Financial&managerial accounting_15e williamshakabettner chap 18

16

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights McGraw-Hill/Irwin Process Costing Process Costing Chapter 18

Transcript of Financial&managerial accounting_15e williamshakabettner chap 18

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 1/16

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rightsMcGraw-Hill/Irwin

Process CostingProcess CostingChapter 18

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 2/16

Job Order Costing

Custom orders

Unique products

Low production volume

High product flexibility

Low to mediumstandardization of labor and material

Process Costing

Repetitive operations

Identical products

High production volume

Low product flexibility

High standardization of labor and material

Production of Goods andProduction of Goods andServices and CostingServices and Costing

SystemsSystems

18-2

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 3/16

Used for production of small,identical, low-cost items.Mass produced in automatedcontinuous production process.

Costs cannot be directly traced toeach unit of product.

Process CostingProcess Costing

Typical process cost applications:Petrochemical refinery

Paint manufacturer

Paper mill18-3

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 4/16

DirectMaterials

FinishedGoods

Cost per unit for

each job

DirectLabor

FactoryOverhead

Jobs

The Work in Processaccount consists of

individual jobs in job costing .

Tracking the Physical Flow Tracking the Physical Flowand Related Productionand Related Production

CostsCosts

18-4

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 5/16

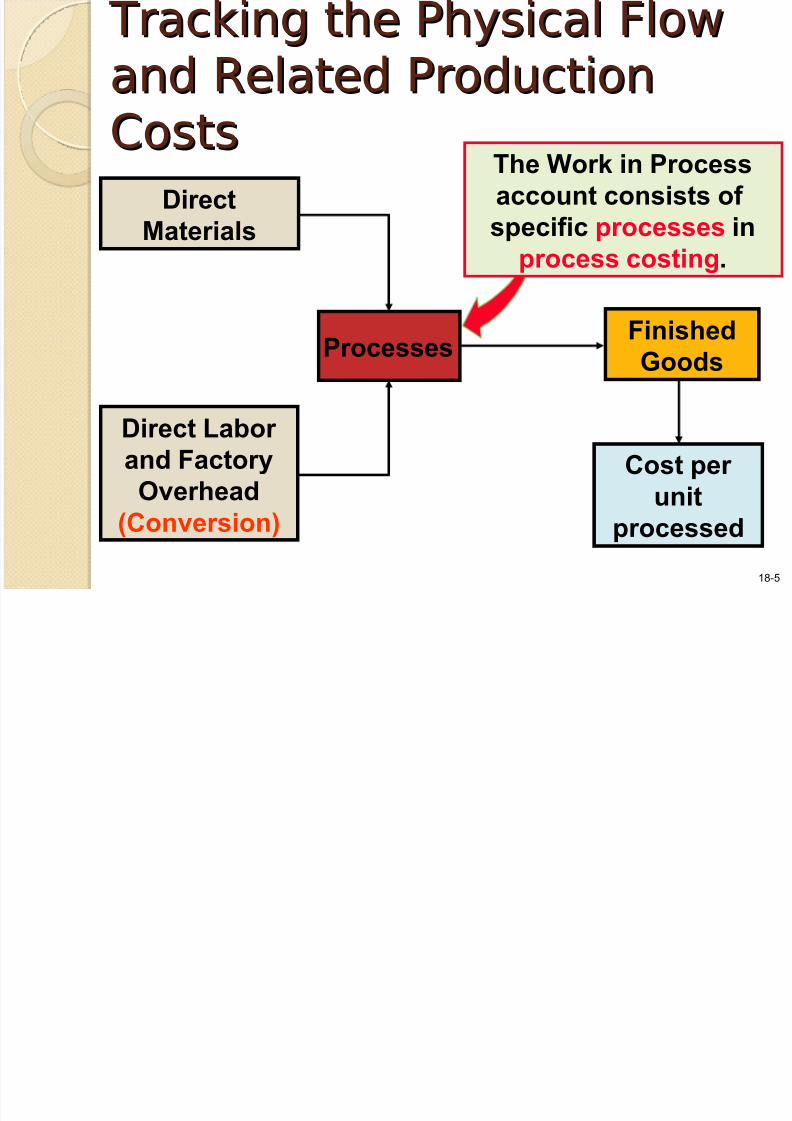

DirectMaterials

FinishedGoods

Direct Labor and Factory

Overhead(Conversion)

Processes

The Work in Processaccount consists of specific processes in

process costing .

Cost per unit

processed

Tracking the Physical Flow Tracking the Physical Flowand Related Productionand Related Production

CostsCosts

18-5

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 6/16

Same objective: to determinethe cost of products

Same inventory accounts: raw materials,work in process, and finished goods

Same overhead assignment method:predetermined rate times actual activity

Tracking the Physical Flow Tracking the Physical Flowand Related Productionand Related Production

CostsCosts

18-6

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 7/16

Work in

ProcessAssembly

Labor

Materials

I n

d i r e c

t

FinishedGoods

ConversionCosts

Direct

Deliveredto

Customers

Work inProcess

Packaging

Understanding Cost FlowsUnderstanding Cost Flows

FactoryOverhead

18-7

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 8/16

Costs are accumulated for a periodof time by process or department.

Costs are accumulated for a periodof time by process or department.

Unit cost is computed by dividing theaccumulated costs by the number of units

produced in the period.

Unit cost is computed by dividing theaccumulated costs by the number of unitsproduced in the period.

Understanding Cost FlowsUnderstanding Cost Flows

If partially complete units remain inprocess, we must use equivalent units as

the divisor to obtain unit costs.

If partially complete units remain inprocess, we must use equivalent units as

the divisor to obtain unit costs.

18-8

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 9/16

Equivalent units is a concept expressing anumber of partially completed units as asmaller number of fully completed units.

Equivalent units is a concept expressing anumber of partially completed units as asmaller number of fully completed units.

Two one-half full pitchers areequivalent to one full pitcher.

+ = 1

Process Costing andProcess Costing andEquivalent UnitsEquivalent Units

18-9

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 10/16

Cost per equivalent

unit

= Product costs for the periodEquivalent units for the period

Cost per Equivalent UnitCost per Equivalent Unit

18-10

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 11/16

Equivalent units may bedifferent for material and

conversion at different stagesof a process.

Equivalent units may bedifferent for material and

conversion at different stagesof a process.

At completion of Stage 1 of the process,material is 40% complete, but conversion

is only 25% complete.

At completion of Stage 1 of the process,material is 40% complete, but conversion

is only 25% complete.

Process Costing andProcess Costing andEquivalent UnitsEquivalent Units

Stage 1

40% of Material

25% of Conversion

18-11

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 12/16

=

=

100%

50%

Process Costing andProcess Costing andEquivalent UnitsEquivalent Units

Stage 2

25% of Conversion

60% of Material

Stage 1

40% of Material

25% of Conversion

+

+

18-12

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 13/16

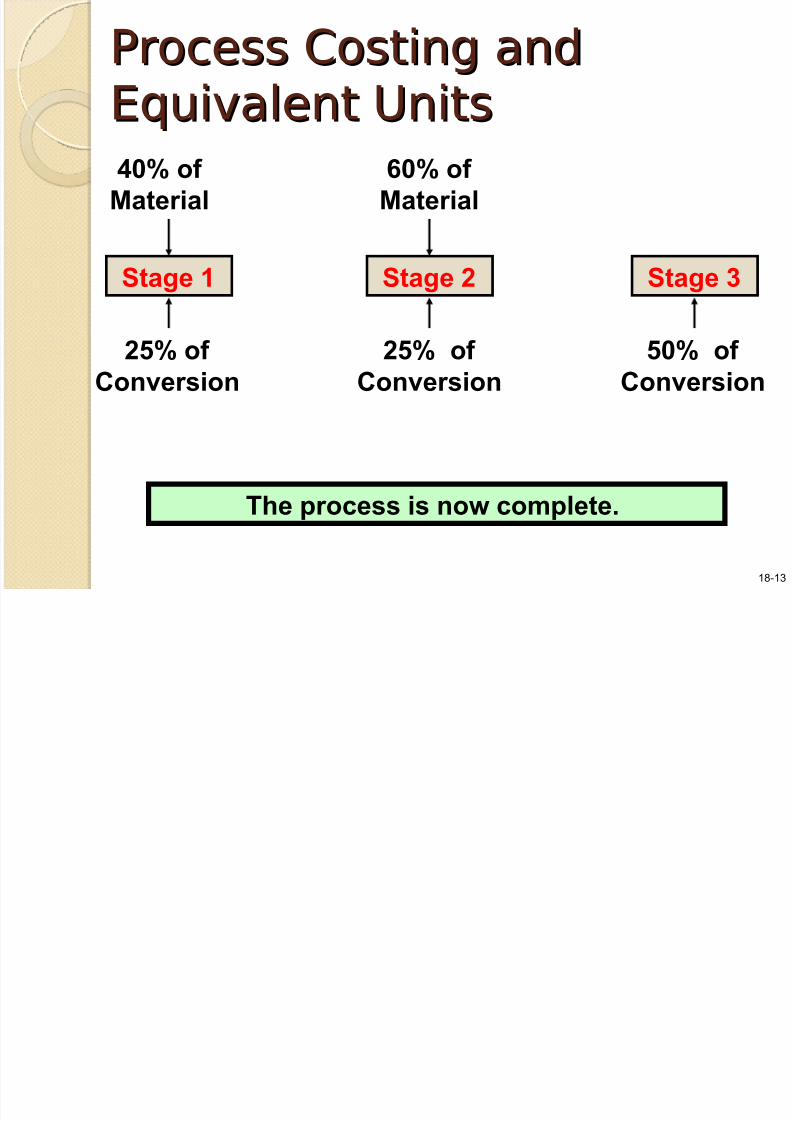

Stage 3

50% of Conversion

The process is now complete.

Stage 2

25% of Conversion

60% of Material

Stage 1

40% of Material

25% of Conversion

Process Costing andProcess Costing andEquivalent UnitsEquivalent Units

18-13

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 14/16

Evaluating DepartmentalEvaluating DepartmentalEfficiencyEfficiency

Only those costs incurred within a department areconsidered for efficiency analysis. Costs transferred

in from other departments should not be allowed to

cloud the picture.

Comparing the current period’s unit costs, for materialand conversion, with budgeted unit costs or with lastperiod’s unit costs are common efficiency measures.

18-14

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 15/16

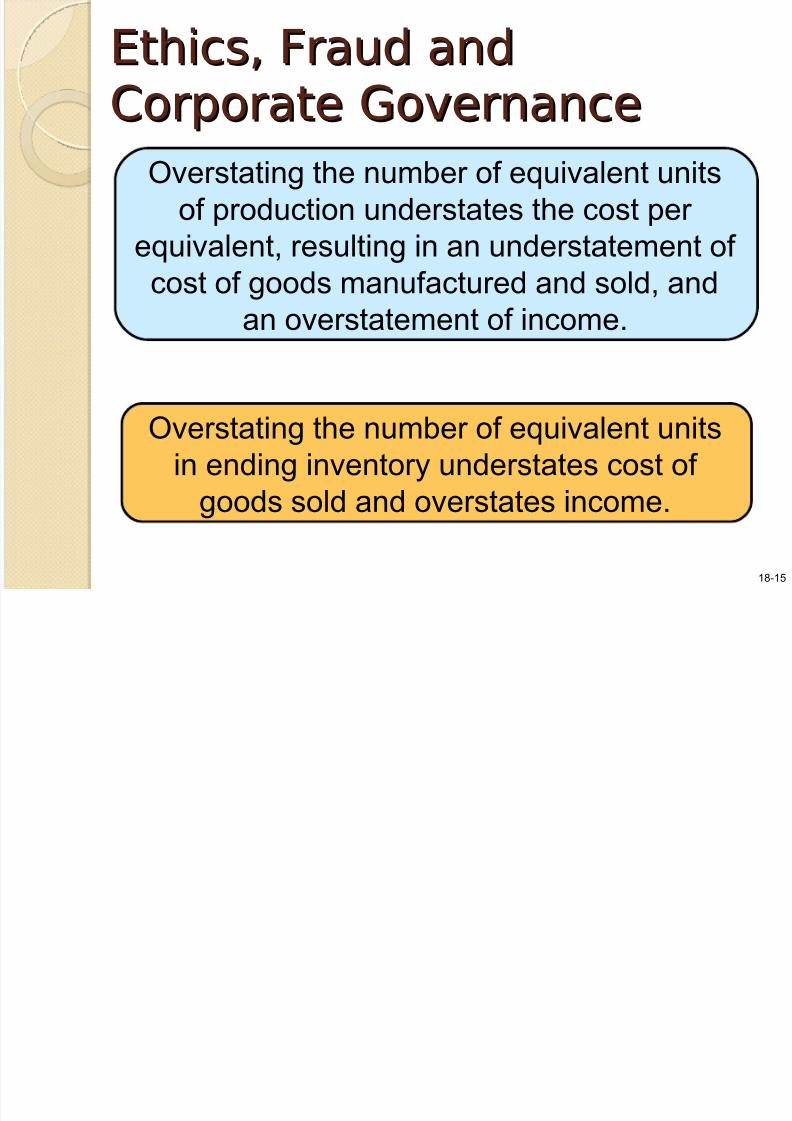

Ethics, Fraud andEthics, Fraud andCorporate GovernanceCorporate Governance

Overstating the number of equivalent unitsof production understates the cost per

equivalent, resulting in an understatement of cost of goods manufactured and sold, and

an overstatement of income.

Overstating the number of equivalent unitsin ending inventory understates cost of

goods sold and overstates income.

18-15

8/14/2019 Financial&managerial accounting_15e williamshakabettner chap 18

http://slidepdf.com/reader/full/financialmanagerial-accounting15e-williamshakabettner-chap-18 16/16

End of Chapter 18End of Chapter 18

18 16