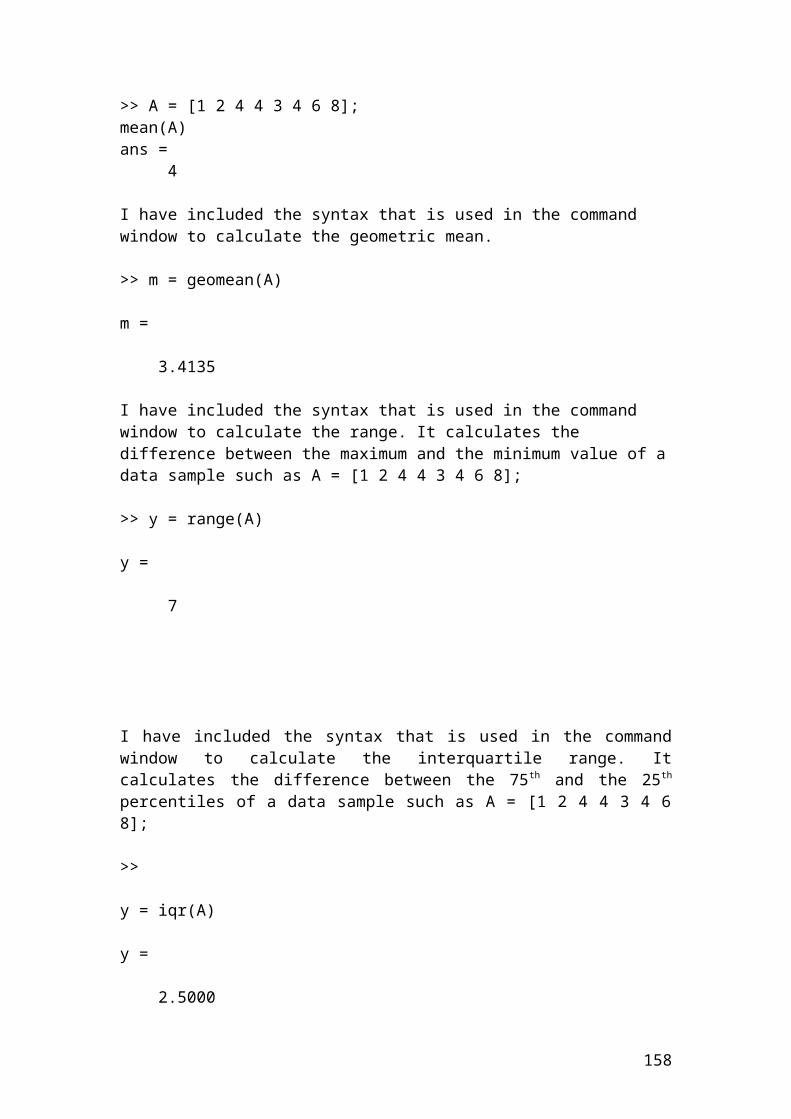

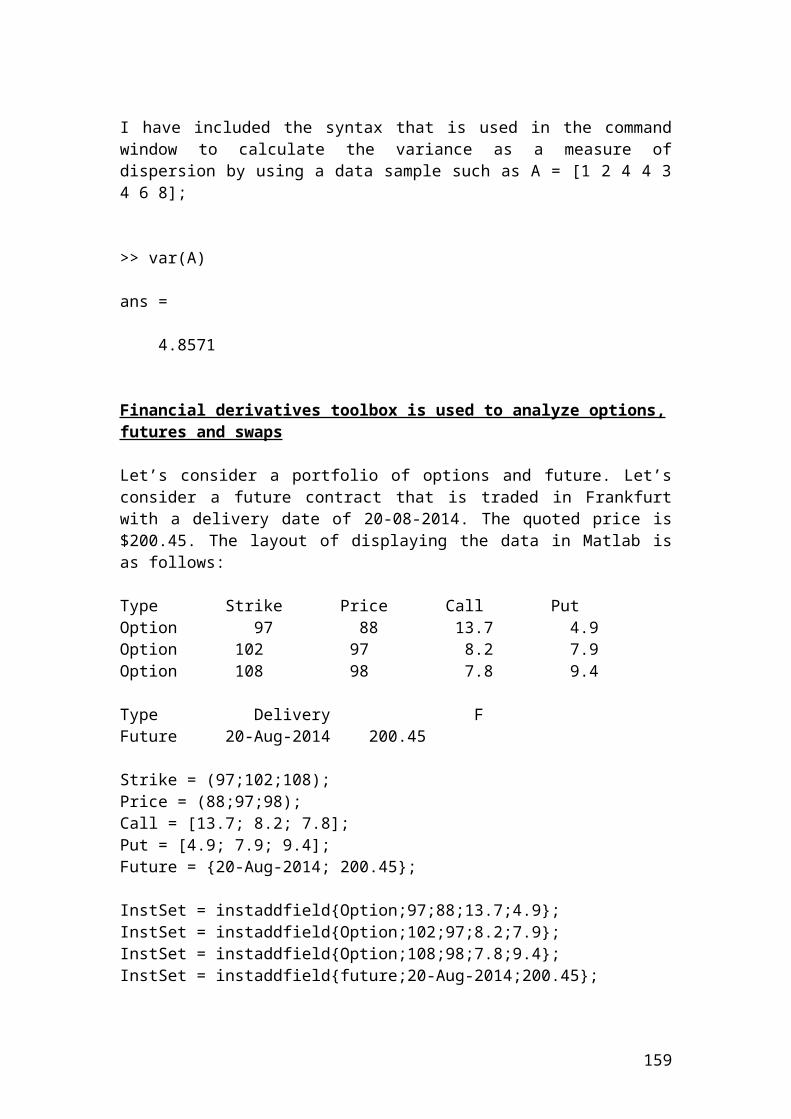

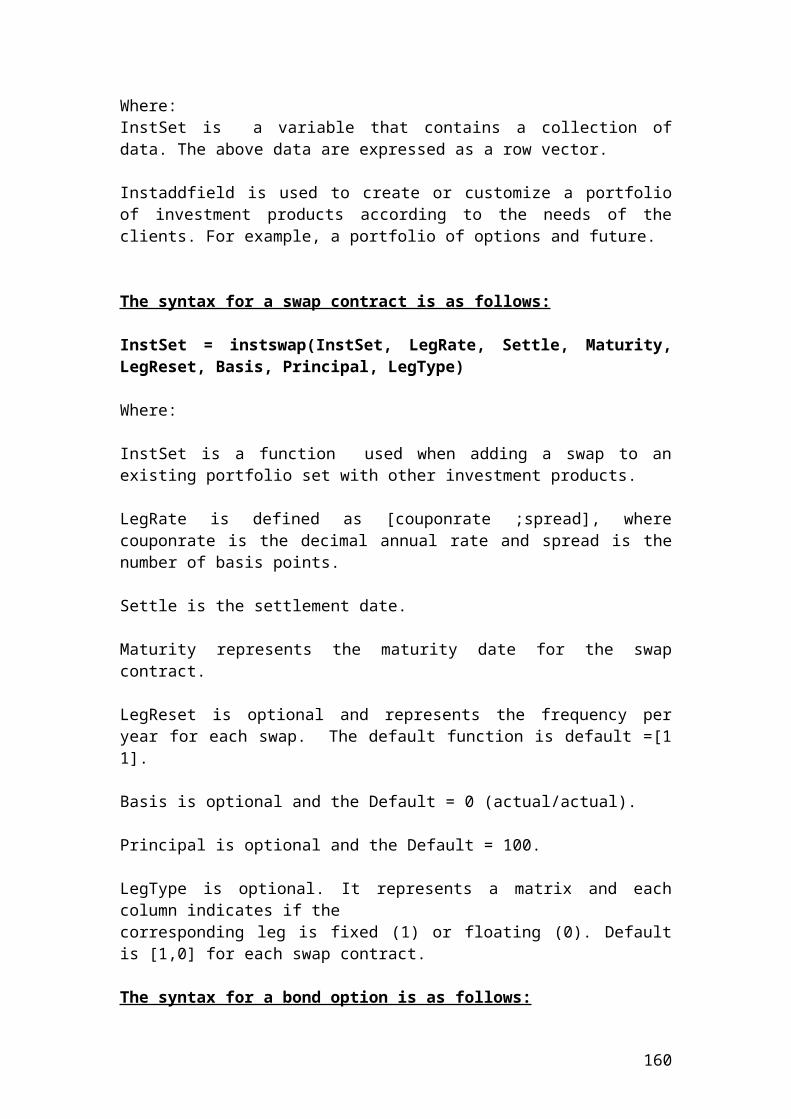

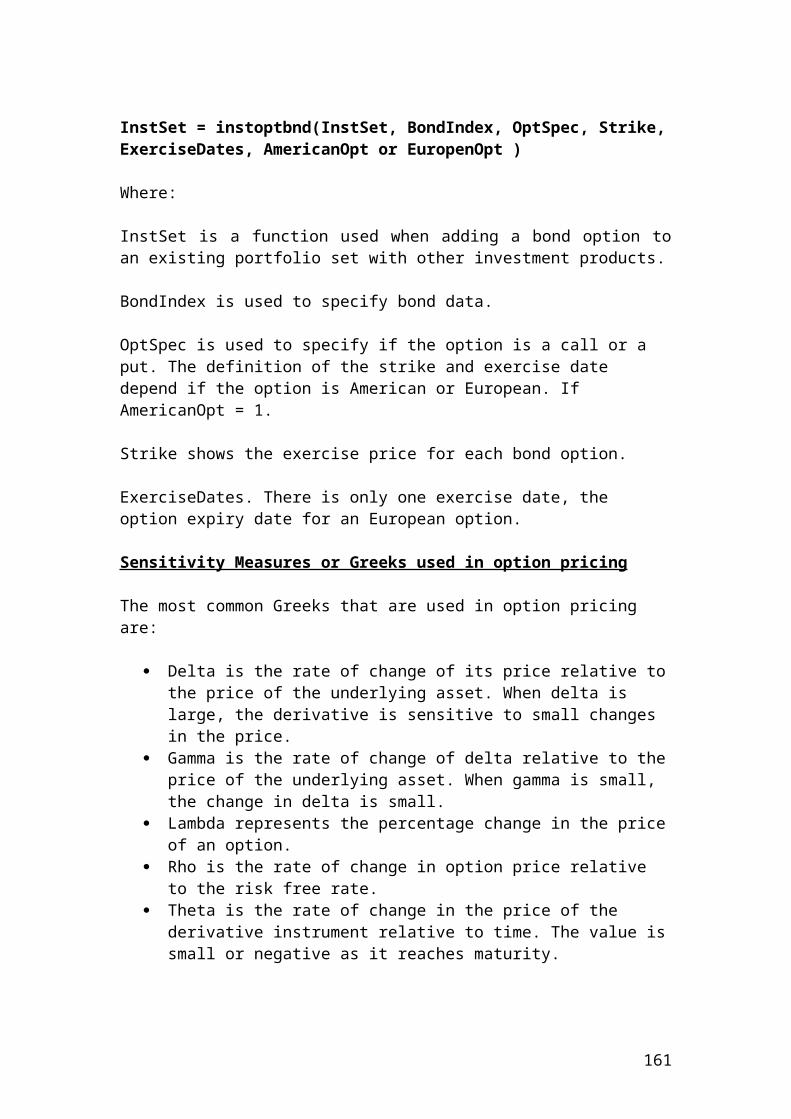

Fixed - income investments 2

425

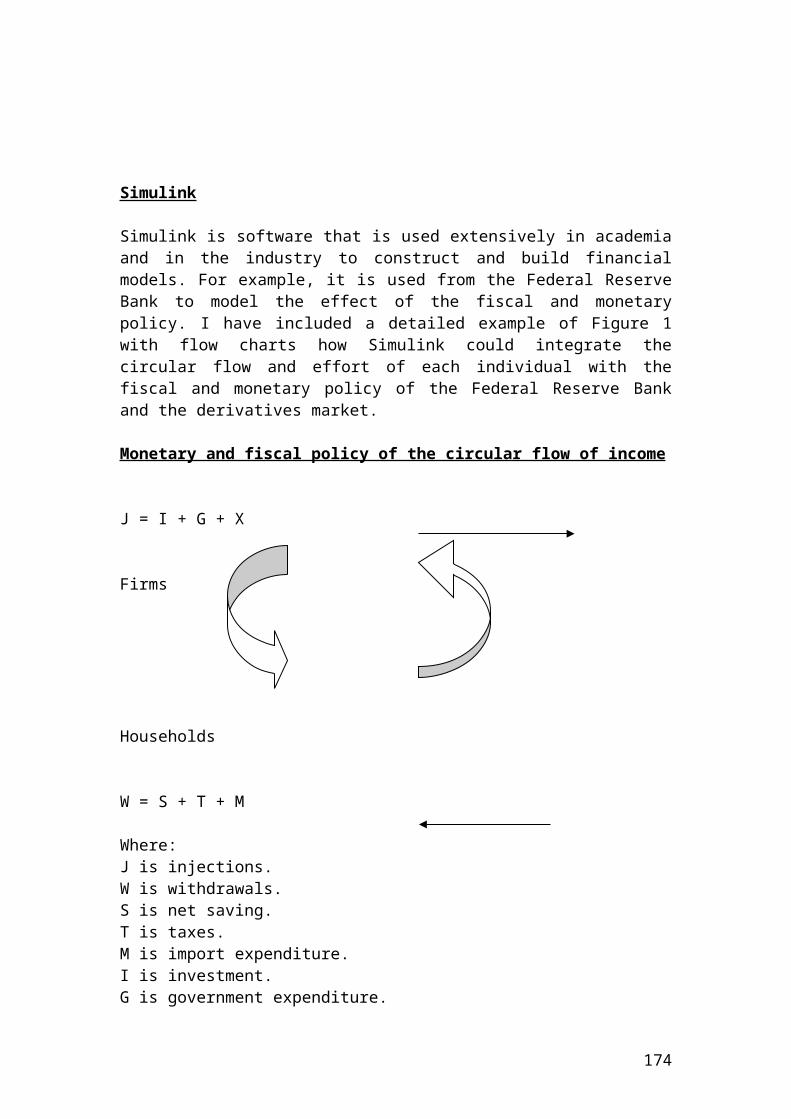

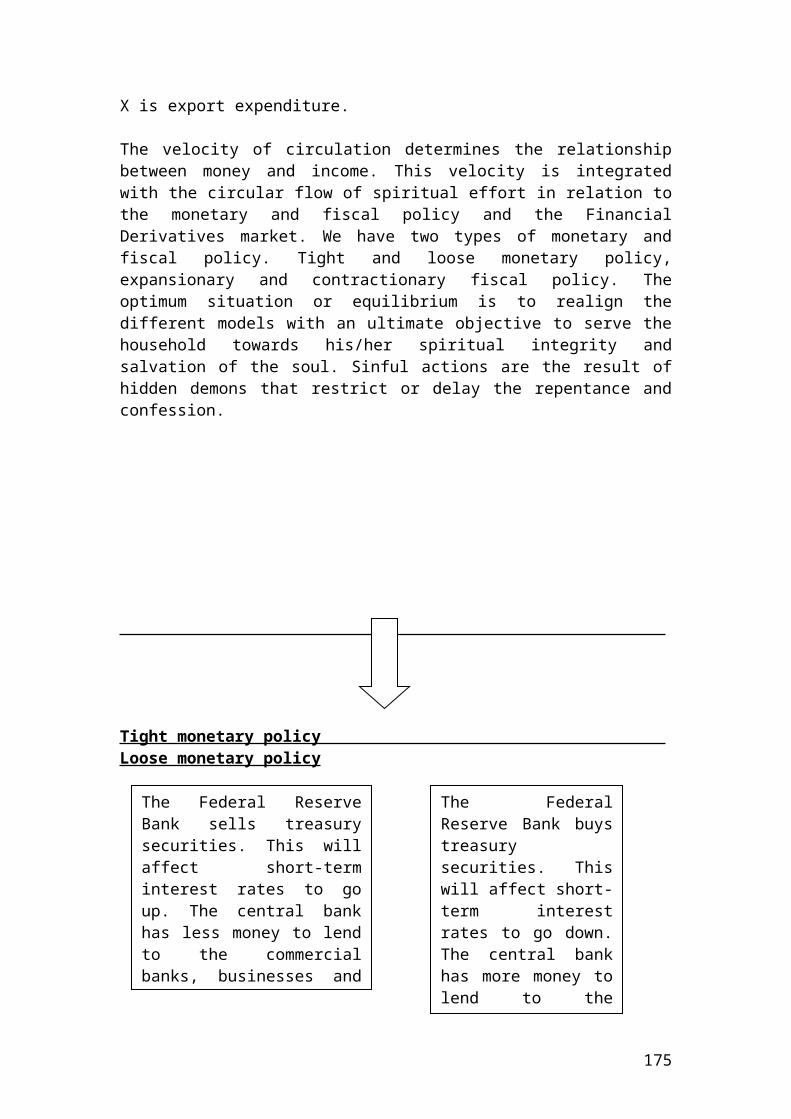

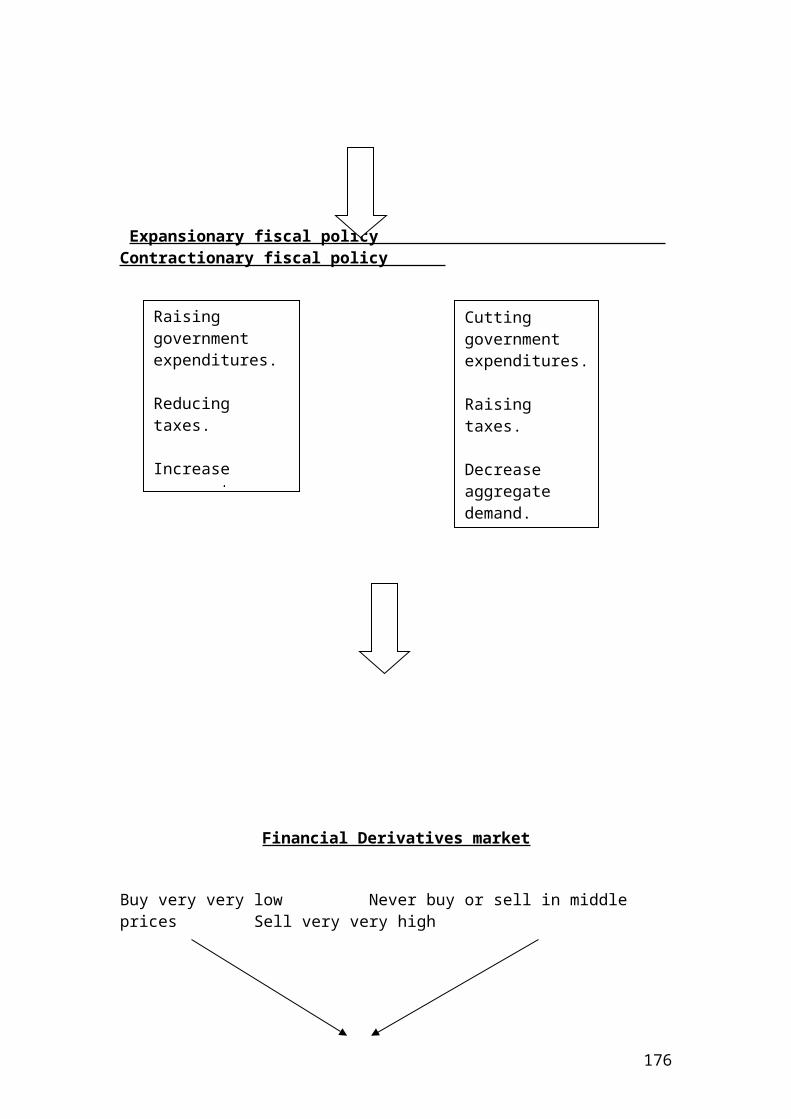

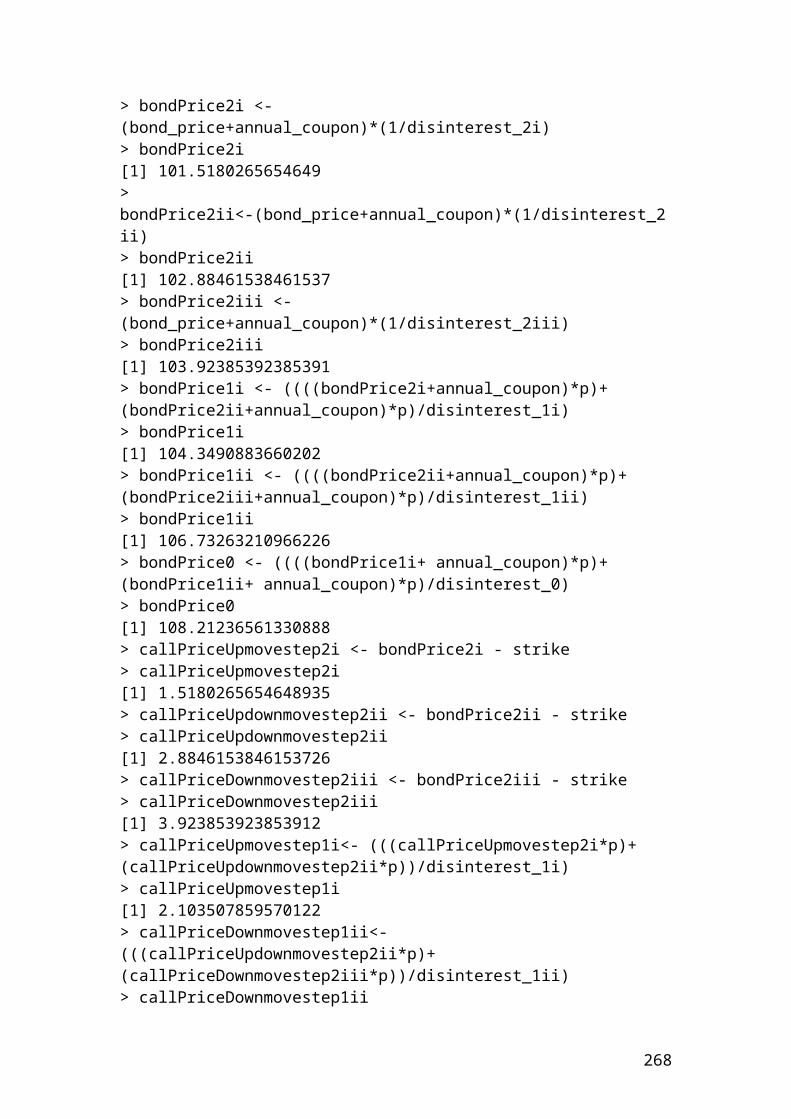

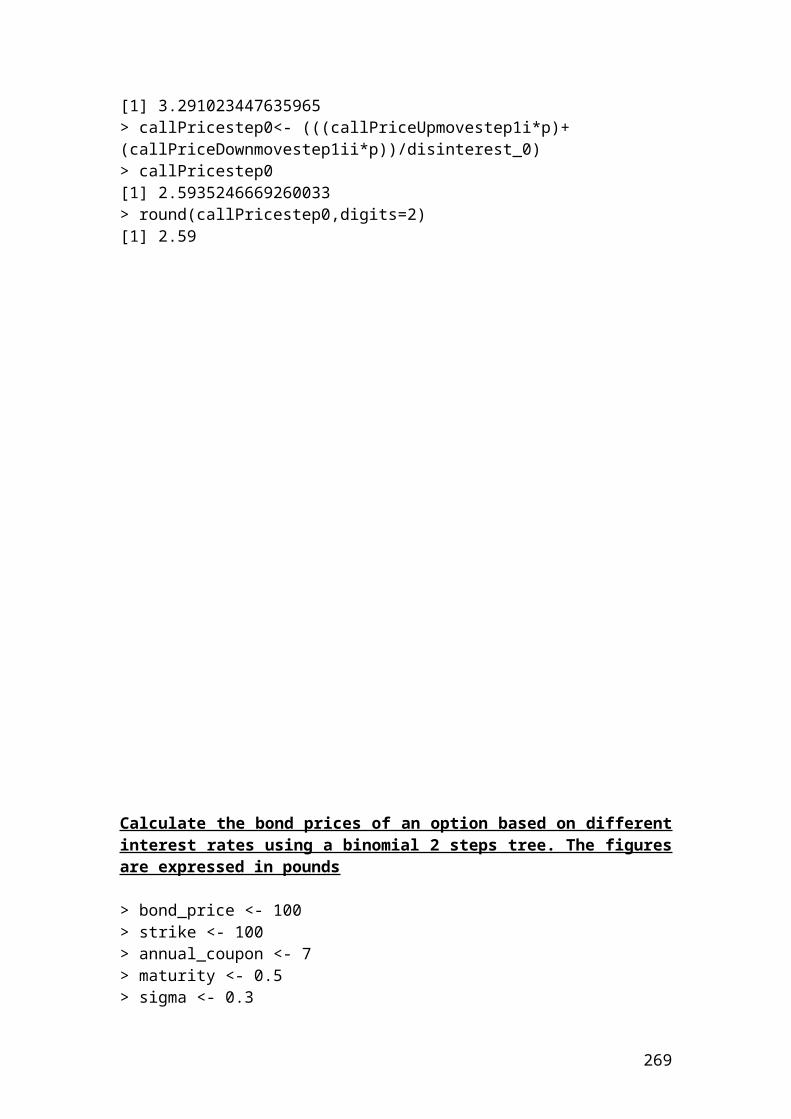

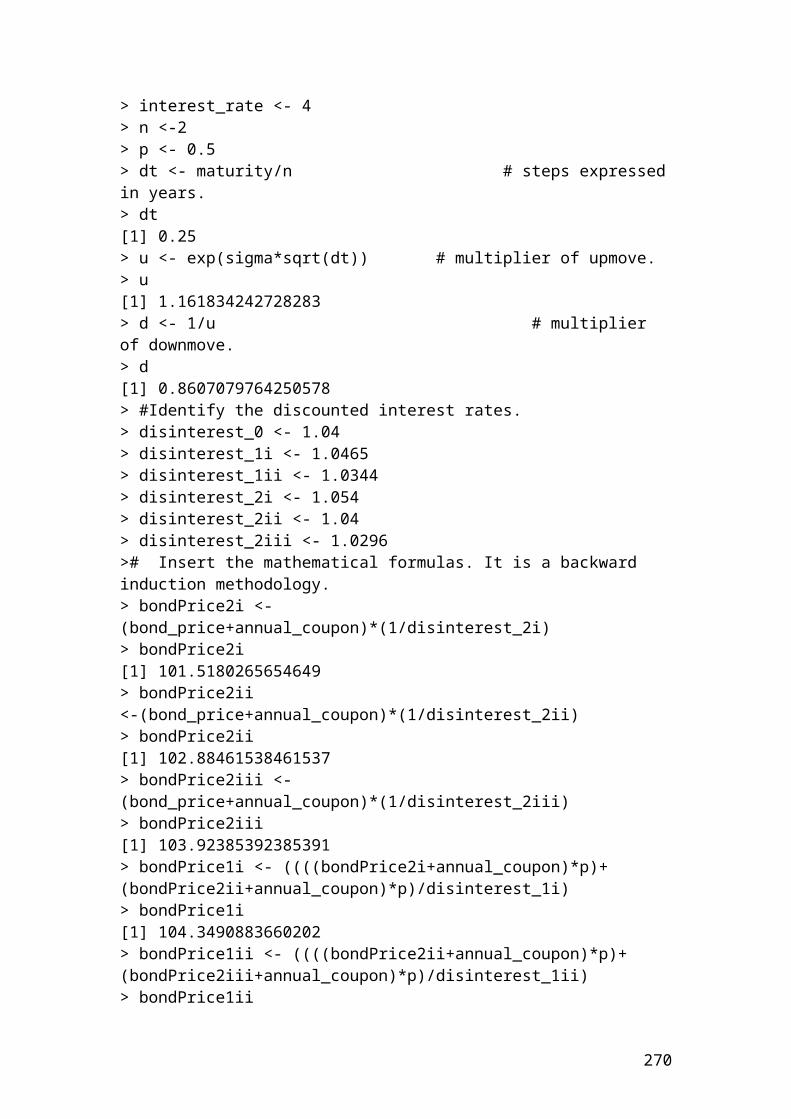

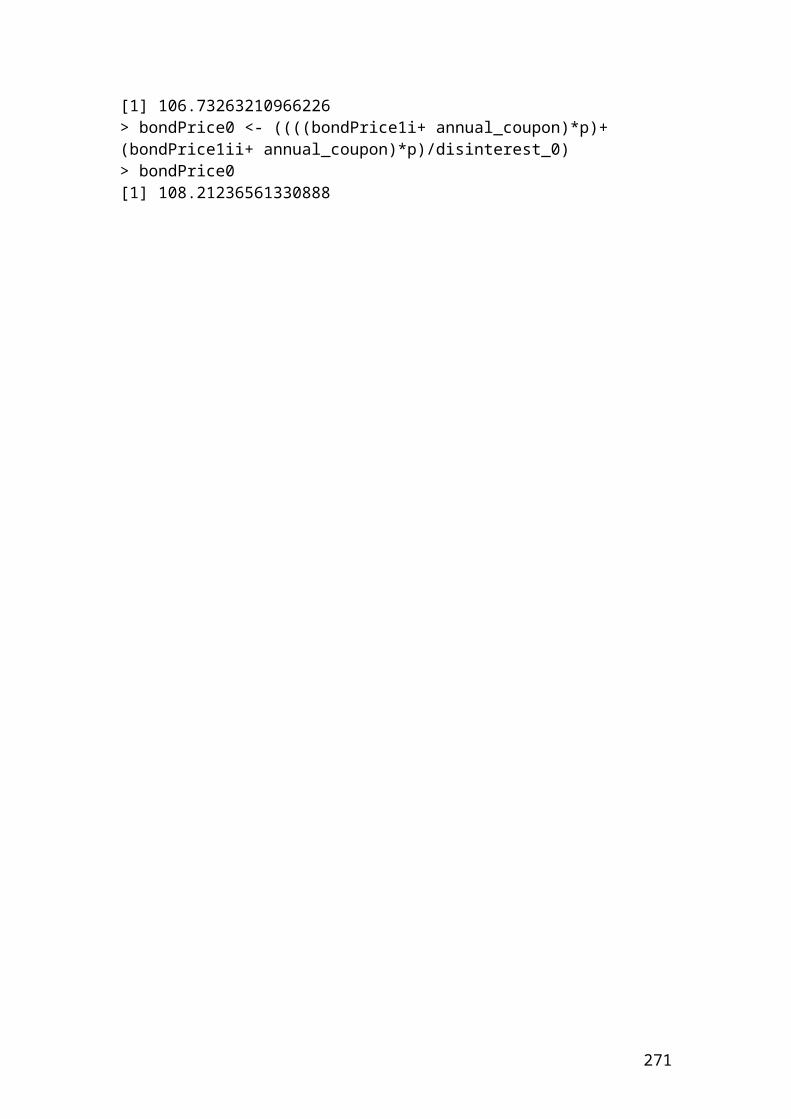

Workshop of structured query language in terms of SQL Both databases are servers that you construct and you can import the data in Excel in terms of pivot table, pivot chart and spreadsheet. To import the data, select data and, then, select import external data and then new SQL server connection or connect to new data source in case of Oracle database. Press open, then, write the name of the server, then, click on the user name and password and input the login and password. Thus, the whole procedure in Excel takes place in the data connection wizard. In addition, you can use the Query wizard to form a SQL query. In this case, you select data, and then import external data. Then, you form new query data. You have the options to choose columns, to filter data, and to sort or order the data in ascending or descending order. Then, by pressing import, you select existing data or data from a new worksheet. In the Query wizard, you have the option to apply multiple filters to sort your data in addition to string operators. It is a function that links Excel reports to SQL query. For example, we create an Excel file with futures contracts for different individuals and companies with monthly, annual returns and profit and loss position. Then, we export this file through new SQL server connection to form and filter different queries in order to form management reports. We then return the data to Excel reports by limiting or extracting the transactions that took place in the futures contract the last 6 months. String operators are used in terms of equals, does not equal, is greater then, is greater than or equal to, is lee than, is less than or equal to. These strings are used as filter value in the drop – down field. These, reports facilitate the derivatives portfolio management. Another example is JP Morgan investment bank that keeps data warehouses of client and company accounts and their related balance. Information related to portfolio management is used as a business intelligence tool in the Query wizard. The Query wizard is a very useful and intermediary tool between Excel and a database for applicants with limited SQL knowledge, as it provides a selection of existing 1

-

Upload

dr-michel-zaki-guirguis -

Category

Documents

-

view

72 -

download

0

Transcript of Fixed - income investments 2

Workshop of structured query language in terms of SQL

Both databases are servers that you construct and you can import the data in Excel in terms of pivot table, pivot chart and spreadsheet. To import the data, select data and, then, select import external data and then new SQL server connection or connect to new data source in case of Oracle database. Press open, then, write the name of the server, then, click on the user name and password and input the login and password. Thus, the whole procedure in Excel takes place in the data connection wizard. In addition, you can use the Query wizard to form a SQL query. In this case, you select data, and then import external data. Then, you form new query data. You have the options to choose columns, to filter data, and to sort or order the data in ascending or descending order. Then, by pressing import, you select existing data or data from a new worksheet. In the Query wizard, you have the option to apply multiple filters to sort your data in addition to string operators. It is a function that links Excel reports to SQL query. For example, we create an Excel file with futures contracts for different individuals and companies with monthly, annual returns and profit and loss position. Then, we export this file through new SQL server connection to form and filter different queries in order to form management reports. We then return the data to Excel reports by limiting or extracting the transactions that took place in the futures contract the last 6 months. String operators are used in terms of equals, does not equal, is greater then, is greater than or equal to, is lee than, is less than or equal to. These strings are used as filter value in the drop – down field. These, reports facilitate the derivatives portfolio management. Another example is JP Morgan investment bank that keeps data warehouses of client and company accounts and their related balance. Information related to portfolio management is used as a business intelligence tool in the Query wizard. The Query wizard is a very useful and intermediary tool between Excel and a database for applicants with limited SQL knowledge, as it provides a selection of existing database tables, views, formula creations, and applications of filter conditions.

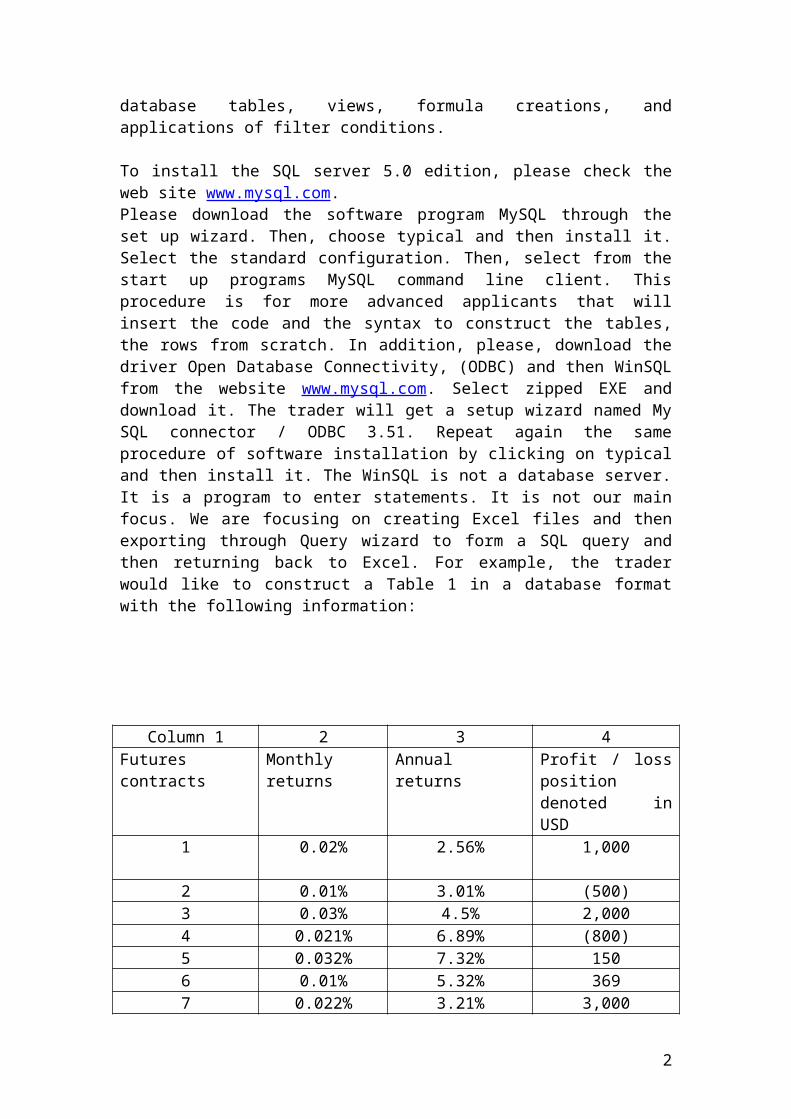

To install the SQL server 5.0 edition, please check the web site www.mysql.com.Please download the software program MySQL through the set up wizard. Then, choose typical and then install it. Select the standard configuration. Then, select from the start up programs MySQL command line client. This procedure is for more advanced applicants that will insert the code and the syntax to construct the tables, the rows from scratch. In addition, please, download the driver Open Database Connectivity, (ODBC) and then WinSQL from the website www.mysql.com. Select zipped EXE and download it. The trader will get a setup wizard named My SQL connector / ODBC 3.51. Repeat again the same procedure of software installation by clicking on typical and then install it. The WinSQL is not a database server. It is a program to enter statements. It is not our main focus. We are focusing on creating Excel files and then exporting through Query wizard to form a SQL query and then returning back to Excel. For example, the trader would like to construct a Table 1 in a database format with the following information:

Column 1 2 3 4

1

Futures contracts Monthly returns Annual returns Profit / loss position denoted in USD

1 0.02% 2.56% 1,000

2 0.01% 3.01% (500)3 0.03% 4.5% 2,0004 0.021% 6.89% (800)5 0.032% 7.32% 1506 0.01% 5.32% 3697 0.022% 3.21% 3,0008 0.001% 1.45% (243)

Total functionAverage function

Source: author’s illustration

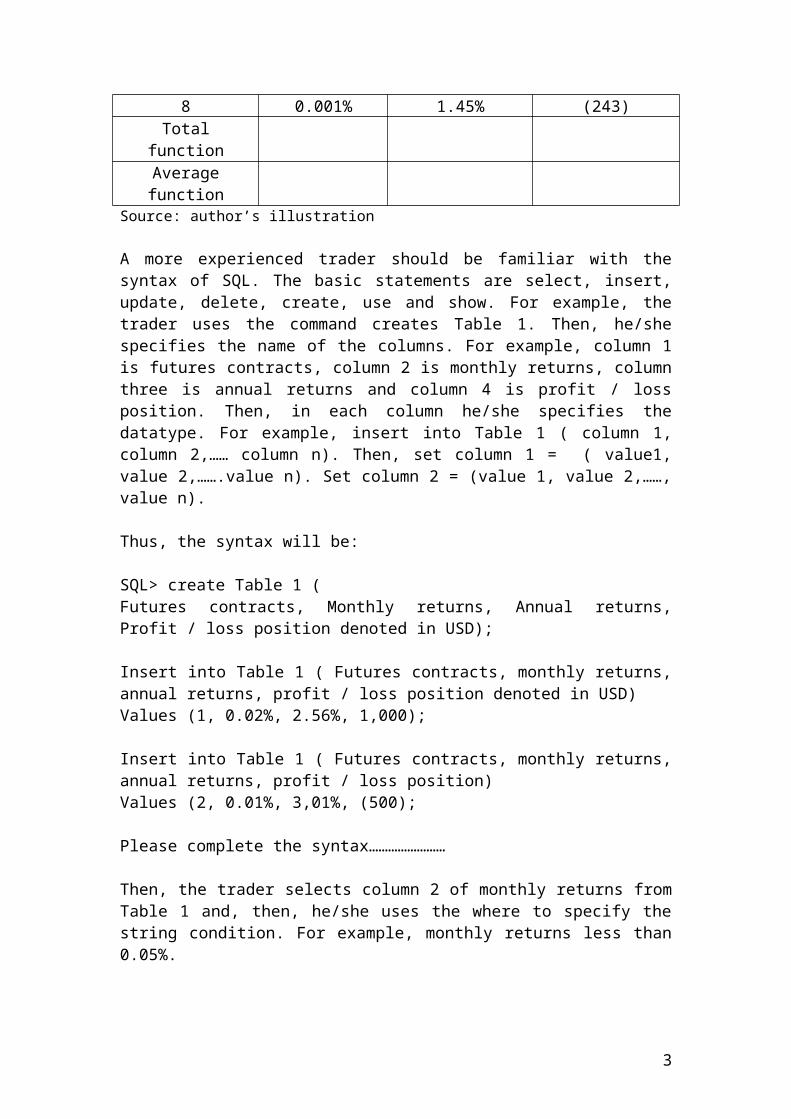

A more experienced trader should be familiar with the syntax of SQL. The basic statements are select, insert, update, delete, create, use and show. For example, the trader uses the command creates Table 1. Then, he/she specifies the name of the columns. For example, column 1 is futures contracts, column 2 is monthly returns, column three is annual returns and column 4 is profit / loss position. Then, in each column he/she specifies the datatype. For example, insert into Table 1 ( column 1, column 2,…… column n). Then, set column 1 = ( value1, value 2,…….value n). Set column 2 = (value 1, value 2,……, value n).

Thus, the syntax will be:

SQL> create Table 1 ( Futures contracts, Monthly returns, Annual returns, Profit / loss position denoted in USD);

Insert into Table 1 ( Futures contracts, monthly returns, annual returns, profit / loss position denoted in USD)Values (1, 0.02%, 2.56%, 1,000);

Insert into Table 1 ( Futures contracts, monthly returns, annual returns, profit / loss position)Values (2, 0.01%, 3,01%, (500);

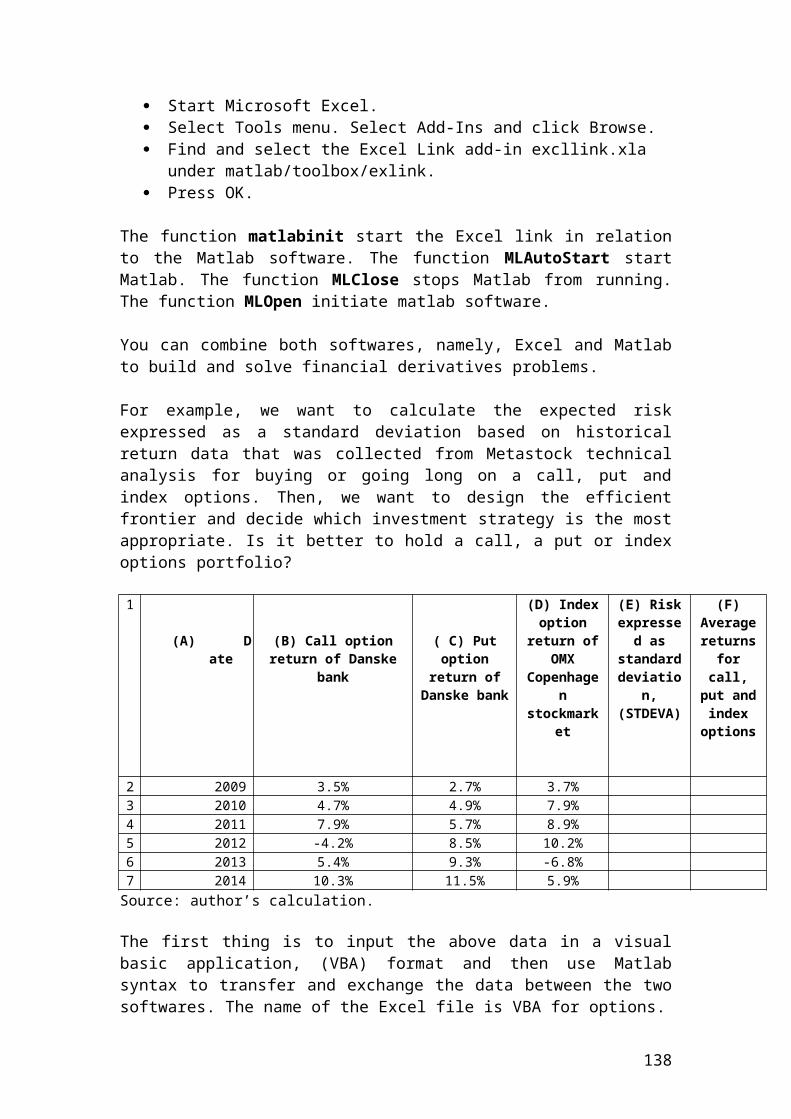

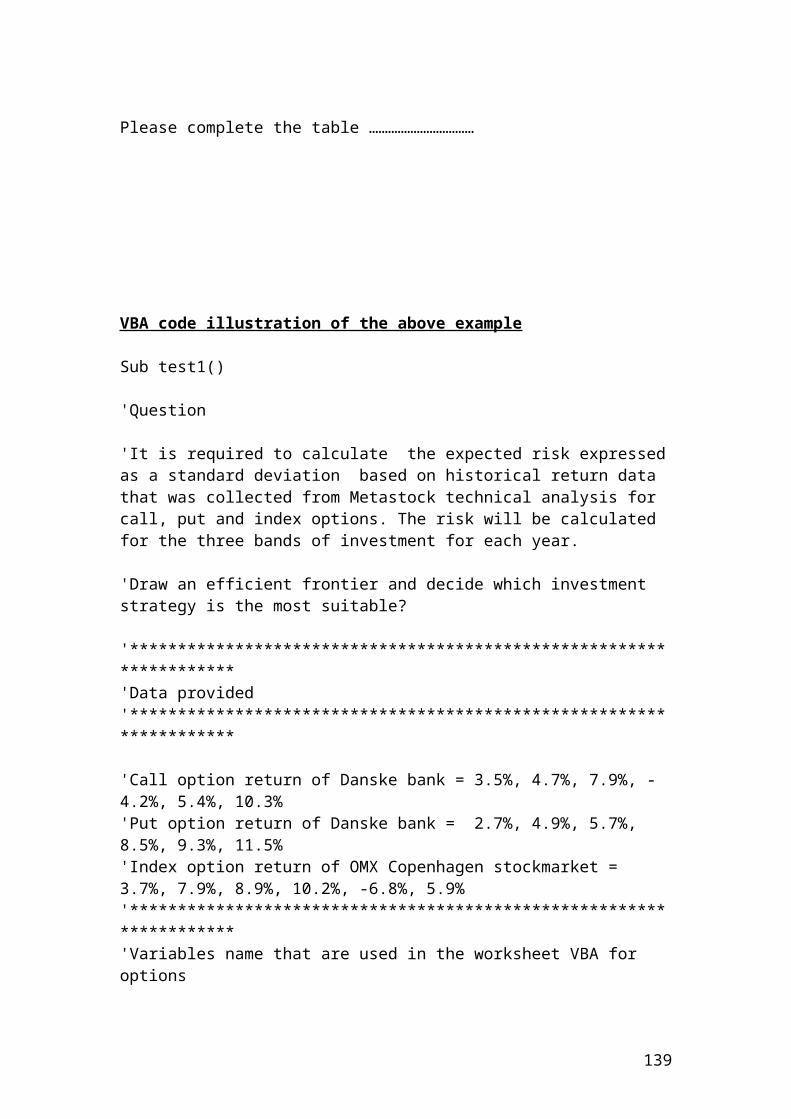

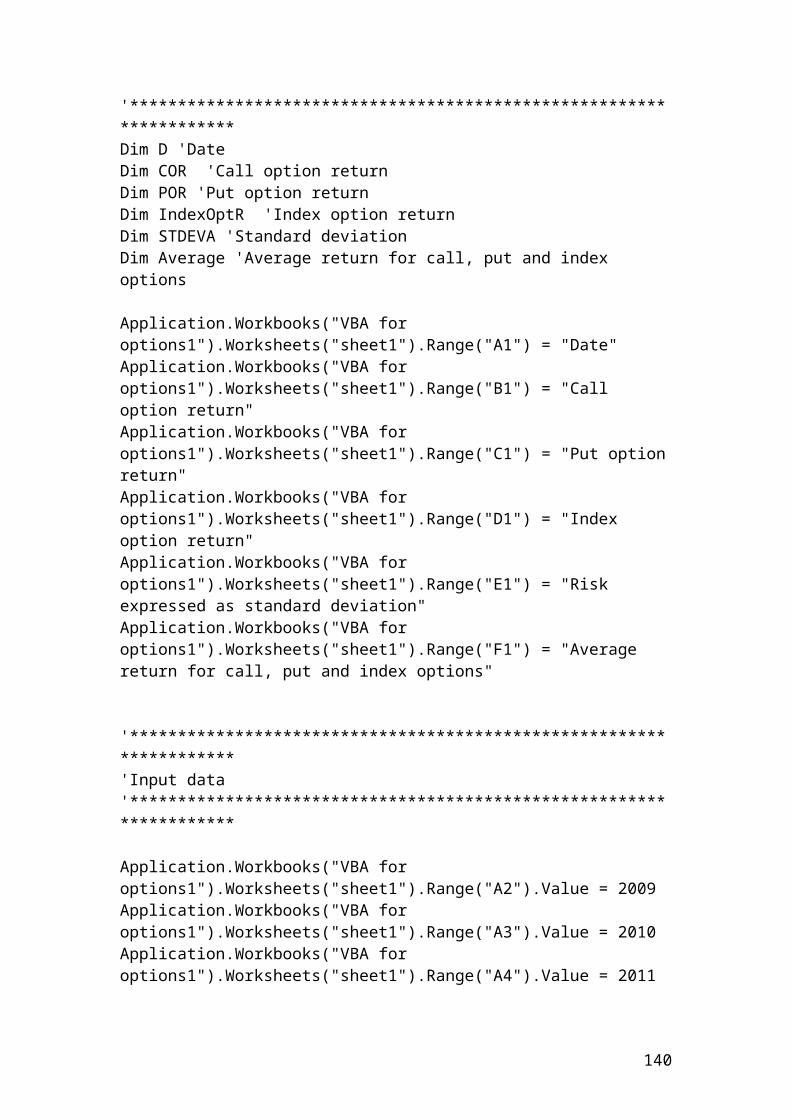

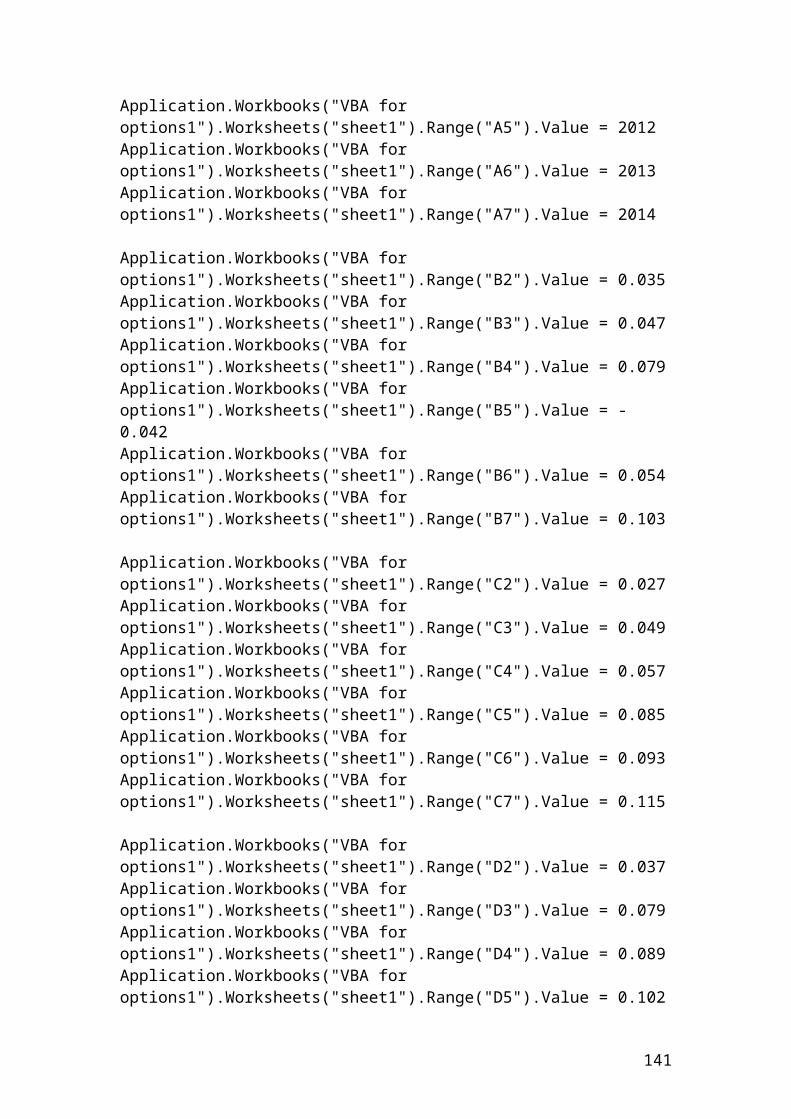

Please complete the syntax……………………

Then, the trader selects column 2 of monthly returns from Table 1 and, then, he/she uses the where to specify the string condition. For example, monthly returns less than 0.05%.

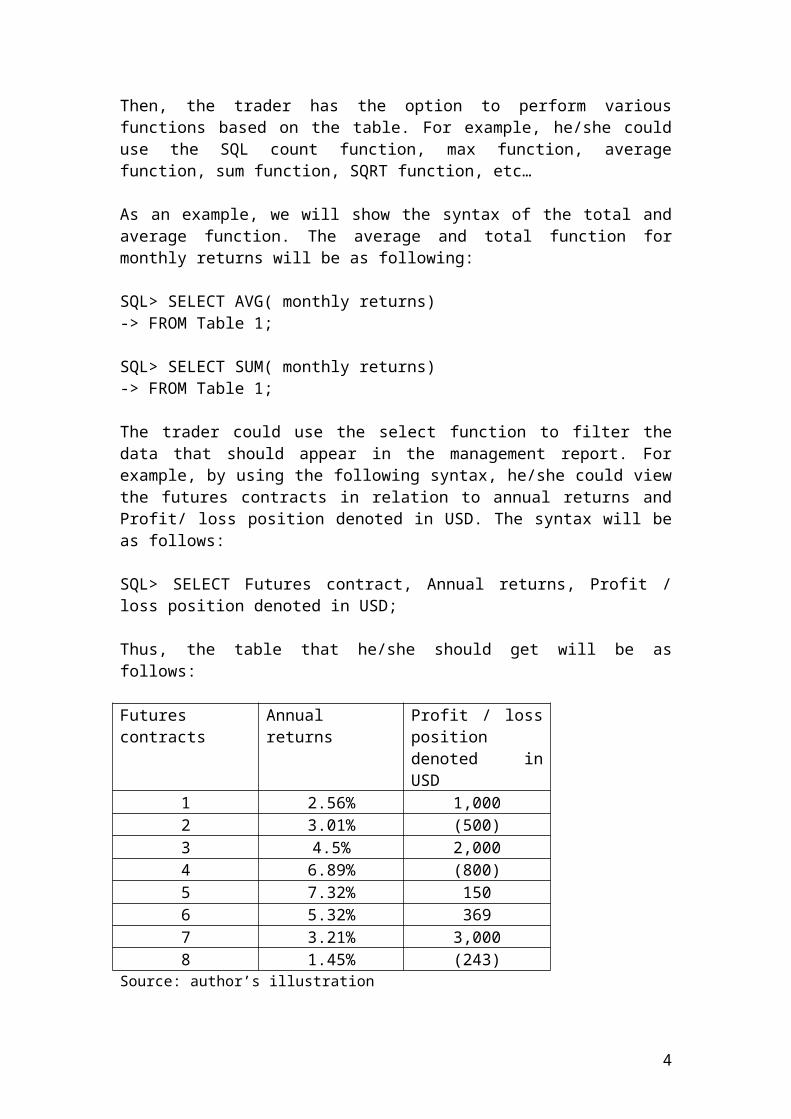

Then, the trader has the option to perform various functions based on the table. For example, he/she could use the SQL count function, max function, average function, sum function, SQRT function, etc…

As an example, we will show the syntax of the total and average function. The average and total function for monthly returns will be as following:

2

SQL> SELECT AVG( monthly returns)-> FROM Table 1;

SQL> SELECT SUM( monthly returns)-> FROM Table 1;

The trader could use the select function to filter the data that should appear in the management report. For example, by using the following syntax, he/she could view the futures contracts in relation to annual returns and Profit/ loss position denoted in USD. The syntax will be as follows:

SQL> SELECT Futures contract, Annual returns, Profit / loss position denoted in USD;

Thus, the table that he/she should get will be as follows:

Futures contracts Annual returns Profit / loss position denoted in USD

1 2.56% 1,0002 3.01% (500)3 4.5% 2,0004 6.89% (800)5 7.32% 1506 5.32% 3697 3.21% 3,0008 1.45% (243)

Source: author’s illustration

3

Workshop of language programming in terms of Python 3.4.1

Python version 3.4.1 Shell is very useful language programming for modeling financial derivatives. You can download and donate for the software by visiting the site www.python.org

The Python organization provides free download for the standard package version 3.4.1 Shell for windows or 3.5.

Python includes a math and a statistical library to import functions and perform basic calculations. Part of Python is the scientific Python package IPython. Components of IPyhton are scipy and Numpy. Scipy is used to calculate the cumulative normal distribution and generate random numbers. Numpy is used to construct array in matrix format which are used in statistics, econometrics and data analysis. We will focus on financial derivatives examples. IPython could be downloaded through the continuum analytics Anaconda website. www.continuum.io/downloads

Anaconda includes the standard Python software and the related libraries of IPython. You can download it for Windows, Linux and Macintosh. Please check for compatibility. version and memory space for fitness with your PC.

Please visit the site www.python.org and check the source code for mathematical statistics functions and the math library.

We will focus mainly on Python version 3.4.1 for doing simple calculations. We will use also the scientific Python package IPython to calculate call, put options and their related Greeks.

I have included basic examples that I have used in the Python version 3.4.1 Shell.

Variable names are written with underscore followed by the equal sign. For example,

>>> interest_rate = 0.03Variable names could also be written with small letters adjacent to each other. For example, interestrate = 0.03

It is better to use underscore to separate them and be able to read them clearly.

Another example that we can mention is if we have two variable values such as:>>> c = 5>>> d = 3>>> c+d 8>>> c*d15

4

I have included another example that shows the multiplication of two interest rates. Then, I have added to the result the second interest rate by using the function >>>interest_rate2+_. Then, I have rounded the final figure to two decimal places.

>>> interest_rate1 = 0.02>>> interest_rate2 = 0.03>>> interest_rate1*interest_rate20.0006>>> interest_rate2+_0.0306>>> round(_,2)0.03

Powers are performed by using twice the symbol**. For example, >>>3**5 243

If you would like to add comments, then, use the symbol # in front of the variable name.The operator # is used to write comments. For example,

>>>sigma = 0.5 # volatility.

Please distinguish between the integer numbers, (int), such as (1,3,4,5,7) and the fractional ones such as (2.0, 1.3) that are float.

Division is performed using the sign / to get a float result. Use the symbol // to get an integer result without fractional part. For example,>>> 7.0 / 3.0 2.33333

In contrast, >>> 7 // 3 2

Lists could be written as numbers separated by commas in brackets. As an example, please consider the following:

>>> squares = [1,2,4,5]>>> squares[1, 2, 4, 5]

Strings should be enclosed in single or double quotes.

5

For example, ‘ volatility’

Use the function range to include numbers from 1 to 10. The function is as follows:

>>> range(1,10)[1, 2, 3, 4, 5, 6, 7, 8, 9]

It is worth to mention the headings that should be included in Python version 3.4.1 Shell and IPython.

The headings are as follows:

>>>from statistics import mean, median, variance, or stdev OR

>>>from statistics import*

>>>data = [1.2,3.4]>>> mean(data)>>>2.3>>> median(data)etc…..

If you want to round then use the function round(_,2)

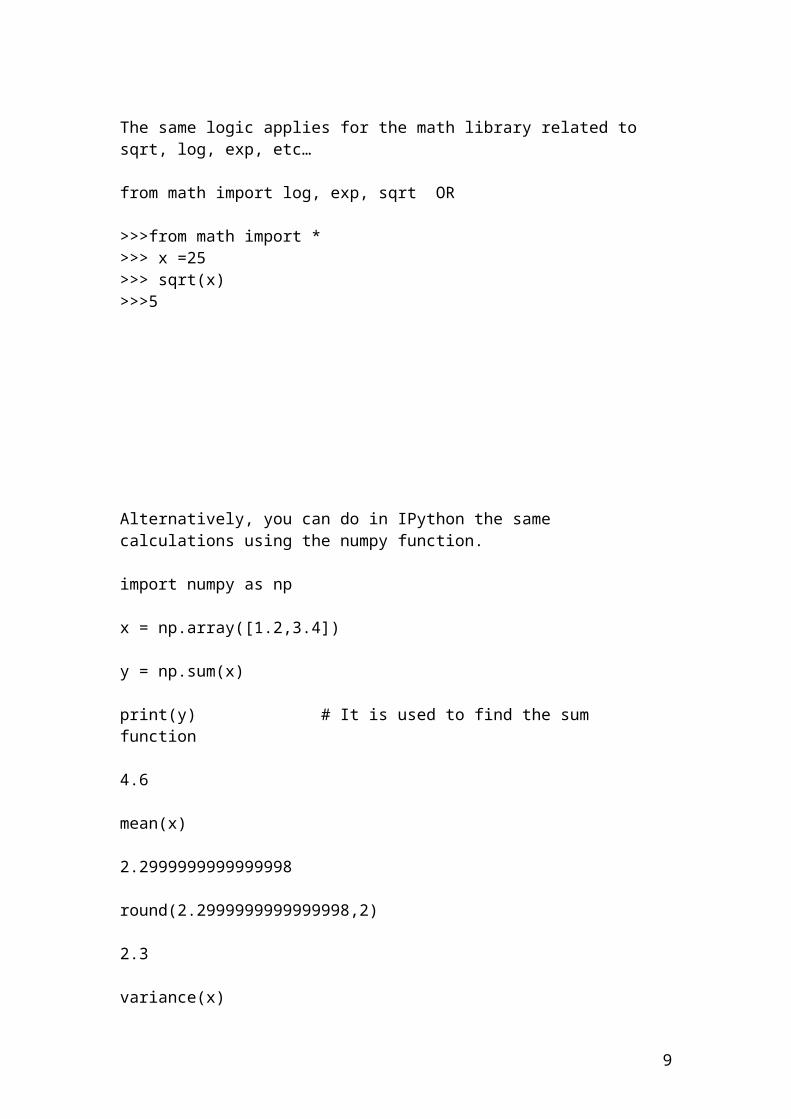

The same logic applies for the math library related to sqrt, log, exp, etc…

from math import log, exp, sqrt OR

>>>from math import *>>> x =25>>> sqrt(x)>>>5

Alternatively, you can do in IPython the same calculations using the numpy function.

import numpy as np

x = np.array([1.2,3.4])

y = np.sum(x)

6

print(y) # It is used to find the sum function

4.6

mean(x)

2.2999999999999998

round(2.2999999999999998,2)

2.3

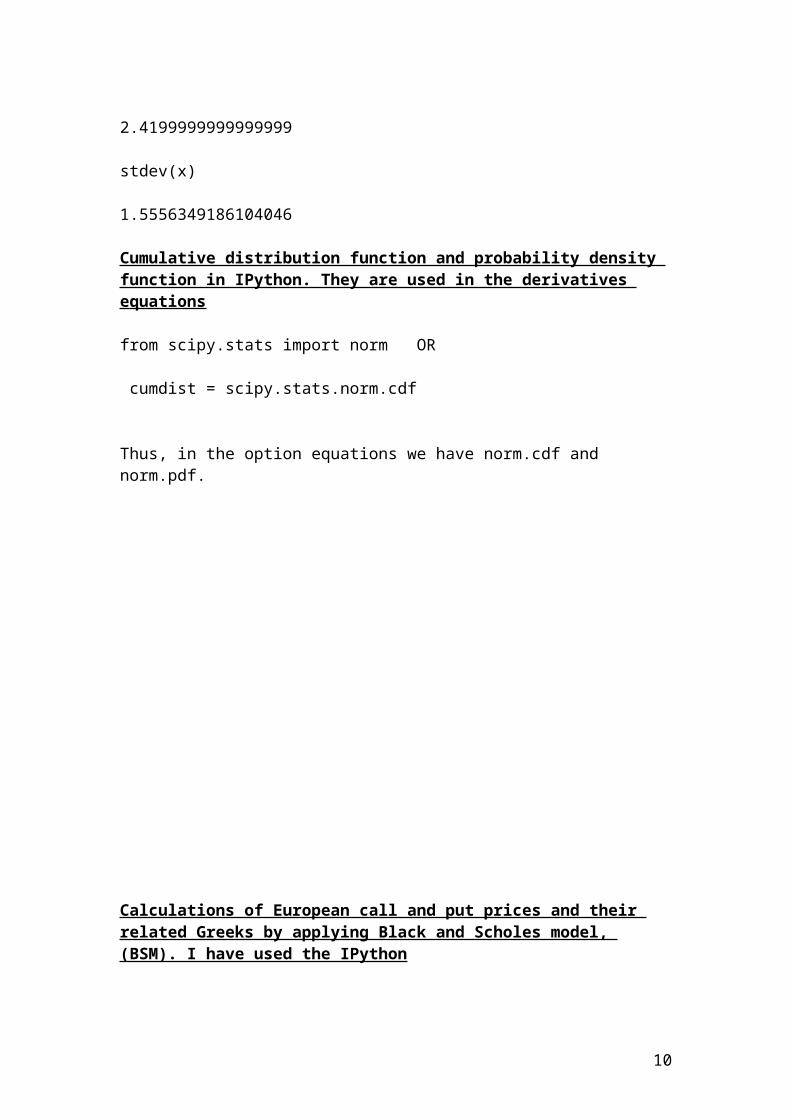

variance(x)

2.4199999999999999

stdev(x)

1.5556349186104046

Cumulative distribution function and probability density function in IPython. They are used in the derivatives equations

from scipy.stats import norm OR

cumdist = scipy.stats.norm.cdf

Thus, in the option equations we have norm.cdf and norm.pdf.

7

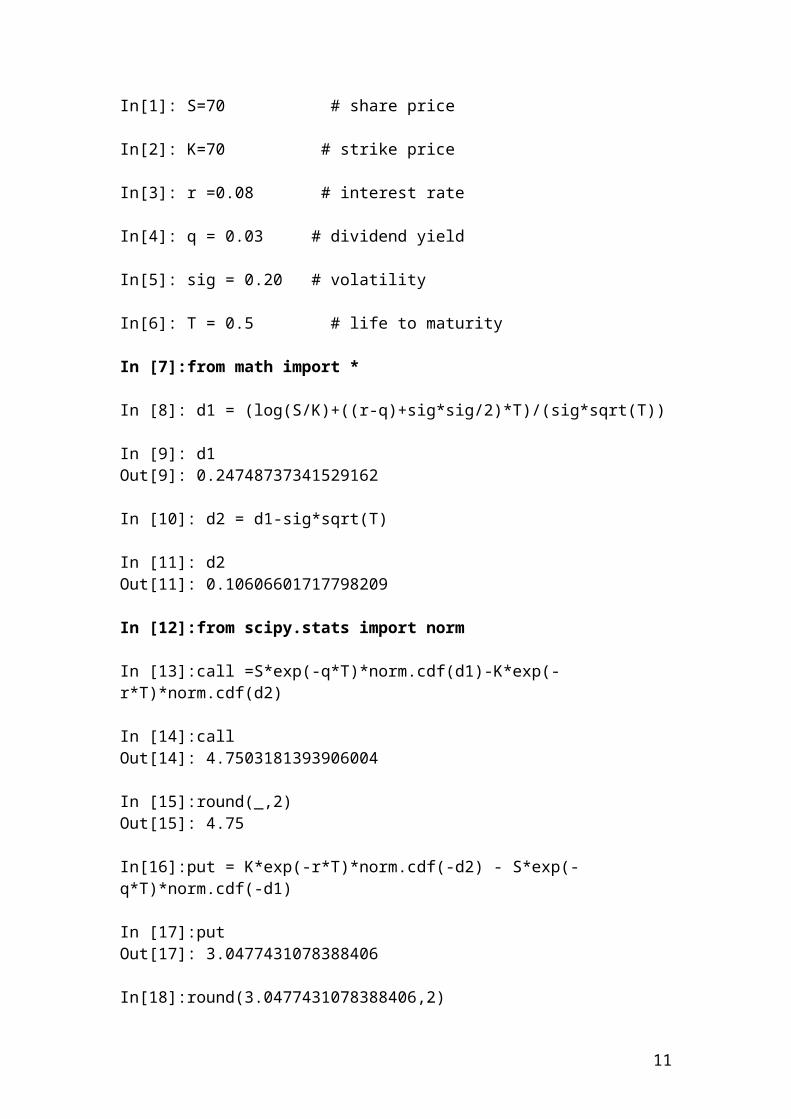

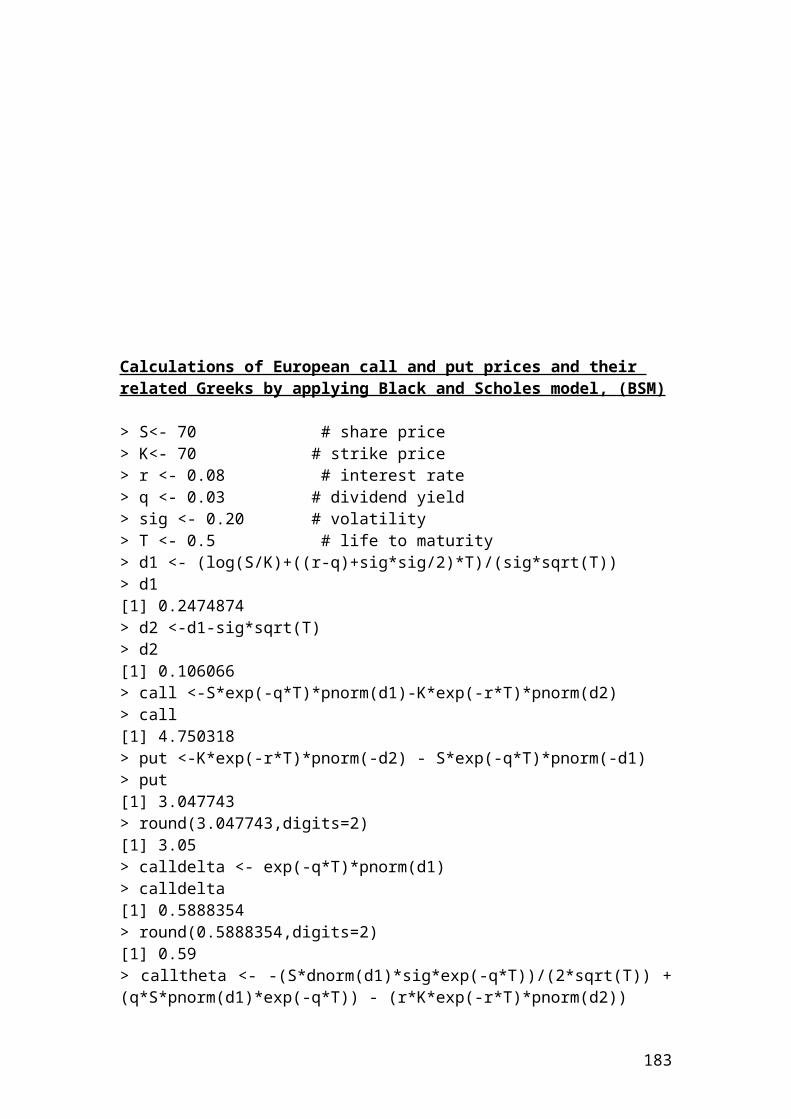

Calculations of European call and put prices and their related Greeks by applying Black and Scholes model, (BSM). I have used the IPython

In[1]: S=70 # share price

In[2]: K=70 # strike price

In[3]: r =0.08 # interest rate

In[4]: q = 0.03 # dividend yield

In[5]: sig = 0.20 # volatility

In[6]: T = 0.5 # life to maturity

In [7]:from math import *

In [8]: d1 = (log(S/K)+((r-q)+sig*sig/2)*T)/(sig*sqrt(T))

In [9]: d1Out[9]: 0.24748737341529162

In [10]: d2 = d1-sig*sqrt(T)

In [11]: d2Out[11]: 0.10606601717798209

In [12]:from scipy.stats import norm

In [13]:call =S*exp(-q*T)*norm.cdf(d1)-K*exp(-r*T)*norm.cdf(d2)

In [14]:callOut[14]: 4.7503181393906004

In [15]:round(_,2)Out[15]: 4.75

In[16]:put = K*exp(-r*T)*norm.cdf(-d2) - S*exp(-q*T)*norm.cdf(-d1)

In [17]:putOut[17]: 3.0477431078388406

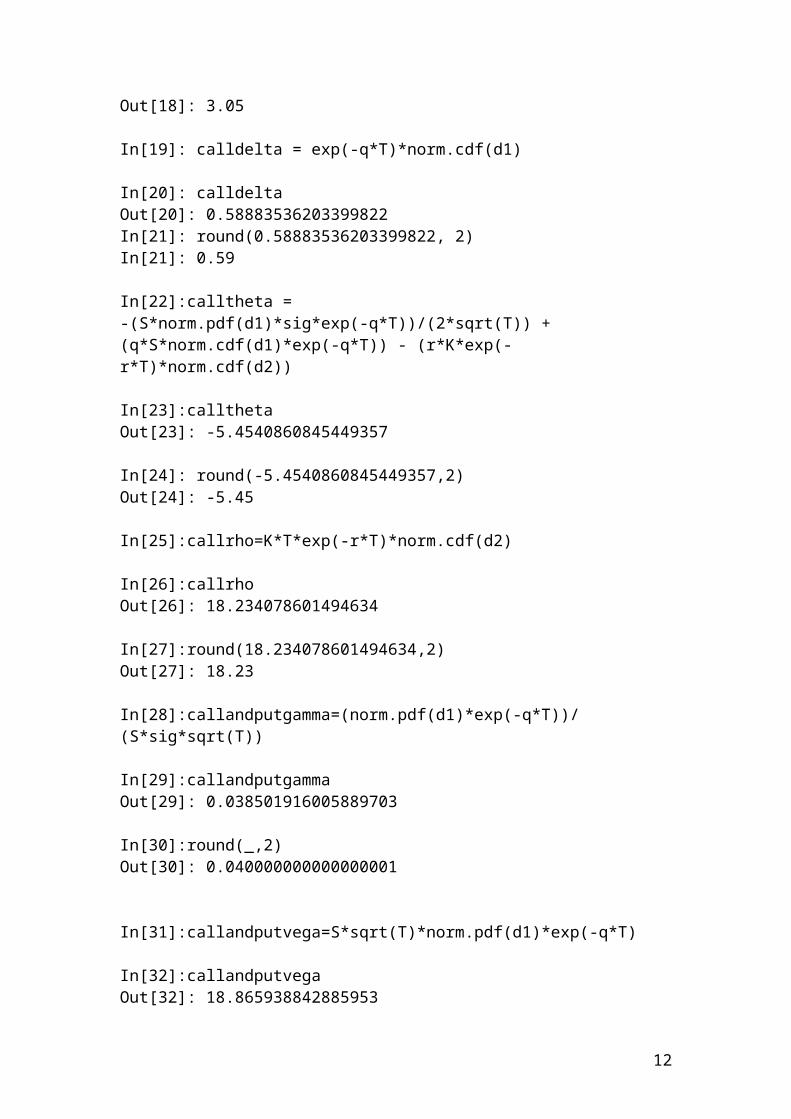

In[18]:round(3.0477431078388406,2)Out[18]: 3.05

In[19]: calldelta = exp(-q*T)*norm.cdf(d1)

In[20]: calldeltaOut[20]: 0.58883536203399822

8

In[21]: round(0.58883536203399822, 2)In[21]: 0.59

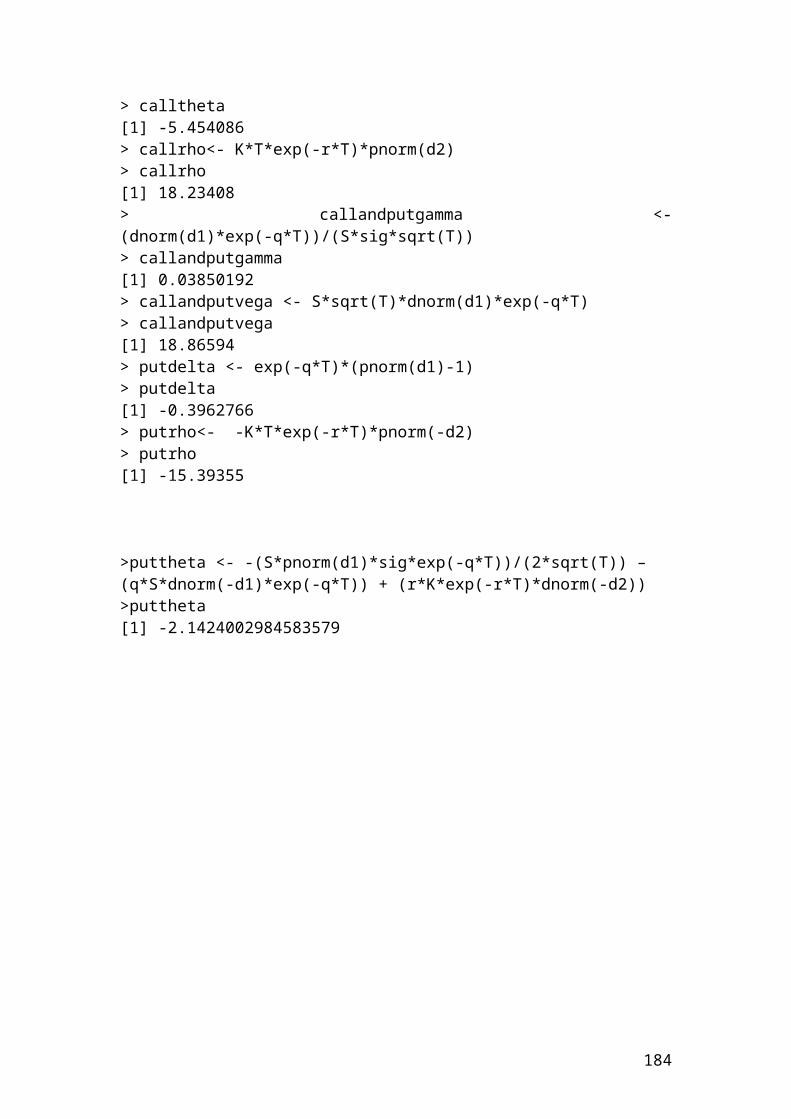

In[22]:calltheta = -(S*norm.pdf(d1)*sig*exp(-q*T))/(2*sqrt(T)) +(q*S*norm.cdf(d1)*exp(-q*T)) - (r*K*exp(-r*T)*norm.cdf(d2))

In[23]:callthetaOut[23]: -5.4540860845449357

In[24]: round(-5.4540860845449357,2)Out[24]: -5.45

In[25]:callrho=K*T*exp(-r*T)*norm.cdf(d2)

In[26]:callrhoOut[26]: 18.234078601494634

In[27]:round(18.234078601494634,2)Out[27]: 18.23

In[28]:callandputgamma=(norm.pdf(d1)*exp(-q*T))/(S*sig*sqrt(T))

In[29]:callandputgammaOut[29]: 0.038501916005889703

In[30]:round(_,2)Out[30]: 0.040000000000000001

In[31]:callandputvega=S*sqrt(T)*norm.pdf(d1)*exp(-q*T)

In[32]:callandputvegaOut[32]: 18.865938842885953

In[33]:round(_,2)Out[33]: 18.870000000000001

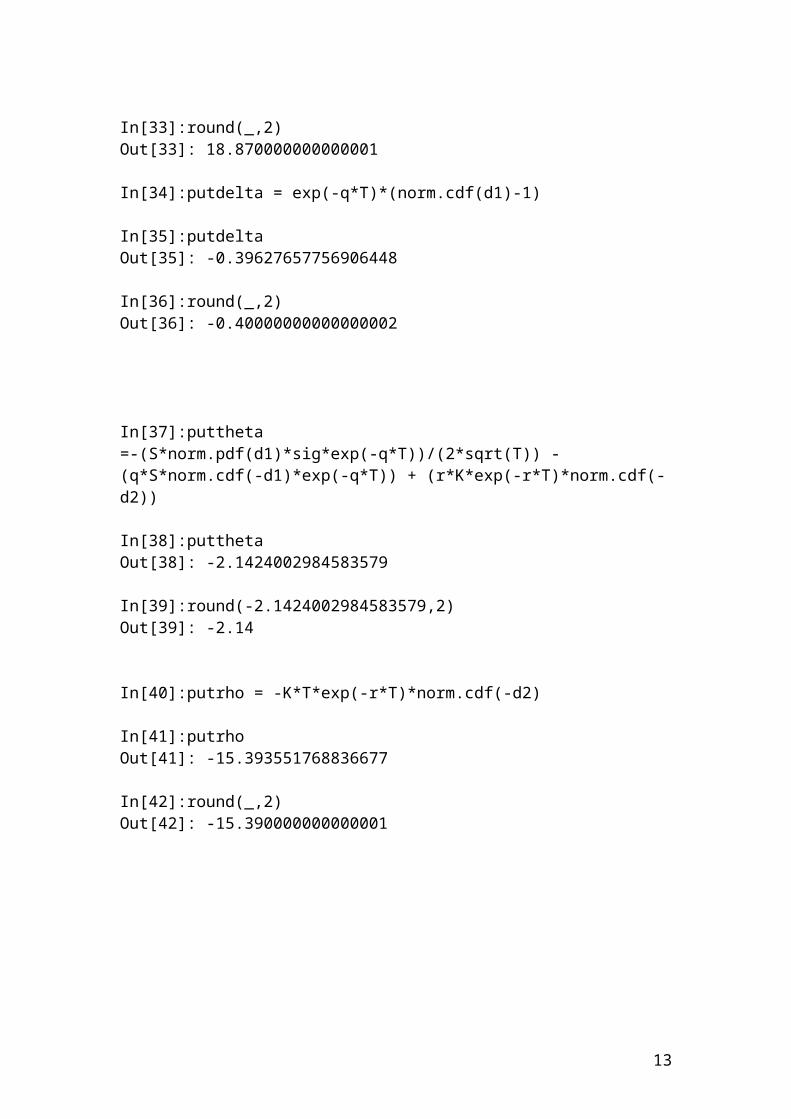

In[34]:putdelta = exp(-q*T)*(norm.cdf(d1)-1)

In[35]:putdeltaOut[35]: -0.39627657756906448

In[36]:round(_,2)Out[36]: -0.40000000000000002

In[37]:puttheta =-(S*norm.pdf(d1)*sig*exp(-q*T))/(2*sqrt(T)) - (q*S*norm.cdf(-d1)*exp(-q*T)) + (r*K*exp(-r*T)*norm.cdf(-d2))

9

In[38]:putthetaOut[38]: -2.1424002984583579

In[39]:round(-2.1424002984583579,2)Out[39]: -2.14

In[40]:putrho = -K*T*exp(-r*T)*norm.cdf(-d2)

In[41]:putrhoOut[41]: -15.393551768836677

In[42]:round(_,2)Out[42]: -15.390000000000001

10

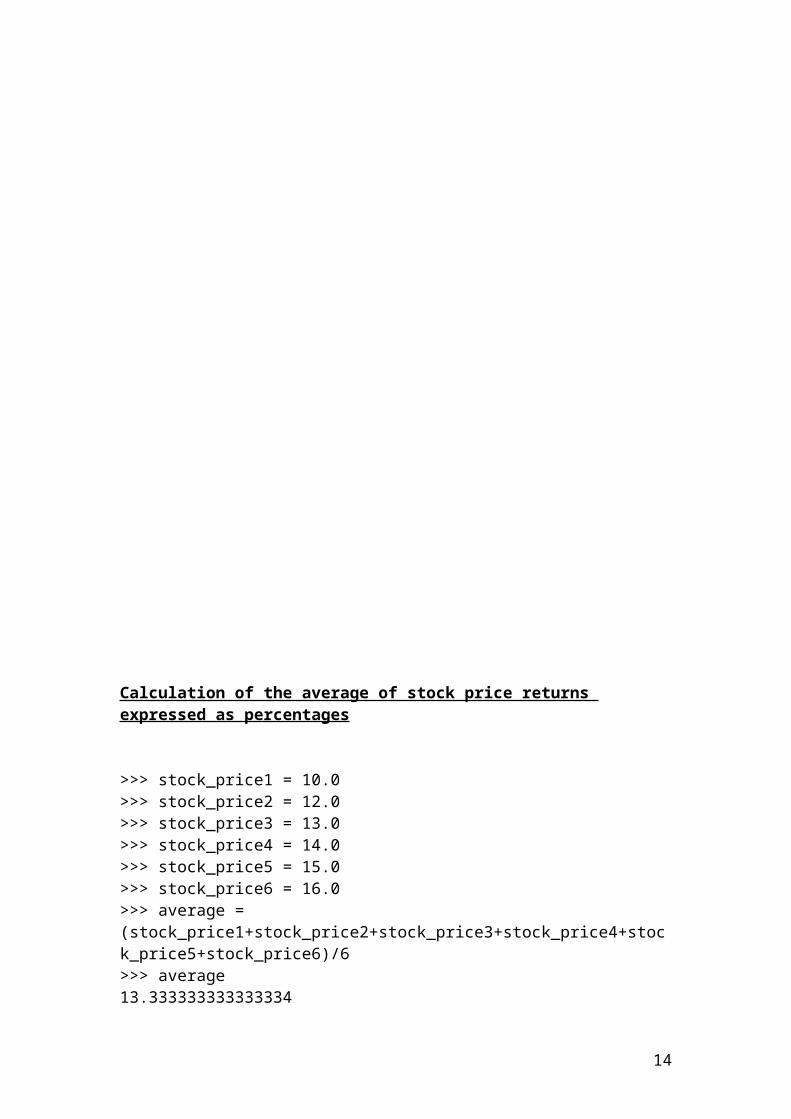

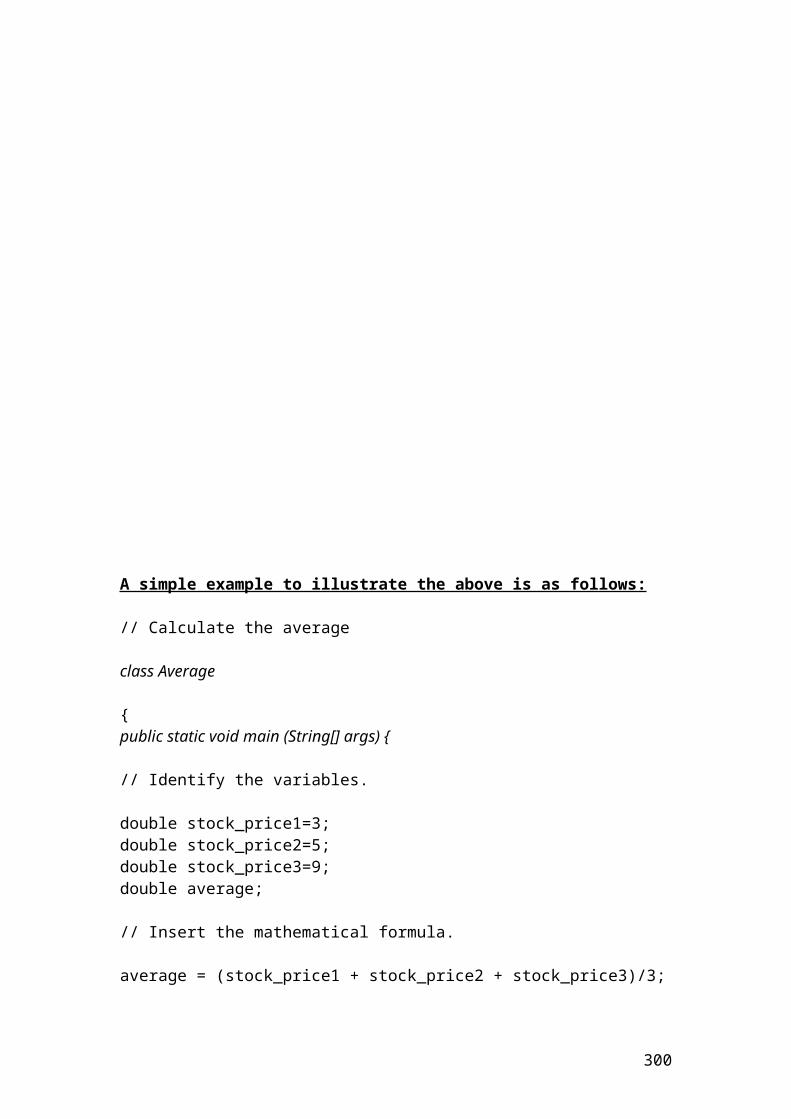

Calculation of the average of stock price returns expressed as percentages

>>> stock_price1 = 10.0>>> stock_price2 = 12.0>>> stock_price3 = 13.0>>> stock_price4 = 14.0>>> stock_price5 = 15.0>>> stock_price6 = 16.0>>> average = (stock_price1+stock_price2+stock_price3+stock_price4+stock_price5+stock_price6)/6>>> average13.333333333333334

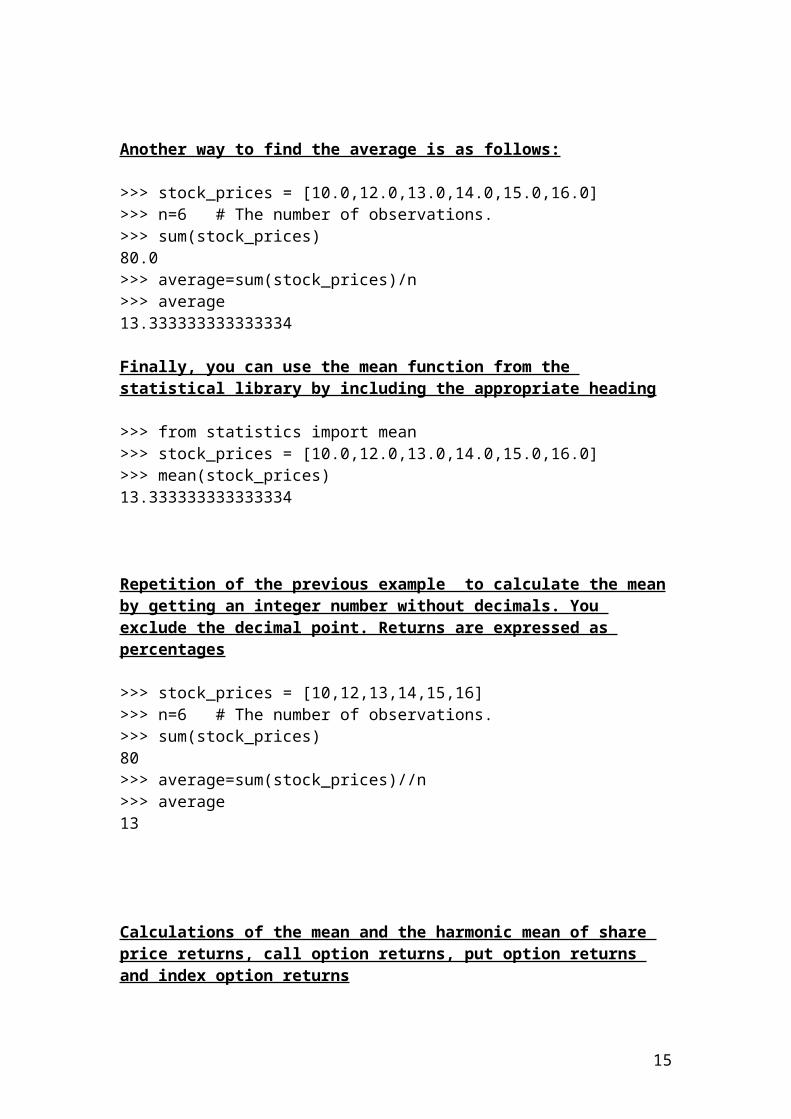

Another way to find the average is as follows:

>>> stock_prices = [10.0,12.0,13.0,14.0,15.0,16.0]>>> n=6 # The number of observations.>>> sum(stock_prices)80.0>>> average=sum(stock_prices)/n>>> average13.333333333333334

Finally, you can use the mean function from the statistical library by including the appropriate heading

>>> from statistics import mean>>> stock_prices = [10.0,12.0,13.0,14.0,15.0,16.0]>>> mean(stock_prices)13.333333333333334

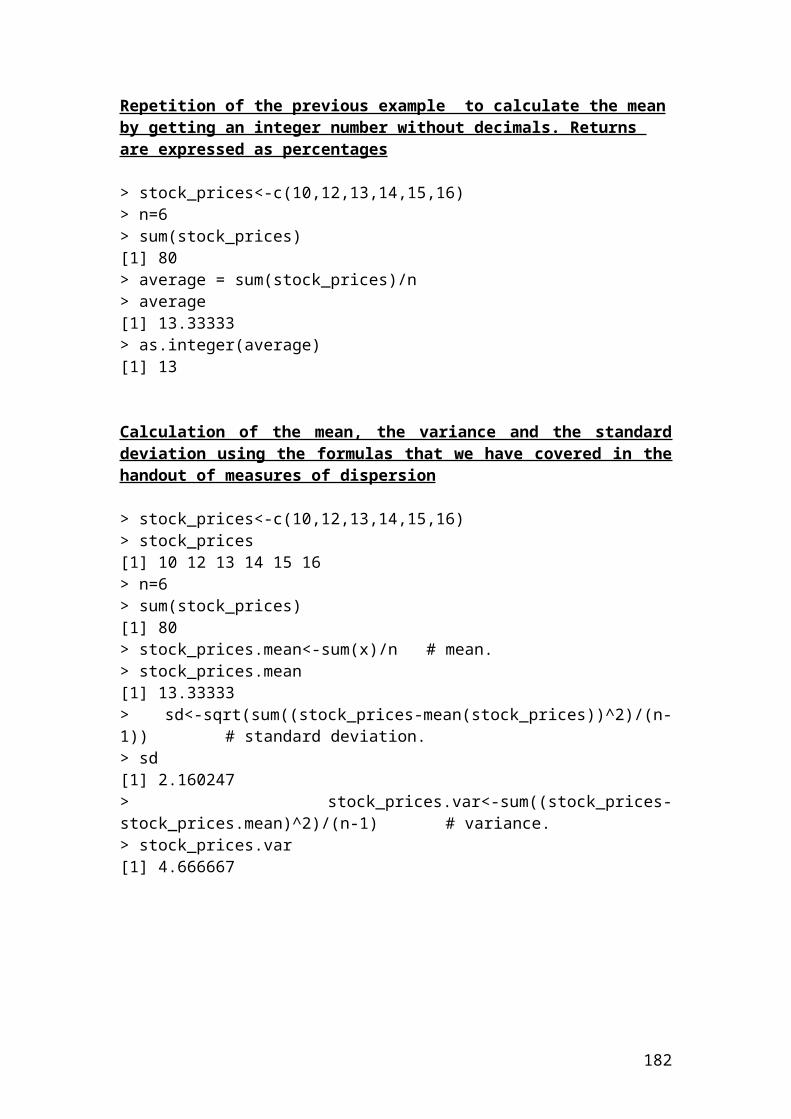

Repetition of the previous example to calculate the mean by getting an integer number without decimals. You exclude the decimal point. Returns are expressed as percentages

>>> stock_prices = [10,12,13,14,15,16]>>> n=6 # The number of observations.>>> sum(stock_prices)80>>> average=sum(stock_prices)//n>>> average13

11

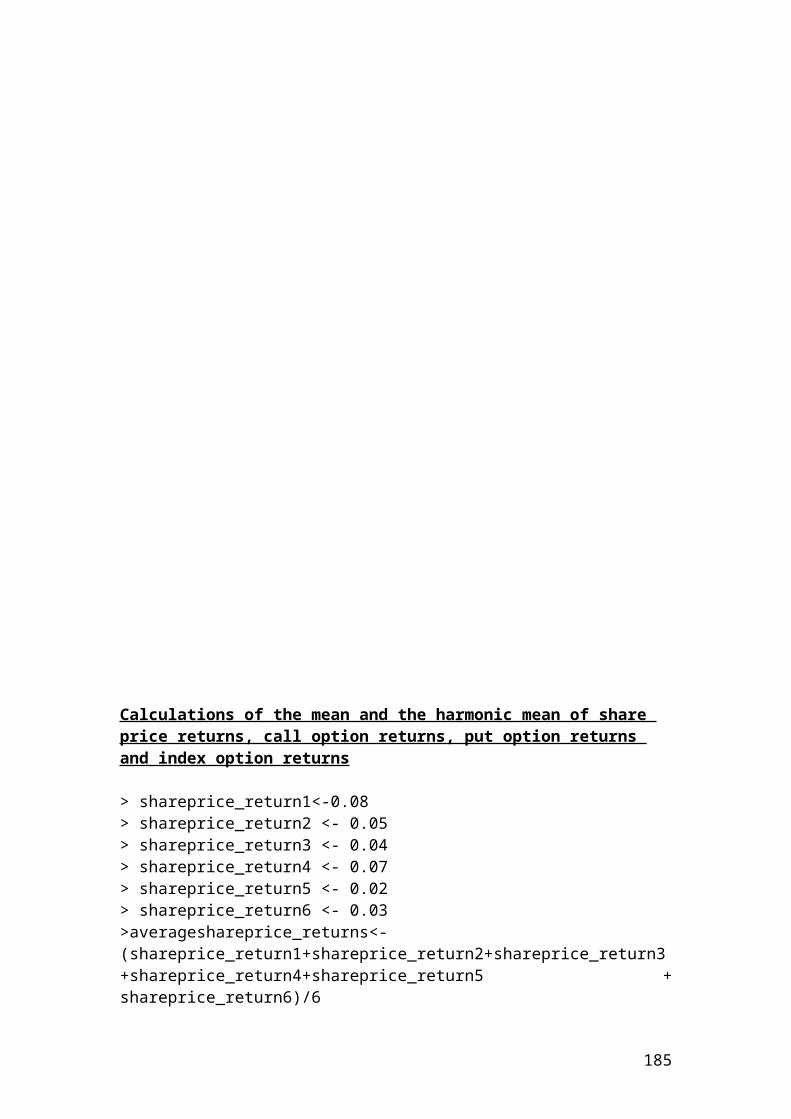

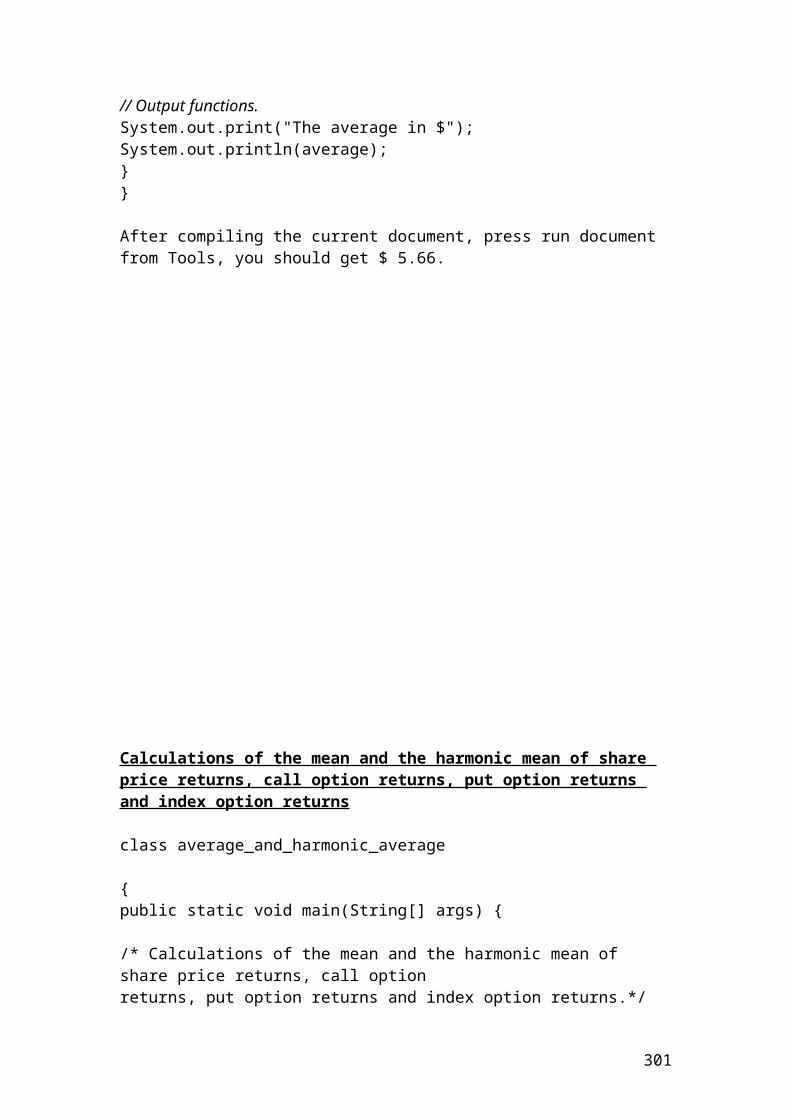

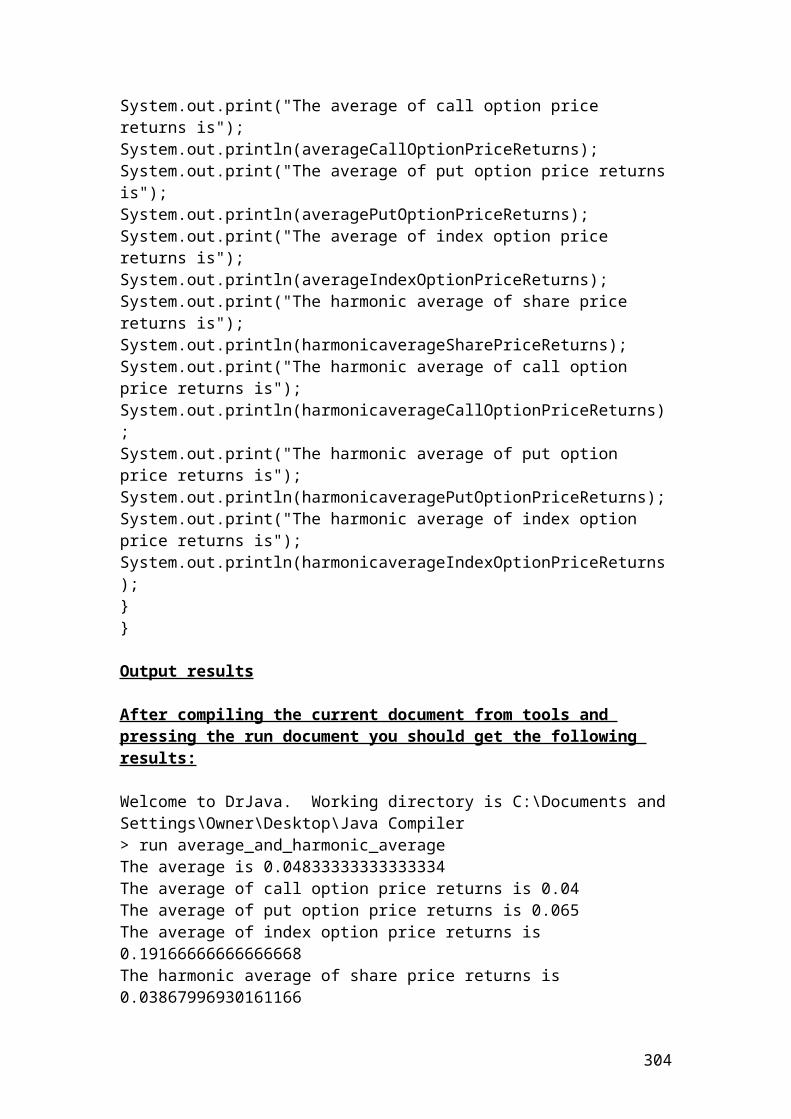

Calculations of the mean and the harmonic mean of share price returns, call option returns, put option returns and index option returns

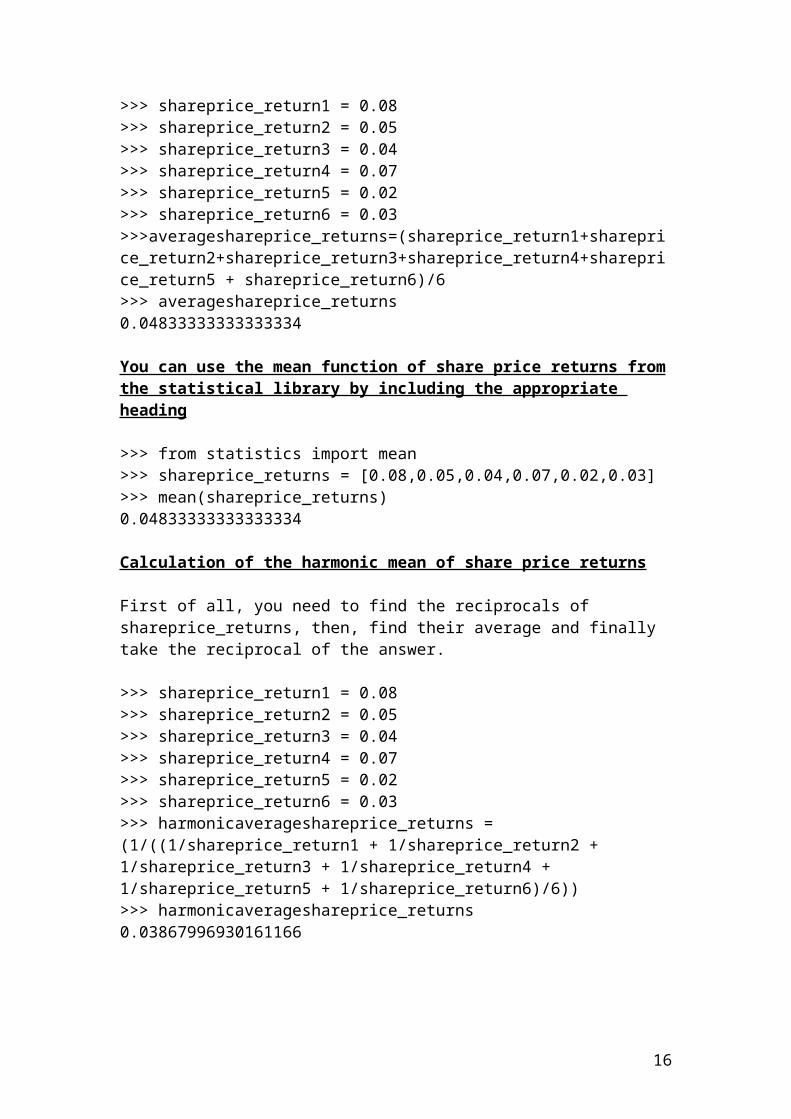

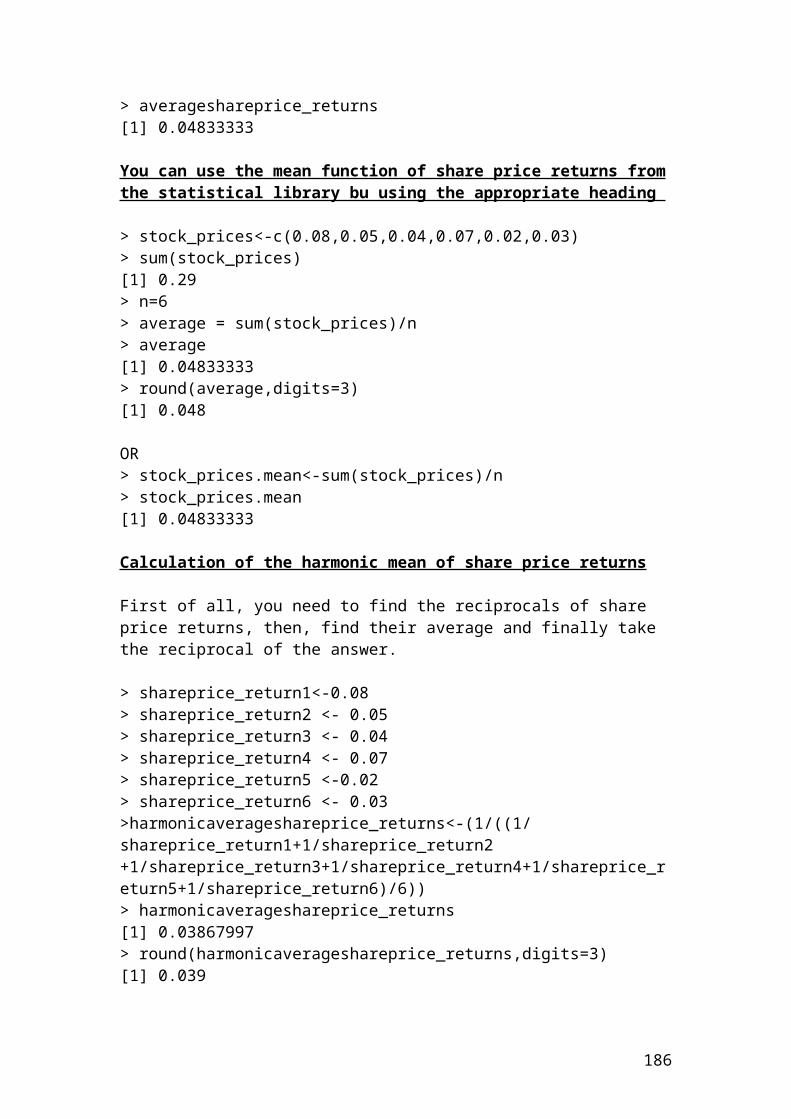

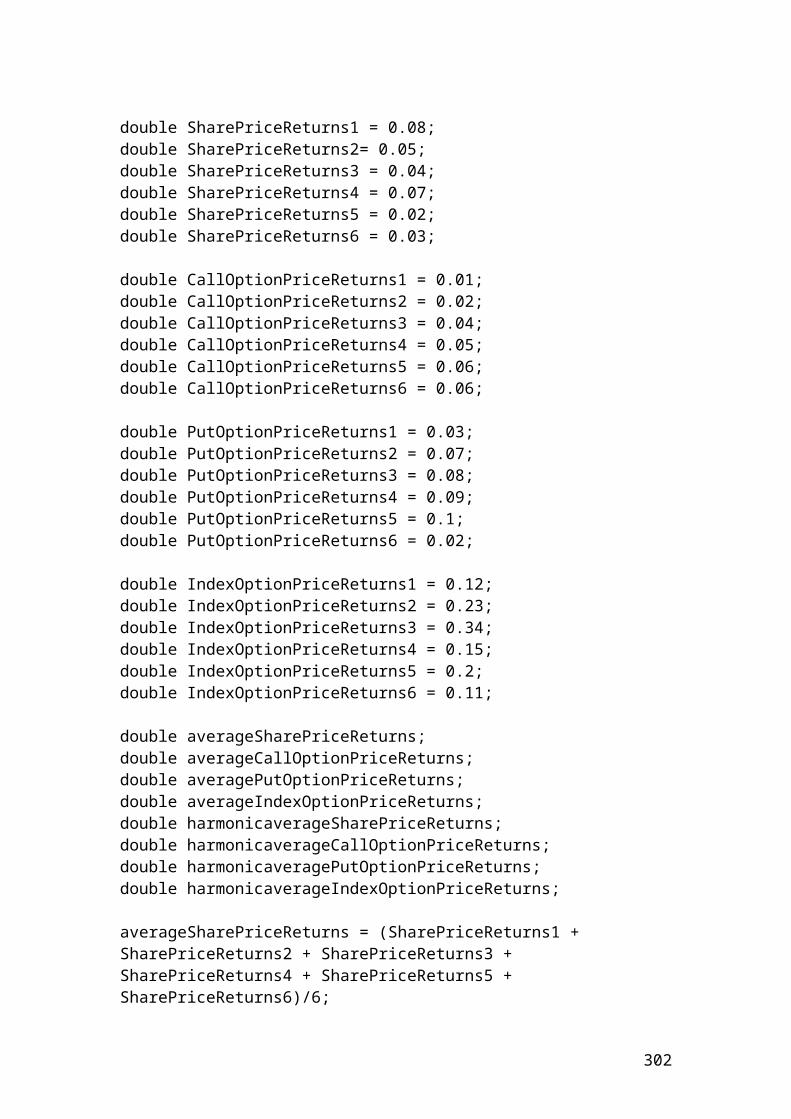

>>> shareprice_return1 = 0.08>>> shareprice_return2 = 0.05>>> shareprice_return3 = 0.04>>> shareprice_return4 = 0.07>>> shareprice_return5 = 0.02>>> shareprice_return6 = 0.03>>>averageshareprice_returns=(shareprice_return1+shareprice_return2+shareprice_return3+shareprice_return4+shareprice_return5 + shareprice_return6)/6>>> averageshareprice_returns0.04833333333333334

You can use the mean function of share price returns from the statistical library by including the appropriate heading

>>> from statistics import mean>>> shareprice_returns = [0.08,0.05,0.04,0.07,0.02,0.03]>>> mean(shareprice_returns)0.04833333333333334

Calculation of the harmonic mean of share price returns

First of all, you need to find the reciprocals of shareprice_returns, then, find their average and finally take the reciprocal of the answer.

>>> shareprice_return1 = 0.08>>> shareprice_return2 = 0.05>>> shareprice_return3 = 0.04>>> shareprice_return4 = 0.07>>> shareprice_return5 = 0.02>>> shareprice_return6 = 0.03>>> harmonicaverageshareprice_returns = (1/((1/shareprice_return1 + 1/shareprice_return2 + 1/shareprice_return3 + 1/shareprice_return4 + 1/shareprice_return5 + 1/shareprice_return6)/6))>>> harmonicaverageshareprice_returns0.03867996930161166

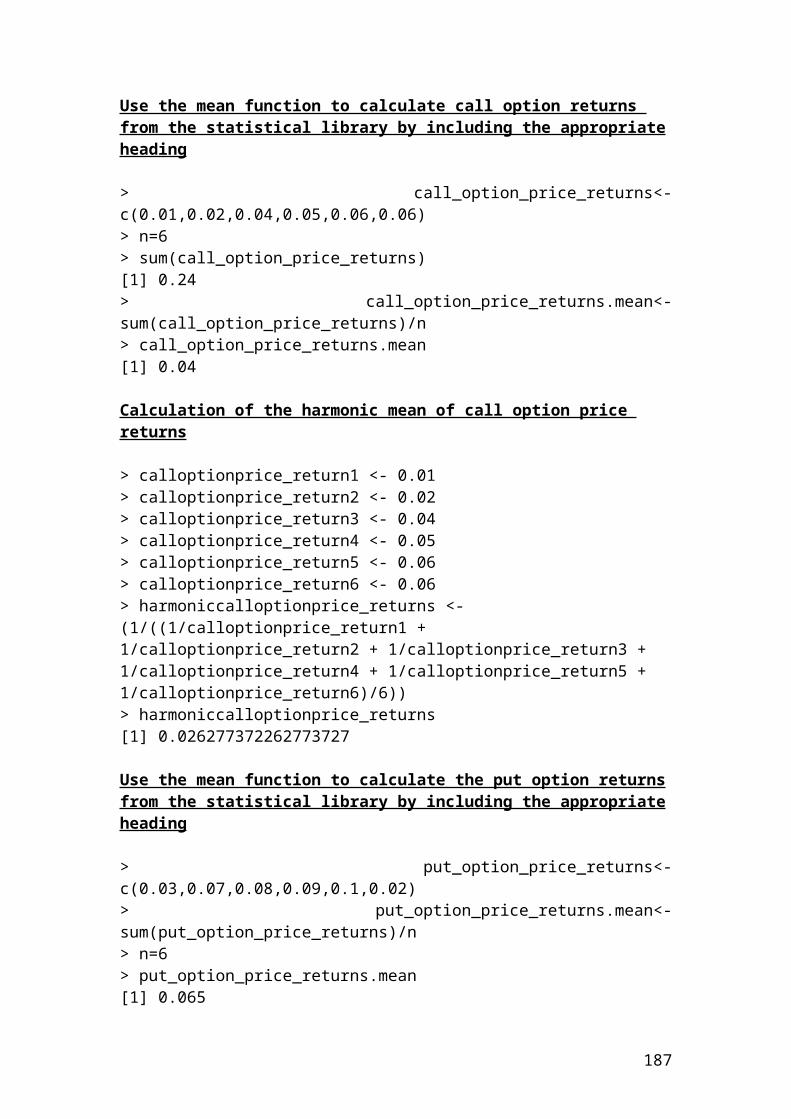

Use the mean function to calculate call option returns from the statistical library by including the appropriate heading

>>> from statistics import mean>>> calloptionprice_returns = [0.01,0.02,0.04,0.05,0.06,0.06]>>> mean(calloptionprice_returns)0.04

12

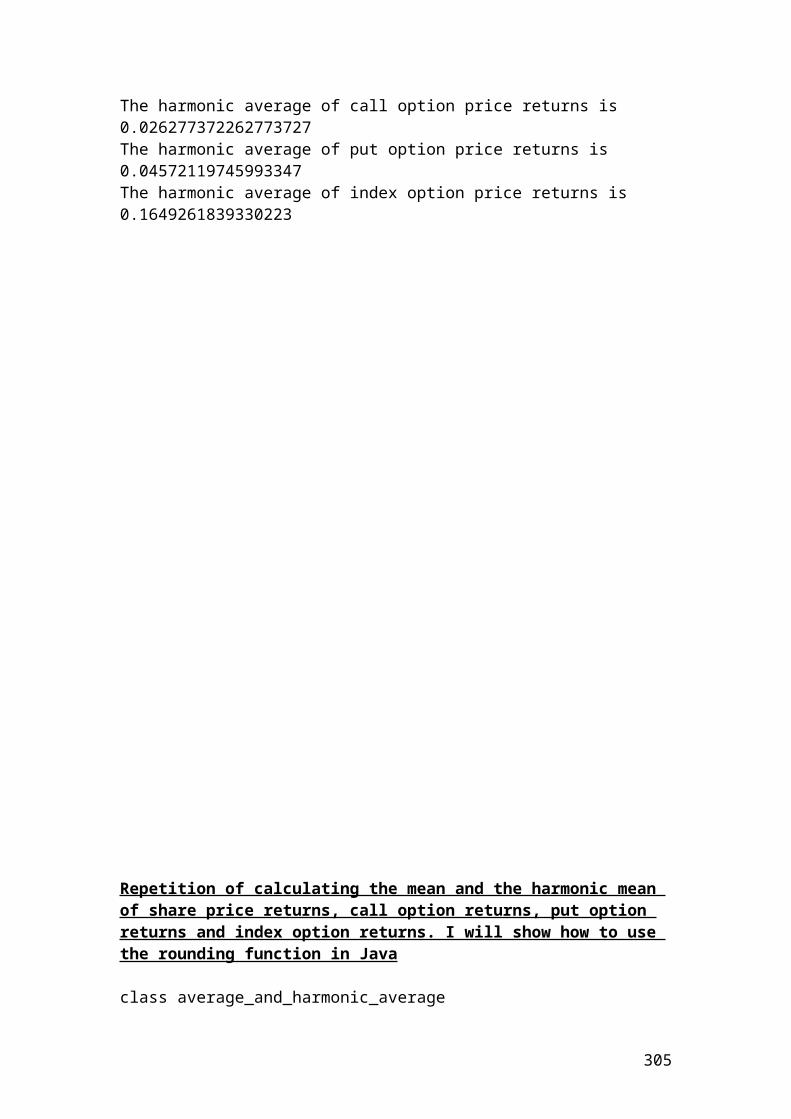

Calculation of the harmonic mean of call option price returns

>>> calloptionprice_return1 = 0.01>>> calloptionprice_return2 = 0.02>>> calloptionprice_return3 = 0.04>>> calloptionprice_return4 = 0.05>>> calloptionprice_return5 = 0.06>>> calloptionprice_return6 = 0.06>>> harmoniccalloptionprice_returns = (1/((1/calloptionprice_return1 + 1/calloptionprice_return2 + 1/calloptionprice_return3 + 1/calloptionprice_return4 + 1/calloptionprice_return5 + 1/calloptionprice_return6)/6))>>> harmoniccalloptionprice_returns0.026277372262773727>>> round(_,2)0.03

Use the mean function to calculate the put option returns from the statistical library by including the appropriate heading

>>> from statistics import mean>>> putoptionprice_returns = [0.03,0.07,0.08,0.09,0.1,0.02]>>> mean(putoptionprice_returns)0.065

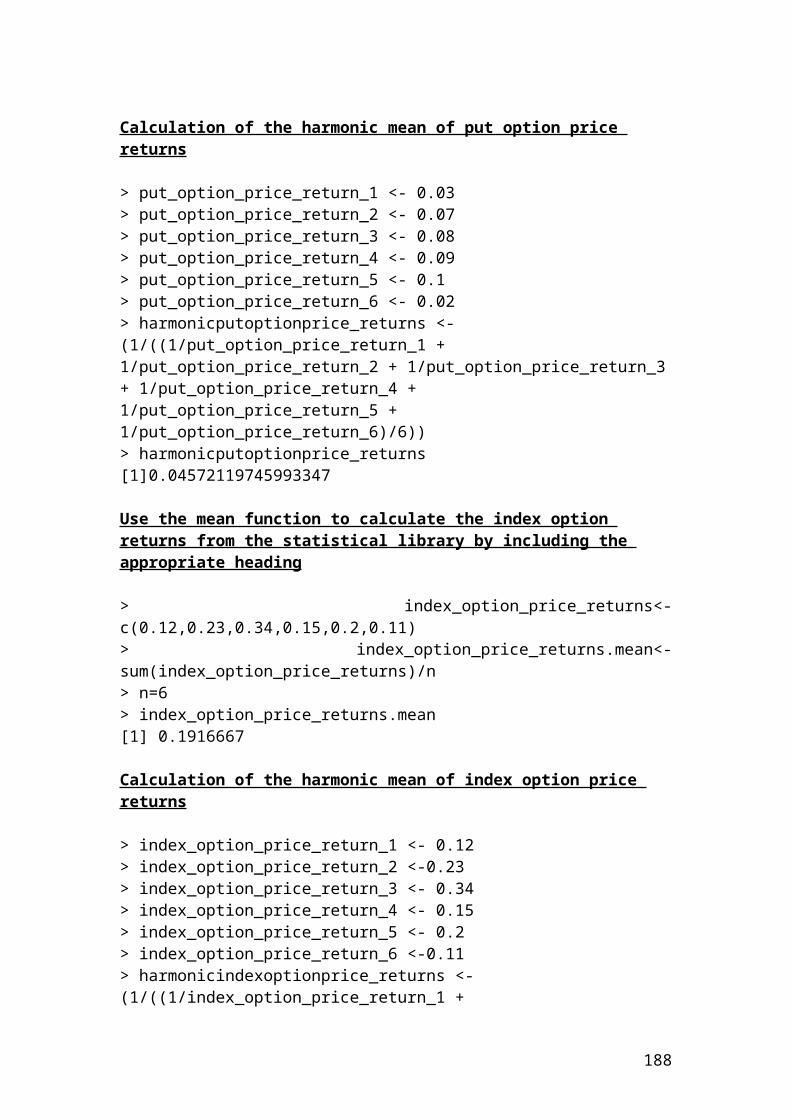

Calculation of the harmonic mean of put option price returns

>>> putoptionprice_return1 = 0.03>>> putoptionprice_return2 = 0.07>>> putoptionprice_return3 = 0.08>>> putoptionprice_return4 = 0.09>>> putoptionprice_return5 = 0.1>>> putoptionprice_return6 = 0.02>>> harmonicputoptionprice_returns = (1/((1/putoptionprice_return1 + 1/putoptionprice_return2 + 1/putoptionprice_return3 + 1/putoptionprice_return4 + 1/putoptionprice_return5 + 1/putoptionprice_return6)/6))>>> harmonicputoptionprice_returns0.04572119745993347>>> round(_,2)0.05

13

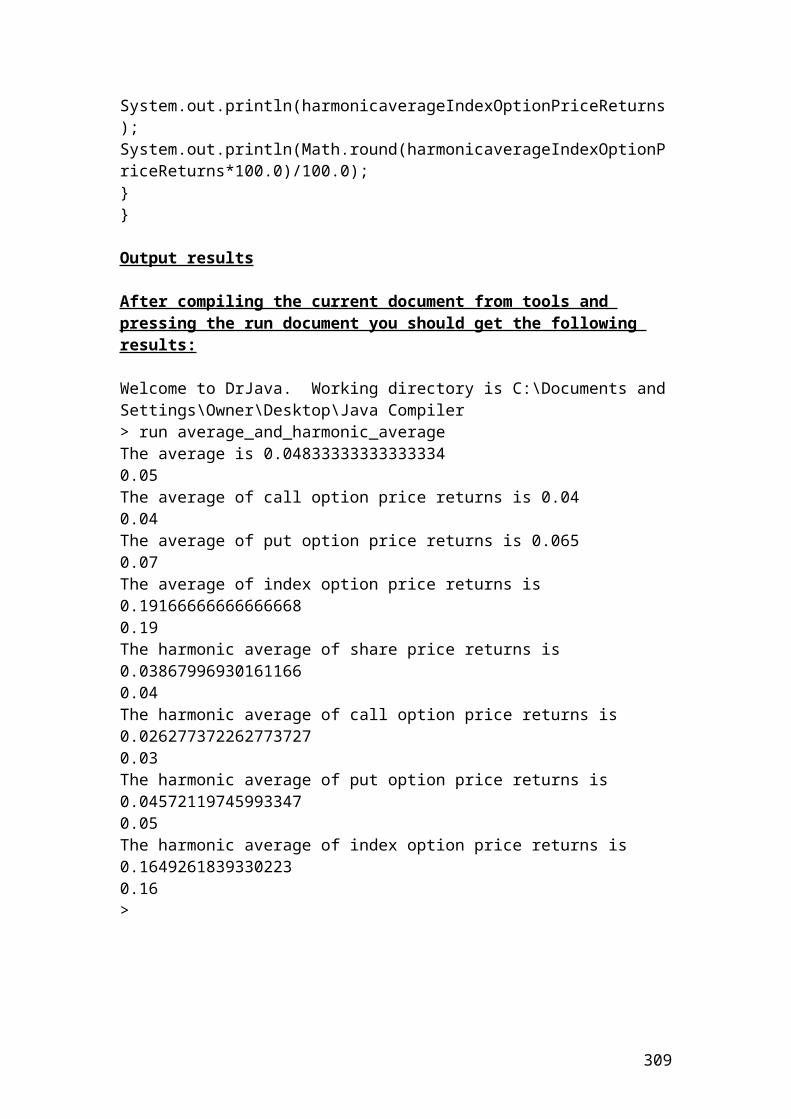

Use the mean function to calculate the index option returns from the statistical library by including the appropriate heading

>>> from statistics import mean>>> indexoptionprice_returns = [0.12,0.23,0.34,0.15,0.2,0.11]>>> mean(indexoptionprice_returns)0.19166666666666668>>> round(_,2)0.19

Calculation of the harmonic mean of index option price returns

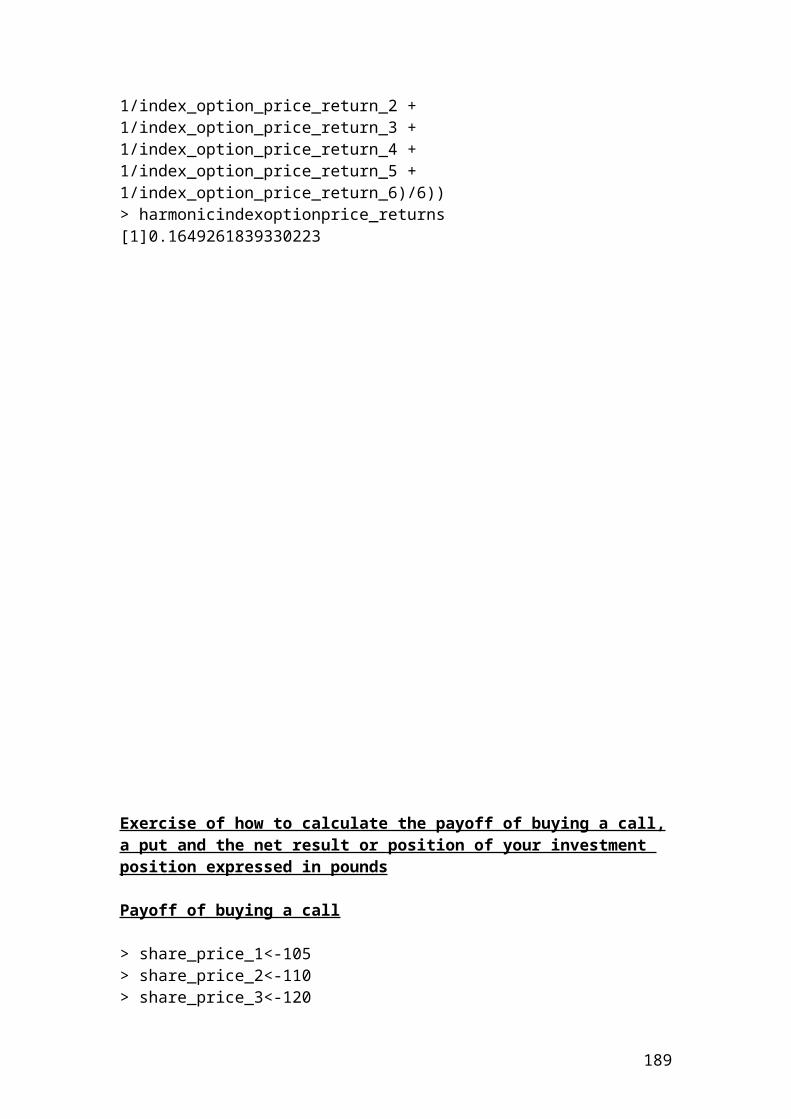

>>> indexoptionprice_return1 = 0.12>>> indexoptionprice_return2 = 0.23>>> indexoptionprice_return3 = 0.34>>> indexoptionprice_return4 = 0.15>>> indexoptionprice_return5 = 0.2>>> indexoptionprice_return6 = 0.11>>> harmonicindexoptionprice_returns = (1/((1/indexoptionprice_return1 + 1/indexoptionprice_return2 + 1/indexoptionprice_return3 + 1/indexoptionprice_return4 + 1/indexoptionprice_return5 + 1/indexoptionprice_return6)/6))>>> harmonicindexoptionprice_returns0.1649261839330223>>> round(_,2)0.16

14

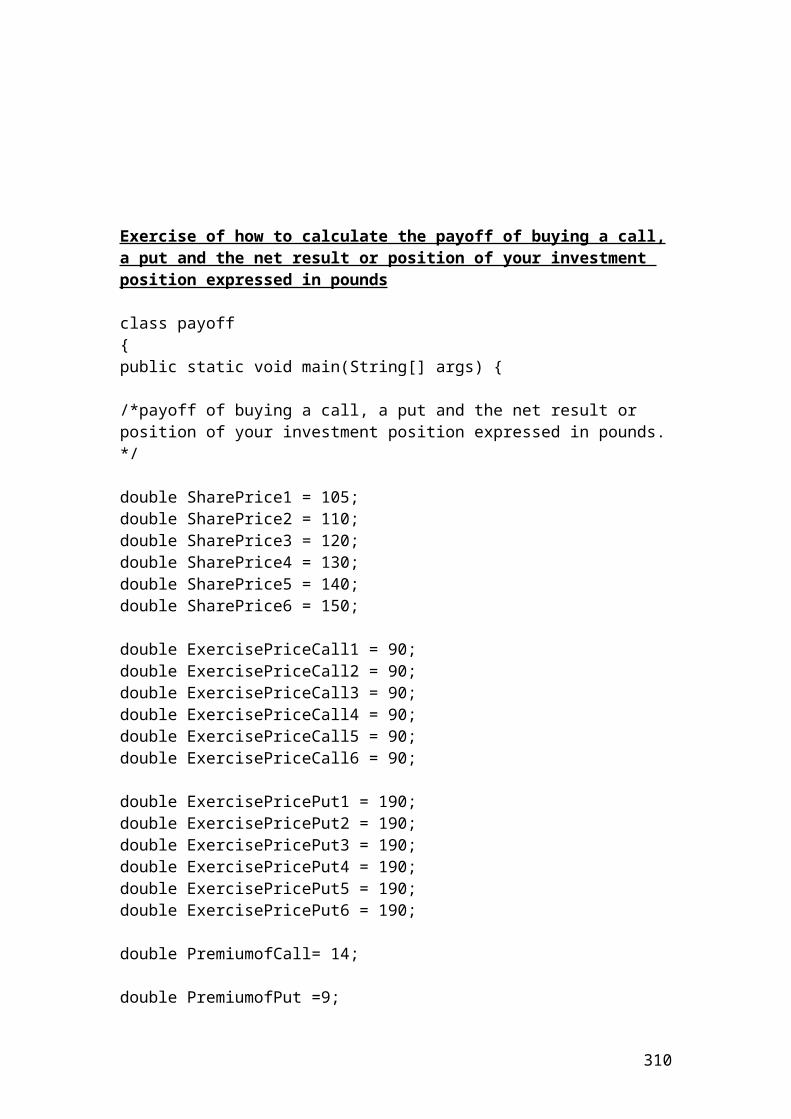

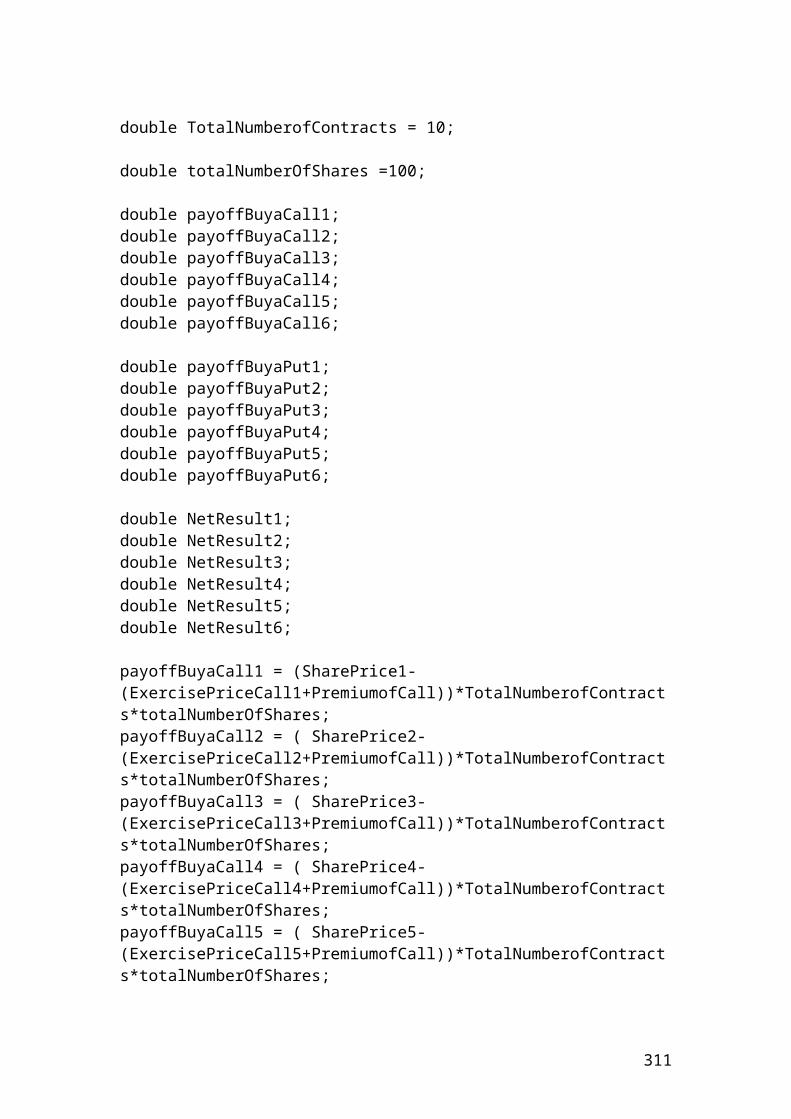

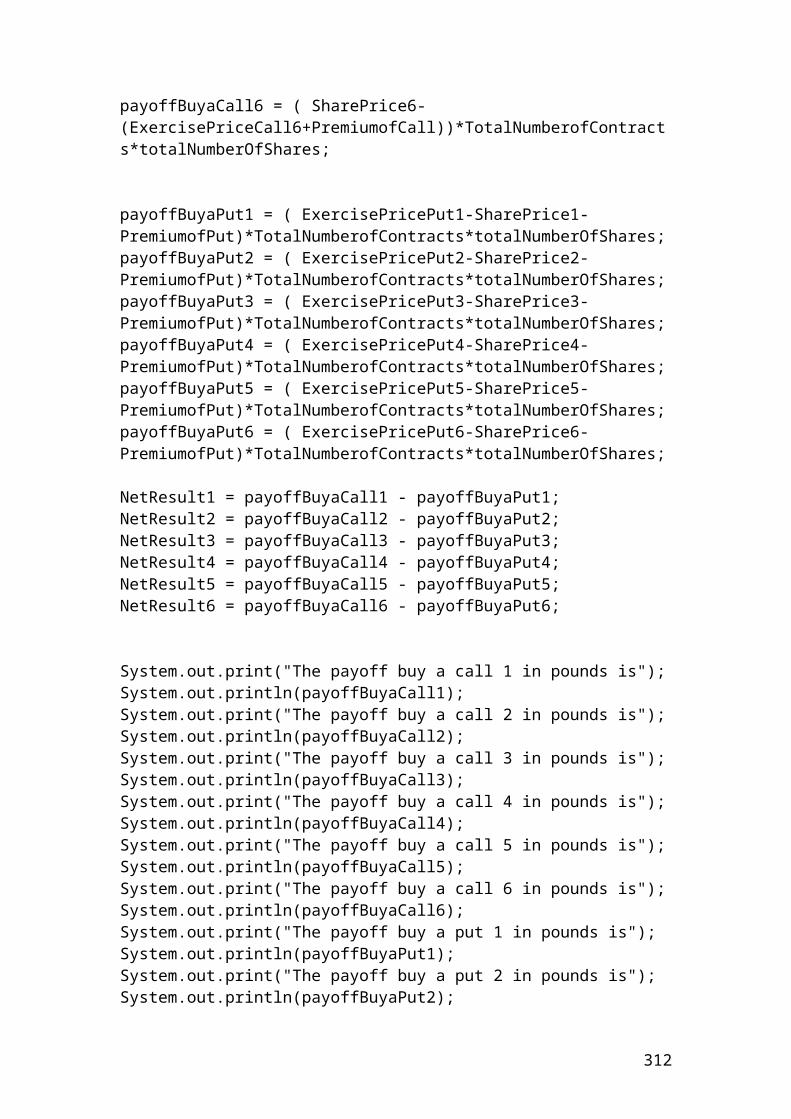

Exercise of how to calculate the payoff of buying a call, a put and the net result or position of your investment position expressed in pounds

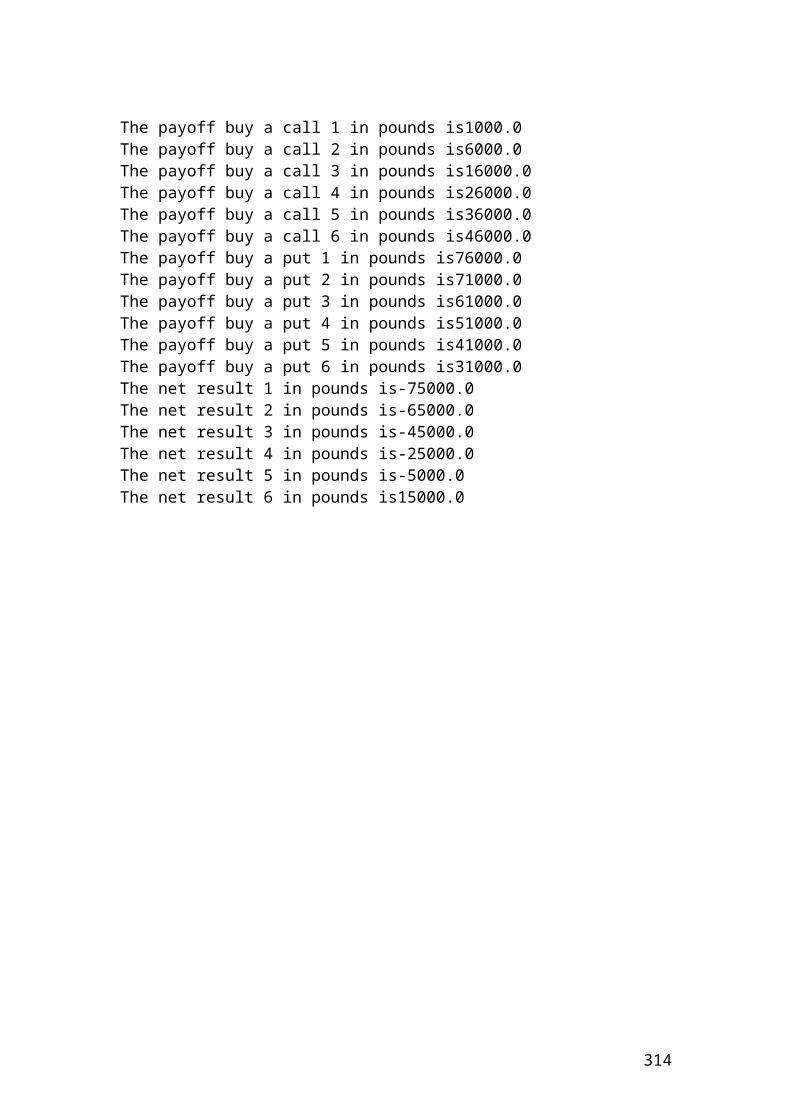

Payoff of buying a call

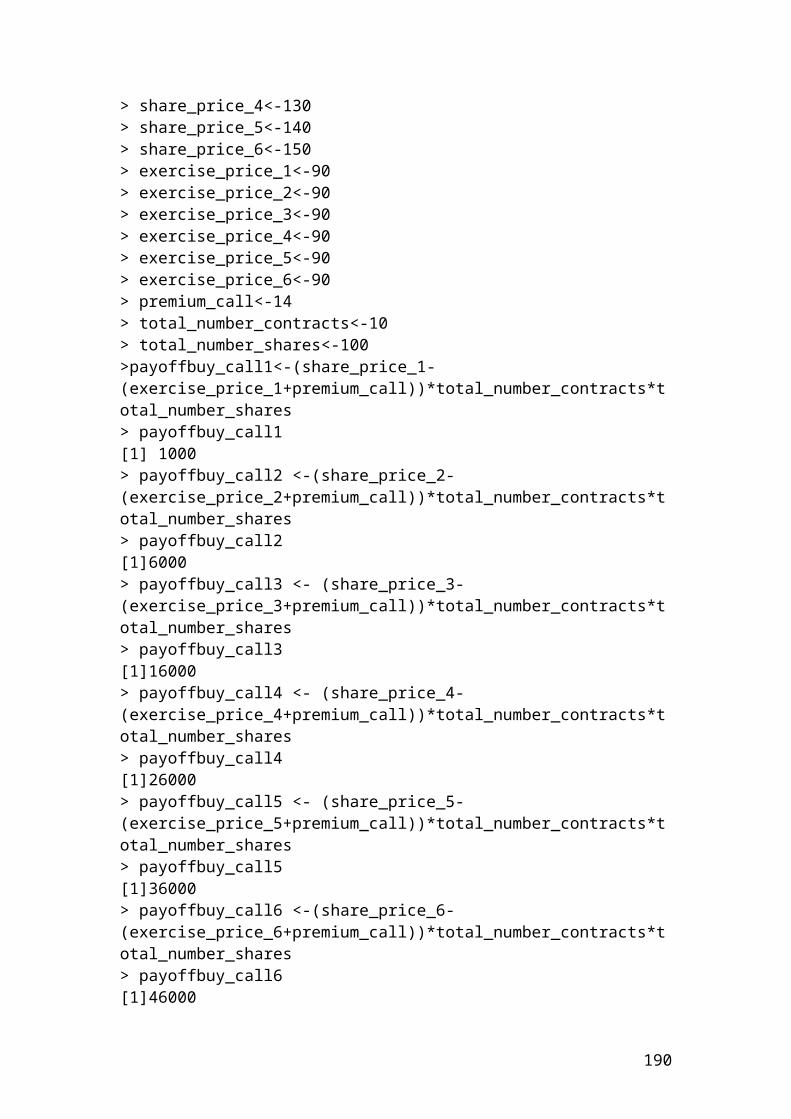

>>> share_price1=105>>> share_price2=110>>> share_price3=120>>> share_price4=130>>> share_price5=140>>> share_price6=150>>> >>> exerciseprice_call1=90>>> exerciseprice_call2=90>>> exerciseprice_call3=90>>> exerciseprice_call4=90>>> exerciseprice_call5=90>>> exerciseprice_call6=90>>> >>> premium_call=14>>> totalnumber_contracts=10>>> totalnumber_shares=100>>> >>> payoffbuy_call1 = (share_price1-(exerciseprice_call1+premium_call))*totalnumber_contracts*totalnumber_shares>>> payoffbuy_call11000>>> payoffbuy_call2 = (share_price2-(exerciseprice_call2+premium_call))*totalnumber_contracts*totalnumber_shares>>> payoffbuy_call26000>>> payoffbuy_call3 = (share_price3-(exerciseprice_call3+premium_call))*totalnumber_contracts*totalnumber_shares>>> payoffbuy_call316000>>> payoffbuy_call4 = (share_price4-(exerciseprice_call4+premium_call))*totalnumber_contracts*totalnumber_shares>>> payoffbuy_call426000>>> payoffbuy_call5 = (share_price5-(exerciseprice_call5+premium_call))*totalnumber_contracts*totalnumber_shares>>> payoffbuy_call536000>>> payoffbuy_call6 = (share_price6-(exerciseprice_call6+premium_call))*totalnumber_contracts*totalnumber_shares>>> payoffbuy_call646000

15

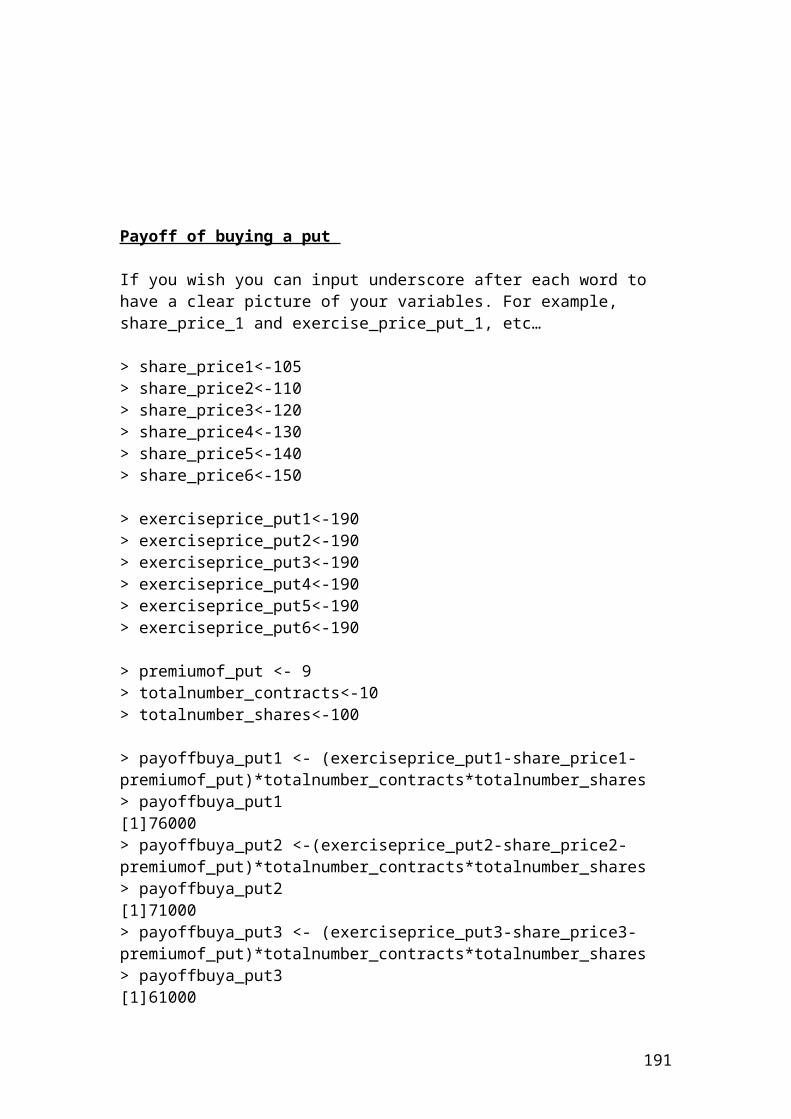

Payoff of buying a put

>>> share_price1=105>>> share_price2=110>>> share_price3=120>>> share_price4=130>>> share_price5=140>>> share_price6=150

>>> exerciseprice_put1=190>>> exerciseprice_put2=190>>> exerciseprice_put3=190>>> exerciseprice_put4=190>>> exerciseprice_put5=190>>> exerciseprice_put6=190

>>> premiumof_put = 9>>> totalnumber_contracts=10>>> totalnumber_shares=100

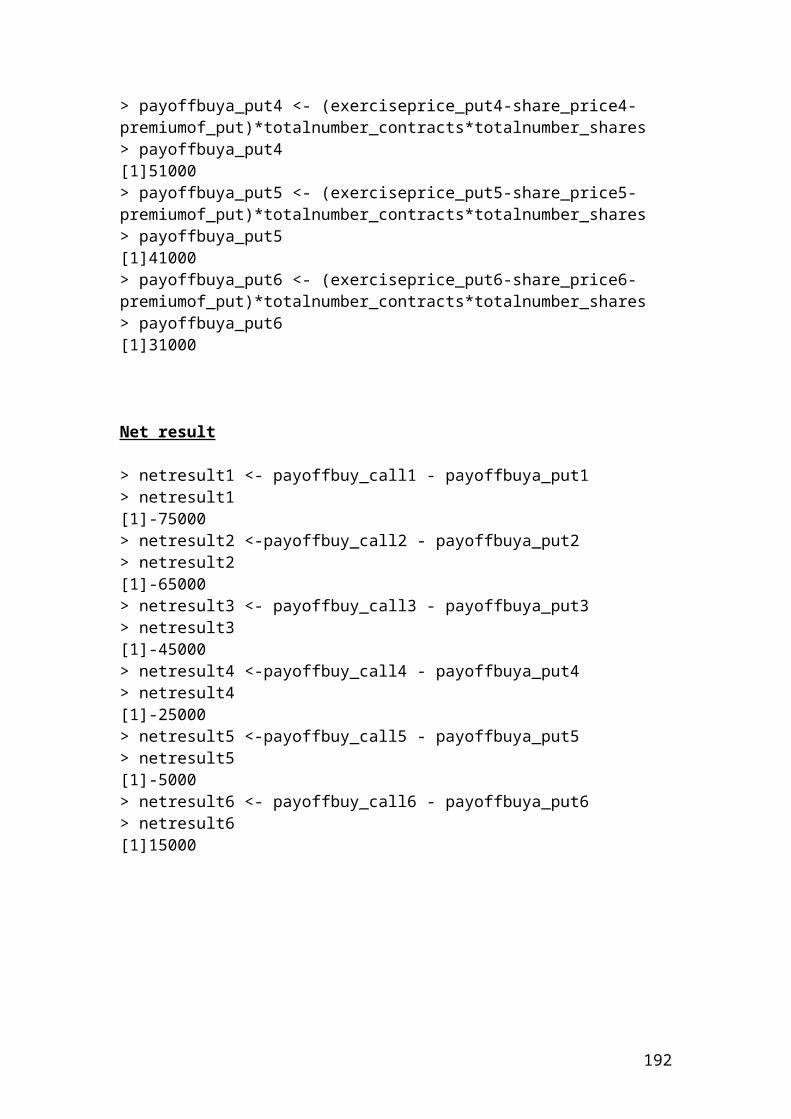

>>> payoffbuya_put1 = (exerciseprice_put1-share_price1-premiumof_put)*totalnumber_contracts*totalnumber_shares>>> payoffbuya_put176000>>> payoffbuya_put2 = (exerciseprice_put2-share_price2-premiumof_put)*totalnumber_contracts*totalnumber_shares>>> payoffbuya_put271000>>> payoffbuya_put3 = (exerciseprice_put3-share_price3-premiumof_put)*totalnumber_contracts*totalnumber_shares>>> payoffbuya_put361000>>> payoffbuya_put4 = (exerciseprice_put4-share_price4-premiumof_put)*totalnumber_contracts*totalnumber_shares>>> payoffbuya_put451000>>> payoffbuya_put5 = (exerciseprice_put5-share_price5-premiumof_put)*totalnumber_contracts*totalnumber_shares>>> payoffbuya_put541000>>> payoffbuya_put6 = (exerciseprice_put6-share_price6-premiumof_put)*totalnumber_contracts*totalnumber_shares>>> payoffbuya_put631000>>>

16

Net result

>>> netresult1 = payoffbuy_call1 - payoffbuya_put1>>> netresult1-75000>>> netresult2 = payoffbuy_call2 - payoffbuya_put2>>> netresult2-65000>>> netresult3 = payoffbuy_call3 - payoffbuya_put3>>> netresult3-45000>>> netresult4 = payoffbuy_call4 - payoffbuya_put4>>> netresult4-25000>>> netresult5 = payoffbuy_call5 - payoffbuya_put5>>> netresult5-5000>>> netresult6 = payoffbuy_call6 - payoffbuya_put6>>> netresult615000>>>

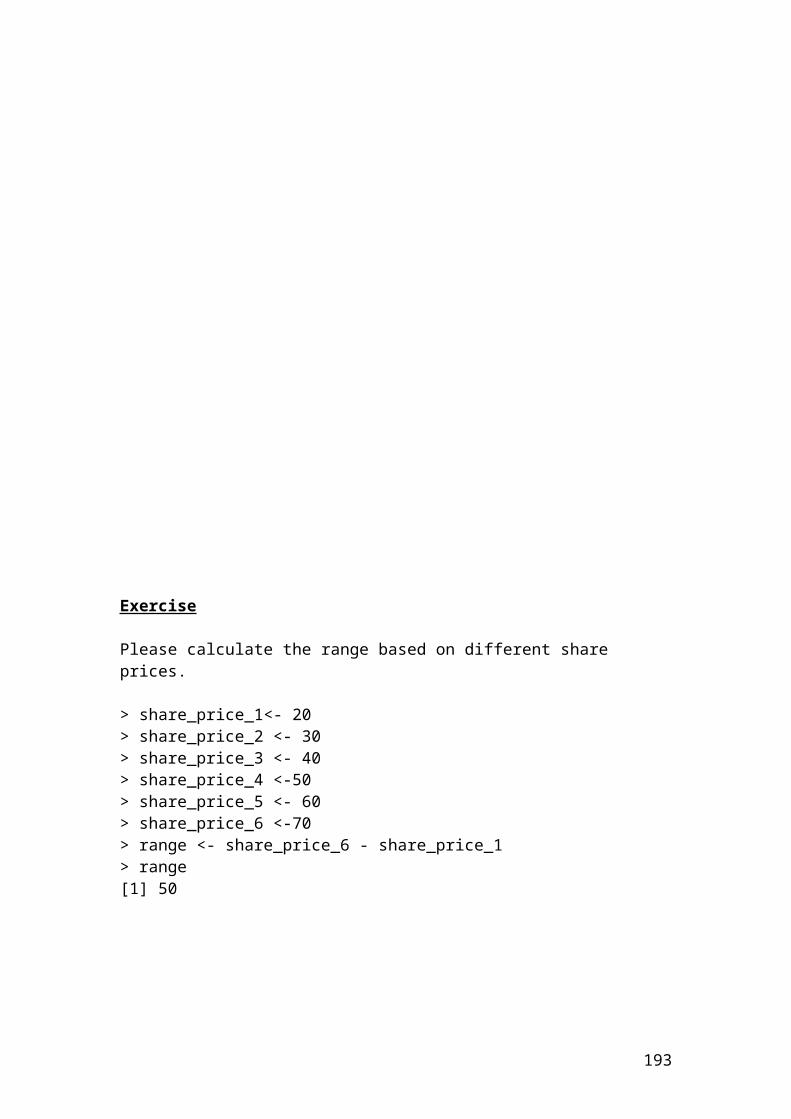

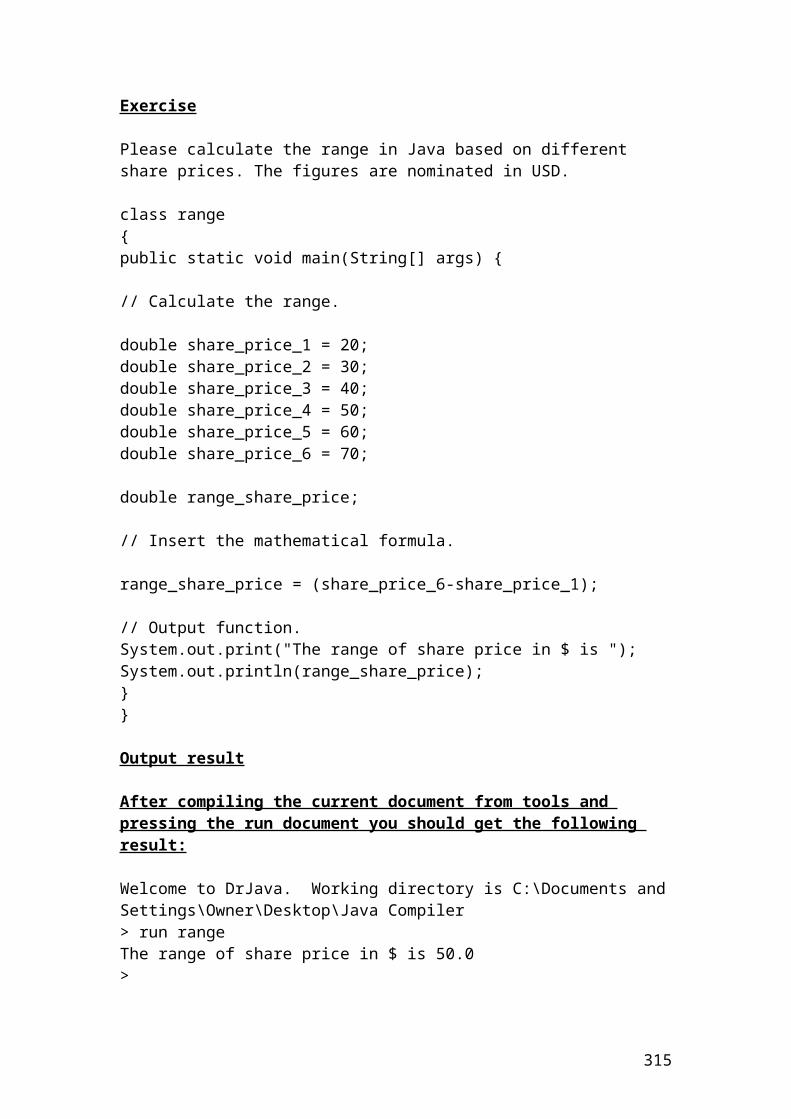

Exercise

Please calculate the range based on different share prices.

>>> share_price1= 20>>> share_price2 = 30>>> share_price3 = 40>>> share_price4 = 50>>> share_price5 = 60>>> share_price6 = 70>>> range = share_price6 - share_price1>>> range50

17

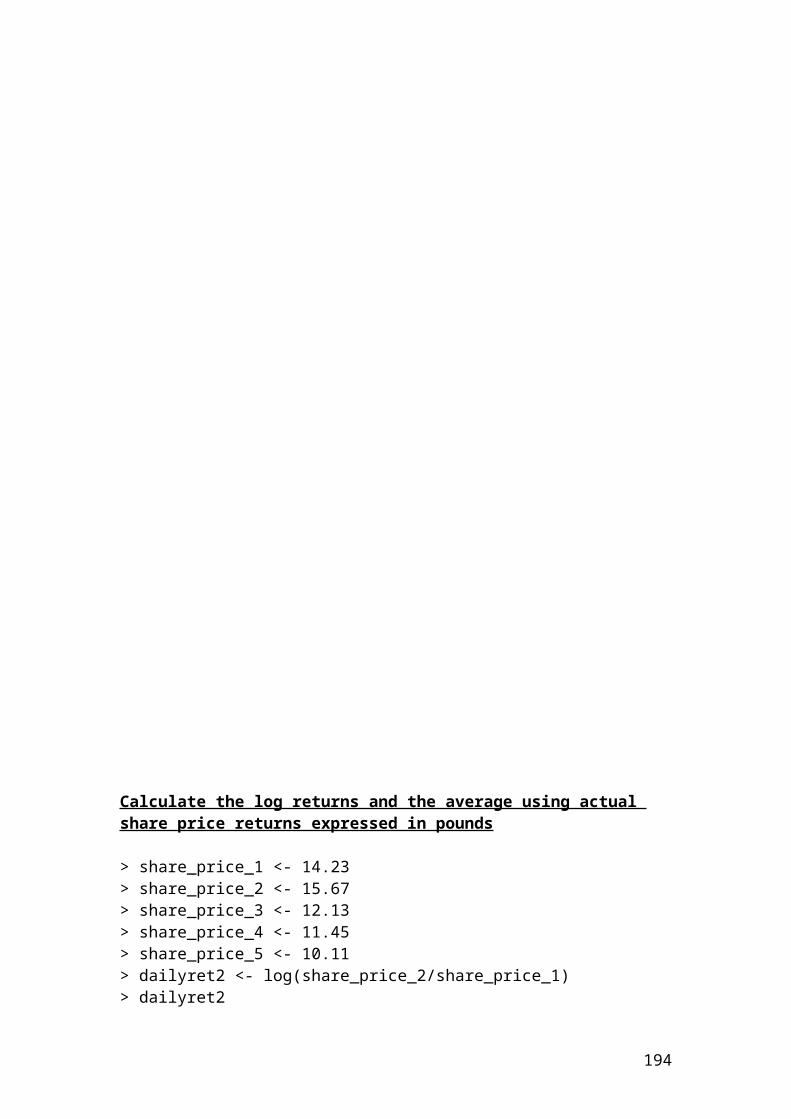

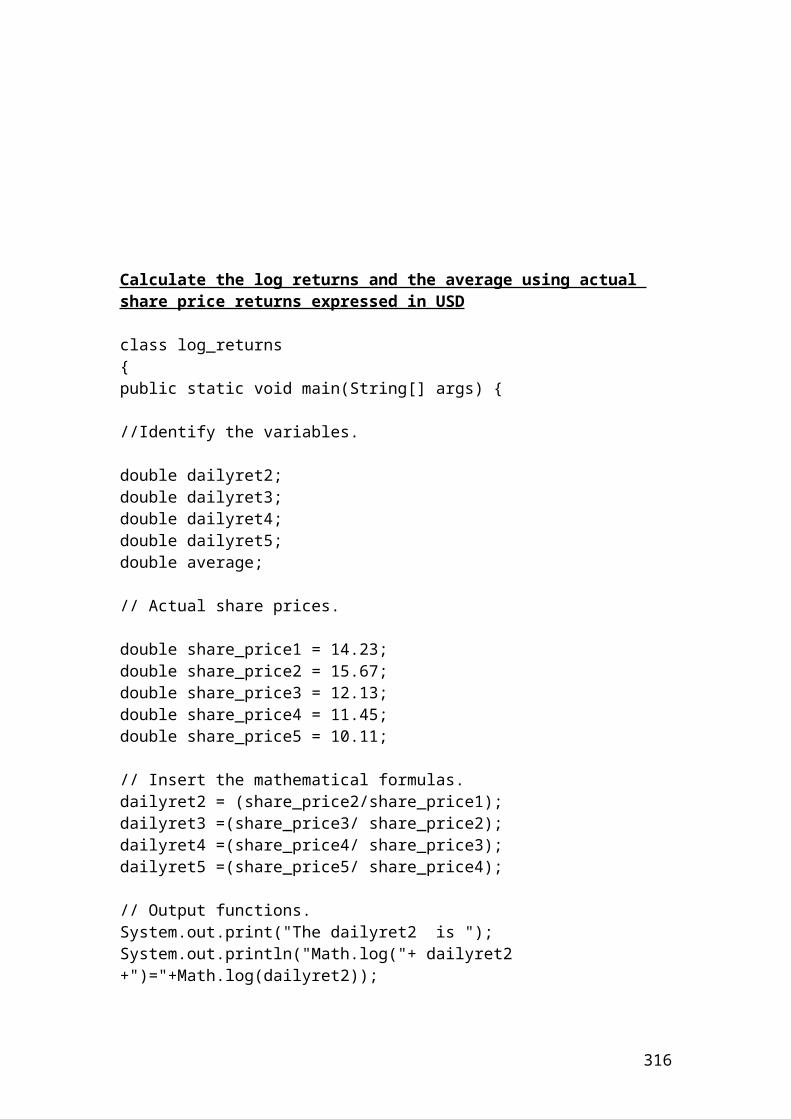

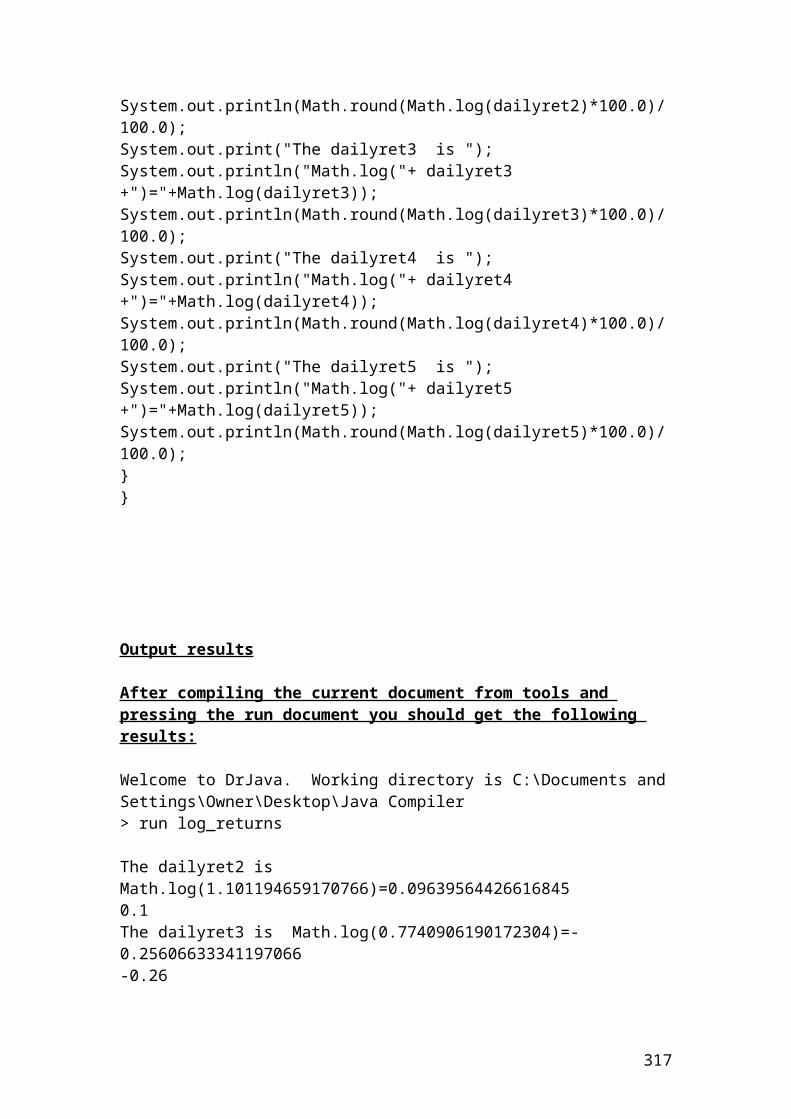

Calculate the log returns and the average using actual share price returns expressed in pounds

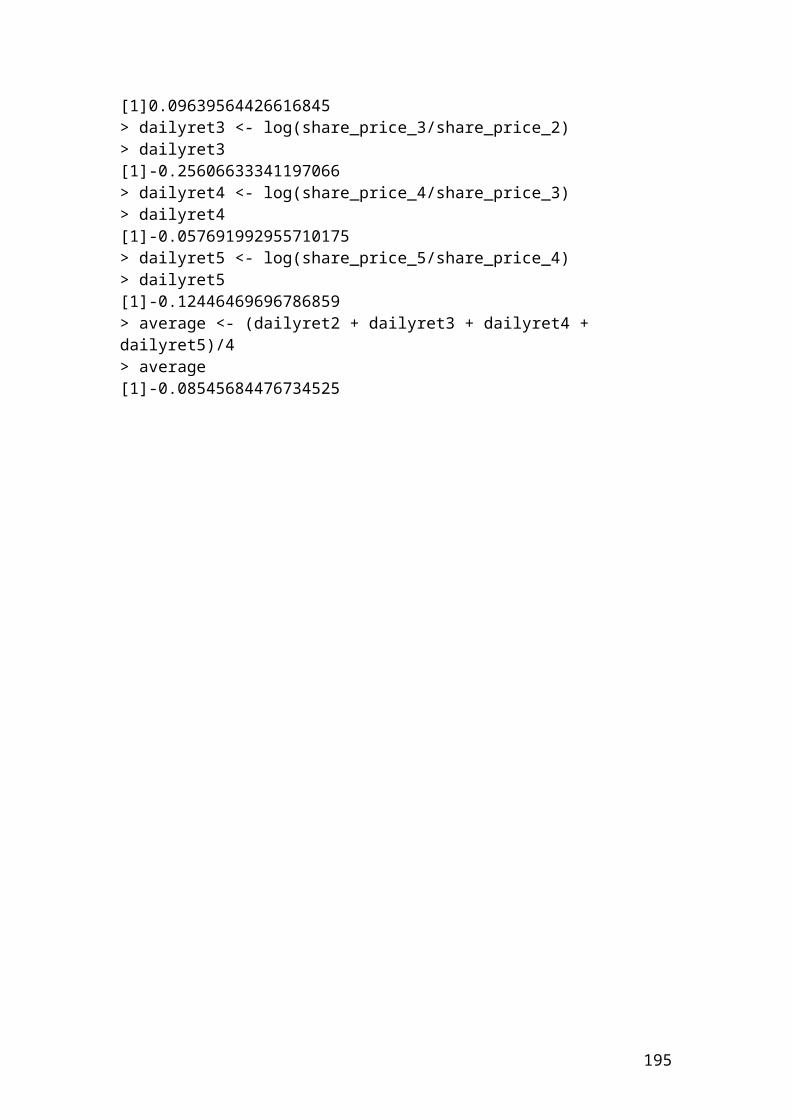

>>> from math import*>>> share_price1 = 14.23>>> share_price2 = 15.67>>> share_price3 = 12.13>>> share_price4 = 11.45>>> share_price5 = 10.11>>> dailyret2 = log(share_price2/share_price1)>>> dailyret20.09639564426616845>>> dailyret3 = log(share_price3/share_price2)>>> dailyret3-0.25606633341197066>>> dailyret4 = log(share_price4/share_price3)>>> dailyret4-0.057691992955710175>>> dailyret5 = log(share_price5/share_price4)>>> dailyret5-0.12446469696786859>>> average = (dailyret2 + dailyret3 + dailyret4 + dailyret5)/4>>> average-0.08545684476734525>>> round(_,2)-0.09>>>

Calculation of the median, the variance and the sample standard deviation of share prices percentage returns

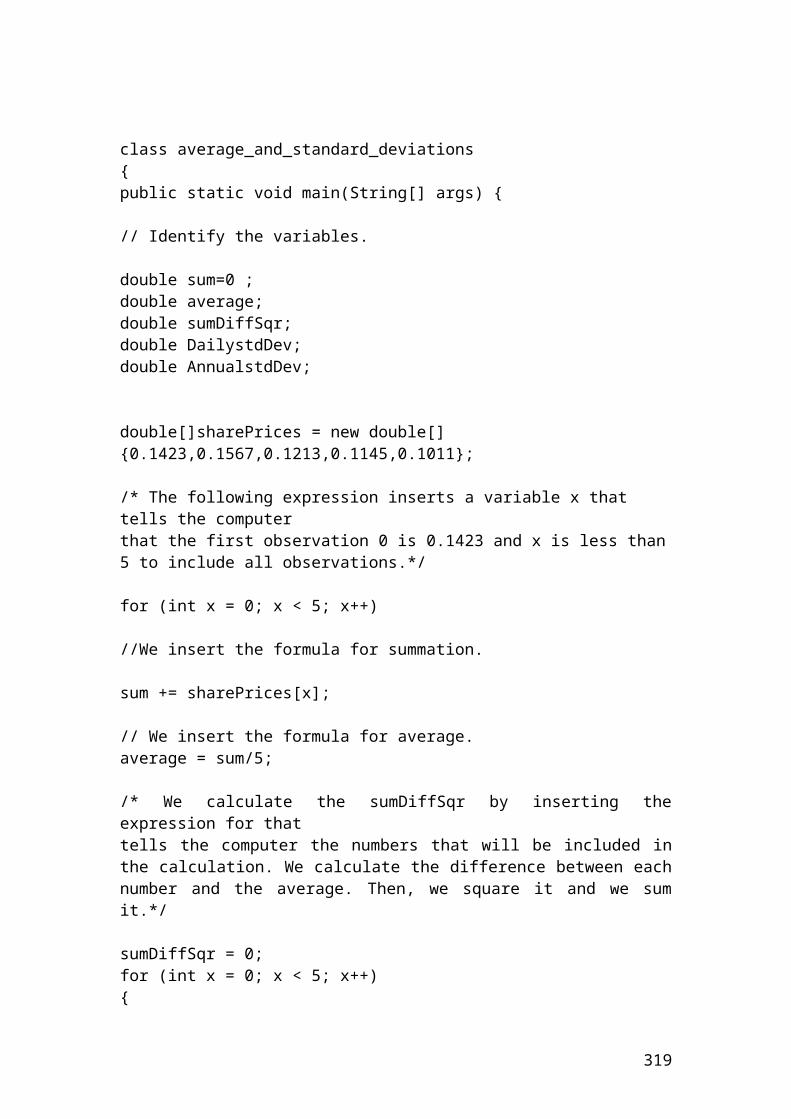

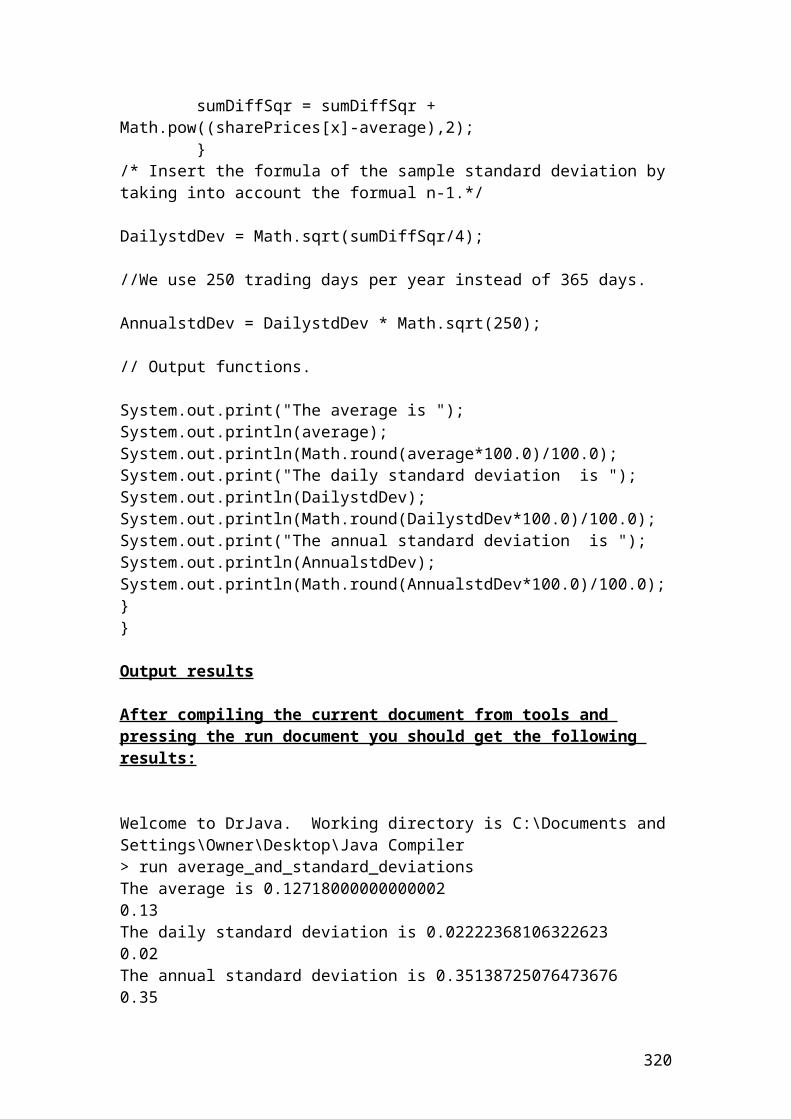

>>> from statistics import*share_prices = [0.1011, 0.1145, 0.1213, 0.1423, 0.1567]>>> median(share_prices)0.1213>>> variance(share_prices)0.0004938920000000002>>> stdev(share_prices)0.022223681063226232>>> round(_,2)0.02

18

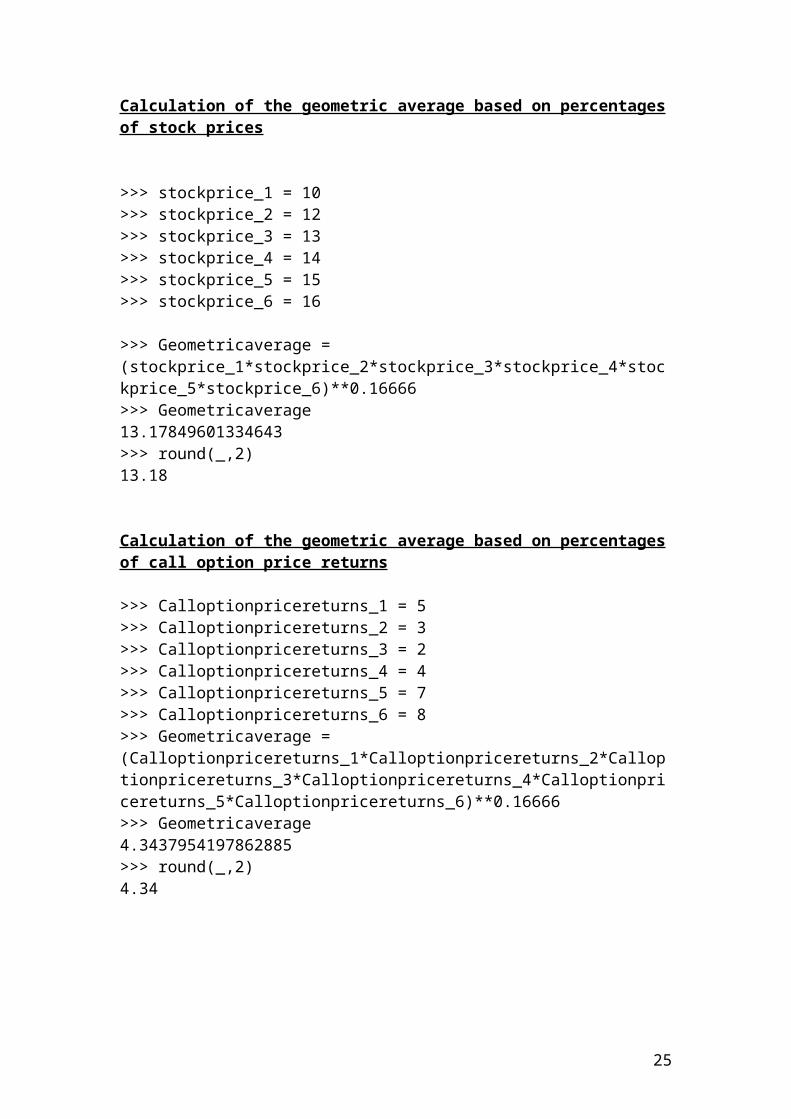

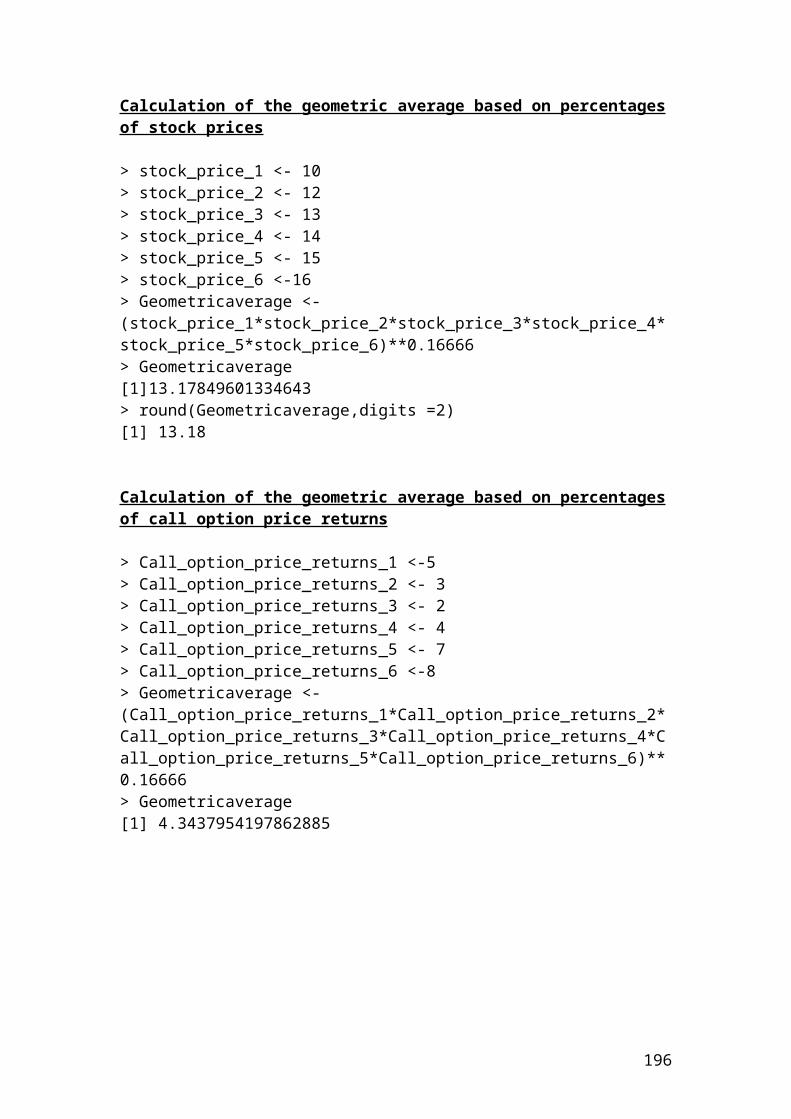

Calculation of the geometric average based on percentages of stock prices

>>> stockprice_1 = 10>>> stockprice_2 = 12>>> stockprice_3 = 13>>> stockprice_4 = 14>>> stockprice_5 = 15>>> stockprice_6 = 16

>>> Geometricaverage = (stockprice_1*stockprice_2*stockprice_3*stockprice_4*stockprice_5*stockprice_6)**0.16666>>> Geometricaverage13.17849601334643>>> round(_,2)13.18

Calculation of the geometric average based on percentages of call option price returns

>>> Calloptionpricereturns_1 = 5>>> Calloptionpricereturns_2 = 3>>> Calloptionpricereturns_3 = 2>>> Calloptionpricereturns_4 = 4>>> Calloptionpricereturns_5 = 7>>> Calloptionpricereturns_6 = 8>>> Geometricaverage = (Calloptionpricereturns_1*Calloptionpricereturns_2*Calloptionpricereturns_3*Calloptionpricereturns_4*Calloptionpricereturns_5*Calloptionpricereturns_6)**0.16666>>> Geometricaverage4.3437954197862885>>> round(_,2)4.34

19

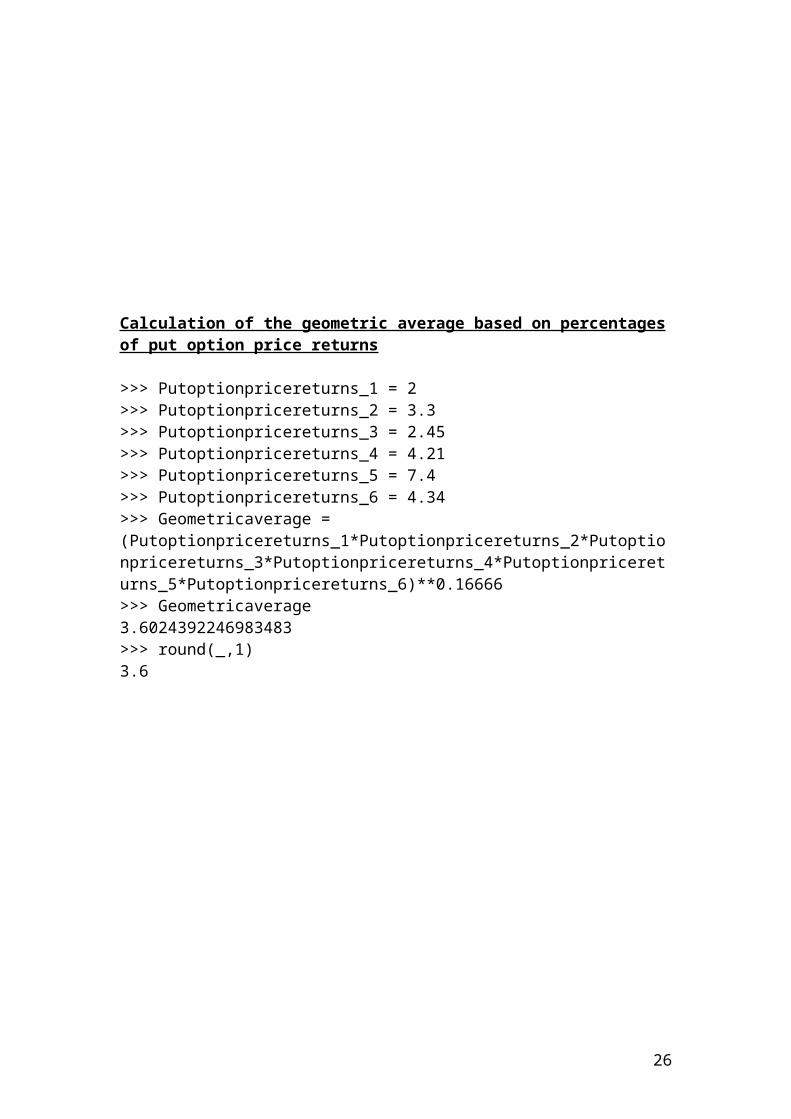

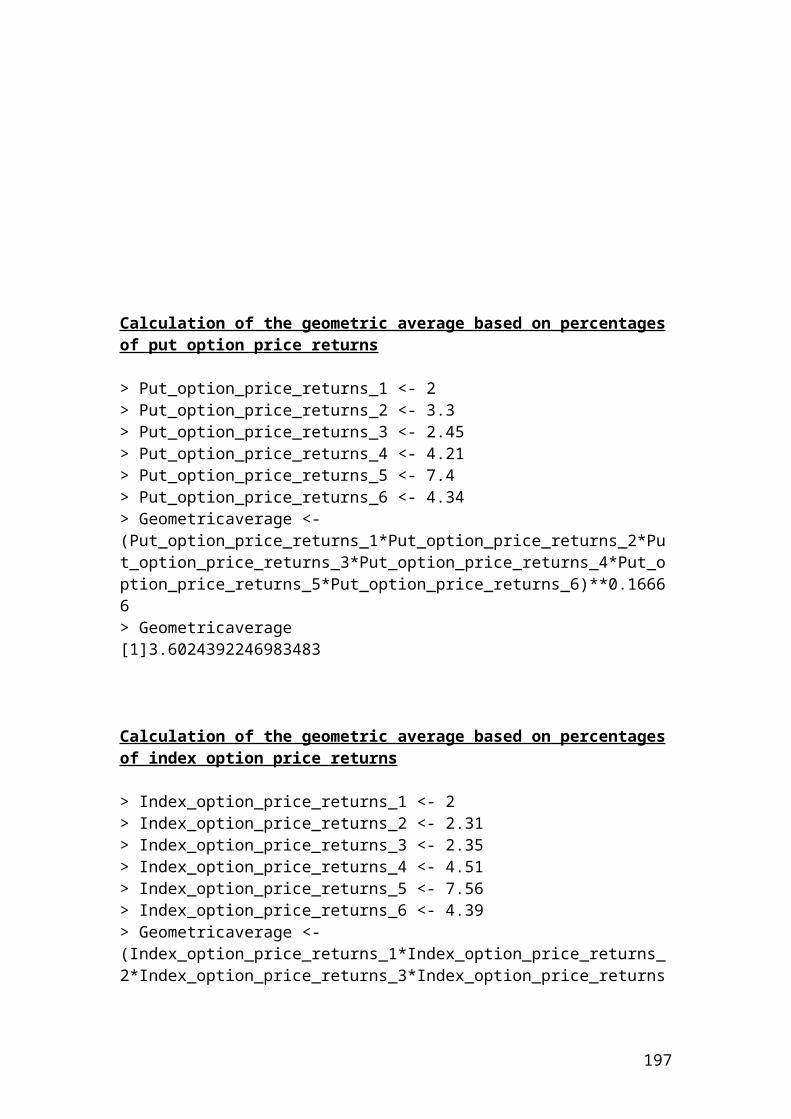

Calculation of the geometric average based on percentages of put option price returns

>>> Putoptionpricereturns_1 = 2>>> Putoptionpricereturns_2 = 3.3>>> Putoptionpricereturns_3 = 2.45>>> Putoptionpricereturns_4 = 4.21>>> Putoptionpricereturns_5 = 7.4>>> Putoptionpricereturns_6 = 4.34>>> Geometricaverage = (Putoptionpricereturns_1*Putoptionpricereturns_2*Putoptionpricereturns_3*Putoptionpricereturns_4*Putoptionpricereturns_5*Putoptionpricereturns_6)**0.16666>>> Geometricaverage3.6024392246983483>>> round(_,1)3.6

20

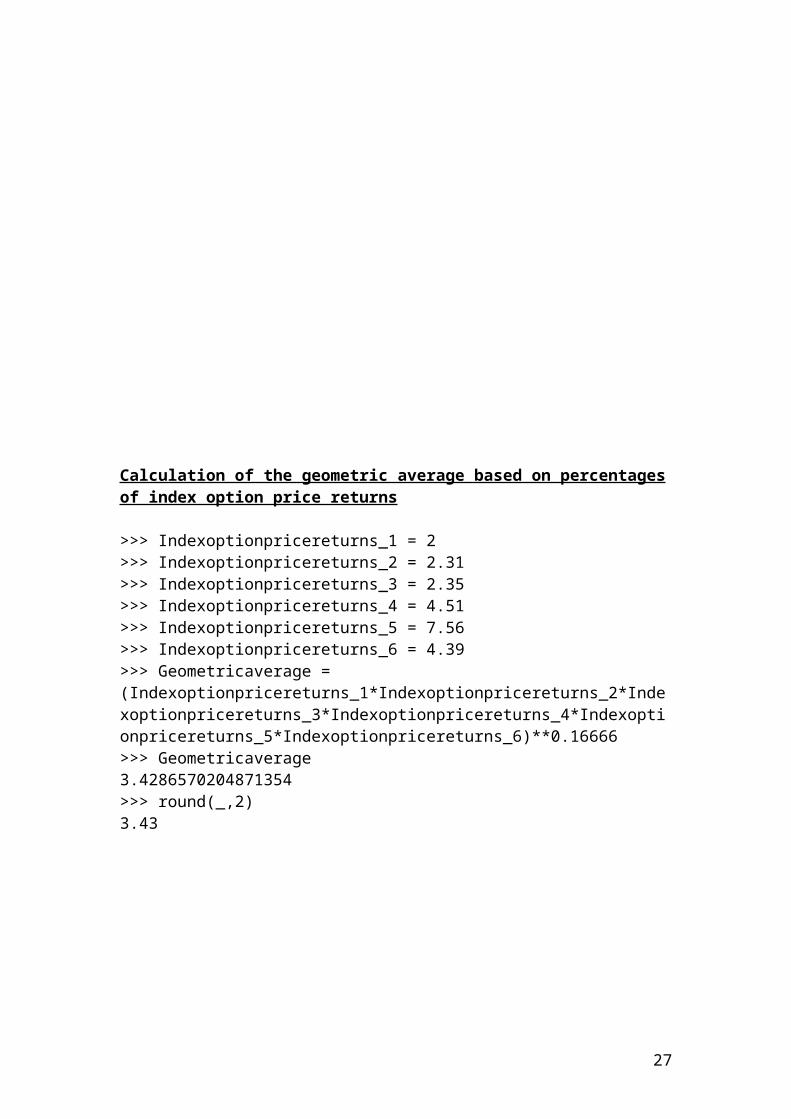

Calculation of the geometric average based on percentages of index option price returns

>>> Indexoptionpricereturns_1 = 2>>> Indexoptionpricereturns_2 = 2.31>>> Indexoptionpricereturns_3 = 2.35>>> Indexoptionpricereturns_4 = 4.51>>> Indexoptionpricereturns_5 = 7.56>>> Indexoptionpricereturns_6 = 4.39>>> Geometricaverage = (Indexoptionpricereturns_1*Indexoptionpricereturns_2*Indexoptionpricereturns_3*Indexoptionpricereturns_4*Indexoptionpricereturns_5*Indexoptionpricereturns_6)**0.16666>>> Geometricaverage3.4286570204871354>>> round(_,2)3.43

21

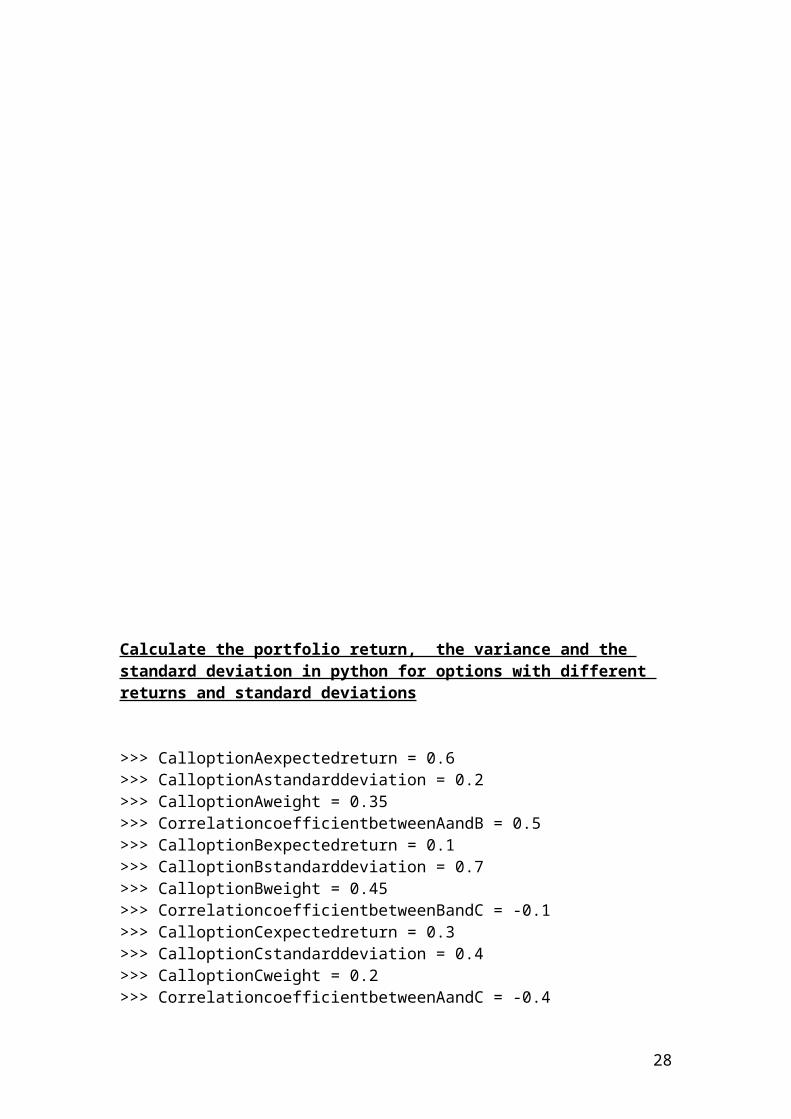

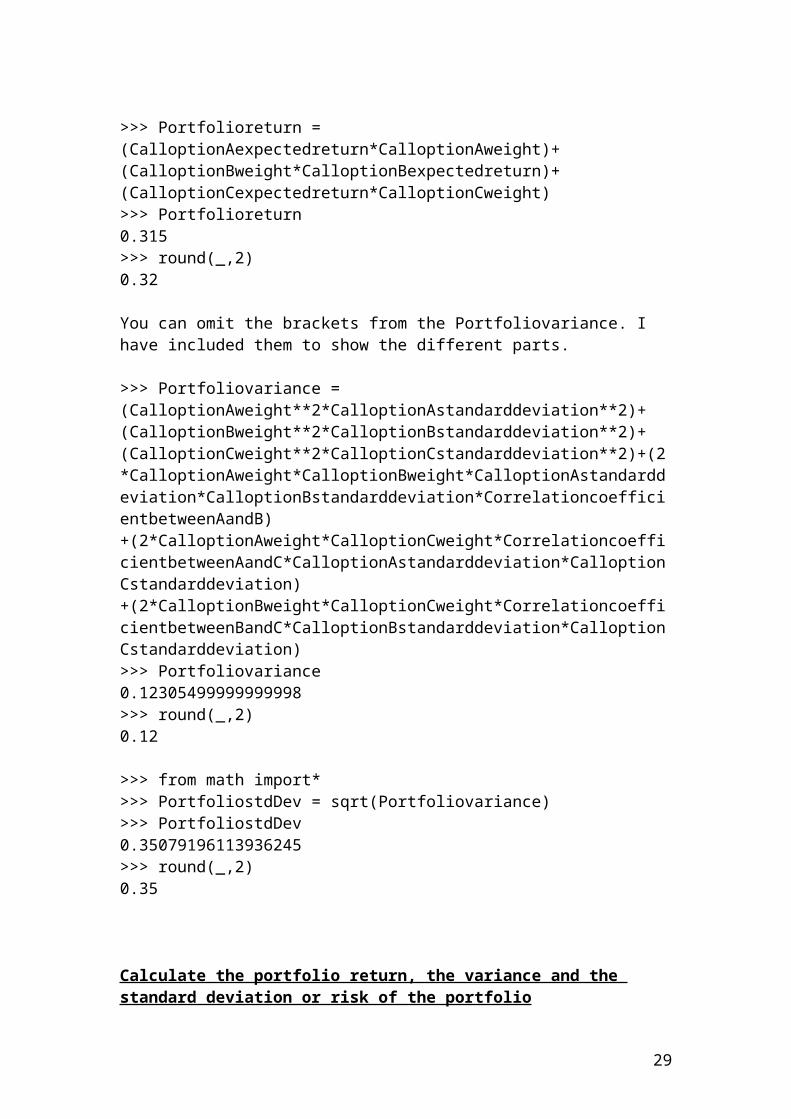

Calculate the portfolio return, the variance and the standard deviation in python for options with different returns and standard deviations

>>> CalloptionAexpectedreturn = 0.6>>> CalloptionAstandarddeviation = 0.2>>> CalloptionAweight = 0.35>>> CorrelationcoefficientbetweenAandB = 0.5>>> CalloptionBexpectedreturn = 0.1>>> CalloptionBstandarddeviation = 0.7>>> CalloptionBweight = 0.45>>> CorrelationcoefficientbetweenBandC = -0.1>>> CalloptionCexpectedreturn = 0.3>>> CalloptionCstandarddeviation = 0.4>>> CalloptionCweight = 0.2>>> CorrelationcoefficientbetweenAandC = -0.4

>>> Portfolioreturn = (CalloptionAexpectedreturn*CalloptionAweight)+(CalloptionBweight*CalloptionBexpectedreturn)+(CalloptionCexpectedreturn*CalloptionCweight)>>> Portfolioreturn0.315>>> round(_,2)0.32

You can omit the brackets from the Portfoliovariance. I have included them to show the different parts.

>>> Portfoliovariance = (CalloptionAweight**2*CalloptionAstandarddeviation**2)+ (CalloptionBweight**2*CalloptionBstandarddeviation**2)+(CalloptionCweight**2*CalloptionCstandarddeviation**2)+(2*CalloptionAweight*CalloptionBweight*CalloptionAstandarddeviation*CalloptionBstandarddeviation*CorrelationcoefficientbetweenAandB)+(2*CalloptionAweight*CalloptionCweight*CorrelationcoefficientbetweenAandC*CalloptionAstandarddeviation*CalloptionCstandarddeviation)+(2*CalloptionBweight*CalloptionCweight*CorrelationcoefficientbetweenBandC*CalloptionBstandarddeviation*CalloptionCstandarddeviation)>>> Portfoliovariance0.12305499999999998>>> round(_,2)0.12

>>> from math import*>>> PortfoliostdDev = sqrt(Portfoliovariance)>>> PortfoliostdDev0.35079196113936245>>> round(_,2)0.35

22

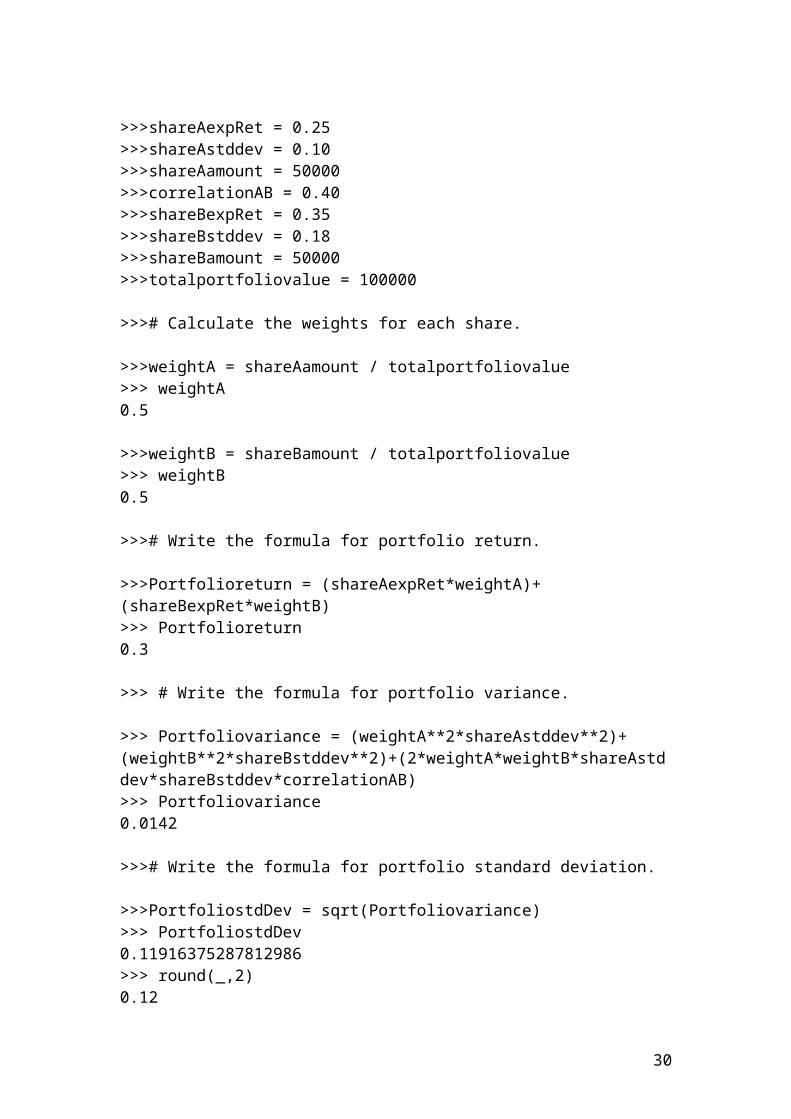

Calculate the portfolio return, the variance and the standard deviation or risk of the portfolio

>>>shareAexpRet = 0.25>>>shareAstddev = 0.10>>>shareAamount = 50000>>>correlationAB = 0.40>>>shareBexpRet = 0.35>>>shareBstddev = 0.18>>>shareBamount = 50000>>>totalportfoliovalue = 100000

>>># Calculate the weights for each share.

>>>weightA = shareAamount / totalportfoliovalue>>> weightA0.5

>>>weightB = shareBamount / totalportfoliovalue>>> weightB0.5

>>># Write the formula for portfolio return.

>>>Portfolioreturn = (shareAexpRet*weightA)+(shareBexpRet*weightB)>>> Portfolioreturn0.3

>>> # Write the formula for portfolio variance.

>>> Portfoliovariance = (weightA**2*shareAstddev**2)+(weightB**2*shareBstddev**2)+(2*weightA*weightB*shareAstddev*shareBstddev*correlationAB)>>> Portfoliovariance0.0142

>>># Write the formula for portfolio standard deviation.

>>>PortfoliostdDev = sqrt(Portfoliovariance)>>> PortfoliostdDev0.11916375287812986>>> round(_,2)0.12

23

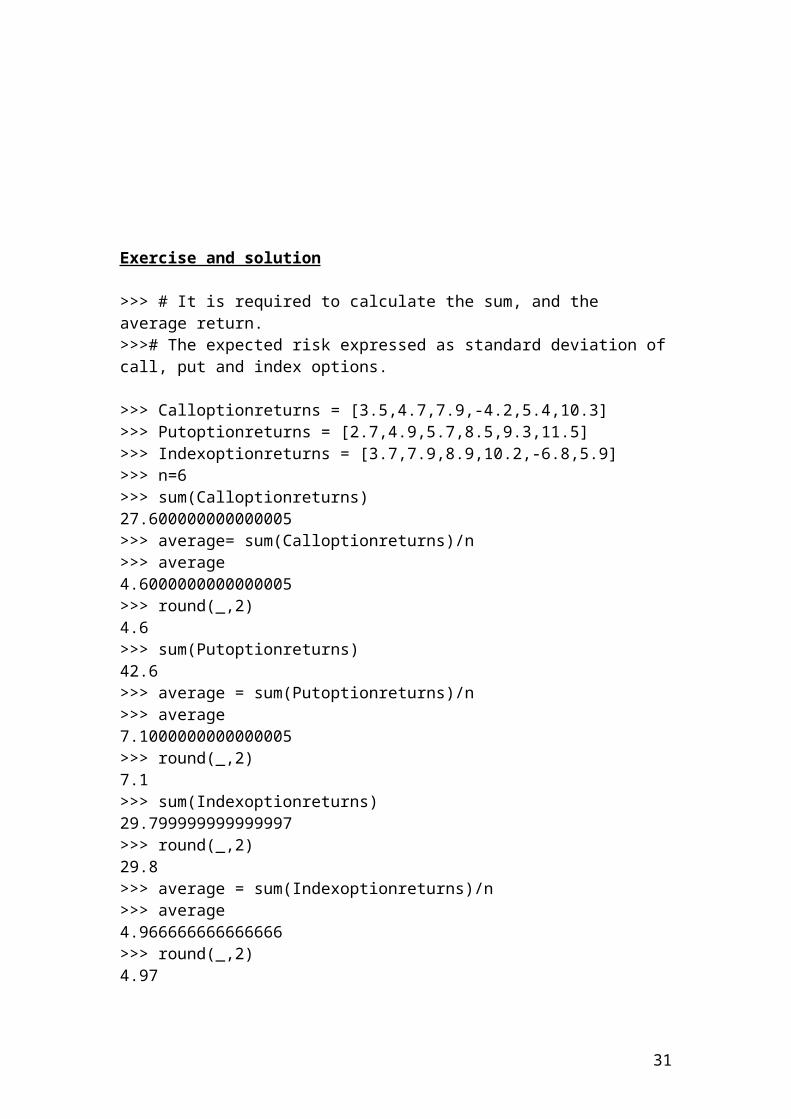

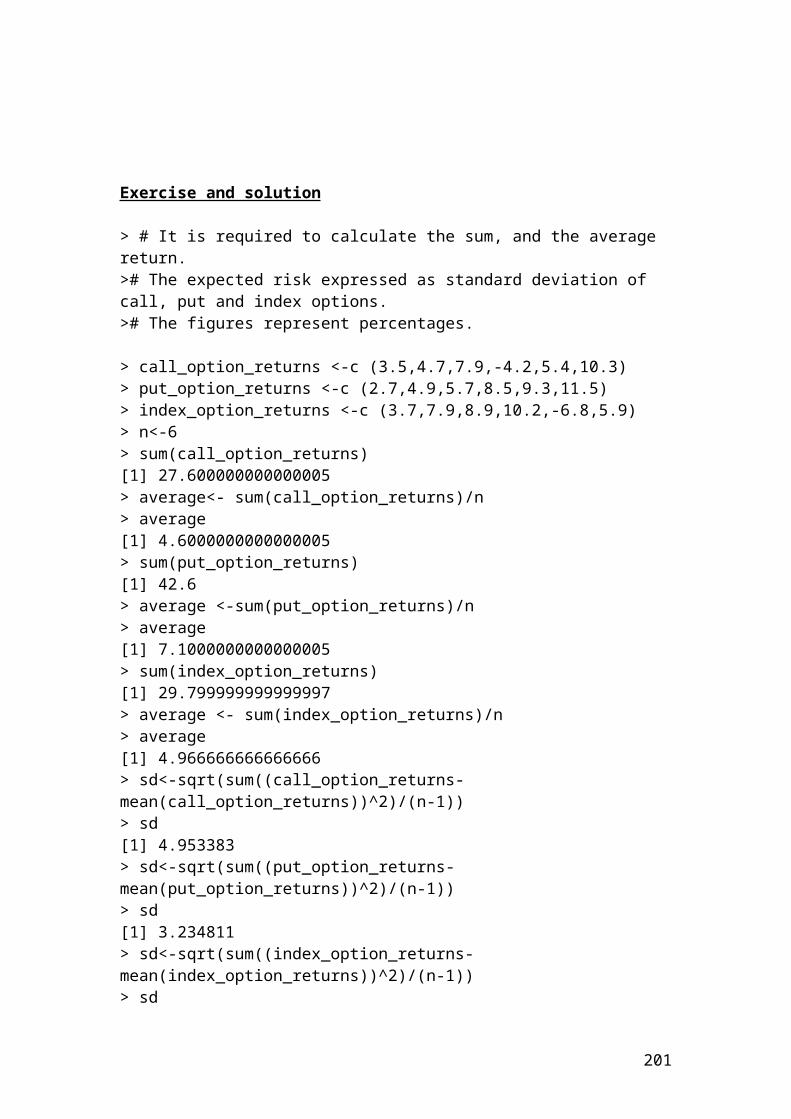

Exercise and solution

>>> # It is required to calculate the sum, and the average return.>>># The expected risk expressed as standard deviation of call, put and index options.

>>> Calloptionreturns = [3.5,4.7,7.9,-4.2,5.4,10.3]>>> Putoptionreturns = [2.7,4.9,5.7,8.5,9.3,11.5]>>> Indexoptionreturns = [3.7,7.9,8.9,10.2,-6.8,5.9]>>> n=6>>> sum(Calloptionreturns)27.600000000000005>>> average= sum(Calloptionreturns)/n>>> average4.6000000000000005>>> round(_,2)4.6>>> sum(Putoptionreturns)42.6>>> average = sum(Putoptionreturns)/n>>> average7.1000000000000005>>> round(_,2)7.1>>> sum(Indexoptionreturns)29.799999999999997>>> round(_,2)29.8>>> average = sum(Indexoptionreturns)/n>>> average4.966666666666666>>> round(_,2)4.97

>>> from statistics import stdev>>> stdev(Calloptionreturns)4.953382682571578>>> round(_,2)4.95>>> stdev(Putoptionreturns)3.234810659064917>>> round(_,2)3.23>>> stdev(Indexoptionreturns)6.203117495797308>>> round(_,2)6.2

24

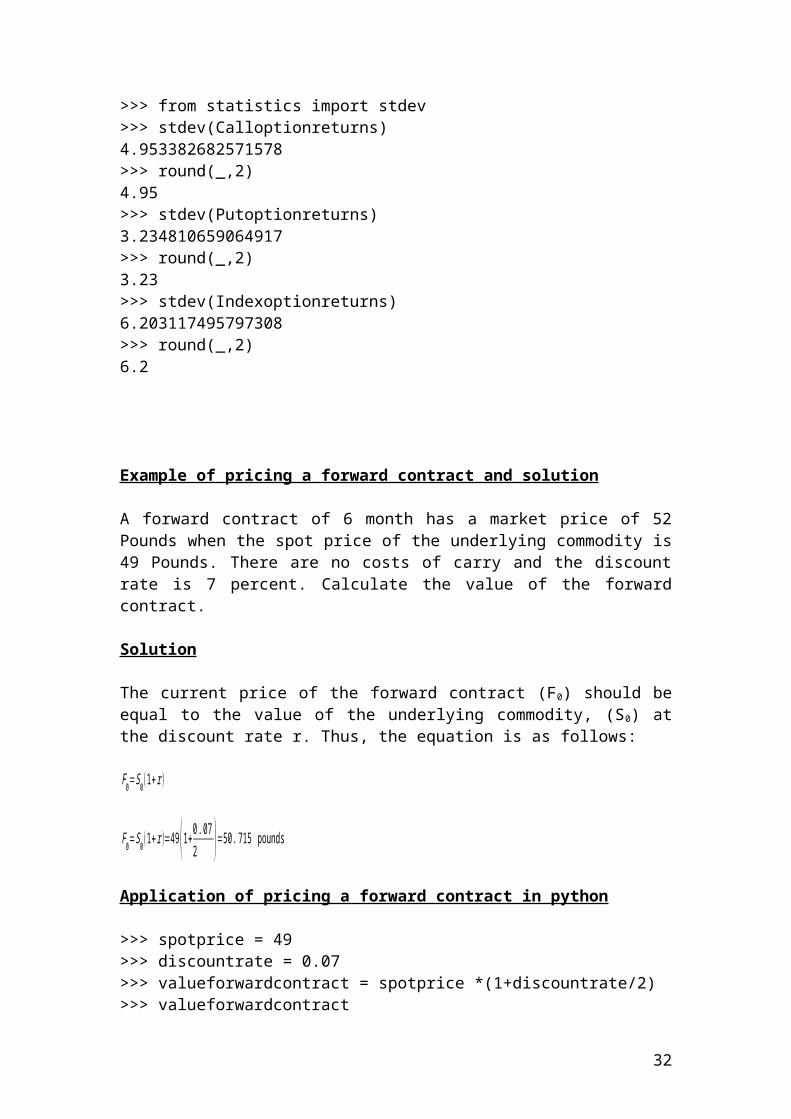

Example of pricing a forward contract and solution

A forward contract of 6 month has a market price of 52 Pounds when the spot price of the underlying commodity is 49 Pounds. There are no costs of carry and the discount rate is 7 percent. Calculate the value of the forward contract.

Solution

The current price of the forward contract (F0) should be equal to the value of the underlying commodity, (S0) at the discount rate r. Thus, the equation is as follows:

F0=S0(1+r )

F0=S0(1+r )=49(1+0 . 072 )=50 . 715 pounds

Application of pricing a forward contract in python

>>> spotprice = 49>>> discountrate = 0.07>>> valueforwardcontract = spotprice *(1+discountrate/2)>>> valueforwardcontract50.714999999999996>>> round(_,2)50.71 # Pounds

25

Example of interest rate payment and solution

A trader wants to calculate the interest amount that he / she will receive in three months from a forward contract of a Euribor deposit paying a Euro deposit rate of 3.55%. The principal amount is 300,000

The mathematical formula is as follows:

Interest payment = principal x [interest rate x (tdays / 360)]

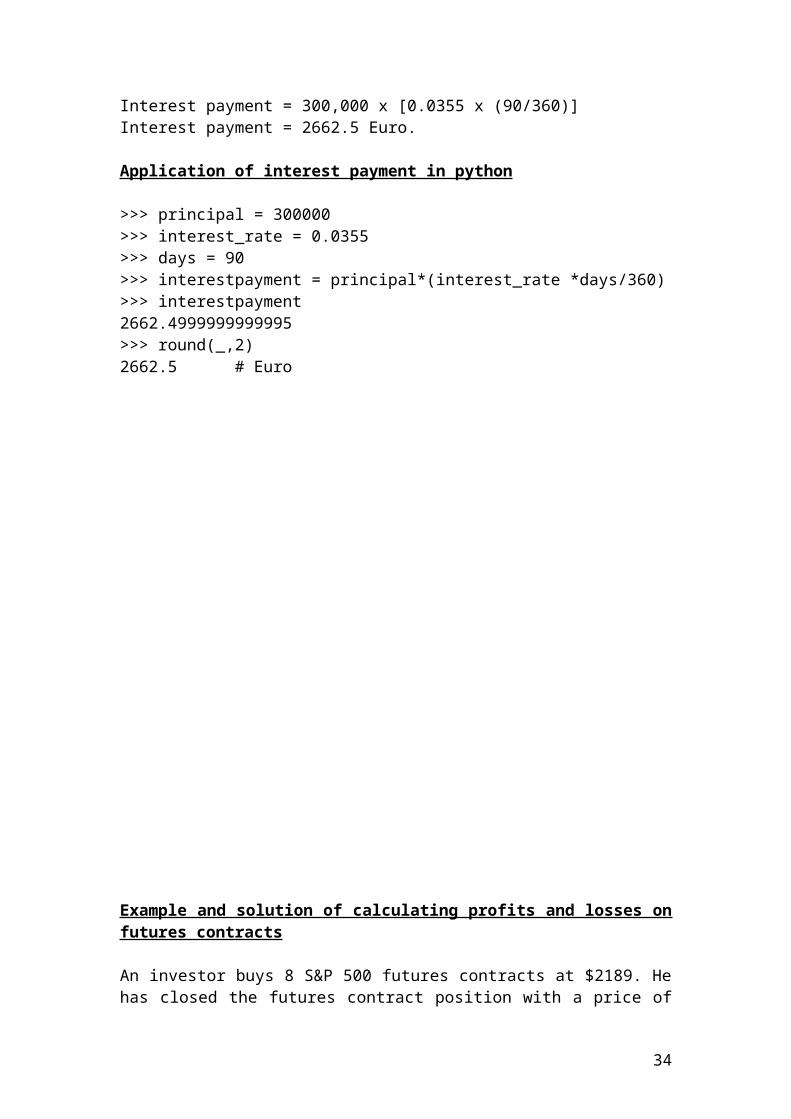

Interest payment = 300,000 x [0.0355 x (90/360)]Interest payment = 2662.5 Euro.

Application of interest payment in python

>>> principal = 300000>>> interest_rate = 0.0355>>> days = 90>>> interestpayment = principal*(interest_rate *days/360)>>> interestpayment2662.4999999999995>>> round(_,2)2662.5 # Euro

26

Example and solution of calculating profits and losses on futures contracts

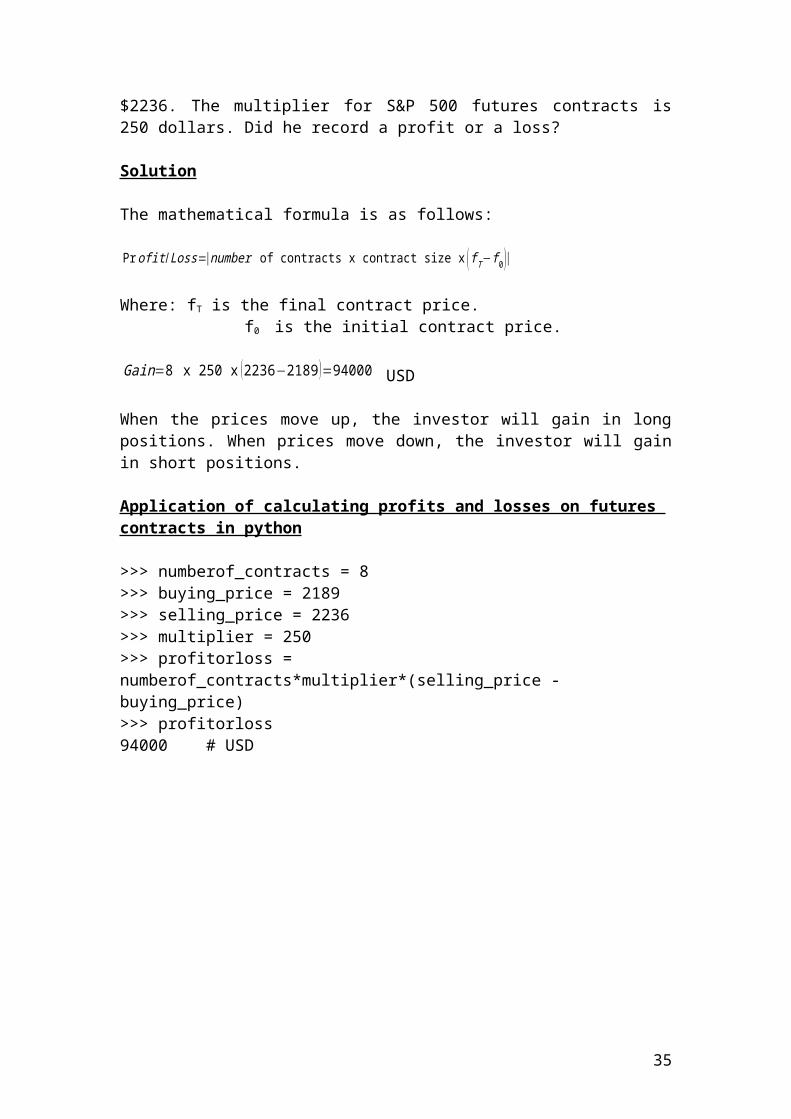

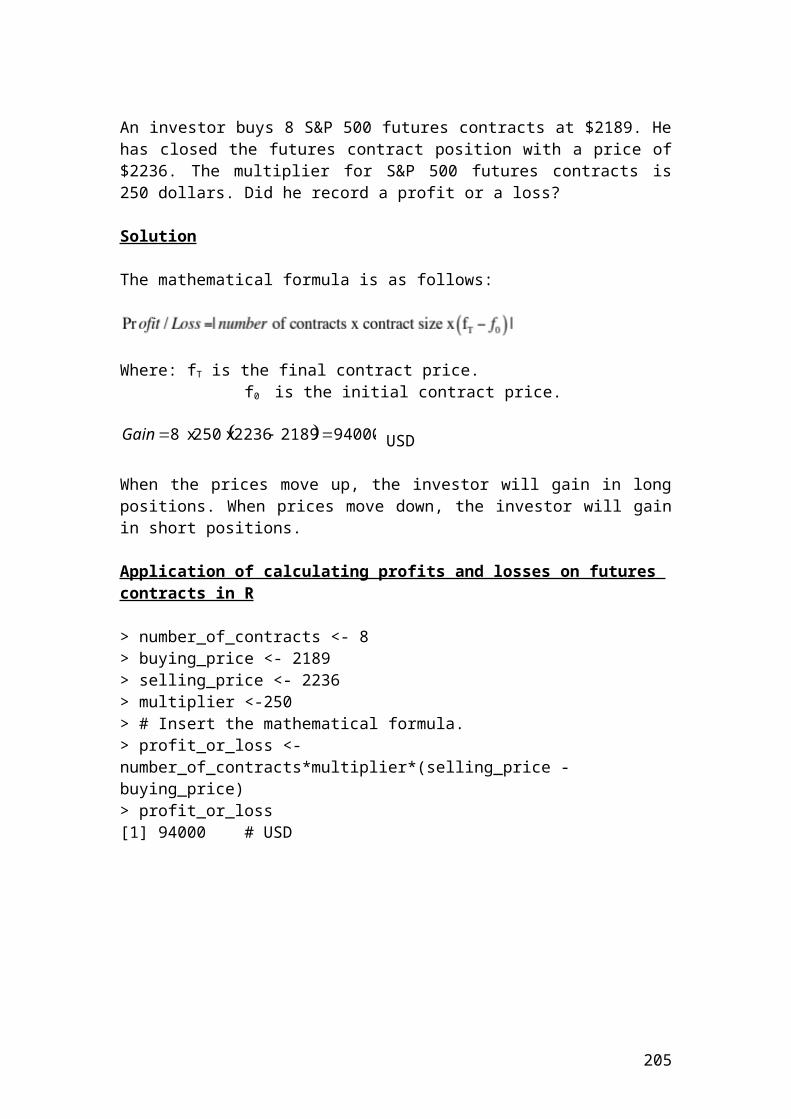

An investor buys 8 S&P 500 futures contracts at $2189. He has closed the futures contract position with a price of $2236. The multiplier for S&P 500 futures contracts is 250 dollars. Did he record a profit or a loss?

Solution

The mathematical formula is as follows:

Pr ofit /Loss=|number of contracts x contract size x ( f T− f 0 )|

Where: fT is the final contract price. f0 is the initial contract price.

Gain=8 x 250 x (2236−2189 )=94000 USD

When the prices move up, the investor will gain in long positions. When prices move down, the investor will gain in short positions.

Application of calculating profits and losses on futures contracts in python

>>> numberof_contracts = 8>>> buying_price = 2189>>> selling_price = 2236>>> multiplier = 250>>> profitorloss = numberof_contracts*multiplier*(selling_price - buying_price)>>> profitorloss94000 # USD

27

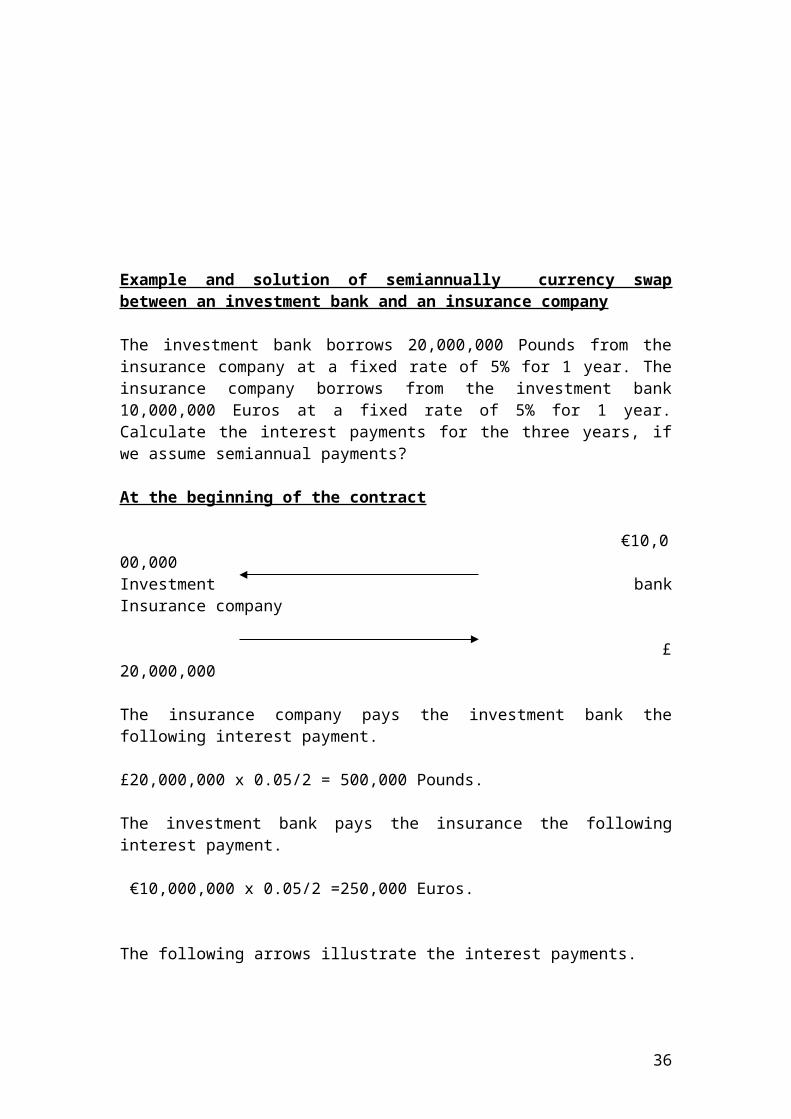

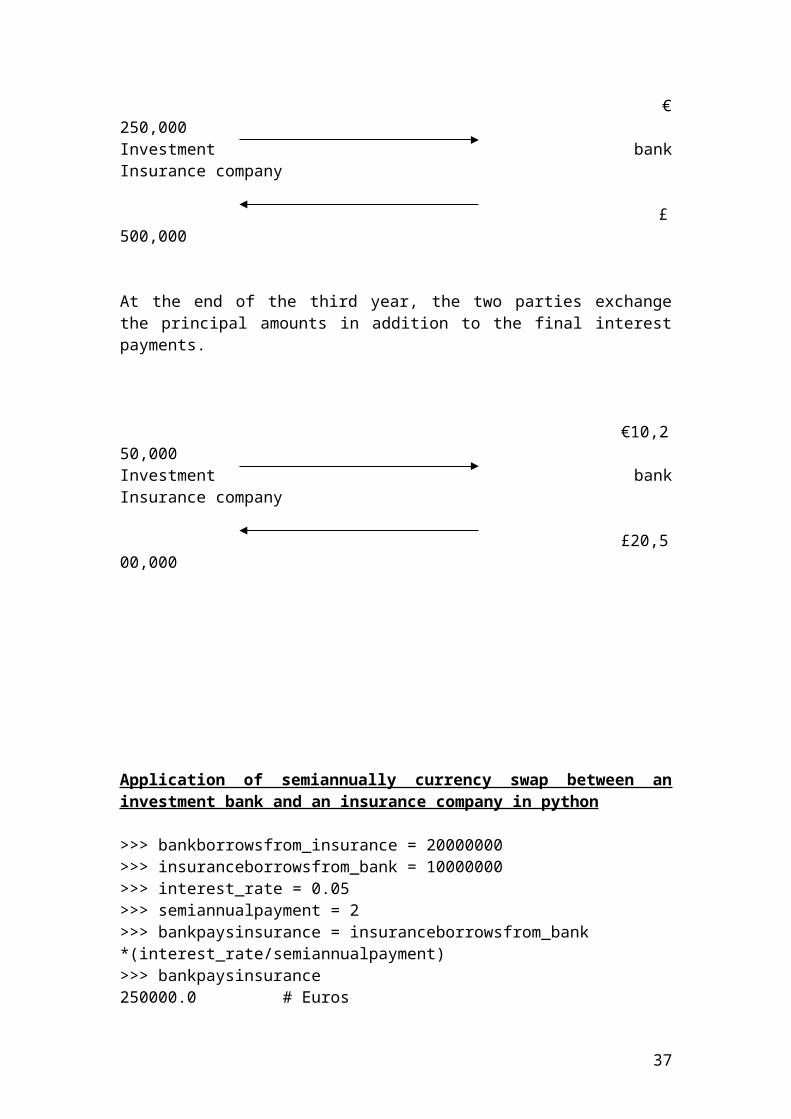

Example and solution of semiannually currency swap between an investment bank and an insurance company

The investment bank borrows 20,000,000 Pounds from the insurance company at a fixed rate of 5% for 1 year. The insurance company borrows from the investment bank 10,000,000 Euros at a fixed rate of 5% for 1 year. Calculate the interest payments for the three years, if we assume semiannual payments?

At the beginning of the contract

€10,000,000Investment bank Insurance company

£ 20,000,000

The insurance company pays the investment bank the following interest payment.

£20,000,000 x 0.05/2 = 500,000 Pounds.

The investment bank pays the insurance the following interest payment.

€10,000,000 x 0.05/2 =250,000 Euros.

The following arrows illustrate the interest payments.

€ 250,000Investment bank Insurance company

£ 500,000

At the end of the third year, the two parties exchange the principal amounts in addition to the final interest payments.

€10,250,000Investment bank Insurance company

£20,500,000

28

Application of semiannually currency swap between an investment bank and an insurance company in python

>>> bankborrowsfrom_insurance = 20000000>>> insuranceborrowsfrom_bank = 10000000>>> interest_rate = 0.05>>> semiannualpayment = 2>>> bankpaysinsurance = insuranceborrowsfrom_bank *(interest_rate/semiannualpayment)>>> bankpaysinsurance250000.0 # Euros>>> insurancepaysbank = bankborrowsfrom_insurance *(interest_rate/semiannualpayment)>>> insurancepaysbank500000.0 # Pounds

29

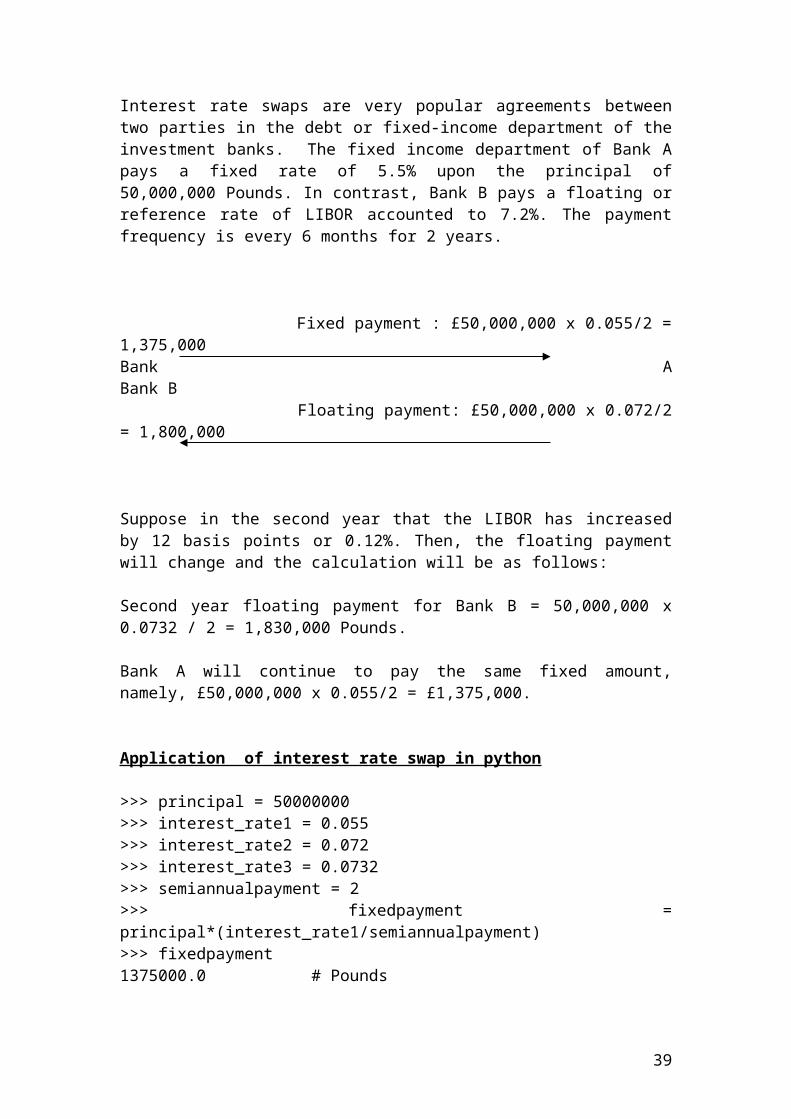

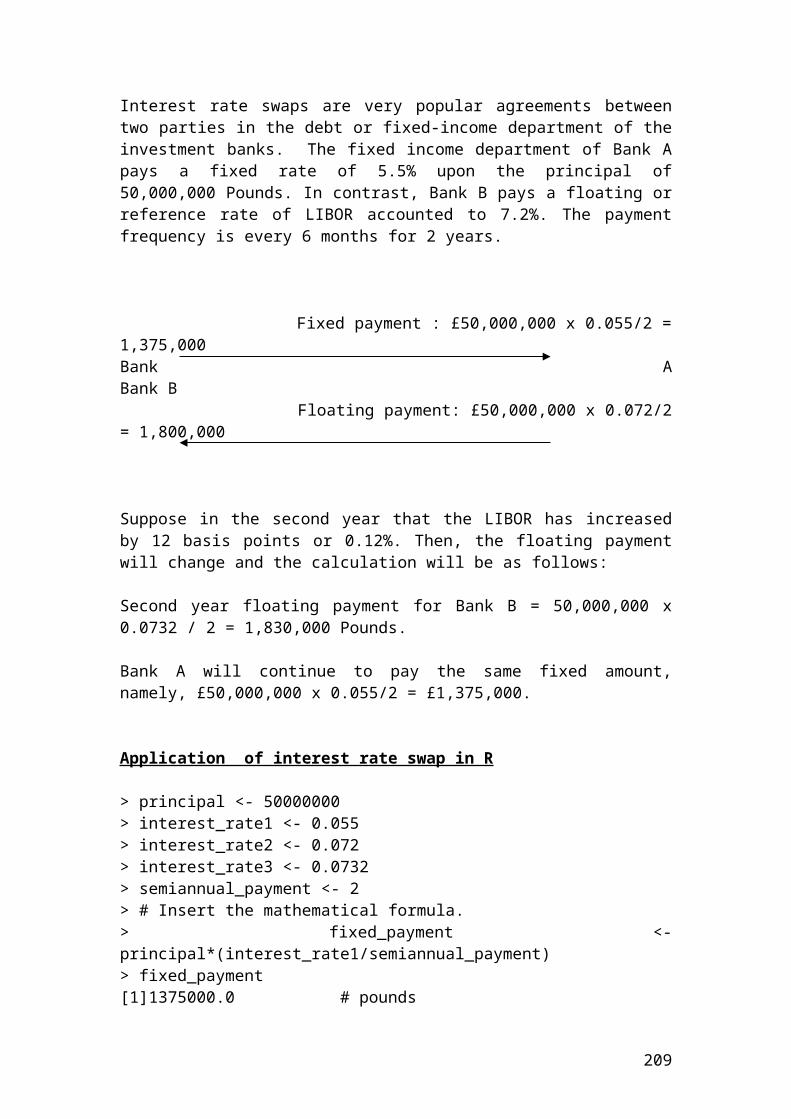

Example and solution of interest rate swap

Interest rate swaps are very popular agreements between two parties in the debt or fixed-income department of the investment banks. The fixed income department of Bank A pays a fixed rate of 5.5% upon the principal of 50,000,000 Pounds. In contrast, Bank B pays a floating or reference rate of LIBOR accounted to 7.2%. The payment frequency is every 6 months for 2 years.

Fixed payment : £50,000,000 x 0.055/2 = 1,375,000 Bank A Bank B Floating payment: £50,000,000 x 0.072/2 = 1,800,000

Suppose in the second year that the LIBOR has increased by 12 basis points or 0.12%. Then, the floating payment will change and the calculation will be as follows:

Second year floating payment for Bank B = 50,000,000 x 0.0732 / 2 = 1,830,000 Pounds.

Bank A will continue to pay the same fixed amount, namely, £50,000,000 x 0.055/2 = £1,375,000.

Application of interest rate swap in python

>>> principal = 50000000>>> interest_rate1 = 0.055>>> interest_rate2 = 0.072>>> interest_rate3 = 0.0732>>> semiannualpayment = 2>>> fixedpayment = principal*(interest_rate1/semiannualpayment)>>> fixedpayment1375000.0 # Pounds>>> floatingpayment1 = principal*(interest_rate2/semiannualpayment)>>> floatingpayment11799999.9999999998>>> round(_,2)1800000.0 # Pounds>>> floatingpayment2 = principal*(interest_rate3/semiannualpayment)>>> floatingpayment21830000.0 # Pounds

30

Delta – neutral hedge

Delta – neutral hedge is common used in risk management to keep the value of the portfolio neutral due to changes in the share price. It is achieved from a long position in a share and a short position in a call option. The mathematical formula to determine the number of options is as follows:

Delta - neutral hedge =Number of shares hedgeddelta of call option

Thus, if the investment bank has bought 30,000 shares of Vodafone and the delta of the call option of the same company is 0.50, then the numbers of call options that are needed to purchase to form a delta-neutral hedge are as follows:

Delta hedge = 30,000 / 0.50 = 60,000 options or 600 option contracts.

Application of delta- neutral hedge in python

>>> numberof_shares = 30000>>> deltaofcall_option = 0.50>>> deltaneutralhedge = numberof_shares/deltaofcall_option>>> deltaneutralhedge60000.0

31

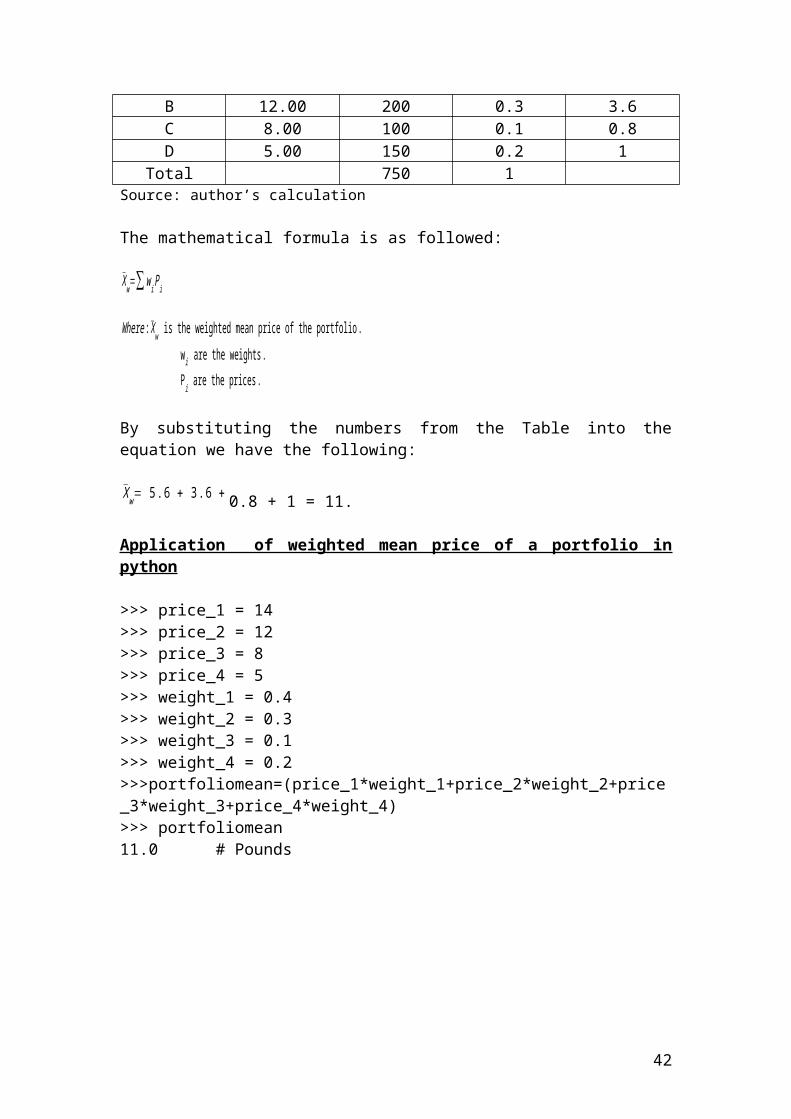

Weighted mean price of a portfolio

Let’s assume that we have a portfolio of four options with their market prices and the number of shares bought. It is required to calculate the weighted mean price of the portfolio.

Options Price expressed in $

Number of shares

Weight Weight x Price

A 14.00 300 0.4 5.6B 12.00 200 0.3 3.6C 8.00 100 0.1 0.8D 5.00 150 0.2 1

Total 750 1Source: author’s calculation

The mathematical formula is as followed:

X̄ w=∑ w i Pi

Where : X̄ w is the weighted mean price of the portfolio . w i are the weights . Pi are the prices .

By substituting the numbers from the Table into the equation we have the following:

X̄ w= 5 . 6 + 3. 6 + 0.8 + 1 = 11.

Application of weighted mean price of a portfolio in python

>>> price_1 = 14>>> price_2 = 12>>> price_3 = 8>>> price_4 = 5>>> weight_1 = 0.4>>> weight_2 = 0.3>>> weight_3 = 0.1>>> weight_4 = 0.2>>>portfoliomean=(price_1*weight_1+price_2*weight_2+price_3*weight_3+price_4*weight_4)>>> portfoliomean11.0 # Pounds

32

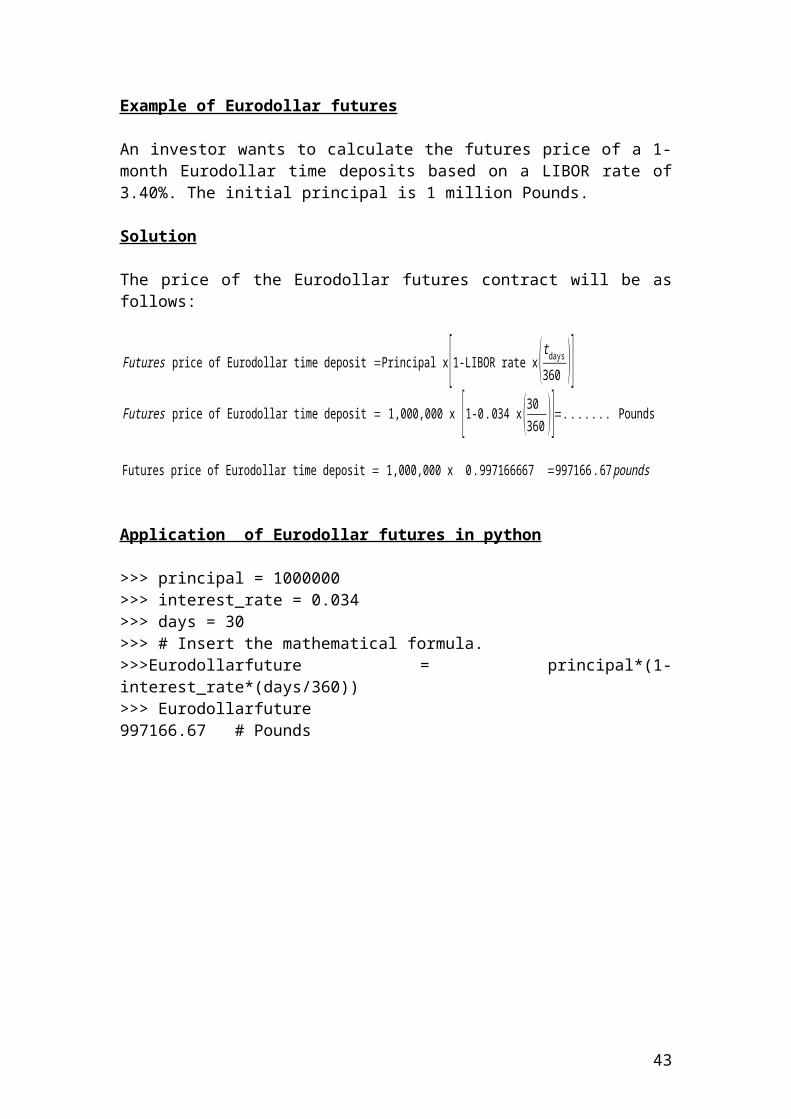

Example of Eurodollar futures

An investor wants to calculate the futures price of a 1-month Eurodollar time deposits based on a LIBOR rate of 3.40%. The initial principal is 1 million Pounds.

Solution

The price of the Eurodollar futures contract will be as follows:

Futures price of Eurodollar time deposit =Principal x[1-LIBOR rate x (tdays

360 )]

Futures price of Eurodollar time deposit = 1,000,000 x [1-0 . 034 x (30360 )]=. . .. .. . Pounds

Futures price of Eurodollar time deposit = 1,000,000 x 0 .997166667 =997166 .67 pounds

Application of Eurodollar futures in python

>>> principal = 1000000>>> interest_rate = 0.034>>> days = 30>>> # Insert the mathematical formula.>>>Eurodollarfuture = principal*(1- interest_rate*(days/360))>>> Eurodollarfuture997166.67 # Pounds

33

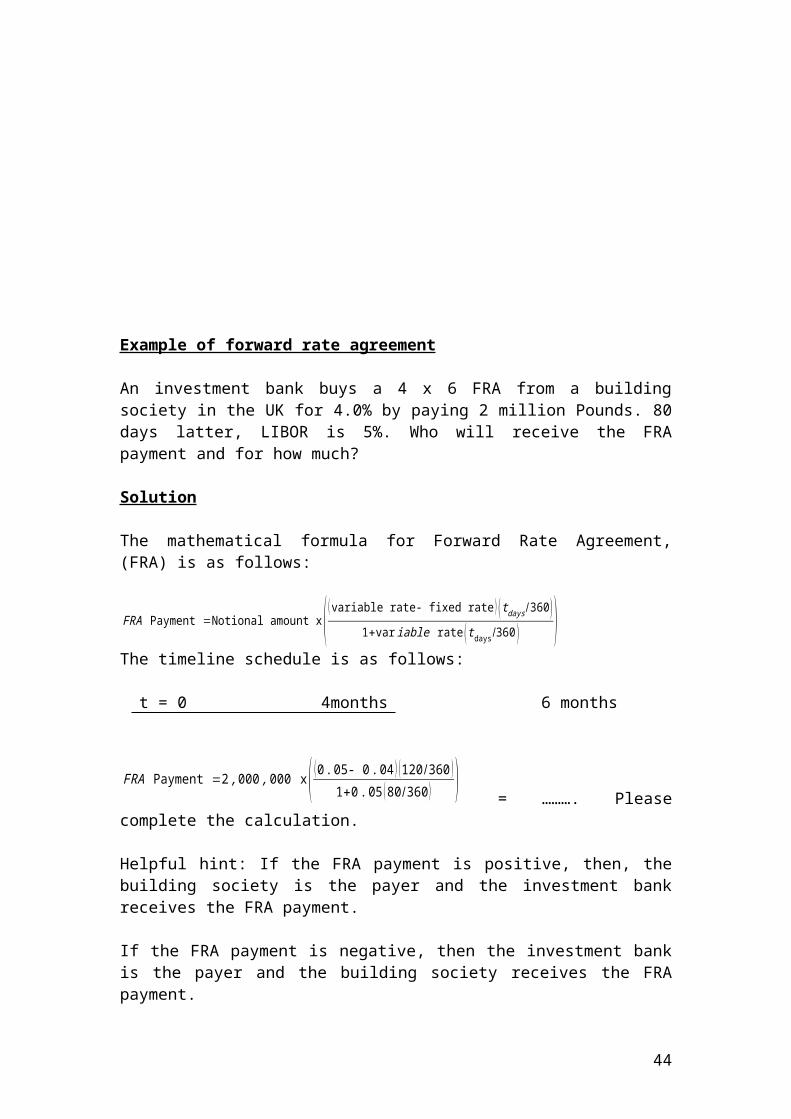

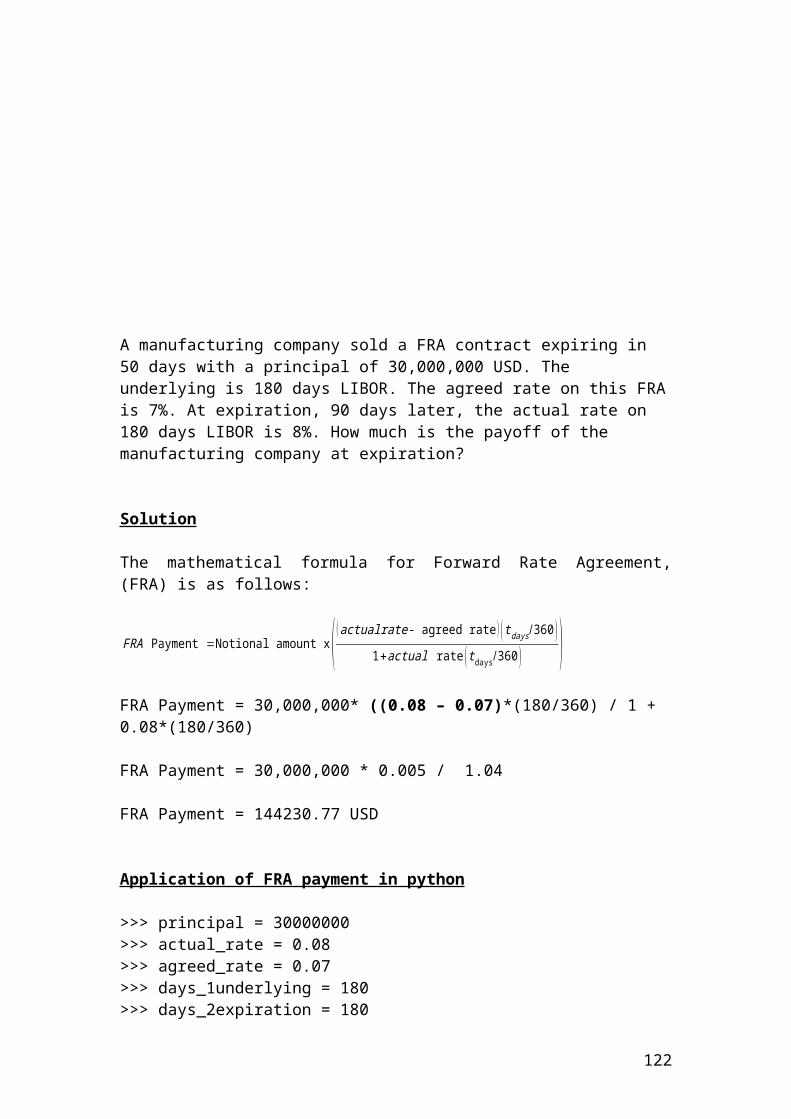

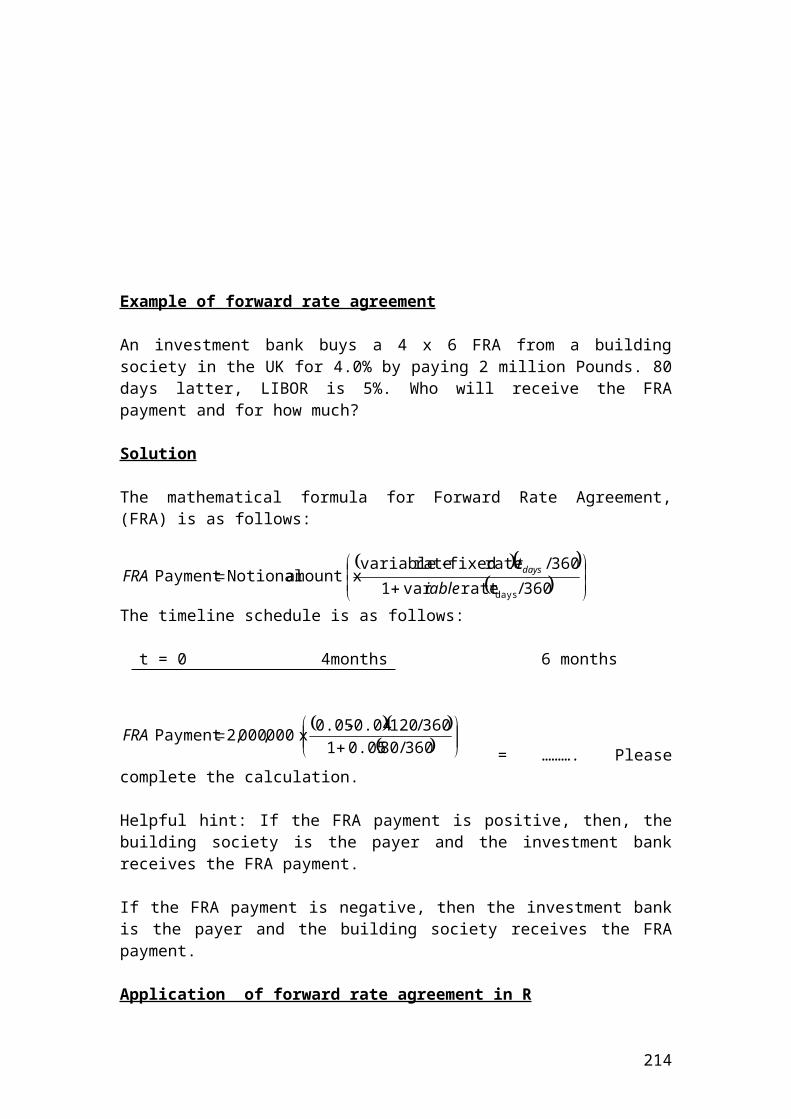

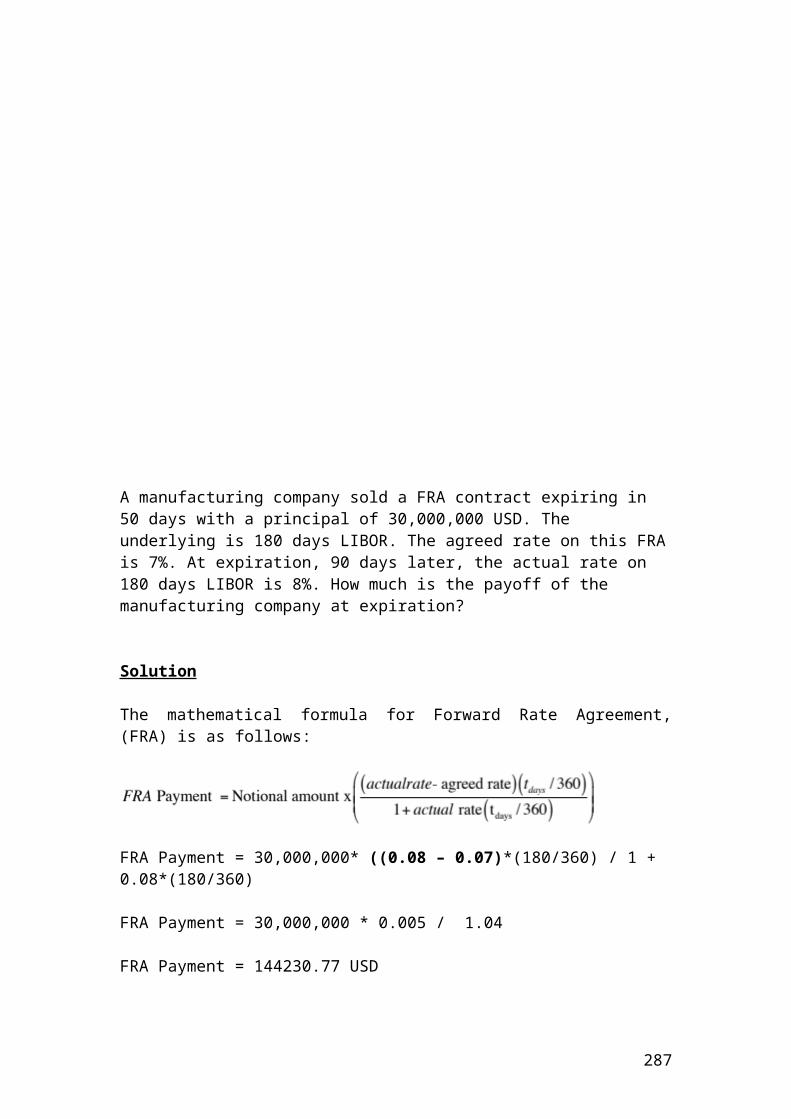

Example of forward rate agreement

An investment bank buys a 4 x 6 FRA from a building society in the UK for 4.0% by paying 2 million Pounds. 80 days latter, LIBOR is 5%. Who will receive the FRA payment and for how much?

Solution

The mathematical formula for Forward Rate Agreement, (FRA) is as follows:

FRA Payment =Notional amount x( ( variable rate- fixed rate ) (t days /360 )1+var iable rate ( tdays/360 ) )

The timeline schedule is as follows:

t = 0 4months 6 months

FRA Payment =2, 000 , 000 x( (0 . 05- 0 . 04 ) (120/360 )1+0 . 05 (80/360 ) )

= ………. Please complete the calculation.

Helpful hint: If the FRA payment is positive, then, the building society is the payer and the investment bank receives the FRA payment.

If the FRA payment is negative, then the investment bank is the payer and the building society receives the FRA payment.

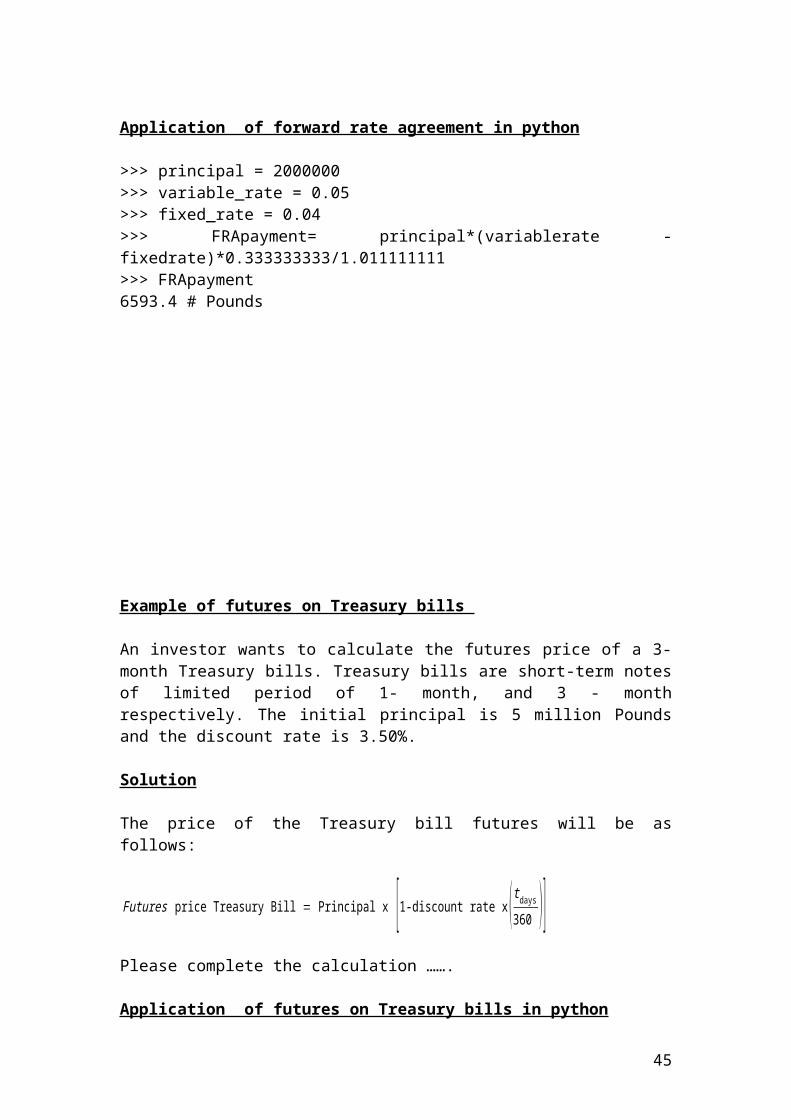

Application of forward rate agreement in python

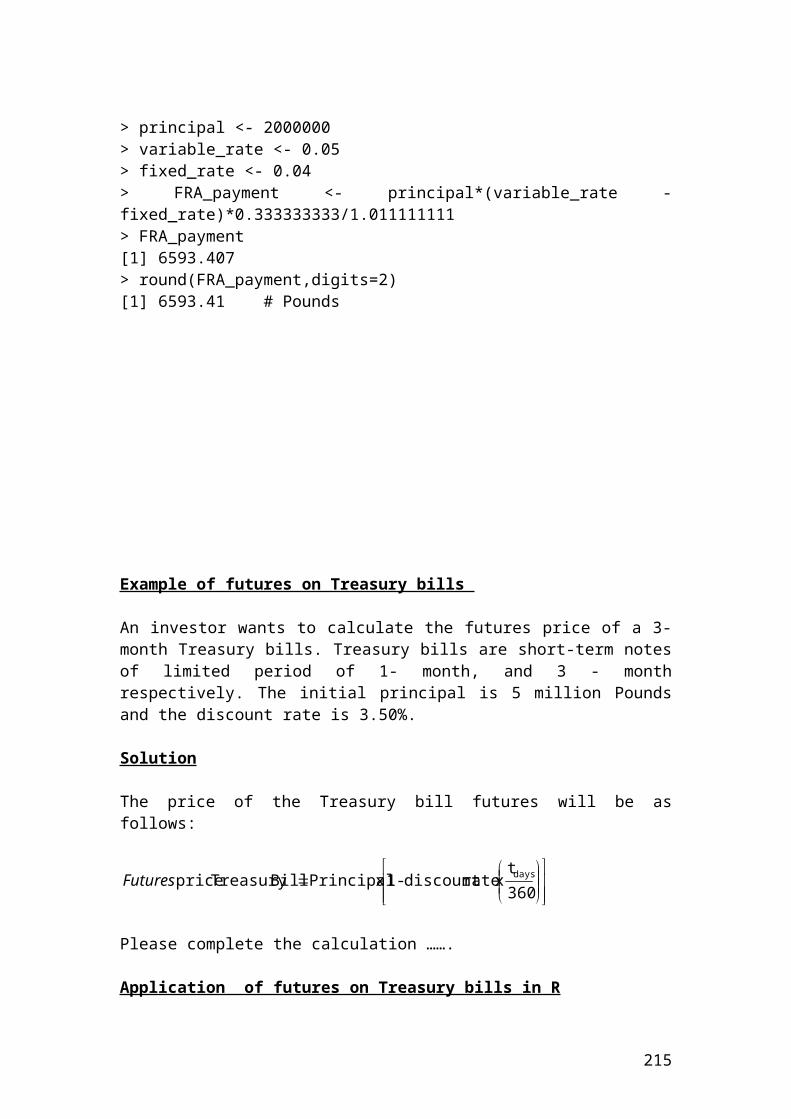

>>> principal = 2000000>>> variable_rate = 0.05>>> fixed_rate = 0.04>>> FRApayment= principal*(variablerate - fixedrate)*0.333333333/1.011111111>>> FRApayment6593.4 # Pounds

34

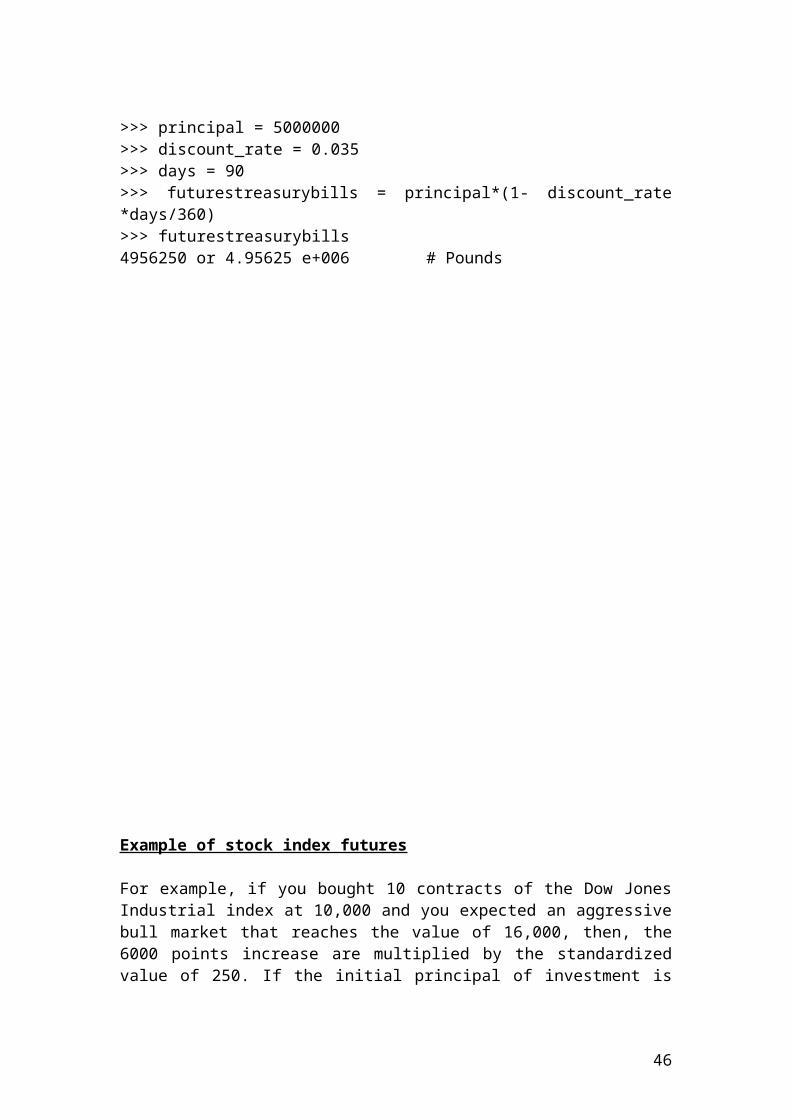

Example of futures on Treasury bills

An investor wants to calculate the futures price of a 3-month Treasury bills. Treasury bills are short-term notes of limited period of 1- month, and 3 - month respectively. The initial principal is 5 million Pounds and the discount rate is 3.50%.

Solution

The price of the Treasury bill futures will be as follows:

Futures price Treasury Bill = Principal x [1-discount rate x (t days

360 )]

Please complete the calculation …….

Application of futures on Treasury bills in python

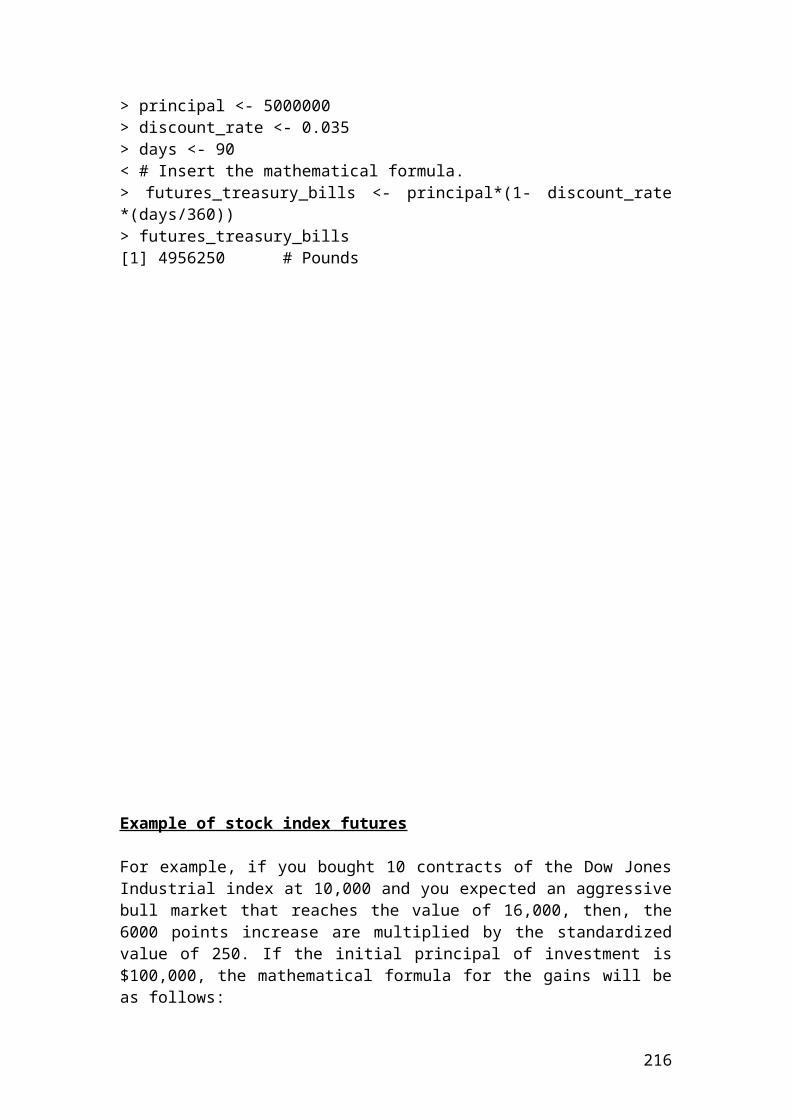

>>> principal = 5000000>>> discount_rate = 0.035>>> days = 90>>> futurestreasurybills = principal*(1- discount_rate *days/360)>>> futurestreasurybills4956250 or 4.95625 e+006 # Pounds

35

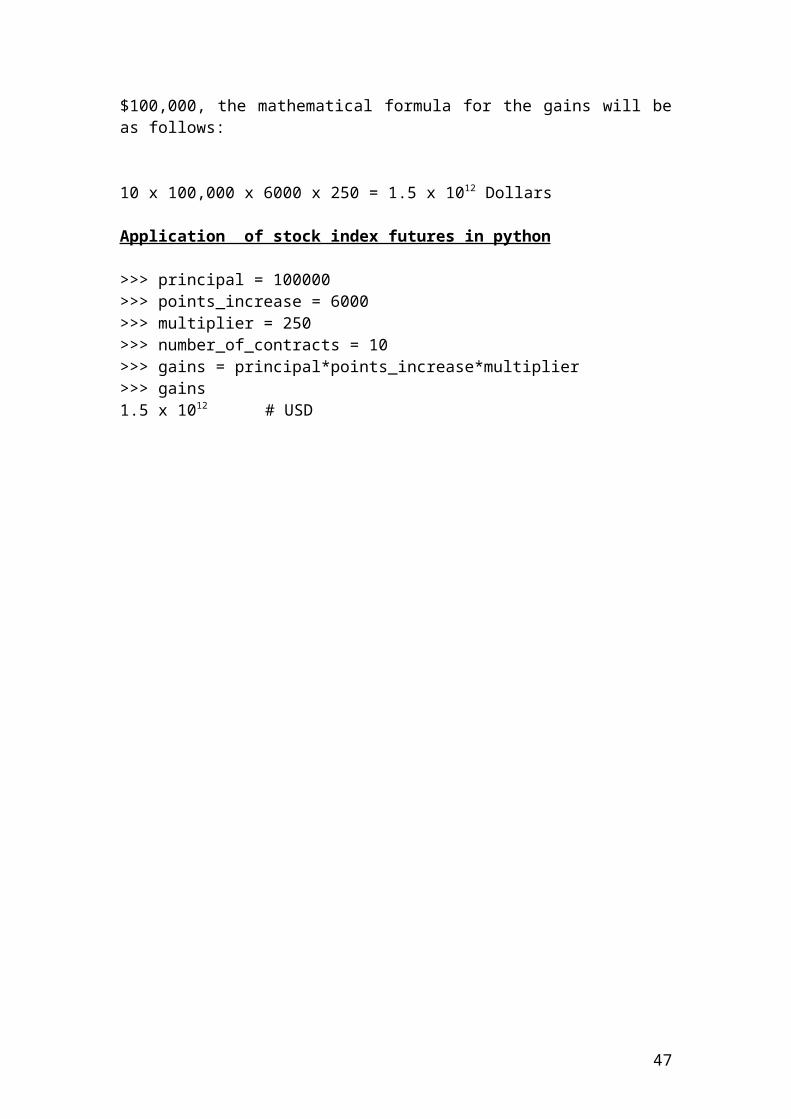

Example of stock index futures

For example, if you bought 10 contracts of the Dow Jones Industrial index at 10,000 and you expected an aggressive bull market that reaches the value of 16,000, then, the 6000 points increase are multiplied by the standardized value of 250. If the initial principal of investment is $100,000, the mathematical formula for the gains will be as follows:

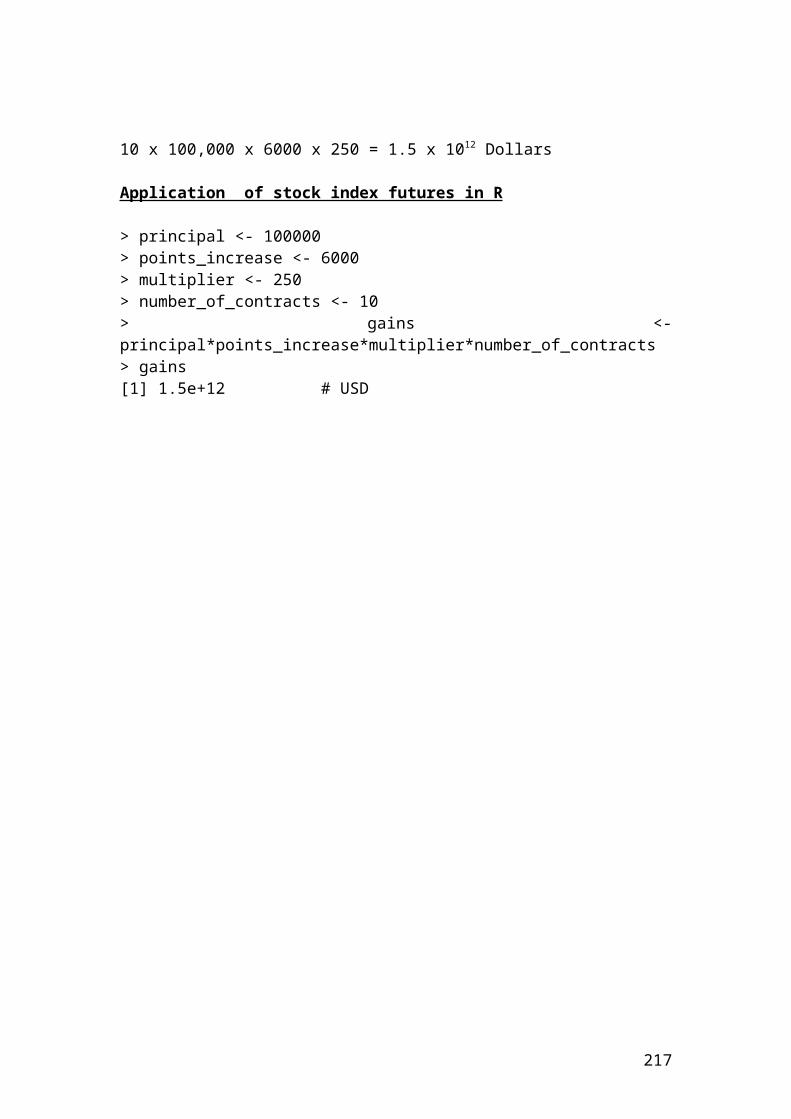

10 x 100,000 x 6000 x 250 = 1.5 x 1012 Dollars

Application of stock index futures in python

>>> principal = 100000>>> points_increase = 6000>>> multiplier = 250>>> number_of_contracts = 10>>> gains = principal*points_increase*multiplier>>> gains1.5 x 1012 # USD

36

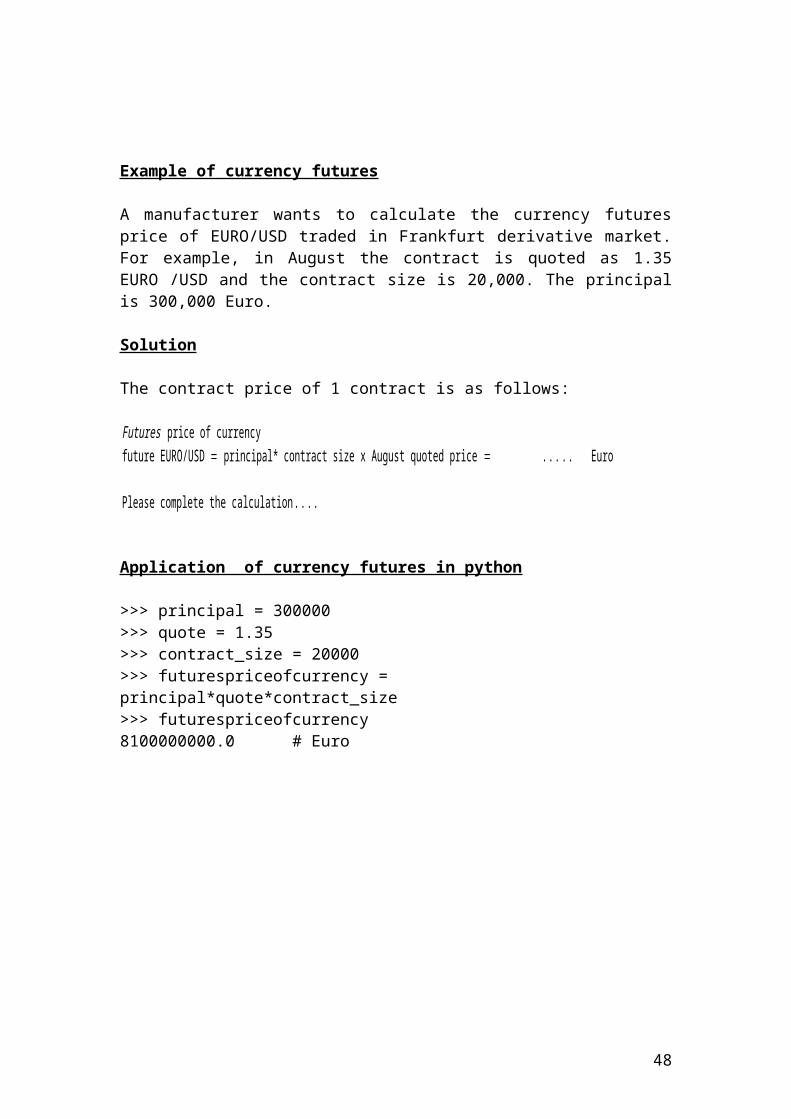

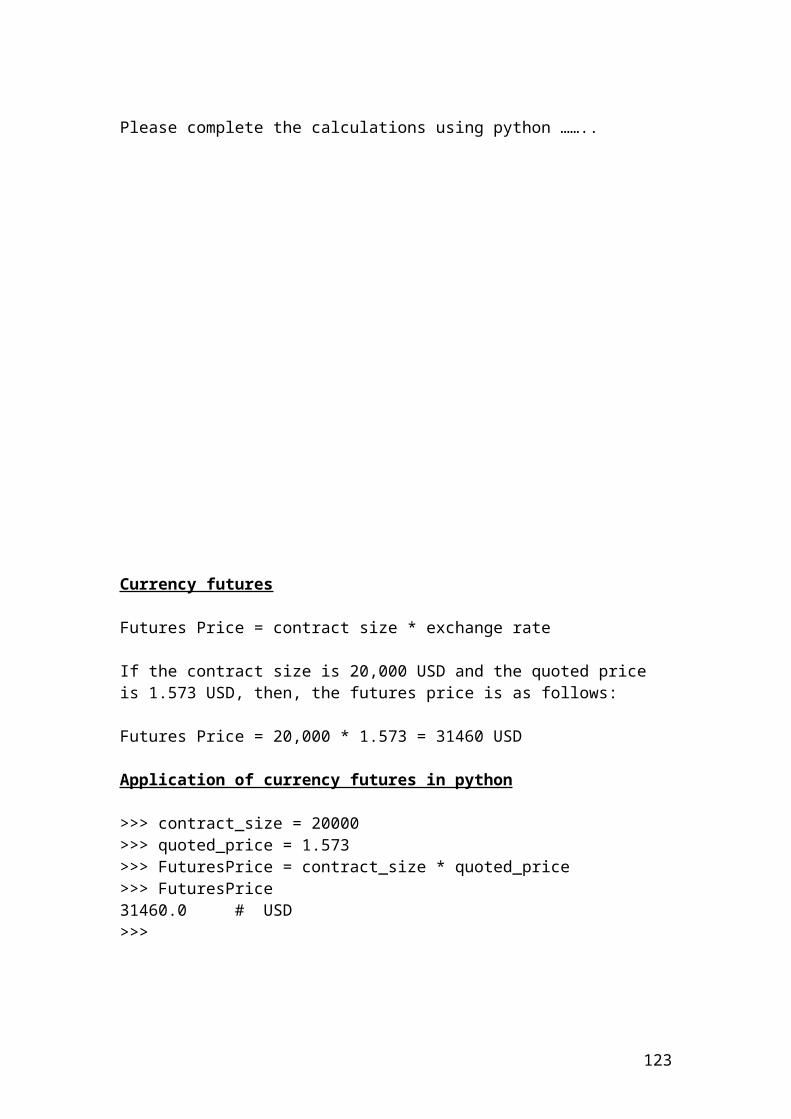

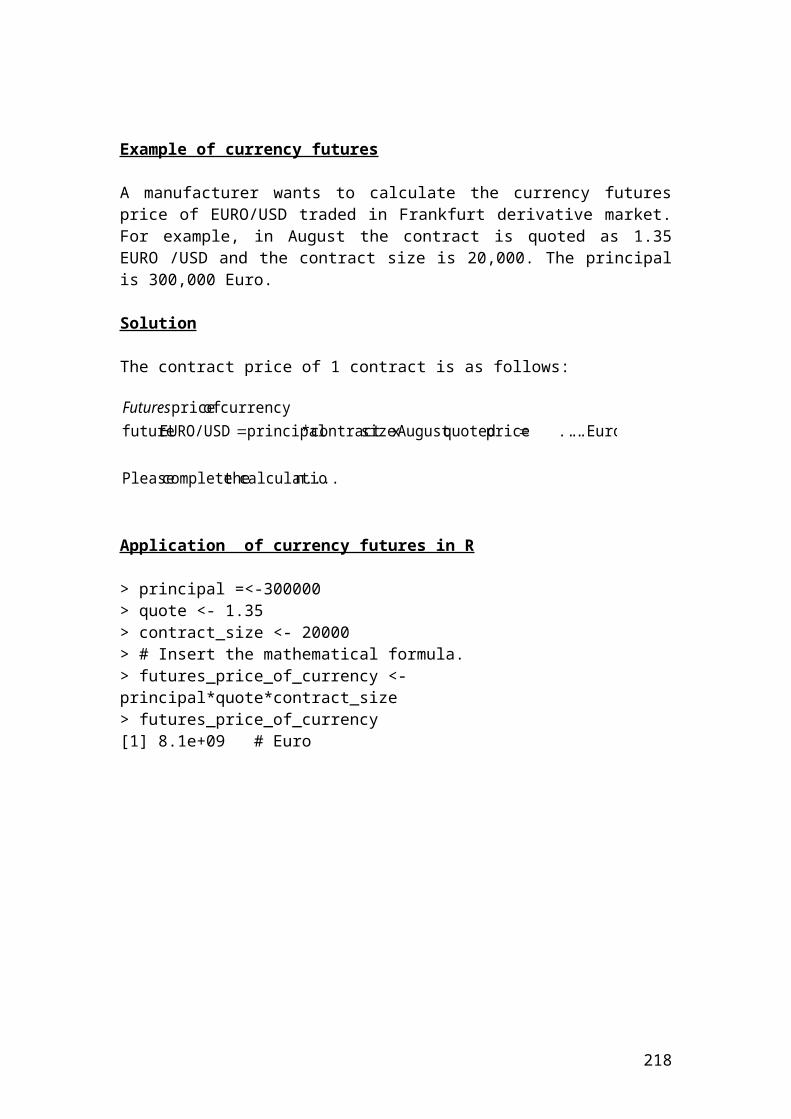

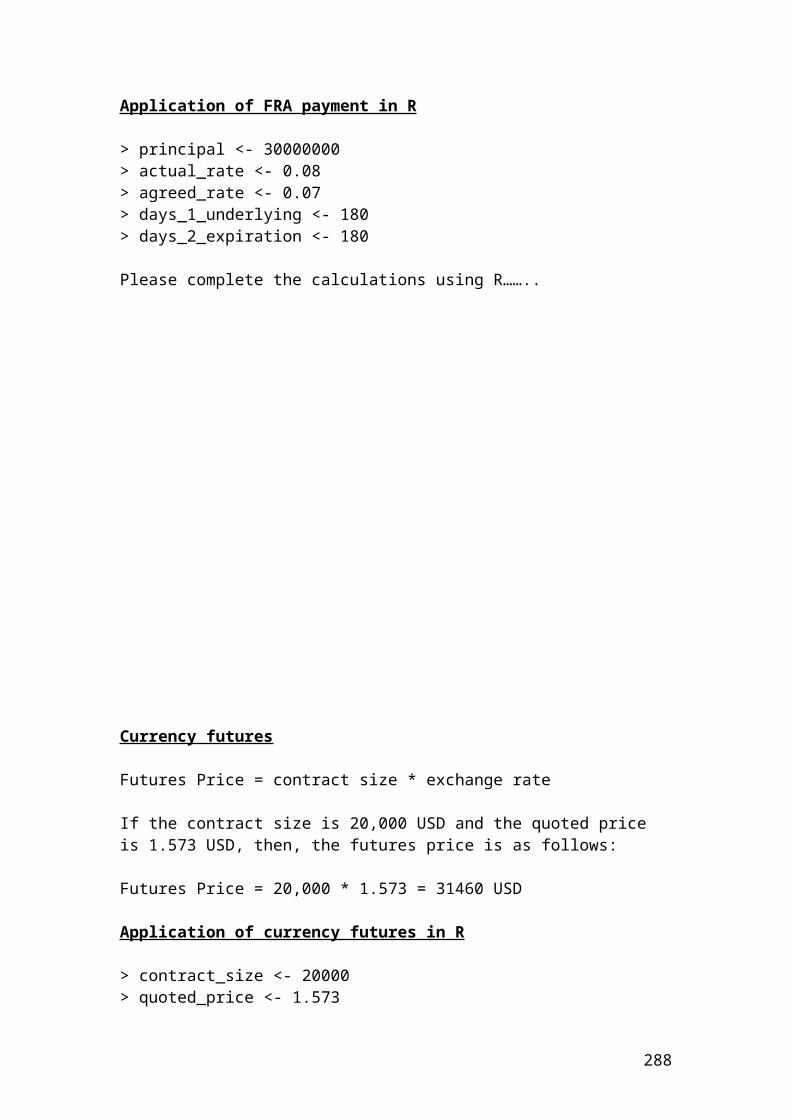

Example of currency futures

A manufacturer wants to calculate the currency futures price of EURO/USD traded in Frankfurt derivative market. For example, in August the contract is quoted as 1.35 EURO /USD and the contract size is 20,000. The principal is 300,000 Euro.

Solution

The contract price of 1 contract is as follows:

Futures price of currency future EURO/USD = principal* contract size x August quoted price = . .. . . Euro

Please complete the calculation . .. .

Application of currency futures in python

>>> principal = 300000>>> quote = 1.35>>> contract_size = 20000>>> futurespriceofcurrency = principal*quote*contract_size>>> futurespriceofcurrency8100000000.0 # Euro

37

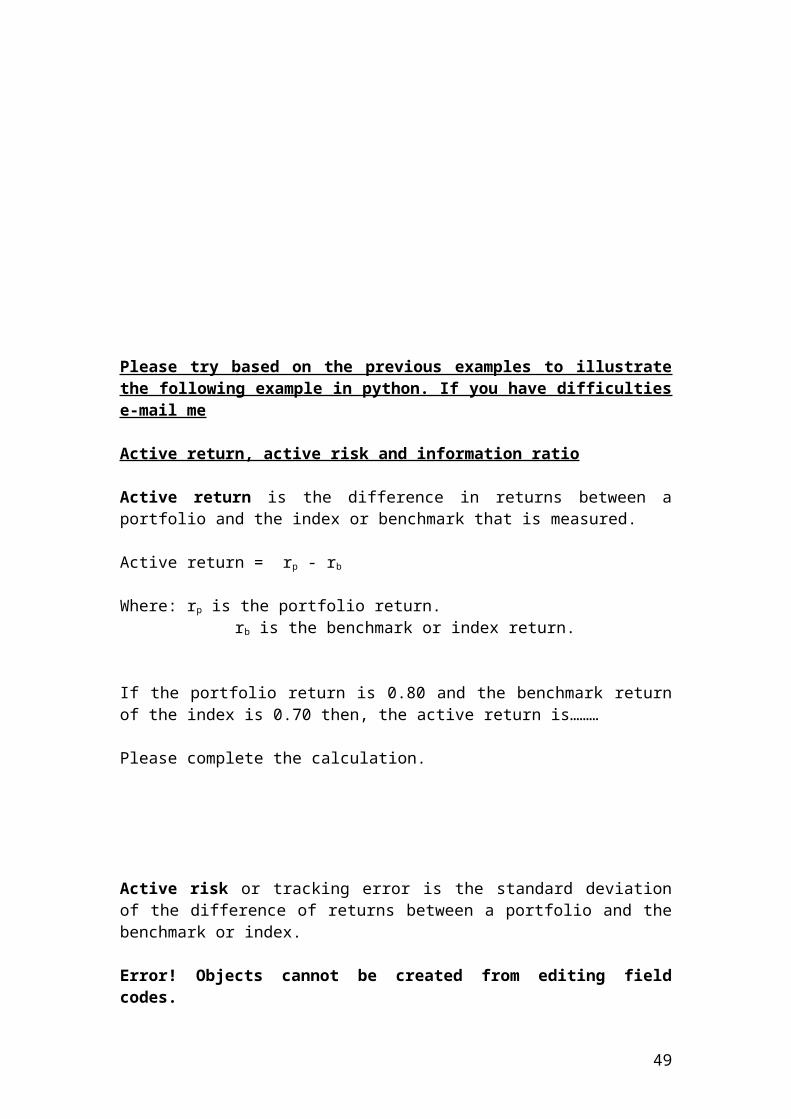

Please try based on the previous examples to illustrate the following example in python. If you have difficulties e-mail me

Active return, active risk and information ratio

Active return is the difference in returns between a portfolio and the index or benchmark that is measured.

Active return = rp - rb

Where: rp is the portfolio return. rb is the benchmark or index return.

If the portfolio return is 0.80 and the benchmark return of the index is 0.70 then, the active return is………

Please complete the calculation.

Active risk or tracking error is the standard deviation of the difference of returns between a portfolio and the benchmark or index.

Error! Objects cannot be created from editing field codes.

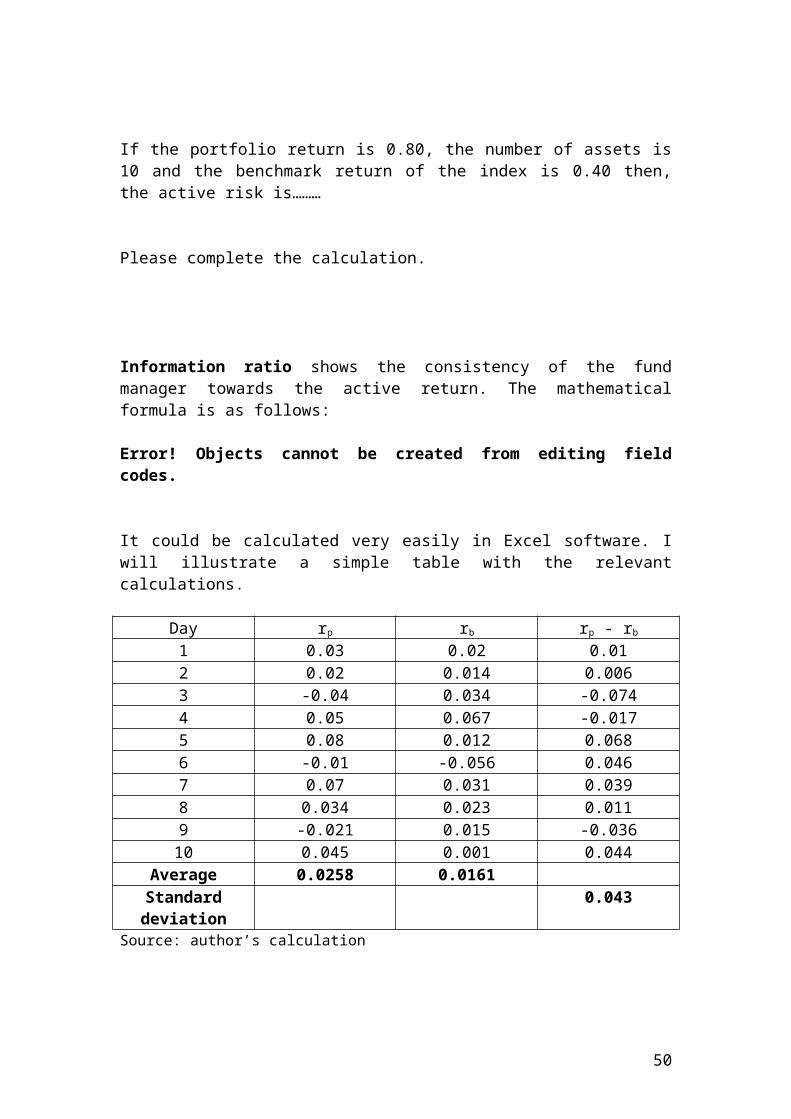

If the portfolio return is 0.80, the number of assets is 10 and the benchmark return of the index is 0.40 then, the active risk is………

Please complete the calculation.

Information ratio shows the consistency of the fund manager towards the active return. The mathematical formula is as follows:

Error! Objects cannot be created from editing field codes.

It could be calculated very easily in Excel software. I will illustrate a simple table with the relevant calculations.

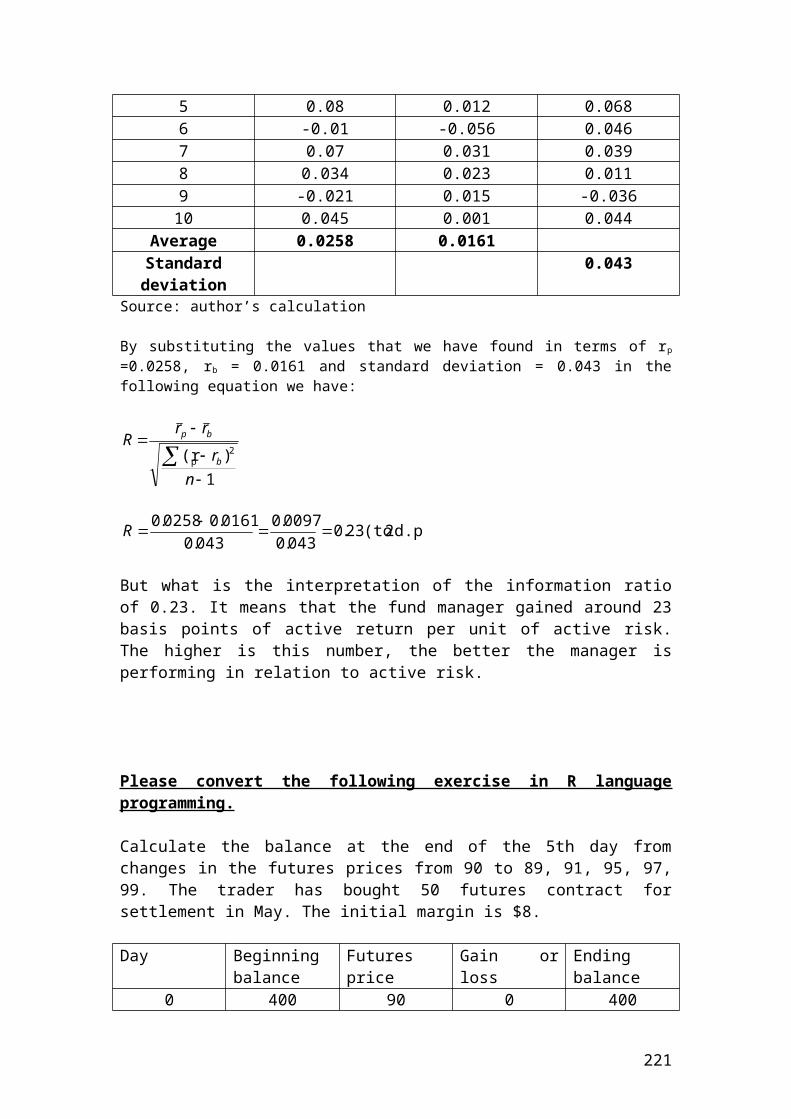

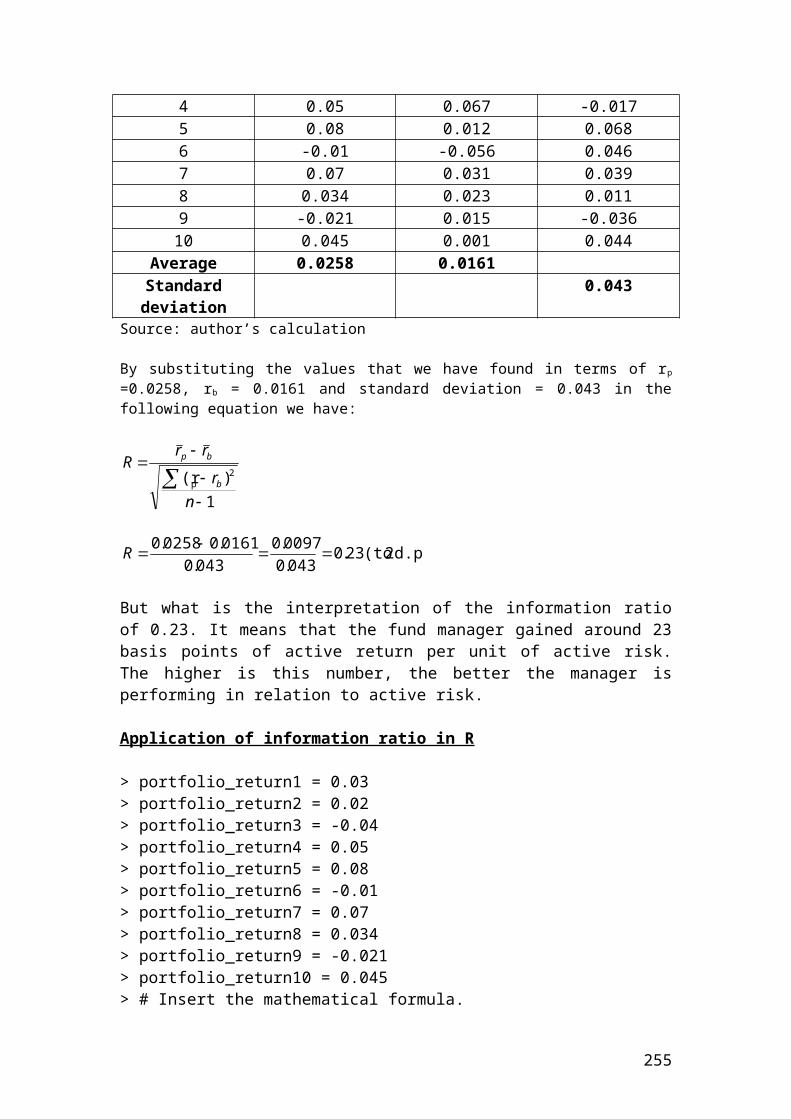

Day rp rb rp - rb

1 0.03 0.02 0.01

38

2 0.02 0.014 0.0063 -0.04 0.034 -0.0744 0.05 0.067 -0.0175 0.08 0.012 0.0686 -0.01 -0.056 0.0467 0.07 0.031 0.0398 0.034 0.023 0.0119 -0.021 0.015 -0.03610 0.045 0.001 0.044

Average 0.0258 0.0161Standard deviation

0.043

Source: author’s calculation

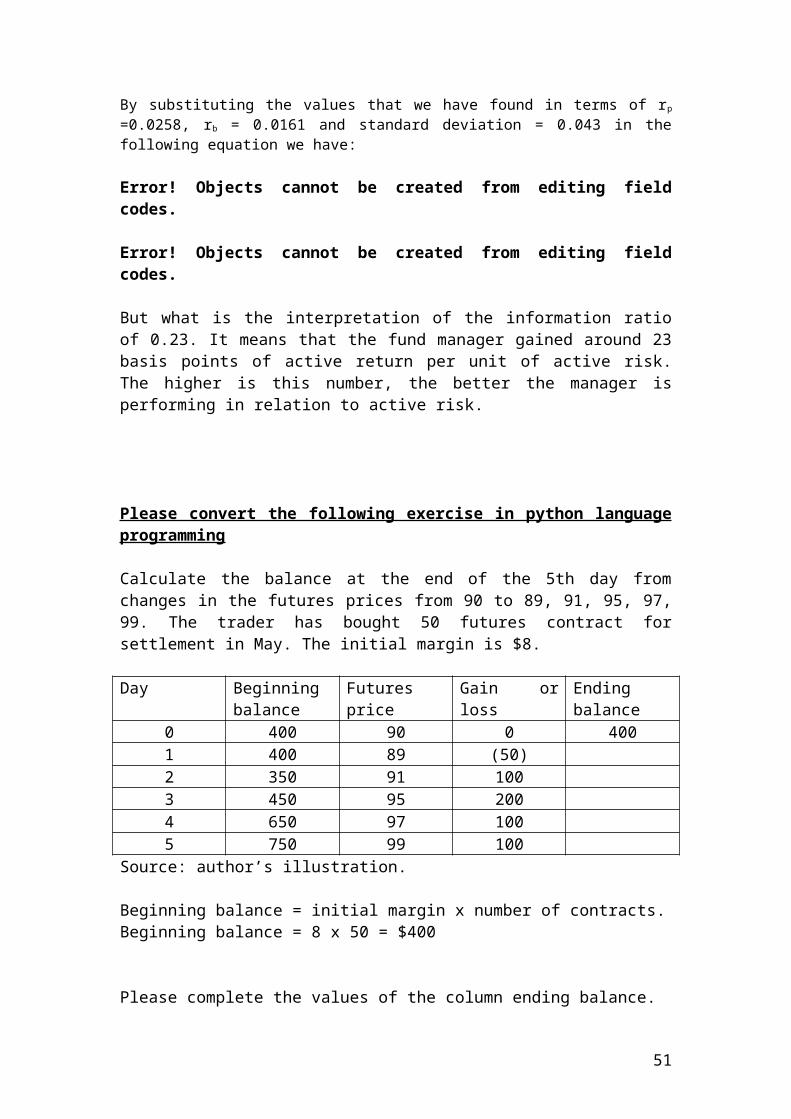

By substituting the values that we have found in terms of rp =0.0258, rb = 0.0161 and standard deviation = 0.043 in the following equation we have:

Error! Objects cannot be created from editing field codes.

Error! Objects cannot be created from editing field codes.

But what is the interpretation of the information ratio of 0.23. It means that the fund manager gained around 23 basis points of active return per unit of active risk. The higher is this number, the better the manager is performing in relation to active risk.

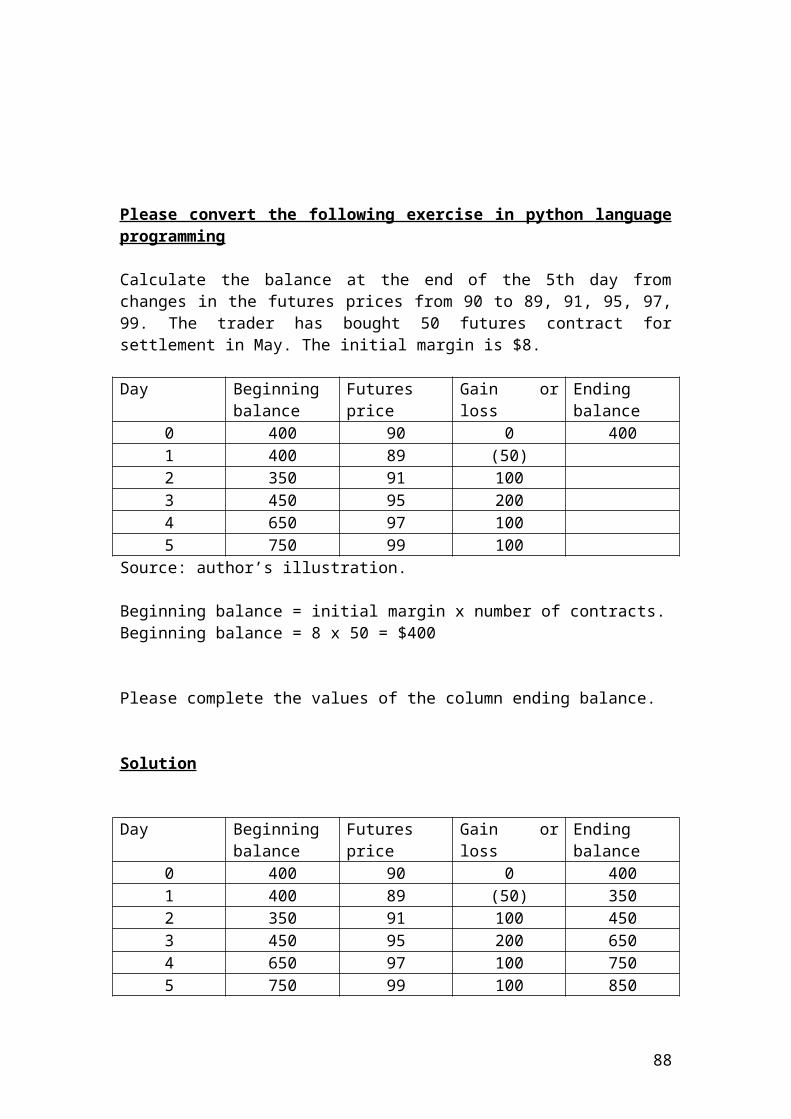

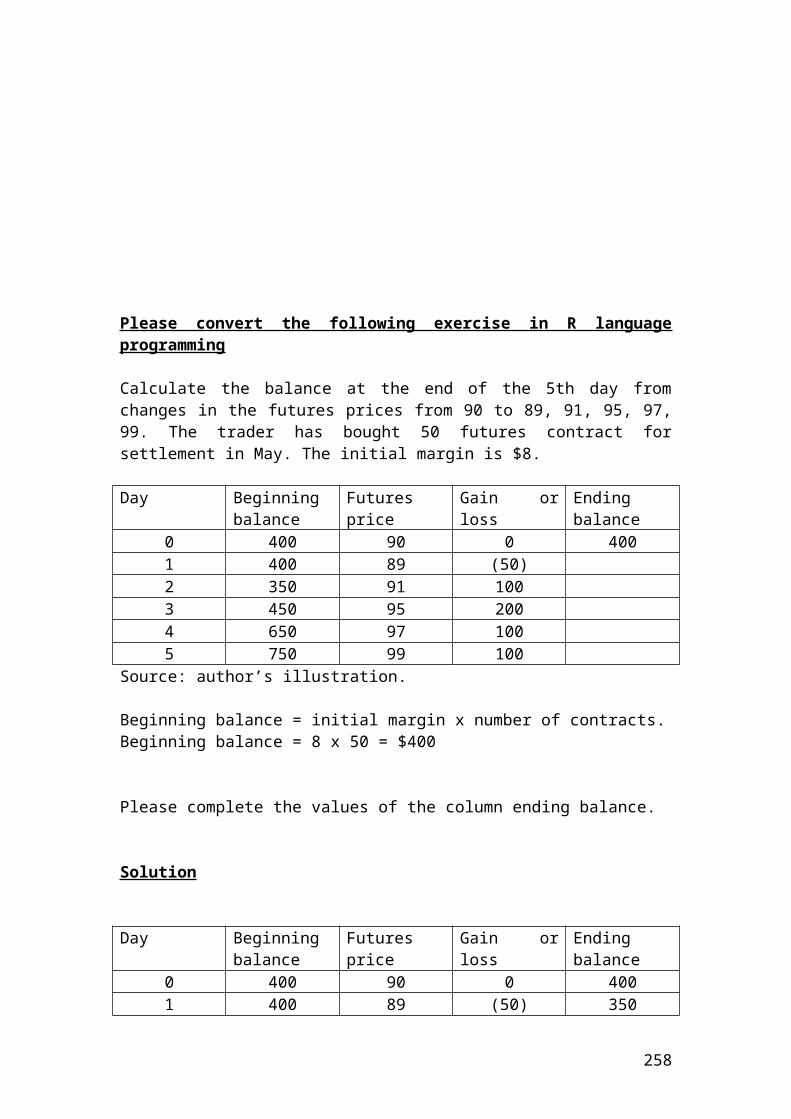

Please convert the following exercise in python language programming

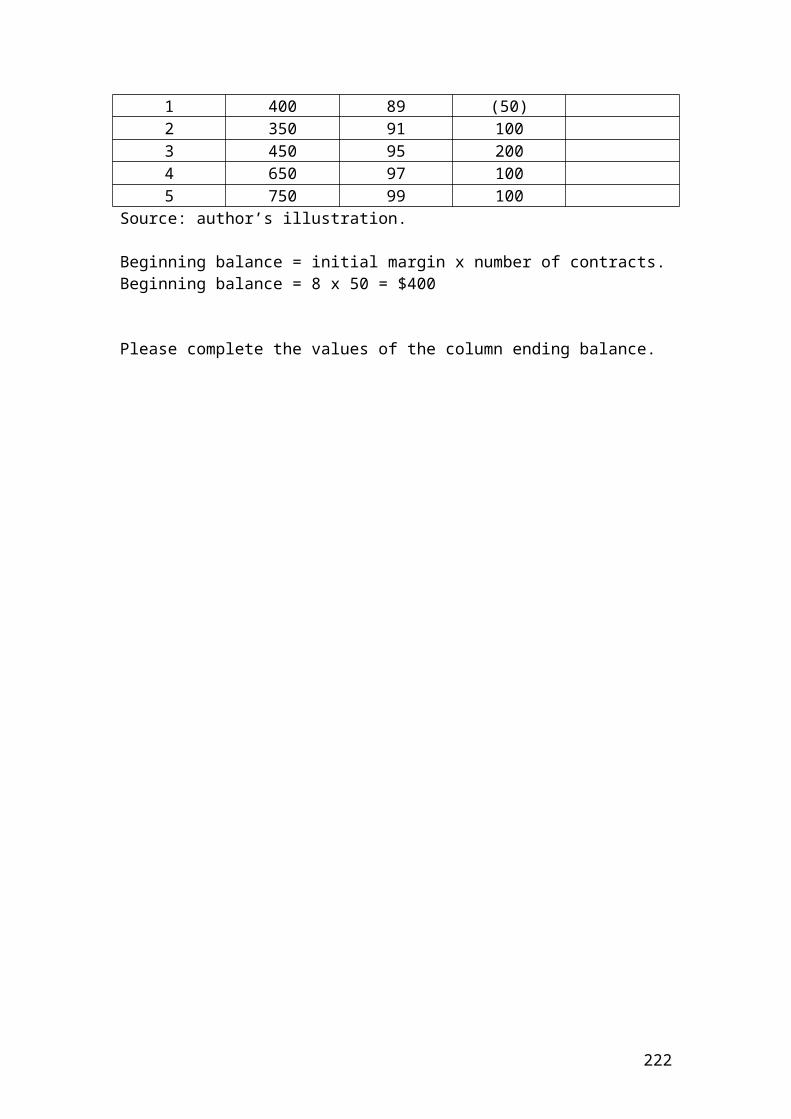

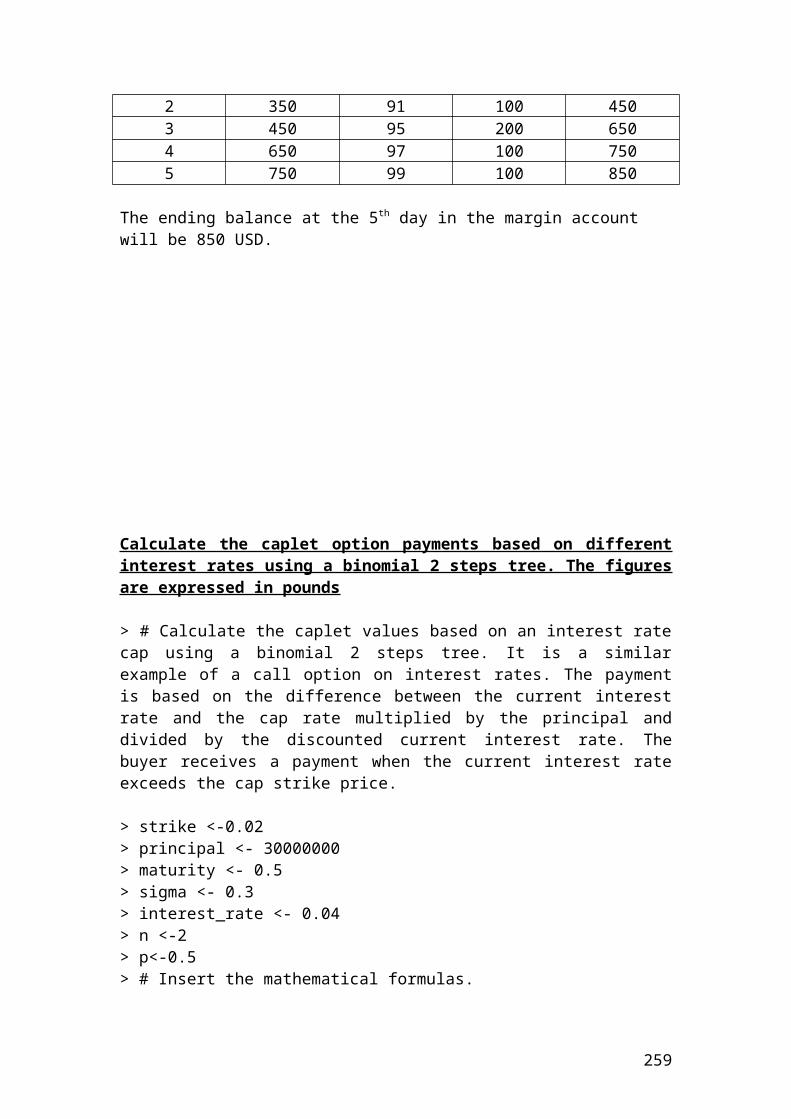

Calculate the balance at the end of the 5th day from changes in the futures prices from 90 to 89, 91, 95, 97, 99. The trader has bought 50 futures contract for settlement in May. The initial margin is $8.

Day Beginning balance

Futures price Gain or loss Ending balance

0 400 90 0 4001 400 89 (50)2 350 91 1003 450 95 2004 650 97 1005 750 99 100

Source: author’s illustration.

Beginning balance = initial margin x number of contracts.Beginning balance = 8 x 50 = $400

Please complete the values of the column ending balance.

39

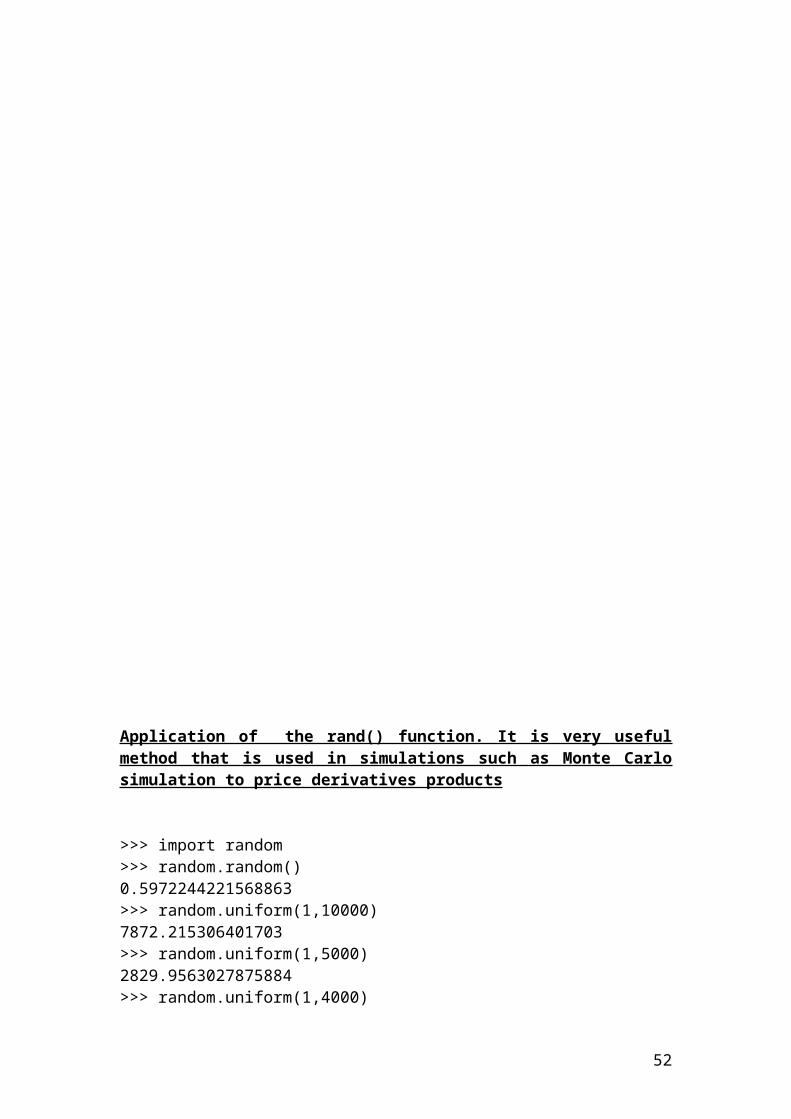

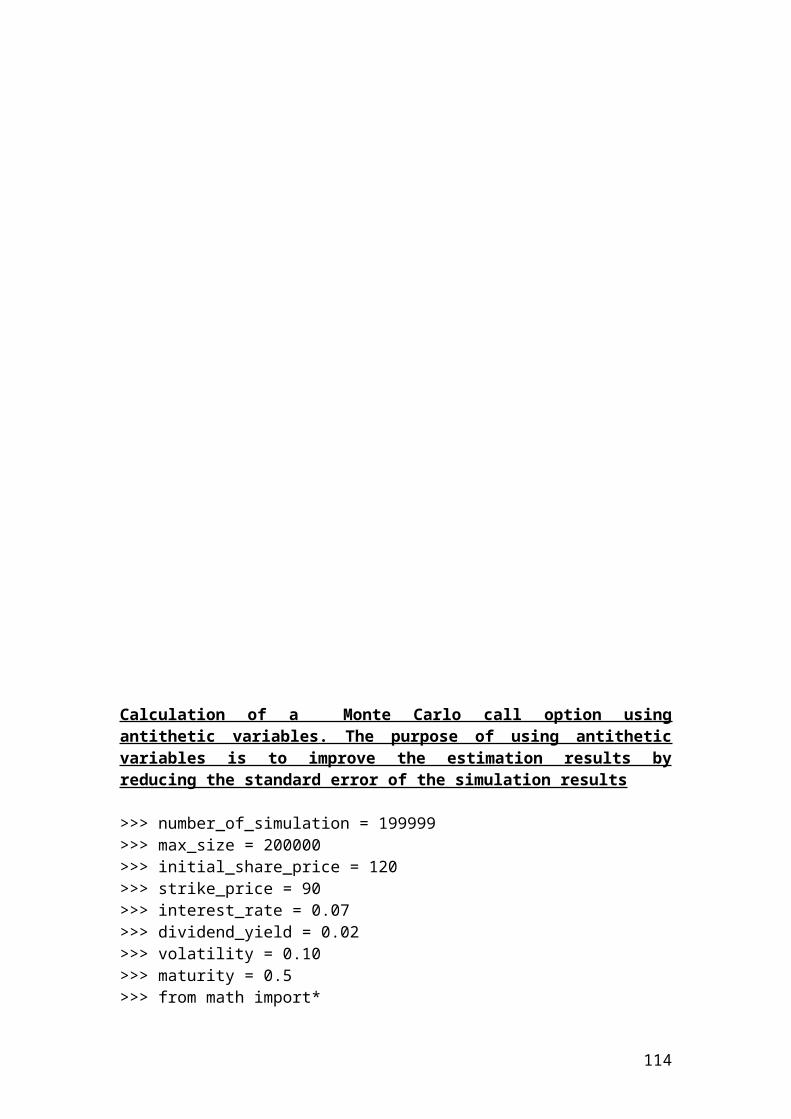

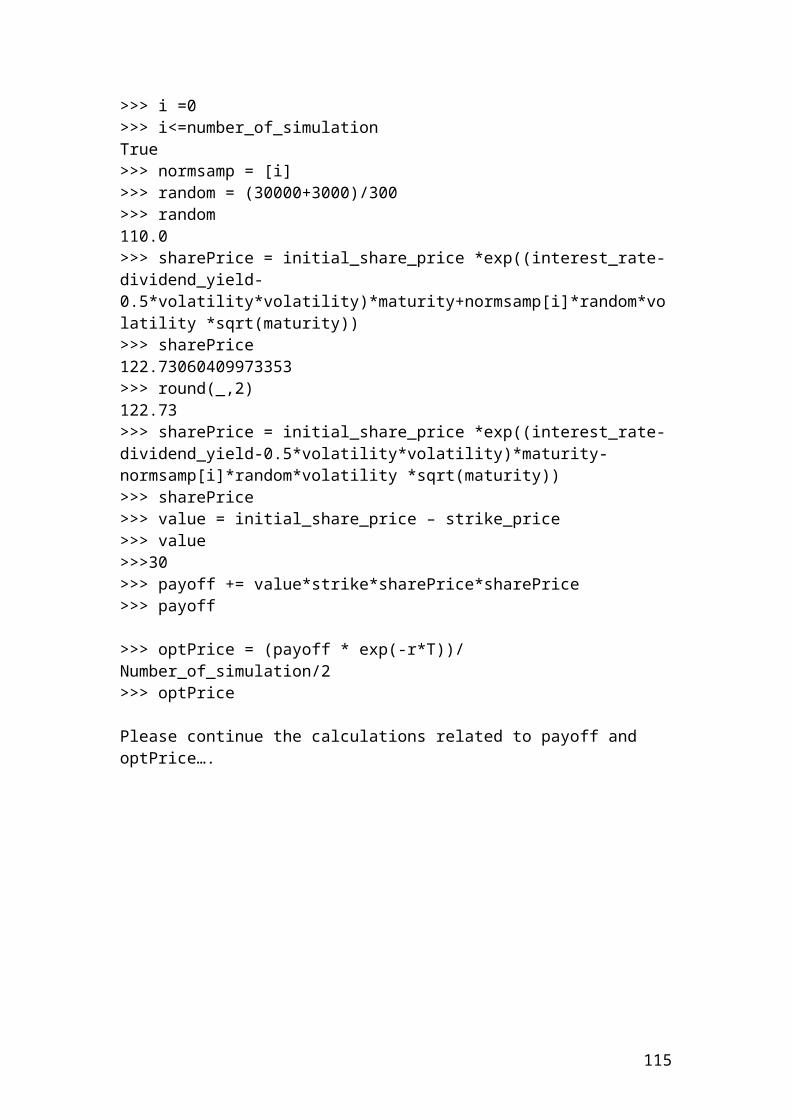

Application of the rand() function. It is very useful method that is used in simulations such as Monte Carlo simulation to price derivatives products

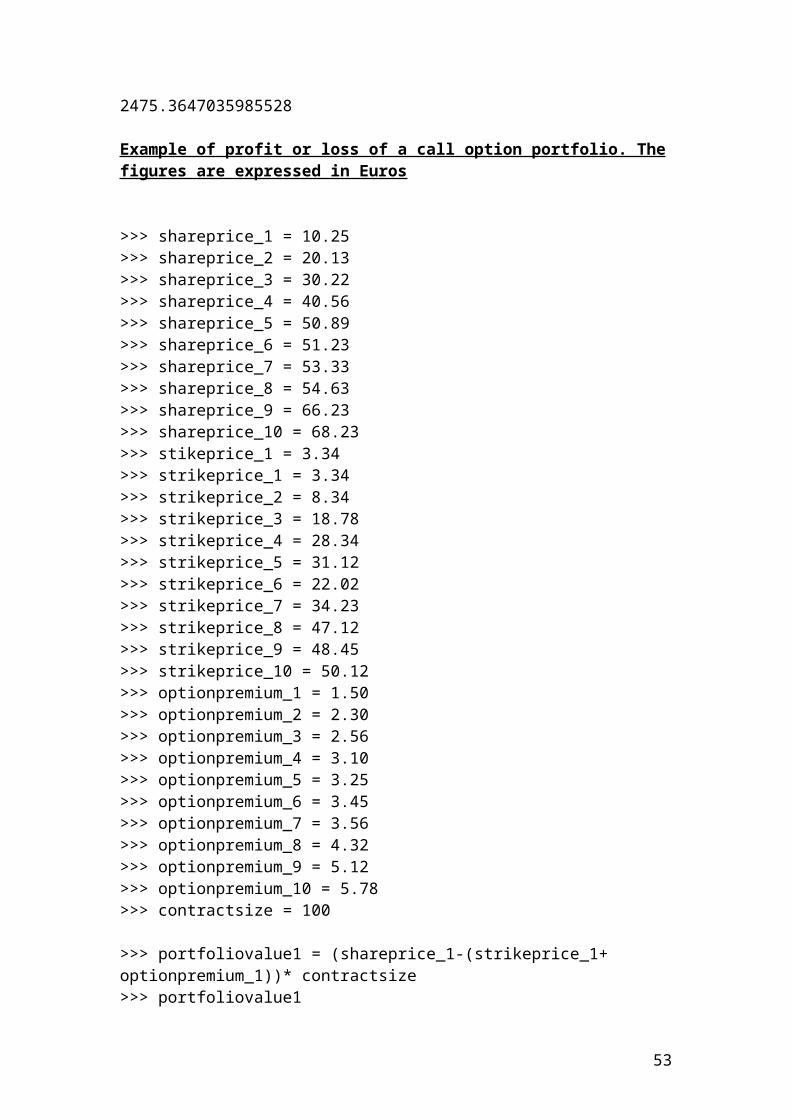

>>> import random>>> random.random()0.5972244221568863>>> random.uniform(1,10000)7872.215306401703>>> random.uniform(1,5000)2829.9563027875884>>> random.uniform(1,4000)2475.3647035985528

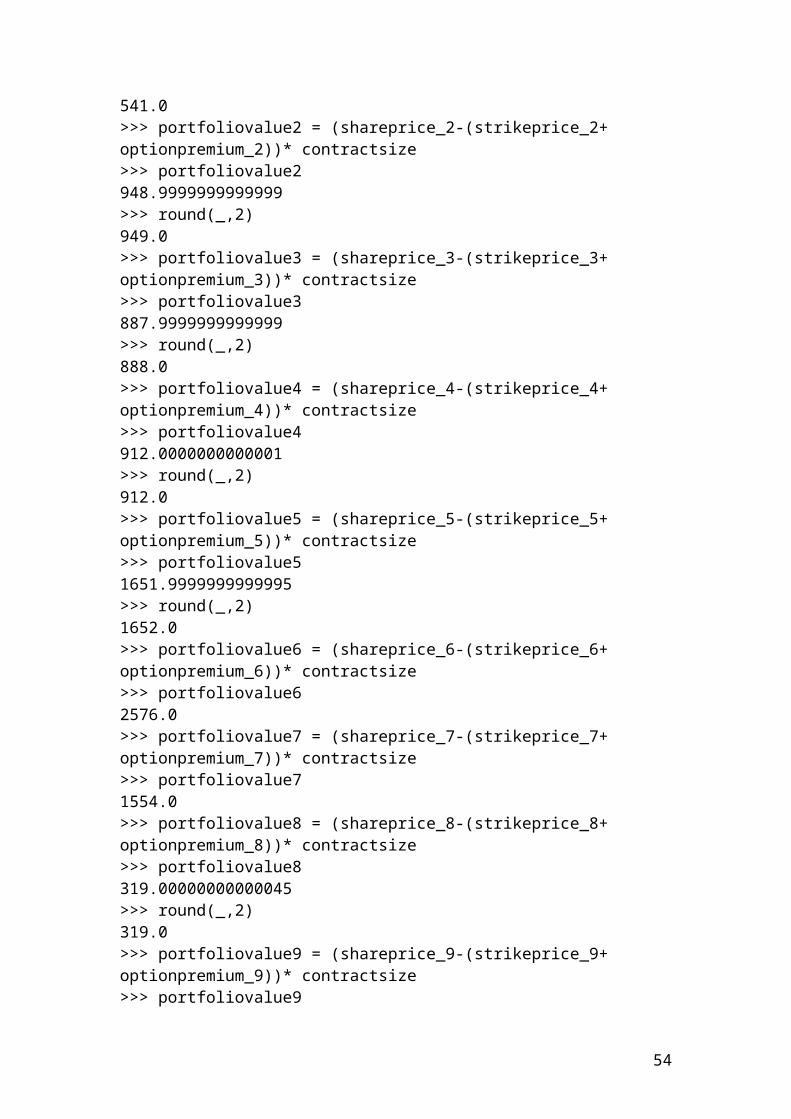

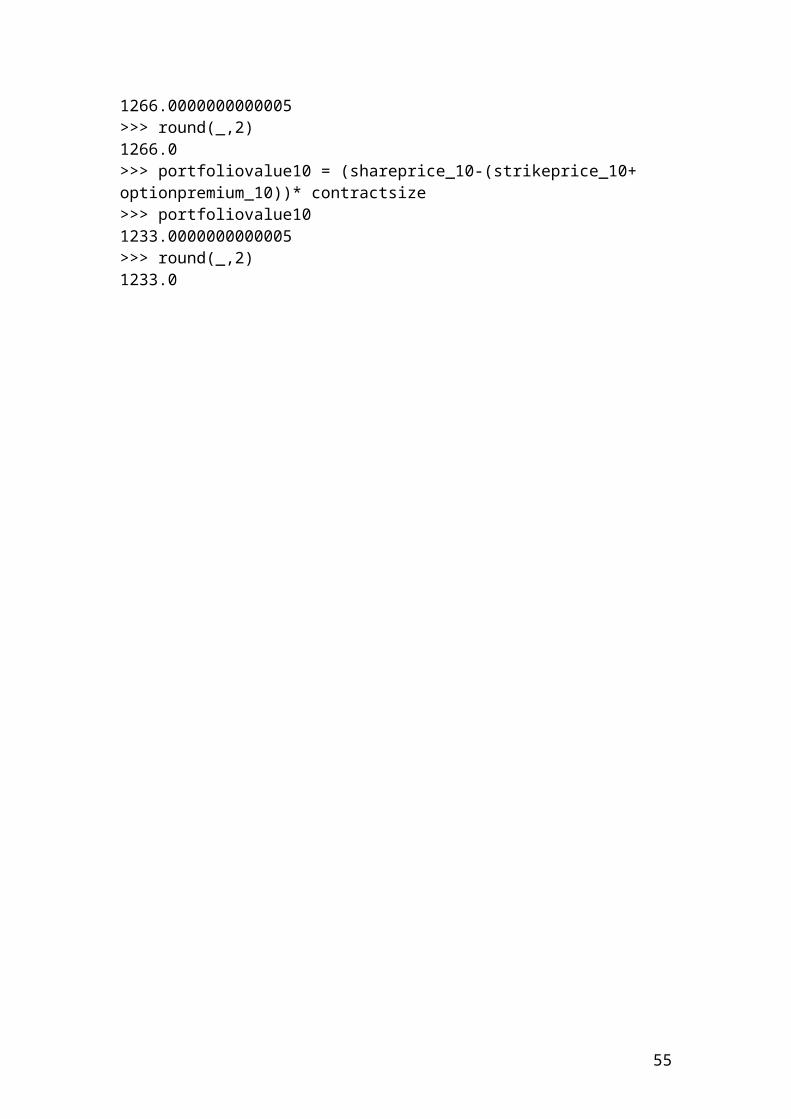

Example of profit or loss of a call option portfolio. The figures are expressed in Euros

>>> shareprice_1 = 10.25>>> shareprice_2 = 20.13>>> shareprice_3 = 30.22>>> shareprice_4 = 40.56

40

>>> shareprice_5 = 50.89>>> shareprice_6 = 51.23>>> shareprice_7 = 53.33>>> shareprice_8 = 54.63>>> shareprice_9 = 66.23>>> shareprice_10 = 68.23>>> stikeprice_1 = 3.34>>> strikeprice_1 = 3.34>>> strikeprice_2 = 8.34>>> strikeprice_3 = 18.78>>> strikeprice_4 = 28.34>>> strikeprice_5 = 31.12>>> strikeprice_6 = 22.02>>> strikeprice_7 = 34.23>>> strikeprice_8 = 47.12>>> strikeprice_9 = 48.45>>> strikeprice_10 = 50.12>>> optionpremium_1 = 1.50>>> optionpremium_2 = 2.30>>> optionpremium_3 = 2.56>>> optionpremium_4 = 3.10>>> optionpremium_5 = 3.25>>> optionpremium_6 = 3.45>>> optionpremium_7 = 3.56>>> optionpremium_8 = 4.32>>> optionpremium_9 = 5.12>>> optionpremium_10 = 5.78>>> contractsize = 100

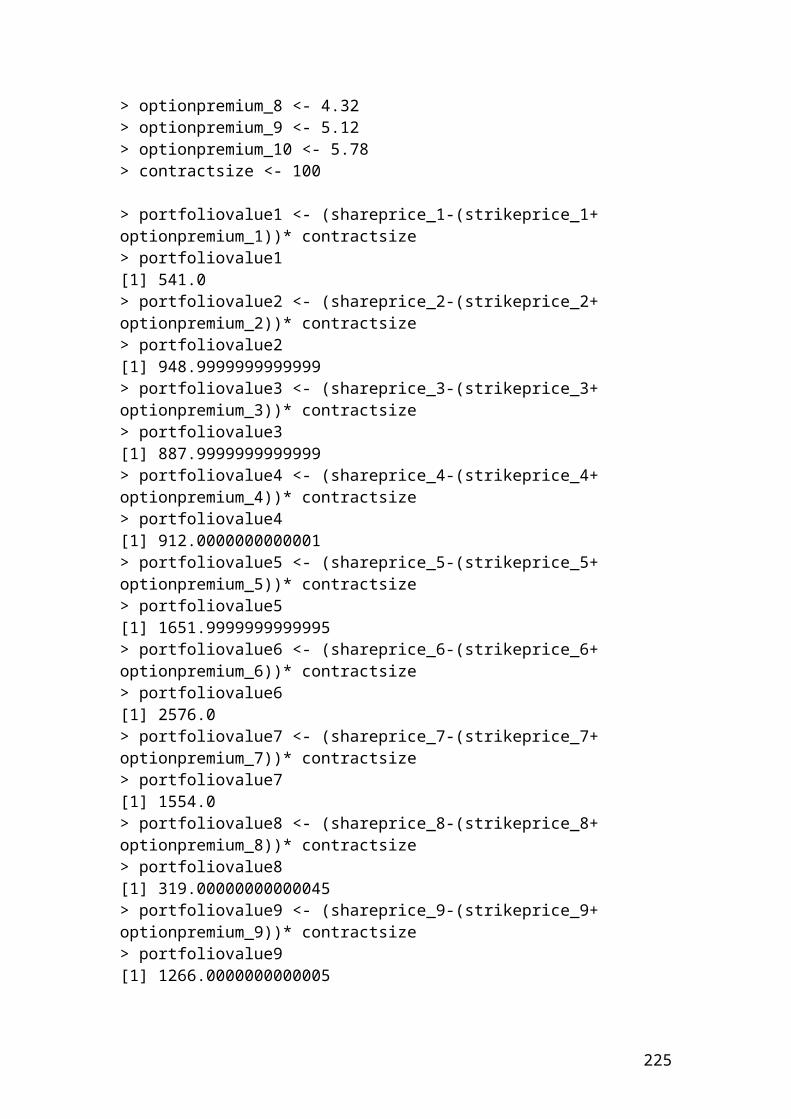

>>> portfoliovalue1 = (shareprice_1-(strikeprice_1+ optionpremium_1))* contractsize>>> portfoliovalue1541.0>>> portfoliovalue2 = (shareprice_2-(strikeprice_2+ optionpremium_2))* contractsize>>> portfoliovalue2948.9999999999999>>> round(_,2)949.0>>> portfoliovalue3 = (shareprice_3-(strikeprice_3+ optionpremium_3))* contractsize>>> portfoliovalue3887.9999999999999>>> round(_,2)888.0>>> portfoliovalue4 = (shareprice_4-(strikeprice_4+ optionpremium_4))* contractsize>>> portfoliovalue4912.0000000000001>>> round(_,2)

41

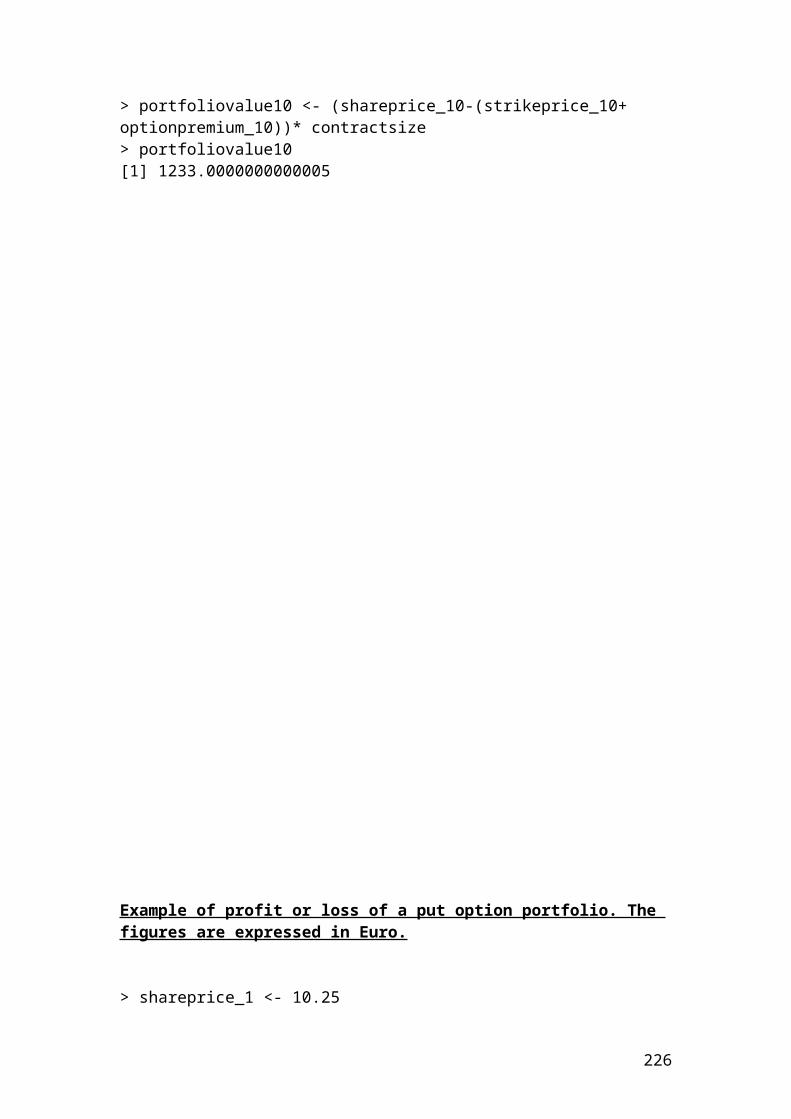

912.0>>> portfoliovalue5 = (shareprice_5-(strikeprice_5+ optionpremium_5))* contractsize>>> portfoliovalue51651.9999999999995>>> round(_,2)1652.0>>> portfoliovalue6 = (shareprice_6-(strikeprice_6+ optionpremium_6))* contractsize>>> portfoliovalue62576.0>>> portfoliovalue7 = (shareprice_7-(strikeprice_7+ optionpremium_7))* contractsize>>> portfoliovalue71554.0>>> portfoliovalue8 = (shareprice_8-(strikeprice_8+ optionpremium_8))* contractsize>>> portfoliovalue8319.00000000000045>>> round(_,2)319.0>>> portfoliovalue9 = (shareprice_9-(strikeprice_9+ optionpremium_9))* contractsize>>> portfoliovalue91266.0000000000005>>> round(_,2)1266.0>>> portfoliovalue10 = (shareprice_10-(strikeprice_10+ optionpremium_10))* contractsize>>> portfoliovalue101233.0000000000005>>> round(_,2)1233.0

42

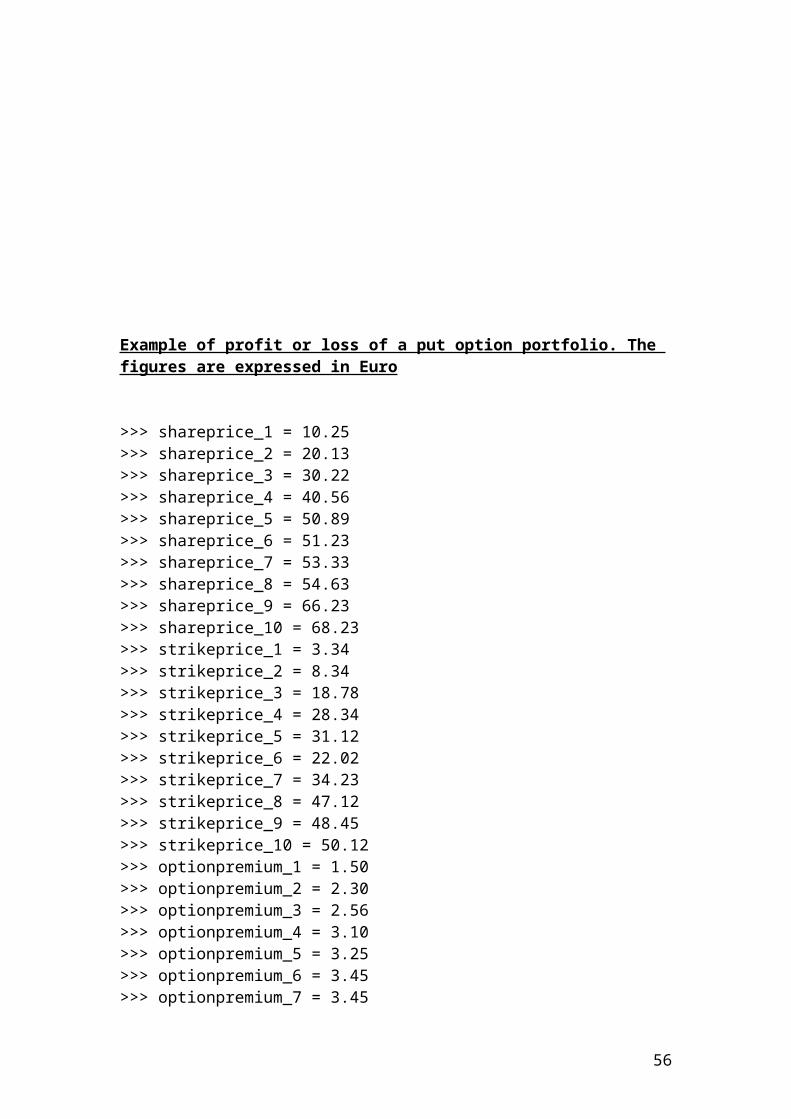

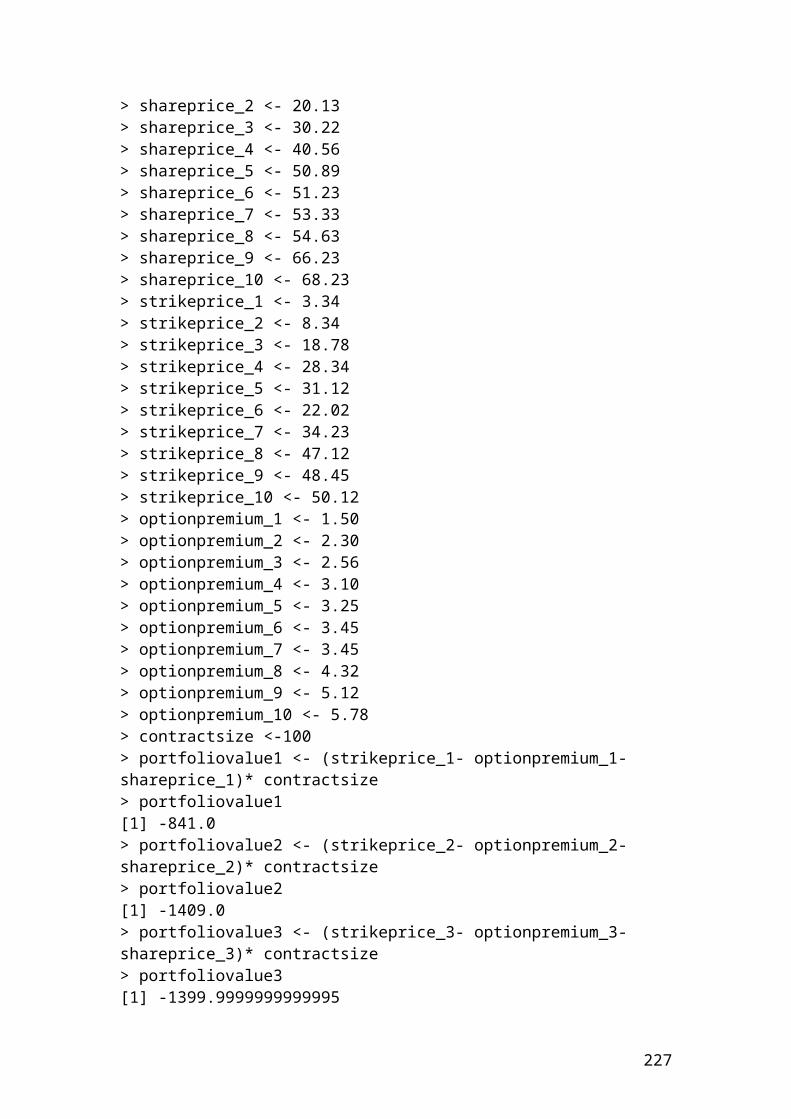

Example of profit or loss of a put option portfolio. The figures are expressed in Euro

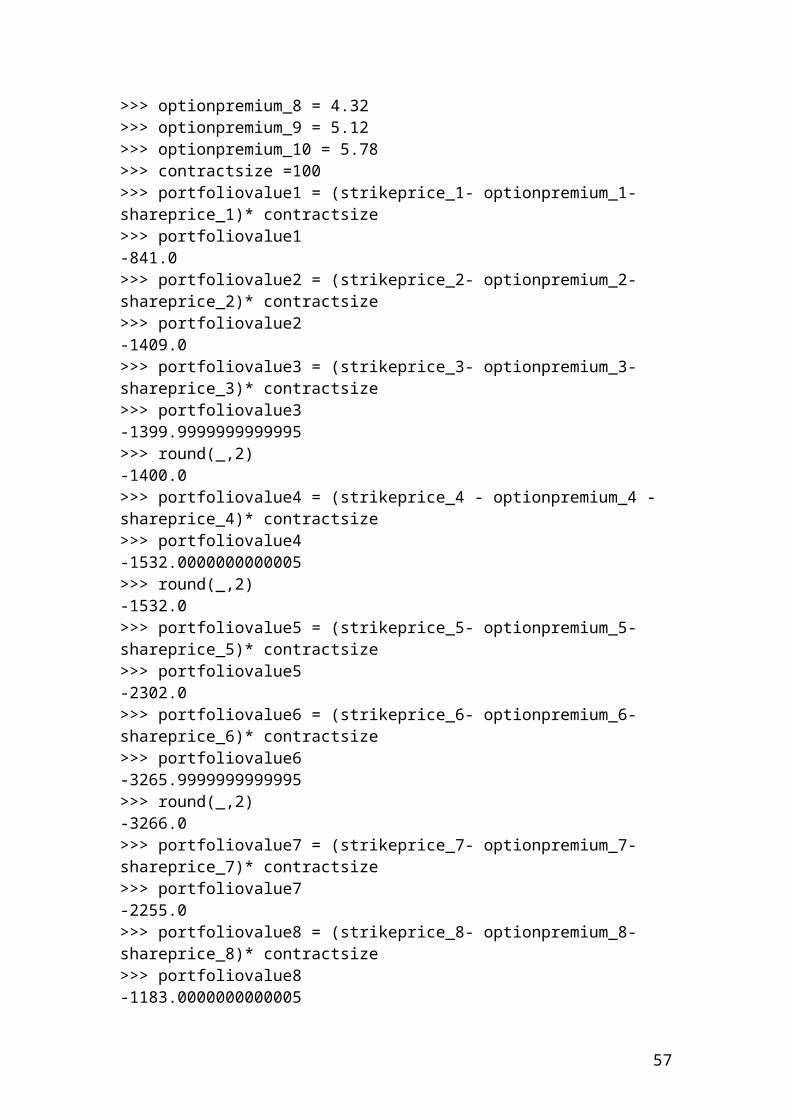

>>> shareprice_1 = 10.25>>> shareprice_2 = 20.13>>> shareprice_3 = 30.22>>> shareprice_4 = 40.56>>> shareprice_5 = 50.89>>> shareprice_6 = 51.23>>> shareprice_7 = 53.33>>> shareprice_8 = 54.63>>> shareprice_9 = 66.23>>> shareprice_10 = 68.23>>> strikeprice_1 = 3.34>>> strikeprice_2 = 8.34>>> strikeprice_3 = 18.78>>> strikeprice_4 = 28.34>>> strikeprice_5 = 31.12>>> strikeprice_6 = 22.02>>> strikeprice_7 = 34.23>>> strikeprice_8 = 47.12>>> strikeprice_9 = 48.45

43

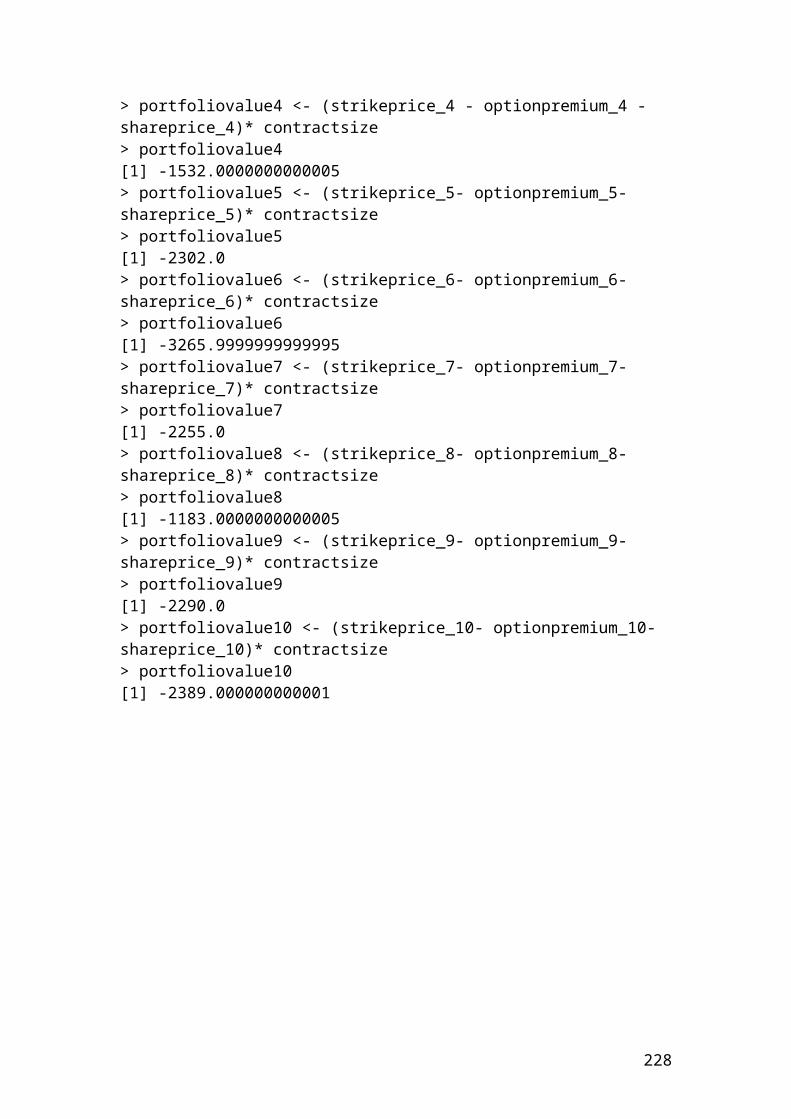

>>> strikeprice_10 = 50.12>>> optionpremium_1 = 1.50>>> optionpremium_2 = 2.30>>> optionpremium_3 = 2.56>>> optionpremium_4 = 3.10>>> optionpremium_5 = 3.25>>> optionpremium_6 = 3.45>>> optionpremium_7 = 3.45>>> optionpremium_8 = 4.32>>> optionpremium_9 = 5.12>>> optionpremium_10 = 5.78>>> contractsize =100>>> portfoliovalue1 = (strikeprice_1- optionpremium_1-shareprice_1)* contractsize>>> portfoliovalue1-841.0>>> portfoliovalue2 = (strikeprice_2- optionpremium_2- shareprice_2)* contractsize>>> portfoliovalue2-1409.0>>> portfoliovalue3 = (strikeprice_3- optionpremium_3- shareprice_3)* contractsize>>> portfoliovalue3-1399.9999999999995>>> round(_,2)-1400.0>>> portfoliovalue4 = (strikeprice_4 - optionpremium_4 - shareprice_4)* contractsize>>> portfoliovalue4-1532.0000000000005>>> round(_,2)-1532.0>>> portfoliovalue5 = (strikeprice_5- optionpremium_5- shareprice_5)* contractsize>>> portfoliovalue5-2302.0>>> portfoliovalue6 = (strikeprice_6- optionpremium_6- shareprice_6)* contractsize>>> portfoliovalue6-3265.9999999999995>>> round(_,2)-3266.0>>> portfoliovalue7 = (strikeprice_7- optionpremium_7- shareprice_7)* contractsize>>> portfoliovalue7-2255.0>>> portfoliovalue8 = (strikeprice_8- optionpremium_8- shareprice_8)* contractsize>>> portfoliovalue8-1183.0000000000005>>> round(_,2)-1183.0>>> portfoliovalue9 = (strikeprice_9- optionpremium_9- shareprice_9)* contractsize>>> portfoliovalue9-2290.0>>> portfoliovalue10 = (strikeprice_10- optionpremium_10- shareprice_10)* contractsize>>> portfoliovalue10

44

-2389.000000000001>>> round(_,2)-2389.0

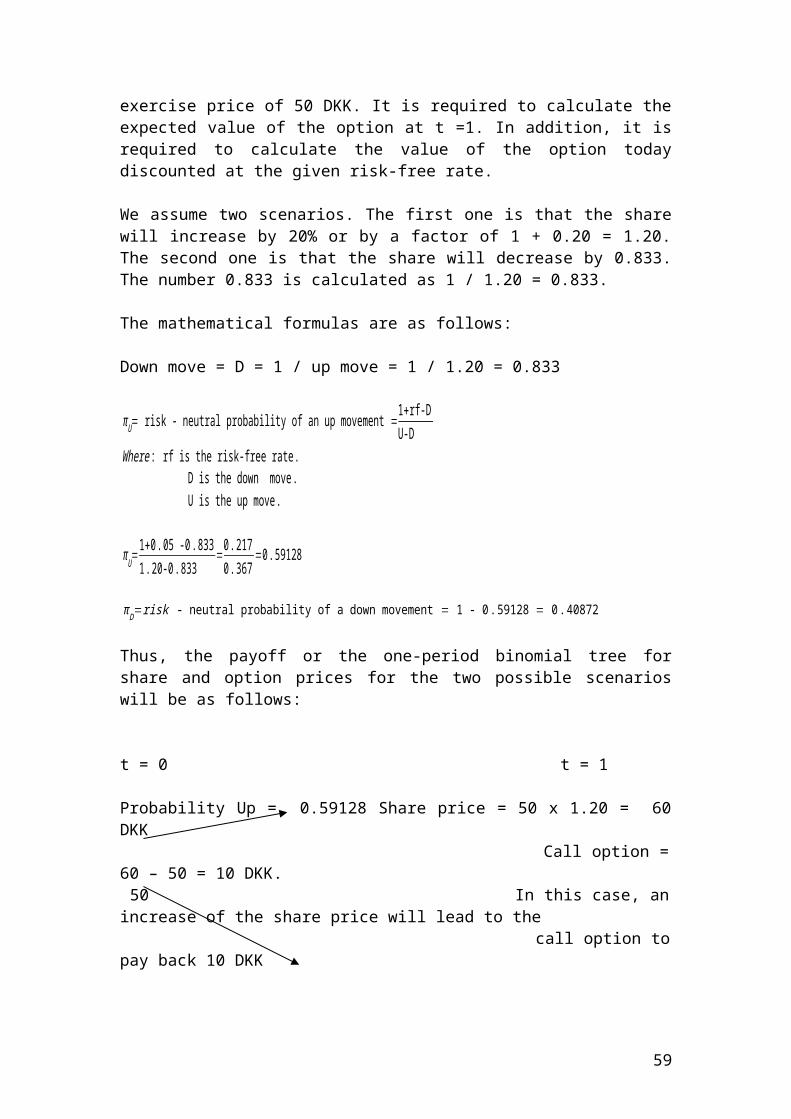

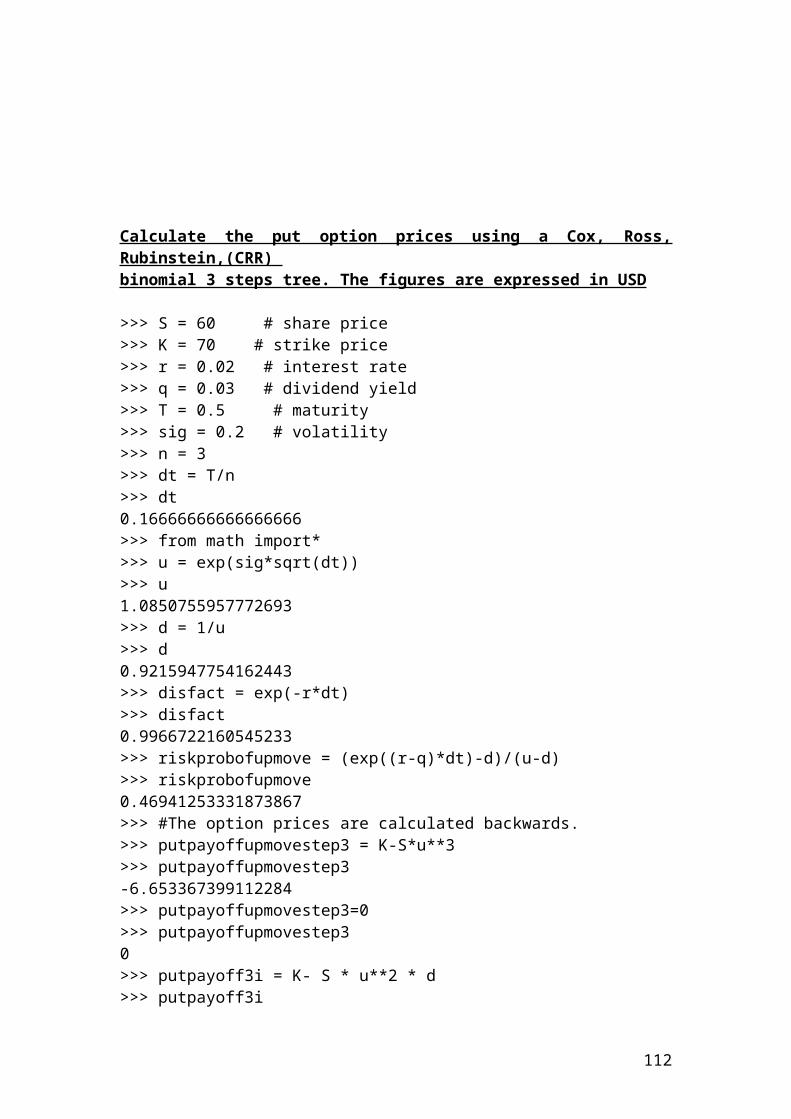

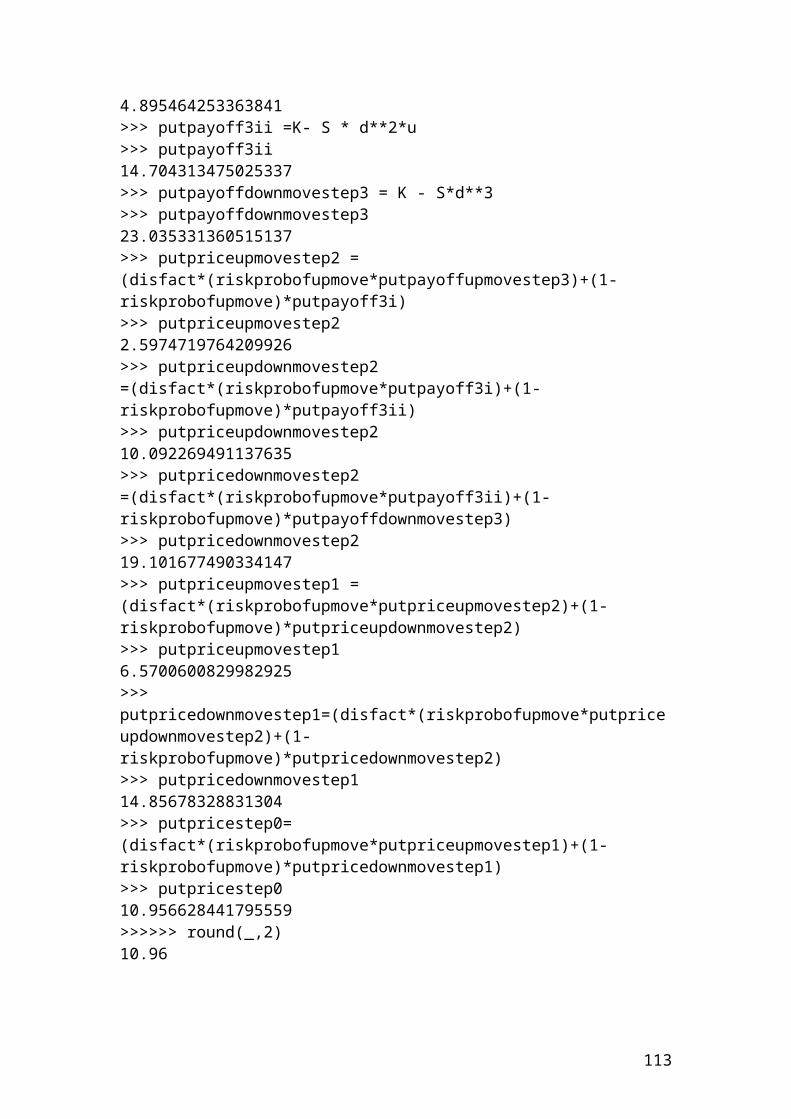

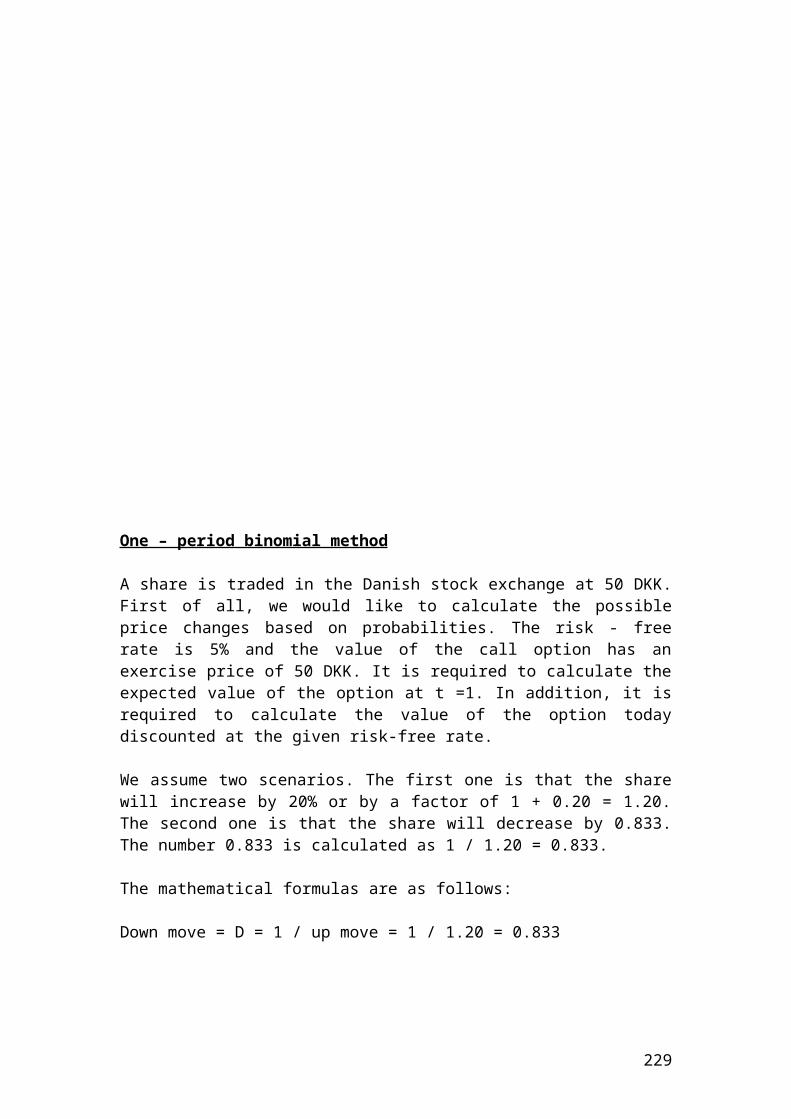

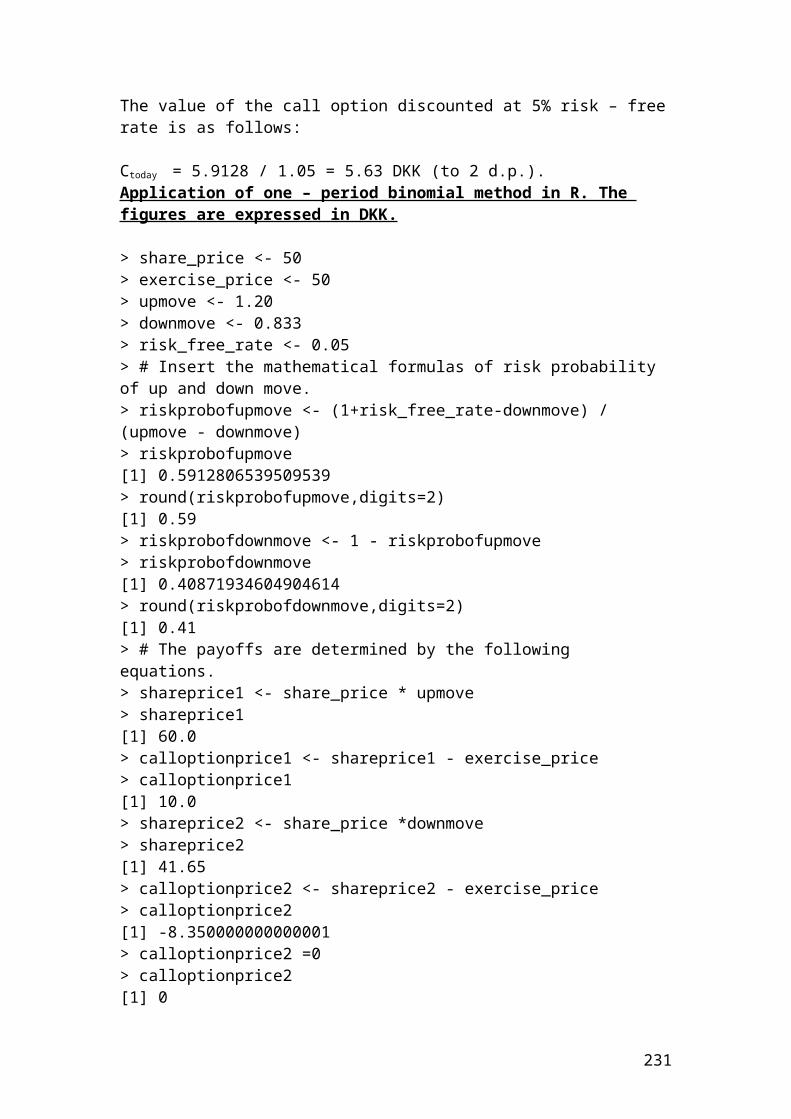

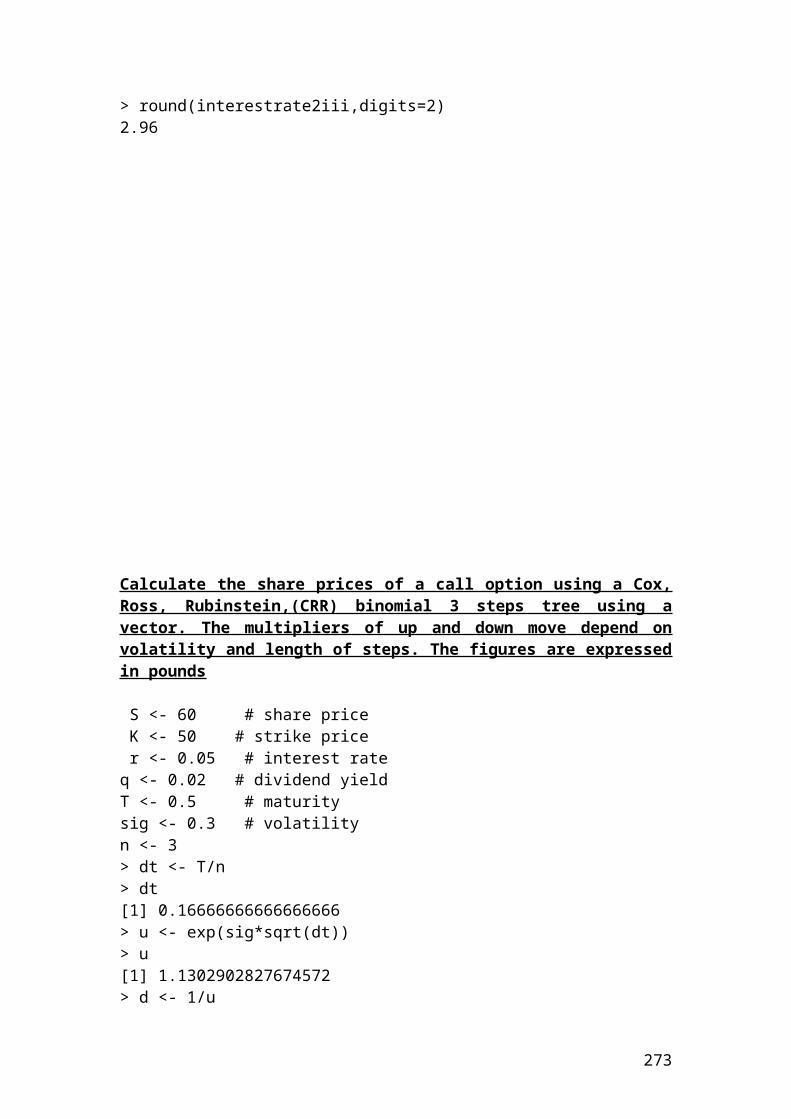

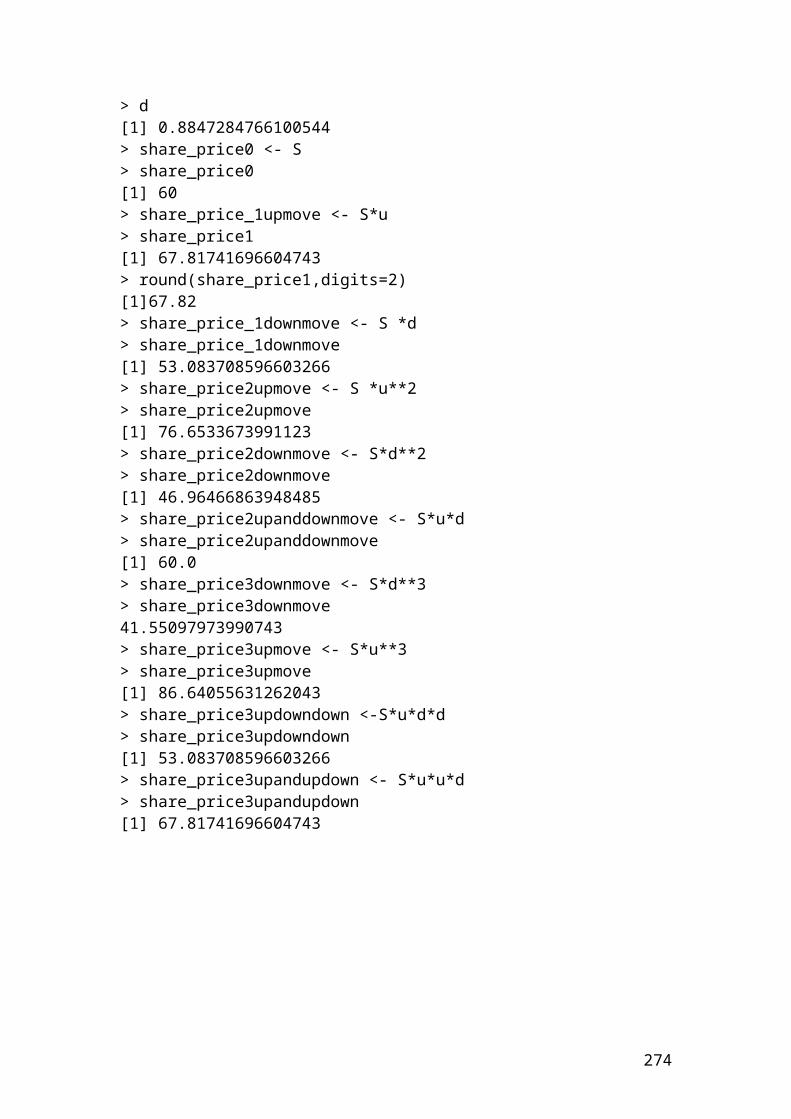

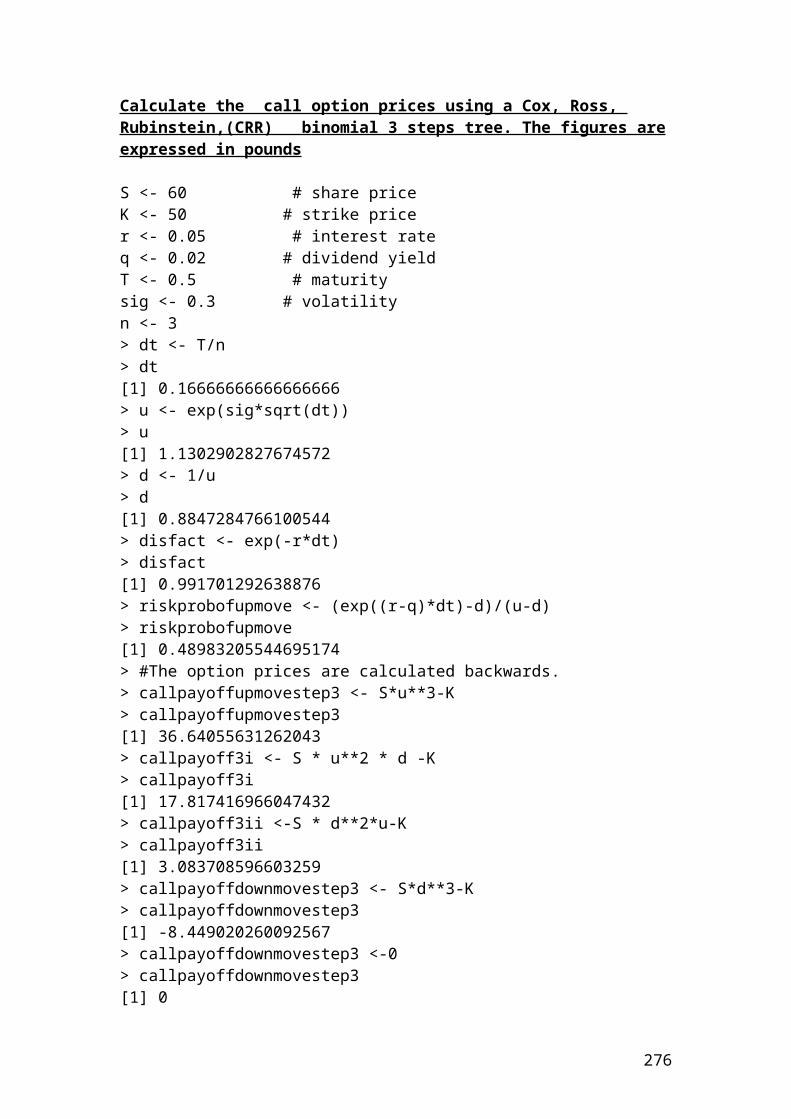

One – period binomial method

A share is traded in the Danish stock exchange at 50 DKK. First of all, we would like to calculate the possible price changes based on probabilities. The risk - free rate is 5% and the value of the call option has an exercise price of 50 DKK. It is required to calculate the expected value of the option at t =1. In addition, it is required to calculate the value of the option today discounted at the given risk-free rate.

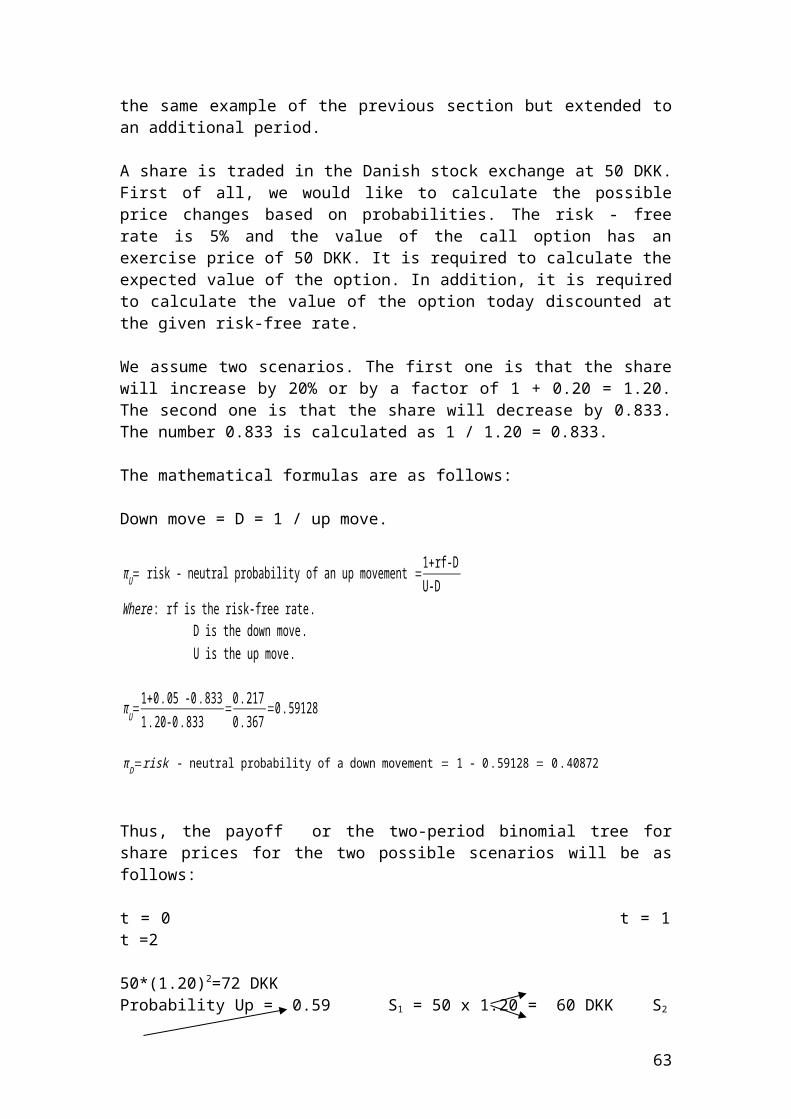

We assume two scenarios. The first one is that the share will increase by 20% or by a factor of 1 + 0.20 = 1.20. The second one is that the share will decrease by 0.833. The number 0.833 is calculated as 1 / 1.20 = 0.833.

The mathematical formulas are as follows:

Down move = D = 1 / up move = 1 / 1.20 = 0.833

45

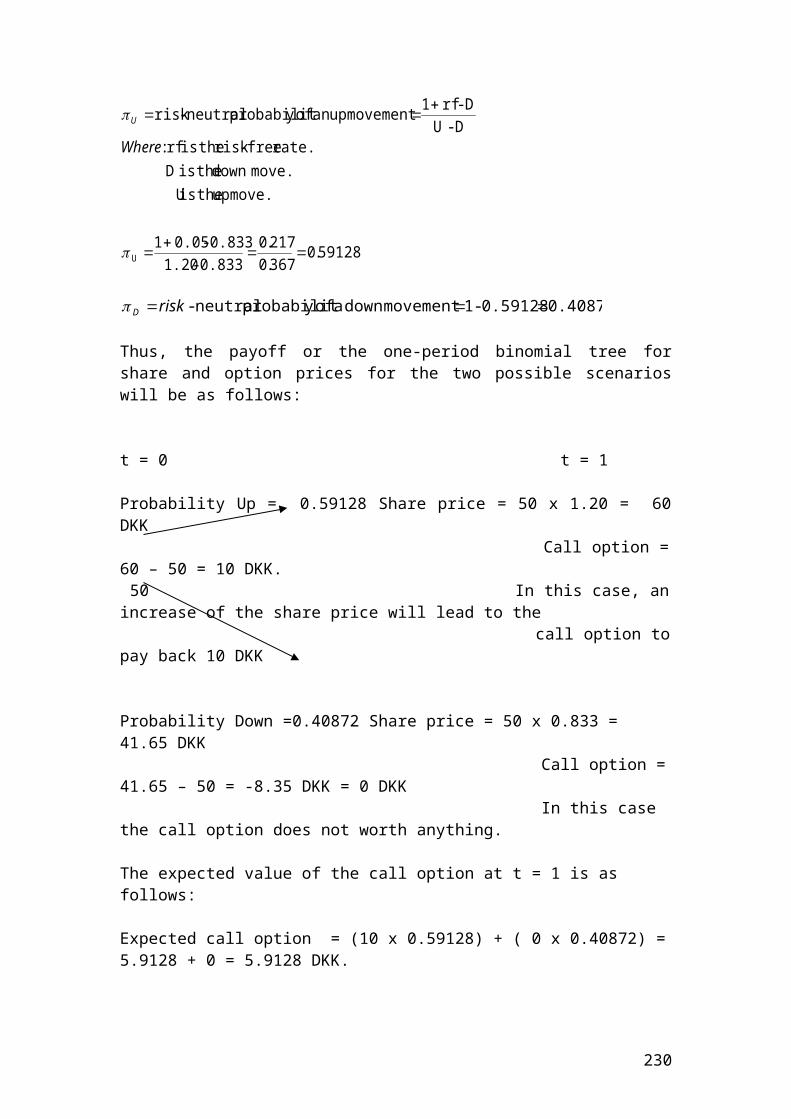

πU= risk - neutral probability of an up movement =1+ rf-DU-D

Where : rf is the risk-free rate . D is the down move . U is the up move.

πU=1+0 . 05 -0 .8331 .20-0 .833

=0 .2170 .367

=0 .59128

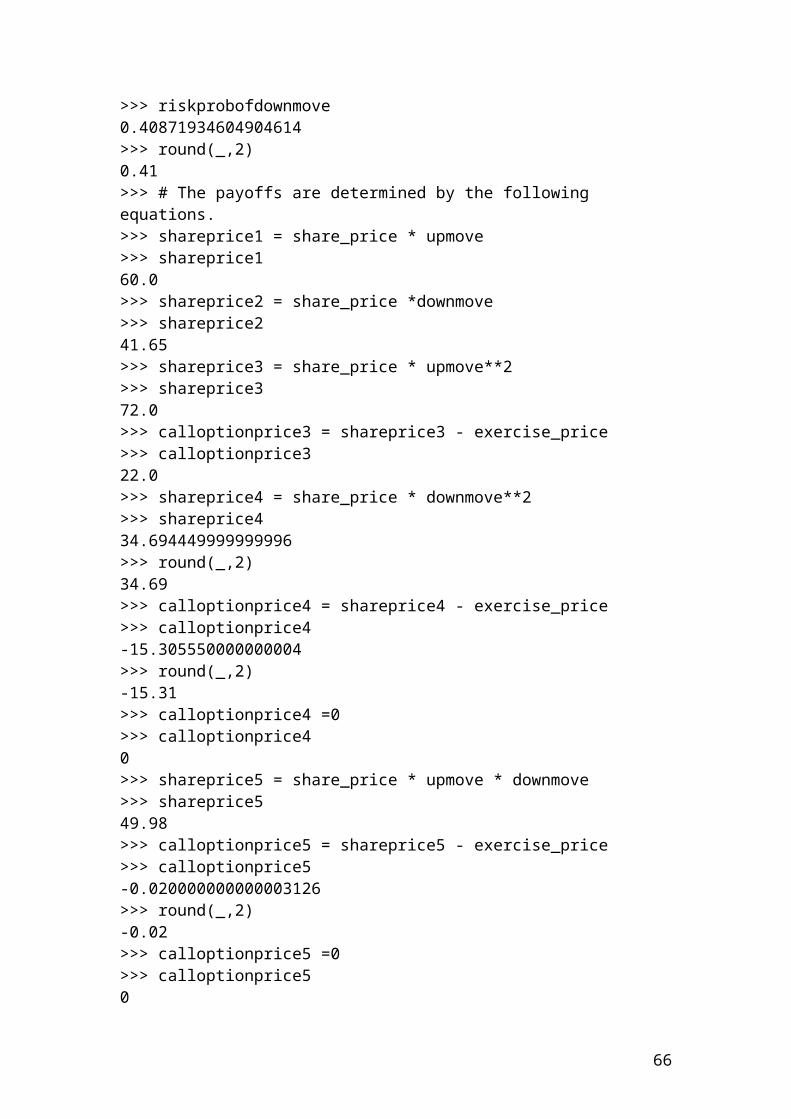

π D=risk - neutral probability of a down movement = 1 - 0 .59128 = 0 . 40872

Thus, the payoff or the one-period binomial tree for share and option prices for the two possible scenarios will be as follows:

t = 0 t = 1

Probability Up = 0.59128 Share price = 50 x 1.20 = 60 DKK Call option = 60 – 50 = 10 DKK. 50 In this case, an increase of the share price will lead to the call option to pay back 10 DKK Probability Down =0.40872 Share price = 50 x 0.833 = 41.65 DKK Call option = 41.65 – 50 = -8.35 DKK = 0 DKK In this case the call option does not worth anything.

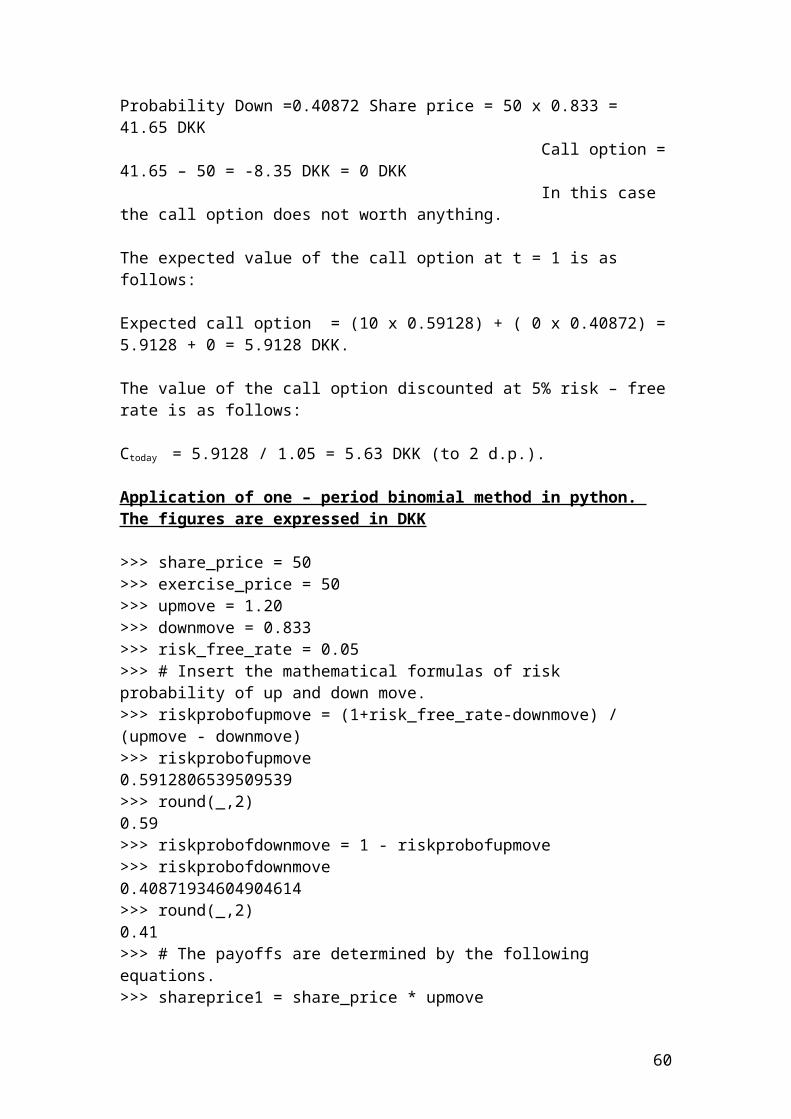

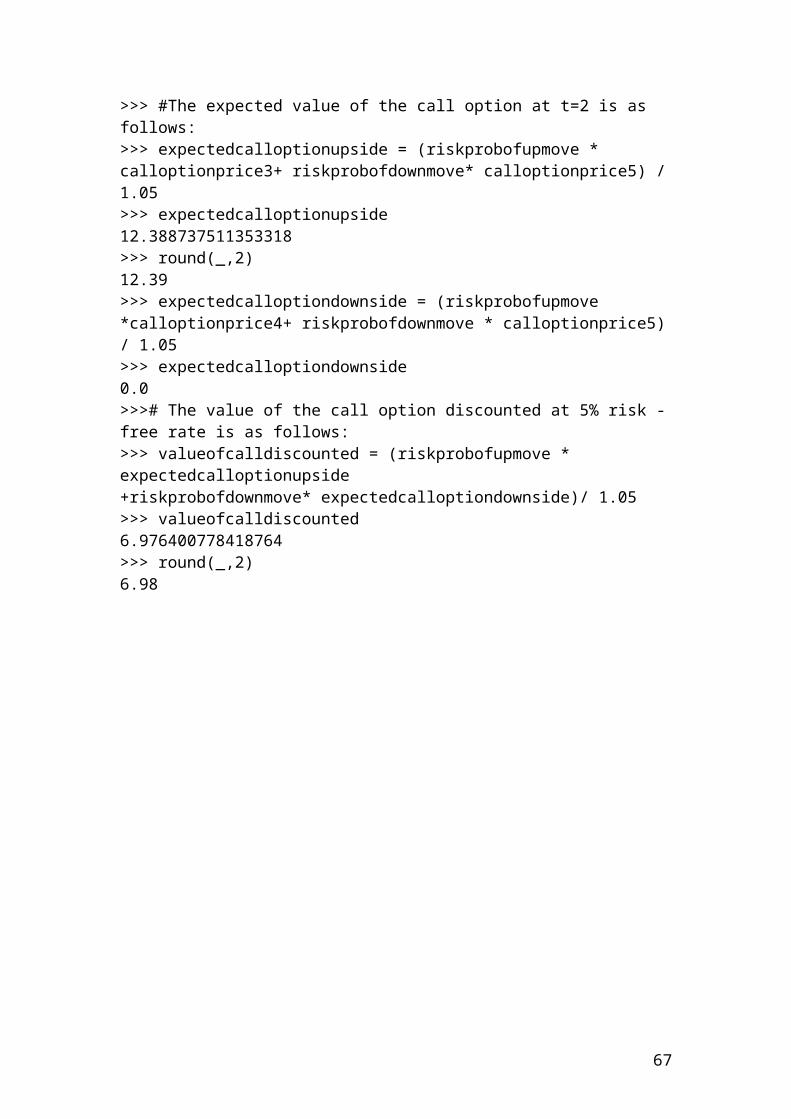

The expected value of the call option at t = 1 is as follows:

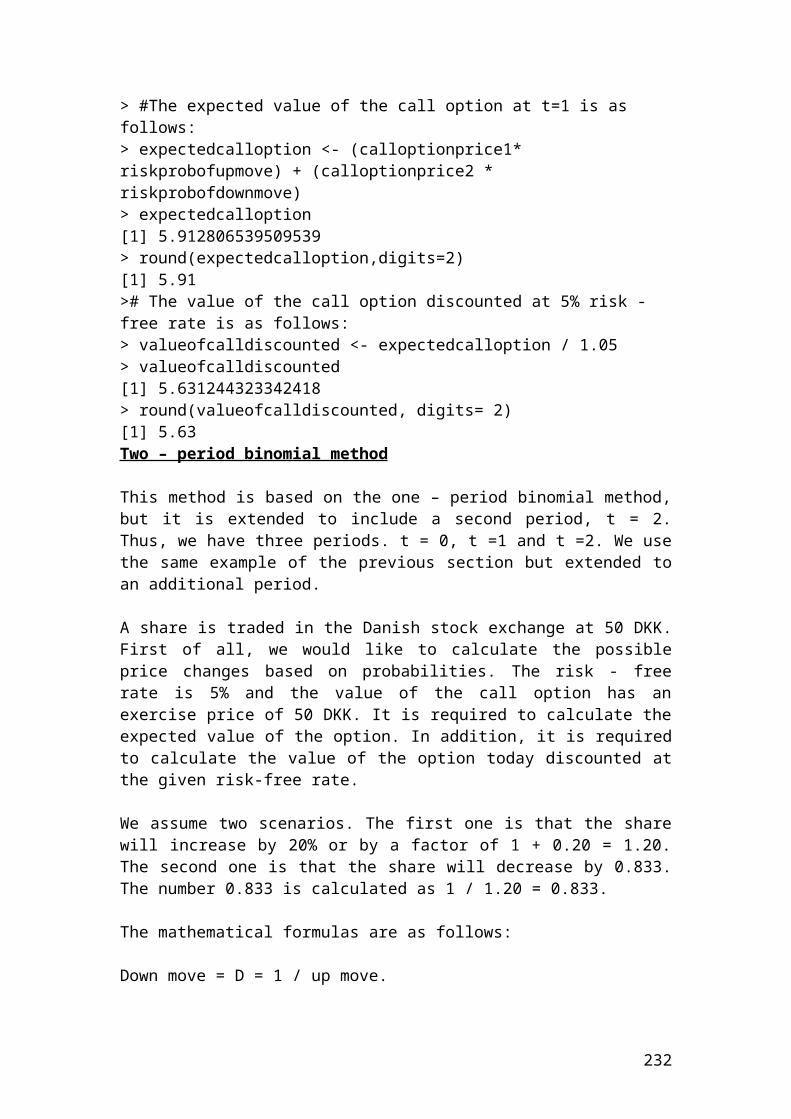

Expected call option = (10 x 0.59128) + ( 0 x 0.40872) = 5.9128 + 0 = 5.9128 DKK.

The value of the call option discounted at 5% risk – free rate is as follows:

Ctoday = 5.9128 / 1.05 = 5.63 DKK (to 2 d.p.).

Application of one – period binomial method in python. The figures are expressed in DKK

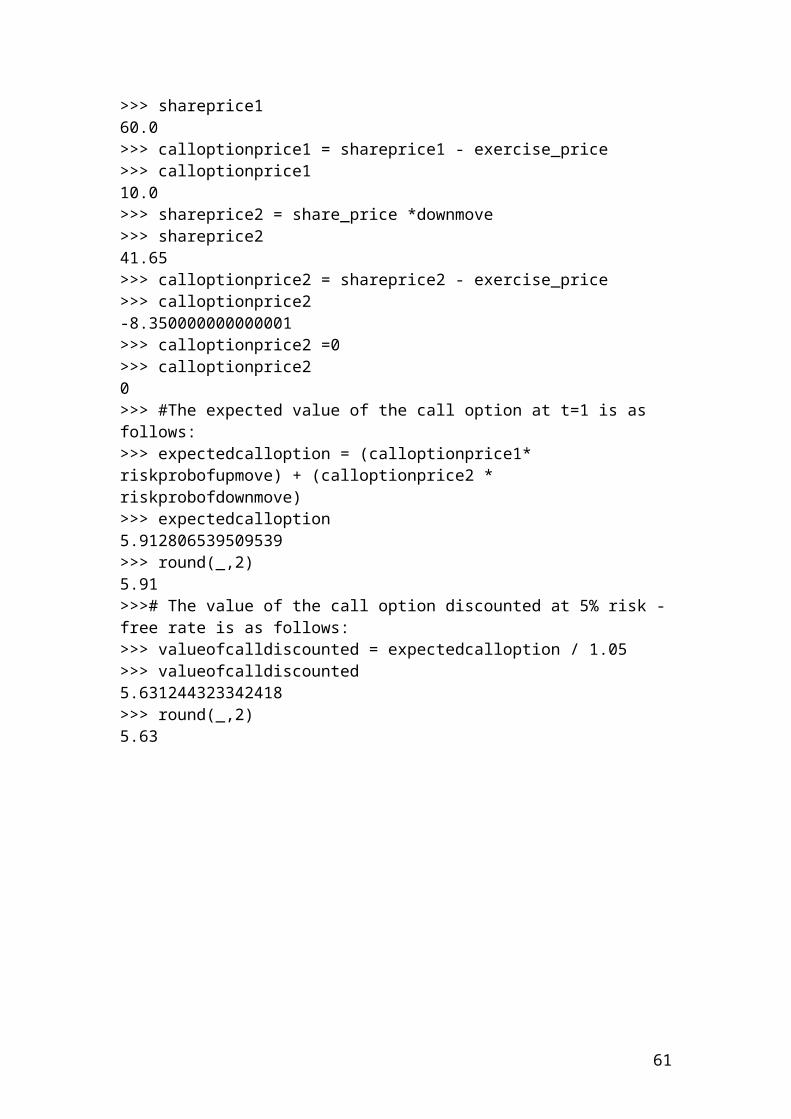

>>> share_price = 50>>> exercise_price = 50>>> upmove = 1.20>>> downmove = 0.833>>> risk_free_rate = 0.05>>> # Insert the mathematical formulas of risk probability of up and down move.>>> riskprobofupmove = (1+risk_free_rate-downmove) / (upmove - downmove)>>> riskprobofupmove0.5912806539509539>>> round(_,2)

46

0.59>>> riskprobofdownmove = 1 - riskprobofupmove>>> riskprobofdownmove0.40871934604904614>>> round(_,2)0.41>>> # The payoffs are determined by the following equations.>>> shareprice1 = share_price * upmove>>> shareprice160.0>>> calloptionprice1 = shareprice1 - exercise_price>>> calloptionprice110.0>>> shareprice2 = share_price *downmove>>> shareprice241.65>>> calloptionprice2 = shareprice2 - exercise_price>>> calloptionprice2-8.350000000000001>>> calloptionprice2 =0>>> calloptionprice20>>> #The expected value of the call option at t=1 is as follows:>>> expectedcalloption = (calloptionprice1* riskprobofupmove) + (calloptionprice2 * riskprobofdownmove)>>> expectedcalloption5.912806539509539>>> round(_,2)5.91>>># The value of the call option discounted at 5% risk - free rate is as follows:>>> valueofcalldiscounted = expectedcalloption / 1.05>>> valueofcalldiscounted5.631244323342418>>> round(_,2)5.63

47

Two – period binomial method

This method is based on the one – period binomial method, but it is extended to include a second period, t = 2. Thus, we have three periods. t = 0, t =1 and t =2. We use the same example of the previous section but extended to an additional period.

A share is traded in the Danish stock exchange at 50 DKK. First of all, we would like to calculate the possible price changes based on probabilities. The risk - free rate is 5% and the value of the call option has an exercise price of 50 DKK. It is required to calculate the expected value of the option. In addition, it is required to calculate the value of the option today discounted at the given risk-free rate.

We assume two scenarios. The first one is that the share will increase by 20% or by a factor of 1 + 0.20 = 1.20. The second one is that the share will decrease by 0.833. The number 0.833 is calculated as 1 / 1.20 = 0.833.

48

The mathematical formulas are as follows:

Down move = D = 1 / up move.

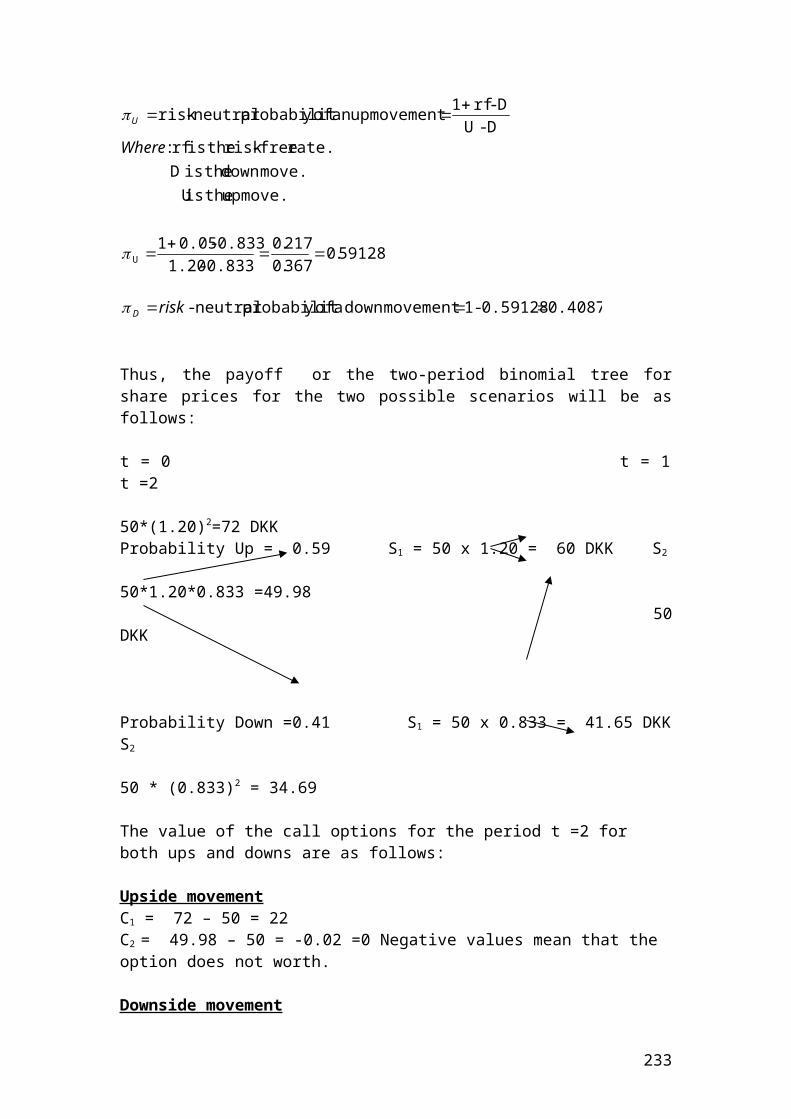

πU= risk - neutral probability of an up movement =1+ rf-DU-D

Where : rf is the risk-free rate . D is the down move . U is the up move.

πU=1+0 . 05 -0 .8331 .20-0 .833

=0 . 2170 . 367

=0 .59128

π D=risk - neutral probability of a down movement = 1 - 0 .59128 = 0 . 40872

Thus, the payoff or the two-period binomial tree for share prices for the two possible scenarios will be as follows:

t = 0 t = 1 t =2 50*(1.20)2=72 DKKProbability Up = 0.59 S1 = 50 x 1.20 = 60 DKK S2 50*1.20*0.833 =49.98 50 DKK Probability Down =0.41 S1 = 50 x 0.833 = 41.65 DKK S2

50 * (0.833)2 = 34.69

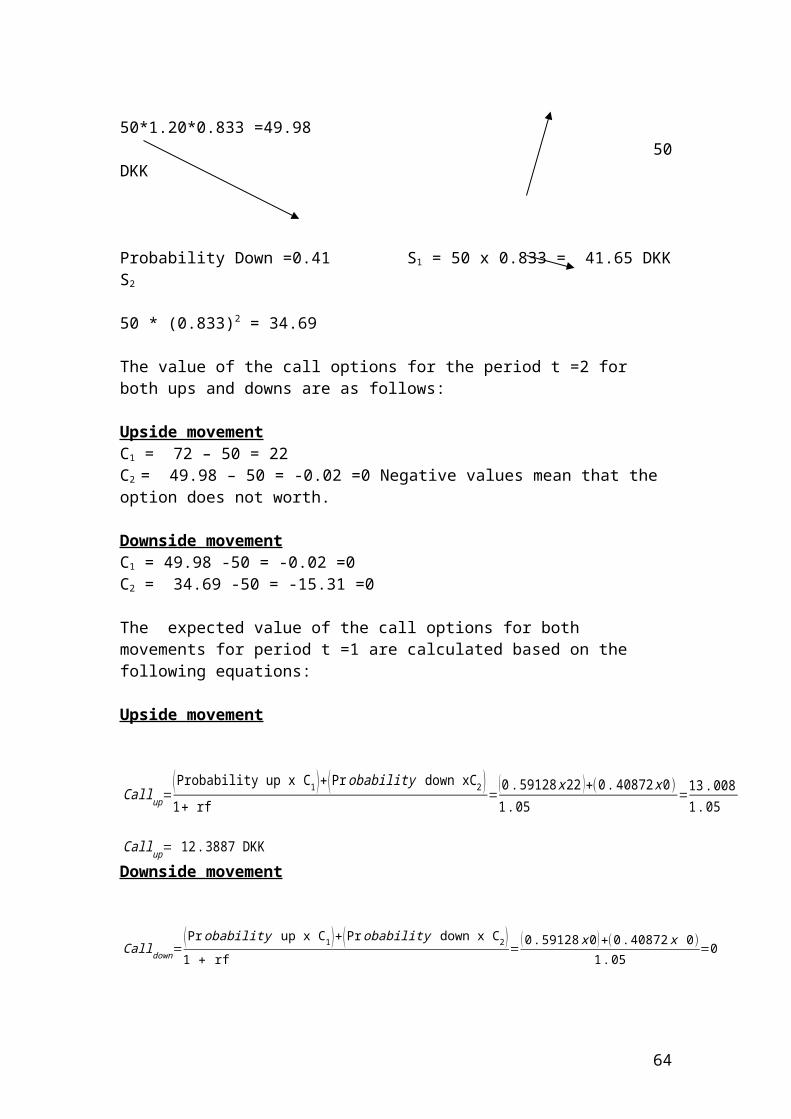

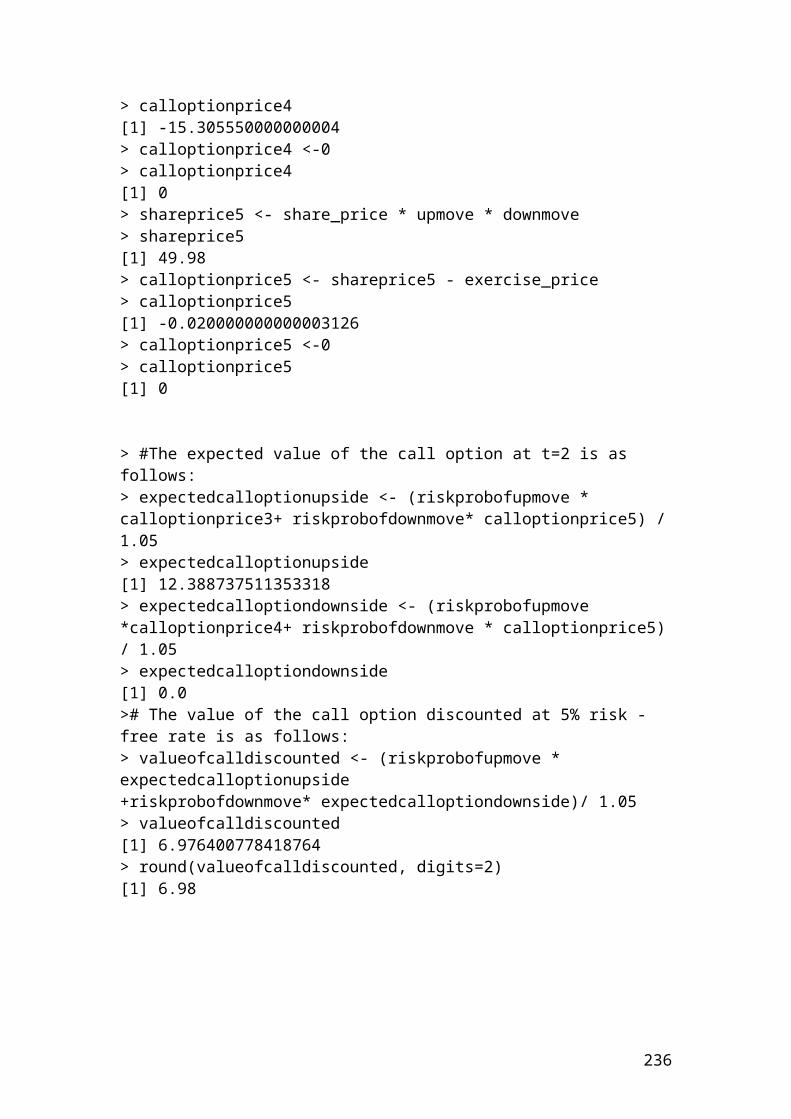

The value of the call options for the period t =2 for both ups and downs are as follows:

Upside movementC1 = 72 – 50 = 22C2 = 49.98 – 50 = -0.02 =0 Negative values mean that the option does not worth.

Downside movementC1 = 49.98 -50 = -0.02 =0C2 = 34.69 -50 = -15.31 =0

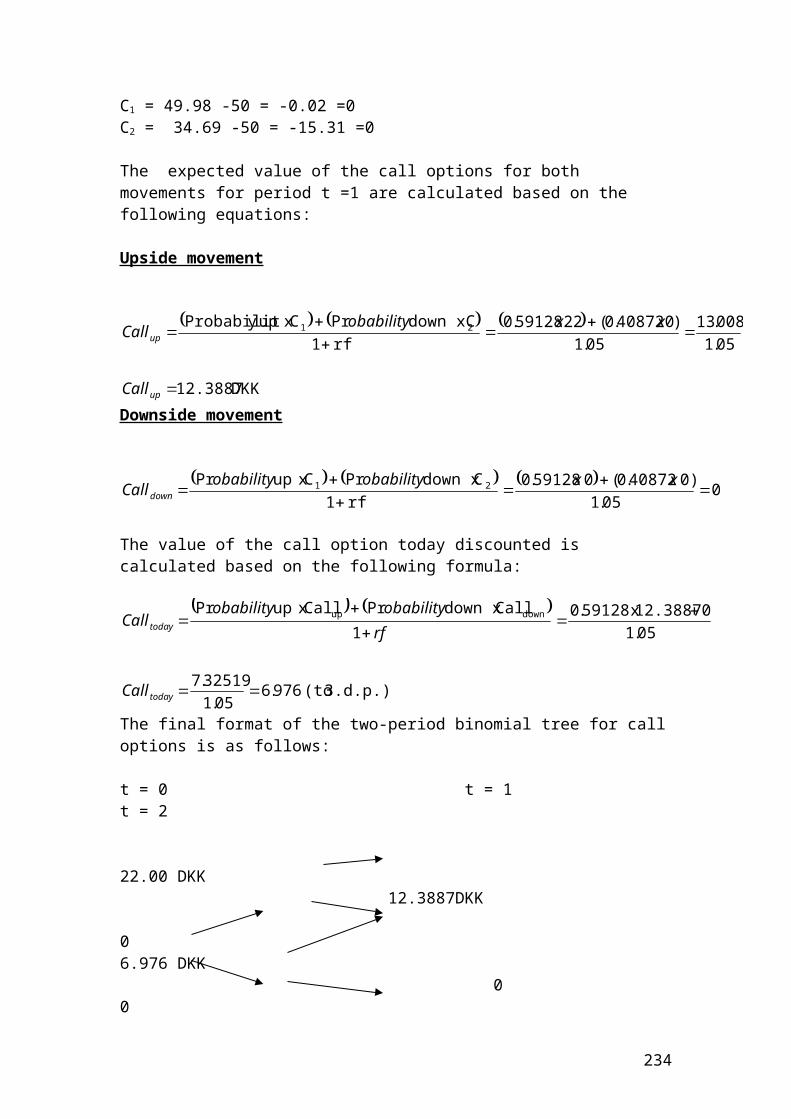

The expected value of the call options for both movements for period t =1 are calculated based on the following equations:

Upside movement

49

Callup=( Probability up x C1 )+( Probability down xC2 )1+ rf

=(0 .59128 x 22 )+(0 . 40872 x 0)1. 05

=13 .0081. 05

Callup= 12 .3887 DKKDownside movement

Calldown=( Pr obability up x C1 )+( Probability down x C2 )1 + rf

=(0 .59128 x0 )+(0 .40872 x 0)

1 .05=0

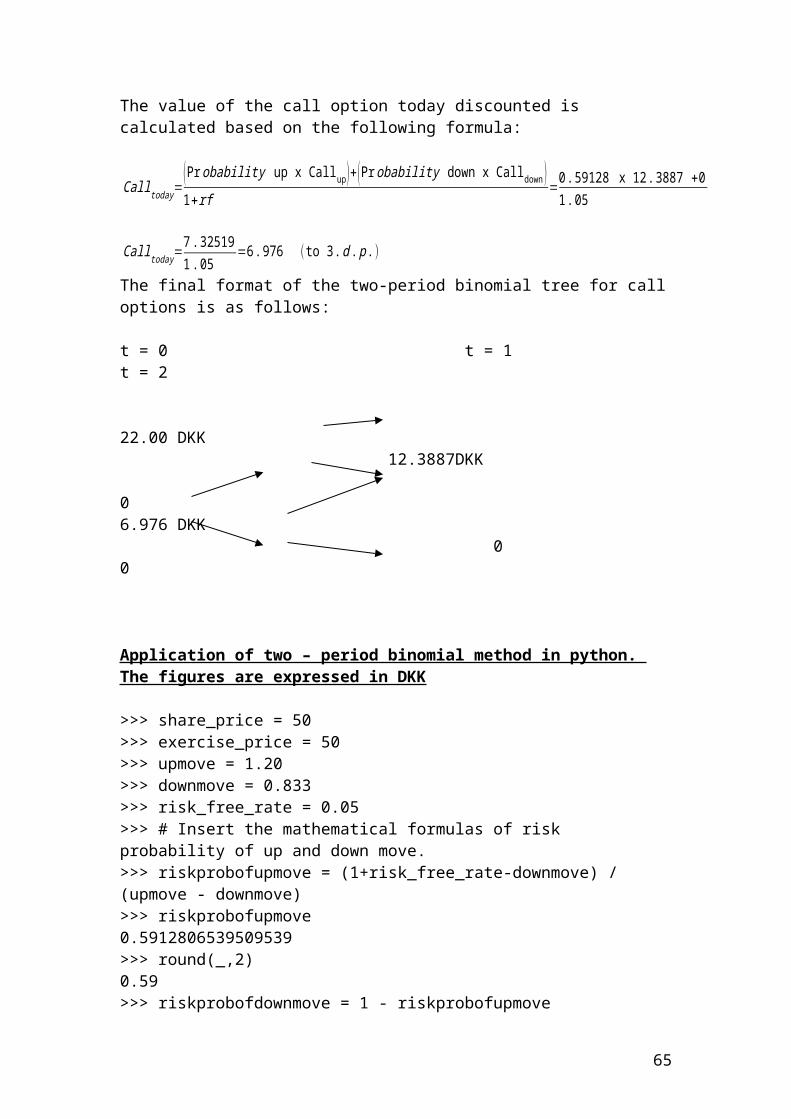

The value of the call option today discounted is calculated based on the following formula:

Calltoday=(Pr obability up x Callup )+( Pr obability down x Calldown )1+rf

=0. 59128 x 12 . 3887 +01 . 05

Calltoday=7 .325191. 05

=6 .976 ( to 3 . d . p .)

The final format of the two-period binomial tree for call options is as follows:

t = 0 t = 1 t = 2

22.00 DKK 12.3887DKK 06.976 DKK 0 0

Application of two – period binomial method in python. The figures are expressed in DKK

>>> share_price = 50>>> exercise_price = 50>>> upmove = 1.20>>> downmove = 0.833>>> risk_free_rate = 0.05>>> # Insert the mathematical formulas of risk probability of up and down move.>>> riskprobofupmove = (1+risk_free_rate-downmove) / (upmove - downmove)>>> riskprobofupmove0.5912806539509539>>> round(_,2)0.59>>> riskprobofdownmove = 1 - riskprobofupmove>>> riskprobofdownmove0.40871934604904614>>> round(_,2)

50

0.41>>> # The payoffs are determined by the following equations.>>> shareprice1 = share_price * upmove>>> shareprice160.0>>> shareprice2 = share_price *downmove>>> shareprice241.65>>> shareprice3 = share_price * upmove**2>>> shareprice372.0>>> calloptionprice3 = shareprice3 - exercise_price>>> calloptionprice322.0>>> shareprice4 = share_price * downmove**2>>> shareprice434.694449999999996>>> round(_,2)34.69>>> calloptionprice4 = shareprice4 - exercise_price>>> calloptionprice4-15.305550000000004>>> round(_,2)-15.31>>> calloptionprice4 =0>>> calloptionprice40>>> shareprice5 = share_price * upmove * downmove>>> shareprice549.98>>> calloptionprice5 = shareprice5 - exercise_price>>> calloptionprice5-0.020000000000003126>>> round(_,2)-0.02>>> calloptionprice5 =0>>> calloptionprice50>>> #The expected value of the call option at t=2 is as follows:>>> expectedcalloptionupside = (riskprobofupmove * calloptionprice3+ riskprobofdownmove* calloptionprice5) / 1.05>>> expectedcalloptionupside12.388737511353318>>> round(_,2)12.39>>> expectedcalloptiondownside = (riskprobofupmove *calloptionprice4+ riskprobofdownmove * calloptionprice5) / 1.05>>> expectedcalloptiondownside0.0>>># The value of the call option discounted at 5% risk - free rate is as follows:

51

>>> valueofcalldiscounted = (riskprobofupmove * expectedcalloptionupside+riskprobofdownmove* expectedcalloptiondownside)/ 1.05>>> valueofcalldiscounted6.976400778418764>>> round(_,2)6.98

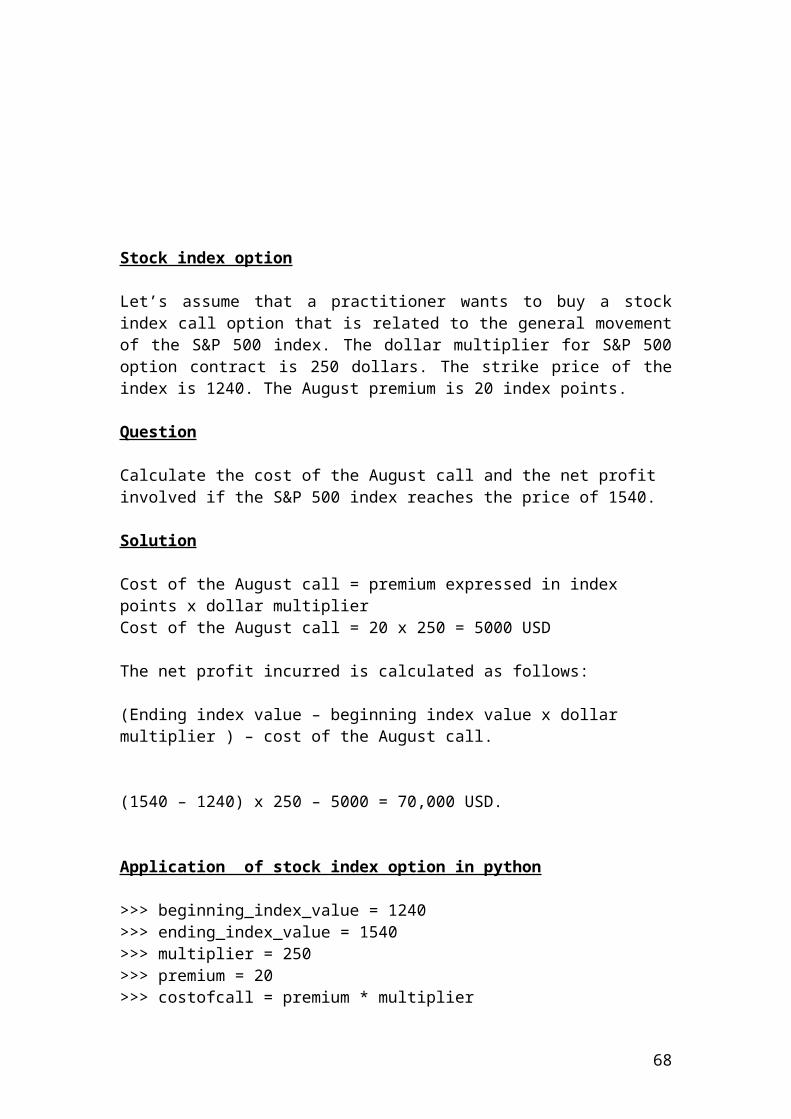

Stock index option

Let’s assume that a practitioner wants to buy a stock index call option that is related to the general movement of the S&P 500 index. The dollar multiplier for S&P 500 option contract is 250 dollars. The strike price of the index is 1240. The August premium is 20 index points.

Question

Calculate the cost of the August call and the net profit involved if the S&P 500 index reaches the price of 1540.

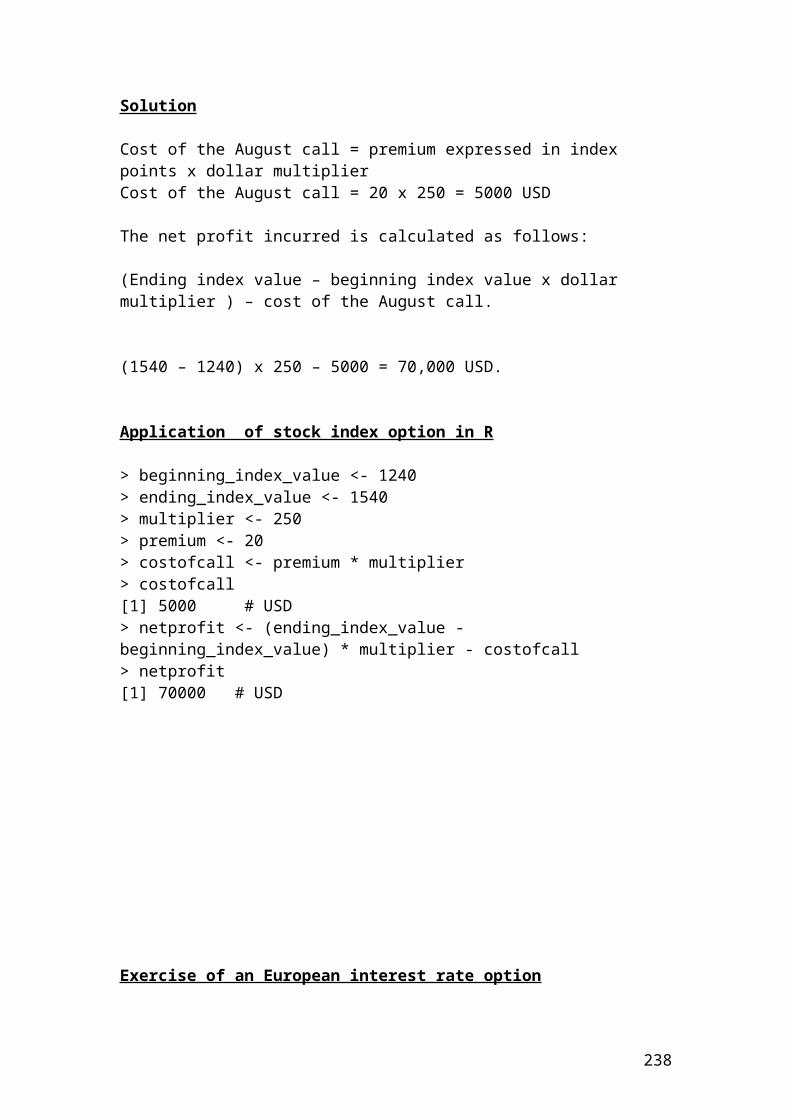

Solution

Cost of the August call = premium expressed in index points x dollar multiplier Cost of the August call = 20 x 250 = 5000 USD

The net profit incurred is calculated as follows:

52

(Ending index value – beginning index value x dollar multiplier ) – cost of the August call.

(1540 – 1240) x 250 – 5000 = 70,000 USD.

Application of stock index option in python

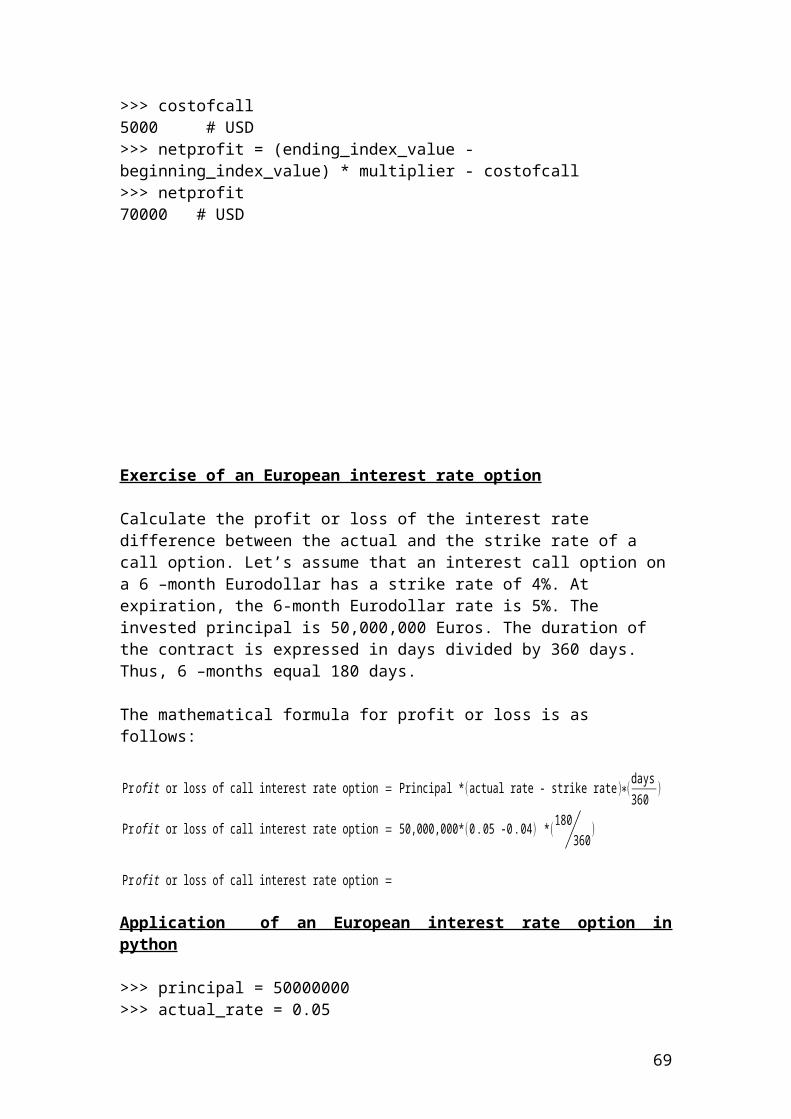

>>> beginning_index_value = 1240>>> ending_index_value = 1540>>> multiplier = 250>>> premium = 20>>> costofcall = premium * multiplier>>> costofcall5000 # USD>>> netprofit = (ending_index_value - beginning_index_value) * multiplier - costofcall>>> netprofit70000 # USD

Exercise of an European interest rate option

Calculate the profit or loss of the interest rate difference between the actual and the strike rate of a call option. Let’s assume that an interest call option on a 6 –month Eurodollar has a strike rate of 4%. At expiration, the 6-month Eurodollar rate is 5%. The invested principal is 50,000,000 Euros. The duration of the contract is expressed in days divided by 360 days. Thus, 6 –months equal 180 days.

The mathematical formula for profit or loss is as follows:

Pr ofit or loss of call interest rate option = Principal * (actual rate - strike rate)∗(days360

)

Pr ofit or loss of call interest rate option = 50,000,000*(0 .05 -0 .04 ) *(180360)

Pr ofit or loss of call interest rate option =

53

Application of an European interest rate option in python

>>> principal = 50000000>>> actual_rate = 0.05>>> strike_rate = 0.04>>> duration = 180>>> days = 360>>> # Insert the mathematical formula.>>> profitorloss =principal*(actual_rate - strike_rate)*duration/days>>> profitorloss250000.00000000003>>> round(_,2)250000.0 # Euros

Currency option

Let’s assume that a wealthy investor buys a call currency option because it expects a rise in the exchange rate parity of the EURO against the USD, EURO/USD. The spot exchange rate is 1/1.3568. The strike price is 1.3568. The premium expressed as cents per Euro is 1.56. The initial principal is 100,000 USD.

Question

Calculate the net profit involved if the strike price increases to 1.3987.

Solution

The wealthy investor to record a profit, he or she should add to the strike price 1.3568 the premium expressed as cents per Euro. In our case, the breakeven point is1.3568 + 0.0156 = 1.3724. Above the price of 1.3724, he or she starts to record a profit. If the strike price reaches 1.3987, then the profit will be as follows:

54

Initial principal x (Ending strike price – beginning strike price – premium paid) =100,000 x (1.3987 – 1.3568 – 0.0156) = 2630 USD net profit

Application of currency option in python

>>> principal = 100000>>> ending_strike_price = 1.3987>>> beginning_strike_price = 1.3568>>> premiumpaid = 0.0156>>> netprofit = principal *(ending_strike_price-beginning_strike_price-premiumpaid)>>> netprofit2630.000000000005>>> round(_,2)2630.0 # USD

Example of calculating the payments of an interest rate cap based on different LIBOR rates

Interest rate cap is an agreement between two parties where one party pay the other at a specified period of time in which the interest rate or London interbank offered rate ,LIBOR, exceeds the strike price. It is used this contract to hedge against interest rate fluctuations. Let’s assume that an interest cap has a value of 5.5% and the LIBOR prices for the next three years are 7.5%, 8.3% and 4.65%. The principal is $50,000,000 and the payments take place semiannually.

The mathematical formula that is used to calculate the payments of each year is as follows:

Interest rate payment =[ principal x (LIBOR rate – cap rate)/0.5]

Therefore, the first year interest rate payment is as follows:

Year 1

55

Interest rate payment = [50,000,000 x (0.075 – 0.055)/2] = $ ………

Application of payments of an interest rate cap based on different LIBOR rates in python

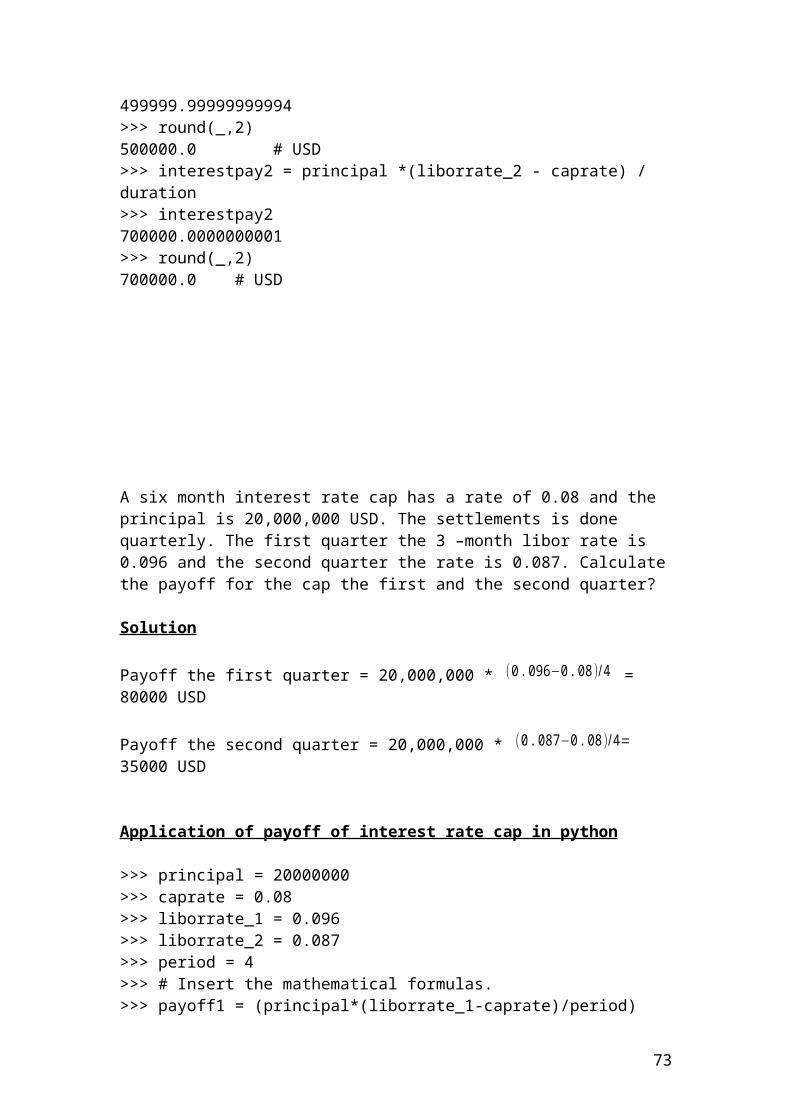

>>> principal = 50000000>>> liborrate_1 = 0.075>>> liborrate_2 = 0.083>>> caprate = 0.055>>> duration = 2>>> interestpay1 = principal *(liborrate_1 - caprate) /duration>>> interestpay1499999.99999999994>>> round(_,2)500000.0 # USD>>> interestpay2 = principal *(liborrate_2 - caprate) / duration>>> interestpay2700000.0000000001>>> round(_,2)700000.0 # USD

A six month interest rate cap has a rate of 0.08 and the principal is 20,000,000 USD. The settlements is done quarterly. The first quarter the 3 –month libor rate is 0.096 and the second quarter the rate is 0.087. Calculate the payoff for the cap the first and the second quarter?

Solution

Payoff the first quarter = 20,000,000 * (0 . 096−0. 08 )/4 = 80000 USD

Payoff the second quarter = 20,000,000 * (0 .087−0. 08 )/4=35000 USD

Application of payoff of interest rate cap in python

>>> principal = 20000000>>> caprate = 0.08>>> liborrate_1 = 0.096>>> liborrate_2 = 0.087

56

>>> period = 4>>> # Insert the mathematical formulas.>>> payoff1 = (principal*(liborrate_1-caprate)/period)>>> payoff180000.0 # USD>>> payoff2 = (principal*(liborrate_2-caprate)/period)>>> payoff234999.99999999996>>> round(_,2)35000.0 # USD

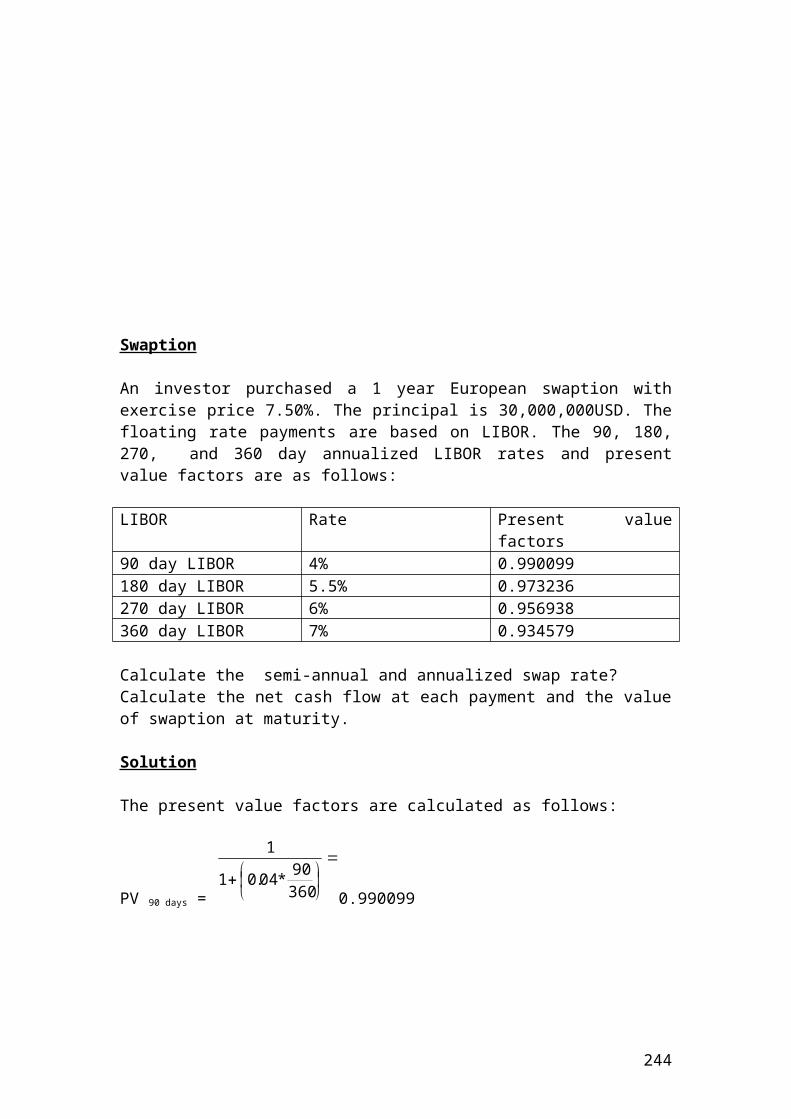

Swaption

An investor purchased a 1 year European swaption with exercise price 7.50%. The principal is 30,000,000USD. The floating rate payments are based on LIBOR. The 90, 180, 270, and 360 day annualized LIBOR rates and present value factors are as follows:

LIBOR Rate Present value factors90 day LIBOR 4% 0.990099180 day LIBOR 5.5% 0.973236270 day LIBOR 6% 0.956938360 day LIBOR 7% 0.934579

Calculate the semi-annual and annualized swap rate?Calculate the net cash flow at each payment and the value of swaption at maturity.

Solution

57

The present value factors are calculated as follows:

PV 90 days = Error! Objects cannot be created from editing field codes.0.990099

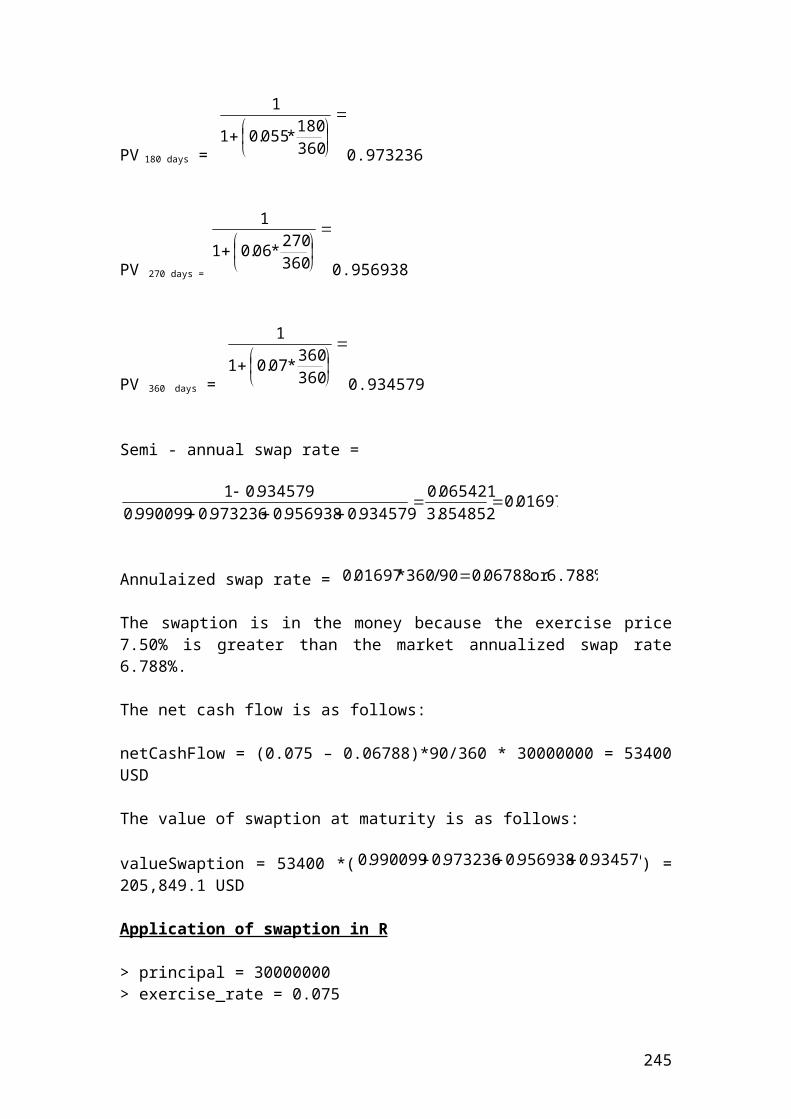

PV 180 days = Error! Objects cannot be created from editing field codes.0.973236

PV 270 days = Error! Objects cannot be created from editing field codes.0.956938

PV 360 days = Error! Objects cannot be created from editing field codes.0.934579

Semi - annual swap rate =

Error! Objects cannot be created from editing field codes.

Annulaized swap rate = Error! Objects cannot be created from editing field codes.

The swaption is in the money because the exercise price 7.50% is greater than the market annualized swap rate 6.788%.

The net cash flow is as follows:

netCashFlow = (0.075 – 0.06788)*90/360 * 30000000 = 53400 USD

The value of swaption at maturity is as follows:

valueSwaption = 53400 *(Error! Objects cannot be created from editing field codes.) = 205,849.1 USD

Application of swaption in python

>>> principal = 30000000>>> exercise_rate = 0.075>>> rate90 = 0.04>>> rate180 = 0.055>>> rate270 = 0.06>>> rate360 = 0.07>>> # Insert the mathematical formulas.>>> PV90 = 1 /(1+(rate90 * 90/360))>>> PV900.9900990099009901>>> PV180 = 1/(1+(rate180 * 180/360))>>> PV1800.97323600973236>>> PV270 = 1/(1+(rate270 * 270/360))

58

>>> PV2700.9569377990430623>>> PV360 = 1/(1+(rate360* 360/360))>>> PV3600.9345794392523364>>> semiAnnualRate = (1-PV360)/(PV90 +PV180 +PV270 +PV360)>>> semiAnnualRate0.01697096448070222>>> round(_,5)0.01697>>> annualizedSwapRate = semiAnnualRate * (360/90)>>> annualizedSwapRate0.06788385792280888>>> round(_,5)0.06788

Please repeat the above swaption problem in python and calculate the net cash flow and the value of swaption at maturity.

Put –call parity

The put – call parity shows the relationship between a call and a put option with the same expiration, strike and share prices. The mathematical formula is as follows:

Error! Objects cannot be created from editing field codes.

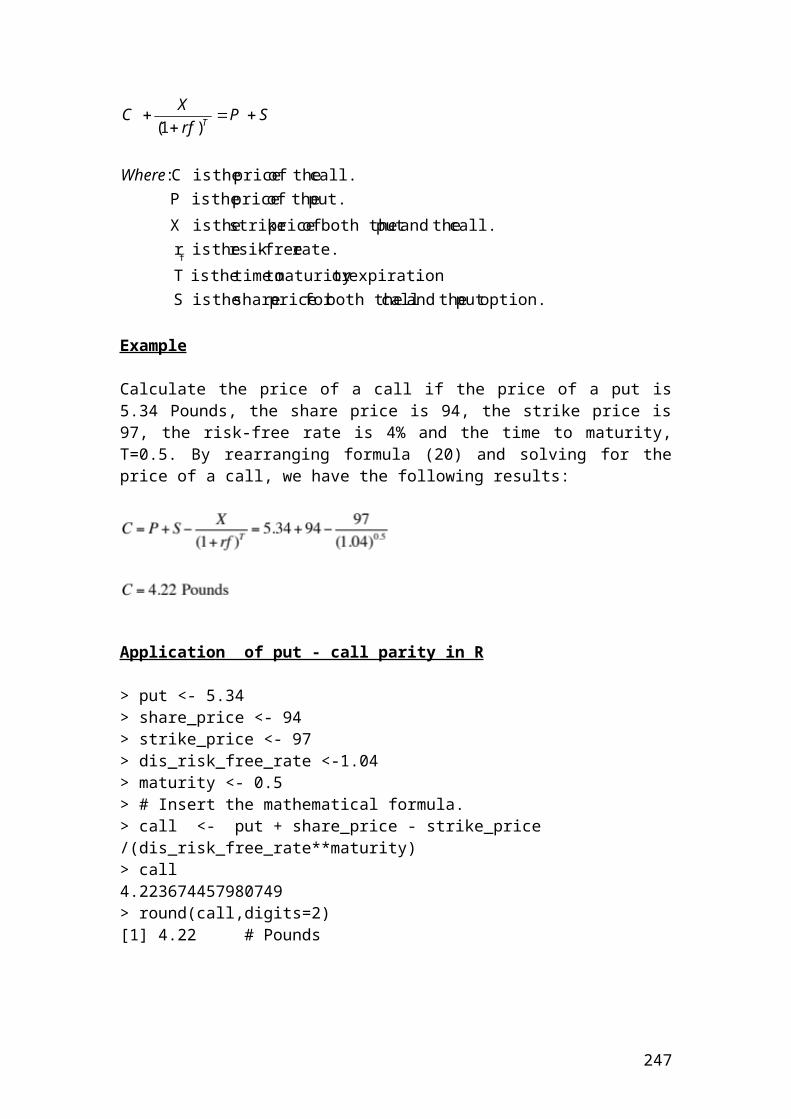

Example

Calculate the price of a call if the price of a put is 5.34 Pounds, the share price is 94, the strike price is 97, the risk-free rate is 4% and the time to maturity, T=0.5. By rearranging formula (20) and solving for the price of a call, we have the following results:

C=P+S− X(1+rf )T

=5 . 34+94−97(1.04 )0 .5

C=4 .22 Pounds

Application of put - call parity in python

>>> put = 5.34>>> share_price = 94>>> strike_price = 97>>> disriskfreerate = 1.04>>> maturity = 0.5>>> # Insert the mathematical formula.>>> call = put + share_price - strike_price /(disriskfreerate**maturity)

59

>>> call4.223674457980749>>> round(_,2)4.22 # Pounds

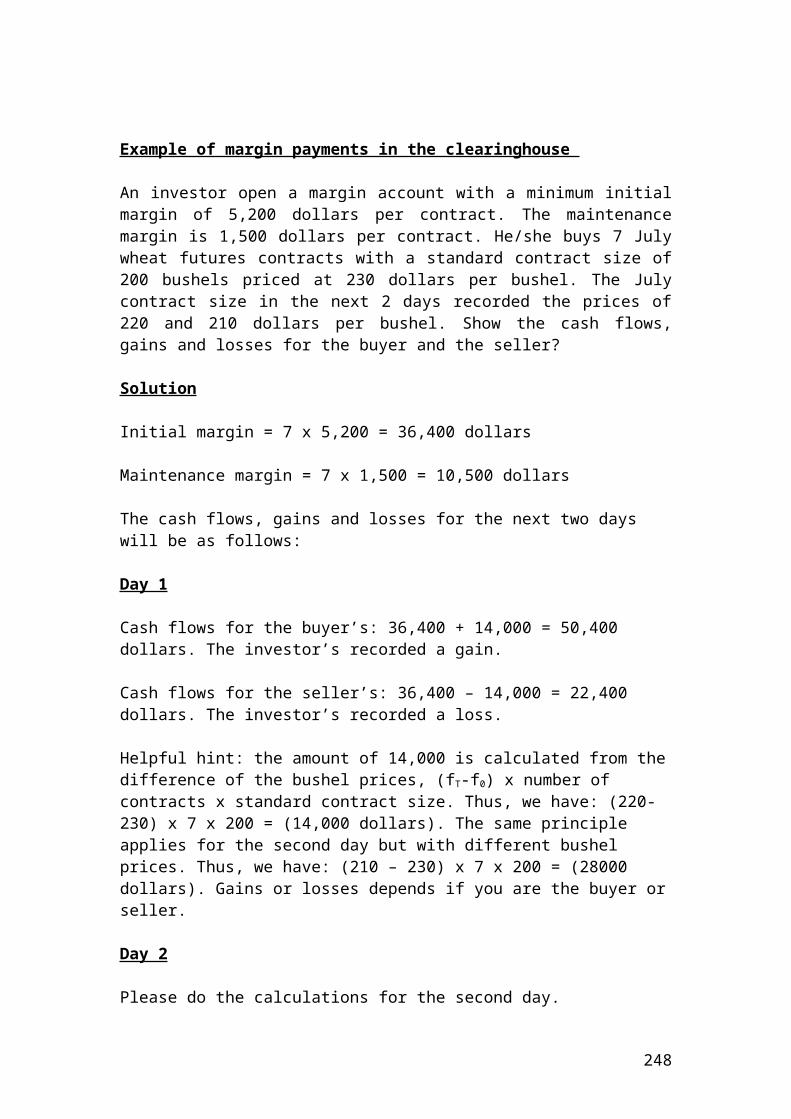

Example of margin payments in the clearinghouse

An investor open a margin account with a minimum initial margin of 5,200 dollars per contract. The maintenance margin is 1,500 dollars per contract. He/she buys 7 July wheat futures contracts with a standard contract size of 200 bushels priced at 230 dollars per bushel. The July contract size in the next 2 days recorded the prices of 220 and 210 dollars per bushel. Show the cash flows, gains and losses for the buyer and the seller?

Solution

Initial margin = 7 x 5,200 = 36,400 dollars

Maintenance margin = 7 x 1,500 = 10,500 dollars

The cash flows, gains and losses for the next two days will be as follows:

Day 1

Cash flows for the buyer’s: 36,400 + 14,000 = 50,400 dollars. The investor’s recorded a gain.

Cash flows for the seller’s: 36,400 – 14,000 = 22,400 dollars. The investor’s recorded a loss.

Helpful hint: the amount of 14,000 is calculated from the difference of the bushel prices, (fT-f0) x number of contracts x standard contract size. Thus, we have: (220-230) x 7 x 200 = (14,000 dollars). The same principle applies for the second day but with different bushel prices. Thus, we have: (210 – 230) x 7 x 200 = (28000 dollars). Gains or losses depends if you are the buyer or seller.

Day 2

Please do the calculations for the second day.

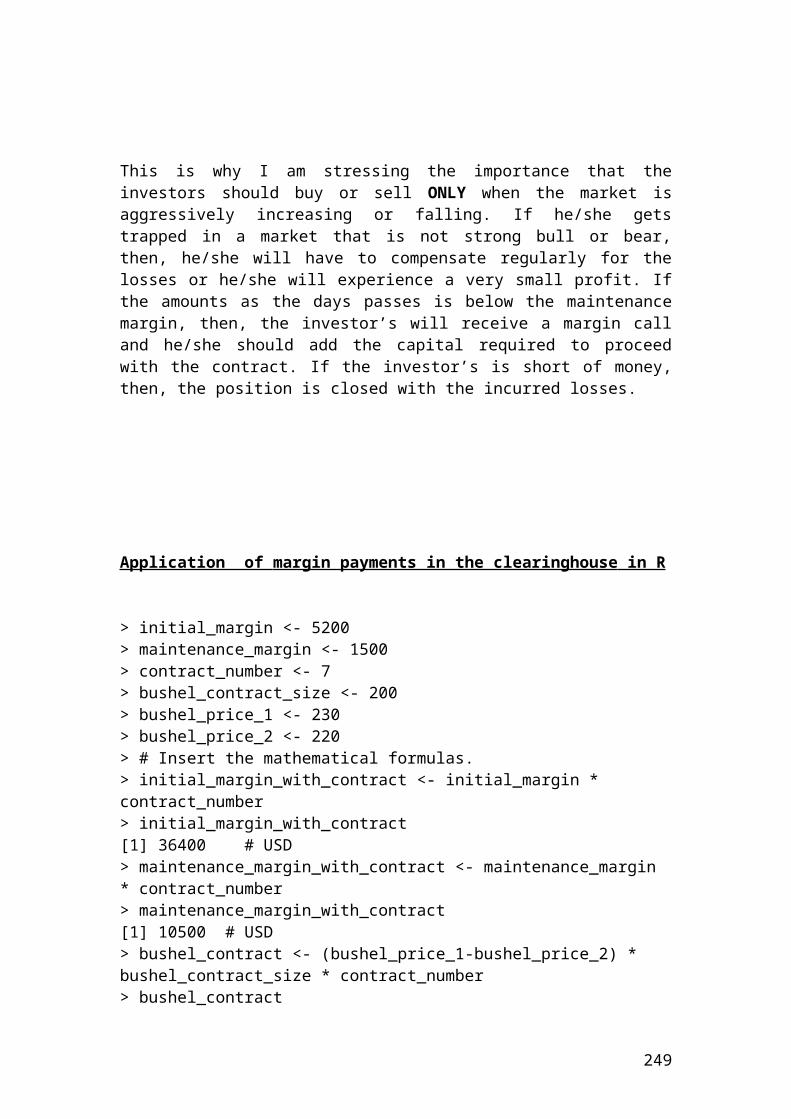

This is why I am stressing the importance that the investors should buy or sell ONLY when the market is aggressively increasing or falling. If he/she gets trapped in a market that is not strong bull or bear, then, he/she will have to compensate regularly for the losses or he/she will experience a very small profit. If the amounts as the days

60

passes is below the maintenance margin, then, the investor’s will receive a margin call and he/she should add the capital required to proceed with the contract. If the investor’s is short of money, then, the position is closed with the incurred losses.

Application of margin payments in the clearinghouse in python

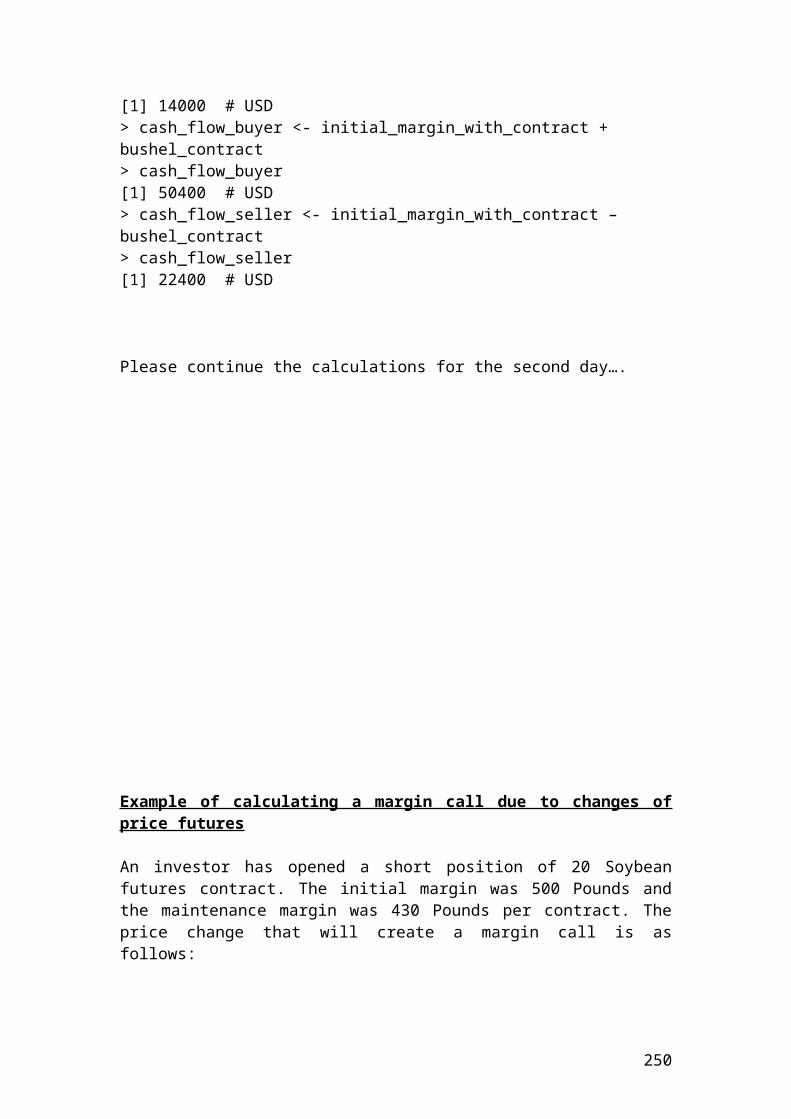

>>> initialmargin = 5200>>> maintenancemargin = 1500>>> contractnumber = 7>>> bushelcontractsize = 200>>> bushelprice_1 = 230>>> bushelprice_2 = 220>>> # Insert the mathematical formulas.>>> initialmarginwithcontract = initialmargin * contractnumber>>> initialmarginwithcontract36400 # USD>>> maintenancemarginwithcontract = maintenancemargin * contractnumber>>> maintenancemarginwithcontract10500 # USD>>> bushelcontract = (bushelprice_1-bushelprice_2) * bushelcontractsize * contractnumber>>> bushelcontract14000 # USD>>> cashflowbuyer = initialmarginwithcontract + bushelcontract>>> cashflowbuyer50400 # USD>>> cashflowseller = initialmarginwithcontract - bushelcontract>>> cashflowseller22400 # USD

Please continue the calculations for the second day….

61

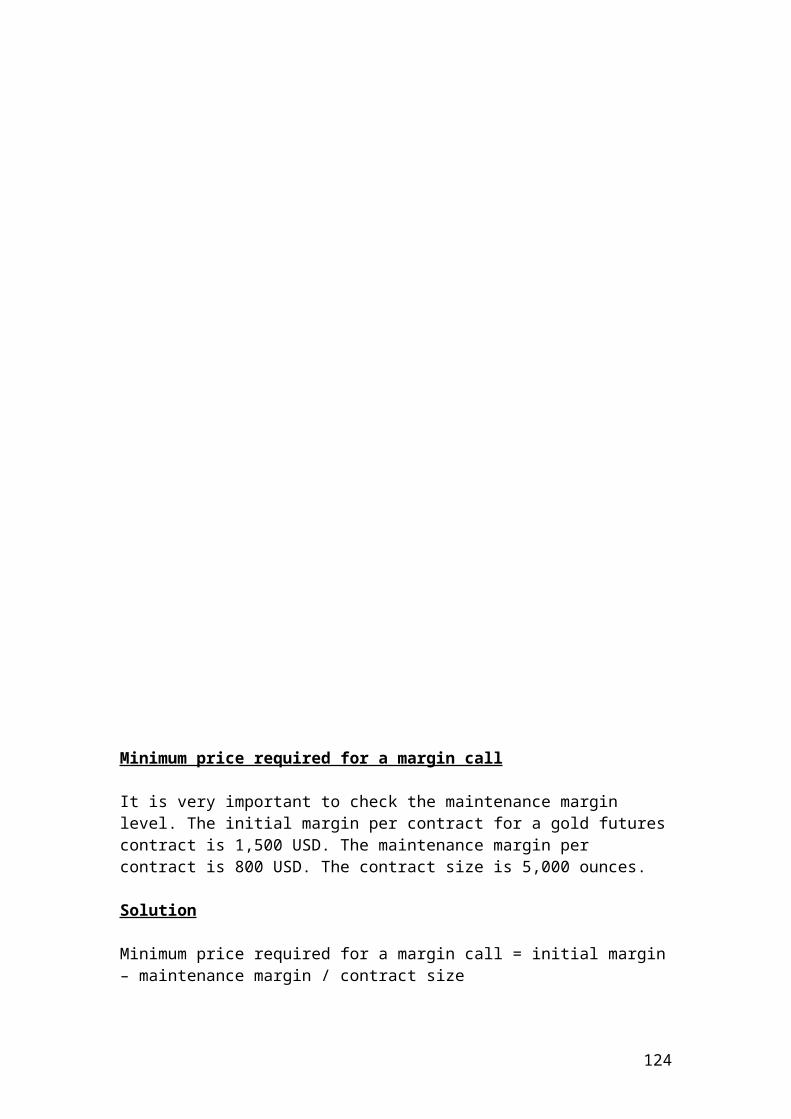

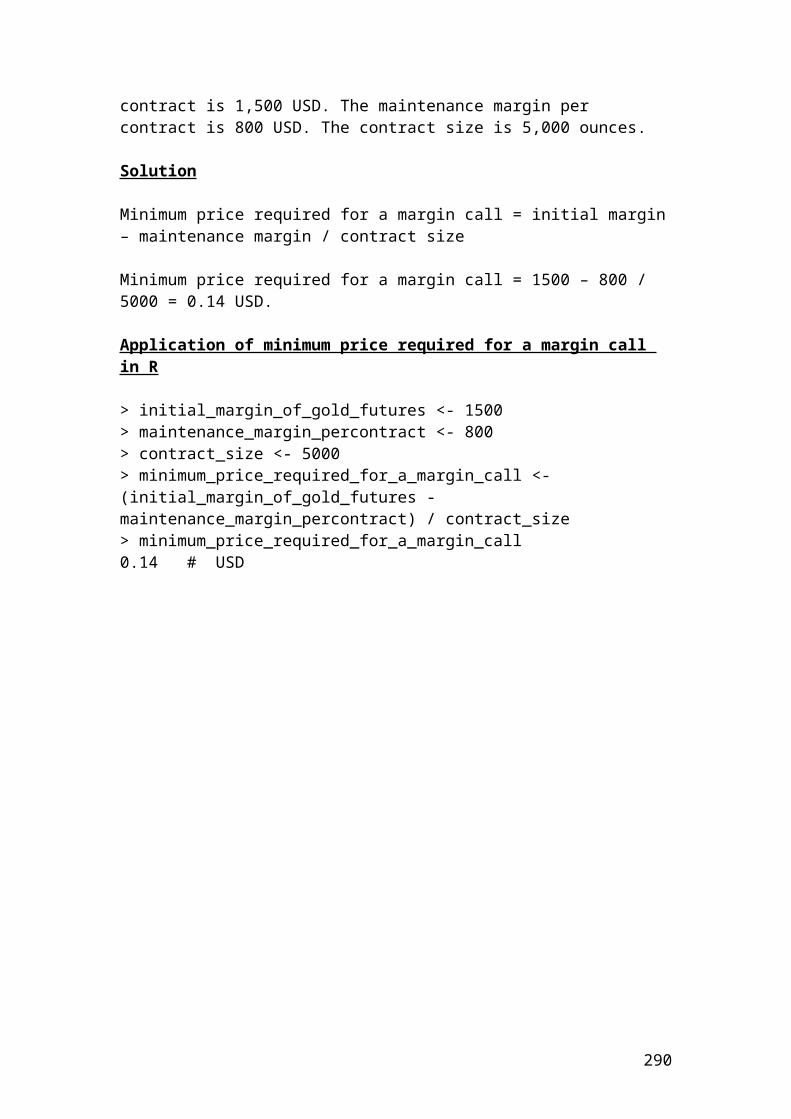

Example of calculating a margin call due to changes of price futures

An investor has opened a short position of 20 Soybean futures contract. The initial margin was 500 Pounds and the maintenance margin was 430 Pounds per contract. The price change that will create a margin call is as follows:

Solution

Margin call created at a price =initial margin - maintenance margincontract size

=500 -43020

=3.5

Pounds

Application of margin call in python

>>> initial_margin = 500>>> maintenance_margin = 430>>> futures_contract = 20>>> # Insert the mathematical formula.>>> margincall =(initial_margin-maintenance_margin) / futures_contract>>> margincall3.5 # Pounds

62

Solution of the above examples

Active return, active risk and information ratio

Active return is the difference in returns between a portfolio and the index or benchmark that is measured.

Active return = rp - rb

Where: rp is the portfolio return. rb is the benchmark or index return.

If the portfolio return is 0.80 and the benchmark return of the index is 0.70 then, the active return is………

Please complete the calculation.

Application of active return in python

>>> portfolio_return = 0.8>>> benchmark_return = 0.7>>> active_return = portfolio_return - benchmark_return>>> active_return0.10000000000000009>>> round(_,2)0.1

63

Active risk or tracking error is the standard deviation of the difference of returns between a portfolio and the benchmark or index.

Active risk =√∑ (r p−r b )2

n−1

Where : rp is portfolio return . rb is portfolio benchmark return . It could be for example an index . n is the number of assets or observations .

If the portfolio return is 0.80, the number of observations is 10 and the benchmark return of the index is 0.40 then, the active risk is………

Please complete the calculation.

Application of active risk in python

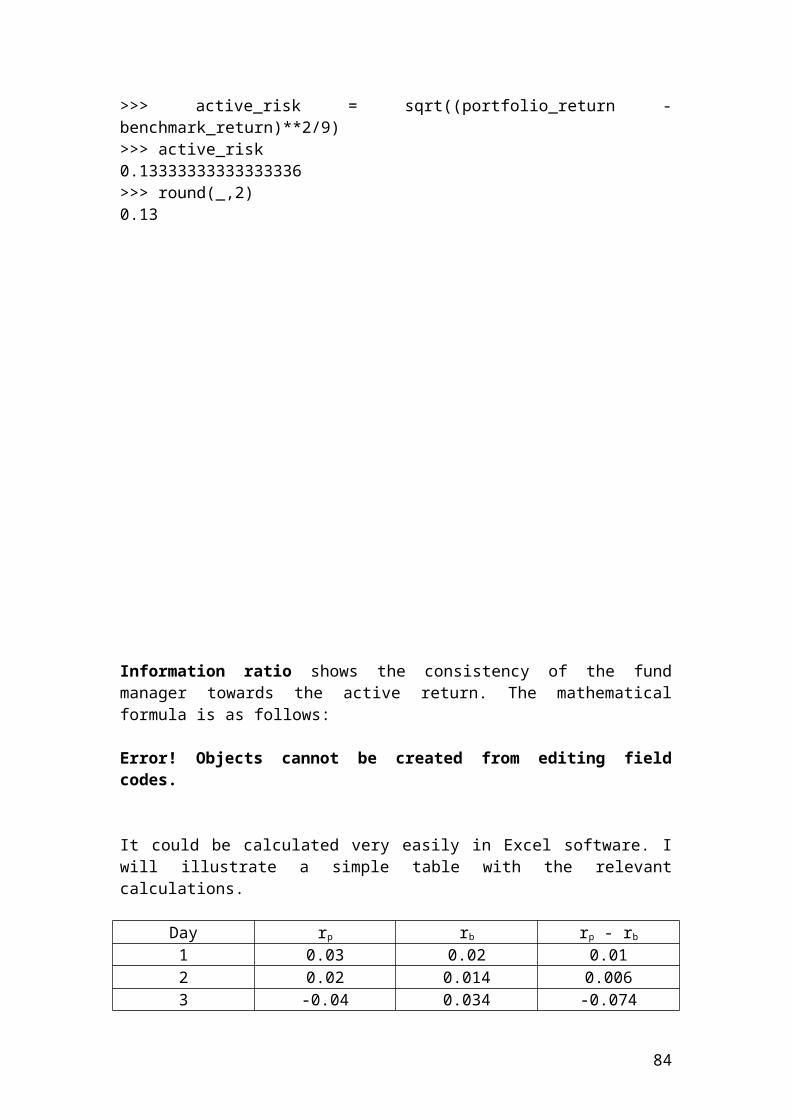

>>> portfolio_return = 0.80>>> benchmark_return = 0.40>>> n =10>>> # Insert the mathematical formula.>>> active_risk = sqrt((portfolio_return - benchmark_return)**2/9)>>> active_risk0.13333333333333336>>> round(_,2)0.13

64

Information ratio shows the consistency of the fund manager towards the active return. The mathematical formula is as follows:

Error! Objects cannot be created from editing field codes.

It could be calculated very easily in Excel software. I will illustrate a simple table with the relevant calculations.

Day rp rb rp - rb

1 0.03 0.02 0.012 0.02 0.014 0.0063 -0.04 0.034 -0.0744 0.05 0.067 -0.0175 0.08 0.012 0.0686 -0.01 -0.056 0.0467 0.07 0.031 0.0398 0.034 0.023 0.0119 -0.021 0.015 -0.03610 0.045 0.001 0.044

Average 0.0258 0.0161Standard deviation

0.043

Source: author’s calculation

By substituting the values that we have found in terms of rp =0.0258, rb = 0.0161 and standard deviation = 0.043 in the following equation we have:

Error! Objects cannot be created from editing field codes.

Error! Objects cannot be created from editing field codes.

But what is the interpretation of the information ratio of 0.23. It means that the fund manager gained around 23 basis points of active return per unit of active risk. The higher is this number, the better the manager is performing in relation to active risk.

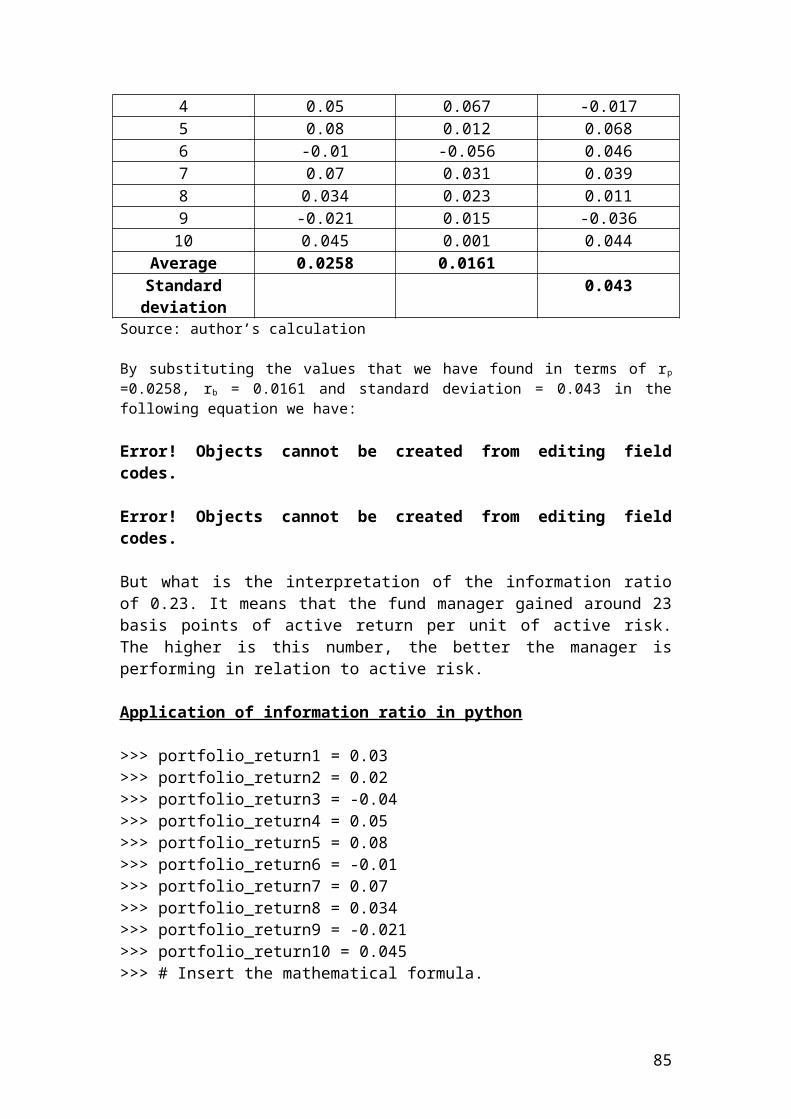

Application of information ratio in python

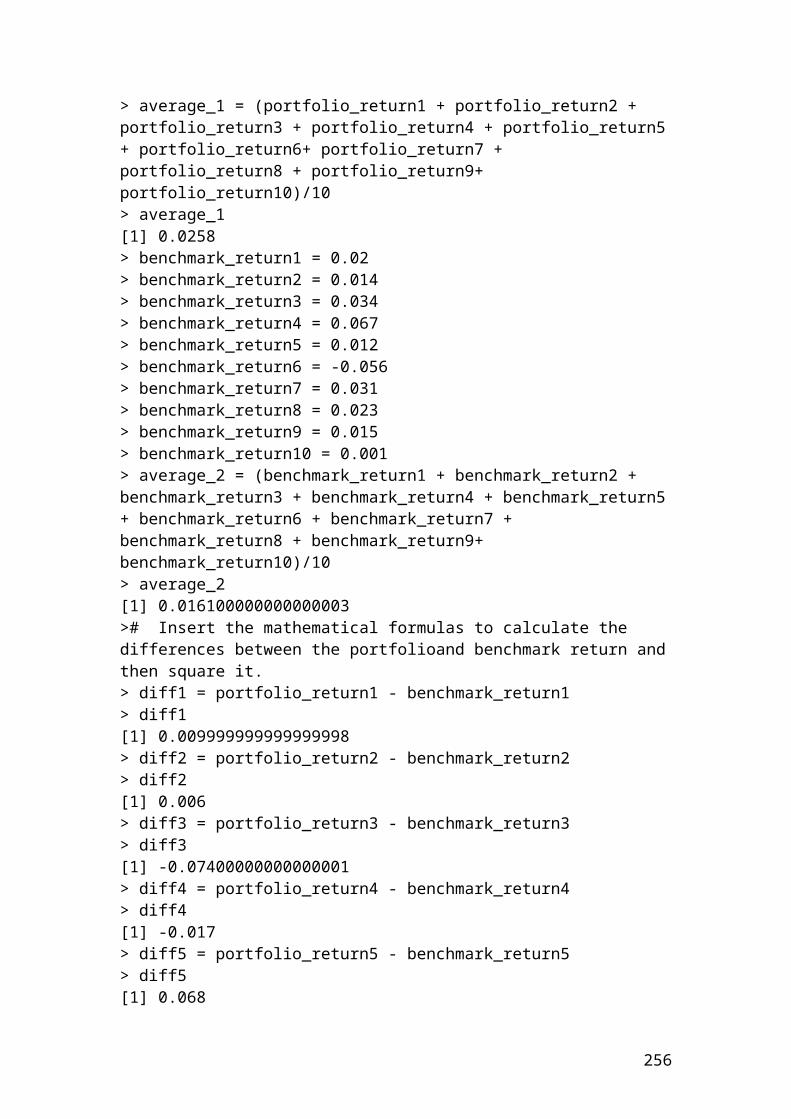

>>> portfolio_return1 = 0.03

65

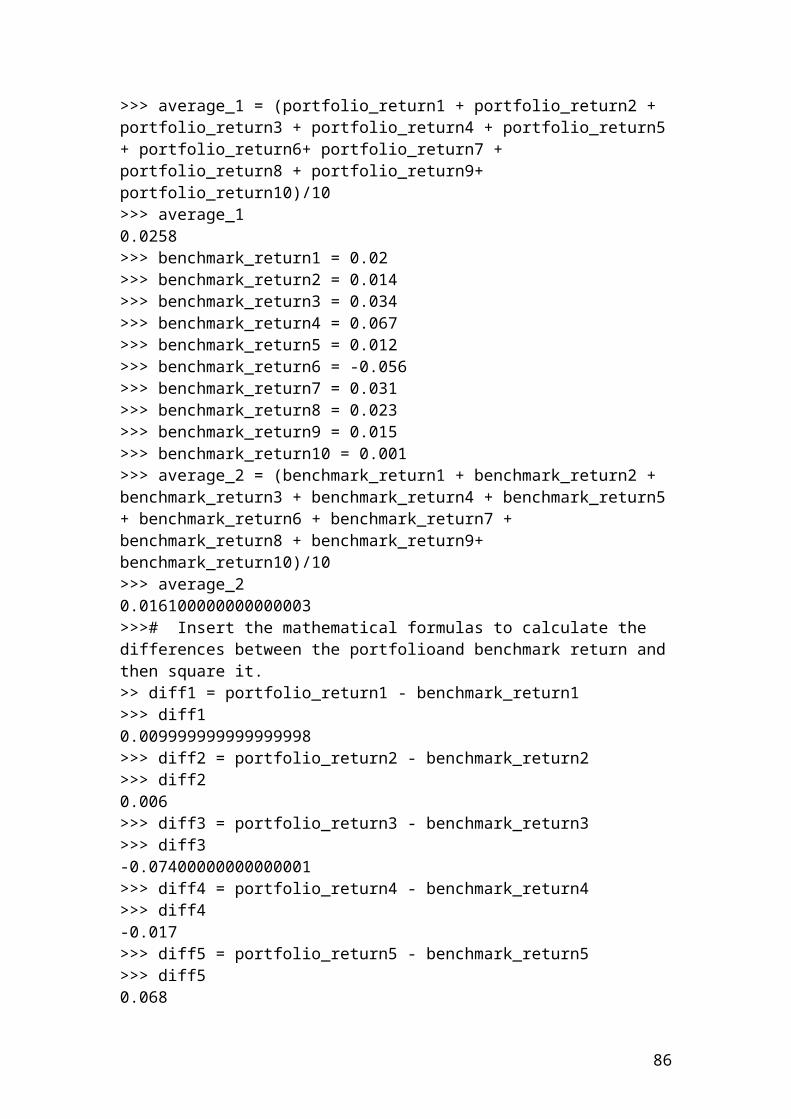

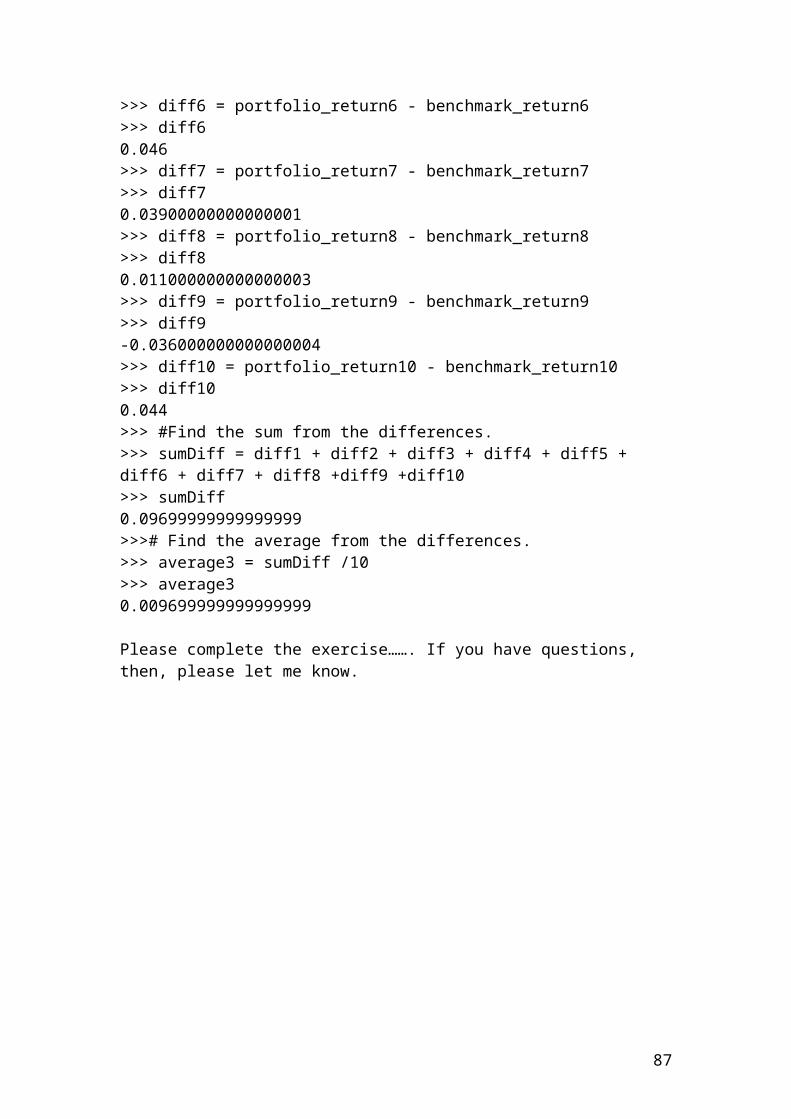

>>> portfolio_return2 = 0.02>>> portfolio_return3 = -0.04>>> portfolio_return4 = 0.05>>> portfolio_return5 = 0.08>>> portfolio_return6 = -0.01>>> portfolio_return7 = 0.07>>> portfolio_return8 = 0.034>>> portfolio_return9 = -0.021>>> portfolio_return10 = 0.045>>> # Insert the mathematical formula.>>> average_1 = (portfolio_return1 + portfolio_return2 + portfolio_return3 + portfolio_return4 + portfolio_return5 + portfolio_return6+ portfolio_return7 + portfolio_return8 + portfolio_return9+ portfolio_return10)/10>>> average_10.0258>>> benchmark_return1 = 0.02>>> benchmark_return2 = 0.014>>> benchmark_return3 = 0.034>>> benchmark_return4 = 0.067>>> benchmark_return5 = 0.012>>> benchmark_return6 = -0.056>>> benchmark_return7 = 0.031>>> benchmark_return8 = 0.023>>> benchmark_return9 = 0.015>>> benchmark_return10 = 0.001>>> average_2 = (benchmark_return1 + benchmark_return2 + benchmark_return3 + benchmark_return4 + benchmark_return5 + benchmark_return6 + benchmark_return7 + benchmark_return8 + benchmark_return9+ benchmark_return10)/10>>> average_20.016100000000000003>>># Insert the mathematical formulas to calculate the differences between the portfolioand benchmark return and then square it.>> diff1 = portfolio_return1 - benchmark_return1>>> diff10.009999999999999998>>> diff2 = portfolio_return2 - benchmark_return2>>> diff20.006>>> diff3 = portfolio_return3 - benchmark_return3>>> diff3-0.07400000000000001>>> diff4 = portfolio_return4 - benchmark_return4>>> diff4-0.017>>> diff5 = portfolio_return5 - benchmark_return5>>> diff50.068>>> diff6 = portfolio_return6 - benchmark_return6>>> diff60.046

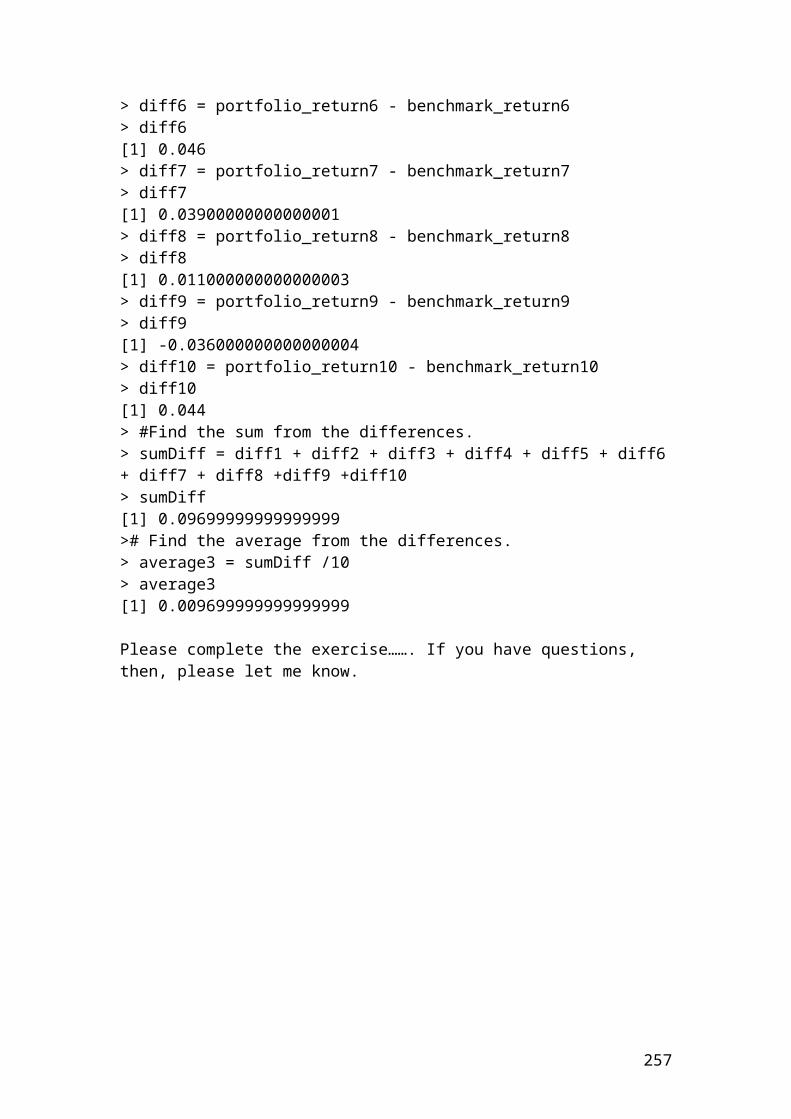

66

>>> diff7 = portfolio_return7 - benchmark_return7>>> diff70.03900000000000001>>> diff8 = portfolio_return8 - benchmark_return8>>> diff80.011000000000000003>>> diff9 = portfolio_return9 - benchmark_return9>>> diff9-0.036000000000000004>>> diff10 = portfolio_return10 - benchmark_return10>>> diff100.044>>> #Find the sum from the differences.>>> sumDiff = diff1 + diff2 + diff3 + diff4 + diff5 + diff6 + diff7 + diff8 +diff9 +diff10>>> sumDiff0.09699999999999999>>># Find the average from the differences.>>> average3 = sumDiff /10>>> average30.009699999999999999

Please complete the exercise……. If you have questions, then, please let me know.

Please convert the following exercise in python language programming

Calculate the balance at the end of the 5th day from changes in the futures prices from 90 to 89, 91, 95, 97, 99. The trader has bought 50 futures contract for settlement in May. The initial margin is $8.

Day Beginning Futures price Gain or loss Ending balance

67

balance0 400 90 0 4001 400 89 (50)2 350 91 1003 450 95 2004 650 97 1005 750 99 100

Source: author’s illustration.

Beginning balance = initial margin x number of contracts.Beginning balance = 8 x 50 = $400

Please complete the values of the column ending balance.

Solution

Day Beginning balance

Futures price Gain or loss Ending balance

0 400 90 0 4001 400 89 (50) 3502 350 91 100 4503 450 95 200 6504 650 97 100 7505 750 99 100 850

The ending balance at the 5th day in the margin account will be 850 USD.

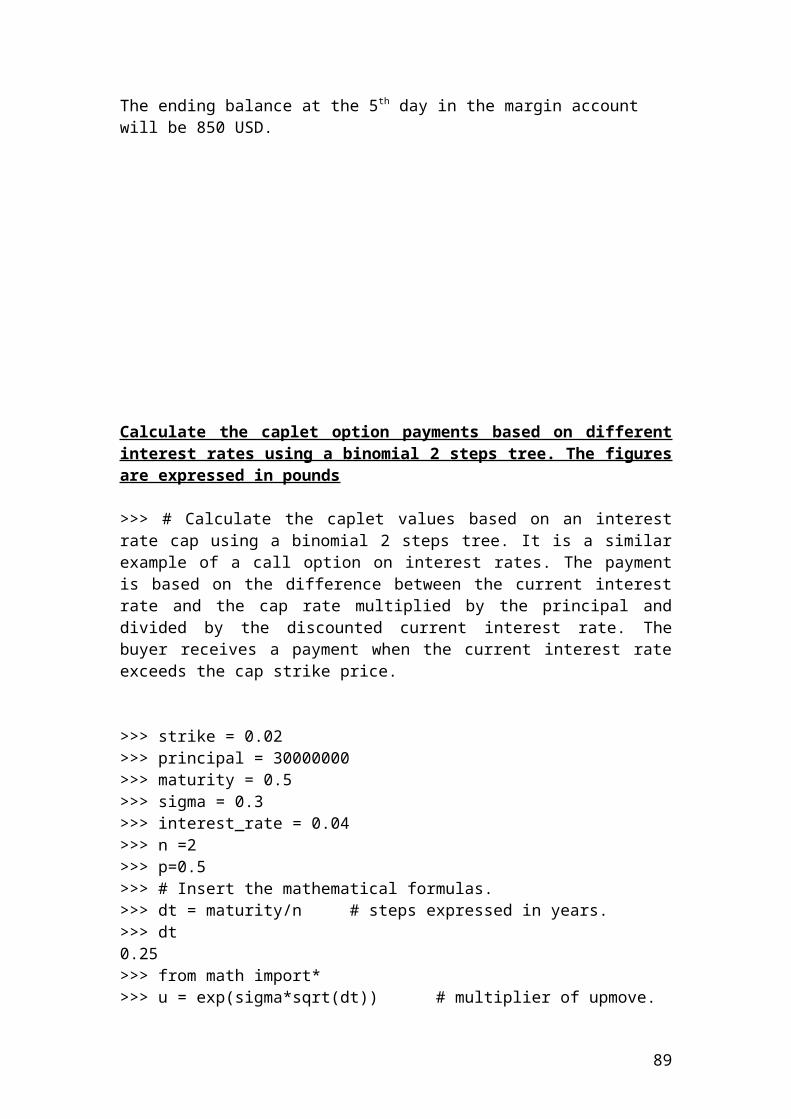

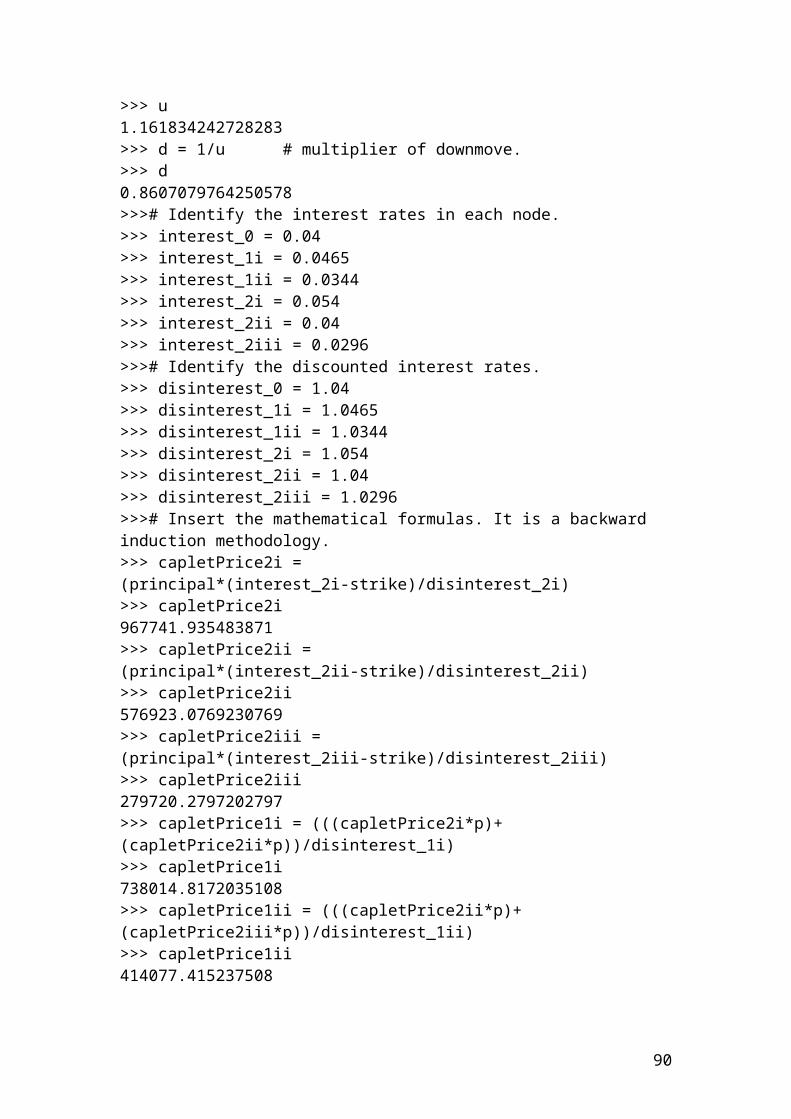

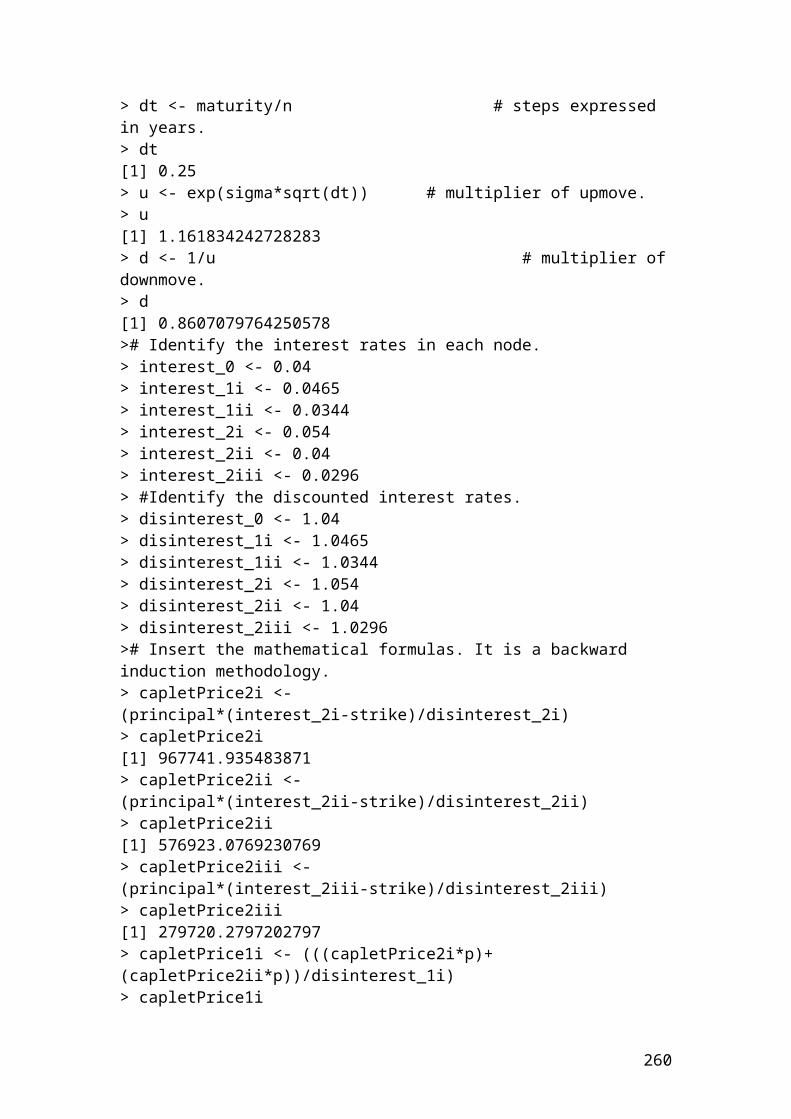

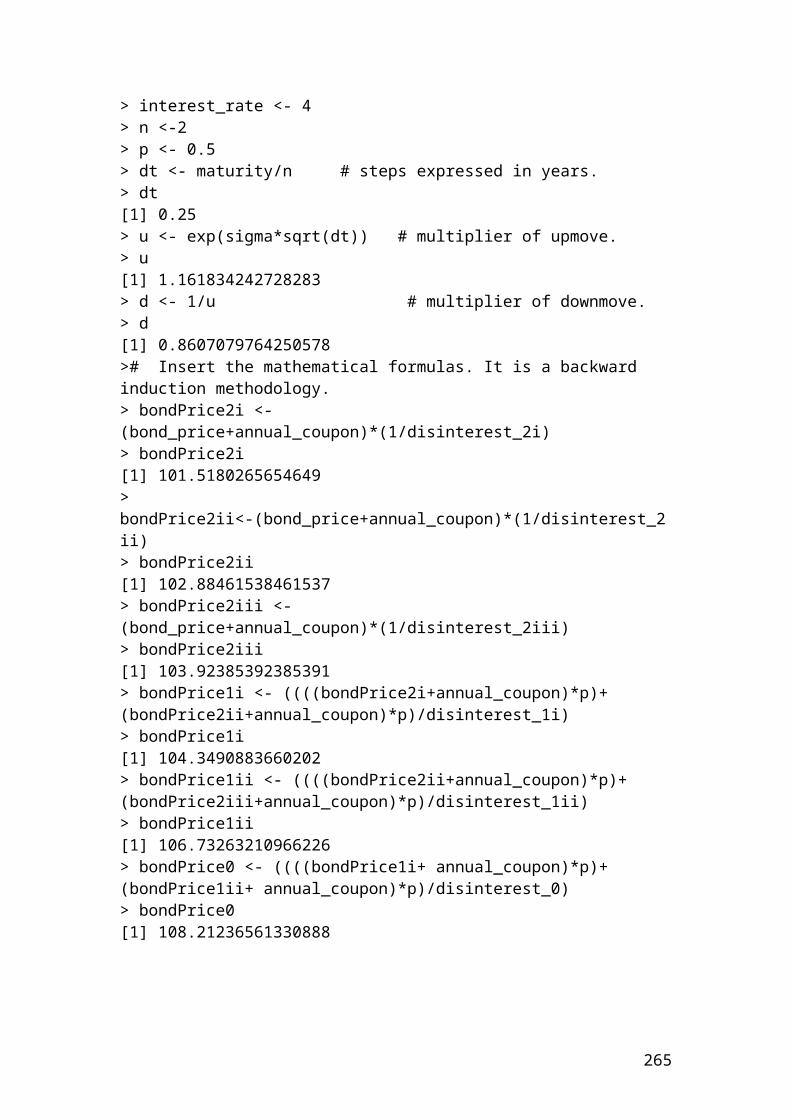

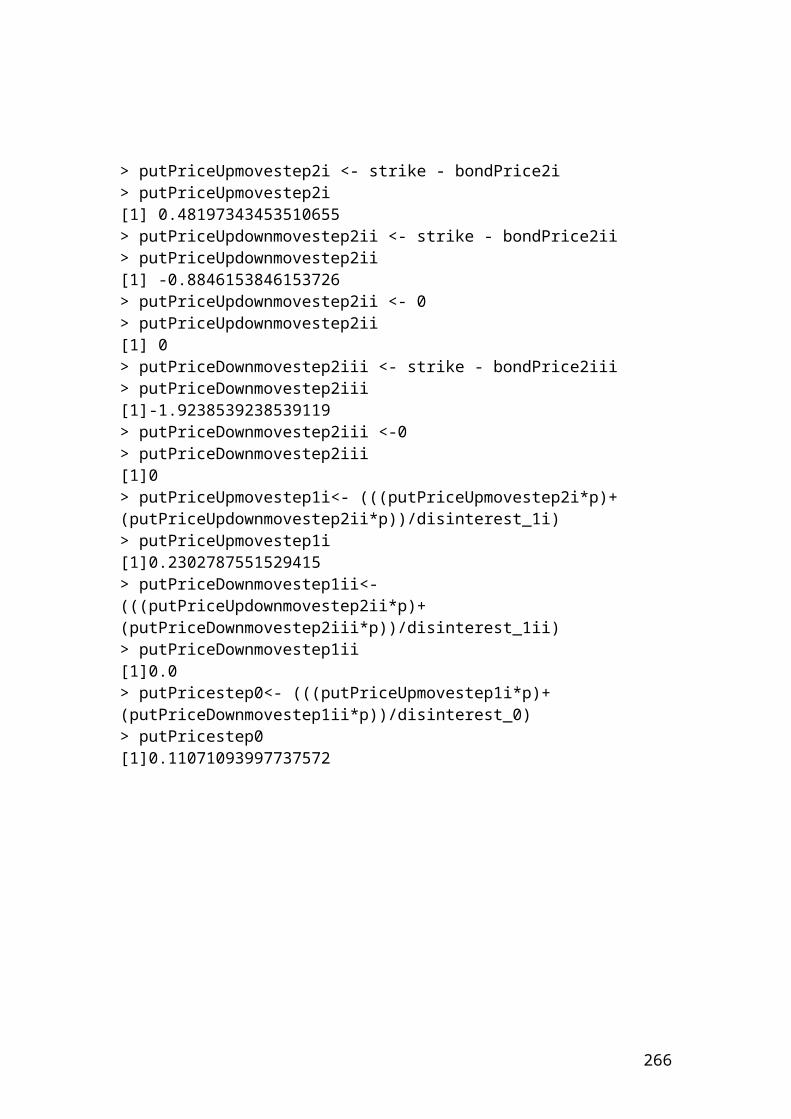

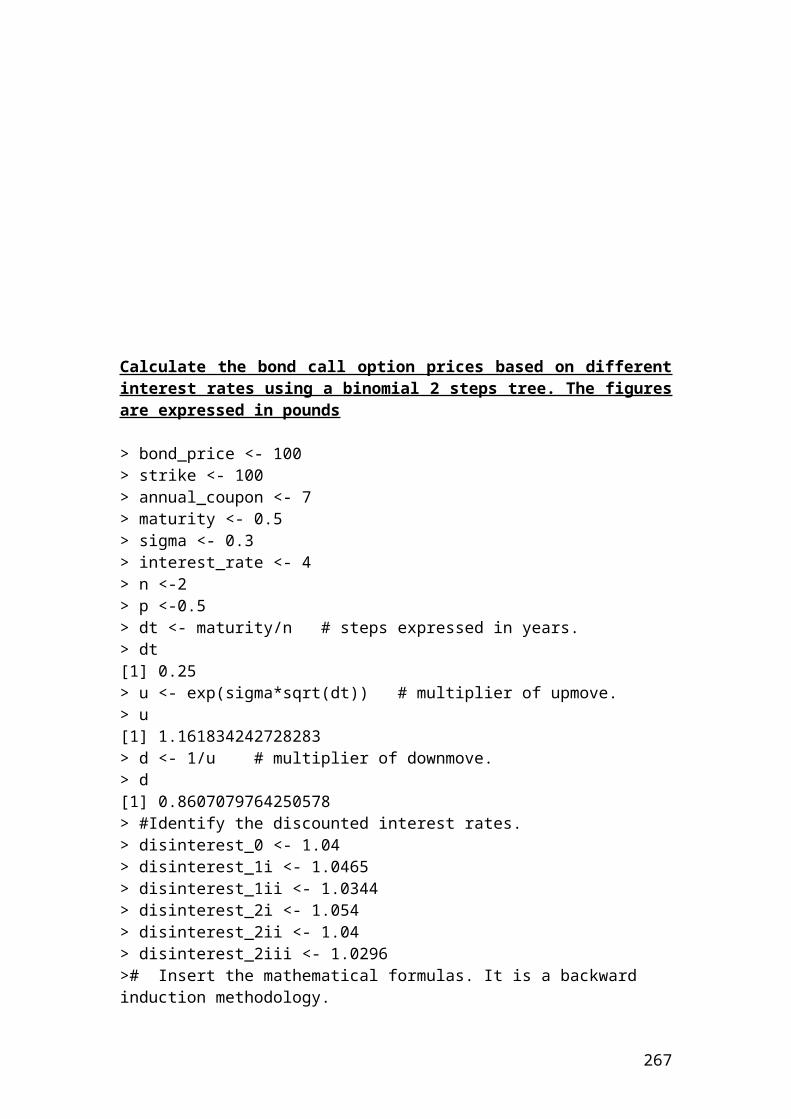

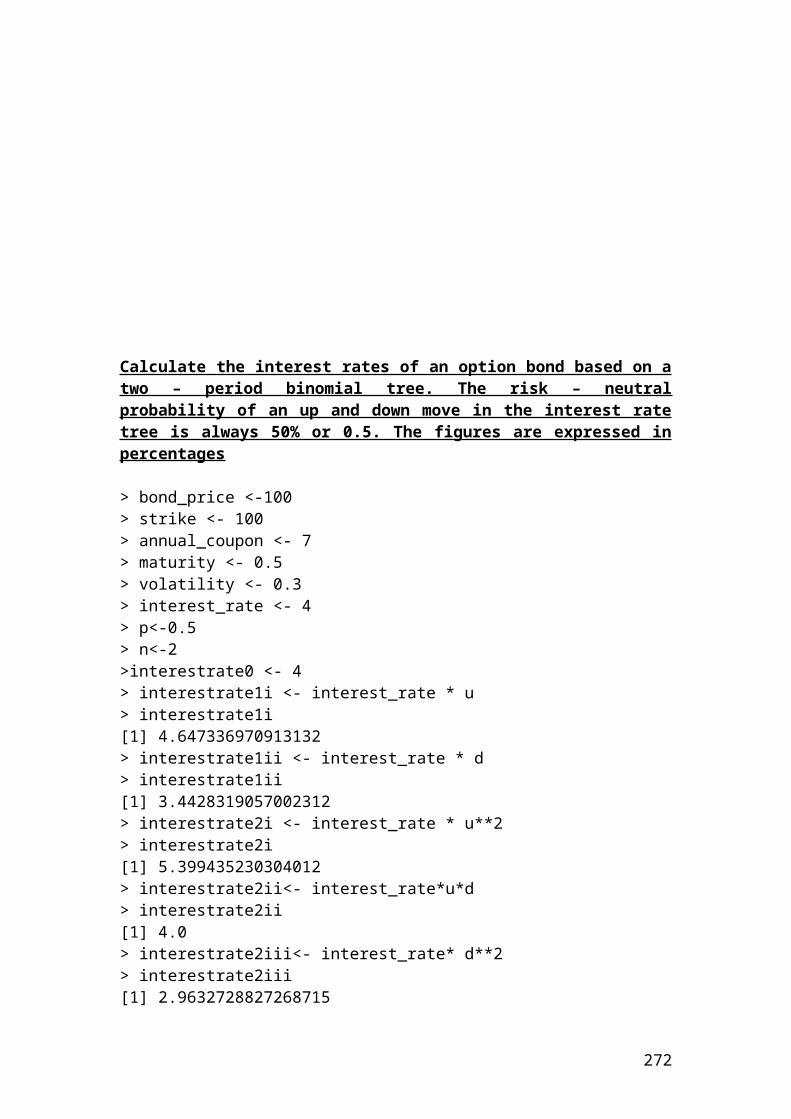

Calculate the caplet option payments based on different interest rates using a binomial 2 steps tree. The figures are expressed in pounds

>>> # Calculate the caplet values based on an interest rate cap using a binomial 2 steps tree. It is a similar example of a call option on interest rates. The payment is based on the difference between the current interest rate and the cap rate multiplied by

68

the principal and divided by the discounted current interest rate. The buyer receives a payment when the current interest rate exceeds the cap strike price.

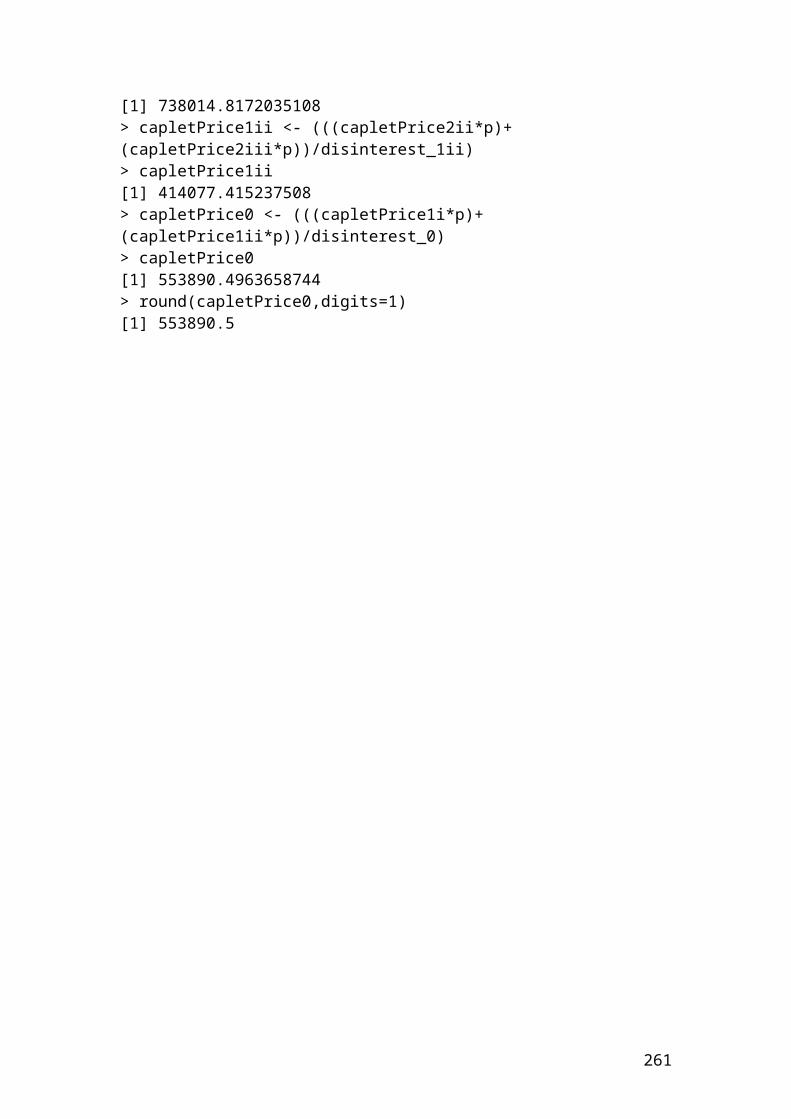

>>> strike = 0.02>>> principal = 30000000>>> maturity = 0.5>>> sigma = 0.3>>> interest_rate = 0.04>>> n =2>>> p=0.5>>> # Insert the mathematical formulas.>>> dt = maturity/n # steps expressed in years.>>> dt0.25>>> from math import*>>> u = exp(sigma*sqrt(dt)) # multiplier of upmove.>>> u1.161834242728283>>> d = 1/u # multiplier of downmove.>>> d0.8607079764250578>>># Identify the interest rates in each node.>>> interest_0 = 0.04>>> interest_1i = 0.0465>>> interest_1ii = 0.0344>>> interest_2i = 0.054>>> interest_2ii = 0.04>>> interest_2iii = 0.0296>>># Identify the discounted interest rates.>>> disinterest_0 = 1.04>>> disinterest_1i = 1.0465>>> disinterest_1ii = 1.0344>>> disinterest_2i = 1.054>>> disinterest_2ii = 1.04>>> disinterest_2iii = 1.0296>>># Insert the mathematical formulas. It is a backward induction methodology.>>> capletPrice2i = (principal*(interest_2i-strike)/disinterest_2i)>>> capletPrice2i967741.935483871>>> capletPrice2ii = (principal*(interest_2ii-strike)/disinterest_2ii)>>> capletPrice2ii576923.0769230769>>> capletPrice2iii = (principal*(interest_2iii-strike)/disinterest_2iii)>>> capletPrice2iii279720.2797202797>>> capletPrice1i = (((capletPrice2i*p)+(capletPrice2ii*p))/disinterest_1i)>>> capletPrice1i738014.8172035108>>> capletPrice1ii = (((capletPrice2ii*p)+(capletPrice2iii*p))/disinterest_1ii)

69

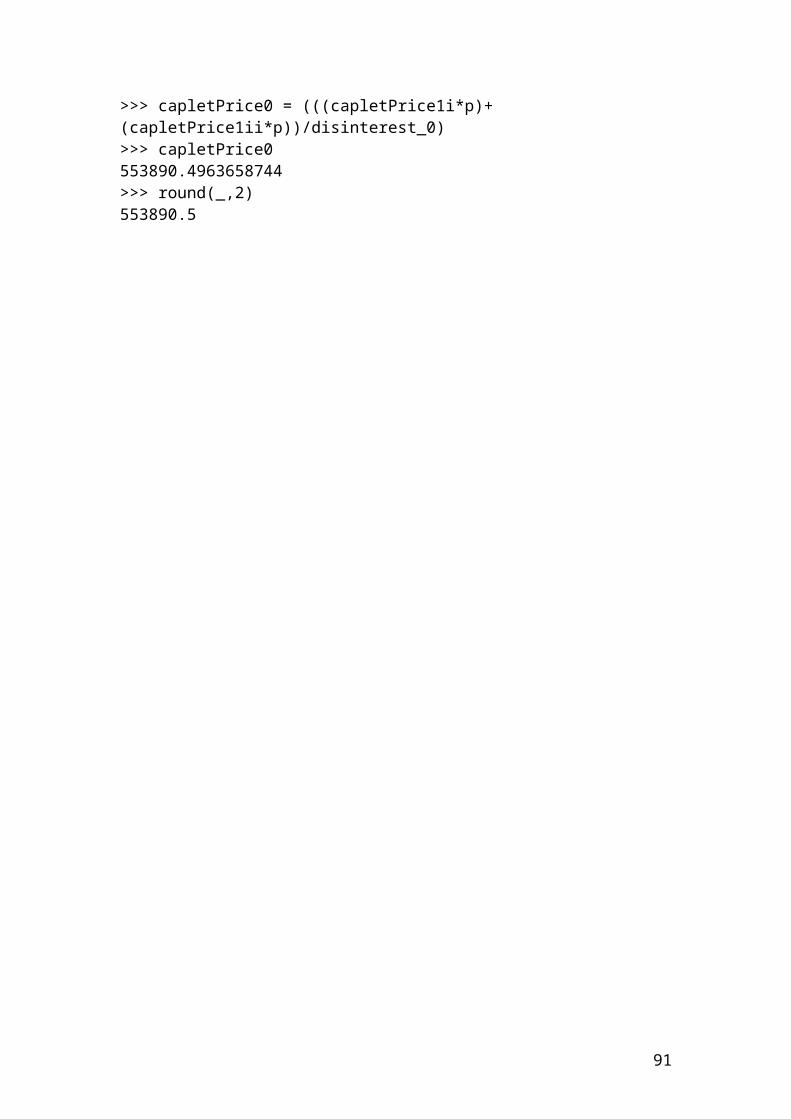

>>> capletPrice1ii414077.415237508>>> capletPrice0 = (((capletPrice1i*p)+(capletPrice1ii*p))/disinterest_0)>>> capletPrice0553890.4963658744>>> round(_,2)553890.5

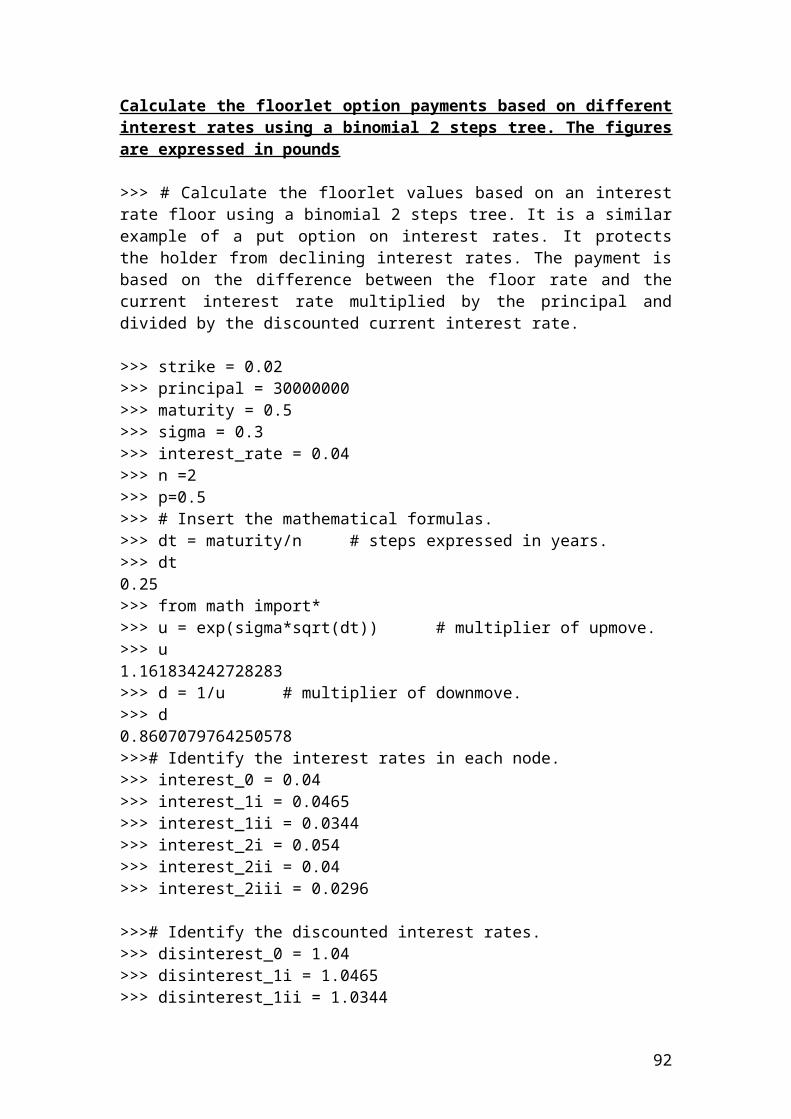

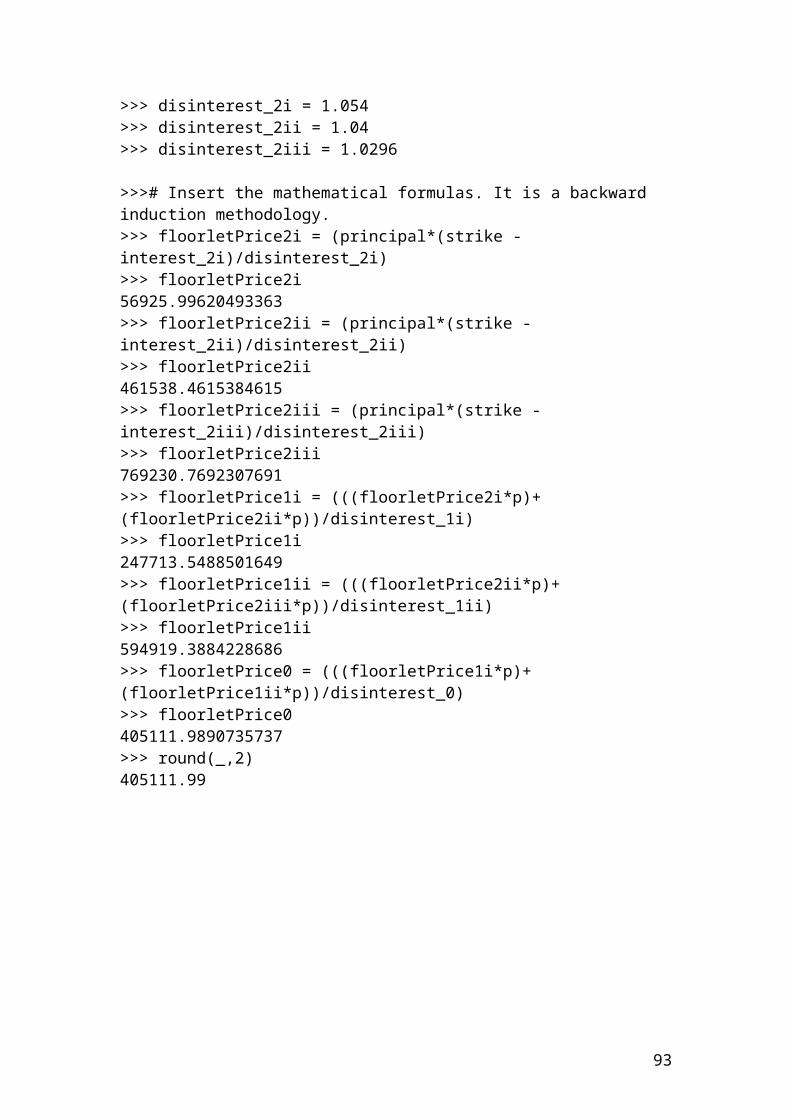

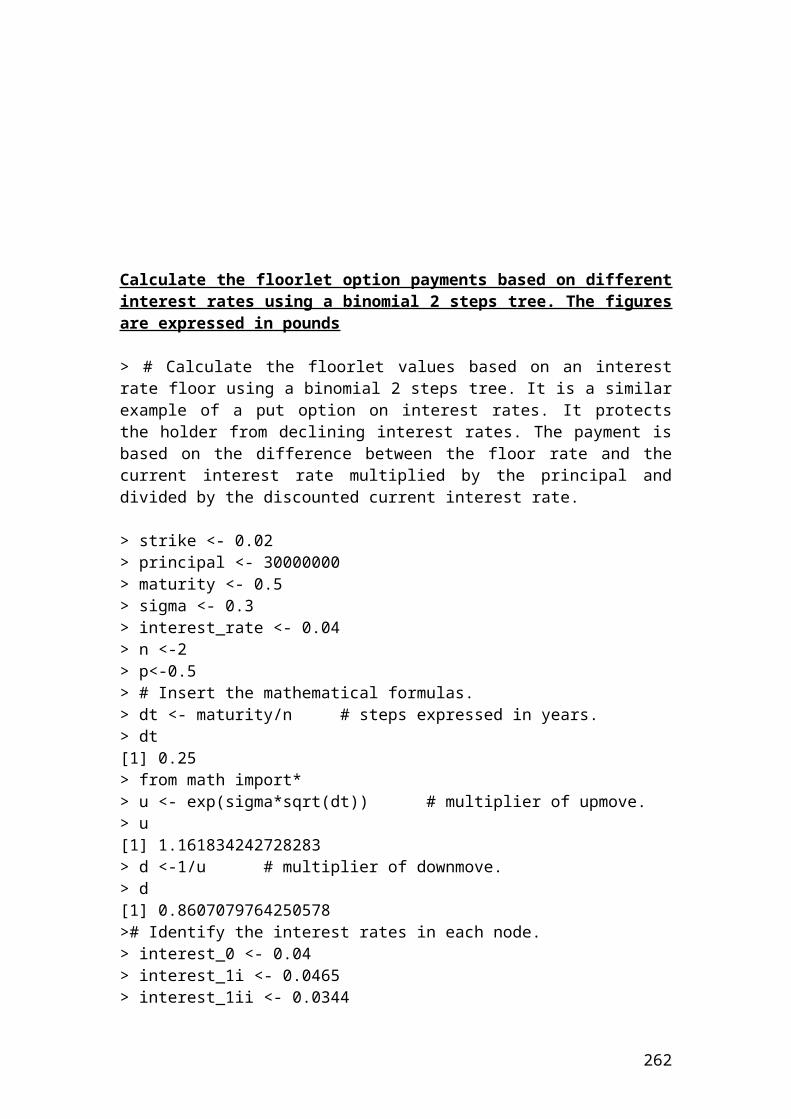

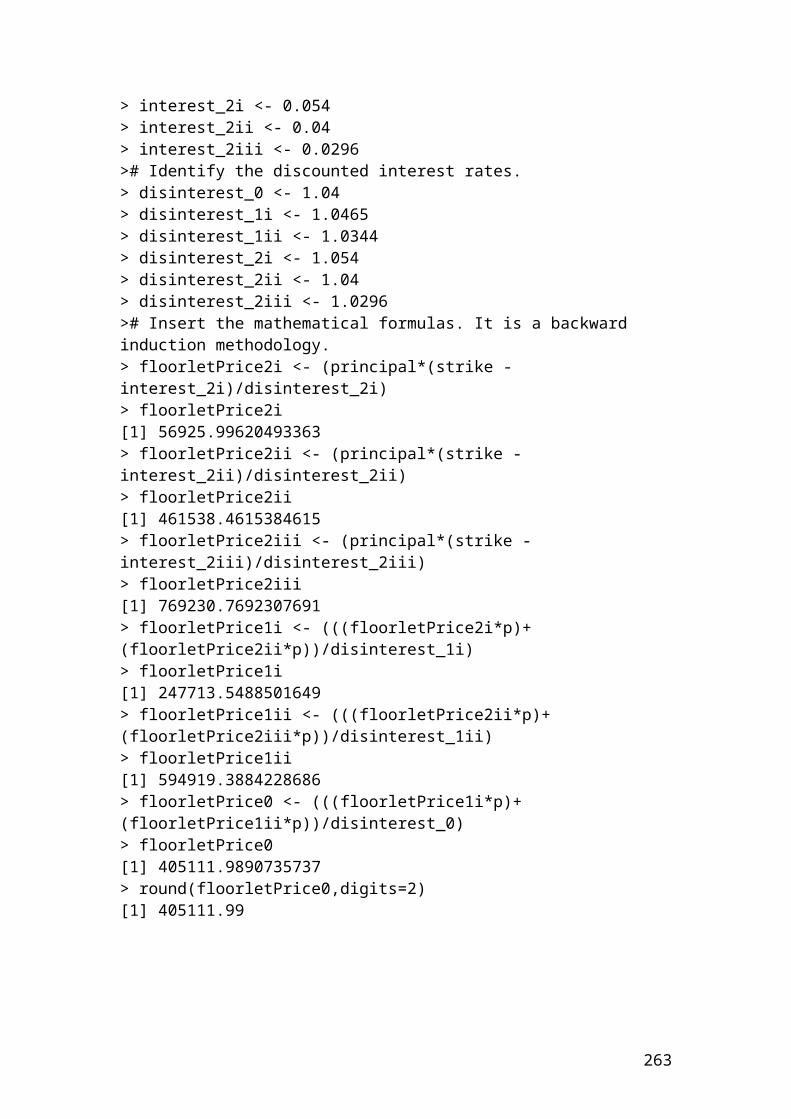

Calculate the floorlet option payments based on different interest rates using a binomial 2 steps tree. The figures are expressed in pounds

>>> # Calculate the floorlet values based on an interest rate floor using a binomial 2 steps tree. It is a similar example of a put option on interest rates. It protects the holder from declining interest rates. The payment is based on the difference between

70

the floor rate and the current interest rate multiplied by the principal and divided by the discounted current interest rate.