Financial Statements for a Sole Proprietorship Why It’s Important Financial statements provide the...

18

Financial Statements for a Sole Proprietorship Why It’s Important Financial statements provide the essential financial information necessary for sound management decisions. Financial statements provide information to owners and managers about how the business is changing as a result of operations.

-

Upload

lily-melton -

Category

Documents

-

view

219 -

download

0

Transcript of Financial Statements for a Sole Proprietorship Why It’s Important Financial statements provide the...

Financial Statements for a Sole Proprietorship

Financial Statements for a Sole ProprietorshipWhy It’s Important

Financial statements provide the essential financial information necessary for sound management decisions. Financial statements provide information to owners and managers about how the business is changing as a result of operations.

Why It’s Important

Financial statements provide the essential financial information necessary for sound management decisions. Financial statements provide information to owners and managers about how the business is changing as a result of operations.

The Seventh Step in the Accounting Cycle: Financial Statements

The primary financial statements

prepared for a sole proprietorship are

the income statement and the balance

sheet. A third statement, the statement

of changes in owner’s equity, is also

often prepared.

The Seventh Step in the Accounting Cycle: Financial Statements

The primary financial statements

prepared for a sole proprietorship are

the income statement and the balance

sheet. A third statement, the statement

of changes in owner’s equity, is also

often prepared.

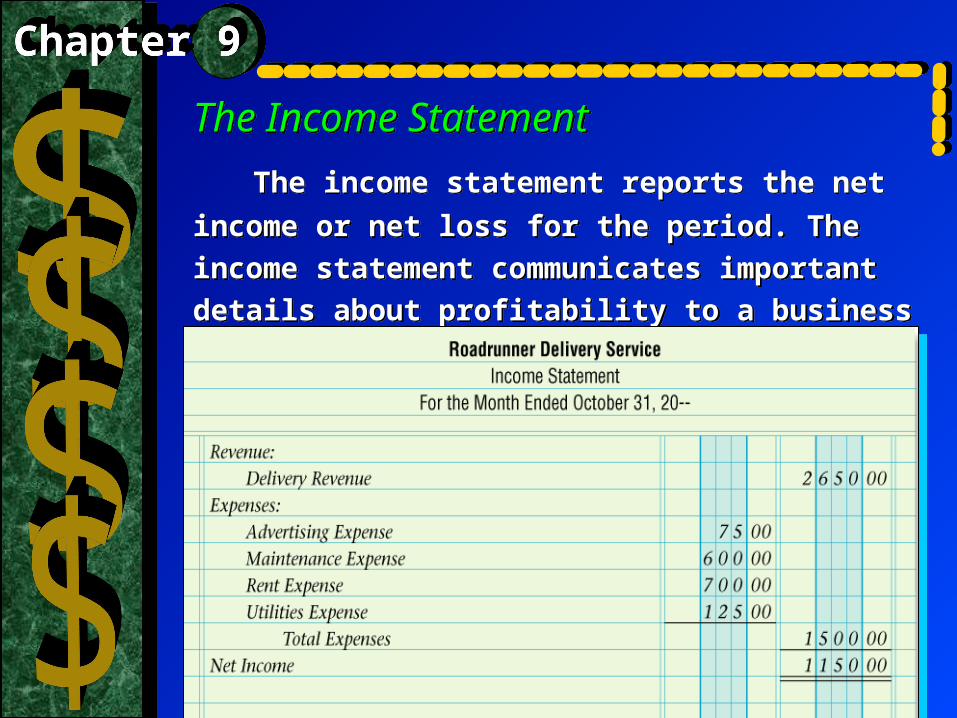

The Income Statement

The income statement reports the net income

or net loss for the period. The income statement

communicates important details about profitability

to a business owner

The Income Statement

The income statement reports the net income

or net loss for the period. The income statement

communicates important details about profitability

to a business owner

The Income Statement with multiple revenue accounts and a Net LossThe Income Statement with multiple revenue accounts and a Net Loss

The Statement of Changes in

Owner’s Equity

One way to evaluate how a business is

performing is by tracking the increase or

decrease in owner’s equity. The statement of

changes in owner’s equity summarizes

changes in the owner’s capital account as a

result of business transactions during the

period.

The Statement of Changes in

Owner’s Equity

One way to evaluate how a business is

performing is by tracking the increase or

decrease in owner’s equity. The statement of

changes in owner’s equity summarizes

changes in the owner’s capital account as a

result of business transactions during the

period.

Preparing The Statement of Changes in Owner’s Equity

The information to prepare this statement is found in three places:

Preparing The Statement of Changes in Owner’s Equity

The information to prepare this statement is found in three places:

the work sheet the work sheet the income statement the income statement the owner’s capital account in the

general ledger

the owner’s capital account in the general ledger

Statement of Changes in Owner’s Equity with Net LossStatement of Changes in Owner’s Equity with Net Loss

Preparing The Statement of Changes in Owner’s EquityPreparing The Statement of Changes in Owner’s Equity

The Balance Sheet

The balance sheet is a report of

the balances in all asset, liability,

and owner’s equity accounts at the

end of the period. The balance

sheet reports the financial position

of a business at a specific point in

time.

The Balance Sheet

The balance sheet is a report of

the balances in all asset, liability,

and owner’s equity accounts at the

end of the period. The balance

sheet reports the financial position

of a business at a specific point in

time.

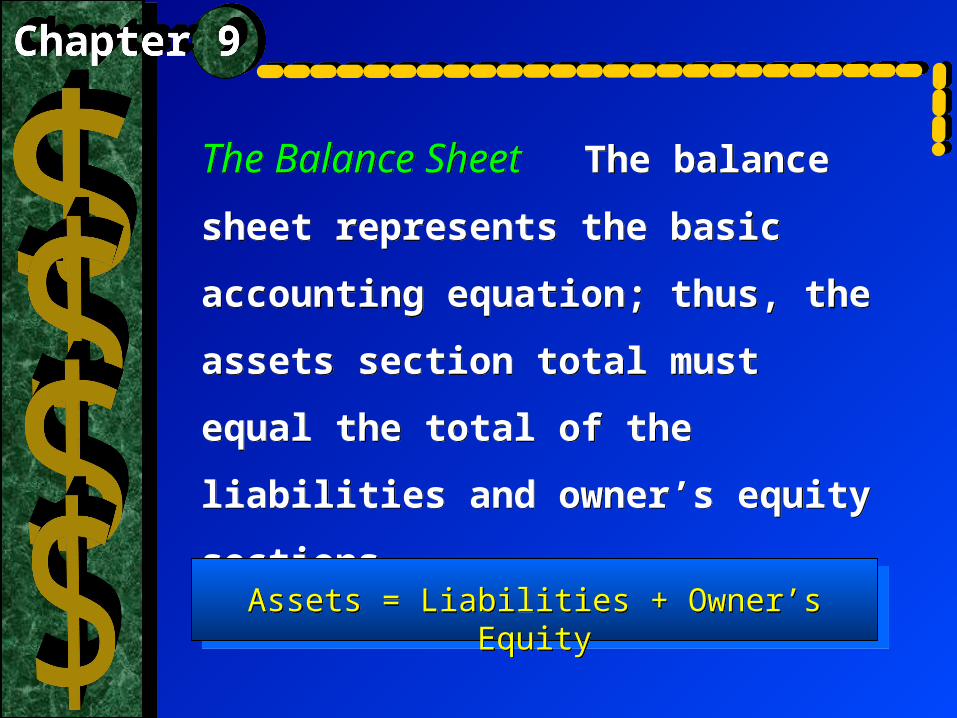

The Balance Sheet The

balance sheet represents the basic

accounting equation; thus, the assets

section total must equal the total of

the liabilities and owner’s equity

sections.

The Balance Sheet The

balance sheet represents the basic

accounting equation; thus, the assets

section total must equal the total of

the liabilities and owner’s equity

sections.

Assets = Liabilities + Owner’s EquityAssets = Liabilities + Owner’s Equity

The Balance Sheet The Balance Sheet

Remember: The capital amount is the updated amount; from the Statement of Changes in Owner’s Equity

Headings on Financial StatementsHeadings on Financial Statements

or Statement of Changes in Owner’s Equity

Ratio AnalysisRatio Analysis

Ratio analysis involves the

comparison of two amounts on

a financial statement and the

evaluation of the relationship

between these amounts.

Used to determine the financial

strength, activity, or debt-

paying ability of a business.

Ratio analysis involves the

comparison of two amounts on

a financial statement and the

evaluation of the relationship

between these amounts.

Used to determine the financial

strength, activity, or debt-

paying ability of a business.

Profitability Ratios• Used to evaluate the earnings performance of the business during the accounting period.

•Return on Sales

Profitability Ratios• Used to evaluate the earnings performance of the business during the accounting period.

•Return on Sales

Return on SalesReturn on Sales

Allows business owners to examine

the portion of each sales dollar that

represents profit.

Allows business owners to examine

the portion of each sales dollar that

represents profit.

Net Income $1,150 net incomeNet Income $1,150 net income== = .434 or 43.4%= .434 or 43.4%

Sales $2,650 salesSales $2,650 sales

Liquidity Ratios• A measure of the ability of a business to pay its current debts as they become due and to provide for unexpected needs of cash.

•Current Ratio•Quick Ratio

• Current Assets – those used up or converted to cashing during the normal operating cycle of the business

• Current Liabilities – debts of the business that must be paid within the next accounting period

Liquidity Ratios• A measure of the ability of a business to pay its current debts as they become due and to provide for unexpected needs of cash.

•Current Ratio•Quick Ratio

• Current Assets – those used up or converted to cashing during the normal operating cycle of the business

• Current Liabilities – debts of the business that must be paid within the next accounting period

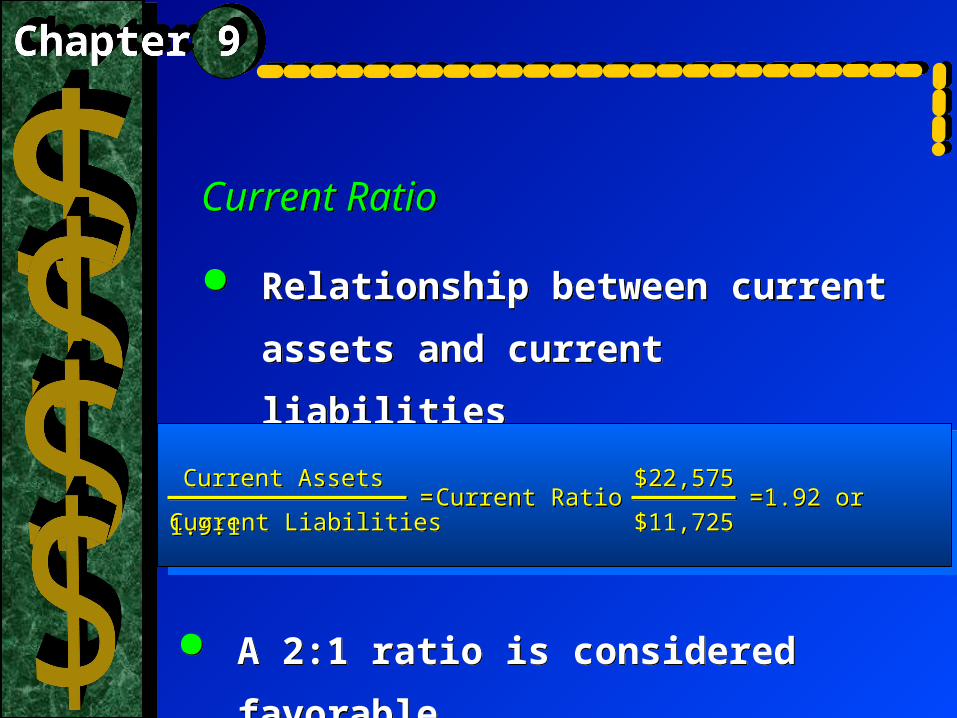

Current RatioCurrent Ratio

Relationship between current

assets and current liabilities

Relationship between current

assets and current liabilities

Current Assets $22,575

Current Liabilities $11,725

Current Assets $22,575

Current Liabilities $11,725= Current Ratio = 1.92 or 1.9:1= Current Ratio = 1.92 or 1.9:1

A 2:1 ratio is considered favorable A 2:1 ratio is considered favorable

Quick RatioQuick Ratio

The relationship between short-

term assets and current liabilities.

The relationship between short-

term assets and current liabilities.

Cash and Receivables $ 22,575

Current Liabilities $11,725

Cash and Receivables $ 22,575

Current Liabilities $11,725= Quick Ratio = 1.92:1= Quick Ratio = 1.92:1

A 1:1 ratio is considered adequate A 1:1 ratio is considered adequate