financial study of infosys BPO limited

74

1 EXECUTIVE SUMMARY Financial analysis of the data can be done on the basis of ratio analysis, is one of the techniques of financial analysis to evaluate the financial condition and performance of a business concern. Simply, ratio means the comparison of one figure to other relevant figure or figures. According to Myers, “Ratio analysis of financial statements is a study of relationship among various financial factors in a business as disclosed by a single set of statements and a study of trend of these factors as shown in a series of statements. There are various groups of people who are interested in analysis of financial position of a company. They use the ratio analysis to work out a particular financial characteristic of the company in which they are interested. Ratio analysis helps the various groups in the following Accounting ratio help to measure the profitability of the business by calculating the various profitability ratios. It helps the management to know about the earning capacity of the business concern. In this way profitability ratios show the actual performance of the business. There is no big increase in profitability ratios of Infosys limited but returns are more than last year. In other side Cipla decrease in profitability ratios. In HDFC the profit margin and returns are good. No major change is HPCL profitability ratios. The Infosys is the I.T sector company has more profitability margin as compare to other 4 industry. To work out the solvency: With the help of solvency ratios, solvency of the company can be measured. These ratios show the relationship between the liabilities and assets. In case external liabilities are more than that of the assets of the company, it shows the unsound position of the business. In this case the business has to make it possible to repay its loans.

-

Upload

nitin-gulgulia -

Category

Education

-

view

403 -

download

3

Transcript of financial study of infosys BPO limited

1

EXECUTIVE SUMMARY

Financial analysis of the data can be done on the basis of ratio analysis, is one of the

techniques of financial analysis to evaluate the financial condition and performance of a

business concern. Simply, ratio means the comparison of one figure to other relevant

figure or figures. According to Myers, “Ratio analysis of financial statements is a study of

relationship among various financial factors in a business as disclosed by a single set of

statements and a study of trend of these factors as shown in a series of statements.

There are various groups of people who are interested in analysis of financial position of

a company. They use the ratio analysis to work out a particular financial characteristic of

the company in which they are interested. Ratio analysis helps the various groups in the

following Accounting ratio help to measure the profitability of the business by calculating

the various profitability ratios. It helps the management to know about the earning

capacity of the business concern. In this way profitability ratios show the actual

performance of the business.

There is no big increase in profitability ratios of Infosys limited but returns are more than

last year. In other side Cipla decrease in profitability ratios. In HDFC the profit margin

and returns are good. No major change is HPCL profitability ratios. The Infosys is the I.T

sector company has more profitability margin as compare to other 4 industry. To work

out the solvency: With the help of solvency ratios, solvency of the company can be

measured. These ratios show the relationship between the liabilities and assets. In case

external liabilities are more than that of the assets of the company, it shows the unsound

position of the business. In this case the business has to make it possible to repay its

loans.

2

1.

INTRODUCTION

3

1.1 COMPANY PROFILE

Infosys BPO Ltd., the business process outsourcing subsidiary of Infosys Ltd. Mr. Anup

Upadhyay is CEO and managing director and Mr. Deepak Bhalla is CFO of Infosys BPO.

(NYSE: INFY), was set up in April 2002. Infosys BPO focuses on integrated end-to-end

outsourcing and delivers transformational benefits to its clients through reduced costs,

ongoing productivity improvements, and process reengineering. Infosys BPO operates in

India, Poland, the Czech Republic, the Netherlands, South Africa, Brazil, Mexico, Costa

Rica, the United States, Puerto Rico, China, the Philippines and Australia, and as of

March 31, 2014, employed 28,581 people.

Infosys business solutions and leadership are recognized by several global forums. We

have earned Level 5, the highest rating for the e-Sourcing Capability Model (eSCM–SP:

v2.0) by Carnegie Mellon University's IT Services Qualification Centre (ITSqc). We are

the second company in India and the third globally to receive the certification. Our senior

leaders participate at industry forums such as BPO Strategists, and speak regularly at

leading business schools including Harvard, Wharton and Sloan.

Infosys BPO addresses your business challenges and unlocks business value by applying

proven process methodologies with integrated IT and business process outsourcing

solutions. The company applies business excellence frameworks to significantly reduce

costs, enhance effectiveness, and optimize business processes. The company focuses on

integrated end-to-end outsourcing and delivery of result-oriented benefits to our clients

through reduced costs, ongoing productivity improvements, and process reengineering.

Our business solutions and leadership are recognized by several global forums. We are

consistently ranked among the leading BPO companies in India by industry bodies such

as Global Outsourcing 100 (The International Association of Outsourcing Professionals),

FAO Today, and Nelson Hall.

Infosys BPO has not only pioneered „Business Value Realization‟ (BVR), but has also

emerged as a trusted and valued collaboration partner through consistent focus on

improving process and end-business metrics. We continue to enable realization of

business value, customer satisfaction, and co-creation to sustain long-term partnerships.

4

Infosys BPO take pride in being a consistent performer and are endorsed by industry

analysts, customers (internal and external), and alliance partners. Infosys BPO is a global

company operating in the Americas, the Asia-Pacific, Australia and Europe with more

than 28,581 employees as of March 31, 2014.infosys BPO leverages global delivery

centres to deliver predictable and flexible business process management services. A key

aspect of our service delivery is the successful migration or transition of business

processes from the client‟s locations to our delivery centre(s).

Infosys BPO have a comprehensive and mature transition methodology that has been

refined and documented during the course of more than 1,000 transitions. Compliance is

monitored through check points at different stages. Company believe that a well managed

transition provides a robust foundation for a stable operation across the outsourcing cycle.

LIST OF INDUSTRIES WHERE INFOSYS BPO RENDER SERVICES

1. Communication and service provider

2. Energy and utility

3. Financial services

4. Health care

5. Insurance

6. Manufacturing

7. Media and entertainment

8. Retail, CPG and logistic

9. services

HISTORY

The company was started as Progeon Limited in April 2002 and is today amongst the

top BPOs in India according to NASSCOM. It was started as a 74% and 26% joint

venture between Infosys and Citibank Investments. In 2006, Infosys bought out Citibank's

share at a price of Rs. 592 per share, Citibank having invested at Rs 0.20 per share.

5

OPERATION

Infosys BPO operates in India, Canada, Czech Republic, Netherlands, United Kingdom,

Poland, Mexico, Brazil, USA, China, the Philippines, Japan, Australia and Costa Rica. It

is headquartered in Bangalore, India. About 60% business of Infosys BPO comes from

overlapping clients with the parent Infosys Ltd. During the FY 2013-14, it earned 48% of

its revenue from North America, 34% from Europe, 4% from India and remaining 14%

from other parts of the world. The proportion of voice and non-voice related revenue was

11:89 in the same financial year.

Main client of Infosys BPO limited are Apple Inc, Hyundai, ministry of finance, income

tax department of India, British telecom, staples limited, state bank of India etc.

LOCATION

Bangalore, India

Chennai, India

Gurgaon, India

Hyderabad, India

Jaipur, India

Pune, India

Belo Horizonte, Brazil

Dalian, China

Hangzhou, China

San José, Costa Rica [5]

Brno, Czech Republic

Prague, Czech Republic

Monterrey, Mexico

Eindhoven, Netherlands [6]

Manila, Philippines

Łódź, Poland

Johannesburg, South Africa

Atlanta, USA

Des Moines, USA [7]

Milwaukee, USA

6

VISION, MISSION, VALUE

"To be a globally respected corporation."

There are some companies who are striving for profit making. For Infosys BPO limited

it‟s not the prime vision to be a highly profit making company. The core objective is to be

a globally respected company. The company is following his own practical approach

toward reaching the core vision. Infosys BPO is using three R approach to reach at his

vision. Three R stand for

Reach

Respect

Relevance

MISSION

"Strategic Partnerships for Building Tomorrow‟s Enterprise."

VALUE

Believe that the softest pillow is a clear conscience. The values that drive us underscore

our commitment to: CLIFE

Client Value: To surpass client expectations consistently.

Leadership by Example: To set standards in our business and transactions and be an

exemplar for the industry and ourselves.

Integrity and Transparency: To be ethical, sincere and open in all our transactions.

Fairness: To be objective and transaction-oriented, and thereby earn trust and respect.

Excellence: To strive relentlessly, constantly improve ourselves, our teams, our services

and products to become the best.

7

1.2 OBJECTIVE

1) How organization can earn most possible return on investment.

2) Assessment of operational efficiency.

3) Analysis of past year financial performance forecasting of various financial and

accounting factor like GP,NP, ratio

4) To find out future trend by study of past data

5) How company can maximize value of shareholder and to find how risky or

riskless is to invest in company

8

1.3 RESEARCH METHODOLOGY

TYPE OF RESEARCH

Project is prepared with consideration of both quantitative and qualitative based research.

At a time it may be treated as exploratory research. As a finance project research is more

likely based in quantitative method hence quantitative theorem is explained more clearly.

DATA SOURCE

SECONDARY DATA

The research is based on secondary data and the data is collected from

various website, journals, magazines, articles and previous research paper.

9

1.4 LIMITATION

Some data were confidential therefore were not available for analysis.

Time and resource were a limiting factor.

Research is fully based on secondary data, there is no primary data hence

there may be mismatch between theory and practical implementation.

Continues previous four year data has been considered for this research

report.

Variance in analysis due to change in accounting and taxation policy lead

to improper analysis.

10

2.

LITERATURE REVIEW

11

2.1 LITERATURE REVIEW

Financial statement analysis:

Financial analysis is the process of identifying the strengths and weakness of the firm

with the help of accounting information provided in the Profit and Loss Account and

Balance Sheet. It is the process of evaluation of relationship between component parts of

financial statements to obtain a better understanding of the firm‟s position and performance.

Financial statement analysis (or financial analysis) is the process of reviewing and analyzing a company's

financial statements to make better economic decisions. These statements include the income

statement, balance sheet, statement of cash flows, and a statement of retained earnings. Financial

statement analysis is a method or process involving specific techniques for evaluating risks, performance,

financial health, and future prospects of an organization.

It is used by a variety of stakeholders, such as credit and equity investors, the government, the public, and

decision-makers within the organization. These stakeholders have different interests and apply a variety

of different techniques to meet their needs. For example, equity investors are interested in the long-term

earnings power of the organization and perhaps the sustainability and growth of dividend payments.

Creditors want to ensure the interest and principal is paid on the organizations debt securities (e.g., bonds)

when due.

Common methods of financial statement analysis

Fundamental analysis

Technical analysis

DuPont analysis

Horizontal and vertical analysis

Financial ratios analysis

All method of financial statement analysis we will discuss in more depth.

12

2.2 FUNDAMENTAL ANALYSIS

Fundamental analysis of a business involves analyzing its financial statements and health,

its management and competitive advantages, and its competitors and markets. When

applied to futures and forex, it focuses on the overall state of the economy, and considers

factors including interest rates, production, earnings, employment, GDP, housing,

manufacturing and management. When analyzing a stock, futures contract, or currency

using fundamental analysis there are two basic approaches one can use; bottom up

analysis and top down analysis. The term is used to distinguish such analysis from other

types of investment analysis, such as quantitative and technical analysis.

Fundamental analysis is performed on historical and present data, but with the goal of

making financial forecasts. There are several possible objectives:

To conduct a company stock valuation and predict its probable price evolution,

To make a projection on its business performance,

To evaluate its management and make internal business decisions,

To calculate its credit risk.

The fundamental school of thought appraised the intrinsic value of

share through

Economic analysis: The level of economic activity has an impact on investment

in many ways. If the economy grows rapidly, the industry can also be expected to

grow rapidly and vice versa, hence there is positive correlation between economy

and industry.

Several factor affect the situation and earning of organisation like GDP,

saving and investment, inflation, interest rates, budget, tax structure, BOP,

monsoon, infrastructure, demographic factor, economic forecasting, economic

indicator etc.

Industry analysis: An industry is a group of firms that have similar technological

structure of production and produce similar product. Industry is classified as

growth industry, cyclical industry, defensive industry, cyclical growth industry.

13

Stages of industry life cycle: pioneering stage, rapid growth stage, maturity and

stabilisation stage, declining stage.

Company analysis: In the company analysis the investor assimilates the several

bits of information related to the company and evaluates the present and future

values of stock. The risk and return associated with the purchase of the stock is

analysed to take better decision.

The valuation process depends upon the investors‟ ability to elicit

information from the relationship and interrelationship among the company

related variable. The present and future values are affected by a number of factor

and they are given below.

Factor affects future price- Competition, earning, capital structure, management,

operating efficiency, financial performance etc.

Factor affect present price- Historic price of stock, P/E ratio, economic

condition, stock market condition etc.

14

2.3 TECHNICAL ANALYSIS

Technical analysis is a process of identifying trend reversal at an earlier stage to

formulate the buying and selling strategy. With the help of several indicators we will

analysis relationship between price volume and supply demand for the overall market and

for individual stock.

ASSUMPTION

1. Market value of scrip is determined by the interaction of supply and demand.

2. The market discounts everything.

3. Market always moves in trend except for some deviation. Trend may be of

increasing and decreasing.

TECHNICAL TOOLS

TREND- in this research trend refers to direction of movement. Price can either increase

or decrease. When trend do deviate it may be called as trend reversal. When trend

increase its called as bull market and when trend decrease it‟s called as bear market.

Further I will divide trend in three different type according to nature.

PRIMARY TREND-each peak remain higher the previous peak and bottom also remain

higher than previous bottom.

SECONDARY TREND-the secondary trend or the intermediate trend moves against the

main trend lead to correction. In the bull market the secondary trend would result in the

fall of about 33-66% of earlier rise. In bear market, the trend carries a price upward and

corrects the main trend. The correction would be 33-66% again.

MINOR TREND-also called as random wriggles. Minor trend tries to correct the

secondary trend movement.

INDICATOR-technical indicators are used to find out the direction of the overall market.

Aggregate forecasting is considered to be more reliable than the individual forecasting.

15

Volume of trade, breadth of market, short sales, odd lot trading, moving average, index

comparison, relative strength, oscillators, graph, chart etc are indicator.

2.4 DuPont ANALYSIS

A method of performance measurement that was started by the DuPont Corporation in the

1920.With this method, assets are measured at their gross book value rather than at net

book value in order to produce a higher return on equity (ROE). It is also known as

"DuPont”.

DuPont analysis tells us that ROE is affected by three things:

1.Operating efficiency, which is measured by profit margin.

2. Asset use efficiency, which is measured by total asset turnover.

3. Financial leverage, which is measured by the equity multiplier.

ROA and ROE ratio

The return on assets (ROA) developed by DuPont for its own use is now used by many

firms to evaluate how effectively assets are used. It measures the combined effects of

profit margins and assets turnover.

ROA= 𝑵𝑬𝑻 𝑰𝑵𝑪𝑶𝑴𝑬 ÷ 𝑻𝑶𝑻𝑨𝑳 𝑺𝑨𝑳𝑬𝑺

The return on equity ratio is measure of the rate of return to stockholders.

ROE= NET INCOME ÷ EQUITY

Why DuPont:

The DuPont Analysis is important determines what is driving a company's ROE; Profit

margin shows the operating efficiency, asset turnover shows the asset use efficiency,

and leverage factor shows how much leverage is being used.

The method goes beyond profit margin to understand how efficiently a company's assets

generate sales or cash and how well a company uses debt to produce incremental returns.

16

Using these three factors, a DuPont analysis allows analysts to dissect a company,

efficiently determine where the company is weak and strong and quickly know what areas

of the business to look at (i.e., inventory management, debt structure, margins) for more

answers. The measure is still broad, however, and is not a substitute for detailed analysis.

The DuPont analysis looks uses both the income statement as well as the balance sheet to

perform the examination. As a result, major asset purchases, acquisitions, or other

significant changes can distort the ROE calculation. Many analysts use average assets and

shareholders' equity to mitigate this distortion, although that approach assumes the

balance sheet changes occurred steadily over the course of the year, which may not be

accurate either

17

2.5 HORIZONTAL AND VERTICAL ANALYSIS

HORIZONTAL ANALYSIS:

Horizontal analysis (also known as trend analysis) is a financial statement analysis

technique that shows changes in the amounts of corresponding financial statement items

over a period of time. It is a useful tool to evaluate the trend situations.

The statements for two or more periods are used in horizontal analysis. The earliest

period is usually used as the base period and the items on the statements for all later

periods are compared with items on the statements of the base period. The changes are

generally shown both in dollars and percentage.

Dollar and percentage changes are computed by using the following formulas:

Horizontal analysis may be conducted for following sources

Balance sheet

Income statement

Schedules of current and fixed assets

And statement of retained earnings

18

VERTICAL ANALYSIS:

Vertical analysis (also known as common-size analysis) is a popular method of financial

statement analysis that shows each item on a statement as a percentage of a base figure

within the statement.

To conduct a vertical analysis of balance sheet, the total of assets and the total of

liabilities and stockholders‟ equity are generally used as base figures. All individual

assets (or groups of assets if condensed form balance sheet is used) are shown as a

percentage of total assets. The current liabilities, long term debts and equities are shown

as a percentage of the total liabilities and stockholders‟ equity.

To conduct a vertical analysis of income statement, sales figure is generally used as the

base and all other components of income statement like cost of sales, gross profit,

operating expenses, income tax, and net income etc. are shown as a percentage of sales.

In a vertical analysis the percentage is computed by using the following formula:

A basic vertical analysis needs an individual statement for a reporting period but

comparative statements may be prepared to increase the usefulness of the analysis.

19

2.6 RATIO ANALYSIS

Ratio analysis is one of the techniques of financial analysis to evaluate the financial

condition and performance of a business concern. Simply, ratio means the comparison of

one figure to other relevant figure or figures. According to Myers , “Ratio analysis of

financial statements is a study of relationship among various financial factors in a

business as disclosed by a single set of statements and a study of trend of these factors as

shown in a series of statements."

Classification of ratio:

1. Liquidity ratio

2. Profitability ratio

3. Activity/turnover ratio

4. Solvency ratio

5. Balance sheet ratio

2.5.1 LIQUIDITY RATIO

Liquidity ratios are probably the most commonly used of all the business ratios. Creditors

may often be particularly interested in these because they show the ability of a business to

quickly generate the cash needed to pay outstanding debt. Liquidity ratios are sometimes

called working capital ratios because that, in essence, is what they measure. The liquidity

ratios are: the current ratio and the quick ratio.

Often liquidity ratios are commonly examined by banks when they are evaluating a loan

application. Once you get the loan, your lender may also require that you continue to

maintain a certain minimum ratio, as part of the loan agreement. A 1:1 is considered as

satisfactory ratio.

The quick ratio measures a company's ability to meet its short-term obligations with its

most liquid assets. The higher the quick ratio better will be the position of the company.

A 2:1 is considered as satisfactory ratio.

CURRENT RATIO = CA ÷ CL

QUCIK RATIO = CA – INVENTORIES ÷ CL

20

2.5.2 PROFITABILITY RATIO

Profitability ratios measure the efficiency of management in the employment of business

resources to earn profits. These ratios indicate the success or failure of a business

enterprise for a particular period of time. Profitability ratios are used by almost all the

parties connected with the business. A strong profitability position ensures common

stockholders a higher dividend income and appreciation in the value of the common stock

in future. Creditors, financial institutions and preferred stockholders expect a prompt

payment of interest and fixed dividend income if the business has good profitability

position. Management needs higher profits to pay dividends and reinvest a portion in the

business to increase the production capacity and strengthen the overall financial position

of the company.

GROSS PROFIT RATIO = GROSS PROFIT ÷ NET SALES X 100

OPERATING PROFIT RATIO

= COST OF GOODS SOLD + OPERATING EXPENSES ÷ NET SALES X 100

EXPENSES RATIO = PARTICULAR EXPENSES ÷ NET SALES X 100

NET PROFIT RATIO = NET PROFIT AFTER TAX ÷ NET SALES X 100

2.5.3 TURNOVER/ ACTIVITY RATIO

Activity ratios (also known as turnover ratios) measure the efficiency of a firm or

company in generating revenues by converting its production into cash or sales. Generally

a fast conversion increases revenues and profits.

Activity ratios show how frequently the assets are converted into cash or sales and,

therefore, are frequently used in conjunction with liquidity ratios for a deep analysis of

liquidity.

INVENTORY TURNOVER RATIO = NET SALES ÷ AVERAGE INVENTORY

RECEVABLE TURNOVER RATIO / DEBTOR TURNOVER RATIO

= NET CREDIT ANNUAL SALES ÷ AVG. TRADE DEBTOR

(Where, trade debtor is sundry debtor and B/R)

21

AVERAGE COLLECTION PERIOD

= AVERAGE TRADE DEBTOR ÷ SALES PER DAY

(Where, sales per day= net sales ÷ No. of working day)

PAYABLE TURNOVER RATIO/ CREDITOR TURNOVER RATIO

= NET CREDIT ANNUAL PURCHASE ÷ AVERAGE TRADE DEBTOR

AVERAGE PAYMENT PERIOD RATIO

= AVERAGE TRADE CREDITOR ÷ AVERAGE DAILY PURCHASE

WORKING CAPITAL TURNOVER RATIO

= COST OF SALES ÷ AVERAGE WORKING CAPITAL

(Where, average working capital = opening w/c + closing w/c ÷ 2)

2.5.4 SOLVENCY RATIO

Solvency ratios (also known as long-term solvency ratios) measure the ability of a

business to survive for a long period of time. These ratios are very important for

stockholders and creditors.

Solvency ratios are normally used to:

Analyze the capital structure of the company

Evaluate the ability of the company to pay interest on long term borrowings

Evaluate the ability of the company to repay principal amount of the long term

loans (debentures, bonds, medium and long term loans etc.).

Evaluate whether the internal equities (stockholders‟ funds) and external equities

(creditors‟ funds) are in right proportion.

DEBT-EQUITY RATIO = OUTSIDERS FUNDS ÷ SHAREHOLDERS FUND

DEBT TO EQUITY RATIO = EXTERNAL EQUTIES ÷ INTERNAL EQUITIES

22

PROPRIETORY/EQUITY RATIO = SHAREHOLDERS FUND ÷ TOTAL ASSETS

SOLVENCY RATIO = TOTAL LIABILITIES ÷ TOTAL ASSETS

FIXED ASSETS TO NETWORTH RATIO = F.A ÷ SHAREHOLDERS FUND

(Where, shareholders fund include equity share capital, preference share capital, capital reserve,

revenue reserve, reserve and surplus, accumulated profit, contingency sinking fund etc.)

23

3.

FINDINGS

24

3.1 FUNDAMENTAL ANALYSIS

3.1.1 ECONOMIC ANALYSIS:

The Indian economy is the fourth largest economy of the world on the basis of Purchasing

Power Parity (PPP). It is one of the most attractive destinations for business and

investment opportunities due to huge manpower base, diversified natural resources and

strong macro-economic fundamentals. Also, the process of economic reforms initiated

since 1991 has been providing an investor-friendly environment through a liberalized

policy framework spanning the whole economy.

The growth and performance of the Indian economy in the world market is explained in

terms of statistical information provided by the various economic parameters. For

example, Gross National Product (GNP), Gross Domestic product (GDP), Net National

Product (NNP), rate of inflation, per capita income, Gross Domestic Capital Formation

(GDCF), etc. are the various indicators relating to the national income sector of the

economy. They provide a wide view of the economy including its productive power for

satisfaction of human wants.

TREND IN ECONOMIC

Figure 1

10.3

6.6

4.7 5

7.6

10.7

9.3

5.115.7

7.2

5.6

0.390

2

4

6

8

10

12

2011 2012 2013 2014

Rat

e

trend in economy

GDP

CPI

WPI

25

Interpretation: for the past four year GDP showed both upward and downward

movement. But ultimately it reduced by fifty percent from 10.5% to 5%. Consumer price

inflation showed overall down movement from 7.6 to 5.11. and wholesale price index

lowered by more than 90% from 5.7 to .39.

GDP: The Gross Domestic Product (GDP) in India expanded 7.50 percent in the fourth

quarter of 2014 over the same quarter of the previous year. GDP Annual Growth Rate in

India averaged 5.83 percent from 1951 until 2014, reaching an all time high of 11.40

percent in the first quarter of 2010 and a record low of -5.20 percent in the fourth quarter

of 1979. GDP Annual Growth Rate in India is reported by the Ministry of Statistics and

program Implementation (MOSPI)

INFLATION RATE: The inflation rate in India was recorded at 5.11 percent in January

of 2015. Inflation Rate in India averaged 8.87 percent from 2012 until 2015, reaching an

all time high of 11.16 percent in November of 2013 and a record low of 4.38 percent in

November of 2014. Inflation Rate in India is reported by the Ministry of Statistics and

Program Implementation (MOSPI), India

CONSUMER PRICE INDEX: Consumer Price Index CPI in India remained unchanged

at 119.40 Index Points in January of 2015 from 119.40 Index Points in December of

2014. Consumer Price Index CPI in India averaged 125.38 Index Points from 2011 until

2015, reaching an all time high of 145.50 Index Points in November of 2014 and a record

low of 105 Index Points in February of 2011. Consumer Price Index CPI in India is

reported by the Ministry of Statistics and Program Implementation (MOSPI), India.

WHOLESALE PRICE INDEX: the wholesale price index (WPI) is the main measure of

inflation. The WPI measures the price of a representative basket of wholesale goods. In

India, wholesale price index is divided into three groups: Primary Articles (20.1 percent

of total weight), Fuel and Power (14.9 percent) and Manufactured Products (65 percent).

Food Articles from the Primary Articles Group account for 14.3 percent of the total

weight. The most important components of the Manufactured Products Group are

Chemicals and Chemical products (12 percent of the total weight); Basic Metals, Alloys

and Metal Products (10.8 percent); Machinery and Machine Tools (8.9 percent); Textiles

26

(7.3 percent) and Transport, Equipment and Parts (5.2 percent). Content for - India

Wholesale Price Index Change - was last refreshed on Monday, February 23, 2015.

Producer Prices in India decreased 0.39 percent in January of 2015 over the same month

in the previous year. Producer Prices Change in India averaged 7.63 percent from 1969

until 2014, reaching an all time high of 34.68 percent in September of 1974 and a record

low of -11.31 percent in May of 1976. Producer Prices Change in India is reported by the

Office of the Economic Advisor, India.

3.1.2 INDUSTRY ANALYSIS:

According to NASSCOM, in fiscal year 2014, India‟s information technology and

business process management (IT-BPM) industry will add $12-15 billion incremental

revenue, to existing industry revenues of $118 billion. During FY 2014, industry‟s

exports are estimated to grow 13 per cent at $86 billion, with domestic revenues up 9.7

per cent at Rs. 1,910 billion. NASSCOM reports also stated that the industry added

160,000 employees in 2013, and provided direct employment to 3.1 million people and

indirect employment to 10 million people.

Exports by India's IT outsourcing sector are expected to rise 13-15 percent in the fiscal

year starting April 2014, as an improving global economy encourages banks and

companies to boost spending on technology. NASSCOM has forecasted IT services

exports in 2014-15 to rise to as much $99 billion. The increase in growth rate compares

with an estimated 13 percent rise in fiscal year 2014. It also states that the Indian IT and

ITeS industry is likely to grow to about $300 billion by 2020, focusing on areas like e-

commerce, software products and the IT market.

Why is the sector growing?

Rapid industrialization and growth of IT parks in the country

Partial privatization of telecommunication

Development of SEZ; which also help IT companies get tax benefits

A large number of resource readily available in the country

Low operating costs

Tax breaks and sops offered by the government

27

Employment Trends

The IT and ITeS sector has generated massive employment in the past and continues the

trend of providing jobs. With online shopping, social media and cloud computing

flourishing more than ever before, there is great demand for IT professionals in e-

commerce and business to consumer firms.

3.1.3 COMPANY ANALYSIS:

Infosys overview: Infosys BPO, the business process outsourcing subsidiary of Infosys

(BSE, NSE, NYSE: INFY), is an end-to-end outsourcing services provider. Infosys BPO

addresses the business challenges and unlocks business value by applying proven process

methodologies with integrated IT and business process outsourcing solutions. The

company applies business excellence frameworks to significantly reduce costs, enhance

effectiveness, and optimize business processes. The company focuses on integrated end-

to-end outsourcing and delivery of result-oriented benefits to our clients through reduced

costs, ongoing productivity improvements, and process reengineering.

Our business solutions and leadership are recognized by several global forums. We are

consistently ranked among the leading BPO companies in India by industry bodies such

as Global Outsourcing 100 (The International Association of Outsourcing Professionals),

FAO Today, and Nelson Hall.

STRENGTH:

Pricing power: Customers typically rebel against price increases by switching to

competing products, but if a company has pricing power, customers will continue using

Infosys BPO‟s products and services. Infosys BPO has the ability to charge customers

higher prices

Financial leverage: financial leverage allows company to expand their assets year by

year.

Cost saving: Lower costs lead to higher profits for Infosys BPO. A low cost leader can

undercut rivals on price.

28

SWOT ANALYSIS:

Strength

Pricing power

Financial leverage

Cost saving

Economies of scale

Faster technology

3R approach

Creation of leader

Weakness

High staff turnover

Online presence

Weak supply chain

Weak management

Weak customer service

Past scam

Frequent changes in senior position

Opportunity

Financial leverage

Innovation

Emerging technology

New market

International expansion

Threat

Mature market

Intense competition

Political risk

Substitute project

Competitive edge

Table 1.

Economies of scale: Economies of scale is the cost advantages that Infosys BPO obtains

due to size. The greater the volume, the greater the advantage

Faster technology: technology used in Infosys is always one step ahead to others. It

provides latest technological based solution to client.

3R approach: Infosys serve client on the basis of 3R approach. Reach, relevance, respect

are the three component they take care about client,

29

Creation of leader: Infosys limited has his own corporate university to develop the skills

of employee. As per the client requirement they create the flexible leader.

WEAKNESS

Past scam: in 2014 there is lot of scam happen in Infosys BPO. That hurts the image and

value of reputed company.

Frequently change in senior position: changing senior position manager lead to

diversion of mission and value. Infosys BPO‟s senior level management is changing

frequently from last two year.

High staff turnover: High staff turnover can hurt Infosys BPO‟s ability to compete,

because replacing valuable staff is expense "High Staff Turnover (Infosys BPO )" has a

significant impact, so an analyst should put more weight into it.

Online presence: The online market is essential for displaying information and selling

products. A weak online presence can result in lost opportunities for Infosys BPO.

Weak supply chain: A weak supply chain can delay the arrival of products to Infosys

BPO‟s customers. Unnecessary delays can hurt Infosys BPO over the long run, because

customers will cancel orders.

Weak management: Weak management increases business risks and reduces profits for

Infosys BPO, because they are responsible for the health of the business.

Weak customer service: Weak management increases business risks and reduces profits

for Infosys BPO, because they are responsible for the health of the business.

OPPORTUNITY

Financial leverage: Leveraging the balance sheet allows Infosys BPO to quickly expand

into other markets and products, especially in fragmented industries.

30

Innovation: Greater innovation can help Infosys BPO to produce unique products and

services that meet customer‟s needs.

Emerging technology: Greater innovation can help Infosys BPO to produce unique

products and services that meet customer‟s needs.

New market: Emerging markets are fast growing regions of the world that enable Infosys

BPO to quickly expand.

International expansion: International markets offer Infosys BPO new opportunities to

expand the business and increase sales.

THREAT

Mature market: Mature markets are competitive. In order for Infosys BPO to grow in a

mature market, it has to increase market share, which is difficult and expensive.

Intense competition: Intense completion can lower Infosys BPO‟s profits, because

competitors can entice consumers away with superior products.

Political risk: Politics can increase Infosys BPO‟s risk factors, because governments can

quickly change business rules that negatively affect Infosys BPO‟s business "Political

Risk has a significant impact, so an analyst should put more weight into it. This statement

will lead to a decrease in profits.

Substitute product: The availability of substitute products hurts Infosys BPO‟s ability to

raise prices, because customers can easily switch to another product or service.

Competitive edge: there is a wide competition in IT and BPO industry. Price cutting is

not only solution for competitive market.

31

EARNING: Infosys BPO has earned revenue of 2,323 crore in financial year 2013-14 as

compared to 1,831 crore in financial year 2012-13. The company ended year with net

profit after tax of ` 512 crore when compared with the previous year of ` 428 crore. The

company‟s profitability after tax for the year is 22.04%. The company continues to be

amongst the most profitable BPO companies in India. The company added 6 (net)

customers and now has 150+ customers as on March 31, 2014. The company ended the

year with 28,658 employees having added 2,855 (net) employees during the year.

SHARE CAPITAL: During the year under review, the company has not issued any

shares and hence the outstanding issued, subscribed and paid-up equity share capital

stands at 33.83 Crore as on March 31, 2014 (33.83 Crore as on March 31, 2013). No

Employee Stock Options were granted and vested during the year.

SUBSIDIARIES:

Infosys BPO have five subsidiaries, namely- Infosys BPO s.r.o, Infosys BPO Poland Sp.

Z.o.o, Infosys McCamish Systems LLC , Portland Group Pty Ltd, and Infosys BPO S. de

R.L. de C.V.

A. Infosys BPO s.r.o

The financial year was a year of growth. We expanded the customer service portfolio

significantly. New lines of business were added and the subsidiary recruited 200+ new

employees. The second half of the year saw the start of an exciting engagement with a

reputed US-based financial institution, where the subsidiary assists the client to enter the

European market. Throughout the year, the Company‟s F&A operations have performed

well on operational parameters.

During the year under review the company generated revenue of ` 113.84 crore as against

a revenue of ` 89.54 crore for the year ended on March 31, 2013 with a loss of 2.56 crore

against the loss of ` 2.67 crore for the year ended on March 31, 2013.

B. Infosys BPO Poland Sp.Z.o.o

The centre continues to grow with existing and new clients (three new projects started in

this fiscal year), focusing on high-end services (Tax, SOX Compliance, FP&A reporting

and analysis, FP&A Consolidation of financial statements, BTS, onsite project work) as

32

well as European language based services as part of Infosys global delivery model. The

Center provides Business Transformation Services for local market companies and is

looking for opportunities to provide BPO services to those companies.

C. Infosys McCamish Systems LLC

During the financial year, the name of the subsidiary company was changed from

McCamish Systems LLC to Infosys McCamish Systems LLC. The Financial year 2014

for Infosys McCamish has been a turnaround year. Significant investment in the first half

of the year were made for the integration of the Des Moines operation which, not only

provided six new marquis logos, but also establishes our footprint in a new line of

business, Employer Sponsored Markets. With the majority of the Des Moines transition

complete, the company expects to finish it by Q2 of FY 15. Significant cost restructuring,

which began in earnest in the middle of the year, has greatly improved the company‟s

financial performance. During this year Infosys McCamish Life Insurance Platform was

recognized as a leader in Gartner's Magic Quadrant.

During Financial Year 2014 the company has generated revenue of ` 324.11 crore as

compared to ` 261.18 crore in the prior year with a profit of ` 7.47 crore as against the

prior year loss of ` 15.90 crore.

D. Portland Group Pty Limited

Portland Group had a strong financial year. There were large / multi-year joint deals sold

and delivered with Infosys Limited and Infosys BPO Limited. The keys financial points

are Revenue growth of 16% and Operating margin (after tax) of 15%.

There was also significant growth in the offshore team with a headcount increase of 58

(28 at 31 March 2013 to 86 as at 31 March 2014), with growth expected to continue. The

start of Financial Year 2015 is off to a promising start with a number of large deals being

sold and also the continuation of the joint deals sold between Portland Group and Infosys.

During the year under review the company generated revenue of ` 212.40 crore as against

a revenue of ` 181.93 crore for the year ended on March 31, 2013 with a profit of ` 22.10

crore against the profit of ` 0.61 crore for the year ended on March 31, 2013.

33

E. Infosys BPO S. de. R.L. de C.V.

During the financial year under review, Infosys have incorporated a subsidiary in Mexico

in the name and style of Infosys BPO S. de. R.L. de C.V. The subsidiary is yet to

commence business operations.

The Company has published the audited consolidated financial statements for the fiscal

year 2014 and the same forms part of this Annual Report. Accordingly, this project

Report does not contain the financial statements of Infosys subsidiaries. The audited

financial statements and related information of subsidiaries are available on company

website, www.infosysbpo.com. These documents will also be available for inspection

during business hours at registered office in Bangalore, India.

34

EARNING OF COMPANY: Consolidated Revenues for the year was ` 3,278.49 Cr. as

against ` 2,572.40 Cr. for the previous year. Gross Margin post depreciation for the year

was ` 1,035.47 Cr. compared to ` 794.97 Cr. during the previous year. Net Income for the

current year was ` 577.79 Cr. as compared to ` 458.49 Cr. for the previous year. Gross

Addition to headcount for the year ended March 31, 2014 was 13,092 compared to 12,152

as at the end of the previous year.

Rupees in crore

Table 2

Figure 2.TREND IN REVENUE, COST AND NET PROFIT OVER THE PAST

FOUR YEAR

Rupees in crore

1471.63 1468.71

2572

3278

1014.071117.91

1699

2152

197.43304.98

458578

0

500

1000

1500

2000

2500

3000

3500

2011 2012 2013 2014

REVENUE

COST

PAT

35

Interpretation: all of the above items are continually moving in upward direction that

show that the market response for the company is comparatively much more better.

Compare to year 2011 the revenue is hiked by more than 122%. And cost is increased by

112%. Overall profit is increased by 193%.

FORECASTING OF REVENUE, COST AND PAT OVER UPCOMING TWO

YEAR

There is upward trend in the sales of company as the percentage of net earnings (profit

after tax) to sales also show bit of upward trend except in year 2014. So, if we predict the

outcome of sales for year 2015 and 2016 by trend method we get 3828.18 and 4480.42

crore rupee sales for year 2015 and 2016 respectively.

Rupees in crore

Figure 3.

REVENUE BY GLOBAL PRESENCE: the major revenue of Infosys BPO is generated

from outside of India. Hence it shows the global presence of Infosys BPO in IT and BPO

industry. Domestic revenue contributes less than 1% in term of rupees. And slowly its

going upward year by year. In 2014 revenue from domestic market(India) is 21.10 crore

that is just .64% of 3257.40 crore. Table is given on next page.

1471.63 1468.71

2572

3278

3828.185

4480.425

1014.07 1117.91

1699

2152

2494.465

2893.953

197.43 304.98458

578708.285

837.758

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2011 2012 2013 2014 2015 2016

revenue

cost

pat

36

PARTICULAR 2011 2012 2013 2014

OVERSEAS 1471.63 1761.31 2554.70 3257.40

DOMESTIC 6.28 7.40 17.10 21.10

TOTAL 1477.91 1468.71 2571.80 3278.50

Table 3.

REVENUE BY INDUSTRY SEGMENT: Infosys BPO offers Business process

outsourcing solutions to several clients and its service offerings span across multiple

industry segments. Following is the revenue by industry:-

Figure 4.

Interpretation: Financial services like insurance, banking, mortgage and manufacturing

services cover more than 65% of total revenue. Lowest revenue comes from retail,

consumer, packaged goods, logistic and life science.

30

35

23

12

REVENUE BY INDUSTRY SEGMENT IN %

Financial service &

insurance

Mfg. services

Energy,utilities,communic

ation

Retail,consumer packaged

goods,logistic and life

science

37

3.2TECHNICAL ANALYSIS:

Infosys BPO limited is a subsidiary company of the Infosys technology limited. Hence

the share of Infosys BPO limited is not directly traded in market. Whole earning and fund

ultimately reflect in his holding company Infosys technologies, and Infosys limited is

cover to the entire subsidiary. So where in requirement of technical analysis in project we

will analysis about Infosys as a whole.

Infosys limited is listed company named as INFY in both Bombay stock exchange and

national stock exchange in India.

PAST FIVE YEAR TREND IN INFOSYS SHARE PRICE

In rupees

Time 2011 2012 2013 2014 2015 02/2015

Open 1722 1379 1163 1749 1962 2279

high 1734 1387 1164 1760 1975 2295

low 1713 1365 1138 1740 1956 2257

Pre. close 1729 1371 1143 1742 1966 2272

value 631.1 k 1.1 M 1 M 448.9 K 1.2 M 1.6 M

Table 4

Where;

K= thousand

M= million

Par value= 5 Rs.

By looking at data we can observe that there has been growth in the share prices over the

past five year but in 2012 and 2013 there is continuously decrease in share price. The

reason behind this may be lower economic position. That we can find by observing the

market index both sensex and nifty.

38

TECHNICAL ANALYSIS OF INFOSYS LIMITED

Figure 5

Interpretation: by looking at the graph we can simply draw a conclusion that price for

Infosys share was lower in 2011 to 2012 end. Again in December 2014 share price come

down till 1450 when founder of Infosys limited sell their personal holding. The reason

behind this was to balance the liquidity.

39

MARKET ANALYSIS OF PAST FIVE YEAR: analysis of market can be done with

the help of market index, beta, alpha and risk associated with stock. to complete this

analysis we assume that the risk of Infosys limited is neutral and flow same as market

index.

Analysis of sensex:

time 3Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015

open 20274 15583 19364 21114 29446

high 20410 15694 19465 21235 29462

low 20274 15406 19346 21113 29178

close 20389 15454 19444 21193 29231

value 330 M 164 M 241 M 221 M 398 M

Table 5.

Figure 6.

Comment: from last five year in there is drastically changes in share market. From 2010

to February 2015 sensex show 70% of hike by touching amount of 29400. In 2015 sensex

remains all time high. From 2009 to 2011 sensex show upward and downward

movements

40

Analysis of nifty:

2011 2012 2013 2014 2015

OPEN 6172 4681 5901 6292 8883

HIGH 6181 4701 5919 6324 8913

LOW 6124 4639 5879 6289 8794

CLOSE 6146 4646 5905 6313 8895

Table 6.

In rupees

Figure 7.

Comment: Current market index as on February 25, 2015 was 8811 rs. In past

performance we can observe that year 2009 to 2010 and end of 2011 to mid of 2013

performance of nifty was very low. And after 2013 there is continuously increment in

nifty index.

In 2010 and 2012 there is lowest performance where index come down till 4500. After

2013 nifty index shows pure increment.

41

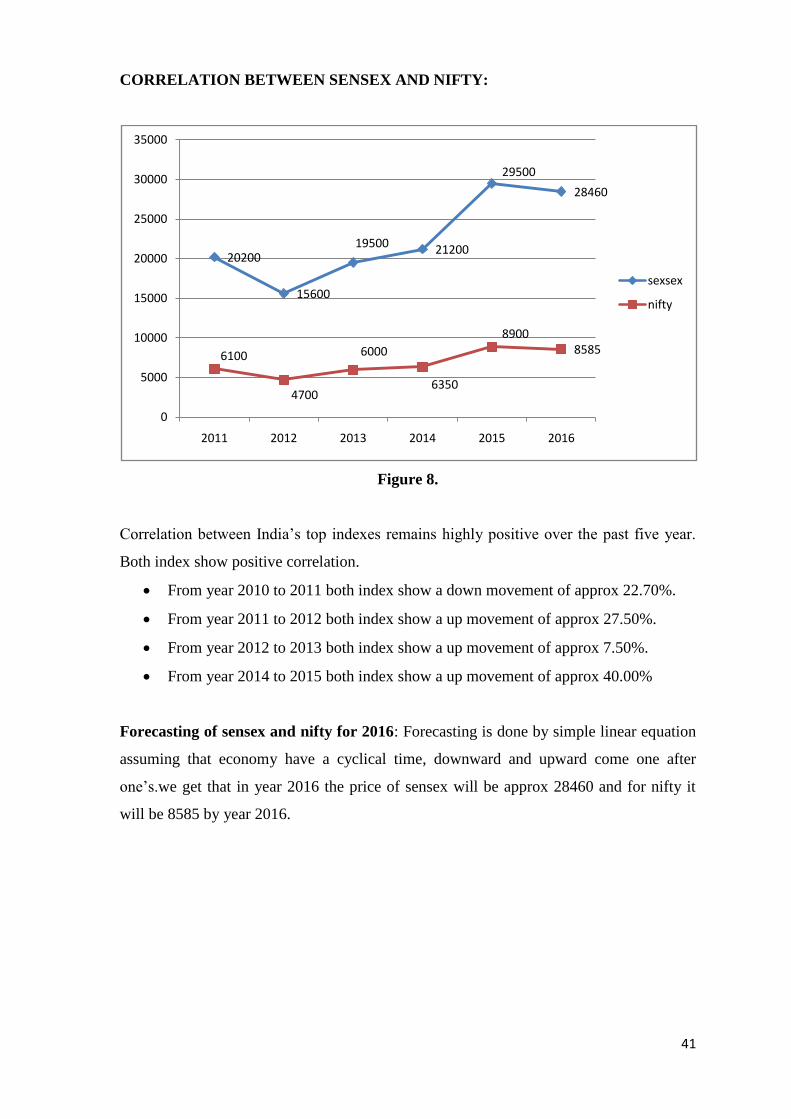

CORRELATION BETWEEN SENSEX AND NIFTY:

Figure 8.

Correlation between India‟s top indexes remains highly positive over the past five year.

Both index show positive correlation.

From year 2010 to 2011 both index show a down movement of approx 22.70%.

From year 2011 to 2012 both index show a up movement of approx 27.50%.

From year 2012 to 2013 both index show a up movement of approx 7.50%.

From year 2014 to 2015 both index show a up movement of approx 40.00%

Forecasting of sensex and nifty for 2016: Forecasting is done by simple linear equation

assuming that economy have a cyclical time, downward and upward come one after

one‟s.we get that in year 2016 the price of sensex will be approx 28460 and for nifty it

will be 8585 by year 2016.

20200

15600

19500 21200

29500

28460

6100

4700

6000

6350

89008585

0

5000

10000

15000

20000

25000

30000

35000

2011 2012 2013 2014 2015 2016

sexsex

nifty

42

PREDICTION OF YEAR 2016 SHARE PRICE:

Figure 9.

As per the announcement by the CEO of Infosys limited Dr. Vishal Sikka, the target price

of one equity share of Infosys is to cross the figure of 3000. If economy and market

remain in growth position it is not a tough task task to attain given figure, statement by

CFO of Infosys limited.

In Q2FY2015 the revenues of Infosys in the reported currency grew by 3.2% QoQ to

$2,201 million (revenues up 3.9% in constant currency terms, volumes up by a decent 3%

and realization up by 0.6% QoQ). On the margin front, the EBIT margin improved by

100BPS to 26.1%, driven by higher utilization and offshore shift. The net income rose by

7.3% QoQ to Rs3,096 crore. Dr. Vishal Sikka has given a strategic roadmap to take

Infosys back to its old way of predictable and sustainable earnings performance in the

coming quarters. Going forward, the emphasis will be on enhancing the service delivery

and product innovation through higher usage of automation, innovation and operational

efficiency, as well as on new technologies like big data analytics and design thinking

among others.

1734

1387

1164

1760

2295

3000

1713

1365

1138

1740

2257

2700

1729

1371

1143

1742

2272 2300

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

2100

2200

2300

2400

2500

2600

2700

2800

2900

3000

3100

2011 2012 2013 2014 2015 2016

open

high

low

previous close

2 per. Mov. Avg. (previous close)

43

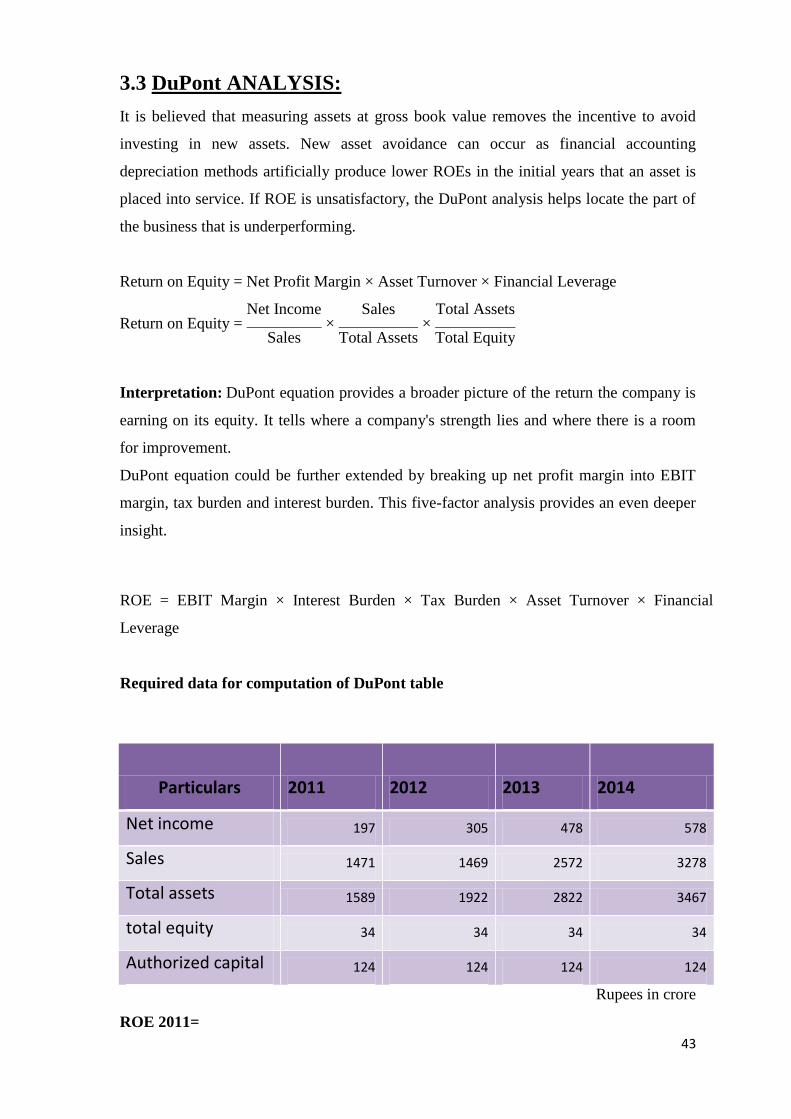

3.3 DuPont ANALYSIS:

It is believed that measuring assets at gross book value removes the incentive to avoid

investing in new assets. New asset avoidance can occur as financial accounting

depreciation methods artificially produce lower ROEs in the initial years that an asset is

placed into service. If ROE is unsatisfactory, the DuPont analysis helps locate the part of

the business that is underperforming.

Return on Equity = Net Profit Margin × Asset Turnover × Financial Leverage

Return on Equity = Net Income

× Sales

× Total Assets

Sales Total Assets Total Equity

Interpretation: DuPont equation provides a broader picture of the return the company is

earning on its equity. It tells where a company's strength lies and where there is a room

for improvement.

DuPont equation could be further extended by breaking up net profit margin into EBIT

margin, tax burden and interest burden. This five-factor analysis provides an even deeper

insight.

ROE = EBIT Margin × Interest Burden × Tax Burden × Asset Turnover × Financial

Leverage

Required data for computation of DuPont table

Particulars 2011 2012 2013 2014

Net income 197 305 478 578

Sales 1471 1469 2572 3278

Total assets 1589 1922 2822 3467

total equity 34 34 34 34

Authorized capital 124 124 124 124

Rupees in crore

ROE 2011=

44

197 ×

1471 ×

1589

1471 1589 34

=5.79%

ROE 2012=

305 ×

1469 ×

1922

1469 1922 34

= 8.97%

ROE 2013=

478 ×

2572 ×

2822

2572 2822 34

=14.05%

ROE 2014=

578 ×

3278 ×

3467

3278 3467 34

= 17.00%

Analysis

Particulars 2011 2012 2013 2014

net profit margin 13.40% 17.20% 17.80% 17.60%

assets turnover 0.92 0.76 0.91 0.94

financial leverage 46.75 56.52 83 101.97

Table 8.

3.4 HORIZONTAL AND VERTICAL ANALYSIS:

45

Consolidated balance sheet of last four year:

Consolidated balance sheet at 2011 2012 2013 2014

Consolidated balance sheet at 2011 2012 2013 2014

Equity and liabilities

Share capital 34 34 34 34

Reserve and surplus 1148 1465 1933 2536

1182 1499 1967 2570

Noncurrent liabilities

Long term provision

Other long term liability 75 70 69 44

75 70 69 44

Current liabilities

Trade payable 5 13 44 7

Other current liabilities 380 428 661 723

Short term provision 42 60 81 123

427 501 786 853

Total 1684 2070 2822 3467

Assets

Non current assets

Fixed assets

Tangible assets 171 248 246 256

Intangible assets 310 477 495 495

Capital work in progress 15 2 3 5

496 727 744 756

Noncurrent investment

3

Deferred tax assets, net 24 25 35 54

Long term loan and advance 108 85 98 110

Other noncurrent assets 24 32 38 47

156 142 171 214

Current assets

Current investment 21 20 151 275

Trade receivable 271 397 548 570

Cash and cash equivalent 567 630 906 1341

Short term loans and advances 123 145 302 311

Other current assets 50 10

1032 1202 1907 2497

46

Table. 9

Trend (Horizontal) analysis of balance sheet:

In %

Figure 10.

For the horizontal analysis year 2011 is been taken as base year as 0%. And share holder

fund include share capital and reserve & surplus. Other liability includes all noncurrent

and current liability. Assets include all kind of assets viz. current assets, noncurrent

assets, noncurrent and current investment.

Highest increment laid for share holder equity as the EPS (earning per share) in 2011

was 61.81 Rs. and for 2014 it touches 170 Rs. Par value of share is Rs. 10 per share.

Vertical analysis of consolidated balance sheet

Rupees in crore

0.00%

26.80%

66.40%

117.42%

0.00%

13.74%

70.30%78.70%

0.00%

22.92%

67.50%

105.87%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

2011 2012 2013 2014

share holder fund

other liability

assets

Total 1684 2070 2822 3467

47

Table 10.

ITEMS 2011 % 2012 % 2013 % 2014 %

EQUITY AND

LIABILITIES

SHARE CAPITAL 34 2.02% 34 1.64% 34 1.20% 34 0.98%

RESERVE AND

SURPLUS 1148 68.17% 1465 70.77% 1933 68.50% 2536 73.15%

1182 70.20% 1499 72.41% 1967 69.70% 2570 74.12%

NON CURRENT

LIABILITIES 75 4.45% 70 3.38% 69 2.44% 44 1.69%

CURRENT

LIABILITIES 427 25.35% 501 24.20% 786 27.85% 853 24.60%

TOTAL 1684 100% 2070 100% 2822 100% 3467 100%

ASSETS

NON CURRENT

ASSETS 496 29.45% 727 53.12% 744 26.36% 756 21.80%

NONCURRENT

INVESTMENT 156 9.26% 142 6.85% 171 6.05% 214 6.17%

CURRENT ASSETS 1032 61.28% 1202 58.06% 1907 67.57% 2497 72.02%

TOTAL 1684 100% 2070 100% 2822 100% 3467 100%

48

CASH AND CASH EQUIVALENTS ITEMS:

The bank balances in India include both Rupee accounts and foreign currency accounts.

The bank balances in overseas current accounts are maintained to meet the expenditure

of the overseas branches and to meet project-related expenditure overseas. The deposit

account represents deposits for short tenures with banks and financial institutions.

Table 11

Consolidated Profit And Loss Account of Past Four Year:

Rupees in crore

consolidated statement of profit

and loss for

year

ended

31,

march

Year

ended

31,

march

Year

ended

31,

march

Year

ended

31,

march

2011 2012 2013 2014

Revenue from business process

management service 1472 1768 2572 3278

Other income 44 53 149 137

Total revenue 1516 1821 2721 3415

49

Expenses

Employee benefit expenses 842 917 1415 1808

Cost of technical subcontractor 76 60 136 185

Travel expenses 66 73 121 127

Cost of software packages 28 25 42 54

Communication expenses 41 32 42 59

Professional charges 28 54 72 63

Other expenses 44 46 56 64

Power and fuel 19 23 28 30

Insurance charges 9 10 11 15

Rent 55 63 87 104

Depreciation expenses 58 60 79 91

Other expenses 28 35 40 66

Total expenses 1294 1400 2129 2666

Profit before tax 222 422 592 749

Tax expenses

Current tax 21 101 147 192

Deferred tax -7 -0.55 -13 -21

14 100 134 171

Profit for the year 209 321 458 578

Earnings per share

Equity share par value of Rs 10 each

Basic 61.81 94.33 135.54 170.8

Diluted 61.81 94.33 135.54 170.8

Weighted Avg. no. Of share used in

computing EPS

Both basic and diluted 33827751 33827751 33827751 33827751

Table 12

50

Vertical analysis of profit and loss statement:

The function wise classification of statement of Profit and Loss account is as follows:

Rupees in crore

Rupees in crore

Table 13

Consolidated Revenues for the year 2014 was ` 3,278.49 Cr. as against ` 2,572.40 Cr. for

the previous year. Gross Margin post depreciation for the year was ` 1,035.47 Cr.

compared to ` 794.97 Cr. during the previous year. Net Income for the current year was `

577.79 Cr. as compared to ` 458.49 Cr. for the previous year. Gross Addition to

headcount for the year ended March 31, 2014 was 13,092 compared to 12,152 as at the

end of the previous year.

51

Revenue segment by industry:

Infosys BPO offers Business process outsourcing solutions to several clients and its

service offerings span across multiple industry segments. Following is the revenue by

industry:-

Table 14

Revenue by geographic segment:

Revenue is also analyzed in terms of the client locations spread across the globe. Infosys

BPO offers services to clients located at different parts of the world, both offshore and

onsite. Revenues by location are:-

Table 15

52

Cash flow statement of year 2014 and 2013

53

Cash flow statement of year 2011 and 2012

Table 16

54

3.5 RATIO ANALYSIS:

LIQUIDITY RATIO: Liquidity ratio determine liquidation position of company. It‟s

a comparative quantitative analysis of current assets to current liability. Past four year

ratio is computed below for Infosys BPO limited.

CURRENT RATIO: Current ratio is the relationship between current asset and

current liability. This ratio is also known as working capital ratio which measures the

other general liquidity and is most widely used to make the analysis of short term

financial position of a firm. It is calculated by dividing the total current asset by total

current liability.

Current Ratio=Current Assets/current Liabilities

A relatively high current ratio is an indication that the firm is liquid and has the ability to

pay its current obligation in time as and when they become due. The rule of thumb is 2:1

i.e. current asset as double the current liability is consider to be satisfactory.

CURRENT RATIO 2011

= 1032÷ 427

= 2.4

CURRENT RATIO 2012=

= 1202 ÷ 501

= 2.4

CURRENT RATIO 2013=

= 1907 ÷ 786

= 2.4

CURRENT RATIO 2014=

= 2497 ÷ 853

= 2.9

55

Significance and interpretation

Current ratio is a useful test of the short-term-debt paying ability of any business. A ratio

of 2:1 or higher is considered satisfactory for most of the companies but analyst should be

very careful while interpreting it. Simply computing the ratio does not disclose the true

liquidity of the business because a high current ratio may not always be a green signal. It

requires a deep analysis of the nature of individual current assets and current liabilities. A

company with high current ratio may not always be able to pay its current liabilities as

they become due if a large portion of its current assets consists of slow moving or

obsolete inventories. On the other hand, a company with low current ratio may be able to

pay its current obligations as they become due if a large portion of its current assets

consists of highly liquid assets i.e., cash, bank balance, marketable securities and fast

moving inventories. Consider the following example to understand how the composition

and nature of individual current assets can differentiate the liquidity position of two

companies having same current ratio figure.

From 2011 to 2014 current ratio is more than satisfactory ratio. That means that the

current assets is more than two time of current liabilities.

56

QUICK RATIO: Quick ratio is computed by reducing the inventories or marketable

securities from current assets. Past four year quick ratio is calculated below.

Quick Ratio= Current Assets - inventories/current Liabilities

Or

QUICK RATIO 2011=

=1032-50/427

= 2.29

QUICK RATIO 2012=

= 1202-10/501

=3.37

QUICK RATIO 2013=

=1907-0/786

=2.4

QUICK RATIO 2014=

=2497-0/853

=2.9

Significance and Interpretation

Quick ratio is considered a more reliable test of short-term solvency than current ratio

because it shows the ability of the business to pay short term debts immediately.

Inventories and prepaid expenses are excluded from current assets for the purpose of

computing quick ratio because inventories may take long period of time to be converted

into cash and prepaid expenses cannot be used to pay current liabilities.

Generally, a quick ratio of 1:1 is considered satisfactory. Like current ratio, this ratio

should also be interpreted carefully.. On the other hand, a company with low quick ratio

may have fast moving inventories. The analyst, therefore, must have a hard look on the

nature of individual assets.

57

PROFITABILITY RATIO: Profitability ratios measure the efficiency of

management in the employment of business resources to earn profits. These ratios

indicate the success or failure of a business enterprise for a particular period of time.

Profitability ratios are used by almost all the parties connected with the business. A strong

profitability position ensures common stockholders a higher dividend income and

appreciation in the value of the common stock in future. Creditors, financial institutions

and preferred stockholders expect a prompt payment of interest and fixed dividend

income if the business has good profitability position. Management needs higher profits

to pay dividends and reinvest a portion in the business to increase the production capacity

and strengthen the overall financial position of the company.

GROSS PROFIT RATIO: gross profit ratio is to compare gross profit to the total sales

by company for a time period. Higher the ratio determines higher the position of

company. Past four year gross profit ratio is computed below.

GROSS PROFIT RATIO 2011:

=222/1472X100

=15.08%

GROSS PROFIT RATIO 2012:

=422/1768X100

=23.86%

GROSS PROFIT RATIO 2013:

=873/2572X100

=33.94%

GROSS PROFIT RATIO 2014:

=1126/3278X100

=34.35%

58

Significance and interpretation:

Gross profit is very important for any business. It should be sufficient to cover all

expenses and provide for profit.

There is no norm or standard to interpret gross profit ratio (GP ratio). Generally, a higher

ratio is considered better.

The ratio can be used to test the business condition by comparing it with past years‟ ratio

and with the ratio of other companies in the industry. A consistent improvement in gross

profit ratio over the past years is the indication of continuous improvement . When the

ratio is compared with that of others in the industry, the analyst must see whether they use

the same accounting systems and practices.

As we see the trend of gross profit ratio its increasing year by year. Higher gross profit

ratio indicate more profit earning. Hence Infosys BPO is earning good gross profit as its

increasing year by year.

59

OPERATING PROFIT / MARGIN RATIO: operating profit ratio compare total

operating expenses to the total revenue received by company in a particular time period.

Past four year operating ratio is given below.

OPERATING PROFIT RATIO 2011:

==222/1472X100

=15.08%

OPERATING PROFIT RATIO 2012:

=422/1768X100

=23.86%

OPERATING PROFIT RATIO 2013:

=873/2572X100

=20.25%

OPERATING PROFIT RATIO 2014:

=703/3278X100

=21.44%

Significance and interpretation:

The operating profit margin ratio is a key indicator for investors and creditors to see how

businesses are supporting their operations. If companies can make enough money from

their operations to support the business, the company is usually considered more stable.

On the other hand, if a company requires both operating and non-operating income to

cover the operation expenses, it shows that the business' operating activities are not

sustainable.

A higher operating margin is more favorable compared with a lower ratio because this

shows that the company is making enough money from its ongoing operations to pay for

its variable costs as well as its fixed costs.

60

NET PROFIT RATIO: net profit ratio is computed by dividing the net income by total

sales of a particular time period. ratio is shown in percentage format. High percent of

ratio show higher profit. The past four year net profit ratio is computed below.

NET PROFIT RATIO 2011:

=209/1472x100

=14.20%

NET PROFIT RATIO 2012:

=321/1768x100

=18.16%

NET PROFIT RATIO 2013:

=458/2572x100

=17.80%

NET PROFIT RATIO 2014:

=578/3278x100

=17.63%

Significance and Interpretation:

Net profit (NP) ratio is a useful tool to measure the overall profitability of the business. A

high ratio indicates the efficient management of the affairs of business.

There is no norm to interpret this ratio. To see whether the business is constantly

improving its profitability or not, the analyst should compare the ratio with the previous

years‟ ratio, the industry‟s average and the budgeted net profit ratio.

The use of net profit ratio in conjunction with the assets turnover ratio helps in

ascertaining how profitably the assets have been used during the period.

61

BALANCE SHEET RATIO:

DEBT TO EQUITY RATIO: debt to equity ratio measure the proportion of capital mix.

It shows the mix of capital of company and how it is distributed among debt to equity. as

there is no debenture in the capital structure of Infosys BPO limited so there won‟t be any

calculation for debt to equity ratio.

CASH AND CASH EQUIVALENT / TOTAL ASSETS RATIO: The balance

sheet shows the amount of cash and cash equivalents at a given point in time, and the cash

flow statement explains the change in cash and cash equivalents over time.

Although there is some leeway for judgment, common examples of cash and cash

equivalents include bank accounts, money market funds, marketable securities, and

Treasury bills. To be considered a "cash equivalent," a security must be so

near maturity that there is little risk of change in its value if interest rates change (this

typically translates to less than three months of remaining maturity).

The Financial Accounting Standards Board (FASB) requires companies to establish

policies concerning which types of short-term, highly liquid investments are treated as

cash equivalents.

CASH AND CASH EQUIVALENT / TOTAL ASSETS RATIO 2011:

= 567/1684x100

=33.66%

CASH AND CASH EQUIVALENT / TOTAL ASSETS RATIO 2012:

=630/2070x100

=30.43%

CASH AND CASH EQUIVALENT / TOTAL ASSETS RATIO 2013:

=906/2822x100

=32.10%

CASH AND CASH EQUIVALENT / TOTAL ASSETS RATIO 2014:

=1341/3467x100

=38.67%

http://www.investinganswers.com/financial-dictionary/financial-statement-analysis/balance-sheet-1083

http://www.investinganswers.com/financial-dictionary/financial-statement-analysis/balance-sheet-1083

62

CASH AND CASH EQUIVALENT / TOTAL REVENUE RATIO:

CASH AND CASH EQUIVALENT / TOTAL REVENUE RATIO 2011:

=567/1516x100

=37.40%

CASH AND CASH EQUIVALENT / TOTAL REVENUE RATIO 2012:

=630/1821x100

=34.60%

CASH AND CASH EQUIVALENT / TOTAL REVENUE RATIO 2013:

=906/2721x100

=33.30%

CASH AND CASH EQUIVALENT / TOTAL REVENUE RATIO 2014:

=1341/3415x100

=39.26%

Significance and Interpretation:

The amount of cash and cash equivalents a company holds is very important and is a large

component of a company's overall operating strategy. For instance, companies with high

amounts of cash and cash equivalents are better able to get through hard times

when sales are low or expenses are particularly high. High cash reserves can also signal

that the company is "saving up" to make some significant acquisition.

However, companies with a lot of cash on hand are often takeover targets because their

excess cash essentially helps buyers finance their purchase. High cash reserves can also

indicate that management has not figured out how to best deploy the cash.

It is important to note that there is an opportunity cost to holding cash; that cost is the

return on equity that company could have earned by investing the cash in a new product

or expanding business.

63

CAPITAL EXPENDITURE / TOTAL REVENUE RATIO: A capital expenditure is

an expense a company incurs when it invests in assets that might increase profit in the

future. For example, if a small-scale farmer buys a new tractor to make it easier to harvest

crops, the money he spends on the new vehicle is a capital expenditure. A company's

capital expenditure ratio is the amount of money it spends on capital divided by total

sales. It indicates how much a company is investing to facilitate growth

CAPITAL EXPENDITURE / TOTAL REVENUE RATIO 2011:

=3.4%

CAPITAL EXPENDITURE / TOTAL REVENUE RATIO 2012:

=13.5%

CAPITAL EXPENDITURE / TOTAL REVENUE RATIO 2013:

=3.2%

CAPITAL EXPENDITURE / TOTAL REVENUE RATIO 2014:

=5.5%

Significance and Interpretation:

Capital expenditure to total revenue shows the relationship between earning and

investment for further revenue. So here the trend analysis is much more important. More

capital expenditure might increase the revenue of further year.

64

OPERATING CASH FLOW / TOTAL REVENUE:

OPERATING CASH FLOW / TOTAL REVENUE 2011:

=173/1516x100

=11.41%

OPERATING CASH FLOW / TOTAL REVENUE 2012:

=263/1821x100

=14.44%

OPERATING CASH FLOW / TOTAL REVENUE 2013:

=347/2822x100

=12.29%

OPERATING CASH FLOW / TOTAL REVENUE 2014:

=406/3467x100

=11.71%

Significance and Interpretation: operating cash flow to total revenue measure the

operational efficiency of company. Higher ratio indicates high operational efficiency

company. Here operating cash flow doesn‟t mean just cash inflow from operational

activity. Its combined of inflow and outflow.

65

Summary table of ratios for year 2013 and 2014:

66

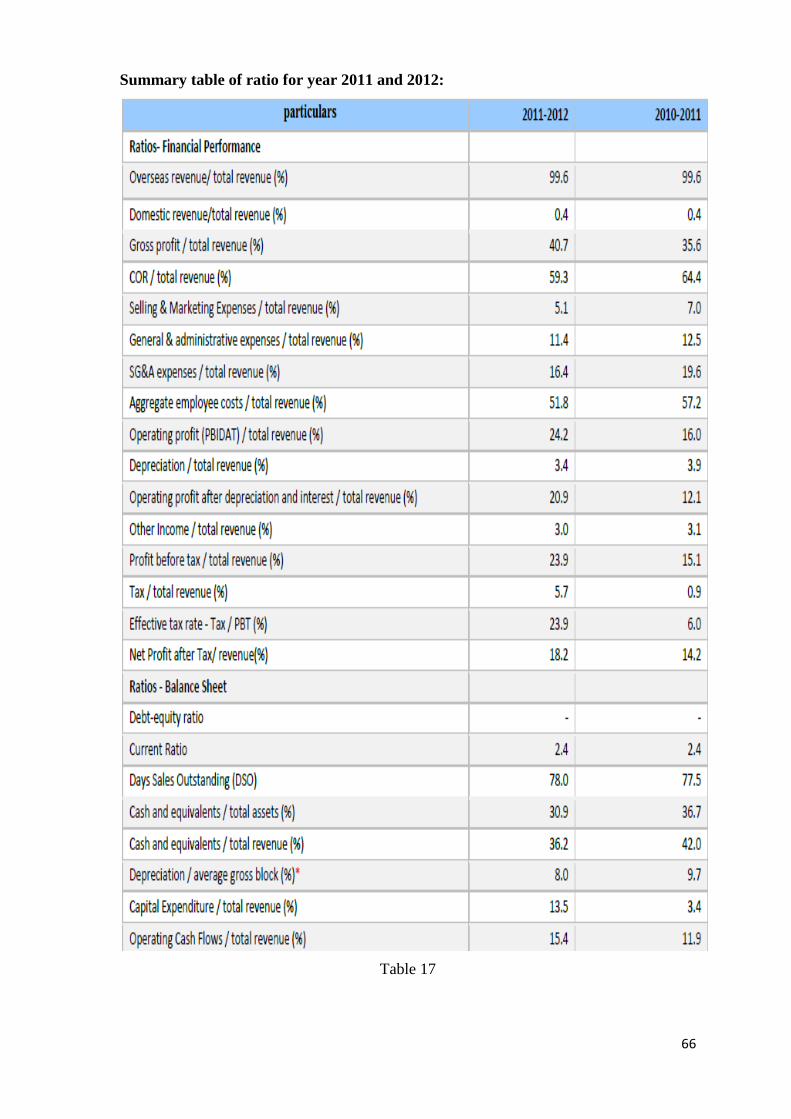

Summary table of ratio for year 2011 and 2012:

Table 17

67

4.

Summary of findings

68

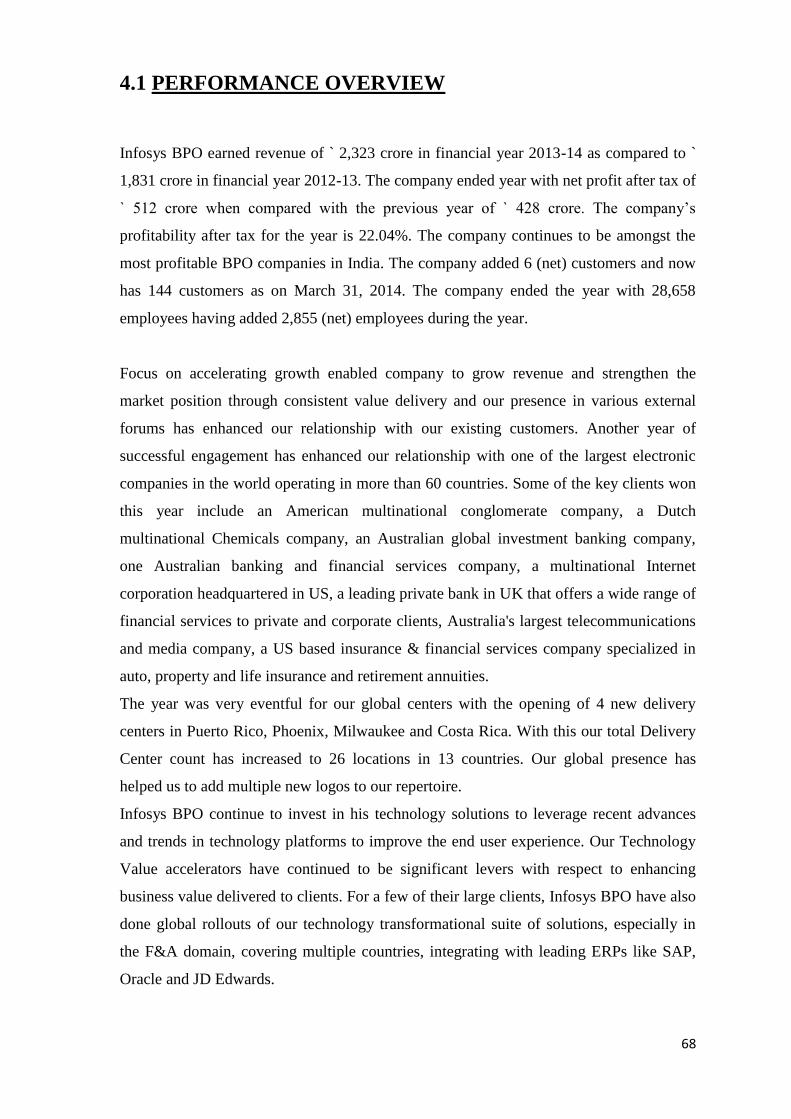

4.1 PERFORMANCE OVERVIEW

Infosys BPO earned revenue of ` 2,323 crore in financial year 2013-14 as compared to `

1,831 crore in financial year 2012-13. The company ended year with net profit after tax of

` 512 crore when compared with the previous year of ` 428 crore. The company‟s

profitability after tax for the year is 22.04%. The company continues to be amongst the

most profitable BPO companies in India. The company added 6 (net) customers and now