Promotional Items and Promotional Products to Promote You Rigorously

98

CHAPTER V

FINANCING SCHEMES, PROMOTIONAL AND

DEVELOPMENTAL ACTIVITIES OF SIDBI

The micro, small and medium enterprises (MSMEs) play a key role in the

economic development of our country. The MSME sector has been passing through a

phase of transformation due to globalisation. Globalisation has compelled the MSME

sector to widen its institutional network and to pursue strategies compatible with

global trends. This sector is an important tool for enhancing industrial production,

employment generation, income generation, resource utilisation and export

promotion. Realising the importance of the sector, the Government of India

introduced Micro, Small and Medium Enterprises Development (MSMED) Act in

2006 to promote and foster the growth of this sector. This Act thus provides for

progressive growth and development of MSMEs. In this context, it is desirable to

mention that Small Industries Development Bank of India (SIDBI) has been

consistently involved in meeting the diverse credit requirements of the MSME sector

through its varied innovative schemes. Being an apex financial institution, SIDBI

provides support to the MSME sector through its various schemes. SIDBI provides

financial assistance to MSMEs through its direct credit and indirect credit schemes.

The direct assistance is provided by the bank through term loans, working capital

loan, MSME receivable finance and non-fund based facility. The indirect assistance is

provided by way of refinance, equity assistance, resource support to Primary Lending

Institutions (PLIs) or Non-Banking Finance Companies (NBFCs) and Micro Finance

Institutions (MFIs). The schemes covered under direct and indirect assistance are

further bifurcated into various categories.

DIRECT CREDIT

The bank provides direct credit in the form of term loan, working capital,

MSME Receivable Finance and non-fund based facility. The term loan assistance is

provided by SIDBI to MSMEs engaged in providing services, through its foreign lines

of credit, Growth Capital and Equity assistance (GEMs), Flexible Assistance for

Capital Expenditure (FACE) and Technology Information, Forecasting and

Assessment Council (TIFAC) for project financing and for technology upgradation,

modernisation, diversification, etc. These schemes are discussed below:

99

TERM LOAN

Eligibility

SIDBI provides direct credit for setting up of new projects as well as for

growth, modernisation, diversification and marketing of existing viable MSME units.

In addition, the bank provides loan for acquiring land and construction of factory with

or without additional plant and machinery, for MSME units relocating to industrial

areas.

General Terms and Conditions

The bank provides need based assistance.

The interest rate is based on risk rating and linked to SIDBI PLR, i.e. at 12.75 per

cent (current PLR).

The security for loan is flexible.

The period for loan should not be more than 7 years.

Service Sector Assistance

Eligibility

The bank grants assistance by way of loan or capital to existing small and

medium service sector enterprises and to promoters having experience in identical

activity for setting up of new projects. The service sector assistance of SIDBI includes

business like hospitality and tourism related activities, health care like setting up of

clinics, hospitals etc., IT enabled services, advertisement, transport services,

restaurants, auto dealers etc.

General Terms and Conditions

Assistance should be provided to service sector unit as per the Section 2(h) of the

SIDBI Act.

100

The project cost limit for service sector projects would be considered upto Rs 75

crore, with bank‟s assistance to individual projects being restricted to Rs 50 crore.

However, in respect of all service sector projects/units like hotels, etc. where the

investment in core equipment is within the limit specified for medium scale

service sector enterprises under MSMED Act viz., Rs 5 crore, it could continue to

remain up to Rs 250 crore.

Both capital expenditure and working capital requirements of the concerns in

these sectors may be considered for financing. In the infrastructure area,

financing of sound social/urban infrastructure projects like inter-state bus

terminus, warehousing complexes, floriculture/horticulture/vegetable auction houses,

etc. may be considered.

Direct Assistance under International Line of Credits

With a view to enhance the quantity and quality of finance to MSMEs, SIDBI

entered into agreement with the Japan International Cooperation Agency (JICA),

Japan, Kreditanstalt fur Wiederaufbau (KfW), Germany, Agence Francaise de

Development (AFD), France, for acquiring lines of credit from these institutions. A

brief detail about the schemes is mentioned below:

Japan International Cooperation Agency (JICA): SIDBI provides direct

assistance as well as refinance to other banks, SFCs and NBFCs for providing

credit at concessional rates to MSMEs for enhancing energy efficiency and

profitability of the units.

Eligibility

For Direct Assistance

Assistance should be provided to new or existing MSME unit according to

MSMED Act, 2006. The existing units must have good performance record and

satisfactory financial position. The rating score of unit should be above the minimum

investment grade rating of SIDBI. Energy saving projects must comply with the

Energy Saving Equipment list displayed on SIDBI website. Any unit that is engaged

in unlawful business is not eligible under the scheme. All those projects having less

than 10 per cent potential for energy saving are also not eligible.

101

The entrepreneur is required to submit complete application form as per the

prescribed format along with a copy of documents to the SIDBI branch office. In

addition, the borrower must also furnish information about the energy saving capacity

of the project for availing assistance under the scheme. Disbursements are made after

complying with the eligibility criteria and the terms and conditions of the sanction.

General Terms and Conditions

The minimum promoter‟s contribution is 25 per cent for existing units and 33 per

cent for new units.

The maximum debt-equity ratio is 2.5:1.

The asset coverage should be at least 1.4:1 for new units and 1.3:1 for existing

units.

The minimum amount of loan is Rs 10 lac.

The rate of interest is 0.75 per cent below the normal lending rate and should be

based upon the credit rating.

A non-refundable upfront fee of 1 per cent of sanctioned loan and service tax as

applicable should be charged.

The maximum time limit for repayment should not be more than 7 years.

The security for loan is first charge over assets acquired under the scheme or

first/second charge over existing assets financed by SIDBI and collateral security,

if necessary.

KfW-SIDBI Financing Scheme

With a view to promote energy efficiency, SIDBI provides credit to MSME‟s

through KfW- Energy Efficiency Scheme, KfW- Cleaner Production Scheme,

KfW- Innovation Finance Programme. These schemes are mentioned below:

KfW- Energy Efficiency Scheme: The bank grants credit to eligible MSMEs

making investment in equipments that leads to energy efficiency projects under a

line of credit from KfW Development Bank in Germany. The energy efficiency

investment includes upgrading or modernising of industrial boilers, optimisation

of air pressure systems, energy efficient lighting etc.

102

Eligibility

Assistance should be provided to new or existing MSME unit defined under

MSMED Act, 2006. The unit must have satisfactory past performance record and

good financial position. The rating score of unit should be above the minimum

investment grade rating of SIDBI. The amount of taxes, import duties, etc. will be

paid by the entrepreneur.

For availing assistance under the scheme, the eligible MSMEs may apply

through filling up a prescribed application form along with necessary documents by

submitting in local SIDBI branch. The entrepreneur can also obtain information about

reducing the energy consumption mechanism from SIDBI.

General Terms and Conditions

The minimum amount of loan is Rs 10 lac.

The minimum promoter‟s contribution is 25 per cent of project cost.

The debt-equity ratio is 2:1

The rate of interest is 0.75 per cent below the normal lending rate and should be

based upon the credit rating.

The Asset Coverage should be 1.75 for service sector units and 1.3 for

manufacturing units.

The loan should be returned in a period of 7 years.

KfW- Cleaner Production Scheme: Under this initiative, SIDBI provides credit

to those MSMEs making investments in cleaner production, reduction of

emissions and pollution through Common Effluent Treatment Plant (CETP)

facilities. The scheme which comprises investments in waste management, waste

reduction, waste recycling, storage and disposal facilities, etc. are considered

eligible for getting assistance. The bank has utilised the entire funds available

under KfW-Cleaner Production Scheme.

103

Eligibility

Assistance should be provided to new or existing MSME unit defined under

MSMED Act, 2006. The unit must have satisfactory past performance record and

good financial position. The rating score of unit should be above the minimum

investment grade rating of SIDBI. The investments will result in reducing air

pollution, water and soil pollution, wastage of raw material etc. The amount of taxes,

import duty etc. will be paid by the entrepreneur.

For getting credit under the scheme, the eligible MSMEs can apply for loan

through duly filled application form along with other necessary documents as

required, to the nearest SIDBI branch office.

General Terms and Conditions

The minimum amount of loan is Rs 10 lac.

The minimum promoter‟s contribution is 25 per cent of project cost.

The debt-equity ratio is 2:1

The rate of interest is based upon the credit rating and is 0.75 per cent below the

normal lending rate.

The asset coverage should be 1.75 for service sector units and 1.3 for

manufacturing units.

The loan should be returned in a period of 7 years.

KfW- Innovation Finance Programme: This scheme focuses on the supply

aspect of clean technologies. Further, a technology can be characterised as

„Innovative‟ if it results in environment protection and is not available in that

particular region.

Eligibility

As per this scheme, assistance will be provided to new as well as existing

MSME units having good performance record. The loan is extended to those units that

are engaged in demonstration, development and commercialisation of innovative

clean technologies in products and services. All projects that are related to waste

water treatment, industrial pollution control activities, units engaged in development

of energy efficient equipments are eligible to avail assistance under this scheme.

104

General Terms and Conditions

The minimum amount of loan is Rs 10 lac.

The minimum promoter‟s contribution, debt-equity ratio, rate of interest,

conditions related to asset coverage and period of repayment should be based

upon direct credit scheme norms issued.

Sustainable Finance Scheme (SFS): SIDBI introduced a new scheme called

sustainable finance scheme during 2012-13 for those sustainable development

projects which contribute in energy efficiency and cleaner production but are not

covered under international or bilateral lines of credit given through international

or bilateral agencies. Thus, all sustainable development projects like renewable

energy projects, green buildings, green micro finance, Bureau of Energy

Efficiency (BEE) star rating and eco-friendly labelling, etc. are covered within the

scope of this scheme. In addition, the financial assistance has also been rendered

to Energy Service Companies (ESCOs) and Original Equipment Manufacturers

(OEMs) engaged in manufacturing energy efficient and cleaner production

equipments (SIDBI Annual Report 2012-13, p. 7).

Growth Capital and Equity Assistance Scheme (GEMs)

During 2011-12, Direct Risk Capital Scheme (DRCS) has been renamed as

Growth Capital and Equity Assistance Scheme (GEMs) for meeting the need of

capital for growth of MSMEs. A separate fund of Rs 2000 crore has been allocated to

SIDBI risk capital in the Union Budget 2008-09. The main objectives of the scheme

are to reduce the gap in methods of finance for expansion, modernisation and

diversification for entrepreneurs keen to make intangible investments like product

development, research and development, brand building, technical know-how etc.

without collateral security. The bank provides risk capital assistance under the MSME

Risk Capital Fund and Venture Capital Fund by way of equity, preference capital,

optionally convertible debentures (OCDs), optionally convertible cumulative

preference shares (OCCPs), etc. Further, to enhance the equity support to MSME

sector, „India Opportunities Venture Fund‟ of Rs 5000 crore with SIDBI has also been

set up as per the Union Budget 2012-13. Since assistance under this scheme is without

asset cover or collateral security, hence a high level of risk is involved. So, new or

existing entrepreneurs having 2 years of satisfactory banking performance record and

3 years of profitability are considered for assistance under the scheme.

105

Flexible Assistance for Capital Expenditure (Face)

The bank has taken a new initiative in 2011-12 to meet the flexible and long

term repayment schedule requirement of the new as well as existing MSME units

making investments in fixed assets. The units which have satisfactory performance

record are eligible for assistance under the scheme. As per this scheme, separate

repayment criteria on the basis of nature of investment, economic life of project, etc.

will be prepared for each component. The interest rate is based upon the tenure of

each component of loan.

The repayment period is need based. For immovable assets the maximum time

period is 10 years including moratorium period. For other fixed assets the maximum

time period is 7 years including moratorium period.

Technology Information, Forecasting and Assessment Council (TIFAC)

SIDBI along with TIFAC entered into an agreement and introduced a scheme

named SRIJAN for development, demonstration and commercialisation of technology

innovation in projects of new as well as existing MSMEs. A revolving fund of Rs 30

crore has been created by TIFAC and managed by SIDBI.

Eligibility

The new and existing MSMEs engaged in the development, demonstration and

up-scaling of technology based product and processes are eligible under the scheme.

The MSME units may send their project proposal to either SIDBI or TIFAC. The

financial performance shall be done by SIDBI and technical evaluation of project

shall be made by TIFAC. On the basis of sound appraisal results the Project Approval

Committee (PAC) (comprising of both SIDBI and TIFAC officials) will recommend

MSME unit eligible for sanction of loan.

General Terms and Conditions

The minimum promoter‟s contribution should be 20 per cent of the project cost.

The scheme will provide assistance in the form of term loan upto Rs 1 crore at the

interest rate upto 5 per cent.

106

The maximum repayment period is 6 years including moratorium period.

The security is first charge on assets for both movable/immovable assets created or to be

created under the project. A personal guarantee of promoters is also stipulated.

WORKING CAPITAL LOAN

Eligibility

The bank is meeting working capital requirements of new as well as existing

MSME and service sector units under MoU with IDBI bank. The bank started

working capital facility during the year 2007-08. The facility was introduced in 26

branches of the bank. In addition, the bank also provides loan to Government

recognised export or trading houses. However, the facility cannot be offered on

standalone basis (i.e. without term loan assistance).

General Terms and Conditions

A processing fee of 0.50 per cent of the limit sanctioned and 0.25 per cent of the

limit at the time of each renewal should be charged.

The rate of interest is based upon credit rating or charged as per floating rate

linked to PLR.

The tenure of loan is one year and renewable after one year @ 0.25 per cent of

renewal fee.

Asset coverage ratio is 1.4 for new units and 1.3 for existing units.

Fixed assets coverage ratio is 0.75 per cent for manufacturing units.

TOL/TNW not more than 4:1.

Current ratio required being 1.33:1.

Interest coverage of 1.5 times.

Margin on stock, receivables should be 30 per cent.

Maximum 90 debtor‟s days.

107

The total amount of sanctions and disbursements by way of term loan and

working capital loan by SIDBI are shown in Table 5.1.

Table 5.1

Sanctions and Disbursements under Term Loan and Working Capital Assistance

(Rs. in crore)

Year Sanctions Disbursements Disbursements as

per cent to Sanctions

1990-91 8.4 0.7 8.33

1991-92 39.3 10.3 26.21

1992-93 68 36 52.94

1993-94 330.4 240.6 72.82

1994-95 1011.5 540.2 53.41

1995-96 267.85 127.81 47.72

1996-97 583.11 187.45 32.15

1997-98 1192.63 430.44 36.09

1998-99 943.64 562.83 59.64

1999-00 1021.72 768.65 75.23

2000-01 995.64 771.01 77.44

2001-02 1276.18 550.74 43.16

2002-03 964.83 474.87 49.22

2003-04 1619.41 666.96 41.19

2004-05 1521.44 994.17 65.34

2005-06 2944.88 1461.81 49.64

2006-07 2263.85 1717.13 75.85

2007-08 1472.33 1646.38 111.82

2008-09 2595.27 2760.94 106.38

2009-10 4286.77 3005.7 70.12

2010-11 7300.75 4126.37 56.52

2011-12 9520.52 4234.2 44.47

2012-13 12269.76 1556.39 12.68

EGR 39.27 41.95 1.93

Mean 2369.48 1168.33 55.15

CV 133.41 107.17 45.96

Source: Compiled from Annual Reports of SIDBI.

108

Table 5.1 highlights that the total amount of sanctions under term loan and

working capital assistance increased from Rs 8.4 crore in 1990-91 to Rs 12269.76

crore in 2012-13 and recorded growth rate of 39.27 per cent during the period. The

amount of disbursements increased from Rs 0.7 crore in 1990-91 to Rs 1556.39 crore

in 2012-13 and registered growth of 41.95 per cent over the period. The average

amount of sanctions and disbursements by way of term loan and working capital loan

were Rs 2369.48 crore and Rs 1168.33 crore during the reference period. The growth

of sanctions showed a high degree of variation (CV=133.41) as compared to the total

disbursements (CV=107.17) over the period. The loan disbursements as percentage to

total sanctions were highest (111.82 per cent) in the year 2007-08 and lowest (8.33

per cent) in the year 1990-91.

MSME RECEIVABLE FINANCE

The scheme was also known as Bills Financing Scheme till 2006-07. After the

enactment of MSMED Act 2006, the scheme was renamed as MSME Receivable

Finance Scheme. The MSME receivable financing scheme of SIDBI is an important

component of providing direct credit to the MSME sector. The major objective of this

scheme is to reduce the problem of delayed payments to MSMEs so as to ensure

timely payment of their bills. The bank has been operating four schemes since 1992-

93 under bills financing namely, Bills Rediscounting, Direct Discounting of Bills

(Equipments), Receivable Financing Scheme (earlier named as Direct Discounting of

Bills (Components)) scheme and during 2005-06 Seller-wise Receivable Finance

Scheme. The Receivable Finance Scheme helps the manufacturers of MSMEs by

increasing their liquidity and cash flow by offering them financial assistance for the

goods and services rendered by them to the purchasers. Under this scheme, the bank

discounts bills arising out of purchase of component parts or sub-assemblies

manufactured by MSME units and by providing services like packing, transportation

etc. to medium or large scale units. Amongst all the schemes, RFS has gained most

acceptability by MSMEs.

Eligibility

Purchaser wise limit

It is required that purchaser should have been in commercial production for at

least five years, earned net profit in 3 out of last 4 years. The corporate entity must

have a good track record and made no default or no statutory arrears to banks or

financial institutions.

109

General Terms and Conditions

The current ratio required being 1.33:1.

The quick ratio should be 0.50:1.

TOL/TNW ratio should not be more than 4:1.

External rating is compulsory for sanction of new limits.

Seller wise limit

It is necessary that seller should be an MSME service provider for at least five

years and should have made profits in at least two out of the three financial years. The

manufacturer or service provider in the MSME sector must be regular in repayment of

dues and made no default or no statutory arrears to banks or financial institutions.

General Terms and Conditions

The minimum loan amount is Rs 25 lac.

For loans up to Rs 1 crore, the asset coverage ratio of 0.75:1 should be

provided by the bank.

The security depends upon the mutual terms and conditions.

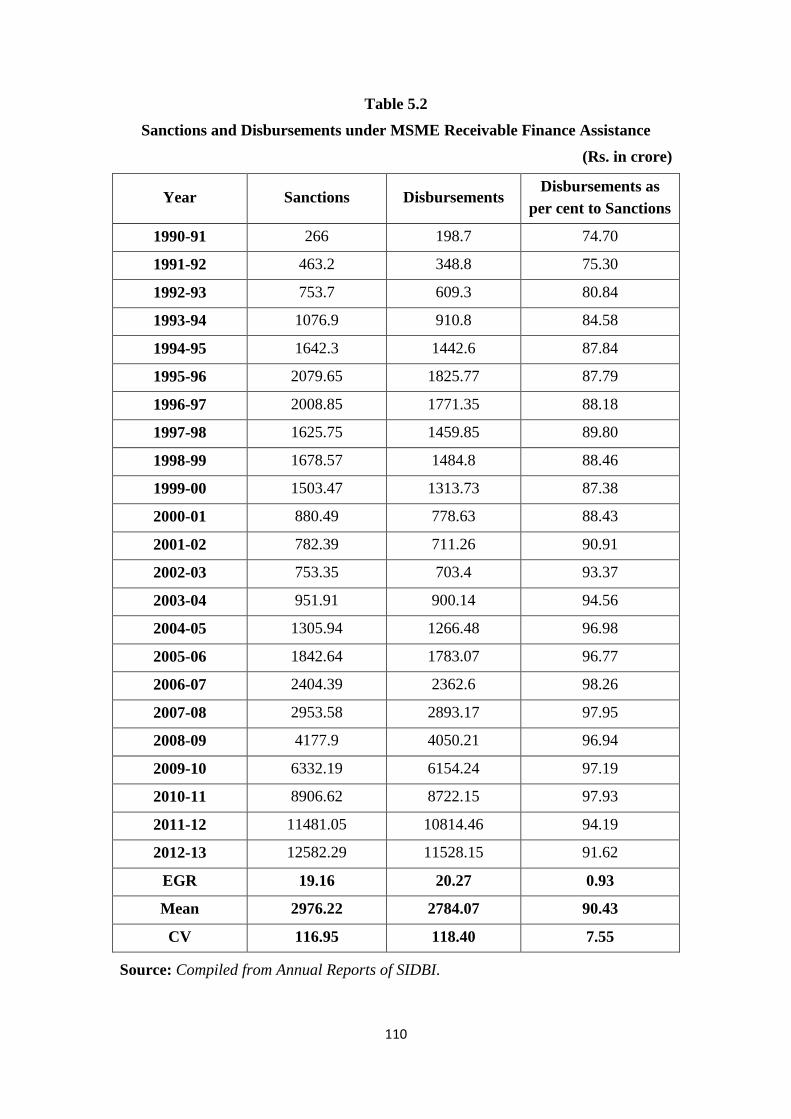

The details about the MSME receivable finance scheme of the SIDBI are

shown in Table 5.2.

Table 5.2 depicts that the total amount of MSME receivable finance sanctions

which increased from Rs 266 crore in 1990-91 to Rs 12582.29 crore in 2012-13 and

registered growth rate of 19.16 per cent over the period. The MSME receivable

finance disbursements increased from Rs 198.7 crore in 1990-91 to Rs 11528.15 crore

in 2012-13 and recorded growth rate of 20.27 per cent during the period. The average

amount of sanctions and disbursements were Rs 2976.22 crore and Rs 2784.07 crore

over the period of study. The growth of disbursements showed lower degree of

consistency (CV=118.40) as compared to the total sanctions (CV=116.95) during the

period. The loan disbursements as percentage of the sanctions were maximum (98.26

per cent) in the year 2006-07 and minimum (74.70 per cent) in the year 1990-91.

110

Table 5.2

Sanctions and Disbursements under MSME Receivable Finance Assistance

(Rs. in crore)

Year Sanctions Disbursements Disbursements as

per cent to Sanctions

1990-91 266 198.7 74.70

1991-92 463.2 348.8 75.30

1992-93 753.7 609.3 80.84

1993-94 1076.9 910.8 84.58

1994-95 1642.3 1442.6 87.84

1995-96 2079.65 1825.77 87.79

1996-97 2008.85 1771.35 88.18

1997-98 1625.75 1459.85 89.80

1998-99 1678.57 1484.8 88.46

1999-00 1503.47 1313.73 87.38

2000-01 880.49 778.63 88.43

2001-02 782.39 711.26 90.91

2002-03 753.35 703.4 93.37

2003-04 951.91 900.14 94.56

2004-05 1305.94 1266.48 96.98

2005-06 1842.64 1783.07 96.77

2006-07 2404.39 2362.6 98.26

2007-08 2953.58 2893.17 97.95

2008-09 4177.9 4050.21 96.94

2009-10 6332.19 6154.24 97.19

2010-11 8906.62 8722.15 97.93

2011-12 11481.05 10814.46 94.19

2012-13 12582.29 11528.15 91.62

EGR 19.16 20.27 0.93

Mean 2976.22 2784.07 90.43

CV 116.95 118.40 7.55

Source: Compiled from Annual Reports of SIDBI.

111

NON-FUND BASED FACILITY

SIDBI also provides non-financial assistance in the form of letters of credit

(both inland and foreign), guarantees, appraisal services etc. as per the requirements

of the MSMEs. The inland letter of credit scheme was introduced in 2005-06 to

provide benefit to SIDBI‟s domestic customers. The guarantee scheme was launched

by SIDBI during the year 2007-08 for providing deferred payment guarantees for its

eligible customers. The bank has disbursed Rs 678.76 crore against 907 letters of

credit (both inland and foreign) from 2007-08 to 2010-11. Further, the bank has given

guarantees with respect to 694 units and cumulatively disbursed Rs 196.15 crore

during the period 2007-08 to 2012-13. Thus, schemes capture favourable response

from MSME clients and is expected that it will become a major source of non-fund

income in the recent years.

Guarantee Scheme

The bank provides Financial Guarantee, Performance Guarantee and Deferred

Payment Guarantee.

Eligibility

The existing customers of SIDBI in MSME sector and service sector units

with satisfactory track record are eligible under the scheme. The new customers of the

bank in need of both fund based and non fund based limits are also eligible under the

scheme. Stand alone facility (i.e. without term loan) is not considered by the bank.

General Terms and Conditions

Processing Charges: 0.25 per cent p.a. to 0.50 per cent p.a. of the guarantee

amount / limit (negotiable) to be charged upfront before issue of the letter of

sanction / renewal of guarantee / guarantee limit + applicable service tax.

Guarantee Commission- Financial Guarantee: 1.50 per cent p.a. to 3 per cent p.a.

+ applicable service tax; performance guarantee: 1 per cent p.a. to 2 per cent p.a. +

applicable service tax.

112

Margin: Minimum margin of 25 per cent of the Guarantee amount shall be

stipulated for all Guarantees with Guarantee period (including the claim period)

less than or equal to three years. For guarantees with guarantee period more than

three years but less than 5 years, minimum margin of 50 per cent of the guarantee

amount shall normally be stipulated.

Margin would be in the form of FDR lien marked to SIDBI. Borrower would be

required to place the FD with SIDBI.

In case of performance guarantee, higher margin would be explored.

Guarantees in favor of court or Government or any other person on behalf of

borrower relating to payment of taxes, excise duty, custom duty or other

Government dues, in dispute, would be issued only against 100 per cent cash

margin.

Loan Facilitation and Syndication Service

Under this scheme, SIDBI develops a mechanism for new and existing units

engaged in manufacturing and service sector in order to avoid any delay in sanction of

loan. This facility is rendered by bank through tie ups by other banks, Rating

Agencies (RAs) and Accredited Consultants (ACs).

Need of Service

This service is necessary to increase the flow of credit to MSME sector by

reducing delay in completing procedural formalities. The ACs will provide

information about the documents required by the bank so as to expedite the process of

sanctioning of loan. In addition, rating by RAs (not compulsory) also enhances the

validity and reliability of the information given by the applicant which in turn results

in quick disposal of loans by banks. Thus, this scheme made the loan process easy and

increases the acceptability of loan proposals by banks.

Guidelines/Procedure of the Loan Facilitation and Syndication Scheme

Firstly, ACs authorised by SIDBI will formulate Basic Information Memorandum

(BIM) on the basis of information given by the MSME entrepreneurs. These

consultants act as an intermediary between entrepreneur and commercial banks

113

and provide necessary information as required by either of them. These

consultants guide entrepreneurs about availability of schemes and clear their

queries, if any, about schemes at the earliest stage.

Secondly, this BIM will be submitted by ACs to SIDBI with prior permission of

MSME entrepreneur.

At the third stage, if required, the bank will forward the proposal to RAs for

rating.

Then, on the basis of information obtained, the bank renders equity/ quasi-

equity support for growth oriented existing units, provides finance for service sector

units and gives credit for energy efficiency and cleaner production processes to

MSMEs.

In other cases, the loan will be provided by Public Sector Banks having

agreement with SIDBI. Thus, in a nutshell, SIDBI supports its entrepreneur

throughout the process of loan processing.

INDIRECT CREDIT

The bank provides indirect credit through refinance assistance, equity

assistance, micro finance assistance and resource support to PLIs or NBFCs and

MFIs. These schemes are discussed below:

REFINANCE ASSISTANCE

SIDBI has been provided with Special Refinance Fund from Reserve Bank of

India and Government of India for enhancing refinance facility to the MSME sector.

In the Union Budget 2013-14, a fund support of Rs 10000 crore was allocated to

SIDBI for enhancing its refinancing capability towards banks, SFCs etc. Since

inception, the bank has been providing some special schemes like assistance under

single window scheme, scheme for tiny projects, women entrepreneurs, composite

loan scheme etc. But in 2005-06, the bank discontinued the process of providing

assistance under some schemes and followed a policy of providing need-based

finance. The refinance assistance has been provided by the bank through Primary

Lending Institutions (PLIs) like State Financial Corporation‟s (SFCs), State Industrial

Development Corporations (SIDCs), Scheduled Commercial Banks (SCBs), State Co-

operative banks etc. for growth, expansion and modernisation of existing units and for

setting up of new industrial projects.

114

Eligibility

All MSME units having investment in Plant and Machinery upto Rs 1 crore

(including ancillaries), small road transport operators in individual firm who owned

maximum 20 vehicles are eligible for assistance. Further, service sector and

infrastructure projects where cost of project does not exceed Rs 20 crore and medium

sector units with investment in plant and machinery upto Rs 10 crore are also eligible

for availing assistance under same.

Further, the MSMEs incorporated as Public or Private Limited Company, Co-

operatives, Partnership, Sole-Proprietorship, Hindu Undivided Family, units owned or

managed by Trusts as defined in Section 2(h) of SIDBI‟s Act 1989 are also eligible

for assistance under SIDBI‟s refinance.

General Terms and Conditions

The promoter‟s contribution lies between 10 per cent and 22.5 per cent.

Debt-equity ratio is 3:1 for loan upto Rs 10 lac and 2:1 for others.

Debt to service coverage ratio of 1.5-2:1 is considered as reasonable.

Maximum amount of term loan is Rs 3 crore.

The rate of interest is fixed by PLIs on case to case basis.

The time limit for availing refinance is 24 months and the time limit is computed

from the date of sanction of refinance by SIDBI.

100 per cent refinance is granted by SIDBI against term loans extended by PLIs to

an individual unit.

As the PLIs assume full credit risk in respect of loans granted by them, the

security to be furnished by the borrowing industrial concern would depend on the

terms and conditions under which the PLIs provide finance.

Procedure for availing refinance

The refinance assistance process has been decentralised and implemented by

ROs/BOs of SIDBI. Refinance assistance to SFCs is centralised and controlled by

DFID (Development Financing Institutions Division), SIDBI, Mumbai.

115

The refinance scheme in banking industry has been in operation for more than

35 years, hence, all the PLIs are well acquainted with the refinance procedure. The

ROs/BOs of SIDBI provides refinance to all eligible PLIs for further assistance in

respect to industrial projects set up in their particular state or union territory.

Refinance procedure is categorised as Automatic Refinance Scheme (ARS) and

Normal Refinance Scheme (NRS).

Under ARS, refinance is provided to the commercial banks through simple

process for loans upto Rs 2 crore per borrower. For loans above Rs 2 crore, refinance

is provided under NRS through filling up of separate application form along with

appraisal memorandum, sanction note of PLIs and the same are verified by SIDBI.

Further, under ARS, a combined application will be submitted by the controlling

office of the individual banks to SIDBI ROs/BOs for sanction and disbursement of

loan. The application is to be submitted within six months from the date of

disbursement of loan by the PLI.

Under NRS, application is submitted for sanction of loan and after getting

approval another application for disbursement of loan is submitted as per the

requirement of the bank. The interest rate is paid quarterly and is applicable as

prevailed on the date of first disbursement of loan by PLIs in individual case.

Payment of principal is made by the PLI as and when they fall due. The bank‟s

sanctions and disbursements under refinance assistance for MSME sector are

presented in Table 5.3.

Table 5.3 reveals that the total amount of sanctions under refinance increased

from Rs 2052.2 crore in 1990-91 to Rs 31781.52 crore in 2012-13 and registered

growth rate of 13.26 per cent during the period. The refinance disbursements

increased from Rs 1561.5 crore in 1990-91 to Rs 22869.78 crore in 2012-13 and

recorded a growth of 12.98 per cent over the period. The average amount of sanctions

and disbursements were Rs 8969.76 crore and Rs 7239.23 crore during the period of

study. The growth of disbursements showed a high degree of variation (CV=111.46)

as compared to the total sanctions (CV=102.38) during the reference period. The loan

disbursements as percentage of the sanctions were highest (99.09 per cent) in the year

2010-11 and lowest (40.44 per cent) in the year 2003-04.

116

Table 5.3

Sanctions and Disbursements under Refinance Assistance

(Rs. in crore)

Year Sanctions Disbursements Disbursements as per

cent to Sanctions

1990-91 2052.2 1561.5 76.09

1991-92 2299 1634.5 71.10

1992-93 2026.8 1449.9 71.54

1993-94 1766.5 1390.9 78.74

1994-95 1672.2 1235.5 73.88

1995-96 2609.12 2123.73 81.40

1996-97 2450.97 1941.74 79.22

1997-98 3171.78 2640.16 83.24

1998-99 4743.77 3247.26 68.45

1999-00 6353.29 4137.85 65.13

2000-01 8087.99 4411.59 54.54

2001-02 6374.97 4144.44 65.01

2002-03 8034.74 4872.1 60.64

2003-04 4250.43 1719 40.44

2004-05 4419.19 2693.6 60.95

2005-06 5897.72 4598.75 77.98

2006-07 5430.14 5189.12 95.56

2007-08 10114.34 9153.57 90.50

2008-09 19260.98 18534.24 96.23

2009-10 19926.09 18584.82 93.27

2010-11 24337.42 24115.94 99.09

2011-12 29243.3 24252.3 82.93

2012-13 31781.52 22869.78 76.31

EGR 13.26 12.98 0.01

Mean 8969.76 7239.23 75.75

CV 102.38 111.46 18.91

Source: Compiled from Annual Reports of SIDBI.

EQUITY ASSISTANCE

The bank also provides equity/seed capital assistance under four schemes

namely National Equity Fund (NEF) Scheme, seed capital, Self- Employment Scheme

for Ex-Servicemen (SEMFEX) and Mahila Udyam Nidhi (MUN) scheme since

117

inception to provide support to those borrowers who have already availed project

assistance from banks and State-level institutions. Bank has discontinued providing

benefit under NEF scheme from May 1, 2007. The benefit under seed capital scheme

has also been withdrawn from 1996-97. The amount of sanctions and disbursements

under equity assistance scheme since inception to 2008-09 are shown in Table 5.4.

Table 5.4

Sanctions and Disbursements under Equity Assistance

(Rs. in crore)

Year Sanctions Disbursements Disbursements as per

cent to Sanctions

1990-91 7.1 5.5 77.46

1991-92 11.7 9.7 82.91

1992-93 9.9 8 80.81

1993-94 6 5.2 86.67

1994-95 11.4 9.3 81.58

1995-96 8.04 5.04 62.69

1996-97 22.72 16.83 74.08

1997-98 31.06 26.36 84.87

1998-99 24.83 22.17 89.29

1999-00 35.63 32.05 89.95

2000-01 20.22 16.85 83.33

2001-02 54.28 35.96 66.25

2002-03 54.76 41.61 75.99

2003-04 42.67 37.7 88.35

2004-05 43.97 39.97 90.90

2005-06 40.56 34.63 85.38

2006-07 34.41 29 84.28

2007-08 25.48 26.21 102.86

2008-09 8.8 9.18 104.32

EGR 1.20 2.89 1.67

Mean 25.98 21.65 83.79

CV 62.39 60.25 12.26

Source: Compiled from Annual Reports of SIDBI.

118

Table 5.4 shows that sanctions under equity assistance increased from Rs 7.1

crore in 1990-91 to Rs 8.8 crore in 2008-09 and recorded growth of 1.20 per cent

during the period. The disbursements under the scheme increased from Rs 5.5 crore in

1990-91 to Rs 9.18 crore in 2008-09 and registered a growth of 2.89 per cent over the

period. The overall average of sanctions and disbursements were Rs 25.98 crore and

Rs 21.65 crore during the reference period. The growth of sanctions showed lower

degree of consistency (CV=62.39) as compared to the total disbursements

(CV=60.25) over the period of study. The equity disbursements as percentage to

sanctions were maximum (104.32 per cent) in the year 2008-09 and minimum (62.69

per cent) in the year 1995-96.

MICRO FINANCE ASSISTANCE

Micro finance scheme has been regarded as an important tool for accelerating

and strengthening the financial capacity of MFIs. SIDBI provides micro credit to the

under privileged sections of the society i.e. women, minorities, backward

communities and poor people in the unorganised sectors of the economy. Thus SIDBI

meets the unmet credit demand of the millions of poor in the country through its

micro finance institutions. Further, keeping in view the importance of micro finance,

the GoI in the Union-Budget 2010-11 announced to create the „India Microfinance

Equity Fund‟ (IMEF) of Rs 100 crore with SIDBI. The objective of creating this fund

was to provide equity and quasi-equity support to small MFIs for enhancing growth

and efficiency in their operations. The fund base has been increased to Rs. 200 crore

by allocating further Rs.100 crore in the budget for Financial Year 2014. As per the

emerging requirements, necessary changes are made in the existing schemes.

General Terms and Conditions

The minimum loan amount to an MFI has been increased to Rs 50 lac.

The tenure of loan is 18-36 months including moratorium period of 3 months from

the date of first disbursement.

Term Deposit Receipts (TDRs) are considered as collateral security.

119

Micro Enterprise Loan

The general terms and conditions for assistance under this scheme are:

Minimum Rs 25 lac shall be provided to those MFIs having professional

experience and competency to manage on-lending transactions.

The loan shall be sanctioned as per the credit rating by professional agency and

flexible security norms.

Responsible Micro Finance

Under this initiative, SIDBI has created a „Lenders Forum‟ in order to increase co-

operation and to maintain better coordination among MFI lenders. This initiative

increases the ability of MFI to invest and earn a higher return across the sector.

SIDBI developed a list of five agencies to perform Code of Conduct Assessment

(COCA) of assisted MFIs by providing them credit services, recovery of credit

etc. In addition the bank creates awareness among MFIs through educating them

on client protection principles and assists them to implement best practices under

its smart campaign partnership.

Salient Features of Micro Finance Programme

This programme asserts the following activities:

(a) Arranging Fixed Deposit for MFIs/NGOs The bank is providing micro-finance

through its network of eligible MFIs/NGOs. To avail loan from SIDBI under this

scheme, security deposits are required from MFIs/NGOs. For this purpose, the

Government of India (GoI) will provide funds to SIDBI which is known as „Portfolio

Risk Fund.‟ This fund will be utilised by SIDBI as a security deposit in return of the

loan amount given to MFIs/NGOs. Then 10 per cent of the loan amount is retained by

SIDBI as fixed deposit. The MFIs/NGOs contributes 25 per cent of the loan amount

and balance 75 per cent of the loan amount would be met out of the funds given by

GoI. The SIDBI will pay interest to the Government at the same rate as applicable to

120

NGOs/MFIs and the bank is responsible for the recovery of loan as well as interest

amount. If loan was not recovered, the bank would adjust fixed deposit and interest

accrued on 25 per cent of the loan amount given by MFIs/NGOs and then adjusts 75

per cent of security deposit contributed by GoI with its prior approval. In case of full

recovery of loan, either Government contribution would be channelized further as a

security or will be returned to the GoI with the prior approval of the Committee.

(b) Training on Micro-Finance Programme The Government of India also assists

SIDBI in meeting the training requirements of NGOs, MFIs, SHGs etc. to upscale

their knowledge about Micro Finance Programmes.

(c) Institution building for ‘Intermediaries’ for identification of viable projects The

GoI also help MFIs/NGOs through identification of intermediary organisations. These

organisations provide guidelines to respective MFIs/NGOs in product identification,

project report formulation, developing forward and backward linkages, market

exposure etc.

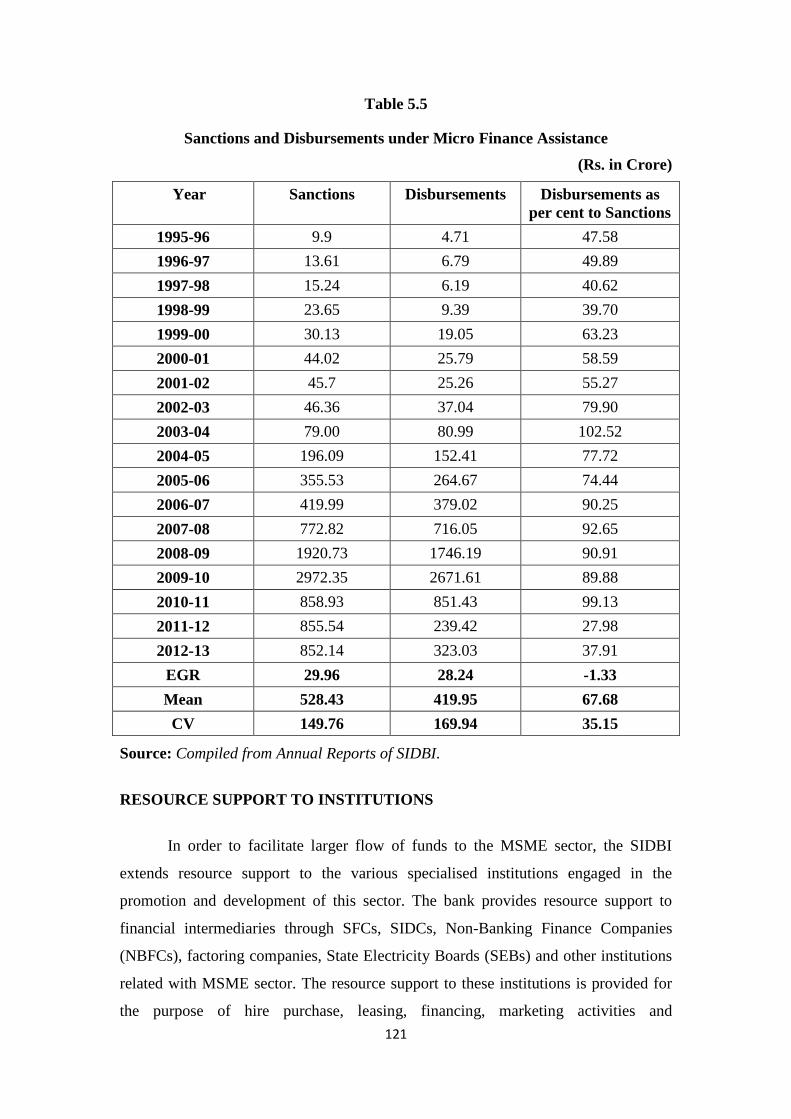

The bank has provided MF assistance to about 322 lac disadvantaged people

especially women as on March 31, 2013. The total sanctions and disbursements under

micro finance operations of SIDBI are shown in Table 5.5.

Table 5.5 shows that micro finance sanctions made by SIDBI increased from

Rs 9.9 crore in 1995-96 to Rs 852.14 crore in 2012-13 and registered growth of 29.96

per cent during the period. The micro finance disbursements also showed an

increasing trend and the amount increased from Rs 4.71 crore in 1995-96 to Rs 323.03

crore in 2012-13 and recorded a growth of 28.24 per cent during the period. The

average amount of micro finance sanctions and disbursements were Rs 528.43 crore

and Rs 419.95 crore over the period. Further, the growth in disbursements showed a

lower degree of consistency (CV=169.94) as compared to total sanctions

(CV=149.76) during the reference period. The loan disbursements as percentage of

the sanctions were highest (102.52 per cent) in the year 2003-04 and lowest (27.98 per

cent) in the year 2011-12.

121

Table 5.5

Sanctions and Disbursements under Micro Finance Assistance

(Rs. in Crore)

Year Sanctions Disbursements Disbursements as

per cent to Sanctions

1995-96 9.9 4.71 47.58

1996-97 13.61 6.79 49.89

1997-98 15.24 6.19 40.62

1998-99 23.65 9.39 39.70

1999-00 30.13 19.05 63.23

2000-01 44.02 25.79 58.59

2001-02 45.7 25.26 55.27

2002-03 46.36 37.04 79.90

2003-04 79.00 80.99 102.52

2004-05 196.09 152.41 77.72

2005-06 355.53 264.67 74.44

2006-07 419.99 379.02 90.25

2007-08 772.82 716.05 92.65

2008-09 1920.73 1746.19 90.91

2009-10 2972.35 2671.61 89.88

2010-11 858.93 851.43 99.13

2011-12 855.54 239.42 27.98

2012-13 852.14 323.03 37.91

EGR 29.96 28.24 -1.33

Mean 528.43 419.95 67.68

CV 149.76 169.94 35.15

Source: Compiled from Annual Reports of SIDBI.

RESOURCE SUPPORT TO INSTITUTIONS

In order to facilitate larger flow of funds to the MSME sector, the SIDBI

extends resource support to the various specialised institutions engaged in the

promotion and development of this sector. The bank provides resource support to

financial intermediaries through SFCs, SIDCs, Non-Banking Finance Companies

(NBFCs), factoring companies, State Electricity Boards (SEBs) and other institutions

related with MSME sector. The resource support to these institutions is provided for

the purpose of hire purchase, leasing, financing, marketing activities and

122

technological development of the sector. Further, short-term loans to power

corporations are extended to meet their credit requirements. The quantum of total

sanctions and disbursements under resource support to various institutions extended

by SIDBI are shown in Table 5.6.

Table 5.6

Sanctions and Disbursements under Resource Support to Institutions

(Rs. in crore)

Year Sanctions Disbursements Disbursements as per

cent to Sanctions

1990-91 75 72.1 96.13

1991-92 32.8 24.1 73.48

1992-93 50 42.6 85.20

1993-94 174.3 123.8 71.03

1994-95 353.4 157.1 44.45

1995-96 1091 713.77 65.42

1996-97 1406.06 660.53 46.98

1997-98 1447.7 677.7 46.81

1998-99 1465.38 958.72 65.42

1999-00 1320.5 692.17 52.42

2000-01 792.24 437.54 55.23

2001-02 492 451.67 91.80

2002-03 1049.56 660.39 62.92

2003-04 1302.86 1009.36 77.47

2004-05 1603.97 1041.2 64.91

2005-06 893.5 956.82 107.09

2006-07 549.5 548.5 99.82

2007-08 825.83 651.83 78.93

2008-09 1224.33 1197.08 97.77

2009-10 2003.94 1501.6 74.93

2010-11 810 980 120.99

2011-12 1399.06 1620 115.79

2012-13 1988.11 4242.5 213.39

EGR 16.06 20.35 3.69

Mean 971.78 844.39 82.97

CV 60.89 101.93 43.26

Source: Compiled from Annual Reports of SIDBI.

123

Table 5.6 shows the amount of sanctions extended by SIDBI as resource

support to various institutions increased from Rs 75 crore in 1990-91 to Rs 1988.11

crore in 2012-13 and recorded growth of 16.06 per cent during the period. The

amount of disbursements under resource support also indicates an impressive growth

during the period and the amount increased from Rs 72.1 crore in 1990-91 to Rs

4242.50 crore in 2012-13 and registered a growth of 20.35 per cent over the period.

The average amount of sanctions and disbursements under the scheme were Rs

971.78 crore and Rs 844.39 crore during the period. The growth rate of disbursements

was highest (20.35 per cent) as compared to sanctions (16.06 per cent) during the

period of study. Further, a high degree of variation has been observed in growth of

disbursements (CV=101.93) as compared to the sanctions (CV=60.89) during the

reference period. The loan disbursements as percentage of the sanctions were

maximum (213.39 per cent) in 2012-13 and minimum (44.45 per cent) in the year

1994-95.

SANCTIONS UNDER DIRECT AND INDIRECT CREDIT TO

TOTAL SANCTIONS

The proportion of loan sanctions made by SIDBI under its direct and indirect

assistance schemes out of the total amount of loan sanctioned are shown in Table 5.7.

Table 5.7 reveals that the total amount of sanctions under direct credit

assistance increased from Rs 274.40 crore in 1990-91 to Rs 24852.06 crore in 2012-

13 and recorded growth rate of 22.73 per cent during the period. The total amount of

sanctions under indirect credit assistance also increased from Rs 2134.30 crore in

1990-91 to Rs 34621.77 crore in 2012-13 and registered growth of 13.50 per cent

during the period. The average amount of sanctions under direct credit and indirect

credit were Rs 5345.71 crore and Rs 10376.55 crore during the reference period. It

has been further observed that total sanctions of the bank increased from Rs 2408.7

crore in 1990-91 to Rs 59473.82 crore in 2012-13 and showed an impressive growth

of 15.69 per cent during the period. The growth of sanctions under direct credit

showed a high degree of variation (CV=123.30) as compared to the total sanctions

124

(CV=103.93) and sanctions under indirect credit (CV=96.38) over the period of study.

The sanctions under direct credit as percentage of total sanctions were highest (56.47

per cent) in the year 1994-95 and lowest (11.39 per cent) in the year 1990-91. The

sanctions under indirect credit as percentage of total sanctions were highest (88.61 per

cent) in the year 1990-91 and lowest (43.35 per cent) in the year 1994-95.

Table 5.7

Sanctions under Direct and Indirect Credit to Total Sanctions

(Rs. in crore)

Year Sanctions under

Direct Credit

Sanctions under

Indirect Credit

Total Sanctions

1990-91 274.40 (11.39) 2134.30 (88.61) 2408.7

1991-92 502.50 (17.66) 2343.50 (82.34) 2846

1992-93 821.70 (28.25) 2086.70 (71.75) 2908.4

1993-94 1407.30 (41.96) 1946.80 (58.04) 3354.1

1994-95 2653.80 (56.47) 2037.00 (43.35) 4699.3

1995-96 2347.50 (38.70) 3718.06 (61.30) 6065.56

1996-97 2591.96 (39.97) 3893.36 (60.03) 6485.32

1997-98 2818.38 (37.66) 4665.78 (62.34) 7484.16

1998-99 2622.21 (29.53) 6257.63 (70.47) 8879.84

1999-00 2525.19 (24.60) 7739.55 (75.40) 10264.74

2000-01 1876.13 (17.34) 8944.47 (82.66) 10820.6

2001-02 2058.57 (22.81) 6966.95 (77.19) 9025.52

2002-03 1718.18 (15.76) 9185.42 (84.24) 10903.6

2003-04 2571.32 (31.18) 5674.96 (68.82) 8246.28

2004-05 2827.38 (31.10) 6263.22 (68.90) 9090.6

2005-06 4787.52 (39.98) 7187.31 (60.02) 11974.83

2006-07 4668.24 (42.05) 6434.04 (57.95) 11102.28

2007-08 4425.91 (27.38) 11738.47 (72.62) 16164.38

2008-09 6773.17 (23.21) 22414.84 (76.79) 29188.01

2009-10 10618.96 (29.89) 24902.38 (70.11) 35521.34

2010-11 16207.37 (38.39) 26006.35 (61.61) 42213.72

2011-12 21001.57 (40.00) 31497.89 (60.00) 52499.47

2012-13 24852.06 (41.79) 34621.77 (58.21) 59473.82

EGR 22.73 13.50 15.69

Mean 5345.71 10376.55 15722.633

CV 123.30 96.38 103.93

Note: The figures given in parentheses show percentages to total sanctions.

Source: Compiled from Annual Reports of SIDBI.

125

DISBURSEMENTS UNDER DIRECT AND INDIRECT CREDIT

TO TOTAL DISBURSEMENTS

The proportion of loan disbursements made by SIDBI under its direct and

indirect assistance schemes out of the total amount of loan disbursed are shown in

Table 5.8.

Table 5.8

Disbursements under Direct and Indirect Credit to Total Disbursements

(Rs. in crore)

Year Disbursements

under Direct

Credit

Disbursements

under Indirect

Credit

Total

Disbursements

1990-91 199.40 (10.85) 1639.10 (89.15) 1838.5

1991-92 359.10 (17.71) 1668.30 (82.29) 2027.4

1992-93 645.30 (30.07) 1500.50 (69.93) 2145.8

1993-94 1151.40 (43.10) 1519.90 (56.90) 2671.3

1994-95 1982.80 (58.57) 1401.90 (41.41) 3385.3

1995-96 1953.58 (40.69) 2847.25 (59.31) 4800.83

1996-97 1958.80 (42.72) 2625.89 (57.28) 4584.69

1997-98 1890.29 (36.07) 3350.41 (63.93) 5240.7

1998-99 2047.63 (32.58) 4237.54 (67.42) 6285.17

1999-00 2082.38 (29.90) 4881.12 (70.10) 6963.5

2000-01 1549.64 (24.06) 4891.77 (75.94) 6441.41

2001-02 1262.00 (21.32) 4657.33 (78.68) 5919.33

2002-03 1178.27 (17.35) 5611.14 (82.65) 6789.41

2003-04 1567.10 (35.50) 2847.05 (64.50) 4414.15

2004-05 2260.65 (36.53) 3927.18 (63.47) 6187.83

2005-06 3244.88 (35.66) 5854.87 (64.34) 9099.75

2006-07 4079.73 (39.90) 6145.64 (60.10) 10225.37

2007-08 4539.55 (30.09) 10547.66 (69.91) 15087.21

2008-09 6811.15 (24.07) 21486.69 (75.93) 28297.84

2009-10 9159.94 (28.70) 22758.03 (71.30) 31917.97

2010-11 12848.52 (33.12) 25947.37 (66.88) 38795.89

2011-12 15048.66 (36.56) 26111.72 (63.44) 41160.38

2012-13 13084.54 (32.29) 27435.31 (67.71) 40519.85

EGR 20.95 13.66 15.09

Mean 3952.40 8430.16 12382.59

CV 110.56 107.80 107.80

Note: The figures given in parentheses show percentages to total disbursements.

Source: Compiled from Annual Reports of SIDBI.

126

Table 5.8 reveals that the total amount of disbursements under direct credit

assistance increased from Rs 199.40 crore in 1990-91 to Rs 13084.54 crore in 2012-

13 and recorded growth rate of 20.95 per cent during the period. The total amount of

disbursements under indirect credit assistance also increased from Rs 1639.10 crore in

1990-91 to Rs 27435.31 crore in 2012-13 and registered growth of 13.66 per cent

during the period. The average amount of disbursements under direct credit and

indirect credit were Rs 3952.40 crore and Rs 8430.16 crore during the reference

period. It has been further observed that total disbursements of the bank increased

from Rs 1838.5 crore in 1990-91 to Rs 40519.85 crore in 2012-13 and recorded

growth of 15.09 per cent during the period. The growth of disbursements under direct

credit showed a high degree of variation (CV=110.56) as compared to the

disbursements under indirect credit and total disbursements (CV=107.80) over the

period of study. The disbursements under direct credit as percentage of total

disbursements were highest (58.57 per cent) in the year 1994-95 and lowest (10.85

per cent) in the year 1990-91. The disbursements under indirect credit as percentage

of total disbursements were highest (89.15 per cent) in the year 1990-91 and lowest

(41.41 per cent) in the year 1994-95.

SIDBI AS NODAL AGENCY FOR GOVERNMENT SCHEMES

Apart from providing direct and indirect assistance to eligible MSMEs, SIDBI

also plays a predominant role by implementing various MSME sector schemes

introduced by Government of India. SIDBI acts as a nodal agency for different

subsidy schemes sponsored by various Ministries and initiated by GoI for

encouraging MSME units in adopting modern technologies. A brief profile of the

schemes is mentioned below:

(i) TECHNOLOGY UPGRADATION FUND SCHEME (TUFS)

With a view to upgrade and modernise the Indian Textile Industry, the

Ministry of Textiles, GoI introduced Technology Upgradation Fund Scheme on April

1, 1999. SIDBI acts as a nodal agency and plays a key role in the implementation of

the scheme. The new as well as existing segment of textile industry as per the

definition of MSMED Act, 2006 are eligible for availing assistance under the scheme.

127

(ii) CREDIT LINKED CAPITAL SUBSIDY SCHEME (CLCSS)

To facilitate technological upgradation in the specified products of the MSME

units, the Ministry of MSME introduced Credit Linked Capital Subsidy Scheme.

SIDBI along with other 9 banks have been processing claims for subsidy as per the

guidelines of the scheme. The new units planning to set up appropriate technology

and existing units planning for upgradation of technology are eligible under the

scheme. As per scheme, 15 per cent capital subsidy for adoption of proven

technologies for approved products/sub-sectors. Subsidy limited to 15 per cent of the

purchase price of plant and machinery with a ceiling on loan under the scheme of Rs 1

crore.

(iii) SCHEME OF TECHNOLOGY UPGRADATION/SETTING UP/

MODERNISATION/ EXPANSION OF FOOD PROCESSING

INDUSTRIES – (FPTUFS).

To upgrade and improve the processing capabilities of MSME units engaged

in food processing like fruits and vegetables, milk products, oilseed products, fishery

etc., the Ministry of Food Processing Industries introduced technology

upgradation/setting up/modernisation/expansion of food processing industries on

April 1, 2007. All those units that are within the scope of banks direct credit scheme

are eligible to avail assistance under the scheme. The scheme is implemented through

SIDBI. The Ministry will provide grant of 25 per cent of the cost of plant and

machinery and for technical civil works and maximum Rs 50 lac in general areas. In

difficult areas like Jammu and Kashmir, Uttarakhand, Andaman & Nicobar Islands,

Lakshwadeep the grant of 33 per cent and maximum assistance up to Rs 75 lac will be

provided by the GoI.

(iv) INTEGRATED DEVELOPMENT OF LEATHER SECTOR SCHEME

(IDLSS): With a view to upgrade the leather industry by providing adequate and

timely finance, the Ministry Of Commerce and Industry launched Integrated

Development of Leather Sector Scheme in November, 2005. This scheme helps

128

existing tanneries, footwear and leather products units to optimize their capacity,

enhance productivity and makes them globally competitive. All the existing units

engaged in leather goods, footwear components and eager to upgrade their

technology are eligible for availing assistance under the scheme.

For scheme for existing units in leather and leather products, GoI provides

grant up to 30 per cent of cost of plant and machinery for MSMEs and 20 per cent for

non MSMEs subject to a ceiling of Rs 50 lac.

(v) TECHNOLOGY AND QUALITY UPGRADATION SUPPORT TO MICRO,

SMALL AND MEDIUM ENTERPRISES (TEQUP)

To enhance the competitiveness of the MSME sector, the Ministry of MSMEs

has introduced a programme named National manufacturing Competitiveness

Programme (NMCP) comprising 10 components related to Indian MSME products.

The programme aims at technology upgradation, raising productivity and enlarging

the domestic and international market share of the MSME units. technology and

quality upgradation support to Micro, Small and Medium Enterprises is one of the

important components of NMCP that focuses on two major aspects. The first

objective is to make MSMEs aware about benefits of energy efficient technologies

that lead to reducing cost of production and emission of Green House Gases (GHGs).

The second objective focuses on enhancing the product quality of Indian MSMEs so

as to make them globally competitive. The major activities covered under the scheme

comprises, capacity building of MSME clusters for Energy Efficiency/Clean

Development Mechanism, implementation of energy efficient technologies, setting up

of Carbon Credit Aggregation Centres (CCA) for introducing and popularizing Clean

Development Mechanism (CDM) in MSME clusters, encouraging MSMEs to acquire

product certification licences from national/international bodies, study of impact of

the scheme, administrative and other activities.

129

PROMOTIONAL AND DEVELOPMENTAL ACTIVITIES OF

SIDBI

Promotional and Developmental (P&D) support to the MSME sector has

always been an integral part of the bank‟s activities. P&D activities pursued by SIDBI

since inception creates new avenues and cater to growth and welfare especially of

rural poor and women. As an apex financial institution, SIDBI meets the varied

developmental needs of the MSME sector through its wide range of promotional and

developmental activities. The objectives behind P&D initiatives of the bank are to

strengthen the micro, small and medium enterprise sector to make them globally

competitive, economic development of poor through self-employment as well as

promotion of micro-enterprises. The bank extends development and support services

in the form of loans and grants to different implementing agencies like Technical

Consultancy Organisations (TCOs), NGOs, associate financial institutions, marketing

agencies, etc. engaged in the promotion and development of MSME units. The

conducting agencies are given the required amount as allocated under this scheme by

SIDBI to conduct the particular activity. These agencies then fulfil the formalities and

follow the procedure as laid by SIDBI till completion of the program. The banks

Regional offices (ROs)/Branch offices (BOs) are fully involved in the implementation

and monitoring of the P&D activities so as to achieve the desired result.

REORIENTATION OF PROMOTIONAL AND DEVELOPMENTAL

ACTIVITIES

It has been recognised that P&D activities of the bank act as a catalyst through

its significant contribution in the overall growth of Micro, Small and Medium

Enterprise (MSME) sector in India. Thus, a strong need was felt to make requisite

changes in the existing schemes so as to enhance credibility of the bank‟s P&D

activities. The promotional and developmental activities of the bank are crystallized

into schemes mentioned below:

(i) Micro Enterprises Promotion Programmes (MEPPs)

(ii) Entrepreneurship Development Programmes (EDPs)

130

(iii) Management Development Programmes

(a) Small Industries Management Programmes (SIMAPs)

(b) Skill-cum-Technology Upgradation Programmes (STUPs)

(iv) Cluster Development Programmes

(v) Other Initiatives of the bank

(a) Environment and Quality Management

(b) Marketing Activities

(c) SIDBI support for North Eastern Region

(d) Other Activities

(i) Micro Enterprises Promotion Programmes (MEPPs)

Micro Enterprises Promotion Programme earlier known as Rural Industries

Programme is a unique approach for providing benefit to rural entrepreneurs. The

programme lays emphasis on stimulating and guiding the potential entrepreneurs in

setting up of industrial enterprises in rural areas. The programme attempts to mitigate

the problems such as rural unemployment, under-utilisation of technical know-how

and resources for development of viable and self-sustaining micro and small

enterprises in India. The MEPPs of SIDBI is a comprehensive Business Development

Service (BDS) programme designed to provide information, training, credit

technology support and marketing of products for promoting rural enterprises.

SIDBI‟s efforts in this direction have been acknowledged at international level and

the bank has bagged the prestigious “ADFIAP Development Award 2003” given by

the Association of Development Finance Institutions in Asia and Pacific (ADFIAP)

under the Countryside Development category. The MEPPs are normally of 3 years

duration and will be further extended on the basis of performance of the

Implementing Agency (IA). The main role of the IA is to inculcate professional inputs

among entrepreneurs and to help them in project identification and implementation.

As per the policy modifications, the programme has been discontinued in non-

performing areas on the basis of results obtained under portfolio review. The start up

support in the form of administrative expenses for reputed implementing agencies has

been increased from Rs 5 lac to Rs 7 lac per district. The performance fee of units

131

requiring higher investment through SIDBI finance has been increased to promote

expansion of the existing units. Since inception, more than 38,000 enterprises have

been promoted under MEPPs which provides benefit to about 1.07 lac persons as on

March 31, 2012. A brief profile of the beneficiaries under MEPPs conducted through

SIDBI is given in Table 5.9.

(ii) Entrepreneurship Development Programmes (EDPs)

Entrepreneurship development is regarded as a key element of small industry

promotion. Entrepreneurship can be developed by training which results in

development of skills and enhancement of managerial capabilities of small

entrepreneurs. As we know that small enterprises are unable to attract professionally

qualified persons so, to make the Entrepreneurship Development Programmes (EDPs)

result-oriented, SIDBI provides training to entrepreneurs to set up their own

enterprises. The Ministry of MSME has set up various institutions at national level for

entrepreneurship development. The EDPs aim at promotion of self-employed ventures

resulting in employment generation especially in rural areas comprising less

privileged sections of the society like women, SCs/STs, minorities, etc. The bank

undertakes EDPs for the MSME entrepreneurs through its Rural Development and

Self-Employment Training Institute (RUDSETI) at Ujire, Entrepreneurship

Development Institute of India (EDII) at Ahmedabad, Technical Consultancy

Organisations (TCOs) and NGOs.

The EDPs are normally of 4-6 weeks duration along with practical training.

The duration can be extended or reduced as per the need of the participants. Each

programme covers about 25 participants for developing their entrepreneurial traits.

According to recent policy guidelines, the capability of new as well as existing

entrepreneurs has been facilitated through adequate training and counselling and by

establishing linkage under SIDBI‟s Micro Enterprise Lending (MEL). The

performance fee structure under EDP has been changed and now is at par with

MEPPs. Under this programme, about 36000 participants have been benefitted

through EDPs supported by the bank as on March 31, 2012. The MEPPs and EDPs

supported by SIDBI are shown in Table 5.9.

132

Table 5.9

MEPPs and EDPs supported by SIDBI

Year MEPPs since

inception %age Change

EDPs since

inception %age Change

1995-96 2700 - - -

1996-97 3950 46.30 623 -

1997-98 4500 13.92 743 19.26

1998-99 5419 20.42 884 18.98

1999-00 6022 11.13 1098 24.21

2000-01 7100 17.90 1317 19.95

2001-02 8485 19.51 1581 20.05

2002-03 10800 27.28 1709 8.10

2003-04 13651 26.40 1943 13.69

2004-05 17376 27.29 2083 7.21

2005-06 22400 28.91 2230 7.06

2006-07 26000 16.07 2376 6.55

2007-08 29600 13.85 2561 7.79

2008-09 32600 10.14 2661 3.90

2009-10 35000 7.36 2732 2.67

2010-11 37000 5.71 2831 3.62

2011-12 38000 2.70 2894 2.23

EGR 17.97 10.78

Mean 17682.53 1891.63

CV 73.13 41.08

Source: Compiled from Annual Reports of SIDBI.

Table 5.9 shows that the number of units promoted under Micro Enterprises

Promotion Programmes since inception by SIDBI increased from 2700 units in 1995-

96 to 38000 units in 2011-12 and registered growth of 17.97 per cent during the

period. The bank supports 17683 units on an average for the period under study. The

133

growth in MEPPs was highest (46.30 per cent) in the year 1996-97 and lowest (2.70

per cent) in the year 2011-12. The Entrepreneurship Development Programmes

conducted by the bank increased from 623 programmes in 1996-97 to 2894

programmes in 2011-12 and recorded growth of 10.78 per cent during the period. The

average number of EDPs supported by the bank is 1892 over the period. The growth

in EDPs was highest (24.21 per cent) in the year 1999-00 and lowest (2.23 per cent) in

the year 2011-12. Further, the table highlights that the EDPs showed greater

consistency (CV=41.08) as compared to MEPPs (CV=73.13) during the reference

period.

(iii) Management Development Programmes (MDPs)

In the present scenario managerial deficiency and lack of adequate skill have

been found a major shortcoming in the growth of MSMEs. In this regard, SIDBI

introduced two schemes under Management Development Programmes for removing

the weaknesses of HRD in MSME sector namely, Small Industries Management

Programmes (SIMAPs) and Skill-cum-Technology Upgradation Programmes

(STUPs). To strengthen the institutional network of the MSME sector, SIDBI

provides support to different specialised management and technology institutions for

conducting SIMAPs and STUPs. These programmes enhance the entrepreneurial skill

and talent that helps them in evaluating technology needs and ensures industry-

institution association. The standalone SIMAP has also been supported by the bank on

a selective basis under its reorientation policy. A separate fund has been allocated by

the bank for providing support to vocational training programmes targeting

underprivileged sections of the society. The total number of management

development programmes (both SIMAPs and STUPs) conducted by the bank since

inception provides benefit to about 39,690 participants at the end of financial year

2012. Both these schemes are explained below:

(a) Small Industries Management Programmes (SIMAPs)

These programmes aim at developing entrepreneurs through training like

industrial managers to assist small entrepreneurs of the MSME sector. Thus, the

programme serves the dual objective by providing second line of industrial managers

134

to the MSME sector and by providing professional qualification to young graduates

for productive employment. SIMAP provides training to unemployed graduates,

diploma holders and industry-sponsored candidates for enhancing managerial

capabilities and making them professionally competent.

The programme is conducted for a period of 14-18 weeks in three stages. Each

programme covers about 20-25 candidates. In the first phase, class-room sessions of

about 5-8 weeks are covered that provides information and skills required for

management of the MSME units. In the second phase, 8 weeks on-the-job practical

training is provided. This is followed by the third phase of 1-2 weeks wherein

refresher session is conducted before awarding programme certificates to the

candidates. In addition, the bank also conducts specialised SIMAPs in the area of

marketing, finance, production, etc. as per the requirement of the specific industry.

These are conducted for only those candidates who have previous work experience

and it also increases the placement chances of candidates. The SIMAPs supported by

the bank are shown in Table 5.10.

(b) Skill-cum-Technology Upgradation Programmes (STUPs)

The objective of STUPs is to enhance the existing skill and competence of the

entrepreneurs to improve the performance of MSME units. The programme

determines ways to strengthen process improvements, technological developments

among MSME units. Thus, programme laid emphasis on upgrading the technology

profile of the existing micro, small and medium enterprises.

The programme imparts training to entrepreneurs or senior executives having

similar composition in terms of their profile, nature of industry, financial position etc.

The duration of the programme is for a period of 4-6 days on full-time basis and 8-12

days on part-time basis covering maximum 25 participants. The programme

concentrates more on specific areas like product and process technology, industrial

design rather than on general topics. The participants should pay only 25 per cent of

the programme fee and balance would be met by SIDBI. The SIMAPs and STUPs

supported by the bank are shown in Table 5.10.

135

Table 5.10

SIMAPs and STUPs Supported by SIDBI

Year SIMAPs since

inception %age Change

STUPs since

inception %age Change

1995-96 93 238

1996-97 120 29.03 338 42.02

1997-98 130 8.33 460 36.09

1998-99 148 13.85 529 15.00

1999-00 180 21.62 677 27.98

2000-01 199 10.56 803 18.61

2001-02 219 10.05 902 12.33

2002-03 240 9.59 1074 19.07

2003-04 260 8.33 1241 15.55

2004-05 265 1.92 1302 4.92

2005-06 270 1.89 1351 3.76

2006-07 276 2.22 1389 2.81

2007-08 281 1.81 1429 2.88

2008-09 284 1.07 1460 2.17

2009-10 288 1.41 1475 1.03

2010-11 292 1.39 1488 0.88

2011-12 295 1.03 1504 1.08

EGR 7.48 12.21

Mean 226 1039

CV 30.06 43.06

Source: Compiled from Annual Reports of SIDBI

Table 5.10 shows that the number of Small Industries Management

Programmes supported by the bank since inception increased from 93 programmes in

1995-96 to 295 programmes in 2011-12 and registered a growth of 7.48 per cent

during the period. The bank supports 226 programmes on an average for the period

136

under study. The growth in SIMAPs was highest (29.03 per cent) in the year 1996-97

and lowest (1.03 per cent) in the year 2011-12. The Skill-cum-Technology

Upgradation Programmes conducted by the bank increased from 238 programmes in

1995-96 to 1504 programmes in 2011-12 and recorded growth of 12.21 per cent

during the period. The average number of STUPs supported by the bank is 1039 over

the period. The growth in STUPs was highest (42.02 per cent) in the year 1996-97 and

lowest (1.03 per cent) in the year 2009-10. Further, the table highlights that the

STUPs showed lower degree of consistency (CV=43.06) as compared to SIMAPs

(CV=30.06) during the reference period.

(iv) Cluster Development Programmes (CDPs)

The primary goal of the bank is technology upgradation of the MSME units

and to expand its benefits to large number of industries. The bank has initiated

number of steps for providing developmental support to MSME units. Under the

CDPs, a new approach was followed for improving the technical capabilities and

competitiveness among MSME units. In this regard, Cluster Development

Programmes have been introduced in homogeneous clusters of industries to improve

the technical and marketing skills of the participants. This approach leads to

upgradation of quality and productivity through reduction in cost of raw material.

During 2002-03, the bank‟s framework of Cluster Development Programme has

changed from a technology centric approach to a comprehensive approach of business

development services. The new approach aims at creating awareness on new

product/design, management practices, skill and technology upgradation etc. Some of

the ongoing clusters where CDPs were implemented are the bicycle and bicycle part

components cluster at Ludhiana, hand tool unit at Jalandhar, Punjab and foundry units

at Howrah, West Bengal etc. Under its reorientation policy, the bank provides

exposure in cluster development through association with agencies like Confederation

of Indian Industry (CII), Punjab State Council for Science and Technology etc. SIDBI

opened retail offices in selected industrial clusters for creating a group of trained

business service provider by providing suitable training to the cluster development

agents.

137

The first step in Cluster Development Programme involves the selection of 5-

10 units in clusters. These clusters must be homogeneous in terms of nature of

technology, products, production levels, trade practices and their capability to absorb

improved technology. Then expert consultancy agencies assess the technology

upgradation need of the individual clusters and formulate unit-specific modernisation

packages. These agencies also outline the domain for grouping of technical

capabilities of existing units. Till date, the bank has supported around 85 CDPs in

India.

(v) Other Initiatives of the bank

In addition to its above mentioned P&D activities, the bank also concentrates

on some other relevant issues. These are:

(a) Environment and Quality Management

An important initiative adopted by bank is to provide support to MSME units

related to environmental issues. It has been realised by the bank that some industrial

units have been causing pollution in the country and MSMEs are unable to exercise

control over this issue. Thus, SIDBI through its environment and management

programmes creates awareness on environmental issues to MSMEs with the help of

demonstration pollution control projects. These programmes should be conducted for

a period of about 2 days for 25-30 homogeneous clusters engaged in the process of

recycling. This will enable the MSMEs to improve technology, material savings and

to implement only those projects having benefits of pollution control. During 2003-

04, this programme became part of the Corporate Social Responsibility of the bank.

As per this principle, the bank will provide credit to only those MSMEs who have

obtained „No Objection Certificate‟ from the Pollution Control Board. Further, the

bank does not provide credit to ozone depleting industries. Some more measures

taken in this regard are introduction of online payment system to avoid printouts so as

to reduce the use of paper, using video conferencing facility for conducting meetings

so as to reduce the travel time and cost, using recycled paper in taking official notes

etc. These benefits results in beneficial effects as regards environment management.

138

Quality Management