Financing Property 2012 - Savills Ireland · Financing Property 2012 ... But, in this presentation...

95

Financing Property 2012 Theme: Who’s in charge – borrowers, lenders or politicians? Our 24 th annual series of presentations

Transcript of Financing Property 2012 - Savills Ireland · Financing Property 2012 ... But, in this presentation...

Financing Property 2012 Theme: Who’s in charge – borrowers, lenders or politicians?

Our 24th annual series of presentations

William Newsom The Property Finance Market

Presentation contents

Mat Oakley The Commercial Property Markets

Faisal Choudhry The Residential Property Markets

Joan Henry The Irish Property Markets

Angus Potterton Conclusions

Angus Potterton Introduction

What are the biggest issues facing the property finance market today?

The Property Finance Market - contents

What has triggered the structural change?

What is the nature of the structural change?

Annual lending activity going forward

Note: This is a re-run (and update) of presentations made in June 2012

What are the biggest issues facing the property

finance market today?

During May 2012, I met 46 property lenders, borrows and market participants

So many different answers, but the main ones were ....

To paraphrase Bill Clinton: “It’s the economy stupid”

The regulatory environment – Basel, Slotting, Solvency, etc.

Scarcity of capital; allocation of capital to property lending; the increased cost of it

In this context, the regulators are in charge

Banks deleveraging

The future of secondary. Whilst fundamental, it is merely a question of pricing.

Some secondary values continue to fall, whilst other assets represent great

opportunities

Other issues raised, but no less important

The crisis in the Eurozone. But no one knows how it will pan out. However, life

will carry on. London is well placed to weather the storm (in some cases

benefiting)

The funding gap. But the world is awash with equity. Trouble is, it’s not in the

right place (not enough with the banks)

The scarcity of suitable product to lend against, particularly for those chasing

prime opportunities. What’s new?

The cost of unwinding swaps. It is a huge issue for existing loan books. It is a

“known known”. The five years burn off by 31.12.2013. Long dated swaps

remain a serious problem

Everything takes so long – purchases, refinancing, approvals processes, extra

layers of due diligence (“business prevention officers”), decision making

But above all, it’s a market full of contradictions

Some say “the market is closed”, or “there’s no new lending”, or “the Germans are

going home”, or “development finance is non-existent”, etc. One borrower (with 40+

years experience) said “This is the worst time ever to raise finance”

But yet:

I have 200+ names of lending organisations in my sights (both commercial and

residential, some coming, some going). The equivalent figure in 1994 was 140

I can name (and will) 16 organisations who can write a cheque for £100M or more

I can name (but won’t) another 50 organisations who are actively lending above

£10M. But, in this presentation I name 75 players in the market

At the Residential Development Funding Conference on 15 March 2012, I named

37 organisations that provide such finance (both senior and mezz). Albeit

selectively

A development company recently received over a dozen offers of finance for a

large office property in central London (7 years income, then total redevelopment)

Why so many contradictions?

Because the property finance market is currently going through huge structural

change

A transition from ‘traditional’ bank lenders to a whole new generation of ‘non-

traditional’ lenders

A transition from those with legacy issues to those without

A transition from those subject to ‘heavy’ regulation to those without (or less of it).

In that context, the regulators are in charge

What has triggered the structural change?

A very favourable lending environment (from a lender’s point of view), attracting

new players into the market (A)

The regulatory environment – for UK banks, that is slotting (B)

Dealing with reducing the debt mountain

I will now examine A and B

-2%

-1%

0%

1%

2%

3%

4%

5%

The message is the same but more so: “Now is a

brilliant time to be lending” (quoted 2009, 2010, 2011)

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Gross cost of money (GCoM): 5

year swap and interest rate margin

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

UK Base Rate

20yr High Coupon Gilts

IPD All Property Equivalent Yield(monthly index)

5yr Semi-annual Interest RateSwaps

2008 2009 2010 2011 2012 2008 2009 2010 2011 2012

A Property yields remain high ...

B The cost of debt remains low ...

C And the spread between

property yields and the cost of

money remains wide

Provided you have the liquidity

2008 2009 2010 2011 2012

IPD APEY less GCoM

8.0%

7.5%

7.0%

6.5%

6.0%

5.5%

5.0%

4.5%

4.0%

A

C

B

Interest rate margins have increased by 100 bps over

the last 9 months. Where do they go from here?

Forecast. Everyone says that they will continue to increase. Correct

However, at the truly prime end, where there is competitive pressure, there is potential for

them to decrease (there are examples of this)

Source: De Montfort University

0

100

200

300

400

500

600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Prime Office

Secondary Office

Forecast

bps

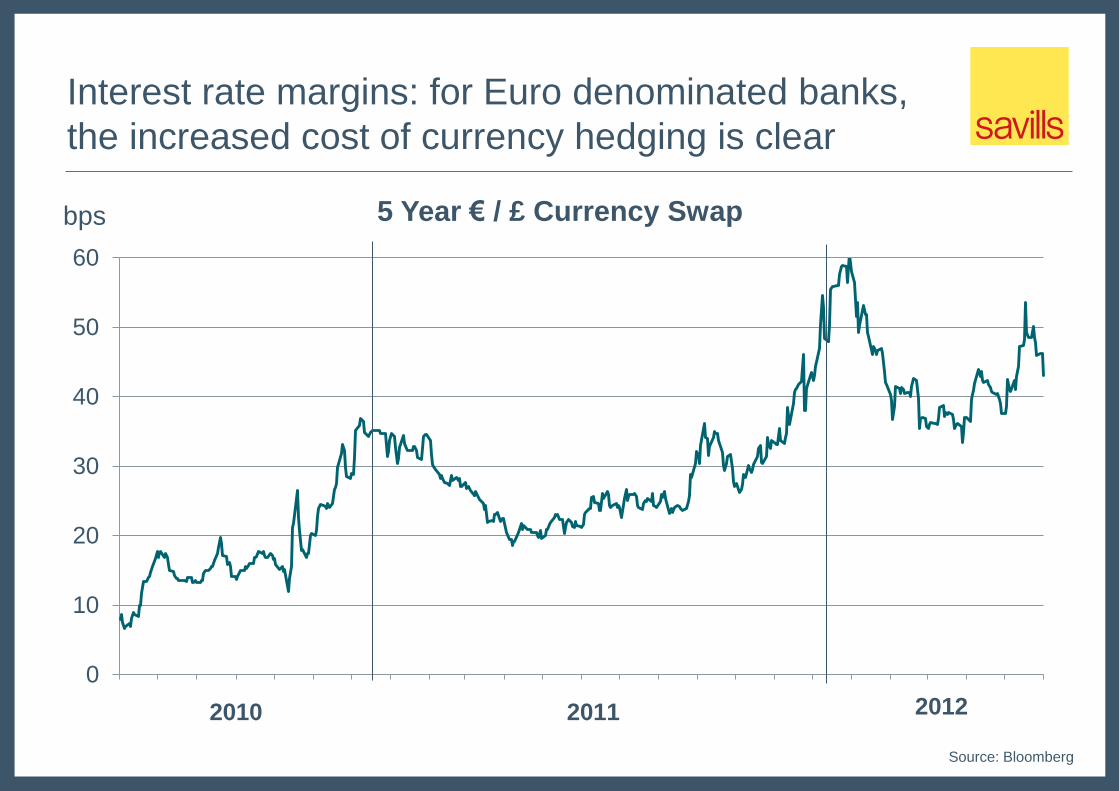

Interest rate margins: for Euro denominated banks,

the increased cost of currency hedging is clear

0

10

20

30

40

50

60

5 Year € / £ Currency Swap

2010 2011 2012

Source: Bloomberg

bps

LTVs: same old story – good for lenders, not so good

for borrowers

Source: De Montfort University

55%

60%

65%

70%

75%

80%

85%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Average maximum LTV ratios for investment sectors

LTV’s have continued to go south; along with higher ICRs, higher margins, higher

arrangement fees, more comprehensive documentation and longer timescales

But there is a consequence of these more onerous lending terms ...

Prime office

Secondary office

The distinction between segments of the capital stack

has become blurred

Because of higher margins, ICRs and fees etc, raising debt finance has become less

attractive for property owners

The structural change is such that for many traditional lenders, their biggest competitors

are those with equity to invest

Source: Savills

Equity 5-15%

Mezzanine/B Notes

5-15% @

Libor + 200/300 bps

Senior debt /

A note 75-

80% @ Libor

+ 75/100 bps

Pre-credit crunch stack Capital stack today

Equity

Senior debt

Preferred equity

Mezzanine

Stretched senior

Slice Target return Comments

/cost

70%-100% 5% - 20%

50%-85% 8% - 15% Have been known

to provide the

senior debt slice too

Up to

50%-65% 6% - 10%

The regulatory environment – for UK banks, that is

slotting

An FSA imposed risk weighting model. Very technical

Under slotting, all loans are to be assessed annually, not just new loans

The EBA is imposing higher Tier 1 capital ratios anyway. Slotting is on top of that

– leading to even higher capital requirements

The process: all property loans are assessed by reference to five criteria and

then slotted into one of four slots: strong, good, satisfactory or weak. Different

risk weightings: 70%, 90%, 115% and 250% respectively

Is being rolled out now. Being phased with different speeds for different banks

Impact? One UK Bank told me it will need nearly three times the capital as a

result of slotting

Which is huge. Two thirds of all lending has been by UK lenders. The UK banks

needs tens of millions of additional capital just to stand still

So what are the consequences of slotting?

Existing loan books: The banks will be under pressure to accelerate the process of

deleveraging. More sales of loan books and other workout scenarios

New lending: UK banks will be constrained

Loans slotted ‘satisfactory’ or ‘weak’ or ‘default’: a no-go area for UK banks?

Banks need to raise more capital. But can they?

Impact for property? We see it as positive. As it will accelerate the sale of loan books (and

other workout scenarios). Which will accelerate resolution of legacy issues. Which will

accelerate sales and/or active management of individual properties. Much needed

Strangely, development finance fits well into slotting (less than 2.5 years). Recent

research by IPD suggests slotting provides “perverse incentive”

What is the nature of the structural change?

Favourable lending terms make the UK very attractive for those with liquidity

Slotting makes the UK attractive for non-UK lenders

Thus, it is hardly surprisingly that we are seeing a massive influx of new players:

• Buyers of loan books

• Americans

• Big ticket lenders (including new entrants)

• Insurance companies

• Senior debt funds

• Mezzanine providers

• CMBS?

I will outline each

At least 6 UK loan books were sold over the

12 months to June 2012

Date Seller Buyer Description Face value Sale price Discount

Jun-11 Anglo Irish

Bank Urbicus

Scottish loan

portfolio £300m Undisclosed -

Sep-11 NAMA Barclay Brothers Maybourne Hotels £696m £696m 0%

Oct-11 Bank of

Ireland Kennedy Wilson UK loan portfolio £1.75bn c£1.4bn 20%

Dec-11 RBS Blackstone Project Isobel £1.36bn £950m 30%

Dec-11 Lloyds Lone Star Project Royal £923m c£550m 30-40%

Dec-11 NAMA Morgan Stanley

REI

Saturn/West

Properties £216m c£75m 60-70%

Mar-12 Eurohypo AXA UK loan portfolio £200m Undisclosed -

Apr-12 Bundesbank PIMCO Lehman’s Diversity

CMBS £1.14bn C£740m 30-40%

£6.585bn

Source: Real Estate Capital Magazine

Note the number of American buyers Sources of finance? Mixed

At least 5 portfolios of property loans were on the

market in June 2012

Seller Portfolio Name Description/notes Nominal

value

Lloyds Banking

Group

Project

Harrogate/

Royal II

Portfolio of 70 loans secured against

about 60 properties, all UK. All in

default

£625m

Allied Irish Bank Project Pivot Mainly small ticket commercial property,

all UK

£400m

Allied Irish Bank Project Kildare Portfolio of commercial property in

Ireland

€645M

Lloyds Banking

Group

Project Prince A mixed portfolio of Irish properties.

Understood to be under offer @ 18

cents/€ to Kennedy Wilson and

Deutsche Bank

€360M

NAMA Chrome Portfolio Understood to be under offer to Pears

Group/Dev Secs

£100M

Source: Real Estate Capital Magazine

Pricing? Large discounts to par may be necessary to get them away

I am forecasting more loan book sales – over some

years to come

Source: De Montfort University and Savills

Further increased loan sales as the cost of unwinding five year swaps written before 31.12.2008 burns off

Not seeing more loan sales till now is in line with expectation, as various stages of market evolution were

necessary before loan sales were to emerge in earnest

0

2

4

6

8

10

12

2010 2011 2012 2013/14 2015/16 2017/18

3 to 7 year play

£800M

£4.0bn

£8 bn+

£10 bn p.a.

£8 bn p.a.

£bn Forecast

£6 bn p.a.

Never before (in 20+ years) have I seen so many

Americans in this market (or looking at it)

A selection of them:

AIG

Apollo

AREA

Bank of America

Blackstone

Cerberus

Chalkhill

Citigroup

Colony Capital

Deutsche Bank

Fortress

GE Capital

Goldman Sachs

Jeffries International

Kennedy Wilson

KKR

Lone Star

Mass Mutual / Cornerstone

Met Life

Morgan Stanley

New York Life

Och Ziff

Perella Weinberg

PIMCO

Pramercia REC

Pricoa

Starwood

Wells Fargo

Westbrook Partners

Source: Savills

What’s that say about the market? The Americans feel more in charge of their destiny. The

US is ahead of us on the curve. The UK offers excellent risk adjusted returns. However, I

think size of platform matters. They will be focused on the larger portfolios/lot sizes

Lenders are seeking larger lot sizes

5%

12%

19%

4%

29% 31%

0%

5%

10%

15%

20%

25%

30%

35%

< £1m £1-4.9M £5-9.9M £10-19.9M £20-49.9M > £50M

Typical loan size in 2011: proportion of organisations’ new lending

Source: De Montfort University

This is a precursor for my list of bigger ticket lenders/...

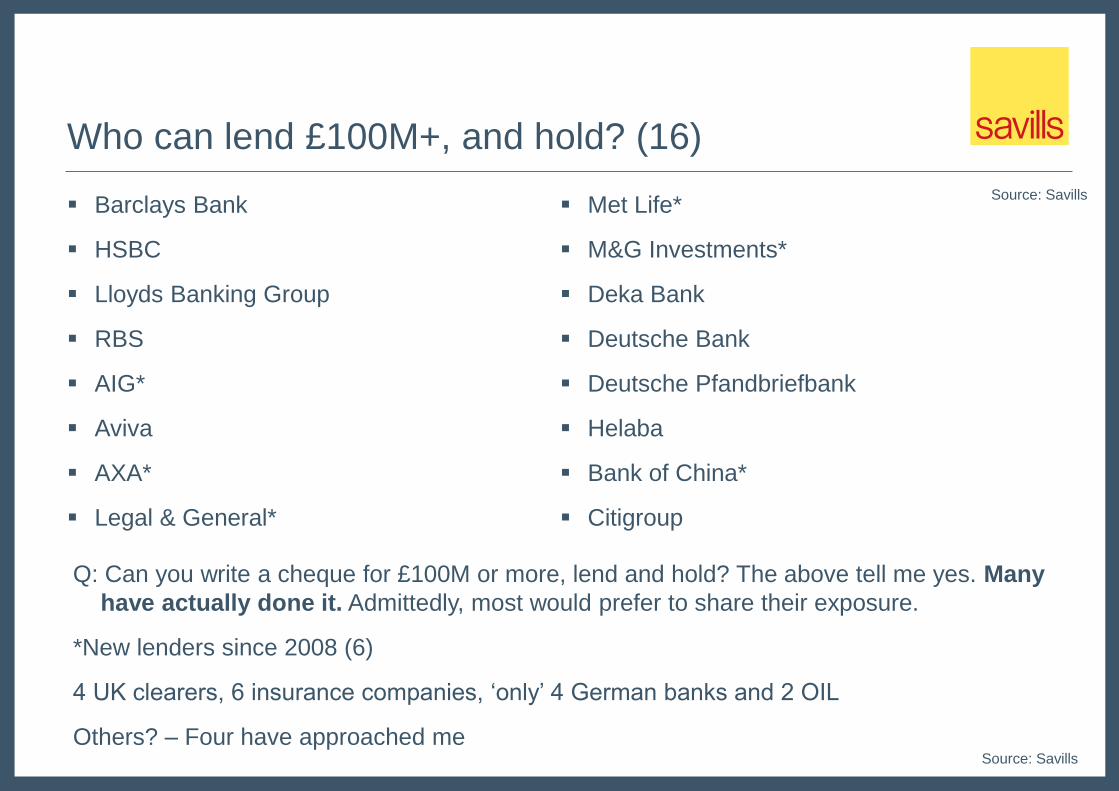

Who can lend £100M+, and hold? (16)

Barclays Bank

HSBC

Lloyds Banking Group

RBS

AIG*

Aviva

AXA*

Legal & General*

Met Life*

M&G Investments*

Deka Bank

Deutsche Bank

Deutsche Pfandbriefbank

Helaba

Bank of China*

Citigroup

Source: Savills

Q: Can you write a cheque for £100M or more, lend and hold? The above tell me yes. Many

have actually done it. Admittedly, most would prefer to share their exposure.

*New lenders since 2008 (6)

4 UK clearers, 6 insurance companies, ‘only’ 4 German banks and 2 OIL

Others? – Four have approached me

Source: Savills

Insurance companies potentially offer huge liquidity

The top 4/5 insurance companies together lent approximately £4bn in 2011, 15% of total lent

Source: Savills

Company Started * Comment

Canada Life 1980 Well established direct property investment and lending team

Aviva 1983 Very active lenders; long term lending; min 15 years

Met Life 2000/2010 Very active lenders

AXA 2008 Very active taking participations. Reported to be doing their first bilateral

M&G Inv. 2009 Very active lenders of both senior and mezzanine

Legal & General 2011 Recently announced their first property lending deal

AIG 2012 Recently announced their first property lending deal

Pricoa/Prudential of US 2012 Recently announced their desire to lend in UK

Mass Mutual/ Cornerstone 2012 Recently announced their desire to lend in UK

Allianz Pending Very active in Europe, but no Sterling denominated business (yet)

Predica Pending The insurance arm of Credit Agricole. Actively lending in France

New York Life Pending Reported to be looking at the UK

*Approx. date they started lending against UK commercial property

Why are insurance companies having such a

good time?

No Basel; nor Slotting; just Solvency 2 (referred to last year) which is considered to be

relatively benign

No capital adequacy issues; real money investors with cash to invest

Little or no legacy issues

Can lend over £100M without the need for participants/clubs (and often do it)

The UK Insurance companies have the back up of experienced direct property investment

teams with analysts. Aviva also has a long standing established property lending platform

No cross-border currency issues for UK insurance companies

No shortage of opportunities

Often lower margins (225-250 bps, above the gilt) and higher LTVs (60%-65%). A magic

combination for borrowers prepared to sign up long term

Many senior debt funds are being set up. Examples:

Source: Real Estate Capital Magazine

Manager Fund raising Strategy

Aeriance Investments €500m Will make senior loans and buy good quality portfolios

AEW Europe €500m

Senior debt fund taking participations up to €50m from banks

Agfe £1.0bn Targeting fixed-income investors

CBRE Global

Investors

€1.0bn Talking to large investors about club deals, investing in stretched and senior

and whole loans

Cordea Savills N/A Potentially moving into senior lending alongside mezzanine for prime

residential fund

Fortress Invest. Group N/A Targeting higher margin senior loans

Goldman Sachs $3bn+ Global debt fund, targeting senior and subordinated loans

Henderson Global $700-800m Joint venture between property and fixed income teams. Initial focus on UK

and Germany

Morgan Stanley $1bn Global debt fund

Renshaw Bay N/A Backed by Jacob Rothschild and South African Reinet Investments

Schroders - In June, announced they were considering entering real estate lending

Starwood €1bn Targeting higher margin senior loans in UK and Germany

Some are at an early stage of fund raising. I don’t think that, or the precise legal structure or

strategy matters. This all represents market capacity

There is a huge number of players seeking to provide

mezzanine ...

To illustrate this, I name half (18) my list of 36 ‘non-traditional’ mezzanine lenders

Probably a third (6) of those named are responsible for 75%+ of the total mezzanine activity

Source: Savills

• Agfe

• Cairn Capital

• Contour Capital (R)

• Davon/Strata Fund (R)

• Duet/DRC Capital

• Ekistics (R)

• European Risk Capital

• European Special

Opportunities

• La Salle Mgt (R)

• Longbow/Rockpoint (R)

• Maslow Cap/Dragonfly (R)

• Och Ziff Cap. Mgt (R)

• Omni Capital (R)

• Partners Group

• Pluto Cap/Mountgrange (R)

• Pramerica

• Safanad (R)

• Urban Exposure (R)

R = Also named on my residential list

Note: Excludes ‘traditional’ lending organisations (9+) that also provide mezzanine

... but how much business are they doing?

In 2010, 6 organisations reported mezzanine lending of £500M

In 2011, the following was reported

Mezzanine lending still remains a tiny element of total loan books at less than

1%. But huge scope for expanding that

One issue is finding a senior debt provider. Some mezz providers resort to

providing the senior too

Source: De Montfort University

Lenders No. of

providers

Mezzanine

provided

‘Traditional’ bank 9 £784M

‘Non-traditional’ 8 £339M

17 £1,123M

So, what’s all that add up to in terms of

annual lending activity going forward?

Annual lending activity: how much money will be

available to be lent?

In terms of new loans, 2011 turned out to be in line with forecast – notwithstanding a perceived

reduction in activity during H2. Why? Impact of new lenders?

I am expecting at least one third of new loans to come from ‘non-traditional’ lenders

Source: De Montfort University & Savills

£0

£10

£20

£30

£40

£50

£60

£70

£80

£90£83.7bn

bn

£15.1bn

£27.5bn

£36bn

Savills’ Forecast

June 2011. June

2012 unchanged!

Extended loans

New loans

Annual value of loan originations

The Property Finance Market - Summary

Who’s in charge? Overwhelmingly, the regulators are seen as being in charge.

Because of slotting, the UK banks effectively are out of the market. For those with

legacy issues, there is still a long way to go

Any new property lending that UK banks do will be as part of a much wider

banking relationship. Been the case for the last 3 years already? Different for

development finance?

If a borrower does not have such relationships, there is no shortage of ‘non-

traditional’ lenders to go to. But who will be the performers? At what cost?

The transition in the property lending market is huge

But you still cannot get finance for “worse than good secondary”

Underlying property fundamentals remain crucial

Over to Mat to shed light on the commercial property fundamentals

Outlook for UK commercial Can a normal market be resumed in a debt-drought?

Mat Oakley

Investment turnover has recovered

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2000 2002 2004 2006 2008 2010 2012 to Aug

Rest

of

UK

as %

of

To

tal

£m

Rest of UK

London

RoUK % of Total

Source: Property Data, Savills

Where is the market functioning?

London investment and part pre-let development generally fundable

by debt/equity

Prime investment around the UK restrained by confidence, not

necessarily funding

Small shops and large shopping centres all appear tradeable

Big sheds always popular in risk-averse times

Development is clearly fundable in central London,

though the undersupply story remains credible

Source: Savills

0

2

4

6

8

10

12

14

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

m s

q f

t

Development Refurbishment Average

Where isn’t the market functioning?

Source: Savills

0

1

2

3

4

5

6

7

8

9

10

Sh

op

pin

g c

en

tre d

evelo

pm

en

t m

sq

ft

Risk aversion continues to widen the yield spread

0

50

100

150

200

250

300

350

400

450

500

bp

s

Prime/Tertiary spread

Prime/Secondary spread

Source: Savills

We remain in a risk-filled world

More risk means continued risk aversion

Non-domestic investors will continue to be attracted to the UK as a “safe-

haven”

London bias will remain, and this will support investment and

development

Shopping centres, leisure and retail warehouse parks will pick up in

popularity

Regional development will remain scarce

Tenants prepared to pre-let will drive some markets. What will happen to

those who cant?

Prime yields remain low (and possibly go lower)

Secondary and tertiary continue to rise (until they attract the risk-

embracers)

What else is different?

Less new debt available and more old debt to pay off

Weaker economic recovery

Vacancy rates lower due to less overbuilding

Structural change in retail

Impending bulge in lease expiries (good and bad thing)

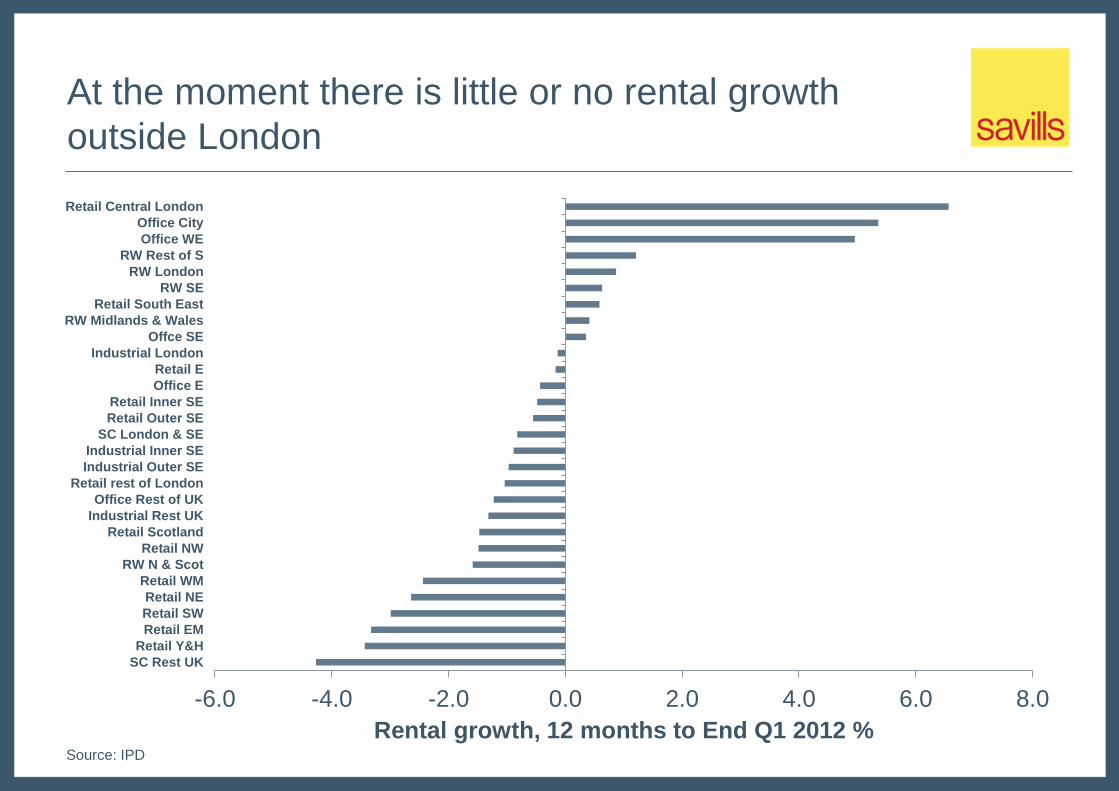

At the moment there is little or no rental growth

outside London

-6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0

SC Rest UK

Retail Y&H

Retail EM

Retail SW

Retail NE

Retail WM

RW N & Scot

Retail NW

Retail Scotland

Industrial Rest UK

Office Rest of UK

Retail rest of London

Industrial Outer SE

Industrial Inner SE

SC London & SE

Retail Outer SE

Retail Inner SE

Office E

Retail E

Industrial London

Offce SE

RW Midlands & Wales

Retail South East

RW SE

RW London

RW Rest of S

Office WE

Office City

Retail Central London

Rental growth, 12 months to End Q1 2012 % Source: IPD

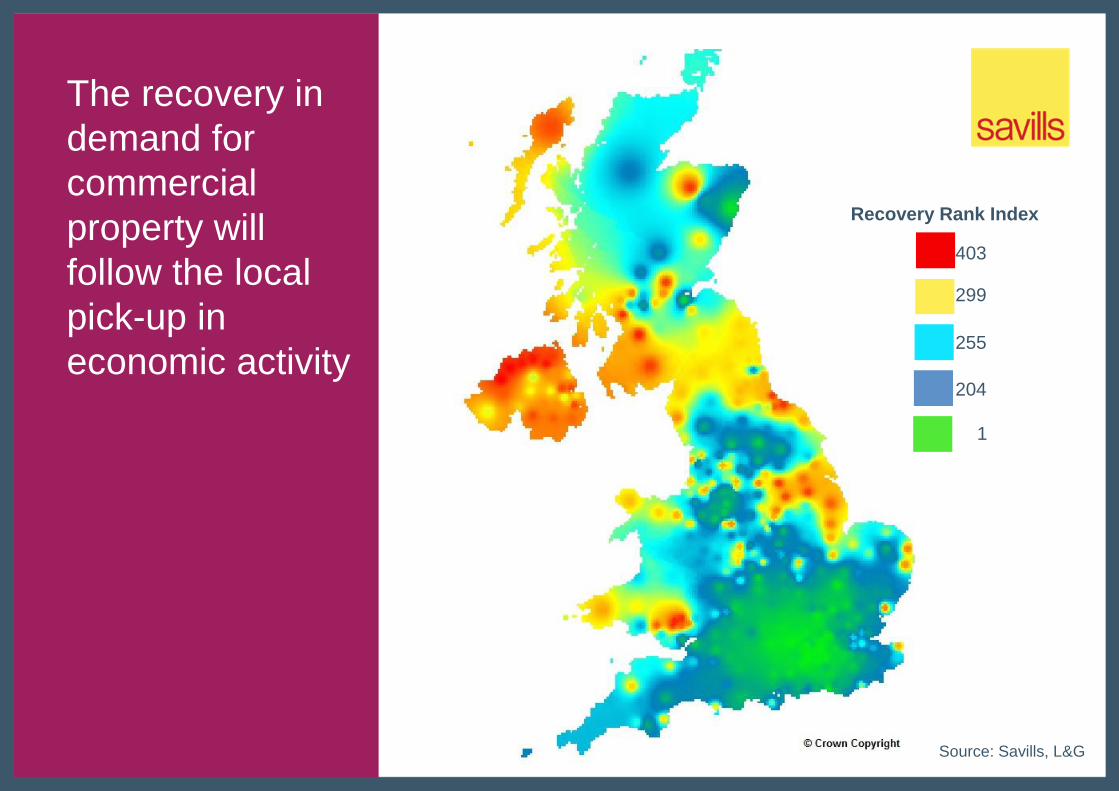

The recovery in

demand for

commercial

property will

follow the local

pick-up in

economic activity

Source: Savills, L&G

299

255

204

1

Recovery Rank Index

403

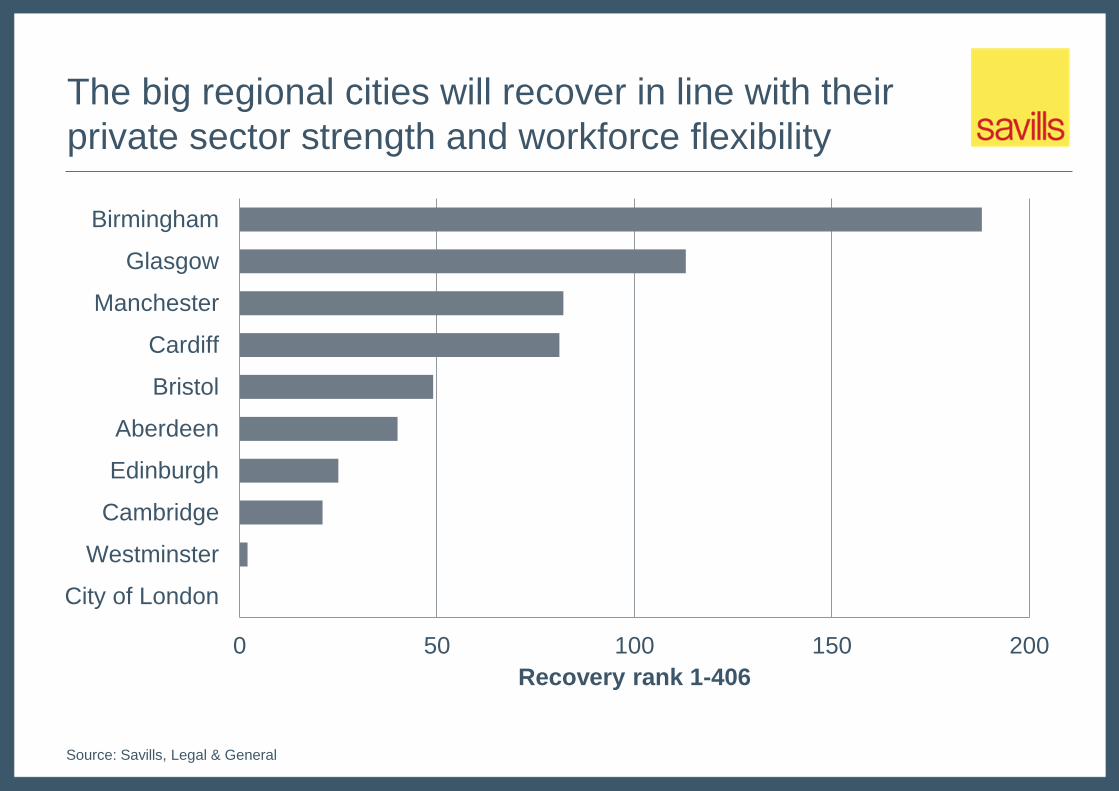

The big regional cities will recover in line with their

private sector strength and workforce flexibility

0 50 100 150 200

City of London

Westminster

Cambridge

Edinburgh

Aberdeen

Bristol

Cardiff

Manchester

Glasgow

Birmingham

Recovery rank 1-406

Source: Savills, Legal & General

Where does structural change leave the “tertiary grot”?

Realistic pricing of property or loan books will enable re-pricing of

rents

Policy help will be needed to resuscitate some locations e.g.

Removal of empty rates liability

Allow temporary change of use to more beneficial uses?

Allow permanent change of use to residential?

Give LEP’s more ability to designate local areas of need?

The best rental growth might not be in the most

obvious “safe” locations

Office:

Strong regional cities where private sector strength balances public sector

contraction

+

Restrained or non-existent development pipeline

=

Better rental growth prospects in some regional cities than in London?

Retail:

Structural change is underway

Some towns will never recover without policy/financial help

But, internet is an opportunity for some segments of retail

Affluent/equity-rich catchments will remain the location of choice

Logistics:

Safe in difficult times

The anti-internet play?

Outlook for UK Residential Structural change in a debt constrained environment

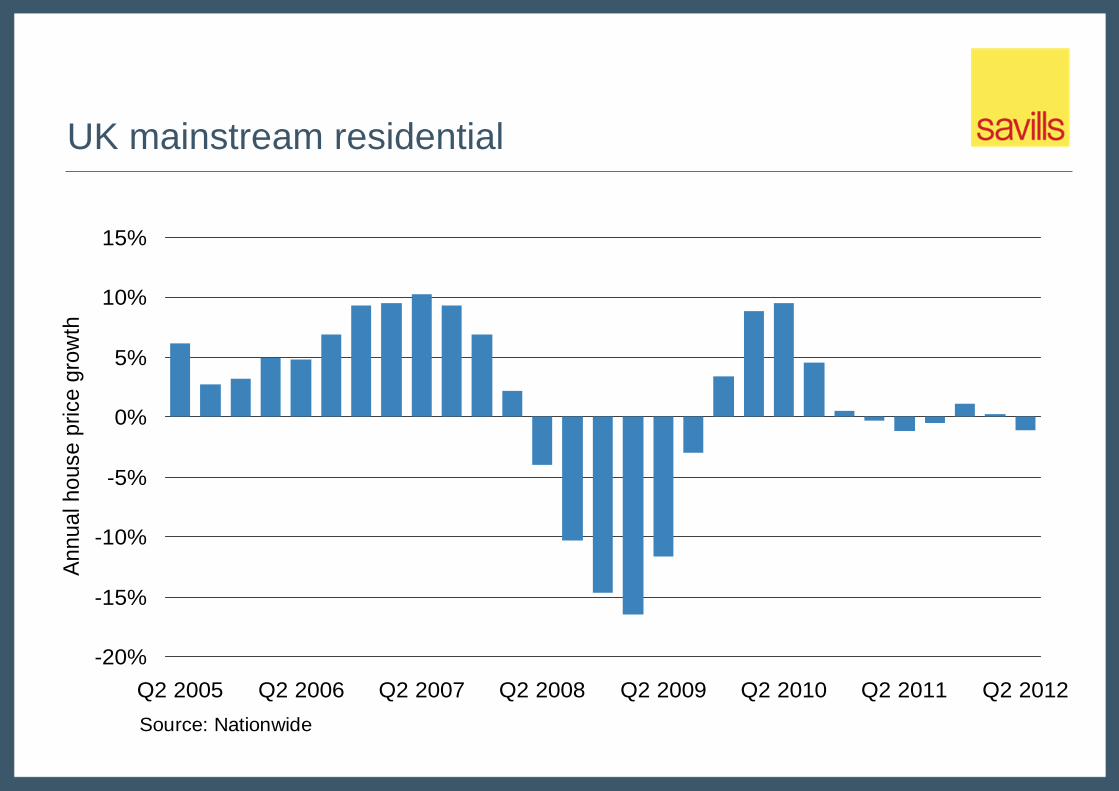

UK mainstream residential

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Q2 2005 Q2 2006 Q2 2007 Q2 2008 Q2 2009 Q2 2010 Q2 2011 Q2 2012

An

nu

al h

ouse

price

gro

wth

Source: Nationwide

UK residential transactions and mortgage lending

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2005Q2 2006Q2 2007Q2 2008Q2 2009Q2 2010Q2 2011Q2 2012Q2

Source: Council of Mortgage Lenders / Land Registry / Registers of Scotland / HMRC

Residential transactions

Number of loans for house purchase lending

The previous ‘stable’ market

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,000

2,000,000

2,250,0001990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Source: Registers of Scotland / HMRC

Resid

ential tr

ansactions (

UK

)

Actual Average 1990-1999

Core markets outperforming - transactions

Source: Land Registry / Registers of Scotland / HMRC

-45% -40% -35% -30% -25% -20% -15% -10% -5% 0%

South West

Greater London

South East

East Anglia

East Midland

Wales

United Kingdom

West Midland

Yorkshire & Humberside

Scotland

North West

North East

Northern Ireland

Oil price

Source: Index Mundi

0

20

40

60

80

100

120

140

160S

ep-0

7

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Cru

de O

il U

S$

per

barr

el

UK Gross Domestic Product (percentage change)

2.80% 2.70%

-0.10%

-4.90%

1.40%

0.70%

-0.40%

1.10%

1.90%2.30% 2.40%

-6.00%

-5.00%

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Actual Independent average of new forecasts

Source: HM Treasury

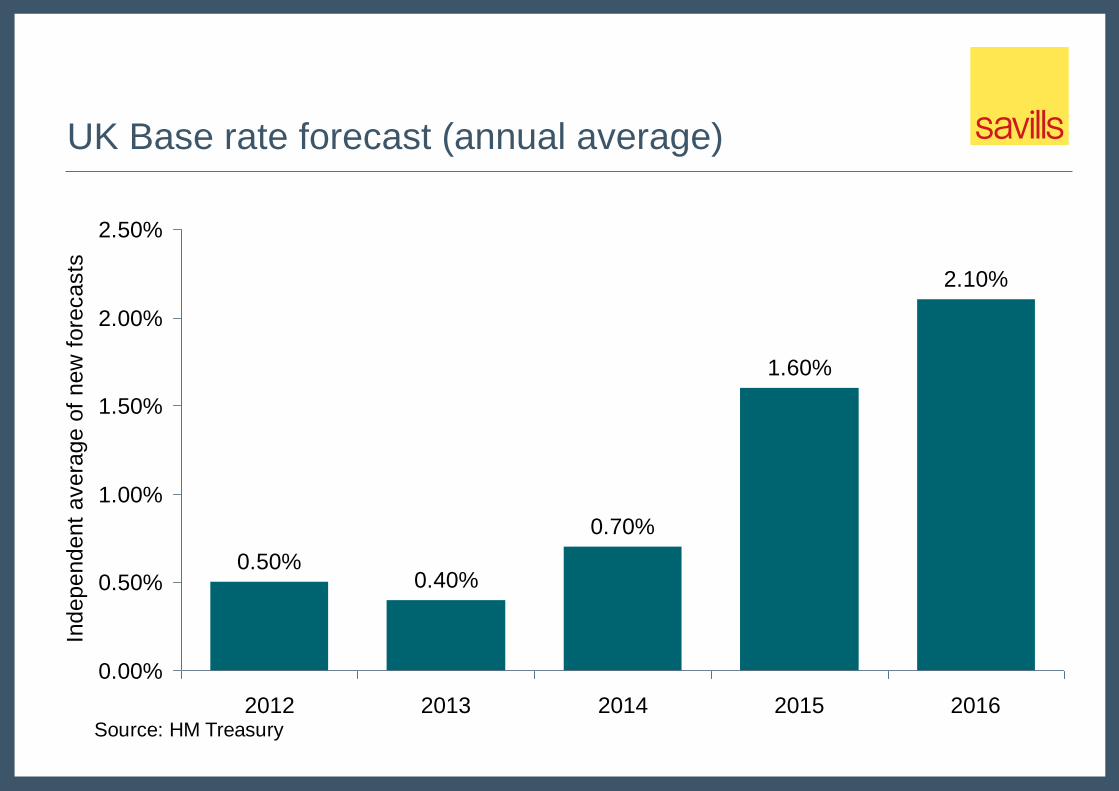

UK Base rate forecast (annual average)

0.50%0.40%

0.70%

1.60%

2.10%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

2012 2013 2014 2015 2016

Independent

avera

ge o

f new

fore

casts

Source: HM Treasury

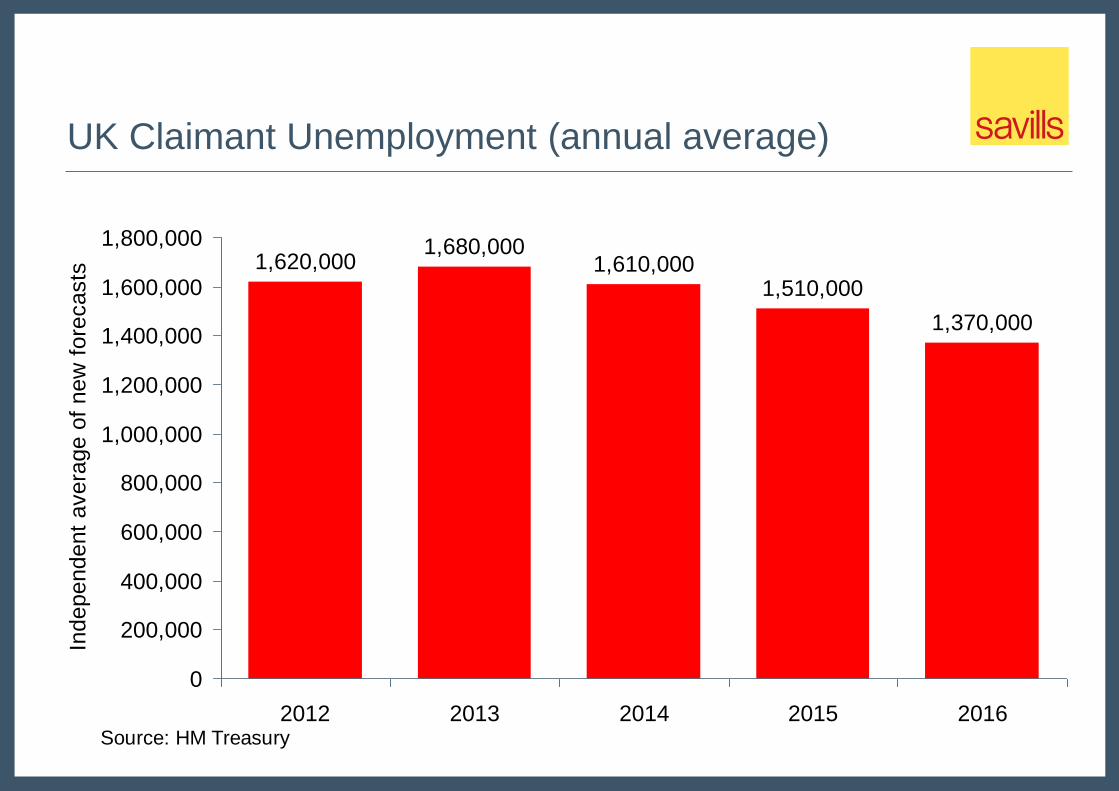

UK Claimant Unemployment (annual average)

1,620,0001,680,000

1,610,0001,510,000

1,370,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2012 2013 2014 2015 2016

Ind

ep

end

ent

ave

rage

of

ne

w f

ore

ca

sts

Source: HM Treasury

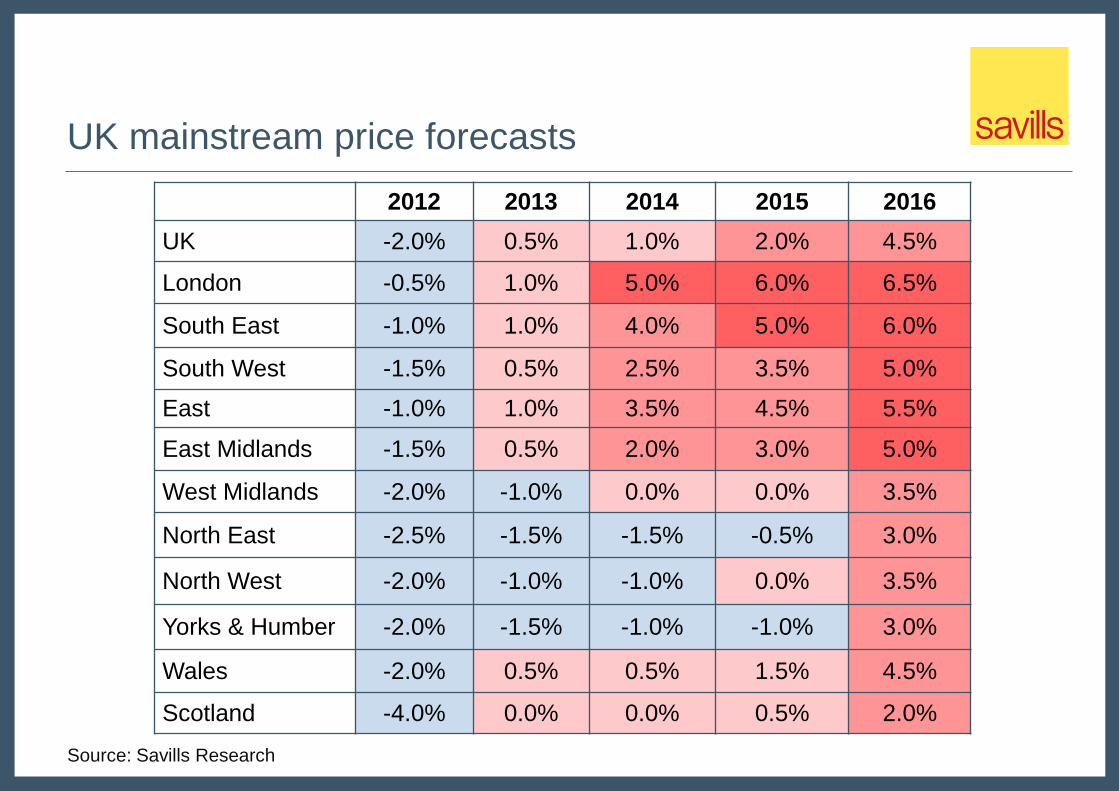

UK mainstream price forecasts

2012 2013 2014 2015 2016

UK -2.0% 0.5% 1.0% 2.0% 4.5%

London -0.5% 1.0% 5.0% 6.0% 6.5%

South East -1.0% 1.0% 4.0% 5.0% 6.0%

South West -1.5% 0.5% 2.5% 3.5% 5.0%

East -1.0% 1.0% 3.5% 4.5% 5.5%

East Midlands -1.5% 0.5% 2.0% 3.0% 5.0%

West Midlands -2.0% -1.0% 0.0% 0.0% 3.5%

North East -2.5% -1.5% -1.5% -0.5% 3.0%

North West -2.0% -1.0% -1.0% 0.0% 3.5%

Yorks & Humber -2.0% -1.5% -1.0% -1.0% 3.0%

Wales -2.0% 0.5% 0.5% 1.5% 4.5%

Scotland -4.0% 0.0% 0.0% 0.5% 2.0%

Source: Savills Research

UK mainstream transaction forecasts

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,0002006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Source: HMRC / Savills Research

Resid

ential tr

ansactions

Actual Forecast

UK prime market

-30%

-20%

-10%

0%

10%

20%

30%

40%

2005Q2 2006Q2 2007Q2 2008Q2 2009Q2 2010Q2 2011Q2 2012Q2

Year

on Y

ear

change in v

alu

e

Prime Central London Prime Regional

Source: Savills Research

Prime London

Prime London driven by

Global wealth - influenced by global economy

Safe haven status

Currency advantage

Recycling of accumulated domestic wealth

Threats

Excessive economic uncertainty (UK and EU)

Taxation

UK residential development

Source: DCLG / Reuters

Estim

ate

-80

-40

0

40

80

120

160

200

240

280

320

360

400

440

(40,000)

(20,000)

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

220,000

2003 2004 2005 2006 2007 2008 2009 2010 2011

Avera

ge g

ross p

rofil (m

illio

n)

Private

housin

g c

om

ple

tions (

UK

)

Private housing completions Average profit of top 8 housebuilders

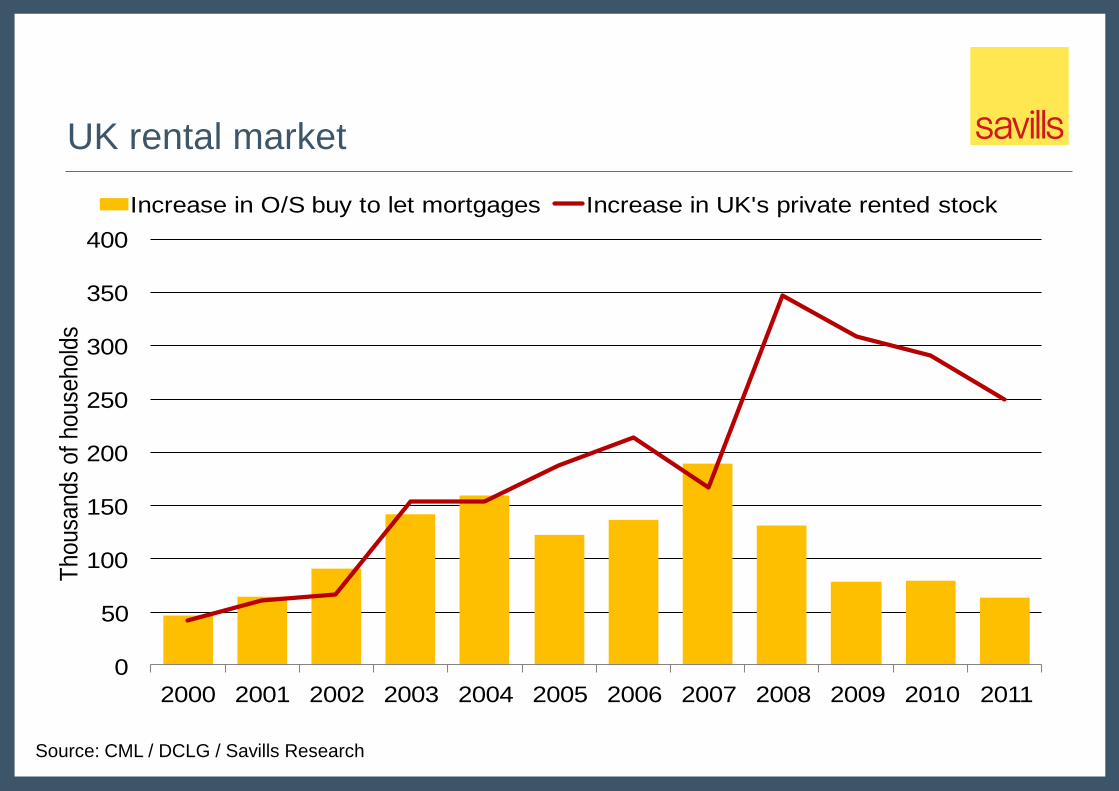

UK rental market

Source: CML / DCLG / Savills Research

0

50

100

150

200

250

300

350

400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Thousa

nds

of

house

hold

s

Increase in O/S buy to let mortgages Increase in UK's private rented stock

Investment Matrix

Less than

6.0% 6.0% to 6.5% 6.5% to 7.0% 7.0% to 7.5% 7.5% to 8.0% Over 8.0%

Less than

50%

Brighton &

Hove

Greater London

Elmbridge

50% to 55% Southend

Bournemouth

Bristol

Colchester

Oxford

Southampton

Reading

Woking

55% to 60% Northampton Portsmouth

Medway Milton Keynes

60% to 65%

Edindurgh

Stockport

Warrington

Cardiff Leicester

Nottingham

65% to 70% Bradford

Newcastle

Leeds

Manchester

Sheffield

Coventry

Birmingham

Over 70% Kirklees Glasgow

Liverpool

Forecast Total Returns 2011 - 2021

Pro

po

rtio

n o

f To

tal R

etu

rn f

rom

Ren

t

House prices and transaction numbers remain stable

Summary

New incentives expected to boost mortgage lending in 2012

Prime Regional looking excellent value for money

Core markets performing better

Economic conditions delaying housing market recovery

Prime London performing strongly but facing threats from recent legislation

Residential development adapting to a new operating environment

Opportunities for investors in the growing private rented sector

Irish Property Market Overview

Joan Henry

Commercial Market Commercial Market

Prime occupier markets holding their own Occupier demand led market activity

Investment market come to life again Investment market stagnant

Market Context

Housing Market Housing Market

Some pick up, rental dominates Activity Weak across the board

Prices remain under pressure Continued fall in prices

Structural problems will drag on recovery

2012 2011

Property Market Overview

2. Occupier Markets

Offices

Retail

Industrial

6.

Investment Market 3.

1. Market Context

Conclusions and Challenges

Housing Market 5.

Hotel Market 4.

2. Occupier Markets

Offices

Dublin Office Market

Source: Savills Research

0%

5%

10%

15%

20%

25%

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Annual Take-Up sq.m(LHS) Completions sq.m(LHS) Vacancy Rate %(RHS)

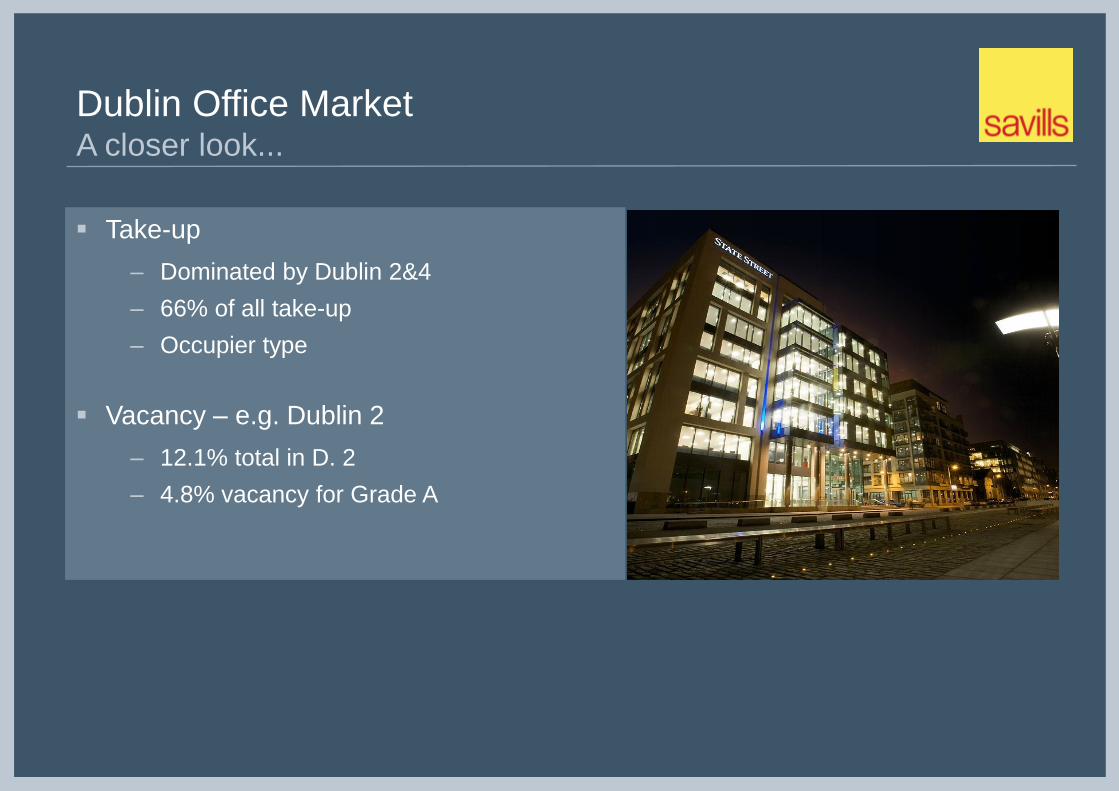

Dublin Office Market A closer look...

Take-up

‒ Dominated by Dublin 2&4

‒ 66% of all take-up

‒ Occupier type

Vacancy – e.g. Dublin 2

‒ 12.1% total in D. 2

‒ 4.8% vacancy for Grade A

Add in pic of State Street

Dublin Office Market Deals in 2012

One Park Place,

Hatch Street, Dublin 2

Size: 2,000sqm

Occupier: Irish Life & Permanent

Kilmore House,

Spencer Dock, Dublin 1

Size: 600sqm

Occupier: Ecclesiastical Insurance

East Point Plaza, East Point

Business Park, Dublin 3

Size: 1,400sqm

Occupier: Chase Paymentech

Office Market Outlook

Prime

Rents

Secondary

Rents Completions Supply Demand

2012 Bottomed

out Bottomed out None Diminishing

Dublin 2 & 4 lead,

Grade A

2013 Trending up

Bump along

the bottom None

Trend to

continue

City locations &

Grade A

Occupier Market

Retail

Retail Consumer Sentiment – upward spike followed by slump

Source: KBC/ESRI, Savills Research

35

40

45

50

55

60

65

70

75

2009 2010 2011 2012 Sep 2012

Source: CSO, Savills Research

Retail Retail Sales – remain under pressure, but narrower range

-15%

-10%

-5%

0%

5%

10%

15%

2007 2008 2009 2010 2011 2012

% C

han

ge

Change in Value of Retail Sales for All Retail (excl. Motors)

Retail Key players

Discount Retailers

‒ Aldi / Lidl / Dealz (30 new stores in 2012) /

Euro 2 etc

International Retailers

‒ H & M / Bestseller / DFS / TK Maxx

Dublin Retail Market Deals in 2012

Dubarry

Location: Dublin 2

Size: 170 sqm

Schuh

Location: Pavilions Swords

Size: 302 sqm

Retail Grafton Street / Henry Street Research

Prime retail streets maintain high

occupancy

Grafton Street at 98%

‒ 5% (11 units) trading but available

Henry Street at 100%

‒ 1% (5 units) trading but available

Key Trend to watch

‒ Increased activity on shorter lease

terms and /or

‒ Turnover rents

Retail Market Outlook

Prime

Rents

Secondary

Rents Supply Demand

2012 Bottoming Under

pressure

Prime-limited

Rest -Oversupply

Prime market

“holding its own”

2013 Prime to

stabilise Under pressure Continuation Prime once again

Occupier Market

Industrial

Dublin Industrial Market Take up and vacancy 2006 - 2012

Source: Savills Research

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2006 2007 2008 2009 2010 2011 2012 est

(sq

m)

Take up Vacancy

Dublin Industrial Market Key Industrial Deal in 2012

5 & 7 Westgate Business

Park, Ballymount,

Dublin 24

Size: Approximately 6,039 sqm

Occupier: TV3

Forest Park,

Mullingar

Co Westmeath

Size: 2,245 sqm

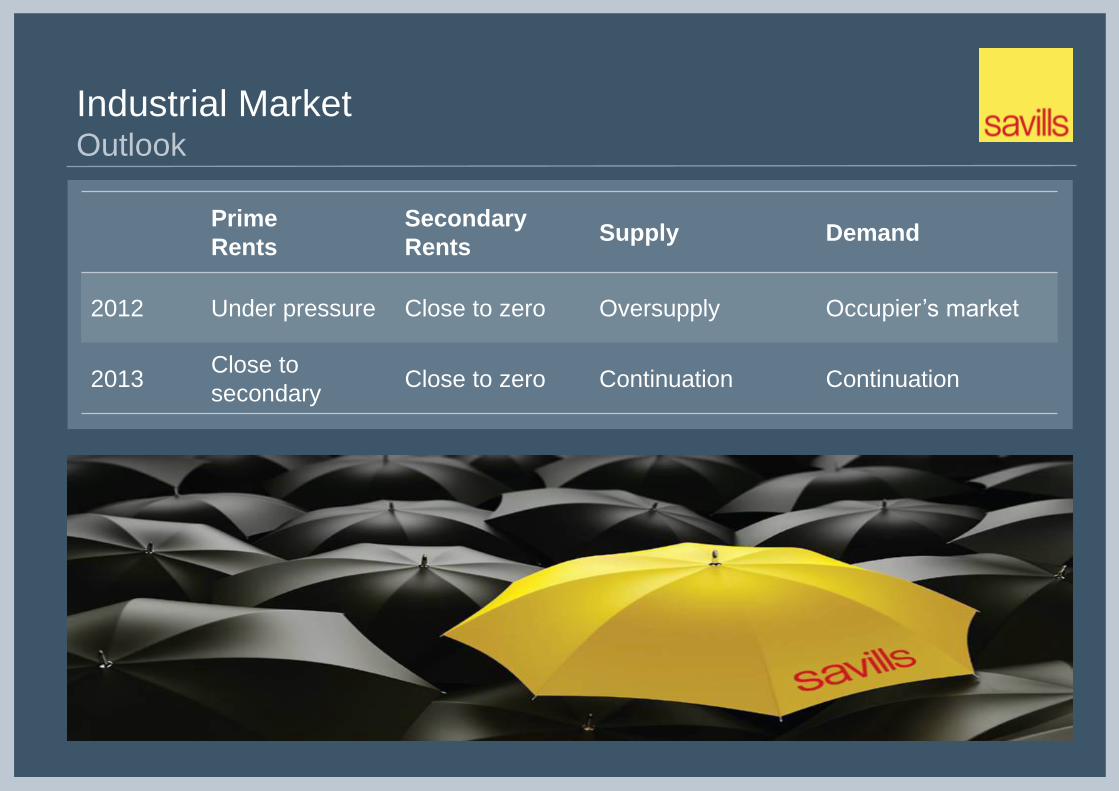

Industrial Market Outlook

Prime

Rents

Secondary

Rents Supply Demand

2012 Under pressure Close to zero Oversupply Occupier’s market

2013 Close to

secondary Close to zero Continuation Continuation

3. Investment Market

Investment Market Turnover and No. of deals – market is recovering

Source: Savills Research

€ M

illio

ns

Source: Savills Research

0

20

40

60

80

100

120

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

No

. o

f D

ea

ls

Tu

rno

ve

r -

€m

Turnover Number of Deals

Riverside II Sir John Rogersons Quay

Lot Size: c. €35m Yield: 8.6%

Investment Market 2012 Deals

Alliance Dublin 4

Lot Size: c. €40m Yield: 6.25%

Residential Deal Office Deal

One Warrington Place Dublin 2

Lot Size: c. €27m Yield: 7.5%

Office Deal

Investment Market Demand/Buyers

Demand Category Category of investment spend

Private/opportunity Equity €20m-€100m plus

Core Institutional Up to €50m

Domestic high net worth Re-emerging up to €25m

Private investors (local & international) €5-15m

Local demand Up to €5m

Investment Market Supply – Large increase

Driven by

Banks (primarily outside NAMA)

Receiverships

c. €400 m stock on Dublin market

Investment Market Outlook

Turnover

Forecast Yields Supply Demand

2012 €500m Stabilising for prime Increasing Active across all

price categories

2013 €700m Stable for prime Increasing Active across all

price categories

4. Hotel Market

Hotel Market Transactional market re-started 2012

Market split by location

Dublin and other cities continue to lead the

recovery in room sales

Varied performance in rural locations

Demand

Domestic and international buyers active

Cash buyers at realistic prices

Bank debt availability is improving

5. Housing Market

Housing Market New homes & residential

New homes supply at lowest on record - 1975

Less than 600 new units completed in Dublin to date in 2012

Significant shortage of supply across most residential sectors

Competitive bidding – some signs

Cash buyers dominate

Houses in need of refurbishment or with planning / title issues need to be

discounted significantly

Greatest value evident at upper end of market

= Rental market very strong

Housing Market Key Trend to watch - Dublin Stock

Average fall in Stock from February 2011 to July 2012

South County Dublin - 32%

North Dublin - 36%

City Centre - 29%

Housing Market Outlook

Prime

Prices

Secondary

Prices

Supply Demand Challenges

2012 Bottoming Under

pressure

No new units

2nd hand limited

Prime to lead

Rental to

dominate

Confidence

Liquidity

2013

Floor,

limited

upside

Case by

case Continuation

Prime once

again

Confidence

Liquidity

6. Conclusions & Challenges

Conclusions

Occupier markets stable - prime

Investment market recovery

Housing market

Rental to dominate/slow to recover

Conclusions and Challenges

Challenges

Economy / Eurozone

Pricing / Values

Asset Management

Overall Conclusions

Angus Potterton