Finished) Construction Productivity 01132012

91

THE MANUAL OF CONSTRUCTION PRODUCTIVITY MEASUREMENT AND PERFORMANCE EVALUATION CONSTRUCTION INDUSTRY INSTITUTE

-

Upload

nguyen-ngoc-dung -

Category

Documents

-

view

373 -

download

14

Transcript of Finished) Construction Productivity 01132012

THE MANUAL OF

CONSTRUCTION PRODUCTIVITY MEASUREMENT

AND PERFORMANCE EVALUATION

CONSTRUCTION

INDUSTRY

INSTITUTE

Page | 1

CHAPTER 1

INSTRODUCTION

Productivity is one the most of frequently discussed topics in the construction

industry. The reason is that productivity translates directly into costs and ultimately in

to contractor profits made or lost on the job. In most projects, productivity is the most

difficult cost component to estimate. It is also the most difficult one to control [7, 14,

17]. Indeed, productivity can be affected by many things, both major and minor. Some

factors are within the control of the contractor may be unaware that adverse factors are

present.

Considering the importance of construction productivity to project cost and

schedule control, one would expected to find a large body of well-codified knowledge

describing how to recognize productivity problems and offering known, sure – to-

successful remedies. In reality, little such information exists on what affects

productivity and, more important, by how much [13]. The range of opinions on factors

is extensive. Some blame global issues such as the economy, union politics, or

government regulations. Others argue that the work ethic is the problem. However, a

growing majority of those closely associated with the construction industry look to the

project itself for the factors affecting productivity. The focus on the way in which

projects are planned, organized, and managed. Fortunately, the implication is that most

of the factors affecting productivity can be identified and controlled to the large

degree. One thing seems relatively certain: Before it can be improves, productivity

must be measured [13].

PURPOSE

The objective of this manual is to describe an approach to construction

productivity measurement that can be used by general and specialty contractors and

owners on small – to medium – sized commercial and industrial projects. Perform

evaluation, which is an extension of productivity measurement, is also discussed. The

concepts are equally applicable to contractors and owners who do not have

productivity measurement system or who need a simple , inexpensive measurement

approach. The approach emphasizes measurements for selected labor-intensive

construction activity at the screw level. The important factors considered I developing

the approach include the size and duration of project; the value of measuring a few

activities instead of the total effort; the relationship to other control systems that may

or may not be used; the need for little or no additional staff or overhead expense; the

need for easy – to – understand, timely, and accurate information; and, last, the needs

of the user.

APPLICATION

The approach described in this manual is not restricted to any particular project

size or type. Appropriate areas of application have been identified on commercial and

industrial project alike. Certain Activities on highway projects and maintenance or

outage work on process, petrochemical, and power plant can be measured using these

techniques. The techniques can be applied equally well to lump sum, unit price, or cost

reimbursable contracts and can be used by owners, contractors, and special

contractors.

Page | 2

This manual is unique in that is a comprehensive guide to measuring

construction productivity. It offer an encouraging and appealing approach to the

measurement task by stating from the outset that productivity measurement is simple,

effective and can be done for little overhead expense. The contractor who implements

the procedures presented in this manual will develop almost immediately an increased

awareness and sensitivity to productivity issues. By following up with corrective

action on the problem that surface, a contractor may easily save 10 percent or more on

the labor cost of the major construction activities that impact total project cost and

schedule.

DEFINITIONS

In this manual, the following terms and definitions are used:

Account – A record or identification scheme used to categorize information about

a specific work item or activity, an account represents a discrete part or category of the

work to be performed. For example, an account may contain the work-hours used in

the erection if formwork for elevated slabs.

Control account – a control account consist of a grouping of related accounts or

activities where each account has a unique degree of difficulty or level effort required.

For example, the account for wall, column, and slabs formwork may be grouped into a

single control account titled formwork.

Control budget – The base estimate of work-hour, quantities, and productivity for

an activity or account, the control budget is used for comparative purposes to evaluate

performance.

Earned value – This technique is used for calculating the percent complete of a

control account. It uses a weighted average approach in which the weight assigned to

each individual account in the control account is based on the initial work-hour

estimate for the account compared to the sum of the initial estimated work-hour for all

accounts included in the control account [5].

Forecasting – The process of projecting the total work-hour required to complete

an account or activity is called forecasting [3].

Performance evaluation – This process involves the comparison of the actual

progress and productivity to the control budget. It includes the comparison of quantity

installation rates and work-hour consumption rates. Forecasting is a part of

performance evaluation.

Performance factor – A measure of construction efficiency, it is the planed

productivity divided by the actual productivity. This ratio is sometimes called a PF

value or a rate ratio. A ratio greater than 1.0 signified better -than – planned

performance.

Productivity – The work-hour require per unit of work, productivity is the input

divided by the output and is calculated for a finite time interval. It is commonly called

the unit rate [17].

Productivity measurement – This process of quantifying the work-hour and

quantities associated with an activity or account provides the measurements used in

productivity calculations and performance evaluations [7].

Page | 3

BARRIER TO MONITORING PRODUCTIVITY

Many contractors do not measure or monitor construction productivity. The most

common reasons for not doing so are:

- I’ve never monitored productivity before.

- I don’t know how to measure productivity.

- Productivity control is a part of a cost control system, which is too complicated

to understand and too expensive to implement

- Productivity cannot be controlled.

- Productivity measurement will not tell me something about my project that o

don’t really know.

The first two reasons cited are really a reflection of past practices where

productivity measurement was not an absolute necessity. Keen competitions for

projects, high inflation rates, increased project complexity, and greater exposure to

unforeseen risks have changed this situation. Productivity measurement has emerged

as an inexpensive way to control one of the more important contractor risks,

specifically the craft work-hours.

Historically, the most widely publicized productivity measurement systems have

emerged from the heavy industrial and power plant construction sectors of the

industry. Here, productivity control has always been treated as subset of the cost

control system. Understandably, many contractors have been discouraged by apparent

complexity and the prohibitive expense of operating a large, complex cost control

system. Until now, the prevailing attitude seems to have been that productivity

measurement must be tied to these types of system [1]. In reality, however, the two

functions of productivity control and cost control can be separated, and, in doing so,

productivity measurement and control can be made simple, inexpensive, effective, and

timely. This manual is the first known comprehensive document that recognizes the

two functions as separable.

The last two challenges to productivity measurement can be considered together.

A growing body of knowledge says that productivity can be controlled [4]. This

assertion is supported by the conclusion that work ethic, labor union, and poorly

motivated workers are not the primary root causes of productivity problems. Studies

have consistently shown that that problems result from the way project are designed,

organized, planned, and managed, and that these conditions exist whether the project is

large or small, commercial or industrial, or union or merit shop [4,144]. The following

are a few of the more commonly reoccurring causes of poor productivity that are

within the exclusive control of the contractor:

- Crews are too large, especially at the beginning and end of and activity.

- Stockpile and storage areas are poorly organized.

- Materials are inadequately marked or not sorted fro easy retrieval.

- Delays result from waiting for tools and equipment.

- Housekeeping practices are poor.

- Inability to maintain continuity or momentum results because screws are

reassigned to different to work or locations.

- Work of one screw interferes with that of another.

- Sequencing and control of the work are poor.

- Material deliveries are untimely.

Page | 4

This list could easily be expanded, but the important point is that many of these

causes exist to varying degrees on all construction projects.

If these causes occur repeatedly, why aren’t they corrected? Actually, many of

them are subtle and appear gradually. Although, they may never be noticed, they are

still there. Often, by the time a problem is noticed, the damage has already been done.

In many other cases, corrective action is perceived to cost more than it would save.

What then is the role of productivity measurement and performance evaluation?

They should provide early warning signals, long before the problem is obvious. They

should answer the question: How serious is the problem? They should be the basis for

measuring the economic impact of alternatives and should be the basis measuring the

economic impact of alternatives and should provide an easy means for quantifying the

results.

ORGANIZATION OF THE MANUAL

This manual is organized into four main parts. The first part, which includes

chapter 2 and 3, describes the framework for productivity measurement. Chapter 2

explains the basic concepts of cost control, cost accounting, and productivity control.

Chapter 3 defines the system criteria and then develops the framework for productivity

measurement and control. Productivity accounts are presented, and the relationship to

other account and control system is described.

Part II of the manual explains the basic concepts of productivity measurement,

reporting, and devaluation. Chapter 4 describes how to measure work-hour and

quantities. Five methods of quantity measurement are described. Chapter 5 shows four

types of productivity calculations and graphically illustrates each. The advantages of

tabular and graphical output are described. Chapter 6 describes performance

evaluation, which is the process of comparing the productivity calculations with the

project estimate. Analytical and graphical forecasting techniques are illustrated.

More advanced concepts are addressed in part III. Rues of credit for complex tasks

and the earned value technique for control accounts are coveted in chapter 7. The

technique the forecasting using standard productivity curves is also detail. Chapter 8

addresses concepts that integrate productivity and schedule parameters.

Part IV presents several case studies and summarizes the results. Chapter 9

describes case studies of three contractors involved primarily in commercial and light

industrial construction. Their long – range objectives in measuring productivities are

describes along with lesions learned during the implementation process. The case

studies illustrate how productivity can be used to understand the factors that affect

productivity, to monitor and control important activities, and to develop labor units for

estimating. Chapter 10 summarizes the case study finding and conclusion.

USE OF THE MANUAL

The manual explains concepts in a general way, which means the techniques can

be applied regardless of the type of control system already in-place, nature of work,

sophistication of the contractors, and so forth. Part I explains the framework for

productivity measurement, and readers who have an understanding of productivity

control using a cost control system may wish to begin directly with chapter 3. For the

experienced user, chapter 2 and 3 describe the context in which measurements are

made. These two chapters will ease apprehension that contractor must implement a

cost control system to used the techniques; no significant changes in current modes if

Page | 5

operation are required. An experienced user should first concentrate on the basic

concepts in part II. As one becomes familiar with these, the first step beyond manual

tracking will probably be to computerize the process, which can be done relatively

easily on a spreadsheet program such as LOTUS 1-2-3 or on an integrated system like

framework II or SYMPHONY. After mastering the basic concepts on several projects,

the contractor may be ready to try some of the advance concepts in part III. The

experienced users may want to review part II before proceeding to part III, or may be

feel comfortable about implementing some of the advanced concepts from the outset.

All reader will find the case studies in part IV to be valuable, as they describe some

specific about implementation and details of lessons learned. The examples illustrate a

wide range of applications.

Page | 6

PART I - FRAMEWORK FOR PRODUCTIVITY CONTROL

An outgrowth of defense systems acquisition and large , cost reimburse

construction projects such as for nuclear power plants, refineries and coal gasification

facilities was the development of sophisticated cost control systems. These systems are

characterized by the breakdown of project expenditures according to code of accounts

Each account can be monitored for excessive costs, and these can be traced to the

source, e.g. , labor, construction equipment, construction materials, permanent plant

equipment, etc. [11].

Cost control systems have also been used to monitor labor productivity but

whether they are the most effective way of monitoring productivity questionable. This

section of the manual will develop the framework around which productivity can be

monitored in a simple and timely manner. Chapter shows that the cost control system

can be used for two purposes, and that the system is used affects the level of detail.

The most detailed form is needed for control purposes. The code of account structure

is designed to isolate problem areas. With this system, all project activities are tracked

in considerable detail, there is a feedback loop, and a support staff is needed. The

second form of the costing model is used only for accounting purposes. This simple

system, which supports the need to develop historical estimating data, concentrates on

accumulating costs at the end of the project. Many contractors use this type of model

because it is easy to understand and inexpensive to carry out. Unfortunately, the need

for controlling the rationale for simplifying the cost control system is then developed.

Chapter 3, the criteria for a productivity measurement and control system presented.

Using these criteria, the code of accounts for petrochemical facility and general

commercial construction are revised to be consistent productivity control needs. A

framework is developed in which productivity control operates separately from the

cost control system.

Page | 7

CHAPTER 2

FRAMEWORK FOR PRODUCTIVITY MEASUREMENT

AND PERFORMANCE EVALUATION

INTRODUCTION

A successful project is generally considered to be one that meets certain technical

objectives, is completed on or ahead of schedule, within the owner’s or contractor’s

budget, and results in a reasonable profit for the contractor. To ensure success, an

effective project control system must be implemented to provide managers and

superintendents with timely and accurate feedback on the consumption of resources.

Historically, this has meant the implementation of a cost control system. Prior to the

development of the productivity measurement system presented in Chapter 3, it is

worthwhile to review the differences in detail and usages of costing systems.

CHARACTERISTICS OF COSTING SYSTEMS

Usages

Costing system are designed to track and account for project costs. The reasons for

doing so are two-fold. First, the tracking function can be used during construction to

control project costs. Tracking highlights activities or areas that deviate significantly

from planned expenditures so that corrective action can be taken. How the system will

be used generally establishes the level of detail and degree of sophistication [11].

Costing system to Support Cost control

The more detailed and sophisticated systems are used to monitor and control cost

during construction. While these systems also support the estimating of future projects,

the requirement for considerable detail and sophistication arises to satisfy three

essential needs related to the control function: 1) to develop comparisons to project

estimates during construction, 2) to provide timely feedback, and 3) to isolate

particular problem areas where cost deviations are significant. Figure 1 shows the

overall cost control process. During construction, the contractor must account for costs

and work-hours and measure progress. Comparisons to the control budget are made

periodically, and corrective action is taken when required.

The framework for cost control is a standard code of accounts which defines how

costs will be categorized. Since costs and work-hours are used to estimate future work,

they must be consistently charged to each account from project to project [10]. Thus,

codes of accounts are typically standardized, and the accounts used for each project are

uniquely selected from the standard codes. The term “standard” should not be

misinterpreted, as there are no standards of practice. In reality, most contractors

develop their own standard codes that are uniquely tailored to their own mode of

operation.

Page | 8

Figure 1: Costing system to Support Cost Control

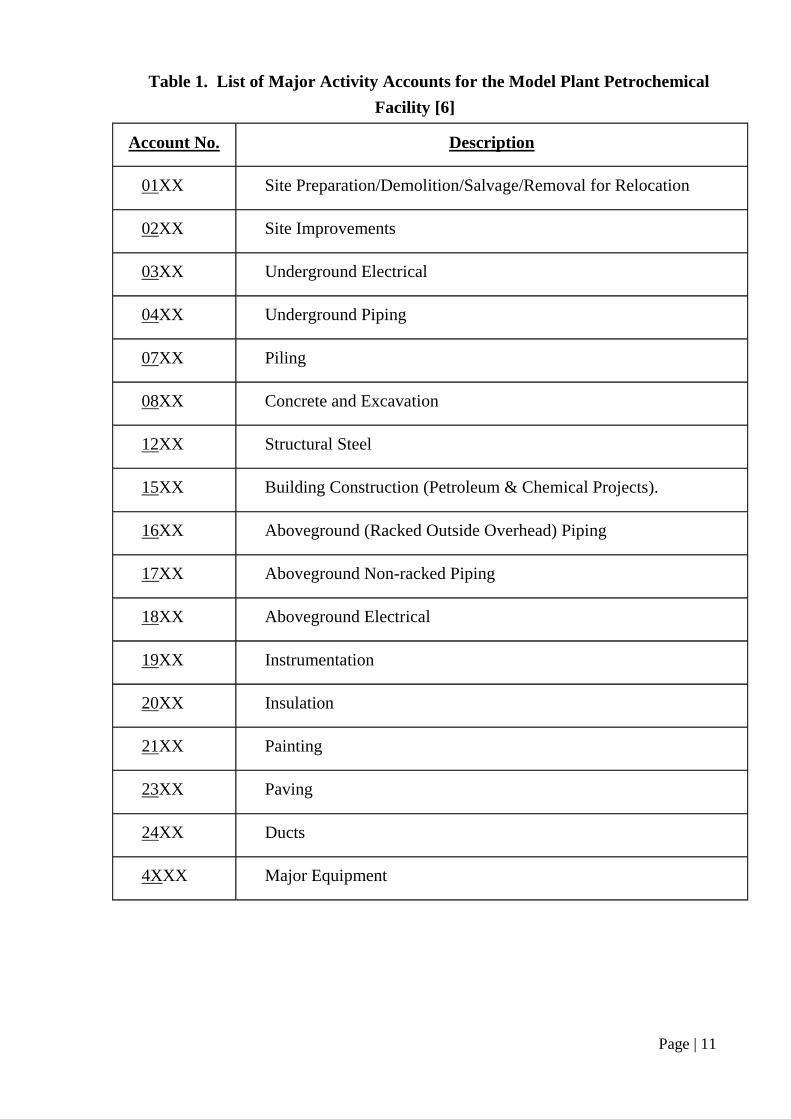

The hierarchical nature of cost codes is illustrated in Figure 2, which shows an

example of a code structure for a grass roots petrochemical facility [6]. Because the

emphasis is on isolating problem areas, the cost indicators allow for the charging of

expenditures to more narrowly defined areas such as direct costs, indirect costs,

subcontract costs, or home office costs. A four-digit activity code is divided into three

levels of detail. The first two digits define major activities or types of work and are

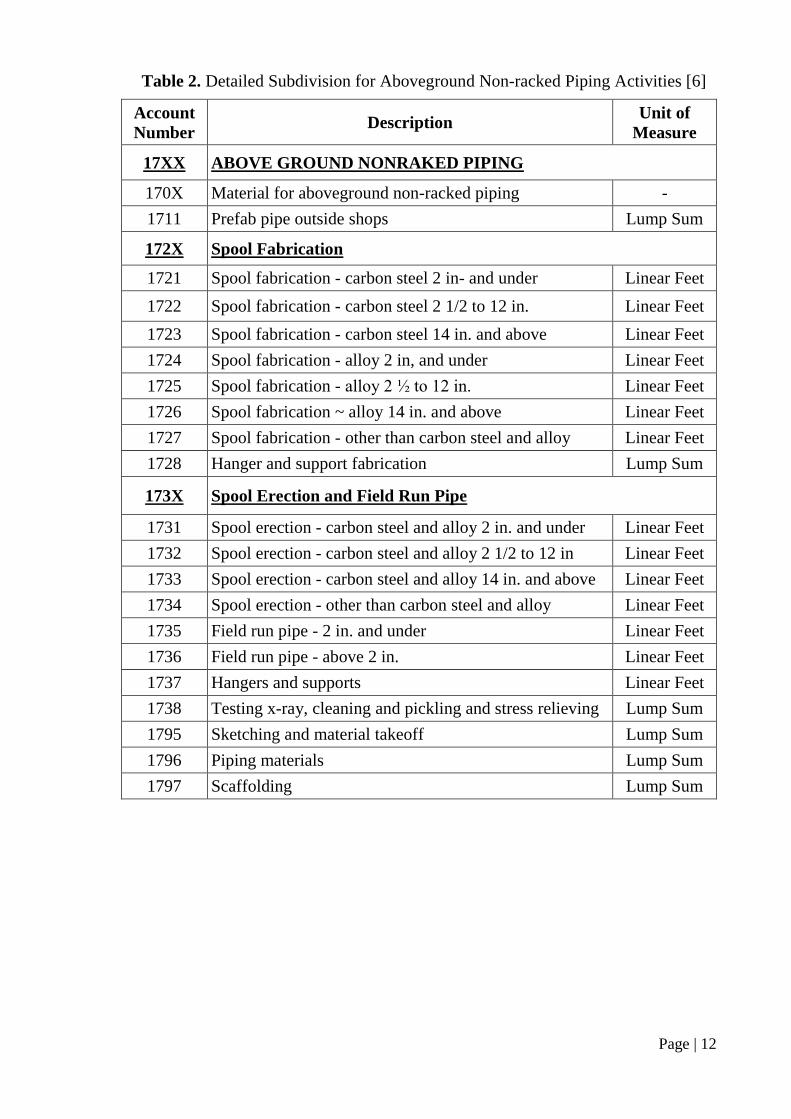

illustrated in Table 1. Table 2 shows the detailed subdivision of account 17xx, which is

aboveground non-racked piping. The cost classification code is used to further divide

the costs into direct labor, construction materials, construction equipment, and so

forth. In a comprehensive cost control system, numerous cost classification codes are

used.

Costing Systems to Support Estimating

The costing systems used only to support the estimating function are less

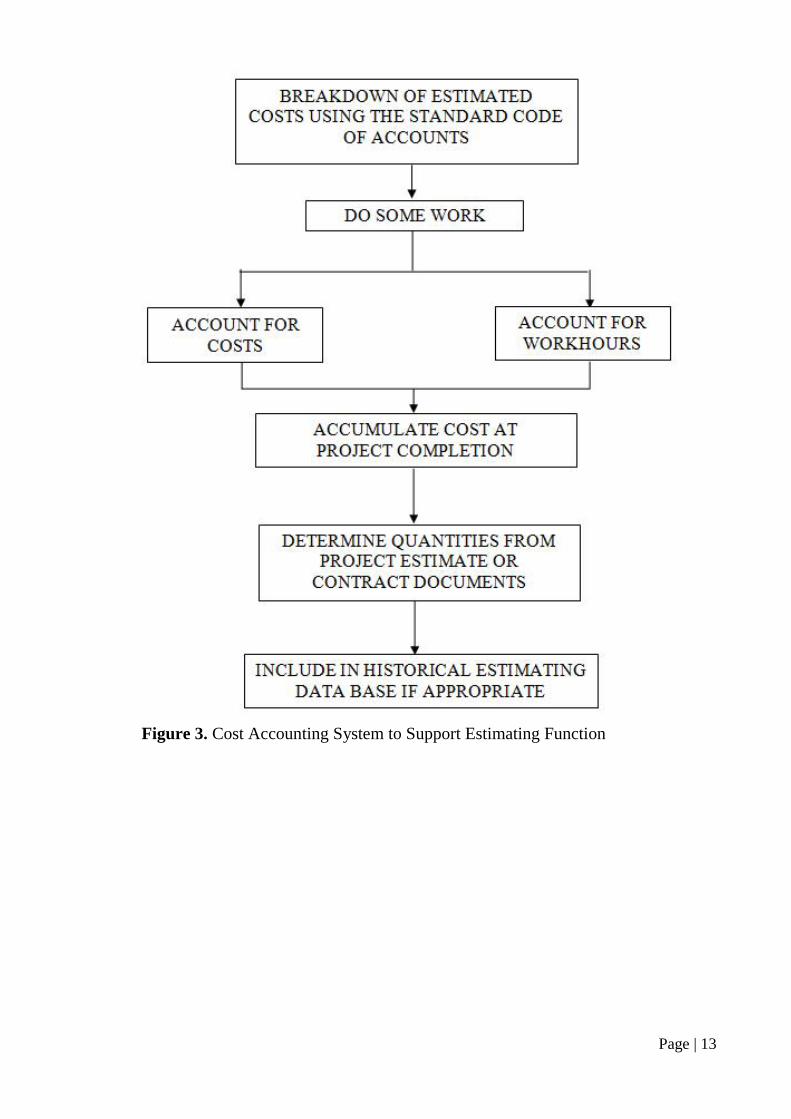

sophisticated and not as detailed as those required for cost control. Figure 3 illustrates

the reason. As can be seen, there are no comparisons to projects estimates, no variance

analyses, and no feedback loop. The main emphasis is on accumulating costs at the

end of the job, so timeliness is not an issue, and minimal or no support staff is needed.

Also, quantities or progress are often not measured but rather are summarized at

project completion. These data may be extracted from the project estimate or contract

documents.

Page | 9

The code of accounts need not be as detailed as that required for cost control two

reasons. First, it is not necessary to divide the project into areas since the code of

accounts is not being used to isolate problem areas. Second, a contractor would prefer

to have certain components of work grouped into a single account. An example would

be piping plus related scaffolding and material handling. Groupings that include

similar work plus the manual direct and indirect support effort facilitate the need to

develop accurate estimates in a relatively short period of time.

The net result is that only part of the code of accounts shown in Figure 2 is

needed. The applicable portion is shown in Figure 4, where the 16 digit code used for

cost control has been reduced to 10 digits. The number of possible entries for the cost

classification part of the code would be greatly reduced, from 50 or more to probably

four or five. The number of cost indicators would probably be reduced as well.

PRODUCTIVITY CONTROL

Historically, productivity measurement and control have been done almost

exclusively as a subset of the larger, more detailed cost control systems. The literature

abounds with articles and advertisements that show how to monitor costs and

productivity using the cost control system [3, 5, 15, 19].

Ironically, the fact that these two control systems are typically viewed as one is

probably a main reason why many contractors do not measure productivity. To these

contractors, cost control systems are too large and complicated, require a support staff

dedicated to measuring and quantifying site activities, and result in an intolerable

overhead expense [5]. Alternatively, these contractors rely on the much simpler

accounting-type systems such as the one shown in Figures 3 and 4. However, these

provide little in the way of control.

Fortunately, productivity measurement can be greatly simplified while still

providing control. If comparisons are to be made with the project estimate, then

productivity control must originate from the same code of accounts as does the cost

control system. Thereafter, productivity measurement and control can be done

separately from the cost control system. This separation allows the freedom necessary

to tailor the system to perform a specific function. The result is a system that is simple,

timely, and inexpensive» The remainder of the chapter develops this concept through

an explanation of the desired goals needed to achieve the cost-effectiveness of the

system.

Page | 10

Figure 2: Cost Account Coding Structure for Cost Control [6]

Project Number: Identifies the Project. (4 digits)

Cost Indicator: (Summary Indicators) One – digit numbers that represent broad

general categories such as direct labor, indirect costs, subcontract costs, or home office

cost. (1 digit)

Area: Designation is reserved for project numbers which relate to geographical

area, process unit, and so forth. (4 digits)

Activity: That part of the code of accounts used to describe a physical item of

work task to be performed. Example activities include piping, duct, backfill, roofing,

and so forth. Activities are the primary labor accounts. (4 digits)

Cost Clarification: Used to categorize the origin of project costs in terms of craft

labor, indirect labor, construction equipment, construction materials, permanent

material, permanent plant equipment, and so forth. (3 digits)

Page | 11

Table 1. List of Major Activity Accounts for the Model Plant Petrochemical

Facility [6]

Account No. Description

01XX Site Preparation/Demolition/Salvage/Removal for Relocation

02XX Site Improvements

03XX Underground Electrical

04XX Underground Piping

07XX Piling

08XX Concrete and Excavation

12XX Structural Steel

15XX Building Construction (Petroleum & Chemical Projects).

16XX Aboveground (Racked Outside Overhead) Piping

17XX Aboveground Non-racked Piping

18XX Aboveground Electrical

19XX Instrumentation

20XX Insulation

21XX Painting

23XX Paving

24XX Ducts

4XXX Major Equipment

Page | 12

Table 2. Detailed Subdivision for Aboveground Non-racked Piping Activities [6]

Account

Number Description

Unit of

Measure

17XX ABOVE GROUND NONRAKED PIPING

170X Material for aboveground non-racked piping -

1711 Prefab pipe outside shops Lump Sum

172X Spool Fabrication

1721 Spool fabrication - carbon steel 2 in- and under Linear Feet

1722 Spool fabrication - carbon steel 2 1/2 to 12 in. Linear Feet

1723 Spool fabrication - carbon steel 14 in. and above Linear Feet

1724 Spool fabrication - alloy 2 in, and under Linear Feet

1725 Spool fabrication - alloy 2 ½ to 12 in. Linear Feet

1726 Spool fabrication ~ alloy 14 in. and above Linear Feet

1727 Spool fabrication - other than carbon steel and alloy Linear Feet

1728 Hanger and support fabrication Lump Sum

173X Spool Erection and Field Run Pipe

1731 Spool erection - carbon steel and alloy 2 in. and under Linear Feet

1732 Spool erection - carbon steel and alloy 2 1/2 to 12 in Linear Feet

1733 Spool erection - carbon steel and alloy 14 in. and above Linear Feet

1734 Spool erection - other than carbon steel and alloy Linear Feet

1735 Field run pipe - 2 in. and under Linear Feet

1736 Field run pipe - above 2 in. Linear Feet

1737 Hangers and supports Linear Feet

1738 Testing x-ray, cleaning and pickling and stress relieving Lump Sum

1795 Sketching and material takeoff Lump Sum

1796 Piping materials Lump Sum

1797 Scaffolding Lump Sum

Page | 13

Figure 3. Cost Accounting System to Support Estimating Function

Page | 14

Figure 4. Cost Account Coding Structure for Estimating

Project Number Identifies the Project. (4 digits)

Cost Indicators (Summary Indicators) One-digit numbers that represent broad

general categories such as direct labor, indirect costs, subcontract costs, c hone office

costs. (1 digit)

Activity That part of the code of accounts used to describe a physical item of work

or work task to be performed. Example activities include piping, duct, backfill,

roofing, and so forth. Activities are the primary labor accounts. (4 digits)

Cost Classification Used to categorize the origin of project costs in terms of

craft labor, indirect labor, construction equipment, construction materials, permanent

material, permanent plant equipment, and so forth. (1 digit)

Denotes the unused portion of the cost code

Track Only Important Activities

It is recognized that, on any given project, most of the work-hours ^are consumed

by a small number of activities. If one controls these activities, he essentially controls

most of the project people resources. The problem inherent with cost control systems

is that they are designed to track all project expenditures. This means that the

contractor needs to measure the output over the total project before he can extract

information about the activities that are truly important. Additional overhead staffs are

often needed to operate the system and to interpret the results. Understandably,

contractors who are not ■ accustomed to measuring productivity are not eager to count

light fixtures, doors, ladders, handrails, valves, pipe hangers, and the thousands of

other minor items that must be installed, 3y tracking productivity separately, the

contractor can choose to monitor only those activities that he feels are important.

Simplify the Code of Accounts

To many contractors, codes of account structures like the ore illustrated in Figure

2 are overly complex. They require detailed narratives of what to include in each

account, and considerable tine may be needed to reconcile errors resulting from costs

being charged-to the wrong account, "When tracking is done separately from the cost

control system/ field personnel need to deal only with the four-digit labor accounts as

shown in Figure 5.

Page | 15

Tailor the Level of Detail

The level of detail in the code of accounts is typically established on the basis of

costs and does not always fully support the productivity control needs. Two examples

illustrate this point. The cost of 6-inch-KHameter stainless steel pipe is different from

that of 2 1/2-inch-diameter carbon steel pipe. In the cost control system, these

commodities are tracked separately. But, from the productivity measurement

viewpoint, the two may be nearly identical. Furthermore, a crew may install several

types of pipe in a single day, thus requiring that the quantities and work-hours be

reported by type. Thus, the costing system places an added burden on a reporting

system that contains more information than may be required for productivity control.

Figure 5. Codes for Productivity Measurement

Activity That part of the code of accounts used to describe a physical item of

work or work task to be performed. Example activities include piping, duct, backfill,

roofing, and so forth. Activities are the primary labor accounts and are thus the

productivity codes. (4 digits)

Denotes the unused portion of the cost code

In the second example, the unit cost difference of structural steel for commercial

multistory and structural steel for warehouse-type buildings may be sufficiently minor

to allow the two to be included in the same cost account. However, the units work-

hours for erection maybe very different. In this case, productivity control requires a

level of detail not available in the costing system. As illustrated in these two examples,

cost control and productivity measurement sometimes require different levels of detail.

Separate tracking allows the flexibility to meet the particular, needs at hand.

Simplify Units of Measure

The units of measure are established by a cost engineer or estimator for his own

particular need* Structural steel is purchased by the ton, so the measurement of

installed quantities is also by the ton. A foreman or superintendent can easily

determine how many pieces of structural steel have been erected and bolted, but to

convert these pieces to tons requires considerable time to study the drawings and to

make calculations. Likewise, an estimator determines the number of pipe hangers on

the basis of so many hangers per linear foot of pipe. Field personnel may know how

many hangers were installed, but, without measuring or studying the isometric

drawing, they will not readily know the footage. Thus, the units of measure used to

Page | 16

support estimating or cost control can sometimes place added burdens on field

personnel by requiring excessive measurement and quantification of the work.

Reduce the Amount of Data

Cost control systems handle sizeable amounts of data. The output generated is

typically in the form of summary statistics or numerical-data. Field supervisors who

would normally make use of productivity data have limited time or enthusiasm for

studying the numbers to make inferences about the progress of their work. Graphical

analyses enhance the ability to quickly interpret information, but, in some cost control

systems, the main emphasis is on generating numerical data, not graphs. The

timeliness of feedback is another concern. Consequently, some cost-control systems

provide information to field personnel in a form that is difficult to interpret, and which

may arrive too late to be of value.

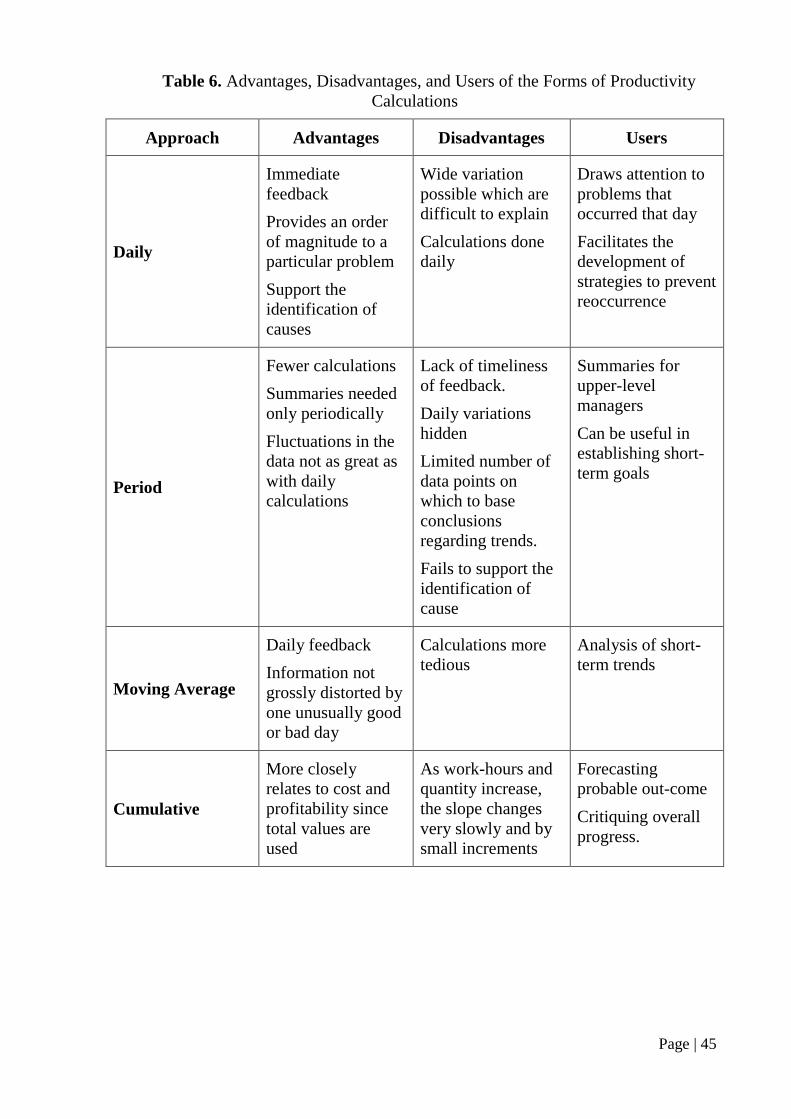

SUMMARY

This chapter has shown that the level of detail in a costing system is related to how

the system is used. Many small- and medium-sized contractors want to collect only

historical estimating data. Their systems are simple and can be used with minimal

overhead expense. However, a system used for cost control purposes is far more

complex and expensive to operate.

Most contractors associate productivity measurement with cost control, but

productivity can be monitored and controlled separately from the cost control system,

and this means of measurement is recommended. Cost-control systems track

everything? Productivity control monitors only a few items controlling the work. The

level of detail needed for productivity control is not always the same as for cost

control. The units of measure are established by cost engineers and estimators, and

these often place unnecessary demands on field personnel for measuring and

quantifying their work. The feedback in cost control systems is sometimes in the form

of numerical data, whereas many field personnel having minimal experience with

measuring productivity prefer graphical output.

Page | 17

CHAPTER 3

CONCEPTUAL DESIGN OF THE PRODUCTIVITY

MEASUREMENT SYSTEM

The productivity measurement and performance evaluation system developed

herein for: 1- Small and medium-sized contractors who do not routinely measure

productivity and 2 - The larger and more sophisticated contractors who are

constructing projects for which the project budget prevents the use of a detailed and

expensive cost control system. Project can be commercial or industrial, or other types

which include labor-intensive activities. Maintenance and outage-type work are also

ideally suited for the productivity measurement system.

BASIS FOR SYSTEM DEVELOPMENT

Project Characteristics

On most commercial projects, the overhead expenses must be kept to a minimum.

The same situation prevails in the heavy industrial sector of the industry. The mega

projects of the 1970s are no longer being built, and shorter and smaller projects place

special demands on cost-control systems such as the one described in Chapter 2. The

structure of the code of accounts makes it difficult to reduce project overhead by

simply reducing the scope of the cost control system. While the support staff can be

trimmed, the need for some support will always exist. Activity durations today are

shorter then they have been in the past. Important controlling activities sometimes last

only 30-60 days. If effective control is to be exercised, feedback must occur quickly.

Even a two-week reporting cycle (most projects function on a monthly reporting cycle)

provides reporting probably too infrequently.

The need to reduce overhead means that quantity tracking must be provided by

those who are responsible for doing the work. Lower level supervisors are neither

accustomed to working with intricate cost codes like the one shown in Figure 2, nor

are they anxious to spend the time necessary to perform anything more than

elementary measurements. Unfortunately, these are the elements needed to drive the

cost control system.

Assumptions

The design of the productivity measurement system must consider the essential

features of cost control system as described in Chapter 2 and relate these to the

environment in which it must function. Therefore, the following assumptions are

presented as the basis for developing the productivity measurement system.

1. The productivity measurement system must be structured around the code of

accounts if comparisons to the project estimate are to be made. However, the tracking

and feedback can be done separately from the costing system.

2. A contractor’s code of account establishes the basis for deciding which activities to monitor. If the codes are too broad to support effective monitoring, the

system can still function as a stand-alone system. However, comparisons to project

estimates may not be possible.

3. Systems presently used by contractors to track or control costs are which

unaffected by the productivity measurement system.

Page | 18

4. The contractor is not required to install a cost control system in order to

measure and control productivity.

5. The productivity measurement system can operate independently from the

estimating or schedule control system. Productivity measurement can yield worthwhile

results, even if one do not have a work-hour, quantity or schedule estimate. However,

performance cannot be evaluated without these estimates.

6. Only direct labor accounts are of interest. The most cost-effective which

approaches to productivity control is to concentrate on the labor-intensive activities.

Such activities are a small percentage of the total number of activities, yet they have

the greatest effort on the project.

7. The focus of the measurement effort is at the crew level.

8. The system is implementable at the job site and able to be done manually.

However, if a microcomputer is available, it will facilitate this task.

System criteria

The assumptions listed provide guidance for developing the productivity

measurement system. The system should satisfy the following criteria:

1. Inexpensive - The system should be easy to implement, require little overhead

to operate, and have the capability to be manually driven

2. Simple – The data requirements should be minimal. Reporting should be done

by foremen using easy-to-comprehend units of measure; output should make liberal

use of graphics.

3. Flexibility – The system should be easily tailored to the operational needs and

objectives of the contractor. Rigid, inflexible systems, which require the contractor

instead, to adjust his mode of operation to the system, are undesirable.

4. Accuracy – The output must reflect what actually occurs at the site. The level of

detail should help to isolate problem areas.

5. Timeliness – Feedback must be given quickly so that corrective action can be

taken on short-duration activities. End-of-the-day feedback is possible, if it is

desirable, thus summaries can be produced weekly. Otherwise, feedback can be

provided at a frequency consistent with the scope and magnitude of the project.

6. Support Performance Evaluation – Labor comparisons to the project estimate

should be possible. This includes comparisons to the estimated work-hours, quantities,

unit rate, and planned duration for labor-intensive activities.

Page | 19

FRAMEWORK FOR PRODUCTIVITY MEASUREMENT

The above criteria have been used in developing the productivity measurement

system that is described throughout the remainder of this manual.

Reporting Requirements

The reporting system relies upon the input of two data items namely work-hours

and quantities (progress) for selected labor-intensive activities. The data collection and

analysis process are shown in Figure 6.

The foreman, on a daily basis, records the work-hours spent by a crew in

performing the particular task in question and the quantities installed or progress made

by the crew that day. Generally, the reporting of work-hours is done for payroll

purpose, so productivity measurement imposes no new work-hour reporting

requirement. The only possible change in reporting work-hours maybe reported

separately those work-hours spent on the activity being-monitored.

The reporting of quantities, or progress, is not routinely done by many contractors.

However, the knowledge of how much work has been done which is a fundamental

requirement for monitoring and control. The quantity-reporting scheme developed

herein, and described in detail in Chapter 4, is simple, is done for only a small number

of labor-intensive activities, is characterized be easy-to-use units of measure, and can

be easily and quickly summarized by the foreman at the end of the day.

As shown in Figure 6, productivity calculations are made using the reported work-

hours and quantities. These calculations can be done manually, but the most efficient

approach is to use a microcomputer. Input can be done by a clerk or time keeper.

Because the amount of data input is miniscule, the entire entry and analysis process

involves minimal effort and time. Feedback should be almost instantaneous, and

computer programmers, systems operators. Quantity surveyors or data entry personnel

are unnecessary.

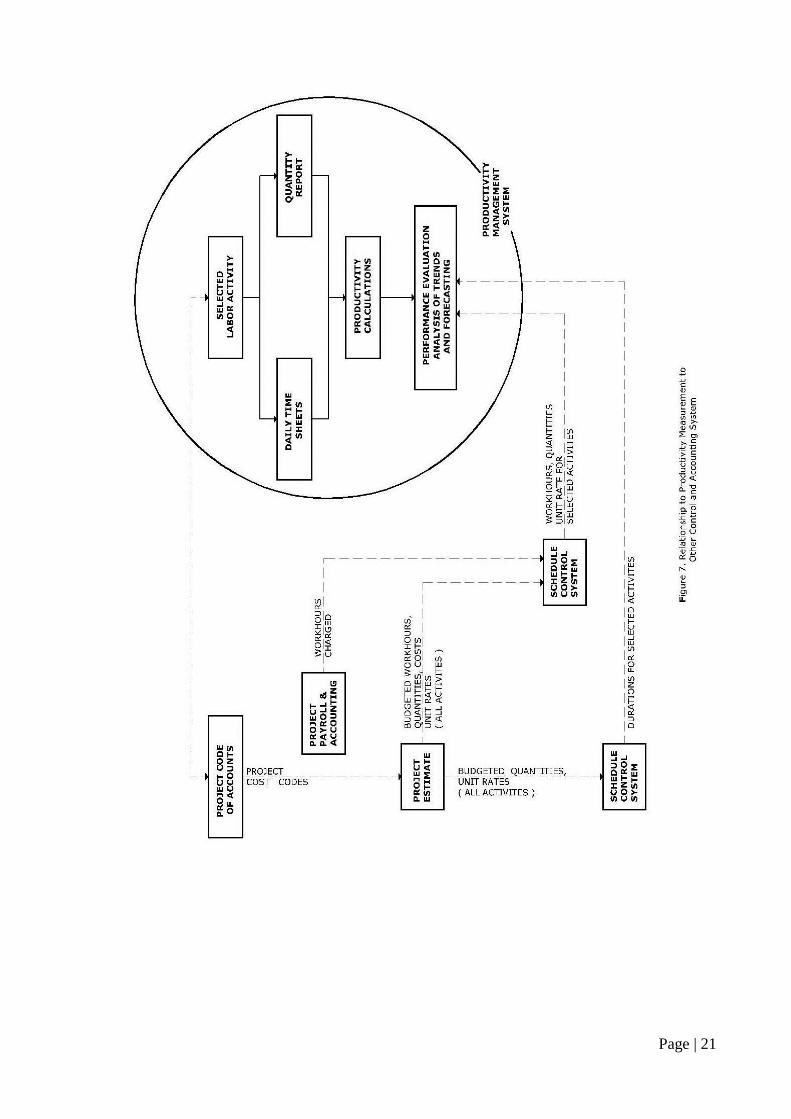

Relationship to Other Accounting or Control Systems

Productivity measurement is designed to be a stand-alone system that is

implemented entirely at the job site. Nevertheless, it is related to several other control

and accounting systems. As shown in Figure 7, the productivity measurement system

utilizes information available from other systems but does not provide feedback to

these systems.

The selection of activities to monitor should be made according to the breakdown

of project activities established by the costing system. The reason for this is quite

simple work-hour reporting will be done this way for both payroll and cost-accounting

purposes. Productivity measurement then can rely on the same work-hour data that is

necessary if comparisons to the project estimate are needed. Where cost accounting

and monitoring systems are already in place, a definition already exists of the items

included in each account, and dual reporting would merely increase the confusion and

amount of paperwork.

Page | 20

Page | 21

Page | 22

Data from the cost accounting and control system are used to prepare project

estimates. Several important pieces of data from the estimate can be used to enhance

the productivity measurement system. These items are the estimated total work-hours

and quantities. The estimated unit rate can also be calculated. These parameters

provide important baselines for comparing current performance.

Although schedule control is generally viewed as separate from cost or

productivity control, productivity and quantity installation rates are an integral part of

predicting completion dates. Therefore, if available, the planned completion date or

estimated duration can be used to evaluate performance.

Selection of activities to monitor

The activities that should be monitored are the ones which affect the success of the

project. To maintain simplicity and minimize project overhead, only those activities

that affect the success of the project should be tracked, those that are labor-intensive.

The labor-intensive activities tend to have the longest durations and therefore are

critical form the schedule point of view.

Often, activities to monitor can be selected on the basis of experience. An

alternative approach is to calculate the total project work-hours and to divide this sum

by the number of line items or accounts. This calculation yields the average work-

hours per line item. Those items or accounts for which the estimated work-hours are

greater than this average can be designated as labor-intensive. This method usually

results in less than one-fourth of the line items or accounts being significant. This list

can be further modified at the prerogative of the manager.

Development of productivity codes

The project code of accounts is structured to support the cost control or accounting

function. However, productivity control is comparatively simple and narrower in

scope. Thus, productivity code structures for industrial and commercial construction

are discussed below.

Figure 5 shows how a 16-digit cost code used for the construction of

petrochemical facilities can be reduced to four digits. The four-digit activity code is

ideally suited for productivity control. This four-digit productivity code defines three

levels of detail. The broadest level, represented by the first two digits, denotes major

construction activities such as aboveground electrical, aboveground non-racked piping,

and so forth. Table 1 provides a complete listing of the 17 major activities. The third

and fourth digits further subdivide each major activity. Figure 8 illustrates the

productivity code for the erection of aboveground conduit. A fifth digit (not shown)

can be added at the user’s discretion to further define the conduit by size or type.

Figure 8. Structure of Productivity Measurement Codes for Industrial

Construction

18 1 2

SUBFEATURE LEVEL

1. Aboveground Conduit

FEATURE LEVEL

2. Electrical Raceways

MAJOR ACTIVITY OR FUNCTION LEVEL

2. Electrical Raceways

Page | 23

The structure of example of productivity measurement code for commercial

constructions is shown in figure 9 to be a five-digit code. The code number represents

structural formwork for concrete columns. The code structure is based upon the master

format published by the construction specifications institute (CSI) [12]. The major

activity or function level is denoted by the first two digits. Among the major activities

is concrete, masonry, metals, mechanical, and electrical work. The remaining three

levels further subdivide the major activities by size and type of work.

Once the code structure has been established, it is necessary to develop the

various project accounts, which is accomplished by examining the complete code of

accounts and identifying likely labor-intensive accounts and identifying likely labor-

intensive activities. The non-labor-intensive accounts and others involving incidental

work can be deleted. The remaining accounts form the productivity measurement

codes. Representative codes are listed in appendices A and B for industrial and

commercial construction, respectively. The total number of accounts has been reduced

by a factor of more than four or five.

Unit of measure

The units of measure should be simple and easy to apply and should not burden

field personnel with unnecessary or time-consuming measurements. Convenient

counting schemes are desirable, and the units of measure must be selected so that

results are accurate.

In most instances, the same units used in the costing system can be used in the

productivity measurement system. However, there are exceptions. The following

partial list shows some of the accounts where the units of measure may be different:

Alternative Units of measure

Item of

work Cost Control Productivity measurement

Structural Steel Ton Piece, level, or tons

Pipe Hangers Linear feet Each

HVAC Duct Ton Linear feet

Sheet Piling Ton Linear feet

Column

Formwork

Square feet of

contract area

Linear feet, each, or square feet of

contract area

Obviously, the units in the costing system reflect how materials are purchased,

whereas, in the productivity system, they should relate to how components are

installed, units can vary from project to project.

Page | 24

Figure 8. Structure of Productivity Measurement Codes for Commercial

Construction

SUMMARY

This chapter has presented the framework for the productivity measurement

system that satisfies five criteria determined by the characteristics of the project and

the field supervisors who must rely upon the system. Crew level reporting is required

on a daily basis, and only labor –intensive activities are monitored. The productivity

measurement codes originate from the code of accounts designed for cost control

purposes, but the number of accounts is greatly reduced by eliminating non-labor-

intensive codes. In some instances, the units of measure have been changed to more

closely reflect how components are installed. Because the productivity measurement

system is not needed to provide feedback to other control systems, it is flexible and

can be tailored to suit particular project needs.

1 1 3

TYPE

1 Slab on grade

2 Elevated Slab

3 Colums4 Footers7 Beams

FEATURE LEVEL

1 Formwork

MAJOR ACTIVITY OR FUNCTION LEVEL03 Concrete

FEATURE LEVEL

1 Structural

03

Page | 25

PART II – BASIC CONCEPTS OFPRODUCTIVITY MEASUREMENT

AND PERFORMANCE EVALUATION

Productivity measurement and performance evaluation are two separate functions.

Productivity measurement involves the collection of information about various

activities. Specifically, production and the corresponding work-hours over o given

period of time are assigned to their respective activities or accounts, and these data can

be examined to determine if productivity is improving or declining.

Performance evaluation, on the other hand, involves a comparative analysis.

Work-hours, quantities, and productivity are evaluated against the planned values used

in the original project estimate. Activity durations can be projected and compared with

the planned or required completion dates of the activities.

Part II of this manual introduces the simplified concepts of productivity

measurement and performance evaluation. Chapter 4 describes five simple concepts of

measuring quantities and provides guidelines for selecting an appropriate measurement

method. The tracking of work-hours is also addressed. Chapter 5 shows how

productivity can be reported. Various calculations and formats are giving, and their

interpretations are illustrated. Principles of performance evaluation are given in

chapter 6, which also explains how to develop work-hour and productivity forecasts.

Page | 26

CHAPTER 4

MEASUREMENT OF QUANTITIES AND WORK-HOURS

INTRODUCTION

The tracking of work-hours alone is inadequate as a monitoring or control measure

because work-hours must be evaluated in the context of the amount of completed

physical work. It follows that effective project monitoring requires the measurement

of both the quantities and the work-hours needed to install these quantities (2, 13, 15,

16) The first part of this two-part chapter describes the basic principles of quantity

measurement (surveying), and the last part addresses the measurement of work-hours.

SIMPLICITY: THE CORNER STONE OF EFFECTIVE MEASUREMENT

Simplicity and effectiveness may at first seem to involve trade-offs, but, in reality,

the two features support each other. When concepts are simple, they are readily

understood. If a technique is simple, and therefore readily understood, it will be easy

to use, and its acceptance and application in a variety of situations will be more likely.

This simplicity encourages users to tailor the technique to their particular needs,

resulting in effective measurement.

Throughout this manual, simplicity has been integrated into the conceptual design

of the system. The most important advancement toward simplicity is the separation of

the productivity measurement system from the cost control system, making possible a

substantial reduction in the number a complexity of cost accounts and the use of

simple and convenient units of measure. These principles were described in Chapter 3

and were used to develop the productivity codes in Appendices A and B.

Freedom from the costing system also means that monitoring can be done the job

site without a need for support personnel. Feedback can be obtaining daily rather than

weekly or monthly. The conciseness of the data means it can be readily digested by the

project superintendent or foreman. Each these aspects are illustrated throughout the

remaining chapters in this manual

PRELIMINARY CONSIDERATIONS

When designing productivity control system for a Specific project, two

preliminary considerations must be made: the selection of the activities the will be

monitored and the level of detail in reporting.

Not all productivity codes are needed to establish effective project control; only

the codes important to the particular project should be used. While no conclusive rules

can be established, consideration should be given activities that are labor-intensive,

last long enough for corrective action be taken, and are interrelated with other

activities. If available, a CPM schedule can be used to identify activities with little or

no float time. Activities should be selected after considering the scope, complexity,

and duration of the work.

The level of detail relates to the scope of work for a particular activity and can

vary from project to project. Three illustrations of labor-intensive activities are given

below. The first involves pipe spool erection and field run pipe on a process facility,

and the second activity is structural steel erection on an office building. The last

Page | 27

activity is cable pulling on a refinery project. The following levels of detail selected

from Appendices A and B are possible:

1. Pipe spool erection on a process plant

17XX ABOVEGROUND NONRACKED PIPING

1730 Spool Erection and Field Run Pipe

1732 Spool Erection, 2 1/2 to 12 in.

1735 Field Run, 2 in. and under

2. Structural steel erection on an office building

05XXX METALS

05100 Structural Framing

05120 Structural Steel

05121 Multistory Type

05122 Warehouse Type

3. Cable pulling on a refinery project

18XX ABOVEGROUND ELECTRICAL

1830 Wire and Cable Installation

1831 Wire and Cable in Conduit

1832 Wire and Cable in Tray

As can be seen, several levels of detail can be used for each activity. The choice is

a matter of selecting the lowest level of detail that is consistent with the needed level

of control over the work. Obviously, not all activities will be monitored at the same

level of detail. Each of the three activities listed above will be used to illustrate

measurement concepts in subsequent discussions.

Page | 28

MEASURING THE AMOUNT OF WORK COMPLETED

How the amount of work completed is determined for a particular activity depends

upon the nature of the work and the particular control needs of the project. The

principal methods available for measuring quantities are

1. Units completed - Quantity surveys or physical measurement of work items are

involved in this method, which is best suited for situations where items can be easily

and quickly measured or counted, like cubic yards of excavation or number of ceiling

tiles in place.

2. Percent complete - A subjective evaluation is made by the foreman or

supervisor.

3. Level of effort - This method relies on predetermined rules to give appropriate

credit for partially completed work that must evolve through several stages. For

example, the stages of formwork are erection, alignment, tightening, stripping, and

cleaning. This method often used for bulk commodity items.

4. Incremental milestones - This variation of the level of effort method is used

where specific milestones can be identified, but quantities of output cannot be easily

measured. An example application is for equipment installation, alignment, and

testing.

5. Start/finish percentages - In this method, another variation of the level of

effort method, the only milestone or phases are starting and finishing.

Each of these methods is described in detail in subsequent paragraphs, and

examples illustrate the type of work for which each method is best suited.

Units Completed (Physical Measurement)

The simplest method of measuring output is to actually measure or count the units

of work completed. For example, one can physically measure how man feet of cable,

cubic yards of excavation, inches of weld, square feet of concrete block wall, or

number of plumbing fixtures which have been completed In a typical commercial or

industrial facility, there are numerous items or activities for which this simple but

effective method can be applied.

Several criteria exist for the proper application of the unit complete method.

These are summarized in Table 3. The scope of the work must be well defined and

relatively straightforward so that the number of output unit and their status can be

quickly ascertained. The units completed method is best applied where the work does

not include a mix of subtasks or where, if i does include a mix, these subtasks are few

in number and can be accomplished in a relatively short time frame.

For example, cable pulling is measured in terms of linear feet of cable pulled. The

scope of work is well defined, and the quantities installed can be quickly determined

from the pull ticket or pulling schedule. Cable pull is straightforward because the work

does not involve subtasks.

The placement of concrete for a slab on grade is a task which involves the subtasks

of placing, vibrating, and finishing- Although three subtasks are involved, all are

measured against cubic yards of concrete in place since the three are executed

simultaneously. The units completed method can be applied to concrete placement

because the quantity is readily measurable.

Page | 29

Table 3. Comparison of Various Methods of Quantity Measurement

Method Criteria Advantages Disadvantages

Units completed

Well-defined scope

Output determined quickly by counting or elementary math

Relatively few subtasks- Short duration for completing each unit of output Single craft or trade

Most detailed and accurate Does not rely on subjective opinions or evaluations Claimed output can be readily verified

Cost and accuracy of data

collection if misapplied

Percent complete

(Supervisor opinion)

Relatively minor tasks where reasonably accurate estimates can be made

Simple

Inexpensive

Quick

Can be very inaccurate and misleading

Level of Effort

Activities involving overlapping subtasks. Subtasks must be measurable or their status easily defined. Best suited where there is a large number of similar items, and the work will be ongoing for an extended period of time.

Greater detail and objectivity than simply estimating how work was done and less expensive than counting or measuring the units completed

More involved than simply estimating the percent complete

Incremental Milestone

Best suited where there are only a few item each subtask is difficult to measure, and the work may lost for an extended period of time

Easy to use

Simple to understand

Long periods may elapse before an intermediate milestone is reached

Start/ Finish

Percentages

Activity lacks intermediate milestone Activity of item of work should be of short duration

Work best for a large number of item

Simple

May be inaccurate, especially if there are few item of if the activity duration is length.

Page | 30

Another criterion for using the units completed method is that the time needed to

perform the completed installation of an individual unit of output should be relatively

short, say a day or less. Trench excavation and the hanging of doors would qualify,

whereas the testing of a piping system or the installation and alignment of equipment

probably would not. Also, work involving multiple crafts is often not well suited to the

units completed method because it can seldom be completed in a day.

The primary advantage of the units completed method is that, when properly

applied, it is the most accurate and therefore reliable method available. It is a

relatively objective method because it does not require a subjective opinion to

determine what has been completed. A third advantage of this method is that an audit

of the reported production is easily accommodated. The main problem with the units

completed method is the cost of data collection when the method is improperly

applied.

It is worth noting that pipe fabrication shops can use this method of measuring

output because there is commonality among many items. Since the fabrication shop is

responsible for a relatively narrow scope of work (bulk quantity items), the breadth of

the reporting system could be reduced without significant increases in manpower or

cost requirements.

Percent Complete (Supervisor Opinion) Method

A simple subjective approach is to ask the supervisor's opinion of the percentage

of the task which is completed. It is useful for relatively minor tasks, usually of short

duration, where development of a more complicated intermediate milestone or level of

effort formula is not justified. Painting, dewatering, architectural trimming, and

landscaping are candidates for this approach.

Level of Effort

A control system requiring the physical measurement of numerous items of work

would too burdensome and costly. One way to simplify the measurement process is to

assign a predetermined percent complete to a task on the basis of the completion of

various subtasks. The percentage is based upon the relative work-hours required to

complete each subtask.

To illustrate the level of effort method, the following example is considered in

which a contractor must install 1,708 small-bore pipe hangers. The following list of

subtasks involved shows the relative level of effort required for each. The relative

level of effort, or weighted completion status, is defined as rules of credit.

Subtask Unit of measure Rules of Credit

Fabricate each 0.40

Install each 0.50

Pre-service inspection each 0.10

Total task each 1.00

Page | 31

If, at sore point in time, 366 hangers have been fabricated, 185 installed, and 41

inspected, then the cumulative number of hangers completed is calculated as follows:

Cumulative Quantity (each) = 366 (0.40) + 185 (0.50) + 41 (0.10) (1)

= 243.0

The subtasks are selected so that the status can be easily determined by the

foreman, and no credit is given until the subtask is finished. The rules of credit remain

the same for all items of work within a given category or account. In this example,

they would be the same for all small-bore hangers, irrespective of the type or size of

hanger.

In another example, a contractor installs modular formwork for a reinforced

concrete basement wall. First, the outside form is erected, braced, and aligned. The

inside form is erected next. Thereafter, the two forms are braced, shored, and plumbed

as a unit. After the concrete placement, the form are stripped, cleaned, and oiled.

Example rules of credit for this task are given below·

Subtask Unit of Measure Rule of credit

Erect initial wall form ft2 0.90

Erect second wall form ft2 0.70

Final bracing and plumbing ft2 0.10

Strip and clean ft2 0.10

Total tasks ft2

The crew cannot take full credit for the work until after the forms have been

removed and cleaned. Notice that the sum of the rules does not add to l.00. This is

because the first = subtasks are applied to only half the total wall area.

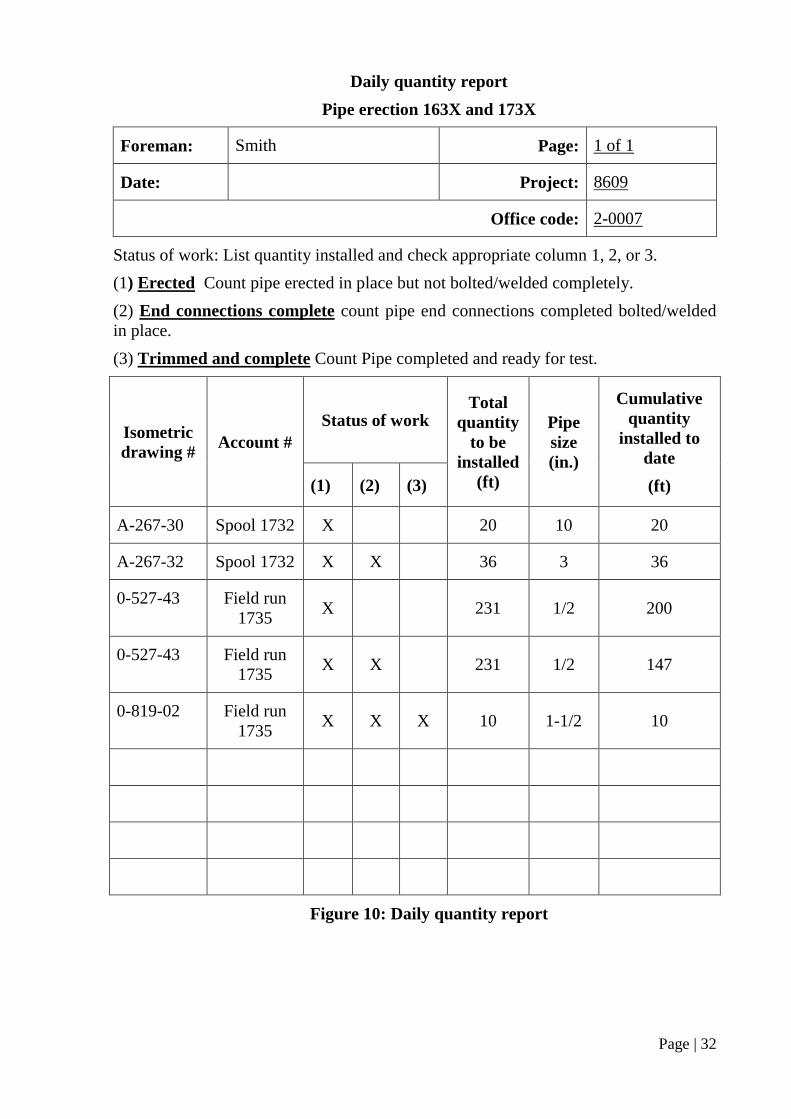

A somewhat more detailed example involves the erection of piping isometrics.

Figure 10 shows the daily quantity report in which the Forman reports the status of

four isometrics. The rules of credit for pipe erection are presented below:

Page | 32

Daily quantity report

Pipe erection 163X and 173X

Foreman: Smith Page: 1 of 1

Date: Project: 8609

Office code: 2-0007

Status of work: List quantity installed and check appropriate column 1, 2, or 3.

(1) Erected Count pipe erected in place but not bolted/welded completely.

(2) End connections complete count pipe end connections completed bolted/welded

in place.

(3) Trimmed and complete Count Pipe completed and ready for test.

Isometric

drawing # Account #

Status of work Total

quantity

to be

installed

(ft)

Pipe

size

(in.)

Cumulative

quantity

installed to

date

(ft) (1) (2) (3)

A-267-30 Spool 1732 X 20 10 20

A-267-32 Spool 1732 X X 36 3 36

0-527-43 Field run

1735 X 231 1/2 200

0-527-43 Field run

1735 X X 231 1/2 147

0-819-02 Field run

1735 X X X 10 1-1/2 10

Figure 10: Daily quantity report

Page | 33

Subtask Unit of measure Rules of credit

Erected ft 0.30

Connections complete ft 0.50

Trimmed ft 0.20

Total task ft 1.00

Figure 10 shows that, for isometric drawing #A-267-30, the entire 20 feet have

been erected. The end connections on isometric #A-267-32 have been completed for

entire 36 feet. The last isometric, #0-819-02, has been entirely finished. However, for

the third isometric (drawing #0-527-43), 200 of 231 feet have been erected, but only

147 feet of the system have the connections completely bolted. The cumulative

footage is calculated as:

Cumulative quantity = 20 (0.30) + 36 (0.30 +0.50) + 200 (0.30) + 147 (0.50) +

10(0.30 + 0.50 + 0.20)

= 178.3 feet (2)

In the above example, the quantities for each of the subtasks are counted the same

way. This will not always be the case, as is illustrated by structural steel building:

Subtask Unit of measure Rules of credit

Erecting Individual pieces 0.50

Bolting (bolt-up) Individual pieces 0.25

Plumbing Pieces grouped by tier 0.15

Tightening (torque bolts) Pieces grouped by tier 0.10

Total task piece 1.00

In this example, output is measured by the number of pieces, i.e. , beams and

columns. Incidental pieces like gusset plates, tie rods, etc., are not counted. Plumbing

is done by tier, and as each tier is completed, the crew is credited for 15 percent of the

pieces associated with that particular tier. Likewise, tightening of high-strength bolts is

tracked according to the pieces per tier.

Importance of rules of credit

Rules of credit are used to specify the installation status of many commodity items

or components. The rules recognize partially completed work and provide an accurate

completion status without the added expense of detailed physical measurements. To

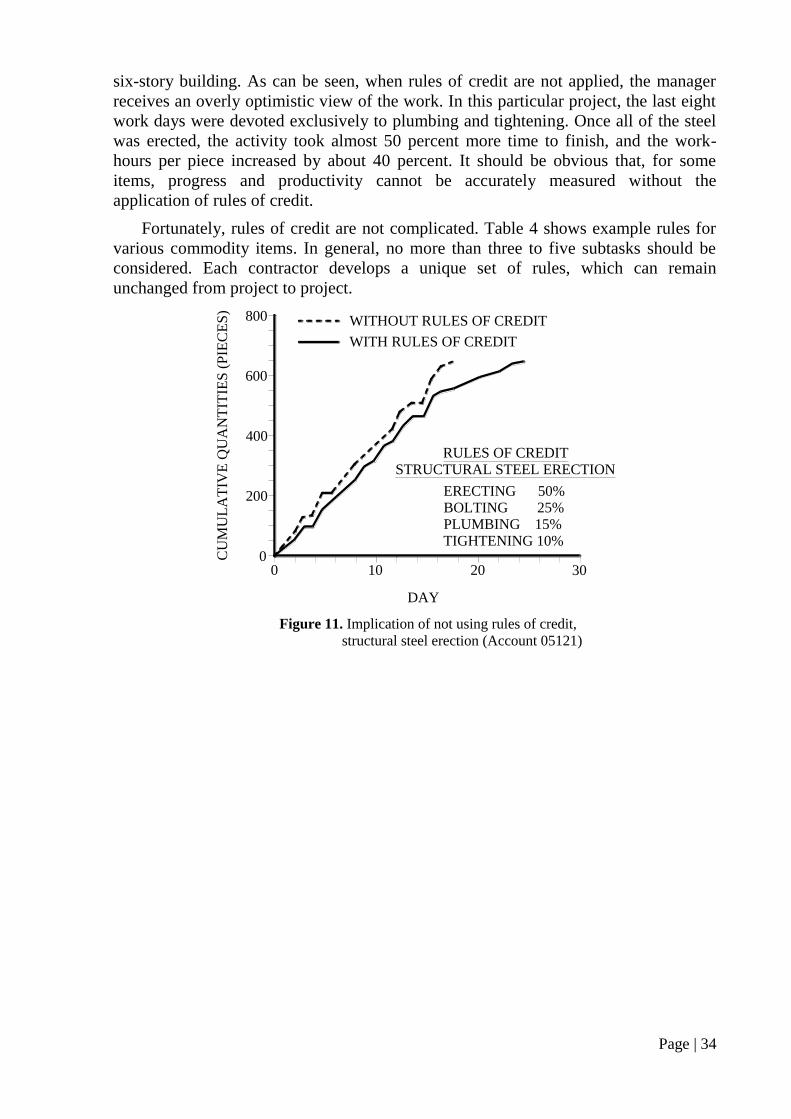

illustrate the influence of rules of credit on the accuracy of output measurements, the

situation represented in Figure 11 shows the cumulative work-hours per piece of

structural steel as a function of time. The task involved the structural steel erection of a

Page | 34

six-story building. As can be seen, when rules of credit are not applied, the manager

receives an overly optimistic view of the work. In this particular project, the last eight

work days were devoted exclusively to plumbing and tightening. Once all of the steel

was erected, the activity took almost 50 percent more time to finish, and the work-

hours per piece increased by about 40 percent. It should be obvious that, for some

items, progress and productivity cannot be accurately measured without the

application of rules of credit.

Fortunately, rules of credit are not complicated. Table 4 shows example rules for

various commodity items. In general, no more than three to five subtasks should be

considered. Each contractor develops a unique set of rules, which can remain

unchanged from project to project.

0

DAY

Figure 11. Implication of not using rules of credit,

structural steel erection (Account 05121)

CU

MU

LA

TIV

E Q

UA

NT

ITIE

S (

PIE

CE

S)

10 20 300

200

400

600

800 WITHOUT RULES OF CREDIT

WITH RULES OF CREDIT

RULES OF CREDITSTRUCTURAL STEEL ERECTION

ERECTING 50%BOLTING 25%PLUMBING 15%TIGHTENING 10%

Page | 35

Criteria

The level of effort method should be used when the manner in which credit is

awarded for partially completed work can lead to misleading interpretation of

progress, productivity, and performance. From the previous examples, it should be

readily apparent that the level of effort method is best suited for those activities that

involve a number of overlapping subtasks. These subtasks may include more than one

craft, but, obviously, each subtask must be measurable. As illustrated by the structural

steel example, measurement concepts can be simplified. To be used effectively, the

status of subtasks must be easy to determine: e.g., a valve has been accepted; a cable,

terminated; or a piece of pipe, aligned. Finally, the level of effort method is well suited

for tasks where there is a large number of similar commodity items and for task that

may be in progress for an extended period of time.

Advantages and Disadvantages

The principle advantage of the level of effort method is that it allows one to obtain

greater objectivity and accuracy than by merely estimating the percent complete, yet it

is not as detailed (and, consequently, time-consuming and costly) as the units

completed method. The main disadvantage is that it can increase the complexity of the

reporting system for some items.

Incremental Milestone

The incremental milestone method of measurement is a variation of the level of

effort method and is characterized by the identification of a series of intermediate

milestones. A predetermined percent complete is associated with each milestone, as is

illustrated in Figure 12, with shows the sequence of installation of a major vessel in a

power plant. This method can be used when only a few items must be considered or

when the subtasks are difficult to measure and the task will take an extended period of

time to complete. In Figure 12, the subtasks are sequential rather than concurrent.

Start/Finish percentages

This method is applicable to task which lack readily definable intermediate

milestones or for which the effort in terms of work-hours required is very difficult to

estimate. It is best suited to short-duration tasks like valve installations. With the

start/finish method, one arbitrarily assigns a percent complete to the start of a task.

Zero is often used, but it can be 20 percent or even 50 percent. When the item is

complete, 100 percent completion is credited. No intermediate percentages are used

because subtasks cannot be identified.

Millwright or mechanical work is sometimes monitored in this way. For example,

alignment of a major fan and motor may take from a few hours to a few weeks,

depending upon the complexity. All one knows for certain is when the work starts and

when it is finished.

Other examples include flushing and cleaning, testing, and major rig operations.

To effectively use this method, the activities or items of work should be of relatively

short duration. Also, a large number of items will tend to reduce the inaccuracies

apparent in the approach.

Page | 36

Task or

commodity

Unit of

measure Rules of credit Description

Mechanical

equipment each

15% set

45% installed

40% accepted

On or near location in building

Bolted, welded, or released for grout

QC accepted after final alignment

and complete hookup

Pipe spool

or field run

pipe

spool or

feet

60% erected

30% welded/bolted

10% accepted

in place to rough line and grade with

fit-up lugs at all welds

all field welds/bolted completed and

accepted

tested and accepted by QC

Electrical

termination each

70% terminated

30% accepted

Terminations completed cable on

both ends and accepted by QC

Tested and accepted by QC

HVAC feet

40% erected

40% connected

20% accepted

In place on permanent hangers

All flanges connected and sealed

Testing and balancing completed;

installation accepted by QC

Pipe hanger

(small-bore) each

40% fabricated

50% installed

10% accepted

Shakeout; shop or field assembly

Attached to support and completely

secured to pipe

Accepted by QC

Masonry

(foundation

wall,

reinforced,

grouted)

square

feet of

wall

70% block

placement

20%grouting

10% paging

Placement of concrete masonry units

Placement of reinforcement and

grouting

Paging of the outside wall

Structural

steel (bolted

connections)

pieces

50% erection

25% bolting

15% plumbing

10% tightening of

bolts

Beam and columns in place

All bolts installed in joints and

connections

Each floor or tier plumbed and

aligned

Final tightening of bolts with impact

wrench

Page | 37

Figure 12. Large equipment installation – incremental milestone

Selection of an appropriate method

The selection of an appropriate method of measurement is relatively simple. For

instance, the incremental milestone and the start/finish percentages methods are

applied in situations where the subtasks are difficult to define or measure. Equipment

installation, alignment, and testing were cited as examples of tasks for which these

methods can be tracked more accurately using other methods. Thus, there are three

primary methods remaining from which to choose: the units completed, level of effort,

and percent completed methods.

In developing a measurement system, the overriding concern is that the system

works for the manager, and not that the manager works for the system. In selecting a

method, four criteria should be considered: Simplicity, degree of control needed,

project complexity, and project scope. The simplest method always be selected. It is

important that quantity measurements and, ultimately, productivity calculations reflect

what actually occurs on the project. The installation and calibration of instruments,

hanging of doors, and electrical terminations can be accomplished with little effort by

simply counting the units completed. On the other hand, it would be foolish to measure

the square footage of painted surface to determine progress. Estimating the percent

complete of painting provides equally useful information with much less effort.

The civil and bulk commodity items are usually labor-intensive and must be

closely monitored. Typically, these items require a significant number of work-hours,

involve the completion of several or more subtasks, utilize multiple crafts, and include

sub commodities of varying complexity. For example, an underground gravity flow

piping system contains pipe, catch basins, manholes, and valve boxes. Also, an

aboveground non racked piping system contains several sizes of pipes, valves, and

hangers. Actual measurement would be impractical and simple estimation of the

RECEIVED AT SITE

0%

50%

100%

SET

ALIGNED

INTERNALS INSTALLED

TESTED

ACCEPTED

Page | 38

percent complete would probably be inaccurate. Therefore, the level of effort method

is appropriate for many of the more important items.

Project complexity and scope are important considerations in selecting a method.

On small projects, or larger ones where the item in question is relatively minor, there

is little justification for establishing control measures based on the level of effort

method. Thus, instrument raceways might be tracked by the percent complete method