Flame Investment Lab

38

Flame Investment Lab Handbook 2015-2016 Made by: FIL Members Complied by: Gopal Vaid

-

Upload

gopal-vaid -

Category

Documents

-

view

93 -

download

0

Transcript of Flame Investment Lab

Flame Investment Lab

Handbook 2015-2016

Made by: FIL Members

Complied by: Gopal Vaid

“Those who don’t work with their hearts and passion may achieve success but

a hollow and half-hearted success which breeds bitterness all around”

Dedicated to Dr.APJ Abdul Kalam

Contents Book Reviews ..................................................................................................................................... 4

Conquering the Chaos: Ravi venkatesan............................................................................................. 4

DHANDHO INVESTOR- by Mohnish Pabarai........................................................................................ 8

George Soros - Investment Philosophy ............................................................................................. 10

The Outsiders ........................................................................................................................................ 11

Moats- Sustainable Value Creation....................................................................................................... 15

Breakout Nations – by Ruchir Sharma .............................................................................................. 21

Interview with Fund Manager Kenneth Andrade ................................................................................. 23

Observations From a Decade in the Investment Business.................................................................... 27

Four Lessons from Druckenmiller ......................................................................................................... 29

Variant Perception is Critical ................................................................................................................. 33

Quotes from the gods of investing ....................................................................................................... 35

Book Reviews

Conquering the Chaos: Ravi venkatesan Prepared by – Gopal Vaid

Ravi Venkatesan is the former chairman of Microsoft India and Cummins India. Prior joining to

Microsoft India as the Chairman of Cummins India, he was instrumental in transformation the

company into the country leading provider of power solutions and engines.

In this book he has summarized what is needed for a company to succeed in India, especially

for an MNC.

Large pool of talent which is doing work ranging from managing business process to running

information systems and engineering.

India has the ability of changing the cost structure of the company and add more to the

profitability

Most multinational companies in India see India primarily as a talent pool. For example IBM

employees around 142,000 Indians as a part of its workforce, which exceeded the number of

Americans working in the company.

Same is the case with Dell and Honeywell with employ 28,000 and 20,000 Indians.

Corruption is not limited to crony capitalism, it is rooted in the Indian system and at every step.

Government officials harass individuals and companies, whether it is to register a land

transaction renew a multitude of licenses, clear shipment through customs or win a public

tender.

Companies find themselves continuously extorted by inspectors who handle pollution control,

labor laws and indirect taxes.

Their choice is between spending countless hours defending themselves or paying one more

tax to individuals so they can focus on business.

There is no uniformity in the policies related to any of the sector.

For example: GVK reedy whose company was making an Investment in the Mumbai airport, the

developer had to deal with over 220 cases over property, environmental and labour disputes

in the process.

The author mentions the term VUCCA which describes well the business environment in India.

Volatility, uncertainty, complexity, Ambiguity and Corruption

“ If the government does not step in and uphold the rule of law, there was every possibility that

India could become a banana republic” – Ratan Tata, the chairperson of Tata Group

“This has been the most destructive period of regulatory environment I have seen in 16 years”-

Sunil Mittal, the chairman of the Bharti Airtel”

“India grows at the night……when the government sleeps”-Gurucharan Das, author of the book

“India grows at night”

According to Indian anticorruption website. www.ipaidbribe.com

45 percent have paid bribe to judiciary

61 percent to obtain registry services and permits.

62 percent have paid off officials in connections with buying and selling of land.

According to KPMG survey, 71 percent companies felt that fraud is “an inevitable cost of

business and 55 percent have experienced fraud.

Minimal government intervention:

All the evidence suggests that industries dependent on state policy, government regulations, and

access to public resources, like infrastructure, mining, and natural resources find tough going in India.

Whereas sectors like IT, Pharmaceuticals and consumer goods have flourished because they have been

kept at an arm’s length from the government.

The winning companies must straddle the pyramid:

By this the author means that the Indian opportunity in most industries is not the small global segment

at the top, but the middle market, and the great companies do not target only the top market but they

focus on the middle markets and develop products tailored for India that span different price points.

Therefore, smart companies will somehow find a way by selling global products to top section of the

society and then find a way to crack down into the middle market.

In order to capture the middle market companies need to bring innovation, so as to make

products which fulfill the Indian requirements and develop localized business model that allows

them to be profitable at low price points.

Focusing on the middle markets is true for both the industrial as well as consumer goods.

Example: India commercial vehicles market, sales in the premium segment are around one hundred

thousand trucks a year, while the market volume is around three hundred thousand trucks.

Companies which have fit the model:

Symphony is a company which is in into manufacturing of air coolers and makes products in

the range of ₹4500-₹17000.

Now, the company target market is not the rich households, but the population which belongs to

Aspirers and deprived section of the Indian Income pyramid. So they have quite successful managed to

place themselves in the middle market which size about 200 million households.

Having a dominant share in the emerging trend because if one does not identify a shift in the

market, then the company instead of being a leader in the market can become just a

competitor toiling hard to maintain itself in the market.

For Example:

Using low cost-chipsets from Chinese company called Mediatek, companies like Micromax,

Karboon started manufacturing mobile handset that could hold two sim cards. Customers in

India liked these features in India as they would swap out the second sim card every month to

get the best deals on outgoing calls. Nokia which had dominant share in the market, was quite

slow to identify this emerging trend and launched its dual sim phones in June 2011 but that at

that point of time it had already lost 30% of market share.

Companies must create localized business model, including a supply chain that overcomes local

challenges and delivers margins even at aggressive price points.

For Example: McDonald’s India makes money even at the price point of ₹ 25 for a burger.

The winning companies take a long term view, trading short term profits for growth and

leadership. They make investments in product localization and distribution and create a brand

which is ahead of demand and ahead of competitors.

MNC’s should look to run India as a geographic profit center empowering the local organization

to grow business.

Is Joint venture the right way to grow in India?

In India joint venture, success rate has been unsatisfactory with nearly 60 percent of the joint

venture being unsuccessful.

For Example : Tata-IBM, Mahindra-Renault, TVS-Suzuki, Godrej-P&G,

Modi-Xerox.

Whereas, ties between some of family owned companies and MNC’S have been fairly

successful. For Example: Kirloskar Cummins, JCB (Escorts)

Joint ventures are usually successful in the industry where each partner complementary

capabilities can reshape an Industry. For example Volvo came into India with Eicher. Volvo

brought modern technology, a global brand and economies of scale, whereas Eicher brought

frugal engineering, local brand, market knowledge and distribution.

For Example in Industry such as telecommunication, defense, mining. MNC’s partner with

Indian firm to get permissions, licenses and permits.

For Example: Telecom Giants Telenor and Etisalat entered into alliance with real estate groups

like Unitech and DB reality.

For JV to succeed partners need to have patience and need to think for the long term.

Personal chemistry between senior leaders is essential for JV’s to succeed.

For Example: In a joint venture, things often get messy; people are imperfect, so disagreements

can lead to distrust. That’s when the two CEO’s must trust each other and cut through the

confusion.

Companies are unwilling to do things differently for the Indian Markets.

For Example: In, Mahindra and Renault joint venture, Renault launched a low cost car (Logan)

that has been successful in Europe but it was too expensive compared to Indian Market, and it

was not sufficiently localized.

Also, Renault rivals lobbied successfully to get the excise duty raised from 8% to 20% on cars

longer than 4 meters. Logan was 4.5 meters and in order to reduce the price. Mahindra wanted

Renault to shorten it. However Renault refused to tinker with its product range. This created a

disagreement between the two companies and finally the joint venture ended with Renault.

Are Acquisition better than JV?

Acquisitions that bring distribution processes, middle market brands and key capabilities can

be useful. The common mistakes are overpaying, inappropriate integration and incompatible

cultures or values.

Acquisitions create value for a company when it has been too late to enter in the market and

company has no other way to gain market share.

Rupee being depreciated, opportunity lies for the foreign companies to come and pursue

mergers and acquisitions.

Checklist to adapt with corruption

Train country manager and senior leaders explicitly accountable for the image, reputation and

influence of the company in India.

Second is to change practices that causes mistrust and focus on corporate governance.

Third, step is to embrace a philosophy of doing well by doing good so that over time, the

company is seen as benevolent, trustworthy and good for India.

DHANDHO INVESTOR- by Mohnish Pabarai

Prepared by – Gopal Vaid

Buy Simple Business, with slow rate of change

• FMCG

• IT Consultancy

• Insurance

MOAT- COMPETATIVE ADVANTAGE

• Company must have a durable and sustainable moat.

• “I do not want an easy business for competitors. I want a business with a moat around it. A very

valuable castle in the middle and then a duke who is in charge of the castle to be very honest

and hardworking and able. Then I want a moat around that castle. The moat can be various

things”

- Warren Buffet

WHAT CAN BE MOATS

• Great Product

• Access to certain specific resources

• Operational efficiency

• Large market share, Higher ROE and Profit margins,

FOCUS ON ARBITRAGE

• Grab the opportunity if the spread is available on two different exchanges.

• It is an ultra-low risk game.

However, today this size of the spread has become very less. As mostly stock trade at roughly same

price on different exchanges

MARGIN OF SAFETY ALWAYS

• In the time of distress in the market, you will see great business available at cheap price because

of fear in the financial markets.

• If any company which has a sound business model, superior cash flows but is in the bad news

place an Infrequent bet.

Also, at that time place huge bets by following the notion

“Heads I win, tails I do not lose much”

INVEST IN COPYCATS NOT IN INNOVATORS

• Copycats who are smart enough to copy the innovation and scale it up to capture large market

will emerge as winners in long run.

• Current Example:

BMW and Tesla motors sharing electric cars tech.

• Business who will always have a market and the products will always be in demand, even in the

bad times are low risk business.

• So go long on those companies whose business risk is less and uncertainty about them in future

is high

E.g. Stationary, Food, and Healthcare.

Avoid the combination of low risk and low uncertainty offered by the guys on the Dalal Street.

George Soros - Investment Philosophy Prepared by – Gopal Vaid

Identify the Herd Instinct

• A gap always exist between perception and reality

• Buy and selling happens not on the present state of fundamentals, but on the expectations.

• Not only the market participants offer their bias, but their bias may also influence the markets.

Theory of Reflexivity: Belief do is alter facts

• Market prices never offer the rational view of the future events. But rather a biased one.

• Search for an unexpected development

• Try to determine what the market total sum of these investors thought at any given point of

time.

• Flawed perceptions cause markets to feed on themselves

Process of reflexivity

• Unrecognized trend (Track)

• Beginning of the self-reinforcing process.(Buy)

• An increasing conviction(hold)

• A divergence between reality and perception(Sell)

• The climax ( test- Shorts)

• Start of mirror image self-reinforcing sequence in the opposite direction ( Massive shorting)

• Trend continued, the significance of speculative transaction grew.

Reflexivity Equation

• Bias affect not only the market price but also the so called fundamentals.

• P = Price

• F = Fundamentals

• B = Bias

P = f(B)……..1

F = f(P)………2

Conclusion

• Look for the events that will bring in cumulative bias and start self –reinforcing loop.

The Outsiders Prepared by Abhir Pandit

CEO’s Selection & Skillsets

“Follow the Money” approach

Buffett Quote

Capital Allocation pg 7 buffet quote on

Focus on Cash-flow not EPS

Buybacks

Patience + Boldness in acquisitions

Focus on per share Value not Overall size

Unorthodox approaches

Comparison of Outsiders vs GE and S&P

Capital Cities (Tom Murphy) vs CBS(Bill Paley)

• X--- 16x , 30 yrs ltr 3x--- x

• Focused Roll Up Approach vs Diversification

• CEO + COO Approach

• Broadcasting + Publishing

• Capital Allocation + Efficient Operations

• Extreme Decentralization Approach

• Debt fueled Acqs & later efficient ops

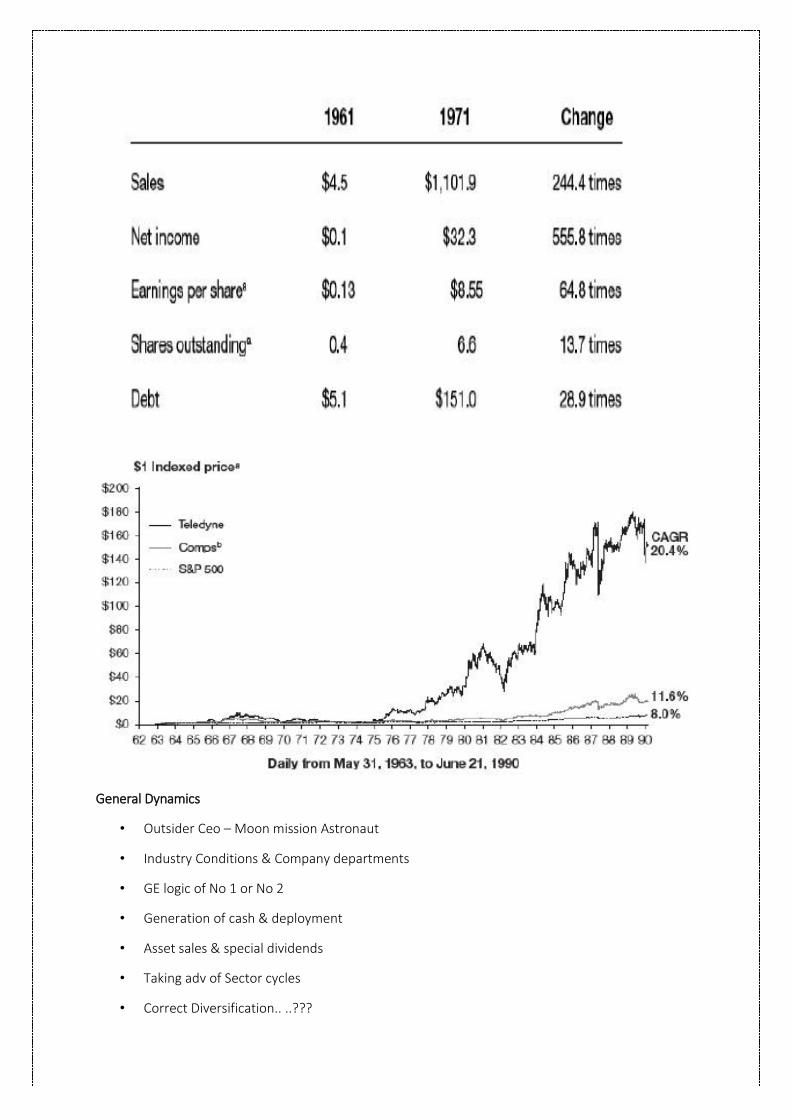

Teledyne – Henry Singleton

• Teledyne Model- Conglomerates

• Select Acqs using Overvalued Stock

• Focus on Cash Flow

• Aggressive Repurchaser

• Unique Approach

• Spin offs and Dividends

General Dynamics

• Outsider Ceo – Moon mission Astronaut

• Industry Conditions & Company departments

• GE logic of No 1 or No 2

• Generation of cash & deployment

• Asset sales & special dividends

• Taking adv of Sector cycles

• Correct Diversification.. ..???

TCI & John Malone

• Cable Industry Characteristics

• Cycle of scale by acq

• Use of Ebitda vs EPS

• Selective Aggressive Acquisitions

• Focus on programming

• Spin-offs strategy

• (read malone again)

• Tax minimization approach

Bill Stibitz- Public LBO

• Fmcg firms – like ITC

• Divestments and Smart acq

• Using leverage since FMCG business

Berkshire Hathway- Warren Buffett

• Generate funds at 3% and invest them at 13%

• Insurance underwriting & smart investing

• “Greedy when others are fearful and fearful when others are greedy”

• Concentrated portfolios

• “No bad Risks , only Bad Rates”

India Examples?

• Persistent

• Cera

• Symphony

• Ashiana

• Tcs

• HDFC bank

• Marico

• Ajay Piramal

• Edelweiss

Moats- Sustainable Value Creation Prepared by – Abhir Pandit

What is an economic moat?

Moat is a competitive advantage that a firm has when compared to its competitors that keeps

its market share alive.

In order to remain in the race businesses should develop an economic moat

Sustainable value creation is a part of economic moat

There are 3 ways competitive advantage can be achieved

Production Advantage(Lower costs of production)

Consumer Advantage(Product Differentiation)

Government

Sustainable Value Creation

Sustainable value creation is one of the most important aspect that managers generally tend

to forget

Sustainable value creation can be broken into two parts, how much economic profit a company

earns and how long can it earn this excess return

To evaluate how this sustainable value occurs, we have to explore many factors such as Industry

Analysis, Firm Specific Analysis, etc.

Industry Analysis

Industry Map

Profit Pool

Industry Stability

Industry Classification

Industry Map

A map that includes all the companies and constituents that might have an impact on the

industry.

The goal of an industry map is to understand the current and potential interactions that

ultimately shape the sustainable value creation prospects for the whole industry as well as for

the individual companies within the industry.

Profit Pool

• A profit pool shows how an industry’s value creation is distributed at a particular point in time.

• Profit pools are particularly effective because they allow you to trace the increases or decreases

in the components of the value-added pie

• It tells whether an firm is creating or destroying value that has been created or existing in the

industry

Cash flow return on investment (CFROI) is the indicator that helps a firm to evaluate the

performance of an investment or product. It can also be termed as the calculation that helps

the stock market to set prices on the basis of cash flow.

Industry Stability

Stability is an important factor because stable industries are more prone to value creation than

volatile industries

We can measure industry stability a couple of ways. One simple but useful proxy is the

steadiness of market share. This analysis looks at the absolute change in market share for the

companies within an industry over some period of about 5 years. We then add up the absolute

changes and divide the sum by the number of competitors. The lower the average absolute

change in market share, the more stable the industry.

Another way to measure stability in an industry is the pricing trend. If a firm has the power

to charge or change prices without losing its market share to its competitors then one can

say that it has created value

Industry Classification

• Classifying industries is an important aspect because each industry has different opportunities

associated with it. For example, for an emerging industry, first mover advantage plays a vital

role. According to me, this opportunity would play a vital role is value creation as the first mover

would hold key advantages when compared to firm that join the industry later. For example,

Technological leadership

Industry Structure—Five Forces Analysis

• An individual company can achieve superior profitability compared to the industry average by

defending against the competitive forces and shaping them to its advantage

• Collective strength of the five forces determines an industry’s potential for value creation.

Competitive Rivalry

• Rivalry among firms addresses how fiercely companies compete with one another along

dimensions such as price, service, new product introductions, promotion, and advertising. In

almost all industries, coordination in these areas improves the collective economic profit of the

firms. For example, competitors increase their profits by coordinating their pricing.

• Another influence of rivalry is firm homogeneity. Rivalry tends to be less intense in industries

with companies that have similar goals, incentive programs, ownership structures, and

corporate philosophies. But in many instances, competitors have very different objectives. For

example, an industry may have companies that are public, privately held, or owned by private

equity firms. These competitors may have disparate financial objectives, incentive structures,

and time horizons. The strategies that companies within an industry pursue will reflect the

heterogeneity of objectives.

• Asset specificity plays a role in rivalry. Specific assets encourage a company to stay in an

industry even when conditions become trying because there is no alternative use for the assets.

Assets include physical assets, such as railroad tracks, as well as intangible assets such as

brands.

• Final consideration in rivalry is industry growth. When the pie of potential excess economic

profits grows, companies can create shareholder value without undermining their competitors.

The game is not zero-sum. In contrast, stagnant industries are zero-sum games, and the only

way to increase value is to take it from others. So a rise in rivalry often accompanies a

decelerating industry growth rate

Disruption

Disruption can be broken down into 2 types – Sustainable and Disruptive innovation

• Sustainable disruption is nothing but product development i.e. continuous development to a

product that a company offers

• Disruptive innovation can be further broken down into 2 parts which are - low-end disruptions

and new-market disruptions

• Low end disruptions offer a product that already exists.

• A new-market disruption is providing a new product which is cheap or simple enough to enable

a new group to own and use it.

• The main point is that sustaining innovations operate within a defined value network—the

“context within which a firm identifies and responds to customers’ needs, solves problems,

procures input, reacts to competitors, and strives for profit.” e.g. Change in size of floppy disk

over time. In disruptive innovations, a new value network is created. E.g. Introduction of C.D’s

as data carriers.

• An example of low end disruptive innovation is most airline industries where the product

offered is not new and is not very different from the product offered by its competitors

• Disruptive innovations initially appeal to relatively few customers who value features such as

low price, smaller size, or greater convenience. Initially the product appeals only a group of

people. The incumbents (dominant firm in the industry) neglect this disruption or are not able

to reallocate their resources to produce this new disruption. Gradually, market share of the

industry is eaten by this disruptive innovation. The mini mills over integrated mills.

• Firm Specific Analysis

Creating value mostly is firm depended i.e. it depends on the strategies it pursues and the way

it handles its competitors.

Value created = willingness-to-pay – opportunity cost

Four strategies to create more value: increase the willingness to pay of your customers; reduce

the willingness to pay of the customers of your competitors; reduce the opportunity cost of

your suppliers; and increase the opportunity cost of suppliers to your competitors.

In firm specific analysis companies try to achieve competitive advantage which can broadly be

divided into 2 categories i.e. lowering production costs(production advantage) and

differentiation(consumer advantage)

Production Advantages

Firms with production advantages create value by delivering products that have a larger spread

between perceived consumer benefit and cost than their competitors, primarily by

outperforming them on the cost side.

A firm creates value if it has a positive spread between its sales and costs, including opportunity

costs i.e. if it has achieved economies of scale

Some points to consider are

Distribution

Purchasing

Research and development

Advertising

Consumer Advantages

Consumer advantage is the second broad source of added value. Firms with consumer

advantages create value by delivering products that have a larger spread between perceived

consumer benefit and cost than its competitors do.

Features of consumer advantages

Habit and high horizontal differentiation. A product is “horizontally differentiated” when some

consumers prefer it to competing products

Experience goods. An experience good is a product that consumers can assess only when

they’ve tried it.

Switching costs and customer lock-in. Customers must bear costs when they switch from one

product to another. The magnitude of switching costs determines the degree to which a

customer is locked in.

Government

The final source of added value is external, or government related. Issues here include

subsidies, tariffs, quotas, and both competitive and environmental regulation. Changes in

government policies can have a meaningful impact on added value.

Breakout Nations – by Ruchir Sharma Prepared by – Gopal Vaid

• Poland and Czech Republic are the breakout nations in Europe.

• Low domestic debt and manageable foreign debt.

• Steady momentum behind economic and political reforms.

• Going for the euro union membership but not for euro zone

• They were able to avoid the problem of internal devaluation.

• For the nations who have faced crisis in Europe, must follow the fried rich Hayek theory.

• Asian tigers, have chosen the path of export oriented model.

• Indonesia in particular has exports which are essentially commodities.

• Look for the “Rise of the second city”.

• Those nations which will build new cities having population more than 1 million could be

breakout nations.

• South Korea has been relatively better as compared to japan and Taiwan by having more

diversified manufacturing and strong brands.

• Follow the KOSPI index to evaluate global trends.

• Reliable data, foreigners own one third of Korean stocks and Korean companies are major

players in broad selection of Industries.

• Korea has been largely unique by showing exception to the rule of transition from

manufacturing sector to manufacturing even after attaining higher level of per capita income

• Major emerging markets are now moving in tandem, unlike previously moving according to

their own unique logic.

• Difference between worst and best performing markets was just 10%.

• Frontier nations who will mature their stock markets will grow.

• Watch out for Angola, which is $100 billion economy, but it has no stock exchange. Angola has

been talking about opening its markets.

• Srilanka is poised to grow, with investments coming up in infrastructure, srilankan currency

being competitive and high level of educated population with English Fluency.

• Vietnam which was backed by foreign investors to grow, lack of governance, infrastructure has

halted their growth.

• In order to spot credit bubbles, the general rule is that if the banking sector expands by more

than 20% a year for five straight years problems usually follow.

• Nigeria and EAC (East African community) may be breakout nations as high growth success

stories tend to appear in geographic clusters.

• Telecommunication services and internet boom is happening as

• The fiber optic network has increased by factor of 12, and internet capacity has increased by

factor of 100.

After the Ecstasy, the laundry

• Commodity market bubble in progress, (30% of global stock markets is in energy and

commodities).

• Historically prices of commodities have fallen, because with new technology the extraction of

commodity has been more efficient.

• Hype and exponential increase in the prices, have happened because of “Financialization of

Commodities”

• According to the U.S based energy research firm, Cornerstone the total volume of trades in

energy futures in 2011 was nearly two billions barrels a day, twenty two times higher than the

daily total global demand for energy.

• The reason behind the commodity bubble that the price of commodities will rise indefinitely

based on expanding china.

• “China is a big growing fish in a shrinking pond” and therefore, it does not imply insatiable

global demand for oil or any other commodity.

• Rise in the energy and commodity prices are putting billions in production facilities on the

estimate that oil and energy consumption of china will rise by 60% by 2015, whereas clear

message is coming from Beijing that investment surge is about to slow.

The third coming

Understand nations like individuals.

Volatility is here to stay.

As today every percentage point increase in income is matched by a 4 percent increase in trade

flows.

Return of boom and bust cycle.

Interview with Fund Manager Kenneth Andrade

Aarati Krishnan talks to Kenneth Andrade, Head, Investments, IDFC AMC, about his

journey in the mutual fund industry

Jul 28, 2015

Aarati Krishnan talks to Kenneth Andrade, Head, Investments,IDFC AMC, about his decision to

move on from the mutual fund industry while taking some last investment ideas from this

renowned portfolio manager.

Meeting Kenneth Andrade of IDFC Mutual Fund was sheer luck. Given that Kenneth has

recently announced his decision to move on from the mutual fund industry to 'pursue

entrepreneurial opportunities', journalists like me may no longer get an opportunity to pick

the brains of one of the true out-of-the-box thinkers in the Indian investment space.

I realise, as soon as the interview gets underway, that I may have to junk the long list of

questions that I've prepared beforehand. The moment I begin my 'what-do-you-think-of-

markets' questions, he pulls up a large Excel sheet on the screen and offers to explain where

he thinks Indian markets are going and how he's constructing his fund portfolios to reflect this

view.

I quickly discover that Kenneth's take on the market is very different from the views doing the

rounds on the Street. Even as most analysts are now rolling over their Sensex targets and

bravely projecting double-digit earnings growth for FY16, Kenneth holds the view that the

market is being too impatient in expecting a quick turnaround in earnings.

Too much too soon

'At the moment, there is a lot of expectation that the economy will turn track in one or two

years and that earnings will pick up in 2016 or 2017. We have a different take on that. Today,

BSE 500 companies have all-time high debt-equity ratios. Corporate balance sheets don't

have the space to grow. Neither do banks. For economic activity to pick up, you need balance

sheets to expand. So how do you grow?' he asks me.

Seeing that I am somewhat speechless, he pulls up a sheet that maps the assets, debt-equity,

net worth and profits of BSE 500 companies for the last ten years. Basically, the numbers show

that India's largest companies have been on an expansion binge in the last ten years, with their

total assets expanding from `8 lakh crore to `55 lakh crore. The expansion has been funded

mainly by debt and hasn't paid off yet. Corporate profits of India Inc have grown at a mere 12

per cent (CAGR) for the last ten years, while their capital employed has zoomed by 24 per cent

a year. As a result, while the aggregate debt-equity ratio has ballooned from 0.35 times to 0.8

times, the return on equity - the key driver of valuations - has dropped from 20.7 per cent to

11.5 per cent over this ten-year period.

This, Kenneth argues, is the real reason why corporate profits are growing at a snail's pace

today. 'I believe that people are building in too strong earnings growth expectations too early

in the cycle. People say that capex cycle will pick up. But from our numbers, it is clear that even

`10 lakh crore of capex may not move the needle much. Therefore, where is the 20 per cent

earnings growth going to come from?' Those numbers have my head reeling, but it is difficult

not to get convinced by Kenneth's conviction and passion for this subject.

Go for quality

As I grapple with all this, Kenneth adds that this doesn't mean he is negative on equity markets.

It is just that the revival that everyone is expecting may take time to materialise. And it is only

during periods of uncertainty that one has the best opportunities to enter into stocks. 'I think

we are close to the bottom of the cycle. Over the next two-three years, India Inc will gradually

increase its profitability. The additional cash flow can be used to pay down debt.' But, he

believes, this revival will be a 'slow grind up'.

So what does this imply for stock choices? Well, Kenneth is avoiding highly leveraged

companies and is negative on banks. 'We are looking for quality companies that dominate their

industry with moderate debt and positive cash flows.' But given that many fund managers are

on the hunt for 'quality', aren't such stocks trading at too-rich valuations? 'They are,' agrees

Kenneth, 'but I would rather take on valuation risks in my portfolios than solvency risks.'

So given this thesis, is there a dearth of good stock-picking opportunities, I ask? He says that

there are plenty of opportunities out there if you don't make market-cap distinctions. He isn't

a believer in small-cap or mid-cap stocks being riskier than large caps.

'Good firms can come from any market-cap range. Smaller firms may have good management

and turn out to be quite capital efficient. Not all large-cap companies have great promoters,'

he points out.

MSME Opportunity

But Kenneth's offbeat market view has meant that the portfolio of the flagship fund IDFC

Premier Equity isn't in sync with indices. The fund has been a middle-of-the-road performer

in the last one year. Given that investors tend to chase returns, will the fund lose out, I query.

'You have to deal with it. It's a competitive landscape. When IDFC Premier was giving a 100 per

cent return, we didn't get 100 per cent of the inflows. I believe as long as there's a structure

and logic to your portfolio construction, investors will understand.' He adds that if one

compares IDFC Premier Equity's returns to the large-cap, mid-cap and diversified equity indices

over the last ten years, the fund outperformed in nine out of ten years - it missed the Nifty by

1 per cent in a down year.

He thinks that the process of consolidation that is on in the markets today will lead to good

investment opportunities over the next few quarters. But he thinks it is important not to go

into an expanding economy with the wrong portfolio. He explains that most investors and fund

managers are scrounging in the same set of sectors, which is a mistake. To outperform over

the long term, you needed to be ahead of the curve on what would drive the next bull market.

'The next bull market can be driven by sectors and stocks which are not on our radar right now,'

predicts Kenneth, citing the example of Indian MSMEs.

'I think Mudra Bank can be a real game-changer for Indian MSMEs. If you look at corporate

India, the promoter's personal balance sheet is different from the company's. He usually

leverages the company's balance sheet. For the small business owner, there is no distinction

between his personal balance sheet and his firm's balance sheet. So if you make capital

available to him at much cheaper rates than the current 20 per cent-plus, he can scale up his

business. His personal spending can then boost the economy too.'He believes that such a

resurgence in Indian MSMEs can rejuvenate primary markets and expand the listed universe

of stocks far beyond what we can imagine today.

Watching them grow

So given his sober view on equities, where has he put his personal money? Is he going for the

mattress, I ask, jokingly. 'I am completely into equities. I believe in giving the market time to

deliver,' he says, stating that if you wait for valuations to get really cheap, you will never be

able to invest.

Then, does he own no fixed-income investments? 'I have been an equity investor all my life. In

equities, if you bide your time, you will get to double-digit returns. Fixed income can generate

double-digit returns for short time periods, but that's not sustainable. I look to debt mainly to

generate regular income,' he says.

So how did Kenneth get into this money management business? Was he always this passionate

about stocks? No, he laughs. 'I had no idea what I would like to become. I applied for a job at

Capital Market magazine after college. At that time, the magazine had in-house analysts who

wrote this column called IPO Monitor. I took the job up for 18 months.' He then worked as a

freelance journalist for a while before joining Apple Mutual Fund in 1994.

He has juggled quite a few jobs since then, working at smaller brokerages, before he got

recruited by SSKI in the late nineties. Then came the 'big break' into Kotak Mutual Fund and

then IDFC Mutual Fund about ten years ago. He stayed on at IDFC until 2015. What made him

stay on with IDFC for so long? He says that fund management fascinated him because it allowed

him to really study businesses. 'I love holding onto companies for really long time periods and

understanding what drives their transformation. I am not a votary of earnings growth. I would

rather buy companies which are efficient with their use of capital.'

Good stock-picking, he feels, is not about predicting whether technology will do well or autos

will do well. 'It is all about buying efficient capital.'

I switch gears to personal questions with some trepidation because Kenneth has this

reputation for being quite reserved. So what does he do in his leisure time? 'I do some reading,'

he says briefly, clamming up after talking freely about markets so far. Kenneth was born and

brought up in Mumbai and is a 'Kalina' boy. And though he does read in his free time, his

passion really is cars. He owns two electric cars ('all the electric ones available in the market')

and spends a lot of his free time 'keeping them in good shape'. 'Are electric cars a pain to drive?

Do they die on you on the road, just like a smartphone?' I ask, being quite irritated with my

phone for dying when I most needed it.

He vehemently defends his electric cars. 'No, my cars have never died on me. I've done 45,000

km on them and have a charging station at home and also one at the office,' he says. Kenneth

is a gadget freak and loves to replace his phone with the latest launch. Weekends are about

reading and experimenting with music. Kenneth has two teenage daughters who share all their

music with him. As I have a teenage son too, we compare notes on the bands they listen to.

The lyrics are awful, we agree, but the music is very catchy.

And when he has spare time, Kenneth takes his cars out for a drive. Where does he go? 'I just

get into my car and drive. I like to go for long drives at 60 km/hour wherever the road takes

me,' he says. Well, that statement may nicely sum up his latest career move too.

I may not get to meet him in his portfolio manager avatar again, but I'm sure with his passion

for investing, original ideas and keen intellect, Kenneth will make waves at his next stint as well.

Observations From a Decade in the Investment Business It was recently brought to my attention that it’s been ten years now since I started my first full-time job in the investment industry. More experienced investors might not think this is a very long time, but it feels like an eternity to me considering my current level of understanding compared to what I knew when I first started out.

Here a some observations about my time in the world of investments from the past decade:

Everything is getting faster. This includes information flow, trading, instant feedback and analysis and market cycles in general. I’ve also noticed that performance updates can no longer wait — investors want up-to-the-minute reporting and the ability to track their market value in real-time. Time frames continue to shorten.

What college you went to doesn’t matter. The only thing a top tier college is good for is getting you your first job through connections. But even that’s diminished these days to some degree because technology makes it easier than ever to network if you know what you’re doing. I went to a small private Division III school without much of a finance program. Right out of school I felt this was a disadvantage, but looking back on it now it was actually a huge benefit because I ended up basically being self-taught. I didn’t start out with any preconceived notions or biases about the way the markets work based on textbook theories that are more or less useless in the real world.

First impressions can be misleading. I’ve found that the people that absolutely wow you right off the bat are usually over-compensating. The ones that try to convince you that they have everything figured out are not the people you want to be listening to in this business.

Career risk is highly under-appreciated. I could come up with a laundry list of the reasons for poor market behavior from professional investors. Career risk would be at the top of that list. Incentives matter a great deal more in the decision-making process than most realize.

Everyone is conflicted in some way. It’s impossible to avoid conflicts of interest in the financial services industry. It is a business after all. The trick is to understand how incentives drive people’s actions and look for those firms and individuals that are up front and honest about any potential conflicts.

Always have a spare suit coat in your office. This one has saved me a few times with last minute (or forgotten) meetings. Also, never wear a blue shirt with a white collar. The Michael Douglas from Wall Street shirt just screams, “Would you like to buy an opaque annuity with ridiculously high fees?”

You get to know people better over dinner or drinks. I’ve always found the standard interview process to be fairly useless. You will always learn more about potential hires or employers by going out to eat or getting a drink together than you do from a formal, sit-down interview. HR-type interviews are too stuffy and rehearsed.

It’s good to have an outlet. Whenever I have the time, I try to workout at lunch. In finance you spend most of your time in front of a computer, in meetings or on conference calls. It’s helpful

to stretch your legs and take the occasional break to re-charge. I find I get the majority of my best thinking done during this time. My other outlet is writing, which I wish I would have started sooner.

Communication is a highly under-rated skill. I always assumed my analytical skills would help set me apart in this business. While you have to have an analytical mind to succeed in finance, without the ability to communicate with a variety of audiences — clients, colleagues, bosses, potential employers, etc. — even top-notch analysis can get lost in the shuffle.

There’s always going to be someone smarter than you. While it’s easy to mock the financial industry for their poor forecasting abilities and potentially damaging advice, there are an insane amount of brilliant people working in finance. At first I was always in awe of the smartest person in the room. But it’s worth acknowledging that intelligence without the requisite common sense does you no good. Brilliance does not always translate into success in the markets, and in fact, it can be to your detriment if it leads to extreme levels of overconfidence.

The best people in this industry are often overlooked. Many great investors out there are overshadowed because they aren’t making a never-ending series of outlandish predictions, they don’t resort to scare tactics, and their main goal is not to push unnecessary products on unwitting clients.

Information is everywhere but people still choose to ignore the evidence. There are academic research papers and real world case studies on nearly every investment strategy known to man yet many investors still choose to wear blinders and only read that which agrees with the way they do things.

Self-awareness is essential for long-term success. I can’t remember exactly when it was that I had my aha moment, when I first really “got it.” But it’s made me a more clear-headed investor. When I say “got it” I don’t mean that I finally figured everything out that there is to know about the markets. Getting it to me meant that I understood that I would never truly have it all figured out. Learning would be a life-long pursuit but there was never going to be a time when I could say, “I’m finished. I’ve figured out everything there is to know about the financial markets and how to be the perfect investor.”

I think it was a combination of watching people much smarter than me fail at the game of investing over and over again and learning about the importance of human psychology on our actions and decision-making abilities. All of these cognitive biases I was reading about I had witnessed first-hand, either through my own actions or by watching other market participants.

The markets can be a very humbling place, but it’s not until you’re willing to show humility that you can start to see lasting improvements in your results over time. It can be extremely difficult for very intelligent people, with years of higher education and professional designations under their belt to be completely honest with themselves about the markets.

The markets are hard. Slowing down is important. A legitimate decision-making process that reduces the impact of your emotions is essential. But none of this is possible without the self-awareness to admit your own limitations.

Four Lessons from Druckenmiller As noted last month, the legendary Stan Druckenmiller officially retiredfrom public money management in August.The media reaction to Druckenmiller’s exit stage right was a classicexample of sic transit gloria — glory fades.With a focus on professed tiredness and stress, short shrift was given tothe fact that Druckenmiller was, undoubtedly, one of the greatestmoney managers of all time.With a track record in his Duqesne fund of 30% compound returns over30 years — with no losing years – Stan Druckenmiller is to moneymanagers as Wayne Gretzky is to hockey, Michael Schumacher is toFormula One racing, or Jack Nicklaus is to golf.(The “Michael Jordan” moniker is taken by Paul Tudor Jones, a good buddy of Druckenmiller’s who isstill active.)Druckenmiller also has the distinction of sharing the most profound piece of wisdom in the entireMarket Wizards series. If you truly understand this observation, then you understand how tobecome rich: The way to attain truly superior long-term returns is to grind it out until you’re up 30 or 40 percent, and then if you have the conviction, go for a 100 percent year. If you can put gether a few near-100 percent years and avoid down years, then you can achieve really utstanding long-term returns- Stanley Druckenmiller, New Market WizardsAnd of course, that is exactly what Stan the Man did…Reflecting on Druckenmiller’s retirement — and track record — leads to four conclusions applicable to traders and investors today. Lesson #1: SIZE MATTERS Yes Virginia, size does matter. But not in the way one might think. (Geez, get your mind out of thegutter!)At the time of Druckenmiller’s retirement announcement, Duquesne Capital Management LLC washandling $12 billion. That’s a lot of dough. In fact, it’s a bit like trying to steer an ocean liner.The great global macro managers are known for their ability to nimbly exploit opportunities in deep,liquid markets. And the more liquid the vehicle the better, because liquidity allows the manager to turnon a dime — or to step aside and quickly go to cash if need be.But the bigger you get, the harder it becomes to implement a pure trading style. Size becomes aheadache in that it’s an impediment to getting in quickly, and sometimes an even bigger impediment togetting out.Forbes Magazine recently estimated Druckenmiller’s personal fortune at $2.8 billion. No wonder hewants to just run a “fun” portion of his own money again, farming out the rest to colleagues through a family office. Cutting back total size to a measly $500 million – $1 billion or so would feel like a speedboat in comparison to the full Duquesne load.As an important takeaway here, size matters to regular investors and traders too, in respect tothe fact that being small comes with a huge advantage!And what is that advantage, you ask? It is the ability to load the boat on your best ideas.If you are trading with anything less than $100 million — or, heck, a few hundred million for that matter — then your highest conviction ideas have a much better chance of adding outperformance tothe portfolio, due to a practical lack of capacity constraints.Hedge fund manager Joel Greenblatt, whose Gotham Capital earned 50%+ returns for more than adecade, explains this phenomenon in his book You Can Be a Stock Market Genius. (A terrible title, buta great read.)To explain the small investor’s edge, Greenblatt uses the example of “Bob,” a pseudonymous friend ofGreenblatt’s tasked with allocating billions under strict institutional rules From a practical standpoint, when Bob [a

bigtime equity fund manager] chooses his favourite stocks and is on pick number twenty, thirty, or eighty, he is pursuing a strategy imposed on him by the dollar size of his portfolio, legal issues, and fiduciary considerations, not because he feels his last picks are as good as his first or because he needs to own all those stocks for maximum portfolio diversification. In short, poor Bob has to come up with scores of great stock ideas, choose from a limited universe of the most widely followed stocks, buy and sell large amounts of individual stocks without affecting their share prices, and perform in a fish bowl where his returns are judged quarterly and even monthly. Fortunately, you don’t.Is it any wonder Druckenmiller grew wary of steering an ocean liner? “I plan on managing a decent chunk of my money, but only an amount that will be fun,” he told Bloomberg. The man wanted to be light and nimble again. (Relatively speaking of course.) Lesson #2: OUTPERFORMANCE IS POSSIBLE If you’ll pardon the color, we at Mercenary Trader can’t help but fully agree with this assessment from Helmut Weymar, a founder of the legendary Commodities Corp:I thought random walk was bullshit… The whole idea that an individual can’t make seriousmoney with a competitive edge over the rest of the market is wacko.Amen to that. (Paul Samuelson, a godfather of EMH and the dean of neoclassical economics, apparently didn’t buy the bullshit either, as fully clarified here.)As Market Wizard Larry Hite once observed, everyone he ever met who believed in efficient markets was poor. The poor eggheads argue, miraculously, that markets have some mysterious source of efficiency, unknown in source or sustenance, that prevents outperformance from being possible, evenfor the alpha dogs supposedly dominating markets in the first place!This line of thought deserves outright scorn and ridicule, and perhaps a sense of wonder at the sheer pigheadedness of the assertion. (Man as consistently rational utility maximizer? No. Talent equallydistributed? No. Information objectively interpreted? No. As Yale professor Robert J. Shiller has observed, the efficient market hypothesis is “one of the most remarkable errors in the history ofeconomic thought.”)When defending EMH in public, academic true believers resort to the “Trained Orangutan” argument,which basically asserts that money managers are little more than lucky coin flippers — and that with enough flippers on hand, one is bound to see the emergence of a few excellent track records solely onthe basis of luck.Warren Buffett, aka the greatest value investor of the age, took on this argument and demolished it ina tour de force titled “The Superinvestors of Graham and Doddsville.” You can read the whole piecehere, or otherwise find it on the web.Buffett’s essential rebuttal was that, if the trained orangutan / lucky coinflip charge held true, then thewinners with long-term track records should have randomly distributed styles of varying logic andrationality.One lucky flipper might believe in reading astrological signs, for example. Yet another might pray to Vishnu, or buy stocks that begin with the letter “R.” Those might be slight exaggerations… point being,though, that if the market winners win based on luck, as the random walkers assert, then thestrategies of the “winners” should be sufficiently varied to suggest random intellectualdistribution as a group.This is not what happens.As Buffett pointed out, in his circle — the value investing circle of the Graham and Dodd school — a class of investors did things the same way, focused on the same things, and applied the samephilosophies and methodological principles to consistently outperforming the market. As Buffett put it,If you were trying to analyze possible causes of a rare type of cancer — with, say, 1,500 casesa year in the United States — and you found that 400 of them occurred in some little miningtown in Montana, you would get very interested in the water there, or the occupation of

thoseafflicted, or other variables. You know it’s not random chance that 400 come from a small area.You would not necessarily know the causal factors, but you would know where to search.I submit to you that there are ways of defining an origin other than geography. In addition togeographical origins, there can be what I call an intellectual origin. I think you will find that ad isproportionate number of successful coin-flippers in the investment world came from a verysmall intellectual village that could be called Graham-and-Doddsville. A concentration ofwinners that simply cannot be explained by chance can be traced to this particular intellectual village.Now, getting back to Druckenmiller — 30% returns compounded over 30 years. Was that a fluke, a quirk of genius, or an otherwise unapproachable result? No.Besides the huge improbability of such a lengthy run via random chance, there is the fact thatDruckenmiller and colleagues come from an “intellectual village” similar in spirit to Buffett’s —one that I call “The Supertraders of Global Macroville.”In other words: Just as a class of value investors has managed to thrive and outperform over decadesusing the tenets of Graham and Dodd, a class of traders — the Supertraders of Global Macroville —has done the same thing using the essential principles as laid down by top practitioners over theyears. Consider the following: Druckenmiller, a global macro specialist (and the architect of Soros’ career-defining BritishPounds trade in 1992), earned 30% returns over 30 years with no losing years. Paul Tudor Jones — the “Michael Jordan” of trading — has compounded at 27.4% annually inhis Tudor Futures Fund since 1984 — more than a quarter century — and, like Druckenmiller, with no losing years. PTJ and Druckenmiller were known to talk virtually every day when Druckenmiller wasactive. (Perhaps they still do…?) Druckenmiller was a protege of George Soros, whose legendary Quantum Fundcompounded at 32%+ between 1969 and 2000 (30+ years).

When Soros published the Alchemy of Finance, Paul Tudor Jones was so enthused by itsinsights he demanded that all his people read it. The habits and philosophies of Druckenmiller, Jones, Bacon, Kovner, Marcus, and other macro trading legends all have traceable links to Commodities Corp, arguably making “Global Macroville” a physical place.The essentials of the macro trading style can be traced even further back, to the timelesstenets first expressed via Reminiscences of a Stock Operator in 1923That sounds very much like an intellectual community founded on replicable strategies andprinciples, does it not? (Which, of course, is exactly what it is.)And of course, opportunities in the global macro or “top down” investing space remain as lucrative today as ever (if not more so), the basic elements of which are laid out in our Integrated MacroAnalysis series. (More episodes are coming by the way — stay tuned!)What’s more, one of the most attractive aspects of global macro — that space in which one treats theintegrated combination of “top down,” “bottom up” and “price action” as Father, Son and Holy Ghost —is its relative imperviousness to supercomputers, High Freqency Trading programs, and otherforms of short-term automated churn.No computer program yet devised can match wits with a skilled and nuanced trader when it comes to isolating, targeting and exploiting the key thematic drivers of the day. In pulling all the threads together,and applying the accumulated lessons of market history and economic knowledge as one does so,there is simply too much embedded complexity for any silicon-based algorithm to handle.As Reminiscences quite correctly observed so long ago,There are men whose gait is far quicker than the mob’s. They are bound to lead—no matter how much the mob changes. Lesson #3: EXCELLENCE TAKES HARD WORK For years, Druckenmiller had lamented that he couldn’t get away — the markets demanded too muchof his time, energy and vigilance. At age 57, and after 30 years, he finally felt ready

to slow down thepace.To stay on top of your trading game, you have to be aggressively in the mix. In some respect, being a top-flight trader is not unlike being a top athlete — golfer, tennis player, NBA star or what have you.To get great and stay great, one must put in the hours, stick with the training, and maintain a ferociouscompetitive focus. There are simply no shortcuts (with the possible exception of having other greattraders share their trades with you in real time).Paul Tudor Jones expressed the core of the trader’s work ethic in this year 2000 interview excerpt:Q: What’s your competitive advantage as a trader? A: The secret to being successful from a trading perspective is to have anindefatigable and an undying and unquenchable thirst for information andknowledge. Because I think there are certain situations where you canabsolutely understand what motivates every buyer and seller and have a pretty good picture of what’s going to happen. And it just requires anenormous amount of grunt work and dedication to finding all possible bits ofinformation. So the #3 lesson from Druckenmiller (and friends) is that it takes a lot of effort to be great (on top ofthat special spark). This in turn reflects on the fact that, to truly do well in markets, one has to trulylove the game.When it comes to trading and investing, those who do not love the game are at a distinct andpermanent disadvantage to those who do.For the individual without passion — or with insufficient passion — trading is hard and grueling workfor which the upside does not outweigh the downside.For the individual who loves all aspects of trading, on the other hand, it becomes the most fascinatingand fulfilling line of work imaginable. Intensity of engagement makes the yoke easy and theburden light. (That is one of the many edges that we as Mercenaries bring to the table. Though Mike McD and I routinely put in ten hour trading days, day in and day out, the vast majority of them feel like play.Sometimes it feels almost criminal…)Trading as one’s prime vocation is unquestionably one of the greatest gigs on the planet. For a certainodd breed, there is nothing better than stepping up and solving the puzzle each day.But sometimes it’s hard — damn hard — in the way that being an ironman triathlete can be hard. The bone-deep level of commitment required can seem nutty for those on the outside looking in.An elevated threshold for psychological pain and discomfort also counts as a “must-have.” You needthe love to overcome the friction, and the joy to overcome the pain. Druckenmiller had it for 30years straight, and then he finally got tired. (Or rather, the tiredness finally got him.)Note again too, Druckenmiller didn’t say he’s retiring completely, but only from public money, withplans to still run a chunk that will be “fun.” The pilot light remains lit.And that leads us to the final (perhaps surprising) lesson: The money doesn’t really matter. Not once you’ve gotten past the thrill at least. (“Woohoo, I’m rich! Wait a minute. Now what?”) Lesson #4: THE MONEY DOESN’T MATTER If you possess the requisite drive, temperament, and talent — and admittedly very few do — trading is unquestionably a viable path to getting rich. As Jack Schwager noted in Market Wizards.Trading provides one of the last great frontiers of opportunity in our economy. It is one of the very few ways in which an individual can start with a relatively small bankroll and actually become a multi-millionaire.Yes, but…But at the end of the day, what matters most is quality of life and overall personal fulfillment, notdollars accumulated, Ferraris parked in the climate-controlled garage, or fleeting accolades achieved.Sic transit gloria, remember? This is partly because the pursuit of monetary wealth, in and of itself, is largely a trick and a trap.Those individuals who pursue money for its own sake are almost invariably chasing some demon, or feeding some insecurity otherwise masking itself as ambition.And in terms of personal stature, no matter how much money you have, someone else will always have

more. If you delude yourself into thinking you’re the richest guy around, that’s just a failure to look around.More importantly, one can be “rich” in plenty of ways above and beyond money. To benchmark one’s sense of self against a bank account balance — equating self worth to net worth — is an invitation toshallow misery.You get the idea… bottom line being, it’s not about the money — no matter how many zeroes are tacked on to your net worth. Besides, as one less-rich-than-before Wall Streeter told the New Yorkerafter the 2008 meltdown: “Once you get above $30 million or so, it’s all philanthropy anyway.”So why did Druckenmiller play the game for 30 years straight, piling up treasure he will likely neverspend (or just wind up giving away)?Most likely for a reason we have already touched on, and the same reason a great athlete fights offretirement until age forces the issue: For the sheer love of the game.Doing what you love, and doing it every day, is a key ingredient in the secret recipe for a blessed andfulfilled life.We’ll close with a bit of wisdom from Zen And The Art of Motorcycle Maintenance:To live only for some future goal is shallow. It’s the sides of the mountain which sustain life, not the top. Here’s where things grow. But of course, without the top you can’t have any sides. It’sthe top that defines the sides.

Variant Perception is Critical

In a must-read book “No Bull: My life in and out of markets”, autobiography of

legendary investor Michael Steinhardt, there is a description of his investment philosophy.

“Throughout the market day, I had an open-door policy. Anyone could walk into my office

and interrupt at any time. They could discuss any investment. The immediacy of in-

formation, a trading opportunity, or a change of view on any position in the portfolio took

precedence over everything else. I might be in the middle of a serious meeting with

corporate executives or some investors when I would be unceremoniously interrupted by

a sloppily dressed, boorish sounding trader who saw a large block of stock for sale at a

compelling price. I could not restrain myself from some discussion of the opportunity, even

if my elegant guests were temporarily put on hold. Equally, if my door was open to my

colleagues, theirs was also open to me. I would often buzz the intercom box and have a

trader or analyst come in, mostly when there was a problem. I am told they usually

dreaded the call. "This stock is down three points," I would say, for example. "Why? What

are we missing?" or "What do you know that the world does not know?" If the person did

not have good answers, a discussion, sometimes heated, would ensue. I expected my

analysts to know everything-indeed, to know far more than I, who took ultimate

responsibility for all of our investments.

I spent much of my time listening to investment ideas that covered the full spectrum of

the marketplace-a range of industries about which, in many cases, I knew little. I became

a very careful listener. For me to be effective in understanding these ideas and monitoring

them over time, I constructed a system that overcame the necessity of specific knowledge

across a wide range of industries. In short, I asked the right questions by seeking the

variant perception inherent in each idea.

A summer intern reminded me years later of the advice I had given him on his first day at

work. I told him that ideally he should be able to tell me, in two minutes, four things: (1)

the idea; (2) the consensus view; (3) his variant perception; and (4) a trigger event. No

mean feat. In those instances where there was no variant perception-that is, solid growth

recommendations within consensus-I generally had no interest and would discourage

investing. Moreover, I would purposely ask provocative, action-oriented questions. If an

analyst bought a stock at 10 and it went up to 12, I would grill him or her: "Do you still

want to own this stock? Are you willing to pay 12 for it?" If there was willingness to buy it

at 12, then the stock should stay in the portfolio. If there was unwillingness to buy it at

12, then the stock might be sold.

The function of trading went beyond efficiently executing orders. It included being the eyes

and ears of the portfolio. At times, through the flow of trading information, one might

sense important fundamental change. There is great homogeneity in the community of

research analysis, but sometimes the actual buyers and sellers tell a different story. We

tried with our positions to learn what that story might be, particularly when trading activity

was at variance with our expectation. Moreover, via active trading, often trading around a

position, we achieved a feel for the market that could not be attained otherwise. We tried

to coordinate our research and trading activities to take advantage of interim price

movement. I liked to say that if we bought a stock at 20 having an objective of 30 through

trading, we would hope to make profits equivalent to the stock going to 40.

I tried to view the portfolio fresh every day. Indeed, investing toward long-term capital

gains treatment was of secondary consideration for me. Thus, there was an inevitable

conflict between my constant measuring of the portfolio and the accumulated investment

time that my analysts had in their positions and were loath to forgo. Stocks rarely go up

or down in straight lines. Often, because of the intensity of my focus, I would sense that

one of our positions was vulnerable in the short term and would be tempted to act. One

of my favorite expressions was "the quick and the dead," meaning that if you did not

respond fast enough to the newest change, even nuance, you might lose. The analyst,

having spent tens of hours becoming intimate with the company, might resent my

tampering with his or her position. I always felt that if an analyst could not strongly defend

an investment, it should not be in our portfolio. I wanted my analysts to have strong

convictions. Otherwise, their investments should not be held in the portfolio, particularly

when there seemed to be short term vulnerability

Quotes from the gods of investing It's not always easy to do what's not popular, but that's where you make your money. Buy stocks

that look bad to less careful investors and hang on until their real value is recognized."

"I've never bought a stock unless, in my view, it was on sale."

"Successful stocks don't tell you when to sell. When you feel like bragging, it's probably time to sell."

Rule No.1 is never lose money. Rule No.2 is never forget rule number one."

"Shares are not mere pieces of paper. They represent part ownership of a business. So, when

contemplating an investment, think like a prospective owner."

"All there is to investing is picking good stocks at good times and staying with them as long as they

remain good companies."

"Look at market fluctuations as your friend rather than your enemy. Profit from folly rather than

participate in it."

"If, when making a stock investment, you're not considering holding it at least ten years, don't waste

more than ten minutes considering it."

"Psychology is probably the most important factor in the market – and one that is least understood."

"I paraphrase Lord Rothschild: ‘The time to buy is when there's blood on the streets.'"

"One of the big problems with growth investing is that we can't estimate earnings very well. I really

want to buy growth at value prices. I always look at trailing earnings when I judge stocks."

"If you have good stocks and you really know them, you'll make money if you're patient over three

years or more."

"I don't want a lot of good investments; I want a few outstanding ones."

"To achieve satisfactory investment results is easier than most people realize; to achieve superior

results is harder than it looks."

" Most of the time stocks are subject to irrational and excessive price fluctuations in both directions

as the consequence of the ingrained tendency of most people to speculate or gamble … to give way

to hope, fear and greed."

"Even the intelligent investor is likely to need considerable willpower to keep from following the

crowd."

"It is absurd to think that the general public can ever make money out of market forecasts."

Profits always take care of themselves but losses never do."

"The average man doesn't wish to be told that it is a bull or a bear market. What he desires is to be

told specifically which particular stock to buy or sell. He wants to get something for nothing. He does

not wish to work. He doesn't even wish to have to think."

"Go for a business that any idiot can run – because sooner or later, any idiot is probably going to run

it."

"If you stay half-alert, you can pick the spectacular performers right from your place of business or

out of the neighborhood shopping mall, and long before Wall Street discovers them."

"Investing without research is like playing stud poker and never looking at the cards."

"Absent a lot of surprises, stocks are relatively predictable over twenty years. As to whether they're

going to be higher or lower in two to three years, you might as well flip a coin to decide."

"If you spend more than 13 minutes analyzing economic and market forecasts, you've wasted 10

minutes."

Value investing means really asking what are the best values, and not assuming that because

something looks expensive that it is, or assuming that because a stock is down in price and trades at

low multiples that it is a bargain … Sometimes growth is cheap and value expensive. . . . The question

is not growth or value, but where is the best value … We construct portfolios by using ‘factor

diversification.' . . . We own a mix of companies whose fundamental valuation factors differ. We

have high P/E and low P/E, high price-to-book and low-price-to-book. Most investors tend to be

relatively undiversified with respect to these valuation factors, with traditional value investors

clustered in low valuations, and growth investors in high valuations … It was in the mid-1990s that

we began to create portfolios that had greater factor diversification, which became our strength

…We own low PE and we own high PE, but we own them for the same reason: we think they are

mispriced. We differ from many value investors in being willing to analyze stocks that look expensive

to see if they really are. Most, in fact, are, but some are not. To the extent we get that right, we will

benefit shareholders and clients.

"I often remind our analysts that 100% of the information you have about a company represents the

past, and 100% of a stock's valuation depends on the future."

"The market does reflect the available information, as the professors tell us. But just as the funhouse

mirrors don't always accurately reflect your weight, the markets don't always accurately reflect that

information. Usually they are too pessimistic when it's bad, and too optimistic when it's good."

"What we try to do is take advantage of errors others make, usually because they are too short-term

oriented, or they react to dramatic events, or they overestimate the impact of events, and so on."

"It's not whether you're right or wrong that's important, but how much money you make when

you're right and how much you lose when you're wrong."

"Invest at the point of maximum pessimism."

I have put these philosophies into a simple statement: Help people. When people are

desperately trying to sell, help them and buy. When people are

enthusiastically trying to buy, help them and sell.

"If you want to have a better performance than the crowd, you must do things differently from the

crowd."

"When asked about living and working in the Bahamas during his management of the Templeton

Group, Templeton replied, "I've found my results for investment clients were far better here than

when I had my office in 30 Rockefeller Plaza. When you're in Manhattan, it's much more difficult to

go opposite the crowd."