Nance L. Schick, Esq. Law Office of Nance L. Schick New York, NY

Upload

fletcher-nance-and-associatesCategory

view

194download

0

http://businessautohomerenterscondoinsurance.blogspot.com/

Fletcher Nance & Associates

http://businessautohomerenterscondoinsurance.blogspot.com/

http://businessautohomerenterscondoinsurance.blogspot.com/

http://businessautohomerenterscondoinsurance.blogspot.com/

http://businessautohomerenterscondoinsurance.blogspot.com/

http://businessautohomerenterscondoinsurance.blogspot.com/

House

http://businessautohomerenterscondoinsurance.blogspot.com/

Apartment or Condo

http://businessautohomerenterscondoinsurance.blogspot.com/

Automobile

http://businessautohomerenterscondoinsurance.blogspot.com/

Mobile Home

http://businessautohomerenterscondoinsurance.blogspot.com/

Insurance Policy:A binding, legal contract between the policyholder and the insurance company to protect their home and belongings if

they are damaged, destroyed or stolen.

http://businessautohomerenterscondoinsurance.blogspot.com/

Protection From Fire, Storm, Weather and Theft

http://businessautohomerenterscondoinsurance.blogspot.com/

Anyone named in the policy: spouse, children, residents or guests

It can Protect detached structures too: garages, sheds, pools

Who & what are protected?

http://businessautohomerenterscondoinsurance.blogspot.com/

Renters InsuranceProtects individuals who live in a house, mobile home, condominium, or apartment that is owned by another person

Protects against:• Theft• Loss of personal property• Loss of use• An average two bedroom apartment can easily contain personal

property that would cost more than $20,000 to replace

http://businessautohomerenterscondoinsurance.blogspot.com/

Your landlord or association may have insurance, but it only protects their

building

Your belongings are not covered under their policy

http://businessautohomerenterscondoinsurance.blogspot.com/

Actual Cash Value (ACV)ACV coverage only pays for what the property was worth at

the time of loss, its current value.

Replacement CostReplacement cost coverage will pay what it actually costs to replace

the items you lost.

http://businessautohomerenterscondoinsurance.blogspot.com/

How to Reduce Risk • Keep an inventory of your personal

belongings• Keep receipts for major items• Lock your doors• Use your deadbolts• Don’t let your house look vacant • Maintain your home

http://businessautohomerenterscondoinsurance.blogspot.com/

PROPERTY INSURANCEInsurance that protects you from loss of real and personal property

Real property- Property attached to land such as a house, business, garage or another building

Personal property- Includes possessions that can be moved like furniture, jewelry and electronic equipment

http://businessautohomerenterscondoinsurance.blogspot.com/

TYPES OF PROPERTY INSURNACEExtended coverage- protects against damage from windstorms, aircraft crashes, hail, falling objects and explosions and vandalism.

Liability Protection- protects you from the costs of injuries to others on your property. It pays for medical expenses and legal costs.

Additional Living Expenses- It pays for the cost of renting another place to live if your home is damages. The coverage is limited to 10-20% of the coverage on your home. The time can be limited from 6-12 months.

http://businessautohomerenterscondoinsurance.blogspot.com/

Business Insurance- Business owners can get insurance to cover the costs of the property and liability insurance to protect themselves from claims by anyone injured on the premises

http://businessautohomerenterscondoinsurance.blogspot.com/

Homeowner’s Policy- provides protection against loss from the eleven perils

Eleven Perils- The most common causes of property damage or loss. They include:Fire or lightning, Loss of property from fire, Windstorm or hail, Explosion, Riots, Aircraft, Vehicles,Smoke, VandalismTheft Breakage of glassAll homeowner’s policies cover the eleven perils.

http://businessautohomerenterscondoinsurance.blogspot.com/

The six types of Homeowner’s policies are:1. HO-1 Basic form is the least expensive policy. This policy protects a

home and personal property against the eleven perils. It also covers liability insurance, damage to personal property and temporary living expenses.

2. HO-2 –the most popular policy or Broad coverage adds 7 additional types of coverage including, ice or snow damage, internal pipe damage causing water damage, electrical fires and falling objects.

3. HO-3-provides maximum protection for the house itself, with less coverage for personal property.

4. HO-4- is the policy for renters covering personal property.

5. HO-5- the all risk policy provides the most comprehensive coverage. It insures a building and its contents with maximum coverage. It is the most expensive policy.

6. HO-6- is a policy for condominium owners. It covers personal property and anything else inside the unit.

http://businessautohomerenterscondoinsurance.blogspot.com/

Homeowner’s PolicySpecial coverage's-Most homeowners policies cover special items such as jewelry for limited amounts. You can buy additional insurance for special items such as coin collections, or other valuables such as antiques.

Rider-An addition to the policy that covers specific property or damages. Riders are often used for jewelry, art or antiques.

NONE of the homeowner’s policies cover loss from floods, earthquakes, landslides, war or nuclear hazards. If you live in a flood zone, you must purchase flood insurance (if you have a mortgage)

http://businessautohomerenterscondoinsurance.blogspot.com/

Amount of InsuranceInsurance companies recommend that you insure your home for 80% of its market value since fires do not destroy the land or foundation.

As the value of your property increases you should also increase the amount of your insurance. You can insure property for either its actual cash value or its replacement cost. The replacement value is the full cost of repairing or replacing the property today, regardless of the depreciated value.

http://businessautohomerenterscondoinsurance.blogspot.com/

Property insurance has many of the same costs vehicle insurance does. The number of claims affects the overall cost. The premium depends on the amount of coverage and the type of policy you want. Factors that affect price include:

1. Deductible-amount of money you pay out of your pocket before insurance coverage begins. The higher the deductible the lower the premium.

2. Location-Urban areas usually cost more. Access to fire hydrants also can affect cost.

3. Type of building-A house made of brick will cost less than a house constructed of wood. The larger the house the higher the premium

4. Preventative measures-burglar alarms or smoke detectors, deadbolts and sprinkler systems.

http://businessautohomerenterscondoinsurance.blogspot.com/

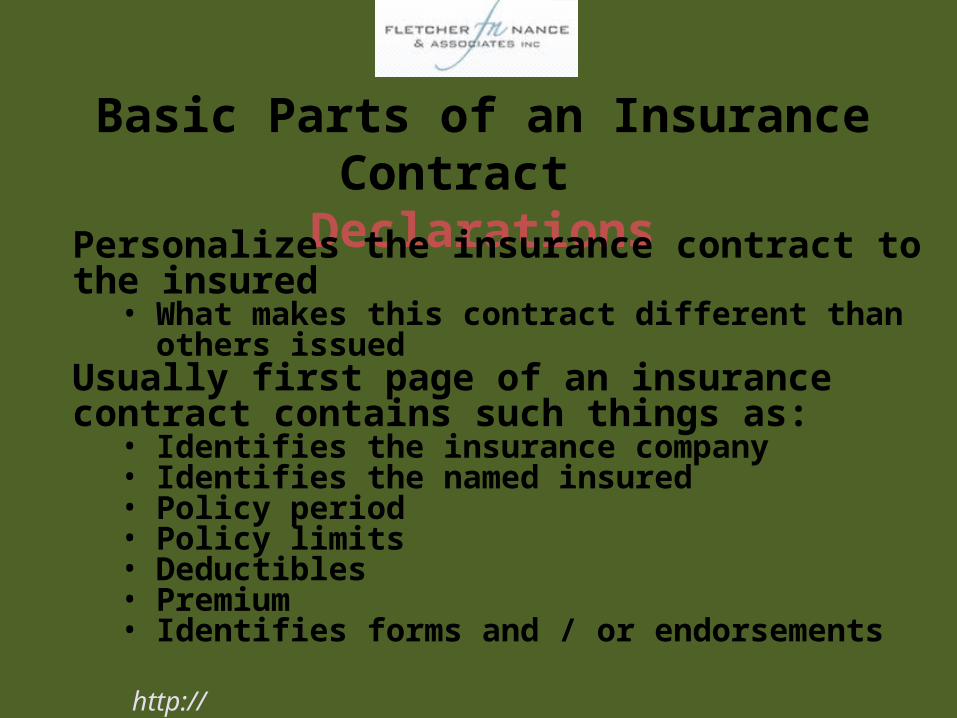

Basic Parts of an Insurance Contract Declarations

Personalizes the insurance contract to the insured

• What makes this contract different than others issued

Usually first page of an insurance contract contains such things as:

• Identifies the insurance company• Identifies the named insured• Policy period• Policy limits• Deductibles• Premium• Identifies forms and / or endorsements

http://businessautohomerenterscondoinsurance.blogspot.com/

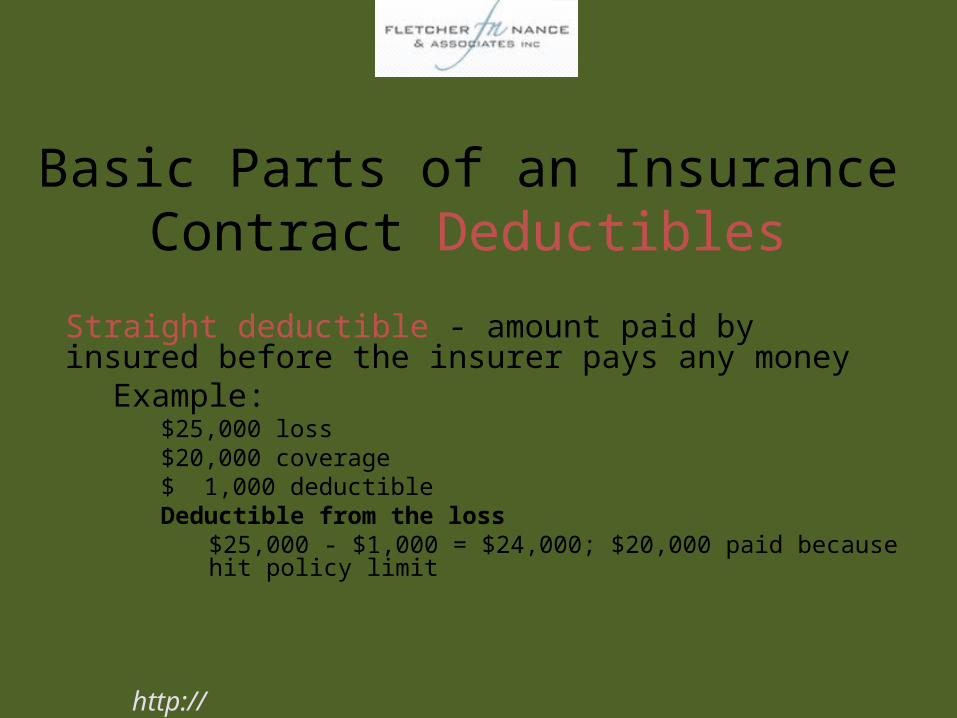

Basic Parts of an Insurance Contract Deductibles

Straight deductible - amount paid by insured before the insurer pays any money

Example:$25,000 loss$20,000 coverage$ 1,000 deductibleDeductible from the loss

$25,000 - $1,000 = $24,000; $20,000 paid because hit policy limit

http://businessautohomerenterscondoinsurance.blogspot.com/

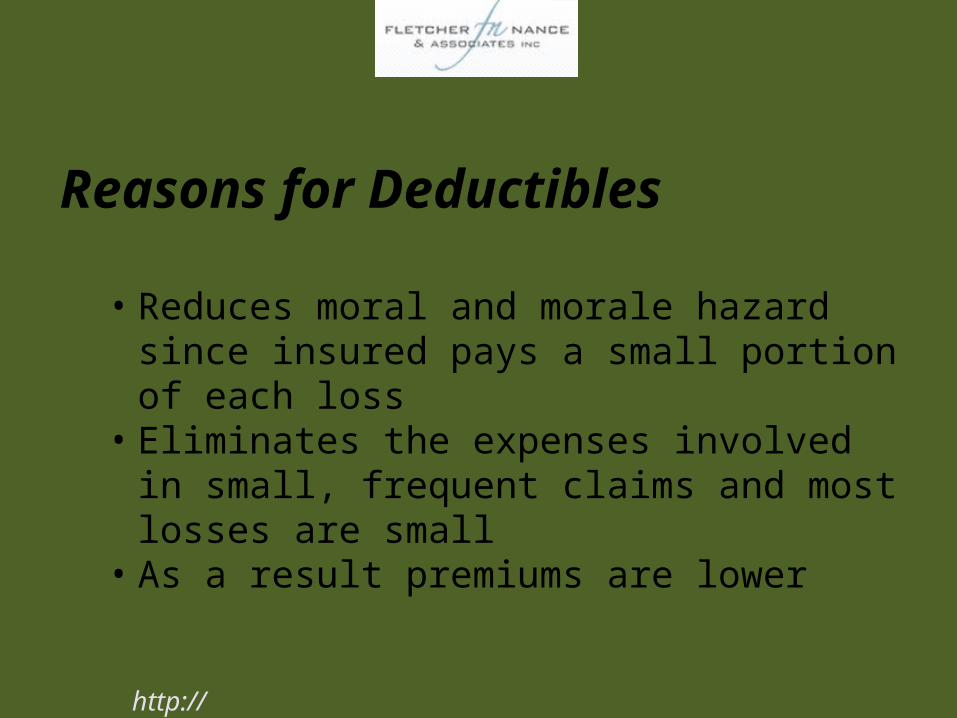

Reasons for Deductibles

• Reduces moral and morale hazard since insured pays a small portion of each loss

• Eliminates the expenses involved in small, frequent claims and most losses are small

• As a result premiums are lower

http://businessautohomerenterscondoinsurance.blogspot.com/

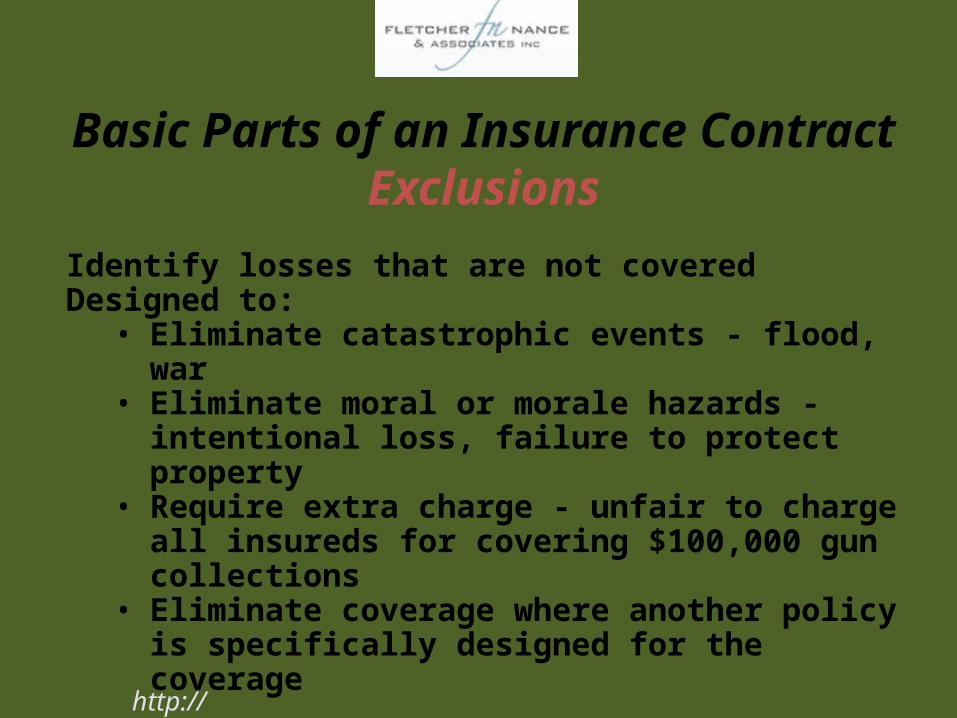

Basic Parts of an Insurance Contract Exclusions

Identify losses that are not coveredDesigned to:

• Eliminate catastrophic events - flood, war• Eliminate moral or morale hazards - intentional

loss, failure to protect property• Require extra charge - unfair to charge all

insureds for covering $100,000 gun collections• Eliminate coverage where another policy is

specifically designed for the coverage

http://businessautohomerenterscondoinsurance.blogspot.com/

Basic Parts of an Insurance Contract Endorsements

Modify standard insurance contracts in predetermined ways - examples

• Expand coverage• Delete exclusions in contract• Change definitions

• e.g.: “ sporadic baby-sitting is not a “business”• Add locations / insureds / perils• Add additional insureds

http://businessautohomerenterscondoinsurance.blogspot.com/

Basic Parts of an Insurance Contract Conditions

If you want the claim paid, you must meet the conditions stated in the contract. These include:

• No Concealment or Fraud• No Suspension of coverage• Cancellation – policy must be in force• Other insurance does not apply or loss is shared• Meet your duties after a loss• Abide by the appraisal procedure• Agree to salvage• Agree to claims payment - time limits

http://businessautohomerenterscondoinsurance.blogspot.com/

Income

PropertyPerson

What Does Insurance Protect?

http://businessautohomerenterscondoinsurance.blogspot.com/

http://businessautohomerenterscondoinsurance.blogspot.com/

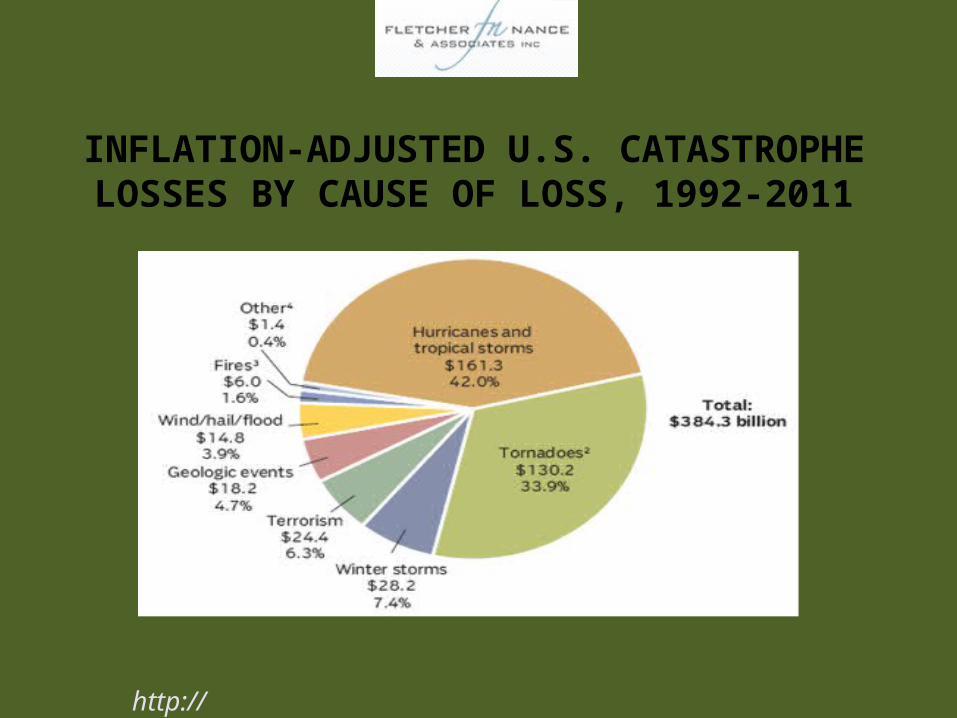

INFLATION-ADJUSTED U.S. CATASTROPHE LOSSES BY CAUSE OF LOSS, 1992-2011

http://businessautohomerenterscondoinsurance.blogspot.com/

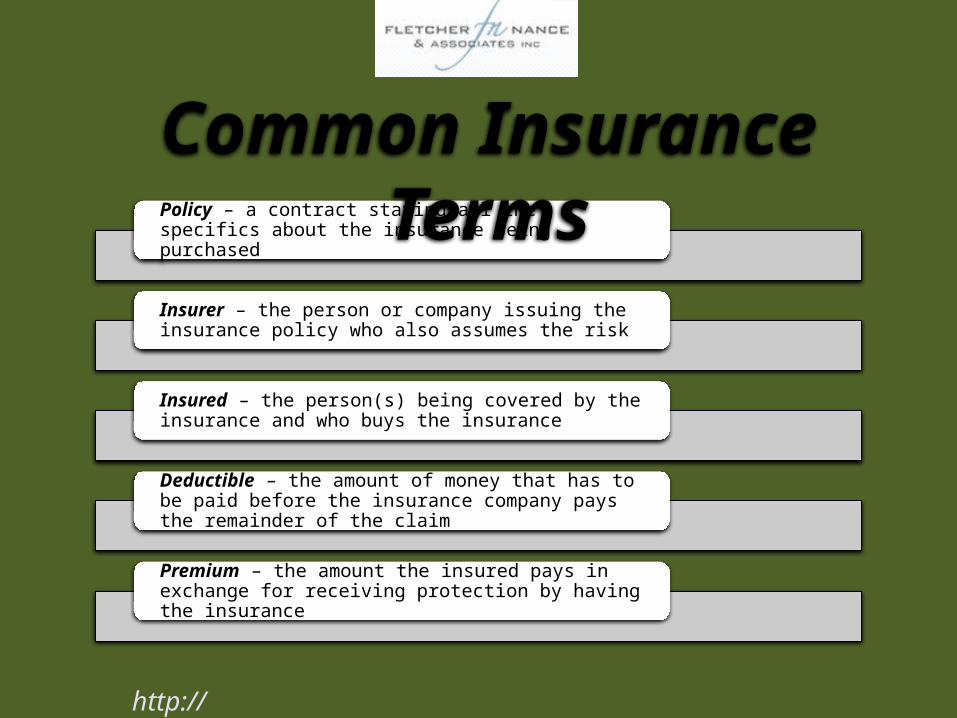

Policy – a contract stating all the specifics about the insurance being purchased

Insurer – the person or company issuing the insurance policy who also assumes the risk

Insured – the person(s) being covered by the insurance and who buys the insurance

Deductible – the amount of money that has to be paid before the insurance company pays the remainder of the claim

Premium – the amount the insured pays in exchange for receiving protection by having the insurance

Common Insurance Terms

http://businessautohomerenterscondoinsurance.blogspot.com/

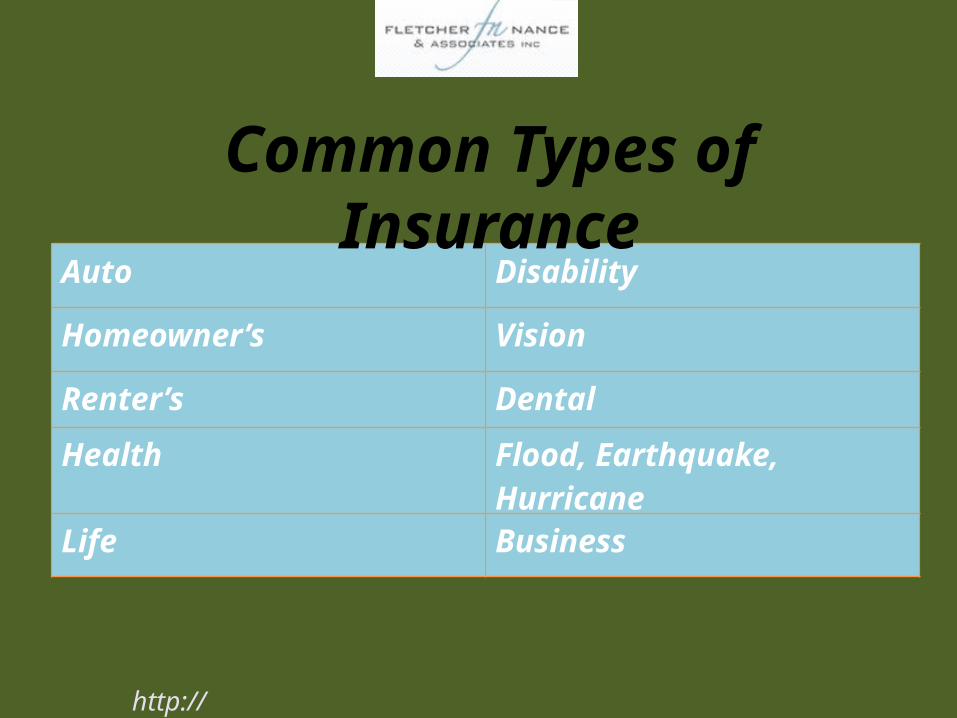

Auto Disability

Homeowner’s Vision

Renter’s DentalHealth Flood, Earthquake,

HurricaneLife Business

Common Types of Insurance

http://businessautohomerenterscondoinsurance.blogspot.com/

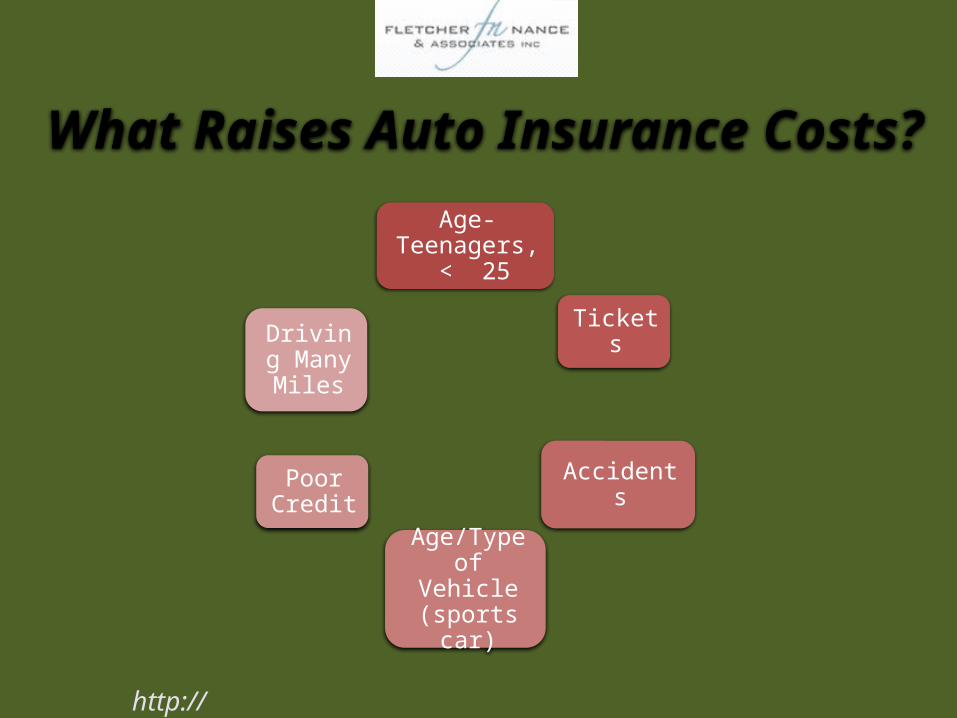

Age-Teenagers, < 25

Tickets

Accidents

Age/Type of Vehicle

(sports car)

Poor Credit

Driving Many Miles

What Raises Auto Insurance Costs?

http://businessautohomerenterscondoinsurance.blogspot.com/

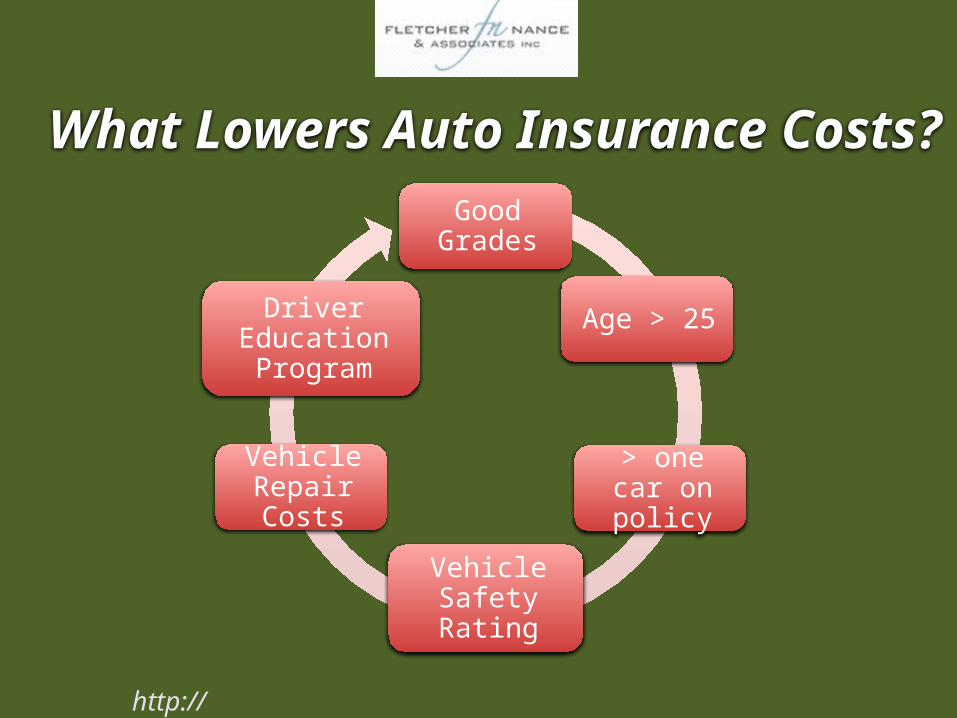

Good Grades

Age > 25

> one car on policy

Vehicle Safety Rating

Vehicle Repair Costs

Driver Education Program

What Lowers Auto Insurance Costs?

http://businessautohomerenterscondoinsurance.blogspot.com/

• Dwelling (the house itself)• Injuries• Theft, fire, tornado• Rider- covers items not

covered in the regular policy, such as higher jewelry amounts

Homeowner’s Insurance

http://businessautohomerenterscondoinsurance.blogspot.com/

Renter’s Insurance

• Damage to property• Theft of property• Possibly living expenses

http://businessautohomerenterscondoinsurance.blogspot.com/

Life Insurance

• Pays a pre-determined amount in the event of death• Usually more appropriate for people with dependents• Usually more appropriate for people with debts and expenses

that will need to be paid for• Can replace lost income if the main wage earner dies

http://businessautohomerenterscondoinsurance.blogspot.com/

Disability Insurance

• Short-term- replaces part of your income for a short time period, maybe up to a year or so, due to injury, illness, or extended maternity leave

• Long-term- income can be partially replaced for a longer time period, possibly years

http://businessautohomerenterscondoinsurance.blogspot.com/

Flood, Earthquake, Hurricane

• Covers property and contents in areas prone to these natural disasters

• The Federal Emergency Management Agency (fema.gov) provides information on preparing for natural disasters and disaster insurance

http://businessautohomerenterscondoinsurance.blogspot.com/

Affordable Care Act

• Signed in March 2010• Makes preventive care more easily accessible and inexpensive for more

people• Allows children to be on a parent’s health insurance plan until 26 years

of age• Beginning in January 2014, pre-existing conditions can no longer be a

cause for denials or higher insurance rates• Enrollment in the Health Insurance Marketplace begins in October 2013• New and expanded coverage begins January 2014

http://businessautohomerenterscondoinsurance.blogspot.com/

Minimize All Kinds Of Risk Using The Right

CombinationOf Insurance Products

FromFletcher Nance

http://businessautohomerenterscondoinsurance.blogspot.com/

Contact Fletcher, Nance and AssociatesFor any additional questions or to have the best insurance portfolio put in place to minimize risk for you and your family

Fletcher, Nance and AssociatesBill Nance