Finding Your Partner - InterVISTAS · Finding Your Partner Outlook: Alliances, ... Analysis...

35

Finding Your Partner Outlook: Alliances, JV’s M&A’s Dr. Emre Serpen Executive Vice President InterVISTAS Consulting Group WORLD ROUTES 2012, ABU DHABI, UAE

Transcript of Finding Your Partner - InterVISTAS · Finding Your Partner Outlook: Alliances, ... Analysis...

Finding Your Partner Outlook: Alliances, JV’s M&A’s

Dr. Emre Serpen

Executive Vice President

InterVISTAS Consulting Group

WORLD ROUTES 2012, ABU DHABI, UAE

Air transport growth is greater in emerging

economies in Asia, Latin America, Middle East,

1 Airbus August 2011 Forecast

Partnership and cooperation with

airlines in emerging markets is critical

for future growth

Shifting market growth: The GDP growth of

emerging economies is significantly higher than

mature economies

Small growth in GDP translates to significant market

growth in Asian, Latin American markets

Using geographic advantage Gulf Carriers and TK are growing

connecting emerging markets in particular Asia, Middle East and

Africa

2

The emergence of Gulf/Middle East carriers causing shift in global traffic flows across major connecting hubs

With significant new aircraft orders, growth is set to increase in coming years

3 Source: Diio Mi Sept 27th, 2012. Both directions total.

Emirates supported its network thru code shares

4 Source: Diio Mi Sept 27th, 2012 (For Sept 2012).

Emirates

Profitable year-on-year growth

Second brand worldwide

Significant marketshare in India, many

African states

Changed dynamics of Kangaroo route

Continuing growth

More market penetration in

US Canada

FlyDubai expanding

regional routes

Positioned to take

advantage of markets with

significant potential – Iraq.

Iran etc

Emirates/QANTAS Partnership Signals Change in Traditional

Alliance Relationships - Immediate impact on One world

5

QANTAS Before Emirates Partnership:

• 5 One-Stop Destinations in Europe (via QF

operations or code shares)

• No service to Middle East/North Africa

QANTAS After Emirates Partnership:

• Stop flying from Singapore and BKK to Europe

• Drop Frankfurt Service

• Drop code share plans with MH to 5 European Countries

• Discontinue BA code share (SIN/TPE), CX (HK/Rome)

• 32 One-Stop Destinations in Europe & 31 One-Stop Destinations in

Middle East/North Africa via DXB

• Revised service to SIN/HKG/KUL for better connectivity to Asia

Source: Sample Summer 2012 schedule

Did BA had to use

its aircraft in flights

beyond Singapore

?

Reduction in feeder

traffic with CX code

shares ?

:JAL – BA Start 1st

October •Include Paris /FR

•19 Flights

LHR/NRT

•March 2013

? Deal with CX, MH

Etihad using code shares supporting its growth

6 Source: Diio Mi Sept 27th, 2012

Etihad adding partnerships to support its growth

strategy

7 Source: Diio Mi Sept 27th, 2012 (For Sept 2012).

2011 profitable

Interim 2012 revenues 30% increase

800,000 passengers from passenger airlines

$ 281 Million from partner airlines

Since 2008 growth fro 2 to 35 code share partners

Mergers and Acquisitions key to 20 year plan

10 year strategic partnership with Virgin Australia

40 %Stake in Air Seychelles

29% Air Berlin Stake, access

to high yield European Markets

? Partnership with Air France &

KLM – one world indicated no

issues with Air Berlin

Economies of Scale in 787 fleet

, 56 aircraft common activities

Strategic Partnerships Cross Alliance Boundaries and

are Becoming More Complex

8

Codeshare/

FFP benefits

under

Discussion

Sample of

selected

strategic

partnerships of

Etihad and

Emirates

Cooperation

under

discussion

The three Global Airline Alliances continues see strong coverage in the Americas, Europe and Asia. Nevertheless, there is notable absence of

membership in the Middle East and India.

Alliance focus on emerging markets, Asia, Middle

East, Latin America

9

Passengers carried by Middle Eastern

airlines that belong to a global alliance

account for only 2.4% of total alliance

passengers and 1.8% of daily departures.

There may be further impacts on Alliances due to JV

and Merger activity

10

joins Star

join SkyTeam

exits SkyTeam

& joins Star

join oneworld

join SkyTeam

Source: OAG Max

join SkyTeam

Membership in Global Alliances is very fluid.

LATAM, Emirates-Qatar Deal

Malaysian

Sri Lankan

Ownership laws, national interests typically

restricts industry consolidation

Perceived national Interest

• Ownership rules

• Singapore/China Eastern

• Public opinion against foreign multinationals

• Some improvements (Malev, Air India)

Competition Law

• The interpretation of the competition law often

inhibit ed consolidation EU/US

• In 2001 DOJ blocked United/US merger on the

grounds that the fares would increase

Practicalities

• Fleets, cultures, work practices, IT, seniority lists

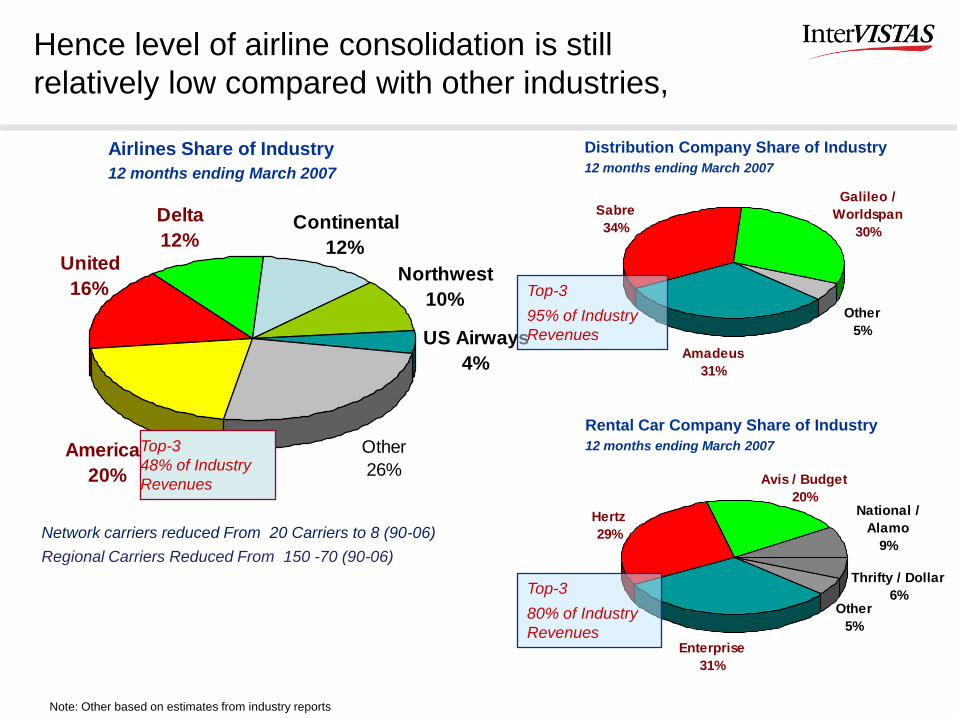

Hence level of airline consolidation is still

relatively low compared with other industries,

Note: Other based on estimates from industry reports

Delta

12%

American

20%

Northwest

10%

US Airways

4%

Other

26%

Continental

12%United

16%

Top-3

48% of Industry

Revenues

Airlines Share of Industry

12 months ending March 2007

Distribution Company Share of Industry

12 months ending March 2007

Sabre

34%

Galileo /

Worldspan

30%

Amadeus

31%

Other

5%

Rental Car Company Share of Industry

12 months ending March 2007

Other

5%

Thrifty / Dollar

6%

Hertz

29%

Avis / Budget

20%

Enterprise

31%

National /

Alamo

9%

Top-3

80% of Industry

Revenues

Top-3

95% of Industry

Revenues

Network carriers reduced From 20 Carriers to 8 (90-06)

Regional Carriers Reduced From 150 -70 (90-06)

Some consolidation has started within EU, also

some flag carriers ceased to exist

The synergies from integration with Swiss, exceeded 200 million Euros

• expanded route network with more destinations and better connections

• interlinked frequent flyer programmes and mutual lounge access

Total synergies from integration of Austrian are estimated at around EUR 80 million Euros (both revenue and cost)

• improved access to international passenger flows and joint international marketing,

• cost advantages and economies of scale

The scope of integration Swiss /Austrian were similar

• Autonomous carrier own business management, own crew and fleet

• Zurich integral part of Lufthansa’s multi hub strategy

The airline related savings of €525 million over three years by combining purchasing, sales and information technology.

Lufthansa

Air France / KLM

Nonstop Total Weekly seats Operated by Lufthansa Group

Aug. 2003–Aug. 2008, Dec. 2008

Depending on further progress of discussions between FAA

– EU in future we could see similar deals between US/EU

Joint ventures increasing in across the board

14

Joint Venture / Anti-trust Immunity relationships allow for better coordination in scheduling and pricing to offer passengers more convenient travel options.

Short haul routes : LCCs have quadrupled their intra-

European market share in the last ten years

RAPID LCC

EXPANSION ACROSS EUROPE LEADING TO

INCREASED MARKET SHARE

2001 2008

FSC

LCC

2001 2004 2008 2012E

Source: OAG, 2011; Lit search;

2012

Similar patterns in Asia, Middle East , also closer business models

may lead to further cooperation between network and LCC

16 Source: Diio Mi Sept 27th, 2012 (For Sept 2012).

Air Arabia

Flydubai

Focus on short haul profitability, reduction in

CASK, Eg Malindo, Air Asia,

Cooperation between Network and LCC carriers

-Eg LH/Jetblue. Etihad/VA et

Network carriers to leverage LCC relationships

much better

Do we have more opportunity for further

partnerships between Network And LCC ??

Increasing Joint Ventures and “Innovative

Partnerships”

Alliances and

Joint Ventures

Mergers

Cross-Border

Innovative

Partnerships

• Central Africa / India / Middle East / CIS carriers likely next to consider Global

alliances membership

• Potential new JVs to form in light of recently announced Emirates / Qantas Joint

Venture and codeshare partnership

• Global Alliances attracting LCCs to join via hybrid partnership platform (SkyTeam)

• Within the EU: Lufthansa with Austrian, Swiss, Brussels Airlines;

• IAG: British Airways and Iberia

• Latin America – AviancaTACA; LATAM Airlines Group

• Potential US-EU airline mergers? (Pending regulatory approvals)

• China Eastern & Qantas (carriers in different competing Global Alliances) to form

Hong Kong based LCC

• Etihad /Australia

• Porter (small, regional Canadian airline) signs interline partnership with South

African Airways via Washington IAD

Finding Partner: Analysis, Strategy, Execution

Analysis Overview Identify changes in region and market

level in both demand, supply, considering circuitry and yield

1. Relative growth of region to region flows considering yield and circuitry

2. Benchmark connectivity with key competitors considering yield

3. Historical growth O/D growth

4. Relative growth of airline market share share compared to O/D market flow considering yield and circuitry

Region A1 A2 A3 Yield

EU-EU 6.2 6.6 8.5 9.6

LA-EU 9.4 9.2 11.0 9.1

EU-NO 9.1 9.1 10.6 9.0

AP-EU 9.5 9.1 8.8 9.3

Connect

Markets 2005 2006 2007 2008 2009 2010

CDG-MED 87 391 853 793 1,717 2,566 DAM-MXP 35 29 56 2,347 2,561 PEK-ODS 1,452 2,050 1,195 1,539 2,539 2,528 BKK-TLV 847 1,294 2,308 3,745 3,679 2,499

Connect

Markets

Service Share O&D Share % Change CCt

Jan-09 Jan-10 2009 2010 Service O&D O&D Yield

BKK-ARN 0.8% 0.9% 2.0% 3.3% 8% 61% 101% 6,786 3.0

PEK-TIP 0.6% 0.7% 1.6% 2.9% 4% 79% 101% 5,968 3.0

IKA-YYZ 1.4% 1.3% 7.3% 8.9% -9% 23% 110% 5,674 2.8

ALG-MED 50.2% 100.0% 86.0% 86.3% 99% 0% 117% 5,196 7.7

Region-Region

Circuitry Yield Onboard O&D Industry O&D Growth A1 Share

Aug-09 Aug-10 Aug-09 Aug-10 Aug-10 Aug-10 A1 Industry of Industry

EU-NO 108% 8.8 9.0 869,909 1,019,118 8,330,229 8,479,367 17.2% 1.8% 12%

NO-EU 109% 8.7 9.1 835,797 986,496 8,330,229 8,479,367 18.0% 1.8% 12%

AP-AF 107% 9.4 9.3 657,943 703,314 5,776,835 5,630,906 6.9% -2.5% 12%

AF-AP 106% 9.4 9.3 655,028 701,660 5,776,835 5,630,906 7.1% -2.5% 12%

Focus on city pairs we want to develop/improve

19

Strategic Evaluation - is critical to establish competitive

strengths and determine scenarios for growth opportunities

Market analysis -the

demand and supply,

competitor activities

and strategic change

Market Growth

compared with Client

Growth, where client

growth may be

slower than market

growth, also vis-a-vis

fare changes.

Strategic evaluation

is used in the of the

development

scenarios

20

Strategic Evaluation Market Analysis and SWOT

Market share growth compared with total market growth

lose marketshare whilst reducing its average fares.

marketshare growth and fare protection in growing markets 21

22

For example growth of competitor activities at airline’s hub. This analysis

shows though this particular client is growing y-o-y 25% on its hub serving

top 500 markets,

23

Other deeper analysis include analysis of an airline’s hub which may be poorly designed

with the lack of a clear arrival/departure bank structure. This for instance equates to lost

opportunities in connecting O/D markets

Market forecasting to determine priorities

24

Top-down elements include GDP-driven passenger growth.

There is an established correlation between year-over-year GDP growth and corresponding growth in passenger volumes.

For increased accuracy, the GDP of respective countries on a route network and point-of-sale data are considered in the analysis

This smoothes temporary fluctuations of bottom up analysis

The bottom-up elements include regression analysis utilizing IATA Paxis and MIDT flown passenger data.

The market forecasting results are then used as an input to network optimisation tools.

Development of Route Strategy

25

Selected scenarios evaluated to establish

route strategy and route structure

Test different scenarios and business models

and evaluate respective differences in

variable contribution towards selection of the

best model

Use of optimisation models.

New destinations with better market growth,

and yield advantages. The route structure

that maximises marketshare, and variable

contribution improving competitiveness is

selected

Identify key changes to Long Haul, Medium

Haul, Regional and Domestic

Identify key changes for better use of alliance and code share partnerships

Deciding on code share, alliance, Joint Venture

Strategies

26

Network Planning

Long & Medium

Term

Shorth Term

Alliances

Pricing

Revenue

Management

Sales

OPerations

Distribution

Other

Finance

Strategic Plan

Market

Forecasting

Capacity

growth (incl

competitors)

Average Fares

Costs

Service

Objectives

Network

Design

Scenario

Development

Hub

Optimisation

Changes to

Fleet Plan

MIDT/BIDT

Network Planning

Long & Medium

Term

Shorth Term

Alliances

Pricing

Revenue

Management

Sales

OPerations

Distribution

Other

Finance

Strategic Plan

Network

Design

Scenario

Development

MIDT/BIDT

Identify value

of current

codeshares

Identify new

codeshare

opportunities to

improve

sustainable

variable

conytribution

Contact

candidate

airlines and

initiate new

codeshare

agreements

Develop code

share

agreement

Monitor

execute

changes to

improve gains

from the

current alliance

Contact

alliances to

initiate

membership

execute

Alliance

Participation

Identify Joint

Venture

Partners to

improve

sustainable

variable

contribution

Contact JV

Partners

towards

agreement

Execute Joint

Venture

AgreementExecute

codeshare

agreements

Identify alliance

to opportunitie

improve

sustainable

variable

contribution

Monitor

Performance of

current

codeshare

agreements

Monitor

Benefits from

JV partnership

27

Following the network optimisation analysis,

bilateral and codeshare development

opportunities can be identified and examined

or long-haul flights with codeshares to other

alliance hubs including beyond points,

medium/short-haul flights in a feeder role.

As some alliances selectively restrict code

shares with rival alliances, the value of current

code shares must be evaluated. beneficial for

the airline.

Example: Value of Current Codeshares

Determination of code share benefits

Evaluation of Alliance Benefits

28

Network Benefits

Additional pax due to

meaningful and advantageous

connections.

Develop the best strategic fit

with the alliance for own

strategy

Different Objectives

feeder to alliance hubs

protect stratetic interests

Bilateral agreements

excluding other airlines

.

Evaluation of ATI Benefits

29

Category Low High Revenue Comes From…

CRM 1.5 1.5 CRM improvements

FFP 5 15Increase costs per KM to

suppliers using Alliance FFP.

Opportunity cost of not having ATI/Open Skies 0 0Could lose many benefits

currently offered from Alliance

Low er COUNTRY distribution costs 6 9 Reduce commissions/overrides

Net Fares in COUNTRY mkts 0 0 Better coordination of net fares

Target corporate accounts 0 0Offer corporations deals for their

entire travel needs

Internet sales increase 0 0Joint coordination of sales

campaigns & promotions

Increase in COUNTRY sales 30 30Combination of pricing, RM, sales

& marketing

Competitive effect in COUNTRY marketplace 0 0Competitive response (pricing,

RM, sales & marketing)

Low er Country distribution costs 39 39 Reduce distribution costs

Negative competitive effect in domestic

marketplace0 0

Competitors erode Client market

share

Franchise Country CTO's 0 0Spin-off Country CTO's through

franchise concept

ATI Benefits:

Commercial and operational

alliance-wide cooperation,

reciprocal participation in each

other’s FFP,

proration of passenger fares,

co-operation on facilities and

passenger handling,

lounge exchange program,

common promotion and

advertising

common procurement

Joint venture success requires careful planning,

stakeholder engagement and change management

30

Realistic assumptions, especially on yield

increases

Governance of network, pricing, revenue

management, distribution

Cultural fit

Tone of the Joint Venture Discussions

Clear execution and communication plan

towards JV, M&A activities

Focus on revenue growth not just cost

reduction

Equity, ownership issues/value part of the

business plan, as well as network and other

benefits

Emphasis of the alternative scenario during

discussions

Critical success factors for successful JV’s and MA’s

Pre-merger Agreements

Delta/Northwest

Sufficient time Both Planning and Execution

AF/KLM

Business Case + Communications Plan + Funds

US Airways / United was blocked.

Realistic expectations + Benefits

Cultural fit + Change management

IT

Don’t Touch Brands

Governance and organisation for JV M&A management

Source: Dr Iatrou, Global symposium on Air Transport Liberalisation ICAO Dubai,

results of global survey of 32 airlines

0% 20% 40% 60% 80% 100%

Hubbing

Economies of Destiny

New Market Growth

Network Optimization

Economies of Scope

Financial Synergies

Marketing Synergies

Corp. Planning Synergies

Maint. Synergies

IT Synergies

Purchasing Synergies

Economies of Scale

Alliances & Mergers

Mergers

Alliances

Benefits

32

InterVISTAS’ Client Experiences

Team Members’ Client Experiences: 60+ Airlines

Sectors Selected Current

Clients

• Qantas

• Malaysian Airlines

• Garuda

• Turkish Airlines,

• MAZ Holding,

• DAS Holding,

• Oman Airways,

• Sri Lanka Airlines,

• RAK airlines,

• Royal Jordanian

• Porter Airlines

• Etihad

• British Airways

• Amadeus

• Belleair

Regions

• Europe,

• Middle East,

• South Asia,

• Eastern Europe

32

Our Airline Practice Service Lines are Focused on Airline

Strategy and Airline Performance Improvement

Strategy – Develop strategy, feasibility studies and

business planning

– Market Forecasting (Airline, Airport, MRO, Cargo)

– Start up Airline and MRO feasibility and business plan

– Mergers and acquistions planning

Network and Fleet Planning – Develop and

optimise network and route plans for airlines

– Route Planning and Schedule Development, Alliances

– Hub design and optimisation, slot remarketing

– Fleet planning , Aircraft leasing and remarketing

Financial Services – Evaluate airline investment

opportunities

– Due diligence (Airline, Airport, MRO, Cargo, GH)

– Privatization and spin-off and financing of Airline, MRO, Pilot

School, GH, Cargo

IT Strategy

Strategy and Finance Performance Improvement

Commercial Improvement – Airline Revenue

Improvement

– Pricing and Revenue Management

– Marketing, Sales and Distribution

– Technology solutions supporting revenue growth

Operations Improvement – Airline

Productivity Improvement and Cost Reduction

– Diagnostic and Cost reduction

– MRO

– Crew Resource Management

– Integrated Operations Control

Restructuring & Change Management –

Airline Transformation and Turnaround

– Restructuring (Airline, MRO, Cargo, Aerospace)

– Start up Implementation

– Performance management

– Organisation improvement and change management.

IT Implementation

33