must analyze the

reproduction cost of their balance sheet. Working our way down the balance sheet, we find the cost pursuant

to a newcomer to the market, if they were to replicate FNFG’s positions identically.

Cash

A new entrant would be forced to pay 100% for the cash account of the business

Commercial Loan Portfolio

In the past, the Bank has sold a small subsections of their commercial loan portfolio, comparable to their

entire commercial loan portfolio. The portfolio was sold at 99.64% of book value. Historically, commercial

portfolios can fetch anywhere between 98-102% of book value when sold. This is determined by many factors

including percentage on non-performing assets (NPA) in the portfolio, as well as the underwriting standards

utilized in constructing the portfolio. Concordant with Graham’s approach, we will assume the newcomer will

can acquire the loan portfolio at the low end of the spectrum, at 98% of book value.

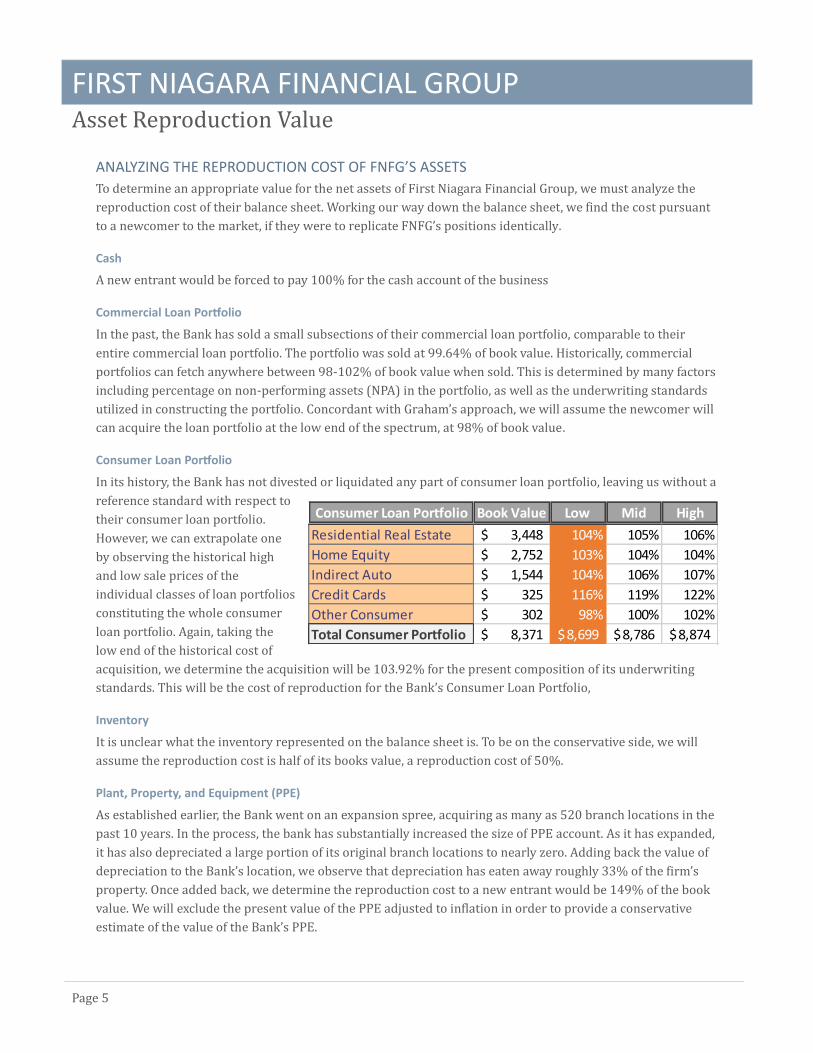

Consumer Loan Portfolio

In its history, the Bank has not divested or liquidated any part of consumer loan portfolio, leaving us without a

reference standard with respect to

their consumer loan portfolio.

However, we can extrapolate one

by observing the historical high

and low sale prices of the

individual classes of loan portfolios

constituting the whole consumer

loan portfolio. Again, taking the

low end of the historical cost of

acquisition, we determine the acquisition will be 103.92% for the present composition of its underwriting

standards. This will be the cost of reproduction for the Bank’s Consumer Loan Portfolio,

Inventory

It is unclear what the inventory represented on the balance sheet is. To be on the conservative side, we will

assume the reproduction cost is half of its books value, a reproduction cost of 50%.

Plant, Property, and Equipment (PPE)

As established earlier, the Bank went on an expansion spree, acquiring as many as 520 branch locations in the

past 10 years. In the process, the bank has substantially increased the size of PPE account. As it has expanded,

it has also depreciated a large portion of its original branch locations to nearly zero. Adding back the value of

depreciation to the Bank’s location, we observe that depreciation has eaten away roughly 33% of the firm’s

property. Once added back, we determine the reproduction cost to a new entrant would be 149% of the book

value. We will exclude the present value of the PPE adjusted to inflation in order to provide a conservative

estimate of the value of the Bank’s PPE.

Consumer Loan Portfolio Book Value Low Mid High

Residential Real Estate 3,448$ 104% 105% 106%

Home Equity 2,752$ 103% 104% 104%

Indirect Auto 1,544$ 104% 106% 107%

Credit Cards 325$ 116% 119% 122%

Other Consumer 302$ 98% 100% 102%

Total Consumer Portfolio 8,371$ 8,699$ 8,786$ 8,874$

FIRST NIAGARA FINANCIAL GROUP

Page 6

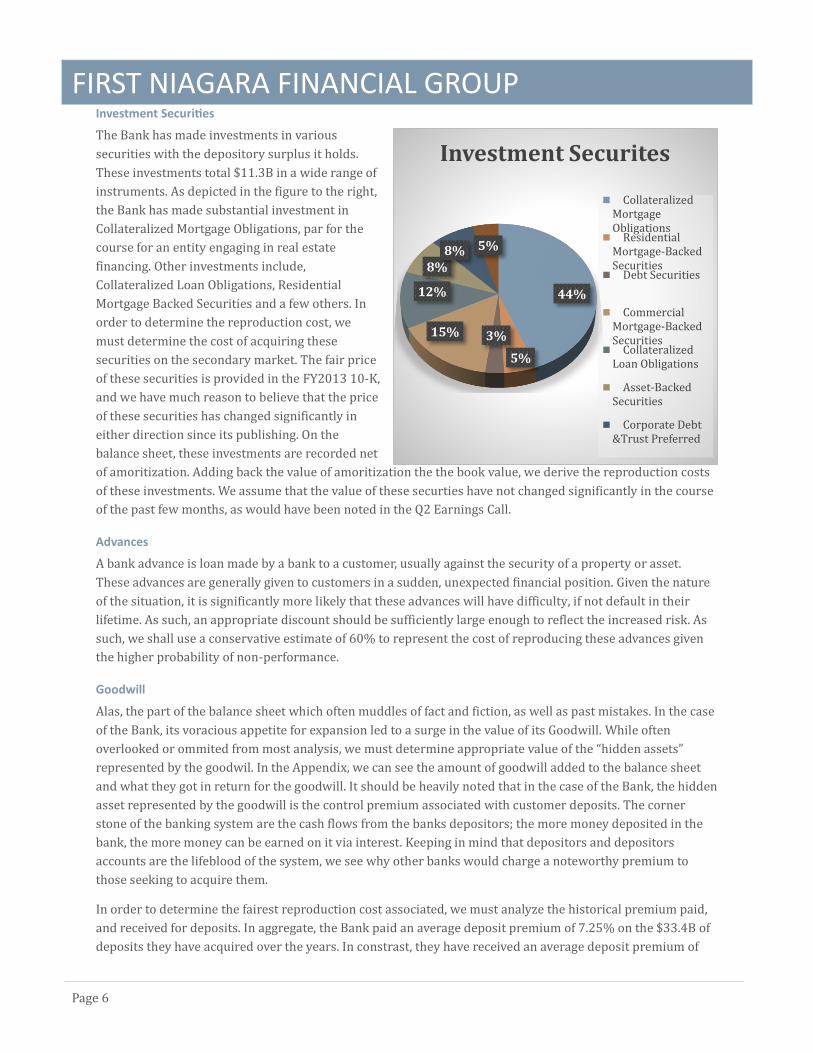

Investment Securities

The Bank has made investments in various

securities with the depository surplus it holds.

These investments total $11.3B in a wide range of

instruments. As depicted in the figure to the right,

the Bank has made substantial investment in

Collateralized Mortgage Obligations, par for the

course for an entity engaging in real estate

financing. Other investments include,

Collateralized Loan Obligations, Residential

Mortgage Backed Securities and a few others. In

order to determine the reproduction cost, we

must determine the cost of acquiring these

securities on the secondary market. The fair price

of these securities is provided in the FY2013 10-K,

and we have much reason to believe that the price

of these securities has changed significantly in

either direction since its publishing. On the

balance sheet, these investments are recorded net

of amoritization. Adding back the value of amoritization the the book value, we derive the reproduction costs

of these investments. We assume that the value of these securties have not changed significantly in the course

of the past few months, as would have been noted in the Q2 Earnings Call.

Advances

A bank advance is loan made by a bank to a customer, usually against the security of a property or asset.

These advances are generally given to customers in a sudden, unexpected financial position. Given the nature

of the situation, it is significantly more likely that these advances will have difficulty, if not default in their

lifetime. As such, an appropriate discount should be sufficiently large enough to reflect the increased risk. As

such, we shall use a conservative estimate of 60% to represent the cost of reproducing these advances given

the higher probability of non-performance.

Goodwill

Alas, the part of the balance sheet which often muddles of fact and fiction, as well as past mistakes. In the case

of the Bank, its voracious appetite for expansion led to a surge in the value of its Goodwill. While often

overlooked or ommited from most analysis, we must determine appropriate value of the “hidden assets”

represented by the goodwil. In the Appendix, we can see the amount of goodwill added to the balance sheet

and what they got in return for the goodwill. It should be heavily noted that in the case of the Bank, the hidden

asset represented by the goodwill is the control premium associated with customer deposits. The corner

stone of the banking system are the cash flows from the banks depositors; the more money deposited in the

bank, the more money can be earned on it via interest. Keeping in mind that depositors and depositors

accounts are the lifeblood of the system, we see why other banks would charge a noteworthy premium to

those seeking to acquire them.

In order to determine the fairest reproduction cost associated, we must analyze the historical premium paid,

and received for deposits. In aggregate, the Bank paid an average deposit premium of 7.25% on the $33.4B of

deposits they have acquired over the years. In constrast, they have received an average deposit premium of

44%

5%

3%15%

12%

8%8% 5%

Investment Securites

CollateralizedMortgageObligations ResidentialMortgage-BackedSecurities Debt Securities

CommercialMortgage-BackedSecurities CollateralizedLoan Obligations

Asset-BackedSecurities

Corporate Debt&Trust Preferred

FIRST NIAGARA FINANCIAL GROUP

Page 7

5.66% on the $3.3B of deposits they have sold to competitors. We will assume a 5.66% control premium for

the deposits on the current $26.7B in customer deposits. The cost pursuant to a newcomer into the market to

acquire the Banks depositis, as well as the value of the Bank’s goodwill is $1.51B, roughly 61% of the Bank’s

recorded goodwill. Adding this amount back to the tangible book value translates into the Bank trading at a

30% discount to its book value, making it an exceptional opportunity both in the case of liquidation, but even

more so as a going concern.

Deposits & Other Assets

We assume that a new entrant must replicate the entirety of the Bank’s core deposits, translating into a

reproduction cost of 100%.

Intangibles

We are giving zero value to the intangibles of the bank including consumer lists, brand value and other human

capital. As consequence, we assume a reproduction cost of 0%.

Liabilities

We are assuming the new entrant must pay the full reproduction cost of the banks liabilities which constitute

the deposits of its customers, a small percentage of debt, relative to the entire capital structure (D/E ≈ .2), as

well as it’s notes payable to suppliers. This represents a reproduction cost of 100% for the firms’ liabilities.

FIRST NIAGARA FINANCIAL GROUP

Page 8

SUMMARY

$ in MM

Reproduction Cost Reproduction Value FY 2013

Cash 100% $463 $463 Marketable Securities

Commercial Loan Portfolio 98% $12,601.82 $12,859.00 Consumer Loan Portfolio

Real Estate 104% $3,586 $3,448 Home Equity 103% $2,835 $2,752 Indirect Auto 104% $1,606 $1,544 Credit Cards 116% $377 $325 Other Consumer Loans 98% $296 $302 Inventory 50% $25 $50 Notes Receivable $0 Other Current Assets $0

Total Current Assets 100.21% $21,789 $21,743

Net PPE 149% $623 $418 Investment Securities

Collateralized Mortgage Obligations 98% $4,882 $4,985 Residential Mortgage-Backed Securities 101% $578 $574 Debt Securities 102% $338 $332 Commercial Mortgage-Backed Securities 104% $1,831 $1,759 Collateralized Loan Obligations 103% $1,431 $1,392 Asset-Backed Securities 101% $905 $896 Corporate Debt &Trust Preferred 101% $872 $863 States & Political Subdivisions 103% $529 $516 Other Non-Current Assets 100% $45 $45 Advances 50% $286.50 $573 Deferred Charges $0 Goodwill 61.7% $1,512 $2,449 Other Intangibles 0% $0 $94 Deposits & Other Assets 100% $989 $989

TOTAL ASSETS 97.30% $36,611 $37,628

Notes Payable 100% $4,822 $4,822 Accounts Payable 100% $26,665 $26,665 Current Portion of Long Term Debt $0 Current Portion of Long Term Debt $0 Accrued Expenses $0 Income Taxes Payable $0 Other Current Liabilities $0

Total Current Liabilities 100% $31,487 $31,487

Deferred Charges (Taxes/Income) $0 Convertible Debt $0 Long Term Debt 100% $734.00 $734 Non-Current Current Capital Leases $0 Other Long Term Liabilities 100% $414.00 $414 Minority Interest (liabilities) $0

Total Liabilities 100% $32,635 $32,635

Tangible Book Value $2,450

Tangible Book Value Per Share $6.95

Average Share Price $8.18

Adjusted Tangible Book Value Per Share $11.28

Adjusted Tangible Book Value $3,975.61

FIRST NIAGARA FINANCIAL GROUP

Page 9

Earning Power Value

ESTABLISHISHING THE VALUE OF EXPECTED FUTURE CASH FLOWS

Having established an adjusted tangible book value for the Bank, we must shift our focus to determining the

value of the cash flows expected from the Bank over the duration of our holding period of 3 years. The bank

distributes part of its net income back to shareholders in the form of dividends. In order to project

conservatively the value of these future cash flows, we must conservatively project the value of the Bank’s Net

Income

Net Income

As the bank expanded in the landscape of the post-financial crisis, it saw the size of its asset base increase

sizably. Intrinsically, the net income of the firm has increased nearly 300% throughout its expansion.

However, this increase in net income came at the

expense of a lower net income margin

throughout the expansion process. It was not

until 2013 that the net income reached a new

equillibrium given the new level of assets (the

Bank had a large non-recurring expense relating

to its HSBC branch acquisition in FY2012.) In

FY2013, the Bank had a net profit margin of

18.72%, slightly higher than their historical

average of 15%. Given the scale of their

expansion, we will assume that they will be able

to sustain this margin as a result of their larger

asset base. We will assume that Net Income

grows at roughly 1% a year, as depicted in

forward projections of net income supplied

above. This assumes that the net income stream grows at the same rate as the Bank’s return on assets,

roughly 1%. With this conservative assumption, we can calculate the value of future dividend we can expect to

receive.

Future Dividends

For a company that appears to be in financial

distress, as observed by the share price, the bank

has paid exceptionally high percentages of its net

income out to shareholders. In 2013, at the end of

its expansion phase, the Bank offered a dividend

payout ratio of 38%, returning $113M to its

common shareholders. This is well below the

historical payout ratio and can serve as a means of

conservatively estimating future dividends.

Assuming the low end of the historical dividend

payout ratio, we can conservatively calculate the

future value of expected dividends.

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00$

in M

M

Fiscal Year

Net Income

0%20%40%60%80%

100%120%140%

% o

f N

et I

nco

me

Fiscal Year

Dividend Payout Ratio

FIRST NIAGARA FINANCIAL GROUP

Page 10

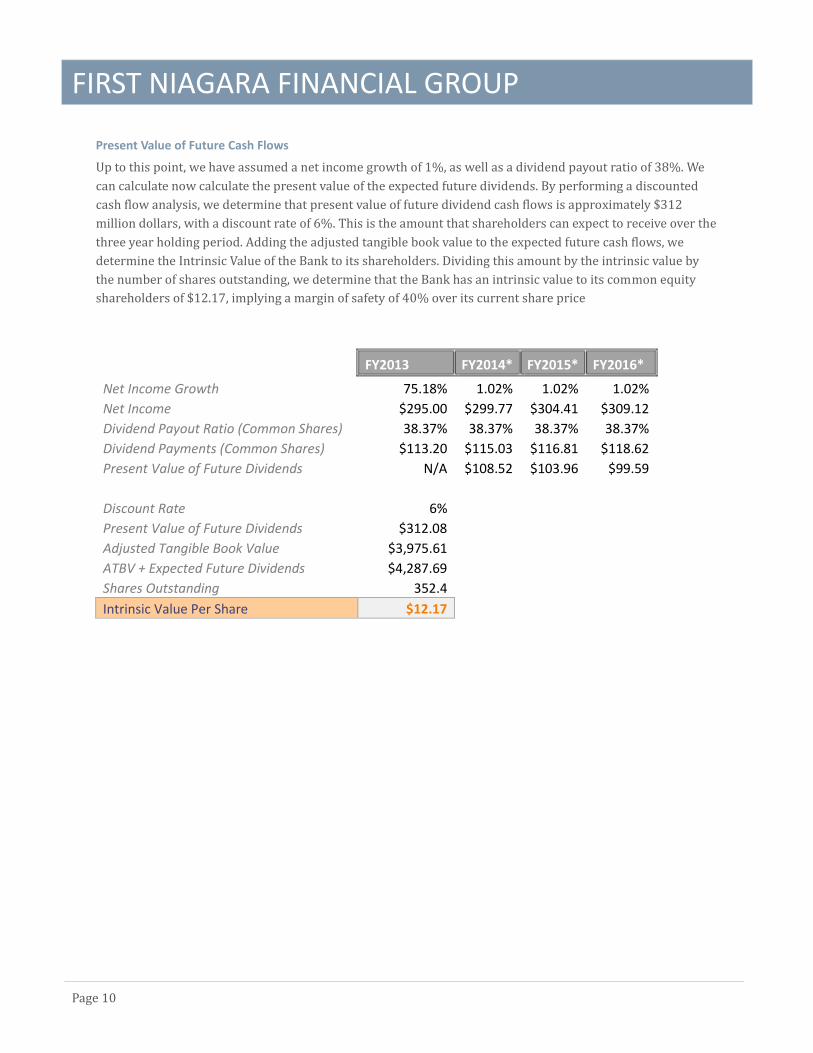

Present Value of Future Cash Flows

Up to this point, we have assumed a net income growth of 1%, as well as a dividend payout ratio of 38%. We

can calculate now calculate the present value of the expected future dividends. By performing a discounted

cash flow analysis, we determine that present value of future dividend cash flows is approximately $312

million dollars, with a discount rate of 6%. This is the amount that shareholders can expect to receive over the

three year holding period. Adding the adjusted tangible book value to the expected future cash flows, we

determine the Intrinsic Value of the Bank to its shareholders. Dividing this amount by the intrinsic value by

the number of shares outstanding, we determine that the Bank has an intrinsic value to its common equity

shareholders of $12.17, implying a margin of safety of 40% over its current share price

FY2013 FY2014* FY2015* FY2016*

Net Income Growth 75.18% 1.02% 1.02% 1.02%

Net Income $295.00 $299.77 $304.41 $309.12

Dividend Payout Ratio (Common Shares) 38.37% 38.37% 38.37% 38.37%

Dividend Payments (Common Shares) $113.20 $115.03 $116.81 $118.62

Present Value of Future Dividends N/A $108.52 $103.96 $99.59

Discount Rate 6%

Present Value of Future Dividends $312.08

Adjusted Tangible Book Value $3,975.61

ATBV + Expected Future Dividends $4,287.69

Shares Outstanding 352.4

Intrinsic Value Per Share $12.17

FIRST NIAGARA FINANCIAL GROUP

Page 11

Catalysts for Growth

In our analysis, we have given almost zero value to growth opportunities. This is because a bird in the hand is

certainly worth more than two in the bush. In our valuation, it is imperative that we restrict our assumptions

regarding the future, less certain cash flows. By giving zero value to growth, we are getting all of the catalysts

for growth for free. This provides an investor the opportunity to get cheap access to a bank operating 1%

below its long-term profitability as a result of historical low interest rates.

IMPROVING NET INTEREST MARGIN

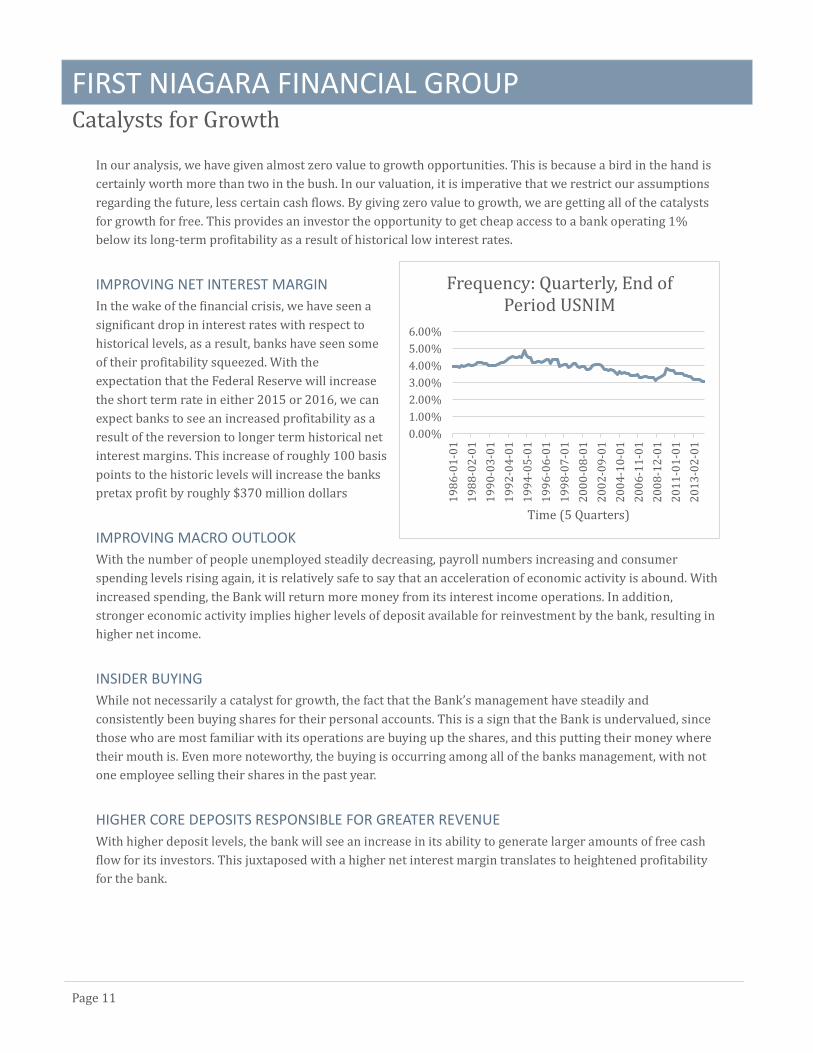

In the wake of the financial crisis, we have seen a

significant drop in interest rates with respect to

historical levels, as a result, banks have seen some

of their profitability squeezed. With the

expectation that the Federal Reserve will increase

the short term rate in either 2015 or 2016, we can

expect banks to see an increased profitability as a

result of the reversion to longer term historical net

interest margins. This increase of roughly 100 basis

points to the historic levels will increase the banks

pretax profit by roughly $370 million dollars

IMPROVING MACRO OUTLOOK

With the number of people unemployed steadily decreasing, payroll numbers increasing and consumer

spending levels rising again, it is relatively safe to say that an acceleration of economic activity is abound. With

increased spending, the Bank will return more money from its interest income operations. In addition,

stronger economic activity implies higher levels of deposit available for reinvestment by the bank, resulting in

higher net income.

INSIDER BUYING

While not necessarily a catalyst for growth, the fact that the Bank’s management have steadily and

consistently been buying shares for their personal accounts. This is a sign that the Bank is undervalued, since

those who are most familiar with its operations are buying up the shares, and this putting their money where

their mouth is. Even more noteworthy, the buying is occurring among all of the banks management, with not

one employee selling their shares in the past year.

HIGHER CORE DEPOSITS RESPONSIBLE FOR GREATER REVENUE

With higher deposit levels, the bank will see an increase in its ability to generate larger amounts of free cash

flow for its investors. This juxtaposed with a higher net interest margin translates to heightened profitability

for the bank.

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

19

86

-01

-01

19

88

-02

-01

19

90

-03

-01

19

92

-04

-01

19

94

-05

-01

19

96

-06

-01

19

98

-07

-01

20

00

-08

-01

20

02

-09

-01

20

04

-10

-01

20

06

-11

-01

20

08

-12

-01

20

11

-01

-01

20

13

-02

-01

Time (5 Quarters)

Frequency: Quarterly, End of Period USNIM

FIRST NIAGARA FINANCIAL GROUP

Page 12

Summary

The history of capital markets are littered with undervalued securities that became so by virtue of human

misjudgments. The story of First Niagara Financial Group is one that shares much in common with these

securities. The three

following phrases adequately

represent the manner in

which this opportunity would

be attractive to an investor

seeking value.

MISUNDERSTOOD

After sailing through the

turbulent vicissitudes of the

financial crisis, the Bank

capitalized on their healthy

position by expanding the

breadth of their operation into an adjacent geographical region (Pennsylvania) as well as strengthening their

hold on their primary market of operation, New York and Connecticut. After three profitable acquisitions, the

Bank paid above 1% of the average premium in an effort to acquire $9B in deposits from HSBC USA Inc. in late

2011. Investors at the time, thought this was a foolish transaction and a sell off ensued. Under pressure from

the remaining shareholders, CEO John Koelmel, who had led the expansion, resigned after holding out for over

a year. During that year, the stock reached record lows. After an interim CEO, Gary Crosby, was announced as

they underwent the search process for a new CEO. The stock surged on hopes of the Bank installing more

“competent” management. Later the Bank announced that Crosby would remain CEO, giving explicit forward

guidance, stating “We’re out of the (mergers and acquisitions) business and we’re going to focus on the

business that we have built over the last handful of years and building long-term shareholder value out of that

business.” With their expanded pool of assets, and new management, the Bank is poised to have a long career

of providing financing to its communities.

UNDERVALUED

While the HSBC transaction did come at the cost of reducing the Bank’s tangible book value, it did not destroy

value you as shareholders wrongly assumed, it merely concealed it in a place that most equity analysts,

bankers and traders would never bother to look, the Goodwill account. Once it is realized that the value of the

goodwill represents the control premium on deposits in their vaults, the stock price will more accurately

reflect its intrinsic value. The Banks asset value alone surpasses the current stock price by 30%, without

including the value of earnings and growth. This provides a sufficient margin of safety in the net assets great

enough to protect the investor from loses in the case of liquidation (low debt in capital structure)

OUT OF FAVOR

In the fallout associated with the financial crisis, many investors with exposure to banks experienced

unprecedented losses. As consequence, banks and other financial service providers have been undervalued on

the whole since 2008. The reason lies in the uncertain future earning power of banks in the face of regulatory

FIRST NIAGARA FINANCIAL GROUP

Page 13

reform pursuant to the Dodd–Frank Wall Street Reform and Consumer Protection Act. With some regulations

still being developed and others still not enforced, it is unclear what the affect will be to banks. Luckily, the

Bank is spared from many of the regulations enacted by Dodd-Frank, since the bank does not have the

requisite $50B in assets to be considered a “Systemically Important Financial Institution.” The largest impact

of the regulations comes in the ability of the bank to purchase certain types of asset-backed securities, which

constitute less than 3% of the Bank’s investment portfolio.

FIRST NIAGARA FINANCIAL GROUP

Page 14

Appendix

GOODWILL ANALYSIS: ACQUISITION

Company Transaction Type

Goodwill Generated ($ in 000’s)

Deposits Acquired ($ in 000’s)

Implied Deposit Premium

HSBC USA. Inc Branch Acquisition $772,000.00 $9,100,000 8.48%

PNC Financial Services Group, Inc.

Branch Acquisition $130,079.00 $3,893,699 3.34%

New Alliance Bancshares Company Acquisition $676,727.00 $8,712,097 7.77%

Harleysville National Corporation

Company Acquisition $130,889.00 $5,646,195 2.32%

Great Lakes Bancorp Company Acquisition $41,769.00 $891,973 4.68%

Hudson River Bancorp Company Acquisition $352,528.00 $2,579,259 13.67%

Troy Financial Corporation Company Acquisition $218,091.00 $1,247,755 17.48%

Finger Lakes Bancorp, Inc Company Acquisition $32,811.00 $387,818 8.46%

Iroquois Bancorp, Inc. Company Acquisition $43,800.00 $595,126 7.36%

CNY Financial Group Company Acquisition $17,000.00 $296,294 5.74%

Albion Banc Corp. Company Acquisition $7,600.00 $78,711 9.66%

Total Goodwill $2,423,294.00

Total Deposits Acquired $33,428,927.00

Average Deposit Premium Paid 7.25%

FIRST NIAGARA FINANCIAL GROUP

Page 15

GOODWILL ANALYSIS: SALES AND DIVESTITURES

Company (Number of Branches) Transaction Type

Premium Received

Deposits Sold Implied Deposit Premium

Financial Institutions, Inc. (8 Branches)

Branch Divestiture $15,032.00

$286,500.00 5.25%

Community Bank System, Inc. (19 Branches)

Branch Divestiture $31,000.00

$797,400.00 3.89%

KeyCorp (37 Branches) Branch Divestiture $115,000.00

$2,000,000.00 5.75%

C.C.Bancorp, Inc. (2 Branches) Branch Divestiture $585.00

$19,700.00 2.97%

Elmira Savings Bank, FSB (4 Branches)

Branch Divestiture $12,230.00

$78,000.00 15.68%

Legacy Bancorp, Inc. (5 Branches) Branch Divestiture $9,770.00

$76,629.00 12.75%

Pathfinder Bancorp Inc. (MHC) (1 Branch)

Branch Divestiture $2,400.00

$26,400.00 9.09%

Total Premium Collected $186,017.00

Total Deposits Sold $3,284,629.00

Average Deposit Premium Collected 5.66%